Comparative Study of Key Supply Chain Management Elements in Sustainability Reports

College of Business Administration, Inha University, Incheon 22212, Korea

*

Author to whom correspondence should be addressed.

Businesses 2021, 1(3), 168-195; https://0-doi-org.brum.beds.ac.uk/10.3390/businesses1030013

Submission received: 18 September 2021

/

Revised: 14 October 2021

/

Accepted: 19 October 2021

/

Published: 1 November 2021

(This article belongs to the Special Issue Inclusive and Innovative Businesses and Sustainability: New Trends in Challenging Times and the Path to Performance and Excellence)

Abstract

:During the COVID-19 pandemic, several issues have emerged as important in evaluating firm value and investment-oriented decision making. These issues include supply chain management, human rights, climate change, safety, and environmental risks. This study analyzed the sustainability reports of four business firms, each in four different countries, covering 2005/2006, 2013, and 2020. The analysis revealed similar factors and their dimensions that are critical for effective supply chain management: environmental and public sector issues, collaboration and cooperation with partner organizations, environmentally friendly production and development systems, human-centered operation plans, and risk management. While the study results delineated several key categories, there were variations among the four firms’ sustainability reports, indicating a need for global standards for comparative analysis. This study highlights the importance of sustainability, its effective measurement, and global standards for sustainability reports. As governments put pressure on businesses to demonstrate their commitments to environmental issues, many firms have embraced the concept of corporate social responsibility by practicing socially responsible codes of conduct throughout their supply chains.

1. Introduction

The social and environmental impact of business activities has garnered much attention in recent decades, facilitating the development of a sustainable environment [1]. Currently, both businesses and social perspectives emphasize sustainability owing to environmental issues. Research on sustainability focuses on financial analysis, customer relationships, brand value, supply chain-related activities, and environmental management systems. Currently, sustainable development is a common goal globally [2]. For instance, Swedish companies have adopted environmental, social, and corporate governance (ESG) since the early 1970s when discussions on corporate social responsibility (CSR) first began. Meanwhile, China announced, in April 2015, that it would preserve the world’s ecology by establishing an ecological civilization [3].

In 2018, the European Union (EU) established and promoted ESG by announcing sustainable finance-related regulations as part of its Sustainable Growth Funding Action Plan, leading to the global development of many standards and initiatives for better sustainability management and monitoring. The influential organizations essential for the standardization of critical factors concerning sustainability reporting are the Global Reporting Initiative (GRI), Sustainable Development Goals (SDG), International Organization for Standardization, Principles for Responsible Investment, and Sustainability Accounting Standards Board [4]. Furthermore, consumers have become more concerned about the environment and started to make more sustainable choices in response to climate change [5], resulting in a notable customer behavior shift [6]. For example, Spaargaren [5] argued that consumers prefer brands not utilizing plastic for packaging.

Therefore, ESG regulations enforced by governments and consumers’ shifts toward sustainable choices have had an immense impact on corporate management. Companies are now adapting to higher environmental standards, safety, and consumer awareness, as sustainability is integral for corporate competitiveness [7]. Similarly, Lee [8] stated that sustainability is being employed to gain a competitive advantage. The ability of a company to comprehend and implement sustainable actions is as imperative as its financial situation, marketing tactics, and product development strategy. In addition to sustainability providing a competitive advantage, sustainable supply chain management (SCM) has been shown to boost operating efficiency, ensure efficient resource utilization, enhance consumer satisfaction, unlock new revenue opportunities, and improve brand loyalty [9]. Moreover, studies have claimed that the competition is no longer between corporations but between supply chains [10].

Increasing performance and efficiency has been the traditional focus of operations management. However, organizations are now being forced to adjust their strategies to incorporate environmental and social sustainability factors owing to governmental and political pressure [11]. In response, many companies have been implementing the concept of CSR, whereby codes of conduct and socially responsible business practices are adopted throughout the supply chain [12]. In addition, SCM is significantly relevant to global logistics and carbon emissions, and its activities are considered as more impactful than those of other industries [13]. According to the Environmental Protection Agency, the freight and transportation sector in the USA was responsible for more than half of total emissions originating from nitric oxide, more than 30% from volatile organic compounds, and over 20% from particulate matter, in 2020 [13]. Thus, sustainable SCM seems vital for the future of companies and humankind in general.

