Overview of the Enablers and Barriers for a Wider Deployment of CSP Tower Technology in Europe

Abstract

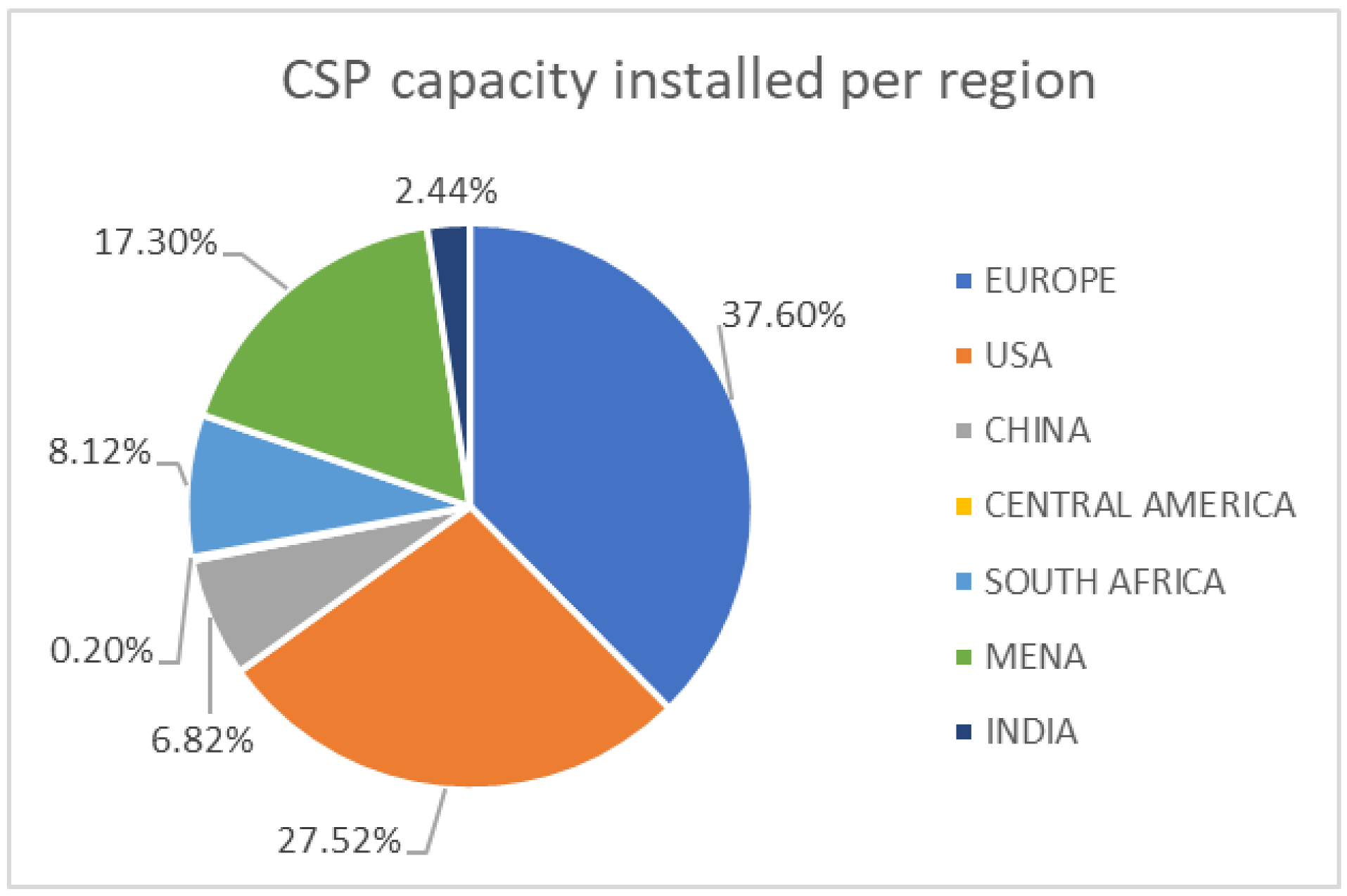

:1. Introduction

2. Economic Considerations of Grid-Connected CSP Towers and the Business Opportunity for Thermal Energy Storage

3. High Temperature Concentrating Solar Heat for Industrial Applications

3.1. Steel, Chemical and Cement Industries

3.2. Desalination

3.3. Green Hydrogen Production Plants

3.4. Business Models for CSP in Industrial Appliances

- Purchasing model: The solar energy provider acts as a contractor and is responsible for the design, dimensioning and installation of the solar energy generator. The solar energy generator is installed on the premises of the industrial customer. The client pays for the installation upon delivery and thus carries the initial investment.

- Rent/lease model: To avoid high upfront investments, industries can decide to rent or lease a solar power plant. In the lease model, the customer obtains the solar power plant on lease from a financing partner by agreeing for a down payment and an agreed lease rental for a fixed period. Leasing does not lead to an increase in liability as the asset stays off the balance sheet of customers. At the end of the lease period, the customer has the option to purchase the investment at the residual value and enjoy free solar power for the remaining lifetime of the plant. In the case of mobile solar power plants, a rental model is also possible. This would allow for maximum flexibility for the client and easy adaptation of the customer’s local energy generation capacity when demand is changing.

- PPA/HPA model: A new financial instrument that would reduce the risk for businesses of adopting a CSH-based solution for their industrial processes is the heat purchase agreement (HPA). The idea of the HPA is similar to the power purchase agreement (PPA) which was introduced to create a level playing field for renewable energy providers. The long-term PPAs protect buyers and sellers from fluctuating energy prices. “With HPAs, utility-scale solar heat producers could set up large CSH utilities and sell heat to multiple smaller firms clustered in industrial parks”, stated World Bank energy consultant Elena Cuadros in an interview with SolarPACES [46]. This would reduce the need for businesses to make capital costs and would give the heat producer a stable revenue stream over the longer term.

