The Effects of Extreme Weather Conditions on Hong Kong and Shenzhen Stock Market Returns

Abstract

:1. Introduction

2. Literature Review

3. Hong Kong and Shenzhen Stock Markets

3.1. Overviews of Hong Kong and Shenzhen Stock Markets

3.2. Investors in Hong Kong and Shenzhen Stock Markets

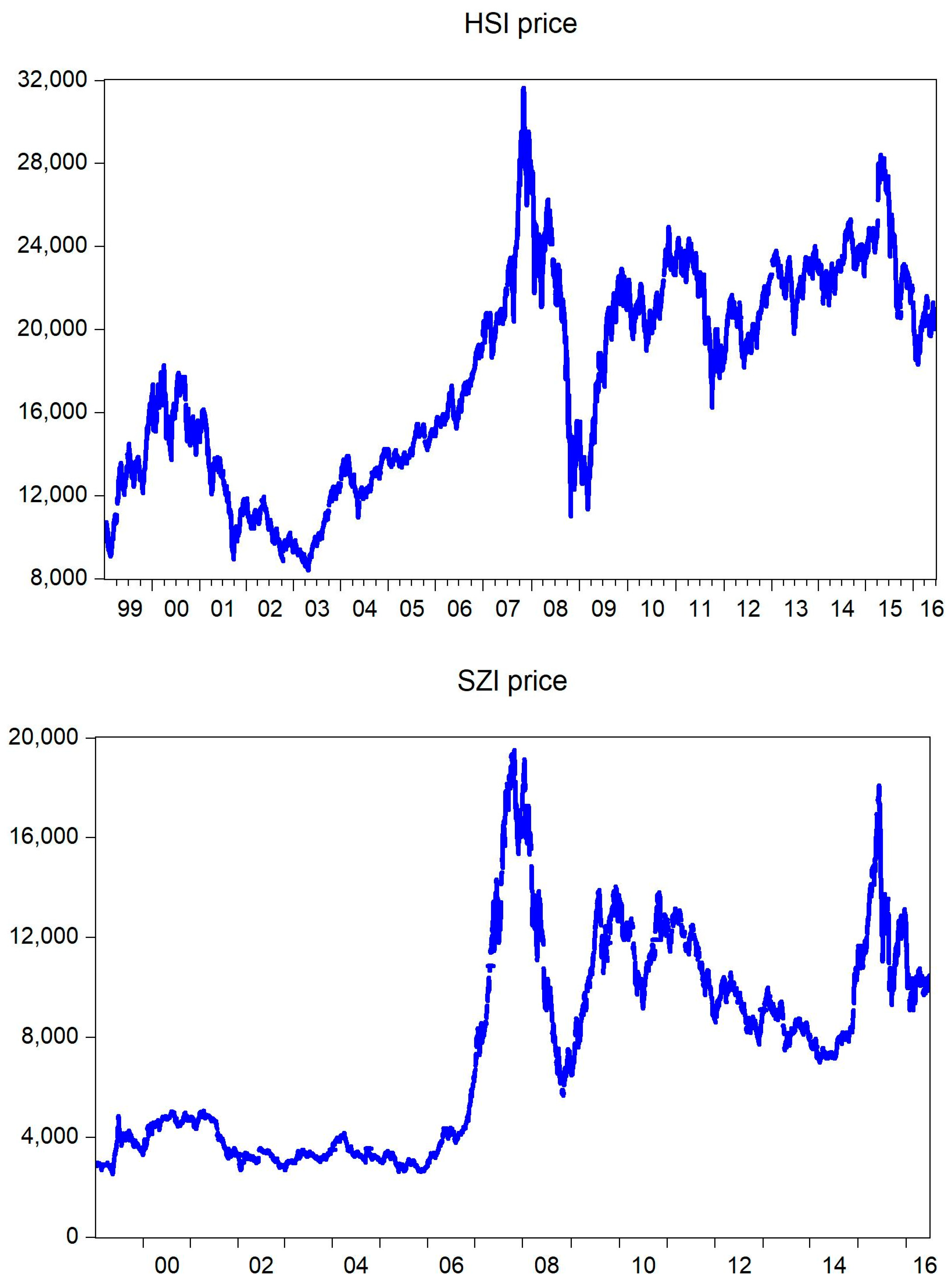

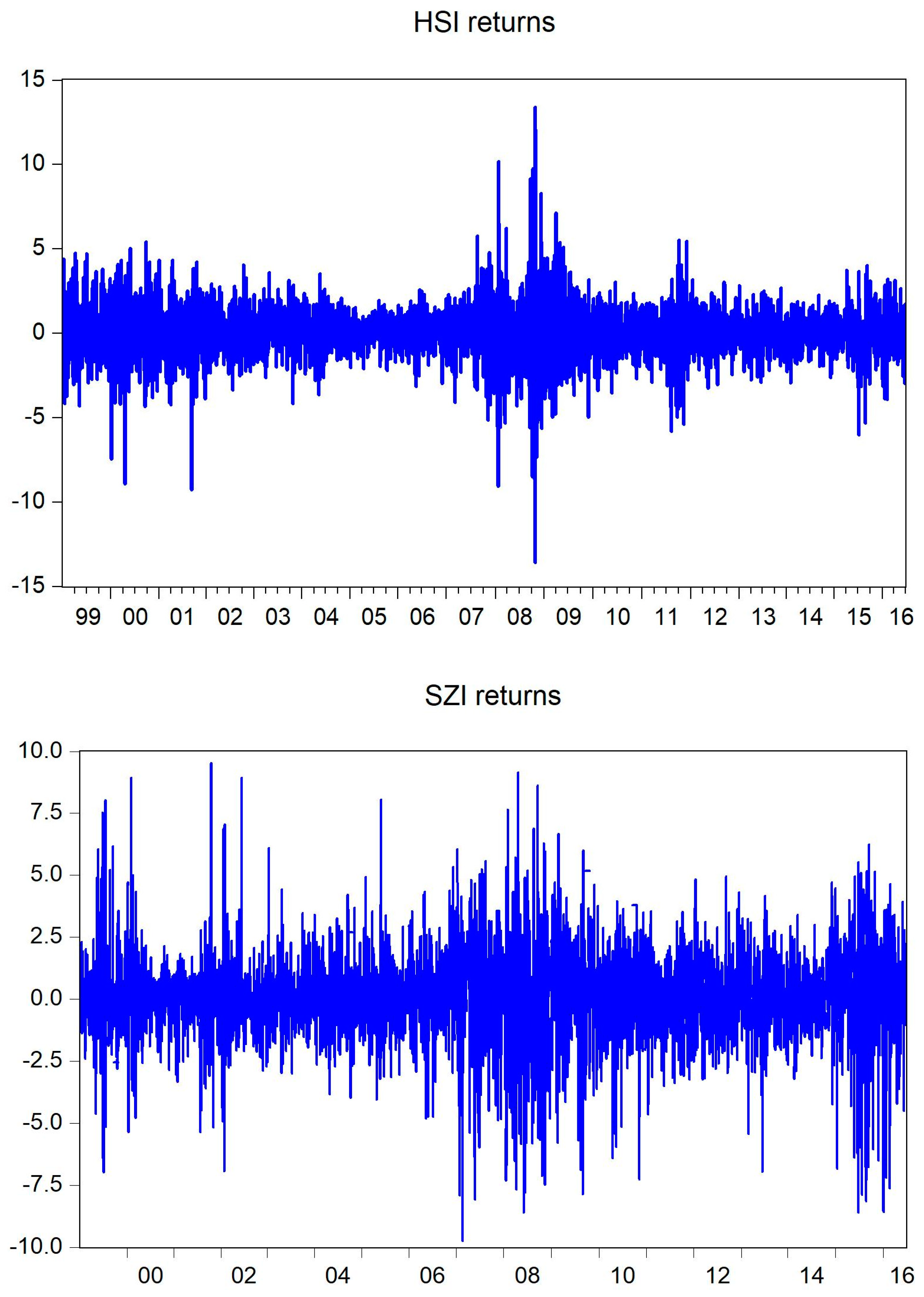

3.3. Descriptive Statistics of Stock Returns

4. Methodology

4.1. Weather Variables

4.2. Model Framework

5. Empirical Results

5.1. Effects of Weather on Hong Kong and Shenzhen Stock Returns

5.2. Market Openness and Effects of Weather on the Shenzhen Stock Returns

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Allen, Margaret A., and Gloria J. Fischer. 1978. Ambient temperature effects on paired associate learning. Ergonomics 21: 95–101. [Google Scholar] [CrossRef]

