Blockchain Technology for Secure Accounting Management: Research Trends Analysis

by

, , and

, , and

Emilio Abad-Segura

1,* ,

,

Alfonso Infante-Moro

2 ,

,

Mariana-Daniela González-Zamar

3,* and

Eloy López-Meneses

4,5

1

Department of Economics and Business, University of Almeria, 04120 Almeria, Spain

2

Department of Financial Economics, Accounting and Operations Management, University of Huelva, 21071 Huelva, Spain

3

Department of Education, University of Almeria, 04120 Almeria, Spain

4

Department of Education and Social Psychology, Pablo de Olavide University, 41013 Sevilla, Spain

5

Research Institute in Social Sciences and Education, Vice-Rectory for Research and Postgraduate, University of Atacama, Copiapó 1530000, Chile

*

Authors to whom correspondence should be addressed.

Mathematics 2021, 9(14), 1631; https://0-doi-org.brum.beds.ac.uk/10.3390/math9141631

Submission received: 22 June 2021

/

Revised: 8 July 2021

/

Accepted: 8 July 2021

/

Published: 10 July 2021

(This article belongs to the Special Issue Uncertainty Quantification Techniques in Statistics, Machine Learning and FinTech)

Abstract

:The scope of blockchain technology, initially associated with the cryptocurrency Bitcoin, is greater due to the multiple applications in various disciplines. Its use in accounting lies mainly in the fact that it reduces risks and the eventuality of fraud, eliminates human error, promotes efficiency, and increases transparency and reliability. This means that different economic sectors assume it as a recording and management instrument. The aim is to examine current and emerging research lines at a global level on blockchain technology for secure accounting management. The evolution of the publication of the number of articles between 2016 and 2020 was analyzed. Statistical and mathematical techniques were applied to a sample of 1130 records from the Scopus database. The data uncovered a polynomial trend in this period. The seven main lines of work were identified: blockchain, network security, information management, digital storage, edge computing, commerce, and the Internet of Things. The ten most outstanding emerging research lines are detected. This study provides the past and future thematic axes on this incipient field of knowledge, which is a tool for decision-making by academics, researchers, and directors of research investment programs.

1. Introduction

In recent years, global and multidisciplinary interest in Blockchain (BC) technology has grown exponentially since the Bitcoin cryptocurrency adopted it in 2008 [1]. In effect, BC refers to chained blocks of information, that is, pages of a book accounting system digitally signed in the internet environment that supports digital payment transactions made with cryptocurrencies [2].

In its most primary context, BC refers to an open information and accounting system, which allows the control and validation of payment transactions with the particularity of being decentralized, avoiding duplication or digital multiplication of currencies. It has a great potential for diffusion and adaptation, its costs are low and its easy accessibility and high security are revolutionizing the way of recording private transactions [3,4].

Beyond cryptocurrencies, its study as a tool in multiple fields has been developed with multiple applications, such as decentralized document registration, medical records, property registration, monitoring of production processes, customs control, voting systems, or digital identity [5,6,7,8].

In BC, each record (transactions or economic events) is kept in all the nodes of a network permanently and unalterable, with a chronological order and using cryptographic techniques to protect the data. These registers are inserted in a block with a protocol that entails their verification and the consensus of all the users of the network. To do this, a series of checks are carried out, such as the absence of duplication and it is chained with the preceding blocks. Therefore, a distributed and replicated database is created in multiple nodes of the network, where each block confirms and links the previous one. Hence, the traceability of the transaction can be tracked with the entire history since its creation, with the assurance that the data could not be altered or modified. To manipulate the data, the consensus of the entire network would be required. Any node can verify that the transaction or event has taken place on the indicated date [9].

In 2005, researcher Ian Grigg developed what can be considered the first application of BC in accounting [10]. In this study, he proposes triple-entry accounting based on distributed ledger technology (DLT), that is, it incorporates value units (tokens) in a third information entry that is registered on the network through the encrypted BC [11]. These tokens can represent cryptocurrencies or with any accounting fact, good, right or obligation. In this way, if accounting can be implemented using BC technology, the accounting model can be extended to a greater scope of information, faster access to it, more security and for the public administration, it would be an instrument towards transparency.

The registration in distributed, irrevocable, and verified databases on the network, with a cryptographic digital signature, makes the BC allow the authenticity of the facts and the accounting information more reliable and transparent. This circumstance has notable importance in the audit of the annual accounts since the execution of smart contracts allows automating processes [12].

In the digitization of accounting, BC and artificial intelligence represent a transformative impulse in accounting processes and in aspects of control and verification. The accounting system is based on control mechanisms carried out manually at times, which requires duplicate efforts, such as reconciliation [13,14]. In short, with the distributed ledger, control and reconciliation actions between the companies are eliminated and, in addition, with the elimination of intermediaries, the results translate into a reduction in time and costs, with an improvement in the efficiency of the system.

The motivation of this work is to identify the main thematic axes that have been developed and detect emerging ones in the research of BC technology for secure accounting management.

Accordingly, the main objective is to examine the current and emerging lines of research at an international level on BC technology for secure accounting management, between 2016 and 2020, that is, from the publication of the first article (2016) until the last full year (2020). To infer adequate judgments and conclusions, mathematical and statistical techniques were applied to a sample composed of 1130 articles selected from Elsevier’s Scopus database. The importance of these mathematical methods and statistical analysis is since these make it possible to obtain reliable indicators, associated with quality. It involves obtaining information from the documents published by the driving agents, that is, with greater scientific productivity of a certain research topic.

The contribution of this work to the field of knowledge on BC technology for secure accounting management consists in that the findings achieved are useful for the actors working on this research topic, since they require an analysis of past research and an approach to the emerging, such as academics, researchers, research institutions, universities, investment planners, or BC developers.

The rest of the study is structured as follows. Section 2 presents the relevant literature. Section 3 shows the inclusion/exclusion process of the sample data and the applied methodology. Section 4 includes the evolution of scientific production, the analysis of the research lines and the description of future thematic axes, all discussed in a broad context. Finally, Section 5 presents the conclusions.

2. Literature Review

Section 2 is the result of an initial analysis of the scientific literature on BC technology for secure accounting management, while its purpose is to show a guide and conceptual framework for global research, which will allow the interpretation of the results. Hence, to consolidate the purpose of this research, the correspondence between the variables that conceptualize this field of knowledge is exposed. After reviewing the literature and identifying the study variables, the research questions are presented.

Table 1 shows the 15 main articles selected after reviewing the literature, establishing a theoretical framework and terminology on the research topic. The analysis of these has allowed determining the problem, the purpose, and the objective of the research, as well as to obtain the key terms (BC, accounting, and management) to apply the methodology specified in the following Section 3. For each of the articles, the following are indicated: reference, year of publication, title, author or authors, journal where they were published, thematic areas of the journal according to the Scopus database, and the key terms that allow defining the objective of the research.

As can be seen in Table 1, during the analyzed period, the selected records have been analyzing the study variables and the journals where they have been published, they considered that the articles related to this topic are linked both to Engineering; Mathematics and Computer Science as with Social Sciences; Business, Management and Accounting; Economics, Econometrics and Finance; Decision Sciences; Arts and Humanities. This varied classification allows to promote discipline, causes synergies, and contributes to the training of academics and researchers.

The previous review provided definitions of the basic concepts/variables on this research topic. Reflections on the terms used in the context of this research are included, which have shaped this field of study. Moreover, with the intention of avoiding different interpretations, the basic concepts that will be used in the development of the study are defined.

2.1. Blockchain Technology

BC is a database shared and distributed among different participants, decentralized, cryptographically protected (it cannot be altered) and organized into blocks of mathematically related transactions [16,30]. In this sense, BC is a system that works like a book for the recording of transactions and allows elements that do not trust each other to maintain a consensus on the existence, status, and evolution of shared factors. This consensus is the key to BC, because it allows all participants to trust the information that is registered in this database. In this way, BC is based on trust and consensus, that is, it does not need a central entity to supervise or validate the processes that are carried out, and it is built from a global network of computers that manage a huge database of data [31,32,33]. This can be (i) public: open to the participation of anyone who wishes (e.g., Bitcoin or Ethereum); or (ii) private: limited to some participants (e.g., Hyperledger, R3 or Ripple).

This digital transfer system is based on the distribution of information (digital data) in a multitude of independent nodes (participants, user computers or miners), which collectively register, validate, and date the information (token) anonymously, excluding intermediaries and preventing the information from being deleted. BC systems use public key cryptography (asymmetric cryptography) to create a time-stamped, immutable, stub-only content chain. Copies of the BC are distributed to each participating node on the network [16,34,35].

In 2009, BC was popularized with Satoshi Nakamoto’s paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System” [36], where a BC data structure as a ledger to securely store transaction history of Bitcoin was proposed. The idea behind BC goes back to a document by Haber and Stornetta in 1991, titled “How to Time-Stamp a Digital Document” [37], where a method for the secure time-stamping of digital documents was proposed, instead of a digital money scheme, to give an approximate idea of when a document was created. With time stamping, the document creation order is accurately reflected.

BCs oriented to cash transactions were made possible by distribution, no one is in control themselves, and this distribution was made possible through consensus algorithms, and a noise reduction mechanism. Thereby, according to [36], to gain the right to propose to other nodes a new piece of information that will be saved in the chain, a computationally complex and expensive puzzle (hash puzzle) must be solved and the proof of that is resolved. This information is then validated by each node on the network based on the rules of a consensus protocol and all nodes that follow the same protocol will eventually store the piece of information and build the same chain.

Although initially BC technology was created for digital currency trading, technologists understood that there are other ways to employ it. BC draws attention due to its unalterable nature to the benefits associated with security and privacy, that is, its media impact is based on the elimination of third factions (decentralization), increased transparency and security [26]. For this reason, BC is a concept that raises an enormous revolution in the economy and in other areas, and its implementation provides practical solutions for functional business problems.

