1. Introduction

The conversation around financial crises and the threat they pose to financial and economic stability needs to be elevated from the country level to a broader global discussion amongst regulators and policymakers. Over the past decade or so, we have witnessed how instabilities emanating from one financial institution propagate to other financial institutions, similarly from financial market to financial market, and ultimately from country to country. Therefore, the focus of these discussions should be on identifying and understanding the system, its risks, and the interlinkages that combine entities, financial markets and countries.

To this end, the magnitude of the cost/loss induced by the financial crisis of 2007–2009 is still to be fully determined. The recent European sovereign debt crisis is one of the latest after-effects of the systemic events of 2007–2009. Funding challenges in the banking sector spilled over to other markets and countries via international transactions and were ultimately transmitted to the sovereign debt market as governments attempted to bail out distressed financial institutions.

Most of the literature examines systemic risk from one perspective, that is, how much distressed institutions contribute to the systemic risk of the whole financial system. Nevertheless, the amount of risk that distressed financial systems add to individual institutions is also of great importance in ensuring stability. This rarely studied viewpoint focused on the sensitivity of financial institutions to systemic events is termed systemic risk exposure. Systemic risk exposure, unlike systemic risk contribution, focuses on how much additional risk is faced by individual institutions in the event of market disruption. Thus, this study builds on and contributes to the literature by using a methodology that is flexible enough to cater for time-varying tail dependence. According to

Sedunov (

2016), institutions that do not initially contribute much to systemic risk, but which are heavily exposed to crises, tend to magnify the distress of the financial system. Against this background, we investigate the cross-border systemic risk exposure of South African banks, and how these banks respond to crises emanating beyond the country’s borders. This will inform regulators and policymakers on the vulnerabilities of South African banks to external markets and assist them to better understand the influences of each institution’s level of systemic risk exposure.

The existing literature in the field of systemic risk and contagion is quite exhaustive. Studies have focused on different aspects, such as the contribution of banks to financial system aggregate risk, the probability of tail events in the banking system, and systemic risk transfer in sovereign debt markets. This study contributes to the existing literature in several ways. First, the analysis focuses on the systemic stress and vulnerability of banks in an attempt to measure how susceptible domestic banks are to foreign shocks. Unlike

Foggitt et al. (

2019), who treat the financial system as a unity, in this study, we disaggregate and treat banks as individuals, allowing for the banks’ different characteristics to come into play. Moreover, this study differs from others that examine the amount of risk that banks contribute to the aggregate risk of the system, such as that by

Manguzvane and Mwamba (

2019), who focused entirely on banks’ exposure to crises across borders. Unlike

Sedunov (

2016), who employs conventional MES, this study uses GAS Copulas in building the MES so as to allow for capturing the dynamic dependence structure between financial assets and markets. The approach offered in this study has several advantages. First, while this study focuses on the banking sector, the techniques presented here can be applied in other sectors, meaning the analysis can be extended to focus on vulnerabilities in other markets, such as sovereign debt. Secondly, the data used in the study are based on banks’ market values, and are readily available, making analysis easy and quick.

The objectives of this paper are two-fold: first, we investigate the systemic risk exposure of South African banks to crises in international financial markets. Second, we determine which international markets have the largest effect on South Africa’s banking sector. These objectives are critical in forecasting how South African banks will perform when there is distress in other countries (mainly the country’s major trading partners), as this will impact the country’s ability to refinance its debts. The reasoning behind studying banks’ systemic risk exposure is that its effects go beyond the banking sector to other markets, such as the sovereign debt, and ultimately affect the welfare of society.

Sedunov (

2016) claims that a country with a risky banking sector may be more likely to have higher sovereign yields because investors expect greater strain on the government’s finances if the government is forced to bail out those banks. Furthermore, a country that provides financial assistance to systemically distressed financial institutions may increase the riskiness of its sovereign debt. Not only will this affect the sovereign debt, but it will also ultimately affect the real economy, as witnessed during the global financial crisis. Moreover, with the significant influence that South Africa’s biggest banks have throughout the African continent, it is of paramount importance to understand how the banks will respond to international crises, as these will have ripple effects on the already fragile African market.

