1. Introduction

The importance of this study is explained by the fact that financial risk management is the key to overcoming the COVID-19 global economic crisis and the tool for the accelerated overcoming of future economic depressions, which are inevitable in the market model of the economy and have become more frequent against the background of the increase in the global economy’s cyclicity, under the influence of technological progress and the aggravation of social and environmental problems (

Anwar et al. 2022;

Bianchi et al. 2022;

Guseva et al. 2019;

Ilbahar et al. 2022;

Li et al. 2022;

Reboredo et al. 2022;

Urbano et al. 2022).

The problem is the contradiction of investments amid economic crises and the subsequent uncertainty during investment decision-making. On the one hand, investments allow raising the rate of economic growth, breaking the decline, and ensuring the rise of an economy (

Giuliani 2022;

Shahbaz et al. 2021). On the other hand, financial risks are particularly high amid a crisis, which reduces the return on investments and, instead of the expected rise of the economy, could lead to its decline in case of investors’ losses (

Alashbaieva et al. 2021;

Ambrocio and Jang 2021;

Sharma et al. 2021).

The existing approach to financial risk management amid the economic crisis proposes the financing of leading technologies for the creation of new markets and new high-tech market segments (

Frith 2021). According to this approach, the perspectives of the COVID-19 crisis resolution are connected to the development of the digital economy (

Guggenberger et al. 2021;

Willems et al. 2021) since digital innovations are considered prospective drivers of economic growth.

However, these expectations as to the digital path of the COVID-19 crisis resolution are based on the experience that was gained before the pandemic. In the pre-crisis global economy, digital innovations received a better reaction in high-tech markets and market segments due to higher effective demand. The crisis changed the market situation—high demand for digital innovations is not guaranteed or even not achievable due to the decrease in the population’s real disposable incomes (

Falato et al. 2021;

Flammer and Ioannou 2021;

Lean and Pizzutilo 2021).

Implementation of digital innovations, like any other technological transit, is accompanied by high social and environmental costs (

Gavlovskaya and Khakimov 2022). For example, an increase in the automatization level of entrepreneurial processes reduces the capacity of social resources and increases the capacity of energy resources in production and distribution. That is why investments in digital innovations might not be justified, which proves the fact that in 2020 (in the most critical phase of the COVID-19 crisis), the leaders of digital competitiveness, according to

IMD (

2021), demonstrated a very large decline in GDP—larger as compared to other countries with a similar level of socio-economic development.

According to the

International Monetary Fund (

2021), the US economic contraction was −3.405% in 2020 (which is much higher than in other countries of the G7), and the decline of the economy of Hong Kong SAR (China) was assessed at −6.081% (which is much higher than in countries of BRICS). In addition to this, the use of digitalization as the basis led to the reduction in the considered countries’ economies’ sustainability. According to the

UN (

2020,

2021), the Sustainable Development Index decreased in the USA—from 76.43 points in 2020 to 76.01 points in 2021, and China (the index is not calculated separately for Hong Kong)—from 73.89 points in 2020 to 72.06 points in 2021.

Thus, it is important to develop an alternative approach to financial risk management amid a crisis, which would be more effective. The question studied here is the following: how to optimize the investment flows amid a crisis to reduce financial risks and achieve economic growth (crisis resolution), and, at the same time, gain advantages for sustainable development? When seeking an answer to this question, it is necessary to take into account the experience of the leaders in the sphere of sustainable development. Their recession amid the COVID-19 crisis was smaller (as compared to the USA and Hong Kong): Sweden’s GDP reduced by 2.795% in 2020, and Denmark’s GDP by −2.061% (

International Monetary Fund 2021). Both countries demonstrated a growth in the Sustainable Development Index: Sweden—from 84.72 points in 2020 to 85.61 points in 2021, and Denmark, from 84.56 points in 2020 to 84.86 points in 2021 (

UN 2020,

2021).

Using the experience of the leaders in the sphere of sustainable development (

Becchetti et al. 2015;

Bilbao-Terol et al. 2016;

Herrera-Cano and Gonzalez-Perez 2016;

Leins 2020), the authors of this paper test the hypothesis: responsible investments have the highest perspective amid a crisis because they allow more effective management of the related financial risks. Responsible investments are treated as investments in socially important objects of infrastructure and projects in the sphere of energetics, transport, water supply, sanitation, and healthcare.

