Existence of the Audit Expectation Gap and Its Impact on Stakeholders’ Confidence: The Moderating Role of the Financial Reporting Council

Abstract

:1. Introduction

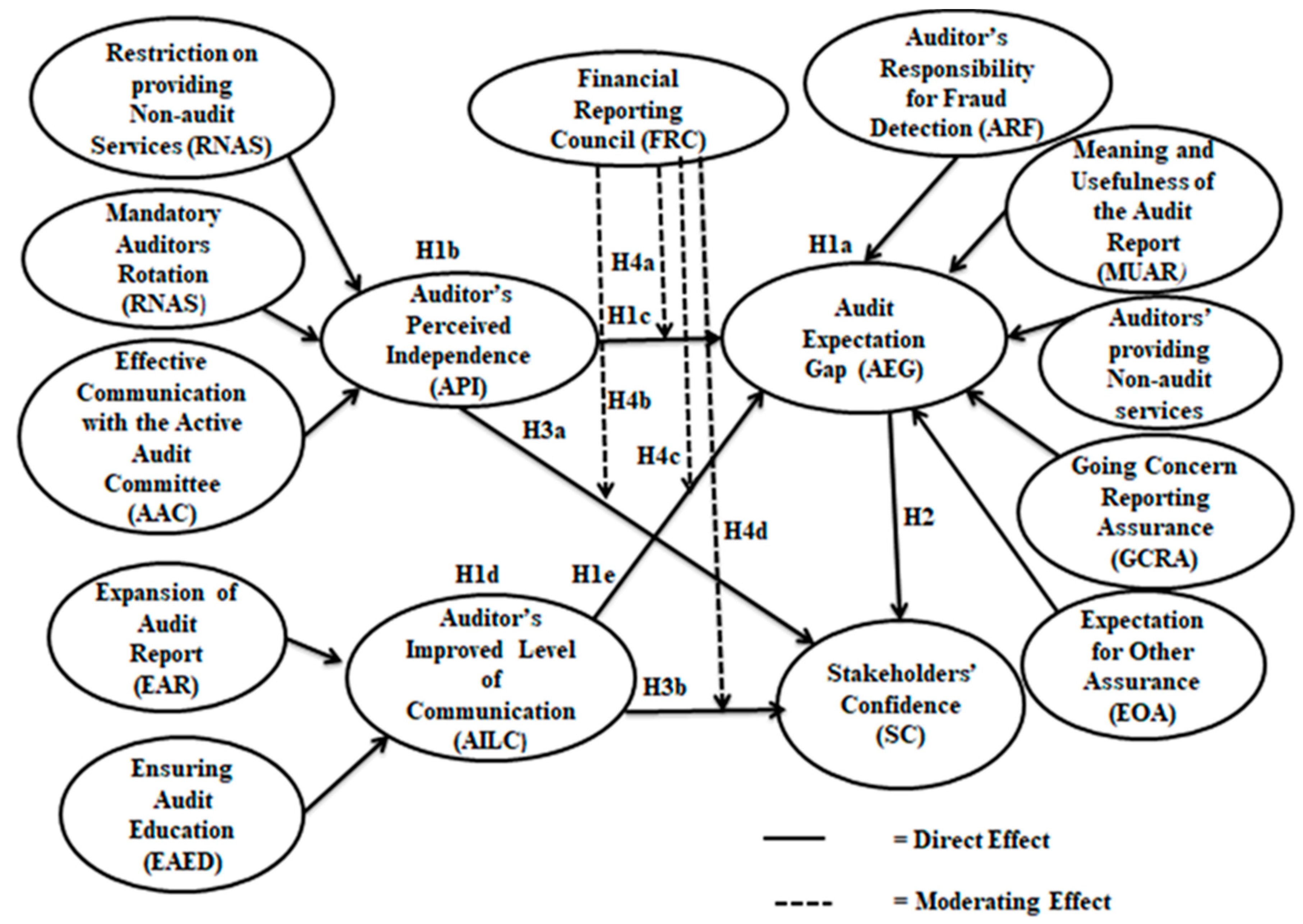

2. Review of Related Literature and Hypothesis Development

2.1. Audit Expectation Gap (AEG)

- Unreasonable gap: The gap between what society believes in their mind what auditors can achieve and what practices they can achieve. It can also be referred to as the failure of the public to understand the aim and scope of the audit and develop unreasonable expectations.

- Sensible gap:

- (i)

- Sensible performance gap: What society can sensibly expect from the auditors about the actual level of performance of auditors and the standard of performance described by the current regulation.

- (ii)

- Sensible standard gap: What society can sensibly expect from the auditors if there is an amendment in the current legislation based on equitable demand from the participants and if it is cost-effectiveness of doing so.

2.2. The Auditor’s Perceived Independence (API)

2.3. The Auditor’s Improved Level of Communication (AILC)

2.4. Stakeholder Confidence

2.5. The Role of Financial Reporting Council (FRC)

3. Research Method

3.1. Data

3.2. Methodology

4. Results

4.1. Assessing the Measurement Model

4.2. Assessing the Structural Model

4.3. Hypothesis Testing of Direct Relationship

4.4. Hypothesis Testing of Moderating Relationship

5. Discussion

6. Conclusions

Data Accessibility Statement

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Constructs | Items | Statement | Source |

|---|---|---|---|

| Auditors’ responsibility for fraud detection (ARF) | ARF1 | The auditor is primarily responsible for the prevention and detection of fraud and error of the entity. | (IAASB 2009a; Pourheydari and Abousaiedi 2011; Dixon et al. 2006; Ruhnke and Schmidt 2014; Siddiqui et al. 2009; Best et al. 2001; Lin and Chen 2004; Stirbu 2010; McEnroe and Martens 2001; Porter 1993; Porter and Gowthorpe 2004; Hogan et al. 2008; Salehi and Azary 2009) |

| ARF2 | Auditor can detect all misstatements due to fraud and error. | ||

| ARF3 | Auditor should be held responsible if the entity goes bankrupt due to fraud. | ||

| ARF4 | Auditor can conclude that there are no illegal operations conducted by the audited company. | ||

| Meaning & usefulness of audit report (MUAR) | MUAR1 | The standard unqualified report is a clean report and gives users significantly high level of confidence in the company’s management, investment soundness, and accomplishment of strategic goal. | (Asare and Wright 2012; Mock et al. 2012; Coram et al. 2011; Gray et al. 2011; Dixon et al. 2006) |

| MUAR2 | A qualified opinion is used when the auditor’s scope has been restricted by clients or the auditor is not independent. | ||

| MUAR3 | Investors take investment decision; lenders take lending decision by observing audit report. | ||

| MUAR4 | The audit report is useful for assessing whether the company is well managed. | ||

| MUAR5 | Audited financial statements are useful for monitoring the performance of the entity | ||

| Provision of Non-audit services (NAS) | NAS1 | auditors non-audit services do not increases economic dependency on client and create threats to independence | (Kinney et al. 2004; Salehi and Rostami 2009; Wallman 1996; Wolf et al. 1999; Zaman et al. 2011 ) |

| NAS2 | If audit firm provides non audit services to the clients, it doesn’t hampers the auditor’s independence. | ||

| NAS3 | If auditors apply safeguards to the threats arise as a result of providing non audit services, Independence will not be hampered | ||

| Expectation for going concern reporting assessment (GCRA) | GCR1 | Auditor make an assessment of an entity’s ability to continue as a going concern | (IAASB 2009d, 2015a; Carson et al. 2012; Gray et al. 2011; Lee et al. 2009) |

| GCR2 | The auditors can conclude that the company will continue as a going concern in the near future. | ||