2.2. Secure Accounting Management

In Accounting, it is key to both maximize security management and reduce risk [38,39]. Computer accounting systems are the main targets due to the value of the information of the companies that they handle, such as, financial records, email addresses, addresses, telephone numbers, bank accounts or credit card information [40,41]. A maxim among corporate accounting professionals is to avoid hacker attacks, since computer accounting systems are packed with information that attackers covet. A good deal of business accounting software products is designed to be secure, and it is critical that security data are protected by a strong password. The principle of BC is decentralized accounting, through which the participants in the network approve, validate, and record the transactions, instead of the responsibility being reincorporated in a single entity.

Likewise, accounting departments archive their documents online for speed, efficiency, and convenience, but the difference with other data is that accountants have confidential customer data. Certain common practices are highly insecure, such as downloading, local storage, or shared internally and with customers via email, exposing sensitive data and allowing hackers to easily steal it. Accountants should share documents with their clients from a secure and encrypted warehouse, rather than using email, and be wary of spear phishing and phishing attacks. When the login credentials of a company’s employees are stored in a password manager, they are less likely to fall for a phishing scam, thus logging in with only the hidden URL and passwords [42,43].

With companies increasing BYOD (bring your own device) policies and the introduction of smartphones and tablets, companies must ensure that an employee’s use of their mobile device does not weaken their cybersecurity posture. Accounting firms should never access or store sensitive information on a mobile device unless it is protected by two-factor authentication [44,45].

Telecommuting has increased dramatically across all industries, especially since the COVID-19 pandemic [46], by expecting employees to work from any location, creating opportunities for data breaches. Accountants should not use public WiFi (Wireless Fidelity) to access or exchange confidential information, as hackers easily access public data streams and intercept data exchanged in plain text format [47]. The most reliable use of using a public computer is with VPN (Virtual Private Network) software, for end-to-end encryption [48,49].

In this tidal wave of insecurity and fraud is where BC arises, a digital information record that is assimilated to an accounting ledger, so that the data that are entered are permanent, that is, once a transaction is written, it is not it can be deleted or modified [17]. This is achieved by replicating the information record on several computers, so that any alteration requires modifying the accounting book of each of the network participants. Hence, with BC, accessible, fast, secure and interconnected public records are created that people can use in different sectors (finance, insurance, citizen participation, judicial or commerce). This BC technology allows overcoming the barriers built by mistrust [50,51].

2.3. Research Questions

The literature reviewed contains various studies that propose and evaluate this purpose, so that the research questions (RQi, where i = 1,2,3) that arise are:

- RQ1:

- What has been the evolution of scientific production in this field of knowledge between 2016 and 2020?

- RQ2:

- What were the main lines of research studied in the 2016–2020 period?

- RQ3:

- What are the emerging research directions on this topic?

These RQ are the formalized expression of the problems or concerns that the research aims to solve. Likewise, the formulation of the RQ are based on the research framework due to their feasibility, interest, novelty and relevance [52].

3. Data and Methods

Section 3 describes (i) the statistical techniques and mathematics used in this research; (ii) the data inclusion/exclusion criteria to determine the sample of articles analyzed; and (iii) the data processing linked to the objective of this study.

3.1. Data Collection

In this analysis of the scientific literature, mathematical and statistical techniques are applied to examine the evolution of its activity. Hence, the objective of this methodology is to search, identify, and analyze trends in a field of study [53]. Bibliometrics has made it possible to review scientific knowledge from numerous scientific fields [54,55,56]. The motivation was to show a vision of the development of research related to BC technology for secure accounting management.

Currently, bibliographic databases provide the quality and validity of an analysis of any scientific field. Numerous works, to analyze the most appropriate scientific database, in terms of comparison and stability of the statistics, to be used in bibliometric studies, have focused on Web of Science (WoS) and Scopus. The conclusions of these studies indicate the use of a database will depend fundamentally on the (i) focus of the analysis; (ii) discipline; and (iii) the time horizon of the study [57]. The two databases were studied and considering the same study variables, the volume of records in WoS (Core Collection) (190) was lower than in Scopus (1130); therefore, Elsevier’s Scopus database was used.

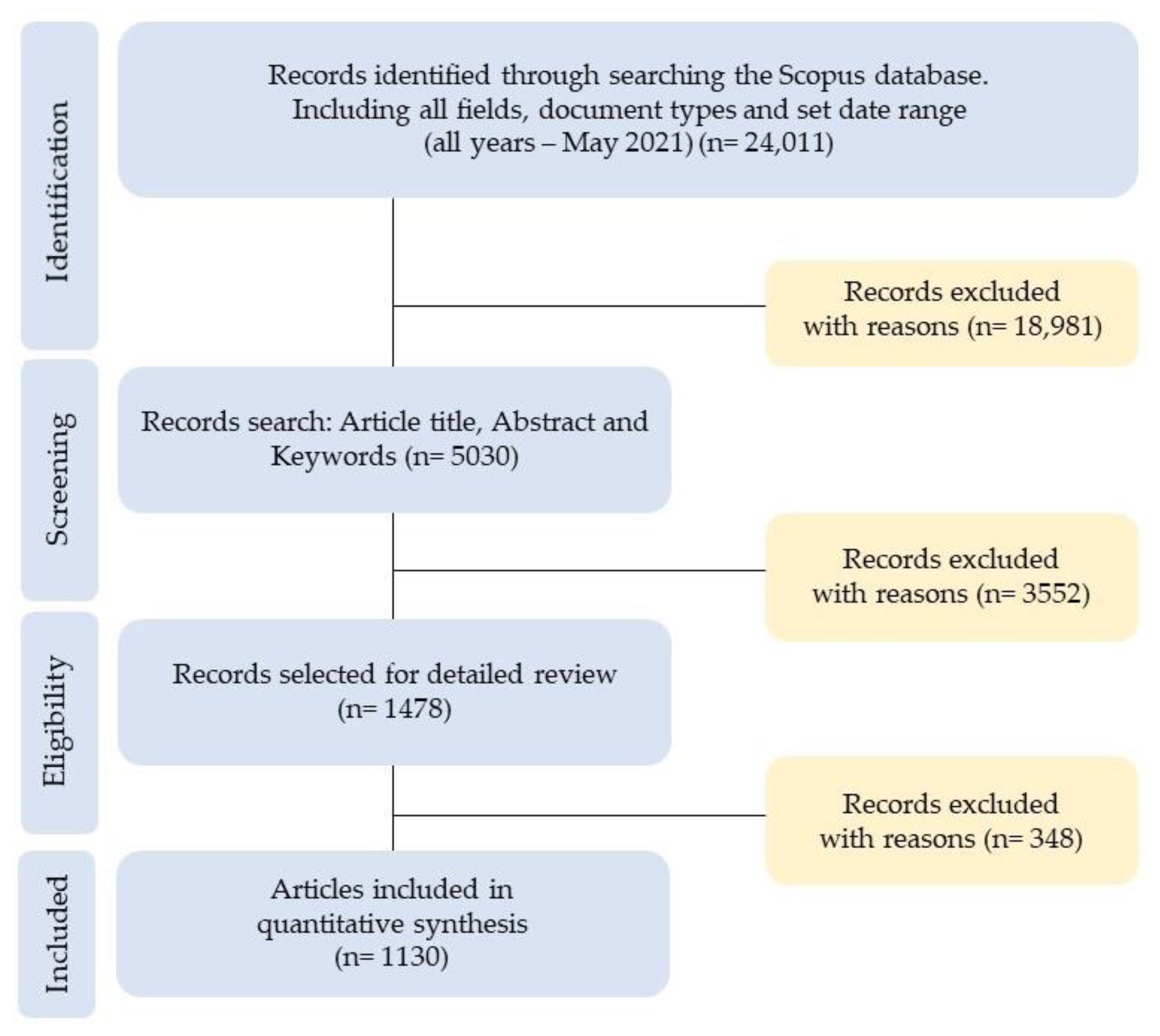

Figure 1 shows the process followed in the collection (inclusion–exclusion) of the sample, in relation to the “Preferred Reporting Items for Systematic Reviews and Meta-Analyses” (PRISMA) [58]:

- Phase 1 (Identification): 24,011 records were detected, considering, for each of the search terms (BC, accounting, and management), obtained from the analysis of the records in Table 1, “all fields”, “all types of documents” and “ all data published in the data range (all years–May 2021)”.

- Phase 2 (Screening): The option “article title, abstract and keywords” was chosen in the field of each search term. In total, 18,981 records were excluded, and 5030 were included.

- Phase 3 (Eligibility): Only “articles” were selected as the type of document, to guarantee the quality of the peer-review process; and, furthermore, in order not to distort the sample, the search was also limited to the subject areas: computer science; business, management and accounting; economics, econometrics and finance; and mathematics. In total, 3552 records were excluded, and 1478 were included.

- Phase 4 (Included): The data referring to the period “every year–2020” were selected, that is, from the first article published on the research topic (2016) to the last full year (2020). In total, 348 records were excluded. Hence, the final sample included 1130 articles (open and non-open access).

3.2. Data Processing

In the context of bibliometrics, data processing is about collecting data and translating it into actionable information. This procedure will be done in detail, so as not to affect the results obtained. In the field of research, the analyzed variables of the articles are: (i) year of publication; and (ii) keywords that identify it [59].

As a bibliometric indicator of relationship (collaboration at the structural level), the co-occurrence method was used, which offers a visual display of the relationships of the concepts represented in the documents. The occurrence attribute shows the number of articles that contain a certain keyword. This method detects the main axes of research, current and future, from the analysis of the key terms, since the articles are reduced to all the joint occurrences between the words that compose them [60,61].