To this end, we measure how distressed international financial markets influence the stability of South Africa’s largest banks. We use available data for seven of the largest banks in South Africa, namely Absa, Capitec, First Rand, Investec, Rand Merchant, Nedbank and Standard Bank, while for international markets, we focus on both developed and emerging economies. The study pays attention to South Africa’s banking sector because, despite being an emerging market, South Africa has a financial services sector that is very well developed. With assets worth over ZAR 6 trillion and contributing more than 10% to GDP, not only does the sector play a vital role in driving the economy forward, but it is also well-placed to be the regional financial center for Africa. The South African banking system’s uniqueness comes in the form that it is relatively large, but heavily concentrated, with around 92 percent of the total assets belonging to only six banks. Moreover, the largest South African banks are heavily active in other African countries, which implies that these banks are not only a threat to South African financial stability, but also pose a systemic threat to a lot of other African countries. South Africa also remains the only Financial Stability Board jurisdiction that does not have an explicit deposit insurance scheme. A deposit insurance scheme is meant to build a comprehensive regulatory system for reducing the social and economic cost of distressed financial institutions.

1The recent rise in pace of globalization requires that the financial sector to be even more integrated with the global financial system. However, integration, along with the reckless chasing of short-term profits, has been proven by the global financial crisis to bring increased stability risk. There is thus an urgent need for regulatory tools that meet international standards and can confirm the build-up of imbalances before they develop into crises. While this study focuses on South Africa only, the findings could be extended to other emerging and developing economies that have similar characteristics to South Africa.

The measure of systemic risk exposure that we use is the marginal expected shortfall (MES). The MES, unlike other systemic risk measures, such as the conditional value at risk (CoVaR), allows us to directly measure the responsiveness of financial institutions to system-wide distress. However, the MES, as proposed by

Acharya et al. (

2012) and modified by

Brownlees and Engle (

2012), does not consider the time-variation of the dependence parameter. To cater for this, we follow the approach proposed in

Eckernkemper (

2018), which uses Copulas to estimate the MES. Copulas offer greater flexibility, as they allow for the separate modeling of marginals and the dependence structure. This separation means that the marginal specification is not restricted by the Copula distribution. As a driving mechanism for time-varying parameters, we use the generalized autoregressive score model (GAS) of

Creal et al. (

2013). A mixed Copula rather than a one-dimensional Copula is used to model asymmetric dependencies in one framework while also distinguishing between upper and lower tail dependence. The mixed Copula has two components, the first being the Clayton Copula, which captures lower tail dependence, and the second being the rotated Clayton, which takes into account upper tail dependence. Our data, much like most financial time series data, are non-normal; therefore, to capture the skewness and excess kurtosis, we estimate our marginal models via an exponential GARCH using the skewed t distribution.

