What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis

1

Faculty of Computer and Mathematical Sciences, Universiti Teknologi MARA, Cawangan Negeri Sembilan, Kampus Seremban, Seremban 70300, Malaysia

2

Department of Mathematical Sciences, Faculty of Science & Technology, Universiti Kebangsaan Malaysia, Bangi 43600, Malaysia

*

Author to whom correspondence should be addressed.

Risks 2022, 10(5), 97; https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050097

Submission received: 16 March 2022

/

Revised: 15 April 2022

/

Accepted: 28 April 2022

/

Published: 5 May 2022

Abstract

:A lapsed policy is an insurance policy that has become inactive due to non-payment of premiums. The word “lapse” is an insurance topic that constantly evolves, proven by the recent increase in publications on this topic. The study explores the life insurance lapse decision through a comprehensive bibliometric analysis throughout the years, concentrating on publication trends; co-authorship networks among countries, authors, and scientific journals; and the field’s evolution. The research is based on the Scopus database. Ultimately, 178 documents were retrieved and analysed, demonstrating increased literature on insurance lapse from 1971 to 2021. The authors’ keyword co-occurrence network was also analysed for possible future directions of the field. Journals originating from the United Kingdom dominate the publication on life insurance lapsation. In contrast, an author from the United States is at the first rank in terms of the co-authorship network’s total link strength. The results may help researchers define the research objective and determine the aspects of the life insurance lapse for future research.

1. Introduction

Insurance is a contract that insurance companies provide individuals or organisations promising financial security or compensation. If the policy terminates or lapses before maturing, all protections will cease. A policy lapse is defined as a policyholder’s failure to pay the periodic premium, which terminates the policy (Russo et al. 2017; Anandalakshmy and Brindha 2017; Poufinas and Michaelide 2018). Conversely, the definition of surrender is the lapse of an insurance policy with a cash value aspect, whereby an active policy cancellation request causes returned cash value (Campbell et al. 2014; Cheng and Li 2018). Policy lapses and surrenders are fascinating, resulting from a deliberate decision to surrender a policy, a forced decision motivated by cash needs, or failure to pay the necessary premiums to ensure the policy is still in force. The topic has gained interest among academicians—precisely, the demand, risks, cancellation policy, or other insurance protection topics—a trend observed in past studies.

The coronavirus (COVID-19) outbreak had extensive economic consequences, triggering financial crises and a worldwide economic downturn. Wang et al. (2021) stated that while the epidemic has had a broad influence on the United Kingdom stock market, household spending habits have altered as people have become more conservative and reluctant to invest. The study found that COVID-19’s consequences resulted in a recession, putting insurers under further pressure from the issue of price sensitivity. Brum and De Rosa (2021) stated that increased poverty is one of the most drastic pandemic consequences experienced by insurance firms in comparison with similar extreme events that impact survival. This intense event induced mass termination wherein most policyholders terminated their life insurance policies (Biagini et al. 2021). Meanwhile Li et al. (2021) mentioned that, in comparison to the global financial crisis, the current pandemic crisis had a more significant impact on consumer spending, total corporate inventory, and unemployment.

The lack of stability will cause many policyholders to take the route of abandoning policies to enable them to have excess money to cover daily expenses. Many countries have recently been shocked by the spread of COVID-19, and this issue has severely affected the country’s economic sectors, including the insurance sector. Despite the current situation showing that demand for coverage should increase due to the pandemic, the converse is that demand for insurance coverage is declining as the unemployment rate rises and household incomes decline (Bernama 2020). According to a study conducted by LIMRA and LifeHappens (Insurance Barometer Study 2021), people need life insurance protection. The market is making it easier to buy coverage than ever before. About 59% of the respondents believed they needed life insurance protection, while 31% were more likely to purchase insurance due to a pandemic. Younger Americans are less likely to be insured, but they are more likely to acquire life insurance in the coming year. Despite the awareness to own life insurance protection, the number of people who own life insurance in the United States has decreased marginally; only 52% of Americans say they have life insurance, compared to 54% in 2020 (Insurance Barometer Study 2021).

The Financial Stability Institute (FSI), in 2020, reported that Malaysia, Belgium, Hong Kong, Japan, and other countries allowed policyholders to defer premium payments or revamp the premium payment schedules to prevent policy expiration or termination (Yong 2020). Observably, policy termination or lapsation is a universal problem for insurers. A lapsed policy affects the insurance company and the policyholder. From an insurance company’s perspective, high lapse rates weaken the ability to recoup costs incurred, such as massive underwriting costs and start-up costs from sales costs and commissions (Milhaud et al. 2011; Subashini and Velmurugan 2015; Xong et al. 2019).

Publications on lapsed policies have increased since the 1990s, with socio-demographics and economics in the study analysis. In the event of a withdrawal (early lapse) from an insurance contract, the behavioural interpretation provides some fascinating insights. The studies on what drives policyholders to lapse their policies, why they lapse, or how to accurately model the lapse rate seem quite popular among researchers. Based on past studies, there are some contradictory views on socio-demographic factors such as age, gender, marital status, number of dependents, and level of education in determining the lapse of a policy. Some researchers found that the age and number of policyholders’ dependents affect the lapsed policy, such as a study by Ćurak et al. (2015) and Gemmo and Götz (2016). On the other hand, some other researchers reported that age and number of dependents did not affect the rate of the lapsed policy, see (Sirak 2015; Yacob et al. 2018), thus recommending not taking into account those factors in future studies. These contradictory views provide interest and opportunity for authors to delve further into the current economic situations.

Even though bibliometric analysis is necessary to provide a systematic overview of the insurance lapse environment, there are limited studies on the subject. Hence, this study incorporated and organised current research by defining fundamental and seminal works of old and new areas before the scholarship to provide future direction using bibliometric analytical techniques to deconstruct the main anchors and evolution. Conclusively, the research objectives identify the research growth and trends to determine the main research theme and the evolved research interests.

2. Life Insurance Lapsation

Over the years, life insurance lapse research has increasingly been explored, especially in the 1990s, with factors such as socio-demographic and economic being considered in the analysis. The Emergency Fund Hypothesis (EFH), the Interest Rate Hypothesis (IRH), and the Policy Replacement Hypothesis (PPP) are the pillars of the lapse policy studies by previous researchers, see Cox and Lin (2006); Kagraoka (2005); Kiesenbauer (2012); Nolte and Schneider (2017); Poufinas and Michaelide (2018); Sirak (2015), and others Vasudev et al. (2016); Yu et al. (2019), and Kuo et al. (2003). The EFH highlights the opinion that policyholders use the cash value as an emergency fund, while IRH stresses the importance of arbitrage when interest rates rise. The PPP emphasises that, when policyholders get a new policy that is better in terms of price and terms, they tend to end the old policy (Russell et al. 2013; Yacob et al. 2018). A paper from St. Gallen University that describes actuarial literature on the lapsed policy found that 49 of the 56 articles studied were published after 2000 (Campbell et al. 2014).

Eling and Kochanski (2013) proposed that the relationship between the theoretical and empirical models for research on lapsed policies be explored and, subsequently, made predictions about lapsed policies. This model can also design products and programs to address why policyholders cancel their policies. Through their literature study, they found that the lapsed policy has become an actively studied area of research in the last few years, with 44 studies on lapsed policy modelling included in their studies. Meanwhile, 12 empirical studies have also been studied mainly on the influence of environmental variables on expired policies. However, studies that consider the policyholder’s information and contract information are lacking as the information is usually kept confidential.

Tennyson (2011) stated that consumers with higher insurance literacy are more likely to take an active and responsible role in considering the appropriate level of personal insurance or seek professional advice on the impact of the decision. The level of consumer insurance literacy is generally low. It is influenced by insufficient product knowledge, low trust in insurance operators, low awareness of risk reduction strategies, and bias when making decisions (Driver et al. 2018). Apart from that, policyholder-cancellation behaviour has been a topic of interest among academicians over the years following the massive cancellation or lapsation of insurance policies (Kuo et al. 2003) and for other reasons (Eling and Kiesenbauer 2014). However, few studies focused on how to model mass cancellation situations. Based on previous studies, it is shown that there are few areas of research in life insurance lapsation explored by researchers. These include modelling the lapse risk and determining the factors behind lapse policies. There have been studies on consumer literacy and behaviour towards purchasing or terminating insurance in recent years. However, based on the previous literature review, we were unable to locate any study that used the bibliometric analysis to evaluate existing research output on life insurance lapsation.

3. Materials and Methods

3.1. Bibliometric Analysis

Recently, bibliometric mapping has gained popularity in numerous fields (Arici et al. 2019; Aria and Cuccurullo 2017; Song et al. 2019). Among the recent bibliometric analyses published and indexed by Scopus were studies by Nobanee et al. (2021a, 2021b). The former authors assessed reputational risk and sustainability research published from 2001 to 2020. The latter authors performed bibliometric analysis concerning “objective risk” or “subjective risk”. According to the findings, using the ranking approach and descriptive statistics to produce a comprehensive bibliometric analysis is insufficient. The authors suggest that a visualisation map must be created and studied using VOSviewer software to construct a more in-depth bibliometric analysis.

The bibliometric analysis involves analysing academic literature through bibliographies to describe, analyse, and monitor published research (Garfield et al. 1964; White and McCain 1989). The study used Bibliometrix R-package software and VOSviewer to conduct the bibliometric analysis. The software contained important algorithms to perform science mapping and statistical analysis. The web interface app (Biblioshiny) was implemented in recent Bibliometrix R-package versions to assist users in conducting bibliometric research without coding. Data can be imported in BibTex, comma-separated values (CSV), or Plain Text format from Scopus or WoS databases using the Biblioshiny interface. Biblioshiny also allows a researcher to filter data. Data can be imported from Scopus in BibTex format by using the Biblioshiny features for the Bibliometrix. Scopus was used as a database in this study because it offers broader content coverage and is more practical due to the availability of individual profiles for all authors, institutions, and serial sources and the interconnected interface of the bibliographic database (Pranckutė 2021).

Janik et al. (2020) stated that the VOSviewer could display network structures comprising multiple elements using a visualisation method based on distance. The study conducted a network analysis on the life insurance lapse concept from the Scopus database. The networks were contrived of nodes and lines, whereby the nodes were represented by keywords, sources, countries, or authors, depending on the research theme (Khan et al. 2020).

3.2. Data Collection

The data collection method was divided into three stages using Scopus to search documents in the first stage. The study also highlighted articles specifically on life insurance lapse or withdrawal. Additionally, the search string comprised several compound keywords linked with the OR and AND operators. Publications wherein the terms “life insurance”, “life assurance”, “life takaful”, “family takaful”, “lapse”, “forfeit”, “withdraw”, “surrender”, and “cancel” appeared as a subject or part of the title, keyword, or abstract were accepted. Meanwhile, the Boolean operator “OR” indicated any of the suggested concepts, while the asterisk (*) was used in the search string to represent any character group, including no character.

