Debt versus Equity—Open Innovation to Reduce Asymmetric Information

1

Department of Management, Universitas Negeri Semarang, Semarang 50229, Indonesia

2

Department of Economics Education, Universitas Negeri Semarang, Semarang 50229, Indonesia

*

Author to whom correspondence should be addressed.

J. Open Innov. Technol. Mark. Complex. 2021, 7(3), 181; https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030181

Submission received: 15 June 2021

/

Revised: 21 July 2021

/

Accepted: 22 July 2021

/

Published: 2 August 2021

Abstract

:The research aims to examine the difference between absence and presence life cycle stage in technology information digitalization (TID) as a form of open innovation in reducing information asymmetry. Furthermore, companies with asymmetric information prefer debt over equity. The study collects 3.343 pooled data observation units of companies listed in the Indonesian capital market period 2008 to 2019. We use OLS regression analysis to determine the difference between the absence and presence lifecycle stage in determining capital structure relations and exploiting growth opportunities. The study found information disclosure obligation of the capital market regulator has not been fully disclosed through TID. As a result, companies choose to pass in growth opportunities with debt or equity in the absence life cycle stage. Presence lifecycle stage, in the introduction stage, the company misses growth opportunities. Growth and mature stage, debt has a positive effect on the utilization of growth opportunities. The company prefers the issuance of debt with lower information sensitivity than equity. Presence culture, such as majority ownership, generates incentives for open innovation from capital market regulators, which still contain information asymmetry.

1. Introduction

Managers as agents with superior information can act in their interests and those of majority shareholders, rather than in debtholders and other shareholders [1,2]. Thus, an information asymmetry situation can occur in Indonesia with a concentrated ownership structure [3] and a family relationship between the manager and controlling shareholders [4].

Companies use leverage signaling to convey information and reduce information asymmetry [5,6,7]. The presence of information asymmetry results in equity friction in the market [8]. It does not follow the company’s claims, so the company prioritizes internal financing, debt, and then equity according to the hierarchical pecking order theory (POT) [7,9]. The POT seems to perform well empirically concerning sending asymmetric information-reducing signals. However, it does not always perform well in reality [10] and remains unexplained mainly [11], depending on the specific firm and institution [12].

The open innovation paradigm is the most important [13]; that is, reporting should use information technology and digitization (TID) to reduce information asymmetry in equity issuance. However, it is not used optimally, meaning that there is still a high cost of equity, which is in line with POT, indicating that leverage is better than equity.

We predict that the POT can explain a situation better when TID, as a form of open innovation, is used to deliver firm specifics and a better life cycle. As a result, information asymmetry is reduced, the POT hierarchy is reversed, and the company prefers equity issuance over debt. Firm-specific variables include size, profitability, and risk [14,15], while the life cycle comprises introduction, growth and maturity stages [16,17]. The open innovation strategy in using TID is mostly done by companies in the introduction and growth stages because the development is faster than their ability, than growth and is mature [18]. As a result, they are more sensitive to financing decisions.

Capital structure decisions are developed based on conflicts of majority and minority shareholders following the characteristics of the ownership structure in Indonesia, which may differ to other developing countries. The Financial Services Authority of the Republic of Indonesia (OJKRI) plays an essential role in developing open innovation [19] and using TID implementation for information disclosure [20], to reduce the level of information content, and it prefers equity over debt. The presence of culture makes the impact of openness on open innovation more complex than without the presence of culture [21]. Disclosure information as a form of openness strategy through TID is primarily determined by a set of norms and values that are widely adopted and adhered to throughout the company (culture).

2. Literature Review

2.1. Open Innovation: A Culture and Complexity with Evolutionary Economics

Open innovation uses the inflow and outflow of knowledge to accelerate internal innovation and expand the market of internal innovation [22]. When a company is an openness to knowledge and information, it has the potential to produce open innovation so that it can take advantage of growth opportunities and better market response [21].

The presence of culture produces a relationship between openness and open innovation, which is more complex than the inverted u-shaped. Absence of culture, companies can increase openness to accelerate open innovation. Still, at the optimal point when companies are more open, it is difficult to manage information and knowledge, which will result in a decrease in open innovation [23].

Culture helps explain firm performance, even when individuals only adopt shared values and norms and is strengthened when adopting organizational values that are the values of the company’s founders [21]. To sum up, a constructive culture impacts cooperation within organizational units and between organizational units that directly or indirectly affect firm performance. Stock market regulators in Indonesia require disclosure of information in the TID as a form of open innovation that stimulates the openness of every issuer listed in the capital market [13]. Thus, a stable environment in the form of disclosure information requirements from OJKRI generates incentives for managers and companies to create a strong culture. Therefore, their capabilities are increasingly exploited in achieving company goals.

The development of the fourth industrial revolution era demands the use of engineering (TID) directly and more heartily than before in responding to the needs of the market and society [24]. Companies as part of an entity from the capital market have more incentives to disclose information as a demand for an open business model. As a result, companies can use technology to connect to the market [25]. They added that the presence of the accelerated IT revolution along with the deepening of the knowledge-based economy resulted in a new business model that connected companies and access to markets more intensively than before.

It is still debatable when it cannot be compared between the benefits and costs due to open innovation. As a result, companies will limit the disclosure of financial information entirely because it can affect their competitive position [26], like the complexity with evolutionary economics hypothesis, which is different from the neo-classic outlook, which prioritizes dynamic analysis over static. Thus placing behavioral, institutional, technological and other explanatory variables in other forms [27].

One possible explanation regarding the difference in benefits and costs in TID use is due to the firm lifecycle [28]. They reported that companies in the mature stage have a better green innovation process than growth stage firms—furthermore, technology capability as a mediation between green innovation performance and life-stage firm.

Thus, regulators from OJKRI and the 4th industry revolution have produced better use of TID in the open business model. It is easier for companies to convey information disclosure to the market through JATS (Jakarta Automated Trading System Next Generation) to reduce asymmetric information [29]. PT Bank Pembangunan Daerah Jawa Barat and Banten, Tbk reports information on last, present performance and business development plans [30]. In addition, a change in the company’s ownership structure was reported through the PMT-HMETD (Capital Additions Without Preemptive Rights Program).

