1. Introduction

Recently emerging literature has identified that stock markets reacted negatively to the COVID-19 outbreak. More specifically, this literature points out that stock market returns declined as laboratory-confirmed cases of COVID-19 increased (

Al-Awadhi et al. 2020;

Ashraf 2020b). This finding is puzzling in the context of the US stock market, which is considered a benchmark worldwide. As shown in

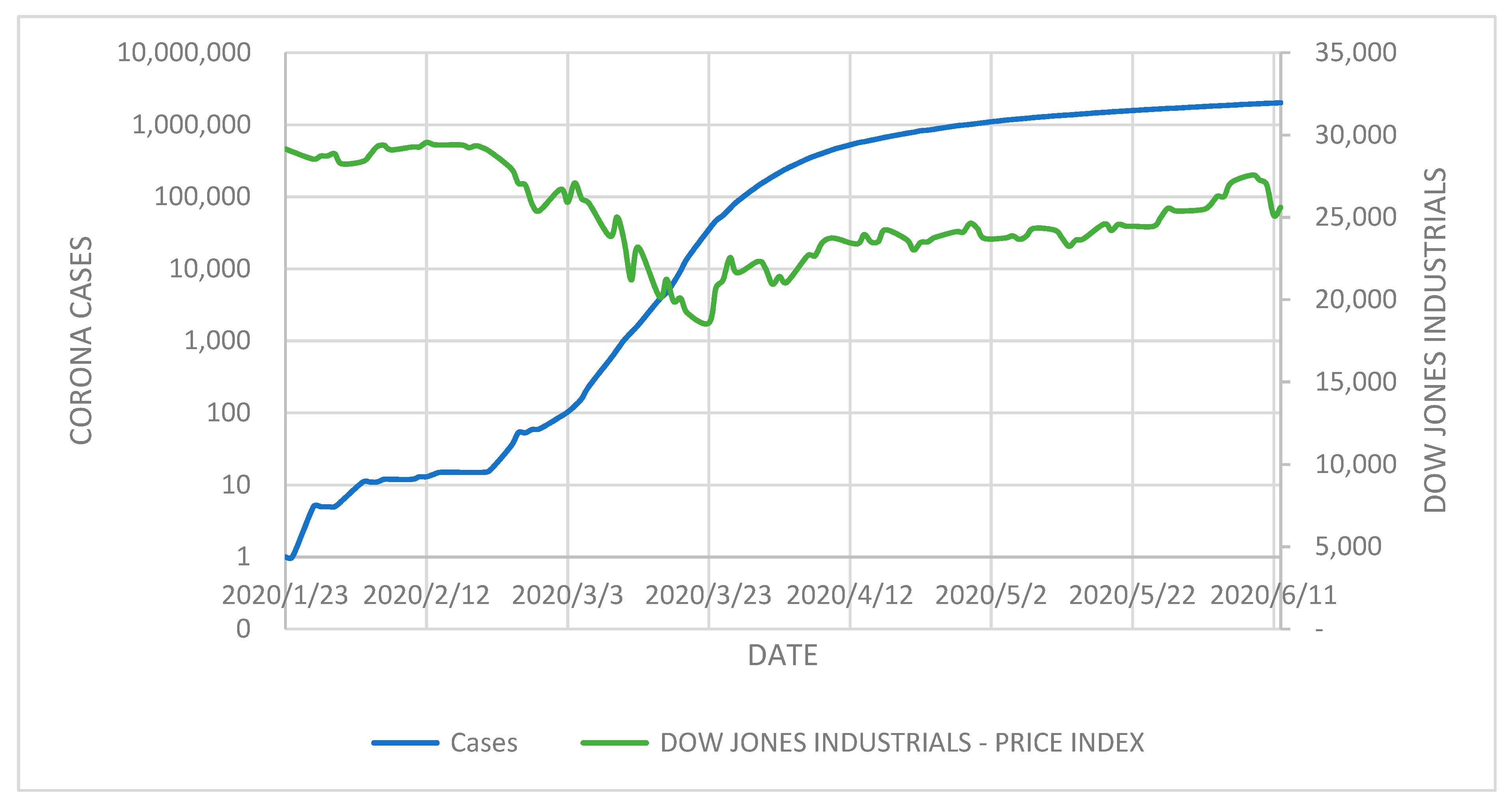

Figure 1, the Dow Jones Industrial Index (DJII from hereafter) was going up in mid-February when confirmed cases of COVID-19 in the US were also on the rise. Further in this regard,

Onali (

2020) fails to find evidence that both the DJII and S&P 500 index reacted negatively to the numbers of confirmed COVID-19 cases and deaths in the US.

One potential reason might be investors’ lack of attention in the early days of the outbreak. Extensive literature sheds light on the relationship between investors’ attention and stock markets. This literature largely suggests investors’ attention has a significant effect on different aspects of the stock market, including trading volume (

Vlastakis and Markellos 2012), market volatility (

Andrei and Hasler 2015) and stock returns both at an individual stock level (

Da et al. 2011) and aggregate level (

Vozlyublennaia 2014).

Huberman and Regev (

2001) explore that it is the investors’ attention after which prices react to any new information. They show that investors’ attention to already available information can increase share prices. In