4. Materials, the Technological Challenge for CSP Uptake

4.1. Materials for Focal Point Receivers

4.2. Heat Transfer Fluids (HTFs)

4.3. Materials for Heat Transfer Fluid and Energy Storage Containers

4.4. Materials Outlook

5. Policy Enablers for CSP

- Feed in tariffs: premium/tariff/payment for newly installed renewable energy sources.

- Net metering: the sales of excess electricity generated by solar systems from households and commercial establishments to the grid.

- Investment tax credits: a percentage of the investments on solar projects, businesses or individuals are allowed to deduct from their taxes.

- Subsidies: a direct monetary aid supplied by a government to a private industrial actor.

- Financing facilitation: financial services such as a renewable energy financing portfolio, low-interest loans or micro-credits, offered by financial institutes to businesses and/or individuals.

- Renewable energy portfolio: penetration targets for renewable energy in the overall electricity supply mix.

- Public investment: government and/or donor-funded projects to support solar energy.

- Government mandates and regulatory provisions: government laws and regulations supporting transmission companies and electricity utilities to supply or purchase electricity generated from renewable energy plants.

6. Barriers, Obstacles and Framework Conditions

6.1. Political

6.2. Economic

6.3. Social

6.4. Technological

- Coating treatments and their high costs, difficulties in the scalability of synthesis, and durability at high temperatures in oxidizing environments. Presently, employing glass-ceramic and organic interlayers can be applied just on SiC-based materials [47].

- Lead as the fluid to use for thermal storage has good characteristics, including good stability and a high boiling point, but it also has a lower thermal conductivity and is more corrosive and more expensive than sodium [21].

- Testing and certification schemes are an obstacle in the replacement of old but functional materials in exchange for innovative and better performing ones. To convince companies of the long term goodness of the innovative solutions available at the R&D stage is a challenge that can be overcome with innovative fast-testing procedures and by making the testing certification easier. An alternative is to include in the provider contracts warranties related to the materials used [51].

