User Innovativeness and Fintech Adoption in Indonesia

,

,  and

and

Abstract

:1. Introduction

2. Literature Reviews, Proposes Hypotheses, and Methodology

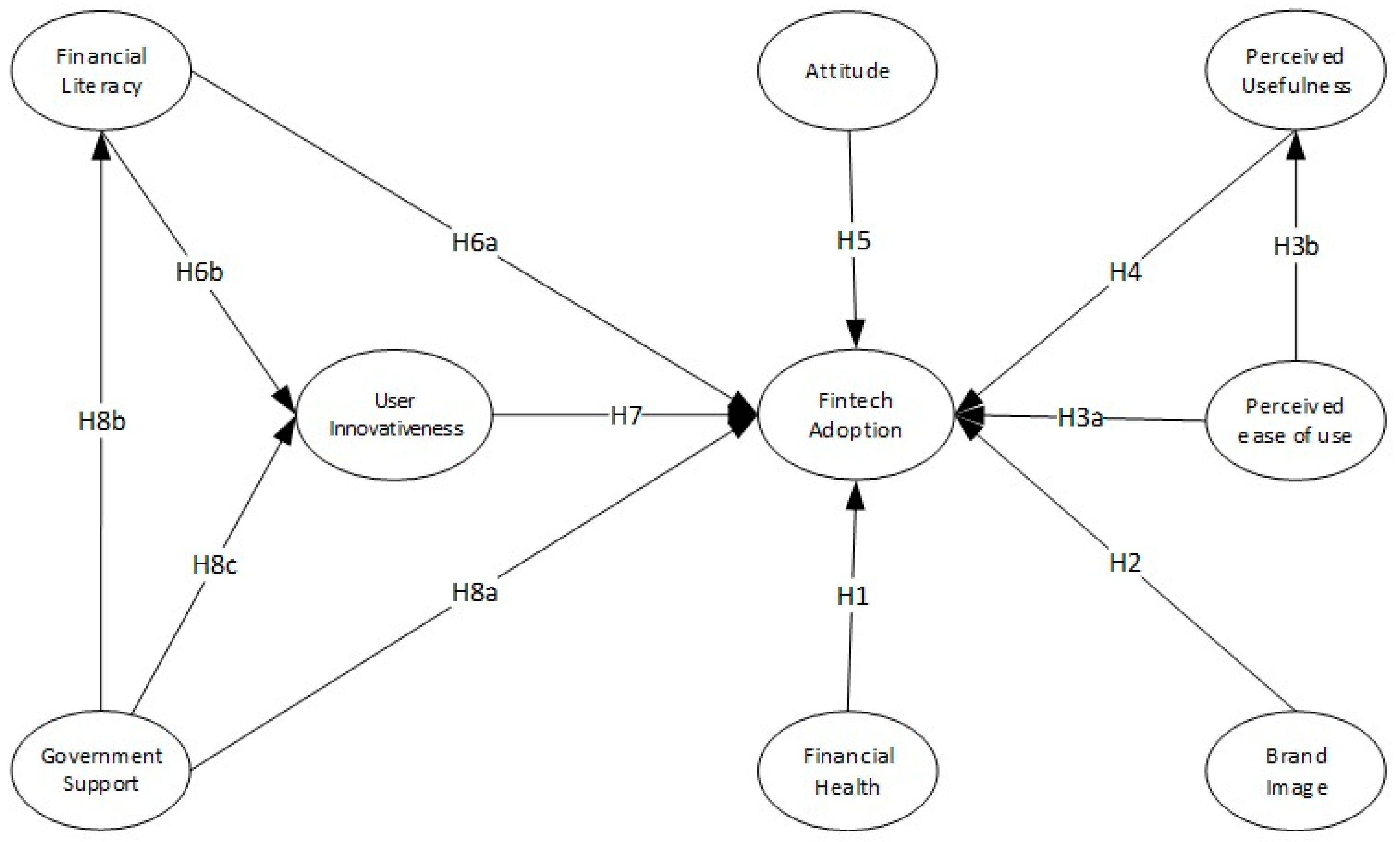

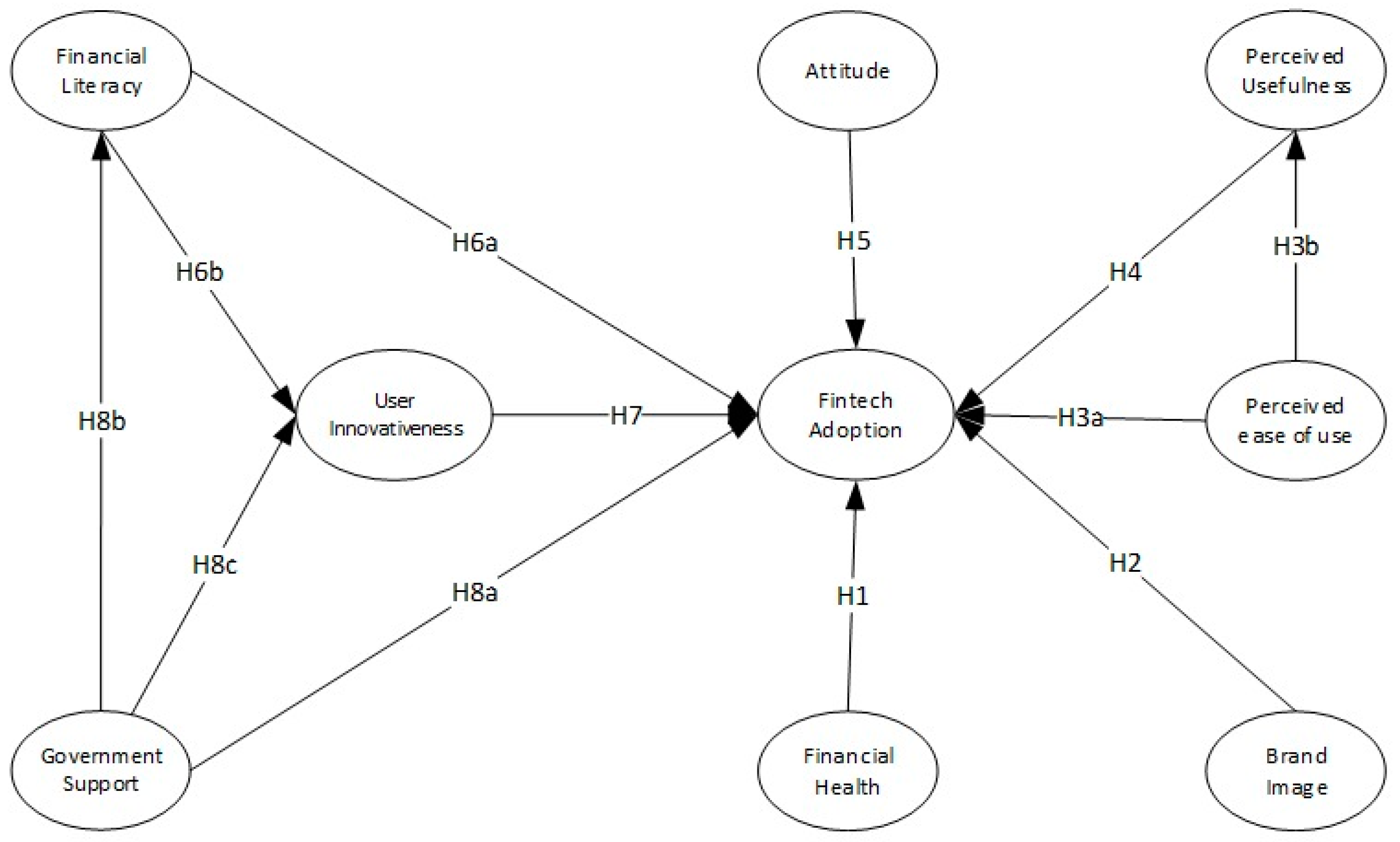

2.1. Literature Review and Proposes Hypotheses

2.2. The Determinants of Fintech Adoption

2.2.1. Financial Health (FH)

2.2.2. Brand Image (BI)

2.2.3. Perceived Ease to Use (PEU)

2.2.4. Perceived Usefulness (PU)

2.2.5. Attitude (AT)

2.2.6. Financial Literacy (FL)

2.2.7. User Innovativeness (UI)

2.2.8. Government Support (GS)

2.3. Methodology

3. Results

3.1. Characteristics of The Respondents

3.2. Results of the SEM Analysis

4. Discussion

4.1. Fintech Adoption in Indonesia

4.2. User Innovativeness on Fintech Adoption

5. Conclusions, Implications, Limitations, and Recommendations

5.1. Conclusions

5.2. Implications

5.3. Limitations and Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ryu, H.-S. Understanding Benefit and Risk Framework of Fintech Adoption: Comparison of Early Adopters and Late Adopters. In Proceedings of the 51st Hawaii International Conference on System Sciences, Hawaii, HI, USA, 3–6 January 2018; pp. 3864–3873. [Google Scholar] [CrossRef] [Green Version]

- Mention, A.L. The Future of Fintech. Res. Technol. Manag. 2019, 62, 59–63. [Google Scholar] [CrossRef]

- Demirguc-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S.; Hess, J. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution; World Bank Publications: Washington, DC, USA, 2018. [Google Scholar]

- Davis, K.; Maddock, R.; Foo, M. Catching up with indonesia’s fintech industry. Law Financ. Mark. Rev. 2017, 11, 33–40. [Google Scholar] [CrossRef]

- Frost, J. The economic forces driving fintech adoption across countries. In The Technological Revolution in Financial Services; University of Toronto Press: Toronto, ON, Canada, 2020; pp. 70–89. [Google Scholar] [CrossRef] [Green Version]

- Hudaefi, F.A. How does Islamic fintech promote the SDGs? Qualitative evidence from Indonesia. Qual. Res. Financ. Mark. 2020, 12, 353–366. [Google Scholar] [CrossRef]

