Moderating Effects of Financial Cognitive Abilities and Considerations on the Attitude–Intentions Nexus of Stock Market Participation

Abstract

:1. Introduction

2. Literature Review

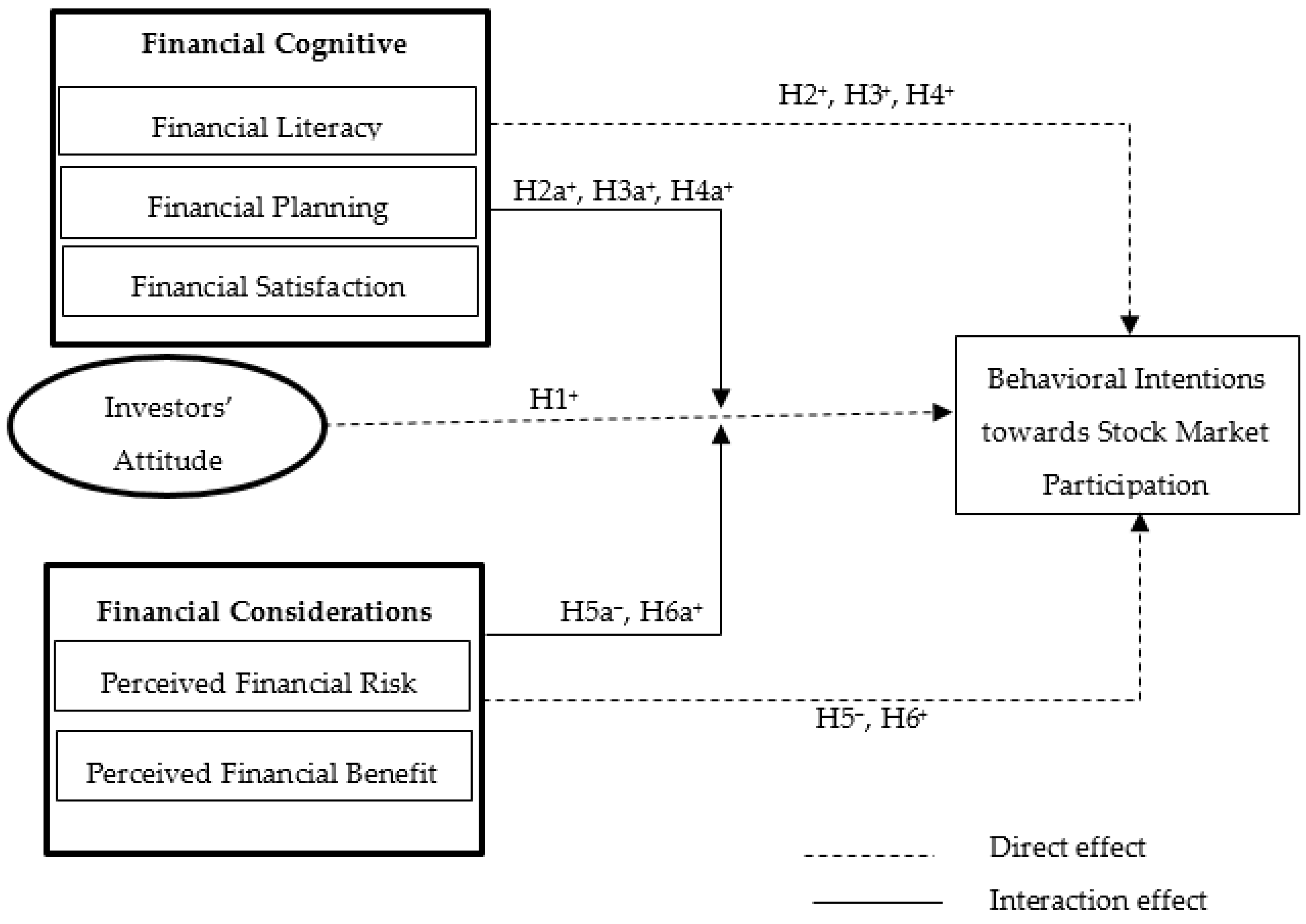

2.1. Attitude and Behavioral Intentions towards Stock Market Participation

2.2. The Moderating Effects of Cognitive Abilities

2.2.1. Financial Literacy

2.2.2. Financial Planning

2.2.3. Financial Satisfaction

2.3. The Moderating Effects of Financial Considerations

2.3.1. Perceived Financial Risk

2.3.2. Perceived Financial Benefit

3. Methodology

3.1. Study Sample: The Case of Dhaka Stock Exchange, Bangladesh

3.2. Questionnaire and Measurement

3.3. Data Collection

3.4. Model and Empirical Estimation

3.4.1. Measurement Model Evaluation

3.4.2. Structural Model Evaluation and Hypothesis Testing

4. Empirical Results Discussion

5. Summary and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| 1. If you spent BDT 70 on lunch on day 1 but only BDT 50 the next day, how much did you spend on lunch over the two days? BDT ________ |

| 2. If a prize draw win of BDT 180,000 is shared equally between six people, how much will each person receive? BDT ________ |

3. If a person takes home BDT 14,000 a month and 50% of this goes to rent, what is their monthly rent?

|

4. If a refrigerator priced at BDT 21,000 is discounted by 10% at a sale, how much would it cost?

|

5. A deposit of BDT 2000 in a savings account earning an interest of 10% annually will become BDT________ after 2 years.

|

6. Suppose that the interest rate on your savings account is less than the inflation rate. Using the money in the account after 1 year, you would be able to buy less goods compared to the amount you could get today.