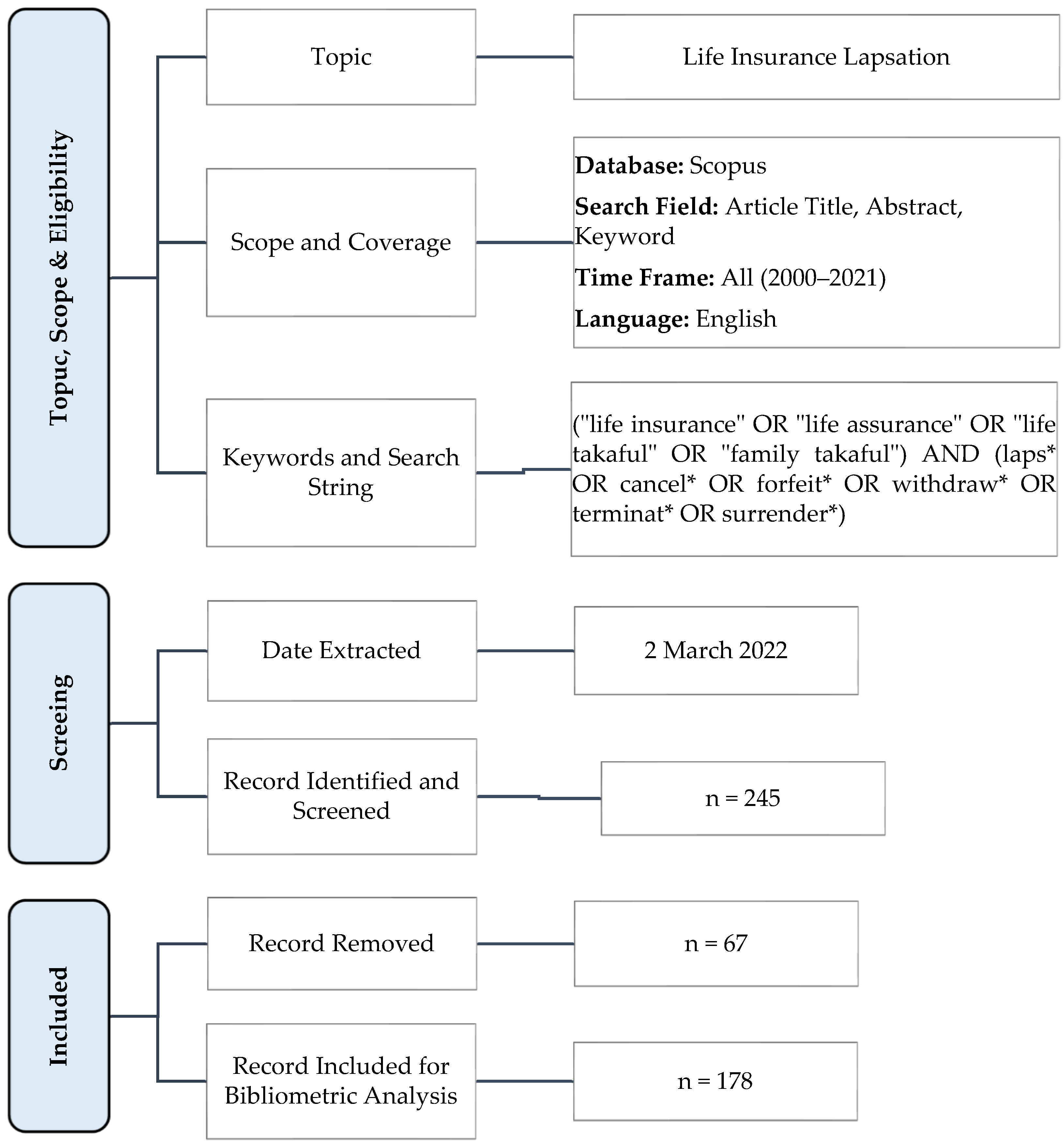

Data search and retrieval were conducted on 2 March 2022, without any filtering, with the initial query of 245 documents. Based on the inclusion and exclusion criteria, the results were filtered to exclude any irrelevant properties. The inclusion and exclusion criteria are depicted in Figure 1, demonstrating the search string combinations, operators, and database filtering using the selected conditions.

The second stage included filtering the data and excluding certain records. The following restrictions were applied: (i) any language besides English was excluded from the analysis, (ii) any documents with no author’s name were excluded, and (iii) only publications ranging from the year 1971 to 2021 were included, and the publications with the year 2022 were excluded since the year has not yet ended during the data search. After the filtration process based on the inclusion and exclusion criteria, 212 out of 245 articles were selected for extraction of the articles. Finally, 178 papers were included for further analysis after a comprehensive screening process based on the abstract.

In the third stage, the Scopus database was uploaded and converted into a Bibliometrix and Plain Text data frame. The Bibliometrix data frame was used for the Biblioshiny analysis and the Plain Text data frame in the VOSviewer analysis. The analysis was divided into five sections: (i) discussing publication growth of life insurance lapse literature; (ii) searching for productive authors, countries, and journals; (iii) explaining the co-occurrence analysis of author keywords; (iv) discovering the most influential documents in life insurance lapse literature; and (v) exploring trend topics and future life insurance lapse research directions.

4. Results and Discussion

4.1. Publication Growth of Life Insurance Lapsation

The data were tabulated based on the document type, defined as a structured document with several legitimate elements and originality, such as an article, conference paper, book review, or book chapter. The study referred to 178 documents in life insurance lapse literature written by 358 authors from 1971 to 2021 indexed in the Scopus database. From the 178 documents analysed, 84.40% were scientific articles, followed by conference papers (7.30%), reviews (2.90%), books (2.20%), and book chapters (1.70%) as shown in Table 1. Meanwhile, analysis of Scopus categories based on subject area revealed that the most discussed themes are economics, econometrics, and finance (33.40%); mathematics (18.90%); business, management and accounting (16.40%); decision sciences (14.08%); and computer science (4.70%). Other categories represent 11.70% of the total publication. It should be noted that certain publications have been categorised in more than one subject area.

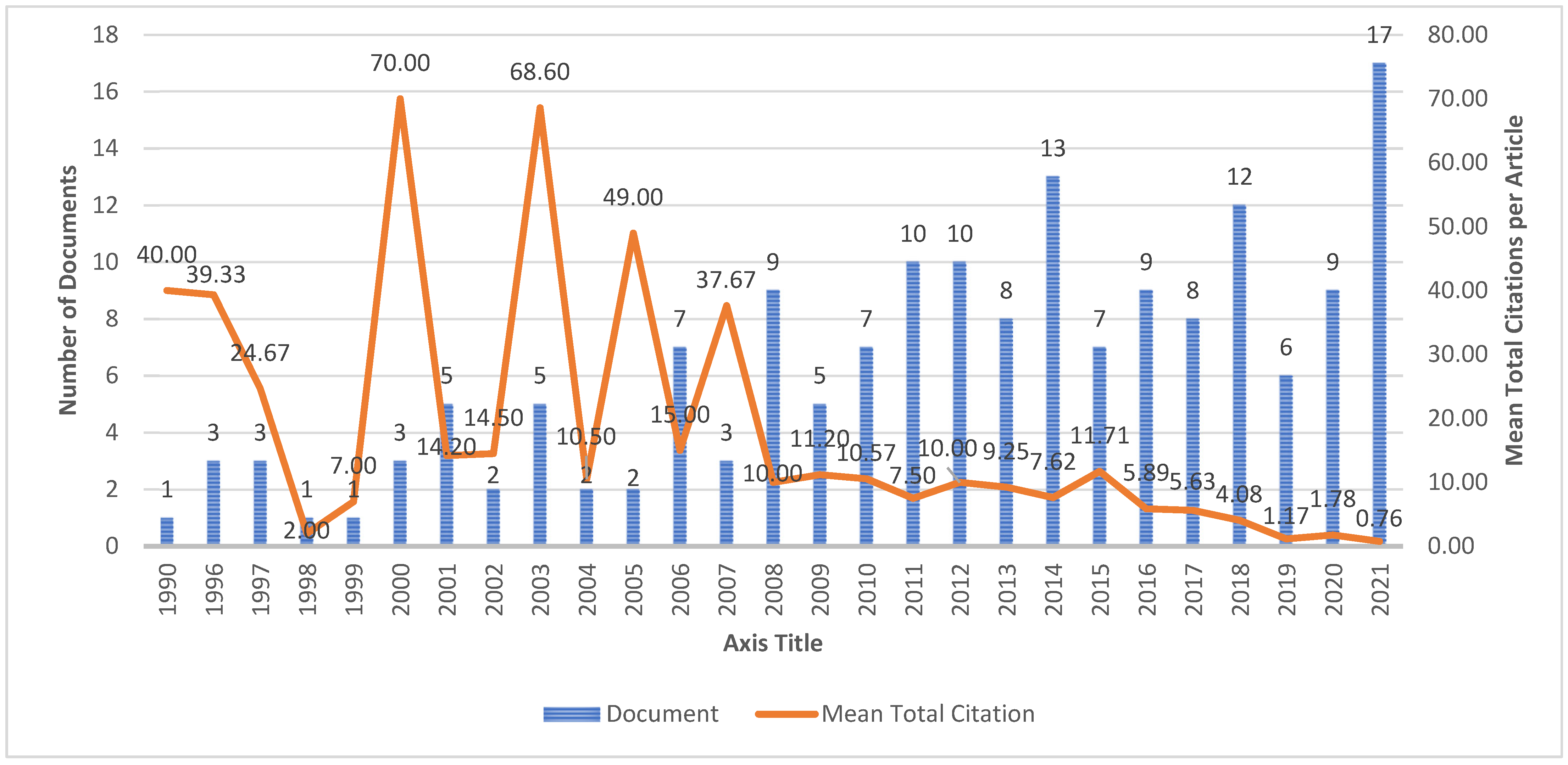

Figure 2 presents the annual publications on the life insurance concept from 1971 to 2021. The publication numbers are almost consistent during the early years, with an increase in life insurance lapse publications from 2001 to 2021. The result extracted from Biblioshiny also showed that the average years from publication was 8.43 years (the average years for an article to be cited), and the average citation per document was 11.75.

