A Socio-Economic Model of Sales Tax Compliance

by

, and

, and

Ahmad Farhan Alshira’h

1,*,

Moh’d Alsqour

1,

Abdalwali Lutfi

2 ,

,

Adi Alsyouf

3 and

and

Malek Alshirah

4 1

Accounting Department, Faculty of Administrative and Financial Sciences, Irbid National University, Irbid 2600, Jordan

2

Accounting Department, College of Business Administration, King Faisal University, Al-Alahsa 81932, Saudi Arabia

3

Department of Managing Health Services & Hospitals, King Abdulaziz University, Jeddah 21589, Saudi Aabia

4

Accounting Department, Faculty of Economics and Administrative Sciences, Al al-Bayt University, Al-Mafraq 130040, Jordan

*

Author to whom correspondence should be addressed.

Economies 2020, 8(4), 88; https://0-doi-org.brum.beds.ac.uk/10.3390/economies8040088

Submission received: 12 July 2020

/

Revised: 30 August 2020

/

Accepted: 1 September 2020

/

Published: 20 October 2020

{kind=link}

Abstract

:Tax compliance is an issue that can be traced back to the introduction of taxes, which is the reason such compliance remains a significant topic in the current literature of academia and practice. Prior studies on the topic of tax compliance or non-compliance can be categorized into two, namely economic and social/psychological theories. In a more serious note, tax evasion has remained a key issue among governments all over the globe, with Jordan being no exception. Jordan has undertaken different fiscal measures to increase compliance in the domestic front in the past decades, but based on annual reports, the country is still experiencing a considerable increase in net public debt and fiscal deficit that can be traced back to the increased tax non-compliance rate. This is specifically true in the case of sales tax in Jordan. To compound the matter further, literature concerning the determinants of sales tax compliance as well as other determinants that drive non-compliance is still scarce, with a universal tax compliance model able to explain the issue with clarity still being elusive. Hence, this work proposed the determinants of sales tax compliance in the context of small and medium-sized enterprises (SMEs) in Jordan, extending Fischer’s model of tax compliance, and adding the moderating role of tax knowledge and direct effect of tax service quality. This study proposed a model encapsulating the social, psychological and economic factors to provide insight into the sales tax compliance of Jordanian SMEs.

JEL Classification:

C34; H57; E70; M451. Introduction

The development and growth of a country generally hinges on the obtained revenues from the economic ventures and investments it takes part in (Alshira’h and Abdul-Jabbar 2020; Samuel and Dieu 2014), and in relation to this, taxes are categorized as one of the key major national sources of a country’s revenue (Alshira’h et al. 2016; Varvarigos 2016). Governments are constantly in need of funds for the purpose of investing and renovating public infrastructure, health services, education and public services, and as such, a need exists to increase tax revenue to boost development and growth (Alshira’h and Abdul-Jabbar 2019a; Bird et al. 2008). Added to this, the past several years have been challenging for the tax authority, particularly following the world economic crisis in 2008, with the fiscal deficit leading to the increase in the requirement for tax revenue, urging governments’ collaboration to solve the non-compliance challenge (Alshira’h and Abdul-Jabbar 2019b; Sawyer 2014). In this regard, the tax revenue can be enhanced through efforts directed towards resolving this issue of non-compliance (Alshira’h et al. 2020; Franzoni 1999). An increase in tax compliance would reasonably enhance the tax revenue level, while non-tax compliance causes intense concern throughout developed and developing nations around the world (Alm et al. 2016; Feinstein 1991). This holds true for the countries in the Middle East, as evidenced in Al-Ttaffi and Abdul-Jabbar’s (2015) study, and thus, tax compliance remains an urgent topic to be investigated in literature. Despite the prior studies conducted to explain the issue, a consensus among the authors concerning the tax payment compliance is still elusive (Randlane 2016), but the expected existence of taxation for years to come will find the persistence of non-compliance if not dealt with.

In the case of sales tax, it has evolved into one of the major strategies to obtain tax revenues throughout different countries, which tends to be the core of tax policy decision-making interest, particularly in the developing countries. Sales tax, commonly referred to as value-added tax (VAT) in the UK, US and France, and goods and services tax (GST) in Australia, Singapore and Malaysia, was first introduced in 1954 in France (Alshira’h 2018; Adams and Webley 2001). Currently, sales tax can be found in around 160 nations all over the world (Azmi et al. 2016), owing to its effectiveness in acquiring tax revenue in significant amounts while deficits are reduced (Lee et al. 2013), notably in the category of developing countries, as evidenced by Faridy et al. (2016). Presently, sales tax is considered as tax revenue able to control the consumption of tax system adopted in several nations (Giesecke and Tran 2012). Nevertheless, compliance towards sales tax has also become an issue along with its introduction throughout the countries, and is a major concern for policy makers in nations, especially the developing ones (Das-Gupta and Gang 2003). Sales tax compliance responsibility aspect is reflected on the small and medium-sized enterprises (SMEs) as a burden compared to compliance to other types of taxes (Alshira’h et al. 2019; Hansford and Hasseldine 2012).

Furthermore, in the Jordanian context, where tax revenue is highly valued for its importance to the public budget, in 2010 to 2016 alone, it contributed 71% to the domestic revenue, as reported by the Ministry of Finance (2016). Tax compliance issues have therefore been raised as a national issue affecting the country’s economy (AL-Shawawreh and AL-Smirat 2016). Despite the government of Jordan’s adoption of different fiscal measures to enhance domestic revenue via national economic development and financial stability, businesses reflect, on their annual reports, that public debt is still at a high (JD27,520 billion) as of 2016 (Ministry of Finance (MOF) 2016). Tax non-compliance has displayed a corresponding rise by 48%, with sales tales making up 71% of the overall non-compliance for the years 2011 to 2015 (Jordan Independent Economic Watch 2014). Evidently, tax non-compliance, specifically when it comes to sales tax, is in need of resolution in the Jordanian context in the face of its limited economic resources, otherwise the persistence of chronic fiscal deficit is expected to stay, requiring fund injection to satisfy the economic and societal developmental needs (Al-Zoubi et al. 2013). Stated clearly, tax compliance resolution is a must to enhance the government revenue, financial stability and its ability to respond to the societal needs.

In the business landscape of Jordan, SMEs play a key role and constitute more than 99% of the total businesses that contribute to the economy, as noted by Lutfi et al. (2017) and the Association of Banks in Jordan (2016), while they contribute 50% of the Gross Domestic Product (GDP), and employ 60% of the whole workforce, capable of boosting exports, providing foreign currency and minimizing the payment deficit, while facilitating major companies’ acquisition of goods and services (Lutfi et al. 2016; Alrousan and Jones 2016; Saymeh and Sabha 2014). Owing to their significant contribution, SMEs are viewed as top contributors to the shadow economy of Jordan, with around 90% contribution (United Nations Development Programme (UNDP) 2012). In contrast, for tax non-compliance, 87% of the enterprises are small businesses, while 34% are medium businesses that report the failed payment of taxes (Young Entrepreneur Association (YEA) 2011). Additionally, the lack of accounting records among SMEs (only 14% had prepared accounting information and 40% open to reporting financial items), highlighted in Al-Bakri et al. (2014) and Al-Smirat’s (2013) studies, lays more stress on the business tax compliance in the fiscal health of the Jordanian government (Joulfaian 2009). The truth to this is evidenced by the country’s businesses collected tax revenues (Joulfaian 2000).

In theory, studies have reported different tax compliance behavior drivers (Alm and Torgler 2011), and it has been noted that the economic approach throughout history argues that deterrence has been the major strategy for the enforcement of tax compliance (Frey 2003). One of the pioneering economic studies that addressed tax non-compliance was contributed on the basis of Becker’s Model (1968), arguing that threats via legal penalties would bring about the prevention of tax crimes (Matthews and Agnew 2008). According to Becker (1968), rational behavior from the taxpayers leads to their expected used of the tax non-compliance gamble, where they determine the benefits and risks that they will face in the case of penalty and tax audit.