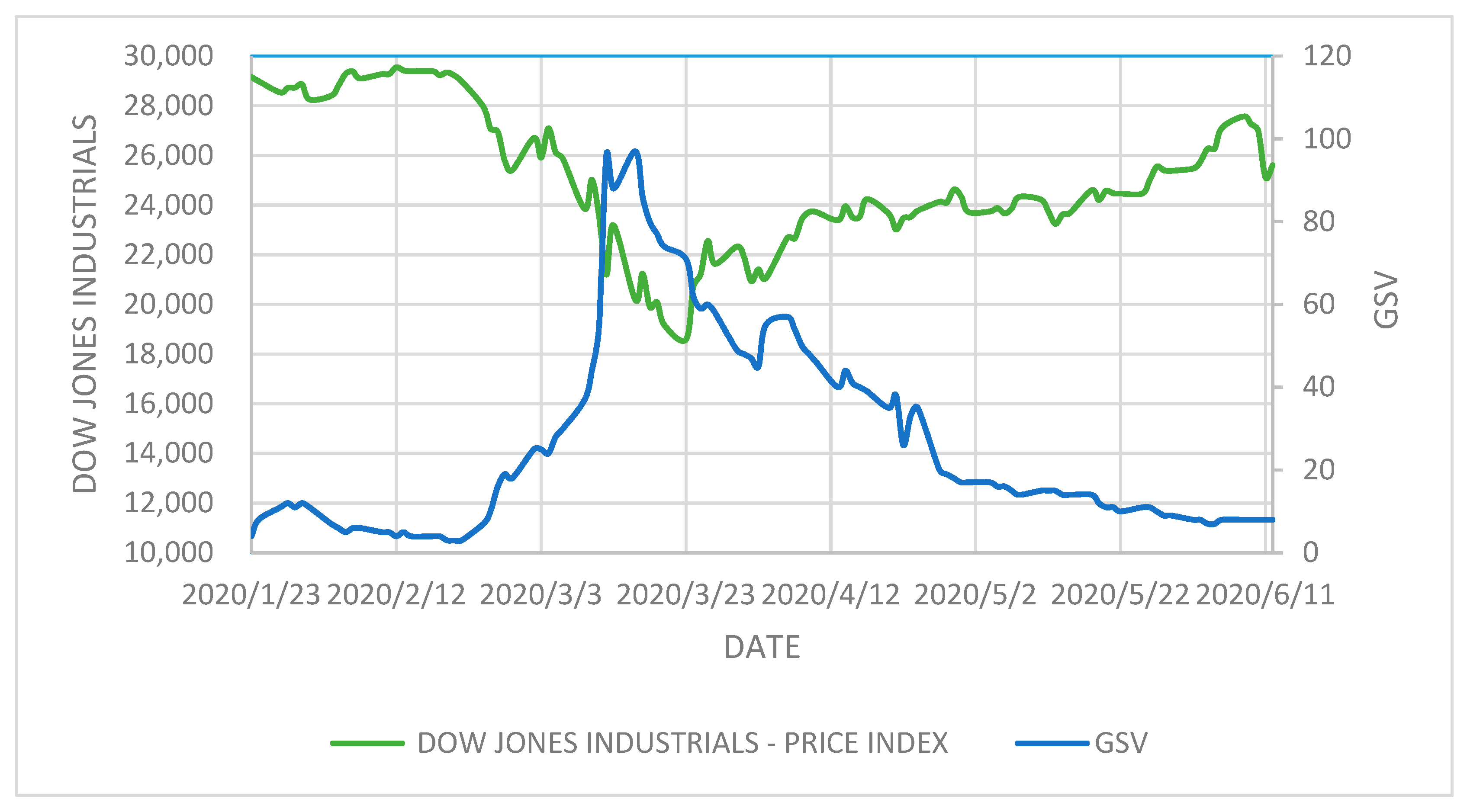

Figure 2, we draw the DJII with Google search volume (GSV from here after) of the word “coronavirus”. It is evident from

Figure 2 that the market moved more closely with the Google searches. The DJII started declining when searches started increasing at the end of February, was off to its lowest value after the searches peaked in mid-March and started recovering after the decline in search volume.

Motivating from this general observation from the benchmark financial market, in this paper, we aim to examine whether and how investors’ attention to COVID-19 has influenced market returns. Further building on

Ashraf (

2020c), who finds that the national culture of investors has a strong bearing on how investors reacted to the COVID-19 shock, we examine whether the relationship between investors’ attention and stock returns is moderated by investors’ level of uncertainty avoidance.

Using data from 34 countries over the period January 23 to June 12, 2020, first we found evidence that investors’ attention has a negative impact on stock returns. Next, using an interaction term between investors’ attention and an uncertainty avoidance variable, we found that the negative impact of investors’ attention on stock market returns is stronger in countries where the level of uncertainty avoidance of investors is higher.

This study makes a three-fold contribution. First, it augments the literature focusing on the relationship between investors’ attention and stock markets. In this vein,

Da et al. (

2011) propose GSV as a new proxy for investor attention and found its significant impact on stock prices and performance of initial public offering (IPO) stocks.

Yuan (

2015) found a significant impact of market-wide attention events on stock returns.

Andrei and Hasler (