2.2. Firm-Specific Leverage and Growth—The Role of Open Innovation

Companies with fewer valuable opportunities can mimic those with more valuable ones. This can result in overvalued securities at companies with fewer valuable opportunities and undervalued securities at companies with more valuable opportunities. Therefore, when growth opportunities have asymmetric information, a good quality company will issue a debt higher than equity [5,6,20] to convey a positive signal to the market. Thus, the company will take advantage of growth opportunities with increased leverage, which indicates that the company’s information asymmetry is lower than if it were to issue equity, in line with the POT. On the other hand, majority shareholders may prevent share dilution through debt issuance when information asymmetry is high. next, [31].

Debt issuance is a mechanism used to reduce the agency problem of ex-ante information asymmetry. Managers who act in the interests of shareholders are better off skipping growth opportunities with leverage [32] because high leverage only increases the risk of bankruptcy and welfare transfer to debtholders [33].

One difference between this study and previous research regarding the relationship between leverage and growth is in using firm-specific terms, including size, profitability, and risk. Large companies have lower information asymmetry than small companies, increasing collateral assets for lenders [12,34]. Larger companies have higher cash flow and more assets, so they have easy access to banking because they are considered less risky borrowers [35]. As support for their behavior, profitability will have an impact on leverage. Managers prefer to keep retained earnings and use debt to finance growth opportunities [36]. When the company-specific risk is high, the shareholders will perform risk-shifting [37] whenever possible. The use of excessive leverage, with the presence of bankruptcy costs and the limited responsibility of shareholders, is a risk for the debtholders who bear it [8].

Market failure among participants is not due to product quality but rather to information asymmetry [38]. In this context, TID is a form of open innovation that can reduce information asymmetry [13]. Thus, the informed agent has a strategic role compared to the uninformed agent in delivering firm-specific information to the market [39]. As a result, equity friction reduces, and equity is prioritized over debt, which is inversely related to the POT.

Hypothesis 1 (H1).

TID open innovation can be in a low level of information asymmetry so that the company prioritized equity financing over debt.

2.3. Firm-Specific Life Cycle Stage—Open Innovation

Each stage of the life cycle produces a different and more specific level of asymmetry [14]. For example, the technology life cycle is more applicable during the growth and maturity stages than the introduction stage [40,41]. Table 1 shows that it was possible to use cash flow for greater investment during the introduction and growth stages, including TID, but cash flow tended to come from debt issuance [16]. Thus, open innovation investment in TID decreased the asymmetric information in the introduction, growth, and maturity stages. Open innovation delivers transparent information, therefore decrease asymmetric information.

Older companies generally have better information credibility, more assets, and a better reputation than younger companies that use more leverage. Therefore, in the maturity stage, a company can substitute debt with internal financing [14] or prefer debt to equity [42] as a form of low information asymmetry.

In addition, the relationship between specific firms and the life cycle is that profitability has a negative effect and leverage has a positive effect. As the age of the company increases, the profitability decreases, and the company prioritizes debt issuance. In particular, leverage is shown as the smallest determinant of financing during the introduction stage [17]. During the early stage, a company faces significant business uncertainty and risk, which is exacerbated by high information asymmetry, so that it prioritizes internal funding [15]. However, when internal funding from profitability has decreased [17], the company prefers debt, which has a lower risk of stock price friction than equity.

A company’s size affects the use of leverage at each stage of the life cycle. During the introduction stage, leverage is low while high during the growth and maturity stages [15]. If there is a large asymmetry problem at the introduction stage, the company uses internal funds to reduce leverage. Companies have less information asymmetry and greater collateral asset ownership during the growth and maturity stages, prioritizing external funding through debt instead of equity [17]. More extremely, companies at an early stage, due to the high information asymmetry, are limited in using external funds. In the next stage, the company performs re-balancing, not by increasing debt, but by substituting internal funding where the frictional risk of share prices is smaller than debt and equity [14].

