Corporate Social Responsibility and Firm Value Protection

1

Doctoral School of Economics and Regional Sciences, Szent Istvan University, 2100 Gödöllő, Hungary

2

Faculty of Economics and Social Sciences, Szent Istvan University, 2100 Gödöllő, Hungary

*

Author to whom correspondence should be addressed.

Int. J. Financial Stud. 2020, 8(4), 72; https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs8040072

Submission received: 21 September 2020

/

Revised: 4 November 2020

/

Accepted: 5 November 2020

/

Published: 18 November 2020

(This article belongs to the Collection Corporate Social Responsibility in Finance)

Abstract

:The conception of Corporate Social Responsibility has continued to gain a lengthy discussion in all aspects of corporate finance with a particular focus on its contributing to financial performance. Despite its prominence globally, many companies have not embraced the concept, as most of them have remained doubtful about its contribution to corporate financial performance. Several companies have digressed the idea to merely an aspect of charity and cost instead of cost reduction and market creation. The fixed-effect model of panel data analysis was applied for the study period from 2010 to 2019 to measure relationships on CSR’s effect on the financial performance of listed companies in Kenya. The study used panel data for the years 2010–2019. The research used trend analysis for ten years to analyse data using canonical correlations, Logistic Regression analysis and ARIMA models to establish relationships among the variables of the study. Our results offer new evidence on the linearity effect of CSR on financial performance suggest that Corporate Social Responsibilities activities are very vital influencers of firm value, as they have a positive influence on the financial performance of companies.

1. Introduction

Corporate Social Responsibility (CSR) concept has received increasing attention among scholars. It is seen as a common thread of discourse by managers in corporate meetings around the world, as companies are seeking to escape the vindictive view that their actions lead to increased harmfulness in the world, both actual environmental toxicity and social toxicity manifesting itself as greed, misogyny and racism. By 2004, more than 50 per cent of Fortune 1000 businesses had released their CSR or Environmental, Social and Governance (ESG) reports detailing their investments and activities aimed at increasing their social responsibility impacts, and had also promised to publish such reports annually (Xie and Ward 2019).

A statement by KPMG in 2011 found that approximately 95% of the top 250 companies report their CSR accounts separately. Stakeholders get non-financial information as well in those CSR reports. Some of the non-financial information include investments in improving unessential environmental techniques, a company’s charitable donations and the proportion of female in leadership, among other details. With the growth in CSR disclosures, consumers currently have a better understanding of CSR activities published in the CSR reports. Consumers are slowly taking an active role in pushing corporations to undertake more socially-responsible activities and investments. Research reports published in 2015 established that 80 per cent of consumers reported that they could try a new product/brand in the market as long as it has a good CSR. Eighty-two per cent said that they would recommend a product to other consumers if the company supported social or environmental issues (Deepak and Deshpande 2015). Corporate Social Responsibility (CSR) concept has gained prominence among corporations. Companies that have fully adopted its tenets are classified as being financially sound. Publishing financial reports, the number of women in the board, the number of years the company has been in operation, charitable donations by the company and the proportion of females in leadership are examples of the various CRS components that have been of concern to companies. While studies have established that CSR engagement promotes financial performance, this research study tries to show how firms can utilise CSR disclosures to protect the firm value and corporate reputation, especially in instances involving adverse CSR events.

There has been discussion on the value-adding role of CSR and financial performance. In their study during the 2008–2009 financial crisis, (Lins et al. 2017) established that firms with higher social capital as a measure of CSR intensity had high stock returns that were four to seven percentage points higher than firms with low social capital. High-CSR firms also experienced higher profitability, growth and sales per employee relative to low-CSR firms, which raised more debt. Evidence from Studies suggests that building trust between the frim, investors and stakeholders pay off, especially when corporations are hit with adverse economic shocks. Early classical economists have argued that the sole objective of companies was to increase shareholders value. Many companies today, therefore, have focused all their attention on doubling their profits. Achieving the aim of profit maximisation, thus, should not result in adverse effects to the society, or to shareholders, as the society itself has a significant influence on attaining business economic goals. This research aimed to address the following two research questions:

- What is the relationship between CSR and financial performance of listed companies?

- What is the role of CSR in Building consumer brand loyalty in listed companies?

This article, therefore, attempts to evaluate Corporate Social Responsibility and Firm Value Protection. None of the studies came up with a model that appreciates the role of CSR in protecting the value of corporations. The study, therefore, sought to establish gaps and new knowledge that would be used to safeguard the interests of shareholders. The study used Board Size, Gender of the Board, Tobin’s Q, Leverage, Size, Market-to-Book Ratio, Dividend Payment, Corporate Social Responsibility Score and Environmental scores as predictor variables, while Return on Equity and Net Profit Margin would be the dependent variables. The remaining part of the paper is organised into Section 2, which presents the key research findings, and Section 3, a discussion of results and how they can be interpreted in the perspective of previous studies. The consequences of the research results are also discussed in broader context, and Section 4 discusses materials and methods, an empirical orientation of previous studies highlighting the critical gaps emanating from those studies.

2. Literature Review

Modern business is continually evolving due to new challenges and threats linked to the broader business climate, such as economic and political uncertainty, high competition in business, rapid technological advances, new migration problems, ageing as a social phenomenon, strong environmental concerns and ethical issues. CSR, therefore, forms an important area of concern to companies in order to remain competitive and relevant in the industry (Grubor et al. 2020).

CSR impact on the performance of companies depends on their size, regardless of their investment motive. CSR consequences are almost immediate in small businesses due to the shortened time between decision making and investment decisions. To determine the relationship between CSR investment decisions (Williams 2020) sampled 50 U.S.-based SME firms in the manufacturing sector. This study used stakeholder and social capital theories to construct a theoretical framework with a particular focus on social and environmental CSR. Findings revealed more significant effects of CSR on the financial performance of SMEs offering services than those dealing with manufacturing. Further, a significant negative association established between combined social and environmental CSR activities and financial performance. It is therefore paramount for the United States of America (USA) SMEs to consider focusing on financial performance or promoting firm value when adopting CSR investment decisions that are beneficial to the company and society at large.

In a similar study, (Su et al. 2020) investigated the effect of differential CSR dimensions on corporate financial performance (CFP) across sectors in 568 Chinese publicly traded firms from 2008–2017. Findings from the study showed that the bulk of the CSR environment has adverse effects on financial performance in capital-intensive manufacturing industries. Besides, the impact of Human Resource expenditure on CFP has a negative influence in the tertiary sector and resource-intensive manufacturing corporations. CSR investment, therefore, has a positive effect in resource-intensive industries and other secondary industries (mining, construction and utilities). Generally, many people think that firms earn more benefits by investing in business and financial stakeholders.

A study by (Berkman et al. 2020) showed that during the Global Financial Crisis (GFC) US firms with high levels of ratings in corporate social responsibility matters increased in value relative to firms with low CSR ratings. These raised questions about the internal and external validity of the inferences in their study. Conflicting results were established for a similar sample of US stocks, concluding that there was no evidence to support the fact that high CSR firms outperformed low CSR firms during the GFC when we used a calendar-time portfolio study that monitors the industry or used value-weighted portfolios. Generally, it was reported that the global financial and economic crisis had contributed much harm to public trust in institutions. The financial crisis underscored the prominence of faith for well-functioning markets and monetarist stability, but dialogues on the role of trust and, more generally, social capital in economic life are not new.

During the great recession, studies conducted by (Chintrakarn et al. 2020) on the independence of the board on CSR investments, independent directors were found to have an unfavourable view on CSR during the crisis. Studies have established that healthy board independence has the capability of leading a reduction in CSR activities. Increasing the board’s independence, therefore has a significant decrease in CSR activities of an enterprise. Several managers tend to over-invest in CSR activities during the crisis as compared to other times, which is not suitable for corporations. Investing in CSR activities during crisis time is motivated by managerial risk preference. CSR can therefore reduce a firm’s financial and performance risks substantially during crisis times, thereby strongly confirming risk mitigation.

In examining the role of capital structure as a mediating variable on CSR, stakeholders’ interest and financial performance, it has been established that CSR and stakeholder interest have both a direct and indirect impact on financial performance. These imply that firms screen out uncertain situations while making capital structure decisions and pursuing CSR-related activities. Evidence reveals the mediating effect of a capital structure in the relationship (Hunjra et al. 2020).

Much of the recent literature has tried to explore the relationship between corporate performance and corporate social responsibility (CSR) initiatives. They are using ROA, ROE and non-financial as constructs of financial performance. A positive relationship was established between CSR initiatives with financial and non-financial indicators. Findings also revealed that customers’ brand trust, customers’ brand loyalty, customer’s perception of quality, and customer satisfaction is positively correlated with non-financial corporate performance. Similar findings were reported in related studies conducted in Bangladesh, Pakistan and Lebanon. (Prieto et al. 2020) in their Ecuadorian study on banks perceived that banks as socially responsible entities invest resources in CSR events as a corporate governance policy to upsurge their financial and non-financial performance.

Research by (Wu et al. 2020) explored the impact of CSR and financial distress on corporate financial performance (CFP). A total of 1445 companies were selected from listed Chinese companies in the manufacturing industry. The study used a regression model, and the findings established that CSR has a significant positive impact on CFP, and the association is more noticeable for firms that are more unwavering. Additionally, it was confirmed that the relationship between CSR and CFP is also more robust in state-owned enterprises (SOEs).