In relation to the co-occurrence analysis, the VOSviewer computer program (version 1.6.16, Leiden University, Leiden, The Netherlands) was used. This software (i) provides data on the evaluation of the content of the records, to determine the research activities of the network; and (ii) recognizes research trends based on the use of certain keywords that identify scientific articles [62].

3.3. Key-Terms Co-Occurrence Analysis

In the analysis of co-occurrences of key terms that define the scientific articles in the sample, to identify current and future research lines on BC technology for secure accounting management, the following terminology from the VOSviewer tool was used [62,63]:

- Link: Co-occurrence connection between terms.

- Total link strength: Intensity of each link, denoted by a positive numerical value. For concurrent links, indicate the number of articles in which two terms appear together.

- Occurrence: Attribute that shows the number of articles that contain a keyword.

- Network map: Set of terms and links.

- Cluster: Set of terms included in a network map. Clusters do not need to comprehensively cover all the components of a network map.

- Weight: Attribute used to describe the term, denoted by numerical value.

- Weight of a term: Significance of the term in the field of research analyzed.

- Link weight: Number of links of a term with other terms.

- Link strength weight: Total strength of the links of a term with other terms.

- Score: Attribute that allows classifying by relevance the key terms of the titles and summaries of the analyzed articles.

To calculate the relevance score of each keyword, it is assumed that the highest-scoring terms provide a better prediction to identify a future line of research [62]. Consequently, starting with the term x in research field a, which in turn is part of research field b, the relevance score of term x in research area a is calculated as follows (see Equation (1)) [63,64]:

- nax: Number of elements in the areas a in which the term x occurs.

- nbx: Number of elements in the areas b in which the term x occurs.

- c: This parameter determines the compensation between the following considerations: (i) the frequency of occurrence of term x in area a relative to the frequency of occurrence of term x in area b can be considered as an indication of the relevance of the term x for area a; and (ii) the absolute frequency of occurrence of term x in area a can also be considered as an indication of the relevance of term x.

3.4. Research Limitations

The application of this methodology in the development of the study has had some limitations that, on the other hand, could be the basis for future research:

- Characteristics of bibliometric analysis, which is a method mainly focused on quantitative analysis, ignoring certain qualitative aspects.

- The methodology of this research could be extended with other quantitative or qualitative tools, such as Google Scholar, meta-analysis, or data mining (which uses methods of artificial intelligence (AI), machine learning (ML), statistics and data systems). databases), which would provide a different perspective on the results.

- The research sample only contains articles published in scientific journals, due to the reliability of the review system by parts; For future research, it would be interesting to include other types of documents, such as books or conference documents, to analyze the variation in the findings.

- Delve into different fields of this discipline, for more specific research on some of the topics related to these topics.

4. Results and Discussion

4.1. Temporal Evolution of Scientific Production (2016–2020)

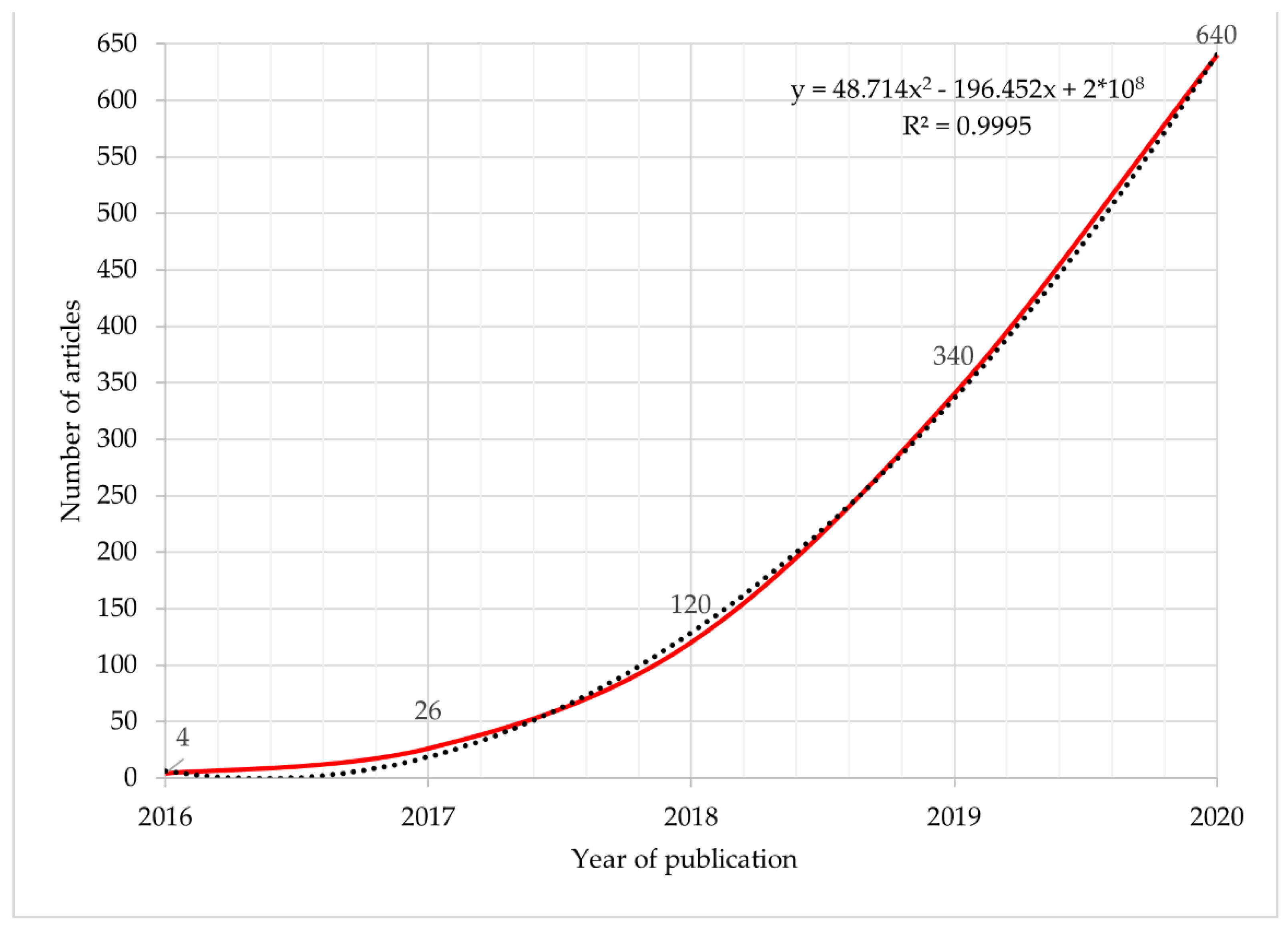

This section seeks to provide an answer to RQ1: What has been the evolution of scientific production in this field of knowledge between 2016 and 2020? Figure 2 shows how the number of articles published between 2016 and 2020 about BC technology for secure accounting management has evolved worldwide. The trend in the publication of documents is polynomial of order 2, it follows a mathematical function of the form: y = 48.714x2 − 196.452x + 2 × 108. The trend line indicates that the number of articles on this topic is increasing faster over time. Furthermore, this line shows its goodness of fit with a coefficient of determination, R2, equal to 0.9995, which denotes the proportion of the variance in the dependent variable (number of articles) that is predictable from the independent variable (year of publication).

Of the 1130 documents published between 2016 and 2020, 640 were in 2020, which represents 56.64%. In 2019, 340 articles were published (30.09%), that is, in the last two years, they accumulate 86.73% of the total, which indicates the incipient development of this topic worldwide, in addition to the recent interest on the part of the scientific and academic community.

Since the development of the digital cryptocurrency, Bitcoin, digital ledger technology has evolved and generated new applications that make up the history of BC [65]. In this sense, research has been increasing in parallel with innovation, since it is necessary to document and examine the utilities of these BC applications, beyond BC, such as the voting system [7], supply chains [66], automated security [67], smart contracts [24], digital identities [68], data registration and verification [69], or cloud storage [70]. Since the launch of Ethereum BC in 2015, research on technology and management for accounting security has a polynomial trend. During this period (2016–2020), governments and private companies finance innovation and applications, since the wide use of this technology in supply management, in the cloud computing business, or the development of the Internet of Things (IoT) was noted.

4.2. Keyword Analysis: Identification of Current Lines of Research

This section seeks to respond to RQ2: What were the main lines of research studied in the 2016–2020 period? In the 1130 scientific articles analyzed (2016–2020), 23,017 keywords were identified, highlighting: Blockchain (in 942 documents), information management (174), Internet of Things (171), supply chain management (108), digital storage (107), network security (99), smart contract (98), data privacy (72), security (71); or access control (66). These keywords are linked to search terms or research variables, which were identified in the initial literature review (see Table 1). The variable “Blockchain” refers to the chain of blocks that contain encoded information of a transaction on the network; “Accounting” to the discipline of economics that functions as a control/recording system of expenses/income and other economic operations carried out by an entity; and “Management” to the action of administering, organizing, and making a certain economic activity function.

Table 2 shows the 15 top keywords in the years 2016, 2017 and 2018. For each term the links, the total link strength, and the occurrences are provided. These are ordered by the number of occurrences.

In 2016, the main keywords (according to the number of occurrences) that are associated with the study variables were: BC (privacy, 2; access control, 1; authenticity, 1; computer security, 1; confidentiality, 1); Accounting (Bitcoin, 1; electronic money, 1; reliability, 1; risk, 1; privacy risk, 1); Management (authorization management, 1; information dissemination, 1; information processing, 1; risk management, 1; copyright, 1). In the first year analyzed, the publications aimed at defining and conceptualizing the subject, such as exploring the types of fraud and malicious activities that can be prevented with BC technology [17], or analyzing how this cryptographic transfer process has made it possible to improve the efficiency of international transactions. of securities subject to legal uncertainty [71].

