The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance

1

DEGEIT—Department of Economics, Management, Industrial Engineering and Tourism, University of Aveiro, Campus Universitário de Santiago, 3810-193 Aveiro, Portugal

2

GOVCOPP—Research Unit on Governance, Competitiveness and Public Policies, Campus Universitário de Santiago, 3810-193 Aveiro, Portugal

3

INESCTEC—Institute for Systems and Computer Engineering, Technology and Science, R. Roberto Frias, 4200-465 Porto, Portugal

4

FEP—Faculty of Economics, University of Porto, R. Roberto Frias, 4200-464 Porto, Portugal

*

Author to whom correspondence should be addressed.

Risks 2022, 10(5), 103; https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050103

Submission received: 16 March 2022

/

Revised: 29 April 2022

/

Accepted: 5 May 2022

/

Published: 12 May 2022

(This article belongs to the Special Issue Managing Financial Risks Based on Corporate Social Responsibility for Sustainable Development)

Abstract

:The article aims to appraise the role of Corporate Social Responsibility (CSR) and innovation strategies as leverages of a company’s financial performance. The theoretical and empirical statement of this link aims to reinforce the importance of these strategical options in both the managerial and the public policy domain. Shedding light on the economic return of these practices will help managers make better strategic decisions. Policy makers will also grasp the required evidence to encompass CSR in policy packages. To address the research question, data were collected from the Thomson Reuters Eikon Datastream covering the 1000 largest companies listed on the stock exchange worldwide. Thereafter, hierarchical linear regressions were performed to produce the econometric results. Two time frames (2015–2019) were compared to address time–space trends. Enrolling in CSR activities entails additional costs which can undermine the company’s financial performance if not properly supported by public policies. Combining CSR and innovation appears to be the best strategy for companies seeking improvements in their financial performance while being socially responsible. The contribution of this study is threefold: first, the analysis covers the largest thousand firms in operation worldwide; secondly, the econometric results demonstrate that combining CSR with innovation positively impacts financial performance; and lastly, the time comparison evidences a positive but slow evolution in CSR adoption. The article provides an applied perspective, of use both for managers and policy makers, as to how they should approach and disseminate involvement in these types of activities.

1. Introduction

The analysis of Corporate Social Responsibility (CSR) has been a subject of intense debate, both for academics and practitioners, especially regarding its effects on corporate strategy and value creation. CSR activities are associated with a combination of economic, social, and environmental factors, three domains that are critical to a company’s strategic success. Involvement in these types of activities, when accurately managed and aligned with the business model, is a driving strategy for value creation. Extant literature (e.g., Ferrell et al. 2016; Ali et al. 2019; Broadstock et al. 2019; Javed et al. 2020; Sameer 2021; Gil 2022) state that companies involved in CSR activities can create indirect value for their business, and this value can be assessed through their relationships with stakeholders. According to Costa et al. (2015), the involvement in these activities also allows them to obtain external knowledge, thus increasing absorptive capacity in knowledge related to their corporate and innovative performance. It is important to consider that the impact of the involvement in these activities is mostly perceived through intangible benefits; however, according to Chong and Tan (2010), these later translate into tangible benefits.

Within the topic of CSR, the link with corporate performance is often more investigated in the literature (e.g., Ali et al. 2019; Lahouel et al. 2020; Wu et al. 2020); however, a significant gap remains when considering the relationship between CSR and innovative performance (Martinez-Conesa et al. 2017). Surprisingly, studies such as Gallego-Álvarez et al. (2011) concluded that the CSR–innovation binomial has negative effects for the company, and involvement in CSR practices does not always allow companies to create value. The study conducted by Im et al. (2020) concluded that involvement in CSR activities also allows the company to create value in various aspects, such as an increase in the commitment of its employees (Fatma et al. 2018), which will allow the company to improve its level of production and innovative efficiency (Ali et al. 2019; Sameer 2021). Other articles from Macgregor and Fontrodona (2008), Mishra (2017), and Cook et al. (2019) are examples of studies that claim that companies with a high level of performance in CSR are more efficient in terms of their innovative performance, as well as the promotion of sustainability practices (Hao and He 2022).

However, despite the evidence suggesting that the relationship between CSR and innovation should be considered as a relevant but positive aspect in the elaboration of the corporative strategy, there is still a lack of consensus on this matter as well as the effective purpose of its underlying cause (Lee et al. 2018; Duque-Grisales and Aguilera-Caracuel 2019; Uyar et al. 2020), especially due to the converse results obtained in empirical studies that assess the performance of this relationship (e.g., Martinez-Conesa et al. 2017).

Still, the present debate, when addressing the relationship between CSR and innovation, points towards an emergent yet controversial topic, responsible innovation. This topic is associated with the negotiation of responsibility between scientists, innovators, and the exogenous environment (Stilgoe et al. 2013) and their effective positioning towards society (Uyar et al. 2020). In the same vein as CSR, the main purpose of this innovation mindset is to understand the impacts of technologies in social, environmental, and economic terms (Von Schomberg 2014). There has been a growing concern in understanding the intended and unintended consequences of the introduction of new technologies in society; however, there is no consensus regarding this assessment due to the difficulty of containing desirable and undesirable effects (Lee et al. 2018; Uyar et al. 2020).

The objective of the paper is multifold: at first, it aims to address the importance of CSR practices in firm performance; secondly, it combines the CSR with innovative practices to better understand if the combined strategy will leverage the positive results for the firm’s financing. Thirdly, it appraises the financial performance through alternative measures to better clarify the outcome of this strategy from different perspectives and time spans, as the financial reporting will be impacted by different timings. Lastly, it compares the achievements in 2015 to those of 2019 to grasp insights about the time trends and the perspectives for the future.

To explore and contribute to the clarification of the precise relations and limitations listed above, hierarchical linear regressions were run using a set of explanatory variables covering the three vectors of analysis: the first includes several variables to assess the company’s achievements in regards to CSR; the second is innovative performance; and the third is financial performance ratios, and controls regarding firm structural traits were also included. Data were collected from the top (largest) 1000 companies listed on the stock exchange from the Thomson Reuters Eikon Datastream database.

The remaining of this paper is structured as follows. Section 2 encompasses a literature review, contextualizing the main concepts in the debate and proposing a conceptual model. Then, Section 3 details the materials and the methods, as well as some exploratory analysis of the collected sample. Section 4 follows, in which the econometric estimations and results are presented. Lastly, Section 5 summarizes the conclusions, limitations, and policy recommendations.

2. Theoretical Background

2.1. CSR from a Diachronic Perspective

Social responsibility is not new to academic study. This topic has been present in society, the entrepreneurial milieu, and the academia for several decades, and its evolution to this day has been the subject of considerable debate, especially when it comes to studying whether companies benefit or not from involvement in activities in favor of society.

The emergence of social responsibility in companies originated in the beginning of the 20th century, where CSR was seen only as a philanthropic act, in which companies performed acts of charity and stewardship towards society (van Marrewijk 2013). However, its definition and purpose began to expand in the early 1950s and 1960s, largely due to an increase in production intensity in companies along with the start of the second phase of the industrial revolution. At this time, due to a high workload and some failures in human management by the companies, the first proposals related to the company’s concern for the well-being of its workers started to appear. It was then that CSR studies began to emerge in the academic area, with the main objective of demonstrating to managers and administrators that, in addition to the economic function, companies should consider the social consequences of their actions. With that, not only would companies be seen as good places to work, it would be possible to achieve competitive advantages over the corporate strategy of their competitors (Barrena Martínez et al. 2016).

With the emergence of more studies, the idea of CSR gained momentum in the late 60s. These works aimed at defining what social responsibility in companies is and how this topic could be correctly addressed by managers. In 1953, Bowen’s seminal book proposed what can be considered as the basis by which managers and academics can be guided to explore this theme. Since then, in the academic area, CSR has been increasingly explored, especially to reach a consensus on how it should be defined, both in the business and academic world (Barrena Martínez et al. 2016). Much of the lack of conceptual consensus is due to the existence of a great abundance of definitions, often biased towards certain specific interests (van Marrewijk 2013) and also due to the different theories that exist to explain the behavior of companies with regard to the problems they face related to their social responsibility (Gallego-Álvarez et al. 2011).

The shareholder theory is considered as the classical view, in which the social responsibility of the firm consists in maximizing its profit, and the responsibilities must come from individuals and not from the business itself (Friedman 1970). According to Quazi and O’Brien (2000), companies should focus on meeting their established objectives, placing greater emphasis on meeting the needs of their customers. Following the stakeholder theory, Freeman and McVea (2001) argue that managers must satisfy a variety of stakeholders, such as customers, workers, and suppliers, while not giving greater emphasis to just one. Davis (1960) states that companies that use their power without being concerned about their impact on the community in which they operate can lose the trust and respect of their stakeholders. More recently, Branco and Rodrigues (2006) state that customers and external stakeholders are attracted to companies that have a good reputation when it comes to issues related to social responsibility. Lastly, the social theory encompasses a vision in which companies are responsible for the society as a whole, since they integrate into and are an essential part of it (van Marrewijk 2013). The existence of a multiplicity of theories associated with the definition of CSR provides no consensus on the its best description. The co-existence of a multiplicity of theoretical frameworks can be explained due to the dissemination of the subject over the years and how it is seen and approached by companies today (Ho 2015).