Effectiveness of CSR disclosures in protecting corporate reputation is also an essential phenomenon of concern to researchers. Supported by the legitimacy theory, firms can signal their legitimacy via non-financial disclosure after the adverse effects of financial restatements. A study by (Zhang et al. 2020) supports the legitimacy theory which shows that restating firms make significant improvements to overall CSR disclosure eminence by fluctuating their reports to a more conservative tone, swelling readability and report length, even though they intentionally disclose less forward-thinking and sustainability-related content. Such improvements, therefore, are more pronounced in restating firms with prior low-quality CSR disclosure, yet CSR disclosure changes after restatements do not additionally improve analyst forecast accurateness. Matched with nondisclosures, restating firms with exposures in CSR suffer significant smaller losses in firm value. Overall, evidence has it that consistent CSR reporting alleviates reputational damage and plays an insurance-like or value protection role during crisis periods (Bastič et al. 2020).

The notion of CSR and financial performance has gained prominence in both public and private corporations. It has been an exciting area that has a direct influence on the financial soundness of companies. In their study, (Hashim et al. 2019) examined the relationship between corporate social responsibility and financial performance in the Association of Southeast Asian Nations (ASEAN), which is a regional intergovernmental organisation encompassing ten countries based in Southeast Asia. The ASEAN promotes intergovernmental cooperation and expedites economic, military, security, political, educational and socio-cultural integration among its members. Among the tenets of CSR were included community, corporate governance, employee relations and the environment. Meanwhile, financial performance is obtained by scrutinising the organisation’s ROA. The study helped build empirical evidence on the possible relationship between CSR and Financial Performance.

A study on the effect of the relationship between CSR performance and firms’ financial performance (Kim et al. 2019) selected a sample of 5040 large US companies. The main focus was to establish the relationship between CSR performance and firms’ financial performance. The study focused on verifying if firms had an assurance to benefit from CSR performance services. Theory suggests in instances where companies value firms using credible information, they then apply a lower discount. Findings revealed that CSR performance is positively associated with the financial performance of the firm. It is believed that CSR assurance services have a significant association with the financial performance of companies, denoting that firms having their CSR accounts assured by external experts experience much more incredible financial performance than firms deprived of such assurance services.

Corporate Social Responsibility is a valuable resource of value chain capabilities. It influences Customer Satisfaction, as well as Financial Performance. CSR demands the practice of social and environmental undertakings. These undertakings mainly concentrate on cultivating the relationships of a firm with its stakeholders, which comprises of shareholders, charitable and community organisations, employees, suppliers, customers and the environment.

Grounded on the traditional value chain model by Porter of the mid-1980s, research in the US and Asia Pacific on the aviation industry analysed the markets, and the findings from this research highlighted the prominence of cultivating and promoting CSR culture and governance to influence the performance of CSR positively. Enticements for managers to invest in CSR in the quest for sustainable performance is an important aspect that cannot be left out. There is a vital requisite for sustainable firm performance in the current environment, but this can only be accomplished where the approach is implanted in the fundamental business by CSR leaders who can apply the models of value creation through a robust CSR culture. Firms achieve sustainable performance, and eventually financial performance through the identification of value chain proficiencies such as CSRL and CSRC (Phillips et al. 2019).

Akben-Selcuk (2019) conducted a study in Turkey to reconnoitre the impact of CSR rendezvous on firm financial performance in a developing country. The focus was to investigate the controlling role of rights concentration in the CSR relationship and financial performance. The study involved non-financial public companies listed in Borsa Istanbul market between 2014 and 2018. Findings revealed a positive connection with financial performance. Ownership concentration played a negative moderating effect on the financial performance of companies even when endogeneity is controlled for.

A closely related study was conducted for the Egyptian stock market using panel data for 2014 to 2017. The purpose of the conducted research was to analyse the role of capital structure and its influence in CSR activities on the firm value. Seventeen companies were used for the study to establish the effect of financial leverage on the firm value with findings demonstrating that financial leverage had a significant influence on the corporate value of the firm. The results of the investigation established a significant effect of financial force on corporate value. Adopting CSR activities does not affect the corporate values, meaning that there is a lack of awareness of investors about the prominence of applying CSR activities in Egypt (Tarek 2019).

Many scholars have focused their studies on CSR and corporate financial performance, thus shedding light on the role of CSR in promoting the financial performance of a company. The authors recalculate ESG performance starting from economical, environmental, governance and social points of view. In a study by (Salvi et al. 2019) they used a Generalised Method of Moments approach (GMM) to tackle the extensively dubious indigeneity issues arising in their databases concerning CSR and CFP. The results aced a positive relationship between CSR, as measured in a tailored manner in this study, and corporate financial performance. Contributions from researchers have recognised the significance of the Board of Directors as an internal corporate governance mechanism which is seen as a control mechanism that plays a significant role.

According to studies, the effectiveness of CSR depends on several factors. The board size the independence of its members, the presence of specialised committees, especially the audit committee, gender diversity and board meetings. Memon et al. (2019) in their study aimed to explore the impact of Corporate Social Responsibility Reporting Index CSRRI on the financial performance of banks. Bank Performance was measured using ROA, EPS and PAT. Trend analysis used panel data for the years 2004 to 2017. CSRRI and bank size were the independent variables. Findings from a regression model revealed that the slope coefficient of intercept and CSRRI were positive except bank size, which is harmful in three models.

The research findings of the current study have shown that CSR reporting might provide welfare for both banks. Developed econometric models suggest that socially responsible banks can attract not only large numbers of customers, but also increase profitability. Inconsistent findings of CSR relationship with financial performance established by (Rao and Dhar 2019) is due to the complexity of the connection between two variables. The convolution of relationship stems from the nature of CSR, which is inseparable from its environment. This nature of association brings unfavourable impact on empirical research. The conclusion obtained from empirical evidence of such association will be exceedingly contextual and lack generality. It is, therefore, imperative that country characteristics govern the affinity of CSR practices, which influences the strength of the CSR relationship with firm value. The selection of CSR forms and measurements to be made is part of a company’s strategy to achieve legitimacy.

Obtaining empirical evidence about CSR, credit interest, and bank size on financial performance is very paramount. These prompted a study by (Bangun 2019) the effect of CSR, bank size and credit interest, on the financial performance of listed banks in the Indonesian Stock Exchange for the years 2015–2017. The study established that credit interest and corporate social responsibility had no significant influence on financial performance, while bank size had a significant positive effect on financial performance.

Dividend policy is also considered as one of the critical elements of CSR. Whether to pay dividends or not to stakeholders depends on the management view on the role played by CSR on financial performance. Several scholars have argued that payment of the dividend is essential, as it sends positive shock waves or shareholder. Shareholders always feel that companies that pay a premium are doing well financially. Companies that do not pay dividends are ever seen as worst-performing. Ullah and Bagh (2019), in their study, said that dividend policy was one of the most significant areas of research in corporate finance due to the consequence it has to all company stakeholders. Dividend policy is affected by many factors like Leverage, Profitability, Business Risk, Liquidity, Growth Opportunities and other micro and macro economy variables. Studying the Pakistanian Stock Exchange for the period 2011 to 2016, it was established that the profitability of the firm, leverage and liquidity are positively and significantly related to dividend payout. Further, it is claimed that increasing the profitability, liquidity and leverage of the firm ultimately increases dividend payment to the shareholder. Therefore, for the board of directors to consider increasing dividend payment to shareholders, they should carefully consider profitability, leverage, liquidity, growth opportunity and business risk.

To investigate the role of peer pressure on banks’ CSR activities and the long-term impacts of their CSR spending on financial performance, (Malik et al. 2019) found that the bank’s CSR expenditure increases significantly with that of its peer-banks. They, however, established that there is no association between a banks CSR expenditure and that of non-peer groups. Spending on CSR is compelled by tax incentive.

In another study on the Korean exchange market, (Cho et al. 2019) analysed whether a corporate social responsibility (CSR) has a systematic relationship with the financial performance and corporate financial performance. This study was conducted using 191 listed firms. The Korea Economic Justice Institute (KEJI) 2015 index was used to measure CSR performance. The firm value and profitability were used to measure corporate financial performance. Return on assets and Tobin’s Q were used as proxies for profitability and firm value, respectively. Using regression and correlation, the results from the study ratify that CSR performance has a partial positive correlation with firm value and profitability. These results are partly in tandem with findings from previous studies reporting, which established a positive correlation between CSR and the financial performance of the Korean firms’ using KEJI index before 2011. Between the variables under review, i.e., CSR performance and profitability, social contribution yielded a positive correlation. Correlation analysis between CSR performance and indicators of financial performance publicised a positive association between corporate soundness and social contribution and the growth rate of total assets. Both corporate resilience and social assistance showed a positive correlation with Tobin’s Q, the measure of corporate value.

According to (Rao and Dhar 2019), inconsistent results of CSR relationship and financial performance is brought about by the intricacy of the relationship between two variables. The relationship stems from the inseparability of CSR from its environment, which has an unfavourable impact on research. This research study proposed variables which contribute to the complexity of CSR and firms financial performance. The variables include country characteristics, as well as forms and dimensions. Country characteristics define the tendency of CSR practices, which finally influence the strength of CSR relationship with financial performance. The selection of CSR forms and measurements to be made is part of a company’s strategy to achieve legitimacy.

According to (Gangi et al. 2019), Corporate social responsibility is a practice of amassing knowledge and experience. In their paper, they aimed to find out how CSR knowledge affects the financial performance of the European banking industry using panel data from 72 European banks between 2009 to 2015. Using a two-stage Heckman model and fixed effects regression analysis findings revealed that the concept of absorptive knowledge capacity and the internal CSR of banks positively affects citizenship performance. Reputational effect of CSR and citizen performance are positive predictors of banks’ financial performances. Accrued internal CSR knowledge is a very significant factor in implementing effective CSR programs for external stakeholders. CSR engagement in external initiatives improves the competitiveness of the bank because of the relationship between citizenship performance, and reputation is positive.