| GCR3 | Auditor can forecast whether the entity has sufficient liquidity to operate through the next year and can provide early warning of corporate failure. | ||

| GCR4 | Audit report should include the auditor’s assessment of entity’s ability to continue as going concern | ||

| Expectation for other assurance services (EOA) | EOA1 | Investors find management commentary, directors report (MD&A), management performance analysis graphs and charts, CSR and environmental report useful and they think that information are audited. | (Bryan and Smith 1997; Mock et al. 2012; Mock et al. 2007; Simnett et al. 2009; Brown-Liburd and Zamora 2014; Cohen et al. 2011) |

| EOA2 | CSR report become more credible when it is assured by auditor | ||

| EOA3 | Entity require assurance on their sustainability information | ||

| Restriction on providing non-audit services (RNAS) | RNAS1 | Audit firm should not provide other services except audit like review, consultancy and other attestation services to retain independence. | (Salehi and Rostami 2009; Beattie et al. 1999; Olagunju 2011; Wolf et al. 1999; DeFond et al. 2002; Ashbaugh et al. 2003; Lim and Tan 2008; Umar and Anandarajan 2004; Haddrill 2018) |

| RNAS2 | Auditors can provide non audit services by taking appropriate safeguard so that independence is not hampered. | ||

| RNAS3 | Prohibition on providing non audit services by the statutory auditors is detrimental for management and it will increase the cost. | ||

| RNAS4 | Restriction on providing non audit services by the audit firm enhances audit independence, therefore increase public trust and confidence. | ||

| Mandatory auditors’ rotation (MAR) | MAR1 | Mandatory Auditors Rotation enhances audit independence/quality | (Bazerman et al. 1997; Yip and Pang 2017; PCAOB 2011a) |

| MAR2 | Earnings quality of the entity deteriorates with extended auditors’ tenure | ||

| MAR3 | Mandatory Auditors Rotation is disruptive for management as the new relationship is unpredictable | ||

| MAR4 | Mandatory Auditors Rotation increase audit startup cost and increase the risk of audit failure | ||

| Communication with the active audit committee (AAC) | AAC1 | Auditors are required to maintain ongoing communication with the specialized committee of the governing body such as Audit committee. | (IAASB 2009b, 2009c; Jensen and Meckling 1976; Salleh and Stewart 2012; Krishnamoorthy et al. 2002) |

| AAC2 | Presence of an effective audit committee can ensure auditors independence and act as a guardian of public interest. | ||

| AAC3 | Audit committee should be independent of management and effectively evaluate the financial reporting and internal control procedure. | ||

| Expansion of audit report (EAR) | EAR1 | Audit report should clarify the auditor’s responsibility and management responsibility in separate section and it increases the communicative value of audit report. | (IAASB 2011, 2012, 2015a; Asare and Wright 2012; European commission 2010; T. J. Mock et al. 2012) |

| EAR2 | If audit report includes the discussion about the key risk factors that materially affects the entity and how auditors responded them, it will add more values to the stakeholders. | ||

| EAR3 | Audit report should include the discussion about material uncertainty with respect to entity’s ability to continue as a going concern. | ||

| Ensure audit education (EAED) | AEd1 | Training program for shareholders specially discuss about role of audit in the annual general meeting enhances better understanding about audit | (Siddiqui et al. 2009; Epstein and Geiger 1994; Monroe and Woodliff 1994b) |

| AEd2 | Public accounting firm should participate in local community activities of college and universities in order to create a good impression for the profession | ||

| AEd3 | Incorporating more audit courses in the undergraduate level for the accounting students in the university and incorporating case based class room study about accounting scandal aware them about the role of auditors | ||

| Stakeholders’ confidence (SC) | SC1 | Maintenance of auditor’s perceived independence ensure stakeholders confidence. | (FRC 2016; Okafor and Otalor 2013; Sikka et al. 1989; European Comission 2010; IAASB 2015a PCAOB 2011b; Baotham and Ussahawanitchakit 2009; Xie 2016) |

| SC2 | Greater competition in audit market ensures better independence and greater confidence on audit | ||

| SC3 | Meeting society’s expectation ensure stakeholders confidence. | ||

| SC4 | communication about the purpose and scope of audit increases the users understanding about audit and they feel confident about the audit services | ||

| Financial reporting council (FRC) | FRC1 | If an independent body e.g., Financial Reporting Council provides license to auditors and approval of the audit firm, it enhances audit independence and ensure public trust | (FRC 2016; Siddiqui 2018; Shil 2015; Ahmed 2017) |

| FRC2 | If an independent body e.g., Financial Reporting Council monitors the work and conduct of all auditors and ensure the compliance with standard and ethical requirements, un biasedness and objectivity will be ensured | ||

| FRC3 | Financial Reporting Council will invite political favorites, culture of biasness and ultimately hampers auditors independence |

| Respondents Group | Auditors-Investors | Auditors-Credit Analysts | Auditors-Regulatory Agencies | Auditors-Managers | ||||

|---|---|---|---|---|---|---|---|---|

| Statements of Differences | Z Values | p Values | Z Values | p Values | Z Values | p Values | Z Values | p Values |

| (i) Auditor’s responsibility for fraud detection: | ||||||||

| 1. The auditor is primarily responsible for the prevention and detection of fraud and error of the entity. | −7 | 0.00 *** | −8 | 0.00 *** | −2.99 | 0.00 *** | −0.9 | 0.37 |

| 2. Auditor can detect all misstatements due to fraud and error. | −7.1 | 0.00 *** | −7.8 | 0.00 *** | −6.6 | 0.00 *** | −8.7 | 0.00 *** |

| 3. Auditor should be held responsible if the entity goes bankrupt due to fraud. | −7.8 | 0.00 *** | −8.6 | 0.00 *** | −7.19 | 0.00 *** | −3.6 | 0.00 *** |

| 4. Auditor can conclude that there are no illegal operations conducted by the audited company. | −7.7 | 0.00 *** | −8.7 | 0.00 *** | −7.23 | 0.00 *** | −1.7 | 0.09 * |

| (ii) Meaning & usefulness of audit report | ||||||||

| 1. The unmodified audit report is a clean report and gives users significantly high level of confidence in the company’s management, investment soundness, and accomplishment of strategic goal. | −5 | 0.00 *** | −8.4 | 0.00 *** | −6.92 | 0.00 *** | −0 | 0.98 |

| 2. A modified opinion is used when the auditor’s scope has been restricted by clients or the auditor is not independent. | −7.6 | 0.00 *** | −8.5 | 0.00 *** | −6.81 | 0.00 *** | −8.8 | 0.00 *** |

| 3. Reasonable assurance means guarantee for the accuracy of the financial statements audited. | −7.5 | 0.00 *** | −8.4 | 0.00 *** | −6.91 | 0.00 *** | −9.3 | 0.00 *** |

| 4. The audit report is useful for assessing whether the company is well managed. | −2.4 | 0.02 ** | −3 | 0.00 *** | −0.95 | 0.34 | −0.7 | 0.46 |

| 5. Audited financial statements are useful for monitoring the performance of the entity | −8 | 0.00 *** | −8.6 | 0.00 *** | −7.17 | 0.00 *** | −9.5 | 0.00 *** |

| (iii) Provision of non-audit services: | ||||||||

| 24. Auditors non-audit services increases economic dependency on client and create threats to independence. | −7.3 | 0.00 *** | −8.7 | 0.00 *** | −7.16 | 0.00 *** | −9.7 | 0.00 *** |