2015) theoretically and empirically link attention and uncertainty to stock prices.

Peltomäki et al. (

2018) found that investors’ attention influences stock market volatility.

Swamy et al. (

2019) investigate whether investors’ attention (proxied by GSV) plays a role in stock returns forecasting or not in an emerging market and found a significant impact of investors’ attention on stock returns. We add to these studies by examining the impact of investors’ attention to an exogenous health crisis, which has economic consequences through human costs and social distancing measures, on stock market returns. Overall, we show that enhanced investors’ attention to the pandemic has resulted in declined stock market returns.

Second, it adds to the evolving literature on COVID-19 and the stock market relationship.

Goodell (

2020) reviews the literature encompassing the economic and financial impact of diseases and suggests that COVID-19 is likely to have an important impact on the functioning of financial markets. Other studies have examined the impact of COVID-19 on stock returns (

Panyagometh 2020;

Butt et al. 2020), risk and volatility (

Zhang et al. 2020), stability and sequential irregularity (

Lahmiri and Bekiros 2020), industry’s returns dependence and the structure of the risk-return relationship (

AZİMLİ 2020), the market crash in March 2020 (

Mazur et al. 2020), fractal contagion effect among stock markets (

Okorie and Lin 2020), returns of companies sharing the name “corona” (

Corbet et al. 2020) and changes in investment, fiscal and export multipliers due to the COVID-19 pandemic (

Derkacz 2020). We contribute by analyzing whether investors’ enhanced attention to COVID-19, measured with the Google search volume of the word “coronavirus”, affects stock market returns.

