The Qualitative Characteristics of Accounting Information, Earnings Quality, and Islamic Banking Performance: Evidence from the Gulf Banking Sector

Abstract

:1. Introduction

Objectives of the Study

2. Literature Review

2.1. Earnings Quality (EQ)

2.2. The Performance

3. The Methodology

3.1. Data Collection and Analysis

3.2. Qualitative Characteristics of Accounting Information

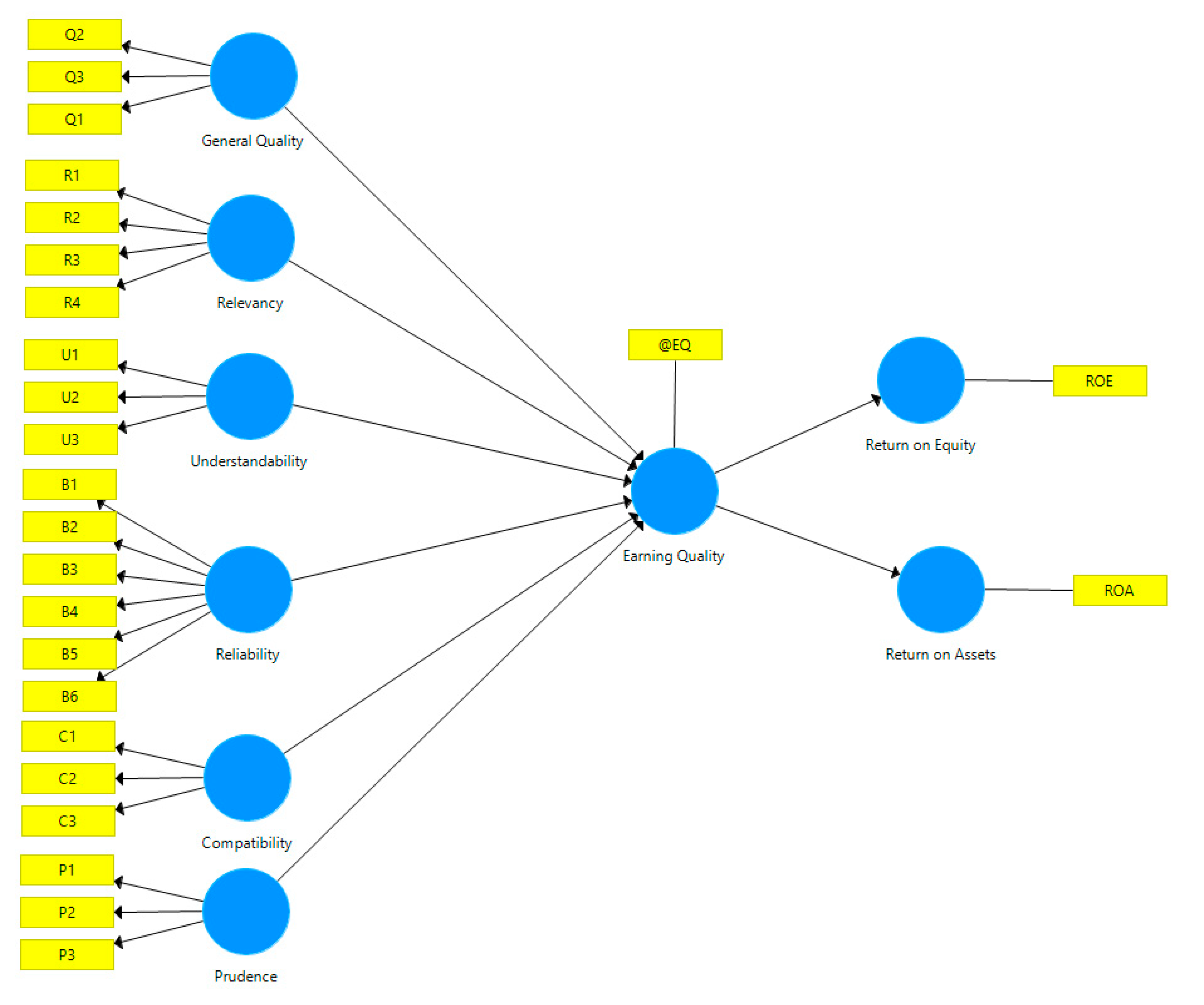

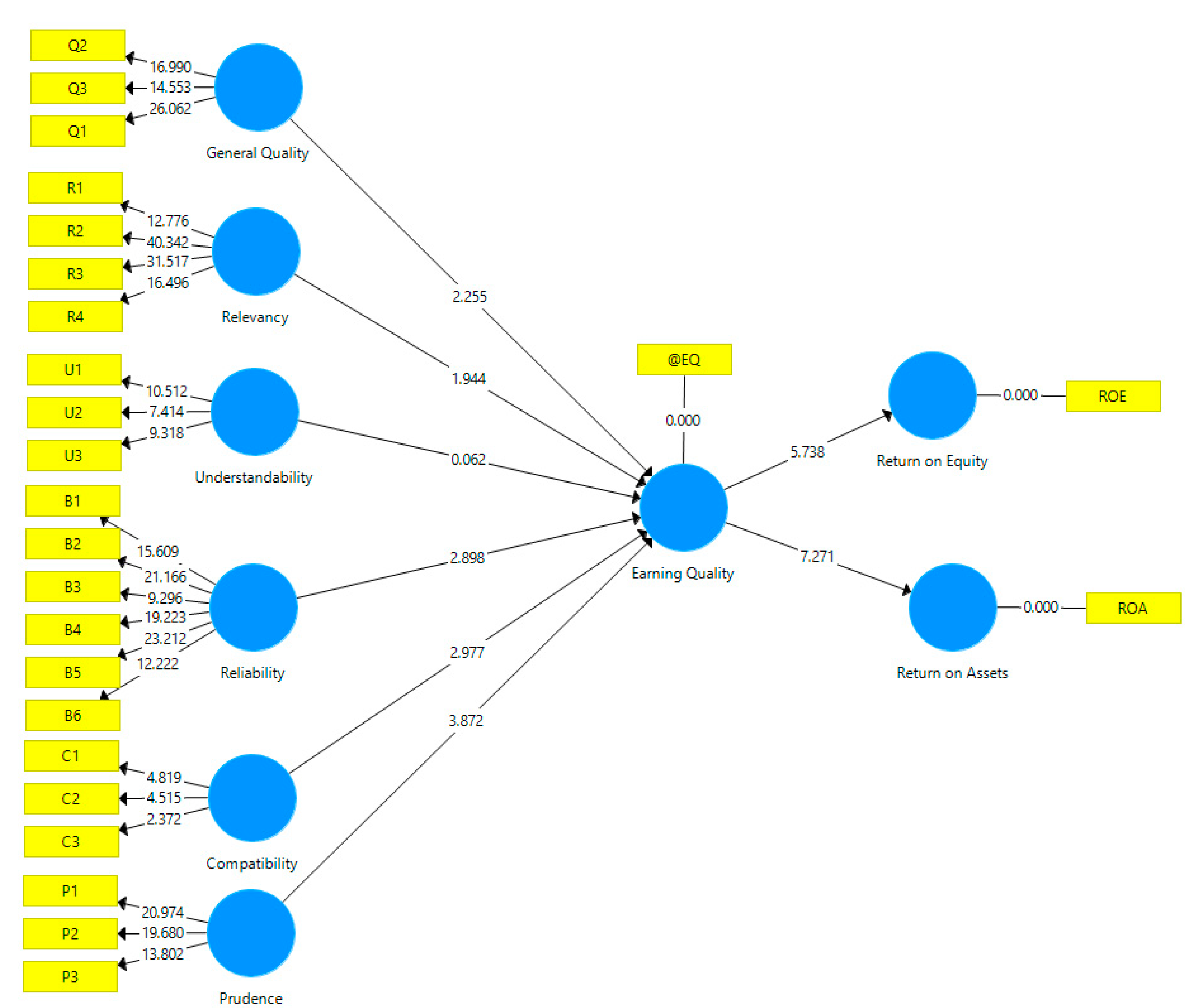

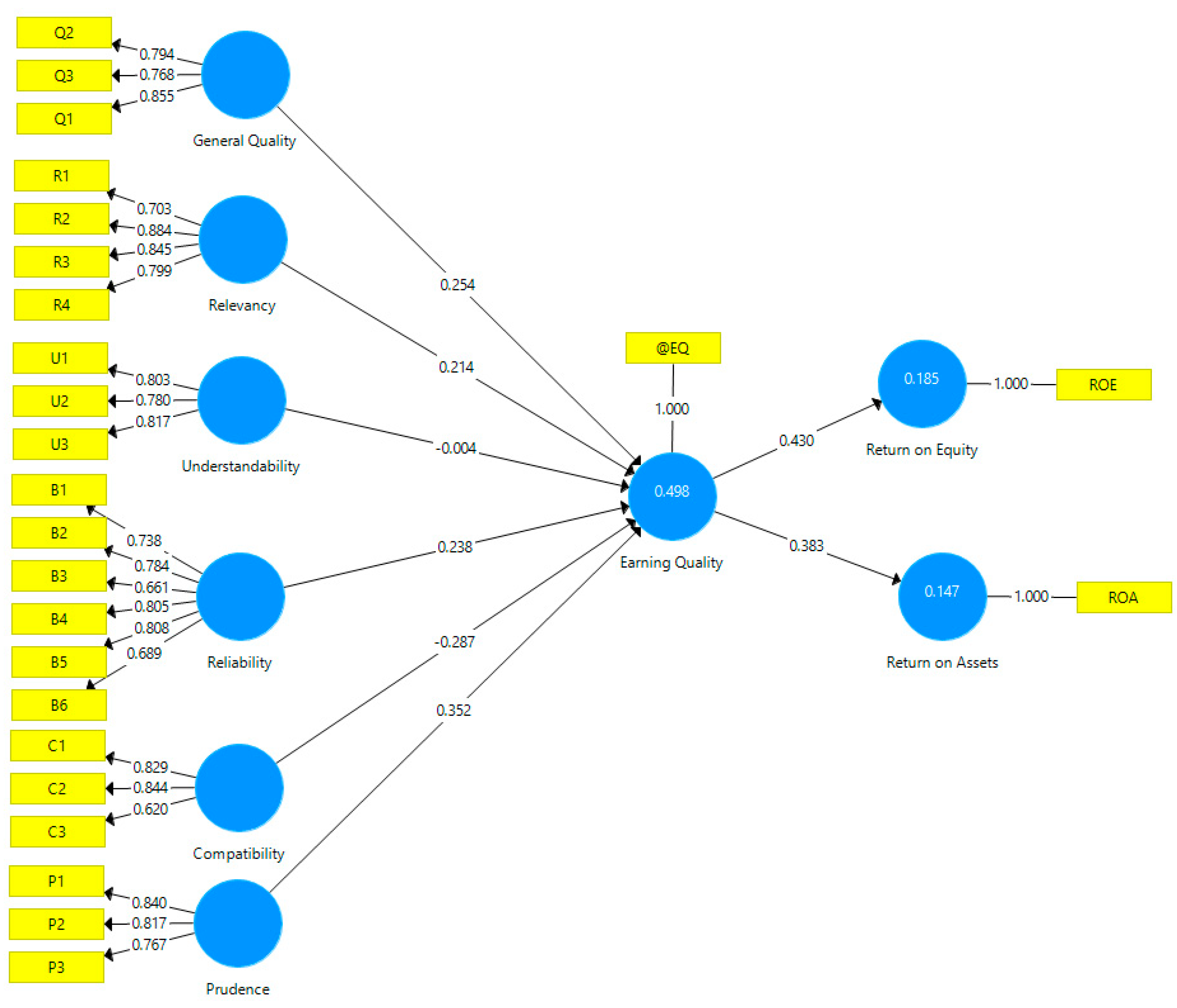

4. Results and Analysis

Assessing the Measurement Model Fit

5. Conclusions

Funding

Acknowledgments

Conflicts of Interest

References

- AAOIFI. 2017. Financial Accounting Standards. Manama: Accounting and Auditing Organization for Islamic Financial Institutions. [Google Scholar]

- Abdul Majid, Nurul Huda, and Abdul Ghafar Ismail. 2008. Determinants of Disclosure Quality in Islamic Banks. Working Paper, Islamic Economics and Finance No. 0803. Bangi: University Kebangsaan Malaysia, pp. 1–14. [Google Scholar]

- Aggarwal, Raj, Varun Jindal, and Rama Seth. 2019. Board diversity and firm performance: The role of business group affiliation. International Business Review 28: 101600. [Google Scholar] [CrossRef]

- Ahmed, Ibrahim Elsiddig. 2012. The Contents of Social Disclosure: A Survey of the UAE Islamic Banks’ Repots. Khartoum University Journal of Management Studies KUJMS 5: 99–121. [Google Scholar]

- Ahmed, Anwer S., and Scott Duellman. 2011. Evidence on the role of accounting conservatism in monitoring managers’ investment decisions. Accounting and Finance 51: 6090–33. [Google Scholar] [CrossRef]