In the same study caliber, Allingham and Sandmo (1972) used Becker’s model deterrence theory to bring forward a tax non-compliance theory they named the A-S model, which is the pioneering model to tackle the resolution of non-adherence to tax payment. In relation to the argument, Feld et al. (2006) showed that a low level of deterrence was followed by high level of compliance in some nations, and as such, the model failed to explain the tax compliance behavior, as other factors may have had a hand in driving tax compliance that were left out from the deterrence theory. In Jackson and Milliron’s (1986) study, the authors underlined the drawbacks of the deterrence theory in its clarification of the tax compliance behavior, and highlighted 14 drivers of non-compliance that can be categorized into four main categories; namely, tax complexity, tax audit, tax penalty and tax rates), attitude and perception (tax moral, tax fairness and peer influence), demographic characteristics (age, gender and education), and non-compliance opportunity (income level, occupation and income source). All the factors were integrated into one model that was developed by Fischer et al. (1992), based on combining the approaches of sociopsychology and economics, after which the model was named the Fischer model. Several studies in literature evidenced the validity of the model (e.g., Kirchler et al. 2007; Andreoni et al. 1998).

In the present study, the author attempts to extend literature in several ways; first, prior literature on the topic focused on the tax compliance drivers by extending Fischer’s model, as in the case of Chau and Leung (2009), Chan et al. (2000) and Hanefah (1996). The extensions related to economic and socio-psychological factors, without mention of direct effect of tax service quality and indirect effect of tax knowledge on sales tax compliance among SMEs, specifically in the Jordanian context. The above-mentioned variables are pertinent to explaining sales tax compliance behavior, specifically in Jordan. Moving on to the second way, the present study contributes by determining sales tax compliance in the level of business as opposed to individual level, using Fischer’s model (Fischer et al. 1992), which entails obtaining the viewpoints of owners/managers of Jordanian SMEs. In a related study, Abdixhiku et al. (2017) revealed that tax non-compliance determinants have been under-examined, and are still lacking among businesses, despite the fact that business tax constitutes a major contribution in most countries (Nur-Tegin 2008; Crocker and Slemrod 2005). In the same token, SMEs have great opportunities to manipulate tax payment, as stated by Woodward and Tan (2015). There also seems to be great concentrated effort in literature in examining individual tax compliance, overlooking the fact that business tax compliance needs equal if not more focus (Alm and McClellan 2012). Moreover, for the consistent compliance of sales tax among SMEs, some of the characteristics of the Fischer model should be dropped, and these include non-compliance opportunity and demographic characteristics.

The third way that this study contributes to literature extension is its attempt to determine the influence of deterrence theory on sales tax compliance, in the face of the majority of studies addressing the relationship between the theory and income tax compliance, with only a few directing their examination towards sales tax (refer to Woodward and Tan 2015; Faridy et al. 2014; Webley et al. 2002). To the researcher’s best knowledge, a study has yet to be carried out to investigate the deterrence theory effects on the sales tax compliance in the context of the Middle Eastern nations, which in this case is Jordan. The fourth contribution of this study is its effort towards establishing the effects of socio-psychological factors on sales tax compliance, because although several studies have done the same, majority of them concentrated on non-economic factors effects on income tax compliance on the individual level, rather than business sales tax level. This may be exemplified by Woodward and Tan (2015), Faridy et al. (2014), Webley et al. (2002). Studies of this caliber have been conducted in the developed nations, but countries in the Middle East have rarely been the study focus.

The fifth contribution is the confirmation of sales tax compliance drivers to minimize the gap in literature as based on the study by Alm and El-Ganainy (2013), studies that examined sales tax are still limited because of the precipitated diffusion as a fundamental revenue tool used by the governments. Meanwhile, in the review of literature dedicated to tax studies, Alshira’h et al. (2016) highlighted the requirement for further studies to look into sales tax compliance, and this is particularly true in Jordan. Finally, this study is a pioneering study to examine the tax knowledge moderating effect on the relationship between sales tax compliance and its determinants. Prior studies of this caliber focused on tax knowledge as an independent variable that relates to income tax compliance (Clotfelter 1983; Kirchler and Maciejovsky 2001; Park and Hyun 2003). In other words, this is the first study to test the moderating effect of tax knowledge on the sales tax compliance-determinants of compliance relationship in the SMEs context.

2. Literature Review

Taxes are generally considered as critical contributors to the total domestic revenue all over the world, with countries largely depending on direct and indirect taxes to promote and enhance their economies (Tehulu and Dinberu 2014; Vadde 2014). In addition, tax payment compliance is compulsory for parties, notwithstanding if they are corporate or individuals—voluntary adherence to tax laws are mandatory, but in reality, some individuals always steer clear of their tax responsibilities (Kirchler et al. 2014). In this regard, tax compliance can be achieved through the participation of taxpayers in the government decisions and expenditures, as evidenced in Alm et al. (1993), and by increasing penalties and tax audit to those that shirk their tax duties (Alm and Torgler 2011). However, regardless of the promotion efforts placed on achieving tax compliance, the issue persists, and the lack of universal definition of tax compliance has been elusive in literature (Devos 2008). Differing scholars defined the concept differently—for instance, Andreoni et al. (1998) referred to tax compliance as the tendency of the taxpayers to adhere to their tax responsibilities laid down by the law of the country for the purpose of a balanced economy. Along a similar definition, Alm (1991) and Jackson and Milliron (1986) defined it as the reporting of the total incomes and payment of taxes required by the established regulations, laws and court judgments.

In the same line of study, compliance was described by Roth et al. (1989) as the taxpayer’s filing of the total required tax returns in a manner that is timely, with the returns encapsulating the right report tax liability on the basis of tax laws, regulations and court decisions applicable. Alm et al. (1993) referred to tax compliance as the act of taxpayers in declaring their taxable income accurately, in filing tax returns as well as in paying their payable taxes in the time period required. In the same line of study, Kirchler et al. (2006) compared tax compliance concept to a game that depends on the reciprocal interactions between the decisions of the taxpayer and the tax authority, as well as the trust of taxpayers in the law, and the tax system fairness. Moreover, the different measurement aspects of tax compliance was revealed in Brown and Mazur’s (2003) study, where the compliance of taxpayers was categorized into three; reporting compliance, filing compliance and payment compliance. In the context of sales tax, compliance is described as adhering to the procedures and legislation, including the actual and accurate sales paid and collected reporting, actual sales liability, payment of the total due taxes in the period laid down, and the filing of tax returns within a specific period (Nura et al. 2017).

Furthermore, tax non-compliance takes two forms, namely tax evasion and tax avoidance. Tax evasion refers to evasion of illegal and intended businesses of entities and individuals for tax due minimization by underreporting sales, income or wealth, heightening deductions, loans or dispensations, or by refraining from filing tax returns in an accurate manner (Ritsatos 2014; Alm 2012). Tax avoidance, on the other hand, is described as the inclination towards mitigating taxes through means that are legal and within the law (Slemrod 2007). Tax non-compliance also adopts different forms, comprised of failure to pay due taxes at its established period, deductions overstatement, income understatement and failing to submit tax return in the established period or even after (Kasipillai and Abdul-Jabbar 2006). According to Alshira’h et al. (2018), sales tax non-compliance is an extensive issue that entails the manipulation of sales tax invoice and modifying tax reports to achieve different targets (e.g., less sales tax payment, increased earnings and mitigated costs based on the accrued benefits) brought about by tax evasion, that hinges on the attitudes, beliefs and norms of the area. Only limited studies examined the economic factors and socio-psychological factors effects on sales tax, and as such, his study attempts to extend tax compliance literature, particularly sales tax. In the next sections, the determinants of sales tax compliance are presented.