Gangi et al. (2019) conducted a study in the European banking industry to investigate whether and how CSR knowledge affects financial performance. Seventy-two banks from 20 European countries were involved in the study for a period of seven years 2009 to 2015. Twofold research findings emanated from this research. First, consistent with the concept of absorptive knowledge capacity, the internal CSR of banks positively affects citizenship performance. Second, citizenship performance is a positive predictor of a bank’s financial performance in line with the reputational effect of CSR. From a knowledge-based perspective, accrued internal CSR knowledge plays a crucial role in executing operative CSR programs for stakeholders outside the company.

Additionally, this study demonstrates how CSR participation in external initiatives will boost the competitiveness of the bank due to the relationship between the success of citizenship and the positive image of the bank. The management of CSR initiatives may favour the sharing of knowledge and the creation of trust affiliations among internal and external stakeholders of the banks. CSR awareness contributes to stretched value creation for the bank as well as society. The CSR knowledge management perspective offers new acumens into business models sustainability of banks, thus contributing to the debate of modes of governance and their effects of CSR. Besides, the CSR perspective proposes additional opportunities for addressing the defies associated with sharing tacit knowledge within and outside of organisations.

Effective management of CSR activities favours knowledge sharing and creation of trust relationships among internal and external shareholders. The knowledge of CSR contributes to expanded value creation for the back, as well as the society which gives insights into the sustainability of the banks’ business model. CSR perspective offers superfluous opportunities for addressing the challenges associated with sharing tacit knowledge within and outside of organisations.

Studies have given considerable attention to establishing the impact of proactive corporate social responsibility on the financial performance of the firm. Grounded in the knowledge-based view (Sinthupundaja et al. 2019) (KBV), examined the significance of the causal combinations of knowledge-acquisition conditions on supporting the engagement of proactive CSR which is a complex precursor of the financial performance of a firm. Results indicate that neglecting any of internal capabilities and forms of external cooperation condition could lead to the low financial performance of the firm. Both internal capabilities and forms of external cooperation, therefore are very vital as they simultaneously support the engagement of proactive CSR.

Corporations practising CSR always benefit from increased stability compared to other index performance criteria (Fides 2018). To study the citizen perception of CSR activities on the performance of financial institutions in Bangladesh, (Mamun 2018) analysed 27 CSR activities in five major areas, (education, health, infrastructural, public awareness and socio-cultural). Citizens very clearly indicated that the health sector activities, infrastructural development and social awareness campaigns for CSR are more societal than profit-oriented. On the other hand, education-related activities to them are, to some extent, societal than profit-driven. Nevertheless, the socio-cultural events they perceive to be more profit-driven than societal. Overall, the citizens’ view regarding these CSR activities are not purely societal, but more societal than profit-oriented.

In their study, (Timbate and Park 2018) examined 500 US companies to establish the relationship between socially responsible firms and firms not embracing CSR, to maintain their financial reporting quality. Findings revealed that socially liable firms are less likely to manage their earnings. Firstly the researcher tried to establish whether firms with practical CSR activities were performing better than those who are not embracing CSR. Secondly was to confirm if the Market rewards companies are behaving responsibly to maintain their financial reporting quality. The study failed to demonstrate significant relationships between investors’ perceptions of earning and CSR. The perception making is measured by earnings response coefficient and stock returns. The findings from the study inferred that CSR activities are motivated by managers’ ethical incentives to serve the interests of stakeholders.

According to (Henriques and Sadorsky 2018), there is an emergent movement which has seen both individual investors and large institutions dissociate from oil companies and fossil fuel producers in general. This paper reconnoitres the inferences of doing so, by matching three portfolios: the first being a portfolio which includes fossil fuel producing companies and utilities, and secondly, a portfolio that swaps fossil fuel-generating companies and utilities with clean energy companies, and thirdly, a portfolio without fossil fuel producing companies, utilities, or pure energy companies. The findings revealed that portfolios divesting from fossil fuels and utilities and invest in clean energy outshine those with fossil fuels and utilities. We also found that risk-averse investors would be willing to pay a fee to make this switch, even when trading costs are included.

Given the modern unclear relational effect amid corporate financial performance and corporate social performance and the potentially myopic behaviour of managers, (Ruggiero and Cupertino 2018) have contributed immensely towards a better understanding of the association between corporate financial performance and corporate social performance. The study analysed the role of innovation activities as a mediator between corporate financial performance and corporate social performance. This study focused on the firms’ financial resources, innovation initiatives, and social and environmental performance. Results from the research demonstrate that innovation is a critical factor in the relationship between CFP and CSP. It empowers organisations to react to new social, economic and environmental factors faster and better than non-innovative organisations. Therefore, investment of financial resources in innovation initiatives is a significant lever to pursue to increase CSP.

A research was conducted to analyse the role of corporate strategy moderation in the influence of CSR performance on corporate financial performance. In the study, company strategy was measured by Product Differentiation, CSR was measured using the Global Reporting Association (GRI) index, while Return on Assets (ROA) was used to measure the financial performance. The research sampled listed mining companies in the Indonesia Stock Exchange (BEI) for the period 2016–2017. The study findings from established that performance of CSR does not show any significant influence to the company’s financial performance and the use of the company’s strategy as a moderator variable indicates that the company’s strategy variable turns out to moderate significantly on the impact of CSR performance on the financial performance of the company (Santoso 2018). In a closely related study, (Bollazzi and Risalvato 2018) conducted a study on the newly listed companies on the Italian Stock Exchange. The purpose of the scholarly work was to find out the importance of the Corporate Social Responsibility factor on the ROA for the period 2009 to 2015. The findings revealed that not all elements contribute to the improvement of performance in the newly listed companies, but it seems to have a greater ROA only the companies that take on responsibilities from an environmental perspective.

Debates on the role of CSR as a risk-reducing factor to the shareholders has gained prominence among scholars. In accordance to this studies shifted attention in testing the following; the purview specific CSR portfolios present pricing inconsistencies that could be captured by the introduction of risk factors accounting for exposition to stakeholder risk; secondly, this risk source is priced in the cross-section of stock returns. Due to these, we restrained in disentangling the contributions of different CSR realms in generating the pricing incongruities. Our findings show the presence of pricing variances related to CSR, the variant in numbers across all the territories under analysis. Specific CSR risk factors are thus not able to capture all pricing anomalies as they shrink their absolute value. Additionally, results from the study established that stakeholder risk is priced in the cross-section of returns and that such additional risk source presents different premiums for each domain (Becchetti et al. 2018).

The connection concerning CSR and corporate financial performance has been a subject of extensive empirical enquiry. The body of evidence has accumulated about the nature of the relationship as equivocal. A universally identified motive for the diverse and incongruous results is measurement issues relating to both notions of interest. Findings from several studies have shown that CSR operationalisations in empirical literature range from multidimensional to one-dimensional and that CSR measurement approaches include reputation indices, content analyses, questionnaire-based surveys and one-dimensional measures. In contrast, CFP measurement approaches include accounting-based measures, market-based measures and combined measures. Lastly, that CSR measurement approach is without shortcomings. In addition to method-specific downsides, two glitches inherent in most practices are researcher partiality and selection bias that might stimulate the nature of the CSR–CFP relationship detected in the empirical literature (Galant and Cadez 2017).

Yang and Baasandorj (2017) analyse the influence of CSR toward the financial performance of low-cost (LCC) and full-service air carriers (FSC). Using a fixed-effect model of panel data, they analysed data for the period between 2006 to 2015. In their findings, the research established that FSCs increase financial performance via environmental and social CSR activities compared to LCCs via increased firm size and environmental CSR activities. Besides, the study demonstrated that Firm age significant but negatively influences LCCs, whereas leverage shows significant mixed influence toward FSCs. CSR increases current and expected financial performances for FSCs and LCCs, respectively. FSCs and LCCs, with further environmental participation, could increase CSR scores and enhance financial performance.

Currently, there has been a developing demand for companies to strengthen their corporate social responsibility. It has become the obligation of syndicates to offer CSR activities of giving back to the society in which they operate and make huge profits. The unfortunate being that there is a wide gap in awareness between companies from developed countries and those nations that are developing.

Entities from developed countries have higher CSR levels of awareness. Besides, they do not face any exertion in disclosing their CSR activities relative to the companies in developing countries. It is also vital to ascertain if the level of CSR disclosure influences the performance of the company in terms of its return on asset (ROA) and firm value (Tobin’s Q). (Bt Abdul Wahab et al. 2017) developed a CSR disclosure index which he used to determine if the company’s performance is related to its contribution to the society. They established positive, negative and insignificant results between CSR activities on the company performance.

Sustainable growth can be a source of firm success and that CSR is a crucial tool for sustainable development. Scholars always ask a question on whether firms should capitalise on CSR without having assurance in the effects and methods of CSR. The study used R & D, CSR motivation and technology commercialisation as core competencies that enrich corporate performance through CSR from a normative stakeholder’s perspective. Strategic management factors, along with CSR motivations, may influence strategic and traditional CSR (Oh et al. 2017).

