The Relationship between Dividend Policy and Earnings Quality: The Role of Accounting Information in Indonesia’s Capital Market

Abstract

:1. Introduction

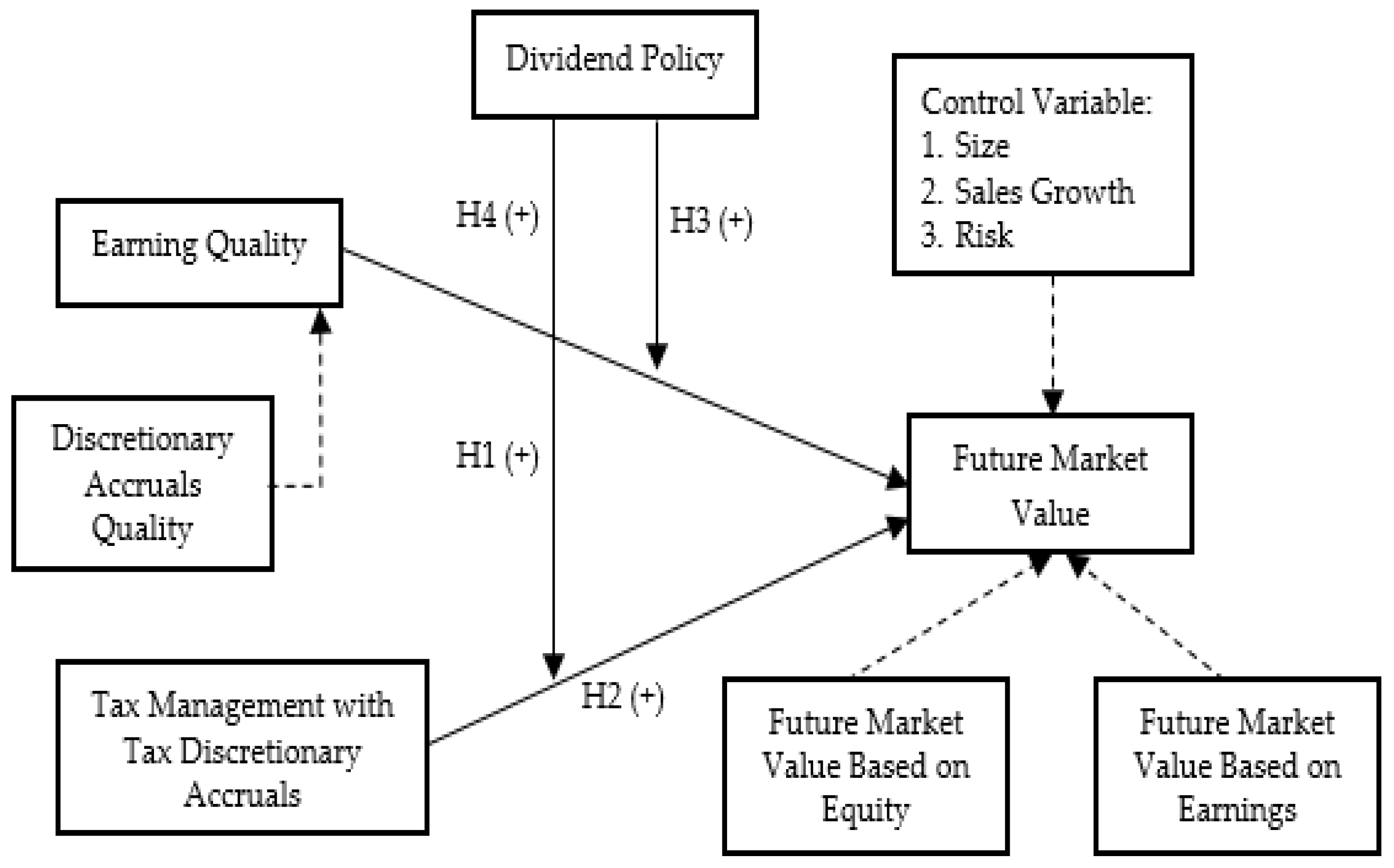

2. Theoretical Framework and Hypothesis

2.1. Hypothesis Development

2.2. The Empirical Conceptual Research Framework

3. Method

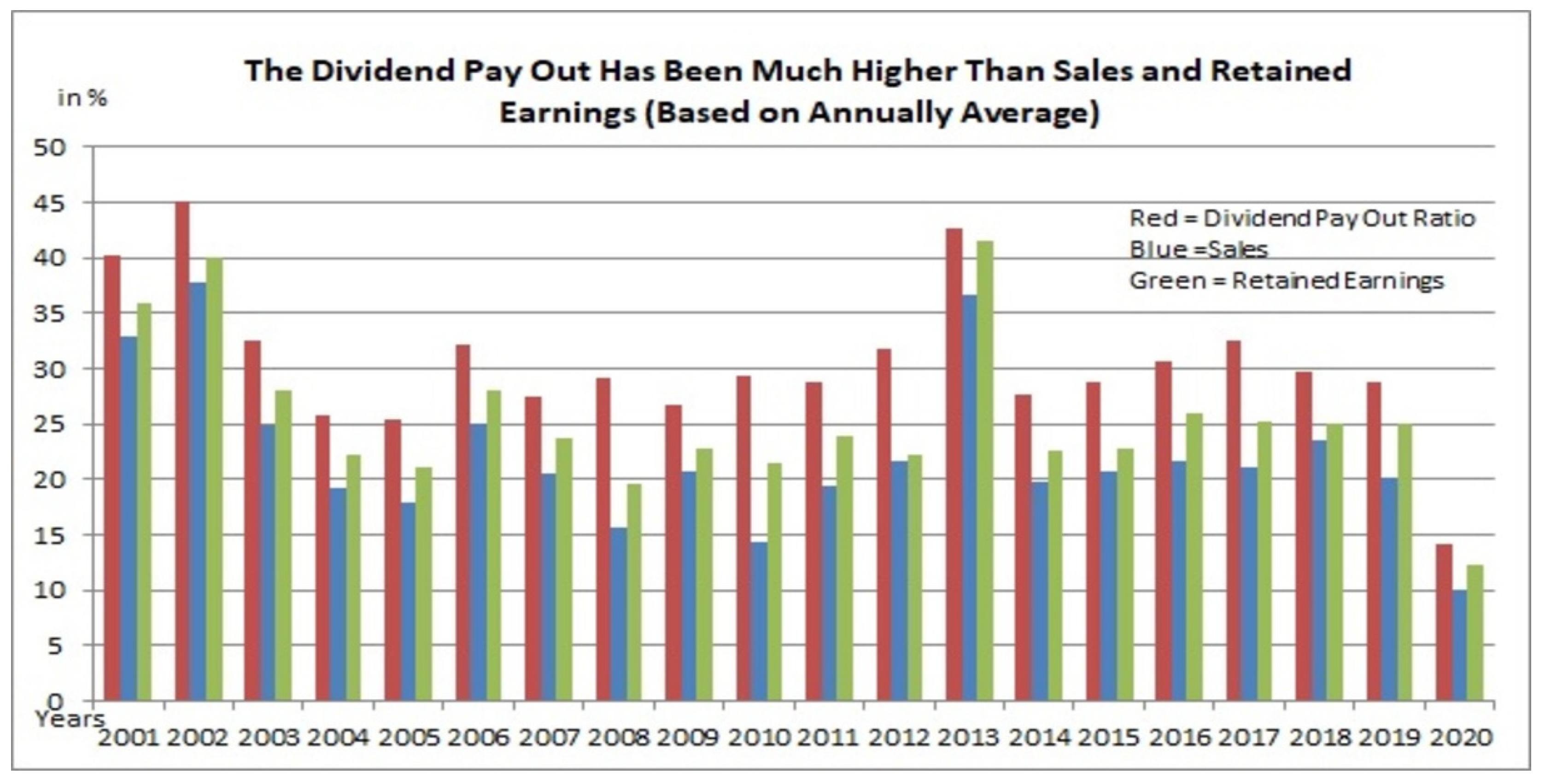

3.1. Sample and Data Collection