- Difficulties in manufacturing large quantities of advanced materials and competition in mass volumes of low-cost products are still an obstacle for the CSP material manufacturers. Lower performances compared to those recorded in a testing environment and high costs can be unattractive for the investors [51].

6.5. Environmental

6.6. Legal

7. Conclusions and Recommendations

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ko, N.; Lorenz, M.; Horn, R.; Krieg, H.; Baumann, M. Sustainability Assessment of Concentrated Solar Power (CSP) Tower Plants—Integrating LCA, LCC and LCWE in One Framework. Proc. CIRP 2018, 69, 395–400. [Google Scholar] [CrossRef]

- Fernández, R.; Ortiz, C.; Chacartegui, R.; Valverde, J.; Becerra, J. Dispatchability of solar photovoltaics from thermochemical energy storage. Energy Convers. Manag. 2019, 191, 237–246. [Google Scholar] [CrossRef]

- McPherson, M.; Mehos, M.; Denholm, P. Leveraging concentrating solar power plant dispatchability: A review of the impacts of global market structures and policy. Energy Policy 2020, 139, 111335. [Google Scholar] [CrossRef]

- Dale, M. A Comparative Analysis of Energy Costs of Photovoltaic, Solar Thermal, and Wind Electricity Generation Technologies. Appl. Sci. 2013, 3, 325–337. [Google Scholar] [CrossRef]

- Awan, A.B.; Zubair, M.; Praveen, R.; Bhatti, A.R. Design and comparative analysis of photovoltaic and parabolic trough based CSP plants. Sol. Energy 2019, 183, 551–565. [Google Scholar] [CrossRef]

- Corona, B.; Miguel, G.S. Environmental analysis of a Concentrated Solar Power (CSP) plant hybridised with different fossil and renewable fuels. Fuel 2015, 145, 63–69. [Google Scholar] [CrossRef] [Green Version]

- European Commission, Initiative for Global Leadership in Concentrated Solar Power—Implementation Plan. 2017. Available online: https://setis.ec.europa.eu/system/files/set_plan_-_csp_initiative_implementation_plan.pdf (accessed on 19 September 2020).

- International Renewable Energy Agency (IRENA). Renewable Energy Statistics; Renewable Energy Agency: Abu Dhabi, UAE, 2019. [Google Scholar]

- Denholm, P.; Mehos, M. Enabling Greater Penetration of Solar Power via the use of CSP with Thermal Energy Storage. In Solar Energy: Application, Economics and Public Perception; Apple Academic Press: Oakland, CA, USA, 2014. [Google Scholar]

- OECD. Technology Roadmap: Concentrating Solar Power; OECD: Paris, France, 2010. [Google Scholar]

- Protermo Solar, Proyectos en el Exterior: Centrales en Operación, Construcción y en Fase de Desarrollo. Available online: https://www.protermosolar.com/proyectos-termosolares/proyectos-en-el-exterior (accessed on 18 August 2020).

- New Energy Update. CSP Today Global Tracker. Available online: http://tracker.newenergyupdate.com/tracker/projects (accessed on 18 August 2020).

- SolarPACES. SolarPACES Database. Available online: https://www.solarpaces.org/csp-technologies/csp-projects-around-the-world/ (accessed on 18 August 2020).

- Focal Line Solar Inc. Crescent Dunes Owner Files for Bankruptcy, Cyprus Starts to Build First CSP Plant. Available online: https://flsnova.com/2020/08/19/crescent-dunes-owner-files-bankruptcy-cyprus-starts-build-first-csp-plant (accessed on 11 September 2020).

- US National Renewable Energy Laboratory (NREL). Concentrating Solar Power Projects. Available online: https://solarpaces.nrel.gov (accessed on 10 June 2020).