|

7. If a person pays the minimum sum of his outstanding credit card balance, he will not have to pay any interest charge

|

8. Commonly, the outstanding balance on a credit card is subject to a financial charge (interest charge) of ____ %

|

9. In hire purchase financing, the owner of the car is ______

|

| 10. The role of this institution is to provide advice on money management and assistance to deal with debt A. Stock Exchange Commission B. Bangladesh Bank C. Credit Information Bureau |

References

- Agarwal, Sumit, and Bhashkar Mazumder. 2013. Cognitive Abilities and Household Financial Decision Making. American Economic Journal: Applied Economics 5: 193–207. [Google Scholar] [CrossRef] [Green Version]

- Ajzen, Icek. 1991. The Theory of Planned Behavior. Organizational Behavior and Human Decision Processes 50: 179–211. [Google Scholar] [CrossRef]

- Ajzen, Icek, and Martin Fishbein. 1975. A Bayesian Analysis of Attribution Processes. Psychological Bulletin 82: 261–77. [Google Scholar] [CrossRef]

- Ajzen, Icek, and Martin Fishbein. 2005. The Influence of Attitudes on Behavior. In The Handbook of Attitudes. Mahwah: Lawrence Erlbaum Associates. [Google Scholar] [CrossRef]

- Ali, Azwadi. 2010. The Mediating Role of Attitudes in Using Investor Relations Websites. Doctoral Dissertation, Victoria University, Footscray, Australia. Available online: https://vuir.vu.edu.Au/ (accessed on 22 November 2021).

- Ali, Azwadi, Mohd Shaari Abdul Rahman, and Alif Bakar. 2015. Financial Satisfaction and the Influence of Financial Literacy in Malaysia. Social Indicators Research 120: 137–56. [Google Scholar] [CrossRef]

- Ali, Muhammad, Syed Ali Raza, Bilal Khamis, Chin Hong Puah, and Hanudin Amin. 2021. How Perceived Risk, Benefit and Trust Determine User Fintech Adoption: A New Dimension for Islamic Finance. Foresight 23: 403–20. [Google Scholar] [CrossRef]

- Al-Tamimi, Hussein A. Hassan, and Al Anood Bin Kalli. 2009. Financial Literacy and Investment Decisions of UAE Investors. The Journal of Risk Finance 10: 500–16. [Google Scholar] [CrossRef] [Green Version]

- Ameriks, John, Andrew Caplin, and John Leahy. 2003. Wealth Accumulation and the Propensity to Plan. The Quarterly Journal of Economics 118: 1007–47. [Google Scholar] [CrossRef]

- Andersen, Steffen, and Kasper Meisner Nielsen. 2010. Participation Constraints in the Stock Market: Evidence from Unexpected Inheritance Due to Sudden Death. The Review of Financial Studies 24: 1667–97. [Google Scholar] [CrossRef]

- Arpana, D., and H. R. Swapna. 2020. Role of planning and risk tolerance as intervening constructs between financial well-being and financial literacy among professionals. International Journal of Economics and Financial Issues 10: 145–49. [Google Scholar] [CrossRef]

- Asandimitra, Nadia, Tony Seno Aji, and Achmad Kautsar. 2019. Financial Behavior of Working Women in Investment Decision-Making. Information Management and Business Review 11: 10–20. [Google Scholar] [CrossRef]

- Atlas, Stephen A., Jialing Lu, P. Dorin Micu, and Nilton Porto. 2019. Financial Knowledge, Confidence, Credit Use, and Financial Satisfaction. Journal of Financial Counseling and Planning 30: 175–90. [Google Scholar] [CrossRef]

- Baker, H. Kent, and Victor Ricciardi. 2014. Investor Behavior: The Psychology of Financial Planning and Investing. Hoboken: John Wiley & Sons. [Google Scholar] [CrossRef]

- Barasinska, Nataliya, Dorothea Schäfer, and Andreas Stephan. 2012. Individual Risk Attitudes and the Composition of Financial Portfolios: Evidence from German Household Portfolios. The Quarterly Review of Economics and Finance 52: 1–14. [Google Scholar] [CrossRef] [Green Version]

- Barman, Babul. 2020. Net Foreign Fund in Stocks Negative for Two Years. The Financial Express. January 3. Available online: https://thefinancialexpress.com.Bd/ (accessed on 27 December 2021).

- Barsky, Robert B., F. Thomas Juster, Miles S. Kimball, and Matthew D. Shapiro. 1997. Preference Parameters and Behavioral Heterogeneity: An Experimental Approach in the Health and Retirement Study. The Quarterly Journal of Economics 112: 537–79. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, Geert, and Campbell R. Harvey. 1998. Capital Markets: An Engine for Economic Growth. The Brown Journal of World Affairs 5: 33–53. Available online: http://www.jstor.Org (accessed on 22 November 2021).

