Intellectual Capital and Innovation Performance: Systematic Literature Review

1

Azman Hashim International Business School, Universiti Teknologi Malaysia, Kuala Lumpur 54100, Malaysia

2

Business Faculty, Middle East University, Amman 11831, Jordan

*

Author to whom correspondence should be addressed.

Risks 2021, 9(9), 170; https://0-doi-org.brum.beds.ac.uk/10.3390/risks9090170

Submission received: 1 September 2021

/

Revised: 10 September 2021

/

Accepted: 13 September 2021

/

Published: 17 September 2021

Abstract

:Over the years, several studies have been conducted to identify the impact of various intellectual capital components on the organizational performances. However, most of these works greatly replicated the applications and uses of different intellectual capital components (human, structural, relational, social) without addressing the shortcomings related to their empowerment toward the innovation perception of the organizations. Based on this fact, we comprehensively reviewed the existing literatures that strongly influenced the innovation performance of the financial sector. Standard inclusion and exclusion criteria were used for the critical and systematic evaluation of the past studies. It identified the main limitations of intellectual capital components efficiency in the financial sector that could considerably affect their desired innovation performances in the dynamic and competitive market scenarios. In addition, a correlation was established among the organizational growth of intellectual capital components and innovation performance, leading to positive implications on intellectual capital components development.

1. Introduction

In recent years, the synergistic effect of various intellectual capital components and success on the innovation performance emerged as a recurring theme in the field of economic growth, especially for the financial sector (Isanzu 2017). So far, fewer investigations have been performed to evaluate the influence of intellectual capital components on the innovation performance and growth correlation in the context of financial sector (Sveiby et al. 2007). The preservation of a successful innovation performance is determined by the efficient and reliable actions based on the organization’s capacity to learn and adjust dynamically (Hsu and Wang 2012). For maintaining and gaining the competitive advantages in the financial sector, every organization must practice them with the emphasis on intellectual capital development.

Earlier reports revealed that intellectual capital components are the mental attributes based on facts, figures, and organizational experiences (Tastan and Davoudi 2015). It was argued that for improving the employees’ knowledge, skill, and perception including the non-sensorial and intangible characteristics the intellectual capital can be exploited thereby acquiring the wealth via the business assets expansion (Ali et al. 2020c; Rindermann et al. 2015). Fundamentally, the definitions of intellectual capital vary according to its scale. Therefore, an organization’s intellectual capital can be used to generate extra benefits or items that may be easily achieved through its employees. The possibility of using intellectual capital components in a customized way to generate valuable assets in a farm have been reported (Deltorn 2017) wherein it was hinted that intellectual capital components deficiency can limit the broader interest of an enterprise and expected value outcomes.

Considering the significant impact of intellectual capital components on innovation performance of the financial sector, this article exhaustively reviewed the existing literature to ascertain a correlation between intellectual capital components and innovation performance in the context of financial sector. The past development, ongoing challenges to empower the intellectual property in the financial sector and future trends of intellectual capital components based organizational growth are underscored. This systematic evaluation may enable us to achieve an in-depth understanding of diverse research variables and relevant background as indicated in the literature (Ali et al. 2020a; Allameh 2018a). Furthermore, this communication chronologically encompassed various studies to indicate the relevance of implementing intellectual capital components to enhance the innovation performance of the organizations. Most of the previous researchers discussed the effects of intellectual capital components on the organization’s innovation performance without establishing a relationship between them (Asiaei et al. 2020; Scafarto et al. 2016; Agostini and Nosella 2017; Chowdhury et al. 2018). Some studies also displayed different views regarding the classification of intellectual capital into components and disagreed with the vital role of intellectual capital components on innovation performance (Chowdhury et al. 2018; Asiaei and Jusoh 2015; Bogdan et al. 2017). From this perspective, it became essential to establish a multi-level correlation amongst various intellectual capital components and innovation performance of an organization to generate new knowledge and develop better understanding on such relationship (Isanzu 2017).

It is worth mentioning the idea that innovation performance of any organization is crucial for achieving competitive advantages in terms of service or/and management quality, strategy formulation, creativity, and so forth (Li et al. 2019; Ferreira and Franco 2017; Wendra et al. 2019). Therefore, most of the studies involving the innovation performance in financial sector and focused mainly on the services and manufacturing sectors (Aluchna et al. 2018; Agostini and Nosella 2017). The observed close connection between the organizations’ intellectual capital and innovation performance was further validated in the contexts of different regions and industries (Nevado et al. 2018). Despite all these efforts, a rudimentary insight of the intellectual capital and its impact as the knowledge resources for the value creation remains deficient. In this rationale, a systematic survey of the existing state-of-the-art studies was conducted to resolve two issues: (i) how do intellectual capital components affect the innovation performance in the financial sector? and (ii) what are the challenges faced by the financial sector to maintain a high level of intellectual capital for taking competitive advantages in the dynamic market scenarios?

This article is organized six broad sections. Section 2 described the methodology of this detailed review and Section 3 highlighted the research progression related to importance of intellectual capital components in the context of financial sector. Section 4 critically evaluated the earlier literary studies to reveal a close connection between intellectual capital components and innovation performance. Section 5 addressed the recent development, challenges, and forthcoming trends of intellectual capital components implementation for attaining improved innovation performance. Section 6 discussed the significant findings on intellectual capital components and innovation performance correlation and summarized the paper.

2. Methodology

As mentioned previously, the present critical evaluation of the previous findings enabled identifying a correlation between intellectual capital components and innovation performance in the financial sector (Dixon-Woods 2010). Furthermore, we compared various pertinent studies and addressed the emergent issues in the field of financial sector and recommended the implementation of intellectual capital components into their working culture for taking the competitive market advantages and thus enhancing the productivity (Borenstein et al. 2009). In order to answer the posed research questions, an in-depth analysis of the existing works were conducted based on the impacts of intellectual capital components on the innovation performance (Bracci et al. 2019; Mention 2012). The identified ongoing debates related to the importance of implementing intellectual capital components in the organization and its effect on the innovation performance provided new insight and opened up avenues for further studies (Agostini et al. 2017; Qurashi et al. 2020; Agostini and Nosella 2017). In this regard, the present review article is distinct from the existing reviews, wherein the previous researchers usually summarized and interpreted the collected findings in a subjective and narrative (selected issues based on expertise) form (Manes-Rossi et al. 2020).

Generally, a review paper follows systematic literature review based on some logical and precise framework that is reproducible to serve as standalone document (Massaro et al. 2016). This allows us to minimize the logical mistakes and biases that originate from the subjective analyses and opinions. In other words, a review article is scientifically essential to provide rudimentary insights of the past works and add new knowledge in the database, showing the challenges and future trends (Pedro et al. 2018a). Due to this reason, articulation of review articles in the field of accounting, management and financial studies has gained renewed interests (Massaro et al. 2016). To achieve better knowledge and understanding, the financial sector worldwide has been exploring the intellectual capital format for improving their innovation performance. Motivated by the significance of intellectual capital components implementation in the financial sector as advocated in various recent studies (Agostini and Nosella 2017; Agostini et al. 2017; Qurashi et al. 2020) this paper followed a structured procedure executed in three stages as described below.