4.2. Productive Authors, Countries, and Journals

4.2.1. Author Network Analysis

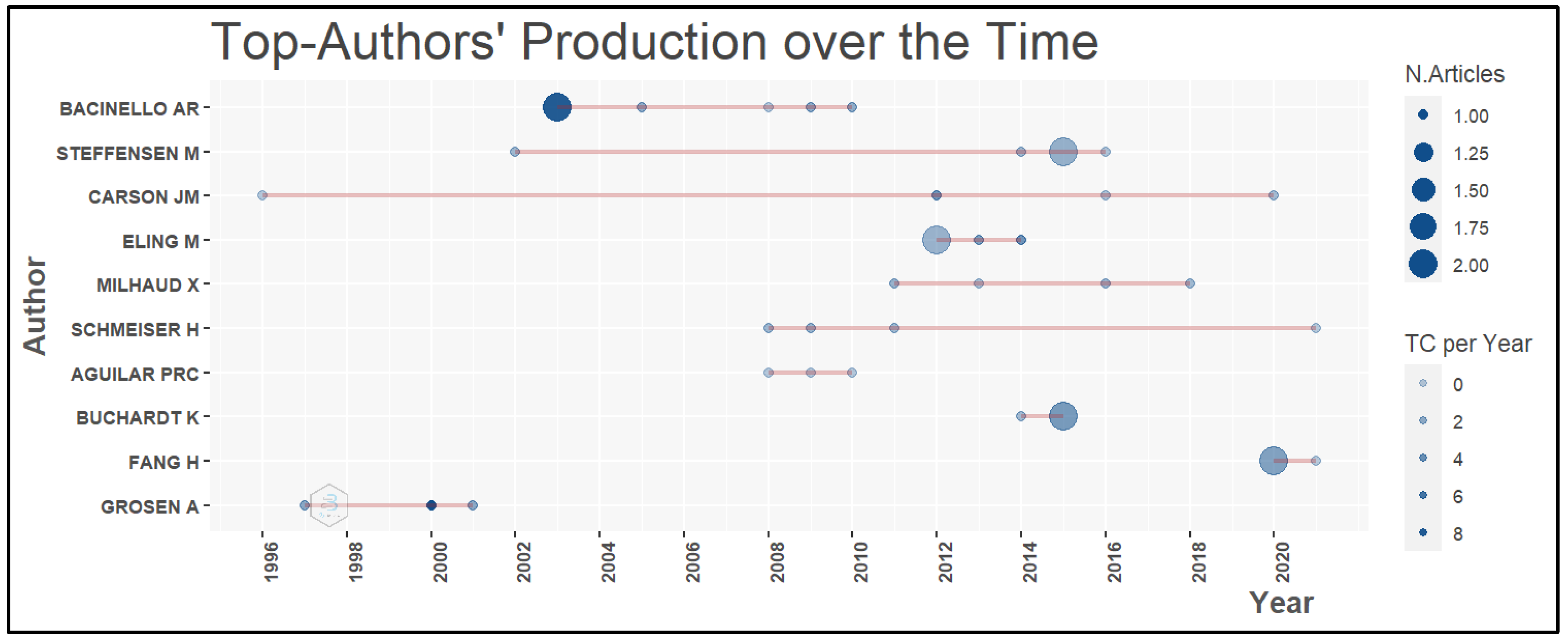

One of the advantages of the Biblioshiny analysis is the revealing of the top productive authors over time—a total of 356 authors published on the topic related to life insurance lapsation. Only two authors (0.56%) published at least five documents, 18 authors (5.06%) published between three to four documents, 34 authors (9.55%) published two documents, and 302 authors (84.83%) published only one document. Figure 3 demonstrates the top ten productive authors in the life insurance lapse literature—the line is an author’s timeline. In contrast, the number of documents by the author per year is proportional to the dot size. The number of yearly citations is proportional to the bubble’s colour intensity, with the first dots on the line indicating when it was first published. The larger the bubble, the more papers an author publishes each year, and the dots with darker colour strength mean more citations.

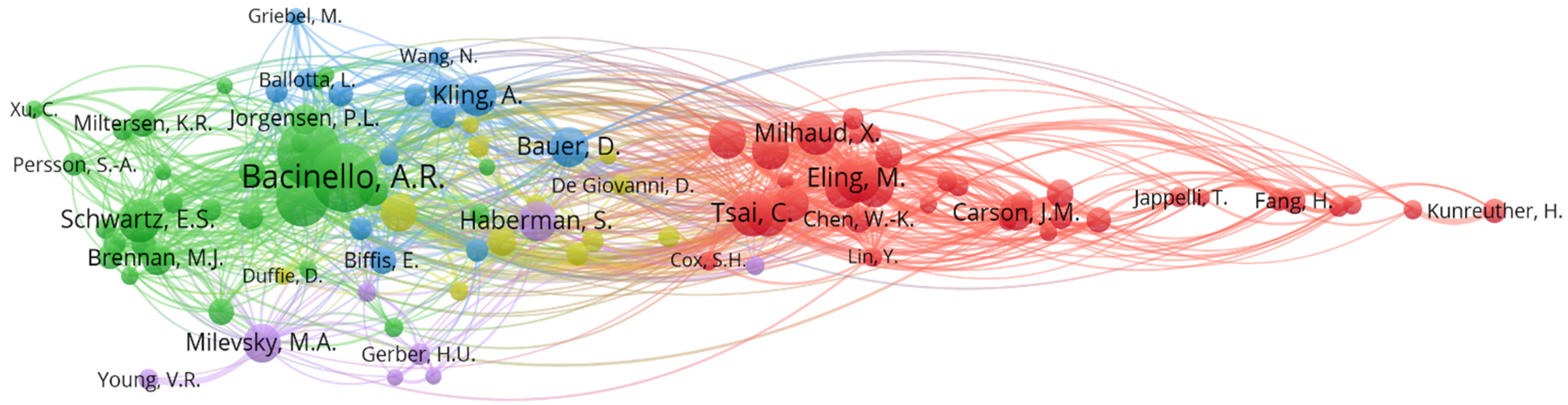

Anna Rita Bacinello appears as the most productive author with six publications in the field of study from 2003 to 2010. The author who remained active in publishing research in life insurance lapse from 1996 to date is James M. Carsom with four publications. Hato Schmeiserstarted his first publication in this field of study in 2008 and remains active to date. Meanwhile, Hanming Fang. has only begun publishing since 2020. One of the studies examines the impact of various factors in explaining life insurance lapsation. The author developed and empirically implemented a dynamic discrete choice model of life insurance decisions (Fang and Kung 2020b). The co-citation study analysed the author’s co-citation network on insurance lapse. Authors’ co-citation analysis is used to classify, trace, and visualise the author’s co-cited work frequency with another author in the citation references (Bayer et al. 1990). Figure 4 demonstrates 178 documents examined from 4012 cited authors with a minimum citation of 2 and the most of 100 citations. Each node in Figure 4 indicates an author, and the size shows the frequency of authors mentioned in the documents. The link between two nodes denotes a co-citation relationship with each link having a strength—the link thickness increases as the strength increases. The VOSviewer software identified five clusters; the nodes with identical colours belong to the same cluster. The green cluster is the most powerful in total link strength and citations, with three of the authors recorded as the top three among all authors.

The cluster highlighting the first group (red cluster, n = 35) of authors included Martin Eling, (51 citations and 48.56 total link strength), Chenghsien Tsai, (49 citations and 47.58 total link strength), and Weiyu Kuo(45 citations and 44.33 total link strength). The second group of co-authors (green cluster, n = 31) included Anna Rita Bacinello (95 citations and 87.50 total link strength), Anders Grosen (90 citations and 84.93 total link strength), and Peter Lohte Jogensen (65 citations and 59.14 total link strength). Table 2 illustrates the top 10 citations of cited authors’ main parameters in life insurance lapsation, which is dominated by authors from clusters 1 (red cluster) and 2 (green cluster).

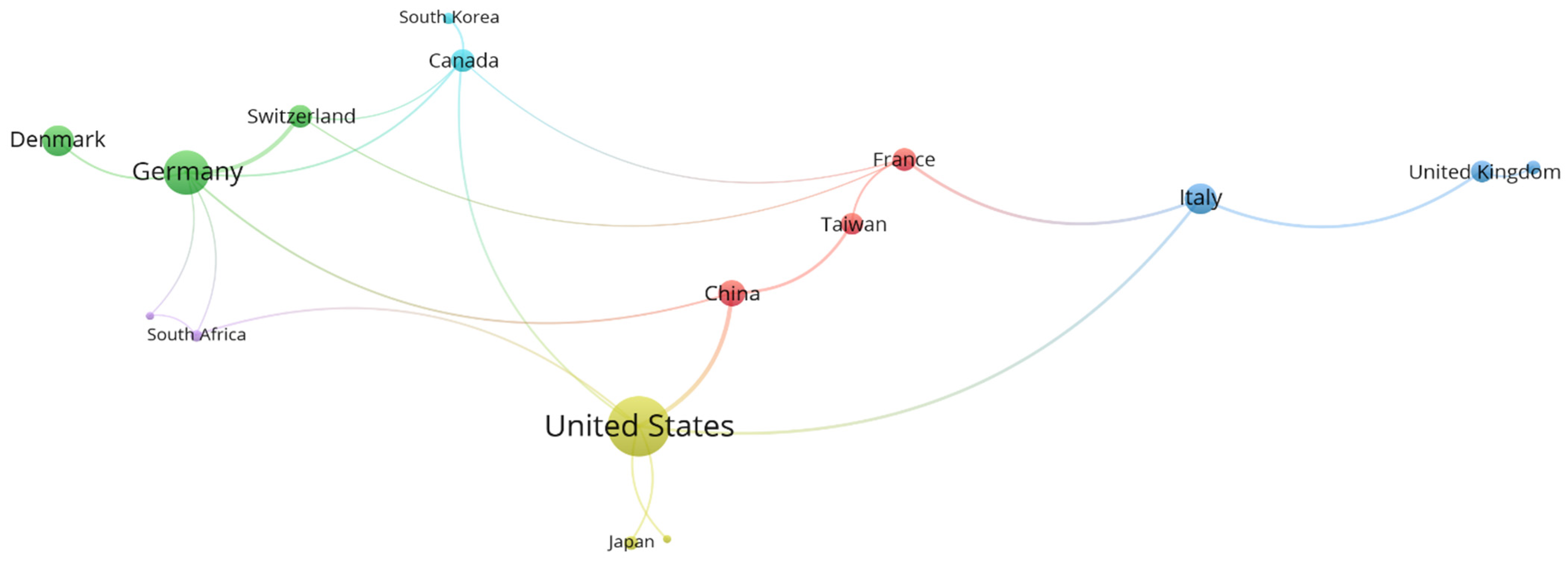

4.2.2. Country Network Analysis

The countries’ co-authorship visualisation occurrences are observable through regional collaboration and research hotspots; Figure 5 displays the countries’ network visualisation map co-occurrences in the life insurance lapse literature. The scale of the circles represents the total occurrences in the documents. Meanwhile, the gap between the circles in individual pairs denotes the collaboration strength, and different circle colours signify other specific collaboration groups. The top 10 countries’ main parameters are illustrated in Table 3. The number of papers published by co-authors from two countries reflects the total relation strength between those two countries. Notably, 22 countries fulfilled the minimum requirement of having published two documents. The United States had the highest total link strength (10), the highest documents (n = 39), and citations (n = 473) regarding international author collaboration. Hence, it can be concluded that as compared to other countries, the United States is considered a major country in scientific publications.