The stakeholder theory is generally present in the literature as conventional CSR theory (Bocquet et al. 2012). Aligning the present study with this statement, in the same vein as the analysis carried out by Dahlsrud (2008), the definition most frequently used and related to this theory is presented by the Commision of the European Communities (2001, p. 4): “A concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis.”

2.2. The Influence of CSR on Corporate Performance Perspectives

The relevance in debating how involvement in responsible activities affects performance in companies, namely whether it improves, decreases, or simply has no effect on their performance, has been high in recent years (Lee et al. 2018; Broadstock et al. 2019; Lin et al. 2019). All in all, over the years there have been several empirical studies that attempt to assess the relationship between CSR and corporate performance and vice versa, with most results showing undefined conclusions (e.g., Lee et al. 2018). However, there are two studies (Orlitzky et al. 2003; Wang et al. 2016), both using a meta-analysis methodology, which assess a large number of studies on the subject. These studies concluded that the relationship is positive and that the involvement of companies in responsible activities improves their financial performance due to improvements in their corporate management. They also reveal that this relationship is stronger for firms from developed economies than for firms from developing economies. Considering the fact that the two variables are directly correlated, the above-mentioned stakeholder theory is the one that best fits this assumption; however it is necessary to better understand the magnitude of the impact that these social activities have on the company in a multiplicity of domains.

At the end of the 20th century, the responsible activities carried out by companies were limited to donations or acts of charity towards society. However, it is important to recognize that the philanthropic nature of these acts has changed to the present day. At the beginning of the 21st century, consumers began to pay more attention to the products they purchased, how their production was carried out, and what the effects of that product on society were (Im et al. 2020). The shift in the mindset began to be seen as increasingly important to the company’s stakeholders, from CEOs to employees and external stakeholders (Branco and Rodrigues 2006; Javed et al. 2020; Gil 2022; Hao and He 2022). In a more present time frame, we can say that more and more companies will not wait for a responsible choice from the user community and will move forward with strategic decisions in terms of social responsibility (Javed et al. 2020; Lahouel et al. 2020). This investment in CSR activities can be understood from two perspectives: proactive CSR, where a company integrates CSR in its business model with an objective of sustainability and building value with several stakeholders; and reactive CSR, where companies only engage in these activities due to legal and risk management issues (Ji et al. 2019; Wu et al. 2020).

When a company invests in CSR activities, it reinforces its reputation as trustworthy and honest, increasing trust among its stakeholders (Im et al. 2020). This reputation, once obtained, is considered as valuable and inimitable, becoming therefore an intangible asset (Russo and Fouts 1997). In the article by Nidumolu et al. (2009) considering future implications, the authors state that only companies that take the sustainability issue into account will be able to achieve a competitive advantage over their competitors. This statement goes in line with Russo and Fouts (1997), who claim that a high level of environmental performance is associated with an increase in the company’s profitability. It is even possible to point out advantages at an internal level (Wu et al. 2020). A company focusing on social responsibility activities is fostering a competitive work environment while building a strong organizational commitment, allowing its employees to acquire new skills while cultivating social empathy (Fatma et al. 2018) and enrolling in responsible leadership training (Javed et al. 2020). The involvement in these types of activities helps companies to develop better skills and organizational processes that increase their preparation for possible changes that involve the entrepreneurial ecosystem (Orlitzky et al. 2003). By creating a strong organizational culture, known for its sustainable reputation, it is also easier to attract top candidates (Russo and Fouts 1997; Fatma et al. 2018), therefore initiating prosperity cycles.

Consequently, the investment in these activities brings important results to companies, with the majority being in the form of intangible resources. All of them involve a cost, and a difficulty may arise here for some investors and company stakeholders related to the assessment of the value of these types of decisions (Broadstock et al. 2019). However, currently these types of resources are considered of high importance for improvements in company’s operations and are classified often as goodwill. Know-how, corporate culture, and reputation are intangible assets which are increasingly important to a company’s financial success (Branco and Rodrigues 2006).

2.3. The Relationship between CSR and Innovation

Within the study of the impact of social responsibility activities on corporate performance, it is important to consider how the first relates to the innovative performance; this missing link constitutes an area of growing interest among both the scientific and non-scientific community. The connection between CSR and innovation is addressed in previous works, which aim at connecting CSR and corporate performance, and the literature suggests that CSR can benefit a company’s performance through the promotion of innovation capabilities (Mc Williams and Siegel 2018). As previously mentioned, some studies on the relationship between CSR and innovation found a positive relationship among them (Ji et al. 2019; Luo and Du 2015), while others highlight the existence of negative associations between the two topics (Gallego-Álvarez et al. 2011).

Below, a conceptual model is drawn, based on the expected connections between the two topics as well as the expectable outcomes. Involvement in CSR activities is considered a powerful source of innovation and thus as reinforcing the existence of competitive advantages (Broadstock et al. 2019); therefore, it is important to acknowledge, in detail, the impact of innovative aspects when combined with the identity of a company, some of those being corporate culture and its employees. Motivated employees who trust their superiors and identify with a responsible business culture offer companies less challenges for hiring to work within the innovation area. This fact relies on the link between responsibility and innovation, often associated due to the positive impact that it is possible to obtain with new sustainable developments. However, it is important to concentrate on the fact that CSR, sustainability, and innovation do not form a sacred trinity, says Bennink (2020).