3.2. Measurement

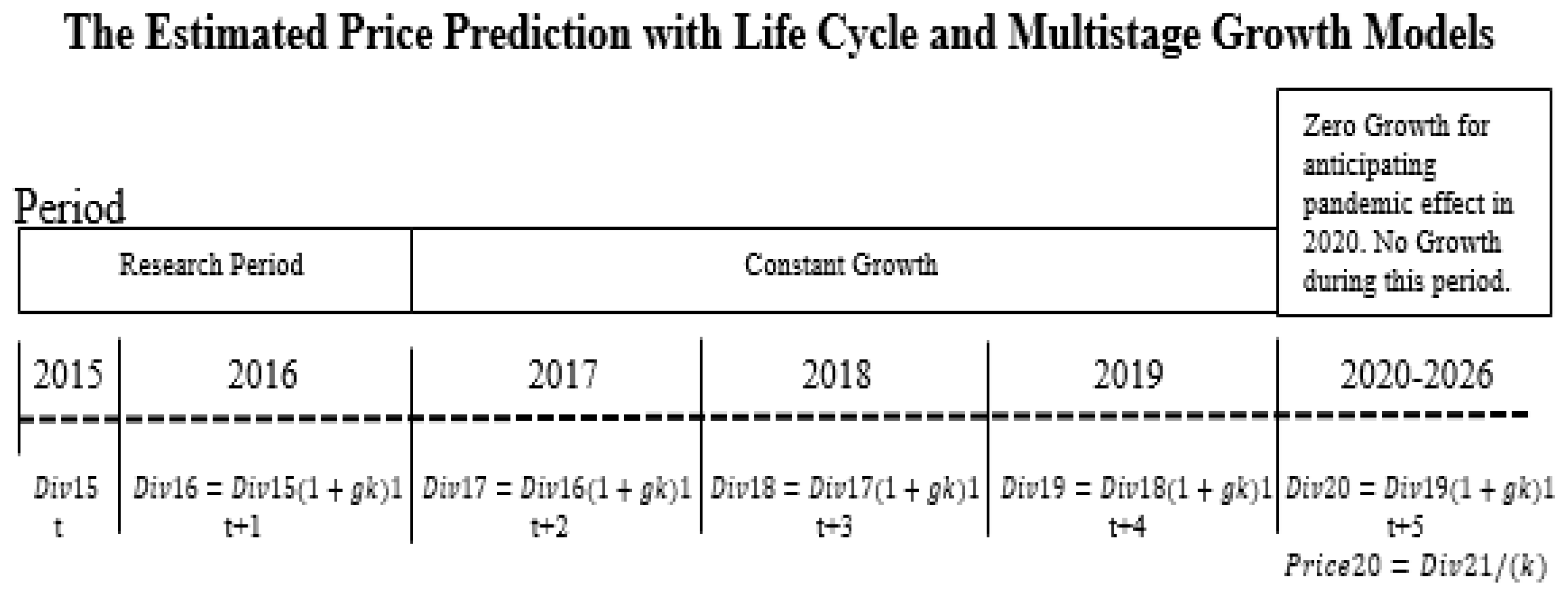

3.2.1. Future Market Value

- Future Market Value is a fact-based and objective indicator of “good news”, an accurately comparative analysis of the current and predicted market prices in the following period. It is related to calculating the risk and cost of capital due to the high probability of reaching a better prospect.

