Europe’s Elite Football: Financial Growth, Sporting Success, Transfer Investment, and Private Majority Investors

Abstract

:1. Introduction

2. Revenues and Financial Growth in Europe’s Elite Football

3. Relevance of Europe’s Elite Football Clubs from a Sporting Perspective

4. Strategies in Europe’s Elite Football

4.1. Contests and the Economics of Overinvestment

4.2. Global Brands: Non-Sport Related Income

4.3. Sugar Daddies: Spending Power Through Financial Resources of Private Majority Owners

5. Theoretical Framework and Literature Review

5.1. Financial Success

5.2. National/International Sporting Success

5.3. Team Investments

6. Method

6.1. Data Source and Collection

6.2. Measures

6.3. Data Analysis

7. Results and Discussion

7.1. Descriptive Statistics

7.2. Variation

7.3. Panel Regression

8. Conclusions

8.1. Summary of Study

8.2. Managerial Implications

8.3. Limitations and Recommendations for Further Research

Acknowledgments

Author Contributions

Conflicts of Interest

Abbreviations

| FIFA: | Fédération Internationale de Football Association |

| UEFA: | Union of European Football Associations |

| OLS: | Ordinary least squares |

| FE: | Fixed effects |

| 2sls: | Two-stage least squares |

| FE IV: | Fixed effects instrumental variables |

| HHI: | Herfindahl–Hirschman Index |

References

- S. Szymanski, and R. Smith. “The English Football Industry: Profit, performance and industrial structure.” Int. Rev. Appl. Econ. 11 (1997): 135–153. [Google Scholar] [CrossRef]

- S.M. Dobson, and J.A. Goddard. “Performance and revenue in professional league football: Evidence from Granger causality tests.” Appl. Econ. 30 (1998): 1641–1651. [Google Scholar] [CrossRef]

- S. Szymanski, and T. Kuypers. Winners & Losers—The Business Strategy of Football. London, UK: Penguin Books, 1999. [Google Scholar]

- N. Scelles, B. Helleu, C. Durand, and L. Bonnal. “Professional sports firm values: Bringing new determinants to the foreground? A study of European soccer, 2005–2013.” J. Sports Econ., 2014. [Google Scholar] [CrossRef]

- M. Rohde, and C. Breuer. “The Financial Impact of (Foreign) Private Investors on Team Investments and Profits in Professional Football: Empirical Evidence from the Premier League.” Appl. Econ. Finance 3 (2016): 243–256. [Google Scholar] [CrossRef]

- S. Kuper. “How to be an elite club?—and will the losers go bust and disappear? Roundtable: “Perspectives and Economic Challenges for Elite Football Clubs”.” Barcelona, Spain: IESE Business School, 2009. Available online: http://www.iese.edu/en/ad/sp-sp/armandcarabnworkshoponfootballeconomics.asp (accessed on 19 August 2014).

- E. Franck. “Private Firm, Public Corporation or Member’s Association Governance Structures in European Football.” Int. J. Sport Finance 5 (2010): 108–127. [Google Scholar]

- E. Franck. “„Zombierennen“ und „Patenonkel“—Warum deutsche Fussballklubs in der Champions League den Kürzeren ziehen.” CRSA Working Paper 36 (2010): 1–13. Available online: http://econpapers.repec.org/paper/isowpaper/0124.htm (accessed on 4 February 2014). [Google Scholar]

- R. Wilson, D. Plumley, and G. Ramchandani. “The relationship between ownership structure and club performance in the English Premier League.” Sport Bus. Manag. Int. J. 3 (2013): 19–36. [Google Scholar] [CrossRef]

- T. Pawlowski, C. Breuer, and A. Hovemann. “Top Clubs’ Performance and the Competitive Situation in European Domestic Football Competitions.” J. Sports Econ. 11 (2010): 186–202. [Google Scholar] [CrossRef]

- N. Scelles, B. Helleu, C. Durand, and L. Bonnal. “Determinants of professional sports firm values in the United States and Europe: A comparison between sports over the period 2004–2011.” Int. J. Sport Finance 8 (2013): 280–293. [Google Scholar]

- S. Szymanski. “The Future of Football in Europe.” In Sports Economics after Fifty Years: Essays in Honour of Simon Rottenberg. Edited by P. Rodriguez, S. Kesenne and J. Garcia. Oviedo, Spain: University of Oviedo Press, 2007. [Google Scholar]