According to Jackson and Milliron (1986), tax complexity is one of the top determinants of tax compliance behavior and in the present study, tax complexity is described as the actions taken to address business issues related to sales tax law, and these include dynamic changes, excessive details, numerous computations and distinct business records details. In Cuccia and Carnes (2001) findings, a negative relationship was supported between tax complexity and the tendency or the capability to comply with tax payment. This was mirrored in Abdul-Jabbar and Pope’s (2008) study, where the authors reported an inverse impact of increased tax complexities and tax laws amendments on the performance of SMEs. The latter showed that tax complexity frequently related to tax compliance costs, and as such, majority of businesses opt not to comply with them. However, in contrasting findings, an insignificant relationship was reported by Morse et al. (2009) and Fauvelle-Aymar (1999) between tax compliance and its complexity, while Yahaya (2015) indicated a positive relationship. Specifically, in sales tax, tax complexity lacked a significant relationship with sales tax compliance as reported by Biabani and Ramezani (2011), but other studies like Woodward and Tan (2015) reported a negative influence of tax complexity on sales tax compliance.

Moving on to another sales tax compliance determinant, tax audit protects and supports such compliance behavior according to Jackson and Milliron’s (1986) study. In the context of sales tax, it is referred to as the ability of the tax authority to promote payment of accurate sales tax among businesses, and to ensure that they register for such payment if their sales turnover is at part to or exceeds the threshold registration. In past studies, a positive relationship was found between tax audit and tax compliance, and these include Feld and Larsen (2012), Alm and McKee (2006), Pommerehne and Weck-Hannemann (1996) and Witte and Woodbury (1985), although a few of them found the absence of the relationship between the variables (e.g., Muche 2014; Tehulu and Dinberu 2014), while some others supported a negative tax audit-compliance association (e.g., Slemrod et al. 2001; Palil et al. 2012). Limited studies have been conducted in the context of sales tax in light of tax audit role on compliance, but what few studies there are supported a positive influence between the variables (e.g., Woodward and Tan 2015). However, Faridy et al. (2014) reported no significant relationship.

Another determinant of compliance worth mentioning in this study is tax ethics, with the concept of ethics being one that is full of complications, explaining the lack of universal definition—however, Jackson and Milliron (1986) referred to the concept simply as the values or principles held by the individual. Moral behavior is the intrinsic motivation that is built on moral principles and ethical values (Young et al. 2016), and in this study, sales tax moral is considered as an intrinsic motivation towards paying sales tax, stemming from the ethics compliance to pay sales tax and the conviction towards contributing to the nation’s development. In this regard, non-economic factors have the top effect on tax compliance behavior more so than economic factors, and as such, moral values were evidenced to be among the top drivers among 45 nations (Richardson 2006). Therefore, this variable has to be taken into consideration when examining tax compliance behavior (Feld and Schneider 2010). In effect, taxpayers having tax moral have a higher tendency not to adhere to tax payment when they are stressed fiscally, or when they view the evaders to be highly moral (Slemrod et al. 2001). Along a similar line of study, Fellner et al. (2013) and Ariel (2012) revealed that moral persuasion does not always result in increased compliance, and in the case of sales tax, although Woodward and Tan (2015) and Adams and Webley (2001) reported a positive tax moral-sales tax compliance relationship, this relationship still requires extensive research.

Tax fairness also falls intothe category of compliance driver, as highlighted by Jackson and Milliron (1986). The dominant argument is such that there is increasing dissatisfaction among tax administrators and taxpayers with the tax system fairness and this leads to the high rate of tax non-compliance (Chau and Leung 2009). Tax fairness are of two dimensions, namely fairness of commerce and interest received for given tax, and justice of taxpayers’ burden in connection to other tax payers (the comprehension of the vertical and horizontal tax laws fairness in the point of view of taxpayers) (Jackson and Milliron 1986). In the present work, tax fairness is defined as the distribution of sales tax registration threshold and sales tax penalties in all fairness by the tax authority entity, with fair cost manifested in registered sales tax. For this construct, Fochmann and Kroll (2015), McKerchar et al. (2013), Kirchler and Wahl (2010) and Feld and Frey (2007) reported a positive tax fairness–tax compliance behavior relationship, Benk et al. (2011) reported the lack of a significant relationship, whereas Saymeh and Sabha (2015) reported a combination of findings. However, in the sales tax context, Woodward and Tan (2015) and Adams and Webley (2001) supported a positive relationship between the two variables.

Viewed from the Fischer Model’s perspective, peer influence is an element forming the attitudes and perceptions, with the peer term referring to the associates of the taxpayer (i.e., his friends, colleagues, relatives and workmates) (Jackson and Milliron 1986). This study considers peer influence among the determinants of sales tax compliance, and defines it as the influence of significant people on the business owners in terms of sales tax compliance decision, forming their attitudes towards complying with tax payment. In literature, several studies supported a negative relationship, others supported a positive relationship, while some others supported no significant relationship. Alon and Hageman (2013) and Frey and Torgler (2007) fell in the first category of studies; Çevik and Yeniçeri (2013) and Tusubira and Nkote (2013) fell in the second category; while Wenzel (2004) and Hite (1988) fell into the last category of studies. In the sales tax case, Woodward and Tan (2015) and Adams and Webley (2001) found a positive relationship between peer influence and sales tax compliance.

Generally speaking, service quality is referred to as the level to which the service delivered in a way that meets or exceeds the needs of the customer, supported and brought about by the system management (Delone and McLean 2003). Service quality is an issue that is significant with the new public management philosophy (Brysland and Curry 2001). Similar to other public sector firms, service quality is an issue that is significant to tax offices, owing to their provision of services to taxpayers. Frecknall-Hughes and Moizer (2015) described tax service quality as the function of brand name and reputation, while Mustapha and Obid (2014) likened it to reliability, responsiveness and formativeness, forming important tax system determinants. Meanwhile, Jackson and Milliron (1986) underlined the services provided by the Internal Revenue Service (IRS) to the taxpayers in the U.S. Other studies including Boonyarat et al. (2014) found a significant influence of tax service quality on the tax collection efficiency, which in turn, impacts the satisfaction and compliance behavior among taxpayers. The inclination of the taxpayers to adhere to the tax authority decisions has been evidenced to increase if the authority views itself as a service institution that provides quality services and treats taxpayers like partners (Torgler and Schneider 2009). Taxpayers’ satisfaction with the services provided by the government and the tax authority also boosts compliance from the taxpayers to the tax regulations (Vigoda-Gadot 2007).

In other studies, enhanced tax compliance in achieving tax obligations necessitates the increase in tax service quality by the tax authorities (Al-Ttaffi and Abdul-Jabbar 2016). In other words, quality service tax provided to the taxpayers and hospitality workers would lead to their comfort along with the provision of tax information system, leading to their increasing compliance. On the other hand, if the taxpayers have a low perception of tax services quality provided by the tax authority (Alabede and Affrin 2011), the result is a negative outcome in that a positive correlation exists between perceived tax service quality and tax compliance behavior. Improving tax service quality by the tax authority will improve the compliance behavior of taxpayers through their perception of tax service quality. Finally, poor service quality will have a likelihood to lead to lowered government trust, and decreased compliance with the laws and regulations of tax. The following section presents the moderating effect of tax service quality between the determinants of sales tax compliance and compliance.

On the whole, literature shows that tax complexity, tax audit, tax ethics, tax fairness, peer influence and tax service quality had mixed findings in their relationship with tax compliance and this requires further investigation. To compound the issue further, tax compliance determinants were mostly examined in literature in light of income tax, rather than sales tax, and at the level of individual as opposed to the level of business (i.e., SMEs). Studies of this caliber also brought forward mixed findings and thus, more efforts should be dedicated towards the relationships’ examination. The findings significance is built on the theoretical underpinnings and to the researcher’s best knowledge, this is the first study to investigate the relationship between the study variables and sales tax compliance among SMEs in Jordan, and as such, this is a new contribution to literature.