Similarly, passive involvement in CSR activities does not have any influence on tax avoidance. The scholars in their study established that asset turnover, the labour-to-equipment ratio, the net income-to-equity ratio the noncurrent liabilities ratio, and all have a positive and significant influence on corporate tax avoidance. The study established that there can be some voluntary method to reduce corporate tax avoidance in firms, and one of the most effective ways is by encouraging firms to engage in CSR activities.

Matuszak and Różańska (2017) conducted a twofold study. First was to investigate the trends of corporate CSR reporting and FP in Polish commercial banks. Secondly, this study examined the impact bank CSR disclosure on their financial performance using ROA, ROE and NIM. Annual financial reports were used for the years 2008 through to 2015 using a trend analysis for eight years. Two significant findings emanated from the study. CSR disclosures had a positive association with the ROA and ROE as measures of profitability. An inverse relationship was established between CSR and NIM. Besides, the study confirmed that banks’ CSR activities are not the dominant predictor of their profitability as compared with other control variables. The above research contributed immensely to the understanding of the relationship between disclosures in CSR and financial performance.

Researches in CSR and its influence on the financial performance of banks has heightened social and environmental concerns of the civil society which has compelled present-day managers to deviate away from the traditional viewpoints of business strategising that merely focuses on shareholder wealth maximisation. Whereas they are primarily tasked with ensuring sound returns on capital and long term economic growth of the firm, the demands of broader society to be socially and environmentally accountable are wielding enormous pressure on them which cannot be ignored. Several scholars have argued that trying to placate the contradictory stakeholder prospects can cause a dent in a firm’s financial performance. These, however, do not mean that the whole concept of CSR has to be left out for companies to maximise shareholder profit. It is therefore established that some companies have been found to create added value to the stakeholders’ wealth maximisation by incorporating responsible economic, environmental and social behaviour into organisations’ strategies. Their pre-emptive moves have abetted them to craft a reputational advantage in an exceedingly competitive industry, hence positively contributing to financial performance by skilfully exploiting the reputational advantage (Nair and Wahh 2017).

CSR is a desirable approach considering that it reduces risks, increases the brand value as well as improving transparency, and has a possible impact on a firm’s financial health. Recently India initiated as an act of philanthropy where it has become a mandatory part of the Companies Act mandating CSR spending. CSR disclosures are believed to lead to better financial performance and vice-versa. According to studies, it has been established that the profitability of companies has a cause and effect relationship with the CSR disclosure with the reverse also being true. These substantiated the theories envisaging that CSR can affect the financial performance of an entity (Gautam et al. 2016).

The idea of CSR has received global attention among many scholars interested in the study of financial performance. Past researchers investigated the relationship between CSR and corporate financial performance (CFP), and findings show varied results. It has been established that CSR is positively and significantly associated with financial performance represented by ROS, ROA and ROE. Socially responsible firm performance can be attached to achieving higher economic benefits, and hence the need for firms to recognise and instil CSR initiatives into their corporate culture and business operations since investment upsurges in CSR can lead to higher CFP while harmonising the needs of their inner and external stakeholders (Asfaw et al. 2016).

After China’s 30 years of rapid development, the country gained significant advances in economic growth at the expense of high environmental and social costs. Listed companies must fulfil their social obligations not only in order to meet the needs of stakeholders, but also in order to enhance management performance, create the right image, cultivate competitive advantage and realise sustainable development. For the reason that the influence of CSR in China is expanding gradually, there is a need to explore the relationship of listed companies in fulfilment of social obligations, information disclosure, and operational risk. Companies listed improving their social responsibilities fulfilment face significantly lower operational risks.

Second, listed companies publishing independent CSR reports face increased considerably operational risk. On the other hand, high-risk companies improving social responsibility fulfilment can substantially condense their operational risk, while publishing independent CSR reports, and this can lead to significantly increased operational risk.

Conventional accretion of raw scores of CSR and its interpreted impact the value of the firm have provided mixed evidence in the literature. Scholars have shown that the value impact of CSR activities relies heavily on the industry-specific relative position of the firm. Only firms that differentiate themselves from their peers are connected with increased firm value. Evidence concerns and portfolio construction can allude to a possible CSR clientele, suggesting the reality of an optimal CSR level (Ding et al. 2016).

The study of corporate social responsibility through its seven societal dimensions has enabled us to understand the guidelines relating to the ISO 26000 standard (Chakroun et al. 2019). However, it does not refer to human rights, fair operating conditions and consumer concerns, because there is no significant connection between these dimensions and financial performance. CSR research has grown exponentially in the last few decades. Nevertheless, significant debate remains about the association between CSR performance and corporate financial performance (CFP). Researches have established convergent result of CSR on financial performance. A similar study conducted in the US established conflicting findings with the one conducted in other western markets. Interesting findings have been established which are not consistent with similar studies using the US and other Western market data. A study by (Rutledge et al. 2014) in China established a significant negative relationship between CSR performance and CFP.

To investigate CSR impact on corporate financial performance (CFP) in Mongolian banks (Ho et al. 2019) collected data from 12 Mongolian banks for the years 2003 to 2012 to construct CSR disclosure index from 65 annual reports. The study established that banks with a duality of Chief Executive Officer as well as larger size unveil higher CSR performance. Besides, banks with higher CSR performance tend to have a lower non-performing loan and higher net interest margin and. Additionally, the CSR association varies before and after the economic crisis. The findings from the study provide meaningful insight to foreign investors regarding the effect of CSR on profitability and credit risk.

(Nkundabanyanga and Okwee 2011) researched to establish the relationship concerning CSR, managerial discretion, competences, learning and efficiency and perceived corporate financial performance in order to establish the legitimacy and value of CSR, taking managers’ perspectives in Uganda. Findings revealed that managerial description and competencies, learning and efficiency are significant forecasters of perceived corporate financial performance whereas CSR is not. Conversely, the results show serendipitously that CSR moderates managerial discretion’s predictive potential of perceived corporate performance. The limitation emanating from the study assented that, Corporate social responsibility concept is not well appreciated but only understood as philanthropic and not viewed as a means for improved financial performance.

Businesses have faced mounting pressures over the last several decades from diverse stakeholders to amend their CSR operations to become more socially and environmentally responsible. Many firms appear to have reacted by adopting more sustainable practices of measuring, documenting and publishing annual CSR reports to showcase ways in which they are addressing critical issues in this area. Research in this purview has not yet analytically scrutinised whether businesses in totality have changed their practices in line with the essential vicissitudes in their institutional context over time. Businesses have become more, not less, irresponsible concerning CSR activities (Mazutis 2018).

To study the empiric literature on corporate social success (Wood and Jones 2016) focused their studies on attempting to associate corporate social with financial performance. Most studies correlate measures of business performance that as yet have no hypothetical relationship. Empirical CSP literature mismatches variables in terms of which stakeholders are relevant to which kind of measure. Second, only the studies using market-based variables and theory show a consistent relationship between social and financial performance, particularly those showing a negative abnormal return to the stock price of companies experiencing product recalls. Even though this paper shows that the CSP build is not yet all around sufficiently determined to create more grounded outcomes, ongoing exploration recommends that much advancement is being made both observationally and hypothetically in creating legitimate and trustworthy proportions of corporate social execution.

Corporate Social Responsibility (CSR) concept is concerned with balancing social, environmental and economic issues in the operations of firms and dealing or relating ethically with corporate stakeholders (Branco and Rodrigues 2016). These imply that businesses should be committed to social, economic and environmental practices as well as ethically relate with their stakeholders (Usman and Amran 2015). With this, a nascent number of top corporate managers and academics has apportioned a significant amount of resources and time to CSR practices. A UN Global Compact-Accenture CEO study in 2010 revealed that ninety-three per cent of 766 CEOs who participated in the study globally considered the concept of CSR as necessary’ or ‘very important’ element for the sustainability of their corporations. The argument is that the sustainability of firms is dependent on how effective firms respond to and manage their relationships with society. However, the success of this relationship is contingent on trust, and trust is shaped by attending and exceeding responsibilities to society (Agyemang and Ansong 2016).

3. Research Methodology and Design

The study used panel data for listed companies in the Nairobi and Securities exchange market for the year 2010 to 2019. The study conducted a ten-year trend analysis. The study used canonical correlations, Logistic Regression analysis and ARIMA models to establish relationships from the study. Sample distribution of the companies based on the industry are as shown below.

Regression Model

where,

ROEit = αo + β1 BOSit + β2 GOBit + β3 TNQit + β4 LEVit + β5 LogAit + β6 MTBit + β7 DIPit +

β8 CSRit + β9 ENVit + ϵit

β8 CSRit + β9 ENVit + ϵit

NPMit = αo + β1 BOSit + β2 GOBit + β3 TNQit + β4 LEVit + β5 LogAit + β6 MTBit + β7 DIPit +

β8 CSRit + β9 ENVit + ϵit

β8 CSRit + β9 ENVit + ϵit

BOSit = Board Size

GOBit = Gender of the Board

TOQit = Tobin’s Q

LEVit = Leverage

LogAit = Size

MTBit = market-to-book ratio

DIPit = Dividend Payment

CSRit = Corporate Social Responsibility Score

ENVit = environmental scores

ROEit = Return on Equity

NPMit = Net Profit Margin

ϵit = Error term of in year t.

The study used environmental scores to measure the CSR scores. Besides other CSR indicators were also used (Board Size, Gender of the Board. Companies that did not have the CSR index in their financial reports were excluded from the study.