- J.M. Gladden, and G.R. Milne. “Examining the Importance of Brand Equity in Professional Sport.” Sport Mark. Q. 8 (1999): 21–29. [Google Scholar]

- T. Pawlowski, and C. Anders. “Stadium attendance in German professional football—The (un)importance of uncertainty of outcome reconsidered.” Appl. Econ. Lett. 19 (2012): 1553–1556. [Google Scholar] [CrossRef]

- Deloitte. Annual Review of Football Finance: A Premium Blend. Manchester, UK: Deloitte & Touche, 2014. [Google Scholar]

- Deloitte. Football Money League: All to Play for. Manchester, UK: Deloitte & Touche, 2014. [Google Scholar]

- Brand Finance. Football 50: The Annual Report on the World’s Most Valuable Football Brands. London, UK: Brand Finance Plc., 2013. [Google Scholar]

- H.M. Dietl, and E. Franck. “Warum Investitionswettläufe und wachsende Erlösasymmetrien das Geschäftsmodell des europäischen Profifußballs zunehmend belasten.” Zeitschrift Führung + Organisation 6 (2006): 333–337. [Google Scholar]

- W.C. Neale. “The Peculiar Economics of Professional Sports: A Contribution to the Theory of the Firm in Sporting Competition and in Market Competition.” Q. J. Econ. 78 (1964): 1–14. [Google Scholar] [CrossRef]

- M.E. Canes. “The social benefits of the restrictions on team quality.” In Government and the Sports Business. Edited by R.G. Noll. Washington, DC, USA: The Brookings Institution, 1974, pp. 77–114. [Google Scholar]

- G. Akerlof. “The Economics of Caste and of the Rat Race and Other Woeful Tales.” Q. J. Econ. 90 (1976): 599–617. [Google Scholar] [CrossRef]

- J.C. Müller, J. Lammert, and G. Hovemann. “The Financial Fair Play regulations of UEFA: An adequate concept to ensure the long-term viability and sustainability of European club football.” Int. J. Sport Finance 7 (2012): 117–140. [Google Scholar]

- H.M. Dietl, E. Franck, and M. Lang. “Overinvestment in Team Sports Leagues: A Contest Theory Model.” Scott. J. Political Econ. 55 (2008): 353–368. [Google Scholar] [CrossRef]

- B. Gerrard. “A resource-utilization model of organizational efficiency in professional sports teams.” J. Sport Manag. 19 (2005): 143–169. [Google Scholar]

- P. Wicker, and C. Breuer. “Scarcity of resources in German non-profit sport clubs.” Sport Manag. Rev. 14 (2011): 188–201. [Google Scholar] [CrossRef]

- B. Wernerfelt. “A resource-based view of the firm.” Strateg. Manag. J. 5 (1984): 171–180. [Google Scholar] [CrossRef]

- D. Conn. “Record income but record losses for Premier League.” The Guardian, 19 May 2011. [Google Scholar]

- A.A. Alchian. “Some Economics of Property Rights.” In Economic Forces at Work. Edited by A.A. Alchian. Indianapolis, IN, USA: Liberty Press, 1977, pp. 127–149. [Google Scholar]

- P. Milgrom, and J. Roberts. Economics, Organization and Management. Englewood Cliffs, NJ, USA: Prentice-Hall, 1992. [Google Scholar]

- H. Demsetz. “Toward a Theory of Property Rights.” Am. Econ. Rev. 57 (1967): 347–359. [Google Scholar]

- A. Picot, H. Dietl, and E. Franck. Organisation—Eine ökonomische Perspektive, 5th ed. Stuttgart, Germany: Schäffer-Poeschel Verlag, 2008. [Google Scholar]

- A. Shleifer, and R. Vishny. “A survey of corporate governance.” J. Finance 52 (1997): 737–783. [Google Scholar] [CrossRef]

- P.E. Dimitropoulos, and A. Tsagkanos. “Financial Performance and Corporate Governance in the European Football Industry.” Int. J. Sport Finance 7 (2012): 280–308. [Google Scholar]

- P. Garcia-del-Barrio, and S. Szymanski. “Goal! Profit Maximization versus Win Maximization in Soccer.” Rev. Ind. Organ. 34 (2009): 45–68. [Google Scholar] [CrossRef]

- A. Baroncelli, and U. Lago. “Italian Football.” J. Sports Econ. 7 (2006): 13–28. [Google Scholar] [CrossRef]

