Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services

Abstract

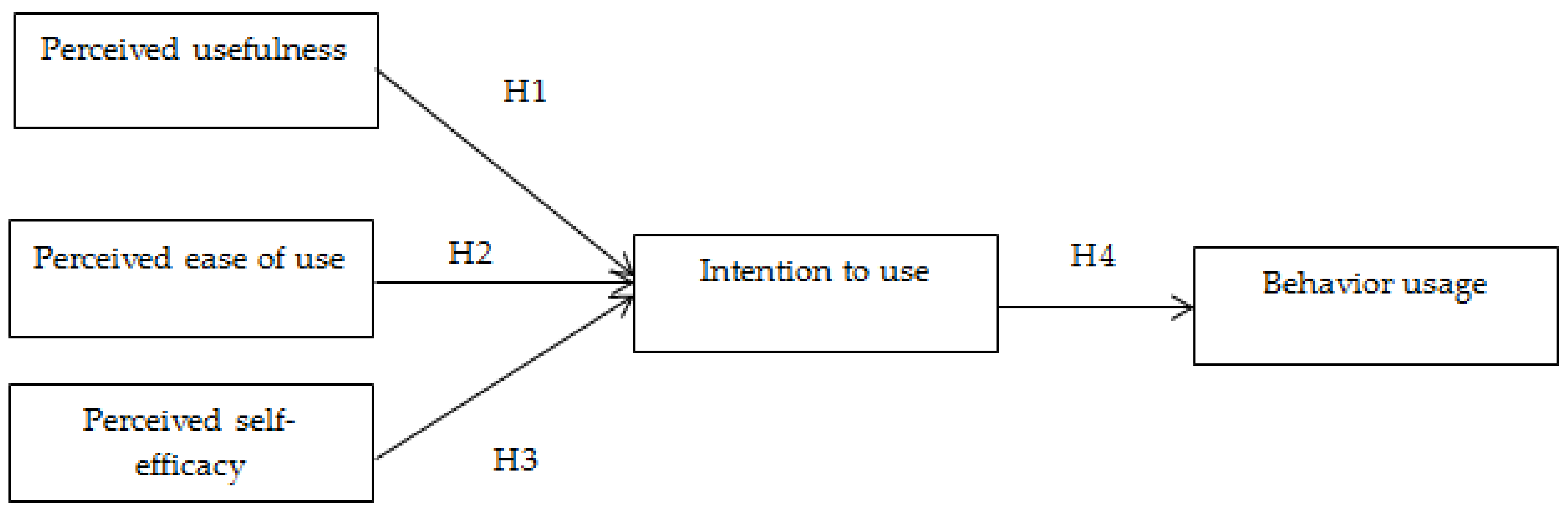

:1. Introduction

2. Materials and Methods

3. Methodology

4. Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Deng, X.; Huang, Z.; Cheng, X. FinTech and Sustainable Development: Evidence from China Based on P2P Data. Sustainability 2019, 11, 6434. [Google Scholar] [CrossRef] [Green Version]

- Shin, Y.J.; Choi, Y. Feasibility of the Fintech Industry as an Innovation Platform for Sustainable Economic Growth in Korea. Sustainability 2019, 11, 5351. [Google Scholar] [CrossRef] [Green Version]

- PRESSE BOX. Available online: https://www.pressebox.com/pressrelease/gartner-uk-ltd/Gartner-Says-Worldwide-Enterprise-IT-Spending-is-Forecast-to-Grow-2-5-Per-Cent-in-2013/boxid/555441 (accessed on 5 June 2020).