4.2.3. Most Relevant Sources

Table 4 presents the ten most frequent journals based on the number of citations (TC) with the impact factor. The influential journals’ analysis reveals whether the articles in the sources contributed to the field of study. Notably, the Insurance: Mathematics and Economics journal (n = 20 publications) ranked first with a CiteScore and SJR of 2.7 and 1.139, respectively, and 493 citations (n = 20 publications). Surprisingly, five out of the ten highest-influence sources were listed in the first quartile, indicating that these journals were highly influential in the life insurance lapsation. For instance, Insurance: Mathematics and Economics had 20 impactful articles related to life insurance lapsation, whereas the Journal of Risk and Insurance had 16 impactful journals related to the field of study.

4.3. Co-Occurrence Analysis of Author Keywords

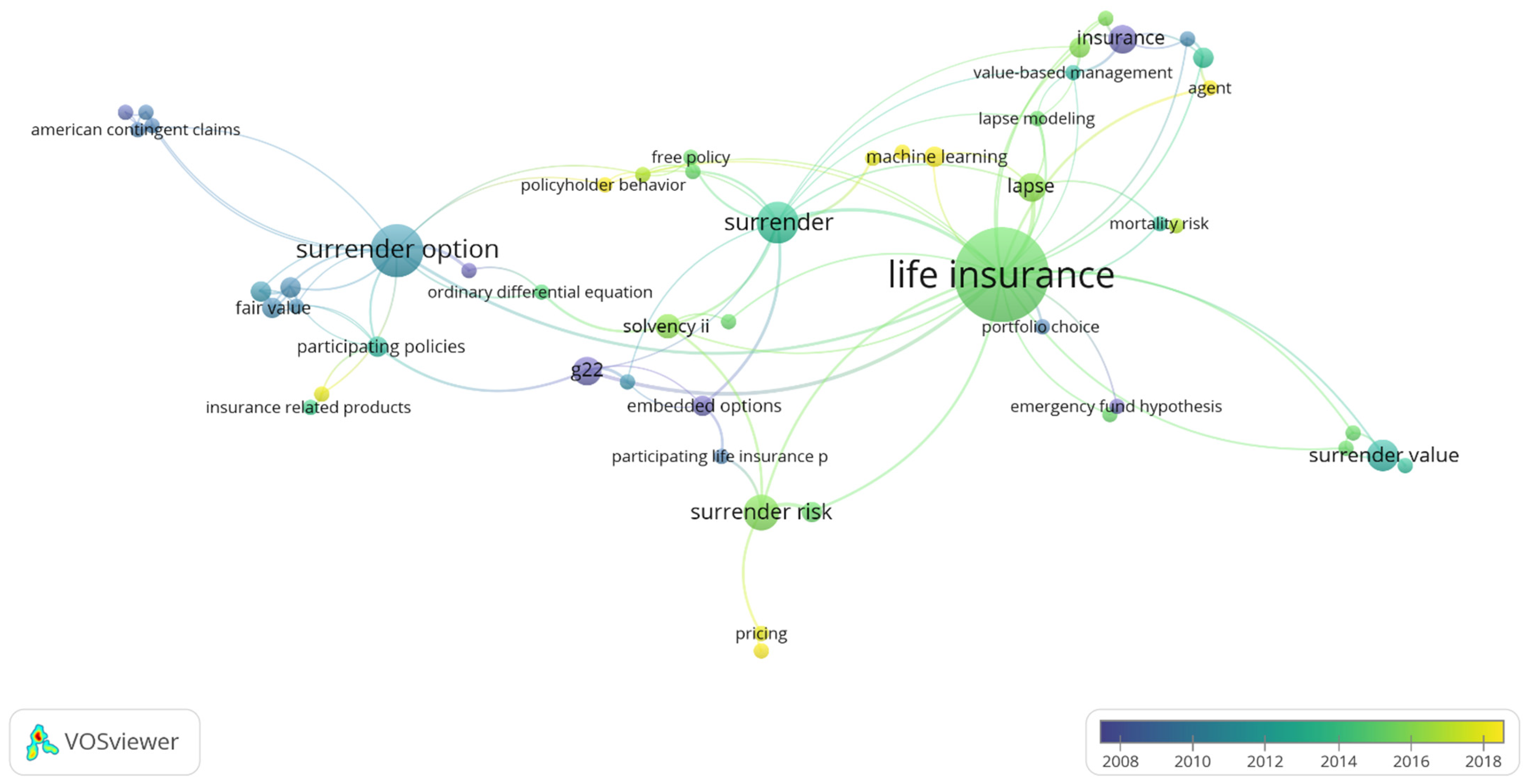

The keyword and co-occurrence network was constructed by capturing an article’s content with greater depth and variety (Della Corte et al. 2019). The study analysed the keyword co-occurrences to visualise the research hotspots in life insurance lapsation with a minimum of two keyword occurrences as a threshold for the study. Out of 443 keywords, 53 meet the threshold. The circle sizes indicate the number of keyword occurrences. Thus, the larger the circle, the more the author’s keywords were co-selected in the life insurance lapse literature. The topic similarity and the relative intensity were identified based on the distance between the individual pairs.

Figure 6 represents a diagram to understand the process, illustrating 11 distinct groups and representing individual subfields of the life insurance lapse research. The links between the keywords indicate the frequency with which the keywords co-occurred. The average year of publication of the keywords was determined using colours. Remarkably, the focus of research from 2008 to 2010 was on life insurance policy characteristics (purple) such as “embedded options”, “free policy option”, “surrender option”, “insurance contract”, “least squares Monte Carlo method”, and “participating life insurance policies”. Meanwhile, the network map reveals a greater focus on modelling life insurance lapsation approaches such as “machine learning”, “policyholder behaviour”, “pricing”, “agent”, “stochastic interest rate”, “logistic regression”, and “lapse risk” from 2018 to date (yellow).

Song et al. (2019) mentioned that the author’s keywords are usually linked to the publication contents, sufficient to extract a sector’s topical aspects. Based on the Biblioshiny analysis, the most commonly occurring keywords were life insurance and surrender option with 32 and 13 total instances, respectively. Surrender (n = 9) and surrender risk (n = 7) also appeared to be among the top frequently occurring keywords. As mentioned above, policyholder behaviour started to gain greater focus among scholars from 2018 to date. However, there are limited studies on policyholder behaviour towards life insurance lapsation.

In 2013, Eling and Kochanski (2013), among the top ten authors in the life insurance lapsation, reviewed research on lapse in life insurance and outlined potential new research areas in this field. The author found out that research on how policyholders behave in extreme scenarios will be interesting topics to consider. Next, in 2014, Eling and Kiesenbauer (2014) recommended additional research to build a policyholder retention programme concentrating on those who are most prone to lapse their policies. One of the studies that considered policyholder behaviour such as insurance literacy and intention to purchase personal insurance is that by Sanjeewa et al. (2019). Most of the authors are prone to consider policyholder characteristics in these studies (Giri 2018; Gemmo and Götz 2016; Yakob et al. 2019; Barucci et al. 2020). Meanwhile, (Subashini and Velmurugan 2015; Xong et al. 2019; Milhaud et al. 2011; Yakob et al. 2019; Ćurak et al. 2015; and Barucci et al. 2020) also take into account on the policy and company characteristics.

4.4. Document Analysis

The following analysis includes a global and local citation on related documents in insurance lapse. The number of citations a text obtains from the entire Scopus database is considered a global citation that assesses the paper’s significance, usually receiving citations from various disciplines. Contrarily, local citation counts the number of citations a document acquired from other documents (Aria and Cuccurullo 2017). Hence, the global citation includes a cross-disciplinary perspective, whereas the local citations only consider citations within a single discipline.

Besides scientific productivity, studies have proven that publication citation numbers are used to determine the importance and scholarly impact (Grant et al. 2000; Waheed et al. 2018). The findings also revealed that the most widely cited paper between 1971 and 2021 was from Grosen and Løchte Jørgensen (2000); its total local and global citations were 39 and 206, respectively. The document examined a participating (or with profit) scheme, one of the most popular life insurance items, demonstrating a standard participating program divided into three parts: a risk-free bond, a bonus option, and a surrender option. The algorithm considered local citation to ensure the impact of documents within a discipline was employed and analysed. Table 5 shows the ten most cited documents from the study dataset.