- D. Czarnitzki, and G. Stadtmann. “Uncertainty of outcome versus reputation: Empirical evidence for the first German football division.” Empiri. Econ. 27 (2002): 101–112. [Google Scholar] [CrossRef]

- H.H. Bauer, N.E. Sauer, and P. Schmitt. “Customer-based brand equity in the team sport industry: Operationalization and impact on the economic success of sport teams.” Eur. J. Mark. 39 (2005): 496–513. [Google Scholar] [CrossRef]

- D. Forrest, and R. Simmons. “Team Salaries and Playing Success in Sports: A Comparative Perspective.” In Sportökonomie. Edited by H. Albach and B. Frick. Wiesbaden, Germany: Gabler Verlag, 2002, pp. 221–238. [Google Scholar]

- S. Hall, S. Szymanski, and A.S. Zimbalist. “Testing Causality between Team Performance and Payroll: The Cases of Major League Baseball and English Soccer.” J. Sports Econ. 3 (2002): 149–168. [Google Scholar] [CrossRef]

- P.E. Dimitropoulos, and V. Limperopoulos. “Player contracts, athletic and financial performance of the Greek football clubs.” Glob. Bus. Econ. Rev. 16 (2014): 123–141. [Google Scholar] [CrossRef]

- B. Frick. “Die Voraussetzungen sportlichen und wirtschaftlichen Erfolges in der Fußball-Bundesliga.” In Business-to-Business-Marketing im Profifußball. Edited by M. Bieling, M. Eschweiler and J. Hardenacke. Wiesbaden, Germany: Deutscher Universitätsverlag, 2004, pp. 71–93. [Google Scholar]

- B. Frick, and R. Simmons. “The impact of managerial quality on organizational performance: Evidence from German soccer.” Manag. Decis. Econ. 29 (2008): 593–600. [Google Scholar] [CrossRef]

- S. Szymanski. “Wages, transfers and the variation of team Performance in the English Premier League.” In Proceedings of the VI Gijon Conference on Sports Economics, Gijon, Spain, 6–7 May 2011.

- E.F. Fama, and M.C. Jensen. “Agency Problems and Residual Claims.” J. Law Econ. 26 (1983): 327–349. [Google Scholar] [CrossRef]

- M. Sass. “Glory Hunters, Sugar Daddies, and Long-Term Competitive Balance under UEFA Financial Fair Play.” J. Sports Econ. 17 (2016): 148–158. [Google Scholar] [CrossRef]

- M. Grossmann. “Evolutionarily Stable Strategies in Sports Contests.” J. Sports Econ. 16 (2015): 108–121. [Google Scholar] [CrossRef]

- J. Mincer. Schooling, Experience, and Earnings. New York, NY, USA: Columbia University Press, 1974. [Google Scholar]

- D. Coates, B. Frick, and T. Jewell. “Superstar Salaries and Soccer Success: The Impact of Designated Players in Major League Soccer.” J. Sports Econ., 2014. [Google Scholar] [CrossRef]

- D.G. Baur, and C. McKeating. “Do Football Clubs Benefit from Initial Public Offerings? ” Int. J. Sport Finance 6 (2011): 40–59. [Google Scholar]

- E. Franck, and M. Lang. “A theoretical analysis of the influence of money injections on risk taking in football clubs.” Scott. J. Political Econ. 61 (2014): 430–454. [Google Scholar] [CrossRef]

- B. Frick. “Salary determination and the pay-performance relationship in professional soccer: Evidence from Germany.” In Sports Economics after Fifty Years: Essays in Honour of Simon Rottenberg. Edited by S. Rodriguez, S. Kesenne and J. Garcia. Oviedo, Spain: Ediciones de la Universidad de Oviedo, 2006, pp. 125–146. [Google Scholar]

- C. Green, F. Lozano, and R. Simmons. “Rank-order tournaments, probability of winning and investing in talent: Evidence from champions’ league qualifying rules.” Natl. Inst. Econ. Rev. 232 (2015): R30–R40. [Google Scholar] [CrossRef] [Green Version]

- J. Durbin. “Errors in Variables.” Rev. Int. Stat. Inst. 22 (1954): 23–32. [Google Scholar] [CrossRef]

- J.A. Hausman. “Specification tests in econometrics.” Econometrica 46 (1978): 1251–1271. [Google Scholar] [CrossRef]

- D.-M. Wu. “Alternative tests of independence between stochastic regressors and disturbances: Finite sample results.” Econometrica 42 (1974): 529–546. [Google Scholar] [CrossRef]