- Bekaert, Geert, and Campbell R Harvey. 2002. Research in Emerging Markets Finance: Looking to the Future. Emerging Markets Review 3: 429–48. [Google Scholar] [CrossRef]

- Boubaker, Sabri, and Duc Khuong Nguyen. 2014a. Corporate Governance in Emerging Markets. Cham: Springer Nature. [Google Scholar] [CrossRef] [Green Version]

- Boubaker, Sabri, and Duc Khuong Nguyen. 2014b. Corporate Governance and Corporate Social Responsibility: Emerging Markets Focus. Singapore: World Scientific. [Google Scholar] [CrossRef] [Green Version]

- Boubaker, Sabri, Bang Dang Nguyen, and Duc Khuong Nguyen. 2012. Corporate Governance: Recent Developments and New Trends. Berlin: Springer. [Google Scholar] [CrossRef]

- Brounen, Dirk, Kees G. Koedijk, and Rachel A. J. Pownall. 2016. Household Financial Planning and Savings Behavior. Journal of International Money and Finance 69: 95–107. [Google Scholar] [CrossRef]

- Calcagno, Riccardo, and Chiara Monticone. 2015. Financial Literacy and the Demand for Financial Advice. Journal of Banking & Finance 50: 363–80. [Google Scholar] [CrossRef]

- Calvet, Laurent Emmanuel, John Y. Campbell, and Paolo Sodini. 2007. Down or Out: Assessing the Welfare Costs of Household Investment Mistakes. Journal of Political Economy 115: 707–47. [Google Scholar] [CrossRef] [Green Version]

- Campbell, John Y., Luis M. Viceira, and Joshua S. White. 2003. Foreign Currency for long-term Investors. The Economic Journal 113: C1–C25. [Google Scholar] [CrossRef] [Green Version]

- Chandon, Pierre, Brian Wansink, and Gilles Laurent. 2000. A Benefit Congruency Framework of Sales Promotion Effectiveness. Journal of Marketing 64: 65–81. [Google Scholar] [CrossRef]

- Chen, Gongmeng, Kenneth A. Kim, John R. Nofsinger, and Oliver M. Rui. 2007. Trading Performance, Disposition Effect, Overconfidence, Representativeness Bias, and Experience of Emerging Market Investors. Journal of Behavioral Decision Making 20: 425–51. [Google Scholar] [CrossRef]

- Christelis, Dimitrios, Tullio Jappelli, and Mario Padula. 2010. Cognitive Abilities and Portfolio Choice. European Economic Review 54: 18–38. [Google Scholar] [CrossRef] [Green Version]

- Clark-Murphy, Marilyn, and Geoffrey Soutar. 2004. What Individual Investors Value: Some Australian Evidence. Journal of Economic Psychology 25: 539–55. [Google Scholar] [CrossRef]

- Cocco, João F., Francisco J. Gomes, and Pascal J. Maenhout. 2005. Consumption and Portfolio Choice over the Life Cycle. The Review of Financial Studies 18: 491–533. [Google Scholar] [CrossRef]

- Cole, Shawn Allen, Anna L. Paulson, and Gauri Kartini Shastry. 2012. Smart Money: The Effect of Education on Financial Behavior. Harvard Business School Finance Working Paper No. 09-071. Harvard: Harvard Business School. Available online: https://ssrn.Com (accessed on 22 November 2021).

- Curcuru, Stephanie, John Heaton, Deborah Lucas, and Damien Moore. 2010. Heterogeneity and Portfolio Choice: Theory and Evidence. In Handbook of Financial Econometrics: Tools and Techniques. Amsterdam: Elsevier BV, pp. 337–82. [Google Scholar] [CrossRef]

- Dimmock, Stephen G., and Roy Kouwenberg. 2010. Loss-Aversion and Household Portfolio Choice. Journal of Empirical Finance 17: 441–59. [Google Scholar] [CrossRef]

- Durand, Martine. 2015. The OECD Better Life Initiative: How’s Life? And the Measurement of Well-Being. Review of Income and Wealth 61: 4–17. [Google Scholar] [CrossRef]

- Fellner-Röhling, Gerlinde, and Boris Maciejovsky. 2007. Risk Attitude and Market Behavior: Evidence from Experimental Asset Markets. Journal of Economic Psychology 28: 338–50. [Google Scholar] [CrossRef] [Green Version]

- Fornell, Claes, and David F. Larcker. 1981. Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. Journal of Marketing Research 18: 382–88. [Google Scholar] [CrossRef]

- Fox, Jonathan, and Suzanne Bartholomae. 2020. Household Finances, Financial Planning, and COVID-19. Financial Planning Review 3: 3–11. [Google Scholar] [CrossRef]

- Ganzach, Yoav. 2000. Judging Risk and Return of Financial Assets. Organizational Behavior and Human Decision Processes 83: 353–70. [Google Scholar] [CrossRef] [Green Version]

- Georgarakos, Dimitris, and Roman Inderst. 2011. Financial Advice and Stock Market Participation. ECB Working Paper No. 1296. Frankfurt: European Central Bank (ECB), 1–47. [Google Scholar] [CrossRef] [Green Version]

- Georgarakos, Dimitris, and Giacomo Pasini. 2011. Trust, Sociability, and Stock Market Participation. Review of Finance 15: 693–725. [Google Scholar] [CrossRef] [Green Version]

- Giannetti, Mariassunta, and Tracy Yue Wang. 2016. Corporate Scandals and Household Stock Market Participation. The Journal of Finance 71: 2591–636. [Google Scholar] [CrossRef]

- Guiso, Luigi, Michael Haliassos, and Tullio Jappelli. 2003. Household Stockholding in Europe: Where Do We Stand and Where Do We Go? Economic Policy 18: 123–70. [Google Scholar] [CrossRef]

- Hadi, Fazal. 2017. Effect of Emotional Intelligence on Investment Decision Making With a Moderating Role of Financial Literacy. China-USA Business Review 16: 53–62. [Google Scholar] [CrossRef] [Green Version]