- Yun, J.H.J.; Zhao, X.; Jung, K.H.; Yigitcanlar, T. The culture for open innovation dynamics. Sustainability 2020, 12, 5076. [Google Scholar] [CrossRef]

- Faraj, S.; Pachidi, S. Beyond Uberization: The co-constitution of technology and organizing. Organ. Theory 2021, 2. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Karjaluoto, K. Mobile banking adoption: A literature review. Telemat. Inform. 2015, 32, 129–142. [Google Scholar] [CrossRef] [Green Version]

- Teo, T.; Ursavaş, Ö.F.; Bahçekapili, E. Efficiency of the technology acceptance model to explain pre-service teachers’ intention to use technology: A Turkish study. Campus-Wide Inf. Syst. 2011, 28, 93–101. [Google Scholar] [CrossRef]

- Davis, G.F.; Sinha, A. Varieties of Uberization: How technology and institutions change the organization(s) of late capitalism. Organ. Theory 2021, 2, 263178772199519. [Google Scholar] [CrossRef]

- Rogers, E.M.; Singhal, A.; Quinlan, M.M. Diffusion of innovations. In An Integrated Approach to Communication Theory and Research; Taylor & Francis Group: Abingdon, UK, 2019. [Google Scholar]

- Ayub, A.F.M.; Zaini, S.H.; Luan, W.S.; Jaafar, W.M.W. The Influence of Mobile Self-efficacy, Personal Innovativeness and Readiness towards Students’ Attitudes towards the use of Mobile Apps in Learning and Teaching. Int. J. Acad. Res. Bus. Soc. Sci. 2018, 7, 364–374. [Google Scholar] [CrossRef]

- Yoon, C.; Lim, D. An empirical study on factors affecting customers’ acceptance of internet-only banks in Korea. Cogent Bus. Manag. 2020, 7, 1792259. [Google Scholar] [CrossRef]

- Von Hippel, E.; Jin, C. The major shift towards user-centred innovation. J. Knowl. Based Innov. China 2008, 1, 16–27. [Google Scholar] [CrossRef]

- Arner, D.W.; Barberis, J.; Buckley, R.P. 150 years of Fintech: An evolutionary analysis. Jassa Finsia J. Appl. Financ. 2016, 3, 22–29. [Google Scholar]

- Singh, T. Fintech Adoption: A Critical Appraisal of the Strategies of Paytm in India. IUP J. Manag. Res. 2020, 19, 7–17. [Google Scholar]

- Moufakkir, M.; Mohammed, Q. The Nexus Between FinTech Adoption and Financial Inclusion. In Impact of Financial Technology (FinTech) on Islamic Finance and Financial Stability; IGI Global: Hershey, PA, USA, 2020. [Google Scholar]

- Haqqi, F.R.; Suzianti, A. Exploring Risk and Benefit Factors Affecting User Adoption Intention of Fintech in Indonesia. In Proceedings of the 3rd Asia Pacific Conference on Research in Industrial and Systems Engineering, Depok, Indonesia, 16–17 June 2020; pp. 13–18. [Google Scholar] [CrossRef]

- Christian, S.; Wiradinata, T.; Herdinata, C.; Setiobudi, A. Environmental Factors Affecting the Acceleration of Financial Technology (Fintech) Adoption by SMEs in the East Java Region. Adv. Econ. Bus. Manag. Res. 2020, 145, 380–385. [Google Scholar] [CrossRef]

- Ernst & Young, Global FinTech Adoption Index 2019. Available online: https://www.ey.com/en_gl/ey-global-fintech-adoption-index (accessed on 11 August 2021).

- Ryu, H.S. What makes users willing or hesitant to use Fintech? The moderating effect of user type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Dermody, J.; Yun, J.H.J.; Della Corte, V. Innovations to advance sustainability behaviours. Serv. Ind. J. 2019, 39, 1029–1033. [Google Scholar] [CrossRef] [Green Version]

- Yoshino, N.; Morgan, P.J.; Long, T.Q. Financial Literacy and Fintech Adoption in Japan. 2020, p. 1095. Available online: https://www.adb.org/sites/default/files/publication/616781/adbi-wp1154.pdf (accessed on 7 June 2021).

- Morgan, P.J.; Trinh, L.Q. FinTech and Financial Literacy in Vietnam; ADBI Working Paper Series; Asian Development Bank Institute: Tokyo, Japan, 2020; pp. 1–23. [Google Scholar]

- Davis, F.D. A Technology Acceptance Model for Empirically Testing New End-User Information Systems: Theory and Results. Ph.D. Thesis, Sloan School of Management, Cambridge, MA, USA, 1985. [Google Scholar]

- Gidhagen, M.; Persson, S.G. Determinants of digitally instigated insurance relationships. Int. J. Bank Mark. 2011, 29, 517–534. [Google Scholar] [CrossRef]

- Akturan, U.; Tezcan, N. Mobile banking adoption of the youth market: Perceptions and intentions. Mark. Intell. Plan. 2012, 30, 444–459. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry 2019, 11, 340. [Google Scholar] [CrossRef] [Green Version]