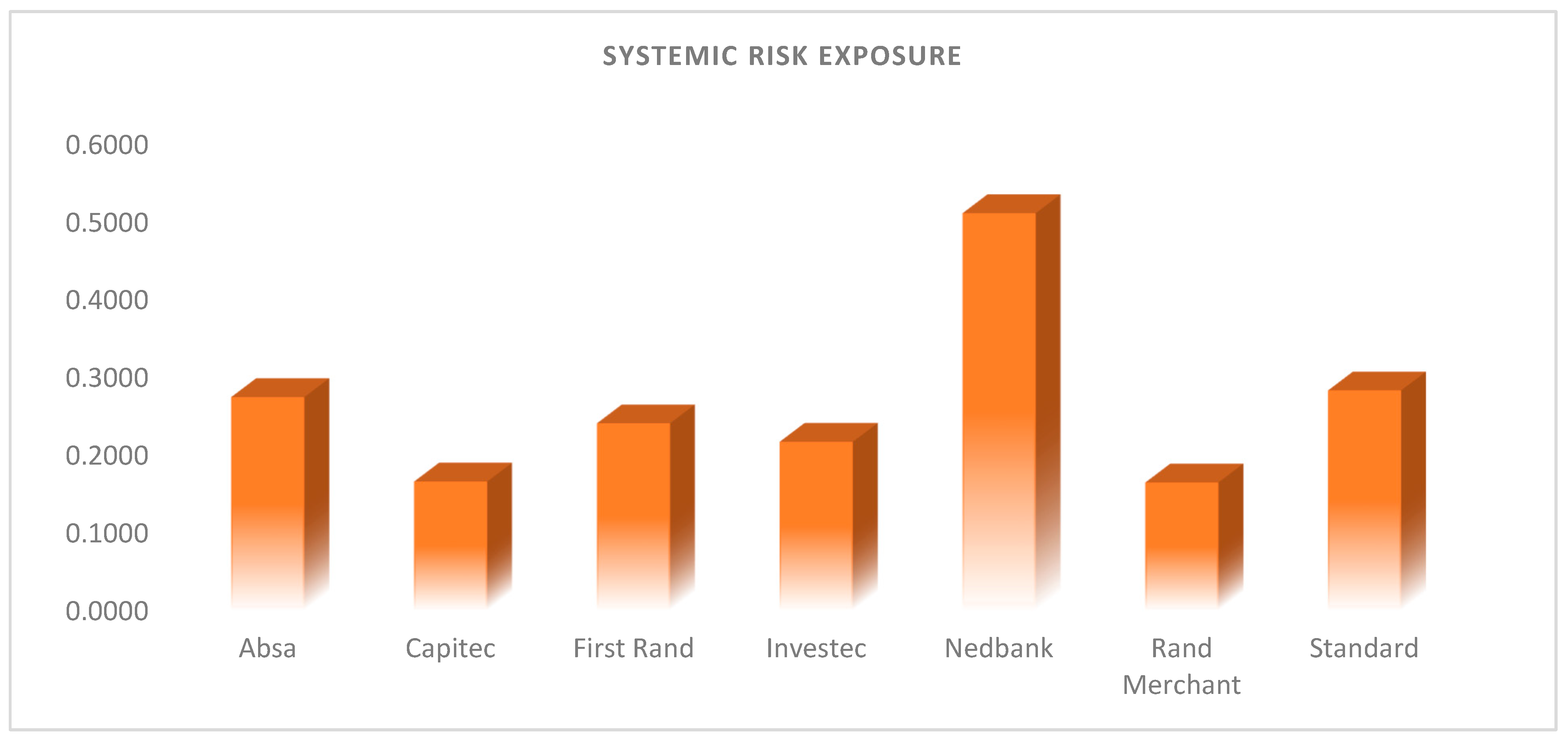

Using a sample running from March 2002 through to May 2020, we find that, on average, Nedbank and Absa are the banks that would be most vulnerable if an international crisis were to occur. This means that of all the South African banks, Nedbank and ABSA are the most systemically exposed to international distress. The international linkages that the two banks have enjoyed over the years would support these findings. These findings are not by chance as ABSA has been a full subsidiary of UK banking giant Barclays PLC for over 90 percent of our sampling period, making it very vulnerable to any problems that Barclays encounters. The third and fourth most endangered banks in this context are Standard Bank and First Rand, which, together with Nedbank and ABSA, make up the four largest banks in South Africa, which gives rise to the “too big to fail” and the “too interconnected to fail” theories. From a regulatory perspective, this shows which institutions would be seriously endangered if an international crisis ensued. Moreover, knowing the systemic risk exposure of banks will enable regulators and policymakers to identify the determinants of the level of exposure.

The rest of the study is organized as follows:

Section 2 presents the empirical literature review related to this study.

Section 3 provides an overview of the methodology employed.

Section 4 presents a discussion of the results, and

Section 5 concludes the study.

