Household Financial Situation during the COVID-19 Pandemic with Particular Emphasis on Savings—An Evidence from Poland Compared to Other CEE States

Abstract

:1. Introduction

2. The Course of COVID-19 Pandemic and Its Relation to the Economy

- The policy of closing economies saves human lives, but significantly reduces economic activity, and thus generates specific economic costs,

- Integrated epidemic and macroeconomic models provide a coherent framework for quantifying the costs and benefits of a policy to foreclose economies. Some of the benefits result from limiting the externalities that would arise if social distancing was voluntary,

- Policies with a lockdown of up to 30% of GDP may be preferred over an alternative with more casualties and a less severe recession.

- A significant drop in demand, which is primarily a consequence of restrictions in movement (both on a national and international scale),

- Disruptions in the supply chain (import of raw materials, semi-finished products, finished products), which is felt both nationally and internationally,

- Downtime caused by the suspension of the activity of some industries (e.g., catering, hotel, commercial), resulting from the introduced restrictions and infection of the staff,

- Unfavorable price changes,

- Significant deterioration of the financial situation of companies, as a consequence of the epidemic, as well as of their employees.

- Financial condition of households when the shock started,

- Effectiveness of political actions aimed at improving the financial situation of households,

- The speed with which the recovery in the labor market occurs.

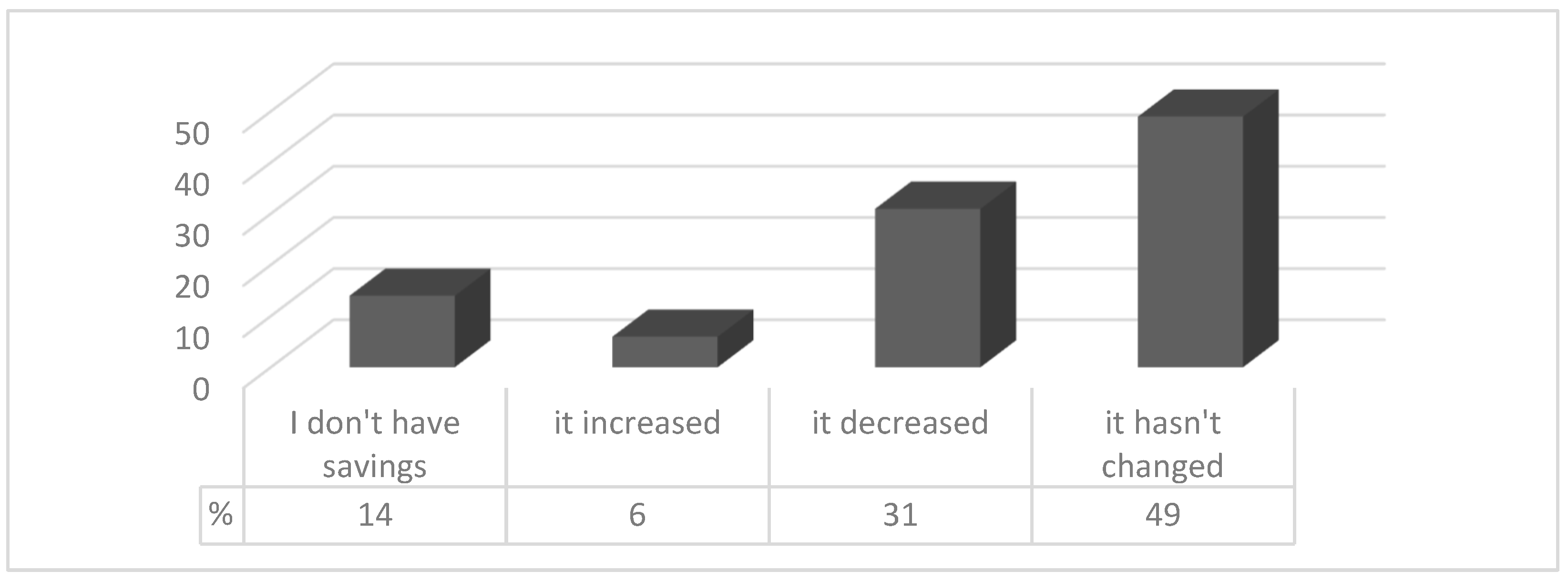

- Low-income households that are indebted or even over-indebted do not notice the deterioration of their financial situation during the health crisis. The measures to be taken must ensure that income levels of these households are maintained and that they prevent the increase in financial burdens (in particular those related to debt management). It should be noted here that low-income households most often do not have savings that would allow them to survive a difficult situation,

- Governments should take the necessary steps to support the efforts of lenders (banks and non-banking institutions) to avoid jeopardizing the stability of the financial sector,

- The use of additional debt by vulnerable households should be limited to weather the crisis in order to avoid a massive increase in over-indebtedness,

- State aid, both at the national and supranational level, must allow not only maintaining the good condition of the financial sector and the entire economy, but also the financial condition of households,

- Another interesting approach is the Spanish initiative to provide a basic income to all citizens, which will protect the most vulnerable ones.