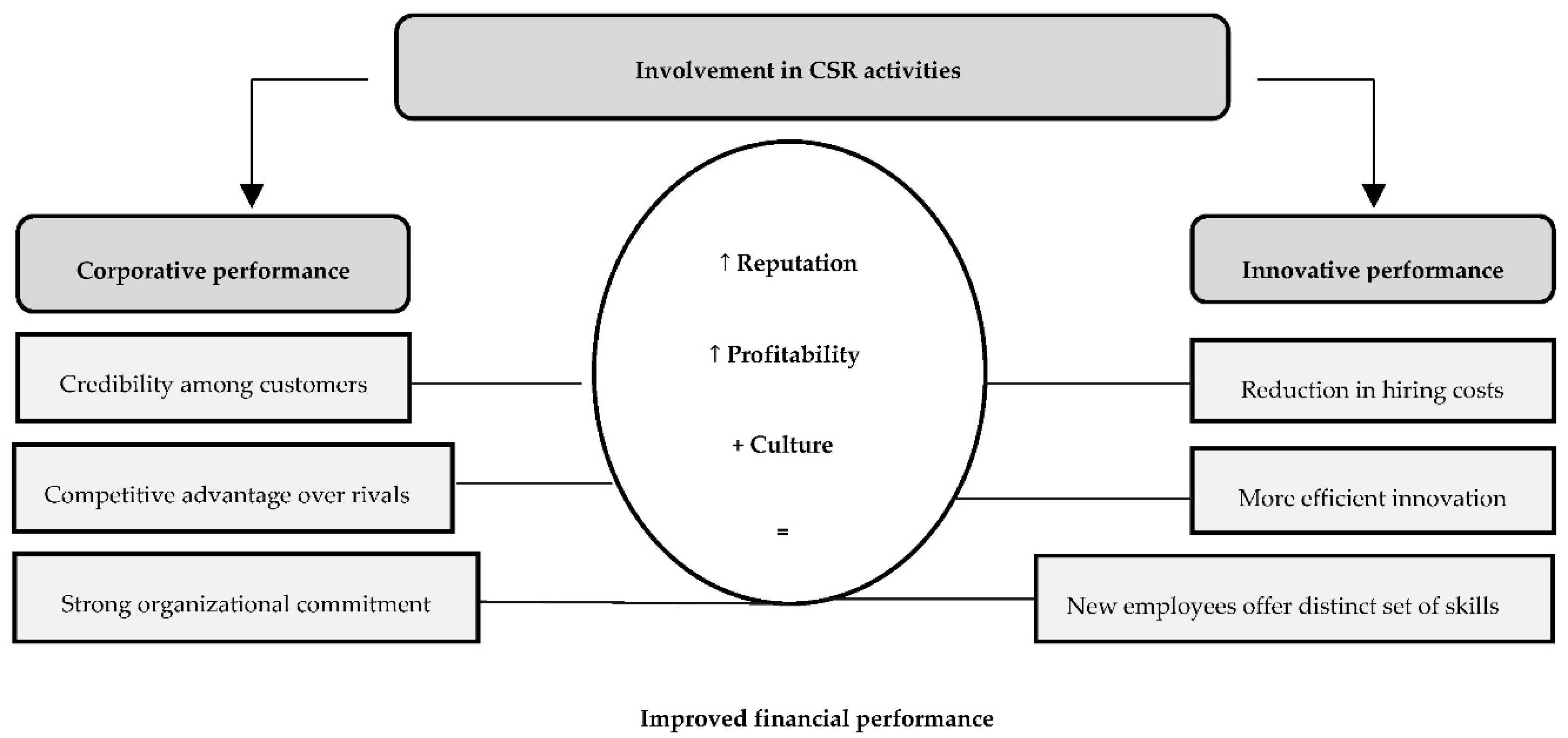

According to the study of Macgregor and Fontrodona (2008), involvement in CSR activities gives companies access to a structure that allows them to innovate sustainably and with less risk. The same author suggests that companies that do not consider CSR activities may have difficulties surviving as they will face problems innovating. A high level of involvement in CSR activities increases the economic value of a company’s innovation due to greater efficiency in innovation activities and lower hiring costs. Moreover, companies involved in CSR activities are able to easily obtain access to financing, thus allowing the company to transfer its innovative ideas to products, services, or even improvements to its organizational processes (Im et al. 2020). Bocquet et al. (2013) states that companies involved in these activities are more likely to be innovative in terms of their productive processes and the generation of new products. Figure 1 presents the interconnection of these aspects, evidencing the two dimensional effect of CSR actions in either innovative and financial dimensions. The involvement in those actions will raise firm reputation and profitability while consolidating its culture which will persistently boost the positioning in the market and increase the attractiveness towards investors and stakeholders.

As a consequence, CSR can be used to develop innovative skills that are new to the company; however, it is important to consider that these skills are not always purely technological and that social innovations, in some cases, can have a more beneficial impact on companies (Broadstock et al. 2019). According to Gallego-Álvarez et al. (2011), CSR offers opportunities for innovation through social, environmental, or sustainability motivations that allow the creation of new ways of working or new work processes. Once again, as in corporate performance, all the possible benefits that can accrue to innovative performance from involvement in socially responsible activities are hard to measure, but are unavoidable to attract the attention of stakeholders.

The outreach of CSR practices seems to be of increased importance, as the entire ecosystem seeks responsible actions and the commitment of managerial strategies towards the preservation of the environment, the respect for society, as well as the improvement of corporate governance. In this vein, innovation will naturally fuel the adoption of new practices that further reinforce firm reputation, increasing the public’s willingness to trust a company. As such, innovation is the missing link to clinch virtuous cycles of sustainability emerging from firms and spreading to the society.

2.4. Appraisal of the Most Cited Literature

Table 1 presents the most cited scientific articles present in Scopus encompassing the main keywords related to the research. It is observed that the type of methodology present in the studies combines theoretical and empirical aspects; however, the empirical studies are sector- or market-specific. Notwithstanding, the results prove that the involvement of companies in social responsibility activities positively affects innovative performance in multiple corporate areas. Having thus analyzed the existing literature, the empirical analysis will be grounded on a central hypothesis: CSR leverages the innovative performance of companies, therefore improving financial performance.

2.5. The Emergence of Responsible Innovation

There is an emergent concept trying to scrutinize the combined effect of responsibility and innovation—responsible innovation. Recent studies in the field have emerged in academic and political literature, despite its emphasis. As previously mentioned, some companies are considering more aspects beyond the economic return of their innovative activities: they are starting consider aspects and impacts at both the social and environmental level (Bennink 2020). Increasingly, the creation and development of new technologies has a significant impact on society, and these impacts can be positive or negative. As in the topic of CSR, there should be a high responsibility towards society on the part of researchers and suppliers of these technologies. In terms of the policy action, it is important that there are specific controls, especially for future implications. There must be an ability to anticipate and prevent eventual negative spillovers before launching new innovations in the market. However, are researchers or companies themselves able to anticipate the possible impacts on their own? This is where responsible innovation comes in. According to the European Commission’s scientific policy team leader Von Schomberg (2014), responsible innovation is: “a transparent, interactive process by which societal actors and innovators become mutually responsive to each other with a view to the (ethical) acceptability, sustainability and societal desirability of the innovation process and its marketable products (in order to allow a proper embedding of scientific and technological advances in our society)”.

While this paradigm is a soundbite, it fails to demonstrate how complicated it is to reach a consensus on what is right and what is considered favorable for all. Von Schomberg (2014) refers to the importance of the existence of government policies capable of socially intervening in the research and innovation process, with the aim of having better control over impacts, whether positive or negative.

3. Methodology

3.1. Sample Description

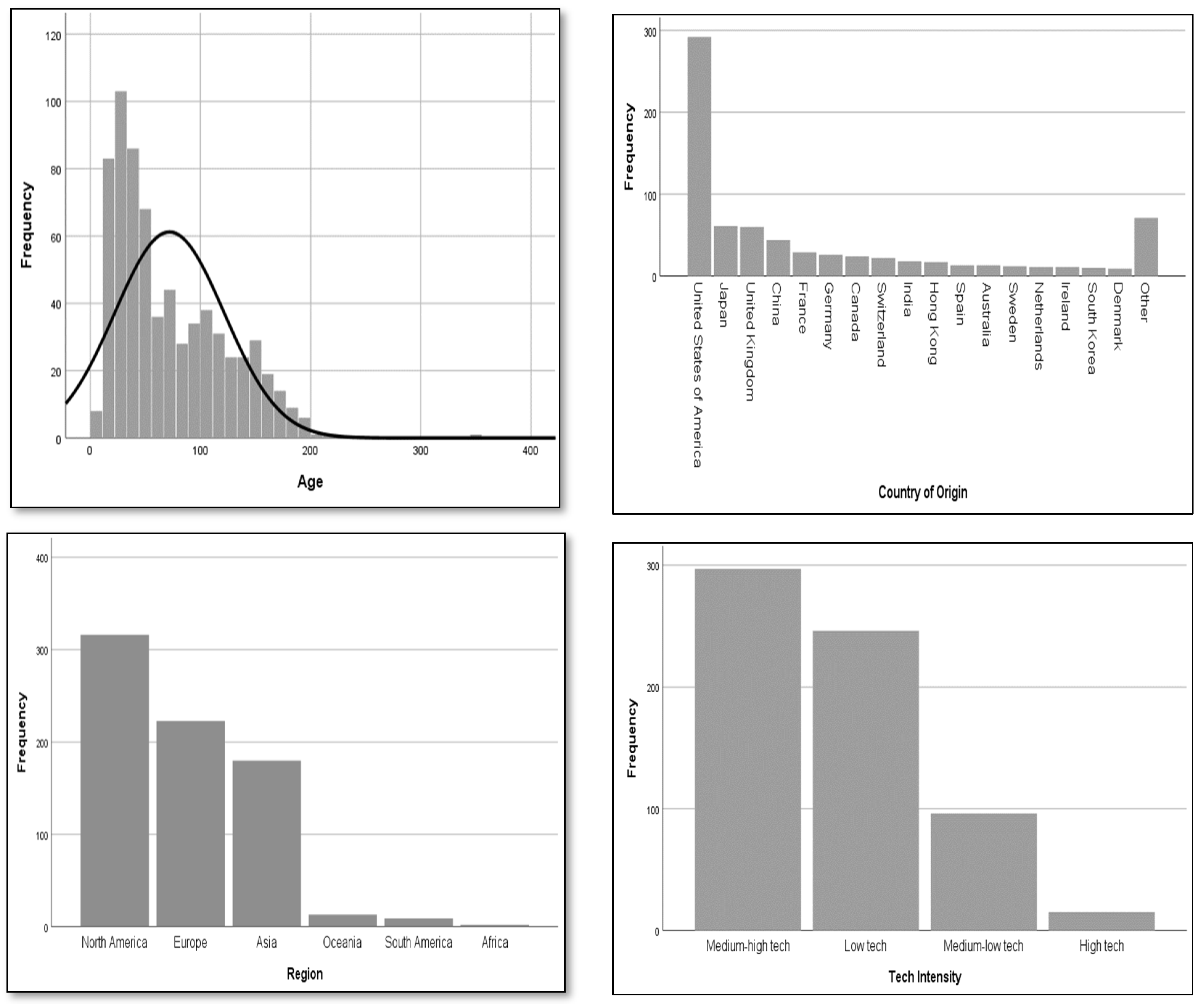

The empirical analysis performed to validate the research question relies on data collected from the top (largest) 1000 companies listed on the Thomson Reuters Eikon Datastream database. The verification of an important number of missing observations for the relevant variables in use allowed the maintenance of 744 of the companies listed, all of them present in the stock exchange. This procedure allowed the construction of a quasi-perfectly balanced panel covering the period of 2015–2019. Data from the last year of analysis were used as a reference. For a complete characterization of the sample and to ensure that any relationship found between innovation and social responsibility activities are not the result of other structural factors, variables such as sectoral technological intensity, age, and company size were also collected. The sample consists of companies spread over 39 countries from 6 different continents, with the most predominant countries being the United States of America (39%), Japan (8.2%), and the United Kingdom (8.1%). The average age presented by companies is 71 years, and 25 different sectors are present, with the financial and electronics industries being the most recurrent. Additional sample information can be found in Figure 2 below.