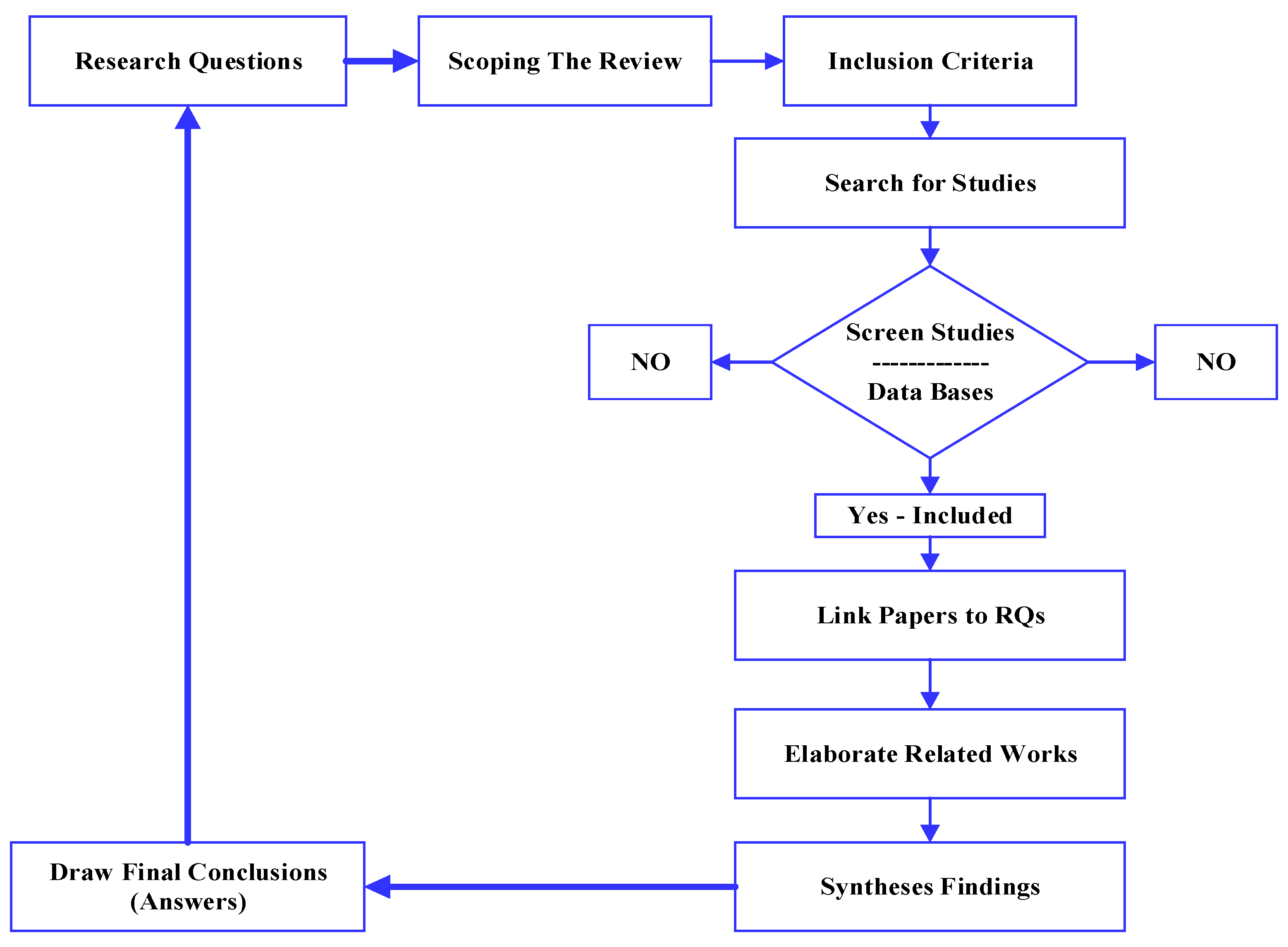

First stage, most of the scientific and relevant articles (published in English and peer-reviewed) were searched, analyzed critically and included depending on specific criteria to fulfil research goals (Cuozzo et al. 2017; Manes Rossi et al. 2016). Various keywords including (((“intellectual capital”) OR (“intangible assets”) OR (“human capital”) OR (“structural capital”) OR (“relational capital”) OR (“social capital”)) AND ((“innovation performance”))) were used in this paper. These articles were collected using different databases such as Scopus, Science Direct, Emerald, and Web of Science during 2015 to 2020. It is needless to mention that a very limited number of articles have been published in the area of social sciences, business managements, finance, and accounts in this period. The research scope for peer-reviewed journal articles selection was further narrowed down (via systematic inclusion and exclusion criteria) to maintain the high quality (Higgins and Green 2009). Other resources including books, edited book chapters, editorials, conference proceedings, papers, and research reports were excluded from this review. It was acknowledged that (Gough 2007) such criteria can enhance the values and quality of judgment in terms of the evidences while revisiting the existing contributory works. A total of 862 papers were collected from various databases. Further, these contributions were manually searched to exclude any duplication, finally selecting 799 of them. Table 1 shows the salient features of the inclusion criteria.

In the second stage, the relevance (Petticrew and Roberts 2008) of these retrieved papers were assessed based on their titles, abstracts, and contents following some standard criteria. This evaluation was mainly centered on intellectual capital components format applicable to the financial sector, resulting in the exclusion of 523 articles. Furthermore, published papers that qualified the SCImago Journal Rank were considered, resulting in the exclusion of another six of them. The third stage involved complementing the selection procedure to achieve better sampling. The manual inspection of the leading journals that published articles on the finances and accounting practices enabled us to choose an extra 16 papers. Another filtering based on the full text was performed to exclude some less significant articles, producing 128 research papers that fit all the selection criteria. Briefly, a total of 128 articles were critically analyzed to present this paper. Figure 1 displays various stages of the reviewing process.

3. Intellectual Capital Components

The notion of so-called intellectual capital was introduced by various scholars in their literary works (Coleman 1988) to describe the perspectives of the non-tangible assets that contribute to the organizational success. Later, the models related to the improvement of the non-tangible assets were developed (Sveiby et al. 2007) based on the strategic perspective. Since then, numerous studies have been carried out concerning the development of intellectual capital that mainly focused on the financial and accounting practices wherein different variables, structures, and measures were analyzed to determine the organizational dimensions (Ali et al. 2020d; Bontis 1998). Over the years, the researchers have started extrapolating the primary conceptual levels of the organizational non-tangible assets (Salicru and Perryer 2007). Many reports suggested different approaches to identify, classify and measure intellectual capital (Bontis et al. 2009). Some studies have defined the underlying concepts of intellectual capital as the expertise, knowledge, and relation of the soft assets in the organizations as a substitute for their physical capitals (Iivari et al. 1998). It was acknowledged that (Chen et al. 2015) intellectual capital can be defined as the human resource knowledge of the organizations that can be used for money-making or other useful purposes like providing the competitive advantages, enhancing the productivity and making long-term sustenance.

Being a non-intangible asset or informational resource of an organization, intellectual capital components can be used at its disposal for making profits, attracting customers, creating a new product, enhancing existing product or improving the business (Subramaniam and Youndt 2005). In essence, intellectual capital is viewed as the aggregate sum of the knowledge or set of intangible assets that the organizations can utilize to improve their operational performance (Vaz et al. 2019). Concisely, it is a multidimensional concept that includes the assets of experiences, knowledge and practical abilities for creating values in the organization (Lardo et al. 2017). It can be perceived as a non-monetary and non-physical resource that enables the organizational development by extracting the knowledge-based values (Ansari et al. 2016). The knowledge held by the employees of the organization is also called the development of its business processes, databases, systems, and relationships. To validate this idea, the effects of intellectual capital on the organizational performance were examined (Pedro et al. 2018a). Many studies have described and explained all the underlying intellectual capital components and provided a basis for understanding its actual meaning (van der Meer-Kooistra and Zijlstra 2001). It was also stated that (Dzenopoljac et al. 2017) intellectual capital includes wisdom, innovations and knowledge. The management, creation, measurement, and evaluation of the core intellectual capital are the essential indicators that determine the values of the corporate competitiveness (Jordão and de Almeida 2017).

Previous studies on the intellectual resources considered three major factors like intangible assets, capabilities for creating and modifying the assets, and social relationships within which all knowledge developments are established (Gallagher and Gallagher 2012). Each factor indicated a different concept of knowledge used in the organization for innovation performance (Cuozzo et al. 2017). Knowledge as an intangible asset of an organization represents the possession of investments, intellectual property rights, structural, human and customer capitals. Several issues are noticeable in the service industries due to the dominance of economies. Nevertheless, the less value-relevant intellectual property reflects poorly respected organization (Nimtrakoon 2015). Following the earlier suggestions, this paper focused on four dominant intellectual capital components (human, structural, relational, and social) (Cabrilo et al. 2018). Except social capital, the other three components was shown to affect the intellectual capital gains of an organization (Massaro et al. 2015). Thus, it is significant to distinguish human capital of an organization from its procedures. Essentially, the organizational procedures refer to various uses of the available resources by its employees at their respective workplace. Conversely, the information system refers to the implementation of the information technology while managing human knowledge (Użienè 2014).

Over the past two decades, many organizations worldwide have realized the necessity to develop intellectual capital components that constitute the basic ingredient in their business growth (Cabrilo et al. 2018). Meanwhile, intellectual capital is accepted as a key component to promote the assets of an organization that is responsible for the improvement of its products for taking the competitive advantages in the changing market environment (Mutuc et al. 2019). Generally, the entrepreneurs were found to be wrongly inclined towards intellectual capital. Therefore, it is mandatory to prepare the educational plans for managing the intellectual capital and rectify such an incorrect attitude (Secundo et al. 2018). In the current globally challenging times, intellectual capital must become a process for any organization that goes beyond routine jobs. According to Bogers et al. 2019, the use of the intellectual capital together with the innovation strategies can bring immense benefits to the organizations provided the abstract theoretical concept of intellectual capital is translated into real practices. It was further argued that when intellectual capital is managed effectively, it is potentially advantageous for mitigating various problems of the organization, providing a competitive advantage (Ferreira et al. 2020).