- Crespo, L. Status of STE Industry and Markets and ESTELA’s Solar European Industry Initiative. In Proceedings of the ASTRI 2015 Symposium Cost Reduction Status of Concentrating Solar Thermal (CST) Technologies, Melbourne, VIC, Australia, 20 February 2015. [Google Scholar]

- Martin, C.; Querolo, N. A $1 Billion Solar Plant was Obsolete before It Ever Went Online. Available online: https://www.bloomberg.com/news/articles/2020-01-06/a-1-billion-solar-plant-was-obsolete-before-it-ever-went-online (accessed on 10 January 2020).

- International Renewable Energy Agency (IRENA). Renewable Power Generation Costs in 2019; Renewable Energy Agency: Abu Dhabi, UAE, 2020. [Google Scholar]

- REN 21. Renewables 2020—Global Status Report. Available online: https://www.ren21.net/gsr-2020 (accessed on 18 August 2020).

- Unknown. How Spain’s Auction Can Achieve the 5 GW of Concentrated Solar Power It Wants. Available online: https://www.evwind.es/2020/09/17/xavier-lara-on-how-spains-q4-auction-can-achieve-the-5-gw-of-concentrated-solar-power-it-wants/77226 (accessed on 23 September 2020).

- Achkari, O.; El Fadar, A. Latest developments on TES and CSP technologies—Energy and environmental issues, applications and research trends. Appl. Therm. Eng. 2020, 167. [Google Scholar] [CrossRef]

- Kerskes, H. Thermochemical Energy Storage; Elsevier: Amsterdam, The Netherlands, 2016; pp. 345–372. [Google Scholar]

- Ma, Z.; Glatzmaier, G.C.; Mehos, M. Development of Solid Particle Thermal Energy Storage for Concentrating Solar Power Plants that use Fluidized Bed Technology. Energy Proc. 2014, 49, 898–907. [Google Scholar] [CrossRef] [Green Version]

- GlobalData. Power Database. Available online: https://www.globaldata.com/industries-we-cover/power (accessed on 21 February 2020).

- Shen, W.; Chen, X.; Qiu, J.A.; Hayward, J.; Sayeef, S.; Osman, P.; Meng, K.; Dong, Z.Y. A comprehensive review of variable renewable energy levelized cost of electricity. Renew. Sustain. Energy Rev. 2020, 133, 110301. [Google Scholar] [CrossRef]

- Colla, M.; Ioannou, A.; Falcone, G. Critical review of competitiveness indicators for energy projects. Renew. Sustain. Energy Rev. 2020, 125, 109794. [Google Scholar] [CrossRef]

- Mulongo, N.Y.; Kholopane, P.A. An economic assessment of South African electricity supply systems. In Proceedings of the International Conference on Industrial Engineering and Operations Management, Paris, France, 26–27 July 2018; pp. 77–85. [Google Scholar]

- Py, X.; Sadiki, N.; Olives, R.; Goetz, V.; Falcoz, Q. Therpmal energy storage for CSP (Concentrating Solar Power). EPJ Web Conf. 2017, 148, 00014. [Google Scholar] [CrossRef]

- Liu, H.; Zhai, R.; Fu, J.; Wang, Y.; Yang, Y. Optimization study of thermal-storage PV-CSP integrated system based on GA-PSO algorithm. Sol. Energy 2019, 184, 391–409. [Google Scholar] [CrossRef]

- Powell, K.M.; Rashid, K.; Ellingwood, K.; Tuttle, J.; Iverson, B.D. Hybrid concentrated solar thermal power systems: A review. Renew. Sustain. Energy Rev. 2017, 80, 215–237. [Google Scholar] [CrossRef] [Green Version]

- Fraunhofer Institute for Solar Energy Systems ISE. From Green Deal to Green Recovery: An Initiative of the European Solar Thermal Industry; Fraunhofer Institute for Solar Energy Systems ISE: Freiburg, Germany, 2020. [Google Scholar]

- Weiss, W.; Spörk-Dür, M. Global Market Development and Trends in 2018; AEE Institute for Sustainable Technologies: Gleisdorf, Austria, 2019. [Google Scholar]

- Reuters. Thyssenkrupp Presents Plan for Carbon Neutral Steel Plant. Available online: https://www.reuters.com/article/thyssenkrupp-steel-hydrogen-idUSL8N2FU1JN2020 (accessed on 18 August 2020).