In 2017: BC (cloud computing, 4; Internet of Things, 4; data privacy, 3; cyber security, 2; distributed computer systems, 2); Accounting (Bitcoin, 4; electronic money, 4; smart contract, 3; Ethereum, 2; accounting blockchain, 1); Management (supply chains, 4; information management, 3; intelligent systems, 3; commerce, 2; identity and access managements, 2). Hence, in 2017, research began to assess BC’s roles in strengthening security on the IoT, where it was observed that the decentralized nature of BC resulted in a low susceptibility to tampering/spoofing by malicious participants [72]; or examining key regulatory challenges affecting BCs, innovative distributed technologies, in the European Union (EU) and the US [73].

In 2018: BC (Internet of Things, 19; digital storage, 15; network security, 12; cryptography, 11; data privacy, 11); Accounting (smart contracts, 11; Bitcoin, 8; electronic money, 7; cryptocurrency 6; Ethereum, 4); and Management (information management, 25; commerce, 8; access control, 7; risk management, 6). In this year, progress was made in research on the subject of study, so that the application of BC in mobile services was examined, as a decentralized data management framework, estimating that to facilitate BC applications in future mobile IoT systems, the solution focuses on multi-access mobile edge computing to solve proof-of-work puzzles for mobile users [74]. Likewise, BC also studied the potential to affect the accounting and auditing fields, as a disruptive emerging technology, and determine the applicability of this technology to support business information systems and continuous monitoring systems [22].

Table 3 shows the 15 top keywords in the years 2019 and 2020, and the full period, 2016–2020. Equally, for each term the links, the total link strength, and the occurrences are provided.

In 2019: BC (Internet of Things, 54; digital storage, 34; data privacy, 27; network security, 27; cryptography, 15); Accounting (smart contract, 32; Ethereum, 20; Big Data, 14; bitcoin, 13; distributed ledger, 13); and Management (information management 49; supply chain management, 30; access control, 19; commerce 19; transparency 10). Hence, the research focused, among other lines, on empirically examining the role of big data, BC and AI in cloud-based accounting information systems [25]. Furthermore, for example, during this year the most traditional databases, Google Sheets and BC, to store and share data on the network, and their applicability to meet the business needs of an accounting entity, in relation to how an accounting organization addresses data governance and this influences business decision making [26].

In 2020: BC (Internet of Things, 93; digital storage, 58; network security 58; authentication, 43; cryptography, 36); Accounting (smart contract 56; distributed ledger, 19; distributed ledger technology, 18; Big Data, 14; costs, 14); and Management (information management 97; supply chain management, 74; access control, 38; decision making, 25; industry 4.0, 21). In this year, research advanced the configuration of BC as a disruptive force in currency, supply chain, information-sharing practices in a variety of industries, in financial reporting and assurance [27,29,75].

In summary, in the period (2016–2020) analyzed: BC (Internet of Things, 171; digital storage, 107; network security, 99); Accounting (smart contract, 98; Ethereum, 40; distributed ledger, 37); and Management (information management, 174; supply chain management; 108; decision making, 31).

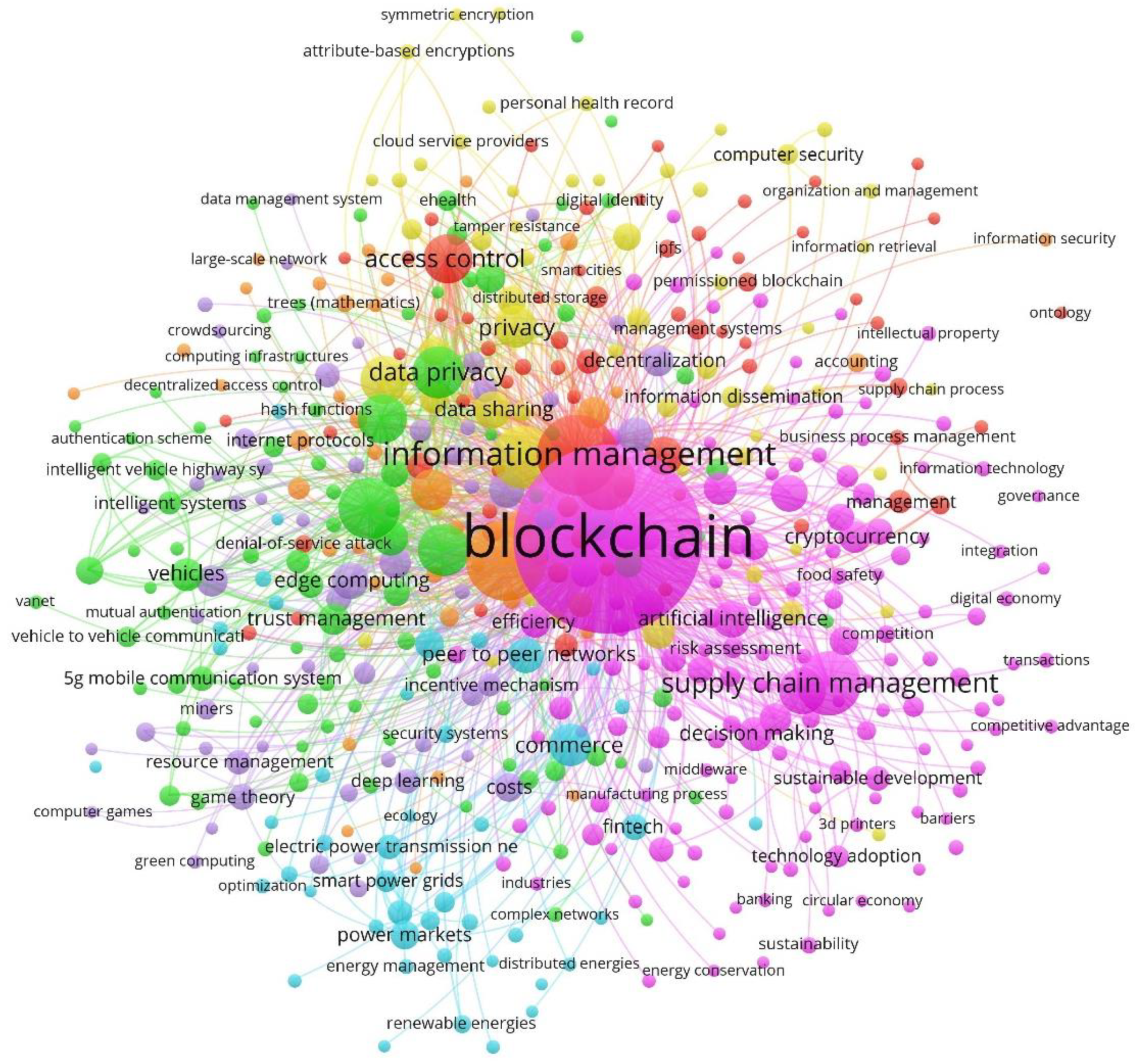

Co-occurrence analysis of the keywords that identify the articles in the sample on the study topic was performed. Figure 3 represents the network display of these keywords. The analysis allowed us to detect that the keywords were classified in seven clusters with homogeneous characteristics. The color of the nodes (keywords) allows differentiating the clusters based on the number of co-occurrences, while the size refers to the number of occurrences. Likewise, the size of each cluster refers to the importance of the keywords that make up the group, and, to show the link in the map display, the thickness of the joining lines between two keywords will be greater the stronger the link between these.

Based on the criterion of density and centrality, the clusters are associated with themes developed during the 2016–2020 period. Cluster 1 (pink), which accumulates 29% of the keywords and presents a high centrality and density, contains the most developed and main topic, that is, it analyzes the general revision aspects of the field of study (blockchain technology). Clusters 2 (green, 18%) and 3 (red, 13%), high density and low centrality, define specialized topics (network security and information management). Cluster 4 (yellow, 12%), low density and high centrality, defines emerging themes (such as digital storage or electronic document exchange). Finally, clusters 5 (cyan, 11%), 6 (purple, 9%) and 7 (orange, 8%), with low density and centrality, define less developed topics (edge computing, commerce, or the link with the IoT).

This analysis of co-occurrences allowed us to recognize the lines of research during the 2016–2020 period and developed by the main driving agents of this research field. Table 4, Table 5, Table 6, Table 7, Table 8, Table 9 and Table 10 show the seven clusters identified by the VOSviewer software. The header of each table indicates the color with which each cluster is identified (see Figure 3) and the percentage of keywords over the total. The 10 most prominent keywords are displayed in each cluster, ordered by the number of occurrences. The keyword with the most occurrences defines the component name. For each keyword, the links and the total link strength are also provided. Hence, the lines of research identified were: “Blockchain”, “Network Security”, “Information Management”, “Digital Storage”, “Edge Computing”, “Commerce” and “Internet of Things”.

The first line of research has developed the general aspects of BC technology, which allows value transactions between users without the intervention of intermediaries in the process, that is, it decentralizes the management of transactions and presents all its participants the same registry book or decentralized database (distributed ledger) [76,77].

This thematic axis is directly related to terms such as Supply Chain, Supply Chain Management [78], Artificial Intelligence [79], Distributed Ledger [80], Decision Making [81], Big Data [82], Cryptocurrency [83] and Industry 4.0 [84], among others, giving an overall sense to the subject of study. In this sense, transactions can be monetary (cryptocurrencies) or of another nature (goods, information, services, etc.) [85] and take place on platforms whose nodes communicate through peer-to-peer networks (P2P1) through Internet connections [86,87]. Likewise, BC offers a dynamic and unalterable representation or record of these transactions over time that replaces trusted intermediaries and centralized authorities that support transactions due to the digital trust that users have placed in this technology [88]. In this context, an analysis of the cryptocurrency market and the drivers of the price of Bitcoin in a speculative environment was carried out [89].