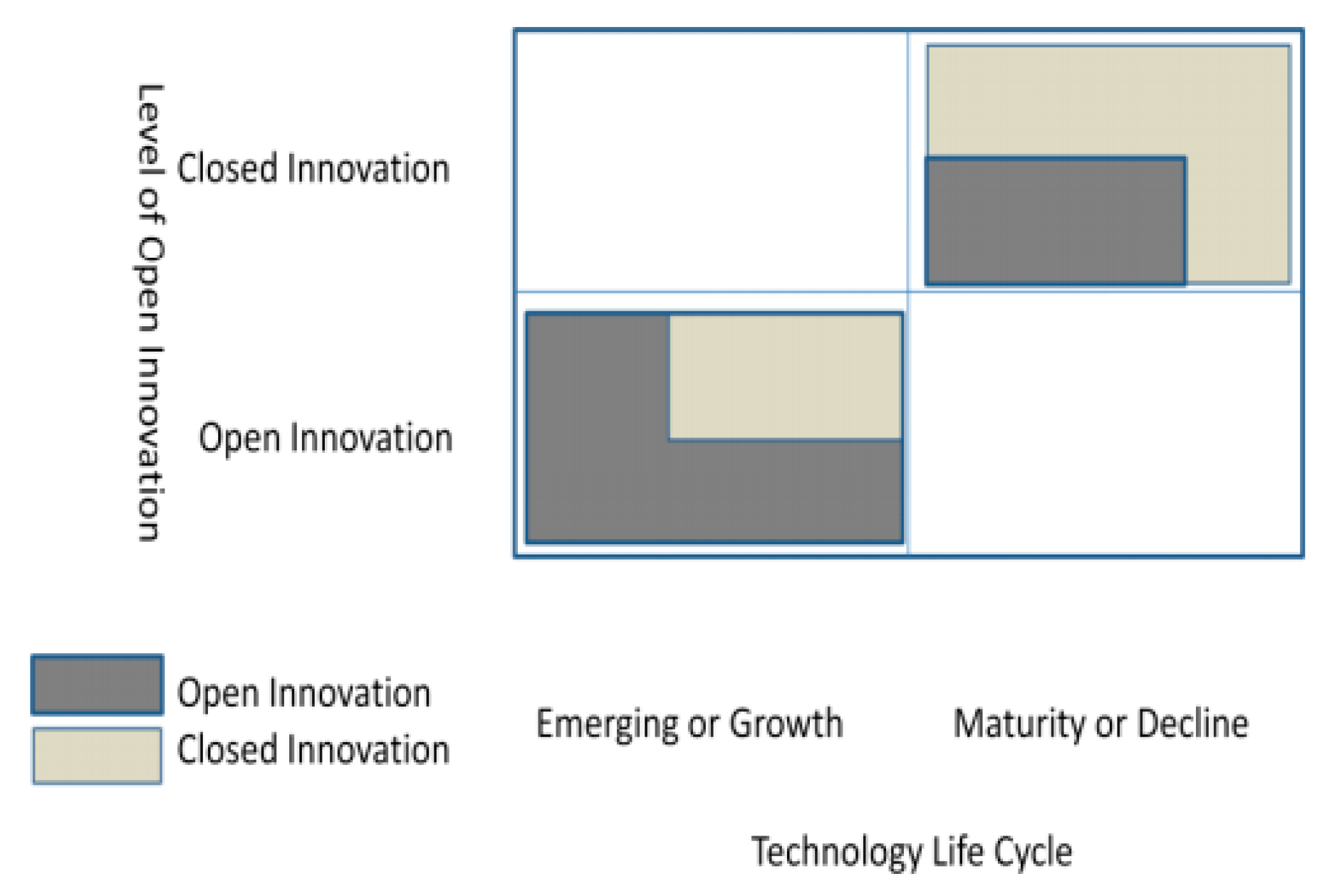

During the introduction stage, companies are faced with higher information asymmetry because of the uncertainty of future cash flows. As a result, they have a higher external cost of capital. As a result, companies face higher levels of risk during the introduction and growth stages, but risk reduces during the maturity stage [43]. The maturity stage gives a chance for stakeholder to collect many information, therefore the risk is reduce. Investment efficiency is low during the introduction stage; however, this increases non-linearly during the growth and maturity stages [15]. Therefore, the POT theory is more applicable during the maturity stage [44,45]. Thus, an increase in lifecycle stages and reduced asymmetric information results in greater closed innovation [18], as shown in Figure 1. As a result, starting from maturity, the financing for open innovation is reduced, and if needed, they prefer equity because there is less asymmetric information.

Hypothesis 2 (H2).

The presence of open innovation and the increasing stages of the life cycle result in reduced asymmetry regarding firm-specific information. Companies prefer equity to leverage when financing growth opportunities.

3. Methods

3.1. Variable Measurement

The total debt ratio to total assets (leverage) was used as the dependent variable in a regression [31]. When growth opportunities reach information asymmetry, the issuance of debt results in companies still being able to issue leverage greater than the total assets, even though market leverage depreciates. Growth opportunities are measured by (total sales t–total sales t 1)/total sales t−1 [46,47].

Our firm-specific variable used in asset as a proxy for size [48], profitability as a return on assets [49], and specific risk as to the variance of return on assets [50]. We used the age measured in years since it was recorded [51]. The life cycle consists of five stages: introduction, growth, maturity, shake-out, and decline [16]. Since cash flow investing, operating, and financing can better explain the life cycle, we used only the first three stages due to the prominent aspect [17]. A company’s life cycle stage was categorized as follows: 1 = introduction, 2 = growth, and 3 = maturity [52].

3.2. Data and Sample Selection

Pooled data of 3343 observations gathered from companies from eight industrial sectors listed on the Indonesian Stock Exchange (IDX) for 2008–2019. Table 2 shows the collinearity of variables used in the analysis and their corresponding VIF values; the financial and banking sectors were excluded due to differences in each company policy [53]. We removed outliers from the dataset by excluding the highest and lowest 5% of values. Data were obtained from eight industrial sectors: agriculture (3.92% of observations), infrastructure (11.22%), utilities and transportation (11.22%), manufacturing (32.93%), mining (9.39%), property (15.23%), real estate and building construction (27.31%), trade, and services and investment. Table 2 indicated a VIF value of about 1 and a correlation between explanatory variables of less than 0.8 [54].

We used OLS regression with a dummy equation or LSDV because the scalable explanatory variable was nominal (introduction, growth and mature), with two dummy categories to avoid dummy traps [54]:

where Y is leveraged; X represents growth opportunities; firm-specific size, profitability and risk; D2i is 1 if the stage is growth; otherwise it is 0; D3i is 1 if the stage is mature; otherwise it is 0; and if D2i = 0 and D3i = 0 then it is the introduction stage.

4. Results

4.1. Data

Table 1 shows that the data has kurtosis, which tends to be homogeneous and has varied skewness as long as the growth stage has a mean leverage greater than the introduction and maturity stages. The increase in leverage from introduction to growth in greater debt issuance reduces information asymmetry [15]. In contrast, there was no significant difference in mean leverage during maturity compared to growth, as an effort to reduce the risk of bankruptcy [43], and a more stable cash flow was used to replace aging equipment instead of paying debt [16].

As long as the growth stage has lower information asymmetry than the introduction stage when assets increase collateral, the company issues more debt. Conversely, during the maturity stage, the information asymmetry is reduced compared to the growth stage. The increase in collateral results in reduce leverage, leading to a company preferring internal financing over equity [14].

As long as a company in the growth stage has cash flow from large investments, it exceeds profitability, making it relatively stable compared to a company in the introduction stage [16], resulting in a decrease in profitability. On the other hand, there is an increase in profitability because investment is more efficient than during maturity [15]. In addition, the business risk decreases as the age of the company increases [15,44].