- Bagozzi, Richard P., Mahesh Gopinath, and Prashanth U. Nyer. 1999. The role of emotions in marketing. Journal of the Academy of Marketing Science 27: 184–206. [Google Scholar] [CrossRef]

- Bassi, Anna, Riccardo Colacito, and Paolo Fulghieri. 2013. O Sole Mio: An experimental analysis of weather and risk attitudes in financial decisions. Review of Financial Studies 26: 1824–52. [Google Scholar] [CrossRef]

- Bell, Paul A., and Robert A. Baron. 1976. Aggression and heat: The mediating role of negative affect. Journal of Applied Social Psychology 6: 18–30. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef] [Green Version]

- Cao, Guangxi, and Yan Han. 2015. Does the weather affect the Chinese stock markets? Evidence from the analysis of DCCA cross-correlation coefficient. International Journal of Modern Physics B 29: 1450236. [Google Scholar] [CrossRef]

- Cao, Melanie, and Jason Wei. 2005. Stock market returns: A note on temperature anomaly. Journal of Banking & Finance 29: 1559–73. [Google Scholar]

- Chang, Tsangyao, Chien-Chung Nieh, Ming Jing Yang, and Tse-Yu Yang. 2006. Are stock market returns related to the weather effects? Empirical evidence from Taiwan. Physica A 364: 343–54. [Google Scholar] [CrossRef]

- Cunningham, Michael R. 1979. Weather, mood, and helping behavior: Quasi-experiments with the sunshine Samaritan. Journal of Personality and Social Psychology 37: 1947–56. [Google Scholar] [CrossRef]

- Dong, Ming, and Andreanne Tremblay. 2018. Does the Weather Influence Global Stock Returns? Available online: https://ssrn.com/abstract=2444035 (accessed on 6 December 2019).

- Dowling, Michael, and Brian M. Lucey. 2005. Weather, biorhythms, beliefs and stock returns-some preliminary Irish evidence. International Review of Financial Analysis 14: 337–55. [Google Scholar] [CrossRef]

- Dowling, Michael, and Brian M. Lucey. 2008. Robust global mood influences in equity pricing. Journal of Multinational Financial Management 18: 145–64. [Google Scholar] [CrossRef]

- Engle, Robert F. 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50: 987–1007. [Google Scholar] [CrossRef]

- Garrett, Ian, Mark J. Kamstra, and Lisa A. Kramer. 2005. Winter blues and time variation in the price of risk. Journal of Empirical Finance 12: 291–316. [Google Scholar] [CrossRef] [Green Version]

- Glosten, Lawrence R., Ravi Jagannathan, and David E. Runkle. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Han, Ze-Xian. 2005. Study on weather effect of China’s stock index returns. Journal of Beijing University of Aeronautics and Astronautics (Social Science Edition) 18: 10–14. [Google Scholar]

- Han, Ze-Xian. 2006. A study on sunshine effect of Chinese stock index returns. Journal of Harbin Institute of Technology 38: 260–3. [Google Scholar]

- Han, Ze-Xian, and Yue-sen Wang. 2005. A study for SAD effect on Chinese market indices return. Journal of Huazhong University of Science and Technology (Social Science Edition) 19: 88–92. [Google Scholar]

- Hirshleifer, David, and Tyler Shumway. 2003. Good day sunshine: Stock returns and the weather. Journal of Finance 58: 1009–32. [Google Scholar] [CrossRef]

- Howarth, Edgar, and Michael S. Hoffman. 1984. A multidimensional approach to the relationship between mood and weather. British Journal of Psychology 75: 15–23. [Google Scholar] [CrossRef]

- Kamstra, Mark J., Lisa A. Kramer, and Maurice D. Levi. 2000. Losing sleep at the market: The daylight saving anomaly. American Economic Review 90: 1005–11. [Google Scholar] [CrossRef] [Green Version]

- Kamstra, Mark J., Lisa A. Kramer, and Maurice D. Levi. 2003. Winter blues: A SAD stock market cycle. American Economic Review 93: 324–43. [Google Scholar] [CrossRef] [Green Version]

- Kang, Sang Hoon, Zhuhua Jiang, Yeonjeong Lee, and Seong-Min Yoon. 2010. Weather effects on the returns and volatility of the Shanghai Stock Market. Physica A 389: 91–99. [Google Scholar] [CrossRef]