- Cziesla, T. A Literature Review on Digital Transformation in the Financial Service Industry. In Proceedings of the Bled eConference, Bled, Slovenia, 1–5 June 2014. [Google Scholar]

- Vial, G. Understanding digital transformation: A review and a research agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Yip, A.W.; Bocken, N.M. Sustainable business model archetypes for the banking industry. J. Clean. Prod. 2018, 174, 150–169. [Google Scholar] [CrossRef]

- Giatsidis, I.; Kitsios, F.; Kamariotou, M. Digital Transformation and User Acceptance of Information Technology in the Banking Industry. In Proceedings of the 8th International Symposium and 30th National Conference on Operational Research, Patra, Greece, 16–18 May 2019. [Google Scholar]

- Zhao, Q.; Tsai, P.H.; Wang, J.L. Improving financial service innovation strategies for enhancing China’s banking industry competitive advantage during the fintech revolution: A Hybrid MCDM model. Sustainability 2019, 11, 1419. [Google Scholar] [CrossRef] [Green Version]

- Moewes, T.; Puschmann, T.; Alt, R. Service-based Integration of IT-Innovations in Customer-Bank-Interaction. In Proceedings of the Internationale Tagung Wirtschaftsinformatik, Zurich, Switzerland, 16–18 February 2011. [Google Scholar]

- Ananda, S.; Devesh, S.; Lawati, A.M.A. What factors drive the adoption of digital banking? An empirical study from the perspective of Omani retail banking. J. Financ. Serv. Mark. 2020, 25, 14–24. [Google Scholar] [CrossRef]

- Boratyńska, K. Impact of digital transformation on value creation in Fintech Services: An innovative approach. J. Promot. Manag. 2019, 25, 631–639. [Google Scholar] [CrossRef]

- Breidbach, C.F.; Keating, B.W.; Lim, C. Fintech: Research directions to explore the digital transformation of financial service systems. J. Serv. Theory Pract. 2019, 30, 79–102. [Google Scholar] [CrossRef]

- Dratva, R. Is open banking driving the financial industry towards a true electronic market? Electron. Mark. 2020, 30, 65–67. [Google Scholar] [CrossRef]

- Hrustek, N.Ž.; Mekovec, R.; Pihir, I. Developing and validating measurement instrument for various aspects of digital economy: E-commerce, E-banking, E-work and E-employment. Int. J. E-Serv. Mob. Appl. 2019, 11, 50–67. [Google Scholar] [CrossRef]

- Khanboubi, F.; Boulmakoul, A. Digital transformation in the banking sector: Surveys exploration and analytics. Int. J. Inf. Syst. Chang. Manag. 2019, 11, 93–127. [Google Scholar] [CrossRef]

- Panda, A. Interview with Dr Anil K. Khandelwal: Leading Transformation of a Public Sector Bank Through People Processes and Building Intangibles. South Asian J. Hum. Resour. Manag. 2020, 7, 135–143. [Google Scholar] [CrossRef]

- Sibanda, W.; Ndiweni, E.; Boulkeroua, M.; Echchabi, A.; Ndlovu, T. Digital technology disruption on bank business models. Int. J. Bus. Perform. Manag. 2020, 21, 184–213. [Google Scholar] [CrossRef]

- Talbot, D.; Ordonez-Ponce, E. Canadian banks’ responses to COVID-19: A strategic positioning analysis. J. Sustain. Financ. Invest. 2020, in press. [Google Scholar] [CrossRef]

- Prensky, M. Digital natives, digital immigrants part 2. Horizon 2001, 9, 1–6. [Google Scholar] [CrossRef] [Green Version]

- Banker, R.; Chen, P.; Liu, F.; Ou, C. Business Value of IT in Commercial Banks. In Proceedings of the International Conference on Information Systems, Phoenix, AZ, USA, 15–18 December 2009. [Google Scholar]

- De Oliveira Santini, F.; Ladeira, W.J.; Sampaio, C.H.; Perin, M.G. Online banking services: A meta-analytic review and assessment of the impact of antecedents and consequents on satisfaction. J. Financ. Serv. Mark. 2018, 23, 168–178. [Google Scholar] [CrossRef]

- Sloboda, L.; Dunas, N.; Limański, A. Contemporary challenges and risks of retail banking development in Ukraine. Banks Bank Syst. 2018, 13, 88–97. [Google Scholar] [CrossRef] [Green Version]