- Guth, K. The SAGE Encyclopedia of Corporate Reputation. SAGE Encycl. Corp. Reput. 2016, 2016. [Google Scholar] [CrossRef] [Green Version]

- Teigland, R.; Siri, S.; Larsson, A.; Puertas, A.M.; Bogusz, C.I. Introduction. Rise Dev. FinTech 2020, 1–18. [Google Scholar] [CrossRef]

- Braido, G.M. AIS Electronic Library (AISeL) Digital Entrepreneurship and Institutional Changes: Fintechs in the Brazilian Mobile Payment System; Academy of Management: Briarcliff Manor, NY, USA, 2020. [Google Scholar]

- Joo, S. Personal Financial Wellness. In Handbook of Consumer Finance Research; Springer: New York, USA, 2008. [Google Scholar]

- Anand, S.; Mishra, K.; Verma, V.; Taruna, T. Financial literacy as a mediator of personal financial health during COVID-19: A structural equation modelling approach. Emerald Open Res. 2020, 2. [Google Scholar] [CrossRef]

- Riyadh, A.N.; Bunker, D.; Rabhi, F. Barriers to E-Finance Adoption in Small and Medium Sized Enterprises (SMEs) in Bangladesh. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1726262 (accessed on 11 August 2021).

- Brexendorf, T.O.; Keller, K.L. Leveraging the corporate brand. Eur. J. Mark. 2017, 51, 1530–1551. [Google Scholar] [CrossRef]

- Caviggioli, F.; Lamberti, L.; Landoni, P.; Meola, P. Technology adoption news and corporate reputation: Sentiment analysis about the introduction of Bitcoin. J. Prod. Brand Manag. 2020, 29, 877–897. [Google Scholar] [CrossRef]

- Kanchanatanee, K.; Suwanno, N.; Jarernvongrayab, A. Effects of Attitude toward Using, Perceived Usefulness, Perceived Ease of Use and Perceived Compatibility on Intention to Use E-Marketing. J. Manag. Res. 2014, 6, 1. [Google Scholar] [CrossRef] [Green Version]

- Niu, G.; Wang, Q.; Zhou, Y. Education and FinTech Adoption: Evidence from China. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3765224 (accessed on 7 June 2021).

- Chen, Y.H.; Barnes, S. Initial trust and online buyer behaviour. Ind. Manag. Data Syst. 2007, 107, 21–36. [Google Scholar] [CrossRef]

- Jaruwachirathanakul, B.; Fink, D. Internet banking adoption strategies for a developing country: The case of Thailand. Internet Res. 2005, 15, 295–311. [Google Scholar] [CrossRef]

- Elhajjar, S.; Ouaida, F. An analysis of factors affecting mobile banking adoption. Int. J. Bank Mark. 2019, 38, 352–367. [Google Scholar] [CrossRef]

- Singh, S.; Sahni, M.M.; Kovid, R.K. What drives FinTech adoption? A multi-method evaluation using an adapted technology acceptance model. Manag. Decis. 2020, 58, 1675–1697. [Google Scholar] [CrossRef]

- Ajzen, I. Attitude theory and the attitude-behavior relation. In New Directions in Attitude Measurement; Krebs, D., Schmidt, P., Eds.; Walter de Gruyter: Berlin, Germany, 1993; pp. 41–57. [Google Scholar]

- Grabner-Kräuter, S.; Faullant, R. Consumer acceptance of internet banking: The influence of internet trust. Int. J. Bank Mark. 2008, 26, 483–504. [Google Scholar] [CrossRef]

- Chuang, L.-M.; Liu, C.-C.; Kao, H.-K. The Adoption of Fintech Service: TAM perspective. Int. J. Manag. Adm. Sci. IJMAS 2016, 3, 1–15. [Google Scholar]

- Lusardi, A. Financial literacy and the need for financial education: Evidence and implications. Swiss J. Econ. Stat. 2019, 155, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Jünger, M.; Mietzner, M. Banking goes digital: The adoption of FinTech services by German households. Financ. Res. Lett. 2020, 34, 101260. [Google Scholar] [CrossRef]

- Liu, B.; Wang, J.; Chan, K.C.; Fung, A. The impact of entrepreneurs’s financial literacy on innovation within small and medium-sized enterprises. Int. Small Bus. J. Res. Entrep. 2021, 39, 228–246. [Google Scholar] [CrossRef]

- Lu, J.; Yao, J.E.; Yu, C.S. Personal innovativeness, social influences and adoption of wireless Internet services via mobile technology. J. Strateg. Inf. Syst. 2005, 14, 245–268. [Google Scholar] [CrossRef]

- Morosan, C.; DeFranco, M. When tradition meets the new technology: An examination of the antecedents of attitudes and intentions to use mobile devices in private clubs. Int. J. Hosp. Manag. 2014, 42, 126–136. [Google Scholar] [CrossRef]