- The Future Market Value has been a trustworthy sign of both over- and undervaluation when the high complexity of accounting information has been an obstacle in analysing the capability of management in keeping a high sustainability in the long run. As a need of a simple indicator of management viewpoint, the dividend policy can be used to estimate the firm value, including a proxy for high obedience and compliance.

- The Future Market Value indicates the real risk and reasonable cost of capital when it refers to the present value of the predicted market price in the following period. By adjusting the present value of the dividend and market price with the expected return, this indicator reflects an accurate illustration in estimating the future return, particularly in overcoming the market risk, which it adopted from the CAPM model.

3.2.2. Future Market Value Based on Equity

3.2.3. Future Market Value Based on Earnings

3.2.4. Dividend Policy

3.2.5. Discretionary Accrual Quality

3.2.6. Tax Management

4. Results

4.1. Descriptive Statistics

4.2. Statistical Testing

- The regression coefficient revealed that a high obedience level to accounting standards positively affects discretionary accrual quality in FMV, as a function of both earnings and equity. This was supported by the moderating variables, suggesting that the dividend push management toward a high obedience level to accounting standards.

- High compliance with tax regulations played a primary role in increasing the accuracy of predicting future returns, as indicated by the effect of discretionary tax accrual quality on FMV as a function of equity and earnings. The moderation of the dividend revealed a different result as the dividend did not strengthen the effect of tax management on FMV as a function of equity and earnings.

- Sales and total assets as control variables had a significant positive contribution to future market value as a function of both equity and earnings. This suggests actual earnings as an indicator of a high probability of better prospects for investors.

- Risk as a control variable had a significant negative impact on future market value as a function of equity and earnings. This indicates a relationship between obedience and agency cost. Thus, opportunistic behavior increases the uncertainty and unpredictability of future earnings.

5. Discussion

- A “positive market value” better indicates a high potential of fulfilling the future expected (bold line); this represents the positive movement of market price and low fluctuation because real earnings are a sign of obtaining a better future return.

- A “negative market value” indicates a low potential of fulfilling the future expected return (thin line); this represents the negative movement of market price and volatile fluctuation due to unsatisfactory performance.

- The regulator in the capital market is provided with feedback to release the regulation, thus giving management an attractive incentive to publish high-quality financial reporting. The regulation should boost investors’ trust as a function of high-quality financial reporting when a legal standing approach has been needed to deduct a high level of accruals as a sign of any infringement.

- Considering the impact of implementing a high-yield dividend, the authoritative regulator must design the preventive effect of this corporate policy by creating some barriers for this dividend policy model, as it generates the high involvement of dominant shareholders, which is a violation of the minority investor.

- The regulator should release the alluring rule to force management to run this dividend policy regularly as a standard corporate policy. Unquestionably, there is no tax on the dividend. Regulators in the capital market should design an appealing controlling and monitoring model for the company to annually and consistently implement a dividend policy model. A high-yield dividend should be intercepted quantitatively by the “flawless” approaches, representing a new obstacle in managing the liquidity of cash flow when funding expanded business activity; this is a widely opened chance for opportunistic behavior.

6. Conclusions

7. Limitations and Future Research Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abraham, Rebecca, Judith Harris, and Joel Auerbach. 2017. Earnings Yield as a Predictor of Return on Assets, Return on Equity, Economic Value Added and the Equity Multiplier. Modern Economy 8: 10–24. Available online: http://www.scirp.org/journal/me (accessed on 1 January 2018). [CrossRef] [Green Version]

- Akerlof, George A. 1970. The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism. Quarterly Journal of Economics 84: 488–500. Available online: http://0-links-jstor-org.brum.beds.ac.uk/sici?sici=0033-5533%28197008%2984%3A3%3C488%3ATMF%22QU%3E2.0.CO%3B2-6 (accessed on 22 January 2022). [CrossRef]

- Alipour, Mohammad, Mehrad Ghanbari, Babak Jamshidinavid, and Aliasghar Taherabadi. 2019. The relationship between environmental disclosure quality and earnings quality: A panel study of an emerging market. Journal of Asia Business Studies 13: 326–47. [Google Scholar] [CrossRef]

- Al-Rassas, Ahmed, and Husein Kamardin. 2016. Earnings quality and audit attributes in high concentrated ownership market. Corporate Governance: The International Journal of Business in Society 16: 377–99. [Google Scholar] [CrossRef]

- Askari, Gholamreza, Madjid Eshaghi Gordji, and Choonkil Park. 2019. The behavioral model and game theory. Palgrave Communications 5: 1–8. [Google Scholar] [CrossRef] [Green Version]

- Báez-Díaz, Anibal, and Pervaiz Alam. 2012. Tax conformity of earnings and the pricing of accruals. Review of Quantitative Finance and Accounting 40: 509–38. [Google Scholar] [CrossRef]