Lastly, we add to the recent literature that explores that national characteristics influence the Covid–stock relationship. Recent studies find that national characteristics can moderate this relationship. For instance,

Ashraf (

2020c) explores that national culture, proxied with the level of uncertainty avoidance, acts as a moderator in the COVID-19 confirmed cases and stock market returns relationship.

Ashraf (

2020a) shows that stringent government social distancing policies weaken the negative association between COVID-19 confirmed cases and stock market returns.

Erdem (

2020) finds the moderating effect of economic freedom on the Covid–stock relationship. Extending this literature, we examine whether the national culture, proxied with the level of uncertainty avoidance, acts as a moderator in the investors’ attention and stock market returns relationship. Moreover, our study also augments the literature that focuses on COVID-19 in the cultural context (e.g.,

Monica-violeta et al. 2020).

The rest of the paper is arranged as follows. The next section discusses the relevant literature and presents hypotheses.

Section 3 outlines the data and empirical model.

Section 4 presents the results and discussion. The last section concludes the study.

4. Results and Discussion

Table 1 presents the summary statistics for our variables. The RSE (i.e., stock market returns) variable shows negative returns, which indicates markets declined during our sample period. The minimum and maximum values are indicating large dispersions in stock returns, which is quite understandable due to the large fluctuations during the sample period. The high standard deviation value of GSV indicates large fluctuations in investors’ attention during the sample period.

Table A5 in

Appendix A presents summary statistics for individual countries.

Table 2 presents a pairwise correlation analysis for all the variables included in the analysis. Our main variable, GSV, is negatively and significantly correlated with stock returns. Other variables also show a negative correlation with returns of stock markets.

Table 3 presents the main results of the panel regression analysis. The first model (1) is the baseline specification where we include the cases growth variable only. Cases growth has significant and negative impact on stock returns, a finding that is consistent with recent studies (

Al-Awadhi et al. 2020;

Ashraf 2020b) and validates our model for further analyses.

Model (2) is the main specification to test the first hypothesis. It is evident that a change in GSV has a significant and negative impact on stock returns, suggesting that an increase in investors’ attention results in lower stock market returns. This finding is in line with

Dzielinski (

2012) and

Yuan (

2015). The finding is also in line with our assumption that selling pressure is more likely to prevail in the market due to the high uncertainty generated by COVID-19. The finding contradicts the attention theory of

Barber and Odean (

2008), which states that increased investors’ attention generates buying pressure. We argue that due to the deteriorating situation in stock markets around the globe, the probability of new buyers entering the market decreased during COVID-19. Hence, existing shareholders become more active due to increased attention and they sold their holdings due to the dispositions effect or rebalancing needs in accordance with the proposition of

Yuan (

2015). Uncertainty avoidance enters the negative, though is insignificant, showing that investors in countries with higher uncertainty avoidance are selling shares at relatively lower prices.

Model (3) presents the results where we include an interaction term. The interaction term is significant and negative suggesting that the negative impact of growth in investors’ attention on stock market returns is stronger for countries with higher uncertainty avoidance. These findings validate our second hypothesis, that national culture plays a moderating role in the investors’ attention and stock market relationship.