The second line of research has developed the concept of network security, which consists of the policies and practices adopted to prevent and monitor unauthorized access, improper use, modification or denial of a computer network and its accessible resources. This involves the authorization of access to data on the network, which is controlled by the network administrator. Furthermore, it is the users who choose (or are assigned) an identification and password (or other authentication information), which allows them to access information and programs within their authorizations [90,91].

In this context, it (i) covers a variety of computer networks, public and private, that are used in everyday jobs, such as conducting transactions and communications between companies, government agencies and individuals; and (ii) protects the network, in addition to protecting and supervising the operations that are carried out [92,93]. This line is linked to concepts such as data privacy, trust management, identity management, security analysis, vehicular ad hoc networks, or mobile telecommunication systems.

The third line of research carried out on this topic has focused on Information Management (IM), which refers to (i) an organizational activity cycle and (ii) development, simulation or modeling of information systems, which are applicable to management areas in organizations to acquire information from one or more sources, the custody and distribution of this to those who need it, and its final disposal through archiving or deletion [94,95].

The cycle of organizational involvement with information involves a variety of stakeholders, including (i) those responsible for ensuring the quality, accessibility, and usefulness of the information acquired; (ii) those responsible for safe storage and disposal; and (iii) those who make decisions with it. Likewise, the interested parties may have the right to originate, change, distribute or eliminate information in accordance with the organizational information management policies [95,96].

IM includes the generic concepts of management (planning, organizing, structuring, processing, controlling, evaluating, and reporting information activities), necessary to meet the needs of those with information-dependent organizational roles or functions. On the other hand, IM is related to the management of data, systems, technology, processes and strategy [49]. This thematic axis is associated with concepts such as smart contract, access control, proposed architectures, trusted third parties, embedded systems, or crime.

The fourth axis of knowledge has developed the concept of digital storage, which refers to the ability to store data or any type of information by a computational storage device. This term arises as a necessity from the development of the new Information and Communication Technologies (ICT). Digital storage has undergone several transformations in its history, motivated by the expansion of the limits of the content that can be created digitally, to save, export, share and download information [97,98].

The progress of storage has passed, among others, from punch cards (960 bytes), Magnetic tapes (5 to 10 Mb), Floppy disks (5.35 and 3.5), CDs, ZIP Disks (between 100 and 750 Mb), USB or flash drives, portable hard drives, even the cloud. In this context, BC is considered a distributed information storage technique, and allows to verify, validate, track and store all kinds of information (from digital certificates, democratic voting systems, logistics/courier services, smart contracts, money and transactions financial) [99,100]. This line is linked to concepts such as cryptography, data sharing, distributed ledger technology, trusted computing, privacy-preserving, public key cryptography, or electronic document exchange.

This fifth line of research has mainly developed the concept of edge computing, which refers to the distributed computing paradigm that brings computing and data storage to the location where it is needed to improve response times and reserve bandwidth. Its origin is content distribution network (CDN), which was created in the late 1990s to serve web and video content while being deployed close to users [101,102].

Later, in the early 2000s, this evolved to host applications and application components on servers at the edge of networks, from which emerged the first edge computing services of hosted applications (dealer locators, shopping carts, real-time data aggregators and ad insertion engines). Edge computing has expanded this approach through virtualization technology, which makes it easier to deploy and run a broader range of applications on edge servers [103,104]. In this period, the volatility of Bitcoin was modeled through key variables of the financial environment [105].

The sixth line of research has studied the influence of BC technology on trade transactions, due to its potential for the industry. BC eliminates intermediaries in a transaction, normally of a financial nature, thus giving relevance to the groups that execute said operation. These transactions are continuously intertwined, creating a massive, unalterable, and permanent accounting book, allowing greater speed, lower costs and more security in transactions [8,106].

Therefore, these characteristics have been of interest in recent years in the field of BC trade. In this way, this thematic axis has analyzed how BC technology is applied in foreign trade and its relationship with smart contracts, that is, computer code that generates the automatic fulfillment of a contract, establishing bank payment commitment clauses, to eliminate doubts about defaults and therefore contribute to the internationalization of companies [107,108]. In addition, during this period, in relation to Fintech, a cryptocurrency was analyzed using an artificial financial market [109].

The seventh line of research detected has developed BC’s link with the IoT concept, proposed in 1999 by Kevin Ashton at the MIT Auto-ID Center. IoT, as is known, allows connecting any physical device (home, business resources, smart devices, among others) designed to work through the transfer of data through wired/wireless networks over the Internet. IoT is designed to collect any information and exchange it with each other [110,111].

Nowadays, many connected devices use BC technology as a safe and fast means of communication, providing security and privacy. This technology has meant promoting the use of the IoT at a global level. In this context, the main lines of development of BC in IoT seek, among others, to integrate systems to lead to the automation of production lines, or to apply to storage and distribution systems of manufactured products and raw materials, that is, Industry 4.0, which needs automation and tokenization from BC [112,113]. The link between IoT and BC applied in homes and community systems has also been developed.

4.3. Future Directions of Research

This section seeks to respond to RQ3: What are the emerging research directions on this topic? After reviewing the literature (Section 2) and an analysis of the keywords that allowed to identify current trends (Section 4.2), the main future/emerging directions of this research field were identified.

International research on BC for secure accounting management evolves adding new concepts and approaches that establish new lines of research. As indicated in Section 3.3, the last terms associated with this research were identified, which allows them to be associated with emerging research directions.

Cluster analysis is an effective process for uncovering emerging trends/problems in a scientific discipline. This consisted of (i) dividing the analysis units into groups of similar elements; (ii) determine the newest terms from the relevance score; and (iii) the terms would be assimilable to emerging thematic lines in this field of research. Table 11 shows the future research directions detected by the relevance score, of which a detailed description is provided later.

4.3.1. Credit Value Evaluation Mechanism

BC is redefining the banking industry, from centralized reliance on the infrastructure of the global banking and financial industry [56]. The disintermediation of centralized trust comes from the characteristics of BC technology, such as the ability to provide global transactions between equals, the immutable ownership of wealth, and instant and open access to financial services, among others.

Banks and financial companies must become value platforms from the traditional platforms of need, that is, for access to credit, custody of wealth and transfers of value. Hence, financial institutions must take advantage of BC solutions to add greater value to their consumer experiences, and gain access to a broader range of new customers wanting financial services [9,114].

Along these lines, BC-based credit reports with their distributed database are more secure than traditional credit reports based on centralized servers, so that they can allow companies to take non-traditional factors into account when calculating credit scores [115].

4.3.2. Enabled Payment Gateway

A payment gateway is a form of payment with which the payments of a company’s clients are processed and authorized. For the sale of a product/service, payment gateways facilitate receiving money quickly and safely. In this sense, payment gateways are the form of payment implemented by all digital businesses, whose function is to make it easier for customers to pay through the web. Its advantages include both the increase in the conversion rate and the results in customer loyalty [116,117].

This payment system has enabled many businesses to expand their activity due to online sales. Therefore, for eCommerce, it is key to integrate payment options that add value to the shopping experience, since a satisfied customer finds the payment method that best suits their needs. The keys to any payment option are to convey confidence, simplicity, and clarity to the user. In this way, eCommerce integrates gateways that allow payment with immediacy, ease and security [118].

4.3.3. Unstructured Supplementary Service Data Message

Unstructured Supplementary Service Data (USSD) is a data sending protocol used, among others, in information services based on interactive menus. BC technology tries to solve its limitations to get it applied to real problems. Hence, BC systems that use public key cryptography should be applied to create an immutable, time-stamped, stub-only content chain, so that copies of the BC are distributed to each participating node in the network. The key to this is that BC systems are theoretically ideal for storing highly sensitive information [116,119].

4.3.4. Consolidated Identity Management

This line of research will study how BC allows people to store data on a chain of blocks, instead of hacked servers. Information is cryptographically protected, once stored, on a and cannot be altered or deleted, making massive data breaches difficult [120].

Among the strategies to be analyzed are (i) eliminating the need for intermediaries by allowing people to store their identities and data directly on a chain of blocks that a user takes with them everywhere online, since, with the digital identities of the users stored cryptographically directly on a chain of blocks within an Internet browser, users theoretically would not need to provide confidential data to any third party; and (ii) allow users to encrypt their personal data in a BC that can be accessed by third parties, although it does not completely eliminate the need for intermediaries, but rather eliminates the need for intermediaries to store sensitive personal data directly on their servers [68,121].

4.3.5. Hyperledger Sawtooth

Hyperledger Sawtooth is an enterprise solution for building, implementing, and running BCs, providing an extremely modular and flexible platform for implementing transaction-based updates to the shared state between untrusted parties coordinated by consensus algorithms. This is a project belonging to the Umbrella organization, focused on ledgers designed to support global business transactions, including major technology, financial, and supply chain giants, with the aim of improving many aspects of performance and reliability, started in 2015 by the Linux Foundation. The project’s objectives include (i) joining several independent efforts to develop open standards and protocols, and (ii) providing a modular framework that supports different components for different uses [122,123].

4.3.6. Hierarchical Lightweight High Throughput Blockchain

In recent years, numerous studies have addressed the possibility of using BC and smart contracts to disrupt the IoT architecture for its security and decentralization guarantees [23,124,125]. This next-generation BC architecture is not scalable enough to meet the requirements of massive data traffic in the IoT environment, because it is necessary to choose the consensus compromise between dealing with high performance or many nodes. So, this situation has impeded the applicability of BC for IoT use cases [126].

In this sense, the research should propose scalable hierarchical BC architectures for IoT, in addition to implementing multiple instances to deal with many nodes, and the scalability of the architecture with the aggregation and prioritization of requests. The based architecture must store and process IoT data securely with custom BC technology, through security and performance analysis [127,128].