Moderating role of tax knowledge

According to Fauziati et al. (2016), tax knowledge generally means the understanding of essential tax policy concepts established in the country and in this regard, the tax policies established by SMEs in the country determines the compliance behavior of the taxpayers with the tax system. SMEs tax knowledge is therefore a crucial component of the establishments’ voluntary compliance with the tax system, specifically in pinpointing their accurate tax liability (Baru 2016). Assisting taxpayers by educating them into becoming more responsible citizens has the potential to yield greater revenue for the tax administration rather than if it were spent on pursuing non-compliers (Devos 2012). Tax knowledge is a necessary component of a voluntary tax compliance system (Kasipillai and Hanefah 2000), and is particularly important in relation to determining an accurate tax liability (Saad 2014). Tax regulation knowledge promotes compliance, owing to the fact that possessing such knowledge can promote awareness of tax obligations. The majority of researchers are of the consensus that higher education does enhance taxation knowledge, without specifying the education content (e.g., Kinsey and Grasmick 1993; Song and Yarbrough 1978; Spicer and Lundstedt 1976). In the same line of study, Cullis and Lewis (1997) found low tax knowledge to be correlated with negative attitudes towards tax payment, and an argument from the author and Eriksen and Fallan (1996) revealed that the education level of the taxpayer is relevant as it contributes to the general taxation understanding in terms of laws and regulations. In the same token, Eriksen and Fallan (1996) proceeded to explain that higher tax knowledge can enhance attitudes towards tax and enhance compliance, while mitigating tax evasion. This is supported by other studies that found decreased complexity and higher tax knowledge to enhance compliance towards tax payment, and these include Clotfelter (1983), Kirchler and Maciejovsky (2001), Park and Hyun (2003), and Palil and Mustapha (2011). The authors indicated that the knowledge of tax would lead to reduced evasion of tax payment. Also, taxpayers with good knowledge of tax will positively perceive the tax system, and be more inclined to comply with its payments (Trisnawati and Nugraheni 2015).

Nevertheless, the findings reported by studies concerning the moderating role of tax knowledge on the relationship between sales tax determinants and its compliance are inconsistent. For instance, in Harris’ (2013) study, the author stated that tax knowledge lacked significant effect on the compliance behavior of taxpayers. The differences in findings may be attributed to different tax jurisdictions, because while the studies are carried out in Malaysia or Australia, Harris’ (2013) study was conducted in the US. Meanwhile, Zimbabwean SMEs have low compliance with legislation in the face of relevant information, which indicates that tax knowledge does exist among such SMEs, but non-compliance is still high. Moreover, in Bird and Zolt’s (2014) study, the author stated that tax knowledge existence constituting general knowledge, legal knowledge and technical knowledge had no significant effect on the SMEs tax compliance behavior. The author explained that taxpayers who held tax knowledge were not compliant to its payment. Comparatively, the findings reported by Alm et al. (2012) showed insignificant change in the attitude towards tax and tax behavior in the face of increased SMEs tax knowledge. In a similar study, tax knowledge did not significant impact tax compliance (Fauziati et al. 2016).

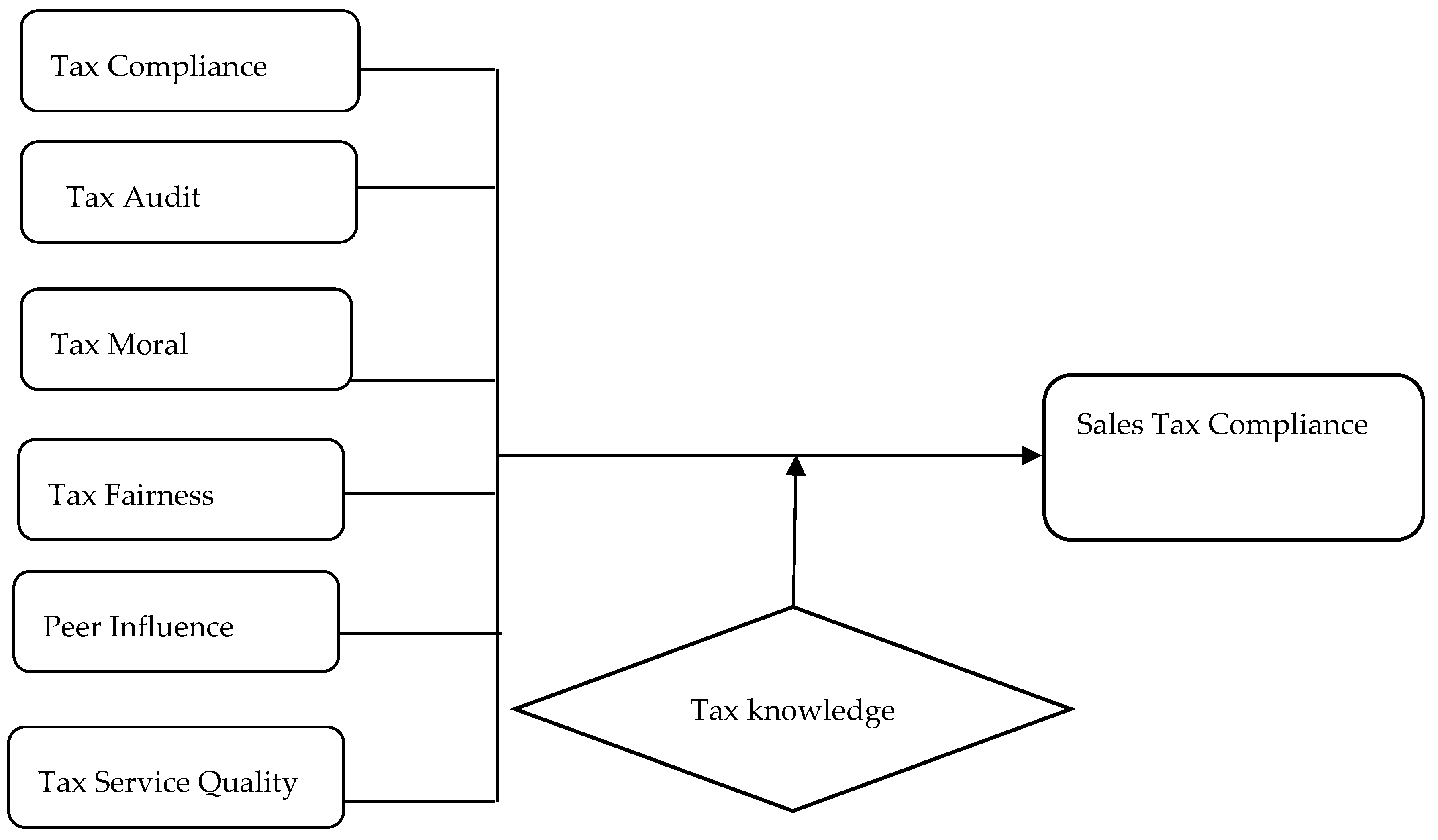

The above mixed findings call for the confirmation of the tax knowledge key role in tax compliance decisions of taxpayers. In its moderating capacity, Baron and Kenny (1986) urged the investigation towards variables moderating effects in case of inconsistencies in findings. Owing to the mixed results of the determinants of tax compliance (tax complexity, tax audit, tax moral, tax fairness, peer influence and tax service quality), with tax compliance, the presence of a moderating variable should be examined. Stated clearly, mixed relationships between economic variables and tax compliance may be explained by a moderating variable, which in this case is tax knowledge. Based on the above reviewed literature, the present study brings forward the following developed conceptual framework (Figure 1).

3. Study Implications

This study is expected to contribute to different sets of stakeholders concerning the tax compliance issue and its significance to the economy and these stakeholders include the governments, tax authorities, and policy makers, and since this study is in the context of Jordan, this is specific to Arab countries and the Middle East. The study contributes to the understanding and knowledge of sales tax compliance, providing insight for the tax authorities concerning the effect of socio-psychological factors and deterrence elements, and their effects on tax compliance behavior. The study is expected to extend literature dedicated to sales tax compliance among SMEs, specifically in Jordan, but may also have implications to all SMEs around the world. To the best of the researcher’s knowledge, this is the first study to examine sales tax compliance of SMEs in the Middle East and North Africa (MENA) region, and in Jordan. This study provides information valuable for the formulation of accurate and effective policies to enhance tax compliance, steering clear of distorted and negative decisions, and increasing tax revenue contribution to the government of Jordan, particularly at this time, when public debt and fiscal budget deficit constitute a primary issue.

