4.2. Results of Case Study 1

In this first case study, we assess our methodology when investigating whether a pooled data source is representative when considering the enrichment of internal data with pooled data in developing a LGD model for regulatory purposes. The proposed methodology aims at assessing the premise of whether the data set in question (Data set Q) is representative with respect to a base data set (Data set B). First, we define Data set Q and Data set B.

We commence by using the SA GCD data set and applied several exclusions. We exclude all observations before the year 2000 and after 2015, as well as the observations from asset classes other than large corporates and SMEs. We only use observations where the LGD is between −0.01 and 1.5. The summary statistics of this generated SA LGD data set that we use in our modelling are displayed in

Table 2.

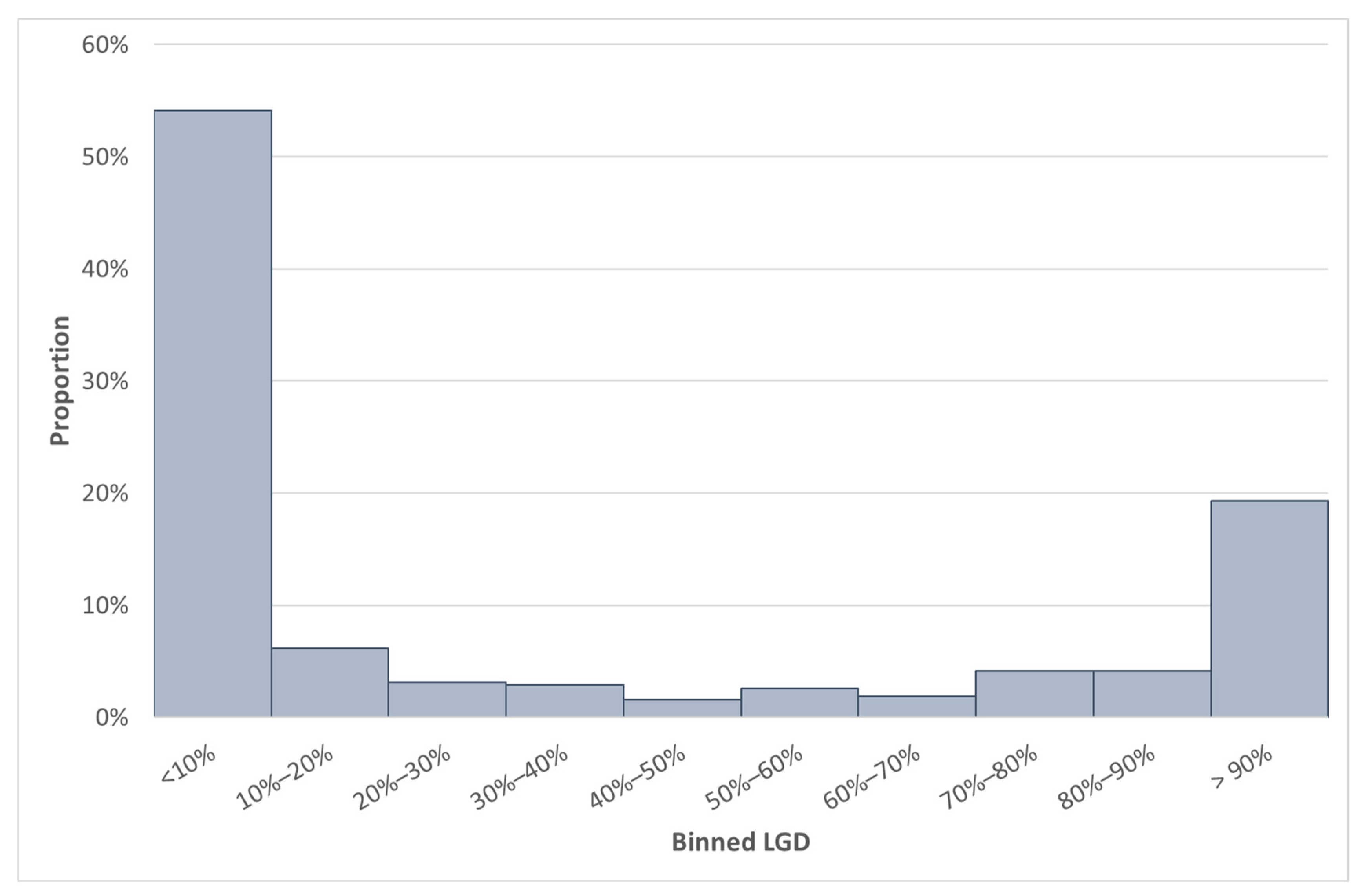

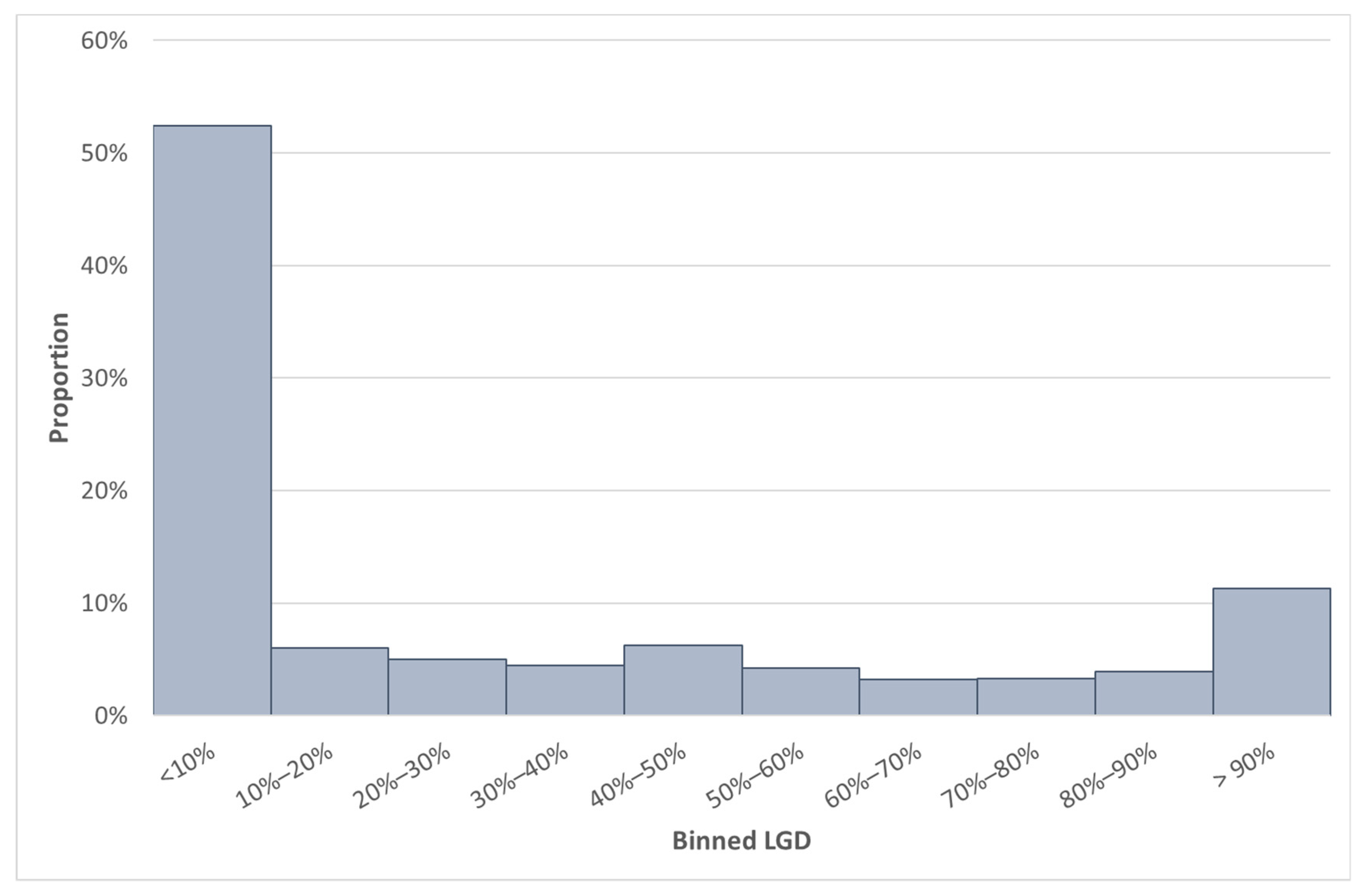

Going forward, we will consider this SA GCD LGD data set, which contains 3831 observations. Due to the confidential nature of some information in the data set, not all the details can be provided. The difference between the median and average LGD for South Africa was 26.04%. The large difference between the mean and the median can be explained by the bimodal distribution of the LGD data, which is also positively skewed (see