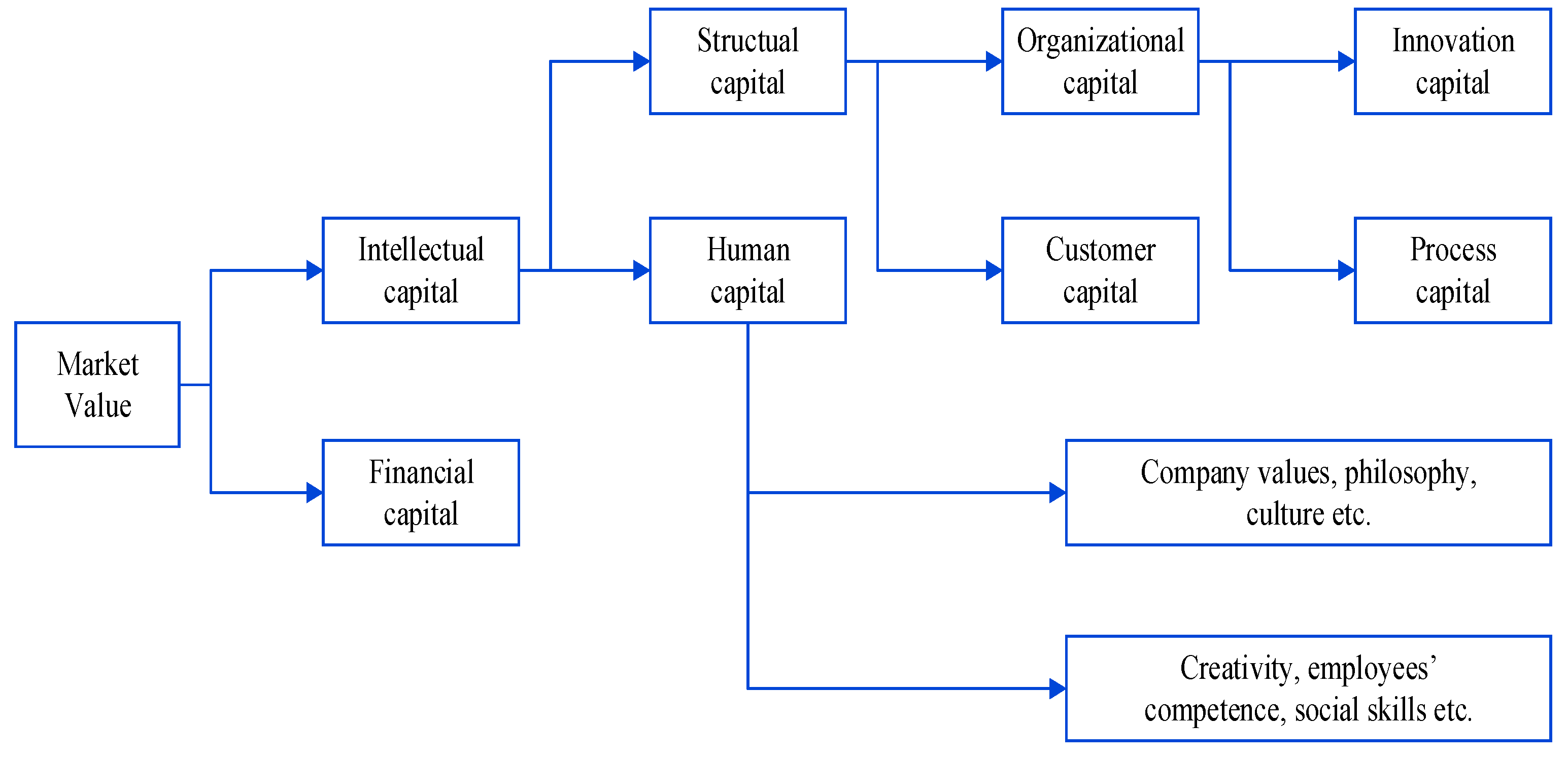

Of late, intellectual capital is becoming increasingly popular for the virtual economy worldwide (Kengatharan 2019). It was demonstrated that intellectual capital is the creative use of combined market strategies, intellectual property, human and intangible assets, and the knowledge for producing the value chain (Secundo et al. 2018). In this regard, intellectual capital can be regarded as the market values minus the organization values (Mutuc et al. 2019). The organizational processes relate to how its employees make knowledge resources available in the workplace. Conversely, the information systems refer to the proper use of information technology for managing the acquired knowledge (Liu and Jiang 2020). Figure 2 illustrates the market value of intellectual capital as referred in (Sveiby et al. 2007).

Systematic studies showed that some aspects of intellectual capital from a multifaceted viewpoint are consistent with the desired objectives of the financial markets (Asiaei et al. 2020). Recently, there has been a growing demand to conduct empirical studies for gaining an in-depth knowledge about intellectual capital components due to their multidimensional traits (Cabrilo and Dahms 2020). However, appropriate hypotheses must be made and the effects of intellectual capital components on the innovation performance of an organization must be measured accurately to develop some comprehensive arguments regarding the proper management of various intellectual resources. The following sections provide a detailed description of the significant intellectual capital components.

3.1. Human Capital

In the modern world, with a knowledge-based economy, human capital has a driven value (Cuozzo et al. 2017). It has been argued that human capital is the primary resource or component in the value creation of an organization (O’Donnell et al. 2003). Prior studies on human capital examined human stocks such as skills, traits, and competencies. Meanwhile, some researchers have acknowledged the importance of relevant narratives concerning human capital (Asiaei et al. 2021; Nadeem et al. 2017). Thus, it can be described as the intangible assets that have been at the center of discussions over the last two decades in financial and accounting studies. Such imperceptible assets have posed various challenges for the governments, regulatory bodies and organizations (Zimmerman 2015). According to another study (Hsu and Wang 2012), human capital must include the training and development, entrepreneurial skills, equity, safety, relations, and welfare of the employees. In addition, human capital was classified as the expertise, knowledge, productivity, skills, values, expert networks and professional teams in an organization (Daou et al. 2014).

It was reported that (Massaro et al. 2015) human capital can be shaped up through the aptitude, competency, experience and skill of an organization’s employees. In addition, human capital is vital for the foundation of an organization, as without it, knowledge cannot be created (Isanzu 2017). Thus, an organization can improve its human capital either by attracting some skillful persons from outside the marketplace or through the internal development of the existing employees’ skills (Berezinets et al. 2016). Overall, the skillful employees’ retention plays a remarkable role in the innovation performance of any organization. An organizations is more likely to use its accessible resources instead of recruiting extra skillful employees with high salaries (McDowell et al. 2018). Earlier study revealed that the training could facilitate human capital development, significantly impacting the innovation performance and enhanced activities of small and medium size organizations (Pedro et al. 2018b).

Therefore, it can be asserted that human capital forms the heart of intellectual capital. It was also stated that in certain conditions, the continued competitive advantages can be ensued from collective human capital (Cabrilo et al. 2018). According to the resource-based theory, an organization evaluates the strength and weakness of its resources before choosing an achievable strategy. Consequently, human capital of an organization is regarded as an underlying strategic resource that can support its accomplishment because employees knowledge and skill are essential in the fast altering competitive market scenarios (Heaton et al. 2019). Briefly, human capital of an organization determines the worthiness of its manpower resource depending on the context of performance (Xu and Wang 2018).

The organizations with higher human capital such as education or skills was shown (Palazzi et al. 2020) to have superior entrepreneurial decision than others. It was inferred that with continual development of human capital, the employees can achieve performances, eventually enhancing the productivity of the organization (Massaro et al. 2015). Thus, the successful strategies should strongly focus on the competencies of human capital (Asiaei et al. 2020) that are linked to the acquired excellence of individual. The higher the human capital stock of an organization, the more successful it is, with higher competitive advantages (Budiarso 2019). Human capital increases with the accumulation of the employees’ specialized information, skills, and knowledge, enabling their efficient communications. This in turn lowers the chance of miscalculation in decision making, thus enhancing the quality and improving the organizational performances (Alhassan and Asare 2016). To sum up, the human capital of an organization is strongly correlated to the development of its performance.

3.2. Structural Capital

The element structural capital of an organization can be defined as a scheme and pattern that enable to set up better productivity of the employees (Hammad Ahmad Khan et al. 2016) wherein such structure remain intact even after the exit of the employees (Edvinsson 1997). Fundamentally, structural capital can be viewed as the supportive and useful infrastructure of the organization (Wu et al. 2007). It includes the procedures, policies, and systems that enable the employees to achieve their optimum productivity, helping them to enhance their capacity and performance (Stewart 1997). In addition, structural capital involves both the infrastructural assets and codified information (such as records, databases, and intellectual property rights) that shape up the company’s context for future sustenance (Buenechea-Elberdin 2017). The present work referred to the organizational concept of structural capital as the network properties and codified information dispersion within the organization (Sharabati et al. 2010).

It was affirmed that (Bontis 1998) structural capital holds the ownership of the intellectual property, which is very important for an organization in developing its human capital, implying that the structural capital is the way to add efficiency to the human capital to achieve optimum organizational performance (Hammad Ahmad Khan et al. 2016). In other words, a supportive environment is very important to exhaust human capital at its optimum level (Asiaei and Jusoh 2017). Structural capital provides supportive tools for human capital to strive for new opportunities (Chowdhury et al. 2018). In addition, structural capital can be considered the main contributor to a specific culture of an organization, which allows the manifestation of human capital during its operation (Widener 2006). Essentially, the structural capital serves as the knowledge directory shared among the employees working in an organization, enabling them to expand their capabilities to the maximum extent (Brown et al. 2007).

According to (Vladu et al. 2017), the information exchanges that make the reputable structure and procedure must conform with the developed and codified rules. Therefore, knowledge inherent to the structural capital tends to build up and must be used in a recognized manner (Budiarti 2017). Structural capital offers a setting that facilitates the organizations to produce and control knowledge (Benevene et al. 2017). An organization having weak systems and processes for tracking its activities may not achieve the targeted potential or goal in its performance (Sladjana Cabrilo et al. 2018). Conversely, an organization with a strong structural capital with compassionate culture can encourage its employees to attempt to discover state-of-the-art knowledge, thereby moving many steps ahead towards improved performance (Xu and Wang 2018).

Previous studies have suggested that the operational processes and commitment of the organizations help to provide sufficient resources that positively impact the performance (Mehralian et al. 2018). Furthermore, the operation, procedure and method of knowledge administration that propel the value-creative actions of the organizations have positive effects on the performances (Haris et al. 2019). Because the organizations are progressively using advanced technologies for competing with the current fluctuating economic conditions, extra care must be taken to properly manage the structural capital for attaining a good organizational performance (Al-Jinini et al. 2019). In this regard, the current study assumed that substantial investment in structural capital is anticipated to improve the performance of financial organizations. Previous studies indicated that an organization having weak procedures and systems for tracking its actions often fails to achieve competence regarding performance (De Luca et al. 2020). Conversely, an organization with a strong structural capital is expected to possess an encouraging work culture for employees that helps them to learn innovative knowledge with refined and improved performances (Asiaei et al. 2020).

3.3. Relational Capital

Relational capital is the capacity of a business or an organization for upholding its pleasant affiliation/union network with the partners (Cuozzo et al. 2017). Networking can be derived from both trustworthy and eminent suppliers and faithful and satisfied customers (Subramaniam and Youndt 2005). In addition, relational capital can be defined as the intangible assets based on the development, maintenance and promotion of high-class affiliations with any business, individuals and groups that affect the organization (Hsu and Wang 2012). Relational capital results from the interactions and collaborations among the employees within an organization through the knowledge and experiences they share with others (Elsetouhi et al. 2015), whereby constant change and innovation are driven by the interrelationships (Lamond et al. 2010). The relational capital of an organization can be defined (Ahn et al. 2003) as the resources connected to the outside relation with its customer, supplier, or partner.

It is the integration (Bonner and Walker 2004) of all the relationships of an organization that can be either internal (among administration and employees as well as amongst employees) or external (with stakeholders such as customers, suppliers and other bodies such as the government). Most of the organizations associated with the relevant and sensitive stakeholders such as customers/patients require direct intervention for the relational capital development. To reach this goal, good relationships must be established and improved between the main players to simplify/smooth out a way for obtaining better results or performance (Zollo et al. 2002).