4. Results and Discussion

4.1. Canonical Correlations

According to Table 1 below, Board Size, Gender of the board, Assets and Corporate Social Responsibility have significant strong positive correlations with Net Profit Margin with r = 0.457 p-Value = 0.000, r = 0.641 and p-Value = 0.000, r = 0.776 and p-Value = 0.000 r = 0.545 and p-Value = 0.010 respectively. All the p-Value were below 0.05; hence, the correlation was significant. Tobin’s Q, Market to Book, Dividend Payout, Environmental Score are positively correlated to Net Profit Margin with r = 0.012, r = 0.218, r = 0.318 and the corresponding p-value = 0.903, 0.022, 0.001 and 0.110, respectively. The relationship between Tobin’s q and NPM was not significant. Leverage has a significant inverse relationship with NPM.

Using ROE as a dependent variable, CSR and Board Size established significant positive correlations r = 0.469 with p-Value and r = 0.208 with p-Value = 0.029. Gender of the board, Assets, Market to Book Ratio, Dividend Payout and Environmental Scores have a positive but insignificant relationship with ROE. The correlations were insignificant since all the p-value for the variables were above 0.05. Tobin’s and Leverage have an inverse and insignificant relationship based on the p-value of 0.045. The study, therefore, established that CSR activities have a significant and positive influence on the financial performance of companies.

4.2. Regression Analysis (ROE)

Regression model findings from Table 2, revealed a correlation of 0.847 between the observed and predicted values of the dependent variable, which is a strong positive correlation. On the other hand, according to the research, 71.8% of the variance in the regression model is accounted for by the Board Size, Gender of Board, Tobin’s Q, Leverage, Log of Assets, Market to Book Ratio, Dividend Payout, Corporate Social Responsibility Score, Environmental Scores. Other external variables bring about 28.2% of the variation. The closely related values of R-Square and Adjusted R Square shows that the regression model can be used to make inferences. The Durbin-Watson statistic is 1.507, which is between 1.5 and 2.5, and therefore the data are not autocorrelated. The regression model coefficient results were presented as shown in Table 3 below.

According to Table 3, all the variance inflation factors (VIF) were below 5. Therefore, multicollinearity did not affect our regression analysis. CSR and GOB had a significantly higher positive correlation with ROE (r = 0.768 p-Value = 0.004 and r = 0.643, p-Value = 0.043 respectively) BOS, TOBNQ, MTB had positive correlations. However, the relationship was not significant based on the p Values above 0.05. LEV, Assets (Log of Assets) and DIP had an insignificant inverse relationship with ROE. The regression model therefore for this study can be stated as;

ROEit = 2.677 + 0.293BOSit + 0.643GOBit − 0.068TNQit + 0.010LEVit − 0.059LogAit + 0.001MTBit − 0.001DIPit +

0.768CSRit + 0.126ENVit + ϵit

0.768CSRit + 0.126ENVit + ϵit

4.3. Regression (NPM)

Based on the Table 4 above, 91.8% of the variance in the regression model is brought about by Board Size, Gender of Board, Tobin’s Q, Leverage, Log of Assets, Market to Book Ratio, Dividend Payout, Corporate Social Responsibility Score, Environmental Scores. 8.2% of the variance is by other external variables outside the study. The variables under study are an excellent measure to establish the relationship between the variables and firm value. The closely related values of R Square and Adjusted R Square means that the regression model was accurate and can be relied upon to make conclusive inferences for the study. Regression coefficients were as shown in Table 5 below.

All the VIF values were below 5. Therefore, the regression model was not affected by multicollinearity. GOB, CSR, BOS and DIP have significant positive correlations with NPM. Assets have a positive correlation, but the relationship is not significant. Besides, TOBNQ, and MTB have very week and non-significant correlations. The regression model for the study was stated as shown below

NPMit = 2.449 + 0.443BOSit + 0.723GOBit − 0.281TNQit + 0.016LEVit + 0.0637LogAit + 0.052MTBit +

0.214DIPit + 0.594CSR it + 0.019ENVit + ϵit

0.214DIPit + 0.594CSR it + 0.019ENVit + ϵit

The standardised residual from the regression analysis was as shown in the Table 2.

NPM is a good measure of financial performance. From the findings above, the data set was normally distributed based on the above histogram in Figure 2.

4.4. Auto-Regressive Moving Average (ARIMA) Model

Time Series Modeler

The ARIMA value of (0,0,0) from Table 6 means that an ordinary regression moulded the model description. The model fit was presented as shown in Table 7 below.

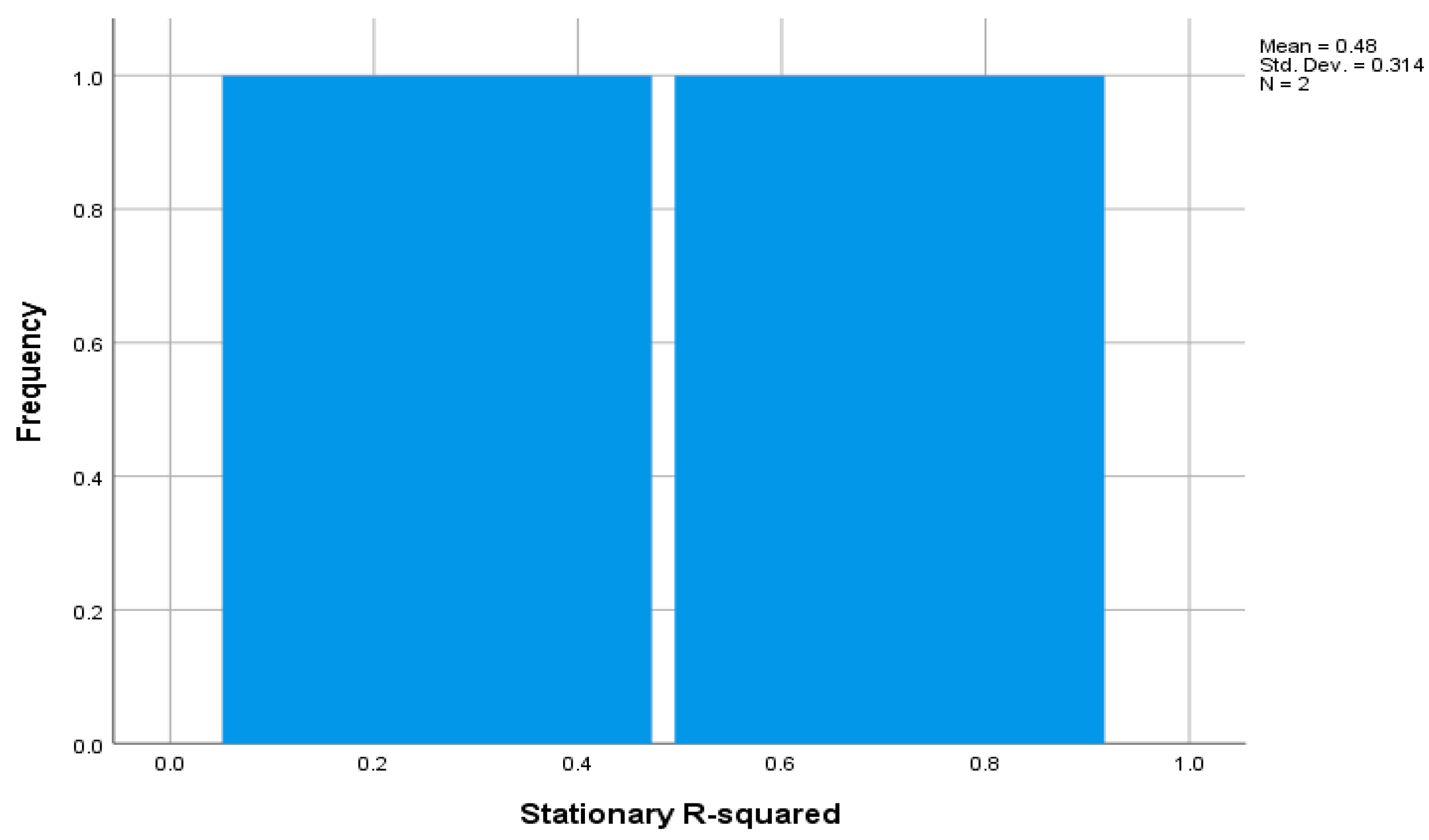

According to Table 7, the Stationary R- Squared of +ve 0.849 means that the model under consideration is better than the baseline model. R squared shows the proportion of the total variation in the series that is explained by the model. The results showed that 84.9% of the variance on the dependent variable is accounted for by independent variables. The Root Mean Square Error (RMSE) of 14.9% measures how much ROE and NPM vary from its model-predicted level, expressed in the same units as the dependent series. Therefore, the model varies by 14.9%

From the table above, Mean Absolute Percentage Error (MAPE) as a measure of prediction accuracy of forecasting established as 34.38 while with a Maximum Absolute Percentage Error (MAXAPE) is a measure useful for imagining a worst-case scenario for your forecasts. In this case, findings established a value of 12.07, which is good forecasting. On the other hand, the MAE is a measure of how much the series varies from its model-predicted level. In this case, a variance of 9.2%, which is not bad.