Figure 2). Furthermore, the standard deviation of the LGD variable in the SA GCD data set was 0.4. The LGD values of the SA GCD data set are depicted in

Figure 2. The typical distribution of LGD is expected to be a bimodal distribution (

GCD 2018;

Riskworx 2011).

In the GCD data set we used, it is possible to identify the country of origination of a loan, but the identity of the specific bank is protected

1. To “synthetically create” a bank’s internal data, we used a 25% random sample from the SA GCD data set, representing a hypothetical SA bank, say ABC Bank. This resulted in a sample of 958 observations from the original 3831 observations in the SA GCD LGD data. The remaining 2873 observations will then be regarded as the data set in question (Data set Q).

The ideal situation would have been to use an actual bank’s internal data and not just a random sample, as described above. This case study, however, aims to illustrate the methodology. We will assume that ABC Bank is considering building a LGD model with only internal data or augmenting their internal data with the pooled data set created as described above. If ABC Bank wants to augment their internal data with this pooled data when developing a regulatory model, they need to assess whether the pooled data set is representative. ABC Bank’s internal data will be the base data (i.e., Data set B), and the SA GCD data will be the data set to be assessed for representativeness (Data set Q). We will illustrate the proposed methodology from the perspective of ABC Bank.

Step 1: Split the base data set (Data set B) into one part for developing a model, namely Data set BB (Base Build), and another part to evaluate the model that was build, say, Data set BT (Base Test).

We split ABC Bank’s data set randomly into an 80% build data set (Data set BB with 767 observations) and a 20% test data set (Data set BT with 191 observations). We will use the Data set BB to build a model (Step 2), and we will evaluate the model performance on the test data set (Data set BT) in Step 4. We will build a second model (Step 3) on the augmented data set (but excluding the test data of ABC Bank), i.e., build a model on Data set Q + BB. This results in 3640 observations, either by calculating 3831 − 191 = 3640 (SA GCD data set less Data set BT) or 2873 + 767 = 3640 (Data set Q + BB). We will evaluate both models on the test data set of ABC Bank, Data set BT (Step 4), as shown in

Figure 3.

Step 2: Build a model on Data set BB (Base Build).

A linear regression model was fitted to the build data set of ABC Bank’s data (Data set BB), using LGD as the dependent variable. The underlying assumptions, as stated in

Section 4.1, were checked and found satisfactory. Only five of the six predictor variables (discussed above) were statistically significant at a level of 5%. The results are shown in

Table 3. One exception was made with the variable Facility type when fitting the model on ABC bank’s data. For this variable, the

p-value was 8%, and the variable was not excluded from the regression, since the literature confirmed that the variable is an important LGD driver. Furthermore, in all other analyses (see

Table 4 and

Section 4.3), this variable (Facility type) had a

p-value of less than 1%.

The R-squared statistic was 32.68%. This value indicates that 32.68% of the variance in LGD can be explained by the five variables. The adjusted R-squared statistic was 32.15%. R-squared values in these ranges are not uncommon for LGD models, as evident from

Loterman et al. (

2012), who reported R-squared values for LGD models in the range of 4–43%.

Step 3: Add the data set in question (Q) together with the base data set (BB) and build a model on this augmented data (Data set Q + BB).

Next, a linear regression was fitted on the Data set Q + BB (this is the SA GCD data set excluding the test data set of ABC Bank and contains 3640 observations). The results of this regression are shown in

Table 4. All six of the variables are statistically significant at the 5% level. The R-squared statistic was 32.16%, and the adjusted R-squared statistic was 32.05%.

Step 4: Evaluate the model performance (e.g., MSE) of these two models on the base test data set (Data set BT) and determine whether the model performance has improved or is similar using the following construct.