- Cantoni, F.; Rossignoli, C. New Distribution Models for Financial Services: The Italian Banks’ Approach to the on Line Trading Development. J. Electron. Commer. Res. 2000, 1, 60–66. [Google Scholar]

- Dufty, N.F.; Savery, L.K.; Soutar, G.N. Banking industry employees and technological change. Prometheus 1987, 5, 284–303. [Google Scholar] [CrossRef]

- Brohman, M.K.; Copeland, D.G. Riverbank financial: Changing the role of information technology. J. Inf. Technol. 1999, 14, 287–293. [Google Scholar] [CrossRef]

- Ahmed, F.; Qin, Y.; Aduamoah, M. Employee readiness for acceptance of decision support systems as a new technology in E-business environments; A proposed research agenda. In Proceedings of the 7th International Conference on Industrial Technology and Management, ICITM 2018, Oxford, UK, 7–9 March 2018. [Google Scholar]

- Anand, V.V.; Banu, C.V.; Rengarajan, V.; Thirumoorthy, G.; Rajkumar, V.; Madhumith, R. Employee engagement- a study with special reference to bank employees in rural areas. Indian J. Sci. Technol. 2016, 9, 1–8. [Google Scholar] [CrossRef]

- Mishra, V.; Singh, V. Analyzing the gap in the adoption of Internet Banking Services: Managers’ perspective. In Proceedings of the 2nd International Conference on Business and Information Management, ICBIM 2014, Durgapur, West Bengal India, India, 9–11 January 2014. [Google Scholar]

- Chemingui, H. Resistance, motivations, trust and intention to use mobile financial services. Int. J. Bank Mark. 2013, 31, 574–592. [Google Scholar] [CrossRef]

- Scott, S.V.; Van Reenen, J.; Zachariadis, M. The long-term effect of digital innovation on bank performance: An empirical study of SWIFT adoption in financial services. Res. Policy 2017, 46, 984–1004. [Google Scholar] [CrossRef] [Green Version]

- Currie, W.L.; Willcocks, L. The New Branch Columbus project at Royal Bank of Scotland: The implementation of large-scale business process re-engineering. J. Strateg. Inf. Syst. 1996, 5, 213–236. [Google Scholar] [CrossRef]

- Angelopoulos, S.; Kitsios, F.; Babulac, E. From e to u: Towards an innovative digital era. In Heterogeneous Next Generation Networking: Innovations and Platform; Kotsopoulos, S., Ioannou, K., Eds.; IGI Global Publishing: Hershey, PA, USA, 2008; Volume 19, pp. 427–444. [Google Scholar]

- Kitsios, F.; Kamariotou, M. Mapping New Service Development: A Review and Synthesis of Literature. Serv. Ind. J. 2020, 40, 682–704. [Google Scholar] [CrossRef]

- Kitsios, F.; Kamariotou, M. Strategic Change Management in Public Sector Transformation: The Case of Middle Manager Leadership in Greece. In Proceedings of the British Academy of Management (BAAM) Conference 2017, Coventry, UK, 5–7 September 2017. [Google Scholar]

- Kitsios, F.; Kamariotou, M. The impact of Information Technology and the alignment between business and service innovation strategy on service innovation performance. In Proceedings of the 3rd IEEE International Conference on Industrial Engineering, Management Science and Applications (ICIMSA 2016), Jeju Island, Korea, 23–26 May 2016. [Google Scholar]

- Kitsios, F.; Angelopoulos, S.; Zannetopoulos, I. Innovation and e-government: An in depth overview on e-services. In Heterogeneous Next Generation Networking: Innovations and Platform; Kotsopoulos, S., Ioannou, K., Eds.; IGI Global Publishing: Hershey, PA, USA, 2008; Volume 18, pp. 415–426. [Google Scholar]

- Ho, S.J.; Mallick, S.K. The impact of information technology on the banking industry. J. Oper. Res. Soc. 2010, 61, 211–221. [Google Scholar] [CrossRef]