4.3.7. BGP Security Infrastructure

Border Gateway Protocol (BGP) is a protocol used on the Internet to exchange routing information between networks, that is, it is the language that allows determining how packets can be sent from one router to another to reach their destination [129]. On the other hand, BGP does not include security mechanisms directly and relies heavily on the trust between network operators that they will protect their systems correctly and will not send incorrect data. In this regard, the problems that can arise if malicious attackers try to affect the routing tables used by BGP should be analyzed. Network operators must understand certain information to protect their routers and to ensure the security and resilience of the overall Internet routing infrastructure [130,131].

4.3.8. Global Supply Chain Risk Analysis

The impact of technology on supply chains and the logistics sector promises to be truly revolutionary. BC will increase (i) the transparency of the supply chain, drastically reducing costs, mainly onerous and complex bureaucracy; and (ii) understanding the global flow of trade, tracking specific items at each stage of its journey and the associated risks, allowing better management and mitigation of these risks [132,133].

BC is key in the daily activities of logistics companies. The application of this technology to documentation and information exchange helps logistics companies. Today, technology and information move the load. Obtaining more data and extracting better analysis from this information can improve efficiencies in supply chains and the logistics process. For all this, it will be analyzed how BC provides a more effective and definitive mechanism to track data in complex supply chains, in addition to increasing efficiency, reducing human errors, and resolving responsibilities and obligations throughout the chain [134].

4.3.9. Extensible Permissioned Blockchain Platform

BC platforms generate a transparent and unalterable chain of information. These features could provide an opportunity for intellectual property (IP) offices to transform the registration of IP rights to make the process more cost-effective, faster, more accurate and more secure. In addition, this technology offers the potential to transform the efficiency and transparency of rights management information [135].

Authorized BCs are an additional BC security system, as they maintain a layer of access control to allow certain actions to be performed only by certain identifiable participants. In this sense, future studies should analyze how BC technology can improve the efficiency of the registration process for drawings and marks by shortening some of these processes and procedures. Likewise, BC technology can also help create a record of unregistered IP rights, such as copyright and unregistered design rights, as it can easily provide proof about the time of creation, information on the management of rights and jurisdictional requirements [136,137].

4.3.10. Centralized Authentication Authorization Auditing

This line of work will develop the centralized authentication authorization audit. To migrate many online services, obstacles arise both related to the ability to secure data and to verify the identity of users. The computer network authentication protocol provides secure communication over the Internet, for client–server applications, that facilitates mutual authentication by which the client and the server can guarantee the authenticity of the other. Currently, online authentication is based on a password and the use of two-factor authentication [138,139].

The problem with these methods is that the passwords are insecure, and the two-factor authentication relies on sending a code via SMS (Short Messaging Service) or a third-party service. Consequently, BC emerges as a potential solution since its cryptographic principles could be applied to authentication. BC can offer this approach by decentralizing ownership of credentials and availability on an immutable chain of data. These are stored in a shared workbook, rather than being stored by an application.

This shared ledger is downloaded by each individual user, reflecting a record of each transaction performed. That is, by distributing a ledger among all members of the network, BC authentication eliminates the power to perversely modify the ledger. Therefore, each time a transaction is added to the chain, most of the network must verify its validity, thus guaranteeing its integrity. This system still has drawbacks and insecurities, so it is key to analyze this technology in detail [140]. In this sense, the feasibility of using public key encryption to send credentials with security will be studied, so that the recipient can verify the shipment against an immutable BC entry, providing security and reliability to identity verification.

5. Conclusions

The main objective is to examine the current and emerging lines of research at an international level on BC technology for secure accounting management, between 2016 and 2020. Mathematical and statistical techniques were applied to a sample of 1130 scientific articles selected from Elsevier’s Scopus database. Basically, the main current and future lines of research on this topic were identified. In relation to the incipient thematic, a polynomial trend is observed in the global publication, with 60% of the total sample in 2020, confirming the interest of the academic and scientific community.

This field of knowledge was developed from the seven main lines of investigation detected: “Blockchain”, “Network security”, “Information management”, “Digital storage”, “Edge Computing”, “Commerce” and “Internet of Things”.

BC technology, as the underlying accounting system, is revolutionizing the process of registration, verification, transparency, and reliability of the accounting information system. The research during the analyzed period has focused on highlighting the benefits that BC represents for business activity and accounting, since all the records in the blockchain are distributed on the network and cryptographically sealed, making it impossible to falsify, modify or delete them. In this sense, the emergence of BC in the process of preparing the accounting information has made it possible to advance from a double-entry system to a triple entry system, so that BC technology is the basis that sustains this third ledger of DLT transactions.

Likewise, due to the evolution of this field of research, new concepts and approaches are added, which institute new lines of work. In this context, ten emerging research lines were detected: (i) Credit Value Evaluation Mechanism; (ii) Enabled Payment Gateway; (iii) Unstructured Supplementary Service Data Message; (iv) Consolidated Identity Management; (v) Hyperledger Sawtooth; (vi) Hierarchical Lightweight High Throughput Blockchain; (vii) BGP Security Infrastructure; (viii) Global Supply Chain Risk Analysis; (ix) Extensible Permissioned Blockchain Platform; and (x) Centralized Authentication Authorization Auditing.

This research contributes to the detection and analysis of additional qualitative knowledge, which plays the role of prelude to future debates by presenting a broad vision of the research carried out in the 2016–2020 period, and from which emerging lines of interest were identified. Consequently, these future research directions should allow academics and researchers to guide their next work and funding entities to envision the objectives to be analyzed.

On the other hand, this study has an aggregate of limitations, among which the following stand out: (i) the terms selected to obtain the article sample, since another review of the literature could have led to the detection of other search terms or basic concepts; (ii) the date range, 2016–2020, since the investigation period could have been shortened by years; (iii) the Scopus database from which the sample of articles was obtained, since new publications included in other databases, such as WoS or Google Scholar, could be included; (iv) (ii) the statistical and mathematical techniques applied, since a qualitative analysis could have been included; or (vi) the VOSviewer software used to view the network maps, since another tool may have identified different clusters and emerging lines. In future work, data mining techniques may be used to study large databases and thus find patterns that allow their behavior to be interpreted.

The main novelty or contribution of this work is the identification of the research lines that have been developed so far, based on the grouping of keywords through the analysis of co-occurrences, to build a map of the work carried out by the driving agents of the theme. Furthermore, based on the methodology developed by the researchers, Ludo Waltman and Nees Jan van Eck, from the Center for Science and Technology Studies (Leiden University, The Netherlands), the ten most relevant emerging lines of research on the link between the BC technology and the secure accounting management, to open new avenues to develop.

In this sense, during the last few years, several bibliometric studies have been published on BC linked to different disciplines, such as health [141], Bitcoin [142], applications in power systems [143], Industry 4.0 [144], among others, or the connecting link with financial transactions [56], in addition to other studies with a more general vision [145,146]. For this reason, this work is a novelty since it has not deepened in the detection of research trends of a technological paradigm.

Conclusively, it is determined that the global research on BC technology for secure accounting management presents an upward trend in the number of articles and schools of thought so far and emerging. This indicates the worldwide interest of the academic/scientific community to advance in the solutions to the new problems that arise derived from a subject in constant evolution. The research is carried out in optimal conditions and with a global interest in the issuance of publications to contribute to the knowledge of BC’s link with the accounting discipline. The findings of this study, mainly, should guide the members of the academic and scientific communities that develop and analyze the research field on the link between BC and accounting, in addition to the funding agencies of future research projects on this subject.

Author Contributions

Conceptualization, methodology, software, formal analysis, resources, data curation and writing—original draft preparation, E.A.-S. and M.-D.G.-Z.; investigation, validation, writing—review and editing, visualization, supervision, project administration, E.A.-S., M.-D.G.-Z., E.L.-M. and A.I.-M.; funding acquisition, E.L.-M. and A.I.-M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data were obtained from Elsevier’s Scopus database (https://0-www-scopus-com.brum.beds.ac.uk/) accessed on 5 May 2021.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Kiviat, T.I. Beyond Bitcoin: Issues in Regulating Blockchain Transactions. Duke Law J. 2015, 65, 569–608. [Google Scholar]

- Alabi, K. Digital Blockchain Networks Appear to Be Following Metcalfe’s Law. Electron. Commer. Res. Appl. 2017, 24, 23–29. [Google Scholar] [CrossRef]

- ALSaqa, Z.H.; Hussein, A.I.; Mahmood, S.M. The Impact of Blockchain on Accounting Information Systems. J. Inf. Technol. Manag. 2019, 11, 62–80. [Google Scholar] [CrossRef]

- Rîndaşu, S.-M. Blockchain in Accounting: Trick or Treat? Qual. Access Success 2019, 20, 143–147. [Google Scholar]

- Wang, P.; Qiao, S. Emerging Applications of Blockchain Technology on a Virtual Platform for English Teaching and Learning. Wirel. Commun. Mob. Comput. 2020, 2020. [Google Scholar] [CrossRef]

- Alexander, A.; McGill, M.; Tarasova, A.; Ferreira, C.; Zurkiya, D. Scanning the Future of Medical Imaging. J. Am. Coll. Radiol. 2019, 16, 501–507. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Tso, R.; Liu, Z.-Y.; Hsiao, J.-H. Distributed E-Voting and E-Bidding Systems Based on Smart Contract. Electronics 2019, 8, 422. [Google Scholar] [CrossRef] [Green Version]

- Papagiannidis, S.; Bourlakis, M.; See-To, E. Social Media in Supply Chains and Logistics: Contemporary Trends and Themes. Int. J. Bus. Sci. Appl. Manag. 2019, 14, 17–34. [Google Scholar]