Step 4.1: Define as the MSE of Data set BT using the model build on Data set Q + BB and as the MSE of Data set BT using the model build on Data set BB.

The models fitted in Steps 2 and 3 were applied on the test data set of ABC Bank (191 observations, Data set BT), and the MSE results on both the build and test data are shown in

Table 5. The first subscript of the MSE indicates the development data set, and the second subscript indicates on what data set the MSE was calculated. The MPAI was also calculated for the instances where the development and test samples were not identical (

Taplin and Hunt 2019). When the MPAI is calculated for examples with identical data sets used during model development and testing, the MPAI will be equal to one, as evident in

Table 5.

Step 4.2: If the model developed on the augmented data has improved the model performance over the model developed only on the base data.

We observe that the is indeed smaller than and conclude that the model developed on the augmented data has improved the model performance. Optionally, we could have performed Step 5 to confirm the significance of the difference between and . The above results imply that, when using the augmented data in the development of the model, improved predictive accuracy of the internal observations (Data set BT) resulted. Based on this argumentation, Step 5 is not applicable in case study 1 due to the outcome of Step 4. We can then conclude that it is safe to continue using the SA GCD data for LGD model development and calibration for ABC Bank. This result is to be expected given the manner in which Data set B was constructed for ABC Bank, i.e., a random sample. The purpose of this case study, however, was to provide a step-by-step implementation guide on how a member bank of an external data provider could use our proposed methodology to assess representativeness.

The results from the MPAI indicate that the average variance of the estimated mean outcome at testing when developing the model using only Data set BB is lower than the average variance of the estimated mean outcome at development. Furthermore, the value of 0.86 is just outside our proposed threshold of 0.9 to 1.1, indicating that further investigation is required. This marginal difference between the conclusion drawn from our proposed technique and the MPAI could be expected as the MPAI was developed for a different objective than our methodology. This is potentially an indication that our proposed thresholds for the MPAI might be too strict, and further refinement might be required. On the positive side, the value indicates that the estimated mean variance of the response at testing is lower than at development. For the model developed on the augmented data (Data set Q + BB), the MPAI of 1.09 indicates that the average variance of the estimated mean outcome at testing is higher than at development but within our proposed range of 0.9 to 1.1, validating our conclusion.

4.3. Results of Case Study 2

In this case study, our proposed methodology is demonstrated with a slightly different aim: we consider which countries in the global GCD data set could be used to augment the SA GCD data in the case of LGD modelling.

Step 1: Split the base data set (Data set B) into subsets, with one subset for building a model, namely Data set BB (Base Build), and another subset to evaluate the model that was build, say, Data set BT (Base Test).

Using the methodology as described in

Section 3, we will use the SA GCD data set as the base data set (Data set B) split into an 80% build data set (Data set BB with 3065 observations) and a 20% test data set (Data set BT with 766 observations) to build a LGD model on Data set BB. We will then investigate another country on the GCD data set and append this country’s data (Data set Q) to the SA data set (Data set BB) and build a LGD model. We will evaluate these two models on Data set BT. We repeated this for all the countries available in the GCD data set. We considered 42 countries after the filters were applied based on a threshold of minimum facilities.