- Hair, Joseph F., Christian M. Ringle, and Marko Sarstedt. 2013. Partial Least Squares Structural Equation Modeling: Rigorous Applications, Better Results and Higher Acceptance. Long Range Planning 46: 1–12. [Google Scholar] [CrossRef]

- Hausman, Angela V., and Jeffrey Sam Siekpe. 2009. The Effect of Web Interface Features on Consumer Online Purchase Intentions. Journal of Business Research 62: 5–13. [Google Scholar] [CrossRef]

- Hayat, Amir, and Muhammad Anwar. 2016. Impact of Behavioral Biases on Investment Decision; Moderating Role of Financial Literacy. Moderating Role of Financial Literacy 1: 1–14. [Google Scholar] [CrossRef]

- Heaton, John, and Deborah Lucas. 2000. Portfolio Choice in the Presence of Background Risk. The Economic Journal 110: 1–26. [Google Scholar] [CrossRef]

- Henseler, Jörg, Christian M. Ringle, and Marko Sarstedt. 2015. A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science 43: 115–35. [Google Scholar] [CrossRef] [Green Version]

- Hoque, Mohammad Enamul, M. Kabir Hassan, Nik Mohd Hazrul Nik Hashim, and Tarek Zaher. 2019. Factors Affecting Islamic Banking Behavioral Intention: The Moderating Effects of Customer Marketing Practices and Financial Considerations. Journal of Financial Services Marketing 24: 44–58. [Google Scholar] [CrossRef]

- Howlett, Elizabeth, Jeremy Kees, and Elyria Kemp. 2008. The Role of Self-Regulation, Future Orientation, and Financial Knowledge in Long-Term Financial Decisions. Journal of Consumer Affairs 42: 223–42. [Google Scholar] [CrossRef]

- Joo, So-Hyun, and John E. Grable. 2004. An Exploratory Framework of the Determinants of Financial Satisfaction. Journal of Family and Economic Issues 25: 25–50. [Google Scholar] [CrossRef]

- Kamal, Abu Hena Mohammed Mustafa. 2021. Kamal ‘baffled’ by a Lack of Confidence in Market. The Daily Star. March 24. Available online: https://www.thedailystar.net/business/News/ (accessed on 1 November 2021).

- Kaplan, Andreas M., Detlef Schoder, and Michael Haenlein. 2007. Factors Influencing the Adoption of Mass Customization: The Impact of Base Category Consumption Frequency and Need Satisfaction. Journal of Product Innovation Management 24: 101–16. [Google Scholar] [CrossRef]

- Kaur, Simarpreet, and Sangeeta Arora. 2021. Role of Perceived Risk in Online Banking and Its Impact on Behavioral Intention: Trust As a Moderator. Journal of Asia Business Studies 15: 1–30. [Google Scholar] [CrossRef]

- Keller, Carmen, and Michael Siegrist. 2006. Investing in Stocks: The Influence of Financial Risk Attitude and Values-Related Money and Stock Market Attitudes. Journal of Economic Psychology 27: 285–303. [Google Scholar] [CrossRef]

- Khalily, M. A. Baqui. 2016. Financial Inclusion, Financial Regulation, and Education in Bangladesh. ADBI Working Paper 621. Tokyo: Asian Development Bank Institute. [Google Scholar] [CrossRef] [Green Version]

- Kline, Rex B. 2011. Principles and Practice of Structural Equation Modeling, 3rd ed. New York: Guilford Press. [Google Scholar]

- Klontz, Bradley, Sonya L Britt, Jennifer Mentzer, and Ted Klontz. 2011. Money Beliefs and Financial Behaviors: Development of the Klontz Money Script Inventory. Journal of Financial Therapy 2: 1. [Google Scholar] [CrossRef]

- Koropp, Christian, Franz W. Kellermanns, Dietmar Grichnik, and Laura Stanley. 2014. Financial Decision Making in Family Firms: An Adaptation of the Theory of Planned Behavior. Family Business Review 27: 307–27. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav, and Miloslav Vosvrda. 2013. Measuring Capital Market Efficiency: Global and Local Correlations Structure. Physica A: Statistical Mechanics and Its Applications 392: 184–93. [Google Scholar] [CrossRef] [Green Version]

- Kumar, Alok, Jeremy K. Page, and Oliver G. Spalt. 2011. Religious Beliefs, Gambling Attitudes, and Financial Market Outcomes. Journal of Financial Economics 102: 671–708. [Google Scholar] [CrossRef] [Green Version]

- Kumari, Thaksila. 2020. The Impact of Financial Literacy on Investment Decisions: With Special Reference to Undergraduates in Western Province, Sri Lanka. Asian Journal of Contemporary Education 4: 110–26. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-De-Silanes, Andrei Shleifer, and Robert Vishny. 2000. Investor Protection and Corporate Governance. Journal of Financial Economics 58: 3–27. [Google Scholar] [CrossRef] [Green Version]

- Lee, Jae Min, Jonghee Lee, and Kyoung Tae Kim. 2019. Consumer Financial Well-Being: Knowledge Is Not Enough. Early Childhood Education Journal 41: 218–28. [Google Scholar] [CrossRef]

- Liu, Matthew Tingchi, James L. Brock, Gui Cheng Shi, Rongwei Chu, and Ting-Hsiang Tseng. 2013. Perceived Benefits, Perceived Risk, and Trust. Asia Pacific Journal of Marketing and Logistics 25: 225–48. [Google Scholar] [CrossRef]