This paper is aimed at developing a new (alternative) approach to financial risk management, which is more effective during a crisis—the proprietary approach predetermines the originality of this paper. This research is conducted by the example of 17 developing countries with lower-middle and upper-middle income from different regions of the world under the conditions of the COVID-19 global crisis (2020–2021). The objective is achieved with the help of a set of the following tasks:

- −

Identifying the level of the financial risk of companies, measuring and discovering the differences in its connection with the commercial and responsible investments;

- −

Modeling the dependence of effectiveness of investments on commercial and responsible investments;

- −

Performing a scenario analysis of the alternatives of financial risk management of companies in 2021 through the increase in the effectiveness of investments based on the optimization of investment flows.

2. Literature Review

This paper uses the framework of the modern Theory of Investment, which, in its turn, is based on Neo-Keynesianism. The fundamental provisions of this theory were formulated by J.M.

Keynes (

1998). The key idea of the Theory of Investment is as follows: to increase the rate of economic growth and, in particular, to overcome a crisis, there is a need for investments, which nature could be different (including financing of the development of business, an increase in consumption through the reduction in savings, government financial support for economic subjects, and foreign direct investment) but which are equal (

Cristiano et al. 2018;

Harvey 2021;

Nisticò 2020).

The central scientific category of this paper is financial risk. The existing literature sources (

Bendall and Stent 2006;

Chiang 2021;

Juszczuk et al. 2022;

Werge 2021;

Ling et al. 2022;

Sohibien et al. 2022) note that one of the most popular and correct indicators of financial results (and through them—financial risks) is such proxy variable as return on assets (ROA). Thus, the measure of financial risk in this paper is the change of return on assets. Financial risk is treated as a negative change (reduction) of return on assets (in the considered period compared to the previous period).

The essence of investment according to the existing approach to financial risk management amid the economic crisis is shown in

Table 1.

As shown in

Table 1, according to the existing approach to financial risk management, the parameters of investments that have to ensure the crisis resolution are as follows:

- −

preference is given to venture investments in technological innovations since they have the highest potential to increase the rate of economic growth (

Conti et al. 2019;

Frimpong et al. 2021);

- −

it is expedient to place commercial (not supported by corporate social responsibility) investments since corporate social responsibility reduces the effectiveness of investments (reduces companies’ profitability because they are connected to additional expenditures) (

Di Persio et al. 2021;

Szemere et al. 2021);

- −

Financial risks are high a priori amid a crisis and cannot be reduced. That is why the period of investing is short, because, first, there is a need for a quick effect for the economy in the form of increasing its growth rate and restoration after the crisis. Second, long-term investments are not profitable for investors due to the uncertainty of the perspectives of receiving a return on capital employed. Long-term investments (peculiar for infrastructural projects)—are a “market gap”, which is overcome through government financing of infrastructural projects (

Cristiana 2021;

Swishchuk 2021);

- −

Investment projects are of a small scale since investors do not possess large financial resources and/or reduce financial risks through the diversification of the investment portfolio (implementation of several small-scale investment projects instead of one large project) (

Batóg and Batóg 2021;

Bouri et al. 2021);

- −

Under the crisis conditions, the role of investments in stimulating sustainable development is focused on support for the implementation of SDG 8 (in the narrow treatment, limited by economic growth) and SDG 9 (in the narrow treatment, limited by industrialization and innovations) (

Chen 2021;

Kang 2020;

Kurniatama et al. 2021).

This paper also uses the provisions of the Theory of Sustainable Development, according to which the investment support for the SDGs is critically important and necessary in a crisis economic environment. Due to this, the consequences of investments amid a crisis must be considered not only from a perspective of economic growth but also from a perspective of sustainable development. The consequences of investments, according to the existing approach to financial risk management amid an economic crisis and taking into account the theory of investments and the theory of sustainable development, are shown in

Figure 1.

As shown in

Figure 1, according to the existing approach to financial risk management amid the economic crisis, the implemented short-term, small-scale investments in technological innovations allow for negative consequences for sustainable development (regress on the SDGs). Their consequences for economic growth are unknown (versatile) and could be connected to the increase in the crisis and restoration of the economy. One of the most probable scenarios according to the existing approach is the combination of negative consequences for sustainable development (regress on the SDGs) and economic growth (an increase in the crisis), which is a sign of the low effectiveness of the existing approach.