The importance of relational capital relies on the ability to control programs, especially achieving complete recovery of the patients in the hospital/medication business (Lardo et al. 2017). In other words, the prolonged treatment and discomfort due to the side effects will make the patient likely to drop out of the treatment, thus declining the relational capital of the medical center. Hence, good management for the relational capital establishment is required. It was indicated that (Lenart 2015) maintenance of good relation with the customer and partner is a prerequisite for good organizational governance. Further significant aspects that influence the relational capital are the feedback and recognition of the customer; the partner needs to offer satisfactory service and uphold healthy relations, thus improving the customers reliability (Scafarto et al. 2016). A conceptualized relational capital of an organization that is depicted as the foundation for cooperative actions in the society has evolved over the past decades.

The characteristics of relational capital may vary significantly between the relations, subject to review and resources used in the relations (Černe and Etinger 2017). Any enhancement in the relational capital of the organization is an indication of the excellence of its employees and enriched knowledge exchange with collaborators (Bontis et al. 2018). Various studies on relational capital suggested the performance of an organization can be improved by involving the customers having intimate relationships with the organization (Al-Jinini et al. 2019). Several manufacturing firms are engaged themselves in intimate relations with the suppliers to use their skill, capability, and knowledge for developing novel and low-cost products at rapid space (Vătămănescu et al. 2019). Thus, friendly relations with the suppliers can positively affect the innovation performance of a manufacturing organization (Cabrilo and Dahms 2020). Based on these factors, this study assumed that relational capital positively affects the innovation performance.

3.4. Social Capital

Social capital refers to a valuable asset that ensures societal security and protection, thus allowing the empowerment of the organizations (Nahapiet and Ghoshal 1998). It can be defined (Allameh 2018a) as “the sum of the actual and potential resources embedded within, available through and derived from the network of relationships possessed by an individual or social unit”. Additionally, social capital denotes the total potential and actual wealth associated with the networks of relations presented by the social units of individuals (Salicru and Perryer 2007). Various reports indicated that social capital plays a vital role in fulfilling all the organizational needs for their survival in the existing competitive scenario worldwide (Bolino et al. 2002).

Social capital is essential for knowledge sharing, competitive advantage enhancement, organizational performance improvement, value creation, and overall organizational development (Li et al. 2019). Different models have been developed concerning the organizational concept of social capital due to its multidimensional characteristics (Abili 2011). Some researchers have exemplified that an organization’s significant breakthrough and competitive advantages are the cumulative outcomes of social capital due to the exchange of tacit and explicit knowledge through various networks within the organizations (Nevado et al. 2018). Thus, close attention must be paid to the development of the social capital of an organization to foster norms and values within the organization that enable healthy interactions, and facilitate strengthening of the relationships and collaborations among the employees (Christensen and Kowalczyk 2017).

It was acknowledged that social capital is an essential element for the innovation performance of an organization (Asiaei et al. 2020). Stable networks and healthy professional relationships can lead to higher levels of trust and goal accomplishment among members of the organizations, exhibiting a direct/positive relationship between their performance and sales growth (Hamad et al. 2019). Often, the internal and external collaborations and information exchanges across the social networks are essential in order to incorporate and synthesize the knowledge of the employees (Tseng et al. 2015). In this regard, it is perceived that social capital can be obtained from the network of relations of the individuals or social units (Stacchezzini et al. 2019). Some researchers believe that the outcomes of social capital could be gained through the exchange of tacit and explicit knowledge, mostly through the networks within the organizations, leading to their significant breakthrough and competitive advantages (Anifowose et al. 2017).

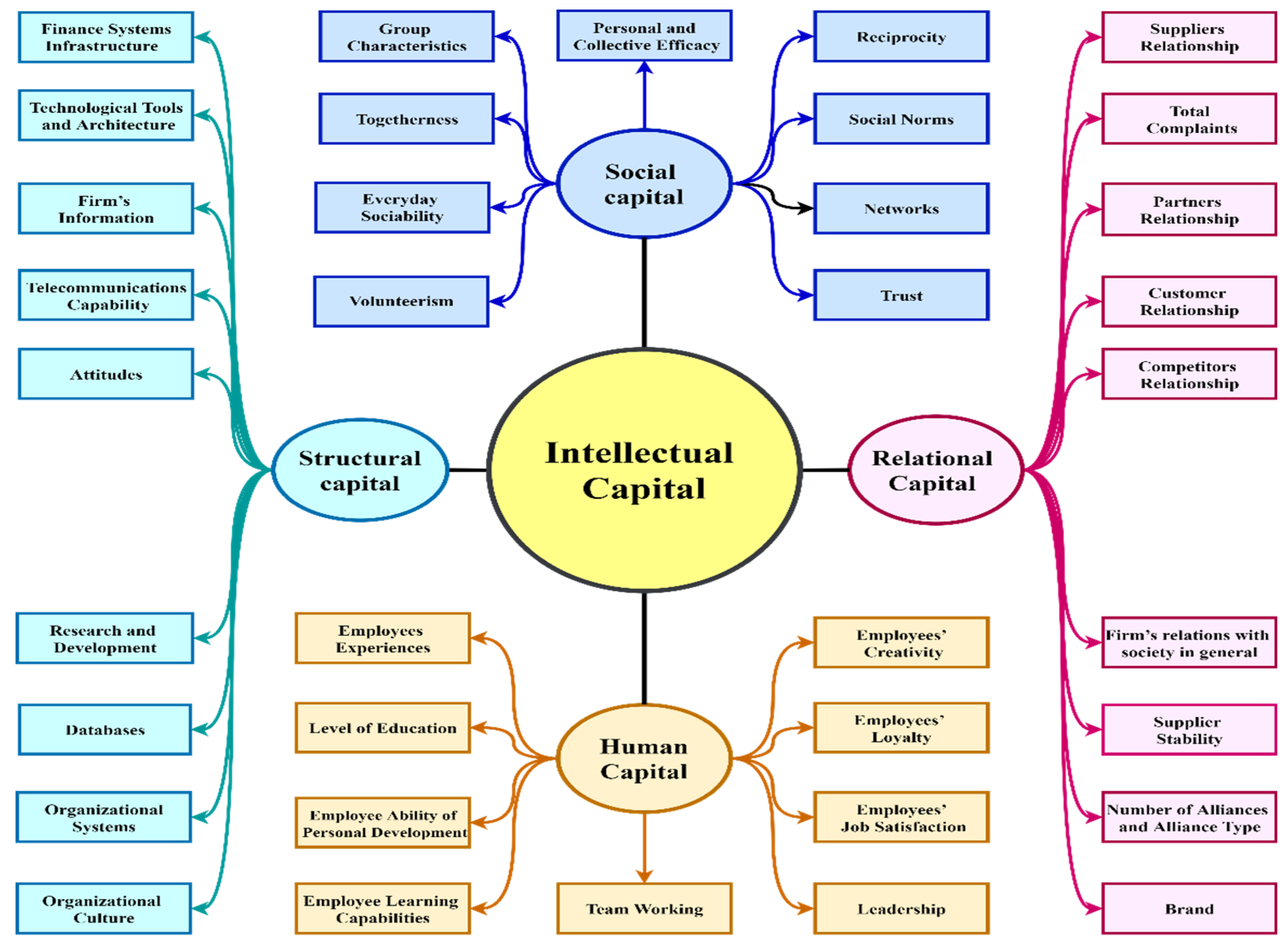

The main purpose of social capital is to empower the assembly and knowledge distributions across the value-chain of an organization, allowing interactions with other communities and businesses (García Lirios 2020). Meanwhile, it was mentioned that (Asiaei et al. 2020) the maintenance of relations by the employees are more precious than these employees. It was asserted that (Liu and Jiang 2020) for businesses, social relations are more significant compared to the resources, especially in the environments with strong networking. Thus, social capital allows the acquisition and generation of new knowledge by means of exterior and interior resources. In this rationale, the problem-solving approach can be polished by improving social capital, enhancing the organizational innovation performance (Al-Musali and Ismail 2015). Figure 3 displays the architecture of intellectual capital components within relevant constructs enclosing dominant components.

4. Innovation Performance

Innovation is considered the improvement or modernization in the creation of new ideas (Koryak et al. 2015) or the development and execution of better/professional work perspectives (Anderson et al. 2014). Thus, it materializes whenever individuals add some value in the commodities, services, processes, promotions, delivery systems, and policies which are incorporated to achieve companies benefits as well as stakeholders trustworthiness on the dealing companies (Shahzad et al. 2019). Thus, the present conceptualization of innovation performance aims to improve the value of the internal structures and processes of businesses, making new merchandise and better-quality service to fulfil the marketplace demands (Kamau and Oluoch 2016). (McDowell et al. 2018) agreed that knowledge and skillfulness of humans are the vital elements for the creation of innovations. Creative and knowledgeable employees generate new ideas or question the conventional programs that routinely run in the organization (Wang and Kafouros 2009; Wendra et al. 2019). The summation of the skillfulness and knowledge of human are the predictors for the organization’s innovation performance s2018). In this regard, innovation performance is regarded as an intermediary variable among some corporate process and overall performance of the organization, thereby facilitating a better depiction of activities and impacts that need to be attained within the organization (Li et al. 2019). Earlier studies disclosed a optimistic correlation among innovation and performance of an organization (Jabbouri et al. 2016). In addition, innovation performance was considered as a conditional parameter for any organization that determines the ultimate productivity (Cabrilo and Dahms 2020).

It was demonstrated that innovation can be a vital stimulating factor that promotes the qualities, effectiveness, profits and efficacies of the organizations (Dženopoljac et al. 2016). To attain continuous innovations, administrators of the organization must focus on various aspects including the procedure, production and technology together with the culture, value and regulations (Marlina and Tjahjadi 2019). Indeed, innovation significantly affects the organizations’ existence, competitiveness, and growth through its influence on customer satisfaction, employees’ productivity, service quality, companies share, market value, and customer retention. Hammad Ahmad Khan et al. 2016 indicated that the innovation performance could increase sales and market shares with considerable customer satisfaction. Additionally, the innovation can potentially generate economic value for the organizations, thereby increasing the profits and improving the performance (Cabrilo et al. 2018). Briefly, the innovation performance of any organization can be described as the degree to which the improvement process can successfully generate the outcomes, leading to novel or significantly improved products or services (Rosenbusch et al. 2019).