There was more debt issuance and a risk-shifting problem [37,55]. When managers and majority shareholders have better quality information about growth opportunities than minority shareholders, they prefer debt to equity. Debtholders are promised high returns if the project is successful, even if the probability of success is low, because if it is successful, the majority manager will benefit. If it fails, the debtholders will share the risk. Conversely, if the risk is unknown, the company will tend to issue equity. Further information asymmetry results in a “mean revision” of the leverage level [34,45]. In this case, it would be better to avoid taking advantage of growth opportunities because they created a new debt agency.

4.2. Regression Analysis

Table 1 showed a significant difference in mean leverage between the growth and introduction stages and the mature and growth stages. However, because this simple description did not include firm-specific size, profitability and risk variables, the findings of an LSDV regression represent in Table 3.

Column 1 of Table 4 shows that when majority and minority shareholders do not have specific firm information, they are faced with uncertainty in cash flow and high risk so that the issuance of debt becomes risky. As a result, they refuse financing for valuable growth opportunities to prevent control over the company [55]. Due to the limited responsibility of shareholders, if there is bankruptcy, the company will be taken over by debtholders. When there is no disclosure of specific firm information, debtholders will not make transactions because it can depreciate debt and equity.

Column 2 of Table 3 shows that as assets increase, the collateral increases; as the specific risk increases, the profitability decreases. The company increases the leverage to finance the rise invaluable growth [10,56]. It also shows that the effect of profitability on leverage is greater than size and risk. Increasing assets and decreasing risk can provide a more positive signal than profitability, which has a negative signal, to the market. Management will issue debt to provide a positive signal to the market [5] to maintain control of a quality company [6]. From the perspective of agency theory, they avoid exposure to the capital market [57].

Thus, the firm-specific information submitted by companies with agency problems still contains asymmetric information. The result is that they issue debt rather than equity when financing growth opportunities. As previously thought, there is still information asymmetry. Even though the manager already has an incentive for open innovation with TID in information disclosure, the POT hierarchy works, following OJKRI regulations. A high cost of equity resulting from asymmetric information has resulted in companies using debt financing [13], despite Indonesia being a bank-based system [58].

Columns 3–5 of Table 4 show the difference in results across life cycle stages. Companies in the introduction stage have high business uncertainty and risk [59]. Managers and majority shareholders have higher quality information than minority shareholders regarding growth opportunities, so growth opportunities lead to greater information asymmetry than total assets [31]. By adding the specific firm size and profitability, managers and majority shareholders missed out on taking advantage of the growth opportunities with leverage. When faced with high risk and reduced profitability, they will not finance growth opportunities with leverage even if there is an increase in collateral assets. However, they perform risk avoidance [55] to prevent loss of control and rent for future corporate value increases.

In the growth stage, companies buy many assets as part of a competitive advantage strategy. As a result, demand for cash flow for investment is greater than the availability of internal financing, and there is lower information asymmetry than during the introduction. Although there is an increase in size as a proxy for collateral and decreased company risk, long-term investment needs are greater than profitability. Hence, the presence of asymmetric information exacerbates this condition, and companies prefer debt issuance to equity [7,16].

The mature stage is a condition with fewer asymmetric information indications than the growth stage. Therefore, companies should issue equity instead of debt, but we found that they still reference debt, which differs from findings of other research [14,31]. Managers and majority shareholders avoid issuing equity because they are more sensitive to the market response than debt or an imbalance of information between insiders and outsiders.

Open innovation carried out by insiders as a mechanism to reduce information asymmetry has proven to be sub-optimal in practice. With the provisions of the OJKRI, they do not have an incentive to issue equity compared to leverage in financing growth opportunities. If they use the equity, they will face a high cost of equity as the production of asymmetric information [13]. The Republic of Indonesia government requires companies to disclose information before, when and after the company is listed on IDX and the accompanying sanctions for not disclosing information [60]. Through TID as information disclosure through the company website and IDX, Open innovation strategy reduces asymmetric information. There are still agents and majority shareholders who have superior information compared to minority shareholders.

As one of the Bakrie Group companies, PT Bakrieland Development requires equity financing with the right issue for business expansion in Bukit Jonggol Asti. Based on interview, Kurniawati Budiman said “the fact is that the rights issue is underpricing due to the finding of differences in investment savings in 2010 Q1 between what was conveyed to the public by PT Bakrie Sumatera Plantation and PT Energi Mega Persada”, which is included in the Bakri Group, and those recorded at PT Bank Capital.

The difference in the investment saving notes shows asymmetric information resulting in adverse selection and right issue underpricing in other companies in the Bakrie Group. Another phenomenon, such as PT Garuda Indonesia, reported an increase in net profit of USD 809.5 million in 2018, resulting from the collaboration between PT Citilink as a subsidiary and PT Mahata Aero Tech, which invested in entertainment equipment on their aircraft. In fact, until December 2018, PT Mahata Aero Tech had not made any payments to PT Citi-link.

The presence of TID as an open innovation strategy provides insiders with incentives to convey information disclosure to the market; however, the information conveyed is not under the actual situation. This is so that stock prices experience a contraction, and they finance growth opportunities by issuing debt, such as the growth and introduction stages. Different companies in a mature stage, such as PT Unilever, with more-lower asymmetric information, and in an overpricing share price in 2000 and 2003, resulting in a stock split. As a result, debt financing began to decrease because during maturity, growth opportunities decreased compared to the previous stage, and the company chose a closed innovation strategy. The company reduced TID investment as an open innovation strategy due to reduced asymmetric information at the mature stage.

Innovation-oriented culture has not yet been manifested in responding to the demands of disclosure of information as the capital market demands. The company has not been able to take the characteristics of the local culture to change the game-oriented to open innovation and therefore can take advantage of growth opportunities. The presence of culture is proven to change the inverted u-shaped relationship between openness and open innovation to become more complex [21]. The company does not optimally use external technology to convey actual company information and knowledge.

Firm culture should encourage innovation and flexibility regarding the core values of treating employees, customers, suppliers and other shareholders. It has not been fully implemented, even though it can directly determine firm performance, in this case reducing undervalued, if the company issues equity. Static study of open innovation inadequacy of openness, aversion to risk-taking, organizational inertia and not invented here (NIH) syndrome has not motivated open innovation in the capital market [21]. OJKRI (The Financial Services Authority of the Republic of Indonesia), as the regulatory body, has carried out open innovation intending to disclose information for all IDX listed issuers and encourages the delivery of information regularly. However, it has not been optimally balanced with the actual delivery of information due to its reluctance to take a risk. Because companies think they will lose their competitive advantage if they tell the truth [26].