- Bassiouny, Sarah Wahid, Mohammed Mohammed Soliman, and Ahmed Ragab. 2016. The impact of ownership structure on dividend payout policies: An empirical study of the listed companies in Egypt. The Business and Management Review 7: 91–102. [Google Scholar]

- Beyer, Anne, Marinovic Ivan, and Guttman Ilan. 2019. Earnings management and earnings quality: Theory and Evidence. The Accounting Review 94: 77–101. [Google Scholar] [CrossRef]

- Bodie, Zvi, Alex Kane, and Alan Jay Marcus. 2013. Investment, 10th ed. New York: McGraw-Hill Education. [Google Scholar]

- Brigham, Eugene F., and Joel F. Houston. 2013. Fundamental of Financial Management, 13th ed. Cengage: Cengage Learnings. [Google Scholar]

- Chansarn, Supachet, and Thanyankorn Chansarn. 2016. Earnings management and dividend policy of small and medium enterprises in Thailand. International Journal of Business and Society 17: 307–28. [Google Scholar] [CrossRef]

- Chaudhary, Ghulam Mujtaba, Shujahat Haider Hashmi, and Shahzada Aqeel Younis. 2016. Does Dividend Announcement Generate Market Signal? Evidence from Pakistan. International Journal of Economics and Financial Issues 6: 65–72. [Google Scholar]

- Chen, Huimin, and Qiang Wu. 2021. Short selling threat and real activity manipulation: Evidence from a natural experiment. Advances in Accounting 52: 100514. [Google Scholar] [CrossRef]

- Choudhary, Preeti, Allison Koester, and Terry Shevlin. 2016. Measuring income tax accrual quality. Review of Accounting Studies 21: 89–139. [Google Scholar] [CrossRef]

- Damodaran, Aswath. 2012. Investment Valuation: Second Edition. Available online: https://0-onlinelibrary-wiley-com.brum.beds.ac.uk/doi/book/10.1002/9781119201786 (accessed on 25 March 2015).

- Datta, Sudip, May Iskandar-Datta, and Vivek Singh. 2013. Product market power, industry structure, and corporate earnings management. Journal of Banking and Finance 37: 3273–85. [Google Scholar] [CrossRef]

- Deng, Lu, Sifei Li, and Mingqing Liao. 2017. Dividends and earnings quality: Evidence from China. International Review of Economics & Finance 48: 255–68. [Google Scholar] [CrossRef]

- Desai, Mihir A., and Dhammika Dharmapala. 2005. Corporate Tax Avoidance and High Powered Incentives. SSRN Electronic Journal 79: 145–79. [Google Scholar] [CrossRef] [Green Version]

- Dichev, Ilia, John Graham, Campbell R. Harvey, and Shiva Rajgopal. 2016. The misrepresentation of earnings. Financial Analysts Journal 72: 22–35. [Google Scholar] [CrossRef]

- Dopuch, Nicholas, Raj Mashruwala, Chandra Seethamraju, and Tzachi Zach. 2012. The impact of a heterogeneous accrual-generating process on empirical accrual models. Journal of Accounting, Auditing and Finance 27: 386–411. [Google Scholar] [CrossRef]

- Duy, Nguyen Vu, and Tien Quang Tran. 2020. The influence of international standards on SME tax compliance in Vietnam. Finance Research Letters 40: 101750. [Google Scholar] [CrossRef]

- El Diri, Malek, Cortas Lambrinoudakis, and Mohammad Alhadab. 2020. Corporate governance and earnings management in concentrated markets. Journal of Business Research 108: 291–308. [Google Scholar] [CrossRef]

- Elayan, Fayek A., Jingyu Li, Zhefeng F. Liu, Thomas O. Meyer, and S. Felton. 2016. Changes in the Covalence Ethical Quote, Financial Performance and Financial Reporting Quality. Journal of Business Ethics 134: 369–95. [Google Scholar] [CrossRef]

- Eldomiaty, Tarek, Yasmeen Saeed, Rasha Hammam, and S. AboulSoud. 2020. The associations between stock prices, inflation rates, interest rates are still persistent: Empirical evidence from stock duration model. Journal of Economics, Finance and Administrative Science 25: 149–61. [Google Scholar] [CrossRef]

- Ezat, Amr Nazieh. 2019. The Impact of Earnings Quality on the Association Between Readability and Cost of Capital: Evidence from Egypt. Journal of Accounting in Emerging Economies 9: 366–85. [Google Scholar] [CrossRef]

- Godfrey, Jayne, Alan Hodgson, Ann Tarca, Jane Hamilton, and Salma Holmes. 2014. Accounting Theory, 9th ed. Hoboken: Wiley & Sons Inc. [Google Scholar]

- Gujarati, Damodar N. 2011. Basic Econometrics, 5th ed. Boston: Mc Graw Hill Boston. [Google Scholar]

- Hair, Joseph, Jr., Willaim C. Black, Barry J. Babin, and Rolph Anderson. 2010. Multivariate Analysis: Global Perspective, 7th ed. Upper Saddle River: Pearson Prentice Hall. [Google Scholar]

- He, Wei, and Nyo Nyo A. Kyaw. 2018. Ownership structure and investment decisions of Chinese SOEs. Research in International Business and Finance 43: 48–57. [Google Scholar] [CrossRef]

- He, Wen, Lilian Ng, Nataliya Zaiats, and Bohui Zhang. 2017. Dividend policy and earnings management across countries. Journal of Corporate Finance 42: 267–86. [Google Scholar] [CrossRef] [Green Version]