- Kaplanski, Guy, Haim Levy, Chris Veld, and Yulia Veld-Merkoulova. 2015. Do happy people make optimistic investors? Journal of Financial and Quantitative Analysis 50: 145–68. [Google Scholar] [CrossRef] [Green Version]

- Kaustia, Markku, and Elias Rantapuska. 2016. Does mood affect trading behavior? Journal of Financial Markets 29: 1–26. [Google Scholar] [CrossRef]

- Keef, Stephen P., and Melvin L. Roush. 2002. The weather and stock returns in New Zealand. Quarterly Journal of Business & Economics 41: 61–79. [Google Scholar]

- Keef, Stephen P., and Melvin L. Roush. 2005. Influence of weather on New Zealand financial securities. Accounting & Finance 45: 415–37. [Google Scholar]

- Keef, Stephen P., and Melvin L. Roush. 2007. Daily weather effects on the returns of Australian stock indices. Applied Financial Economics 17: 173–84. [Google Scholar] [CrossRef]

- Nelson, Daniel B. 1991. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 59: 347–70. [Google Scholar] [CrossRef]

- Nofsinger, John R. 2002. Do optimists make the best investors? Corporate Finance Review 6: 11–17. [Google Scholar]

- Novy-Marx, Robert. 2014. Predicting anomaly performance with politics, the weather, global warming, sunspots, and the stars. Journal of Financial Economics 112: 137–46. [Google Scholar] [CrossRef]

- Pizzutilo, Fabio, and Valeria Roncone. 2017. Red sky at night or in the morning, to the equity market neither a delight nor a warning: The weather effect re-examined using intraday stock data. European Journal of Finance 23: 1280–310. [Google Scholar] [CrossRef]

- Rind, Bruce. 1996. Effect of beliefs about weather conditions on tipping. Journal of Applied Social Psychology 26: 137–47. [Google Scholar] [CrossRef]

- Saunders, Edward M., Jr. 1993. Stock prices and the Wall Street weather. American Economic Review 83: 1337–45. [Google Scholar]

- Schmittmann, Jochen M., Jenny Pirschel, Steffen Meyer, and Andreas Hackethal. 2015. The impact of weather on German retail investors. Review of Finance 19: 1143–83. [Google Scholar] [CrossRef]

- Shenzhen Stock Exchange Fact Book. 2016. Available online: http://english.sse.com.cn/indices/publications/factbook/ (accessed on 6 December 2019).

- Shim, Hyein, Maria H. Kim, and Doojin Ryu. 2017. Effects of intraday weather changes on asset returns and volatilities. Zbornik Radova Ekonomskog Fakulteta u Rijeci (Proceedings of Rijeka School of Economics) 35: 301–30. [Google Scholar] [CrossRef]

- Wright, William F., and Gordon H. Bower. 1992. Mood effects on subjective probability assessment. Organizational Behavior and Human Decision Processes 52: 276–91. [Google Scholar] [CrossRef]

- Yi, C., and J. Wang. 2005. Weather, seasonal mood disorder and stock returns. Statistics and Decision-Making 6: 79–82. [Google Scholar]

- Yoon, Seong-Min, and Sang Hoon Kang. 2009. Weather effects on returns: Evidence from the Korean stock market. Physica A 388: 682–90. [Google Scholar] [CrossRef]

| 1 | For examples, Saunders (1993), Kamstra et al. (2000, 2003), Keef and Roush (2002, 2005, 2007), Hirshleifer and Shumway (2003), Cao and Wei (2005), Garrett et al. (2005), Dowling and Lucey (2005, 2008), Chang et al. (2006), Yoon and Kang (2009), Novy-Marx (2014), Kaplanski et al. (2015), Schmittmann et al. (2015), Kaustia and Rantapuska (2016), and Dong and Tremblay (2018). |

| 2 | Since July 2003, foreign investors have started to trade A-shares on a limited basis as a part of the Qualified Foreign Institutional Investor (QFII) plan. |

| 3 | The Growth Enterprise Market (GEM) caters to companies which cannot satisfy some profit track records necessary to be listed on the Main Board of the Stock Exchange. |

| 4 | All of the data were obtained from the RESSET Financial Research Database. |