4. Conclusions

Chan et al. (2000) suggested Fischer’s model as a viable conceptual framework for research on taxpayer compliance behavior. Despite a great deal of attention being focused on the tax compliance studies, very little has been related specifically to the sales tax context. Consequently, the current study enhances this knowledge by providing a comprehensive conceptual model, grounded based on the Fisher model, which was built on the integration of both deterrence and socio-psychological theories (behavioral and economic).

Sales tax in Jordan has significant contributions to the revenue of the government, making a solid niche in the government policies implementation decisions that are focused on realizing the development plans of the country. In this background, sales tax non-compliance has led to budget deficits of the government and ultimately impacts the development and development of the country. Therefore, there is a constant fight against sales tax non-compliance in an attempt to heighten its compliance level as a part of the government plan to increase tax revenues and government competencies. In relation to this, despite studies from several economic disciplines having delved into the tax compliance issue, the present study is unique in a sense that it proposes a model to explain sales tax compliance in the Jordanian SMEs context. The study extended Fischer’s model and considered the moderating role of tax knowledge on the association between socio-economic factors and sales tax compliance. The study framework has many implications to the determination of the factors that influence such compliance among SMEs that could serve several stakeholder groups. With the model’s validation, the research would adopt a positivist method in data collection process, and the findings are expected to provide insight into policy evaluation and establishment, in light of sales tax compliance among SMEs. The findings of the study are also expected to provide practical implications to realizing Jordan’s Vision 2025. Future studies may examine other factors in addition to the factors examined in the study, such as government subsidy removal and cost of sales tax compliance among the tax compliance of SMEs.

Author Contributions

A.F.A.: conceptualization, methodology, original draft preparation, writing; M.A. (Moh’d Alsqour): validation, resources; A.L.: data curation, project administration; A.A.: theoretical analysis; M.A. (Malek Alshirah): review and edit. All authors have read and agreed on the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abdixhiku, Lumir, Besnik Krasniqi, Geoff Pugh, and Iraj Hashi. 2017. Firm-level determinants of tax evasion in transition economies. Economic Systems 41: 354–66. [Google Scholar] [CrossRef]

- Abdul-Jabbar, Hijattulah, and Jeff Pope. 2008. Exploring the relationship between tax compliance costs and compliance issues in Malaysia. Journal of Applied Law and Policy 1: 1–20. [Google Scholar]

- Adams, Caroline, and Paul Webley. 2001. Small business owners’ attitudes on VAT compliance in the UK. Journal of Economic Psychology 22: 195–21. [Google Scholar] [CrossRef]

- Alabede, James, and Zaimah Zainal Affrin. 2011. Tax service quality and compliance behaviour in Nigeria: Do taxpayer’s financial condition and risk preference play any moderating role? European Journal of Economics, Finance and Administrative Sciences 35: 90–108. [Google Scholar]

- Al-Bakri, Anas, Mohammed Matar, and Abdul Naser Nour. 2014. The required information and financial statements disclosure in SMEs. Journal of Finance and Accountancy 16: 1–15. [Google Scholar]

- Allingham, Michael, and Agnar Sandmo. 1972. Income tax evasion: A theoretical analysis. Journal of Public Economics 1: 323–38. [Google Scholar] [CrossRef] [Green Version]

- Alm, James. 1991. A perspective on the experimental analysis of taxpayer reporting. The Accounting Review 66: 577–93. [Google Scholar]

- Alm, James. 2012. Measuring, explaining, and controlling tax evasion: Lessons from theory, experiments, and field studies. International Tax and Public Finance 19: 54–77. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Asmaa El-Ganainy. 2013. Value-added taxation and consumption. International Tax and Public Finance 20: 105–28. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Chandler McClellan. 2012. Tax morale and tax compliance from the firm’s perspective. Kyklos 65: 1–17. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Michael McKee. 2006. Audit certainty, audit productivity, and taxpayer compliance. Andrew Young School of Policy Studies Research 59: 801–816. [Google Scholar]

- Alm, James, and Benno Torgler. 2011. Do ethics matter? Tax compliance and morality. Journal of Business Ethics 101: 635–51. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, Betty R. Jackson, and Michael McKee. 1993. Fiscal exchange, collective decision institutions, and tax compliance. Journal of Economic Behavior & Organization 22: 285–303. [Google Scholar] [CrossRef]

- Alm, James, Erich Kirchler, Stephan Muehlbacher, Katharina Gangl, Eva Hofmann, Christoph Kogler, and Maria Pollai. 2012. Rethinking the research paradigms for analysing tax compliance behaviour. In CESifo Forum. München: IfoInstitut-Leibniz-Institutfür Wirtschaftsforschung an der Universität München, vol. 13, pp. 33–40. [Google Scholar]

- Alm, James, Jeremy Clark, and Kara Leibel. 2016. Enforcement, socioeconomic diversity, and tax filing compliance in the United States. Southern Economic Journal 82: 725–47. [Google Scholar] [CrossRef] [Green Version]

- Alon, Anna, and Amy M. Hageman. 2013. The impact of corruption on firm tax compliance in transition economies: Whom do you trust? Journal of Business Ethics 116: 479–94. [Google Scholar] [CrossRef]

- Alrousan, Mohammad Kasem, and Eleri Jones. 2016. A conceptual model of factors affecting e-commerce adoption by SME owner/managers in Jordan. International Journal of Business Information Systems 21: 269–308. [Google Scholar] [CrossRef]

- AL-Shawawreh, Taha Barakat, and Belal Yousef AL-Smirat. 2016. Economic effects of tax evasion on Jordanian economy. International Journal of Economics and Finance 8: 344–48. [Google Scholar] [CrossRef] [Green Version]

- Alshira’h, Ahmad Farhan, Hijattulah Abdul-Jabbar, and Rose Shamsiah Samsudin. 2016. Determinants of sales tax compliance in small and medium enterprises in Jordan: A call for empirical research. World Journal of Management and Behavioral Studies 4: 41–46. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan. 2018. Determinants of Sales Tax Compliance among Jordanian SMEs: The Moderating Effect of Public Governance. Unpublished Doctoral dissertation, Universiti Utara Malaysia, Changlun, Malaysia. [Google Scholar]

- Alshira’h, Ahmad Farhan, and Hijattulah Abdul-Jabbar. 2019a. The effect of tax fairness on sales tax compliance among Jordanian manufacturing SMEs. Academy of Accounting and Financial Studies Journal 23: 1–11. [Google Scholar]

- Alshira’h, Ahmad Farhan, and Hijattulah Abdul-Jabbar. 2019b. A conceptual model of sales tax compliance among Jordanian SMEs and its implications for future research. International Journal of Economics and Finance 11: 114–14. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, and Hijattulah Abdul-Jabbar. 2020. Moderating role of patriotism on sales tax compliance among Jordanian SMEs. International Journal of Islamic and Middle Eastern Finance and Management 13: 389–415. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, Hijattulah Abdul-Jabbar, and Rose Shamsiah Samsudin. 2018. Sales tax compliance model for the Jordanian Small and medium enterprises research. Journal of Advanced Research in Social and Behavioural Sciences 10: 115–30. [Google Scholar]

- Alshira’h, Ahmad Farhan, Hijattulah Abdul-Jabbar, and Rose Shamsiah Samsudin. 2019. The effect of tax moral on sales tax compliance among Jordanian SMEs. International Journal of Academic Research in Accounting, Finance and Management Sciences 9: 30–41. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, Hasan Mahmoud AL-Shatnawi, Mohammad Khalil Alsqour, and Malek Hamed Alshirah. 2020. The Influence of Tax Complexity on Sales Tax Compliance among Jordanian SMEs. International Journal of Academic Research in Accounting, Finance and Management Sciences 10: 250–60. [Google Scholar] [CrossRef]

- Al-Smirat, Belal Yousef. 2013. The use of accounting information by small and medium enterprises in South District of Jordan (An empirical study). Research Journal of Finance and Accounting 4: 169–75. [Google Scholar]