Observing the characteristics of the sample present in Table 2, the analyzed sample is mainly constituted by large companies with very high turnover values, evidencing the vast experience in the market they operate in. The choice of these types of companies relies on their impact on and representativeness of the business world as well as the societies in which they operate.

3.2. Proxying Corporate Social Responsibility

Due to the complexity of accurately measuring CSR and the narrowness of using single perspectives regarding the effect on company performance, four different variables were collected. Despite not being a perfect metric for evaluation, the ESG Score was observed as the richest and most complete variable in ranking company achievements, being used in several articles in the literature (e.g., Gil 2022). Notwithstanding the ESG metrics are uneven across data sources, being sometimes an increasing scale (e.g., Datastream/Refinitiv1) or a risk measurement (e.g., ESG Risk Sustainalitics2).

As the theme of CSR is in constant evolution, the ESG score given in the case of Datastream/Refinitiv seems to be a good starting point for conducting an analysis of the company’s performance in these domains. It consists of measuring a company’s performance in key environmental, social, and governmental attributes through 10 different categories: emissions, innovation, use of resources, human rights, product responsibility, workers, the community where it operates, business management, shareholders, and CSR strategy.

It is commonly accepted that ESG is a natural proxy for firms’ commitment towards sustainability, albeit, in the present, the score must evidence the social willingness to trust a certain organization, emphasizing the importance of communication and visibility. This view leads us to additionally include the strategy score, along with the reporting and the importance given to these governance domains by means of enrolling some of the staff members (committee) specifically to CSR. As such, the present research proposes a multidimensional proxy for CSR actions, covering not only the internal actions but also their perception in the community.

According to the data source (Refinitiv 2021), this score is assigned so that it is possible to transparently and objectively measure the performance, commitment, and effectiveness of a company in the environmental, social, and governmental spheres based on data publicly disclosed by the same companies. Table 3 provides a brief description of the variables used and their evaluation method.

When analyzing Table 4, there is a generalized positive evolution of the variables used to assess CSR between 2015 and 2019. Companies located in Asian and North American countries registered the greatest growth in social responsibility, with European countries not being far behind. Despite being late compared to the other regions, the topic of CSR in the Asian region has been gaining more relevance. As the involvement in CSR activities has been characterized as fundamental to the success of a company’s strategy, companies in the Asian region felt compelled to follow the standards established by the other regions.

This growth, when it occurs, is especially notorious in multinational companies (Chapple and Moon 2005). The adherence to CSR by Asian countries is considered important due to the impact that companies located in this region have on the world economy. Analyzing only the database used in this study, companies in the Asian region represent 60% of the sum of the annual turnover.

Converse to this pattern of growth, the South American companies present a decreasing trend, being the single region to evidence a decrease in the ESG score attributed to their companies and the smallest growth in the CSR Strategy Score. As a region comprised of developing countries, Visser (2009) states that the topic of CSR in these countries has been and continues to be strongly shaped by the weak socio-economic and political conditions, which tend to aggravate many environmental and social problems.

3.3. The Impact of CSR and Innovation on Financial Performance

To understand the relationship between CSR and innovative performance, and subsequently the effect on financial performance, several variables were collected. As aforementioned, some of the impacts felt by CSR appear to be hard to quantify, making it difficult to measure the impact felt by companies. The measurement of the innovative performance, the variables of investment in R&D, the net value obtained by companies through brands and patents, and whether companies develop eco-designed products were collected.

Financial performance was appraised from different perspectives, aiming to grasp evidence concerning instantaneous and postponed effects. To do so, five alternative dependent variables were collected: ROA, ROE, Tobin’s Q, Sales per Employee, and Annual Turnover. As control variables, the size of the company (number of employees), age, and technological intensity of the industrial sector in which they operate were used. Table 5 briefly describes the variables and their units of account.

Once more, choosing these five dependent variables will allow for assessing the impact on financial performance from different angles and time frames. When analyzing the effect on the Annual Turnover, it is expectable to find a quasi-instantaneous response, which means that in the present models, which are static, the effect should be of a higher magnitude. Through T’sQ, it is possible to understand the effect through the market and shareholders, which usually takes longer to be felt.

The evolution of variables shown in Table 6 follows the same growth pattern observed in terms of CSR. There is an increasing trend among companies belonging to the regions of North America, Asia, and Europe, especially noticeable in the variables that are related to the measurement of innovative performance. The highest scores are highlighted in bold below.

3.4. Descriptive Statistics and Correlations

Table 7 presents the descriptive statistics of all the variables in use, as well as the values of the correlations between them. To analyze the strength of the relationship between the variables, the evaluation method presented by Cohen (1988) was followed: 0.10 to 0.29—weak; 0.30 to 0.49—average; 0.50 to 1.0—strong. Following this assessment scale, we can observe high values of correlation between the CSR variables; the remaining variables have weak correlations, proving the independence among them. To further reinforce this information and confirm the inexistence of multicollinearity, correlations between variables were assessed once more along with linear regressions with Variance Inflation Factor (VIF) and tolerance tests, which presented values below the thresholds, rejecting the collinearity hypothesis.

4. Econometric Analysis

4.1. Econometric Estimations

To test our main hypothesis, a hierarchical linear regression was employed using three different models: model 1 tested the effect between the CSR variables (predictors) and the dependent variables; model 2 added the innovation performance variables to the predictors; model 3 added the control variables to the former predictors.

The addition of variables at each step aims to address if the addition of predictors consolidates the explanatory capacity of the model. Rather than performing a multiple regression analysis where the predictors are all simultaneously added to the regression, the idea is to add predictors to the model in a series of steps to understand what the impact of each vector of analysis is, and especially what the observed impact of the relationship between CSR and innovation is on the dependent variables.

Before running the econometric estimations, assumption tests were run. Shapiro–Wilk tests were performed on all dependent variables, which evidenced that none of them were normally distributed. To overcome this constraint, linear transformations were made for each dependent variable: square root transformation for ROA and ROE; and log10 transformation to T’sQ, SPEmp, and AT. Despite not achieving full normality, the new histograms evidenced a distribution much closer to the normal distribution curve. Correlations between the variables were once more evaluated to diagnose for multicollinearity due to the high correlations between the CSR variables in Table 7. Some correlations remained strong, although the VIF and tolerance tests completely ruled out the existence of multicollinearity. The inexistence of homoscedasticity was also confirmed, and identified outliers were left in the data for econometric estimations given their non-randomness (see Table 8).

4.2. Results and Discussion

This study was conducted to determine the impact of the relationship between CSR and innovation on the financial performance of companies. The central hypothesis is that the dependent variables (ROA, ROE, TsQ, SPEmp, and AT) can be predicted by two vectors of predictors which can measure the company’s CSR and innovation performance.

For Model 1, comprised of CSR variables as predictors, the impact is proven to be partially statistically significant for the dependent variables ROA and T’sQ, albeit with a negative impact, meaning that CSR deters financial performance. On the other hand, Models 2 and 3 evidence statistical significance in all dependent variables except for SPEmp.

The first set of models only encompasses CSR variables to appraise its importance on the different dimensions of financial performance. In line with Sameer (2021), the impact of CSR on ROA is negative; this result is contrary from Lu et al. (2020) and Maqbool and Zameer (2018), which evidence a positive effect. Notwithstanding, this may be due to the fact that the authors use an indicator which addresses “corporate governance, environmental and social issues and covers the 15 first-level indicators”, and the CSR strategy used here comprises the communication strategies.

The present results show that there is no impact of CSR on ROE. This result is divergent from Sameer (2021), which evidences a negative impact of environmental involvement. On the contrary, Maqbool and Zameer (2018) present a positive impact of ROE.

Moreover, Lu et al. (2020) only use one proxy for the financial performance, rather than the five alternatives proposed here. Maqbool and Zameer (2018) and Sameer (2021) test the effect of CSR on ROA and ROE. The other proxies for financial performance appraisal are seldom used; however, they fail to be statistically significant.

The second set of models includes alternative proxies for the innovation performance; this link is somehow similar to Hao and He (2022) but to us, innovative strategy is still an explanatory vector which connects to the CSR strategy, mutually reinforcing the financial performance. Here, innovative efforts positively influence the financial performance in different dimensions.

Lastly, Model 3 include firms’ structural characteristics such as size and technological intensity. The present results differ from extant literature such as Hao and He (2022) and Liao et al. (2022), as the structural characteristics are not detrimental to the financial performance.