The national innovation system demands constant knowledge creation and transfer; thereby, innovation occurs and contributes to the economic growth of the country (Inkinen et al. 2017). Additionally, the innovation performance of the organizations is effective for promoting the capacity of the national innovation system (Hameed et al. 2018). In a national innovation system, innovation performance is considered synonymous with all the activities that enable measuring the technological innovation outcomes (Alford and Duan 2018). According to Amin and Aslam 2017, the productivities such as patents or number of state-of-the-art goods may be useful for measuring the innovation performance of the organization. It was also argued (Hameed et al. 2018) that the product development cost is a significant determinant for the innovation performance in the financial sector because the organizations invest substantial outlays to develop state-of-the-art goods, thus acquiring a competitive advantage in the targeted markets (Rosenbusch et al. 2019).

Several studies were conducted to evaluate the performance on financial measures that could be related to the primary objective of innovation in new product and service to increase the profits (Bogers et al. 2019). Performance indicators discussed in the literature are measured largely by the organization’s financial outcomes; however, there has been a revolution in performance measurement in the last ten years. The success of an innovation is seldom defined by a sole factor rather by several aspects. (Alford and Duan 2018; Isanzu 2017) argued that not a single factor but rather several aspects measure the success of innovation performance. Nevertheless, several aspects of the innovation such as increased customer loyalty are neglected by using only financial factors (Isanzu 2017). Measurements that rely only on financial data are being placed by integrated system which combines both financial and non-financial aspects (Rosenbusch et al. 2019).

Studies on innovation performance in recent years have received focused attention due to its multidimensional nature. It was indicated that (Gimenez-Fernandez et al. 2020) for the enhanced economic advancement, innovations and productions play a significant role. Therefore, the national innovation systems particularly the financial sectors require constant knowledge creation and transferring. The innovation was shown to contribute to the economic progress in the developing nations (Samson et al. 2017). Basically, innovation performance is effectual to promote the development of national financial system capacity in relation to various intellectual capital properties (Kamau and Oluoch 2016). It was asserted that (Amin and Aslam 2017) the detail information related to the sectoral aspects remains deficient. So far, fewer studies have been conducted to reveal a close connection between innovation and growing value of the performance in the financial sector. In order to increase the economic share a significant workforce is required for the expansion of company (Babelytė-Labanauskė and Nedzinskas 2017). In addition, the studies on the practical operations related to the successful of innovation performance in different economic subsectors are lacking (Shahzad et al. 2019). From the abovementioned discussions, it is clear that multidimensional services and viewpoints that constitute the innovation require further systematic analysis to develop a correlation among intellectual capital components and innovation performance (Buenechea-Elberdin et al. 2018). Thus, this paper contributes to the financial sector by emphasizing the impacts of intellectual capital components on innovation performance.

5. Challenges of Intellectual Capital

An attempt is made to improve the understanding concerning the importance and implications of employees’ intellectual capital components in the financial sector. This knowledge is relevant to attain better innovation performance in the financial and accounting practices of different organizations. Due to the deficiency in number of papers in the cited topic, this article may not fully clarify or explore the issues related to the impacts of intellectual capital components possessed by the employees of an organization on its innovation performance (Abdullah et al. 2015; Ramadan et al. 2017; Aminu and Mahmood 2015; Singh and Rao 2016; Thanh Nhon et al. 2020; Jordão and de Almeida 2017; Pedro et al. 2018b; Asiaei et al. 2020; Wendra et al. 2019; Li et al. 2019). Hence, the article reviewed the previous works systematically to validate the claims concerning the shortage of intellectual capital practices and its necessity for innovation performance of an organization (Souza and Takahashi 2019; Alonso and Kok 2020; Breznik et al. 2019; Khan et al. 2021; Furnival et al. 2019). In addition, it focused on the impacts of those capabilities in developing innovation performance in the financial sector. The main objective is to uncover the theoretical perspectives and practical impacts of intellectual capital components in terms of scientific, and statistical measures, thus developing a better understanding of intellectual capital components and innovation performance relationship. The challenges faced by various organizations to develop the intellectual capital components are also highlighted (Cenciarelli et al. 2018; Sardo and Serrasqueiro 2017; Januškaitė and Užienė 2018; Tran and Vo 2018; Ramírez et al. 2017; Engelman and Fracasso 2017).

No studies have been carried out to accurately quantify the impact of intellectual capital components on innovation performance of an organization, although it was hinted that several factors of the financial sector are responsible which inhibit the exact measurement of the possession of its intellectual capital properties. First, appropriate inputs regarding the intellectual capital property of the employees are needed for formulating and implementing the strategies of intellectual capital development. Because plans and strategies are required for making decisions and updating the prevailing reporting procedures that incorporate data related to intellectual properties. Last, precise assessment of intellectual property requires constant investigations to improve innovation performance in the financial practice. All these challenges made the financial institutions unable to develop the intellectual capital properties for their employees. Thus, proper measurement tools are required to quantify the full capacity of intangible capital of an organization that leads to it growth and value creation.

The difficulty of determining the real contributions of the selected organization and validating the levels of intellectual capital property of its employees are underscored. It was affirmed that (Giuliani 2016) the presence of sense-making and sense-giving processes may not produce accurate results because of the complexity of the relationship between intellectual capital components. Some reports (Otcenášková and Bureš 2018; Vaz et al. 2019) indicated that despite the availability of empirical suggestions on the differences in resource distribution among intellectual capital components, the advantages associated with each intellectual capital components, as well as their complexity and diversity towards solving these issues, are yet to be addressed in research studies (Ali et al. 2020b). Therefore, the level of intellectual capital components can positively impact the financial performance, making accurate measurement of intellectual capital components challenging. It has been suggested as future works in many studies since the measurement of intellectual capital in any organization implies the measurement of the performance and productivity in the organization, specifically the financial sector.

6. Conclusions and Limitation

This communication has provided evidence that intellectual capital components can immensely contribute to the innovation performance of financial organization wherein inclusion and exclusion criteria were used in the reviewing process. It explored various relevant constructs based on multidimensional views of the financial sector in terms of three aspects. First, possession of intellectual capital components by a financial organization was shown to improve its innovation performance via the interaction and combination of appropriate constructs. Second, this relation was frequently explained as separate indicators for overall economic growth of the company. Last, strong practical implication was found to exist concerning the impact of intellectual capital components on the organization’s innovation performance and other qualities of improvements. It was inferred that the diverse challenges encountered by the financial sector to maintain a high level of intellectual capital can be mainly due to the deficiency of appropriate measurement methods (Meles et al. 2016; Mention and Bontis 2013). Only a few reports in the literature analyzed the issues related to the development of various intellectual capital components (human, structural, relational, social). In this respect, this article substantiated the outlook that appropriate constructs must be combined to maintain high innovation performance in the financial sector. This enables us to obtain a better understanding of the knowledge-based interpretation of innovation performance, emphasizing the need for assessing the impact of intellectual capital components in the financial sector to gain competitive advantages (Sharma and Dharni 2017; Abhayawansa and Guthrie 2016; Anifowose et al. 2018).

To determine a significant correlation amongst intellectual capital components and innovation performance in the financial sector various concepts must be combined. As revealed by many empirical studies, proper implementation of intellectual capital components concept in the banking sectors in different countries was found to contribute positively on innovation performance (Forte et al. 2017; Cabrilo et al. 2018; Mention and Bontis 2013; Meles et al. 2016). Although the research interests on the significance and measure of intellectual capital components development in the financial and accounting fields have been increasing, quantitative studies on intellectual capital components and innovation performance correlation are limited. Therefore, it is essential to foster some novel empirical and theoretical method to evaluate effects of intellectual capital components on the organization’s innovation performance, wherein, smart and combined plans can be useful to manage various intangible assets, promoting the sustainability, economic prospects and productivity of the regions. Amongst all the intellectual capital components, human capital was observed to contribute the most in achieving a high level of innovation performance. It can be concluded that knowledge-based interactions of the employees of an organization lead to more productivity, new values and wealth creation, helping the company to take competitive advantages and become more sustainable.

Based on the limited number of available journal papers of national and international repute, this review established three major aspects. First, a rudimentary insight concerning the positive effects of intellectual capital components on the financial company’s innovation performance was provided based on multi-dimensional analysis of the existing state-of-the-art reports. Second, it may serve as taxonomy for the researchers navigating into the field of intellectual capital components and innovation performance correlation. Third, this in-depth analysis on the identification and implementation of intellectual capital components in the financial sectors (public and private) may facilitate their managers to make wise decisions and meticulous strategies using the intellectual capital perception to control qualities of services and productivity, leading to improved innovation performance. Additionally, for the first time, we emphasized the necessity to strengthen the empirical investigations at the regional and national levels to accomplish better understanding of intellectual capital components and innovation performance relationships.

In brief, this paper has demonstrated the significance of the innovation performance assessment of an organization, based on the interactions of four intellectual capital components. It was found that the level of intellectual capital is intimately related to their degree of uses. It was shown that financial organizations’ reliance on intellectual capital components had a strong impact on their innovation performance in the banks. Intellectual capital components of any organization are useful maintaining knowledge-based wealth, trustworthiness and values. Thus, it is recommended that various organizations worldwide must emphasize intellectual capital components development for long-term sustenance and value-chain creation. Furthermore, the national and regional public policies must be reformed to include the aspects of intellectual capital components for their economic growth.

Undoubtedly, intellectual capital is a significant factor for the creation of values in the organization, region and nation, wherein strong participation of government is required to obtain easy access to data information and structure. This will not only enhance the articulation of knowledge transfer among the academics and the public, but will immensely help the organization’s administrator and policy makers to improve the performance and values. We only focused on the reported empirical studies, which is the main limitation. The other limitation was related to the deficiency of efficient analyses of various indicators used to measure the obtained samples. It is claimed that to obtain more knowledge of intellectual capital components’ impact on innovation performance, it is worthwhile to focus on the national and regional systems which may contribute considerably to the policies of organizations. This in turn will facilitate in fostering the intangible asset-based improved performance, efficient governance to make the organization more competitive and sustainable.