- Efimova, L.G. The Mechanism of Credit Transfers via the Blockchain. Int. Account. 2020, 23, 567–584. [Google Scholar] [CrossRef]

- Griggs, D.; Smith, M.S.; Rockström, J.; Öhman, M.C.; Gaffney, O.; Glaser, G.; Kanie, N.; Noble, I.; Steffen, W.; Shyamsundar, P. An Integrated Framework for Sustainable Development Goals. Ecol. Soc. 2014, 19. [Google Scholar] [CrossRef]

- Perdana, A.; Robb, A.; Balachandran, V.; Rohde, F. Distributed Ledger Technology: Its Evolutionary Path and the Road Ahead. Inf. Manag. 2021, 58, 103316. [Google Scholar] [CrossRef]

- Bonyuet, D. Overview and Impact of Blockchain on Auditing. Int. J. Digit. Account. Res. 2020, 20, 31–43. [Google Scholar] [CrossRef]

- Coyne, J.G.J.G.; McMickle, P.L.P.L. Can Blockchains Serve an Accounting Purpose? J. Emerg. Technol. Account. 2017, 14, 101–111. [Google Scholar] [CrossRef]

- Church, K.S.; Stein Smith, S.; Kinory, E. Accounting Implications of Blockchain-A Hyperledger Composer Use Case for Intangible Assets. J. Emerg. Technol. Account. 2020. [Google Scholar] [CrossRef]

- Christidis, K.; Devetsikiotis, M. Blockchains and Smart Contracts for the Internet of Things. IEEE Access 2016, 4, 2292–2303. [Google Scholar] [CrossRef]

- Lemieux, V.L. Trusting Records: Is Blockchain Technology the Answer? Rec. Manag. J. 2016, 26, 110–139. [Google Scholar] [CrossRef]

- Cai, Y.; Zhu, D. Fraud Detections for Online Businesses: A Perspective from Blockchain Technology. Financ. Innov. 2016, 2, 1–10. [Google Scholar] [CrossRef] [Green Version]

- Egelund-Müller, B.; Elsman, M.; Henglein, F.; Ross, O. Automated Execution of Financial Contracts on Blockchains. Bus. Inf. Syst. Eng. 2017, 59, 457–467. [Google Scholar] [CrossRef]

- Dai, J.; Vasarhelyi, M.A.M.A. Toward Blockchain-Based Accounting and Assurance. J. Inf. Syst. 2017, 31, 5–21. [Google Scholar] [CrossRef]

- Rozario, A.M.; Thomas, C. Reengineering the Audit with Blockchain and Smart Contracts. J. Emerg. Technol. Account. 2019, 16, 21–35. [Google Scholar] [CrossRef]

- Procházka, D. Accounting for Bitcoin and Other Cryptocurrencies under IFRS: A Comparison and Assessment of Competing Models. Int. J. Digit. Account. Res. 2018, 18, 161–188. [Google Scholar] [CrossRef]

- Wang, Y.; Kogan, A. Designing Confidentiality-Preserving Blockchain-Based Transaction Processing Systems. Int. J. Account. Inf. Syst. 2018, 30, 1–18. [Google Scholar] [CrossRef]

- Gießmann, S. Money, Credit, and Digital Payment 1971/2014: From the Credit Card to Apple Pay. Adm. Soc. 2018, 50, 1259–1279. [Google Scholar] [CrossRef]

- de Graaf, T.J. From Old to New: From Internet to Smart Contracts and from People to Smart Contracts. Comput. Law Secur. Rev. 2019, 35, 105322. [Google Scholar] [CrossRef]

- Ionescu, L. Big Data, Blockchain, and Artificial Intelligence in Cloud-Based Accounting Information Systems. Anal. Metaphys. 2019, 18, 44–49. [Google Scholar] [CrossRef]

- McAliney, P.J.P.J.; Ang, B. Blockchain: Business’ next New “It” Technology—a Comparison of Blockchain, Relational Databases, and Google Sheets. Int. J. Discl. Gov. 2019, 16, 163–173. [Google Scholar] [CrossRef]

- Smith, S.S.; Castonguay, J.J. Blockchain and Accounting Governance: Emerging Issues and Considerations for Accounting and Assurance Professionals. J. Emerg. Technol. Account. 2020, 17, 119–131. [Google Scholar] [CrossRef]

- Mosteanu, N.R.; Faccia, A. Digital Systems and New Challenges of Financial Management – Fintech, XBRL, Blockchain and Cryptocurrencies. Qual. Access Success 2020, 21, 159–166. [Google Scholar]

- Demirkan, S.; Demirkan, I.; McKee, A. Blockchain Technology in the Future of Business Cyber Security and Accounting. J. Manag. Anal. 2020, 7, 189–208. [Google Scholar] [CrossRef]

- Tapscott, D.; Kirkland, R. How Blockchains Could Change the World. McKinsey Q. 2016, 2016, 110–113. [Google Scholar]

- Xu, J.J. Are Blockchains Immune to All Malicious Attacks? Financ. Innov. 2016, 2, 25. [Google Scholar] [CrossRef] [Green Version]

- Abou Jaoude, J.; George Saade, R. Blockchain Applications - Usage in Different Domains. IEEE Access 2019, 7, 45360–45381. [Google Scholar] [CrossRef]

- Yuan, Y.; Wang, F.Y. Blockchain: The State of the Art and Future Trends. Zidonghua Xuebao/Acta Autom. Sin. 2016, 42, 481–494. [Google Scholar] [CrossRef]

- He, W.; Zhang, Z.J.; Li, W. Information Technology Solutions, Challenges, and Suggestions for Tackling the COVID-19 Pandemic. Int. J. Inf. Manag. 2021, 57, 102287. [Google Scholar] [CrossRef] [PubMed]

- Minakova, I.; Nosachevsky, K. Management Control in the Big Companies: New Approaches. Econ. Ann. XXI 2019, 180, 130–137. [Google Scholar] [CrossRef]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 2019, pp. 1–11. Available online: www.bitcoin.org (accessed on 20 June 2021). [CrossRef]

- Haber, S.; Stornetta, W.S. How to Time-Stamp a Digital Document. In Advances in Cryptology-CRYPT0’ 90; Springer: Berlin/Heidelberg, Germany, 1991; Volume 537 LNCS, pp. 437–455. [Google Scholar]

- Huerta, E.; Jensen, S. An Accounting Information Systems Perspective on Data Analytics and Big Data. J. Inf. Syst. 2017, 31, 101–114. [Google Scholar] [CrossRef]

- Dunk, A.S. Product Life Cycle Cost Analysis: The Impact of Customer Profiling, Competitive Advantage, and Quality of IS Information. Manag. Account. Res. 2004, 15, 401–414. [Google Scholar] [CrossRef]

- Hayes, A. The Socio-Technological Lives of Bitcoin. Theory Cult. Soc. 2019, 36, 49–72. [Google Scholar] [CrossRef]

- O’Connor, N.G.; Martinsons, M.G. Management of Information Systems: Insights from Accounting Research. Inf. Manag. 2006, 43, 1014–1024. [Google Scholar] [CrossRef]

- Tauscher, L.; Greenberg, S. How People Revisit Web Pages: Empirical Findings and Implications for the Design of History Systems. Int. J. Hum. Comput. Stud. 1997, 47, 97–137. [Google Scholar] [CrossRef] [Green Version]

- Shi, L.; Li, X.; Gao, Z.; Duan, P.; Liu, N.; Chen, H. Worm Computing: A Blockchain-Based Resource Sharing and Cybersecurity Framework. J. Netw. Comput. Appl. 2021, 185, 103081. [Google Scholar] [CrossRef]

- Thomson, G. BYOD: Enabling the Chaos. Netw. Secur. 2012, 2012, 5–8. [Google Scholar] [CrossRef]

- Zahadat, N.; Blessner, P.; Blackburn, T.; Olson, B.A. BYOD Security Engineering: A Framework and Its Analysis. Comput. Secur. 2015, 55, 81–99. [Google Scholar] [CrossRef]

- Ebrahim, S.H.; Ahmed, Q.A.; Gozzer, E.; Schlagenhauf, P.; Memish, Z.A. Covid-19 and Community Mitigation Strategies in a Pandemic. BMJ 2020, 368, m1066. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Brincat, A.A.; Lombardo, A.; Morabito, G.; Quattropani, S. On the Use of Blockchain Technologies in WiFi Networks. Comput. Netw. 2019, 162, 106855. [Google Scholar] [CrossRef]

- Hu, D.; Li, Y.; Pan, L.; Li, M.; Zheng, S. A Blockchain-Based Trading System for Big Data. Comput. Netw. 2021, 191, 107994. [Google Scholar] [CrossRef]

- Chen, Y.; Chen, S.; Liang, J.; Feagan, L.W.; Han, W.; Huang, S.; Wang, X.S. Decentralized Data Access Control over Consortium Blockchains. Inf. Syst. 2020, 94, 101590. [Google Scholar] [CrossRef]

- O’Leary, D.E. Some Issues in Blockchain for Accounting and the Supply Chain, with an Application of Distributed Databases to Virtual Organizations. Intell. Syst. Account. Financ. Manag. 2019, 26, 137–149. [Google Scholar] [CrossRef]

- Calderón, J.; Stratopoulos, T.C. What Accountants Need to Know about Blockchain*. Account. Perspect. 2020, 19, 303–323. [Google Scholar] [CrossRef]

- Musante, S. Learning How to Ask Research Questions. BioScience 2010, 60, 266. [Google Scholar] [CrossRef] [Green Version]

- Abramo, G. Revisiting the Scientometric Conceptualization of Impact and Its Measurement. J. Informetr. 2018, 12, 590–597. [Google Scholar] [CrossRef] [Green Version]