| 25. If audit firm provides non audit services to the clients, it hampers the auditor’s independence. | −4.2 | 0.00 *** | −5.1 | 0.00 *** | −4.47 | 0.00 *** | −4.7 | 0.00 *** |

| 26. If auditors apply safeguards to the threats arise as a result of providing non audit services, Independence will not be hampered | −6.6 | 0 *** | −4.7 | 0.00*** | −0.74 | 0.04** | −2 | 0.03 |

| (iv) Auditor’s responsibility for going concern reporting: | ||||||||

| 24. Auditors makes an assessment of an entity’s ability to continue as a going concern. | −6.6 | 0.00 *** | −0.3 | 0.78 | −0.71 | 0.48 | −0.1 | 0.91 |

| 25. The auditors can conclude that the company will continue as a going concern in the near future. | −7.6 | 0.00 *** | −8.6 | 0.00 *** | −7.18 | 0.00 *** | −9.5 | 0.00 *** |

| 26. Auditor can forecast whether the entity has sufficient liquidity to operate through the next year. | −7.5 | 0.00 *** | −8.4 | 0.00 *** | −6.99 | 0.00 *** | −0.6 | 0.55 |

| 27. Auditor can provide early warning of corporate failure. | −5 | 0.00 *** | −7.9 | 0.00 *** | −0.03 | 0.98 | −0.4 | 0.66 |

| (v) Expectation for other assurance services: | ||||||||

| 28. Information contained in the management commentary, directors’ report, management discussion & analysis (MD&A), management performance analysis graphs and charts, CSR and environmental report are useful and that information are audited. | −2.5 | 0.01 ** | −4.1 | 0.00 *** | −2.89 | 0.04 ** | −2.1 | 0.05 ** |

| 29. CSR report become more credible when it is assured by auditor | −1.5 | 0.04 ** | −0.2 | 0.08 * | −3.39 | 0.08 * | −2.3 | 0.04 ** |

| 30.Entity require assurance on their sustainability information | −2 | 0.03 ** | −6.1 | 0.00 *** | −2.38 | 0.07 * | −2.4 | 0.07 * |

References

- Ahmed, Mustaq. 2017. Role and Responsibilities of Professional Accountants. Speech in Seminar on Financial Reporting Act, ICMAB News. The Cost and Management 45: 54. [Google Scholar]

- American Institute of Certified Public Accountants (AICPA). 1978. Commission on Auditors, Responsibilities Report: Conclusions and Recommendations. New York: AICPA. [Google Scholar]

- Akther, Taslima, and Fengju Xu. 2018. Stakeholders’ Trust Towards the Role of Auditors: A Synopsis of Audit Expectation Gap. In 15th International Conference on Innovation & Management. Wuhan: Wuhan University of Technology Press. [Google Scholar]

- Andreev, Pavel, Tsipi Heart, Hanan Maoz, and Nava Pliskin. 2009. Validating Formative Partial Least Squares (PLS) Models: Methodological Review and Empirical Illustration. In Proceedings of ICIS 2009. Phoenix: AISeL. [Google Scholar]

- Armstrong, Mary Beth, and Janice I. Vincent. 1988. Public accounting: A profession at a crossroads. Accounting Horizons 2: 94. [Google Scholar]

- Asare, Stephen Kwaku, and Arnold M. Wright. 2012. Investors, Auditors, and Lenders Understanding of the Message Conveyed by the Standard Audit Report on the Financial Statements. Accounting Horizons 26: 193–217. [Google Scholar] [CrossRef] [Green Version]

- Ashbaugh, Hollis, Ryan LaFond, and Brian W. Mayhew. 2003. Do Nonaudit Services Compromise Auditor Independence? Further Evidence. The Accounting Review 78: 611–39. [Google Scholar] [CrossRef]

- Baker, C. Richard, Jean Bédard, and Christian Prat dit Hauret. 2014. The Regulation of Statutory Auditing: An Institutional Theory Approach. Managerial Auditing Journal 29: 371–94. [Google Scholar] [CrossRef]

- Baotham, Sumintorn, and Phapruke Ussahawanitchakit. 2009. Audit Independence, Quality, and Credibility: Effects on Reputation and Sustainable Success of CPAs in Thailand. International Journal of Business Research 9: 1–25. [Google Scholar]

- Barker, Patricia. 2002. Audit Committees: Solution to a Crisis of Trust? Accountancy Ireland 34: 6. [Google Scholar]

- Bazerman, Max H., and Don Moore. 2011. Is it Time for Auditor Independence Yet? Accounting, Organizations and Society 36: 310–2. [Google Scholar] [CrossRef]

- Bazerman, Max H., Kimberly P. Morgan, and George F. Loewenstein. 1997. The Impossibility of Auditor Independence. Sloan Management Review 38: 89–94. [Google Scholar]

- Beattie, Vivien, Richard Brandt, and Stella Fearnley. 1999. Perceptions of Auditor Independence: U.K. Evidence. Journal of International Accounting, Auditing, and Taxation 8: 67–107. [Google Scholar] [CrossRef] [Green Version]

- Becker, Jan-Michael, Kristina Klein, and Martin Wetzels. 2012. Hierarchical Latent Variable Models in PLS-SEM: Guidelines for Using Reflective-Formative Type Models. Long Range Planning 45: 359–94. [Google Scholar] [CrossRef]

- Belal, Ataur, Crawford Spence, Chris Carter, and Jingqi Zhu. 2017. The Big 4 in Bangladesh: Caught between the Global and the Local. Accounting, Auditing & Accountability Journal 30: 145–63. [Google Scholar]

- Best, Peter, Sherrena Buckby, and Clarice Tan. 2001. Evidence of the Audit Expectation Gap in Singapore. Managerial Auditing Journal 16: 134–44. [Google Scholar] [CrossRef] [Green Version]

- Broderick, Anne. 1999. Role Theory and the Management of Service Encounters. The Service Industries Journal 19: 117–31. [Google Scholar] [CrossRef]

- Brown-Liburd, Helen, and Valentina L. Zamora. 2014. The role of corporate social responsibility (CSR) assurance in investors’ judgments when managerial pay is explicitly tied to CSR performance. Auditing: A Journal of Practice & Theory 34: 75–96. [Google Scholar]

- Bryan, Barry J., and L. Murphy Smith. 1997. Faculty perspectives of auditing topics. Issues in Accounting Education 12: 1. [Google Scholar]

- Burns, Alvin C., and Ronald F. Bush. 2003. Marketing Research: Online Research Applications. Upper Saddle River: Prentice Hall. [Google Scholar]

- Carson, Elizabeth, Neil L. Fargher, Marshall A. Geiger, Clive S. Lennox, Kannan Raghunandan, and Marleen Willekens. 2012. Audit Reporting for Going-Concern Uncertainty: A Research Synthesis. AUDITING: A Journal of Practice & Theory 32: 353–84. [Google Scholar]

- Chowdhury, Riazur R., John Innes, and Reza Kouhy. 2005. The public sector audit expectations gap in Bangladesh. Managerial Auditing Journal 20: 893–908. [Google Scholar] [CrossRef]

- Cohen, Jacob, and Patricia Cohen. 1983. Applied Multiple Regression/Correlation Analysis for Behavioral Sciences. Hillsdale: Lawrence Erlbaum Associates. [Google Scholar]

- Cohen, Jeffrey R., Lisa Milici Gaynor, Ganesh Krishnamoorthy, and Arnold M. Wright. 2011. The impact on auditor judgments of CEO influence on audit committee independence. Auditing: A Journal of Practice & Theory 30: 129–47. [Google Scholar]