2. Literature Review

The literature on systemic risk has expanded rapidly since the onset of the global financial crisis, mainly highlighting the importance of investigating this global phenomenon. Interestingly, little empirical evidence has been provided on the transfer of systemic risk across borders or the susceptibility of banks in one country to crises emanating from across borders. This paper, however, relates to multiple strands of literature. The first stream of literature that relates to the current study focuses on quantifying the amount of risk that one financial institution poses to its domestic financial system when it is under stress. For example,

Laeven et al. (

2016) employed the CoVaR and MES to measure the systemic risk contribution of financial institutions with a market capitalization of more than USD 10 billion in over 30 countries. Their findings are substantiated by

Buch et al. (

2019), who show that the systemic risk contribution is closely related to both the relative and the absolute size of a bank. Similarly,

Pham et al. (

2021) examined the systemic risk contribution of Asian banks through the application of four techniques, namely, the CoVaR, SRISK, component expected shortfall, and the MES. The four methodologies are found to be consistent in quantifying the amount of risk each bank adds to the aggregate risk of the system.

Several other studies have indulged in this stream of research.

Manguzvane and Mwamba (

2019) applied the CoVaR technique to model systemic risk in the South African banking sector, whereas

Karimalis and Nomikos (

2018) proposed a Copula-based CoVaR to examine the common market factors that trigger systemic risk periods.

Billio et al. (

2012) employed granger causality tests and principal component analysis to examine systemic risk in the US and found a large number of interconnections that pose a real threat to financial markets as a whole.

An interesting strand in the literature takes an opposite view from the first strand. This group examines how financial institutions are affected when the whole financial system is in distress. This strand looks at the systemic risk exposure of institutions.

Acharya et al. (

2012) developed the marginal expected shortfall, which measures how the equity value of a given financial institution will drop when the financial system enters distress.

Sedunov (

2016) used several measures to investigate the amount of systemic risk exposure that US banks face. This study is based on the premise that regulators do not have relevant knowledge on the exposure of financial institutions, hence rendering them ineffective in managing institutions during crisis. Thus, their study focuses on assessing which institutions will be seriously affected by a financial crisis by employing the MES and exposure CoVaR. First, they find that the exposure CoVaR captures systemic risk exposure much more effectively compared to the MES. Secondly, their results show that the exposure of institutions to the risk posed by the markets was very high just before and during the global financial crisis.

Brownlees and Engle (

2012) derived similar results in a study measuring the expected capital shortfall of a firm following a severe market decline. Their results were obtained by employing the SRISK measure, which is an extension of the MES and has proven to be very useful in outlining the events that took place during the subprime mortgage crisis.

A third strand in the literature concentrating on systemic risk focuses on cross-border linkages. Several studies have taken this route; among them,

Drakos and Kouretas (

2015) examined the effect of foreign banks on the stability of the US financial system. Their analysis, based on data collected from 2000 through 2012, concludes that non-US banks contribute significantly to the disruption of the provision of financial services and financial instability in the US. However, this contribution is relatively low compared to that of domestic banks.

Dungey and Gajurel (

2015) employed GARCH models to investigate whether banks’ increased international exposure destabilizes the domestic financial sector. The study covered 45 countries, and the results show that crisis shocks transmitted from a foreign jurisdiction via idiosyncratic contagion increase the likelihood of a systemic crisis.

Tonzer (

2015) took a similar approach by analyzing whether international linkages in interbank markets affect the stability of interconnected banking systems. They applied a relatively new technique in the field of financial economics in the form of spatial econometrics using bilateral cross-border banking exposure data collected from the Bank of International Settlements. Evidence from this study suggests that foreign exposures in the banking sector are a significant contributor to overall banking risk across countries. A more recent example is

Foggitt et al. (

2019), who studied the transfer of risk from the US to South Africa. Instead of only using traditional MES, they combined it with the DCC GARCH model, and the results show a strong spillover of systemic risk from the US to South Africa.

Xu et al. (

2021) dealt with the problem of risk transmission between different economic sectors. Employing a tail-driven network to study dependence, the authors found that the banking sector is the principal risk-spreader in the Chinese economy. Similarly,

Zhu et al. (

2021) showed how sector-induced contagion effects propagate during economic and financial crises. Their findings, obtained using time-varying Copulas, reveal the presence of significant systemic risk spillovers between the energy and agriculture sectors.