- Zhang, T.; Lu, C.; Kizildag, M. Banking ‘on-the-go’: Examining consumers’ adoption of mobile banking services. Int. J. Qual. Serv. Sci. 2018, 10, 279–295. [Google Scholar] [CrossRef]

- Goo, J.J.; Heo, J.Y. The impact of the regulatory sandbox on the fintech industry, with a discussion on the relation between regulatory sandboxes and open innovation. J. Open Innov. Technol. Mark. Complex. 2020, 6, 43. [Google Scholar] [CrossRef]

- Marakarkandy, B.; Yajnik, N.; Dasgupta, C. Enabling internet banking adoption: An empirical examination with an augmented technology acceptance model (TAM). J. Enterp. Inf. Manag. 2017, 30, 263–294. [Google Scholar] [CrossRef]

- Loehlin, J.C.; Beaujean, A.A. Latent Variable Models: An Introduction to Factor, Path, and Structural Equation Analysis; Taylor & Francis: Abingdon, UK, 2016. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis. Vectors 2010. [Google Scholar] [CrossRef]

- Patel, K.; Patel, H.J. Adoption of internet banking services in Gujarat: An extension of TAM with perceived security and social influence. Int. J. Bank Mark. 2017, 36, 147–169. [Google Scholar] [CrossRef]

- Hair, J.F.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.; Sarstedt, M. A New Criterion for Assessing Discriminant Validity in Variance-based Structural Equation Modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Association of Indonesian Internet Service Providers. Laporan Survey Internet APJII 2019-2020 (Q2). 2020. Available online: https://apjii.or.id/survei2019x/kirimlink (accessed on 12 August 2021).

- Meyliana, M.; Fernando, E.; Surjandy, S. The Influence of Perceived Risk and Trust in Adoption of FinTech Services in Indonesia. CommIT Commun. Inf. Technol. J. 2019, 13, 31–37. [Google Scholar] [CrossRef] [Green Version]

- Lien, N.T.K.; Doan, T.T.T.; Bui, T.N. Fintech and banking: Evidence from Vietnam. J. Asian Financ. Econ. Bus. 2020, 7. [Google Scholar] [CrossRef]

- Tun-Pin, C.; Keng-Soon, W.C.; Yen-San, Y.; Pui-Yee, C.; Hong-Leong, N.; Shwu-Shing, J.T. An Adoption of Fintech Service in Malaysia. South East Asia J. Contemp. Bus. Econ. Law 2019, 18, 134–147. [Google Scholar]

- Celik, K. The Relationship between Individual Innovativeness and Self-efficacy Levels of Student Teachers. Int. J. Sci. Res. Educ. 2013, 6, 56–67. [Google Scholar]

- Pratoom, K.; Savatsomboon, G. Explaining factors affecting individual innovation: The case of producer group members in Thailand. Asia Pac. J. Manag. 2012, 29, 1063–1087. [Google Scholar] [CrossRef] [Green Version]

- Aldahdouh, T.Z.; Korhonen, V.; Nokelainen, P. What contributes to individual innovativeness? A multilevel perspective. Int. J. Innov. Stud. 2019, 3, 23–39. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| No | Construct Variable | Reference | Indicator | Indicator Code |

|---|---|---|---|---|

| 1 | Fintech Adoption | [54,57] | I will continue using Fintech service | FA1 |

| I haven’t used but would like to use Fintech services soon | FA2 | |||

| I will recommend Fintech services to my friends | FA3 | |||

| 2 | Financial Health | [25,34] | My earnings are reduced and savings eroded due to pandemic COVID-19 | FH1 |

| Impulsive use of credit card is happening | FH2 | |||

| Forced to do panic buying and hoarding products | FH3 | |||

| There is a rise in prices of essential goods | FH4 | |||

| Tend to withdraw cash more often now | FH5 | |||

| 3 | Brand Image | [29,37] | I prefer to accept the Fintech services provided by familiar brands | BI1 |

| Fintech overall has a good reputation | BI2 | |||

| I can recognize Fintech services in Indonesia | BI3 | |||

| 4 | Perceived Ease to Use | [29,38,39] | It is easy to use Fintech services | PEU1 |

| I think the operation interface of Fintech is friendly and understandable | PEU2 | |||

| It is easy to have device to use Fintech services (cellphone, APP, WIFI, et al.) | PEU3 | |||

| 5 | Fintech Perceived Usefulness | [42,43] | Using Fintech can meet my service needs | FPU1 |

| Fintech services can save time | FPU2 | |||

| Fintech services can improve efficiency | FPU3 | |||

| Overall, Fintech services are useful to me | FPU4 | |||

| 6 | Attitude | [29,45,46] | I believe using Fintech services is a good idea | Att1 |

| Using Fintech services gives me pleasant experience | Att2 | |||

| I am interested in Fintech services | Att3 | |||

| 7 | Financial Literacy | [47,48] | I have knowledge of compounding interest | FL1 |

| I have knowledge of inflation | FL2 | |||

| I have knowledge of risk diversification | FL3 | |||

| 8 | User Innovativeness | [52] | When I hear about a new product, I look for ways to try it | FI1 |