- Coram, Paul J., Theodore J. Mock, Jerry L. Turner, and Glen L. Gray. 2011. The Communicative Value of the Auditor’s Report. Australian Accounting Review 21: 235–52. [Google Scholar] [CrossRef]

- DeFond, Mark L., Kannan Raghunandan, and Subramanyam. 2002. Do Non–Audit Service Fees Impair Auditor Independence? Evidence from Going Concern Audit Opinions. Journal of Accounting Research 40: 1247–74. [Google Scholar] [CrossRef]

- Diamantopoulos, Adamantios, and Judy A. Siguaw. 2000. Introducing LISREL. Thousand Oaks: Sage. [Google Scholar]

- Diamantopoulos, Adamantios, and Judy A. Siguaw. 2006. Formative Versus Reflective Indicators in Organizational Measure Development: A Comparison and Empirical Illustration. British Journal of Management 17: 263–82. [Google Scholar] [CrossRef]

- Diamantopoulos, Adamantios, and Heidi M. Winklhofer. 2001. Index Construction with Formative Indicators: An Alternative to Scale Development. Journal of Marketing Research 38: 269–77. [Google Scholar] [CrossRef]

- Dijkstra, Theo K. 2010. Latent Variables and Indices: Herman Wold’s Basic Design and Partial Least Squares. In Handbook of Partial Least Squares: Concepts, Methods, and Applications (Springer Handbooks of Computational Statistics Series, Vol. II). Heidelberg and New York: Springer, pp. 23–46. [Google Scholar]

- Dijkstra, Theo K., and Jörg Henseler. 2015. Consistent Partial Least Squares Path Modeling. MIS Quarterly 39: 297–316. [Google Scholar] [CrossRef]

- Dijkstra, Theo Karin, and Karin Schermelleh-Engel. 2014. Consistent Partial Least Squares for Nonlinear Structural Equation Models. Psychometrika 79: 585–604. [Google Scholar] [CrossRef] [PubMed]

- Dixon, R., A.D. Woodhead, and M. Sohliman. 2006. An investigation of the expectation gap in Egypt. Managerial Auditing Journal 21: 293–302. [Google Scholar] [CrossRef]

- Edwards, Jeffrey R., and Richard P. Bagozzi. 2000. On the Nature and Direction of Relationships between Constructs and Measures. Psychological Methods 5: 155–74. [Google Scholar] [CrossRef]

- Elliott, W. Brooke, Frank D. Hodge, Jane Jollineau Kennedy, and Maarten Pronk. 2007. Are M.B.A. Students a Good Proxy for Nonprofessional Investors? The Accounting Review 82: 139–68. [Google Scholar] [CrossRef] [Green Version]

- Epstein, Marc J., and Marshall A. Geiger. 1994. Investor Views of Audit Assurance: Recent Evidence of the Expectation Gap. Journal of Accountancy 177: 60. [Google Scholar]

- European Commission. 2010. Green Paper Audit Policy: Lessons from the Crisis. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52010DC0561 (accessed on 22 December 2018).

- Fadzly, Mohamed N., and Zauwiyah Ahmad. 2004. Audit Expectation Gap: The Case of Malaysia. Managerial Auditing Journal 19: 897–915. [Google Scholar] [CrossRef]

- Financial Accounting Standard Board (FASB). 2008. Proposed Statement of Financial Accounting Standards, Going Concern. File Reference No. 1650-100. Norwalk: FASB. [Google Scholar]

- Financial Accounting Standard Board (FASB). 2011. Disclosures about Risks and Uncertainties and the Liquidation Basis of Accounting. Norwalk: FASB. [Google Scholar]

- Frank, Kimberly E., James K. Smith, and D. Jordan Lowe. 2001. The Expectation Gap: Perceptual Differences between Auditors, Jurors and Students. Managerial Auditing Journal 16: 145–50. [Google Scholar] [CrossRef]

- Financial Reporting Council (FRC). 2016. Enhancing Confidence in the Value of Audit, A Research Report Commissioned by the Financial Reporting Council. Available online: https: //www.frc.org.uk/getattachment/382e1ad9–5b7a–4297–849b1d415420fdc4/Impact–Assessment–Audit–Regulation–and–Directive–September–2015.pdf (accessed on 18 January 2018).

- Gay, Grant, Peter Schelluch, and Ian Reid. 1997. Users Perceptions of the Auditing Responsibilities for the Prevention, Detection, and Reporting of Fraud, Other Illegal Acts and Error. Australian Accounting Review 7: 51–61. [Google Scholar] [CrossRef]

- Gold, Anna, Ulfert Gronewold, and Christiane Pott. 2012. The ISA 700 Auditor’s Report and the Audit Expectation Gap–Do Explanations Matter? International Journal of Auditing 16: 286–307. [Google Scholar] [CrossRef]

- Gray, Glen L., Jerry L. Turner, Paul J. Coram, and Theodore J. Mock. 2011. Perceptions and Misperceptions Regarding the Unqualified Auditor’s Report by Financial Statement Preparers, Users, and Auditors. Accounting Horizons 25: 659–84. [Google Scholar] [CrossRef] [Green Version]

- Haddrill, Stephen. 2011. Speech by Stephen Haddrill, Chief Executive of the U.K. Financial Reporting Council, to the European Commission Conference on Financial Reporting and Auditing on Thursday 10th February 2011. Available online: http://www.frc.org.uk/images/uploaded/documents/CEO%20Audit%20speech%20Brussels%2010%20Feb1.pdf (accessed on 10 August 2018).

- Haddrill, Stephen. 2018. FRC’s Annual Development Audit. Available online: https://www.frc.org.uk/getattachment/f211c972-73ab-4bf2-b696-820eadc538bf/SH-Developments-in-Audit-FINAL-v2.pdf (accessed on 10 December 2018).

- Hair, Joseph F., Rolph E. Anderson, Ronald L. Tatham, and William C. Black. 1995. Multivariate Data Analyses with Readings. New Jersey: Englewood Cliffs. [Google Scholar]

- Hair, Joe F., Christian M. Ringle, and Marko Sarstedt. 2011. PLS-SEM: Indeed a Silver Bullet. Journal of Marketing Theory and Practice 19: 139–52. [Google Scholar] [CrossRef]

- Hair, Joe F., Marko Sarstedt, Christian M. Ringle, and Jeannette A. Mena. 2012. An Assessment of the Use of Partial Least Squares Structural Equation Modeling in Marketing Research. Journal of the Academy of Marketing Science 40: 414–33. [Google Scholar] [CrossRef]

- Hanson, J. D. 2016. PCAOB Update–Recent Activities and Next Steps. In 2016 SEC and Financial Reporting Institute Conference. Los Angeles: PCAOB. [Google Scholar]

- Hendrickson, Harvey. 1998. Relevant Financial Reporting Questions not Asked by the Accounting Profession. Critical Perspectives on Accounting 9: 489–505. [Google Scholar] [CrossRef]

- Hogan, Chris E., Zabihollah Rezaee, Richard A. Riley, and Uma K. Velury. 2008. Financial Statement Fraud: Insights from the Academic Literature. AUDITING: A Journal of Practice & Theory 27: 231–52. [Google Scholar]

- Hossen, Md Sahadat. 2016. Financial Reporting Act (FRA), 2015: A Revolutionary Era for Ensuring Effective Capital Market and Economic Development in Bangladesh. Global Journal of Management and Business Research 16: 13–20. [Google Scholar]

- Howieson, Bryan. 2013. Quis Auditoret Ipsos Auditores? Can Auditors Be Trusted? Australian Accounting Review 23: 295–306. [Google Scholar] [CrossRef]