- Akhtar, Muhammad Farhan, Khizer Ali, and Shama Sadaqat. 2011. Factors Influencing the Profitability of Islamic Banks of Pakistan. International Research Journal of Finance and Economics 66: 125–32. [Google Scholar]

- Al-Asiry, Majedh. 2017. Determinants of Quality of Corporate Voluntary Disclosure in Emerging Countries: A Cross National Study. Ph.D. dissertation, University of Southampton, Southampton, UK; pp. 1–215. [Google Scholar]

- Alfraih, Mishari M., and Abdullah M. Almutawa. 2014. Firm-Specific Characteristics and Corporate Financial Disclosure: Evidence from an Emerging Market. International Journal of Accounting and Taxation 2: 55–78. [Google Scholar] [CrossRef] [Green Version]

- Aljifri, Khaled, and Sunil Kumar Khandelwal. 2013. Financial Contracts in Conventional and Islamic Financial Institutions: An Agency Theory Perspective. Review of Business & Finance Studies 4: 79–88. [Google Scholar]

- Allegret, Jean-Pierre, Hélène Raymond, and Houda Rharrabti. 2016. The Impact of the Eurozone Crisis on European Banks Stocks, Contagion or Interdependence. European Research Studies Journal 19: 129–47. [Google Scholar] [CrossRef] [Green Version]

- Anderson, Mark C., Soonchul Hyun, and Hussein A. 2014. Corporate Social Responsibility, Earnings Management, and Firm Performance: Evidence from Panel VAR Estimation. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2379826 (accessed on 11 May 2020).

- Asegdew, Kirubel. 2016. Determinants of Financial Reporting Quality: Evidence from Large Manufacturing Share Companies of Addis Ababa. Master’s dissertation, Department of Accounting and Finance, College of Business and Economics, Addis Ababa University-Ethiopia, Addis Ababa, Ethiopia. [Google Scholar]

- Bahrini, Raéf. 2017. Efficiency Analysis of Islamic Banks in the Middle East and North Africa Region: A Bootstrap DEA Approach. International Journal of Financial Studies 5: 7. [Google Scholar] [CrossRef] [Green Version]

- Barth, Mary E., William H. Beaver, and Wayne R. Landsman. 2001. The Relevance of the Value Relevance Literature for Financial Accounting Standard Setting: Another View. Journal of Accounting and Economics 31: 77–104. [Google Scholar] [CrossRef]

- Barth, Mary E., Wayne R. Landsman, and Mark H. Lang. 2008. International Accounting Standards and Accounting Quality. Journal of Accounting Research 46: 467–98. [Google Scholar] [CrossRef] [Green Version]

- Barton, Jan, and Paul J. Simko. 2002. The balance sheet as an earnings management constraint. The Accounting Review 77: 1–27. [Google Scholar] [CrossRef]

- Bashir, Abdel-Hameed M. 2001. Assessing the performance of Islamic Banks: Some evidence from the Middle East. Islamic Economic Studies 11: 31–60. [Google Scholar]

- Bhattacharya, Nilabhra, Hemang Desai, and Kumar Venkataraman. 2013. Does Earnings Quality Affect Information Asymmetry? Evidence from Trading Costs. Contemporary Accounting Research 30: 482–516. [Google Scholar] [CrossRef]

- Bill, Francis, Iftekhar Hassan, Sureshbabu Many, and Ye Pengfei. 2016. Relative Peer Quality and Firm Performance. Economics 122: 196–219. [Google Scholar]

- Braam, Geert, and Ferdy Van Beest. 2013. Conceptually-Based Financial Reporting Quality Assessment: An Empirical Analysis on Quality Differences between UK Annual Reports and US 10-K Reports. NiCE Working Paper. Nijmegen: Institute for Management Research, Radboud University Nijmegen, pp. 1–34. [Google Scholar]

- Chakroun, Raïda, and Khaled Hussainey. 2014. Disclosure Quality in Tunisian Annual Reports. Corporate Ownership and Control 11: 58–80. [Google Scholar] [CrossRef]

- Chan, Konan, Louis K. C. Chan, Narasimhan Jegadeesh, and Josef Lakonishok. 2006. Earnings Quality and Stock Returns. Journal of Business 79: 1041–82. [Google Scholar] [CrossRef] [Green Version]