- Heizer, Jay, Barry Render, and Chuck dan Munson. 2017. Operations Management: Sustainbility and Supply Chain Management, 11th ed. Hoboken: Prentice Hall. [Google Scholar]

- Hoang, Trang Cam, Indra Abeysekera, and Shiguang Ma. 2019. Earnings Quality and Corporate Social Disclosure: The Moderating Role of State and Foreign Ownership in Vietnamese Listed Firms. Emerging Markets Finance and Trade 55: 272–88. [Google Scholar] [CrossRef] [Green Version]

- Homer, Sidney, Martin L. Leibowitz, Anthony Bova, and Stanley Kogelman. 2013. Inside the Yield Book: The Classic That Created the Science of Bond Analysis. Hoboken: John Wiley & Sons, Inc. [Google Scholar]

- Hu, Nanwei, Qiang Cao, and Lulu Zheng. 2015. Listed companies’ income tax planning and earnings management: Based on China’s capital market. Journal of Industrial Engineering and Management 8: 417–34. [Google Scholar] [CrossRef]

- Hutton, Amy P., and Philip C. Stocken. 2021. Prior Forecasting Accuracy and Investor Reaction to Management Earnings Forecasts. Journal of Financial Reporting 6: 87–107. [Google Scholar] [CrossRef]

- IDX, ISE. 2001–2020. Annual Report, Indonesia Stock Exchange from period 2000 until 2020. Available online: http://www.idx.co.id (accessed on 20 May 2015).

- Ifada, Luluk Muhimatul, and Nova Wulandari. 2015. The effect of deferred tax and tax planning toward earnings management practice: An empirical study on non manufacturing companies listed in Indonesia Stock Exchange in the period of 2008–2012. International Journal of Organizational Innovation 8: 155–71. [Google Scholar]

- Jabbouri, Imad. 2016. Determinants of corporate dividend policy in emerging markets: Evidence from MENA stock markets. Research in International Business and Finance 37: 283–98. [Google Scholar] [CrossRef]

- Jacob, Martin, and Harm H. Schütt. 2020. Firm Valuation and the Uncertainty of Future Tax Avoidance. European Accounting Review 29: 409–35. [Google Scholar] [CrossRef] [Green Version]

- Jeong, Bon Kim, and Byungcheri Charlie Sohn. 2013. Real Earnings Management and Cost of Capital. Journal Accounting Public Policy 32: 518–43. [Google Scholar] [CrossRef] [Green Version]

- Jeong, Kwang Hwa, and Seung Uk Choi. 2019. Does Real Activities Management Influence Earnings Quality and Stock Returns in Emerging Markets? Evidence from Korea. Emerging Markets Finance and Trade 55: 2834–50. [Google Scholar] [CrossRef]

- Kałdoński, Michael, and Tomasz Jewartowski. 2020. Do firms using real earnings management care about taxes? Evidence from a high book-tax conformity country. Finance Research Letters 35: 101351. [Google Scholar] [CrossRef]

- Kaplan. 1996. Decision Theory as Philosophy. Cambridge: Cambridge University Press. [Google Scholar]

- Kasanen, Eero, Juha Kinnunen, and Jyrki Niskanen. 1996. Dividend-Based Earnings Management: Empirical evidence from Finland. Journal of Accounting and Economics 22: 283–312. [Google Scholar] [CrossRef]

- Kato, Hideyaki Kiyoshi, Uri Loewenstein, and Wenyuh Tsay. 2002. Dividend policy, cash flow, and investment in Japan. Pacific Basin Finance Journal 10: 443–73. [Google Scholar] [CrossRef]

- Kothari, Sri Prakash. 2001. Capital markets research in. Journal of Accounting and Economics 31: 105–231. Available online: http://0-www-sciencedirect-com.brum.beds.ac.uk/science/article/pii/S0165410101000301 (accessed on 16 May 2015). [CrossRef]

- Kothari, Sri Prakash, Andre J. Leone, and Charles E. Wesley. 2005. Performance matched discretionary accrual measures. Journal of Accounting and Economics 39: 163–97. Available online: https://0-www-sciencedirect-com.brum.beds.ac.uk/science/article/pii/S0165410104000849 (accessed on 16 May 2015). [CrossRef]

- Kothari, Sri Prakash, Natalie Mizik, and Sugata Roychowdhury. 2016. Managing for the moment: The role of earnings management via real activities versus accruals in SEO valuation. Accounting Review 91: 100855. [Google Scholar] [CrossRef]

- Lebert, Sebastian. 2019. Rounding up performance measures in German firms: Earnings cosmetics or earnings management on a larger scale? Rounding up performance measures in German firms: Earnings cosmetics or earnings management on a larger scale? Journal of Business Finance & Accounting 48: 564–86. [Google Scholar]

- Lee, Hyun Ah. 2016. The usefulness of the tax avoidance proxy: Evidence from Korea. Journal of Applied Business Research 32: 607–20. [Google Scholar] [CrossRef]

- Lennox, Clive, Petro Lisowsky, and Jeffrey Pittman. 2013. Tax Aggressiveness and Accounting Fraud. Journal of Accounting Research 51: 739–78. [Google Scholar] [CrossRef]

- Li, Valerie. 2019. The effect of real earnings management on the persistence and in formativeness of earnings. British Accounting Review 51: 402–23. [Google Scholar] [CrossRef]