- Lo, Andrew W. 2005. Reconciling Efficient Markets with Behavioral Finance: The Adaptive Markets Hypothesis. Journal of Investment Consulting 7: 21–44. [Google Scholar] [CrossRef]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2007. Baby Boomer Retirement Security: The Roles of Planning, Financial Literacy, and Housing Wealth. Journal of Monetary Economics 54: 205–24. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2008. Planning and Financial Literacy: How Do Women Fare? American Economic Review 98: 413–17. [Google Scholar] [CrossRef] [Green Version]

- Mandell, Lewis, and Kermit O. Hanson. 2009. The Impact of Financial Education in High School and College on Financial Literacy and Subsequent Financial Decision Making. Paper presented at American Economic Association Meetings, San Francisco, CA, USA, January 4; Volume 51. [Google Scholar]

- Markowitz, Harry. 1952. The Utility of Wealth. Journal of Political Economy 60: 151–58. [Google Scholar] [CrossRef]

- Mate, Rashmi, and Leena Dam. 2018. Role of an attitude and financial literacy in stock market participation. International Journal of Management, IT and Engineering 7: 137–49. [Google Scholar] [CrossRef]

- Nadeem, Muhammad Asif, Muhammad Ali Jibran Qamar, Mian Sajid Nazir, Israr Ahmad, Anton Timoshin, and Khurram Shehzad. 2020. How Investors Attitudes Shape Stock Market Participation in the Presence of Financial Self-Efficacy. Frontiers in Psychology 11: 553351. [Google Scholar] [CrossRef]

- Ng, Adam, Mansor H. Ibrahim, and Abbas Mirakhor. 2016. Does Trust Contribute to Stock Market Development? Economic Modelling 52: 239–50. [Google Scholar] [CrossRef]

- Niu, Geng, Qi Wang, Han Li, and Yang Zhou. 2020. Number of Brothers, Risk Sharing, and Stock Market Participation. Journal of Banking & Finance 113: 105757. [Google Scholar] [CrossRef]

- Noussair, Charles N., Stefan T. Trautmann, and Gijs van de Kuilen. 2014. Higher Order Risk Attitudes, Demographics, and Financial Decisions. The Review of Economic Studies 81: 325–55. [Google Scholar] [CrossRef] [Green Version]

- Oehler, Andreas, Matthias Horn, and Florian Wedlich. 2018. Young adults’ Subjective and Objective Risk Attitude in Financial Decision Making. Review of Behavioral Finance 10: 274–94. [Google Scholar] [CrossRef]

- Özbilgin, H. Murat. 2010. Financial Market Participation and the Developing Country Business Cycle. Journal of Development Economics 92: 125–37. [Google Scholar] [CrossRef]

- Parmitasari, Rika Dwi Ayu, Djabir Hamzah, Syamsu Alam, and Abdul Rakhman Laba. 2018. Analysis of Ethics and Investor Behavior and Its Impact on Financial Satisfaction of Capital Market Investors. Scienctific Research Journal 4: 51–69. Available online: www.scrij.Org (accessed on 22 November 2021).

- Perry, Vanessa G., and Marlene D. Morris. 2005. Who Is in Control? The Role of Self-Perception, Knowledge, and Income in Explaining Consumer Financial Behavior. Journal of Consumer Affairs 39: 299–313. [Google Scholar] [CrossRef]

- Phan, Khoa Cuong, and Jian Zhou. 2014. Factors Influencing Individual Investor Behavior: An Empirical Study of the Vietnamese Stock Market. American Journal of Business and Management 3: 77–94. [Google Scholar]

- Pinjisakikool, Teerapong. 2017. The Effect of Personality Traits on households’ Financial Literacy. Citizenship, Social and Economics Education 16: 39–51. [Google Scholar] [CrossRef]

- Popat, Disha A., and Hemal B. Pandya. 2018. Evaluating the Effect of Financial Knowledge on Investment Decisions of Investors from Gandhinagar District. International Journal of Engineering and Management Research 8: 226–37. [Google Scholar] [CrossRef]

- Rao, Yulei, Lixing Mei, and Rui Zhu. 2016. Happiness and Stock-Market Participation: Empirical Evidence from China. Journal of Happiness Studies 17: 271–93. [Google Scholar] [CrossRef]

- Rimal, Rajiv N., and Kevin Real. 2003. Perceived Risk and Efficacy Beliefs as Motivators of Change: Use of the risk perception attitude (RPA) framework to understand health behaviors. Human Communication Research 29: 370–99. [Google Scholar] [CrossRef]

- Sahi, Shalini Kalra. 2017. Psychological Biases of Individual Investors and Financial Satisfaction. Journal of Consumer Behaviour 16: 511–35. [Google Scholar] [CrossRef]

- Shehata, Saleh M., Alaa M. Abdeljawad, Loqman A. Mazouz, Lamia Yousif Khalaf Aldossary, Maryam Y. AlSaeed, and Mohamed Noureldin Sayed. 2021. The Moderating Role of Perceived Risks in the Relationship Between Financial Knowledge and the Intention to Invest in the Saudi Arabian Stock Market. International Journal of Financial Studies 9: 9. [Google Scholar] [CrossRef]

- Shih, Tsui-Yii, and Sheng-Chen Ke. 2014. Determinates of Financial Behavior: Insights into Consumer Money Attitudes and Financial Literacy. Service Business 8: 217–38. [Google Scholar] [CrossRef]