- Moslehpour, M.; Pham, V.K.; Wong, W.K.; Bilgiçli, İ. E-purchase intention of Taiwanese consumers: Sustainable mediation of perceived usefulness and perceived ease of use. Sustainability 2018, 10, 234. [Google Scholar] [CrossRef] [Green Version]

- Suhaimi, A.I.H.; Bin Abu Hassan, M.S. Determinants of Branchless Digital Banking Acceptance Among Generation Y in Malaysia. In Proceedings of the 2018 IEEE Conference on E-Learning, e-Management and e-Services (IC3e), Langkawi, Malaysia, 21–22 November 2018. [Google Scholar]

- Venkatesh, V.; Bala, H. Technology acceptance model 3 and a research agenda on interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef] [Green Version]

- Davis, F.D. User acceptance of information technology: System characteristics, user perceptions and behavioral impacts. Int. J. Man-Mach. Stud. 1993, 38, 475–487. [Google Scholar] [CrossRef] [Green Version]

- Setia, P.; Venkatesh, V.; Joglekar, S. Leveraging digital technologies: How information quality leads to localized capabilities and customer service performance. MIS Q. 2013, 37, 565–590. [Google Scholar] [CrossRef] [Green Version]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User acceptance of computer technology: A comparison of two theoretical models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef] [Green Version]

- Munoz-Leiva, F.; Climent-Climent, S.; Liébana-Cabanillas, F. Determinants of intention to use the mobile banking apps: An extension of the classic TAM model. Span. J. Mark.-ESIC 2017, 21, 25–38. [Google Scholar] [CrossRef]

- Pikkarainen, T.; Pikkarainen, K.; Karjaluoto, H.; Pahnila, S. Consumer acceptance of online banking: An extension of the technology acceptance model. Internet Res. 2004, 14, 224–235. [Google Scholar] [CrossRef] [Green Version]

- Amin, H.; Supinah, R.; Aris, M.M.; Baba, R. Receptiveness of mobile banking by Malaysian local customers in Sabah: An empirical investigation. J. Internet Bank. Commer. 2012, 17, 1–13. [Google Scholar] [CrossRef]

- Legris, P.; Ingham, J.; Collerette, P. Why do people use information technology? A critical review of the technology acceptance model. Inf. Manag. 2003, 40, 191–204. [Google Scholar] [CrossRef]

- Kachigan, S.K. Multivariate Statistical Analysis: A Conceptual Introduction, 2nd ed.; Radius Press: Santa Fe, NM, USA, 1991. [Google Scholar]

- Newkirk, H.E.; Lederer, A.L.; Srinivasan, C. Strategic information systems planning: Too little or too much? J. Strateg. Inf. Syst. 2003, 12, 201–228. [Google Scholar] [CrossRef]

- Kitsios, F.; Kamariotou, M. Job satisfaction behind motivation: An empirical study in public health workers. Heliyon 2021, 7, e06857. [Google Scholar] [CrossRef] [PubMed]

- Kamariotou, M.; Kitsios, F. How Managers Use Information Systems for Strategy Implementation in Agritourism SMEs. Information 2020, 11, 331. [Google Scholar] [CrossRef]

- Kitsios, F.; Kamariotou, M. Strategizing Information Systems: An empirical analysis of IT Alignment and Success in SMEs. Computers 2019, 8, 74. [Google Scholar] [CrossRef] [Green Version]

- Kitsios, F.; Kamariotou, M. Strategic IT Alignment and Business Performance in SMEs: An Empirical Investigation. In Business Information Systems Workshops, Springer LNBIP 373; Abramowicz, W., Corchuelo, R., Eds.; Springer Nature: Basingstoke, UK, 2019; Volume 373, pp. 113–123. [Google Scholar]

- Sudarsono, H.; Nugrohowati, R.N.I.; Tumewang, Y.K. The effect of COVID-19 pandemic on the adoption of Internet banking in Indonesia: Islamic bank and conventional bank. J. Asian Financ. Econ. Bus. 2020, 7, 789–800. [Google Scholar] [CrossRef]