| Among my peers, I am usually the first one to try a new product | FI2 | |||

| I like to experiment with new Fintech services | FI3 | |||

| 9 | Government Support | [53,54] | The government support and improve the use of Fintech services | GS1 |

| The government has introduced favorable legislation and regulations for Fintech services | GS2 | |||

| The government is active in setting up all kinds of infrastructure such as telecom network which has a positive role in promoting Fintech services | GS3 |

| Characteristic | Criteria | Frequency (n = 485) | Percentage (%) |

|---|---|---|---|

| Gender | Male | 184 | 37.9% |

| Female | 301 | 62.1% | |

| Age | 18–25 | 203 | 41.9% |

| 26–35 | 147 | 30.3% | |

| 36–45 | 124 | 25.6% | |

| >45 | 11 | 2.3% | |

| Education | High School | 178 | 36.7% |

| Bachelor’s Degree | 208 | 42.9% | |

| Master’s or Doctorate Degree | 99 | 20.4% | |

| Net Income | <3 million IDR | 177 | 36.5% |

| 3–5 million IDR | 96 | 19.8% | |

| 6–10 million IDR | 91 | 18.8% | |

| >10 million IDR | 121 | 24.9% | |

| Experience using Fintech | never use | 76 | 15.7% |

| one time | 163 | 33.6% | |

| 2–3 times | 108 | 22.3% | |

| >4 times | 138 | 28.5% |

| No | Construct Variable | Indicator | Code | Mean | Std. Deviation |

|---|---|---|---|---|---|

| 1 | Fintech Adoption | I will continue using Fintech service | FA1 | 3.7897 | 0.9432 |

| I haven’t used but would like to use Fintech services soon | FA2 | 3.1052 | 1.3092 | ||

| I will recommend Fintech services to my friends | FA3 | 3.6825 | 0.9970 | ||

| 2 | Financial Health | My earnings are reduced and savings eroded due to pandemic COVID-19 | FH1 | 3.6062 | 1.2967 |

| Impulsive use of credit card is happening | FH2 | 2.7876 | 1.3735 | ||

| Forced to do panic buying and hoarding products | FH3 | 2.3567 | 1.3231 | ||

| There is a rise in prices of essential goods | FH4 | 3.6309 | 1.1436 | ||

| Tend to withdraw cash more often now | FH5 | 2.9340 | 1.2759 | ||

| 3 | Brand Image | I prefer to accept the Fintech services provided by familiar brands | BI1 | 4.1381 | 0.9423 |

| Fintech overall has a good reputation | BI2 | 3.9237 | 0.8082 | ||

| I can recognize Fintech services in Indonesia | BI3 | 3.8660 | 0.8747 | ||

| 4 | Perceived Ease to Use | It is easy to use Fintech services | PEU1 | 4.2289 | 0.8401 |

| I think the operation interface of Fintech is friendly and understandable | PEU2 | 4.0268 | 0.9345 | ||

| It is easy to have device to use Fintech services (cellphone. APP, WIFI, et al.) | PEU3 | 4.3052 | 0.8167 | ||

| 5 | Fintech Perceived Usefulness | Using Fintech can meet my service needs | FPU1 | 3.8330 | 1.0138 |

| Fintech services can save time | FPU2 | 4.2825 | 0.8934 | ||

| Fintech services can improve efficiency | FPU3 | 4.1299 | 0.9235 | ||

| Overall, Fintech services are useful to me | FPU4 | 4.1691 | 0.9138 | ||

| 6 | Attitude | I believe using Fintech services is a good idea | Att1 | 3.7753 | 0.8913 |

| Using Fintech services gives me pleasant experience | Att2 | 3.8000 | 0.8903 | ||

| I am interested in Fintech services | Att3 | 3.8577 | 0.9284 | ||

| 7 | Financial Literacy | I have knowledge of compounding interest | FL1 | 3.1464 | 1.2420 |

| I have knowledge of inflation | FL2 | 3.6969 | 1.0409 | ||

| I have knowledge of risk diversification | FL3 | 3.3381 | 1.1875 | ||

| 8 | User Innovativeness | When I hear about a new product, I look for ways to try it | FI1 | 3.4598 | 1.0587 |

| Among my peers, I am usually the first one to try a new product | FI2 | 3.0722 | 1.1735 | ||

| I like to experiment with new Fintech services | FI3 | 3.1093 | 1.1599 | ||

| 9 | Government Support | The government support and improve the use of Fintech services | GS1 | 3.8619 | 0.8403 |

| The government has introduced favorable legislation and regulations for Fintech services | GS2 | 3.7649 | 0.8470 | ||

| The government is active in setting up all kinds of infrastructure such as telecom network which has a positive role in promoting Fintech services | GS3 | 3.7320 | 0.9104 |

| Construct | Outer Loadings | Cronbrach Alpha’s | Composite Reliability | Average Variance Extracted (AVE) |