4.5. Trend Topics and Future Directions

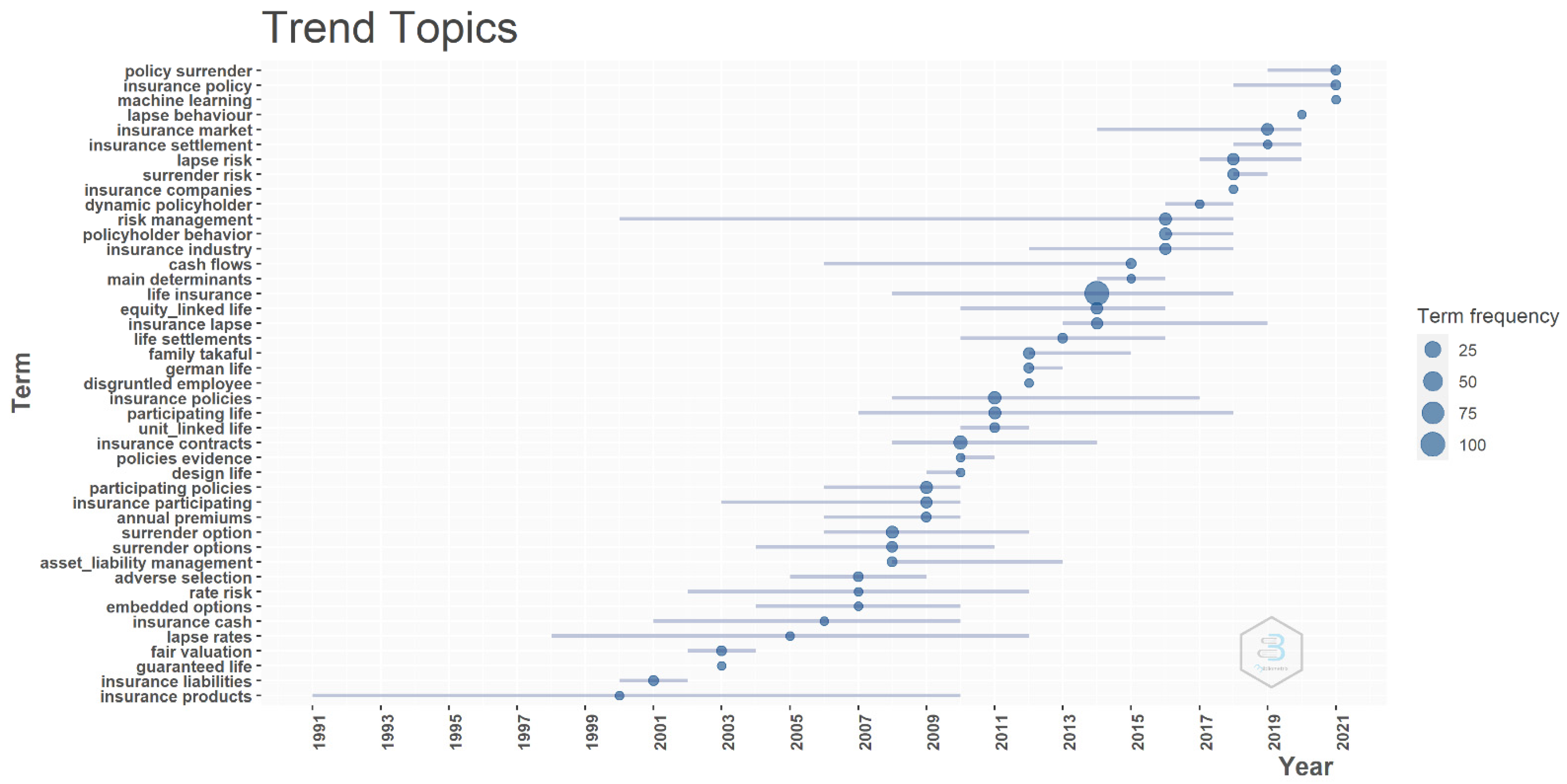

Next, an overview of the trending subject was performed based on the dataset titles using Biblioshiny. The following parameters were set in the analysis: the word minimum frequency was two; the number of words per year was three; and the N-grams was Bigrams, which means two consecutive terms in a sentence were selected. Over time, the study delved further into the trending issues of keyword occurrences in insurance lapse literature. Although the author keyword co-occurrences network (Figure 6) signified several authors’ keywords, Figure 7 illustrated the hierarchical topic structure in life insurance lapse environments addressed by scholars yearly. Therefore, the subjects could relate to life insurance lapse environments.

From Figure 7, the most popular topics based on Bigrams on Biblioshiny among the reviewed documents were as follows: “life insurance” (n = 104), which gained popularity from 2008 until 2018, and “insurance contract” (n = 12), from 2008 to 2014. Meanwhile, documents containing the term “surrender option” in their title gained interest among scholars from 2004 to 2012. Then, since 2013, authors have used “insurance lapse” as a title for their research. One of the most cited articles published in 2013 on surrender and lapse was a study by Eling and Kochanski (2013), with 34 global citations. The authors reviewed the existing research on life insurance lapse and identified future research opportunities in life insurance lapse. The authors found that the financial consequences of lapse are significant. As a result, lapsation is of great interest to academicians, businesses, regulators, and policymakers.

From 1998 to 2012, researchers were more interested in the topics “lapse rate”; meanwhile, the research topic “policy surrender” gained interest in the later years, from 2019 to 2021, a vital domain of the life insurance lapse literature along with “lapse risk” in 2017 to 2020 and “machine learning” in 2021. Authors started delving into policyholder behaviour since 2016 onwards and lapse behaviour in 2020. (Buchardt and Møller 2015) investigated the problem of valuing life insurance payouts in the context of policyholder behaviour. They found that modelling policyholder behaviour impacts both the market value and the cash flow structure.

Since then, we have observed a significant increase in life insurance lapse research. For example, in 2020, a study by Barucci et al. (2020) used microdata on each contract and relevant macroeconomic indicators to analyse the causes of the insured persons’ lapse decisions. The authors next used a panel analysis to look at the impact of macroeconomic variables on breaches at the regional level. They concluded that there is some evidence on the linkage between lapse rates and personal financial or economic challenges. Ultimately, the trend analysis showed that the topic gained scholars’ interest over time as it evolved.

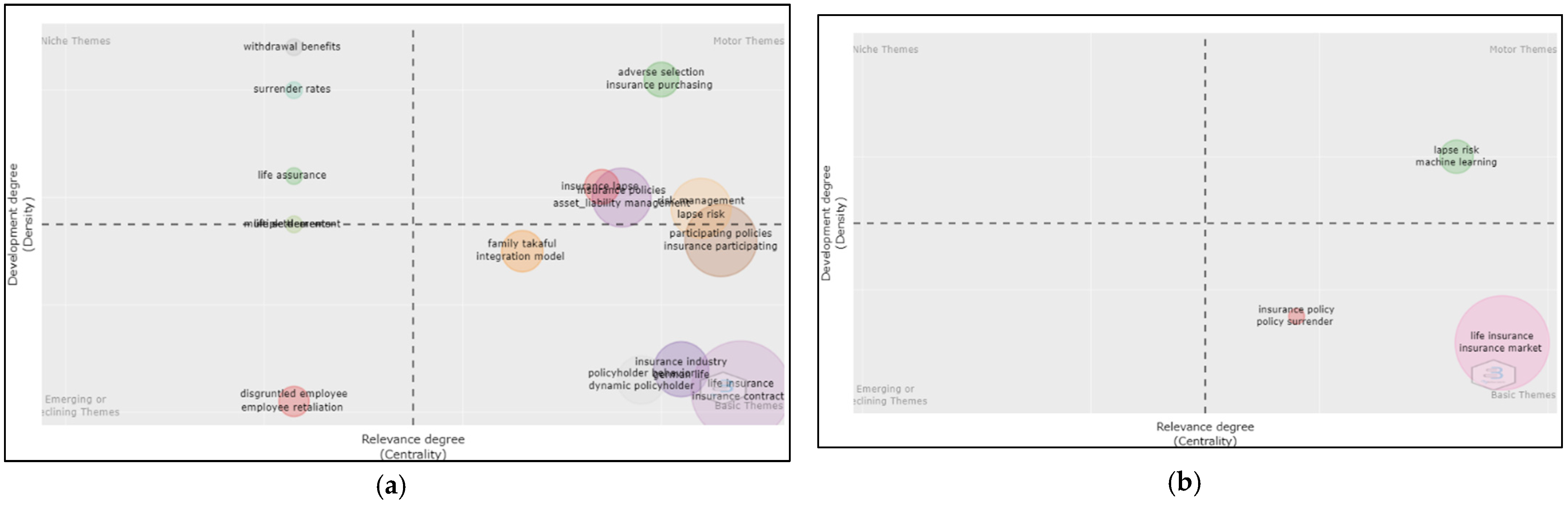

The coronavirus (COVID-19) outbreak had extensive economic consequences, triggering financial crises and a worldwide economic downturn. Therefore, we have also analysed the thematic evolution before and after COVID-19 in the study of life insurance lapse as an additional information relating to the trend topics. Figure 8 shows the thematic map based on these thresholds; thematic evolution is based on titles, the minimum number of labels is two, and the number of cutting points is one, with the cutting year being 2019. Figure 8a presented the thematic evolution map of titles before COVID-19, which covers the period of 1974 to 2019. There were 152 publications during this period, with 15 clusters generated using Biblioshiny. Due to high centrality and density at this period, the “insurance lapse”, “insurance policies”, “risk management”, and “adverse selection” themes are in the motor theme quadrant and are highly developed topics. Among the basic themes are “family takaful”, “insurance industry”, “policyholder behaviour”, “participating policies”, and “insurance industry”. In the upper-left quadrant, the niche theme shows high density but low centrality; hence, they have only a minor contribution in the field. “Withdrawal benefits”, “surrender rates”, and “life assurance” are in the niche theme. Meanwhile, “disgruntled employee” and “employee retaliation” seem to become emerging or declining themes.

The thematic map after COVID-19, which covers 2020 to 2021, is shown in Figure 8b, with 26 publications and three clusters. The motor themes “lapse risk” and “machine learning” appear to be the most highly developed themes, as they have the highest density and centrality degrees. Meanwhile, in the lower-right quadrant, “insurance policy”, “policy surrender”, “life insurance”, and “insurance market” are the basic themes. Hence, analysing the thematic map may help future researchers decide on what themes to explore and identify the themes that have fallen under the emerging and declining quadrant.

In this bibliometric analysis, we discovered that life insurance lapsation has been an interesting topic to be explored by researchers. Table 6 presents the extra information on what has been done by previous authors, including their recommendations for future research. The lists were extracted from the reviewed documents. Out of 178 documents reviewed, 10 documents published in 2020 and 2021 that have received global citations were analysed, and the summary of the output is presented in Table 6.

Based on Table 6, we have concluded some reflections on the implications for insurance companies of the study of life insurance lapsation. From insurers’ perspectives, these studies could benefit them in many ways. Using a clustering-based technique that incorporates geodemographic spatial data allows the organisation to better understand their customers and make better judgments in recognising customers who have a high tendency to cancel their policies (Hu et al. 2021). Hence, they will be able to tailor marketing and initiate policy retention campaigns accordingly, resulting in a significant decrease in customer churn and in cost savings for the insurance business.

Besides that, one of the implications of the study of life insurance lapsation is that it may benefit insurance companies in determining the risks or factors that may contribute to lapse decisions among policyholders. Last but not least, the study on life insurance lapsation may give some insight to insurance companies on models to consider in determining the lapse rate. Barucci et al. (2020) found distinct characteristics of lapse rate for different types of products, supported by Biagini et al. (2021). Traditional (participating) contract lapse rates and unit-linked contract lapse rates differ. Hence, it is crucial for organisations to appropriately model the lapse rate to avoid miscalculations that could lead to undesirable costs and improve future lapse behaviour prediction.

5. Conclusions

The study provided a comprehensive overview of scientific publications in insurance lapse literature using the bibliometric analysis. The descriptive analysis showed that 84.40% out of 178 documents were articles with increasing publication trends over the years. The most productive author and source of insurance lapse literature were Bacinello, A.R., with six publications, and the Insurance: Mathematics and Economics journal, respectively. The analysis also showed an increasing growth in life insurance lapse research. The United Kingdom dominated in the top ten highest-influence sources based on total citations, and among the listed sources were Journal of Risk and Insurance, North American Actuarial Journal, Scandinavian Actuarial Journal, Journal of Risk Finance, and Astin Bulletin. However, the United States came in first in terms of total link strength of international co-authorship and the highest number of papers and citations.