In Table 9, it can be observed that Model 2 includes a set of variables where innovation variables were added to the CSR ones, and the R2 change and the significant F values show that this addition realized significantly better values for almost every analysis made. Model 3, with a broader perspective, provided us with a more detailed analysis given the broader set of predictors.

According to Table 9 and the significance of the values, we can conclude that the relationship between CSR and innovation is able to leverage a firm’s financial performance. Still, the standard coefficient values are not high across Models 2 and 3, which indicates that the strength of the effect of CSR and innovation on the dependent variable is somehow feeble. Notwithstanding this, the values related to R&D and especially EDPro are the most meaningful ones. According to descriptive statistics, although there are few companies involved in these types of activities, this variable proved to be the one with the greatest impact on the analyzed hypothesis. This evidences that companies which combine innovation with sustainability generate internal and external positive spillovers.

Since some companies do not feel fully confident in adopting a strong CSR strategy, public policies could focus on eco-designed activities as a starting point for responsible activities.

The control variables were also statistically significant albeit with a very small magnitude, which can be related to the sample being composed of very homogeneous individuals. Although some are larger, all of them are world giants; some will have more years in operation, but all of them have a significant impact on the global market, and hence they have reached market positions which make their effects very similar among them. The technological regime also does not make any impact on profitability. This result was quite expectable, as the sampling criteria allowed for the collection of the top revenues worldwide.

When performing the same analysis with data from 2015, Model 3 presents statistically significant values of CSR for some of the dependent variables, although the results are less impacting. The compared statics with 2019 evidenced the growth pattern relating to CSR. This shows that there exists a mature path towards true CSR and innovation integration in the same vein as that proposed by Macgregor and Fontrodona (2008).

5. Conclusions

5.1. Theoretical and Empirical Findings

The empirical results emerging from the econometric estimations evidence that innovation is one of the main driving forces for sustainable development and the promotion of financial growth in companies. It is evident that investments in R&D as well as in eco-design have overwhelming effects on firm performance compared to other strategies.

The involvement in CSR activities appears as insignificant or even as a sunk cost to the operation. This result needs further assessment as this evidence endangers the dissemination of CSR practices, mostly in times of crisis. It seems that much more has to be done on the part of policy makers to compensate for these so-far voluntary actions or to make them compulsory. Notwithstanding this, the user community is playing its role, as the adoption of eco-design products appears to positively influence company profitability. This strategy is to some extent a demand-driven combination of CSR and innovation that also needs more support from policy packages given its desirability. The importance of this result evidences that when a company develops an innovative strategy based upon responsible practices, there is an economic return. In doing so, it also manages to make the most of CSR, however indirectly, and from a different perspective that is a narrow interpretation of the framework.

These results can also be considered disturbing for companies that are merely seeking to add value through their involvement in CSR activities. They should be taken as a good starting point for policy makers to build a strategy that encourages the development and growth of these types of activities for companies more afraid to dig into the subject.

Once more, the results obtained for eco-design are promising as they contribute to the literature highlighting the emergence and the centrality of responsible innovation. As stated, almost all studies in the academic world related to responsible innovation are theoretical. This is mainly due to the difficulty in obtaining the correct metrics to measure it. Observing the significant values obtained with the EDPro variable, we can suggest it as a possible metric for evaluating how companies manage to innovate responsibly.

Finally, it is evident that the user community has an important awareness of the importance of sustainable and responsible practices, and the monetary votes of consumers are playing their role. Companies did perceive the market’s pulse, and those adopting these practices are leveraging their economic return. It seems that the loose link comes from governance, as the voluntary adoption of CSR practices with regard to reporting, publication, and the company committee, among others, are at present an economic burden. Urgent actions need to be taken, as adverse economic contexts will make those responsible organizations throw in the towel, as the evidence from South American corporations in the sample has shown.

5.2. Limitations and Future Research

The present study is comprised only of large multinational companies with vast experience in the market where they operate due to either their market share or to their years in operation, being world giants present in the most representative stock exchanges. As a consequence, and due to their establishment in their industry, the impact of these activities may not be traceable in their billion-dollar financial statements. It would be interesting to see the effect on smaller companies with broader representativeness and understand the effect on their financial performance when they combine CSR and innovation.

Moreover, the analysis encompassed a specific time frame, and it needs further reinforcement to verify the time consistency. Notwithstanding this, the present analysis did compare two time frames returning consistent results. However, in future research, it would be interesting to obtain data for proactive and reactive CSR to try to understand the effect felt on financial performance through the two possible strategies of adoption by companies. It would also be interesting to conduct a dynamic analysis in which it would be possible to better assess the effects felt over time. Conducting this type of analysis will bring even more consistent results since these types of strategies require some time to fully assess the impact felt on companies’ performance.

5.3. Policy Recommendations

Based on the results obtained, it is possible to state that the combined relationship between CSR and innovation positively impacts a company’s financial performance. However, the single adoption of CSR procedures reboots some skeptical achievements in performance. Taking this into consideration, this evidence must consubstantiate a good foundation for policy makers to keep promoting and improving CSR activities in companies. Since the involvement in CSR activities are accompanied with costs, which can lead to a decrease in a company’s financial performance, it is important that public policies can foster the persistent promotion of more responsible actions while supporting them.

Comparing the results obtained from the 2015 and 2019 analysis, it is possible to state that this type of strategy may take some time to impact companies’ performance. This evidence demonstrates that this type of strategy has not been properly supported by the governments, which need to globality devote more attention to this problem. If there had been the correct support for companies during this period, the effect felt on corporate performance could have been accelerated and felt in less time. It is also important to state that through the results obtained, public policies should broadly support all sectors of activity and not focus on certain ones.

The positive results with the eco-designed innovative products would be a good starting point for policy makers to encourage and improve these types of activities in companies, supporting those who promote sustainability and innovation together while responsibly taking care of the community. The already existing policies related to the theme of eco-designed products need to be review and consolidated in a way that will help to ensure that the impact felt takes less time to be observed and that manages to captivate more companies to join this type of innovation mindset.

Globally, policy makers, especially those operating in Europe, are not finding the right instruments to foster involvement in CSR activities as they should when compared with their North American and Asian counterparts. The strategies of the regions referred to need to be observed as good practices to accelerate this transition in Europe, such that the growth impact is felt with the same intensity. It will be even more important for transnational institutions as well as world leaders to promote quick growth in the regions of South America and Africa, as these continue to be hampered by their weak socio-economic conditions. The most important thing in achieving similar results across all regions will be for the business world to continue to contribute to improving society’s quality of life and contributing to achieving sustainable development goals established by the United Nations. It seems that the aim of providing the people a useful and decent life while respecting the planet may be possible if all players understand and play their role, and responsible practices in innovation and management have proven to be core to this agenda.

Author Contributions

Conceptualization, J.C.; methodology J.C. and J.P.F.; software, J.P.F.; validation, J.C.; formal analysis, J.C.; investigation, J.C. and J.P.F.; resources, J.P.F.; data curation, J.P.F. and J.C.; writing, J.C.; review and editing, J.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data were collected from the Thomson Reuters Eikon Datastream database.

Conflicts of Interest

The authors declare no conflict of interest.

| 1 | |

| 2 | https://www.sustainalytics.com/esg-data (accessed on 15 February 2022). |

| 3 | Rating used to rank: Eurostat NACE Rev.2 3-digit level—Classification of manufacturing industries. |

References

- Ali, Rizwan, Muhammad S. Sial, Talles V. Brugni, Jinsoo Hwang, Nguyen V. Khuong, and Thai H. T. Khanh. 2019. Does CSR Moderate the Relationship between Corporate Governance and Chinese Firm’s Financial Performance? Evidence from the Shanghai Stock Exchange (SSE) Firms. Sustainability 12: 149. [Google Scholar] [CrossRef] [Green Version]

- Barrena Martínez, Jesus, Macarena López Fernández, and Pedro Miguel Romero Fernández. 2016. Corporate social responsibility: Evolution through institutional and stakeholder perspectives. European Journal of Management and Business Economics 25: 8–14. [Google Scholar] [CrossRef] [Green Version]

- Bennink, Hans. 2020. Understanding and Managing Responsible Innovation. Philosophy of Management 19: 317–48. [Google Scholar] [CrossRef]

- Bocquet, Rachel, Christian Le Bas, Caroline Mothe, and Nicolas Poussing. 2012. CSR Firm Profiles and Innovation: An Empirical Exploration with Survey Data. SSRN Electronic Journal. [Google Scholar] [CrossRef] [Green Version]

- Bocquet, Rachel, Christian Le Bas, Caroline Mothe, and Nicolas Poussing. 2013. Are firms with different CSR profiles equally innovative? Empirical analysis with survey data. European Management Journal 31: 642–54. [Google Scholar] [CrossRef] [Green Version]