|---|---|---|---|---|

| Fintech Adoption (Intention) | 0.8066 | 0.9117 | 0.8378 | |

| FA1 | 0.9221 | |||

| FA3 | 0.9085 | |||

| Financial Health | 0.7905 | 0.8756 | 0.7016 | |

| FH2 | 0.8797 | |||

| FH3 | 0.8417 | |||

| FH5 | 0.7890 | |||

| Brand Image | 0.7952 | 0.8797 | 0.7095 | |

| BI1 | 0.7848 | |||

| BI2 | 0.8786 | |||

| BI3 | 0.8606 | |||

| Perceived Ease to Use | 0.8761 | 0.9237 | 0.8015 | |

| PEU1 | 0.9085 | |||

| PEU2 | 0.8814 | |||

| PEU3 | 0.8956 | |||

| Fintech Perceived Usefulness | 0.8697 | 0.9200 | 0.7931 | |

| FPU1 | 0.8774 | |||

| FPU3 | 0.8963 | |||

| FPU4 | 0.8978 | |||

| Attitude | 1 | 1 | 1 | |

| Att1 | 1 | |||

| Financial Literacy | 0.8279 | 0.8970 | 0.7440 | |

| FL1 | 0.8800 | |||

| FL2 | 0.8317 | |||

| FL3 | 0.8751 | |||

| User Innovativeness | 0.8728 | 0.9218 | 0.7972 | |

| FI1 | 0.8725 | |||

| FI2 | 0.9097 | |||

| FI3 | 0.8960 | |||

| Government Support | 0.8566 | 0.9128 | 0.7774 | |

| GS1 | 0.8815 | |||

| GS2 | 0.9126 | |||

| GS3 | 0.8499 |

| AT | BI | FA | FH | FL | PEU | FPU | GS | |

|---|---|---|---|---|---|---|---|---|

| AT | ||||||||

| BI | 0.678 | |||||||

| FI | 0.822 | 0.839 | ||||||

| FH | 0.224 | 0.170 | 0.271 | |||||

| FL | 0.371 | 0.444 | 0.506 | 0.206 | ||||

| PEU | 0.563 | 0.857 | 0.703 | 0.090 | 0.410 | |||

| FPU | 0.704 | 0.794 | 0.834 | 0.085 | 0.453 | 0.866 | ||

| GS | 0.610 | 0.826 | 0.716 | 0.323 | 0.393 | 0.646 | 0.638 | |

| US | 0.587 | 0.564 | 0.669 | 0.513 | 0.461 | 0.399 | 0.411 | 0.623 |

| Construct | VIF | Construct | VIF |

|---|---|---|---|

| Fintech Adoption (Intention) | Attitude | ||

| FA1 | 1.84102519 | Att1 | 1 |

| FA3 | 1.84102519 | ||

| Financial Health | Financial Literacy | ||

| FH2 | 1.69585048 | FL1 | 2.03073350 |

| FH3 | 1.84267147 | FL2 | 1.67142607 |

| FH5 | 1.54717257 | FL3 | 2.15740800 |

| Brand Image | User Innovativeness | ||

| BI1 | 1.52589600 | FI1 | 2.01717081 |

| BI2 | 1.92993997 | FI2 | 2.90770523 |

| BI3 | 1.77368794 | FI3 | 2.52508112 |

| Perceived Ease to Use | Government Support | ||

| PEU1 | 2.57243586 | GS1 | 2.17803232 |

| PEU2 | 2.20288289 | GS2 | 2.60156244 |

| PEU3 | 2.43797089 | GS3 | 1.9426931 |

| Fintech Perceived Usefulness | |||

| FPU1 | 2.13003015 | ||