- Debnath, Pranesh. 2017. Assaying the Impact of Firm’s Growth and Performance on Earnings Management: An Empirical Observation of Indian Economy. International Journal of Research in Business Studies and Management 4: 30–40. [Google Scholar]

- Dedman, Elisabeth, Stephen W. J. Lin, Arun J. Prakash, and Chun Hao Chang. 2008. Voluntary disclosure and its impact on share prices: Evidence from the UK biotechnology sector. Journal of Accounting and Public Policy 27: 195–216. [Google Scholar] [CrossRef]

- Deltuvaitė, Vilma. 2010. The concentration Stability Relationship in the Banking System: An Empirical Study. Economics and Management 15: 900–9. [Google Scholar]

- Dijkstra, Theo K., and Jörg Henseler. 2015. Consistent Partial Least Squares Path Modeling. MIS Quarterly 39: 297–316. [Google Scholar] [CrossRef]

- Dospinescu, Nicoleta, and Octavian Dospinescu. 2019. A Profitability Regression Model in Financial Communication of Romanian Stock Exchange’s Companies. EcoForum 8. [Google Scholar]

- Dospinescu, Octavian, Bogdan Anastasiei, and Nicoleta Dospinescu. 2019. Key Factors Determining the Expected Benefit of Customers When Using Bank Cards: An Analysis on Millennials and Generation Z in Romania. Symmetry 11: 1449. [Google Scholar] [CrossRef] [Green Version]

- Du, Ke-Lin, and Madisetti NS Swamy. 2006. Neural Networks in a Soft Computing Framework. London: Springer. [Google Scholar]

- Duha, M. Abu Jledan. 2016. Earnings Management Behavior of Islamic Banks and Conventional Banks: Evidence from Jordan and Gulf Banks. Available online: https://www.academia.edu/23095375/ (accessed on 11 May 2020).

- Ebrahimabadi, Ziba, and Abdorreza Asadi. 2016. The Study of Relationship between Corporate Characteristics and Voluntary Disclosure in Tehran Stock Exchange. International Business Management 10: 1170–76. [Google Scholar]

- El Moussawi, Chawki, and Hassan Obeid. 2010. Evaluating the Productive Efficiency of Islamic Banking in GCC: A Non-Parametric Approach. International Research Journal of Finance and Economics 53: 178–90. [Google Scholar]

- Farooq, Omar, and Allaa AbdelBari. 2015. Earnings management behavior of Shariah-compliant firms and non-Shariah compliant firms: Evidence from the MENA region. Journal of Islamic Accounting and Business Research 6: 173–88. [Google Scholar] [CrossRef]

- Fathi, Jouini. 2013. The Determinants of the Quality of Financial Information Disclosed by French Listed Companies. Mediterranean Journal of Social Sciences 4: 319–36. [Google Scholar] [CrossRef]

- Haji, Abdifatah Ahmed, and Nazli Anum Mohd Ghazali. 2013. The Quality and Determinants of Voluntary Disclosures in Annual Reports of Shari’ah Compliant Companies in Malaysia. Humanomics 29: 24–42. [Google Scholar] [CrossRef]

- Henseler, Jörg, Christian M. Ringle, and Marko Sarstedt. 2015. A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science 43: 115–35. [Google Scholar] [CrossRef] [Green Version]

- Jaballah, Emna, Wided Yousfi, and Z. M. Ali. 2014. Quality of financial reports: Evidence from the Tunisian firms. Journal of Business Management and Economics 5: 30–38. [Google Scholar]

- Jang, Geun Bae, and Weon-Jae Kim. 2017. Effects of Key Financial Indicators on Earnings Management in Korea’s Ready Mixed Concrete Industry. Journal of Applied Business Research 33: 329–42. [Google Scholar] [CrossRef] [Green Version]

- Jing, Zhou. 2007. Earnings Quality, Analyst, Institutional Investor and Stock Price Synchronicity. Ph.D. dissertation, Hong Kong Polytechnic University, Hong Kong, China. [Google Scholar]

- Kuznetsova, Yelena Vyacheslavovna, Irina Nikolayevna Bogataya, Natalya Nikolayevna Khakhonova, and Svyatoslav Pavlovich Katerinin. 2017. Methodology of Building up the Accounting and Analytical Management Support for Organizations in Russia. European Research Studies Journal 20: 257–66. [Google Scholar] [CrossRef]

- Lara, Juan Manuel García, Beatriz García Osma, and Fernando Penalva. 2011. Conditional conservatism and cost of capital. Review of Accounting Studies 16: 247–71. [Google Scholar] [CrossRef] [Green Version]