- Liu, Haijing, and Hyun Ah Lee. 2019. The effect of corporate social responsibility on earnings management and tax avoidance in Chinese listed companies. International Journal of Accounting and Information Management 27: 632–52. [Google Scholar] [CrossRef]

- Mehrani, Sasan, Mohammad Moradi, and Hoda Eskandar. 2017. Institutional Ownership Type and Earnings Quality: Evidence from Iran. Emerging Markets Finance and Trade 53: 54–73. [Google Scholar] [CrossRef]

- Miiller, Diego Lopes, and Antonio Lopo Martinez. 2016. Book-Tax Difference, Earnings Management and Bond Ratings in the Brazilian Market. Revista Universo Contábil 12: 91–109. [Google Scholar] [CrossRef] [Green Version]

- Mongrut, Samuel, and Diego Winkelried. 2019. Unintended effects of IFRS adoption on earnings management: The case of Latin America. Emerging Markets Review 38: 377–88. [Google Scholar] [CrossRef]

- Mousa, Gehan, and Abdelmohsen Desoky. 2019. The effect of dividend payments and firm’s attributes on earnings quality: Empirical evidence from Egypt. Investment Management and Financial Innovations 16: 14–29. [Google Scholar] [CrossRef]

- Nekhili, Mehdi, Ines Fakhfakh Ben Amar, Tawhid Chtioui, and Faten Lakhal. 2016. Free cash flow and earnings management: The moderating role of governance and ownership. Journal of Applied Business Research 32: 255–68. [Google Scholar] [CrossRef]

- Orazalin, Nurlan, and Rassulah Akhmetzhanov. 2019. Earnings management, audit quality, and cost of debt: Evidence from a Central Asian economy. Managerial Auditing Journal 34: 696–721. [Google Scholar] [CrossRef]

- Ozili, Peterson K. 2016. Earnings Quality and IFRS Research in Africa: Recent Evidence, Issues and Future Direction. Research Journal of Finance and Accounting 7: 84–94. [Google Scholar]

- Park, Sam Bock, Sung Kyoo Kim, and Sangryui Lee. 2021. Earnings management of insolvent firms and the prediction of corporate defaults via discretionary accruals. International Journal of Financial Studies 9: 17. [Google Scholar] [CrossRef]

- Pathak, Rajesh, and Ranajee. 2020. Earnings quality and corporate payout policy linkages: An Indian context. The North American Journal of Economics and Finance 51: 1–10. [Google Scholar] [CrossRef]

- Perotti, Pietro, and Alfred Wagenhofer. 2014. Earnings quality measures and excess returns. Journal of Business Finance and Accounting 41: 545–71. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Persakis, Anthony, and George Emmanuel Iatridis. 2017. The joint effect of investor protection, IFRS and earnings quality on cost of capital: An international study. Journal of International Financial Markets, Institutions and Money 46: 1–29. [Google Scholar] [CrossRef]

- Ping, Ke. 2016. Do Investors Price Accruals Quality for Firms Charged with Poor Reporting 2. Literature Review and Hypothesis Development 7: 2–23. [Google Scholar]

- Pompili, Marco, and Marco Tutino. 2019. Fair Value Accounting and Earning Management: The Impact of Unobservable Inputs On Earning Quality. Evidence from The US. Control Ownership & Control 16: 8–18. [Google Scholar]

- Ross, Stephen A., Randolph W. Westerfield, and Bradford D. Jordan. 2010. Fundalmental of Corporate Finance, 9th ed. New York: Mc Graw Hill, Available online: https://www.academia.edu/38763730/_Fundamentals_of_Corp_Finance_Ross_Westerfield_26_Jordan_9th_Edition (accessed on 19 April 2015).

- Sakaki, Hamid, Surendranath Jory, and Dave Jackson. 2021. Institutional investors’ ownership stability and their investee firms’ equity mispricing. North American Journal of Economics and Finance 57: 1–34. [Google Scholar] [CrossRef]

- Salihu, Ibrahim Aramide, Siti Normala Shiekh Obid, and Hairul Azlan Annuar. 2013. Measures of corporate tax avoidance: Empirical evidence from an emerging economy. International Journal of Business and Society 14: 412–27. [Google Scholar]

- Salleh, Nik Muhammad Zaki, Rasidah Abdul Rahman, and Wan Masliza Wan Muhammad. 2011. A Panel Data Analysis on the Effects of Independent Directors Characteristics, Ethnicity and the Level of risks on Discretionary Accruals in Malaysian Manufacturing Companies (2003–2009). Available online: https://www.researchgate.net/publication/259459832_A_Panel_Data_Analysis_on_the_Effects_of_Independent_Directors_Characteristics_Ethnicity_and_the_Level_of_risks_on_Discretionary_Accruals_in_Malaysian_Manufacturing_Companies_2003-2009 (accessed on 9 January 2017).

- Savor, Pavel, and Mungon Wilson. 2016. Earnings Announcements and Systematic Risk. Journal of Finance 71: 83–138. [Google Scholar] [CrossRef]

- Scott, William R. 2016. Financial Accounting Theory, 9th ed. London: Pearson Inc. [Google Scholar]

- Sekaran, Uma, and Roger Bougie. 2016. Research Methods for Business: A Skill Building Approach, 7th ed. Hoboken: Wiley & Sons. [Google Scholar]

- Shah, Syed Zulfiqar, Hui Yuan, and Nousheen Zafar. 2010. Earnings management and dividend policy an empirical comparison between Pakistani listed companies and Chinese listed companies. International Research Journal of Finance and Economics 35: 51–60. [Google Scholar]

- Siladjaja, Muljanto, and Yuli Anwar. 2020. The Impact Of Innate Accruals Quality On The Future Market Value Moderated By Dividend Policy. Asian Journal of Accounting Research 5: 269–83. [Google Scholar] [CrossRef]

- Stigler, G. 2012. The theory of economic regulation. Christopher Carrigan and Cary Coglianese 20: 287–99. Available online: https://tspppa.gwu.edu/sites/g/files/zaxdzs2001/f/Carrigan%20Coglianese%202015%20George%20J.%20Stigler.pdf (accessed on 14 April 2013).