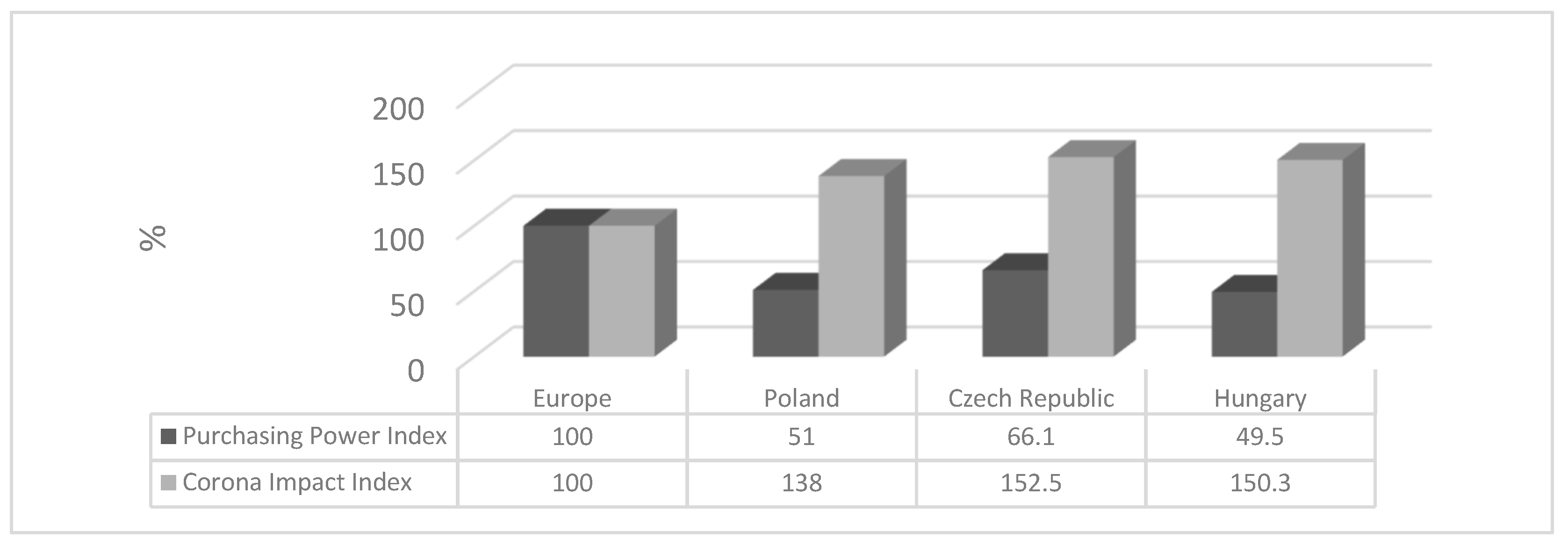

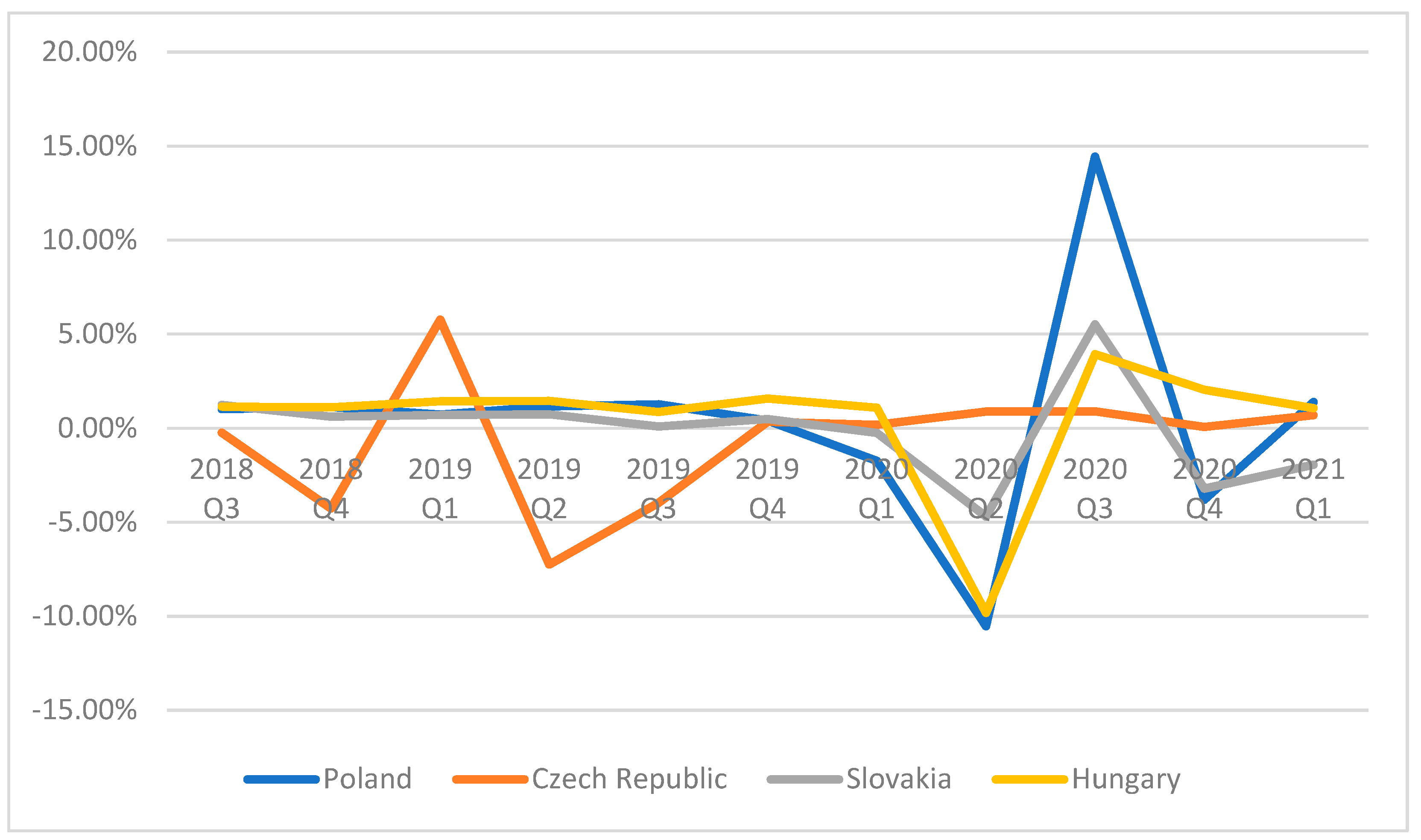

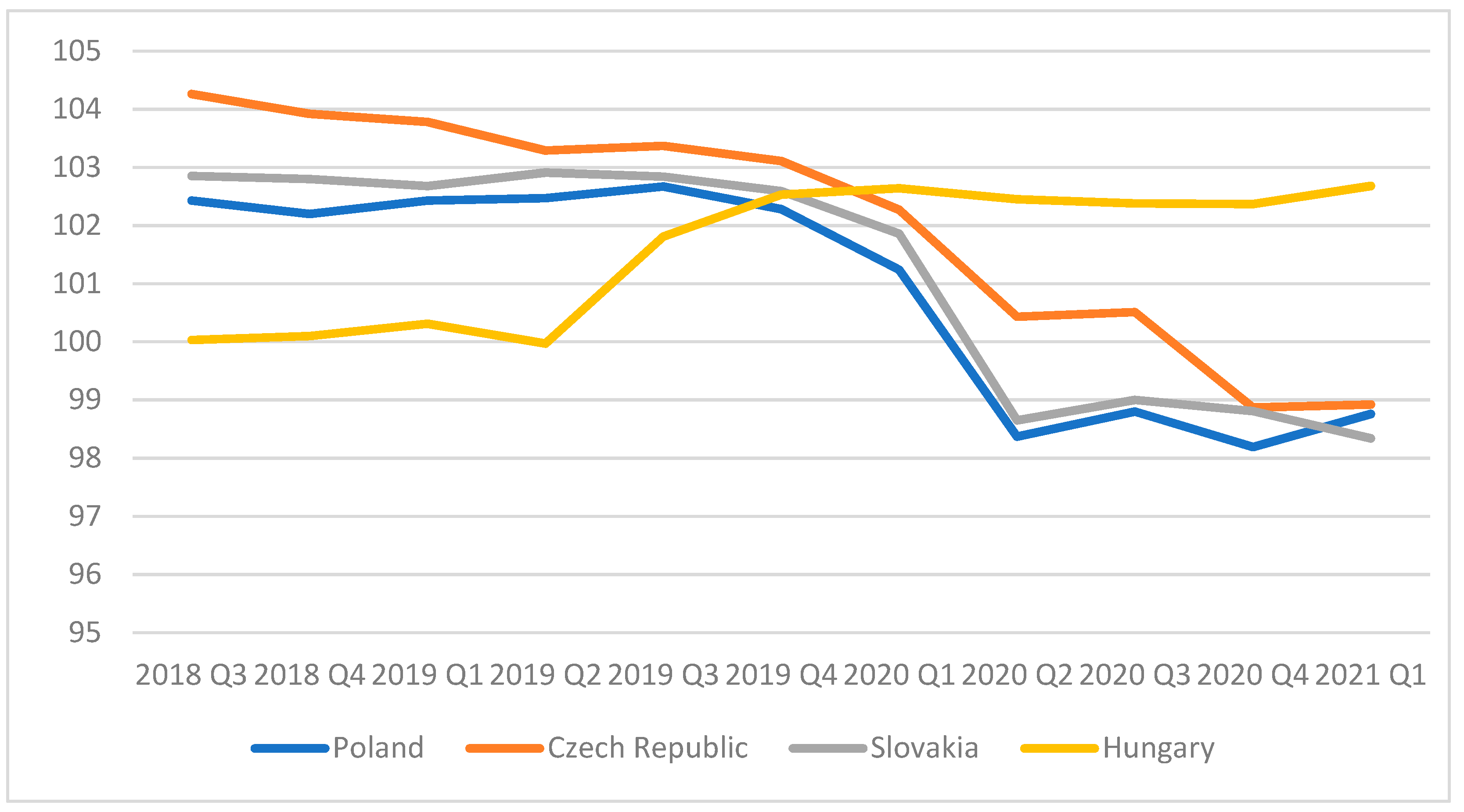

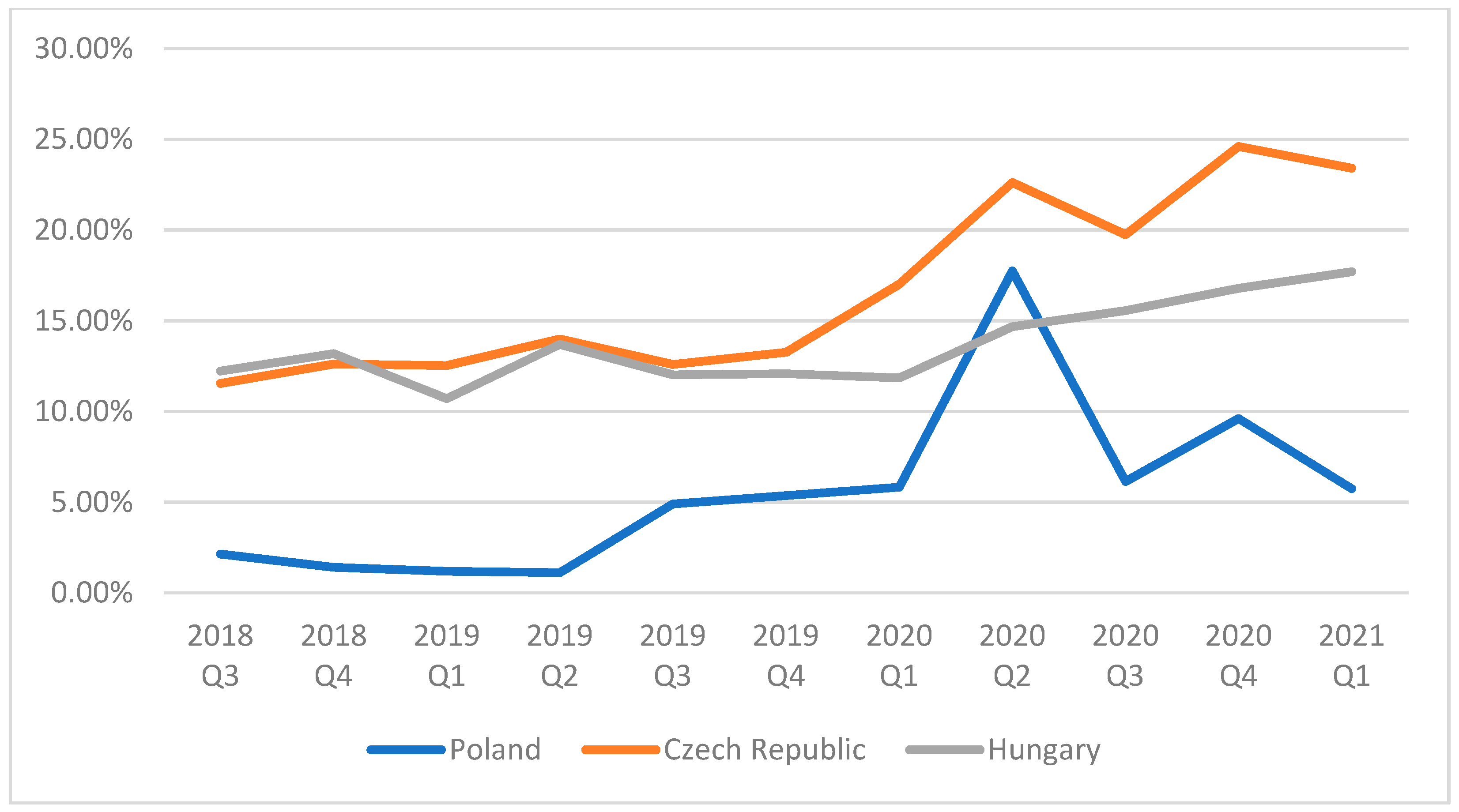

3. COVID-19 Pandemic and Households’ Situation in Poland against the Background of Selected EU Economies

- “having control over one’s finance,

- having a financial cushion, which can be used against emergencies,

- having financial goals,

- being able to make choices that allow to live a happy life”.