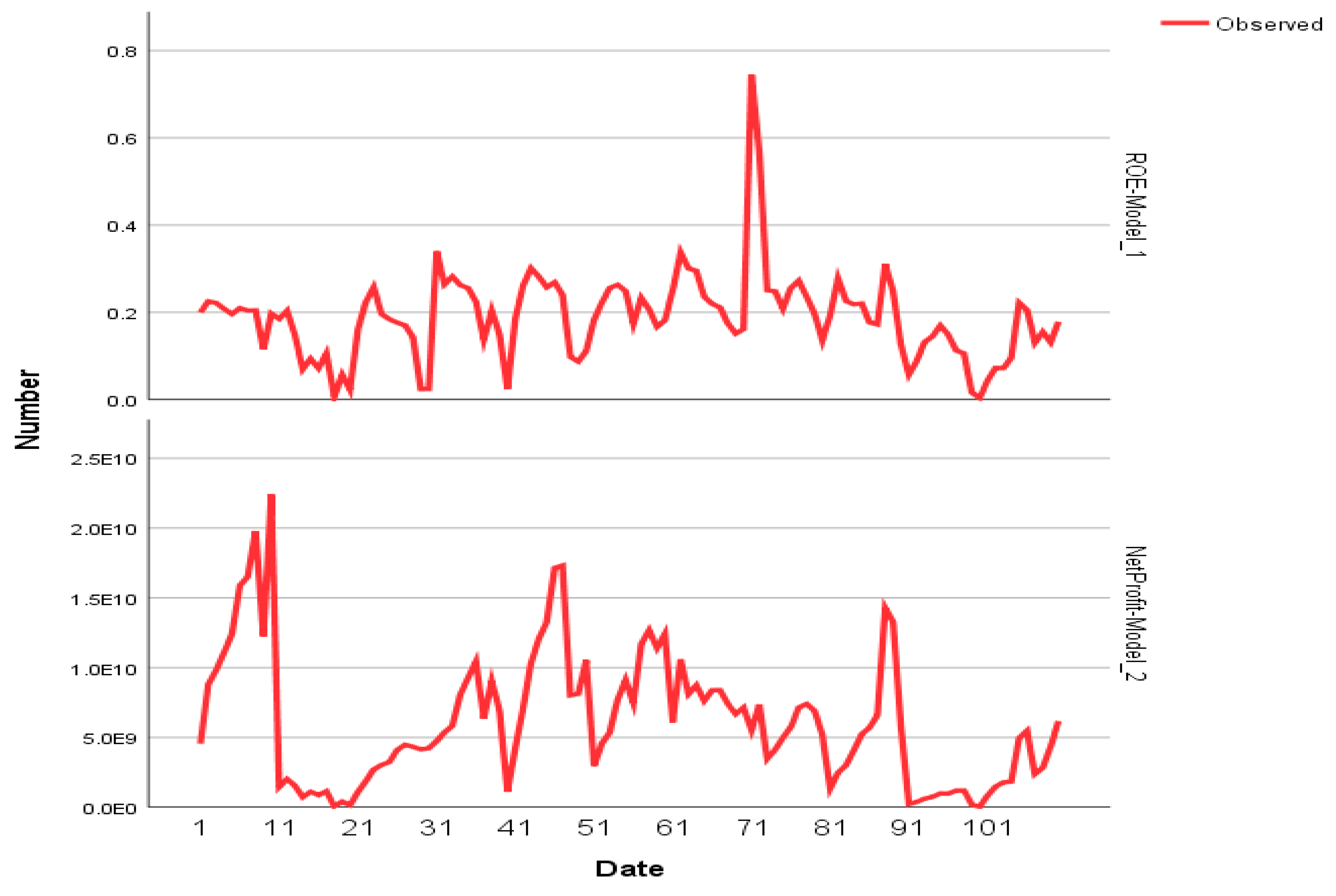

According to Table 8 below, Net profit is the best estimator of financial performance since it contributes 70.6%. The higher the Model Statistics Stationary R-Squared, the better. p-Value of 0.06 is below 0.05 hence a significant modeller. ROE has a small value hence not a good predictor of financial performance in the study. The p-Value of 0.00 in ROE is also significant for the study. Both models are statistically significant with p-Values of 0.000 and 0.006. The summary is captured in the residual volatility graph shown below.

The above plots in Figure 3 show the volatility of the residual and the error term in time (t). The results show the non-constant conditional variance of errors. The Residual ACF and PACF were also presented as shown in the figures below.

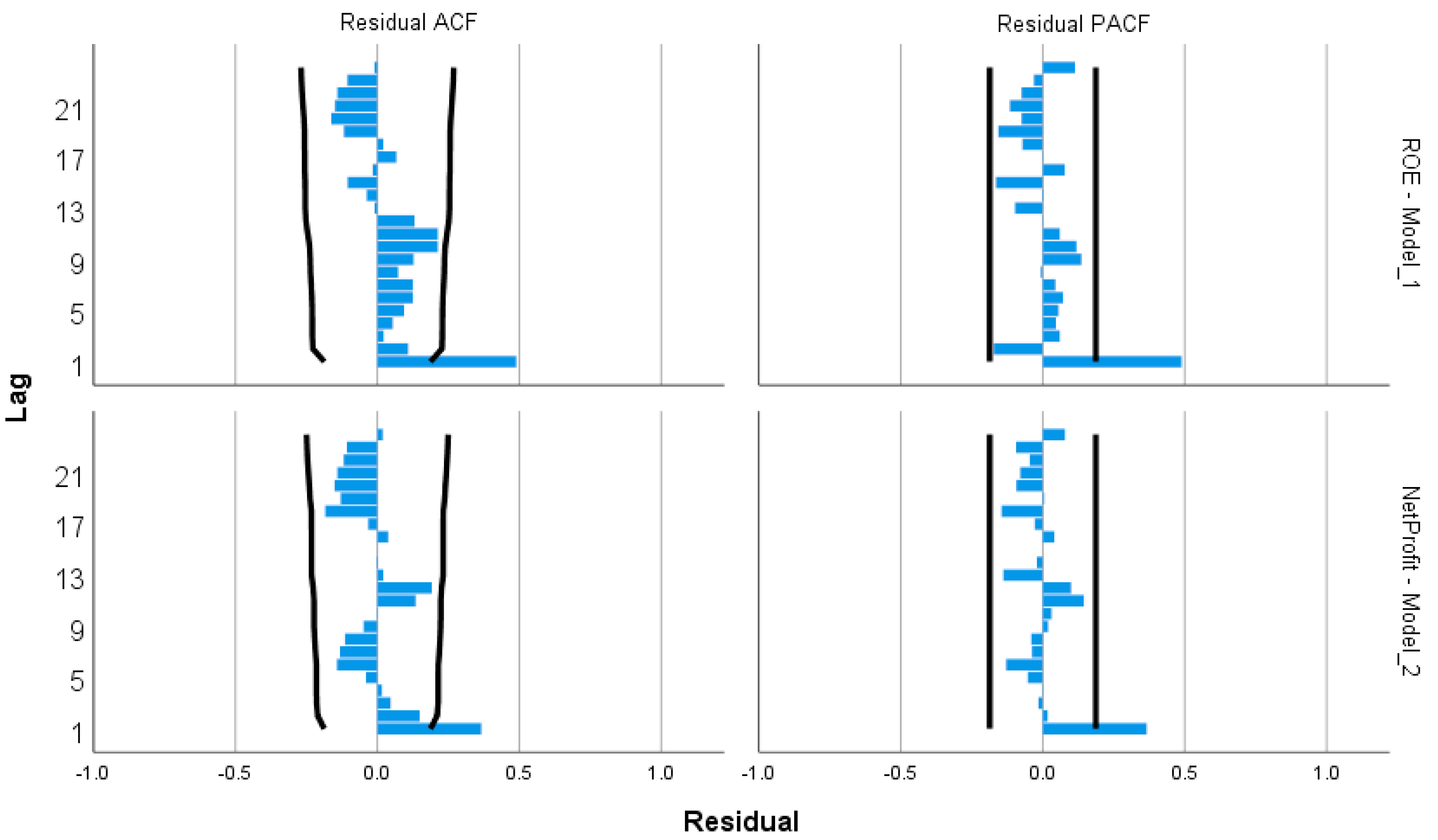

The plots in Figure 4 above show the residual square o the first estimates. Results suggest that there is autocorrelation on the squares of the residuals. The model summaries were shown in the Appendix A as Figure A1 and Figure A2.

There is a wide-ranging discussion on the validity and importance of a socially responsible company. CSR ranges from publishing financial reports for external stakeholders, and having both genders on the board, expanding the board of directors to have shareholders’ effective representation on the board, among others. There are no generally acceptable and fixed measures of CSR activities in a corporation, but rather a combination of many variables and factors. Several individuals always feel that maximisation of the shareholders should be the sole goal of a corporation. Several certain benefits to business have been identified as being socially responsible for addressing the issue of CSR concerning financial performance. Using 10-year data from listed companies in the Nairobi Securities and Exchange, the study conducted a trend analysis to establish relationships over time between 2010 to 2019. Results from the study, therefore, established that CSR activities have a significant and positive influence on the financial performance of companies supporting the findings of (Su et al. 2020; Hunjra et al. 2020; Cho et al. 2020; Benlemlih et al. 2020; Prieto et al. 2020; Kim et al. 2019; Bastič et al. 2020; Hashim et al. 2019). A firm with CSR exposure suffers significantly less in the value of the firm. The reverse is true.

Voluntary non-financial CSR disclosures have a contribution on how the market reacts to especially in terms of stock prices. It is therefore imperative to establish if the degree of a firm’s conservatism in financial reporting is associated with its empirical and theoretical studies. Consequently, the degree of reporting the financial statements is dependent on voluntary disclosures and the credibility of the financial statements. When interpreting CSR disclosures, stakeholders need to consider a firm’s financial reporting policies. The reaction of the market to a firm’s CSR disclosure is reduced when its financial reporting is more conservative. Studies have found out that firms that adopt conventional financial reporting are less likely to disclose CSR information, and furthermore, that the quality and quantity of CSR disclosures are associated with the degree of accounting conservatism (Cho et al. 2020).