- Shinohara, Kazumitsu. 2016. Perceptual and Cognitive Processes in Human Behavior. In Cognitive Neuroscience Robotics B. Tokyo: Springer, pp. 1–22. [Google Scholar] [CrossRef]

- Shusha, Amir Amir Ali. 2017. Does Financial Literacy Moderate the Relationship Among Demographic Characteristics and Financial Risk Tolerance? Evidence from Egypt. Australasian Business, Accounting and Finance Journal 11: 67–86. [Google Scholar] [CrossRef] [Green Version]

- Simon, Herbert A. 1955. A Behavioral Model of Rational Choice. The Quarterly Journal of Economics 69: 99–118. [Google Scholar] [CrossRef]

- Spector, Paul E., and Michael T. Brannick. 2011. Methodological Urban Legends: The Misuse of Statistical Control Variables. Organizational Research Methods 14: 287–305. [Google Scholar] [CrossRef]

- Van Rooij, Maarten, and Federica Teppa. 2014. Personal Traits and Individual Choices: Taking Action in Economic and Non-Economic Decisions. Journal of Economic Behavior & Organization 100: 33–43. [Google Scholar] [CrossRef]

- Van Rooij, Maarten, Annamaria Lusardi, and Rob Alessie. 2007. Financial Literacy and Stock Market Participation. Financial Literacy and Stock Market Participation 101: 449–72. [Google Scholar] [CrossRef]

- Vissing-Jørgensen, Annette, and Orazio P. Attanasio. 2003. Stock-Market Participation, Intertemporal Substitution, and Risk-Aversion. American Economic Review 93: 383–91. [Google Scholar] [CrossRef] [Green Version]

- Von Gaudecker, Hans-Martin. 2015. How Does Household Portfolio Diversification Vary With Financial Literacy and Financial Advice? The Journal of Finance 70: 489–507. [Google Scholar] [CrossRef]

- Vroom, Victor Harold. 1964. Work and Motivation. Hoboken: Wiley. [Google Scholar]

- Waheed, Haseeb, Zeeshan Ahmedb, Qasim Saleemc, Sajid Mohy Ul Dind, and Bilal Ahmede. 2020. The Mediating Role of Risk Perception in the Rela-Tionship between Financial Literacy and Investment Decision. International Journal of Innovation, Creativity and Change 14: 112–31. [Google Scholar] [CrossRef]

- Wäneryd, Karl-Erik. 2001. Stock-Market Psychology: How People Value and Trade Stocks. North-Hampton: Edward Elgar Publishing. [Google Scholar]

- Weber, Elke U. 2010. Risk Attitude and Preference. Wiley Interdisciplinary Reviews: Cognitive Science 1: 79–88. [Google Scholar] [CrossRef]

- Weber, Elke U., Ann-Renee Blais, and Nancy E. Betz. 2002. A domain-specific risk-attitude scale: Measuring risk perceptions and risk behaviors. Journal of Behavioral Decision Making 15: 263–90. [Google Scholar] [CrossRef]

- Wicker, Allan W. 1969. Attitudes versus Actions: The Relationship of Verbal and Overt Behavioral Responses to Attitude Objects. Journal of Social Issues 25: 41–78. [Google Scholar] [CrossRef] [Green Version]

- Wicker, Allan W., and Richard J. Pomazal. 1971. The Relationship between Attitudes and Behavior As a Function of Specificity of Attitude Object and Presence of a Significant Person During Assessment Conditions. Representative Research in Social Psychology 2: 26–31. [Google Scholar]

- Wilson, Warner R. 1967. Correlates of Avowed Happiness. Psychological Bulletin 67: 294–306. [Google Scholar] [CrossRef] [PubMed]

- Xiao, Jing Jian, and Nilton Porto. 2017. Financial Education and Financial Satisfaction. International Journal of Bank Marketing 35: 805–17. [Google Scholar] [CrossRef]

- Xiao, Jing Jian, Barbara O’Neill, Janice M. Prochaska, Claudia M. Kerbel, Patricia Brennan, and Barbara J. Bristow. 2004. A Consumer Education Programme Based on the Transtheoretical Model of Change. International Journal of Consumer Studies 28: 55–65. [Google Scholar] [CrossRef]

- Yang, Marvello, Abdullah Mamun, Muhammad Mohiuddin, Sayed Al-Shami, and Noor Zainol. 2021. Predicting Stock Market Investment Intention and Behavior among Malaysian Working Adults Using Partial Least Squares Structural Equation Modeling. Mathematics 9: 873. [Google Scholar] [CrossRef]

- Yeske, Dave, and Elissa Buie. 2014. Policy-Based Financial Planning: Decision Rules for a Changing World. In Investor Behavior: The Psychology of Financial Planning and Investing. Hoboken: John Wiley & Sons, pp. 189–208. [Google Scholar] [CrossRef]

- Zhang, Yu, and Honggang Li. 2011. Investors’ Risk Attitudes and Stock Price Fluctuation Asymmetry. Physica A: Statistical Mechanics and Its Applications 390: 1655–61. [Google Scholar] [CrossRef]