- Takacs, Andras, Tamas Szucs, Daniel Kehl, and Andrew Fodor. 2020. The effect of fair valuation on banks’ earnings quality: Empirical evidence from developed and emerging European countries. Heliyon 6: 1–7. [Google Scholar] [CrossRef] [PubMed]

- Taleb, Ghassan Al. 2012. Measurement of Impact Agency Costs Level of Firms on Dividend and Leverage Policy: An Empirical Study. Institute of Interdisciplinary Business Research 3: 234–44. [Google Scholar]

- Tang, Tanya, and Michael Firth. 2011. Can book-tax differences capture earnings management and tax Management? Empirical evidence from China. International Journal of Accounting 46: 175–204. [Google Scholar] [CrossRef]

- Wang, Rui, and Lianfa Li. 2020. Dynamic relationship between the stock market and macroeconomy in China (1995–2018): New evidence from the continuous wavelet analysis. Economic Research-Ekonomska Istrazivanja 33: 521–39. [Google Scholar] [CrossRef]

- Watts, Ross L., and Jerold L. Zimmerman. 2003. Positive Accounting Theory. Hoboken: Prentice Hall. [Google Scholar]

- Wilcox, Stephen E. 2007. The Adjusted Earnings Yield. Financial Analysts Journal 63: 54–68. [Google Scholar] [CrossRef]

- Wu, Peng, Lei Gao, and Tingting Gu. 2016. Business strategy, market competition and earnings management: Evidence from China. Chinese Management Studies 9: 401–24. [Google Scholar] [CrossRef]

- Yoon, Soon Suk, Hyo Jin Kim, and Gregg S. Woodruff. 2012. On The Models and Estimation of Discretionary Accruals. IFAS. University Xiamen. Available online: http://www.kaa-edu.or.kr/online3/2014_1/2 (accessed on 17 April 2013).

- Yorke, Sally Mingie, Mohammed Amidu, and Cletus Agyemin-Boateng. 2016. The effects of earnings management and corporate tax avoidance on firm value. International Journal of Management Practice 9: 112–31. [Google Scholar] [CrossRef]

- Zarowin, Paul. 2015. Estimation of Discretionary Accruals and the Detection of Earnings Management. Oxford Handbooks Online, 1–20. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Period | Prediction | Dividend Yield | Capital Gain |

|---|---|---|---|

| 2015 | Price Estimated at 2016 | ||

| 2016 | Price Estimated at 2017 | ||

| 2017 | Price Estimated at 2018 | ||

| 2018 | Price Estimated at 2019 | ||

| 2019 | Price Estimated at 2020 | ||

| 2020 | Price Estimated at 2021 |

| Variable | Measurement Formula | Scale |

|---|---|---|

| The dependent variable, as a measurement indicator of variable future market value | Ratio | |

| Ratio | ||

| Tax management as a measurement indicator of discretionary tax accrual | Ratio | |

| Moderating variable using dividend policy | Measurement of period dividend policy t and net income period t − 1 | Ratio |

| First control variable (size) | Ratio | |

| Second control variable (sales growth) | short-term debt + long-term debt | Ratio |

| Description | N | Minimum | Maximum | Mean | Standard Deviation |

|---|---|---|---|---|---|

| Future market value based on equity | 204 | 0.234 | 0.821 | 0.419 | 0.017 |

| Future market value based on earnings | 204 | 0.161 | 0.736 | 0.293 | 0.143 |

| Discretionary accrual quality | 204 | −0.820 | 0.682 | 0.499 | 0.502 |

| Discretionary tax accrual quality | 204 | −0.960 | 0.890 | 0.426 | 0.620 |

| Dividend payout | 204 | 0.030 | 0.500 | 0.276 | 0.136 |

| Discretionary accrual quality × dividend | 204 | −0.246 | 0.951 | 0.752 | 0.561 |

| Discretionary tax accrual quality × dividend | 204 | −0.531 | 1.286 | 0.914 | 0.472 |

| Total assets (in thousands) | 204 | 476,149 | 1,447,865 | 859,497 | 63,617 |

| Growth of sales (in thousands) | 204 | −3.238 | 0.720 | −0.296 | 0.036 |

| Risk (beta) | 204 | 0.000 | 1.010 | 0.458 | 0.201 |

| Description Variables | KS (*) | Sig | Note |

|---|---|---|---|

| Discretionary accrual quality (XDAQ) | 0.043 | 0.186 | Ab and Hetero |

| Discretionary tax accrual quality (XDTQ) | 0.029 | 0.448 | Ab and Hetero |

| Future market value based on equity | 0.037 | (**) | Abnormal |

| Future market value based on earnings | 0.016 | (**) | Abnormal |

| Dividend payout (XDiv) | 0.953 | 0.007 | Normal and Homo |

| Discretionary accrual quality × dividend (XMDiv1) | 0.017 | 0.179 | Ab and Hetero |