Thus, a gap in the literature is the difference between the Theory of Investment and the Theory of Sustainable Development, which consists of the uncertainty of perspectives of the simultaneous overcoming of the economic crisis and support for sustainable development during the management of financial risks of investments. This paper is aimed to bridge the described literature gap.

3. Method and Data

This paper is an applied quantitative study for which the materials of the

World Bank (

2021a,

2021b,

2021c,

2021d,

2021e,

2021f) were used to create a sample of 17 countries whose companies are included in the ranking of

Forbes (

2022) Global 2000 in 2020–2021. The structure of the sample of countries by the level of income and geographical location is shown in

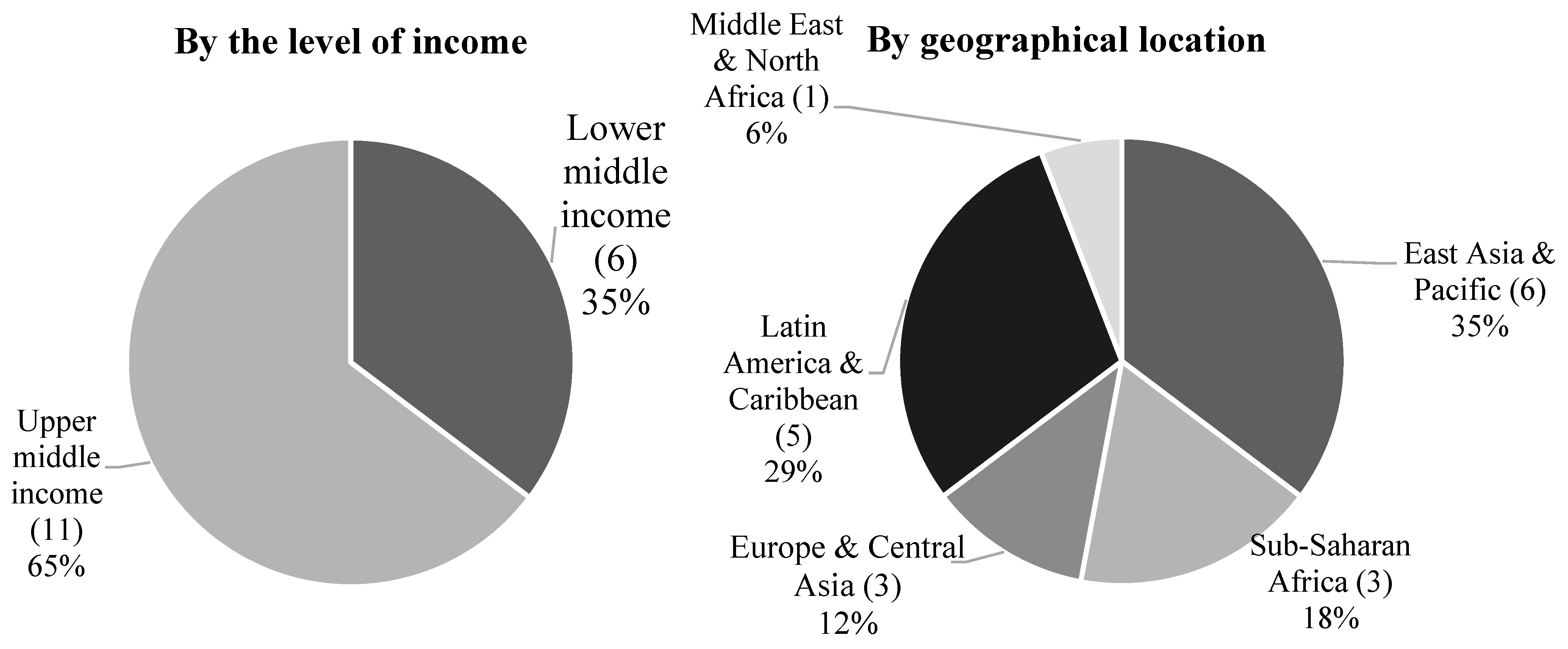

Figure 2.

It should be noted that to avoid the presence of countries for which we do not have data for any of the studied indicators; we reduced the standard list of the World Bank, removing countries with a large deficit of data. Given the topic of this research, these were primarily developed countries—countries with high income—and countries with lower income, which face a deficit in statistics. As a result, we used a sample of mostly developing countries: with upper-middle income (65%) and lower-middle income (35%), a total of 17 countries.