- Abad-Segura, E.; González-Zamar, M.D.; López-Meneses, E.; Vázquez-Cano, E. Financial Technology: Review of Trends, Approaches and Management. Mathematics 2020, 8, 951. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.-D.D. Research Analysis on Emerging Technologies in Corporate Accounting. Mathematics 2020, 8, 1589. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.D. Global Research Trends in Financial Transactions. Mathematics 2020, 8, 614. [Google Scholar] [CrossRef]

- Mongeon, P.; Paul-Hus, A. The Journal Coverage of Web of Science and Scopus: A Comparative Analysis. Scientometrics 2016, 106, 213–228. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; Altman, D.G.; Antes, G.; Atkins, D.; Barbour, V.; Barrowman, N.; Berlin, J.A.; et al. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. PLoS Med. 2009, 6, 1–6. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ding, Y.; Chowdhury, G.G.; Foo, S. Bibliometric Cartography of Information Retrieval Research by Using Co-Word Analysis. Inf. Process. Manag. 2001, 37, 817–842. [Google Scholar] [CrossRef] [Green Version]

- van Eck, N.J.; Waltman, L. Visualizing Bibliometric Networks. In Measuring Scholarly Impact; Springer International Publishing: Cham, Switzerland, 2014; pp. 285–320. [Google Scholar]

- Van Eck, N.J.; Waltman, L. How to Normalize Cooccurrence Data? An Analysis of Some Well-Known Similarity Measures. J. Am. Soc. Inf. Sci. Technol. 2009, 60, 1635–1651. [Google Scholar] [CrossRef] [Green Version]

- van Eck, N.J.; Waltman, L. Software Survey: VOSviewer, a Computer Program for Bibliometric Mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [Green Version]

- Waltman, L.; Van Eck, N.J. A New Methodology for Constructing a Publication-Level Classification System of Science. J. Am. Soc. Inf. Sci. Technol. 2012, 63, 2378–2392. [Google Scholar] [CrossRef] [Green Version]

- Van Eck, N.; Waltman, L.; Den Berg, J.; Kaymak, U. Visualizing the Computational Intelligence Field. IEEE Comput. Intell. Mag. 2006, 1, 6–10. [Google Scholar] [CrossRef] [Green Version]

- Sockin, M.; Xiong, W. A Model of Cryptocurrencies. NBER Work. Pap. Series 2020, 1–57. [Google Scholar] [CrossRef]

- Queiroz, M.M.; Telles, R.; Bonilla, S.H. Blockchain and supply chain management integration: A systematic review of the literature. Supply Chain Manag. 2019, 25, 241–254. [Google Scholar] [CrossRef]

- Kim, T.H.; Kumar, G.; Saha, R.; Rai, M.K.; Buchanan, W.J.; Thomas, R.; Alazab, M. A Privacy Preserving Distributed Ledger Framework for Global Human Resource Record Management: The Blockchain Aspect. IEEE Access 2020, 8, 96455–96467. [Google Scholar] [CrossRef]

- Nygard, K.E.; Bugalwi, A.; Alruwaythi, M.; Rastogi, A.; Kambhampaty, K.; Kotala, P. Situational Trust and Reputation in Cyberspace. Int. J. Comput. Appl. 2019, 26, 154–163. [Google Scholar]

- Ren, Y.; Zhu, F.; Qi, J.; Wang, J.; Sangaiah, A.K. Identity Management and Access Control Based on Blockchain under Edge Computing for the Industrial Internet of Things. Appl. Sci. 2019, 9, 2058. [Google Scholar] [CrossRef] [Green Version]

- Munn, L.; Hristova, T.; Magee, L. Clouded Data: Privacy and the Promise of Encryption. Big Data Soc. 2019, 6, 205395171984878. [Google Scholar] [CrossRef]

- Paech, P. Securities, Intermediation and the Blockchain: An Inevitable Choice between Liquidity and Legal Certainty? Unif. Law Rev. 2016, 21, 612–639. [Google Scholar] [CrossRef]

- Kshetri, N. Can Blockchain Strengthen the Internet of Things? IT Prof. 2017, 19, 68–72. [Google Scholar] [CrossRef] [Green Version]

- Yeoh, P. Regulatory Issues in Blockchain Technology. J. Financ. Regul. Compliance 2017, 25, 196–208. [Google Scholar] [CrossRef]

- Xiong, Z.; Zhang, Y.; Niyato, D.; Wang, P.; Han, Z. When Mobile Blockchain Meets Edge Computing. IEEE Commun. Mag. 2018, 56, 33–39. [Google Scholar] [CrossRef] [Green Version]

- Dwivedi, S.K.; Amin, R.; Vollala, S. Blockchain Based Secured Information Sharing Protocol in Supply Chain Management System with Key Distribution Mechanism. J. Inf. Secur. Appl. 2020, 54, 102554. [Google Scholar] [CrossRef]

- Lee, S.Y. PHR System Using Blockchain Technology. Int. J. Adv. Trends Comput. Sci. Eng. 2019, 8, 3188–3193. [Google Scholar] [CrossRef]

- Di Francesco Maesa, D.; Mori, P. Blockchain 3.0 Applications Survey. J. Parallel Distrib. Comput. 2020, 138, 99–114. [Google Scholar] [CrossRef]

- Francisco, K.; Swanson, D. The Supply Chain Has No Clothes: Technology Adoption of Blockchain for Supply Chain Transparency. Logistics 2018, 2, 2. [Google Scholar] [CrossRef] [Green Version]

- Katyayani, J.; Varalakshmi, C. Cognitive Computational Model for Evaluation of Fintech Products and Services with Respect to Vijayawada City, Ap. Int. J. Innov. Technol. Explor. Eng. 2019, 8, 1733–1736. [Google Scholar] [CrossRef]

- Yu, F.R.; Liu, J.; He, Y.; Si, P.; Zhang, Y. Virtualization for Distributed Ledger Technology (VDLT). IEEE Access 2018, 6, 25019–25028. [Google Scholar] [CrossRef]

- Ar, I.M.; Erol, I.; Peker, I.; Ozdemir, A.I.; Medeni, T.D.; Medeni, I.T. Evaluating the Feasibility of Blockchain in Logistics Operations: A Decision Framework. Expert Syst. Appl. 2020, 158, 113543. [Google Scholar] [CrossRef]

- Chen, J.; Lv, Z.; Song, H. Design of Personnel Big Data Management System Based on Blockchain. Future Gener. Comput. Syst. 2019, 101, 1122–1129. [Google Scholar] [CrossRef] [Green Version]

- Buocz, T.; Ehrke-Rabel, T.; Hödl, E.; Eisenberger, I. Bitcoin and the GDPR: Allocating Responsibility in Distributed Networks. Comput. Law Secur. Rev. 2019, 35, 182–198. [Google Scholar] [CrossRef]

- Tang, C.S.; Veelenturf, L.P. The Strategic Role of Logistics in the Industry 4.0 Era. Transp. Res. Part E Logist. Transp. Rev. 2019, 129, 1–11. [Google Scholar] [CrossRef]

- Sebastião, H.; Godinho, P. Forecasting and Trading Cryptocurrencies with Machine Learning under Changing Market Conditions. Financ. Innov. 2021, 7, 1–30. [Google Scholar] [CrossRef]

- Weiss, M.B.H.; Werbach, K.; Sicker, D.C.; Bastidas, C.E.C. On the Application of Blockchains to Spectrum Management. IEEE Trans. Cogn. Commun. Netw. 2019, 5, 193–205. [Google Scholar] [CrossRef] [Green Version]

- Yin, H.; Guo, D.; Wang, K.; Jiang, Z.; Lyu, Y.; Xing, J. Hyperconnected Network: A Decentralized Trusted Computing and Networking Paradigm. IEEE Netw. 2018, 32, 112–117. [Google Scholar] [CrossRef]

- Schmidt, C.G.; Wagner, S.M. Blockchain and Supply Chain Relations: A Transaction Cost Theory Perspective. J. Purch. Supply Manag. 2019, 25, 100552. [Google Scholar] [CrossRef]

- Kaya, Y. Analysis of Cryptocurrency Market and Drivers of the Bitcoin Price: Understanding the Price Drivers of Bitcoinunder Speculative Environment. 2018. Available online: http://www.diva-portal.org/smash/record.jsf?pid=diva2%3A1295584&dswid=-2630 (accessed on 7 July 2021).

- Ahmad, F.; Kerrache, C.A.; Kurugollu, F.; Hussain, R. Realization of Blockchain in Named Data Networking-Based Internet-of-Vehicles. IT Prof. 2019, 21, 41–47. [Google Scholar] [CrossRef] [Green Version]

- Potts, M. The State of Information Security. Netw. Secur. 2012, 2012, 9–11. [Google Scholar] [CrossRef]

- Sullivan, C.; Burger, E. E-Residency and Blockchain. Comput. Law Secur. Rev. 2017, 33, 470–481. [Google Scholar] [CrossRef]

- Hassan, M.A.; Shukur, Z.; Hasan, M.K. An Efficient Secure Electronic Payment System for E-Commerce. Computers 2020, 9, 66. [Google Scholar] [CrossRef]

- Channgam, S.; Nilsook, P.; Wannapiroon, P. Intelligent Information Management with Digitization Workflow. Int. J. Mach. Learn. Comput. 2019, 9, 886–892. [Google Scholar] [CrossRef]

- Messina, D.; Barros, A.C.; Soares, A.L.; Matopoulos, A. An Information Management Approach for Supply Chain Disruption Recovery. Int. J. Logist. Manag. 2020, 31, 489–519. [Google Scholar] [CrossRef]

- Yue, G. Design of Information Management System for Structural Monitoring Based on Network Fragmentation. Int. J. Internet Protoc. Technol. 2020, 13, 202–210. [Google Scholar] [CrossRef]