Finally the Table 9 shows company distribution by the industries in which they are operate.

The companies included in the study were distributed among 13 sectors as shown in the Table 9 above.

5. Conclusions

The concept of CSR has received very little attention from companies due to the failure of many companies in establishing the financial implication on the firm value of companies that adopt it. This research has evaluated several previous studies which have been conducted to establish the value of CSR on company success. Successful adoption of CSR by companies has tremendous positive results on the financial performance of the company, as well as building customer confidence. The ranking of companies in terms of financial performance saw most Hitech companies high on the list with Microsoft being top on the list, followed by NVIDIA Corp, Apple Inc. and Intel Corp, among others. It was established that the above companies are highly involved in CSR activities, which may have led to increased firm value. It is important to remember that CSR companies such as Microsoft also provide a healthy working environment, and so therefore if ownership is broadened, then most owners and firms will opt to maximise long-term value for business.

Therefore, findings from this study have helped a lot in building a case for the role of CSR in value protection of listed companies in the NSE. Based on the data from listed companies between 2010–2019, the study chose Board Size, Gender of the Board, Tobin’s Q, Leverage, Size, market-to-book, ratio, Dividend Payment, Corporate Social Responsibility Score and environmental scores as variables of concern for the study. From this study, it can be concluded that firms which are facing stock market undervaluation are more likely to release CSR news, and the effect is resolute in firms with low CSR commitment and low stock price informativeness. Evidence from studies suggests that the stock market reacts positively to CSR news released by undervalued firms, and more so for undervalued firms with high information asymmetry. Financially strong businesses can continue to invest in ways that have a longer-term strategic impact, such as delivering services to the community and its workers. Such allocations could be strategically connected to a more robust public image and enhanced ties with the government, as well as an improved ability to recruit more professional employees.

It has been established that CSR consequences are almost immediate in small businesses due to the shortened time between decision making and investment decisions. On the other hand, companies with financial problems usually allocate their resources in projects with a shorter horizon. Other arguments propose that financial performance also depends on good or socially responsible performance. Socially responsible corporations also have less risk of rare negative events. Companies that adopt the CSR principles are more transparent and have less risk of bribery and corruption. The findings indicate that CSR is positively related to better financial performance and this relationship is statistically significant, supporting, therefore, the view that socially responsible corporate performance can be associated with a series of bottom-line benefits. This study is, therefore, in line with the risk mitigation hypothesis, therefore supporting CSR activities because they are believed significantly lower the risk of a corporation. This study, therefore, contributes immensely to literature in the field of financial economics and management. Shareholders, managers, executives, investors, as well as regulators, will find this article very helpful.

Author Contributions

All the authors participated actively throughout the main document. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

Special acknowledgement to the Tempus Public Foundation for the PhD scholarship to study in Hungary. Special thanks also to all faculty lecturers, as well as other staff of the Szent Istvan University.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Figure A1.

Model Summary Chart 1.

Figure A2.

Model Summary Chart 2.

References

- Agyemang, Otuo Serebour, and Agyemang Abraham Ansong. 2016. Journal of Global Responsibility. Journal of Global Responsibility Social Responsibility Journal Social Responsibility Journal 8: 47–62. [Google Scholar] [CrossRef]

- Akben-Selcuk, Elif. 2019. Corporate social responsibility and financial performance: The moderating role of ownership concentration in Turkey. Sustainability 11: 3643. [Google Scholar] [CrossRef] [Green Version]

- Asfaw, Yitbarek Asfaw Abrha, Araya Hagos Gebreegziabher, and Hiwot Kebede Aregawi. 2016. Examining the Relationship between Corporate Social Responsibility and Financial Performance of Manufacturing Companies in Tigray Regional State, Ethiopia. Ethiopian Journal of Business and Economics 5: 214. [Google Scholar] [CrossRef] [Green Version]

- Bangun, Nurainun. 2019. The Effect of CSR; Credit Interest; and Bank Size on Financial Performance. Jurnal Akuntansi 23: 177. [Google Scholar] [CrossRef] [Green Version]

- Bastič, Majda, Matjaz Mulej, and Mira Zore. 2020. CSR and Financial Performance—Linked by Innovative Activities. Naše Gospodarstvo/Our Economy 66: 1–14. [Google Scholar] [CrossRef]

- Becchetti, Leonardo, Rocco Ciciretti, and Ambrogio Dalò. 2018. Fishing Corporate Social Responsibility risk factors. Journal of Financial Stability 37: 25–48. [Google Scholar] [CrossRef]

- Benlemlih, Mohammed, Jingwen Ge, and Sujiao Emma Zhao. 2020. Undervaluation and Non-Financial Disclosure: Evidence from Voluntary CSR News Releases. SSRN Electronic Journal, 1–49. [Google Scholar] [CrossRef]

- Berkman, Henk, Michelle Li, and Hellen Lu. 2020. Trust and the Value of CSR during the Global Financial Crisis. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Bollazzi, Francesco, and Giuseppe Risalvato. 2018. Corporate responsibility and ROA: Evidence from the Italian stock exchange. Asian Economic and Financial Review 8: 565–70. [Google Scholar] [CrossRef]

- Branco, Manuel, and Lucia Rodrigues. 2016. Corporate social responsibility and resource-based perspectives. Journal of Business Ethics 69: 111–32. [Google Scholar] [CrossRef]

- Bt Abdul Wahab, Norwazli, Noryati Bt Ahmad, and Haslinda Bt Yusoff. 2017. CSR Inflections: An Overview of CSR Practices on Financial Performance by Public Listed Companies in Malaysia. In SHS Web of Conferences. Shah Alam: Universiti Technology of MARA. [Google Scholar] [CrossRef] [Green Version]

- Chakroun, Salma, Bassem Salhi, Anis Ben Amar, and Anis Jarboui. 2019. The impact of ISO 26000 social responsibility standard adoption on firm financial performance: Evidence from France. Management Research Review 43: 545–71. [Google Scholar] [CrossRef]

- Chintrakarn, Pandej, Pornsit Jiraporn, and Sirimon Treepongkaruna. 2020. How do independent directors view corporate social responsibility (CSR) during a stressful time? Evidence from the financial crisis. International Review of Economics & Finance. [Google Scholar] [CrossRef]

- Cho, Sang Jun, Chune Young Chung, and Jason Young. 2019. Study on the relationship between CSR and financial performance. Sustainability 11: 343. [Google Scholar] [CrossRef] [Green Version]

- Cho, Soung Young, Pyung Kyung Kang, Cheol Lee, and Cheong Park. 2020. Financial reporting conservatism and voluntary CSR disclosure. Accounting Horizons 34: 63–82. [Google Scholar] [CrossRef]

- Deepak, Padmanabhan, and Prasad Manikarao Deshpande. 2015. The road ahead. In SpringerBriefs in Computer Science. New York: Springer, pp. 105–13. [Google Scholar]

- Ding, Ding, Christo Ferreira, and Udomsak Wongchoti. 2016. Does it pay to be different? Relative CSR and its impact on firm value. International Review of Financial Analysis 47: 86–98. [Google Scholar] [CrossRef]

- Fides, Elizabeth. 2018. Corporate Social Responsibility and Financial Performance: An Examination of the Dow Jones Sustainability North American Index. Applied Economics Theses. Available online: http://digitalcommons.buffalostate.edu/economics_theses/33 (accessed on 4 November 2020).

- Galant, Adriana, and Simon Cadez. 2017. Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research-Ekonomska Istrazivanja 30: 676–93. [Google Scholar] [CrossRef]

- Gangi, Francesco, Mario Mustilli, and Nicola Varrone. 2019. The impact of corporate social responsibility (CSR) knowledge on corporate financial performance: Evidence from the European banking industry. Journal of Knowledge Management 23: 110–34. [Google Scholar] [CrossRef]

- Gautam, Richa, Anju Singh, and Debraj Bhowmick. 2016. Demystifying relationship between Corporate Social Responsibility (CSR) and financial performance: An Indian business perspective. Independent Journal of Management & Production 7: 1034–62. [Google Scholar] [CrossRef] [Green Version]

- Grubor, Aleksandar, Nemanja Berber, Marko Aleksi, and Radmila Bjeki. 2020. The Influence of Corporate Social Responsibility on Organisational Performance: The Mediating Role of Market Orientation. The Annals of the Faculty of Economics in Subotica 56: 3–13. [Google Scholar] [CrossRef]

- Hashim, Fathyah, Essia Ahmad Ries, and Ng Teck Huai. 2019. Corporate Social Responsibility and Financial Performance: The Case of ASEAN Telecommunications Companies. KnE Social Sciences 2019: 892–913. [Google Scholar] [CrossRef]

- Henriques, Irene, and Perry Sadorsky. 2018. Investor implications of divesting from fossil fuels. Global Finance Journal 38: 30–44. [Google Scholar] [CrossRef]

- Ho, Amy Yueh-Fang, Hsin-Yu Liang, and Tumurbaatar Tumurbaatar. 2019. The Impact of Corporate Social Responsibility on Financial Performance: Evidence from Commercial Banks in Mongolia. Advances in Pacific Basin Business, Economics and Finance 7: 109–53. [Google Scholar] [CrossRef]

- Hunjra, Ahmed Imran, Peter Verhoeven, and Qasim Zureigat. 2020. Capital Structure as a Mediating Factor in the Relationship between Uncertainty, CSR, Stakeholder Interest and Financial Performance. Journal of Risk and Financial Management 13: 117. [Google Scholar] [CrossRef]