By the geographical location, countries from East Asia and the Pacific (35) dominated the created sample. The share of countries of Latin America and the Caribbean was 29%, countries of Europe and Central Asia—12%, Sub-Saharan Africa—18%. The share of countries in the Middle East and North America—6%. The research strategy is presented in

Table 2.

According to the strategy of this research (

Table 2), within the first task, correlation analysis was used to discover the level of the financial risk of companies and to measure and discover the differences in its connection with commercial and responsible investments. To find the change of financial risk, the method of horizontal analysis was used to calculate the change of return on assets in 2021 as compared to 2020 (∆ROA = ROA

2021/ROA

2020). The change in the volume and ratio of responsible and commercial investments in 2019–2020 was also calculated.

To find the impact of investments (responsible and commercial) on the financial risk of companies, the method of correlation analysis was used to reveal the connection between the percentage change of return on assets in 2021 as compared to 2020 (∆ROA) and the volume of investments in 2020. Positive values of the correlation coefficients show the contribution of investments to the reduction in companies’ financial risk.

Within the second research task, to model the dependence of the effectiveness of investments on commercial and responsible investments, using the methods of regression and comparative analysis, we calculated the impact of investments (responsible and irresponsible) on the results of a company’s financial activity. The research model of this paper is given as follows:

where ROA is the return on assets of the company—national leader in the ranking Global 2000 in 2021 (resulting variable); const constant; b is coefficient of regression at the factor variable; Ienerg is Investment in energy with private participation in 2020 (factor variable); Iwater is Investment in water and sanitation with private participation in 2020 (factor variable); Itransp is Investment in transport with private participation in 2020 (factor variable); Ihealth is Domestic private health expenditure in 2020 (factor variable); Iforeign is Foreign direct investment, net inflows in 2020 (factor variable).

It should be noted that return on investments comes not in the period of their placement but in the next period. So to obtain correct results of the analysis, the dependent (resulting) variable must exist at the moment (t), and all independent (factor) variables must exist at the moment (t − 1)—to reduce the probability of reverse causality (i.e., return from investments might influence their volume). Therefore ROA in the model (1) was based on the data for 2021 and all investments—on the data for the preceding year of 2020.

In the research model (1), the indicator of financial results is the return on assets (ROA). This indicator was calculated at the level of companies, but companies do not disclose the structure of their responsible investments, which is provided at the level of countries. To ensure the compatibility of data, the values for identifying ROA are taken from the materials of the company—national leader in the ranking Global 2000 in 2021 (

Forbes 2022).

A different number of companies from each country has been included in the ranking of

Forbes (

2022). To unify the data on countries, the statistics on only one company from one country were taken—the one that has the best position in the ranking. Return on assets (ROA) is calculated by finding the profits/assets ratio (the higher the value, the larger the return on assets—the better).

- −

Investment in energy with private participation (Ienerg);

- −

Investment in water and sanitation with private participation (Iwater);

- −

Investment in transport with private participation (Itransp);

- −

Domestic private health expenditure (Ihealth) per capita, PPP (current international

$) (

World Bank 2021a).

In the statistics, the indicators of foreign direct investment, net inflows (

World Bank 2021b), investment in energy with private participation (

World Bank 2021c), investment in water and sanitation with private participation (

World Bank 2021e), and investment in transport with private participation (

World Bank 2021d) are measured in current US

$, but we turn them into current US

$ per capita for the research purposes. For this, we calculated the indicators’ initial values/population ratio (Population, total, according to the materials of the

World Bank 2021g).

The choice of the indicators for reflecting responsible investments is explained by the fact that they are based on the mechanism of public-private partnership and thus deliberately envisage a high level of corporate social responsibility. All these indicators also reflect the investments in socially important infrastructure, which are traditionally regarded as unattractive for private businesses due to limited opportunities for receipt of profit. More detailed information on the indicators is given in

Table S4. The statistics of the World Bank are given in

Table S1, and the statistics of

Forbes (

2022) are in

Table S2.

To ensure the reliability of the research results, it is necessary to study the potential shift of endogeneity during the assessment (1). If the variables are endogenous, the assessments will be biased and invalid. The assessment of endogeneity of the factor variables is shown in

Table 3.

The results of the assessment from

Table 3 demonstrate the absence of endogeneity of the factor variables, which allows using them in full in the course of further research.

The proposed hypothesis was deemed proved as the coefficients of regression (b) at the indicators of responsible investments were higher than at the indicator of commercial investments (benerg > bforeign and/or btransp > bforeign and/or bwater > bforeign and/or bhealth > bforeign).