- J.H. Stock, and M. Yogo. “Testing for weak instruments in linear IV regression.” In Identification and Inference for Econometric Models: Essays in Honor of Thomas Rothenberg. Edited by D.W.K. Andrews and J.H. Stock. New York, NY, USA: Cambridge University Press, 2005, pp. 80–108. [Google Scholar]

- J. Bound, D.A. Jaeger, and R.M. Baker. “Problems with instrumental variables estimation when the correlation between the instruments and the endogenous explanatory variable is weak.” J. Am. Stat. Assoc. 90 (1995): 443–450. [Google Scholar] [CrossRef]

- 1Without the foreign majority investor dummy, private majority investors are shown to have a positive and significant impact on team investments at the 5% level. Results are available upon request.

{kind=link}

{kind=link}

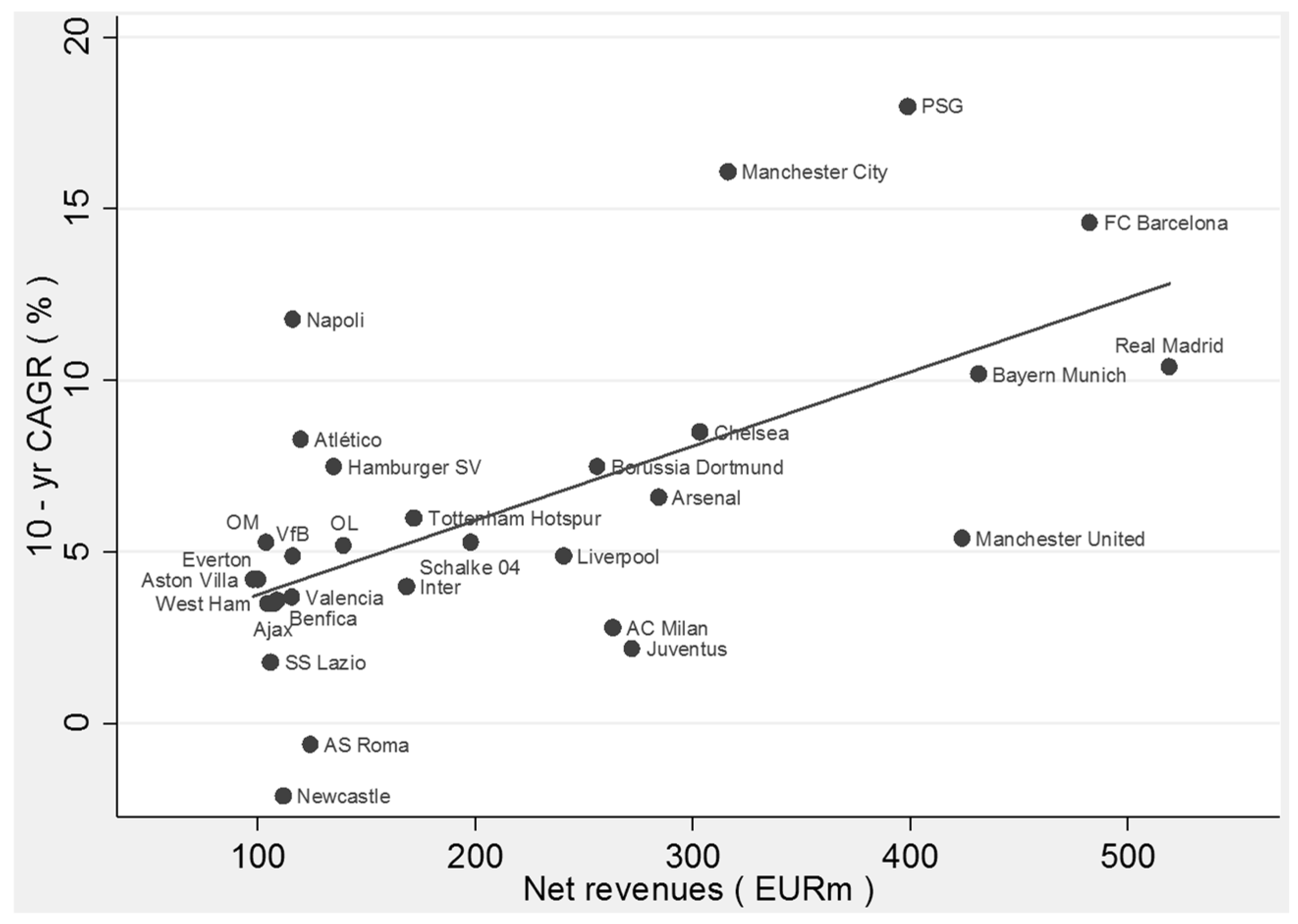

| # | Club | Country | Majority Owner | Avg. Annual Rev. Growth 2004–2013 (% p.a.) |