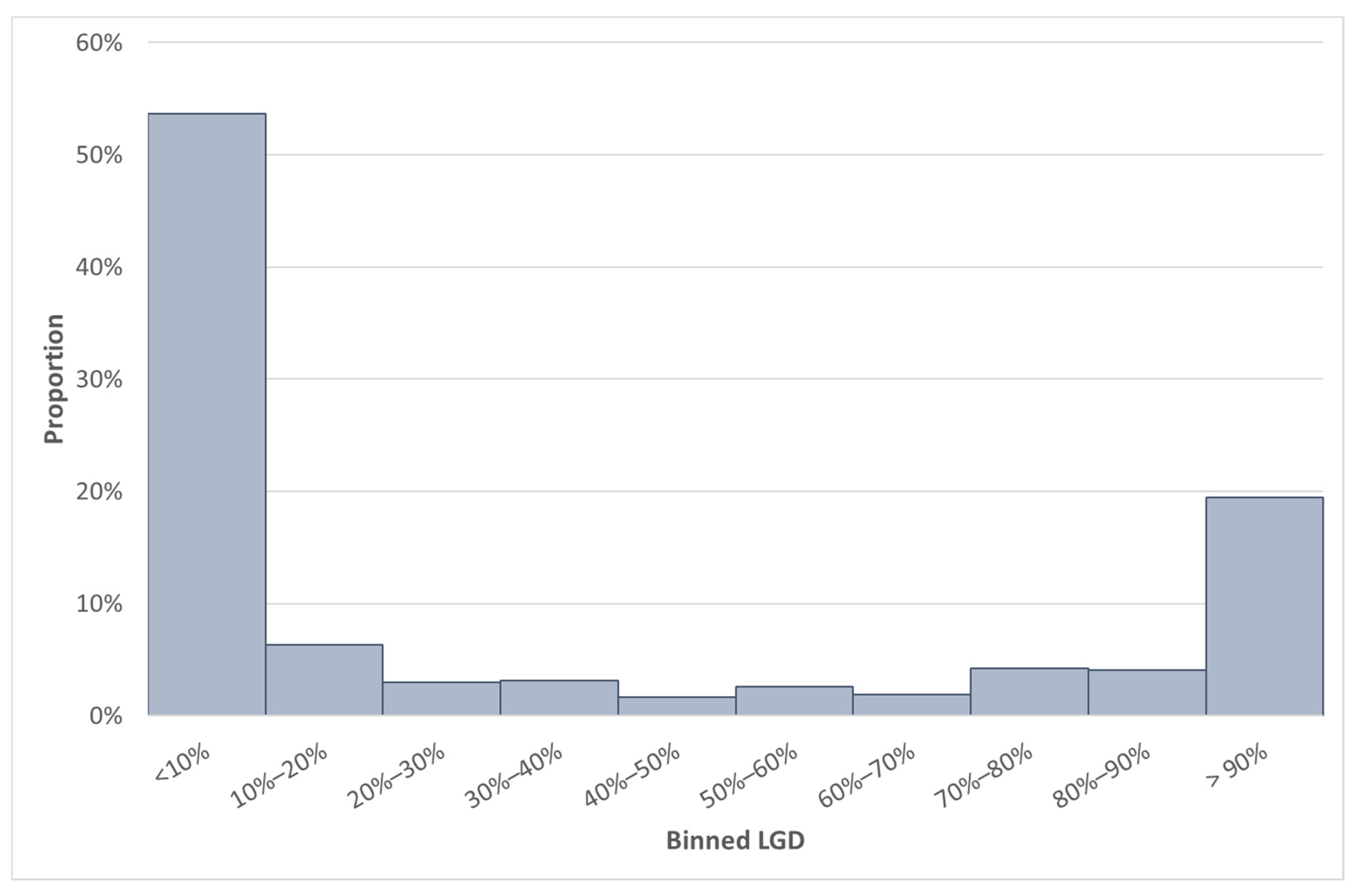

Some summary statistics of Data set BB are shown in

Table 6 and the distribution of the GCD LGD value (of Data set BB) in

Figure 4.

Step 2: Build a model on Data set BB (Base Build).

A linear regression model was fitted on the SA GCD build data set (Data set BB) after the independent variables were binned, quantified and the resulting binning info was applied to the SA test data set (Data set BT). Once more, all underlying model assumptions were acceptably adhered to. Five of the six variables were statistically significant at the level of 5%. The results are shown in

Table 7.

The R-squared value was 32.51%, and the adjusted R-squared value was 32.40%. Note that the results of Step 1 of case study 2 are comparable to the results of Step 2 of case study 1, as both used the SA GCD LGD data set. The difference, however, is that, for case study 1, the test data set of ABC Bank was excluded, and for case study 2, the test data set for SA was excluded.

Step 3: Add the data set in question (Q) together with the base data set (BB) and build a model on this augmented data (Data set Q + BB).

Next, a linear regression was fitted on the augmented data set. The augmented data set is the SA GCD build data set (Data set BB) and one country from the GCD data set (Data set Q). Note that, before fitting a linear regression, the independent variables were binned and quantified on Data set Q + BB, and the resulting binning info was applied to the SA test data set (Data set BT). We repeated this exercise and fitted linear regressions to each of the 42 countries.