- Humphrey, Christopher, Christopher Moizer, and Stuart Turley. 1992. The Audit Expectations Gap—Plus Ca Change, Plus C’est La Meme Chose? Critical Perspectives on Accounting 3: 137–61. [Google Scholar] [CrossRef]

- Humphrey, Christopher, Peter Moizer, and Stuart Turley. 1993a. The Audit Expectations Gap in Britain: An Empirical Investigation. Accounting and Business Research 23: 395–411. [Google Scholar] [CrossRef]

- Humphrey, Christopher, Stuart Turley, and Peter Moizer. 1993b. Protecting against Detection: The Case of Auditors and Fraud? Accounting, Auditing & Accountability Journal 6: 39–62. [Google Scholar]

- International Auditing & Assurance Standard Board (IAASB). 2009a. ISA 240 Summary: The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statement. New York: IAASB. [Google Scholar]

- International Auditing & Assurance Standard Board (IAASB). 2009b. Communication with those Charged with Governance, ISA 260. New York: IAASB. [Google Scholar]

- International Auditing & Assurance Standard Board (IAASB). 2009c. Communicating Deficiencies in Internal Control to those Charged with Governance and Management, ISA 265. New York: IAASB. [Google Scholar]

- International Auditing & Assurance Standard Board (IAASB). 2009d. Going Concern, ISA 570. New York: IAASB. [Google Scholar]

- IAASB. 2011. Enhancing the Value of Auditor Reporting: Exploring Options for Change. Available online: http://www.ifac.org/sites/default/files/publications/exposure–drafts/CP_Auditor_Reporting–Final.pdf (accessed on 30 August 2018).

- International Auditing & Assurance Standard Board (IAASB). 2012. Invitation to Comment: Improving the Auditor’s Report. New York: International Federation of Accountants. [Google Scholar]

- IAASB. 2014. A Framework for Audit Quality, 1–6. Available online: https://www.ifac.org/auditing- assurance/focus-audit-quality (accessed on 4 September 2018).

- International Auditing & Assurance Standard Board (IAASB). 2015a. The New Auditor’s Report: Greater Transparency into the Financial Statement Audit. Available online: www.iaasb.org/auditor-reporting (accessed on 10 January 2019).

- International Auditing & Assurance Standard Board (IAASB). 2015b. Forming an Opinion and Reporting on Financial Statements, ISA700 Revised. New York: IAASB. [Google Scholar]

- International Auditing & Assurance Standard Board (IAASB). 2015c. Communicating Key Audit Matters in the Independent Auditor’s Report, ISA 701. New York: IAASB. [Google Scholar]

- Institute of Chartered Accountants of England & Wales (ICAEW). 2008. Reconciling Stakeholders Expectation of Audit. Audit Quality Forum. Available online: www.icaew.co.uk/auditquality (accessed on 5 January 2019).

- International Federation of Accountants (IFAC). 2017. Legal and Regulatory Environment. IFAC, Bangladesh. Available online: https://www.ifac.org/about-ifac/membership/country/bangladesh (accessed on 12 September 2018).

- Jamal, Karim, and Shyam Sunder. 2011. Is Mandated Independence Necessary for Audit Quality? Accounting, Organizations and Society 36: 284–92. [Google Scholar] [CrossRef]

- Jarque, Carlos, and Anil Bera. 1980. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Econometric Letters 6: 255–25. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Kinney, William. R., Jr., Zoe-Vonna Palmrose, and Susan Scholz. 2004. Auditor independence, non-audit services, and restatements: Was the US government right? Journal of Accounting Research 42: 561–88. [Google Scholar] [CrossRef]

- Krishnamoorthy, Ganesh, Arnie Wright, and Jeffrey Cohen. 2002. Audit Committee Effectiveness and Financial Reporting Quality: Implications for Auditor Independence. Australian Accounting Review 12: 3–13. [Google Scholar] [CrossRef]

- Md Ali, A., T. H. Lee, and Juergen Dieter Gloeck. 2009. The Audit Expectation Gap in Malaysia: An Investigation into its Causes and Remedies. Southern African Journal of Accountability and Auditing Research 9: 57–88. [Google Scholar]

- Lim, Chee-Yeow-Y., and Hun-Tong Tan. 2008. Non-Audit Service Fees and Audit Quality: The Impact of Auditor Specialization. Journal of Accounting Research 46: 199–246. [Google Scholar] [CrossRef]

- Lin, Z. Jun, and Feng Chen. 2004. An Empirical Study of Audit ‘Expectation Gap’ in the People’s Republic of China. International Journal of Auditing 8: 93–115. [Google Scholar] [CrossRef]

- McEnroe, John E., and Stanley C. Martens. 2001. Auditors’ and Investors’ Perceptions of the “Expectation Gap”. Accounting Horizons 15: 345–58. [Google Scholar] [CrossRef]

- Mo Koo, Chi, and Ho Seog Sim. 1999. On the role conflict of auditors in Korea. Accounting. Auditing & Accountability Journal 12: 206–19. [Google Scholar]

- Mock, Theodore J., Christiane Strohm, and Kevin M. Swartz. 2007. An examination of worldwide assured sustainability reporting. Australian Accounting Review 17: 67–77. [Google Scholar] [CrossRef]

- Mock, Theodore J., Jean Bédard, Paul J. Coram, Shawn M. Davis, Reza Espahbodi, and Rick C. Warne. 2012. The Audit Reporting Model: Current Research Synthesis and Implications. AUDITING: A Journal of Practice & Theory 32: 323–51. [Google Scholar]

- Monroe, Gary S., and David R. Woodliff. 1993. The Effect of Education on the Audit Expectation Gap. Accounting & Finance 33: 61–78. [Google Scholar]

- Monroe, Gary S., and David R. Woodliff. 1994a. Great Expectations: Public Perceptions of the Auditor’s Role. Australian Accounting Review 4: 42–53. [Google Scholar] [CrossRef]

- Monroe, Gary S., and David R. Woodliff. 1994b. An Empirical Investigation of the Audit Expectation Gap: Australian Evidence. Accounting & Finance 34: 47–74. [Google Scholar]

- Nachar, Nadim. 2008. The Mann-Whitney U: A test for assessing whether two independent samples come from the same distribution. Tutorials in Quantitative Methods for Psychology 4: 13–20. [Google Scholar] [CrossRef]

- Nair, Raghavan, and Larry Rittenberg. 1987. Messages perceived from audit, review, and compilation reports: Extension to more diverse groups. Auditing: A Journal of Practice & Theory 7: 15–38. [Google Scholar]

- Nelson, Mark W. 2006. Ameliorating Conflicts of Interest in Auditing: Effects of Recent Reforms on Auditors and their Clients. The Academy of Management Review 31: 30–42. [Google Scholar] [CrossRef]

- Okafor, Chinwuba A., and John I. Otalor. 2013. Narrowing the expectation gap in auditing: the role of the auditing profession. Research Journal of Finance and Accounting 4: 43–52. [Google Scholar]

- Olagunju, Adebayo. 2011. An Empirical Analysis of the Impact of Auditors Independence on the Credibility of the Financial Statement in Nigeria. Research Journal of Finance and Accounting 2: 82–99. [Google Scholar]

- Public Company Accounting Oversight Board (PCAOB). 2011a. Concept Release on Auditor Independence and Audit Firm Rotation. Washington, DC: PCAOB. [Google Scholar]

- Public Company Accounting Oversight Board (PCAOB). 2011b. Concept Release on Possible Revisions to PCAOB Standards Related to Reports on Audited Financial Statements and Related Amendments to PCAOB Standards. Washington: PCAOB. [Google Scholar]

- Petter, Stacie, Detmar Straub, and Arun Rai. 2007. Specifying Formative Constructs in Information Systems Research. MIS Quarterly 31: 623–56. [Google Scholar] [CrossRef] [Green Version]

- Pickard, Jim, and Madison Marriage. 2018. Labour Consider Breaking up Big Four Accounting Firms. The Financial Times. September 21. Available online: https://www.ft.com/content/43fbd564-bc30-11e8-94b2-17176fbf93f5 (accessed on 12 December 2018).