- European-Green-Deal-Communication_en. Available online: https://ec.europa.eu/info/publications/communication-european-green-deal_en (accessed on 10 September 2020).

- Low Carbon Roadmap Pathways to a CO2-Neutral European Steel Industry. 2019. Available online: www.eurofer.eu (accessed on 8 January 2020).

- Mohammadi, K.; Saghafifar, M.; Ellingwood, K.; Powell, K. Hybrid concentrated solar power (CSP)-desalination systems: A review. Desalination 2019, 468, 114083. [Google Scholar] [CrossRef]

- HELIOCSP. Neom to Build Desal Plant with Solar Dome technology. Available online: http://helioscsp.com/neom-to-build-desal-plant-with-solar-dome-technology (accessed on 10 June 2020).

- Alhaj, M.; Al-Ghamdi, S.G. Why is powering thermal desalination with concentrated solar power expensive? Assessing economic feasibility and market commercialization barriers. Sol. Energy 2019, 189, 480–490. [Google Scholar] [CrossRef]

- Mata-Torres, C.; Escobar, R.A.; Cardemil, J.M. Techno-economic analysis of CSP+PV+MED plant: Electricity and water production for mining industry in Northern Chile. AIP Conf. Proc. 2018, 2033, 180007. [Google Scholar] [CrossRef]

- Gonzalez, R.A.C.; Zheng, Y.; Hatzell, K.B.; Hatzell, M.C. Optimizing a Cogeneration sCO2 CSP-MED Plant using Neural Networks. ACS ES&T Eng. 2021, 1, 393–403. [Google Scholar] [CrossRef]

- Cekirge, H.M.; Erturan, S.E.; Thorsen, R.S. CSP (Concentrated Solar Power)—Tower Solar Thermal Desalination Plant. Am. J. Mod. Energy 2020, 6, 51. [Google Scholar] [CrossRef]

- International Renewable Energy Agency (IRENA). The Future of Hydrogen Executive Summary and Recommendations; International Renewable Energy Agency (IRENA): Abu Dhabi, UAE, 2019. [Google Scholar]

- Gielen, D.; Taibi, E.; Miranda, R. Hydrogen: A Renewable Energy Perspective; International Renewable Energy Agency (IRENA): Abu Dhabi, UAE, 2018. [Google Scholar]

- International Renewable Energy Agency. Hydrogen from Renewable Power: Technology Outlook for the Energy Transition; International Renewable Energy Agency (IRENA): Abu Dhabi, UAE, 2018. [Google Scholar]

- Scott Carpenter. Swedish Steelmaker uses Hydrogen Instead of Coal to Make Fossil-Free Steel. Available online: https://www.forbes.com/sites/scottcarpenter/2020/08/31/swedish-steelmaker-uses-hydrogen-instead-of-coal-to-make-fossil-free-steel/#609fd33d2c8b (accessed on 18 August 2020).

- Kraemer, S. Concentrated Solar Heat Could Decarbonize Industrial Heat Globally. Available online: https://helioscsp.com/concentrated-solar-power-could-decarbonize-industrial-heat/ (accessed on 22 September 2020).