Within the third task of the research, we used the least-squares method to identify and compared various Pareto optimums of the change of effectiveness of investments (ROA) with different options of an investment portfolio for scenario analysis of the alternatives of financial risk management of companies in 2021 through an increase in the effectiveness of investments based on the optimization of investments flows.

4. Results

Determining the level of the financial risk of companies, measuring and revealing the differences in its connection with the commercial and responsible investments

Within the first task of the research, to determine the level of the financial risk of companies, we found the ratio of ROA in 2021 to ROA in 2020. Based on the data from

Table S1, we calculated the effectiveness of investments (return on assets) by finding the ratio of net profit to the market capitalization of companies: in 2020 and 2021. The results of the assessment of the financial risk in 2021 are presented in

Table 4.

The results of the assessment from

Table 4 show that the effectiveness of investments was reduced in companies of almost all countries (except for Kenya, where it grew by 9.41%). On average, the return on assets in 2020 was assessed at 0.66, and in 2021—0.58. Financial risk (change of ROA in 2021 as compared to 2020) in 2021 (on average) was assessed at −47.85%. Variation of return on assets and financial risk is rather high, which additionally confirms the representativeness of the sample.

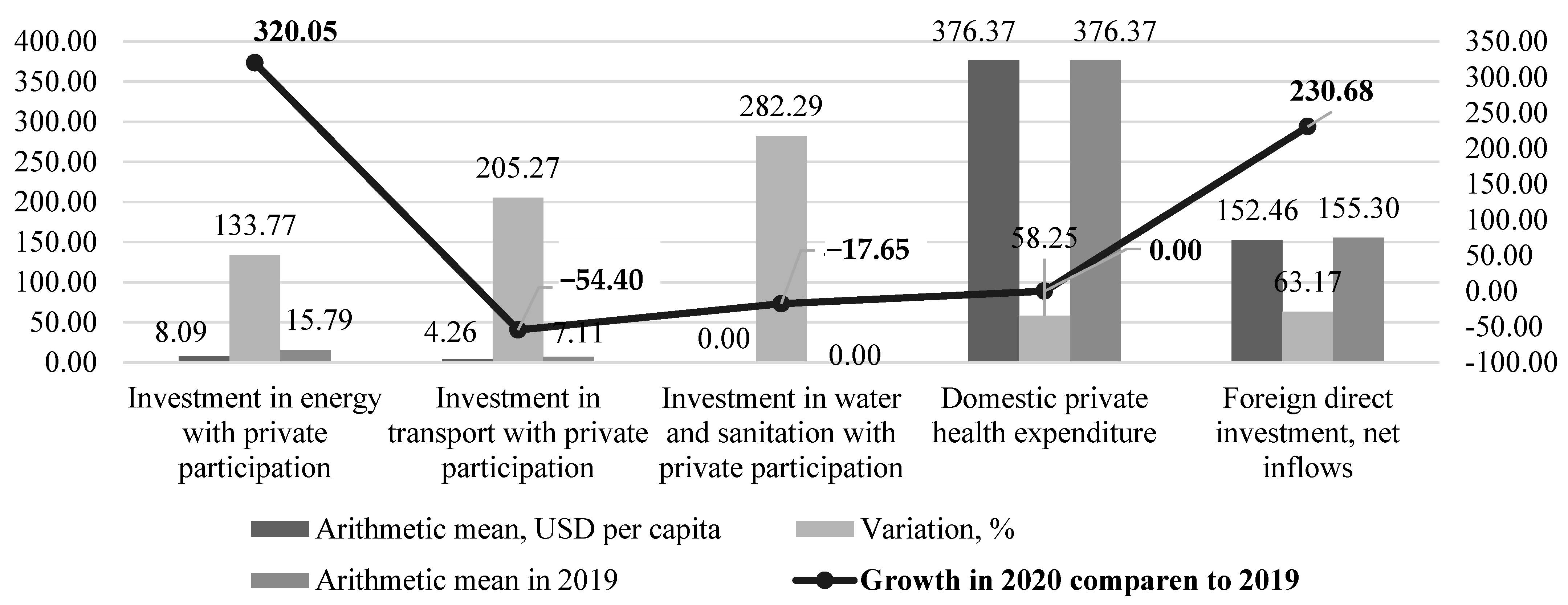

To form a systemic view of the investment flows in 2020, the data from

Table S1 were used to calculate arithmetic means and variation of responsible and commercial investments (

Figure 3).