Author Contributions

Conceptualization, M.A.A., N.H., H.H., R.A.-A. and I.A.A.; methodology, M.A.A. and N.H.; formal analysis M.A.A., N.H., H.H., R.A.-A. and I.A.A.; investigation, M.A.A. and N.H.; resources, M.A.A. and N.H.; writing original draft preparation, M.A.A.; writing review and editing, M.A.A. and N.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

The authors are grateful to the editor and the anonymous reviewers for providing very constructive and useful comments that enabled us to make additional efforts to improve the clarity and quality of our research.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abdullah, D. F., S. Sofian, and N. H. Bajuri. 2015. Intellectual Capital as the Essence of Sustainable Corporate Performance. Pertanika Journal of Social Science and Humanities 23: 131–44. [Google Scholar]

- Abhayawansa, Subhash, and James Guthrie. 2016. Drivers and Semantic Properties of Intellectual Capital Information in Sell-Side Analysts’ Reports. Journal of Accounting and Organizational Change 12: 434–71. [Google Scholar] [CrossRef]

- Abili, Khodayar. 2011. Social Capital Management in Iranian Knowledge-Based Organizations. Electronic Journal of Knowledge Management 9: 203–10. [Google Scholar]

- Agostini, Lara, and Anna Nosella. 2017. Enhancing Radical Innovation Performance through Intellectual Capital Components. Journal of Intellectual Capital 18: 789–806. [Google Scholar] [CrossRef]

- Agostini, Lara, Anna Nosella, and Roberto Filippini. 2017. Does Intellectual Capital Allow Improving Innovation Performance? A Quantitative Analysis in the SME Context. Journal of Intellectual Capital 18: 400–18. [Google Scholar] [CrossRef]

- Ahn, M. H., S. Aoki, H. Bhang, S. Boyd, D. Casper, J. H. Choi, S. Fukuda, Y. Fukuda, W. Gajewski, and T. Hara. 2003. Indications of Neutrino Oscillation in a 250 Km Long-Baseline Experiment. Physical Review Letters 90: 41801. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Alford, Philip, and Yanqing Duan. 2018. Understanding Collaborative Innovation from a Dynamic Capabilities Perspective. International Journal of Contemporary Hospitality Management 30: 2396–416. [Google Scholar] [CrossRef] [Green Version]

- Alhassan, Abdul Latif, and Nicholas Asare. 2016. Intellectual Capital and Bank Productivity in Emerging Markets: Evidence from Ghana. Management Decision 54: 589–609. [Google Scholar] [CrossRef]

- Ali, Mostafa A., Nazimah Hussin, Ibtihal A. Abed, Bilal Khalid Khalaf, and Ayat Nader. 2020a. Systematic Literature Review of Intellectual Capital Components (Multi-View). no. 4682. [Google Scholar]

- Ali, Mostafa A., Nazimah Hussin, Ibtihal A. Abed, Rafidah Othman, and Mohammed A. Mohammed. 2020b. Analysis and Measurement of Human Capital Based on Multi-Criteria Decision-Making (MCDM) Technique. Technology Reports of Kansai University 62: 4799–825. [Google Scholar]

- Ali, Mostafa A., Nazimah Hussin, Ibtihal A. Abed, Rafidah Othman, and Nazahan Qahatan. 2020c. Systematic Review of Intellectual Capital and Firm Performance. Technology Reports of Kansai University 62: 4199–216. [Google Scholar]

- Ali, Mostafa A., Nazimah Hussin, H. K. Jabbar, Ibtihal A. Abed, Rafidah Othman, and A. Mohammed. 2020d. Intellectual Capital and Firm Performance Classification and Motivation: Systematic Literature Review. TEST Engineering & Management 3: 28691–703. [Google Scholar]

- Al-Jinini, Dina Khalid, Samer Eid Dahiyat, and Nick Bontis. 2019. Intellectual Capital, Entrepreneurial Orientation, and Technical Innovation in Small and Medium-Sized Enterprises. Knowledge and Process Management 26: 69–85. [Google Scholar] [CrossRef]

- Allameh, Sayyed Mohsen. 2018a. Antecedents and Consequences of Intellectual Capital: The Role of Social Capital, Knowledge Sharing and Innovation. Journal of Intellectual Capital 19: 858–74. [Google Scholar] [CrossRef]

- Al-Musali, Mahfoudh Abdul Karem, and Ku Nor Izah Ku Ismail. 2015. Intellectual Capital and Its Effect on Financial Performance of Banks: Evidence from Saudi Arabia. Procedia—Social and Behavioral Sciences 164: 201–7. [Google Scholar] [CrossRef] [Green Version]

- Alonso, Abel Duarte, and Seng Kiat Kok. 2020. Sensing, Seizing and Reconfiguring: Understanding Wine Tourism Development in Emerging Economies through the Dynamic Capabilities Approach. Tourism Analysis 25: 2–3. [Google Scholar] [CrossRef]

- Aluchna, Maria, Iryna Kytsyuk, and Maria Roszkowska-Menkes. 2018. The Evolution of Non-Financial Reporting in Poland. Przegląd Organizacji 10: 3–9. [Google Scholar] [CrossRef]

- Amin, Shahid, and Shoaib Aslam. 2017. Intellectual Capital, Innovation and Firm Performance of Pharmaceuticals: A Study of the London Stock Exchange. Journal of Information & Knowledge Management 16: 1750017. [Google Scholar] [CrossRef]

- Aminu, Mohammed Ibrahim, and Rosli Mahmood. 2015. Mediating Role of Dynamic Capabilities on the Relationship between Intellectual Capital and Performance: A Hierarchical Component Model Perspective in PLS-SEM Path Modeling. Research Journal of Business Management 9: 443–56. [Google Scholar] [CrossRef]

- Anderson, Neil, Kristina Potočnik, and Jing Zhou. 2014. Innovation and Creativity in Organizations: A State-of-the-Science Review, Prospective Commentary, and Guiding Framework. Journal of Management 40: 1297–333. [Google Scholar] [CrossRef] [Green Version]

- Anifowose, Mutalib, Hafiz Majdi Abdul Rashid, and Hairul Azlan Annuar. 2017. Intellectual Capital Disclosure and Corporate Market Value: Does Board Diversity Matter? Journal of Accounting in Emerging Economies 7: 369–98. [Google Scholar] [CrossRef]

- Anifowose, Mutalib, Hafiz Majdi Abdul Rashid, Hairul Azlan Annuar, and Hassan Ibrahim. 2018. Intellectual Capital Efficiency and Corporate Book Value: Evidence from Nigerian Economy. Journal of Intellectual Capital 19: 644–68. [Google Scholar] [CrossRef] [Green Version]

- Ansari, Reza, Azar Barati, and Ali Akbar Abedi Sharabiani. 2016. The Role of Dynamic Capability in Intellectual Capital and Innovative Performance. International Journal of Innovation and Learning 20: 47–67. [Google Scholar] [CrossRef]

- Asiaei, Kaveh, and Ruzita Jusoh. 2015. A Multidimensional View of Intellectual Capital: The Impact on Organizational Performance. Management Decision 53: 668–97. [Google Scholar] [CrossRef] [Green Version]

- Asiaei, Kaveh, and Ruzita Jusoh. 2017. Using a Robust Performance Measurement System to Illuminate Intellectual Capital. International Journal of Accounting Information Systems 26: 1–19. [Google Scholar] [CrossRef]

- Asiaei, Kaveh, Omid Barani, Nick Bontis, and Maryam Arabahmadi. 2020. Unpacking the Black Box: How Intrapreneurship Intervenes in the Intellectual Capital-Performance Relationship? Journal of Intellectual Capital 21: 809–34. [Google Scholar] [CrossRef]

- Asiaei, Kaveh, Nick Bontis, Raziye Alizadeh, and Mehdi Yaghoubi. 2021. Green Intellectual Capital and Environmental Management Accounting: Natural Resource Orchestration in Favor of Environmental Performance. Business Strategy and the Environment, 1–18. [Google Scholar] [CrossRef]

- Babelytė-Labanauskė, Kristina, and Šarunas Nedzinskas. 2017. Dynamic Capabilities and Their Impact on Research Organizations’ R&D and Innovation Performance. Journal of Modelling in Management 12: 603–30. [Google Scholar] [CrossRef]

- Benevene, Paula, Eric Kong, Barbara Barbieri, Massimiliano Lucchesi, and Michela Cortini. 2017. Representation of Intellectual Capital’s Components amongst Italian Social Enterprises. Journal of Intellectual Capital 18: 564–87. [Google Scholar] [CrossRef]

- Berezinets, Irina, Tatiana Garanina, and Yulia Ilina. 2016. Intellectual Capital of a Board of Directors and Its Elements: Introduction to the Concepts. Journal of Intellectual Capital 17: 632–53. [Google Scholar] [CrossRef]

- Bogdan, Victoria, Claudia Diana Sabău Popa, Mărioara Beleneşi, Vasile Burja, and Dorina Nicoleta Popa. 2017. Empirical Analysis of Intellectual Capital Disclosure and Financial Performance—Romanian Evidence. Economic Computation and Economic Cybernetics Studies and Research 51: 125–43. [Google Scholar]

- Bogers, Marcel, Henry Chesbrough, Sohvi Heaton, and David J. Teece. 2019. Strategic Management of Open Innovation: A Dynamic Capabilities Perspective. California Management Review 62: 77–94. [Google Scholar] [CrossRef]

- Bolino, Mark C., William H. Turnley, and James M. Bloodgood. 2002. Citizenship Behavior and the Creation of Social Capital in Organizations. Academy of Management Review 27: 505–22. [Google Scholar] [CrossRef]