- Leuz, Christian, Dhananjay Nanda, and Peter D. Wysocki. 2003. Earnings management and investor protection: An international comparison. Journal of financial Economics 69: 505–27. [Google Scholar] [CrossRef]

- Liapis, Konstantinos J., and Eleftherios Thalassinos. 2013. A Comparative Analysis for the Accounting Reporting of “Employee Benefits” between IFRS and other Accounting Standards: A Case Study for the Biggest Listed Entities in Greece. International Journal of Economics and Business Administration 1: 91–116. [Google Scholar] [CrossRef] [Green Version]

- Lin, Chan-Jane, Tawei Wang, and Chao-Jung Pan. 2016. Financial reporting quality and investment decisions for family firms. Asia Pacific Journal of Management 33: 499–532. [Google Scholar] [CrossRef]

- Marston, Claire L., and Philip J. Shrives. 1991. The Use of Disclosure Indices in Accounting Research: A Review Article. British Accounting Review 23: 195–210. [Google Scholar] [CrossRef]

- Mbobo, Mbobo Erasmus, and Ntiedo Bassey Ekpo. 2016. Operationalizing the Qualitative Characteristics of Financial Reporting. International Journal of Finance and Accounting 5: 184–92. [Google Scholar]

- Monday, Ikpor Isaac, and Agha Nancy. 2016. Determinants of Voluntary Disclosure Quality in Emerging Economies: Evidence from Firms Listed in Nigeria Stock Exchange. International Journal of Research in Engineering and Technology 4: 37–50. [Google Scholar]

- Nichols, D. Craig, and James M. Wahlen. 2004. How do Earnings Numbers Relate to Stock Returns? A Review of Classic Accounting Research with Updated Evidence. Accounting Horizons 18: 263–86. [Google Scholar] [CrossRef]

- Nwaobia, A. N., Jerry Kwarbai, Jayeoba Olajumoke, and A. T. Ajibade. 2016. Financial Reporting Quality on Investors’ Decisions. International Journal of Economics and Financial Research 2: 140–47. [Google Scholar]

- Olson, Dennis, and Taisier A. Zoubi. 2011. Efficiency and bank profitability in MENA countries. Emerging Markets Review 12: 94–110. [Google Scholar] [CrossRef]

- Pivac, Snjezana, Tina Vuko, and Marko Cular. 2017. Analysis of Annual Report Disclosure Quality for Listed Companies in Transition Countries. Economic Research-EkonomskaIstraživanja 30: 721–31. [Google Scholar] [CrossRef] [Green Version]

- Raffournier, A. 2006. The Determinants of Voluntary Financial Disclosure by Swiss Nonfinancial listed Firms. European Accounting Review 4: 261–80. [Google Scholar] [CrossRef]

- Sadeghi, Seyed Arash, and Batool Zareie. 2015. Relationship between earnings management and financial ratios at the family firms listed in the Tehran stock exchange. Indian Journal of Fundamental and Applied Life Sciences 5: 1411–20. [Google Scholar]

- Sarea, Adel Mohamm. 2012. The Level of Compliance with AAOIFI Accounting Standards: Evidence from Bahrain. International Management Review 8: 27–32. [Google Scholar]

- Savina, Tatyana N. 2016. The Institutionalization of the Concept of Corporate Social Responsibility: Opportunities and Prospects. European Research Studies Journal 19: 56–76. [Google Scholar] [CrossRef]

- Soheilyfar, Fatemeh, Mohammad Tamimi, Mohammad Ramezan Ahmadi, and Nasrollah Takhtaei. 2014. Disclosure Quality and Corporate Governance: Evidence from Iran. Asian Journal and Finance and Accounting 6: 75–86. [Google Scholar] [CrossRef] [Green Version]

- Steven, F. Cahan, David Emanuel, and Jerry Sun. 2009. The effect of earnings quality and country-level institutions on the value relevance of earnings. Review of Quantitative Finance and Accounting 33: 371–91. [Google Scholar]

- Sutan, Emir Hidayat, and Abdulla Abdulrahman Nayla. 2014. An Analysis on Disclosures in the Annual Reports of Islamic Banks in Bahrain. International Journal of Pedagogical Innovations 2: 1–5. [Google Scholar]

- Suryanto, Tulus. 2017. Cultural Ethics and Consequences in Whistle-Blowing among Professional Accountants: An Empirical Analysis. Journal of Applied Economic Sciences 6: 1725–31. [Google Scholar]