- Porter, Brenda. 1991. Narrowing the Audit Expectation-Performance Gap: A Contemporary Approach. Pacific Accounting Review 3: 1–36. [Google Scholar]

- Porter, Brenda. 1993. An Empirical Study of the Audit Expectation-Performance Gap. Accounting and Business Research 24: 49–68. [Google Scholar] [CrossRef]

- Porter, Brenda A. 2009. The Audit Trinity: The Key to Securing Corporate Accountability. Managerial Auditing Journal 24: 156–82. [Google Scholar] [CrossRef]

- Porter, Brend, and Catherine Gowthorpe. 2004. Audit Expectation-Performance Gap in the United Kingdom in 1999 and Comparison with the Gap in New Zealand in 1989 and 1999. Edinburgh: The Institute of Chartered Accountants of Scotland. [Google Scholar]

- Porter, Brenda, Jon Simon, and David J. Hatherly. 2008. Principles of External Auditing. Hoboken: John Wiley & Sons, vol. 3. [Google Scholar]

- Porter, Brenda, Ó hÓgartaigh C. Hogartaigh, and Rachel Baskerville. 2012. Audit Expectation-Performance Gap Revisited: Evidence from New Zealand and the United Kingdom. Part 1: The Gap in New Zealand and the United Kingdom in 2008. International Journal of Auditing 16: 101–29. [Google Scholar] [CrossRef]

- Pourheydari, Omid, and Mina Abousaiedi. 2011. An Empirical Investigation of the Audit Expectations Gap in Iran. Journal of Islamic Accounting and Business Research 2: 63–76. [Google Scholar] [CrossRef]

- Ringle, Christian M., Sven Wende, and Jan-Michael Becker. 2015. SmartPLS 3. Available online: http://www.smartpls.com (accessed on 24 January 2019).

- Ruhnke, Klaus, and Martin Schmidt. 2014. The Audit Expectation Gap: Existence, Causes, and the Impact of Changes. Accounting and Business Research 44: 572–601. [Google Scholar] [CrossRef]

- Salehi, Mahdi, and Zhila Azary. 2009. Fraud Detection and Audit Expectation Gap: Empirical Evidence from Iranian Bankers. International Journal of Business and Management 3: 65–77. [Google Scholar] [CrossRef] [Green Version]

- Salehi, Mahdi, and Vahab Rostami. 2009. Audit expectation gap: International evidence. International Journal of Academic Research 1. [Google Scholar]

- Salleh, Zalailah, and Jenny Stewart. 2012. The Role of the Audit Committee in Resolving Auditor-Client Disagreements: A Malaysian Study. Accounting, Auditing & Accountability Journal 25: 1340–72. [Google Scholar]

- Schelluch, Peter, and Grant Gay. 2006. Assurance Provided by Auditors’ Reports on Prospective Financial Information: Implications for the Expectation Gap. Accounting & Finance 46: 653–76. [Google Scholar]

- Schelluch, Peter, and Wendy Green. 1996. The Expectation Gap: The Next Step. Australian Accounting Review 6: 19–23. [Google Scholar] [CrossRef]

- Shil, Nikhil Chandra. 2015. Stewardship, Transparency, Accountability, and Reporting [Star] Framework. A Journey Enlightening. The Cost and Management 43: 5–12. [Google Scholar]

- Siddiqui, Javed. 2018. Making the Financial Reporting Council functional. The Financial Express. February 3. Available online: https://thefinancialexpress.com.bd/views/making-financial-reporting-council-functional-1517669468 (accessed on 20 February 2019).

- Siddiqui, Javed, Taslima Nasreen, and Aklema Choudhury-Lema. 2009. The Audit Expectations Gap and the Role of Audit Education: The Case of an Emerging Economy. Managerial Auditing Journal 24: 564–83. [Google Scholar] [CrossRef]

- Sikka, Prem, Hugh Willmott, and Tony Lowe. 1989. Guardians of Knowledge and Public Interest: Evidence and Issues of Accountability in the UK Accountancy Profession. Accounting, Auditing & Accountability Journal 2. [Google Scholar]

- Sikka, Prem, Anthony Puxty, Hugh Willmott, and Christine Cooper. 1998. The Impossibility of Eliminating the Expectations Gap: Some Theory and Evidence. Critical Perspectives on Accounting 9: 299–330. [Google Scholar] [CrossRef] [Green Version]

- Simnett, Roger, Ann Vanstraelen, and Wai Fong Chua. 2009. An assurance on sustainability reports: An international comparison. The Accounting Review 84: 937–67. [Google Scholar] [CrossRef]

- Stephen, Kingsley. 2018. Auditing’s Expectation Gap is Worse than ever Financial Times. The Financial Times. January 14. Available online: https://www.ft.com (accessed on 10 August 2018).

- Stevenson, Mark. 2019. Can Auditors Close the Great Expectation Gap for Good? Pivot Magazine. February 2 CPA. Available online: https://www.cpacanada.ca/en/news/pivot-magazine/2019-01-02-expectation-gap-roundtable (accessed on 10 February 2019).

- Stirbu, Dan Aurelian A. 2010. Current Controversy on Audit Functions. In Annals of DAAAM & Proceedings of the 21st International DAAAM Symposium. Vienna: DAAAM Interenational. [Google Scholar]

- Tavakol, Mohsen, and Reg Dennick. 2011. Making Sense of Cronbach’s Alpha. International Journal of Medical Education 2: 53–55. [Google Scholar] [CrossRef]

- Umar, Ahson, and Asokan Anandarajan. 2004. Dimensions of Pressures Faced by Auditors and its Impact on Auditors’ Independence: A Comparative Study of the USA and Australia. Managerial Auditing Journal 19: 99–116. [Google Scholar] [CrossRef]

- Van Riel, Allard CR, Jörg Henseler, Ildikó Kemény, and Zuzana Sasovova. 2017. Estimating Hierarchical Constructs Using Consistent Partial Least Squares: The Case of Second-Order Composites of Common Factors. Industrial Management & Data Systems 117: 459–77. [Google Scholar]

- Wallman, Steven MH. 1996. The future of accounting, part III: Reliability and auditor independence. Accounting Horizons 10: 76. [Google Scholar]

- Wolf, Fran M., Gregory A. Claypool, and James A. Tackett. 1999. Audit Disaster Futures: Antidotes for the Expectation Gap? Managerial Auditing Journal 14: 468–78. [Google Scholar] [CrossRef]

- Xie, Fujiao. 2016. Competition, Auditor Independence and Audit Quality. Ph.D. dissertation, University of Hawaii, Honolulu, HI, USA. [Google Scholar]

- Yip, Peter Chi-Wan, and Elvy Pang. 2017. Investors’ Perceptions of Auditor Independence: Evidence from Hong Kong. E-Journal of Social & Behavioural Research in Business 8: 70–82. [Google Scholar]