Another strand in the literature that is closely related to our study focuses on the transmission of shocks between countries’ sovereign debt markets. This pays attention to how changes in one country’s sovereign debt yields are influenced by another’s debt yields.

Beirne and Fratzscher (

2013) concentrated on analyzing whether there was contagion during the European sovereign debt crisis. Using data collected from 31 countries, including some emerging market economies, their analysis concluded that there was significant contagion between 2010 and 2012. Spreads of between 100 and 200 basis point increases in the sovereign yields of European countries, such as Greece, Italy, Portugal and Spain, have been attributed to international risk spillovers. Similarly,

Brutti and Sauré (

2015) analyzed the role played by financial interlinkages in the transmission of risk between European states during the European sovereign debt crisis. The empirical part of this study is based on a vector autoregressive model, augmented to cater for time-varying shock transmission.

Lucas et al. (

2014) applied GAS models in assessing the likelihood of joint and conditional sovereign debt defaults in Europe. They found strong evidence of time-varying distress dependence and spillover effects in sovereign default risk. These findings are supported by

Reboredo and Ugolini (

2015), who applied Copula CoVaR, and found that before the debt crisis, sovereign debt markets were all coupled, and systemic risk was similar for most countries.

Borri (

2018) investigated the susceptibility of emerging countries to systemic risk for local currency-denominated government debt. A quantile regression-based CoVaR was employed, and their findings reveal that emerging countries’ vulnerabilities increase with the share of local currency-denominated debt held by foreign investors.