- Nasri, W. Acceptance of Internet Banking in Tunisian Banks: Evidence from Modified UTAUT Model. Int. J. E-Bus. Res. 2021, 17, 22–41. [Google Scholar] [CrossRef]

- Shahabi, V.; Azar, A.; Razi, F.F.; Shams, M.F.F. Simulation of the effect of COVID-19 outbreak on the development of branchless banking in Iran: Case study of Resalat Qard–al-Hasan Bank. Rev. Behav. Financ. 2021, 13, 85–108. [Google Scholar] [CrossRef]

- Kitsios, F.; Stefanakakis, S.; Kamariotou, M.; Dermentzoglou, L. E-service Evaluation: User Satisfaction Measurement and Implications in Health Sector. Comput. Stand. Interfaces J. 2019, 63, 16–26. [Google Scholar] [CrossRef]

- Kitsios, F.; Kamariotou, M. Open Data Hackathons: An Innovative Strategy to Enhance Entrepreneurial Intention. Int. J. Innov. Sci. 2018, 10, 519–538. [Google Scholar] [CrossRef]

- Kitsios, F.; Grigoroudis, E.; Giannikopoulos, K.; Doumpos, M.; Zopounidis, C. Strategic decision making using multicriteria analysis: New service development in Greek hotels. Int. J. Data Anal. Tech. Strateg. 2015, 7, 187–202. [Google Scholar] [CrossRef]

- Kitsios, F.; Kamariotou, M. Service innovation process digitization: Areas for exploitation and exploration. J. Hosp. Tour. Technol. 2021, 12, 4–18. [Google Scholar] [CrossRef]

- Kitsios, F.; Kamariotou, M. Critical success factors in service innovation strategies: An annotated bibliography on NSD. In Proceedings of the British Academy of Management (BAM) Conference 2016, Newcastle, UK, 6–8 September 2016. [Google Scholar]

- Kitsios, F.; Kamariotou, M.; Talias, M. Corporate Sustainability Strategies and Decision Support Methods: A Bibliometric Analysis. Sustainability 2020, 12, 521. [Google Scholar] [CrossRef] [Green Version]

- Kamariotou, M.; Kitsios, F. Critical Factors of Strategic Information Systems Planning Phases in SMEs. In Information Systems. EMCIS 2018. Lecture Notes in Business Information Processing; Themistocleous, M., Rupino da Cunha, P., Eds.; Springer: Cham, Switzerland, 2019; Volume 341, pp. 503–517. [Google Scholar]

- Kitsios, F.; Kamariotou, M. Artificial Intelligence and Business Strategy towards Digital Transformation: A Research Agenda. Sustainability 2021, 13, 2025. [Google Scholar] [CrossRef]

- Mitroulis, D.; Kitsios, F. Using multicriteria decision analysis to evaluate the effect of digital transformation on organizational performance: Evidence from Greek tourism SMEs. Int. J. Decis. Support Syst. 2019, 4, 143–158. [Google Scholar] [CrossRef]

- Mitroulis, D.; Kitsios, F. Evaluating digital transformation strategies: A MCDA analysis of Greek tourism SMEs. In Proceedings of the 14th European Conference on Innovation and Entrepreneurship (ECIE19), Kalamata, Greece, 19–20 September 2019. [Google Scholar]

- Casquejo, M.; Himang, C.; Ocampo, L.; Ancheta, R.; Himang, M.; Bongo, M. The Way of Expanding Technology Acceptance—Open Innovation Dynamics. J. Open Innov. Technol. Mark. Complex. 2020, 6, 8. [Google Scholar] [CrossRef] [Green Version]

- Lee, S.; Kwon, Y.; Quoc, N.N.; Danon, C.; Mehler, M.; Elm, K.; Bauret, R.; Cho, S. Red Queen Effect in German Bank Industry: Implication of Banking Digitalization for Open Innovation Dynamics. J. Open Innov. Technol. Mark. Complex. 2021, 7, 90. [Google Scholar] [CrossRef]