|---|---|---|---|---|

| 1 | Paris Saint-Germain | France | Qatar Sport Investments | 18.0% |

| 2 | Manchester City | England | Sheikh Mansour | 16.1% |

| 3 | FC Barcelona | Spain | Club members | 14.6% |

| 4 | SSC Napoli | Italy | Filmauro | 11.8% |

| 5 | Real Madrid | Spain | Club members | 10.4% |

| 6 | Bayern Munich | Germany | Club members | 10.2% |

| 7 | Chelsea FC | England | Roman Abramovich | 8.5% |

| 8 | Atlético Madrid | Spain | Miguel Angel Gil | 8.3% |

| 9 | Borussia Dortmund | Germany | Distributed ownership | 7.5% |

| 10 | Hamburger SV | Germany | Club members | 7.5% |

| 11 | Arsenal FC | England | Stan Kroenke | 6.6% |

| 12 | Tottenham Hotspur FC | England | Enic International Limited | 6.0% |

| 13 | Manchester United | England | Glazer family | 5.4% |

| 14 | Olympique de Marseille | France | Margarita Louis-Dreyfus | 5.3% |

| 15 | FC Schalke 04 | Germany | Club members | 5.3% |

| 16 | Olympique Lyonnais | France | Jean-Michel Aulas | 5.2% |

| 17 | VfB Stuttgart | Germany | Club members | 4.9% |

| 18 | Liverpool FC | England | Fenway Sports Group | 4.9% |

| 19 | Aston Villa FC | England | Randy Lerner | 4.2% |

| 20 | Everton FC | England | Distributed ownership | 4.2% |

| 21 | Valencia CF | Spain | Club members | 3.7% |

| 22 | Benfica | Portugal | Club members | 3.6% |

| 23 | West Ham United | England | David Sullivan/David Gold | 3.5% |

| 24 | Ajax Amsterdam | The Netherlands | Club members | 3.5% |

| 25 | AC Milan | Italy | Silvio Berlusconi | 2.8% |

| 26 | Juventus | Italy | Agnelli family | 2.2% |

| 27 | SS Lazio | Italy | Claudio Lotito | 1.8% |

| 28 | Inter Milan | Italy | Massimo Moratti | 0.4% |

| 29 | AS Roma | Italy | Thomas R. DiBenedetto | (0.6%) |

| 30 | Newcastle United | England | Mike Ashley | (2.1%) |

| # | England | France | Germany | Italy | Spain |

|---|---|---|---|---|---|

| 2004 | Arsenal FC | Ol. Lyonnais | Werder Bremen 1 | AC Milan | Valencia CF |

| 2005 | Chelsea FC | Ol. Lyonnais | Bayern Munich | Juventus 3 | FC Barcelona |

| 2006 | Chelsea FC | Ol. Lyonnais | Bayern Munich | Inter Milan | FC Barcelona |

| 2007 | Manchester Utd. | Ol. Lyonnais | VfB Stuttgart | Inter Milan | Real Madrid |

| 2008 | Manchester Utd. | Ol. Lyonnais | Bayern Munich | Inter Milan | Real Madrid |

| 2009 | Manchester Utd. | Bordeaux 1 | VfL Wolfsburg 2 | Inter Milan | FC Barcelona |

| 2010 | Chelsea FC | Ol. Marseille | Bayern Munich | Inter Milan | FC Barcelona |

| 2011 | Manchester Utd. | Lille OSC | Bor. Dortmund | AC Milan | FC Barcelona |

| 2012 | Manchester City | Montpellier | Bor. Dortmund | Juventus | Real Madrid |