| 5 | We also analyzed using cloud cover instead of sunshine duration and found similar results. As the two variables are very highly correlated each other, both variables should not be included in the regression equation due to multicollinearity problem. |

| 6 | |

| 7 | The 31-day MA and MSD method can be similarly formalized to the case of 31-day. See Yoon and Kang (2009) for the case of 21-day. |

| 8 | The GARCH (generalized autoregressive conditional heteroscedasticity) model proposed by Bollerslev (1986) is a generalization of ARCH model of Engle (1982) to consider a volatility clustering. The standard GARCH model has been extended to the GJR-GARCH model (Glosten et al. 1993) and EGARCH model (Nelson 1991) to capture an asymmetry of volatility and FIGARCH model to capture a long memory feature of volatility. In the empirical study, we apply the standard and popular GARCH model to focus on the conditional mean equation of Equation (4). |

{kind=link}

{kind=link}

| Hong Kong Exchange | Shenzhen Stock Exchange | |||

|---|---|---|---|---|

| Main Board | GEM | A-Share | B-Share | |

| No. of listed companies | 1713 | 260 | 1859 | 49 |

| No. of listed H-shares | 218 | 23 | n.a. | n.a. |

| No. of listed red-chips stocks | 147 | 6 | n.a. | n.a. |

| No. of listed securities | 8330 | 261 | n.a. | n.a. |

| Market capitalization (Billion) | HK$24,450 | HK$311 | RMB 22,222 | RMB 86 |

| Average P/E ratio (Times) | 10.53 | 71.31 | 41.62 | 11.15 |

| Turnover volume (average daily) (Million shares) | 129,733 | 1419 | 13,085 | 17 |

| Turnover value (average daily) (Million) | HK$54,775 | HK$582 | RMB 193,984 | RMB 131 |

| Year | Local Individual Investors | Local Institutional Investors | Foreign Institutional Investors | Foreign Individual Investors | The Exchange |

|---|---|---|---|---|---|

| 2006 | 28 | 25 | 39 | 4 | 4 |

| 2009 | 25 | 24 | 38 | 4 | 8 |

| 2012 | 17 | 21 | 42 | 4 | 15 |

| 2015 | 19 | 19 | 31 | 8 | 22 |

| Year | No. of PersonalInvestors | No. of Company Investors | Total |

|---|---|---|---|

| 2009 | 8542.60 | 28.15 | 8570.75 |

| 2012 | 10,537.82 | 35.48 | 10,573.30 |

| 2016 | 20,841.00 | 56.12 | 20,897.13 |

| Variables | Obs. | Mean | Max. | Min. | Std. Dev. | Skew. | Kurt. | Jarque-Bera |

|---|---|---|---|---|---|---|---|---|

| HSI | 4350 | 0.02 | 13.41 | −13.58 | 1.54 | −0.06 | 10.19 | 9378.8 *** |

| SZI | 4228 | 0.03 | 9.53 | −9.75 | 1.86 | −0.25 | 6.19 | 1841.2 *** |

| Variables | Obs. | Mean | Max. | Min. | Std. Dev. | Skew. | Kurt. | Jarque-Bera |