We first display the expanded results of two countries: Country L in

Table 8 and Country AH in

Table 9. The reason for choosing these two countries is because Country L performed the best on the test results and Country AH performed the worst. We then present the abbreviated results of all 42 countries in

Table 10.

Considering Country L, the resulting augmented data set contained 3337 observations (3065 from SA build plus 272 from Country L). Five of the six variables were significant at a 5% level. The R-squared value was 28.26% and the adjusted R-squared value 28.14%, as observed in

Table 8.

Considering Country AH, the resulting augmented data set contained 21,645 observations (3065 from SA build plus 18,580 from Country AH). All six variables were significant at the 5% level. The R-squared value was 7.42% and the adjusted R-squared value 7.39% (much lower than previous models), as observed from

Table 9.

Step 4: Evaluate the model performance (e.g., MSE) of these two models on the base test data set (Data set BT) and determine whether the model performance has improved or is similar.

Step 4.1: Define as the MSE of Data set BT using the model build on Data set Q + BB and as the MSE of Data set BT using the model build on Data set BB.

The models fitted in Step 2 (one model, Data set BB) and Step 3 (42 models, Data set Q + BB) were applied to the test data set of the SA GCD LGD data (766 observations, Data set BT) in Step 4.

Step 4.2: If the model developed on the augmented data has improved the model performance compared to the model developed only on the base data.

The model developed in Step 2 resulted in and not one of the 42 models developed in Step 2 obtained MSE values () lower than this. However, many of the values were closely related to the of the model in Step 2.

Step 5: If , a dependent two-sample test (by comparing residual statistics) is performed to determine whether the model developed on the augmented data has a similar model performance to the model developed only on the base data. If the test concludes that the is not statistically different from the , we deduce that the model developed on the augmented data has a similar model performance than the model developed only on the base data.

In this step, we assess whether the model performances were statistically significantly different from one another. We created paired observations for the absolute error and paired observations for the squared error. The normality assumption for the

t-test was checked, and both the absolute error and the squared error followed a normal distribution. Using the paired

t-test, the observations were compared to see if the average errors were statistically different (i.e.,

p-value < 0.05). This was repeated for all 42 countries using both error statistics and is shown in

Table 10. We also calculated the test statistics and associated

p-values for the nonparametric tests (sign test and Wilcoxon signed-rank test). In all cases, similar conclusions followed based on the results of the nonparametric tests, and therefore, the results were omitted from

Table 10. Given the results, 12 countries were identified that had a

p-value of 0.05 and were greater on both the squared error and the absolute error, together with a MPAI value between 0.9 and 1.1. When considering either the squared error or the absolute error, some more countries were identified that could potentially be used to enrich the base data for model development and calibration. The highlighted cells in

Table 10 indicate either the absolute error or the squared error or where the MPAI signifies that the models developed on the augmented data (of these countries) have similar model performances compared to the models developed only on the base data. When focusing on MPAI values less than 0.9 (and greater than 1.1), there is an exact correspondence to our methodology where either the squared error or the absolute error has a

p-value less than 0.05. When changing the direction of comparison by inspecting the

p-values obtained from our proposed methodology, there are only three countries out of 42 where both the squared error and the absolute error had

p-values less than 0.05, with a corresponding MPAI value between 0.9 and 1.1 (i.e., conflicting results between our proposed methodology and the MPAI). This marginal difference between our proposed methodology and the MPAI could be expected, as we have already indicated that the MPAI was developed for a different objective than our methodology.

In summary, when considering the last three columns of

Table 10, 12 countries were found to have

that was not statistically different from the

, and we deduced that, for these 12 counties, the model developed on the augmented data (Data set Q + BT) had a similar model performance to the model developed only on the base data (Data set BB).