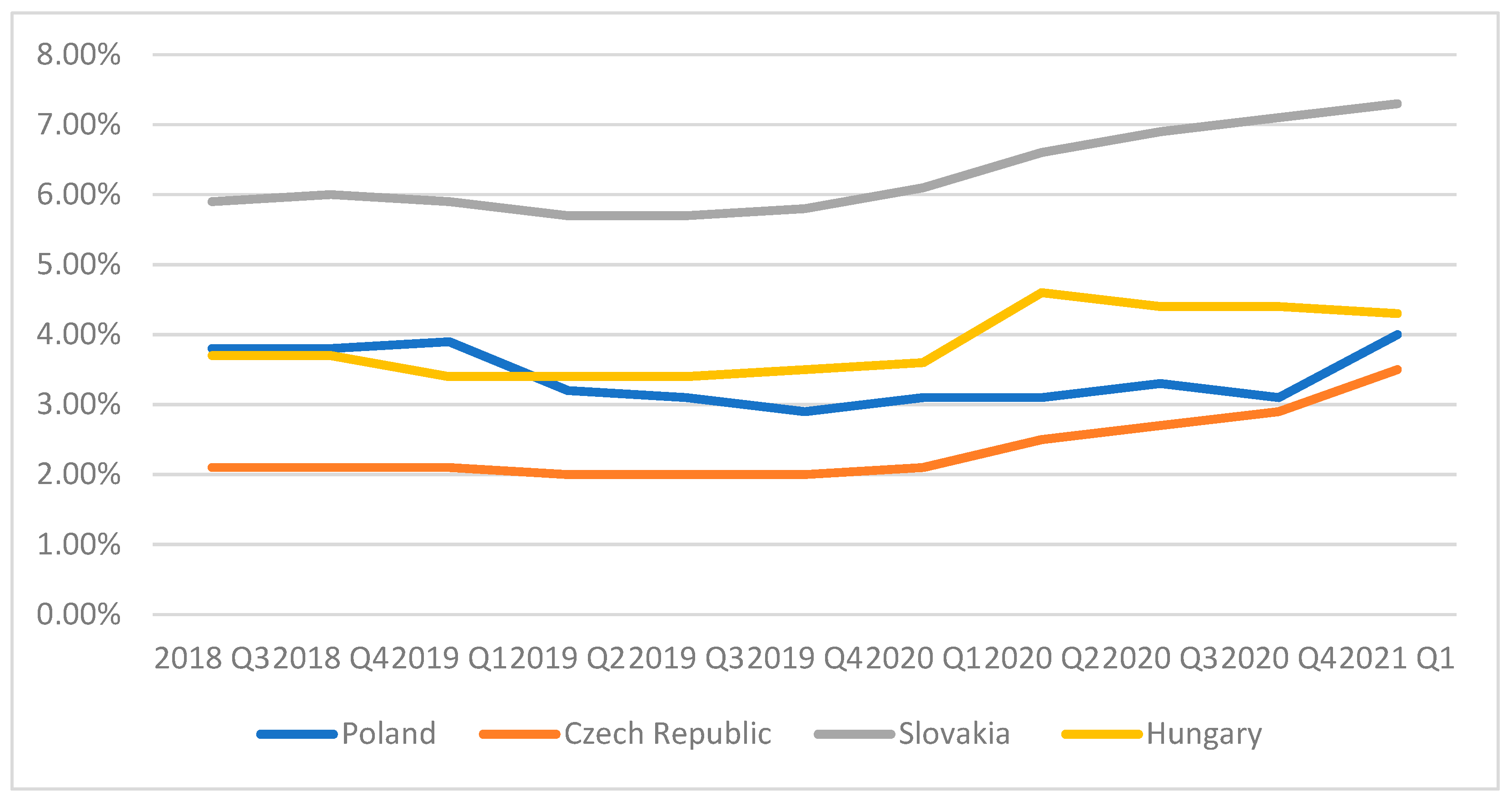

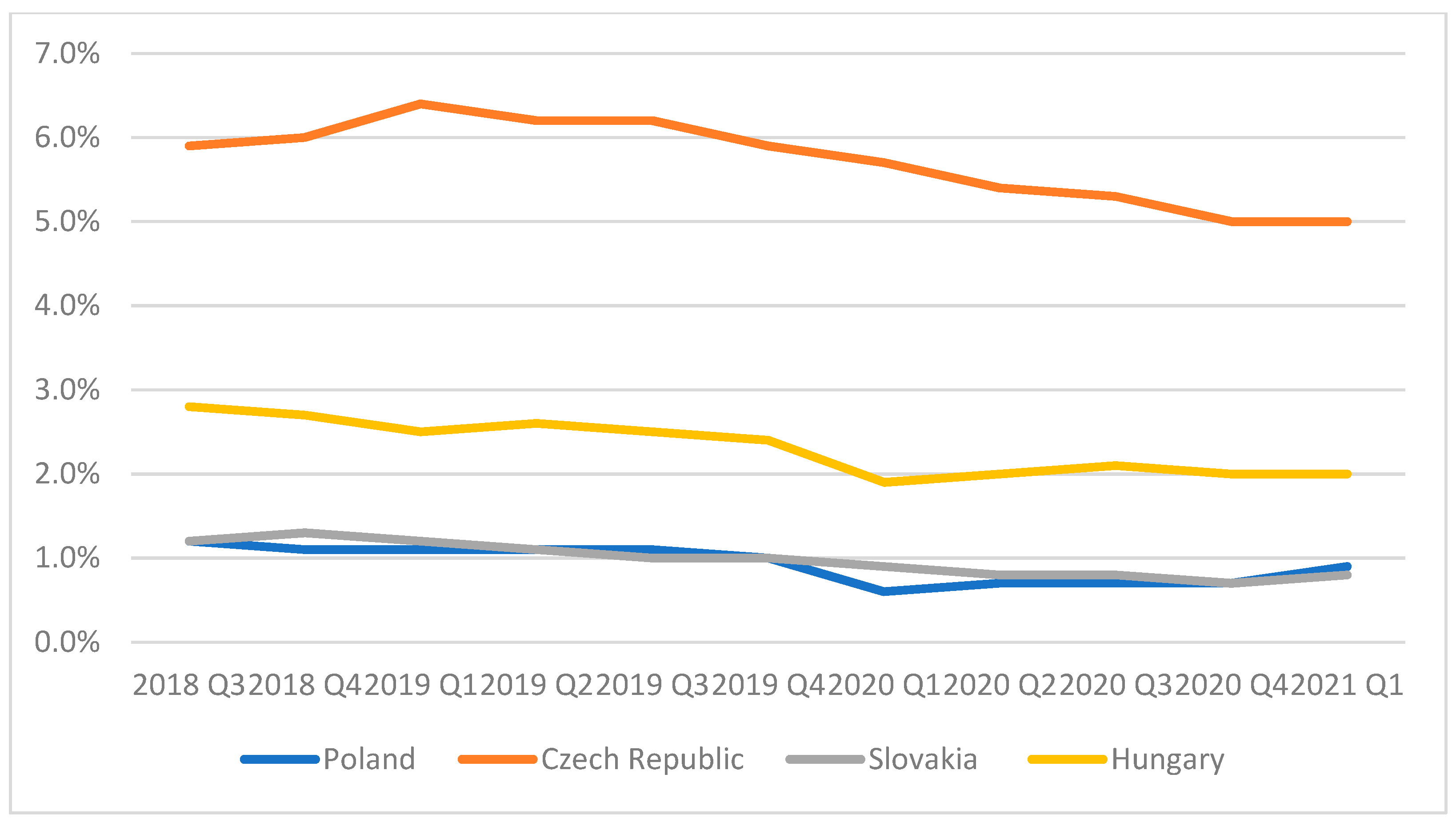

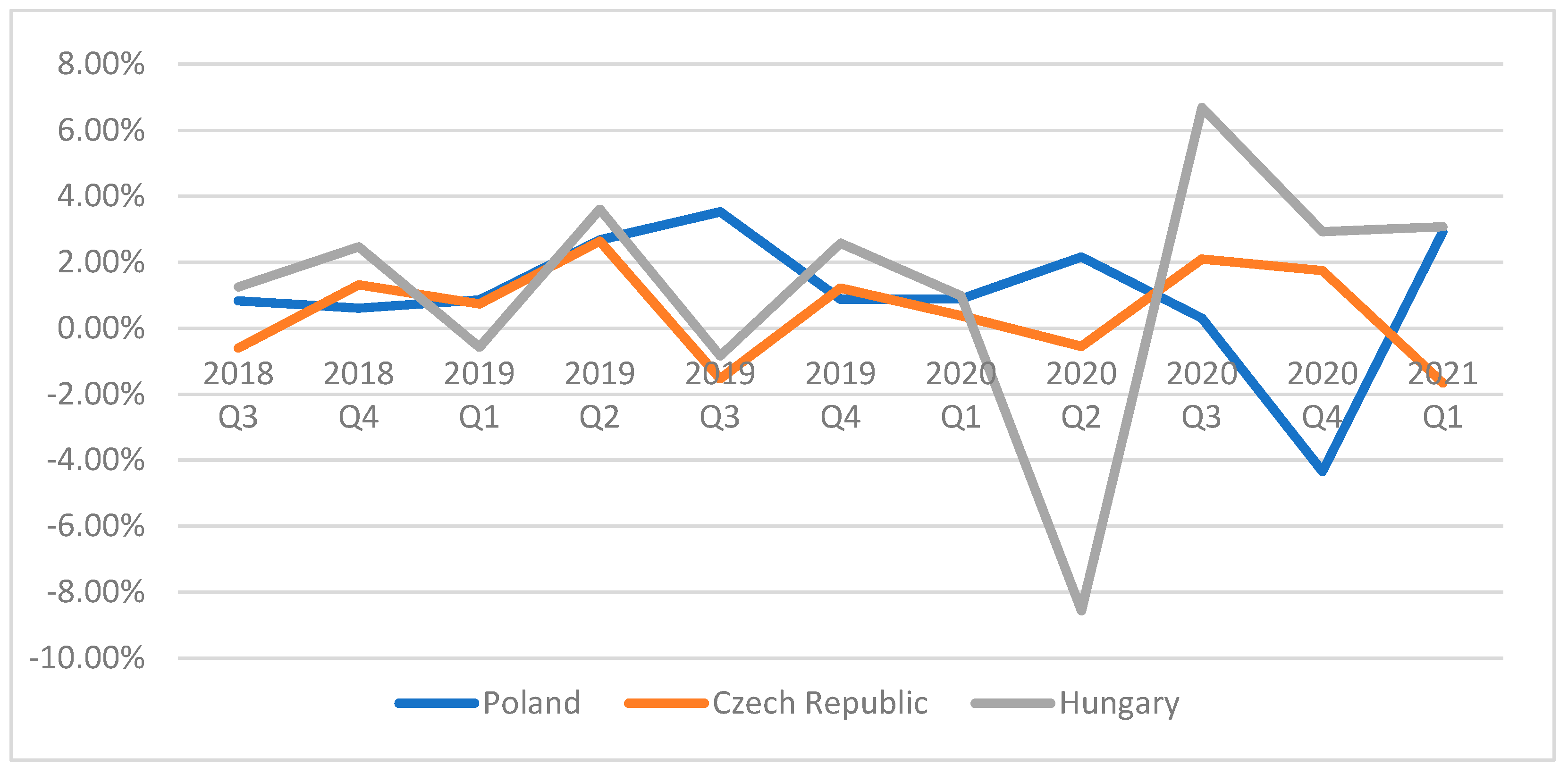

4. The Level of Household’s Savings and Its Predictors—A Linear Regression Model

- The level of unemployment (in %)—UN,

- Real gross disposable income per capita, growth rate (in %)—DI,

- Real final consumption expenditure per capita, growth rate (in %)—FCE,

- Consumer Confidence Index, growth rate (in %)—CCI,

- The level of gross domestic product (in mln EUR)—GDP.

- Household gross saving rate (HS)—OECD Database (data from Q3 2018–Q1-2021),

- The level of unemployment (UN)—Eurostat Database, The Central Statistical Office (Poland), Czech Statistical Office, Statistical office of The Slovak Republic and Hungarian Central Statistical Office (data from Q3 2018–Q1 2021),

- Real gross disposable income per capita (DI)—OECD Database (data from Q3 2018–Q1 2021),

- Real final consumption expenditure per capita (FCE)—OECD Database (data from Q3 2018–Q1 2021).

- Consumer Confidence Index (CCI)—OECD Database (data from Q3 2018–Q1-2021),