- Al-Ttaffi, Lutfi Hassen Ali, and Hijattullah Abdul-Jabbar. 2015. A conceptual framework for tax non-compliance studies in a Muslim country: A proposed framework for the case of Yemen. International Postgraduate Business Journal 7: 1–16. [Google Scholar]

- Al-Ttaffi, Lutfi Hassen Ali, and Hijattullah Abdul-Jabbar. 2016. Service quality and income tax non-compliance among small and medium enterprises in Yemen. Journal of Advanced Research in Business and Management Studies 4: 12–21. [Google Scholar]

- Al-Zoubi, A., H. Khatatba, R. B. Salama, and M. Khatataba. 2013. Methods of tax avoidance and evasion: The incapability of the Jordanian income tax law to face tax avoidance and evasion. Journal Almanara 19: 9–36. [Google Scholar]

- Andreoni, James, Brian Erard, and Jonathan Feinstein. 1998. Tax compliance. Journal of Economic Literature 36: 818–60. [Google Scholar]

- Ariel, Barak. 2012. Deterrence and moral persuasion effects on corporate tax compliance: Findings from a randomized controlled trial. Criminology 50: 27–69. [Google Scholar] [CrossRef]

- Association of Banks in Jordan. 2016. Small and Medium Enterprises in Jordan, Analysis of Supplies-Side and Demand-Side Focusing on Banking Financing. Studies Department. Available online: http://www.abj.org.jo/ar-jo/otherstudies.aspx (accessed on 9 July 2017).

- Azmi, Anna, Noor Sharoja Sapiei, Mohd Zulkhairi Mustapha, and Mazni Abdullah. 2016. SMEs’ tax compliance costs and IT adoption: The case of a value-added tax. International Journal of Accounting Information Systems 23: 1–13. [Google Scholar] [CrossRef]

- Baron, Reuben M., and David A. Kenny. 1986. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Ppersonality and SsocialPpsychology 51: 1173. [Google Scholar] [CrossRef]

- Baru, A. 2016. The impact of tax knowledge on tax compliance. Journal of Advanced Research in Business and Management Studies 6: 22–30. [Google Scholar]

- Becker, Gary. 1968. Crime and punishment: An economic approach. The Journal of Political Economy 76: 169–217. [Google Scholar] [CrossRef] [Green Version]

- Benk, Serkan, Ahmet Ferda Cakmak, and Tamer Budak. 2011. An investigation of tax compliance intention: A theory of planned behavior approach. European Journal of Economics, Finance and Administrative Sciences 28: 180–88. [Google Scholar]

- Biabani, Shaer, and Adeleh Ramezani. 2011. An investigation of the factors effective on the compliance behavior of the tax payers in the VAT system: A case study of Qazvin tax affairs general department. African Journal of Business Management 5: 10760–68. [Google Scholar]

- Bird, Richard M., and Eric M. Zolt. 2014. Redistribution via taxation: The limited role of the personal income tax in developing countries. Annals of Economics and Finance 15: 625–83. [Google Scholar]

- Bird, Richard M., Jorge Martinez-Vazquez, and Benno Torgler. 2008. Tax effort in developing countries and high income countries: The impact of corruption, voice and accountability. Economic Analysis and Policy 38: 55–71. [Google Scholar] [CrossRef] [Green Version]

- Boonyarat, Nichapat, Syed Sofian, and Wanida Wadeecharoen. 2014. The antecedents of taxpayers’ compliance behavior and the effectiveness of Thai local government levied tax. International Business Management 9: 23–39. [Google Scholar]

- Brown, Robert E., and Mark J. Mazur. 2003. IRS’s comprehensive approach to compliance measurement. National Tax Journal 56: 689–700. [Google Scholar] [CrossRef] [Green Version]

- Brysland, Alexandria, and Adrienne Curry. 2001. Service improvements in public services using SERVQUAL. Managing Service Quality: An International Journal 11: 389–401. [Google Scholar] [CrossRef]

- Çevik, Savaş, and Harun Yeniçeri. 2013. The relationship between social norms and tax compliance: The moderating role of the effectiveness of tax administration. International Journal of Economic Sciences 2: 166–80. [Google Scholar]

- Chan, Chris W., Coleen S. Troutman, and David O’Bryan. 2000. An expanded model of taxpayer compliance: Empirical evidence from the United States and Hong Kong. Journal of International Accounting, Auditing and Taxation 9: 83–103. [Google Scholar] [CrossRef]

- Chau, K. K. G., and Patrick Leung. 2009. A critical review of Fischer tax compliance model: A research synthesis. Journal of Accounting and Taxation 1: 34–40. [Google Scholar]

- Clotfelter, Charles. 1983. Tax evasion and tax rates: An analysis of individual returns. The Review of Economics and Statistics 65: 363–73. [Google Scholar] [CrossRef]

- Crocker, Keith J., and Joel Slemrod. 2005. Corporate tax evasion with agency costs. Journal of Public Economics 89: 1593–610. [Google Scholar] [CrossRef] [Green Version]

- Cuccia, Andrew D., and Gregory A. Carnes. 2001. A closer look at the relation between tax complexity and tax equity perceptions. Journal of Economic Psychology 22: 113–40. [Google Scholar] [CrossRef]

- Cullis, John G., and Alan Lewis. 1997. Why people pay taxes: From a conventional economic model to a model of social convention. Journal of Economic Psychology 18: 305–21. [Google Scholar] [CrossRef]

- Das-Gupta, Arindam, and Ira Gang. 2003. Value added tax evasion, auditing and transactions matching. In Institutional Elements of Tax Design and Reform. Edited by John Maclarn. Washington, DC: The World Bank, pp. 25–48. [Google Scholar]

- Delone, William H., and Ephraim R. McLean. 2003. The DeLone and McLean model of information systems success: A ten-year update. Journal of Management Information Systems 19: 9–30. [Google Scholar] [CrossRef]

- Devos, Ken. 2008. Tax evasion behaviour and demographic factors: An exploratory study in Australia. Revenue Law Journal 18: 1–45. [Google Scholar]

- Devos, Ken. 2012. A comparative study of compliant and non-compliant individual taxpayers in Australia. Journal of Business and Policy Research 7: 180–96. [Google Scholar]

- Eriksen, Knut, and Lars Fallan. 1996. Tax knowledge and attitudes towards taxation; A report on a quasi-experiment. Journal of Economic Psychology 17: 387–402. [Google Scholar] [CrossRef]

- Faridy, Nahida, Richard Copp, Brett Freudenberg, and Tapan Sarker. 2014. Complexity, compliance costs and non compliance with VAT by small and medium enterprises in Bangladesh: Is there a relationship. Australian Tax Forum 29: 281–329. [Google Scholar] [CrossRef]

- Faridy, Nahida, Brett Freudenberg, Tapan Sarker, and Richard Copp. 2016. The hidden compliance cost of VAT: An exploration of psychological and corruption costs of VAT in a developing country. eJournal of Tax Research 14: 166–205. [Google Scholar]

- Fauvelle-Aymar, Christine. 1999. The political and tax capacity of government in developing countries. Kyklos 52: 391–413. [Google Scholar] [CrossRef]

- Fauziati, Penerbit, A. F. Minovia, R. Y. Muslim, and R. Nasrah. 2016. The impact of tax knowledge on tax compliance case study in kotapadang, Indonesia. Journal of Advanced Research in Business and Management Studies 2: 22–30. [Google Scholar]

- Feinstein, Jonathan S. 1991. An econometric analysis of income tax evasion and its detection. The RAND Journal of Economics 22: 14–35. [Google Scholar] [CrossRef]

- Feld, Lars P., and Bruno S. Frey. 2007. Tax compliance as the result of a psychological tax contract: The role of incentives and responsive regulation. Law and Policy 29: 102–20. [Google Scholar] [CrossRef] [Green Version]

- Feld, Lars P., and Claus Larsen. 2012. Self-perceptions, government policies and tax compliance in Germany. International Tax and Public Finance 19: 78–103. [Google Scholar] [CrossRef]