- Peñarroya-Farell, M.; Miralles, F. Business Model Dynamics from Interaction with Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 81. [Google Scholar] [CrossRef]

- Wu, B.; Gong, C. Impact of open innovation communities on enterprise innovation performance: A system dynamics perspective. Sustainability 2019, 11, 4794. [Google Scholar] [CrossRef] [Green Version]

- Yun, J.J.; Park, K.; Hahm, S.D.; Kim, D. Basic income with high open innovation dynamics: The way to the entrepreneurial state. J. Open Innov. Technol. Mark. Complex. 2019, 5, 41. [Google Scholar] [CrossRef] [Green Version]

- Yun, J.J.; Zhao, X.; Jung, K.; Yigitcanlar, T. The culture for open innovation dynamics. Sustainability 2020, 12, 5076. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Questions | References |

|---|---|---|

| Perceived usefulness | The use of digital banking applications or systems improves the quality of my work The use of digital banking applications or systems makes my job more regulated The use of digital banking applications or systems helps me complete my tasks faster The use of digital banking applications or systems supports essential aspects of my work The use of digital banking applications or systems increases my productivity at work The use of digital banking applications or systems enhances my efficiency at work The use of digital banking applications or systems allows me to conduct more work than would otherwise be possible The use of digital banking applications or systems increases my work effectiveness The use of digital banking applications or systems simplifies my work Overall, I think that digital banking applications or systems are helpful for my work in general | [39,40,41,47,48] |

| Perceived ease of use | I consider it difficult to use automated digital banking applications or systems It is easy for me to learn how to run digital banking applications or systems Interaction with digital banking systems or applications is always challenging I find digital banking applications or systems easy to use to do what I want to do Digital banking applications or systems connect rigidly and inflexibly I can easily recall how to execute my tasks using digital banking applications or systems The interaction with digital banking applications or systems requires a great deal of mental effort My experience with digital banking applications or systems is transparent and understandable I think it takes a great deal of effort to use digital banking applications or systems in general I think digital banking applications or systems are easy to use | [39,40,41,47,48] |

| Perceived self-efficacy | I could perform my duties with digital banking applications or systems… …if there was nobody around to tell me what to do when I went …if I just had a built-in assistance facility …if someone taught me how to do this first …if I had used similar applications to do the same job before this one. | [40,47] |

| Intention to use | If I had access to digital banking applications or systems, I would use them If I had access to digital banking applications or systems, then I foresee using them Over the next < n > months, I plan to use digital banking applications or systems | [39,40,48] |

| Usage behavior | On average, how much time do you spend every day on using digital banking applications or systems? | [39,40,47,48] |

| Variables | Cronbach α |

|---|---|

| Perceived usefulness | 0.860 |

| Perceived ease of use | 0.863 |

| Perceived self-efficacy | 0.881 |

| Intention to use | 0.866 |

| Usage behavior | 0.911 |

| Perceived Usefulness | Perceived Ease of Use | Perceived Self-Efficacy | Intention to Use | Usage Behavior | |

|---|---|---|---|---|---|

| Perceived usefulness | 1.000 | 0.798 | 0.652 | 0.766 | |

| Perceived ease of use | 0.798 | 1.000 | 0.718 | 0.741 | |

| Perceived self-efficacy | 0.652 | 0.718 | 1.000 | 0.651 | |

| Intention to use | 0.766 | 0.741 | 0.651 | 1.000 | 0.573 |

| Usage behavior | 0.573 | 1.000 |

| Model | R | R2 | Adjusted R2 | Estimate Standard Error | Durbin-Watson |

|---|---|---|---|---|---|

| 1 | 0.805 | 0.648 | 0.641 | 0.525 | 2.141 |

| 2 | 0.573 | 0.328 | 0.324 | 0.833 | 1.949 |

| Model | Sum of Square | Df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|---|