| 2013 | Manchester Utd. | Paris SG | Bayern Munich | Juventus | FC Barcelona |

| Top 30 (%) | 100% | 70% | 80% | 100% | 100% |

| # | Winner | Runner-Up | Half Finalist 1 | Half Finalist 2 | Top 30 (%) |

|---|---|---|---|---|---|

| 2004 | FC Porto | AS Monaco | Chelsea FC | Dep. La Coruna | 25% |

| 2005 | Liverpool FC | AC Milan | Chelsea FC | PSV Eindhoven | 75% |

| 2006 | FC Barcelona | Arsenal FC | AC Milan | FC Villareal | 75% |

| 2007 | AC Milan | Liverpool FC | Chelsea FC | Manchester Utd. | 100% |

| 2008 | Manchester Utd. | Chelsea FC | FC Barcelona | Liverpool FC | 100% |

| 2009 | FC Barcelona | Manchester Utd. | Arsenal FC | Chelsea FC | 100% |

| 2010 | Inter Milan | Bayern Munich | Ol. Lyonnais | FC Barcelona | 100% |

| 2011 | FC Barcelona | Manchester Utd. | Real Madrid | FC Schalke 04 | 100% |

| 2012 | Chelsea FC | Bayern Munich | Real Madrid | FC Barcelona | 100% |

| 2013 | Bayern Munich | Borussia Dortmund | Real Madrid | FC Barcelona | 100% |

| Top 30 (%) | 90% | 90% | 85% | n/a | 88% |

| # | Club | Country | Brand Value 2013 (€ m) |

|---|---|---|---|

| 1 | Bayern Munich | Germany | 668 |

| 2 | Manchester United | England | 650 |

| 3 | Real Madrid | Spain | 483 |

| 4 | FC Barcelona | Spain | 444 |

| 5 | Chelsea FC | England | 325 |

| 6 | Arsenal FC | England | 319 |

| 7 | Liverpool FC | England | 280 |

| 8 | Manchester City | England | 257 |

| 9 | AC Milan | Italy | 204 |

| 10 | Borussia Dortmund | Germany | 202 |

| 11 | FC Schalke 04 | Germany | 201 |

| 12 | Tottenham Hotspur FC | England | 170 |

| 13 | Juventus | Italy | 139 |

| 14 | Ajax Amsterdam | The Netherlands | 126 |

| 15 | Inter Milan | Italy | 117 |

| 16 | Hamburger SV | Germany | 112 |

| 17 | Galatasaray | Turkey | 90 |

| 18 | Olympique Lyonnais | France | 90 |

| 19 | Olympique de Marseille | France | 86 |

| 20 | SC Corinthians Paulista | Brazil | 80 |

| 21 | SSC Napoli | Italy | 79 |

| 22 | Fenerbahce SK | Turkey | 74 |

| 23 | Bayer 04 Leverkusen | Germany | 70 |

| 24 | Paris Saint-Germain | France | 66 |

| 25 | VfB Stuttgart | Germany | 65 |

| 26 | Valencia CF | Spain | 64 |

| 27 | VfL Wolfsburg | Germany | 64 |

| 28 | AS Roma | Italy | 64 |

| 29 | West Ham United FC | England | 64 |

| 30 | Newcastle United | England | 63 |

| Variable | Description | Scale |

|---|---|---|

| rev | Revenues excl. transfer fees (€ m) | Metric |

| lppg | League points per game (#) | Metric |

| cupwin | Win of national cup (e.g., FA Cup) (1 = yes, 0 = no) | Dummy |

| ucec | UEFA club coefficient (excl. country part) (#) | Metric |

| tra_inv | Net team transfer investments (€ m) | Metric |

| inv_maj | Private majority investor (1 = yes, 0 = no) | Dummy |

| inv_min | Private minority investor (1 = yes, 0 = no) | Dummy |

| inv_maj_for | Foreign majority investor (1 = yes, 0 = no) | Dummy |

| tra_tax | Top personal income tax rate (%) | Metric |

| bra_val | Brand value (€ m) | Metric |

| tv_sch | TV scheme (1 = Decentralized, 0 = Centralized) | Dummy |

| takeover | Takeover by new owner(s) (1 = yes; 0 = no) | Dummy |

| rev_lag | Lagged revenues excl. transfer fees (€ m) | Metric |

| lppg_lag | Lagged league points per game (#) | Metric |

| ucec_lag | Lagged UEFA club coefficient (excl. country part) (#) | Metric |

| tra_inv_lag | Lagged net team transfer investments (€ m) | Metric |

| y1–y10 | Year dummies (2004–2013; 2013 is omitted) | Dummy |

| cdum1–cdum30 | Club dummies (Top 30 clubs by revenue; Real Madrid is omitted) | Dummy |