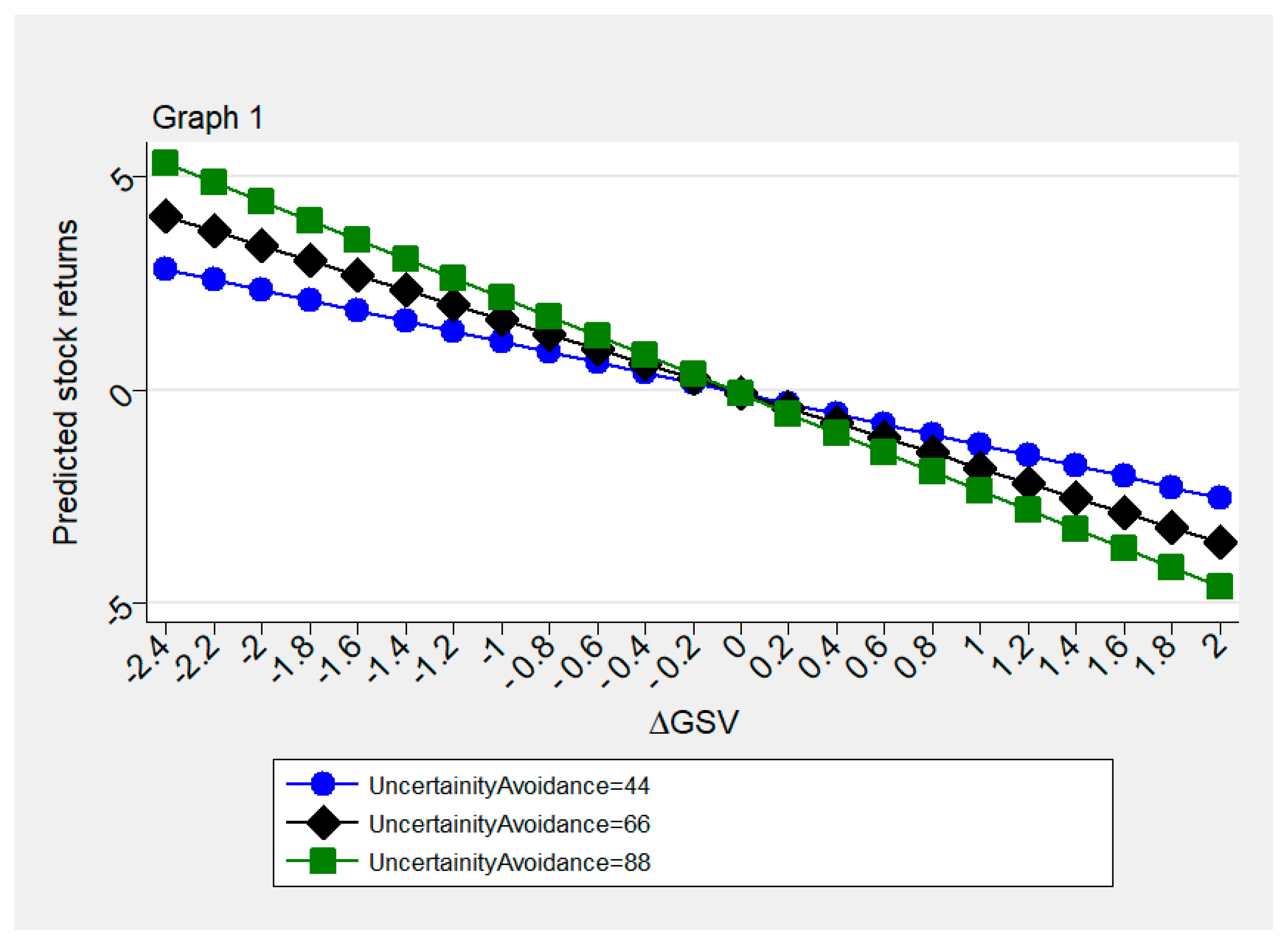

To further elaborate this moderation effect, we present the relationship between the stock market and investors’ attention by drawing a graph (