- Casalegno, V.; Balerna, S.G.E.; Balerna, L.F.E.; Ferraris, M.; Calendario, V.M. New high performance SiC-based solar receivers for CSP. In Proceedings of the EEEIC Conference, Madrid, Spain, 9–12 June 2020. [Google Scholar]

- Ho, C.K. Advances in central receivers for concentrating solar applications. Sol. Energy 2017, 152, 38–56. [Google Scholar] [CrossRef]

- Hoffschmidt, B. Receivers for Solar Tower Systems; DLR: Font Romeu, France, 2014. [Google Scholar]

- Ho, C.K.; Mahoney, A.R.; Ambrosini, A.; Bencomo, M.; Hall, A.; Lambert, T.N. Characterization of Pyromark 2500 for High-Temperature Solar Receivers. In Energy Sustainability; American Society of Mechanical Engineers: New York, NY, USA, 2012; pp. 509–518. [Google Scholar]

- Smit, S.; Sterling, R. Report on market analysis and impacts, NEXTOWER project.Partner responsible for the deliverable: R2M Solution Spain SL. Available online: https://www.h2020-nextower.eu/ (accessed on 20 October 2020).

- Chen, D.; Colas, J.; Mercier, F.; Boichot, R.; Charpentier, L.; Escape, C.; Balat-Pichelin, M.; Pons, M. High temperature properties of AlN coatings deposited by chemical vapor deposition for solar central receivers. Surf. Coatings Technol. 2019, 377, 124872. [Google Scholar] [CrossRef]

- KIC-Inno Energy. Future Renewable Energy Costs: Solar-Thermal Electricity Renewable Energies; KIC-Inno Energy: Eindhoven, The Netherlands, 2018. [Google Scholar]

- Pacio, J.; Fritsch, A.; Singer, C.; Uhlig, R. Liquid Metals as Efficient Coolants for High-intensity Point-focus Receivers: Implications to the Design and Performance of Next-generation CSP Systems. Energy Proc. 2014, 49, 647–655. [Google Scholar] [CrossRef] [Green Version]

- Kribus, A. Concentrated Solar Power: Components and materials. EPJ Web Conf. 2017, 148, 00009. [Google Scholar] [CrossRef] [Green Version]

- Weinstein, L.A.; Loomis, J.; Bhatia, B.S.; Bierman, D.M.; Wang, E.N.; Chen, G. Concentrating Solar Power. Chem. Rev. 2015, 115, 12797–12838. [Google Scholar] [CrossRef] [PubMed]

- Lim, J.; Hwang, I.S.; Kim, J.H. Design of alumina forming FeCrAl steels for lead or lead–bismuth cooled fast reactors. J. Nucl. Mater. 2013, 441, 650–660. [Google Scholar] [CrossRef]

- Dömstedt, P.; Ejenstam, J.; Szakalos, P. High Temperature Corrosion of a Lean Alloyed FeCrAl-steel and the Effects of Impurities in Liquid Lead. In Proceedings of the EEEIC Conference, Madrid, Spain, 9–12 June 2020. [Google Scholar]

- Dömstedt, P.; Lundberg, M.; Szakalos, P. Corrosion Studies of Low-Alloyed FeCrAl Steels in Liquid Lead at 750 °C. Oxid. Met. 2019, 91, 511–524. [Google Scholar] [CrossRef] [Green Version]

- Li, N.; Parker, S.S.; Wood, E.S.; Nelson, A.T. Oxide Morphology of a FeCrAl Alloy, Kanthal APMT, Following Extended Aging in Air at 300–600 °C. Met. Mater. Trans. A 2018, 49, 2940–2950. [Google Scholar] [CrossRef]

- KANTHAL® APMT. Description of the Product. Available online: https://www.kanthal.com/en/products/material-datasheets/tube/kanthal-apmt (accessed on 15 June 2020).