It is undeniable that the reluctance of voluntary information disclosure results in greater opportunities for financial distress than non-financial distress. In fact, because the culture in companies with the majority and concentrated ownership prevents the risk of losing discretionary power, they avoid being issued shared because the capital market will be monitored [57]. Therefore, the culture may be static towards open innovation from capital market regulations.

4.3. Technology Life Cycle, and Open Innovation

Based on the life-cycle stage, differences in the company’s growth depend on the availability of resources, and opportunities are characteristic of each stage [28]. Moving through each stage of the lifecycle requires innovation processes in different TIDs [18,22]. In the initial stage, the company develops technology (TID) as an innovation process. In the growth stage, the company deploys technology so that the company’s mature stage gets a positive profit (harvest technology). When the decline stage occurs, the company needs to develop new technology.

Implementation of TID improves financial performance because it results in a better quality of financial reporting [26], thereby reducing information asymmetry between managers and shareholders and debtholders. Higher information asymmetry and the use of new technology during the introduction stimulate companies to miss growth opportunities through debt or equity issues. They prefer big data in new technology and have not combined market-based [24]. The level of information asymmetry is lower at the growth and maturity stages than the introduction and the ability to connect technology with the market better, encouraging better disclosure of information to the market.

Thus, the presence of an openness culture produced by the majority and concentrated ownership determines open innovation technology in information disclosure. An interesting finding, when open innovation of technology is less actualized in the introduction, in contrast, companies in Korea are in the initial stage of developing IT medical care, IT industrial robots so that the next stage can be informed in the market to earn profits [18]. Companies in Indonesia develop open innovation of technology that relates to core business more than reducing information asymmetry.

To sum up, we added a model proof in the introduction. The company focuses more on new technology based on core business than on the latest technology based on information disclosure as OJK’s obligation [18]. During the introduction, the company is small, so managers are oriented to aligning open innovation with the company’s strategy (core business) to overcome potential obstacles and failures when implemented. As a result, information disclosure has not been fully carried out because it prevents capital market monitoring [57], then the issuance of debt and equity depreciated and missed growth opportunities. In contrast to growth and maturity, when they are aligned with open innovation and strategy, their technology is used for greater openness, according to OJK regulations. It still does not reduce information asymmetry because it prefers debt over equity. The presence of a culture of ownership structure results in the existence of information asymmetry, even though TID is actually able to reduce it.

5. Conclusions

Managers have a strategic role in open innovation using TID for information disclosure. In the absence of firm-specific information, the issuance of leverage or equity will only depreciate. Conversely, when firm-specific information is added as a disclosure of information, there is still information asymmetry, thus to the issuance of equity, which is more sensitive to market responses, they issue debt.

When adding firm-specific life cycles to test the effect of growth on leverage, the company did not issue debt to finance growth opportunities during the introduction stage even though it had lower market sensitivity than equity. However, the next stage showed severe asymmetric information when companies disclosed firm-specific information but still used debt financing to finance growth opportunities.

In the overall sample without including the life cycle, firms preferred the issuance of leverage over equity when firm-specific information was included. The disclosure of information as a form of open innovation did not incentivize companies to prefer equity issuance over debt during growth and maturity. Managers and majority shareholders have more incentives to prevent equity, which results in dilution, even though there was disclosure of information, which is their obligation. Furthermore, because as long as mature has reduced growth opportunities and tends to be closed innovation, the need for financing is less. If it is necessary, they prioritize debt over equity because it is still found that equity issuance is more sensitive in the capital market than debt [38]. With regard to the limitations of our research, some variables may have been committed in the modeling procedure. First, the agents who act in majority shareholders’ interests are still likely to have better information than other shareholders, even though information disclosure is required as a form of open innovation. Second, we did not explore firm heterogeneity via the data panel.

Author Contributions

A.Y. is generating an idea for this research. He proposes and contributing to the literature review, research method, discussion. R.S.W. arranges and develops literature review, data analysis, and results and findings. W. analyzes data and contributes to the discussion and administrative project. All authors have read and agreed to the published version of the manuscript.

Funding

Authors would like to express gratitude to the Ministry of Education, Culture, Research, and Technology of the Republic of Indonesia, Universitas Negeri Semarang, and Institute of Research and Community Service (LPPM) UNNES with grant number 136.26.4/UN37/PPK.3.1/2021.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data is available by request to the authors.

Acknowledgments

Authors would like to express gratitude to the Institute of Research and Community Service (LPPM) Universitas Negeri Semarang to support the research.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Cariola, A.; la Rocca, M.; la Rocca, T. Overinvestment and Underinvestment Problems: Determining Factors, Consequences and Solutions. SSRN Electron. J. 2011. [Google Scholar] [CrossRef] [Green Version]

- Lepetit, L.; Meslier, C.; Wardhana, L.I. Do Asymmetric Information and Ownership Structure Matter for Dividend Payout Decisions? Evidence from European Banks. SSRN Electron. J. 2015. [Google Scholar] [CrossRef] [Green Version]

- la Porta, R.; Lopez-de-Silanes, F.; Shleifer, A. Corporate ownership around the world. J. Financ. 1999, 54, 471–517. [Google Scholar] [CrossRef]

- Claessens, S.; Djankov, S.; Lang, L.H.P. The separation of ownership and control in East Asian Corporations. J. Financ. Econ. 2000, 58, 81–112. [Google Scholar] [CrossRef]

- Ross, S.A. Determination of Financial Structure: The Incentive-Signalling Approach. Bell J. Econ. 1977, 8, 23–40. [Google Scholar] [CrossRef]

- Leland, H.; Pyle, D. Information asymmetries, financial structure, and financial intermediation. J. Financ. 1977, 32, 371–387. [Google Scholar] [CrossRef]