- Branco, Manuel Castelo, and Lúcia Lima Rodrigues. 2006. Corporate social responsibility and resource-based perspectives. Journal of Business Ethics 69: 111–32. [Google Scholar] [CrossRef]

- Broadstock, David, Roman Matousek, Martin Meyer, and Nickolaus Tzeremes. 2019. Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental and social governance implementation and innovation performance. Journal of Business Research 119: 99–110. [Google Scholar] [CrossRef]

- Chapple, Wendy, and Jeremy Moon. 2005. Corporate social responsibility (CSR) in Asia a seven-country study of CSR Web site reporting. Business and Society 44: 415–41. [Google Scholar] [CrossRef] [Green Version]

- Chong, Wei, and Gilbert Tan. 2010. Obtaining Intangible and Tangible Benefits from Corporate Social Responsibility International Review of Business Research Papers Corporate Social Responsibility. Singapore: Institutional Knowledge at Singapore Management University, pp. 360–71. [Google Scholar]

- Cohen, Jacob. 1988. Statistical Power Analysis for the Behavioral Sciences, 2nd ed. London: Routledge. [Google Scholar]

- Commision of the European Communities. 2001. Green Paper—Promoting a European framework for Corporate Social Responsibility. Brussels: Commision of the European Communities. [Google Scholar]

- Cook, Kristen, Andrea Romi, Daniela Sánchez, and Juan Sánchez. 2019. The influence of corporate social responsibility on investment efficiency and innovation. Journal of Business Finance and Accounting 46: 494–537. [Google Scholar] [CrossRef]

- Costa, Cláudia, Luís Lages, and Paula Hortinha. 2015. The bright and dark side of CSR in export markets: Its impact on innovation and performance. International Business Review 24: 749–57. [Google Scholar] [CrossRef]

- Dahlsrud, Alexander. 2008. How corporate social responsibility is defined: An analysis of 37 definitions. Corporate Social Responsibility and Environmental Management 15: 1–13. [Google Scholar] [CrossRef]

- Davis, Keith. 1960. Can business afford to ignore social responsibilities? Corporate Social Responsibility 2: 23–29. [Google Scholar] [CrossRef]

- Duque-Grisales, Eduardo, and Javier Aguilera-Caracuel. 2019. Environmental, Social and Governance (ESG) scores and financial performance of multilatinas: Moderating effects of geographic international diversification and financial slack. Journal of Business Ethics 168: 315–34. [Google Scholar] [CrossRef]

- Fatma Mobin, Imran Khan, and Zillur Rahman. 2018. Striving for legitimacy through CSR: An exploration of employees responses in controversial industry sector. Social Responsibility Journal 15: 924–38. [Google Scholar] [CrossRef]

- Ferrell, Allen, Liang Hao, and Luc Renneboog. 2016. Socially responsible firms. Journal of Financial Economics 122: 585–606. [Google Scholar] [CrossRef] [Green Version]

- Freeman, Edward, and John McVea. 2001. A Stakeholder Approach to Strategic Management. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Friedman, Milton. 1970. The social responsibility of business is to increase its profits. Corporate Social Responsibility, 31–35. [Google Scholar]

- Gallego-Álvarez, Isabel, José Manuel Prado-Lorenzo, and Isabel Maria García-Sánchez. 2011. Corporate social responsibility and innovation: A resource-based theory. Management Decision 49: 1709–27. [Google Scholar] [CrossRef]

- Gil, Cohen. 2022. What can we learn from the financial market about sustainability? Environment Systems and Decisions 42: 1–7. [Google Scholar] [CrossRef]

- Hao, Jing, and Feng He. 2022. Corporate Social Responsibility (CSR) Performance and Green Innovation: Evidence from China. Finance Research Letters 48: 102889. [Google Scholar] [CrossRef]

- Ho, Virginia Harper. 2015. Corporate Social Responsibility in China: Law and the Business Case for Strategic CSR. SCJ Journal of International Business & Law. Available online: https://0-heinonline-org.brum.beds.ac.uk/hol-cgi-bin/get_pdf.cgi?handle=hein.journals/scjilb12andsection=5 (accessed on 22 March 2022).

- Im, Hyun, Roy Song, and Meng Zhao. 2020. CSR Performance and the Economic Value of Innovation. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Javed, Muhzar, Muhammad Rashid, Ghulam Hussain, and Hafiz Ali. 2020. The effects of corporate social responsibility on corporate reputation and firm financial performance: Moderating role of responsible leadership. Corporate Social Responsibility and Environmental Management 27: 1395–409. [Google Scholar] [CrossRef]

- Ji, Huanyong, Guannan Xu, Yuan Zhou, and Zhongzhen Miao. 2019. The impact of Corporate Social Responsibility on firms’ innovation in China: The role of institutional support. Sustainability 11: 6369. [Google Scholar] [CrossRef] [Green Version]

- Lahouel, Béchir, Younes Zaied, Yaoyao Song, and Guao-Liang Yang. 2020. Corporate social performance and financial performance relationship: A data envelopment analysis approach without explicit input. Finance Research Letters 69: 101656. [Google Scholar] [CrossRef]

- Lee, Jegoo, Samuel Graves, and Sandra Waddock. 2018. Doing good does not preclude doing well: Corporate responsibility and financial performance. Social Responsibility Journal 14: 764–81. [Google Scholar] [CrossRef]

- Liao, Yu, Xiadong Qiu, Anni Wu, Qian Sun, Haomin Shen, and Peyiang Li. 2022. Assessing the Impact of Green Innovation on Corporate Sustainable Development. Frontiers in Energy Research 9: 800848. [Google Scholar] [CrossRef]

- Lin, Lin, Pi-Hsia Hung, De-Way Chou, and Christine Lai. 2019. Financial performance and corporate social responsibility: Empirical evidence from Taiwan. Asia Pacific Management Review 24: 61–71. [Google Scholar] [CrossRef]

- Lu, Jintao, Licheng Ren, Chong Zhang, Chunyan Wang, Zahra Shahid, and Justas Streimikis. 2020. The Influence of a Firm’s CSR Initiatives on Brand Loyalty and Brand Image. Journal of Competitiveness 12: 106–124. [Google Scholar] [CrossRef]

- Luo, Xueming, and Shuili Du. 2015. Exploring the relationship between corporate social responsibility and firm innovation. Marketing Letters 26: 703–14. [Google Scholar] [CrossRef]

- Macgregor, Steven, and Joan Fontrodona. 2008. Exploring the fit between CSR and innovation. Business 3: 23. [Google Scholar] [CrossRef] [Green Version]

- Maqbool, Shafat, and Nasir Zameer. 2018. Corporate social responsibility and financial performance: An empirical analysis of Indian banks. Future Business Journal 4: 84–93. [Google Scholar] [CrossRef]

- Martinez-Conesa, Isabel, Pedro Soto-Acosta, and Mercedes Palacios-Manzano. 2017. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. Journal of Cleaner Production 142: 2374–83. [Google Scholar] [CrossRef]

- Mc Williams, Abagail, and Donald Siegel. 2018. Corporate social responsibility: A theory of the firm perspective. Business Ethics and Strategy 26: 137–47. [Google Scholar] [CrossRef]

- Mishra, Dev. 2017. Post-innovation CSR Performance and Firm Value. Journal of Business Ethics 140: 285–306. [Google Scholar] [CrossRef]

- Nidumolu, Ram, C. K. Prahalad, and M. R. Rangaswami. 2009. Why sustainability is now the key driver of innovation. Harvard Business Review 87: 9. [Google Scholar]

- Orlitzky, Marc, Frank Schmidt, and Sara Rynes. 2003. Corporate Social and Financial Performance: A meta-analysis. Organization Studies 24: 403–41. [Google Scholar] [CrossRef]

- Quazi, Ali, and Dennis O’Brien. 2000. An Empirical Corporate Test of a Model of Social Responsibility. Journal of Business Ethics 25: 33–51. [Google Scholar] [CrossRef]

- Refinitiv. 2021. Refinitiv ESG Company Scores. Refinitiv. Available online: https://www.refinitiv.com/en/sustainable-finance/esg-scores (accessed on 8 November 2021).