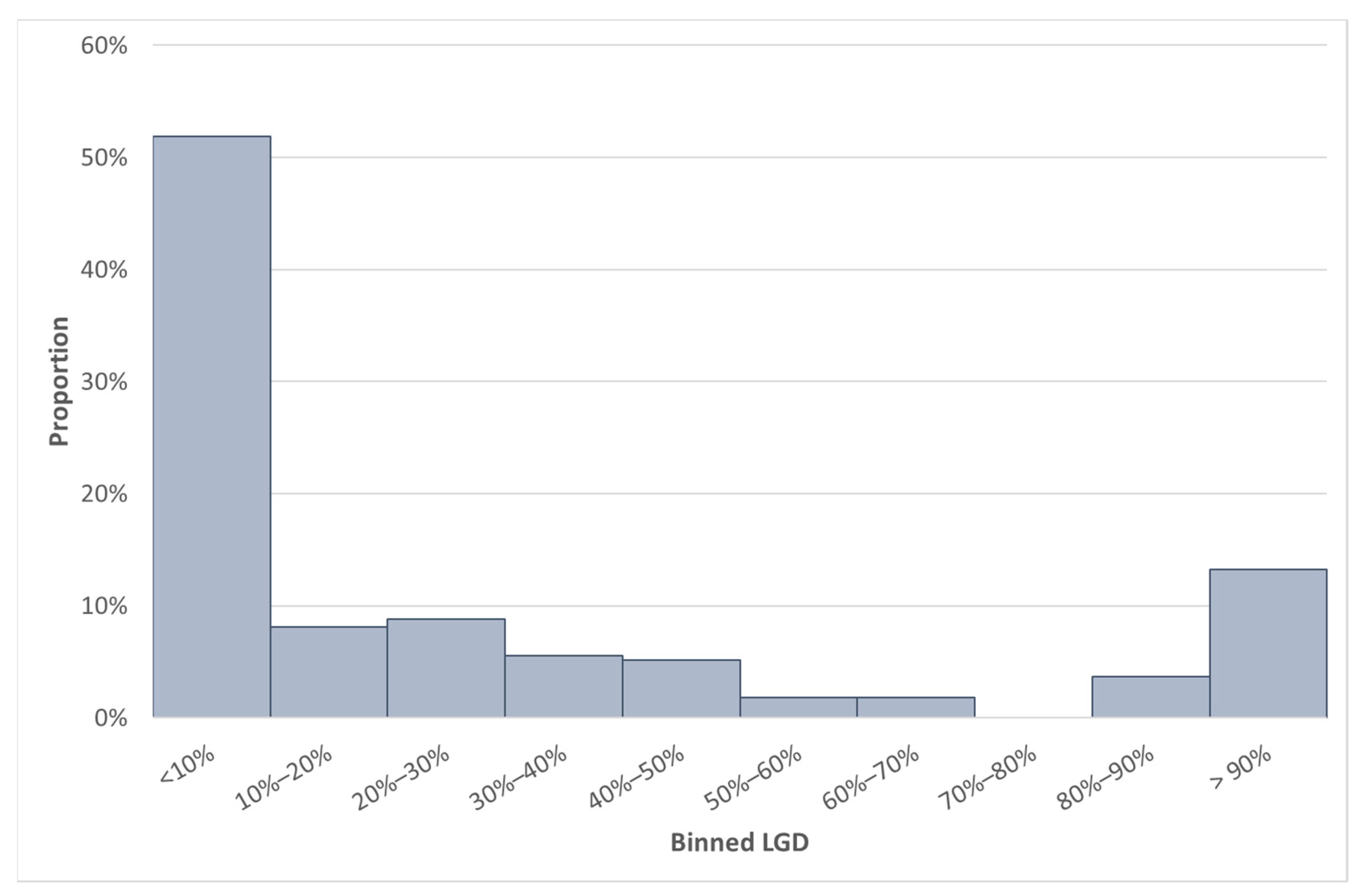

To use our methodology for calibration purposes, it is essential to observe the level of the LGD values. We first focus on Country L (the best-performing Country on the test data set). When comparing

Table 11 with

Table 6 and

Figure 4 with

Figure 5, we observed that Country L has a mean LGD value that is more than 10% lower compared to the mean SA LGD. However, the median LGDs of these countries are closely related.

Next, we compare the South African data with the worst-performing MSE. When comparing

Table 12 with

Table 6 and

Figure 4 with

Figure 6, we note that Country AH had 18,580 observations. We observed that Country AH has a mean (median) LGD value of 35.3% (7.4%). The mean LGD is lower than the SA mean LGD, but the median LGD are once more closely related.

The summary LGD statistics of all 12 countries that have an absolute and squared error that are not statistically different when compared to the SA data are provided in

Table 13.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}