| Variable | N | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| rev | 289 1 | 164.5 | 97.2 | 12.1 | 518.9 |

| lppg | 291 2 | 1.78 | 0.40 | 0.84 | 2.68 |

| cupwin | 300 | 13.0% | - | 0 | 1 |

| ucec | 225 3 | 15.4 | 7.36 | 1 | 33 |

| tra_inv | 300 | 14.4 | 34.4 | −80.3 | 171.3 |

| inv_maj | 300 | 75.7% | - | 0 | 1 |

| inv_min | 300 | 8.7% | - | 0 | 1 |

| inv_maj_for | 300 | 20.7% | - | 0 | 1 |

| tra_tax | 300 | 45.8% | 4.0% | 40.0% | 56.5% |

| bra_val | 231 4 | 158.9 | 128.9 | 27.3 | 667.9 |

| tv_sch | 300 | 27.3% | - | 0 | 1 |

| takeover | 300 | 4.7% | - | 0 | 1 |

| y1–y10 | 300 | 10.0% | - | 0 | 1 |

| cdum1–cdum30 | 300 | 3.3% | - | 0 | 1 |

| N | 300 |

| Within Variation from Individual Average (“xtsum”) | ||||||

|---|---|---|---|---|---|---|

| Variable | Mean | Sd | Min | Max | Count | |

| inv_maj | overall | 75.7% | 43.0% | 0 | 1 | N = 300 |

| between | 41.2% | 0 | 1 | n = 30 | ||

| within | 14.3% | –4.3% | 145.6% | T = 10 | ||

| inv_min | overall | 8.67% | 28.2% | 0 | 1 | N = 300 |

| between | 27.1% | 0 | 1 | n = 30 | ||

| within | 9.0% | –51.3% | 48.7% | T = 10 | ||

| inv_maj_for | overall | 20.7% | 40.6% | 0 | 1 | N = 300 |

| between | 34.8% | 0 | 1 | n = 30 | ||

| within | 21.6% | –69.3% | 100.7% | T = 10 | ||

| Decomposition of Counts into between and within Variation (“xttab”) | ||||||

| Overall | between | within | ||||

| Variable | Freq. | Percent | Freq. | Percent | Percent | |

| inv_maj | 0 | 73 | 24.33 | 9 | 30.00 | 81.11 |

| 1 | 227 | 75.67 | 24 | 80.00 | 94.58 | |

| Total | 300 | 100.00 | 33 | 110.00 | 90.91 | |

| inv_min | 0 | 274 | 91.33 | 28 | 93.33 | 97.86 |

| 1 | 26 | 8.67 | 3 | 10.00 | 86.67 | |

| Total | 300 | 100.00 | 31 | 103.33 | 96.77 | |

| inv_maj_for | 0 | 238 | 79.33 | 29 | 96.67 | 82.07 |

| 1 | 62 | 20.67 | 9 | 30.00 | 68.89 | |

| Total | 300 | 100.00 | 38 | 126.67 | 78.95 | |

| Transition Probabilities (“xttrans”) | ||||||

| Variable | 0 | 1 | Total | |||

| inv_maj | 0 | 95.52 | 4.48 | 100.00 | ||

| 1 | 0.00 | 100.00 | 100.00 | |||

| Total | 23.70 | 76.30 | 100.00 | |||

| inv_min | 0 | 99.60 | 0.40 | 100.00 | ||

| 1 | 0.00 | 100.00 | 100.00 | |||

| Total | 91.11 | 8.89 | 100.00 | |||

| inv_maj_for | 0 | 96.31 | 3.69 | 100.00 | ||

| 1 | 0.00 | 100.00 | 100.00 | |||

| Total | 77.41 | 22.59 | 100.00 | |||

| DV | logrev | logrev | logrev |

|---|---|---|---|

| Model | OLS with cluster-robust SEs | FE model | FE IV model (2sls) |

| ucec | 0.0074 *** | 0.0092 *** | 0.0087 *** |

| (0.0016) | (0.0013) | (0.0013) | |

| lppg | 0.0867 | 0.0993 ** | 0.1196 *** |

| (0.0541) | (0.0293) | (0.0333) | |

| cupwin | 0.0177 | 0.0356 (+) | 0.0578 ** |

| (0.0230) | (0.0207) | (0.0222) | |

| logbra_val | 0.1619 * | 0.2003 *** | 0.1091 (+) |

| (0.0754) | (0.0442) | (0.0669) | |

| tv_sch | 0.0107 | 0.0503 | 0.0187 |

| (0.0265) | (0.0416) | (0.0405) | |

| logrev_lag | 0.6182 *** | 0.3294 *** | 0.5095 ** |

| (0.1073) | (0.0604) | (0.1525) | |

| Constant | 0.9423 *** | 2.2138 *** | 1.6737 ** |