- Russo, Michael, and Paul Fouts. 1997. A resource-based perspective on corporate environmental performance and profitability. Academy of Management Journal 40: 534–59. [Google Scholar] [CrossRef]

- Sameer, Ibrahim. 2021. Impact of corporate social responsibility on organization’s financial performance: Evidence from Maldives public limited companies. Future Business Journal 7: 29. [Google Scholar] [CrossRef]

- Stilgoe, Jack, Richard Owen, and Phil Macnaghten. 2013. Developing a framework for responsible innovation. Research Policy 42: 1568–80. [Google Scholar] [CrossRef] [Green Version]

- Uyar, Ali, Abdullah Karaman, and Merve Kılıç. 2020. Is corporate social responsibility reporting a tool of signaling or greenwashing? Evidence from the worldwide logistics sector. Journal of Cleaner Production 253: 119997. [Google Scholar] [CrossRef]

- van Marrewijk, Marcel. 2013. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. Journal of Business Ethics 2: 95–105. [Google Scholar] [CrossRef]

- Visser, Wayne. 2009. Corporate Social Responsibility in Developing Countries. Oxford: The Oxford Handbook of Corporate Social Responsibility, pp. 1–28. [Google Scholar] [CrossRef] [Green Version]

- Von Schomberg, René. 2014. Prospects for Technology Assessment in a Framework of Responsible Research and Innovation. SSRN Electronic Journal, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Wang, Qian, Junsheng Dou, and Shenghua Jia. 2016. A Meta-Analytic Review of Corporate Social Responsibility and Corporate Financial Performance: The Moderating Effect of Contextual Factors. Business and Society 55: 8. [Google Scholar] [CrossRef]

- Wu, Liu, Zhen Shao, Changhui Yang, Tao Ding, and Wan Zhang. 2020. The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry. Sustainability 12: 6799. [Google Scholar] [CrossRef]

Figure 1.

The impact of CSR on corporative and innovative performance.

Figure 2.

Database structural traits in 2019.

{kind=link}

{kind=link}

Table 1.

Most cited articles within the research topic.

| Title | Authors | Journal | Objective | Methodology | Results | Citations |

|---|---|---|---|---|---|---|

| Social issues in supply chains: Capabilities link responsibility, risk (opportunity), and performance | Robert D. Klassen, Ann Vereecke | International Journal of Production Economics | Understand which social management capabilities contribute to competitiveness and how they can be linked to social responsibility, risk, opportunity, and performance in the supply chain. | Construction of a framework by joining information from various case studies along with interview responses. | Four links explain the existing relationship: exposure, audit, mitigation, and development. | 311 |

| Corporate social responsibility and its effect on innovation and firm performance: Empirical research in SMEs | Isabel Martinez-Conesa, Pedro Soto-Acosta, Mercedes Palacios-Manzano | Journal of Cleaner Production | Understand the relationship between CSR and organizational innovation and corporate performance in Spanish SMEs. | Construction of an equation model to evaluate data collected from a sample of 552 Spanish companies. | They proved the positive effect of CSR activities on companies’ innovation. | 137 |

| Exploring the Relationship Between Business Model Innovation, Corporate Sustainability and Organizational Values within the Fashion Industry | Esben Rahbek Gjerdrum Pedersen, Wencke Gwozdz, Kerli Kant Hvass | Journal of Business Ethics | Analyze the relationship between business model innovation, corporate sustainability, and underlying organizational values. | Interviews conducted with 492 managers in the Swedish fashion industry. | Fashion companies that exhibit high levels of business model innovation are more likely to be proactive on the sustainability agenda. | 95 |

| Who Needs CSR? The Impact of Corporate Social Responsibility on National Competitiveness | Ioanna Boulouta, Christos N. Pitelis | Journal of Business Ethics | Explore if and how CSR can impact the competitiveness of nations. | Analysis of data collected from a sample of 19 developed countries over a 6-year period. | CSR can make a significant positive contribution to national competitiveness, as measured by national standards of living. | 94 |

| The influence of corporate social responsibility practices on organizational performance: evidence from Eco-Responsible Spanish firms | Carmelo Reverte, Eduardo Gomez-Melero, Juan Gabriel Cegarra-Navarro | Journal of Cleaner Production | Analyze the impact of CSR practices on organizational performance, covering financial, and non-financial indicators, and study the potential mediating role of innovation in the CSR–performance relationship. | Construction of an equation model to evaluate data from a sample of 133 Spanish eco-responsible companies. | Positive and significant direct effects of CSR on innovation and organizational performance in all groups of companies. | 93 |

Table 2.

Sample characteristics in 2019.

| N° of Companies | % | |

|---|---|---|

| N° Employees | ||

| Less than 1000 | 10 | 1.3 |

| Between 1000 and 100,000 | 106 | 14.2 |

| Between 100.000 and 500,000 | 282 | 37.9 |

| More than 500.000 | 297 | 39.9 |

| Age | ||

| Less than 50 years | 312 | 41.9 |

| Between 50 and 100 years | 182 | 24.5 |

| Between 100 and150 years | 135 | 18.1 |

| More than 150 years | 59 | 7.9 |

| Sector | ||

| Financial | 170 | 22.8 |

| Electronic | 95 | 12.8 |

| Utility Services | 62 | 8.4 |

| Drugs, Cosmetics, and Health Care | 52 | 6.9 |

| Remaining | 365 | 49.1 |

| Annual Turnover | ||

| Less than 5 million | 162 | 21.8 |

| Between 5 and 10 million | 125 | 16.8 |

| Between 10 and 20 million | 134 | 18 |

| More than 20 million | 320 | 43.2 |

Table 3.

Description of CSR proxies.

| Variables | Abbrev | Description | Evaluation |

|---|---|---|---|

| ESG Score (1) | ESG | Overall score given to the company based on information reported by management on the environmental, social, and corporate governance pillars. | Percentage |

| CSR Strategy Score (2) | CSRStr | Reflects the company’s practices in communicating that it integrates the economic, social, and environmental dimensions in its decision-making processes. | Percentage |

| CSR Sustainability Committee (3) | CSRCom | Whether the company has a CSR committee or team. | 0 = No; 1 = Yes |

| CSR Sustainability Reporting (4) | CSRRep | Whether the company publishes a separate report or a section in its annual CSR/sustainability report. | 0 = No; 1 = Yes |

Table 4.

Evolution of CSR variables from 2015 to 2019 (in p.p.).

| North America | South America | Asia | Africa | Europe | Oceania | |

|---|---|---|---|---|---|---|

| ESG | 0.066 | −0.017 | 0.100 | 0.029 | 0.054 | 0.019 |

| CSRStr | 0.129 | 0.019 | 0.118 | 0.037 | 0.093 | 0.031 |

| CSRRep | 0.17 | 0.00 | 0.18 | 0.00 | 0.06 | 0.00 |

| CSRCom | 0.10 | 0.33 | 0.10 | 0.00 | 0.05 | 0.15 |

Table 5.

Description of corporate and innovative performance variables.

| Variables | Abbreviation | Description | Measurement |

|---|---|---|---|

| Research and Development (5) | R&D | Represents all direct and indirect costs related to the creation and development of new processes, techniques, applications, and products with commercial possibilities. | Absolute value |

| Eco-design Products (6) | EDPro | Whether the company reports specific products that aim to reuse, recycle, or reduce environmental impacts. | 0 = No; 1 = Yes |

| Brands and Patents (7) | B&P | Represents the net value of brands, patents, and registered trademarks. | Absolute value |

| ROA (8) | ROA | Financial indicator of how profitable a company’s assets are. | Percentage |

| ROE (9) | ROE | Financial indicator of a company’s ability to add value using its own resources. | Percentage |

| Tobin’s Q (10) | TsQ | Indicator with the objective of estimating whether a particular business or market is overvalued or undervalued. | Decimal |

| Sales Per Employee (11) | SPEmp | Ratio of a company’s annual sales and the total number of employees. | Ratio |

| Annual Turnover (12) | AT | Gross sales and other operating income less discounts, returns, and rebates. | Absolute value |

| Employees (13) | Emp | Represents the total number of employees in the company (company dimension). | Absolute value |

| Age (14) | Age | Number of years in operation. | Absolute value |

| Industry Tech Intensity (15) | ITI | Characterization of the technological intensity of the industrial sector. | 1 to 43 |

Table 6.

Evolution of financial and innovative performance variables.

| Variables | North America | South America | Asia | Africa | Europe | Oceania |

|---|---|---|---|---|---|---|

| R&D (in millions) | 0.56 | 0.03 | 0.27 | −0.01 | 0.22 | 0.01 |

| EDPro (in p.p.) | 5.3 | 0.0 | 4.4 | 0.0 | 6.7 | 7.7 |

| B&P (in millions) | 0.36 | −0.24 | 0.02 | 0.23 | 0.90 | −0.28 |

| ROA (in p.p.) | 0.02 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 |

| ROE (in p.p.) | 1.11 | 0.12 | −0.01 | 0.34 | −0.08 | 0.05 |

| T’sQ (ratio) | 0.37 | 0.44 | 0.02 | 0.14 | 0.00 | 0.29 |

| SPEmp (in thousands) | 0.16 | 0.05 | 0.06 | 0.05 | 1.45 | −0.05 |

| AT (in millions) | 5.94 | 3.52 | 22.68 | 0.35 | 4.06 | −1.21 |

| Emp (absolute value) | 4236 | −11,922 | 17,825 | −12,092 | 5104 | −2395 |

Table 7.