Figure 3) from Model (3) and

Table 3. The graph is formulated by using the mean and ±1 standard deviation of ∆GSV and stock returns. The line (L2) with the embedded rhombus depicts a mean value for the uncertainty avoidance index, while the line (L1) with embedded circles represents the lower values of the index and line (L3) with the embedded squares represents the highest values of the uncertainty avoidance index. All the lines are downward sloped, which shows that stock returns and investors’ attention has a negative relationship. As we move from L1 to L3 we can observe that lines are becoming steeper (L1) to the steepest (L3). This implies that the negative relationship between investors’ attention and stock returns is getting stronger as uncertainty avoidance is increasing. Thus, we can conclude that investors’ attention has a more negative impact on stock returns for countries with higher uncertainty avoidance. Considering that people in countries with high uncertainty avoidance like to mitigate uncertainty on priority basis, it is understandable that such investors are lured towards selling their shares to reduce the uncertainty caused by COVID-19.

We use several robustness checks for our estimated results. At first, we used two global factors as additional control variables to control for global equity and volatility factors that can influence stock returns. The first factor is the All Countries World Index (ACWI) by Morgan Stanley Capital International (MSCI). It is the flagship global equity index of MSCI, and it represents the set of large- and mid-cap stocks across 23 developed and 26 emerging markets. As of December 2019, it covers more than 3000 constituents across 11 sectors and approximately 85% of the free float-adjusted market capitalization in each market. The index has been used as a benchmark for global equity markets in previous studies as well (e.g.,

García Petit et al. 2019). The second factor is the Volatility Index (VIX) of the Chicago Board Options Exchange (CBOE). The CBOE has computed the index since 1993 “to measure market expectations of the near-term volatility implied by stock index option prices” (

Fernandes et al. 2014). Previous studies e.g.,

Marfatia (

2020) suggest that the VIX has a significant impact on the US and other leading stock markets.

Table A4 in

Appendix A presents results after controlling for these global factors. The results are largely consistent with our main findings in

Table 3.

As a second robustness check, we used random effect panel analysis. Specifically, we re-estimated all models of

Table 3 with a panel random-effects model.

Table A5 in

Appendix A presents the results for this analysis. Column 1 shows results for cases growth as an independent variable. Columns 2 and 3 present results without and with an interaction term, respectively. The findings are consistent with our previous findings in

Table 3.

5. Conclusions

We investigated the relationship between investors’ attention and stock market returns during the COVID-19 pandemic. To proxy investors’ attention, Google search volume (GSV) data from Google Trends is used. The motivation behind using this measure lies in the literature, which supports that this measure provides timely and action-oriented behavior of investors. For empirical analysis, we used daily data from 34 countries over the period January 23 to June 12, 2020. We found that investors’ higher attention to COVID-19 led to negative market returns. These findings contradict the attention theory (i.e.,

Barber and Odean 2008;

Da et al. 2011) which predicts a positive relationship between investors’ enhanced attention and stock market returns based on the notion that an increase in investors’ attention increases share prices and hence returns. However, our findings are in line with the results of

Yuan (

2015), who argues that attention theory is more applicable to new investors, and existing investors increase selling due to the disposition effect or portfolio rebalancing needs.

We further extended our analysis by including uncertainty avoidance as a moderating variable. Our findings from this analysis show that national culture as measured by the uncertainty avoidance index has a significant moderating effect on the relationship between investors’ attention and stock market returns. These findings suggest that national culture is an important factor for determining the stock market and investors’ attention relationship.

Overall, our findings have important implications for attention theory by showing that investors’ enhanced attention to an adverse shock, even one that originates in the health sector, leads to negative returns in financial markets. Our analysis suggests enhanced attention would not always lead to positive returns especially if attention increases during the crisis. Further, the influence of cultural values of individuals cannot be neglected even though investors try to base their decisions on more sophisticated information collection by paying higher attention.

One limitation of this study is that our proxy of GSV just considers the term “coronavirus” while several other terms, such as COVID-19, have also been widely used during the pandemic. Future research may construct a more comprehensive proxy of investors’ attention.

{kind=link}

{kind=link}

{kind=link}