As shown in

Figure 3, in the structure of investment flows in 2020 (and among responsible investments), investments in healthcare dominate (USD 376.37 per capita)—their variation was moderate (58.25%). The second position belonged to direct foreign investments (USD 152.46 per capita)—their variation was also moderate (63.47%). Other types of responsible investments were presented poorly. Investments in energy (USD 8.09 per capita), investments in transport (USD 4.26 per capita), and investments in water and sanitation (USD 0.001 per capita). Their variation was high: 133.77%, 205.27%, and 282.29%, accordingly.

On the whole, the share of responsible investments in the structure of investment flows in 2020 equaled 71.83%, and the share of commercial investments was 28.17%. The decrease in responsible investments took place: investments in energy—by 48.74%, investments in transport—by 39.98%, and investments in water and sanitation—by 66.67%. At the same time, commercial investments grew by 1.83%.

To measure and discover the differences in its connection with commercial and responsible investments, we found the impact of investments (responsible and commercial) on the financial risk of companies, using the method of correlation analysis, and reveal the connection between the percentage change of return on assets in 2021 as compared to 2020 (∆ROA) and the volume of investments in 2020 (

Figure 4).

Positive values of the coefficients of correlation in

Figure 4 demonstrate a contribution of investments to the reduction in companies’ financial risk. A positive correlation with return on assets of companies was observed only with responsible investments in water and sanitation (23.34%), healthcare (2.23%), and transport (16.95%).

Thus, there is a high level of financial risk for companies, which was proved by the fact that the return on assets of almost all companies in the sample significantly (by 47.85% on average) reduced in 2021 as compared to 2020. We also revealed the differences in its connection with commercial and responsible investments. Commercial investments did not demonstrate a positive connection with the return on assets of companies in 2021, while the sought positive connection was revealed with responsible investments in transport and energy. This was a sign of a large potential of responsible investments to reduce companies’ financial risks.

Modeling the Dependence of the Effectiveness of Investments on Commercial and Responsible Investments

Within the second task of the research, we performed modeling of the dependence of effectiveness of investments on commercial and responsible investments. For the most precise determination of the role of CSR in financial risk management, we used the results of the regression analysis of the dependence of return on assets in 2021 on different types of investments in 2020 (

Table 5).

Based on the results of the regression analysis and the research model (1), the following equation of multiple linear regression (2) was obtained:

The results of the regression analysis in

Table 5 show that the growth of commercial investments (shown by the example of foreign direct investments) did not increase but decreased return on assets (this is proved by the negative value of the regression coefficient: b

foreign = −0.003). Contrary to it, responsible investments are economically effective. An increase in the volume of investments in transport by USD 1 per capita led to an increase in return on assets by 0.04%.

An increase in the volume of investments in water and sanitation by USD 1 per capita ensures an increase in return on assets by 554.30%. An increase in the volume of investments in healthcare by USD 1 per capita leads to an increase in return on assets by 0.003%. In the course of progress in the provision of the statistics of investments in healthcare for 2021, it is possible to expect that the contribution of investments in healthcare to market capitalization will be larger, given the pandemic nature of the COVID-19 crisis. The results of the analysis of variance demonstrate the reliability of the obtained regression model at the significance level of 0.05 (significance F = 0.030109).

To select the next research method, let us use the Hausman test, which allows comparing the assessments of the least-squares method and the instrumental variables method. The main hypothesis is that the factors of the model are exogenous, and the alternative hypothesis states that they are endogenous. In both cases, the instrumental variables method provides substantial evaluations (tools are initially considered exogenous). The least-squares method provides substantial evaluations only if the factors are exogenous. Thus, if the main hypothesis is proved, the evaluations of different methods are asymptotically equivalent; in the opposite case, the difference between them will be significant. Thus, the test allows assessing the exogeneity of the model’s factors.

The Hausman test, which was conducted for model (2), showed that coefficients at the additional variables were jointly significant (tested by standard tests—F-test, t-Statistics); therefore, the regressors are exogenous (endogenous variables are absent in the model). The result of the F-test was as follows. At the level of significance of 0.05 for 5 variables (k1 = m = 5) and 17 observations (k2 = n – m – 1 = 17 – 5 – 1 = 16), F table equaled 3.20. The observed F value equaled 3.809132. Since the observed value exceeds the table value, the F-test has been passed. This proves the main hypothesis and demonstrates the expedience of using the least-squares method.