- Bonner, Joseph M., and Orville C. Walker Jr. 2004. Selecting Influential Business-to-business Customers in New Product Development: Relational Embeddedness and Knowledge Heterogeneity Considerations. Journal of Product Innovation Management 21: 155–69. [Google Scholar] [CrossRef]

- Bontis, Nick. 1998. Intellectual Capital: An Exploratory Study That Develops Measures and Models. Management Decision 36: 63–76. [Google Scholar] [CrossRef] [Green Version]

- Bontis, Nick, Christopher Bart, Robert G. Isaac, Irene M. Herremans, and Theresa J. B. Kline. 2009. Intellectual Capital Management: Pathways to Wealth Creation. Journal of Intellectual Capital 10: 81–92. [Google Scholar]

- Bontis, Nick, Massimo Ciambotti, Federica Palazzi, and Francesca Sgro. 2018. Intellectual Capital and Financial Performance in Social Cooperative Enterprises. Journal of Intellectual Capital 19: 712–31. [Google Scholar] [CrossRef]

- Borenstein, M., L. V. Hedges, J. P. T. Higgins, and H. R. Rothstein. 2009. Prediction Intervals. In Introduction to Meta-Analysis. New York: Taylor & Francis, pp. 127–33. [Google Scholar]

- Bracci, Enrico, Luca Papi, Michele Bigoni, Enrico Deidda Gagliardo, and Hans-Jürgen Bruns. 2019. Public Value and Public Sector Accounting Research: A Structured Literature Review. Journal of Public Budgeting, Accounting & Financial Management 31: 103–36. [Google Scholar]

- Breznik, Lidija, Matej Lahovnik, and Vlado Dimovski. 2019. Exploiting Firm Capabilities by Sensing, Seizing and Reconfiguring Capabilities: An Empirical Investigation. Economic & Business Review 21: 1. [Google Scholar] [CrossRef]

- Brown, A. W., J. D. Adams, and A. A. Amjad. 2007. The Relationship between Human Capital and Time Performance in Project Management: A Path Analysis. International Journal of Project Management 25: 77–89. [Google Scholar] [CrossRef]

- Budiarso, Novi Swandari. 2019. Intellectual Capital in Public Sector. Accountability 8: 42. [Google Scholar] [CrossRef]

- Budiarti, Isniar. 2017. Knowledge Management and Intellectual Capital-A Theoretical Perspective of Human Resource Strategies and Practices. European Journal of Economics and Business Studies 3: 148–55. [Google Scholar] [CrossRef] [Green Version]

- Buenechea-Elberdin, Marta. 2017. Structured Literature Review about Intellectual Capital and Innovation. Journal of Intellectual Capital 18: 262–85. [Google Scholar] [CrossRef] [Green Version]

- Buenechea-Elberdin, Marta, Josune Sáenz, and Aino Kianto. 2018. Knowledge Management Strategies, Intellectual Capital, and Innovation Performance: A Comparison between High-and Low-Tech Firms. Journal of Knowledge Management 22: 1757–81. [Google Scholar] [CrossRef]

- Cabrilo, Slaðana, and Sven Dahms. 2020. The Role of Multidimensional Intellectual Capital and Organizational Learning Practices in Innovation Performance. European Management Review 17: 835–55. [Google Scholar] [CrossRef]

- Cabrilo, Sladjana, Aino Kianto, and Bojana Milic. 2018. The Effect of IC Components on Innovation Performance in Serbian Companies. VINE Journal of Information and Knowledge Management Systems 48: 448–66. [Google Scholar] [CrossRef]

- Cenciarelli, Velia Gabriella, Giulio Greco, and Marco Allegrini. 2018. Does Intellectual Capital Help Predict Bankruptcy? Journal of Intellectual Capital 19: 321–37. [Google Scholar] [CrossRef]

- Černe, Ksenija, and Darko Etinger. 2017. IT as a Part of Intellectual Capital and Its Impact on the Performance of Business Entities. Croatian Operational Research Review 7: 389–408. [Google Scholar] [CrossRef] [Green Version]

- Chen, Jin, Xiaoting Zhao, and Yuandi Wang. 2015. A New Measurement of Intellectual Capital and Its Impact on Innovation Performance in an Open Innovation Paradigm. International Journal of Technology Management 67: 1–25. [Google Scholar] [CrossRef]

- Chowdhury, Leena Afroz Mostofa, Tarek Rana, Mahmuda Akter, and Mahfuzul Hoque. 2018. Impact of Intellectual Capital on Financial Performance: Evidence from the Bangladeshi Textile Sector. Journal of Accounting and Organizational Change 14: 429–54. [Google Scholar] [CrossRef]

- Christensen, Bent Jesper, and Carsten Kowalczyk. 2017. Globalization: Strategies and Effects. Globalization: Strategies and Effects, 1–617. [Google Scholar] [CrossRef]

- Coleman, James S. 1988. Social Capital in the Creation of Human Capital. American Journal of Sociology 94: S95–S120. [Google Scholar] [CrossRef]

- Cuozzo, Benedetta, John Dumay, Matteo Palmaccio, and Rosa Lombardi. 2017. Intellectual Capital Disclosure: A Structured Literature Review. Journal of Intellectual Capital 18: 9–28. [Google Scholar] [CrossRef]

- Daou, Alain, Egide Karuranga, and Zhan Su. 2014. Towards a Better Understanding of Intellectual Capital in Mexican SMEs. Journal of Intellectual Capital 15: 316–32. [Google Scholar] [CrossRef]

- De Luca, Francesco, Andrea Cardoni, Ho-Tan-Phat Phan, and Evgeniia Kiseleva. 2020. Does Structural Capital Affect SDGs Risk-Related Disclosure Quality? An Empirical Investigation of Italian Large Listed Companies. Sustainability 12: 1776. [Google Scholar] [CrossRef] [Green Version]

- Deltorn, Jean-Marc. 2017. Deep Creations: Intellectual Property and the Automata. Frontiers in Digital Humanities 4: 3. [Google Scholar] [CrossRef] [Green Version]

- Dixon-Woods, Mary. 2010. Why Is Patient Safety so Hard? A Selective Review of Ethnographic Studies. Journal of Health Services Research & Policy 15: 11–16. [Google Scholar]

- Dženopoljac, Vladimir, Stevo Janoševic, and Nick Bontis. 2016. Intellectual Capital and Financial Performance in the Serbian ICT Industry. Journal of Intellectual Capital 17: 373–96. [Google Scholar] [CrossRef]

- Dzenopoljac, Vladimir, Chadi Yaacoub, Nasser Elkanj, and Nick Bontis. 2017. Impact of Intellectual Capital on Corporate Performance: Evidence from the Arab Region. Journal of Intellectual Capital 18: 884–903. [Google Scholar] [CrossRef]

- Edvinsson, Leif. 1997. Developing Intellectual Capital at Skandia. Long Range Planning 30: 366–73. [Google Scholar] [CrossRef]

- Elsetouhi, Ahmed, Ibrahim Elbeltagi, and Mohamed Yacine Haddoud. 2015. Intellectual Capital and Innovations: Is Organisational Capital a Missing Link in the Service Sector? International Journal of Innovation Management 19: 1550020. [Google Scholar] [CrossRef]

- Engelman, Raquel Machado, and Edi Madalena Fracasso. 2017. Intellectual Capital, Absorptive Capacity and Product Innovation. Management Decision. no. 2001. [Google Scholar] [CrossRef]

- Ferreira, António, and Mário Franco. 2017. Strategic Alliances, Intellectual Capital and Organisational Performance in Technology-Based SMEs: Is There Really a Connection? International Journal of Business and Globalisation 18: 130–51. [Google Scholar] [CrossRef]

- Ferreira, Jorge, Arnaldo Coelho, and Luiz Moutinho. 2020. Dynamic Capabilities, Creativity and Innovation Capability and Their Impact on Competitive Advantage and Firm Performance: The Moderating Role of Entrepreneurial Orientation. Technovation 92: 102061. [Google Scholar] [CrossRef]

- Forte, William, Jon Tucker, Gaetano Matonti, and Giuseppe Nicolò. 2017. Measuring the Intellectual Capital of Italian Listed Companies. Journal of Intellectual Capital 18: 710–32. [Google Scholar] [CrossRef] [Green Version]

- Furnival, Joy, Ruth Boaden, and Kieran Walshe. 2019. A Dynamic Capabilities View of Improvement Capability. Journal of Health Organization and Management 33: 821–34. [Google Scholar] [CrossRef]

- Gallagher, Kevin P., and Vickie Coleman Gallagher. 2012. Organizing for Post-Implementation ERP: A Contingency Theory Perspective. Journal of Enterprise Information Management 25: 170–85. [Google Scholar] [CrossRef] [Green Version]

- García Lirios, Cruz. 2020. Specification a Model for Study of Intellectual Capital. Behavior Studies in Organizations 3: 1–4. [Google Scholar] [CrossRef]

- Gimenez-Fernandez, Elena M., Francesco D. Sandulli, and Marcel Bogers. 2020. Unpacking Liabilities of Newness and Smallness in Innovative Start-Ups: Investigating the Differences in Innovation Performance between New and Older Small Firms. Research Policy 49: 104049. [Google Scholar] [CrossRef]

- Giuliani, Marco. 2016. Sensemaking, Sensegiving and Sensebreaking: The Case of Intellectual Capital Measurements. Journal of Intellectual Capital 17: 218–37. [Google Scholar] [CrossRef]

- Gough, David. 2007. Weight of Evidence: A Framework for the Appraisal of the Quality and Relevance of Evidence. Research Papers in Education 22: 213–28. [Google Scholar] [CrossRef]

- Hamad, Ahmed Abdulqader, Şule Tuzlukaya, and Erdem Kırkbeşoğlu. 2019. The Effect of Social Capital on Operational Performance: Research in Banking Sector in Erbil. Copernican Journal of Finance & Accounting 8: 101. [Google Scholar] [CrossRef]