- The level of gross domestic product (GDP)—Eurostat Database (data from Q3 2018–Q1 2021).

5. Conclusions: The Assessment Is Ambiguous

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Andrejovská, Alena, and Ján Buleca. 2015. Regression Analysis of Factors Influencing Volume of Households’ savings in the V4 Countries. Mediterranean Journal of Social Sciences 7: 213. [Google Scholar] [CrossRef] [Green Version]

- Anna Unton. 2020. Mapa biedy i bogactwa. Tak wyglądamy na tle Europy (Map of Poverty and Wealth. This Is What We Look Like Compared to Europe). Available online: https://www.money.pl/gospodarka/mapa-zarobkow-tak-wygladamy-na-tle-europy-6572025341844160a.html (accessed on 16 April 2021).

- Anna Unton. 2021. Najniższe bezrobocie to tylko jedna strona medalu. Gorzej jest z szukaniem pracy. Jesteśmy w ogonie UE (The Lowest Unemployment Rate Is Only One Side of the Coin. It Is Worse with Looking for a Job. We Are in the Tail of the EU). Available online: https://www.money.pl/gospodarka/najnizsze-bezrobocie-to-tylko-jedna-strona-medalu-gorzej-jest-z-szukaniem-pracy-jestesmy-w-ogonie-ue-6619792698981024a.html (accessed on 22 March 2021).

- Barrafrem, Kinga, Daniel Västfjäll, and Gustav Tinghög. 2020. Financial well-being, COVID-19, and the financial better-than-average-effect. Journal of Behavioral and Experimental Finance 28: 100410. [Google Scholar] [CrossRef] [PubMed]

- Bilyk, Olga, Anson T. Y. Ho, Mikael Khan, and Geneviève Vallée. 2020. Household Indebtedness Risks in the Wake of COVID-19. Available online: https://www.bankofcanada.ca/2020/06/staff-analytical-note-2020-8/ (accessed on 3 May 2021).

- Boissay, Frédéric, Daniel Rees, and Phurichai Rungcharoenkitkul. 2020. Dealing with Covid-19: Understanding the Policy Choices. Basel: Bank for International Settlements. [Google Scholar]

- Brobeck, Stephen James. 2008. Understanding the Emergency Savings Needs of Low and Moderate-Income Households: A Survey Based Analysis of Impacts, Causes and Remedies. Washington, DC: Consumer Federation of America. [Google Scholar]

- Carbone, Enrica, and John Hey. 1999. The Effect of Unemployment on Saving: An Experimental Analysis. Available online: https://www.researchgate.net/publication/228494796 (accessed on 1 August 2021).