| Discretionary tax accrual quality × dividend (XMDiv2) | 0.002 | 0.427 | Ab and Hetero |

| Log total asset (XTA) | 0.751 | 0.019 | Normal and Homo |

| Growth sales (XSa) | 0.496 | 0.043 | Normal and Homo |

| Risk (XRi) | 0.614 | 0.035 | Normal and Homo |

| Phase-In Testing Data Panel | FMV Based on Equity First Model | FMV Based on Earnings Second Model |

|---|---|---|

| Chow testing | p value = 0.083 (>0.05) H0 accepted Common effect model | p value = 0.006 (<0.05) H0 rejected Fixed effect model |

| Hausman testing | Not applied | p value = 0.004 (<0.05) H0 rejected Fixed effect model |

| Lagrange multiplier testing | Prob. Breusch–Pagan = 0.093 (>0.05) H0 rejected Fixed effect model | Not applied |

| Description of Variable | Future Market Value-Based on Equity | Future Market Value-Based on Earnings | |||||

|---|---|---|---|---|---|---|---|

| Coefficient | t | Sig(*) | Hypothesis | Coefficient | t | Sig(*) | |

| Constant | −0.871 | −0.782 | 0.089 | −0.792 | −0.632 | 0.296 | |

| Dependent variables | |||||||

| Discretionary accrual quality (XDAQ) | 0.127 | 4.181 | 0.007 | H1a and H1b accepted | 0.091 | 4.792 | 0.009 |

| Discretionary tax accrual quality (XDTQ) | 0.108 | 2.413 | 0.028 | H2a and H2b accepted | 0.228 | 1.892 | 0.031 |

| Dividend payout (XDiv) | 0.274 | 5.041 | 0.004 | 0.239 | 4.812 | 0.007 | |

| Discretionary accrual quality × dividend (XMDiv1) | 0.313 | 3.424 | 0.018 | H3a and H3b accepted | 0.205 | 2.819 | 0.021 |

| Discretionary tax accrual quality × dividend (XMDiv2) | −0.051 | −0.763 | 0.197 | H4a and H4b rejected | −0.037 | −0.926 | 0.231 |

| Control variables | Note | ||||||

| Log total asset (XTA) | 0.071 | 2.859 | 0.017 | Significant | 0.058 | 2.042 | 0.032 |

| Growth sales (XSa) | 0.114 | 5.581 | 0.002 | Significant | 0.179 | 4.259 | 0.007 |

| Risk (XRi) | −0.373 | −2.085 | 0.023 | Significant | −0.486 | −1.664 | 0.038 |

| Analysis of variance F-test calculated Sig. level Adjusted R-square Coefficient R-square Durbin Watson value | 8.341 (>FTable 0.338) 0.0000 (<0.05) 0.245 0.301 2.087 (1.845 < X < 2.154) | 3.872 (>FTable 0.338) 0.0000 (<0.05) 0.206 0.274 1.965 (1.845 < X < 2.154) | |||||

| Description of Variable | Future Market Value Based on Equity | Future Market Value Based on Earnings | ||||

|---|---|---|---|---|---|---|

| Coefficient | t | Sig(*) | Coefficient | t | Sig(*) | |

| Constant | −0.041 | −0.982 | 0.101 | −0.092 | −0.771 | 0.383 |

| Dependent variables | ||||||

| Discretionary accrual quality (XDAQ) | 0.201 | 5.981 | 0.004 | 0.137 | 5.483 | 0.005 |

| Discretionary tax accrual quality (XDTQ) | 0.117 | 3.123 | 0.011 | 0.294 | 3.194 | 0.019 |

| Dividend payout (XDiv) | 0.296 | 6.147 | 0.003 | 0.262 | 4.984 | 0.006 |

| Discretionary accrual quality × dividend (XMDiv1) | 0.417 | 4.134 | 0.009 | 0.368 | 3.019 | 0.014 |

| Control variables | ||||||

| Log total asset (XTA) | 0.091 | 4.715 | 0.008 | 0.083 | 2.331 | 0.016 |

| Growth sales (XSa) | 0.197 | 6.912 | 0.000 | 0.284 | 6.262 | 0.002 |

| Risk (XRi) | −0.461 | −4.326 | 0.007 | −0.509 | −3.457 | 0.013 |

| Analysis of variance F-test calculated Sig. level Adjusted R-square Coefficient R-square Durbin Watson value | 11.435 (>FTable 0.271) 0.0000 (<0.05) 0.297 0.342 2.095 (1.845 < X < 2.154) | 5.564 (>FTable 0.271) 0.0000 (<0.05) 0.247 0.304 2.001 (1.845 < X < 2.154) | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Siladjaja, M.; Anwar, Y.; Djan, I. The Relationship between Dividend Policy and Earnings Quality: The Role of Accounting Information in Indonesia’s Capital Market. Economies 2022, 10, 140. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10060140

Siladjaja M, Anwar Y, Djan I. The Relationship between Dividend Policy and Earnings Quality: The Role of Accounting Information in Indonesia’s Capital Market. Economies. 2022; 10(6):140. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10060140

Chicago/Turabian StyleSiladjaja, Muljanto, Yuli Anwar, and Ismulyana Djan. 2022. "The Relationship between Dividend Policy and Earnings Quality: The Role of Accounting Information in Indonesia’s Capital Market" Economies 10, no. 6: 140. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10060140