Thus, a reliable evidential base of the offered hypothesis has been formed. Though different responsible investments contribute differently to the improvement of companies’ financial indicators, the results obtained clearly show the preference for responsible investments compared to commercial investments for companies’ financial risk management.

Scenario Analysis of the Alternatives of Financial Risk Management of Companies in 2021 through an Increase in the Effectiveness of Investments Based on the Optimization of Investment Flows

Within the third research task, for the scenario analysis of the alternatives of financial risk management of companies in 2021 through an increase in the effectiveness of investments, let us use the model from

Table 5. The optimization of investment flows with the help of the least-squares method has revealed various Pareto optimums of the change of the effectiveness of investments (ROA) at different options of an investment portfolio (

Table 6).

The results from

Table 6 show the presence of two perspective scenarios of financial risk management of companies in 2021 based on the optimization of investment flows in 2020. Both these scenarios would have allowed avoiding the financial risk in 2021. The first scenario is the scenario of reduction in the financial risk. It envisages a moderate (below 10%) increase in responsible investments. The perspective Pareto optimum implies the following:

- −

Increase in investments in transport by 0.73%: from USD 4.26 per capita to USD 4.30 per capita;

- −

Increase in investments in water and sanitation by 2.68%: from USD 0.0012 per capita to USD 0.0012079 per capita;

- −

Increase in investments in healthcare by 5.13%: from USD 376.37 per capita to USD 395.69 per capita.

Due to this, return on assets (ROA) in 2021 would have been at the level of 2020 and would have equaled 0.66, i.e., it would have been 14.37% higher than the factual level of 2021. Accordingly, the change of return on assets would have been zero (financial risk would have been absent).

The second scenario of prevention of the financial risk implies an increase in investments in water and sanitation by 750%: from USD 0.0012 per capita to USD 0.01 per capita. Due to this, return on assets (ROA) in 2021 would have been equaled 1.23, i.e., it would have been 847.55% higher than the factual level of 2021. Accordingly, the change of return on assets would have been positive (+727.31%), which would have allowed a guaranteed absence of financial risk.

5. Discussion

This paper contributes to the development of the Theory of Investments, proving the hypothesis that, in crisis conditions, responsible investments have the best perspectives since they allow more effective management of the connected financial risks. The received results confirm the fundamental thesis of Neo-Keynesianism—investments are necessary for overcoming the economic crisis—but specify the preferable types of investments, of which this paper proposes responsible investments.

The essence of investments in the new (alternative) approach to financial risk management amid the economic crisis, which is based on corporate social responsibility, is shown in

Table 7.

As shown in

Table 7, according to the new (alternative) approach to financial risk management amid the economic crisis, which is based on corporate social responsibility, the parameters of investments that are to ensure the overcoming of the crisis are as follows:

- −

Preference is given to investments based on the mechanism of public-private partnership since the participation of the government ensures the co-financing of investment projects and the distribution of risks between the partners. Public-private partnership also guarantees high demand for products that are received as a result of implementing the investment projects since it envisages the implementation of projects that are in high demand in society. This is the difference between the obtained results and the existing literature (

Conti et al. 2019;

Frimpong et al. 2021);

- −

It is expedient to make social—supported by corporate social responsibility—investments since its raises the effectiveness of investments (increases the profitability of companies). This is the difference between the obtained results and the existing literature (

Di Persio et al. 2021;

Szemere et al. 2021);

- −

During crises, financial risks could be reduced through the optimization of the investment portfolio. That is why long-term investments are allowed and are the most preferable (peculiar for infrastructural projects), for the perspectives of receiving a return on capital employed are most favorable. This is the difference between the obtained results and the existing literature (

Cristiana 2021;

Swishchuk 2021);

- −

Investment projects are of large scale since it is preferable to concentrate investments on the most profitable responsible investments (it is necessary to refuse the diversification of the investment portfolio). This is the difference between the obtained results and the existing literature (

Batóg and Batóg 2021;

Bouri et al. 2021);

- −

Amid a crisis, investments in responsible innovations are most perspective, for they have the largest potential for an increase in market capitalization. The role of investments in stimulating sustainable development has several aspects and includes the support for the implementation of SDG 7 (during investment in energy), SDG 11 (during investment in transport and logistics), SDG 6 (during investment in water and sanitation), SDG 3 (during investment in healthcare), SDG 8 (in the wide treatment, which covers not only economic growth but also decent work), and SDG 9 (in the wide treatment, which covers not only industry and innovations but also infrastructure). This is the difference between the obtained results and the existing literature (

Chen 2021;

Kang 2020;

Kurniatama et al. 2021).