- Chetty, Raj, John Friedman, Nathaniel Hendren, Michael Stepner, and The Opportunity Insights Team. 2020. The Economic Impacts of Covid-19: Evidence from a New Public Database Built Using Private Sector Data. Available online: https://opportunityinsights.org/wp-content/uploads/2020/05/tracker_paper.pdf (accessed on 23 April 2021).

- Collins, J. Michael, and Carly Urban. 2019. Measuring Financial Well-being Over the Lifecourse. European Journal of Finance 26: 341–59. [Google Scholar] [CrossRef]

- Comiesięczne zestawienie informacji o oszczędnościach (Monthly Information on Savings). 2021. Warsaw: Polski Fundusz Rozwoju.

- Consumer Financial Protection Bureau. 2015. Measuring Financial Well-Being: A Guide to Using the CFPB Financial Well-Being Scale. Available online: https://files.consumerfinance.gov/f/201512_cfpb_financialwell-being-user-guide-scale.pdf (accessed on 30 June 2021).

- Cooper, Cheryl R., Maura Mullins, and Lida R. Weinstock. 2020. Covid-19: Household Debt during the Pandemic. Available online: https://www.everycrsreport.com/reports/R46578.html (accessed on 30 June 2021).

- Dolan, Paul, Tessa Peasgood, and Mathew White. 2008. Do we really know what makes us happy? A review of the economic literature on the factors associated with subjective well-being. Journal of Economic Psychology 29: 94–122. [Google Scholar] [CrossRef]

- Duszyński, Jerzego, Aneta Afelt, Anna Ochab-Marcinek, Radosław Owczuk, Krzysztof Pyrć, Magdalena Rosińska, Andrzej Rychard, and Tomasz Smiatacz. 2020. Zrozumieć COVID-19 (To Understand COVID-19). Warszawa: Polska Akademia Nauk. [Google Scholar]

- Edukacjagieldowa.pl. 2020. Available online: https://www.edukacjagieldowa.pl/2020/10/koronawirus-w-nierownomierny-sposob-wplywa-na-oszczedwww.edukacjagieldowa.plnosci/ (accessed on 15 April 2021).

- Eurostat Database. 2021. Available online: https://ec.europa.eu/eurostat (accessed on 20 August 2021).

- Finanse Polaków w czasie COVID-19 (Poles’ finances during COVID-19). 2020. Federacja Konsumentów. Warszawa: Fundacja Rozwoju Rynku Kapitałowego.

- Fox, Jonathan, and Suzanne Bartholomae. 2020. Household finances, financial planning, and COVID-19. Financial Planning Review 3: e1103. [Google Scholar] [CrossRef]

- Gerrans, Paul, Craig Speelman, and Guillermo Campitelli. 2014. The Relationship Between Personal Financial Wellness and Financial Wellbeing: A Structural Equation Modelling Approach. Journal of Family and Economic Issues 35: 145–60. [Google Scholar] [CrossRef] [Green Version]

- GfK Purchasing Power Europe. 2020. Free Compendium for All 42 European Countries. Available online: https://insights.gfk.com/gfk-purchasing-power-europe-2020-download-compendium (accessed on 16 April 2021).

- Gliński, Zdzisław, and Andrzej Żmuda. 2020. Epidemia i pandemie chorób zakaźnych (Epidemics and Pandemics of Infectious Diseases), Życie weterynaryjne no 95. Available online: https://www.vetpol.org.pl/dmdocuments/ZW-09-2020-02.pdf (accessed on 2 April 2021).

- Grzeszak, Jacek, Filip Leśniewicz, and Paweł Śliwowski. 2020. Pandemics. Zestaw Narzędzi Fiskalnych i Monetarnych w Czasach Kryzysu (Pandemics. A Set of Fiscal and Monetary Tools in Times of Crisis). Warszawa: Polski Instytut Wydawniczy. [Google Scholar]

- Janecki, Jarosław. 2020. Wymuszone Oszczędności w Okresie Pandemii (Forced Savings during a Pandemic). Available online: https://www.obserwatorfinansowy.pl/bez-kategorii/rotator/wymuszone-oszczednosci-w-okresie-pandemii/ (accessed on 2 May 2021).

- Jerusalmy, Olivier. 2020. Coronavirus: A Dangerous Wave of Personal Over-Indebtedness Is on Its Way: Here Is How to Avoid It. Available online: https://www.finance-watch.org/coronavirus-a-dangerous-wave-of-personal-over-indebtedness-is-on-its-way-here-is-how-to-avoid-it/ (accessed on 2 May 2021).

- Kahneman, Daniel, and Alan B. Krueger. 2006. Developments in the measurement of subjective well-being. Journal of Economic Perspectives 20: 3–24. [Google Scholar] [CrossRef] [Green Version]

- Kansiime, Monica K., Justice A. Tambo, Idah Mugambi, Mary Bundi, Augustine Kara, and Charles Owuor. 2021. COVID-19 implications on household income and food security in Kenyaand Uganda: Findings from a rapid assessment. World Development 137: 105199. [Google Scholar] [CrossRef] [PubMed]

- Kłopocka, Aneta Maria, Tomasz Kopczyński, and Grażyna Lenicka-Bajer. 2014. Financial Situation and Attitudes towards Saving in Polish Society: Evidence from Micro-Data. Annals of the Economy Series. Special Volume. Târgu Jiu: Constantin Brâncuşi” University of Târgu Jiu. [Google Scholar]

- Kłopocka, Aneta Maria. 2016. Does Consumer Confidence Forecast Household Saving and Borrowing Behavior? Evidence for Poland 133: 693–717. Available online: https://0-link-springer-com.brum.beds.ac.uk/content/pdf/10.1007/s11205-016-1376-4.pdf (accessed on 7 August 2021).