- Takhtaei, N., Zahra Mousavi, Mohammad Tamimi, and Iman Farahbakhsh. 2014. Determinants of Disclosure Quality: Empirical Evidence from Iran. Asian Journal of Finance and Accounting 6: 422–38. [Google Scholar] [CrossRef]

- Thalassinos, Eleftherios, Mirela Pintea, and Patricia Iulia Ratiu. 2015. The recent financial crisis and its impact on the performance indicators of selected countries during the crisis period: A reply. International Journal of Economics & Business Administration 3: 3–20. [Google Scholar]

- Uyar, Ali, Merve Kilic, and Nizamettin Bayyurt. 2013. Association between Firm Characteristics and Corporate Voluntary Disclosures: Evidence from Turkish Non-financial listed Firms. Journal of Intangible Capital 9: 1080–112. [Google Scholar]

- Uyen, Dang. 2011. The CAMEL Rating System in Banking Supervision. A Case Study. Ph.D. dissertation, Arcada University of Applied Sciences, Helsinki, Finland. ARCADA 10312. [Google Scholar]

- Van Beest, F., G. J. M. Braam, and Suzanne Boelens. 2009. Quality of Financial Reporting: Measuring Qualitative Characteristics. Working Paper. Nijmegan: Radboud University, pp. 1–108. [Google Scholar]

- Van Tendeloo, Brenda, and Ann Vanstraelen. 2005. Earnings Management under German GAAP versus IFRS. European Accounting Review 14: 155–80. [Google Scholar] [CrossRef]

- Vovchenko, Natalia G., Evgeniy N. Tishchenko, Tatiana V. Epifanova, and Mark B. Gontmacher. 2017. Electronic currency: The potential risks to national security and methods to minimize them. European Research Studies Journal 20: 36–48. [Google Scholar]

- Yao, Hongxing, Muhammad Haris, and Gulzara Tariq. 2018. Profitability Determinants of Financial Institutions: Evidence from Banks in Pakistan. International Journal of Financial Studies 6: 53. [Google Scholar] [CrossRef] [Green Version]

- Yurisandi, Try, and Evita Puspitasari. 2015. Financial quality reporting, before and after IFRS adoption using NiCE qualitative characteristics measurement. Procedia: Social and Behavioral Sciences 2: 644–52. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

| Qualitative Category | Definition | Criteria/Measures of the Category |

|---|---|---|

| General Quality (GQ) | The conceptual framework develops objectives and concepts that lead to high-quality accounting standards and financial accounting processes, which in turn also lead to high-quality financial reporting information that is useful for making decisions. | Q1: True and Fair Value, Q2: Decision Usefulness Q3: Transparency |

| Relevance (R) | Relevance refers to the existence of a close relationship between the financial accounting information and the objectives for which it was prepared. The relevance of that information to one or more decisions made by users is an indicator of usefulness. | R1: Predictive Value R2: Feedback Value R3: Timeliness R4: Frequency and Length |

| Understandability (U) | Understandability is the ability to know the comprehensive meaning of information. It is enhanced through proper classification as well as concise and clear presentation. It depends on the contents of financial statements and the presentation style as well as the background and abilities of users. | U1: Classification that is meaningful to users U2: Well-organized juxtaposition of data U3: Clear and sufficient notes U4: Presentations of net figures that users need |

| Reliability (RL) | Reliability is the characteristic that allows users to confidently depend on information. Reliability means that the method selected to measure and/or disclose its effects produces information that reflects the substance of the event. As per Sharia principles, estimates and judgments in applying accounting methods are not preferred. | B1: Representational Faithfulness B2: Neutrality B3: Substance and Form B4: Completeness B5: Verifiability B6: Consistency |

| Comparability (C) | Comparability allows users to identify similarities and differences among institutions and over a time horizon. | C1: Comparison of the current with previous financial periods C2: Comparison with other banks or industries C3: Analysis and explanation of the implications of changes C4: Presentation of ratios, index scores, or benchmarks |

| Prudence (P) | Prudence is needed under uncertainty to reflect the inclusion of a degree of caution in the exercise of the judgments needed in making the estimates, such that assets or income are not overstated and liabilities or expenses are not understated. | P1: Present reasonable information about uncertainties P2: Indicate bases of judgment P3: No hidden reserves or more provisions |