|---|---|---|---|---|---|---|---|---|

| Panel A: Hong Kong | ||||||||

| TEMP | 4350 | 23.5 | 31.8 | 7.4 | 5.12 | −0.53 | 2.27 | 304.3 *** |

| HUMI | 4350 | 78.2 | 99.0 | 27.0 | 10.29 | −0.99 | 4.89 | 1350.8 *** |

| SUNSH | 4350 | 5.0 | 12.4 | 0.0 | 3.89 | 0.04 | 1.52 | 398.7 *** |

| Panel B: Shenzhen | ||||||||

| TEMP | 4228 | 23.6 | 31.8 | 7.4 | 5.09 | −0.52 | 2.25 | 291.8 *** |

| HUMI | 4228 | 78.3 | 99.0 | 27.0 | 10.28 | −1.00 | 4.95 | 1380.1 *** |

| SUNSH | 4228 | 5.1 | 12.4 | 0.0 | 3.89 | 0.03 | 1.52 | 387.4 *** |

| Weather Dummies | Description |

|---|---|

| Extremely low temperature | |

| Extremely high temperature | |

| Extremely low humidity | |

| Extremely high humidity | |

| Extremely short sunshine duration | |

| Extremely long sunshine duration |

| HSI | SZI | |||||||

|---|---|---|---|---|---|---|---|---|

| Whole Period | Pre-QFII Period | Post-QFII Period | ||||||

| Coeff. | t-Value | Coeff. | t-Value | Coeff. | t-Value | Coeff. | t-Value | |

| 0.0499 | 1.83 | 0.1701 | 2.13 | 0.1963 | 1.94 | 0.1748 | 1.34 | |

| −0.0265 | −0.44 | 0.0158 | 0.20 | 0.2294 | 2.19 | −0.2384 | −1.84 | |

| 0.0156 | 0.38 | −0.0024 | −2.31 | −0.0029 | −2.14 | −0.0024 | −1.42 | |

| 0.0274 | 0.35 | 0.1904 | 1.88 | 0.3161 | 2.46 | 0.0479 | 0.30 | |

| −0.0610 | −0.86 | −0.0652 | −0.75 | 0.0940 | 0.82 | −0.1925 | −1.41 | |

| −0.0670 | −0.89 | −0.1067 | −1.12 | −0.1045 | −0.79 | −0.0907 | −0.62 | |

| 0.0670 | 0.81 | 0.0875 | 0.88 | 0.0073 | 0.06 | 0.2002 | 1.27 | |

| 0.1100 | 1.88 | 0.0952 | 0.90 | 0.0267 | 0.21 | 0.1617 | 0.84 | |

| −0.1802 | −1.98 | −0.0035 | −0.04 | 0.0236 | 0.17 | −0.0722 | −0.58 | |

| −0.0259 | −0.16 | 0.1025 | 0.56 | −0.1060 | −0.45 | 0.3027 | 1.03 | |

| −0.1837 | −1.28 | −0.2119 | −1.18 | −0.1502 | −0.68 | −0.3050 | −1.04 | |

| −0.1304 | −0.52 | −0.2328 | −1.44 | −0.3022 | −1.60 | −0.1277 | −0.45 | |

| 0.2064 | 1.39 | −0.3651 | −1.37 | −0.5177 | −1.42 | 0.0659 | 0.14 | |

| 0.1588 | 1.16 | 0.2601 | 1.39 | 0.2461 | 1.06 | 0.1750 | 0.57 | |

| −0.2212 | −1.27 | 0.3731 | 1.68 | 0.3600 | 1.17 | 0.2812 | 0.82 | |

| −0.1362 | −1.00 | −0.3089 | −0.87 | −0.3930 | −0.78 | −0.3076 | −0.61 | |

| 0.0566 | 0.21 | −0.1740 | −0.97 | −0.5476 | −2.30 | 0.2854 | 1.04 | |

| −0.0589 | −0.50 | −0.3764 | −1.31 | −0.3622 | −1.19 | −0.0322 | −0.04 | |

| 0.3764 | 1.17 | −0.0593 | −0.40 | −0.1708 | −0.78 | 0.0758 | 0.34 | |

| 0.4496 | 0.94 | 0.1339 | 0.84 | 0.1222 | 0.59 | 0.1656 | 0.63 | |

| 0.1230 | 0.92 | −0.5671 | −1.26 | −0.1634 | −0.27 | −1.1766 | −1.41 | |

| 0.0152 | 5.07 | 0.0397 | 6.23 | 0.0722 | 4.95 | 0.0266 | 3.47 | |

| 0.0627 | 12.68 | 0.0779 | 14.53 | 0.1159 | 10.88 | 0.0504 | 9.54 | |

| 0.9307 | 164.29 | 0.9125 | 173.8 | 0.8574 | 69.13 | 0.9438 | 173.9 | |

| −7285.2039 | −8123.7431 | −3275.7723 | −4815.9844 | |||||

| 14,618.4077 | 16,295.4862 | 6599.5446 | 9679.9687 | |||||

| HSI | SZI | |||||||

|---|---|---|---|---|---|---|---|---|

| Whole Period | Pre−QFII Period | Post−QFII Period | ||||||