- Myers, S.; Majluf, N. Corporate Financing and Investment Decisions When Firms Have Information the Investors Do Not Have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Modigliani, F.; Miller, M. The Cost of Capital, Corporation Finance and the Theory of Investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar] [CrossRef] [Green Version]

- Myers, S. Capital structure puzzle. J. Financ. 1984, 39, 574–592. [Google Scholar] [CrossRef]

- Halov, N.; Heider, F. Capital structure, Asymmetric Information and Risk. Q. J. Financ. 2003, 1, 767–809. [Google Scholar] [CrossRef]

- Fosu, S. Capital structure, product market competition and firm performance: Evidence from South Africa. Q. Rev. Econ. Financ. 2013, 53, 140–151. [Google Scholar] [CrossRef] [Green Version]

- Klein, L.S.; O’Brien, T.J.; Peters, S.R. Debt vs. equity and asymmetric information: A review. Financ. Rev. 2002, 37, 317–349. [Google Scholar] [CrossRef]

- Muslim, A.I.; Setiawan, D. Information asymmetry, ownership structure and cost of equity capital: The formation for open innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 48. [Google Scholar] [CrossRef]

- la Rocca, M.; la Rocca, T.; Cariola, A. Capital structure decisions during a firm’s life cycle. Small Bus. Econ. 2011, 37, 107–130. [Google Scholar] [CrossRef]

- Ahmed, B.; Akbar, M.; Sabahat, T.; Ali, S.; Hussain, A.; Akbar, A.; Hongming, X. Does firm life cycle impact corporate investment efficiency? Sustainability 2021, 13, 197. [Google Scholar] [CrossRef]

- Dickinson, V. Cash Flow Patterns as a Proxy for Firm Life Cycle. Account. Rev. 2011, 86, 1969–1994. [Google Scholar] [CrossRef]

- Castro, P.; Fernández, M.T.T.; Amor-Tapia, B.; de Miguel, A. Target leverage and speed of adjustment along the life cycle of European listed firms. BRQ Bus. Res. Q. 2015, 19, 188–205. [Google Scholar] [CrossRef] [Green Version]

- Jin-Hyo, Y.; Mohan, A. A Study on the Difference of Open Innovation Effect according to Technology Life Cycle. 2009. Available online: http://openinnovation-tmc.org (accessed on 24 May 2021).

- Feller, J.; Hayes, J.; O’Reilly, P.; Finnegan, P. Institutionalising information asymmetry: Governance structures for open innovation. Inf. Technol. People 2009, 22, 297–316. [Google Scholar] [CrossRef]

- Financial Services Authority. 2015; pp. 1–15. Available online: https://www.ojk.go.id/id (accessed on 25 May 2021).

- Yun, J.H.J.; Zhao, X.; Jung, K.H.; Yigitcanlar, T. The culture for open innovation dynamics. Sustainability 2020, 12, 5076. [Google Scholar] [CrossRef]

- Chesbrough, H. Open innovation: A new paradigm for understanding industrial innovation. In Open Innovation: Researching a New Paradigm; Oxford University Press: Oxford, UK, 2006; pp. 1–19. [Google Scholar]

- Sartori, R.; Favretto, G.; Ceschi, A. The relationships between innovation and human and psychological capital in organizations: A review. Innov. J. 2013, 18, 1–18. [Google Scholar]

- Yun, J.J.; Kim, D.; Yan, M.R. Open innovation engineering—preliminary study on new entrance of technology to market. Electronics 2020, 9, 791. [Google Scholar] [CrossRef]

- Yun, J.J.; Yang, J.; Park, K. Open Innovation to Business Model: New Perspective to connect between technology and market. Sci. Technol. Soc. 2016, 21, 324–348. [Google Scholar] [CrossRef]

- Mohd-Sam, M.; Subramanian, N.; Mustafa, R. Financial Effects of Open Innovation in The Manufacturing: Companies in Malacca, Malaysia. Manag. Decis. 2015, 53, 1527–1544. [Google Scholar] [CrossRef]

- Dopfer, K. Evolution and Complexity in Economics Revisited. Pap. Econ. Evol. 2011. [Google Scholar] [CrossRef] [Green Version]

- Tariq, A.; Badir, Y.F.; Safdar, U.; Tariq, W.; Badar, K. Linking firms’ life cycle, capabilities, and green innovation. J. Manuf. Technol. Manag. 2020, 31, 284–305. [Google Scholar] [CrossRef]

- IDX. PT Bursa Efek Indonesia. Idx. 2020. Available online: https://www.idx.co.id/%0Awww.idx.co.id (accessed on 23 May 2021).

- BJBR. Information Disclosure Capital Addition Plan Without Providing First Effect Order Rights As Used In Regulation No. 38/Pojk.04/2014, in The Framework of Company Capital Additions From West Government And Banten Government; West Java nad Banten Bank: Bandung, Indonesia, 2018; pp. 2–5. [Google Scholar]

- Lang, L.; Ofek, E.; Stulz, R.M. Leverage, Investment, and Firm Growth. J. Financ. Econ. 1996, 40, 3–29. [Google Scholar] [CrossRef] [Green Version]

- Dybvig, P.H.; Zender, J.F. Capital structure and dividend irrelevance with asymmetric information. Rev. Financ. Stud. 1991, 4, 201–219. [Google Scholar] [CrossRef]

- la Rocca, M.; la Rocca, T.; Cariola, A. Overinvestment and underinvestment problems: Determining factors, consequences and solutions. Corp. Ownersh. Control. 2007, 5, 79–95. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Capital structure choices. Crit. Financ. Rev. 2012. [Google Scholar] [CrossRef]

- Rajan, R.; Zingales, L. What Do We Know About Capital Structure? Some Evidence from International Data. J. Financ. 1995, 50, 1421–1460. [Google Scholar]

- Michaelas, N.; Chittenden, F.; Poutziouris, P. Financial Policy and Capital Structure Choice in U.K. SMEs: Empirical Evidence from Company Panel Data. Small Bus. Econ. 1999, 12, 113–130. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of The Firm: Managerial Behavior, Agency Cost and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Akerlof, G. The market for ‘lemons’: Quality uncertainty and the market mechanism. Q. J. Financ. Econ. 1970, 84, 488–500. [Google Scholar] [CrossRef]