- Kosny, Marek, and Maria Piotrowska. 2013. Economic Security of Households and Their Savings and Credits. National Bank of Poland Working Paper no. 146. Warsaw: National Bank of Poland. [Google Scholar]

- Kurowski, Łukasz. 2021. Household’s Overindebtedness during the COVID-19 Crisis: The Role of Debt and Financial Literacy. Risks 9: 62. [Google Scholar] [CrossRef]

- Levine, Ross, Chen Lin, Mingzhu Tai, and Wensi Xie. 2020. How Did Depositors Respond to COVID-19? The Review of Financial Studies, hhab062. [Google Scholar] [CrossRef]

- Marcinkowska, Monika. 2020. Kapitał Relacyjny Banków a Kryzys Pandemiczny. Działania Polskich Banków Względem Interesariuszy w obliczu COVID-19 (Banks’ Relational Capital and the Pandemic Crisis. Actions of Polish Banks towards Stakeholders in the Face of COVID-19). Łódź: Wydawnictwo SIZ. [Google Scholar]

- Muranyi, Thomas, and Julia Richter. 2020. Europeans Have around €773 Less in 2020 Due to COVID-19. GfK, October 20. [Google Scholar]

- OECD Database. 2021. Available online: Data.oecd.org (accessed on 20 May 2021).

- Pogorzelski, Karol. 2020. Wpływ Covid-19 na finanse osobiste Polaków oraz mieszkańców Europy (The Impact of Covid-19 on the Personal Finances of Poles and European Citizens). Amsterdam: ING Bank. [Google Scholar]

- Raport Banku Pekao. 2020. Gospodarka w czasach pandemii. Spojrzenie sektorowe na bazie pierwszych doświadczeń globalnych” (Pekao Bank Report “Economy in a Pandemic. Sectoral View Based on the First Global Experiences”). Available online: https://www.pekao.com.pl/o-banku/aktualnosci/084c4abc-018b-4af4-bb32-ee1c44236326/raport-banku-pekao-gospodarka-w-czasach-pandemii-spojrzenie-sektorowe-na-bazie-pierwszych-doswiadczen-globalnych.html (accessed on 27 April 2021).

- Rozporządzenie Ministra Zdrowia. 2020. Rozporządzenie Ministra Zdrowia z dnia 20 marca 2020 r. w sprawie ogłoszenia na obszarze rzeczypospolitej polskiej stanu epidemii (Regulation of the Minister of Health of March 20. 2020 on the declaration of an epidemic in the territory of the Republic of Poland) (Dz. U. z 2020 r., poz. 433). Available online: https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU20200000491 (accessed on 30 June 2021).

- Suomi, Aino, Timothy P. Schofield, and Peter Butterworth. 2020. Unemployment, Employability and COVID19: How the Global Socioeconomic Shock Challenged Negative Perceptions Toward the Less Fortunate in the Australian Context. Frontiers in Psychology 11: 2745. Available online: https://www.frontiersin.org/articles/10.3389/fpsyg.2020.594837/full#B10 (accessed on 14 April 2021). [CrossRef] [PubMed]

- Ventura, Luca. 2020. Unemployment Rates Around the World 2020, Global Finance, 22 October. Available online: https://www.gfmag.com/global-data/economic-data/worlds-unemployment-ratescom (accessed on 16 April 2021).

- WHO Announces a Pandemic. 2020. Available online: https://www.euro.who.int/en/health-topics/health-emergencies/coronavirus-covid-19/news/news/2020/3/who-announces-covid-19-outbreak-a-pandemic (accessed on 20 April 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| The Spanish Flu | SARS | |

|---|---|---|

| Similarities to COVID-19 | High mortality, external shock difficult to predict It spread practically all over the world Application of the lockdown strategy | Similar channels of influence Source of the epidemic—China |

| Main differences | Less importance of the service sector in economies It mainly killed young people Consequences of the pandemic compounded by war losses Less interdependence between economies | A smaller scale of disturbances in the economy Different nature of international ties |

| An Area of Influence | Characteristics |

|---|---|

| Supply channel | Lack of staff Lack of resources |

| Demand channel | Consumption drop Private investment decline Breakdown in selected sectors |

| Social moods | Decline in consumer and business confidence Investors panic in the financial markets |

| Financial system | Declines in the prices of financial assets Increase in risk aversion Credit availability decline Increase in non-performing loans Liquidity decline Decline in the stability of the financial system |

| Country | Statistically Significant Variables | Estimates of Regression Coefficients |

|---|---|---|

| Poland (PL) | UN (p value = 0.00641) CCI (p value = 0.0155) GDP (p value = 0.01625) | |

| Czech Republic (CZ) | CCI (p value = 0.000000015) GDP (p value = 0.014625) | |

| Hungary (HU) | UN (p value = 0.00032) GDP (p value = 0.02648) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Szustak, G.; Gradoń, W.; Szewczyk, Ł. Household Financial Situation during the COVID-19 Pandemic with Particular Emphasis on Savings—An Evidence from Poland Compared to Other CEE States. Risks 2021, 9, 166. https://0-doi-org.brum.beds.ac.uk/10.3390/risks9090166

Szustak G, Gradoń W, Szewczyk Ł. Household Financial Situation during the COVID-19 Pandemic with Particular Emphasis on Savings—An Evidence from Poland Compared to Other CEE States. Risks. 2021; 9(9):166. https://0-doi-org.brum.beds.ac.uk/10.3390/risks9090166

Chicago/Turabian StyleSzustak, Grażyna, Witold Gradoń, and Łukasz Szewczyk. 2021. "Household Financial Situation during the COVID-19 Pandemic with Particular Emphasis on Savings—An Evidence from Poland Compared to Other CEE States" Risks 9, no. 9: 166. https://0-doi-org.brum.beds.ac.uk/10.3390/risks9090166