This paper also contributes to the development of the Theory of Sustainable Development because it reconsiders and specifies the consequences of investments according to the new (alternative) approach to financial risk management amid the economic crisis, which is based on corporate social responsibility (

Figure 5).

According to

Figure 5, during the new (alternative) approach to financial risk management amid the economic crisis, which is based on corporate social responsibility, long-term, large-scale investments in social and ecological innovations are made, which require positive consequences for sustainable development (support for the achievement of the SDGs). Along with that, there is a need for support for economic growth (contribution to the quick restoration of the economy). One of the most probable scenarios with the new approach is the combination of positive consequences for sustainable development and economic growth, which is a sign of high effectiveness and preference of the proposed new (alternative) approach.

Thus, this paper has filled the gap in the existing literature and bridged the gap between the Theory of Investment and the Theory of Sustainable Development—outlining the prospects of the simultaneous overcoming of economic crisis and support of sustainable development during the management of financial risks of investments based on corporate social responsibility. This paper has also answered the research question, proposing optimizing the investment flows during a crisis through the focus on responsible investment to reduce financial risks and achieve economic growth (crisis recovery) and, at the same time, gain advantages for sustainable development.

6. Conclusions

To conclude, the results of the research are as follows:

1. By the example of 17 developing countries with lower-middle and upper-middle income from different regions of the world amid the COVID-19 global crisis (2020–2021), we have proved the low effectiveness of the existing approach to managing the financial risks of investments. It has been demonstrated that amid the COVID-19 crisis, investors use the existing approach to financial risk management and reduce responsible investments (investments in energy, transport, and water and sanitation) while increasing commercial investments (shown by the example of foreign direct investments). The reduction in the volume of socially responsible investments is predetermined simply by limitations and termination of operations that were initiated by all government bodies.

We have also revealed an absence of a vivid positive connection between commercial investments and the financial results that are expected from them. At the same time, there is a positive correlation between responsible investments and the change of return on assets in 2021 compared to 2021, i.e., the potential of responsible investments to reduce companies’ financial risks. Therefore, the existing approach to financial risk management is inefficient in practice and fragmentary (“narrow”, imprecise, and contradictory) in theory;

2. As an alternative, we have offered a new approach to financial risk management of investments that is based on CSR. It implies long-term, large-scale investments in social and environmental innovations based on the mechanism of public-private partnership. All considered directions of responsible investments are important:

- −

It is expedient to support investments in renewable energy sources during a crisis: expenditures for energy resources grow, and this is a problem, while the decarbonization of the economy is necessary for preventing future epidemics and pandemics;

- −

Investments in transport are important to support the continued work of the key sectors of the economy even under the conditions of social distancing and economic limitations;

- −

Investments in healthcare are critically important during the pandemic;

- −

Investments in water and sanitation supplement them since they raise the level of hygiene and allow for fighting the current pandemic and preventing future epidemics and pandemics.

3. High effectiveness and preference of the new approach have been substantiated. For example, in 2021, the optimization of investment flows (increase in responsible investments) based on CSR would have allowed overcoming companies’ financial risks. In addition to this, the new approach supports SDG 7, SDG 11, SDG 6, SDG 3, SDG 8, and SDG 9.

The foregoing predetermines the theoretical importance of this paper. Its practical importance consists in substantiation of the fact that commercial (not supported by corporate social responsibility) investments should be replaced with responsible (based on the principles of corporate social responsibility) investments.

The new (alternative) approach to financial risk management amid a crisis is more effective (compared to the existing approach): for business (provides a larger return on investments and allows avoiding losses), government (makes a larger contribution to economic growth, the probability of which achievement is higher), and society (supports the SDGs and contributes to sustainable development to a larger extent).

The limitations of this study are as follows: the new (alternative) approach to financial risk management amid an economic crisis has been presented in a generalized way. It is recommended to use corporate social responsibility, and the two most perspective directions of responsible investments are offered: investment in transport and investment in healthcare. For practical implementation, the new approach requires more detailed recommendations, which should be developed in future scientific studies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}