- Hameed, Waseem Ul, Muhammad Farhan Basheer, Jawad Iqbal, Ayesha Anwar, and Hafiz Khalil Ahmad. 2018. Determinants of Firm’s Open Innovation Performance and the Role of R & D Department: An Empirical Evidence from Malaysian SME’s. Journal of Global Entrepreneurship Research 8: 1–20. [Google Scholar]

- Hammad Ahmad Khan, Hafizah, Mahazril Aini Yaacob, Hussin Abdullah, and Siti Hajar Abu Bakar Ah. 2016. Factors Affecting Performance of Co-Operatives in Malaysia. International Journal of Productivity and Performance Management 65: 641–71. [Google Scholar] [CrossRef] [Green Version]

- Haris, Muhammad, HongXing Yao, Gulzara Tariq, Ali Malik, and Hafiz Javaid. 2019. Intellectual Capital Performance and Profitability of Banks: Evidence from Pakistan. Journal of Risk and Financial Management 12: 56. [Google Scholar] [CrossRef] [Green Version]

- Heaton, Sohvi, Donald S. Siegel, and David J. Teece. 2019. Universities and Innovation Ecosystems: A Dynamic Capabilities Perspective. Industrial and Corporate Change 28: 921–39. [Google Scholar] [CrossRef]

- Higgins, J. P. T., and S. Green. 2009. CCHB Cochrane Handbook for Systematic Reviews of Interventions. Cincinnati: CCHB. [Google Scholar]

- Hsu, Li-Chang, and Chao-Hung Wang. 2012. Clarifying the Effect of Intellectual Capital on Performance: The Mediating Role of Dynamic Capability. British Journal of Management 23: 179–205. [Google Scholar] [CrossRef]

- Iivari, Juhani, Rudy Hirschheim, and Heinz K Klein. 1998. A Paradigmatic Analysis Contrasting Information Systems Development Approaches and Methodologies. Information Systems Research 9: 164–93. [Google Scholar] [CrossRef] [Green Version]

- Inkinen, Henri, Aino Kianto, Mika Vanhala, and Paavo Ritala. 2017. Structure of Intellectual Capital–an International Comparison. Accounting, Auditing & Accountability Journal 30: 1160–83. [Google Scholar]

- Isanzu, Janeth N. 2017. The Relationship between Intellectual Capital and Financial Performance of Banks in Tanzania. Journal on Innovation and Sustainability 7: 28. [Google Scholar] [CrossRef] [Green Version]

- Jabbouri, Nada Ismaeel, Rusinah Siron, Ibrahim Zahari, and Mahmoud Khalid. 2016. Impact of Information Technology Infrastructure on Innovation Performance: An Empirical Study on Private Universities in Iraq. Procedia Economics and Finance 39: 861–69. [Google Scholar] [CrossRef] [Green Version]

- Januškaitė, Virginija, and Lina Užienė. 2018. Intellectual Capital as a Factor of Sustainable Regional Competitiveness. Sustainability 10: 4848. [Google Scholar] [CrossRef] [Green Version]

- Jordão, Ricardo Vinícius Dias, and Vander Ribeiro de Almeida. 2017. Performance Measurement, Intellectual Capital and Financial Sustainability. Journal of Intellectual Capital 18: 643–66. [Google Scholar] [CrossRef]

- Kamau, Daniel Mwangi, and Josphat Oluoch. 2016. Relationship between Financial Innovation and Commercial Bank Performance in Kenya. International Journal of Social Sciences and Information Technology 2: 34–47. [Google Scholar]

- Kengatharan, Navaneethakrishnan. 2019. A Knowledge-Based Theory of the Firm: Nexus of Intellectual Capital, Productivity and Firms’ Performance. International Journal of Manpower 40: 1056–74. [Google Scholar] [CrossRef]

- Khan, Owais, Tiberio Daddi, and Fabio Iraldo. 2021. Sensing, Seizing, and Reconfiguring: Key Capabilities and Organizational Routines for Circular Economy Implementation. Journal of Cleaner Production 287: 125565. [Google Scholar] [CrossRef]

- Koryak, Oksana, Kevin F. Mole, Andy Lockett, James C. Hayton, Deniz Ucbasaran, and Gerard P. Hodgkinson. 2015. Entrepreneurial Leadership, Capabilities and Firm Growth. International Small Business Journal 33: 89–105. [Google Scholar] [CrossRef]

- Lamond, David, Yi-Chun Huang, and Yen-Chun Jim Wu. 2010. Intellectual Capital and Knowledge Productivity: The Taiwan Biotech Industry. Management Decision 48: 580–99. [Google Scholar]

- Lardo, Alessandra, John Dumay, Raffaele Trequattrini, and Giuseppe Russo. 2017. Social Media Networks as Drivers for Intellectual Capital Disclosure: Evidence from Professional Football Clubs. Journal of Intellectual Capital 18: 63–80. [Google Scholar] [CrossRef]

- Lenart, Regina. 2015. Relational Capital for Managing the Uncertainty of the Environment. Zeszyty Naukowe/Wyższa Szkoła Oficerska Wojsk Lądowych Im. Gen. T. Kościuszki, 58–68. [Google Scholar] [CrossRef]

- Li, Yongfu, Yu Song, Jinxin Wang, and Chengwei Li. 2019. Intellectual Capital, Knowledge Sharing, and Innovation Performance: Evidence from the Chinese Construction Industry. Sustainability 11: 2713. [Google Scholar] [CrossRef] [Green Version]

- Liu, Chih-Hsing, and Jing-Feng Jiang. 2020. Assessing the Moderating Roles of Brand Equity, Intellectual Capital and Social Capital in Chinese Luxury Hotels. Journal of Hospitality and Tourism Management 43: 139–48. [Google Scholar] [CrossRef]

- Manes Rossi, Francesca, Francesca Citro, Marco Bisogno, Francesca Manes Rossi, Francesca Citro, and Marco Bisogno. 2016. Intellectual Capital in Action: Evidence from Italian Local Governments. Journal of Intellectual Capital 17: 696–713. [Google Scholar] [CrossRef]

- Manes-Rossi, Francesca, Giuseppe Nicolò, and Daniela Argento. 2020. Non-Financial Reporting Formats in Public Sector Organizations: A Structured Literature Review. Journal of Public Budgeting, Accounting & Financial Management 32: 639–69. [Google Scholar]

- Marlina, Evi, and Bambang Tjahjadi. 2019. Relationship between Management Accounting Innovations and Cost Performance in University. In International Conference of CELSciTech 2019-Social Sciences and Humanities Track (ICCELST-SS 2019). Amsterdam: Atlantis Press. [Google Scholar]

- Massaro, Maurizio, John Dumay, and Carlo Bagnoli. 2015. Where There Is a Will There Is a Way: IC, Strategic Intent, Diversification and Firm Performance. Journal of Intellectual Capital 16: 490–517. [Google Scholar] [CrossRef]

- Massaro, Maurizio, John Dumay, and James Guthrie. 2016. On the Shoulders of Giants: Undertaking a Structured Literature Review in Accounting. Accounting, Auditing & Accountability Journal 29: 767–801. [Google Scholar]

- McDowell, William C., Whitney O. Peake, Le Anne Coder, and Michael L. Harris. 2018. Building Small Firm Performance through Intellectual Capital Development: Exploring Innovation as the ‘Black Box’. Journal of Business Research 88: 321–27. [Google Scholar] [CrossRef]

- Mehralian, Gholamhossein, Jamal A. Nazari, and Peivand Ghasemzadeh. 2018. The Effects of Knowledge Creation Process on Organizational Performance Using the BSC Approach: The Mediating Role of Intellectual Capital. Journal of Knowledge Management 22: 802–23. [Google Scholar] [CrossRef]

- Meles, Antonio, Claudio Porzio, Gabriele Sampagnaro, and Vincenzo Verdoliva. 2016. The Impact of Intellectual Capital Efficiency on Commercial Bank Performance: Evidence from the US. Journal of Multinational Financial Management 36: 64–74. [Google Scholar] [CrossRef]

- Mention, Anne-Laure. 2012. Intellectual Capital, Innovation and Performance: A Systematic Review of the Literature. Business and Economic Research 2. [Google Scholar] [CrossRef]

- Mention, Anne-Laure, and Nick Bontis. 2013. Intellectual Capital and Performance within the Banking Sector of Luxembourg and Belgium. Journal of Intellectual Capital 14: 286–309. [Google Scholar] [CrossRef]

- Mutuc, Eugene B., Jen-Sin Lee, and Fu-Sheng Tsai. 2019. Doing Good with Creative Accounting? Linking Corporate Social Responsibility to Earnings Management in Market Economy, Country and Business Sector Contexts. Sustainability 11: 4568. [Google Scholar] [CrossRef] [Green Version]

- Nadeem, Muhammad, Christopher Gan, and Cuong Nguyen. 2017. Does Intellectual Capital Efficiency Improve Firm Performance in BRICS Economies? A Dynamic Panel Estimation. Measuring Business Excellence 21: 65–85. [Google Scholar] [CrossRef]

- Nahapiet, Janine, and Sumantra Ghoshal. 1998. Social Capital, Intellectual Capital, and the Organizational Advantage. Academy of Management Review 23: 242–66. [Google Scholar] [CrossRef]

- Nevado, Bruno, Natalia Contreras-Ortiz, Colin Hughes, and Dmitry A. Filatov. 2018. Pleistocene Glacial Cycles Drive Isolation, Gene Flow and Speciation in the High-elevation Andes. New Phytologist 219: 779–93. [Google Scholar] [CrossRef] [Green Version]

- Nimtrakoon, Sirinuch. 2015. The Relationship between Intellectual Capital, Firms’ Market Value and Financial Performance. Journal of Intellectual Capital 16: 587–618. [Google Scholar] [CrossRef]

- O’Donnell, David, Philip O’Regan, Brian Coates, Tom Kennedy, Brian Keary, and Gerry Berkery. 2003. Human Interaction: The Critical Source of Intangible Value. Journal of Intellectual Capital 4: 82–99. [Google Scholar] [CrossRef]