- Zaman, Mahbub, Mohammed Hudaib, and Roszaini Haniffa. 2011. Corporate governance quality, audit fees and nominees of Auditor Independence: Evidence from Hong & Accounting. Journal of Business Finance & Accounting 38: 165–97. [Google Scholar]

| Respondent Group and Basic Question | |||||

|---|---|---|---|---|---|

| Variable/Dimension | Frequency | Percentage | Variable/Dimension | Frequency | Percentage |

| Respondents Groups | Read audit report | ||||

| Auditors | 33 | 19 | Auditors | 33 | 19 |

| Investors | 42 | 24 | Investors | 6 | 3 |

| Investment Analysts | 36 | 21 | Investment Analysts | 15 | 9 |

| Credit Analysts | 35 | 20 | Credit Analysts | 18 | 10 |

| Regulatory Agencies | 28 | 16 | Regulatory Agencies | 10 | 6 |

| Total | 174 | 100 | Total | 82 | 47 |

| Level of Education | Take Decision Based on the audit report | ||||

| Graduate | 73 | 42 | Auditors | 33 | 19 |

| Post-Graduate | 49 | 28 | Investors | 2 | 1 |

| Professional Degree, e.g., ACA/ACMA/FCA/FCMA | 47 | 27 | Investment Analysts | 12 | 7 |

| Ph.D./others | 5 | 3 | Credit Analysts | 15 | 9 |

| Total | 174 | 100 | Regulatory Agencies | 8 | 5 |

| Total | 70 | 40 | |||

| Accounting and Audit related Experiences | Compared with International Standards | ||||

| 1–3 years | 45 | 26 | Auditors | 24 | 14 |

| 4–6 years | 72 | 41 | Investors | 4 | 2 |

| 7–9 years | 36 | 21 | Investment Analysts | 10 | 6 |

| 10 years+ | 21 | 12 | Credit Analysts | 12 | 7 |

| Total | 174 | 100 | Regulatory Agencies | 10 | 6 |

| Total | 60 | 35 | |||

| Formation of First-Order Construct and Items | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Path | Indicator Loading | Indicator Weight | T-stat | VIF | Path | Indicator Loading | Indicator | T-Stat | VIF |