| FPU3 | 2.50413543 | ||

| FPU4 | 2.32382409 |

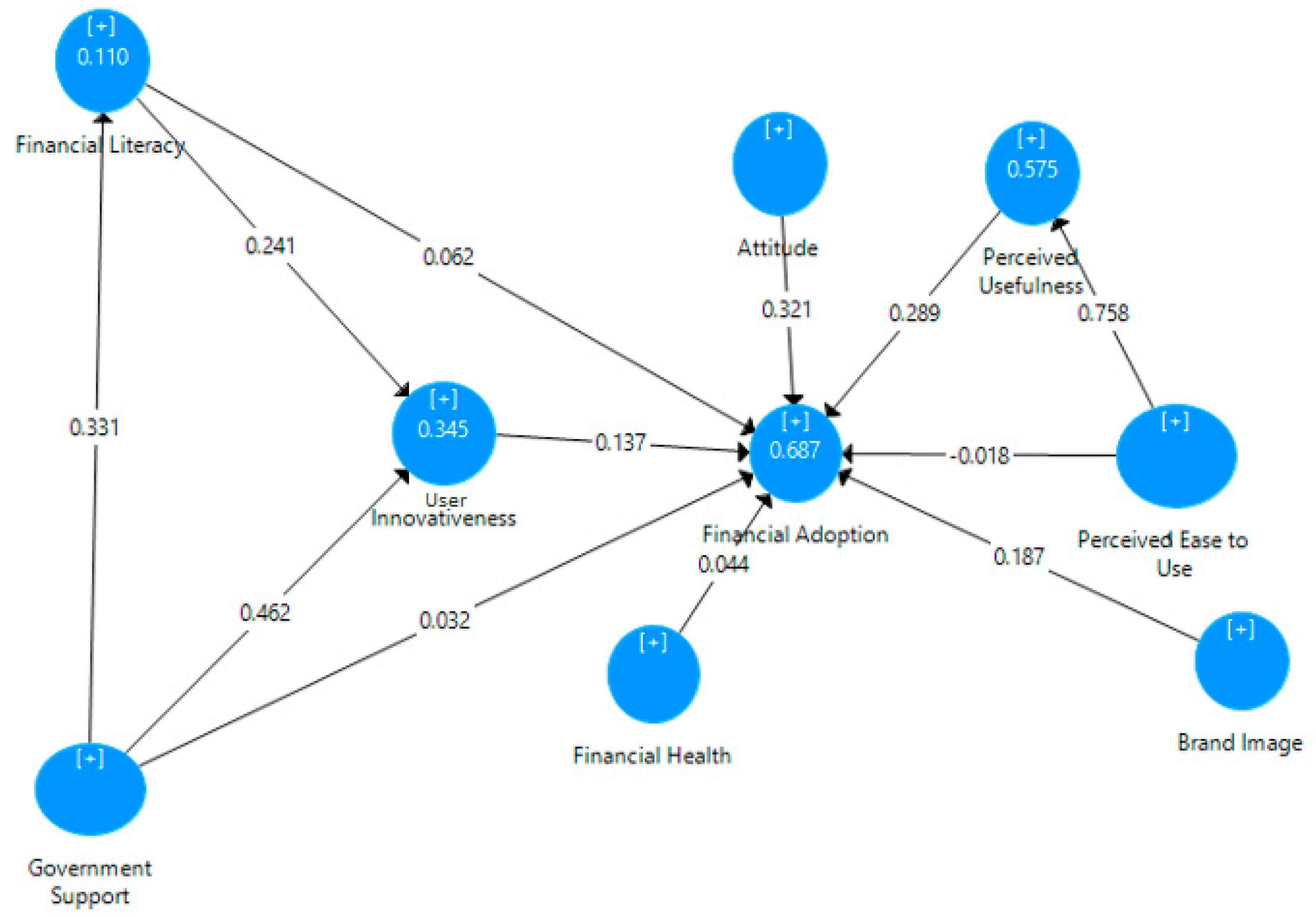

| R-Square | R-Square Adjusted | |

|---|---|---|

| Fintech Adoption | 0.687 | 0.682 |

| Financial Literacy | 0.110 | 0.108 |

| Fintech Perceived Usefulness | 0.575 | 0.574 |

| User Innovativeness | 0.345 | 0.342 |

| Hypotheses | Original Sample/β | p-Value | Decision | |

|---|---|---|---|---|

| H1 | Financial Health →Fintech Adoption | 0.0438 | 0.1355 | not supported |

| H2 | Brand Image →Fintech Adoption | 0.1872 | 0.0002 *** | supported |

| H3(a) | Perceived Ease to Use →Fintech Adoption | −0.0179 | 0.7248 | not supported |

| H3(b) | Perceived Ease to Use →Fintech Perceived Usefulness →Fintech Adoption | 0.2190 | 0 *** | supported |

| H4 | Fintech Perceived Usefulness →Fintech Adoption | 0.2889 | 0 *** | supported |

| H5 | Attitude →Fintech Adoption | 0.3206 | 0 *** | supported |

| H6(a) | Financial Literacy →Fintech Adoption | 0.0624 | 0.0318 ** | supported |

| H6(b) | Financial Literacy →User Innovativeness →Fintech Adoption | 0.0329 | 0.0018 *** | supported |

| H7 | User Innovativeness →Fintech Adoption | 0.1369 | 0.0001 *** | supported |

| H8(a) | Government Support →Fintech Adoption | 0.0317 | 0.4797 | not supported |

| H8(b) | Government Support →Financial Literacy →Fintech Adoption | 0.021 | 0.0494 ** | supported |

| H8(c) | Government Support →User Innovativeness →Fintech Adoption | 0.0632 | 0.0003 *** | supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Setiawan, B.; Nugraha, D.P.; Irawan, A.; Nathan, R.J.; Zoltan, Z. User Innovativeness and Fintech Adoption in Indonesia. J. Open Innov. Technol. Mark. Complex. 2021, 7, 188. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030188

Setiawan B, Nugraha DP, Irawan A, Nathan RJ, Zoltan Z. User Innovativeness and Fintech Adoption in Indonesia. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(3):188. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030188

Chicago/Turabian StyleSetiawan, Budi, Deni Pandu Nugraha, Atika Irawan, Robert Jeyakumar Nathan, and Zeman Zoltan. 2021. "User Innovativeness and Fintech Adoption in Indonesia" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 3: 188. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030188