Nevertheless, based on the occurrences of the keywords “life insurance”, life insurance is still a trending theme to be explored by scholars. The trend topics analysis also showed that interest in the life insurance lapse topic had evolved significantly from early publication years. “Policy surrender” and “machine learning” were the most trending topics in 2021. Meanwhile, the research theme on “policyholder behaviour” and “lapse behaviour” has gained scholars’ interest since 2016. Therefore, it is suggested that future researchers who wish to investigate further on life insurance lapse look for articles with the terms lapse behaviour, policyholder behaviour, and policy surrender apart from other related words. Apart from that, we believe that with the advancement of technology, future research may enhance the study of life insurance lapse risk or model the lapse policyholder behaviour using predictive models or machine learning algorithms as it is a trending topic nowadays. As supported by Hu et al. (2021), the use of a clustering-based approach may assist the insurance company in gaining insights into the spatial characteristics of its policyholders, adjusting marketing and customer retention strategies as needed and improving future lapse behaviour prediction.

Despite the efforts to conduct the bibliometric analysis as efficiently and precisely as possible, the study has several limitations. Firstly, the research focused solely on the Scopus database as the primary source. Although Scopus provides unrivalled and continuous access to the most important research output from across the world (Elsevier B.V. 2020), the collected and analysed database excluded available sources such as Web of Science, Google Scholar, and Dimensions that could have been used to produce more valuable results by combining the data from different sources. Secondly, the databases used only extracted and analysed sources in English, excluding non-English publications as a medium in the research theme. Thus, future studies should consider combining databases from various sources when possible. Conclusively, the study contributes to the field by providing a thorough growth and trend analysis on life insurance lapse literature; presenting the productive scholars, countries, and journals; and analysing the keyword network, co-occurrence networks, and trend topics. The findings may benefit researchers in defining the research objective and identifying the aspects of insurance lapse that should be explored to advance future studies.

Author Contributions

Conceptualisation, S.N.S. and N.I.; methodology, S.N.S.; software, S.N.S.; resources, S.N.S., writing—original draft preparation, S.N.S.; writing—review and editing, N.I. and N.F.R.; visualisation, S.N.S.; supervision, N.I. and N.F.R. All authors have read and agreed to the published version of the manuscript.

Funding

The authors gratefully acknowledge the partial financial support received through research grants (FRGS/1/2019/STG06/UKM/01/5) from Ministry of Education, Malaysia and (GUP-2019-031) from Universiti Kebangsaan Malaysia. No additional external funding was received for this study.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

S.N.S. would like to thank N.I. and N.F.R. on various technical issues examined in this paper and for their advice and comments. S.N.S., however, bear full responsibility for the paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Adams, Mike, Lars-Fredrik Andersson, Magnus Lindmark, Liselotte Eriksson, and Elena Veprauskaite. 2020. Managing Policy Lapse Risk in Sweden’s Life Insurance Market between 1915 and 1947. Business History 62: 222–39. [Google Scholar] [CrossRef] [Green Version]

- Anandalakshmy, A., and K. Brindha. 2017. Policy Holders’ Awareness and Factors Influencing Purchase Decision towards Health Insurance in Coimbatore District. International Journal of Commerce and Management Research 3: 12–16. Available online: www.managejournal.com (accessed on 20 November 2021).

- Aria, Massimo, and Corrado Cuccurullo. 2017. Bibliometrix: An R-Tool for Comprehensive Science Mapping Analysis. Journal of Informetrics 11: 959–75. [Google Scholar] [CrossRef]

- Arici, Faruk, Pelin Yildirim, Şeyma Caliklar, and Rabia M. Yilmaz. 2019. Research Trends in the Use of Augmented Reality in Science Education: Content and Bibliometric Mapping Analysis. Computers & Education 142: 103647. [Google Scholar]

- Bacinello, Anna Rita. 2003a. Pricing Guaranteed Life Insurance Participating Policies with Annual Premiums and Surrender Option. North American Actuarial Journal 7: 1–17. [Google Scholar] [CrossRef]

- Bacinello, Anna Rita. 2003b. Fair Valuation of a Guaranteed Life Insurance Participating Contract Embedding a Surrender Option. Journal of Risk and Insurance 70: 461–87. [Google Scholar] [CrossRef]

- Bacinello, Anna Rita. 2005. Endogenous Model of Surrender Conditions in Equity-Linked Life Insurance. Insurance: Mathematics and Economics 37: 270–96. [Google Scholar] [CrossRef]

- Barucci, Emilio, Tommaso Colozza, Daniele Marazzina, and Edit Rroji. 2020. The Determinants of Lapse Rates in the Italian Life Insurance Market. European Actuarial Journal 10: 149–78. [Google Scholar] [CrossRef] [Green Version]

- Bayer, Alan E., John Carson Smart, and Gerald W. McLaughlin. 1990. Mapping Intellectual Structure of a Scientific Subfield through Author Cocitations. Journal of the American Society for Information Science 41: 444–52. [Google Scholar] [CrossRef]

- Bernama. 2020. Allianz Sees More Payment Defaults in October When Moratorium Ends. Available online: https://www.Thestar.Com.My/Business/Business-News/2020/05/19/Allianz-See-More-Payment-Defaults-in-October-When-Moratorium-Ends (accessed on 16 February 2022).

- Biagini, Francesca, Tobias Huber, Johannes G. Jaspersen, and Andrea Mazzon. 2021. Estimating Extreme Cancellation Rates in Life Insurance. Journal of Risk and Insurance 88: 971–1000. [Google Scholar] [CrossRef]

- Brum, Matias, and Mauricio De Rosa. 2021. Too Little but Not Too Late: Nowcasting Poverty and Cash Transfers’ Incidence during COVID-19’s Crisis. World Development 140: 105227. [Google Scholar] [CrossRef] [PubMed]

- Buchardt, Kristian, and Thomas Møller. 2015. Life Insurance Cash Flows with Policyholder Behavior. Risks 3: 290–317. [Google Scholar] [CrossRef] [Green Version]

- Campbell, Jason, Michael Chan, Kate Li, Louise Lombardi, Lucian Lombardi, Marianne Purushotham, and Anand Rao. 2014. Modeling of Policyholder Behavior for Life Insurance and Annuity Products. Report. Schaumburg: Society of Actuaries. [Google Scholar]

- Carson, James M., Cameron McNeill Ellis, Robert E. Hoyt, and Krzysztof Ostaszewski. 2020. Sunk Costs and Screening: Two-Part Tariffs in Life Insurance. Journal of Risk and Insurance 87: 689–718. [Google Scholar] [CrossRef]

- Cheng, Chunli, and Jing Li. 2018. Early Default Risk and Surrender Risk: Impacts on Participating Life Insurance Policies. Insurance: Mathematics and Economics 78: 30–43. [Google Scholar] [CrossRef]

- Cole, Cassandra, and Stephen G. Fier. 2021. An Examination of Life Insurance Policy Surrender and Loan Activity. Journal of Risk and Insurance 88: 483–516. [Google Scholar] [CrossRef]

- Cox, Samuel Hanson, and Yijia Lin. 2006. Annuity Lapse Rate Modeling: Tobit or Not Tobit? Working Paper. Schaumburg: Society of Actuaries. [Google Scholar]

- Ćurak, Marijana, Doris Podrug, and Klime Poposki. 2015. Policyholder and Insurance Policy Features as Determinants of Life Insurance Lapse-Evidence from Croatia. Economics and Business Review 1: 58–77. [Google Scholar] [CrossRef]

- Della Corte, Valentina, Giovanna Del Gaudio, Fabiana Sepe, and Fabiana Sciarelli. 2019. Sustainable Tourism in the Open Innovation Realm: A Bibliometric Analysis. Sustainability 11: 6114. [Google Scholar] [CrossRef] [Green Version]

- De Giovanni, Domenico. 2010. Lapse Rate Modeling: A Rational Expectation Approach. Scandinavian Actuarial Journal 2010: 56–67. [Google Scholar] [CrossRef]

- Driver, Tania, Mark Brimble, Brett Freudenberg, and Katherine Hunt. 2018. Insurance Literacy in Australia: Not Knowing the Value of Personal Insurance. Financial Planning Research Journal 1: 53. [Google Scholar]

- Eling, Martin, and Dieter Kiesenbauer. 2014. What Policy Features Determine Life Insurance Lapse? An Analysis of the German Market. Journal of Risk and Insurance 81: 241–69. [Google Scholar] [CrossRef]

- Eling, Martin, and Michael Kochanski. 2013. Research on Lapse in Life Insurance—What Has Been Done and What Needs to Be Done? The Journal of Risk Finance 14: 392–413. [Google Scholar] [CrossRef] [Green Version]

- Elsevier B.V. 2020. Scopus Preview-Scopus-Welcome to Scopus. Amsterdam: Elsevier B.V. [Google Scholar]

- Falden, Debbie Kusch, and Anna Kamille Nyegaard. 2021. Retrospective Reserves and Bonus with Policyholder Behavior. Risks 9: 15. [Google Scholar] [CrossRef]

- Fang, Hangmin, and Edward Kung. 2020a. Life Insurance and Life Settlements: The Case for Health-Contingent Cash Surrender Values. Journal of Risk and Insurance 87: 7–39. [Google Scholar] [CrossRef]

- Fang, Hangmin, and Edward Kung. 2020b. Why Do Life Insurance Policyholders Lapse? The Roles of Income, Health, and Bequest Motive Shocks. Journal of Risk and Insurance 88: 937–70. [Google Scholar] [CrossRef]

- Fang, Hanming, and Zenan Wu. 2020. Life Insurance and Life Settlement Markets with Overconfident Policyholders. Journal of Economic Theory 189: 105093. [Google Scholar] [CrossRef]

- Garfield, Eugene, Irving H. Sher, and Ricahrd J. Torpie. 1964. The Use of Citation Data in Writing the History of Science. Philadelphia: Institute for Scientific Information. [Google Scholar]

- Gemmo, Irina, and Martin Götz. 2016. Life Insurance and Demographic Change: An Empirical Analysis of Surrender Decisions Based on Panel Data. 240. SAFE Sustainable Architecture for Finance in Europe. Available online: https://ssrn.com/abstract=3230274Electroniccopyavailableat:https://ssrn.com/abstract=3230274Electroniccopyavailableat:https://ssrn.com/abstract=3230274Electroniccopyavailableat:https://ssrn.com/abstract=3230274 (accessed on 2 March 2022).