Descriptive statistics and correlations.

| Variables | N | Min | Max | Mean | S D | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ESG (1) | 743 | 0 | 0.94 | 0.64 | 0.20 | 1 | |||||||||||||

| CSRStr (2) | 743 | 0 | 1.00 | 0.63 | 0.32 | 0.73 *** | 1 | ||||||||||||

| CSRCom (3) | 728 | 0 | 1.00 | 0.78 | 0.41 | 0.61 *** | 0.64 *** | 1 | |||||||||||

| CSRRep (4) | 728 | 0 | 1.00 | 0.88 | 0.33 | 0.62 *** | 0.73 *** | 0.58 *** | 1 | ||||||||||

| R&D (5) | 354 | 0.01 | 29.46 | 1.41 | 2.82 | 0.15 ** | 0.02 | 0.09 | −0.02 | 1 | |||||||||

| EDPro (6) | 710 | 0 | 1.00 | 0.21 | 0.40 | 0.26 *** | 0.16 *** | 0.17 *** | 0.17 *** | 0.13 ** | 1 | ||||||||

| B&P (7) | 269 | −0.01 | 63.58 | 2.35 | 6.27 | 0.14 ** | 0.10 | 0.12 ** | 0.06 | 0.14 * | 0.11 * | 1 | |||||||

| ROA (8) | 743 | −0.18 | 0.44 | 0.08 | 0.07 | 0.00 | −0.04 | 0.01 | −0.02 | 0.14 *** | 0.14 *** | −0.06 | 1 | ||||||

| ROE (9) | 738 | −0.48 | 1.81 | 0.18 | 0.21 | 0.01 | 0.06 | 0.05 | 0.06 | 0.11 ** | 0.04 | −0.01 | 0.46 *** | 1 | |||||

| TsQ (10) | 743 | 0.45 | 20.83 | 2.42 | 2.13 | −0.12 *** | −0.15 *** | −0.13 *** | −0.13 | 0.05 | 0.04 | −0.08 | 0.69 *** | 0.35 *** | 1 | ||||

| SPEmp (11) | 695 | 0.02 | 243.41 | 1.05 | 9.43 | 0.02 | 0.00 | 0.00 | −0.00 | 0.06 | −0.02 | 0.03 | −0.03 | 0.00 | −0.03 | 1 | |||

| AT (12) | 741 | 0.01 | 2297.15 | 53.73 | 146.80 | 0.06 * | 0.04 | 0.07 * | 0.03 | 0.24 *** | 0.03 | 0.14 ** | −0.05 | −0.04 | −0.09 ** | −0.01 | 1 | ||

| Emp (13) | 694 | 2 | 2,200,000 | 78,763 | 127,864 | 0.14 *** | 0.12 *** | 0.13 *** | 0.09 ** | 0.37 *** | 0.03 | 0.08 | −0.06 | 0.01 | −0.12 *** | −0.02 | 0.22 | 1 | |

| Age (14) | 687 | 8 | 353 | 72 | 50 | 0.25 *** | 0.21 *** | 0.18 *** | 0.12 *** | 0.00 | 0.16 *** | 0.12 * | −0.08 ** | 0.03 | −0.16 *** | 0.02 | −0.02 | 0.06 | 1 |

| ITI (15) | 654 | 1 | 4 | 2.12 | 0.95 | 0.07 * | 0.04 | 0.07 * | 0.10 ** | 0.06 | 0.18 *** | −0.13 * | 0.21 *** | 0.08 ** | 0.12 *** | −0.07 * | 0.03 | −0.08 * | −0.04 |

* significant at 0.1 (2 tailed); ** significant at 0.05 (2 tailed); *** significant at 0.05 (2 tailed).

Table 8.

Econometric estimations.

| Model | Predictors | ROA | ROE | Ts’Q | SPEmp | AT |

|---|---|---|---|---|---|---|

| 1 | ESG | 0.106 | −0.013 | 0.154 | 0.228 | 0.599 |

| (0.086) | (0.177) | (0.226) | (0.247) | (0.445) | ||

| CSRStr | −0.164 *** | −0.043 | −0.361 ** | 0.123 | 0.063 | |

| (0.056) | (0.113) | (0.147) | (0.160) | (0.288) | ||

| CSRCom | 0.009 | 0.094 | −0.039 | −0.158 | 0.041 | |

| (0.035) | (0.070) | (0.091) | (0.099) | (0.180) | ||

| CSRRep | 0.062 | 0.079 | 0.062 | −0.003 | −0.183 | |

| (0.053) | (0.111) | (0.139) | (0.151) | (0.273) | ||

| 2 | ESG | 0.031 | −0.296 | 0.001 | 0.135 | 0.084 |

| (0.089) | (0.180) | (0.236) | (0.261) | (0.441) | ||

| CSRStr | −0.155 *** | −0.021 | −0.337 ** | 0.119 | 0.040 | |

| (0.055) | (0.108) | (0.144) | (0.160) | (0.269) | ||

| CSRCom | 0.001 | 0.073 | −0.056 | −0.169 * | −0.012 | |

| (0.034) | (0.067) | (0.090) | (0.099) | (0.168) | ||

| CSRRep | 0.064 | 0.086 | 0.064 | 0.021 | −0.084 | |

| (0.052) | (0.024) | (0.136) | (0.151) | (0.255) | ||

| R&D | 0.006 | 0.024 *** | 0.017 | 0.025 ** | 0.082 *** | |

| (0.004) | (0.009) | (0.011) | (0.013) | (0.021) | ||

| EDPro | 0.050 ** | 0.083 * | 0.100 * | −0.022 | 0.051 | |

| (0.021) | (0.043) | (0.056) | (0.062) | (0.105) | ||

| B&P | −0.001 | −0.004 | −0.005 | 0.001 | 0.009 | |

| (0.001) | (0.002) | (0.003) | (0.003) | (0.006) | ||

| 3 | ESG | 0.006 | −0.321 * | −0.095 | 0.076 | 0.316 |

| (0.088) | (0.181) | (0.216) | (0.260) | (0.394) | ||

| CSRStr | −0.145 *** | −0.010 | −0.287 ** | 0.104 | −0.171 | |

| (0.054) | (0.110 | (0.133) | (0.161) | (0.243) | ||

| CSRCom | 0.011 | 0.088 | −0.016 | −0.144 | −0.017 | |

| (0.033) | (0.068) | (0.083) | (0.099) | (0.150) | ||

| CSRRep | 0.058 | 0.074 | 0.030 | 0.037 | 0.039 | |

| (0.051) | (0.107) | (0.125) | (0.150) | (0.228) | ||

| R&D | 0.010 ** | 0.029 *** | 0.031 *** | 0.036 *** | 0.073 *** | |

| (0.004) | (0.009) | (0.011) | (0.013) | (0.020) | ||

| EDPro | 0.058 *** | 0.093 ** | 0.138 ** | −0.013 | 0.018 | |

| (0.021) | (0.044) | (0.053) | (0.063) | (0.096) | ||

| B&P | −0.002 | −0.004 | −0.005 | −0.001 | 0.004 | |

| (0.001) | (0.002) | (0.003) | (0.004) | (0.005) | ||

| Emp | −0.000 *** | −0.000 | −0.000 *** | −0.000 * | 0.000 *** | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | ||

| Age | −0.000 | 0.000 | −0.001 | 0.000 | 0.000 | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | ||

| ITI | −0.016 | −0.020 | −0.050 | −0.068 * | −0.094 | |

| (0.013) | (0.027) | (0.032) | (0.039) | (0.059) |

Standard error in parentheses; *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 9.

Model summary.

| Model | Test | ROA | ROE | T’sQ | SPEmp | AT |

|---|---|---|---|---|---|---|

| 1 | R2 | 0.071 | 0.027 | 0.084 | 0.031 | 0.029 |

| R2 change | 0.071 | 0.027 | 0.084 | 0.031 | 0.029 | |

| Sig F change | 0.064 | 0.533 | 0.031 | 0.438 | 0.476 | |

| 2 | R2 | 0.142 | 0.140 | 0.142 | 0.067 | 0.180 |

| R2 change | 0.071 | 0.113 | 0.058 | 0.011 | 0.151 | |

| Sig F change | 0.025 | 0.003 | 0.055 | 0.220 | 0.000 | |

| 3 | R2 | 0.210 | 0.169 | 0.308 | 0.113 | 0.373 |

| R2 change | 0.068 | 0.029 | 0.167 | 0.047 | 0.193 | |

| Sig F change | 0.024 | 0.292 | 0.000 | 0.122 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Costa, J.; Fonseca, J.P. The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance. Risks 2022, 10, 103. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050103

AMA Style

Costa J, Fonseca JP. The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance. Risks. 2022; 10(5):103. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050103

Chicago/Turabian StyleCosta, Joana, and José Pedro Fonseca. 2022. "The Impact of Corporate Social Responsibility and Innovative Strategies on Financial Performance" Risks 10, no. 5: 103. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050103

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.