| 1 | Regression | 79.587 | 3 | 26.529 | 96.191 | 0.000 |

| Residual | 43.299 | 158 | 0.276 | |||

| Total | 122.886 | 161 | ||||

| 2 | Regression | 53.979 | 2 | 53.979 | 77.677 | 0.000 |

| Residual | 110.493 | 159 | 0.695 | |||

| Total | 164.472 | 161 |

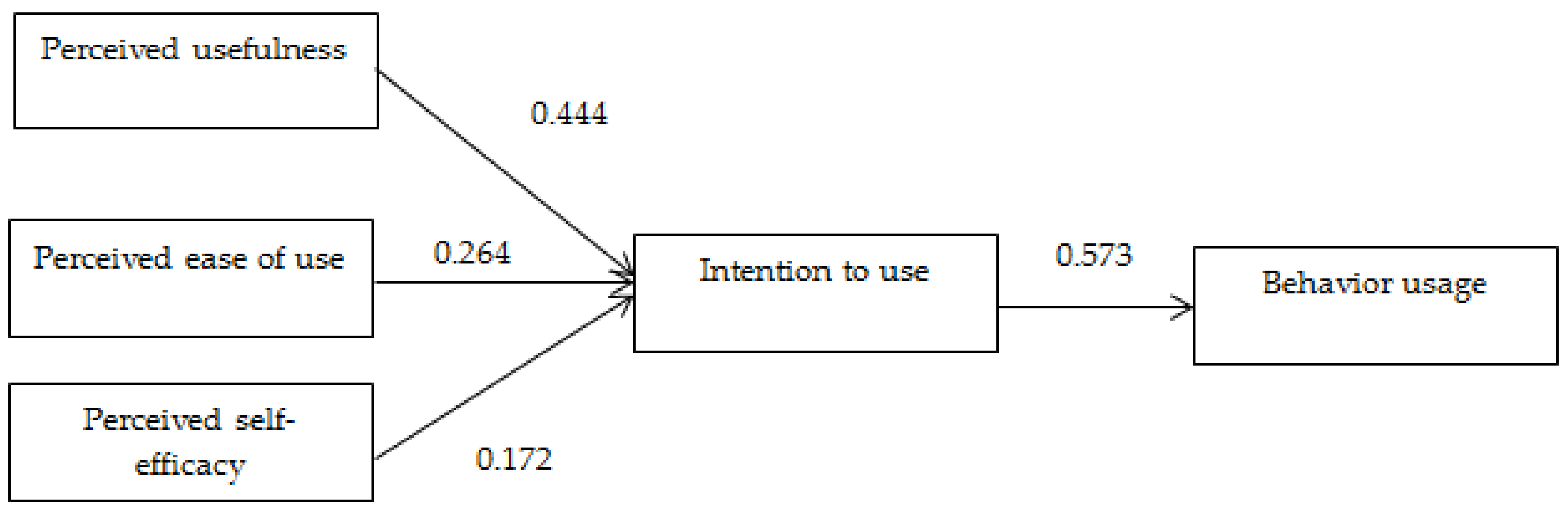

| Model | β | t-Value | Sig. | VIF |

|---|---|---|---|---|

| Perceived usefulness | 0.444 | 5.547 | 0.000 | 2.853 |

| Perceived ease of use | 0.264 | 3.027 | 0.005 | 3.384 |

| Perceived self-efficacy | 0.172 | 2.482 | 0.026 | 2.139 |

| Intention to use | 0.573 | 8.813 | 0.000 | 1.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kitsios, F.; Giatsidis, I.; Kamariotou, M. Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services. J. Open Innov. Technol. Mark. Complex. 2021, 7, 204. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030204

Kitsios F, Giatsidis I, Kamariotou M. Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(3):204. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030204

Chicago/Turabian StyleKitsios, Fotis, Ioannis Giatsidis, and Maria Kamariotou. 2021. "Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 3: 204. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7030204