- Zhang, Don C., Scott Highhouse, and Christopher D. Nye. 2019. Development and Validation of the General Risk Propensity Scale (GRiPS). Journal of Behavioral Decision Making 32: 152–67. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Category | Group | Numbers of Respondents | Frequency |

|---|---|---|---|

| Gender | Male | 259 | 67.1% |

| Female | 127 | 32.9% | |

| Age | 18–25 Years | 27 | 7.0% |

| 26–35 Years | 139 | 36.0% | |

| 36–45 Years | 120 | 31.1% | |

| 46–55 Years | 58 | 15.0% | |

| 55+ Years | 42 | 10.9% | |

| Educational Background | SSC | 23 | 6.0% |

| HSC | 65 | 16.8% | |

| Honors | 184 | 47.7% | |

| Masters | 114 | 29.5% |

| Construct | Measurement Items | Factor Loading | Cronbach’s Alpha (>0.70) | rho_A | Composite Reliability (>0.70) | AVE (>0.50) |

|---|---|---|---|---|---|---|

| Attitude (ATT) | ATT1: Choosing the stock market is a good idea | 0.707 | 0.839 | 0.866 | 0.878 | 0.509 |

| ATT2: I like to invest in the capital market | 0.698 | |||||

| ATT3: Most people who are important to me have investments in the stock market | 0.674 | |||||

| ATT4: My family members prefer the stock market | 0.597 | |||||

| ATT5: I prefer the stock market because it is interest-free income | 0.794 | |||||

| ATT6: I prefer the stock market because of the capital gain opportunities | 0.825 | |||||

| ATT7: I can trade or invest in the stock market whenever I want | 0.674 | |||||

| Perceived Benefit (PB) | PB1: The profit from the share market is higher than other investments | 0.719 | 0.852 | 0.862 | 0.894 | 0.628 |

| PB2: Investing in the stock market seems to generate high returns for me (e.g., dividends and capital gains) | 0.798 | |||||

| PB3: I believe the stocks I invested in will perform satisfactorily in the future | 0.851 | |||||

| PB4: I think investing in stocks is highly rewarding | 0.811 | |||||

| PB5: Higher returns motivate me to invest in the share market | 0.777 | |||||

| Perceived Risk (PR) | PR1: It is a risky decision to invest in the share market | 0.67 | 0.717 | 1.868 | 0.785 | 0.564 |

| PR2: I may lose money due to the uncertainty in the stock market | 0.90 | |||||

| PR3: It is important to avoid monetary losses | 0.66 | |||||

| Financial Literacy (FL) * | FL Is a single item construct with a score ranging from 0 to 10 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| Financial Planning (FP) | FP1: I save money for retirement | 0.637 | 0.709 | 0.749 | 0.815 | 0.525 |

| FP2: At any time, I have some money saved for emergencies | 0.717 | |||||

| FP3: I ensure that with every pay, I save some | 0.813 | |||||

| FP5: My insurance/takaful coverage is sufficient to meet costs related to emergency events | 0.722 | |||||

| Financial Satisfaction (FS) | FS2: I am satisfied with my current financial situation | 0.756 | 0.835 | 0.838 | 0.883 | 0.602 |

| FS3: I can do little to improve my current financial situation | 0.824 | |||||

| FS4: I rarely run short of money | 0.794 | |||||

| FS5: Based on my current financial situation, I could easily obtain a loan if I needed one (e.g., car loans, personal loans) | 0.786 | |||||

| FS6: If I had a major loss of income I could manage for a period of time (e.g., for 3 months) | 0.715 | |||||

| Behavioral Intention (BI) | BI1: I will invest in the share market | 0.767 | 0.840 | 0.841 | 0.893 | 0.677 |

| BI3: I will speak favorably about investing in the share market | 0.823 | |||||

| BI4: I will recommend investing in the share market if someone asks for my advice | 0.877 | |||||

| BI5: I will encourage my friends and family to invest in the share market | 0.819 |