- Coventry, J.S. Performance of a concentrating photovoltaic/thermal solar collector. Sol. Energy 2005, 78, 211–222. [Google Scholar] [CrossRef]

- Buffiere, J.-Y.; Maire, E.; Adrien, J.; Masse, J.-P.; Boller, E. In Situ Experiments with X ray Tomography: An Attractive Tool for Experimental Mechanics. Exp. Mech. 2010, 50, 289–305. [Google Scholar] [CrossRef]

- Salvo, L.; Suéry, M.; Marmottant, A.; Limodin, N.; Bernard, D. 3D imaging in material science: Application of X-ray tomography. Comptes Rendus Phys. 2010, 11, 641–649. [Google Scholar] [CrossRef]

- Salvo, L.; Cloetens, P.; Maire, E.; Zabler, S.; Blandin, J.; Buffière, J.; Ludwig, W.; Boller, E.; Bellet, D.; Josserond, C. X-ray micro-tomography an attractive characterisation technique in materials science. Nucl. Instrum. Methods Phys. Res. Sect. B Beam Interact. Mater. Atoms 2003, 200, 273–286. [Google Scholar] [CrossRef]

- Barhli, S.; Saucedo-Mora, L.; Jordan, M.; Cinar, A.; Reinhard, C.; Mostafavi, M.; Marrow, T. Synchrotron X-ray characterization of crack strain fields in polygranular graphite. Carbon 2017, 124, 357–371. [Google Scholar] [CrossRef] [Green Version]

- Duffield, J.S. The politics of renewable power in Spain. Eur. J. Gov. Econ. 2020, 9, 5–25. [Google Scholar] [CrossRef]

- SolarPower Europe EU Market Outlook. Available online: https://www.solarpowereurope.org/european-market-outlook-for-solar-power-2020-2024 (accessed on 22 June 2020).

- Solar Energy Industry Application (SEIA). Concentrating Solar Power. Available online: https://www.seia.org/initiatives/concentrating-solar-power (accessed on 18 August 2020).

- Office of the European Union. Clean Energy for all Europeans Energy; Office of the European Union: Luxembourg, 2019. [Google Scholar] [CrossRef]

- Jorgenson, J.; Denholm, P.; Mehos, M. Estimating the Value of Utility-Scale Solar Technologies in California Under a 40% Renewable Portfolio Standard; National Renewable Energy Lab. (NREL): Golden, CO, USA, 2014. [Google Scholar]

- Mehos, M.; Turchi, C.; Jorgenson, J.; Denholm, P.; Ho, C.; Armijo, K. On the Path to SunShot: Advancing Concentrating Solar Power Technology Performance and Dispatchability; United States Department of Energy: Washington, DC, USA, 2016.

- Kiefer, C.P.; Del Río, P. Analysing the barriers and drivers to concentrating solar power in the European Union. Policy implications. J. Clean. Prod. 2020, 251, 119400. [Google Scholar] [CrossRef]

- Simsek, Y.; Watts, D.; Escobar, R. Sustainability evaluation of Concentrated Solar Power (CSP) projects under Clean Development Mechanism (CDM) by using Multi Criteria Decision Method (MCDM). Renew. Sustain. Energy Rev. 2018, 93, 421–438. [Google Scholar] [CrossRef]

- Viebahn, P.; Lechon, Y.; Trieb, F. The potential role of concentrated solar power (CSP) in Africa and Europe—A dynamic assessment of technology development, cost development and life cycle inventories until 2050. Energy Policy 2011, 39, 4420–4430. [Google Scholar] [CrossRef] [Green Version]

- Cekirge, H.M.; Erturan, S.E.; Thorsen, R.S. The CSP (Concentrated Solar Power) Plant with Brayton Cycle: A Third Generation CSP System. Am. J. Mod. Energy 2020, 6, 43. [Google Scholar] [CrossRef]

- Matsumura, M.W. Latest Data on Fossil-Fuel Consumption Subsidies. 2018. Available online: https://www.iea.org/weo/energysubsidies (accessed on 12 February 2020).