| Coeff. | t-Value | Coeff. | t-Value | Coeff. | t-Value | Coeff. | t-Value | |

| 0.1518 | 2.28 | 0.1114 | 1.21 | 0.0914 | 0.77 | 0.1571 | 1.04 | |

| −0.0421 | −0.69 | 0.0086 | 0.11 | 0.2121 | 2.00 | −0.2426 | −1.86 | |

| −0.0016 | −1.75 | −0.0014 | −1.16 | −0.0012 | −0.79 | −0.0017 | −0.88 | |

| 0.0711 | 0.84 | 0.0497 | 0.51 | 0.3286 | 2.36 | −0.2075 | −1.33 | |

| −0.0606 | −0.87 | −0.1004 | −1.19 | −0.1467 | −1.28 | −0.0310 | −0.24 | |

| −0.0273 | −0.34 | 0.0571 | 0.56 | 0.1710 | 1.35 | −0.0760 | −0.46 | |

| 0.0748 | 0.88 | 0.0531 | 0.46 | −0.1020 | −0.75 | 0.2205 | 1.11 | |

| −0.0725 | −0.97 | −0.0045 | −0.05 | −0.0406 | −0.33 | −0.0366 | −0.25 | |

| 0.0460 | 0.74 | 0.0073 | 0.09 | −0.0630 | −0.52 | 0.0373 | 0.30 | |

| −0.0089 | −0.06 | 0.0628 | 0.33 | −0.5710 | −2.35 | 0.8206 | 2.66 | |

| −0.1001 | −0.74 | −0.2393 | −1.37 | −0.1956 | −0.91 | −0.3042 | −1.06 | |

| 0.0551 | 0.43 | 0.0543 | 0.33 | −0.1816 | −0.86 | 0.2774 | 1.04 | |

| −0.0351 | −0.16 | −0.1315 | −0.61 | 0.0677 | 0.22 | −0.2426 | −0.72 | |

| −0.0824 | −0.59 | −0.2522 | −1.55 | −0.3138 | −1.54 | −0.3357 | −1.24 | |

| 0.0676 | 0.36 | 0.2264 | 0.79 | 0.2749 | 0.81 | 0.3765 | 0.60 | |

| −0.0159 | −0.06 | −0.1791 | −0.59 | 0.0209 | 0.05 | −0.3067 | −0.60 | |

| 0.1096 | 0.85 | 0.3403 | 2.32 | 0.5366 | 2.88 | 0.1659 | 0.66 | |

| 0.0497 | 0.21 | −0.3724 | −0.93 | 0.1867 | 0.32 | −0.5358 | −0.88 | |

| −0.0976 | −0.84 | −0.1349 | −1.00 | −0.1336 | −0.76 | −0.0873 | −0.39 | |

| 0.0623 | 0.51 | 0.0673 | 0.43 | 0.1027 | 0.54 | 0.0970 | 0.38 | |

| −0.2786 | −0.39 | 0.0119 | 0.01 | 0.3870 | 0.02 | −0.3814 | −0.30 | |

| 0.0152 | 4.95 | 0.0407 | 6.43 | 0.0803 | 5.12 | 0.0259 | 3.53 | |

| 0.0616 | 12.74 | 0.0763 | 14.54 | 0.1140 | 10.47 | 0.0487 | 9.73 | |

| 0.9318 | 166.6 | 0.9136 | 177.1 | 0.8552 | 64.67 | 0.9456 | 186.4 | |

| −7287.6306 | −8129.1059 | −3282.2657 | −4813.8673 | |||||

| 14623.2612 | 16306.2117 | 6612.5313 | 9675.7345 | |||||

| HSI | SZI | |||

|---|---|---|---|---|

| Whole | Pre-QFII Period | Post-QFII Period | ||

| 11-day MA-MSD | 2 | 2 | 2 | 0 |

| 31-day MA-MSD | 0 | 1 | 3 | 1 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jiang, Z.; Kang, S.H.; Cheong, C.; Yoon, S.-M. The Effects of Extreme Weather Conditions on Hong Kong and Shenzhen Stock Market Returns. Int. J. Financial Stud. 2019, 7, 70. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs7040070

Jiang Z, Kang SH, Cheong C, Yoon S-M. The Effects of Extreme Weather Conditions on Hong Kong and Shenzhen Stock Market Returns. International Journal of Financial Studies. 2019; 7(4):70. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs7040070

Chicago/Turabian StyleJiang, Zhuhua, Sang Hoon Kang, Chongcheul Cheong, and Seong-Min Yoon. 2019. "The Effects of Extreme Weather Conditions on Hong Kong and Shenzhen Stock Market Returns" International Journal of Financial Studies 7, no. 4: 70. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs7040070