| (0.2462) | (0.2504) | (0.5209) | |

| Instrumented | - | - | logrev_lag |

| Instruments | - | - | tra_inv_lag, logmv_lag |

| R-squared | 0.9226 | 0.8371 | 0.9709 |

| Observations | 188 | 188 | 144 1 |

| No. of groups | 29 | 29 | 29 |

| DV | lppg | lppg | lppg | ucec | ucec | ucec |

|---|---|---|---|---|---|---|

| Model | OLS with cluster-robust SEs | FE model | FE IV model (2sls) | OLS with cluster-robust SEs | FE model | FE IV model (2sls) |

| tra_inv | 0.0017 ** | 0.0014 * | 0.0020 *** | 0.0335 * | 0.0264 (+) | 0.0295 * |

| (0.0005) | (0.0006) | (0.0005) | (0.0127) | (0.0142) | (0.0139) | |

| lppg_lag | 0.6935 *** | 0.2956 *** | 0.6546 *** | |||

| (0.0496) | (0.0634) | (0.0479) | ||||

| ucec_lag | 0.3589 *** | 0.2920 *** | 0.5054 *** | |||

| (0.0779) | (0.0776) | (0.1006) | ||||

| Constant | 0.5313 *** | 1.3191 *** | 0.5952 *** | 9.7698 *** | 12.2321 *** | 8.5046 *** |

| (0.0886) | (0.1261) | (0.1001) | (1.3407) | (2.0751) | (2.664) | |

| Instrumented | - | - | lppg_lag | - | - | ucec_lag |

| Instruments | - | - | winpct_lag, lppg_uclqual_lag | - | - | ucl_lag, uclgames_lag |

| R-squared | 0.4718 | 0.1279 | 0.5078 | 0.1485 | 0.1630 | 0.2083 |

| Observations | 286 | 286 | 286 | 191 | 191 | 191 |

| No. of groups | 30 | 30 | 30 | 29 | 29 | 29 |

| DV | tra_inv | tra_inv | tra_inv |

|---|---|---|---|

| Model | OLS with cluster-robust SEs | FE model | FE IV model (2sls) |

| inv_maj_for | 17.1300 ** | 25.0511 ** | 20.5512 * |

| (5.5069) | (8.9279) | (8.6083) | |

| inv_maj | −1.6025 | 17.2249 | 9.8423 |

| (5.0823) | (11.1083) | (10.9342) | |

| inv_min | 2.8834 | −1.6068 | −0.7108 |

| (7.4699) | (18.9601) | (17.4554) | |

| inv_tax | −0.8375 | −1.9195 ** | −1.5317 * |

| (0.5182) | (0.7319) | (0.6959) | |

| takeover | 14.1890 | 16.1443 (+) | 9.5330 |

| (12.2726) | (8.6981) | (8.3547) | |

| tra_inv_lag | 0.4089 *** | 0.1544 * | 0.3482 * |

| (0.0659) | (0.0636) | (0.1706) | |

| Constant | 43.6692 | 86.2301 * | 74.5595 * |

| (25.8184) | (36.8275) | (38.1173) | |

| Instrumented | - | - | tra_inv_lag |

| Instruments | - | - | newntlplayers_lag |

| R-squared | 0.2526 | 0.1221 | 0.3741 |

| Observations | 300 | 300 | 296 |

| No. of groups | 30 | 30 | 30 |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rohde, M.; Breuer, C. Europe’s Elite Football: Financial Growth, Sporting Success, Transfer Investment, and Private Majority Investors. Int. J. Financial Stud. 2016, 4, 12. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs4020012

Rohde M, Breuer C. Europe’s Elite Football: Financial Growth, Sporting Success, Transfer Investment, and Private Majority Investors. International Journal of Financial Studies. 2016; 4(2):12. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs4020012

Chicago/Turabian StyleRohde, Marc, and Christoph Breuer. 2016. "Europe’s Elite Football: Financial Growth, Sporting Success, Transfer Investment, and Private Majority Investors" International Journal of Financial Studies 4, no. 2: 12. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs4020012