- Abbas, R.; Montes, M.; Rovira, A.; Martínez-Val, J. Parabolic trough collector or linear Fresnel collector? A comparison of optical features including thermal quality based on commercial solutions. Sol. Energy 2016, 124, 198–215. [Google Scholar] [CrossRef]

- Woersdorfer, J.S.; Kaus, W. Will nonowners follow pioneer consumers in the adoption of solar thermal systems? Empirical evidence for northwestern Germany. Ecol. Econ. 2011, 70, 2282–2291. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). Global Energy Review The Impacts of the COVID-19 Crisis on Global Energy Demand and CO 2 Emissions; IEA: Paris, France, 2020. [Google Scholar]

- Sæþórsdóttir, A.D.; Ólafsdóttir, R. Not in my back yard or not on my playground: Residents and tourists’ attitudes towards wind turbines in Icelandic landscapes. Energy Sustain. Dev. 2020, 54, 127–138. [Google Scholar] [CrossRef]

- Bell, D.; Gray, T.; Haggett, C. The ‘Social Gap’ in Wind Farm Siting Decisions: Explanations and Policy Responses. Environ. Politi 2005, 14, 460–477. [Google Scholar] [CrossRef]

- SolarPACES. CSP Could Decarbonize Industrial Heat Globally. Available online: https://csp-eranet.eu/new/concentrated-solar-heat-could-decarbonize-industrial-heat-globally (accessed on 15 June 2020).

- Macknick, J.; Newmark, R.; Turchi, C. Operational Water Consumption and Withdrawal Factors for Electricity Generating Technologies: A Review of Existing Literature. In Proceedings of the AWRA 2011 Spring Specialty Conference: Managing Climate Change Impacts on Water Resources: Adaptation Issues, Options and Strategies, Golden, CO, USA, 18 April 2011. [Google Scholar]

- Carter, N.T.; Campbell, R.J. CRS Report for Congress Water Issues of Concentrating Solar Power (CSP) Electricity in the U.S. Southwest Specialist in Natural Resources Policy. 2009. Available online: www.crs.gov (accessed on 15 January 2020).

- Liqreina, A.; Qoaider, L. Dry cooling of concentrating solar power (CSP) plants, an economic competitive option for the desert regions of the MENA region. Sol. Energy 2014, 103, 417–424. [Google Scholar] [CrossRef]

- Klein, S.J.; Rubin, E.S. Life cycle assessment of greenhouse gas emissions, water and land use for concentrated solar power plants with different energy backup systems. Energy Policy 2013, 63, 935–950. [Google Scholar] [CrossRef]

- Sánchez, A.M. Towards the market through Standards. In Proceedings of the EEEIC Conference, Madrid, Spain, 9–12 June 2020. [Google Scholar]

{kind=link}

{kind=link}

| Enablers | Barriers |

|---|---|

| Need for wider promotion of CSP as clean technology | High water uses for cooling and cleaning |

| Enhance storage capacity to improve dispatchability | Need for high solar radiation and large land areas |

| High frequency of negative electricity prices | High LCOE compared to other renewable energies |

| Knowledge transfer to nuclear sector can speed up material development | Material performances at high temperature and difficulties in testing them |

| New policies and subsidies for CSP are currently under discussion | Lack of acknowledgement from politics about the advantages of CSP |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aprà, F.M.; Smit, S.; Sterling, R.; Loureiro, T. Overview of the Enablers and Barriers for a Wider Deployment of CSP Tower Technology in Europe. Clean Technol. 2021, 3, 377-394. https://0-doi-org.brum.beds.ac.uk/10.3390/cleantechnol3020021

Aprà FM, Smit S, Sterling R, Loureiro T. Overview of the Enablers and Barriers for a Wider Deployment of CSP Tower Technology in Europe. Clean Technologies. 2021; 3(2):377-394. https://0-doi-org.brum.beds.ac.uk/10.3390/cleantechnol3020021

Chicago/Turabian StyleAprà, Fabio Maria, Sander Smit, Raymond Sterling, and Tatiana Loureiro. 2021. "Overview of the Enablers and Barriers for a Wider Deployment of CSP Tower Technology in Europe" Clean Technologies 3, no. 2: 377-394. https://0-doi-org.brum.beds.ac.uk/10.3390/cleantechnol3020021