| ATT | BI | FL | FP | FS | PB | |

|---|---|---|---|---|---|---|

| BI | 0.768 | |||||

| FL | 0.042 | 0.045 | ||||

| FP | 0.509 | 0.494 | 0.233 | |||

| FS | 0.351 | 0.255 | 0.096 | 0.405 | ||

| PB | 0.744 | 0.676 | 0.037 | 0.487 | 0.276 | |

| PR | 0.164 | 0.126 | 0.045 | 0.120 | 0.182 | 0.097 |

| ATT | BI | FL | FP | FS | PB | PR | |

|---|---|---|---|---|---|---|---|

| ATT | 0.714 | ||||||

| BI | 0.667 | 0.823 | |||||

| FL | 0.003 | 0.005 | 1.000 | ||||

| FP | 0.402 | 0.406 | 0.191 | 0.725 | |||

| FS | 0.291 | 0.216 | −0.032 | 0.331 | 0.776 | ||

| PB | 0.640 | 0.580 | 0.013 | 0.384 | 0.230 | 0.793 | |

| PR | −0.082 | −0.121 | 0.000 | −0.016 | 0.012 | 0.048 | 0.751 |

| Hypotheses | Coefficient | SD | t Statistics | Decision for Hypothesis | |

|---|---|---|---|---|---|

| Panel A: Control Variables | |||||

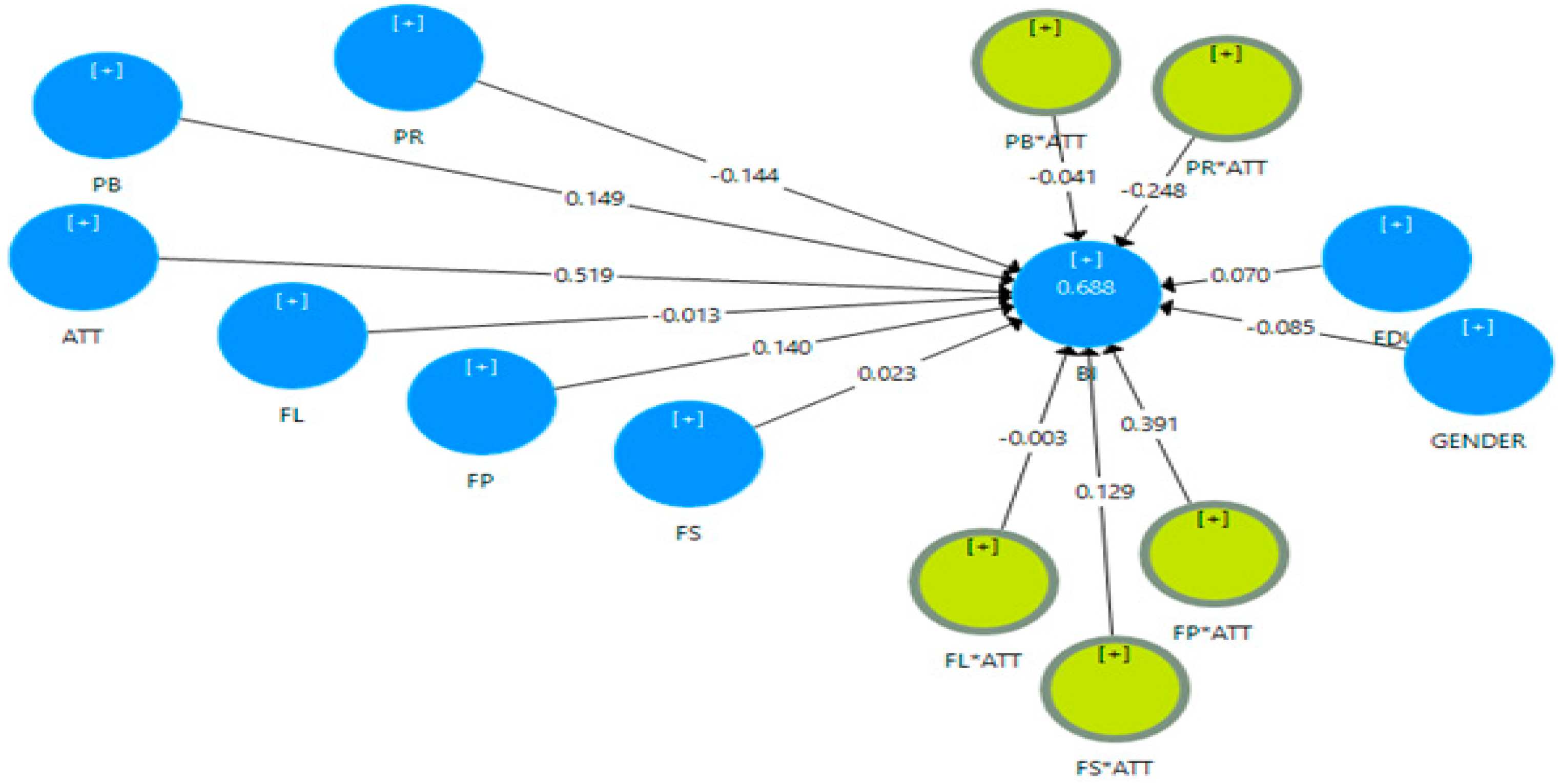

| GENDER -> BI | −0.085 | 0.067 | −1.269 | NA | |

| EDU -> BI | 0.070 | 0.022 | 3.182 ** | NA | |

| Panel B: Exogenous Variables | |||||

| H1 | ATT -> BI | 0.519 | 0.068 | 7.632 *** | Supported |

| H2 | FL -> BI | −0.013 | 0.122 | −0.107 | Not Supported |

| H3 | FP -> BI | 0.140 | 0.066 | 2.121 ** | Supported |

| H4 | FS -> BI | 0.023 | 0.059 | 0.390 | Not Supported |

| H5 | PR -> BI | −0.144 | 0.039 | −3.692 *** | Supported |

| H6 | PB -> BI | 0.149 | 0.071 | 2.099 ** | Supported |

| Panel C: Moderating Terms | |||||

| H2a | FL*ATT -> BI | −0.003 | 0.059 | −0.051 | Not Supported |

| H3a | FP*ATT -> BI | 0.391 | 0.049 | 7.947 *** | Supported |

| H4a | FS*ATT -> BI | 0.129 | 0.053 | 2.434 ** | Supported |

| H5a | PR*ATT -> BI | −0.248 | 0.072 | −3.444 *** | Supported |

| H6a | PB*ATT -> BI | −0.041 | 0.106 | −0.387 | Not Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Akhter, T.; Hoque, M.E. Moderating Effects of Financial Cognitive Abilities and Considerations on the Attitude–Intentions Nexus of Stock Market Participation. Int. J. Financial Stud. 2022, 10, 5. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10010005

Akhter T, Hoque ME. Moderating Effects of Financial Cognitive Abilities and Considerations on the Attitude–Intentions Nexus of Stock Market Participation. International Journal of Financial Studies. 2022; 10(1):5. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10010005

Chicago/Turabian StyleAkhter, Tahmina, and Mohammad Enamul Hoque. 2022. "Moderating Effects of Financial Cognitive Abilities and Considerations on the Attitude–Intentions Nexus of Stock Market Participation" International Journal of Financial Studies 10, no. 1: 5. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10010005