5. Conclusions

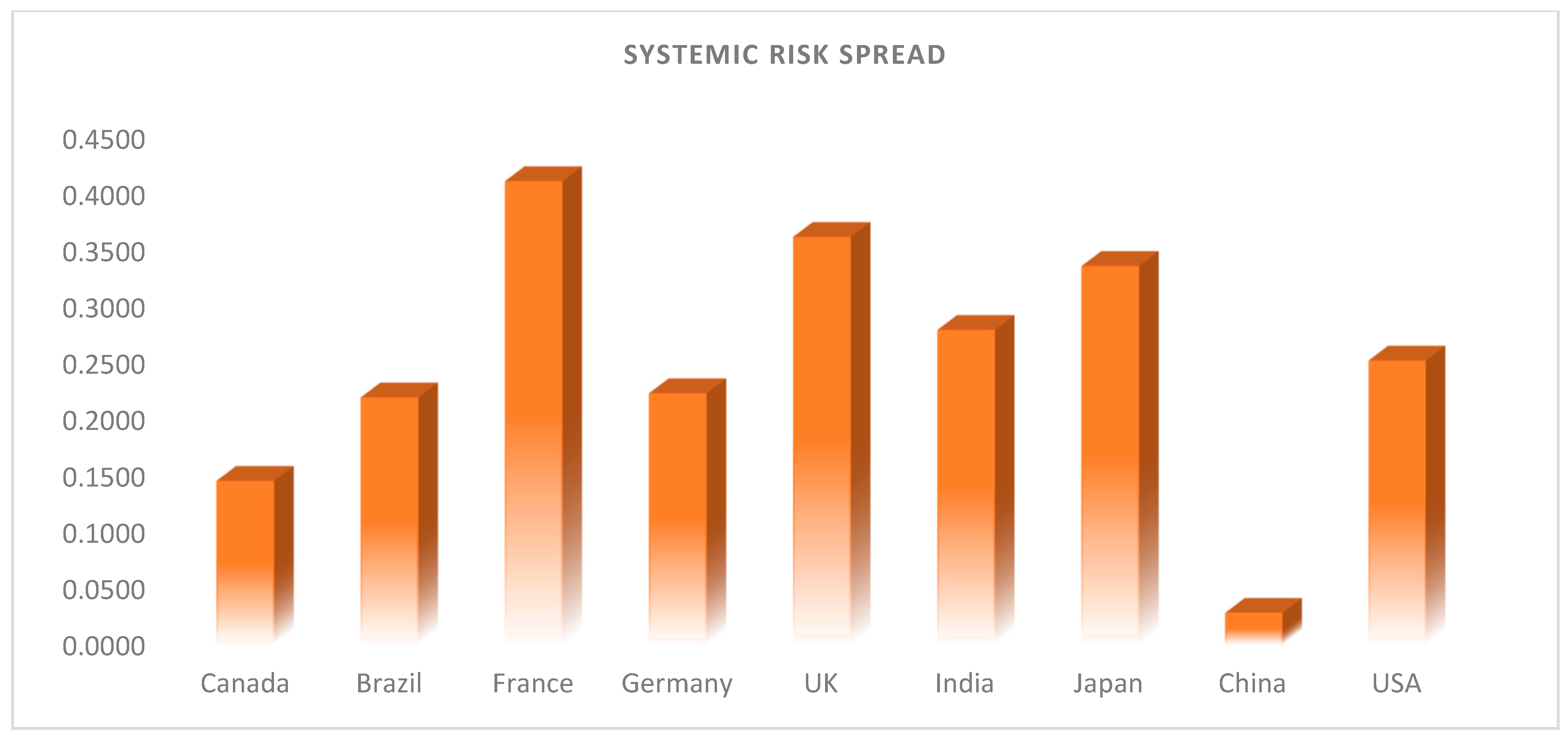

This paper implements the MES to investigate the systemic risk exposure of South African banks to international crises. We employ the marginal expected shortfall technique; however, we use the updated model rather than the original. The updated model is based on GAS Copulas, which enable us to account for non-linear and time-varying dependence structures. Mixture Copulas rather than one-dimensional Copulas are used to ensure that asymmetric dependence structures are captured in one framework, while clearly separating upper and lower dependence. As the data show that it does not follow a normal distribution, and rather has long and fat tails, we run our marginal models based on an exponential GARCH with a skewed t distribution. The empirical results provide some interesting findings that are very useful for regulators and policymakers. First, the results outline the exposure of each bank should a certain international market go into a state of distress. As expected, ABSA is found to be the most affected by a crisis in the UK, whereas Standard Bank is the most exposed to China and Germany. The emerging markets in India and Brazil have the largest effect on Capitec Bank and Standard Bank, respectively. This first set of findings is an indication to regulators of how the different institutions react to crises in different countries and shows how much danger each institution will be in when a certain market enters depression.

Second, we aggregate the initial findings so as to rank the banks in terms their systemic risk exposure, regardless of the country in distress. The results indicate that the most exposed banks are Nedbank and Absa. These findings are not random, as Nedbank and ABSA were controlled subsidiaries of the UK financial institutions Old Mutual and Barclays for over 80% of our sample period, making them very vulnerable to any problems that UK financial institutions encounter. The other banks making up the top three most systemically exposed also happen to comprise the top four biggest banks in South Africa. This implies that the much discussed “too big to fail” paradigm also exists when it comes to the vulnerability of banks in South Africa. Moreover, we are able to pinpoint which international markets have the biggest effect on South Africa. The findings explain some of the effects of the 2008 global financial crisis.

Globalization has brought with it the increased integration of financial markets, and this has caused great debate on whether it has effects on the stability of financial markets in different countries. This study finds that cross-border linkages leave banks vulnerable to crises in other countries. Integration has brought with it benefits; however, it causes negative spillovers when the stability of a certain market is low. Hence, policymakers should not just focus on the benefits of financial markets’ integration, but also on the risks that banks are exposed to due to integration. Therefore, a proper investigation into the linkages that the South African banking system has with other countries, and how cross-border exposures endanger South African banks, will go a long way in ensuring a stable and safer financial system, which will serve South African society better.

This paper contributes to economics and finance literature by quantifying the systemic vulnerability of individual banks. This investigation offers support to policymakers and regulators who are attempting to understand the relationships between domestic banks and international financial institutions. Nonetheless, the study could be extended beyond its current limitations by empirically analyzing factors that drive systemic risk exposure. This study did not focus on this area given the unavailability of data; however, such an effort would solidify the findings and help policymakers and regulators in their attempt to build a stable financial system.

{kind=link}

{kind=link}