- Barbaroux, P. From market failures to market opportunities: Managing innovation under asymmetric information. J. Innov. Entrep. 2014, 3, 5. [Google Scholar] [CrossRef] [Green Version]

- Shahmarichatghieh, M.; Tolonen, A.; Haapasalo, H. Product Life Cycle, Technology Life Cycle and Market Life Cycle; Similarities, Differences and Applications. In Proceedings of the MakeLearn and TIIM Joint International Conference 2015, Bari, Italy, 27–29 May 2015; pp. 1143–1151. [Google Scholar]

- Martinez, C.; Lawless, M.; O’Toole, C. The Determinants of SME Capital Structure across the Lifecycle. 2019. Available online: https://www.econstor.eu/handle/10419/193950 (accessed on 22 May 2021).

- Akbar, A.; Akbar, M.; Tang, W.; Qureshi, M.A. Is bankruptcy risk tied to corporate life-cycle? Evidence from Pakistan. Sustainability 2019, 11, 678. [Google Scholar] [CrossRef] [Green Version]

- Frank, M.; Goyal, V. Testing the pecking order theory of capital structure. J. Financ. Econ. 2003, 67, 217–248. [Google Scholar] [CrossRef] [Green Version]

- Frank, M.; Goyal, V. Capital structure decisions. SSRN 2003. [Google Scholar] [CrossRef]

- Opler, T.C.; Saron, M.; Titman, S. Designing capital structure to create shareholder value. J. Appl. Corp. 1997, 10, 21–32. [Google Scholar] [CrossRef]

- Javadi, S.M.; Alimoradi, A.; Ashtiani, M. Relationship between Financial Leverage and Firm Growth in the Oil and Gas Industry: Evidence from OPEC. Pet. Bus. Rev. 2017, 1, 9–21. [Google Scholar]

- Hwang, J.Y.T.; Qi, G.Z.; Hamdan, R.; Liwan, A.; Hui, J.K.S.; Razali, M.W.B.M.; Abdullah, M.A.B. The Effects of Ownership Structures on Firm Information Asymmetry in Malaysia. Int. J. Acad. Res. Bus. Soc. Sci. 2019, 9, 950–977. [Google Scholar] [CrossRef] [Green Version]

- Huang, S.Y.; Chung, Y.-H.; Chiu, A.-A.; Chen, Y.-C. Growth opportunity and risk: Empirical investigation on earnings management decision. Invest. Manag. Financ. Innov. 2015, 12, 299–309. [Google Scholar]

- Trong, N.N.; Nguyen, C.T. Firm performance: The moderation impact of debt and dividend policies on overinvestment. J. Asian Bus. Econ. Stud. 2020. preprint. [Google Scholar] [CrossRef]

- Almazan, A.; Molina, C.A. Intra-industry capital structure dispersion. J. Econ. Manag. Strat. 2005, 14, 263–297. [Google Scholar] [CrossRef]

- Bhama, V.; Jain, P.K.; Yadav, S.S. Relationship between the pecking order theory and firm’s age: Empirical evidences from India. IIMB Manag. Rev. 2018, 30, 104–114. [Google Scholar] [CrossRef]

- Martono, S.; Yulianto, A.; Witiastuti, R.S.; Wijaya, A.P. The role of institutional ownership and industry characteristics on the propensity to pay dividend: An insight from company open innovation. J. Open Innov. Technol. Mark. Complex. 2020, 6, 74. [Google Scholar] [CrossRef]

- Gujarati, D.; Porter, D. Basic Econometrics; McGraw Hill: Boston, MA, USA, 2014. [Google Scholar]

- Yoo, J.; Lee, S.; Park, S. The effect of firm life cycle on the relationship between R & D expenditures and future performance, earnings uncertainty, and sustainable growth. Sustainability 2019, 11, 2371. [Google Scholar] [CrossRef] [Green Version]

- Lofgren, K.; Persson, T.; Weibull, J.W. Markets with Asymmetric Information: The Contributions of George Akerlof, Michael Spence and Joseph Stiglitz. Scand. J. Econ. 2002, 104, 195–211. [Google Scholar] [CrossRef]

- Jensen, M. Agency costs of free cash flow, corporate finance, and takeovers. Am. Econ. Rev. 1986, 76, 323–329. [Google Scholar]

- Warjiyo, P. Indonesia: Changing Patterns of Financial Intermediation and Their Implications for Central Bank Policy; Bank of Indonesia: Jakarta, Indonesia, 2015. [Google Scholar]

- Securities Exchange Act. Secruties Exchange Act No. 8; 1995. Available online: https://law.moj.gov.tw/ENG/LawClass/LawAll.aspx?pcode=G0400001 (accessed on 20 May 2021).

- Brito, J.A.; John, K. Leverage and Growth Opportunities: Risk-Avoidance Induced by Risky Debt. SSRN Electron. J. 2002. [Google Scholar] [CrossRef] [Green Version]

- Wijantini, W. Voluntary Disclosure in the Annual Reports of Financially Distressed Companies in Indonesia. Gadjah Mada Int. J. Bus. 2006, 8, 343. [Google Scholar] [CrossRef]

Figure 1.

Relationship between Technology Life Cycle and Open Innovation.

{kind=link}

Table 1.

Cashflow patterns for each life cycle stage.

| Cashflow | Introduction | Growth | Mature | Shake out | Decline |

|---|---|---|---|---|---|

| Operating | − | + | + | Void in theory | − |

| Invest | − | − | − | Void in theory | + |

| Financing | + | + | − | Void in theory | + or |

Table 2.