- Giri, Manohar. 2018. A Behavioral Study of Life Insurance Purchase Decisions. Indian Institute of Technology Kanpur. Ph.D. thesis, Industrial and Management Engineering, Kanpur, India. [Google Scholar]

- Grant, Jonathan, Robert Cottrell, Françoise Cluzeau, and Gail Fawcett. 2000. Evaluating ‘Payback’ on Biomedical Research from Papers Cited in Clinical Guidelines: Applied Bibliometric Study. BMJ 320: 1107–11. [Google Scholar] [CrossRef] [Green Version]

- Grosen, Anders, and Peter Lochte Jorgensen. 1997. Valuation of Early Exercisable Interest Rate Guarantees. The Journal of Risk and Insurance 64: 481. [Google Scholar] [CrossRef]

- Grosen, Anders, and Peter Løchte Jørgensen. 2000. Fair Valuation of Life Insurance Liabilities: The Impact of Interest Rate Guarantees, Surrender Options, and Bonus Policies. Insurance: Mathematics and Economics 26: 221–53. [Google Scholar] [CrossRef]

- Hong, Jimin. 2020. The Effect of Life Insurance Settlement on Insurance Market and Consumer Welfare. Communications for Statistical Applications and Methods 27: 689–99. [Google Scholar] [CrossRef]

- Hu, Sen, Adrian O’Hagan, James Sweeney, and Mohammadhossein Ghahramani. 2021. A Spatial Machine Learning Model for Analysing Customers’ Lapse Behaviour in Life Insurance. Annals of Actuarial Science 15: 367–93. [Google Scholar] [CrossRef]

- Insurance Barometer Study. 2021. Insurance Barometer Study, LIMRA and Life Happens. COVID-19 Drives Interest in Life Insurance. Available online: https://www.limra.com/siteassets/newsroom/help-protect-our-families/2022_covid-drives-li-awareness_infographic.pdf (accessed on 2 March 2022).

- Janik, Agnieszka, Adam Ryszko, and Marek Szafraniec. 2020. Scientific Landscape of Smart and Sustainable Cities Literature: A Bibliometric Analysis. Sustainability 12: 799. [Google Scholar] [CrossRef] [Green Version]

- Jensen, Bjarke, Peter Løchte Jørgensen, and Anders Grosen. 2001. A Finite Difference Approach to the Valuation of Path Dependent Life Insurance Liabilities. The Geneva Papers on Risk and Insurance Theory 26: 57–84. [Google Scholar] [CrossRef]

- Kagraoka, Yusho. 2005. Modeling Insurance Surrenders by the Negative Binomial Model. Working Paper. Amsterdam: Elsevier Science, Available online: http://www.musashi.jp/ (accessed on 10 November 2020).

- Khan, Ashraf, Mohammad Kabir Hassan, Andrea Paltrinieri, Alberto Dreassi, and Salman Bahoo. 2020. A Bibliometric Review of Takaful Literature. International Review of Economics and Finance 69: 389–405. [Google Scholar] [CrossRef]

- Kiesenbauer, Dieter. 2012. Main Determinants of Lapse in the German Life Insurance Industry. North American Actuarial Journal 16: 52–73. [Google Scholar] [CrossRef]

- Kuo, Weiyu, Chenghsien Tsai, and Wei-Kuang Chen. 2003. An Empirical Study on the Lapse Rate: The Cointegration Approach. Journal of Risk and Insurance 70: 489–508. [Google Scholar] [CrossRef]

- Li, Zongyun, Panteha Farmanesh, Dervis Kirikkaleli, and Rania Itani. 2021. A Comparative Analysis of COVID-19 and Global Financial Crises: Evidence from US Economy. Economic Research-Ekonomska Istraživanja 2021: 1–15. [Google Scholar] [CrossRef]

- Milhaud, Xavier, Stéphane Loisel, and Véronique Maume-Deschamps. 2011. Surrender Triggers in Life Insurance: What Main Features Affect the Surrender Behavior in a Classical Economic Context? Institut Des Actuaires 11: 5–48. [Google Scholar]

- Nobanee, Haitham, Maryam Alhajjar, Ghada Abushairah, and Safaa Al Harbi. 2021a. Reputational Risk and Sustainability: A Bibliometric Analysis of Relevant Literature. Risks 9: 134. [Google Scholar] [CrossRef]

- Nobanee, Haitham, Maryam Alhajjar, Mohammed Ahmed Alkaabi, Majed Musabah Almemari, Mohamed Abdulla Alhassani, Naema Khamis Alkaabi, Saeed Abdulla Alshamsi, and Hanan Hamed AlBlooshi. 2021b. A Bibliometric Analysis of Objective and Subjective Risk. Risks 9: 128. [Google Scholar] [CrossRef]

- Nolte, Sven, and Judith C. Schneider. 2017. Don’t Lapse into Temptation: A Behavioral Explanation for Policy Surrender. Journal of Banking and Finance 79: 12–27. [Google Scholar] [CrossRef]

- Outreville, Jean-Francois. 1990. Whole-Life Insurance Lapse Rates and the Emergency Fund Hypothesis. Insurance Mathematics and Economics 9: 249–55. [Google Scholar] [CrossRef]

- Poufinas, Thomas, and Gina Michaelide. 2018. Determinants of Life Insurance Policy Surrenders. Modern Economy 9: 1400–22. [Google Scholar] [CrossRef] [Green Version]

- Pranckutė, Raminta. 2021. Web of Science (Wos) and Scopus: The Titans of Bibliographic Information in Today’s Academic World. Publications 9: 12. [Google Scholar] [CrossRef]

- Russell, David T., Stephen G. Fier, James M. Carson, and Randy E. Dumm. 2013. An Empirical Analysis of Life Insurance Policy Surrender Activity. Journal of Insurance Issues 36: 35–57. [Google Scholar]

- Russo, Vincenzo, Rosella Giacometti, and Frank J. Fabozzi. 2017. Intensity-Based Framework for Surrender Modeling in Life Insurance. Insurance: Mathematics and Economics 72: 189–96. [Google Scholar] [CrossRef]

- Sanjeewa, Weedige Sampath, Hongbing Ouyang, Yao Gao, and Yaqing Liu. 2019. Decision Making in Personal Insurance: Impact of Insurance Literacy. Sustainability 11: 6795. [Google Scholar] [CrossRef] [Green Version]

- Sirak, Adjmal S. 2015. Income and Unemployment Effects on Life Insurance Lapse. Working Paper. Available online: https://www.researchgate.net/publication/299455763 (accessed on 22 November 2021).

- Song, Yu, Xieling Chen, Tianyong Hao, Zhinan Liu, and Zixin Lan. 2019. Exploring Two Decades of Research on Classroom Dialogue by Using Bibliometric Analysis. Computers & Education 137: 12–31. [Google Scholar] [CrossRef]

- Steffensen, Mogens. 2002. Intervention Options in Life Insurance. Insurance: Mathematics and Economics 31: 71–85. [Google Scholar] [CrossRef]

- Subashini, S., and Ramaswamy Velmurugan. 2015. Lapsation in Life Insurance Policies. International Journal of Advance Research in Computer Science and Management Studies 3: 41–45. Available online: www.ijarcsms.com (accessed on 22 November 2021).

- Tennyson, Sharon. 2011. Consumers’ Insurance Literacy: Evidence from Survey Data. Financial Services Review 20: 165–79. Available online: https://www.researchgate.net/publication/267094407 (accessed on 1 March 2022).

- Vasudev, Mohnish, Raheja Bajaj, and Antonio Alegre Escolano. 2016. On the Drivers of Lapse Rates in Life Insurance. Sarjana thesis, University of Barcelona, Barcelona, Spain. [Google Scholar]

- Waheed, Hajra, Saeed-Ul Hassan, Naif Radi Aljohani, and Muhammad Wasif. 2018. A Bibliometric Perspective of Learning Analytics Research Landscape. Behaviour & Information Technology 37: 10–11. [Google Scholar] [CrossRef]

- Wang, Fanyi, Ruobing Zhang, Faraz Ahmed, and Syed Mir Muhammed Shah. 2021. Impact of Investment Behaviour on Financial Markets during COVID-19: A Case of UK. Economic Research-Ekonomska Istraživanja 2021: 1–19. [Google Scholar] [CrossRef]

- White, H. D., and K. W McCain. 1989. Bibliometrics. Annual Review of Information Science and Technology 24: 119–86. [Google Scholar]

- Xong, Lim Jin, Lim Jin Xong, and Ho Ming Kang. 2019. A Comparison of Classification Models for Life Insurance Lapse Risk. International Journal of Recent Technology and Engineering 7: 245–50. [Google Scholar]

- Yacob, Rubayah, Mohd Hafizuddin Bangaan Abdullah, and Norasykeen Mohd Baharom. 2018. Analisis Polisi Luput Pelan Takaful Keluarga. Journal of Muamalat and Islamic Finance Research 15: 109–24. [Google Scholar] [CrossRef]

- Yakob, Rubayah, B.A.M. Hafizuddin-Syah, and Nurfarhana Hani Badrul Hisham. 2019. Demographic Analysis towards the Understanding of Education Takaful (Islamic Insurance) Plan. Malaysian Journal of Society and Space 15: 92–105. [Google Scholar] [CrossRef]

- Yong, Jeffery. 2020. Insurance Regulatory Measures in Response to COVID-19. FSI Briefs No. 4. Financial Stability Institute. Available online: www.bis.org/emailalerts.htm (accessed on 30 December 2021).

- Yu, Lu, Jiang Cheng, and Tzuting Lin. 2019. Life Insurance Lapse Behaviour: Evidence from China. Geneva Papers on Risk and Insurance: Issues and Practice 44: 653–78. [Google Scholar] [CrossRef]

- Zakaria, Rahimah, Aidi Ahmi, Asma Hayati Ahmad, and Zahiruddin Othman. 2021. Worldwide Melatonin Research: A Bibliometric Analysis of the Published Literature between 2015 and 2019. Chronobiology International 38: 1–11. [Google Scholar] [CrossRef]

Figure 1.

Flow diagram of the research process. Source: author’s extraction from Scopus using framework proposed by Zakaria et al. (2021).

Figure 1.

Flow diagram of the research process. Source: author’s extraction from Scopus using framework proposed by Zakaria et al. (2021).

Figure 2.

The life insurance lapsation publication trend and total mean citations of articles annually from 1990 until 2021.

Figure 2.

The life insurance lapsation publication trend and total mean citations of articles annually from 1990 until 2021.

Figure 3.

The most productive authors.

Figure 4.

Authors’ co-citation network visualisation.

Figure 5.

Network visualisation map of international co-authorship.

Figure 6.

Author keyword co-occurrences overlay visualisation in the life insurance lapse literature.

Figure 6.

Author keyword co-occurrences overlay visualisation in the life insurance lapse literature.

Figure 7.

Trend topics based on life insurance lapse title.

Figure 8.

(a) Thematic map for the period 1974–2019 (before COVID-19); (b) thematic map for the period 2020–2021 (after COVID-19).

Figure 8.

(a) Thematic map for the period 1974–2019 (before COVID-19); (b) thematic map for the period 2020–2021 (after COVID-19).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Document type from journal.

| Document Type | Frequency | Percentage (n = 373) |

|---|---|---|

| Article | 151 | 84.40 |

| Conference paper | 13 | 7.30 |

| Review | 7 | 3.90 |

| Book | 4 | 2.20 |

| Book chapter | 3 | 1.70 |

| Total | 178 | 100.00 |

Table 2.