| R2 | Adjusted R2 | |

|---|---|---|

| Earnings Quality | 0.4982 | 0.4727 |

| Return on Assets | 0.1470 | 0.1400 |

| Return on Equity | 0.1849 | 0.1783 |

| Cronbach’s Alpha | Rho A | Composite Reliability | Average Variance Extracted (AVE) | |

|---|---|---|---|---|

| Comparability | 0.6844 | 0.7337 | 0.8121 | 0.5944 |

| General Quality | 0.7335 | 0.7560 | 0.8476 | 0.6500 |

| Prudence | 0.7402 | 0.7560 | 0.8496 | 0.6535 |

| Relevancy | 0.8257 | 0.8500 | 0.8839 | 0.6571 |

| Reliability | 0.8450 | 0.8567 | 0.8844 | 0.5620 |

| Understandability | 0.7232 | 0.7343 | 0.8422 | 0.6402 |

| Comparability | Earnings Quality | General Quality | Prudence | Relevancy | Reliability | Understandability | |

|---|---|---|---|---|---|---|---|

| Compatibility | 0.7710 | ||||||

| General Quality | 0.3736 | 0.5577 | 0.8063 | ||||

| Prudence | 0.6078 | 0.50067 | 0.4304 | 0.8084 | |||

| Relevancy | 0.3220 | 0.5481 | 0.6812 | 0.4699 | 0.8106 | ||

| Reliability | 0.4013 | 0.4965 | 0.4880 | 0.4835 | 0.3795 | 0.7497 | |

| Understandability | 0.0062 | 0.2731 | 0.3517 | 0.2367 | 0.287 | 0.1913 | 0.8001 |

| Compatibility | Earnings Quality | General Quality | Prudence | Relevancy | Reliability | Understandability | |

|---|---|---|---|---|---|---|---|

| Compatibility | |||||||

| General Quality | 0.5432 | 0.6310 | |||||

| Prudence | 0.8399 | 0.5625 | 0.5719 | ||||

| Relevancy | 0.4226 | 0.5916 | 0.8829 | 0.5952 | |||

| Reliability | 0.4886 | 0.5193 | 0.5982 | 0.6106 | 0.4501 | ||

| Understandability | 0.1084 | 0.3138 | 0.4797 | 0.3181 | 0.3914 | 0.2457 |

| Fit Summary | Saturated Model | Estimated Model |

|---|---|---|

| SRMR | 0.0841 | 0.1034 |

| d_ULS | 2.2982 | 3.4713 |

| d_G | 0.9547 | 1.1835 |

| Chi-Square | 638.7540 | 748.1588 |

| NFI | 0.6249 | 0.5606 |

| Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/STDEV|) | p-Value | Decision | |

|---|---|---|---|---|---|

| Comparability -> Earnings Quality | −0.2292 | 0.0965 | 2.9774 | 0.0029 | Supported |

| Earnings Quality -> Return on Assets | 0.3858 | 0.0527 | 7.2714 | 0.0039 | Supported |

| Earnings Quality -> Return on Equity | 0.4305 | 0.0749 | 5.7376 | 0.0017 | Supported |

| General Quality -> Earnings Quality | 0.2359 | 0.1124 | 2.2551 | 0.0242 | Supported |

| Prudence -> Earnings Quality | 0.3176 | 0.0909 | 3.8721 | 0.0001 | Supported |

| Relevancy -> Earnings Quality | 0.2214 | 0.1099 | 1.9439 | 0.0419 | Supported |

| Reliability -> Earnings Quality | 0.2369 | 0.0820 | 2.8975 | 0.0038 | Supported |

| Understandability -> Earnings Quality | 0.0158 | 0.0703 | 0.0625 | 0.9502 | Not Supported |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Elsiddig Ahmed, I. The Qualitative Characteristics of Accounting Information, Earnings Quality, and Islamic Banking Performance: Evidence from the Gulf Banking Sector. Int. J. Financial Stud. 2020, 8, 30. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs8020030

Elsiddig Ahmed I. The Qualitative Characteristics of Accounting Information, Earnings Quality, and Islamic Banking Performance: Evidence from the Gulf Banking Sector. International Journal of Financial Studies. 2020; 8(2):30. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs8020030

Chicago/Turabian StyleElsiddig Ahmed, Ibrahim. 2020. "The Qualitative Characteristics of Accounting Information, Earnings Quality, and Islamic Banking Performance: Evidence from the Gulf Banking Sector" International Journal of Financial Studies 8, no. 2: 30. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs8020030