| Weight | |||||||||

| ARF1-ARF | 0.696 | 0.292 | 10.336 | 1.353 | ARF1-AEG | 0.467 | 0.016 | 2.411 | 1.647 |

| ARF2-ARF | 0.914 | 0.312 | 17.922 | 1.537 | ARF2-AEG | 0.470 | 0.006 | 1.988 | 1.575 |

| ARF3-ARF | 0.897 | 0.307 | 17.558 | 4.528 | ARF3-AEG | 0.346 | 0.026 | 2.070 | 4.558 |

| ARF4-ARF | 0.770 | 0.307 | 9.628 | 5.134 | ARF4- AEG | 0.347 | 0.027 | 2.768 | 5.444 |

| MUAR1-MUAR | 0.790 | 0.216 | 16.305 | 2.008 | MUAR1-AEG | 0.556 | 0.004 | 2.081 | 2.271 |

| MUAR2-MUAR | 0.871 | 0.240 | 17.833 | 2.657 | MUAR2-AEG | 0.611 | 0.019 | 2.351 | 2.923 |

| MUAR3-MUAR | 0.794 | 0.237 | 16.795 | 2.024 | MUAR3-AEG | 0.591 | 0.054 | 1.980 | 2.392 |

| MUAR4-MUAR | 0.885 | 0.244 | 20.842 | 2.999 | MUAR4-AEG | 0.623 | 0.114 | 2.068 | 3.325 |

| MUAR5-MUAR | 0.879 | 0.247 | 20.171 | 2.885 | MUAR5-AEG | 0.620 | 0.018 | 2.304 | 3.350 |

| NAS1-NAS | 0.861 | 0.549 | 5.294 | 1.150 | NAS1-AEG | 0.590 | 0.130 | 1.920 | 1.300 |

| NAS2-NAS | 0.893 | 0.590 | 13.797 | 1.391 | NAS2-AEG | 0.662 | 0.119 | 2.866 | 1.637 |

| NAS3-NAS | 0.039 | 0.023 | 13.273 | 1.421 | NAS3-AEG | 0.020 | 0.035 | 1.849 | 1.960 |

| GCRA1-GCR | 0.531 | 0.243 | 5.207 | 1.151 | GCRA1 -AEG | 0.344 | 0.049 | 2.874 | 1.260 |

| GCRA2- GCR | 0.563 | 0.275 | 4.562 | 1.955 | GCRA2 -AEG | 0.420 | 0.120 | 1.924 | 1.206 |

| GCRA3-GCR | 0.808 | 0.440 | 7.735 | 1.419 | GCRA3 -AEG | 0.621 | 0.063 | 1.771 | 1.124 |

| GCRA4-GCR | 0.724 | 0.296 | 7.503 | 1.801 | GCRA4 -AEG | 0.415 | 0.004 | 1.773 | 1.279 |

| OA1-OA | 0.596 | 0.305 | 15.271 | 1.421 | OA1-AEG | 0.409 | 0.127 | 1.845 | 2.053 |

| OA2-OA | 0.833 | 0.485 | 15.295 | 1.426 | OA2-AEG | 0.706 | 0.235 | 1.718 | 2.078 |

| OA3-OA | 0.843 | 0.491 | 2.318 | 1.012 | OA3-AEG | 0.710 | 0.147 | 1.749 | 1.132 |

| RNAS1-RNAS | 0.673 | 0.262 | 8.802 | 1.195 | RNAS1-API | 0.487 | 0.085 | 2.152 | 1.292 |

| RNAS2-RNAS | 0.770 | 0.276 | 13.363 | 1.400 | RNAS2-API | 0.501 | 0.053 | 1.736 | 1.485 |

| RNAS3-RNAS | 0.839 | 0.383 | 18.242 | 1.900 | RNAS3-API | 0.694 | 0.151 | 2.892 | 2.156 |

| MAR 1-MAR | 0.694 | 0.344 | 8.183 | 1.250 | MAR 1-API | 0.442 | 0.042 | 3.938 | 1.333 |

| MAR 2-MAR | 0.839 | 0.411 | 15.504 | 1.565 | MAR 2-API | 0.522 | 0.043 | 3.767 | 2.663 |

| MAR 3- MAR | 0.832 | 0.500 | 14.455 | 1.450 | MAR 3-API | 0.639 | 0.189 | 3.299 | 1.736 |

| CAAC1-AAC | 0.799 | 0.493 | 13.733 | 1.325 | AAC1-API | 0.601 | 0.182 | 3.315 | 1.447 |

| CAAC2-AAC | 0.811 | 0.464 | 13.516 | 1.350 | AAC2-API | 0.564 | 0.083 | 3.456 | 1.510 |

| CAAC3-AAC | 0.633 | 0.363 | 7.551 | 1.114 | AAC3-API | 0.442 | 0.065 | 1.730 | 1.053 |

| EAR1-EAR | 0.725 | 0.214 | 9.301 | 1.961 | EAR1-AILC | 0.488 | 0.062 | 1.772 | 2.041 |

| EAR2-EAR | 0.925 | 0.226 | 10.946 | 2.736 | EAR2-AILC | 0.501 | 0.099 | 1.769 | 2.872 |

| EAR3-EAR | 0.802 | 0.215 | 8.840 | 2.969 | EAR3-AILC | 0.476 | 0.120 | 1.713 | 3.042 |

| EAED1-EAED | 0.843 | 0.510 | 10.410 | 1.306 | EAED1-AILC | 0.587 | 0.230 | 3.450 | 1.495 |

| EAED2-EAED | 0.790 | 0.426 | 12.789 | 1.383 | EAED2-AILC | 0.485 | 0.141 | 2.648 | 1.450 |

| EAED3-EAED | 0.665 | 0.349 | 8.295 | 1.235 | EAED3-AILC | 0.401 | 0.112 | 2.292 | 1.322 |

| SC1-SC | 0.658 | 0.288 | 7.098 | 1.428 | - | - | - | - | - |

| SC2-SC | 0.825 | 0.383 | 10.812 | 1.701 | - | - | - | - | - |

| SC3-SC | 0.823 | 0.344 | 10.833 | 2.733 | - | - | - | - | - |

| SC4-SC | 0.789 | 0.268 | 8.659 | 2.623 | - | - | - | - | - |

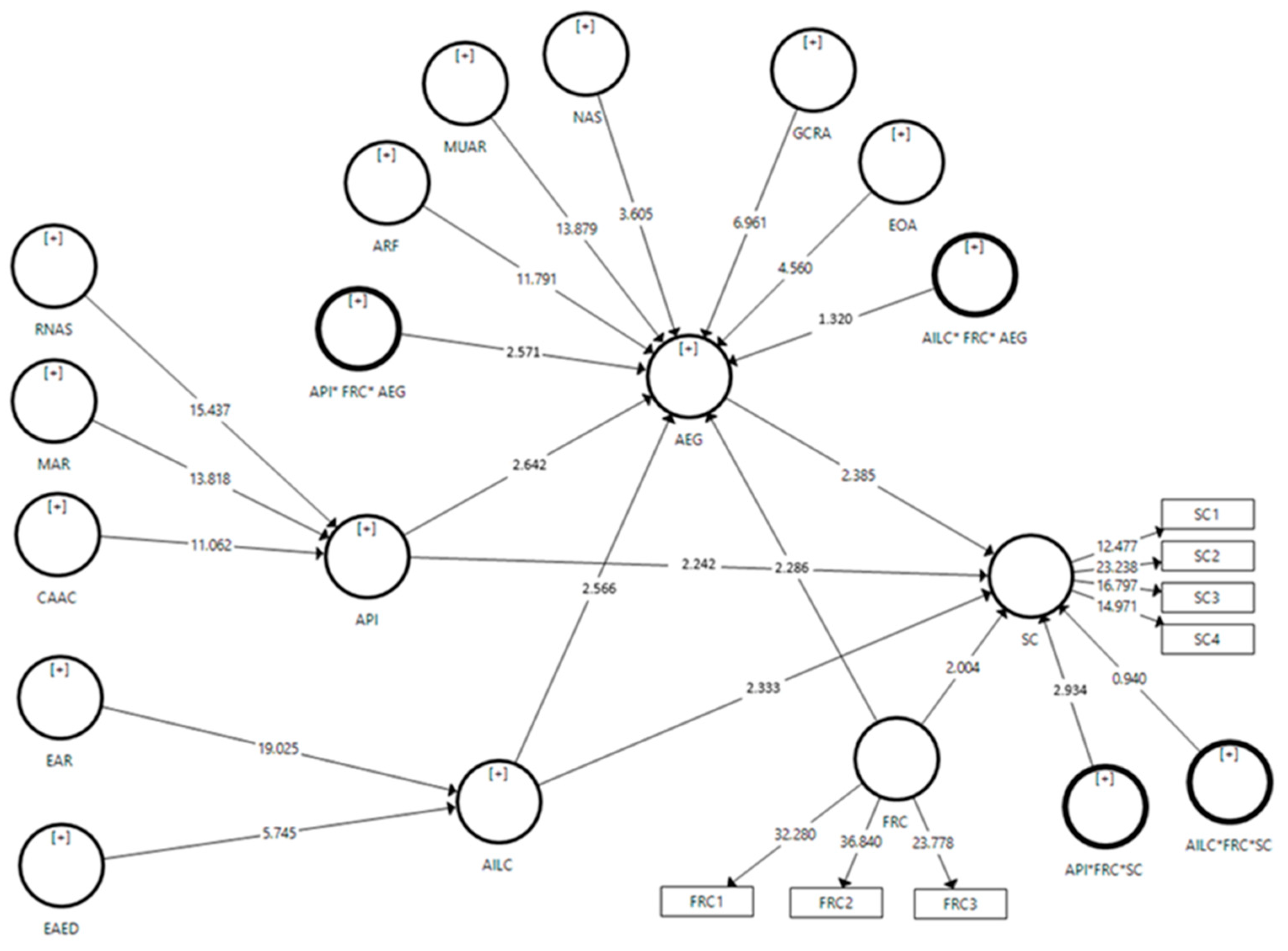

| AEG is Linked with ARF, MUAR, NAS, GCRA and EOA; API is Linked with RNAS, MAR and AAC, and AILC is Linked with EAR and EAE | ||||

|---|---|---|---|---|

| Second-Order Construct | First-Order Construct | Std. Beta | T-Statistic | p-Value |

| AEG | ARF | 0.018 | 11.791 | 0.000 *** |

| MUAR | 0.026 | 13.879 | 0.000 *** | |

| NAS | 0.159 | 3.605 | 0.016 ** | |

| GCRA | 0.025 | 6.961 | 0.000 *** | |

| EOA | 0.020 | 4.560 | 0.000 *** | |

| API | RNAS | 0.031 | 15.437 | 0.000 *** |

| MAR | 0.029 | 13.818 | 0.000 *** | |

| AAC | 0.028 | 11.062 | 0.000 *** | |

| AILC | EAR | 0.042 | 19.025 | 0.000 *** |

| EAED | 0.055 | 5.745 | 0.000 *** | |

| API andAILC Negatively Impact AEG and Positively Impact SC, Whereas a Negative Relation between AEG and SC | |||||

|---|---|---|---|---|---|

| Hypothesis | Path | Std. Beta | T-Statistic | p-Value | Decision |

| H1c | API -> AEG | −0.013 | 2.642 | 0.000 *** | Supported |

| H1e | AILC -> AEG | −0.050 | 2.566 | 0.000 *** | Supported |

| H2 | AEG -> SC | −0.123 | 2.385 | 0.035 ** | Supported |

| H3a | API -> SC | 0.100 | 2.242 | 0.030 ** | Supported |

| H3b | AILC -> SC | 0.060 | 2.333 | 0.020 ** | Supported |

| FRC Positively Moderates to Ensure Auditors’ Perceived Independence (API) | |||||

|---|---|---|---|---|---|

| Hypothesis | Path | Std. Beta | T-Statistic | p-Value | Decision |

| H4a | FRC*API -> AEG | −0.017 | 2.571 | 0.010 ** | Supported |

| H4b | FRC*AILC -> AEG | −0.104 | 0.940 | 0.348 | Unsupported |

| H4c | FRC*API -> SC | 0.049 | 2.280 | 0.038 ** | Supported |

| H4d | FRC*AILC -> SC | 0.108 | 0.885 | 0.371 | Unsupported |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Akther, T.; Xu, F. Existence of the Audit Expectation Gap and Its Impact on Stakeholders’ Confidence: The Moderating Role of the Financial Reporting Council. Int. J. Financial Stud. 2020, 8, 4. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs8010004

Akther T, Xu F. Existence of the Audit Expectation Gap and Its Impact on Stakeholders’ Confidence: The Moderating Role of the Financial Reporting Council. International Journal of Financial Studies. 2020; 8(1):4. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs8010004

Chicago/Turabian StyleAkther, Taslima, and Fengju Xu. 2020. "Existence of the Audit Expectation Gap and Its Impact on Stakeholders’ Confidence: The Moderating Role of the Financial Reporting Council" International Journal of Financial Studies 8, no. 1: 4. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs8010004