Top ten authors in the co-citation network of the author cited in the life insurance literature ranked by the total link strength.

Table 2.

Top ten authors in the co-citation network of the author cited in the life insurance literature ranked by the total link strength.

| Author | TLS | NL | Citations | Cluster |

|---|---|---|---|---|

| Anna Rita Bacinello | 87.50 | 89 | 95 | 2 |

| Anders Grosen | 84.93 | 90 | 90 | 2 |

| Peter Lohte Jørgensen | 59.14 | 86 | 65 | 2 |

| Martin Eling | 48.56 | 87 | 51 | 1 |

| Chenghsien Tsai | 47.58 | 89 | 49 | 1 |

| Weiyu Kuo | 44.33 | 89 | 45 | 1 |

| Eduardo Schwartz | 43.83 | 72 | 47 | 2 |

| Nadine Gatzert | 40.67 | 87 | 43 | 1 |

| Xavier Milhaud | 40.13 | 72 | 44 | 1 |

| Alexander Kling | 39.74 | 87 | 41 | 3 |

TLS = total link strength; NL = number of links.

Table 3.

Top ten countries in the co-authorship network ranked by the total link strength.

| Country | TLS | NL | Documents | Citations | Cluster |

|---|---|---|---|---|---|

| United States | 10 | 6 | 39 | 473 | 4 |

| Germany | 8 | 6 | 24 | 245 | 2 |

| China | 7 | 3 | 11 | 17 | 1 |

| Italy | 6 | 3 | 14 | 289 | 3 |

| Switzerland | 5 | 3 | 9 | 185 | 2 |

| Canada | 4 | 5 | 9 | 116 | 6 |

| France | 4 | 4 | 9 | 72 | 1 |

| Taiwan | 3 | 2 | 8 | 31 | 1 |

| United Kingdom | 3 | 2 | 8 | 234 | 3 |

| South Africa | 2 | 3 | 3 | 10 | 5 |

TLS = total link strength; NL = number of links.

Table 4.

Top ten highest-influence sources based on total citations.

| Journal | Country | TC | TP | CS | SJR | Quartile |

|---|---|---|---|---|---|---|

| Insurance: Mathematics and Economics | Netherlands | 493 | 20 | 2.7 | 1.139 | Q1 |

| Journal of Risk and Insurance | United Kingdom | 366 | 16 | 3.6 | 1.055 | Q1 |

| North American Actuarial Journal | United Kingdom | 129 | 8 | 1.6 | 0.936 | Q2 |

| Scandinavian Actuarial Journal | United Kingdom | 78 | 6 | 2.7 | 1.061 | Q1 |

| Journal of Banking and Finance | Netherlands | 106 | 3 | 4.4 | 1.58 | Q1 |

| Journal of Risk Finance | United Kingdom | 45 | 4 | 2.1 | 0.295 | Q3 |

| Risks | Switzerland | 27 | 5 | 1.4 | 0.403 | Q2 |

| Astin Bulletin | United Kingdom | 8 | 2 | 2.1 | 1.113 | Q1 |

| European Actuarial Journal | Switzerland | 18 | 3 | 1.4 | 0.661 | Q2 |

| Geneva Papers on Risk and Insurance: Issues and Practice | United States | 10 | 3 | 2.0 | 0.535 | Q2 |

TC = total citations; TP = total publications; CS = CiteScore 2020; SJR = SJR 2020; Q = quartile.

Table 5.

The top ten most cited documents based on the number of local citations.

| No. | Author(s) | Document Title | Source | LC | GC | NLC |

|---|---|---|---|---|---|---|

| 1 | Grosen and Løchte Jørgensen (2000) | Fair valuation of life insurance liabilities: The impact of interest rate guarantees, surrender options, and bonus policies | Insurance: Mathematics and Economics | 39 | 206 | 18.93 |

| 2 | Bacinello (2003b) | Fair valuation of a guaranteed life insurance participating contract embedding a surrender option | Journal of Risk and Insurance | 27 | 98 | 27.55 |

| 3 | Bacinello (2003a) | Pricing guaranteed life insurance participating policies with annual premiums and surrender option | North American Actuarial Journal | 22 | 61 | 36.07 |

| 4 | Grosen and Jorgensen (1997) | Valuation of early exercisable interest rate guarantees | Journal of Risk and Insurance | 20 | 62 | 32.26 |

| 5 | De Giovanni (2010) | Lapse rate modelling: a rational expectation approach | Scandinavian Actuarial Journal | 18 | 31 | 58.06 |

| 6 | Outreville (1990) | Whole-life insurance lapse rates and the emergency fund hypothesis | Insurance: Mathematics and Economics | 17 | 40 | 42.50 |

| 7 | Bacinello (2005) | Endogenous model of surrender conditions in equity-linked life insurance | Insurance: Mathematics and Economics | 15 | 36 | 41.67 |

| 8 | Steffensen (2002) | Intervention options in life insurance | Insurance: Mathematics and Economics | 13 | 28 | 46.43 |

| 9 | Jensen et al. (2001) | A finite-difference approach to the valuation of path-dependent life insurance liabilities | The Geneva Papers on Risk and Insurance Theory | 13 | 51 | 25.49 |

| 10 | Eling and Kiesenbauer (2014) | What policy features determine life insurance lapse? An analysis of the German market | Journal of Risk and Insurance | 12 | 34 | 35.29 |

LC = local citations; GC = global citations; NLC = normalised local citations.

Table 6.

Latest documents published in 2020 and 2021 in life insurance lapse cited at least once.

| Author(s) | TC | Title | Method(s) | Variable(s) | Main Result(s) | Recommendation(s) |

|---|---|---|---|---|---|---|

| Hu et al. (2021) | 5 | A spatial machine learning model for analysing customers’ lapse behaviour in life insurance | Spatial analysis and logistic regression | Sum assured, age, duration, gender, total number of policies, number of lapsed policies, household composition, education level, employment status | Adding census clustering at the local population level to the company’s current internal data does not improve lapse prediction. | Use a larger dataset such as an all-Ireland dataset to understand the relationship between cluster characteristics and policyholder lapse behaviour. |

| Falden and Nyegaard (2021) | 4 | Retrospective reserves and bonus with policyholder behaviour | Markov model | Age of policyholder, age of retirement, termination, premium, annuity, term insurance | The study derives accurate differential equations for the state-wise projections of the savings account and surplus with the optimal free-policy factor where all benefits are governed by bonus. However, it fails to predict the savings account and surplus with an optimal free-policy factor when policyholder behaviour is considered. | Adding a more complex dividend strategy to the model and allowing for dependencies on assets and market values. Another research topic is, How to determine the best dividend approach in a multi-state setting? |

| Fang and Wu (2020) | 4 | Life insurance and life settlement markets with overconfident policyholders | Utility function | Income, health status, bequest motives, preference, timing, commitment, and contracts | When overconfident consumers are sufficiently susceptible to strong intertemporal consumption substitution elasticity, a life settlement market may raise their equilibrium welfare. | Should experimentally test the existence of policyholder overconfidence based on the predictions in this study. Study the settlement market’s welfare consequences in a unified framework where lapsation is driven by both bequest motive and negative income shocks. |

| Fang and Kung (2020a) | 4 | Life insurance and life settlements: The case for health-contingent cash surrender values | Utility function | Income, health status, bequest motives, timing, commitment, and contracts | The consumer welfare loss induced by the settlement market can be partially mitigated by optimally determining cash surrender values, but only if the cash surrender values are allowed to be conditional on health status. | - |

| Cole and Fier (2021) | 3 | An examination of life insurance policy surrender and loan activity | Logistic regression | Major expenses, income drop, expenditure, unemployment, late loan, credit status, net worth, inflation, marital status, age, number of children | While some overlaps in the circumstances cause families to use their cash value policies to attain some goal(s), households perceive surrenders and loans as separate activities. | - |

| Carson et al. (2020) | 3 | Sunk costs and screening: Two-part tariffs in life insurance | Cox proportional hazard model | Backdate, days after birthday, lapse, face amount, annual premium, days in force | Even when correcting for arbitrary nonlinearity in premium effects on lapse proclivity, life insurance clients demonstrate behaviour consistent with the sunk cost fallacy in their lapsing behaviour. | Further studies on the optimal menu of contracts. |

| Adams et al. (2020) | 2 | Managing policy lapse risk in Sweden’s life insurance market between 1915 and 1947 | Panel data | Unemployment, wage growth, interest rate, pension, regulation, new policies, firm size, organisation form, policy size, age, death rate, lapse total, cash surrender, surrender, expense cash, dividends, bonus | The findings support previous emergency fund tests and interest rate explanations for voluntary life insurance policy cancellations. | - |

| Biagini et al. (2021) | 1 | Estimating extreme cancellation rates in life insurance | Dynamic peaks-over-threshold (POT) | Direct written premium, policies lapsed, policies surrendered, policies lost, policies issued, policies revived, policies assumed, term life in force, permanent life in force, total in force, share of term policies, share of issued policies, interest rate changes, cancellation rates | There is a positive relationship between new company activity and high cancellation rates. There is no correlation between interest rate changes and high cancellation rates. | Future research should use the dynamic POT approach on a larger dataset to examine the mass cancellation scenario in the German market by product category. Further research using different periods. |

| Barucci et al. (2020) | 1 | The determinants of lapse rates in the Italian life insurance market | Generalised linear modelling and survival analysis | Age, contract age, contract size, product type, gender, premium frequency, region, profession, inflation rate, growth rate of disposable income, growth rate of the European stock index | There is modest evidence supporting the Interest Rate Hypothesis, a positive link between interest and lapse rates, for contracts signed a few years ago. Instead, some data suggest that lapse rates are linked to personal financial/economic issues (the emergency fund hypothesis). | - |

| Hong (2020) | 1 | The effect of life insurance settlement on insurance market and consumer welfare | Utility function | The introduction of settlement can enhance insurance demand and customer welfare even when the trading cost is higher than the liquidity cost. The monopolistic insurer can either boost or decrease insurance demand depending on the population distribution and policyholders’ liquidity risk. | - |

TC = total citations.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Shamsuddin, S.N.; Ismail, N.; Roslan, N.F. What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis. Risks 2022, 10, 97. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050097

AMA Style

Shamsuddin SN, Ismail N, Roslan NF. What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis. Risks. 2022; 10(5):97. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050097

Chicago/Turabian StyleShamsuddin, Siti Nurasyikin, Noriszura Ismail, and Nur Firyal Roslan. 2022. "What We Know about Research on Life Insurance Lapse: A Bibliometric Analysis" Risks 10, no. 5: 97. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10050097

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.