Multicollinearity test result among variables.

| Panel A | Correlation Matrix | ||||

|---|---|---|---|---|---|

| Leverage | Growth | Size | Profitability | Risk-Specific | |

| Leverage | 1 | ||||

| Growth Ops. | 0.002446 | 1 | |||

| Size | 0.12642 | 0.01661 | 1 | ||

| Profitability | 0.24849 | 0.118867 | 0.114479 | 1 | |

| Risk−Specific | 0.020752 | 0.02165 | 0.06079 | 0.36919 | 1 |

| Panel B | VIF Factors | ||||

| Variables | VIF | ||||

| Growth Ops. | 1.096 | ||||

| Size | 1.017 | ||||

| Profitability | 1.042 | ||||

| Risk−Specific | 1.109 | ||||

Table 3.

Descriptive Statistics and Mean Differences.

| Panel A | Descriptive Statistics | ||||||||

| Life Cycle | Obs | Variables | Mean | 25th Quartile | Median | 75th Quartile | St. Dev | Kurtosis | Skewness |

| Introduction | 692 | Leverage | 0.456 | 0.284 | 0.458 | 0.611 | 0.222 | 2069 | 0.511 |

| 692 | Growth Ops. | 0.169 | 0.035 | 0.109 | 0.267 | 0.393 | 6.008 | 1894 | |

| 692 | Size | 28,250 | 27,328 | 28,287 | 29,219 | 1420 | 11,362 | 1.121 | |

| 692 | Profitability | 0.035 | 0.003 | 0.035 | 0.075 | 0.089 | 15,951 | 1604 | |

| 692 | Risk−Specific | 0.008 | 0.000 | 0.001 | 0.005 | 0.033 | 235,562 | 13,538 | |

| Growth | 1682 | Leverage | 0.486 | 0.321 | 0.475 | 0.637 | 0.217 | 0.131 | 0.326 |

| 1682 | Growth Ops. | 0.122 | 0.050 | 0.079 | 0.221 | 0.323 | 8,411 | 2.085 | |

| 1682 | Size | 28,442 | 27,190 | 28,507 | 29,677 | 1761 | 0.050 | 0.134 | |

| 1682 | Profitability | 0.029 | 0.001 | 0.028 | 0.070 | 0.131 | 214,966 | 9860 | |

| 1682 | Risk−Specific | 0.017 | 0.000 | 0.001 | 0.006 | 0.254 | 1,302,150 | 34,864 | |

| Mature | 969 | Leverage | 0.484 | 0.302 | 0.479 | 0.616 | 0.248 | 6.441 | 1283 |

| 969 | Growth Ops. | 0.093 | 0.031 | 0.072 | 0.175 | 0.262 | 9.817 | 1881 | |

| 969 | Size | 28,626 | 27.375 | 28,560 | 29,962 | 1.858 | 0.212 | 0.099 | |

| 969 | Profitability | 0.061 | 0.009 | 0.045 | 0.098 | 0.141 | 37,755 | 2.342 | |

| 969 | Risk−Specific | 0.021 | 0.000 | 0.002 | 0.008 | 0.129 | 460,111 | 19,271 | |

| Total | 3343 | Leverage | 0.479 | 0.308 | 0.473 | 0.629 | 0.228 | 3001 | 0.721 |

| 3343 | Growth Ops. | 0.123 | 0.041 | 0.081 | 0.217 | 0.324 | 8558 | 2092 | |

| 3343 | Size | 28,456 | 27,270 | 28,453 | 29,610 | 1730 | 1.150 | 0.129 | |

| 3343 | Profitability | 0.040 | 0.003 | 0.034 | 0.079 | 0.128 | 141,355 | 4.581 | |

| 3343 | Risk−Specific | 0.016 | 0.000 | 0.001 | 0.006 | 0.194 | 1,962,489 | 41,208 | |

| Panel B | Mean Differences | ||||||||

| Variables | Growth vs. Introduction | Mature vs. Growth | |||||||

| Leverage | 0.030 * | 0.002 | |||||||

| Growth Ops. | 0.047 * | 0.029 * | |||||||

| Size | 0.192 * | 0.185 * | |||||||

| Profitability | 0.006 * | 0.032 * | |||||||

| risk | 0.063 * | 0.004 | |||||||

* Significant at 0.05.

Table 4.

Regression Analysis.

| Variables | All Firms | All Firms | Introduction | Growth | Maturity |

|---|---|---|---|---|---|

| Constant | 0.479 * | 0.087 | 0.572 * | 0.089 | 0.042 |

| 0.000 | 0.160 | 0.000 | 0.265 | 0.713 | |

| Growth Op | 0.002 | 0.027 * | 0.015 | 0.033 * | 0.135 * |

| 0.888 | 0.019 | 0.437 | 0.034 | 0.000 | |

| Size | 0.021 * | 0.037 * | 0.021 * | 0.016 * | |

| 0.000 | 0.000 | 0.000 | 0.000 | ||

| Profitability | 0.536 * | 0.989 * | 0.815 * | 0.627 * | |

| 0.000 | 0.000 | 0.000 | 0.000 | ||

| Risk Specific | 0.094 * | 0.318 | 0.280 * | 0.514 * | |

| 0.000 | 0.198 | 0.000 | 0.000 | ||

| Obs | 3343 | 3343 | 692 | 1682 | 969 |

| F Test | 0.019 | 85,482 | 43,193 | 69,663 | 36,473 |

| Sig F Test | 0.888 | 0.000 | 0.000 | 0.000 | 0.000 |

| Multiple R | 0.002 | 0.305 | 0.448 | 0.377 | 0.363 |

| R Square | 0.000 | 0.093 | 0.201 | 0.142 | 0.131 |

* Significant at 0.05.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Yulianto, A.; Witiastuti, R.S.; Widiyanto. Debt versus Equity—Open Innovation to Reduce Asymmetric Information. J. Open Innov. Technol. Mark. Complex. 2021, 7, 181. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030181

AMA Style

Yulianto A, Witiastuti RS, Widiyanto. Debt versus Equity—Open Innovation to Reduce Asymmetric Information. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(3):181. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030181

Chicago/Turabian StyleYulianto, Arief, Rini Setyo Witiastuti, and Widiyanto. 2021. "Debt versus Equity—Open Innovation to Reduce Asymmetric Information" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 3: 181. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030181