- Kim, Jintae, Kangho Cho, and Cheong Park. 2019. Does CSR assurance affect the relationship between CSR performance and financial performance? Sustainability 11: 5682. [Google Scholar] [CrossRef] [Green Version]

- Lins, Karl, Henri Servaes, and Ane Tamayo. 2017. Social Capital, Trust, and Firm Performance: The Value of Corporate Social Responsibility during the Financial Crisis. Journal of Finance 72: 1785–824. [Google Scholar] [CrossRef] [Green Version]

- Malik, Mahfuja, Md Al Mamun, and Abu Amin. 2019. Peer pressure, CSR spending, and long-term financial performance. Asia-Pacific Journal of Accounting and Economics 26: 241–60. [Google Scholar] [CrossRef]

- Mamun, Muhammad. 2018. Citizens’ Perspective of Corporate Social Responsibility (CSR) Activities by the Financial Institutions of Bangladesh: Are They Societal or Promotional? International Review of Financial Consumers 3: 9–28. [Google Scholar] [CrossRef]

- Matuszak, Łukasz, and Ewa Różańska. 2017. An examination of the relationship between CSR disclosure and financial performance: The case of Polish banks. Journal of Accounting and Management Information Systems 16: 522–33. [Google Scholar] [CrossRef]

- Mazutis, Diana. 2018. Much Ado about Nothing: The Glacial Pace of CSR Implementation in Practice. Corporate Social Responsibility 2: 177–243. [Google Scholar] [CrossRef]

- Memon, Sundas, Waqar Sethar, Adnan Pitafi, and Wasim Uddin. 2019. Impact of CSR on Financial Performance of Banks: A Case Study. Journal of Accounting and Finance in Emerging Economies 5: 129–40. [Google Scholar] [CrossRef] [Green Version]

- Nair, Praveen Balakrishnan, and Ricky Wong Baah Wahh. 2017. Strategic CSR, reputational advantage and financial performance: A framework and case example. World Review of Science, Technology and Sustainable Development 13: 37–55. [Google Scholar] [CrossRef]

- Nkundabanyanga, Stephen, and Alfred Okwee. 2011. Institutionalising corporate social responsibility (CSR) in Uganda: Does it matter? Social Responsibility Journal 7: 665–80. [Google Scholar] [CrossRef]

- Oh, Seungwoo, Ahreum Hong, and Junseok Hwang. 2017. An analysis of CSR on firm financial performance in stakeholder perspectives. Sustainability 9: 1023. [Google Scholar] [CrossRef] [Green Version]

- Phillips, Schavana, Vinh Thai, and Zaheed Halim. 2019. Airline Value Chain Capabilities and CSR Performance: The Connection Between CSR Leadership and CSR Culture with CSR Performance, Customer Satisfaction and Financial Performance. Asian Journal of Shipping and Logistics 35: 30–40. [Google Scholar] [CrossRef]

- Prieto, Ana Belen Tulcanaza, Hokyun Shin, Younghwan Lee, and Chang Lee. 2020. The relationship among CSR initiatives and financial and non-financial corporate performance in the Ecuadorian banking environment. Sustainability 12: 1621. [Google Scholar] [CrossRef] [Green Version]

- Rao, Chalapati, and Biswajit Dhar. 2019. Book Review of India’s Recent Inward Foreign Direct Investment: An Book Review of India’s Recent Inward Foreign Direct Investment. Emerging Markets Journal 7: 2018–20. [Google Scholar] [CrossRef]

- Ruggiero, Pasquale, and Sebastiano Cupertino. 2018. CSR strategic approach, financial resources and corporate social performance: The mediating effect of innovation. Sustainability 5: 122. [Google Scholar] [CrossRef] [Green Version]

- Rutledge, Robert, Khondkar Karim, Mark Aleksanyan, and Chenlong Wu. 1108. Responsibility and Financial Performance: The Case of Chinese State-Owned Enterprises. Accounting for the Environment: More Talk and Little Progress 5: 23–47. [Google Scholar]

- Salvi, Antonia, Emanuele Doronzo, Anastasia Giakoumelou, and Felice Petruzzella. 2019. CSR and Corporate Financial Performance: An Inter-Sectorial Analysis. International Journal of Business and Management 14: 193. [Google Scholar] [CrossRef] [Green Version]

- Santoso, Budi. 2018. Influence of Moderation of Company Strategy on Csr Disclosures and Financial Performance Mining Company in Indonesia. International Journal of Social Science and Business 2: 93–100. [Google Scholar] [CrossRef]

- Sinthupundaja, Janthorn, Navee Chiadamrong, and Youji Kohda. 2019. Internal capabilities, external cooperation and proactive CSR on financial performance. Service Industries Journal 39: 1099–122. [Google Scholar] [CrossRef]

- Su, Rongjia, Chunping Liu, and Weili Teng. 2020. the Heterogeneous Effects of Csr Dimensions on Financial Performance—A New Approach for Csr Measurement. Journal of Business Economics and Management 21: 987–1009. [Google Scholar] [CrossRef]

- Tarek, Yasmeen. 2019. The Impact of Financial Leverage and CSR on the Corporate Value: Egyptian Case. International Journal of Economics and Finance 11: 74. [Google Scholar] [CrossRef]

- Timbate, Lukas, and Cheong Kyu Park. 2018. CSR performance, financial reporting, and investors’ perception of financial reporting. Sustainability 10: 522. [Google Scholar] [CrossRef] [Green Version]

- Ullah, Kamau, and Tanveer Bagh. 2019. Finance and Management Scholar at Riphah International University Islamabad, Pakistan. Faculty of Management Sciences 10: 78–87. [Google Scholar] [CrossRef]

- Usman, Aliyu Baba, and Noor Afza Amran. 2015. Corporate social responsibility practice and corporate financial performance: Evidence from Nigeria companies. Social Responsibility Journal 11: 749–63. [Google Scholar] [CrossRef]

- Williams, Revlon Orlando. 2020. Corporate Social Responsibility and Financial Performance of US Manufacturing and Service Small- and Medium-Sized Enterprises. Walden Dissertations and Doctoral Studies Collection. Available online: https://scholarworks.waldenu.edu/dissanddoc/ (accessed on 4 November 2020).

- Wood, Donna, and Raymond Jones. 2016. Stakeholder Mismatching: A Theoretical Problem in Empirical Research on Corporate Social Performance. The Corporation and Its Stakeholders 3: 229–67. [Google Scholar] [CrossRef]

- Wu, Liu, Zhen Shao, Changhui Yang, Tao Ding, and Wan Zhang. 2020. The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry. Sustainability 12: 6799. [Google Scholar] [CrossRef]

- Xie, Xiaolin, and Patrick Ward. 2019. The Impact of Corporate Social Responsibilities on Financial Performance in China. Master’s thesis, Duke University, Durham, NC, USA. [Google Scholar]

- Yang, Ann Shawing, and Suyd Baasandorj. 2017. Exploring CSR and financial performance of full-service and low-cost air carriers. Finance Research Letters 23: 291–99. [Google Scholar] [CrossRef]

- Zhang, Lu, Yuan George Shan, and Millicent Chang. 2020. Can CSR Disclosure Protect Firm Reputation During Financial Restatements? Journal of Business Ethics, 1–28. [Google Scholar] [CrossRef]

Figure 1.

Regression Standardised Residual.

Figure 2.

Regression Standardised Residual.

Figure 3.

ROE and Net Profit Model.

Figure 4.

Residual ACF and PACF for ROE and Net Profit.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Canonical Correlations.

| N = 110 | BOS | GOB | TBNQ | LEV | LogA | MTB | DIP | CSR | ENV | ROE | NPM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BOS | r-Coefficient | 1 | ||||||||||

| p-Value | ||||||||||||

| GOB | r-Coefficient | 0.261 ** | 1 | |||||||||

| p-Value | 0.006 | |||||||||||

| TBNQ | r-Coefficient | 0.120 | −0.136 | 1 | ||||||||

| p-Value | 0.211 | 0.158 | ||||||||||

| LEV | r-Coefficient | −0.180 | −0.059 | −0.073 | 1 | |||||||

| p-Value | 0.059 | 0.540 | 0.450 | |||||||||

| LogA | r-Coefficient | 0.361 ** | 0.687 ** | 0.014 | −0.326 ** | 1 | ||||||

| p-Value | 0.000 | 0.000 | 0.888 | 0.001 | ||||||||

| MTB | r-Coefficient | 0.019 | −0.027 | −0.057 | −0.034 | 0.222 * | 1 | |||||

| p-Value | 0.841 | 0.781 | 0.554 | 0.722 | 0.020 | |||||||

| DIP | r-Coefficient | 0.108 | 0.467 ** | −0.114 | −0.062 | 0.274 ** | 0.274 ** | 1 | ||||

| p-Value | 0.262 | 0.000 | 0.234 | 0.517 | 0.004 | 0.004 | ||||||

| CSR | r-Coefficient | −0.143 | −0.078 | 0.233 * | 0.468 ** | −0.325 ** | −0.122 | −0.099 | 1 | |||

| p-Value | 0.135 | 0.417 | 0.014 | 0.000 | 0.001 | 0.204 | 0.302 | |||||

| ENV | r-Coefficient | −0.121 | −0.153 | −0.067 | −0.018 | 0.014 | 0.249 ** | −0.092 | −0.039 | 1 | ||

| p-Value | 0.209 | 0.110 | 0.488 | 0.849 | 0.887 | 0.009 | 0.341 | 0.687 | ||||