- Feld, Lars P., and Friedrich Schneider. 2010. Survey on the Shadow Economy and Undeclared Earnings in OECD Countries. German Economic Review 11: 109–49. [Google Scholar] [CrossRef]

- Feld, Lars P., Bruno S. Frey, and Benno Torgler. 2006. Rewarding Honest Taypayers? Evidence on the Impact of Rewards from Field Exeperiments. Working Paper. Basel and Zürich: Center for Research in Economics, Management and the Arts. [Google Scholar]

- Fellner, Gerlinde, Rupert Sausgruber, and Christian Traxler. 2013. Testing enforcement strategies in the field: Threat, moral appeal and social information. Journal of the European Economic Association 11: 634–60. [Google Scholar] [CrossRef] [Green Version]

- Fischer, Carol M., Martha Wartick, and Melvin M. Mark. 1992. Detection probability and taxpayer compliance: A review of the literature. Journal of Accounting Literature 11: 1–25. [Google Scholar]

- Fochmann, Martin, and Eike B. Kroll. 2015. The effects of rewards on tax compliance decisions. Journal of Economic Psychology 52: 38–55. [Google Scholar] [CrossRef] [Green Version]

- Franzoni, Luigi A. 1999. Tax evasion and tax compliance. In Encyclopedia of Law and Economics. Edited by B. Bouckaert and G. De Geest. Cheltenham: Edward Elgar, pp. 52–94. [Google Scholar]

- Frecknall-Hughes, Jane, and Peter Moizer. 2015. Assessing the quality of services provided by UK tax practitioners. eJournal of Tax Research 13: 51. [Google Scholar]

- Frey, Bruno S. 2003. Deterrence and tax morale in the European Union. European Review 11: 385–406. [Google Scholar] [CrossRef]

- Frey, Bruno S., and Benno Torgler. 2007. Tax morale and conditional cooperation. Journal of Comparative Economics 35: 136–59. [Google Scholar] [CrossRef] [Green Version]

- Giesecke, James, and Nhi Hoang Tran. 2012. A general framework for measuring VAT compliance rates. Applied Economics 44: 1867–89. [Google Scholar] [CrossRef] [Green Version]

- Hanefah, H. 1996. An Evaluation of the Malaysian Tax Administrative System and Tax Payers’ Perceptions towards Assessment Systems, Tax Law Fairness, and Tax Law Complexity. Ph.D. thesis, Universiti Utara Malaysia, Bukit KayuHitam, Malaysia. Unpublished. [Google Scholar]

- Hansford, Ann, and John Hasseldine. 2012. Tax compliance costs for small and medium sized enterprises: The case of the UK. eJournal of Tax Research 10: 288–303. [Google Scholar]

- Harris, Thomas Donald. 2013. The effect of tax knowledge on individual’s perceptions of fairness and compliance with federal income tax system: An empirical study. Unpublished manuscript. South Carolina: University of South Carolina. [Google Scholar]

- Hite, Peggy A. 1988. The effect of peer reporting behavior on taxpayer compliance. Journal of the American Taxation Association 9: 47–64. [Google Scholar]

- Jackson, Betty R., and Valerie C. Milliron. 1986. Tax compliance research: Findings, problems and prospects. Journal of Accounting Literature 5: 125–65. [Google Scholar]

- Jordan Independent Economic Watch. 2014. Tax Burden in Jordan, Reality & Prospects. Available online: http://www.identity-center.org (accessed on 12 July 2018).

- Joulfaian, David. 2000. Corporate income tax evasion and managerial preferences. Review of Economics and Statistics 82: 698–701. [Google Scholar] [CrossRef]

- Joulfaian, David. 2009. Bribes and business tax evasion. European Journal of Comparative Economics 6: 227–44. [Google Scholar]

- Kasipillai, Jeyapalan, and Hijattullah Abdul-Jabbar. 2006. Gender and ethnicity differences in tax compliance. Asian Academy of Management Journal 11: 73–88. [Google Scholar]

- Kasipillai, Jeyapalan, and Mustafa Mohd Hanefah. 2000. Tax professionals’ views on self assessment system. Analisis 7: 107–22. [Google Scholar]

- Kinsey, Karyl A., and Harold G. Grasmick. 1993. Did the Tax Reform Act of 1986 improve compliance? Three studies of pre-and post-TRA compliance attitudes. Law & Policy 15: 293–325. [Google Scholar]

- Kirchler, Erich, and Boris Maciejovsky. 2001. Tax compliance within the context of gain and loss situations, expected and current asset position, and profession. Journal of Economic Psychology 22: 173–94. [Google Scholar] [CrossRef]

- Kirchler, Erich, and Ingrid Wah. 2010. Tax compliance inventory TAX-I: Designing an inventory for surveys of tax compliance. Journal of Economic Psychology 31: 331–46. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kirchler, Erich, Apolonia Niemirowski, and Alexander Wearing. 2006. Shared subjective views, intent to cooperate and tax compliance: Similarities between Australian taxpayers and tax officers. Journal of Economic Psychology 27: 502–17. [Google Scholar] [CrossRef]

- Kirchler, Erich, Stephan Muehlbacher, Barbara Kastlunger, and Ingrid Wahl. 2007. Why Pay Taxes? A Review of Tax Compliance Decisions. International Studies Program Working Paper. Atlanta: Georgia State University. [Google Scholar]

- Kirchler, Erich, Christoph Kogler, and Stephan Muehlbacher. 2014. Cooperative tax compliance: From deterrence to deference. Current Directions in Psychological Science 23: 87–92. [Google Scholar] [CrossRef]

- Lee, Dongwon, Dongil Kim, and Thomas E. Borcherding. 2013. Tax structure and government spending: Does the value-added tax increase the size of government? National Tax Journal 66: 541–70. [Google Scholar] [CrossRef] [Green Version]

- Lutf, Abd Alwali, Kamil Md Idris, and Rosli Mohamad. 2016. The influence of technological, organizational and environmental factors on accounting information system usage among Jordanian small and medium-sized enterprises. International Journal of Economics and Financial Issues 6: 240–48. [Google Scholar]

- Lutfi, Abd Alwali, Kamil Md Idris, and Rosli Mohamad. 2017. AIS usage factors and impact among Jordanian SMEs: The moderating effect of environmental uncertainty. Journal of Advanced Research in Business and Management Studies 6: 24–38. [Google Scholar]

- Matthews, Shelley Keith, and Robert Agnew. 2008. Extending deterrence theory: Do delinquent peers condition the relationship between perceptions of getting caught and offending? Journal of Research in Crime and Delinquency 45: 91–118. [Google Scholar] [CrossRef]

- McKerchar, Margaret, Kim Bloomquist, and Jeff Pope. 2013. Indicators of tax morale: An exploratory study. eJournal of Tax Research 11: 5–22. [Google Scholar]

- Ministry of Finance. 2016. General Government Financial Statements. General Government Bulletins for December. Available online: http://www.mof.gov.jo (accessed on 20 February 2018).

- Morse, Susan Cleary, Stewart Karlinsky, and Joseph Bankman. 2009. Cash businesses and tax evasion. Stanford Law and Policy Review 20: 1–67. [Google Scholar]

- Muche, B. 2014. Determinants of tax payer’s voluntary compliance with taxation in east Gojjam-Ethiopia. Research Journal of Economics &Businrss Studies 3: 41–50. [Google Scholar]

- Mustapha, Bojuwon, and Siti Normala Bt Sheikh Obid. 2014. The influence of technology characteristics towards an online tax system usage: The case of Nigerian self-employed taxpayer. International Journal of Computer Applications 105: 30–36. [Google Scholar]

- Nura, Mohammed, Hijattulah Abdul-Jabbar, and Idawati Ibrahim. 2017. VAT compliance and the influence of political and business environment: A proposed framework for Nigerian SMEs. Asian Journal of Business Management Studies 8: 13–20. [Google Scholar]

- Nur-Tegin, Kanybek. 2008. Determinants of business tax compliance. The BE Journal of Economic Analysis & Policy 8: 1–28. [Google Scholar] [CrossRef]

- Palil, Mohd Rizal, and Ahmad Fariq Mustapha. 2011. Determinants of tax compliance in Asia: A case of Malaysia. European Journal of Social Sciences 24: 7–32. [Google Scholar]

- Palil, M. R., N. H. M. Zain, and S. M. Faizal. 2012. Political affiliation and tax compliance in Malaysia. Humanities and Social Sciences Review 1: 395–402. [Google Scholar]

- Park, Chang-Gyun, and Jin Kwon Hyun. 2003. Examining the determinants of tax compliance by experimental data: A case of Korea. Journal of Policy Modeling 25: 673–84. [Google Scholar] [CrossRef]

- Pommerehne, Werner W., and Hannelore Weck-Hannemann. 1996. Tax rates, tax administration and income tax evasion in Switzerland. Public Choice 88: 161–70. [Google Scholar] [CrossRef]

- Randlane, Kerly. 2016. Tax Compliance as a system: Mapping the field. International Journal of Public Administration 39: 515–25. [Google Scholar] [CrossRef]

- Richardson, Grant. 2006. Determinants of tax evasion: A cross-country investigation. Journal of International Accounting, Auditing and Taxation 15: 150–69. [Google Scholar] [CrossRef]

- Ritsatos, Titos. 2014. Tax evasion and compliance: From the neo classical paradigm to behavioural economics, a review. Journal of Accounting & Organizational Change 10: 244–62. [Google Scholar] [CrossRef]

- Roth, Jeffrey A., John T. Scholz, and Ann Dryden Witte. 1989. Taxpayer Compliance, Volume 1: An Agenda for Research. Philadelphia: University of Pennsylvania Press. [Google Scholar] [CrossRef]

- Saad, Natrah. 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-Social and Behavioral Sciences 109: 1069–75. [Google Scholar] [CrossRef] [Green Version]

- Samuel, Mutarindwa, and Rutikanga Jean De Dieu. 2014. The impact of taxpayers’ financial statements audit on tax revenue growth. International Journal of Business and Economic Development 2: 51–60. [Google Scholar]

- Sawyer, Adrian. 2014. Comparing the Swiss and United Kingdom cooperation agreements with their respective agreements under the Foreign account tax compliance act. eJournal of Tax Research 12: 285–318. [Google Scholar]

- Saymeh, Abdul Aziz Farid, and Sulieman Abu Sabha. 2014. Assessment of Small Enterprise Financing, case of Jordan. Global Journal of Management and Business Research 14: 6–18. [Google Scholar]

- Saymeh, Abdul Aziz Farid, and Sulieman Abu Sabha. 2015. A proposed model of non-compliance behaviour on excise duty: A moderating effects of tax agents. Procedia—Social and Behavioral Sciences 2011: 299–305. [Google Scholar] [CrossRef] [Green Version]

- Slemrod, Joel. 2007. Cheating ourselves: The economics of tax evasion. The Journal of Economic Perspectives 21: 25–48. [Google Scholar] [CrossRef] [Green Version]

- Slemrod, Joel, Marsha Blumenthal, and Charles Christian. 2001. Taxpayer response to an increased probability of audit: Results from a controlledexperiement in Minnesota. Journal of Public Economics 79: 455–83. [Google Scholar] [CrossRef] [Green Version]

- Song, Young-dahl, and Tinsley E. Yarbrough. 1978. Tax ethics and taxpayer attitudes: A survey. Public Administration Review 38: 442–52. [Google Scholar] [CrossRef]

- Spicer, Michael W., and Scott B. Lundstedt. 1976. Understanding tax evasion. Public Finance = Finances Publiques 31: 295–305. [Google Scholar]

- Tehulu, Tilahun Aemiro, and Yidersal Dagnaw Dinberu. 2014. Determinants of tax compliance behavior in Ethiopia: The case of bahirdar city taxpayers. Journal of Economics and Sustainable Development 5: 268–74. [Google Scholar]

- Torgler, Benno, and Friedrich Schneider. 2009. The impact of tax morale and institutional quality on the shadow economy. Journal of Economic Psychology 30: 228–45. [Google Scholar] [CrossRef] [Green Version]

- Trisnawati, Rina, and Destia Nugraheni. 2015. The analysis of information asymmetry, profitability, and deferred tax expense on integrated earning management. South East Asia Journal of Contemporary Business, Economics and Law 7: 17–24. [Google Scholar]

- Tusubira, Festo Nyende, and Isaac Nabeta Nkote. 2013. Social Norms, taxpayers’ morale and tax compliance: The case of small business enterprises in Uganda. Journal of Accounting Taxation and Performance Evaluation 2: 1–10. [Google Scholar]

- United Nations Development Programme. 2012. The Panoramic Study of the Informal Economy in Jordan. Ministry of Planning. Available online: http://inform.gov.jo/en-us/By-Date/Report-Details/ArticleId/37/mid/420/Article-Category/205/The-Panoramic-Study-of-the-Informal-Economy-in-Jordan (accessed on 23 September 2017).

- Vadde, Suresh. 2014. Compliance and non compliance behavior of business profit taxpayers’ towards the tax system: A case study of Mekelle city. Scholars Journal of Economics, Business and Management 1: 525–31. [Google Scholar] [CrossRef]

- Varvarigos, Dimitrios. 2016. Cultural norms, the persistence of tax evasion, and economic growth. Economic Theory 21: 1–35. [Google Scholar] [CrossRef] [Green Version]

- Vigoda-Gadot, Eran. 2007. Citizens’ perceptions of politics and ethics in public administration: A five-year national study of their relationship to satisfaction with services, trust in governance, and voice orientations. Journal of Public Administration Research and Theory 17: 285–305. [Google Scholar] [CrossRef]

- Webley, Paul, Carolyn Adams, and Henk Elffers. 2002. VAT Compliance in the United Kindom. (Working Paper No. 41). Canberra: Centre for Tax System Integrity Research School of Social Sciences, Australian National University. [Google Scholar]

- Wenzel, MichaelM. 2004. An analysis of norm processes in tax compliance. Journal of Economic Psychology 25: 213–28. [Google Scholar] [CrossRef] [Green Version]

- Witte, Ann D., and Diane F. Woodbury. 1985. The effect of tax laws and tax administration on tax compliance: The case of the US individual income tax. National Tax Journal 38: 1–13. [Google Scholar]

- Woodward, Lynley, and Lin Mei Tan. 2015. Small business owners attitudes toward GST compliance: A preliminary study. Australian Tax Forum 30: 517–50. [Google Scholar] [CrossRef]

- Yahaya, Lawan. 2015. The perception of corporate taxpayers’ compliance behaviour under self-assessment system in Nigeria. Journal of Management Research 7: 343. [Google Scholar] [CrossRef] [Green Version]

- Young Entrepreneur Association. 2011. Small and Medium Business Agenda. Available online: http://www.cipe-Arabia.org (accessed on 20 August 2018).

- Young, Angus, Lawrence Lei, Brossa Wong, and Betty Kwok. 2016. Individual tax compliance in China: A review. International Journal of Law and Management 58: 1–12. [Google Scholar] [CrossRef]

Figure 1.

Proposed research framework for sales tax compliance.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Alshira’h, A.F.; Alsqour, M.; Lutfi, A.; Alsyouf, A.; Alshirah, M. A Socio-Economic Model of Sales Tax Compliance. Economies 2020, 8, 88. https://0-doi-org.brum.beds.ac.uk/10.3390/economies8040088

AMA Style

Alshira’h AF, Alsqour M, Lutfi A, Alsyouf A, Alshirah M. A Socio-Economic Model of Sales Tax Compliance. Economies. 2020; 8(4):88. https://0-doi-org.brum.beds.ac.uk/10.3390/economies8040088

Chicago/Turabian StyleAlshira’h, Ahmad Farhan, Moh’d Alsqour, Abdalwali Lutfi, Adi Alsyouf, and Malek Alshirah. 2020. "A Socio-Economic Model of Sales Tax Compliance" Economies 8, no. 4: 88. https://0-doi-org.brum.beds.ac.uk/10.3390/economies8040088

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.