However, different standards are utilized by firms across different countries when formulating sustainability reports. Therefore a consistent evaluation and effective comparison may be achieved only when such reports are based on similar global standards. Hence, this study develops methods to evaluate firms’ sustainability reports using the same core elements regardless of country. However, according to DiMaggio and Powell [14], whose work focused on explaining homogeneity and institutional theory, homogenization becomes inescapable when a field becomes well established. Furthermore, institutional theory considers the environment (i.e., economic, legal, and cultural) wherein companies operate [15]. A good understanding of institutional theory is, thus, essential to understanding sustainability and reporting across countries [15]. Within a structured industry, organizations respond to an environment wherein other organizations respond to their environment [14]. Therefore, homogeneity exists when isomorphism is applied regardless of the field and cultural environment [14]. As study of DiMaggio and Powell was carried out on a theoretical basis, we aim to examine institutional theory in the sustainability field.

Accordingly, this study has the following objectives: (1) analyzing the country-specific (USA, Sweden, China, and Korea) characteristics of sustainability reports by investigating those published in 2005/2006, 2013, and 2020; (2) exploring the core characteristics and strategies of SCM in selected companies; and (3) examining the suggestions by DiMaggio and Powell [14] and the later work of Ruiz et al. [15] that organizations’ structures are consistent and similar through a manual comparison of each country and company.

The remainder of this paper is structured as follows. In Section 2, we provide the sustainability background of the chosen countries; in Section 3, we provide information about the selected companies; in Section 4, we organize the characteristics of SCM in the sustainability reports in each country; lastly, in Section 5, we present the conclusions and discussion.

2. Review of the Sustainability Background

Many companies publish sustainability reports annually because of the increased worldwide focus on sustainability issues. These reports are known by various terms such as sustainability management reports, environmental reports, social responsibility management reports, CSR, and ESG. Sustainability reports also comprise social, environmental, and relevant quality reports, although these constitute nonfinancial factors [16]. Notably, each country/company reports according to its perspective because no unified international standard for sustainability reports exists. The GRI, which has become a usual standard, describes the presentation of sustainability reports in four categories: economy, environment, society, and governance. Many companies have adopted this. In this study, sustainability reports in four countries (the USA, Sweden, China, and Korea) were reviewed to identify their characteristics.

2.1. USA

The USA’s sustainability movement and reporting date back to the first Earth Day held on 22 April 1970 [17]. The United Nations (UN) report titled “Our Common Future” supported the globalization of sustainability reporting when first published in 1987 [17]. Initially, the chemical industries issued sustainability (environmental reports) reports, followed by the tobacco industries, and recently, by most of the S&P 500 (Standard & Poor’s 500 stock market index), G250 (250 largest companies by revenue based on the Fortune 500 ranking), and N100 (100 largest companies in 41 countries) companies.

Upon its inception in 1908, the U.S. Environmental Protection Agency passed acts concerning clean air, water, and endangered species, which have played a vital role in the process of environmental reporting [17]. Further, although not mandatory in the USA, many companies choose to engage in sustainability reporting owing to pressure from investors and regulators, who wish to receive information about the nonfinancial performance of all investments [17]. Hence, the trend of sustainability reporting has recently increased in the USA. According to the KPMG Survey of Sustainability Reporting [7], 98% of the N100 and G250 companies in the USA and 90% of the S&P 500 companies [18] report sustainability. A study described that this trend would rise as the new generation workforce becomes aware of the necessity of sustainability and sustainability reports, allowing companies to understand risks, attract investors, and build loyal customers [19].

2.2. Sweden

The EU is the region most concerned with sustainability reporting [20], having published 47% of all sustainability reports issued worldwide in 2012 [20]. According to Forbes [21], the top 10 countries in environmentally conscious performance are European countries, and Sweden has retained its position for nearly a decade.

In 1967, as the first-comer, Sweden passed the first Environmental Protection Act. Then, in 1972, it hosted the first UN conference on the global environment [22]. Since 1990, although Sweden’s population has grown by more than 1.6 million people and its economy has nearly doubled, its carbon dioxide emissions decreased by 27% between 1990 and 2018 [23]. Undoubtedly, Sweden has a long history of sustainability reporting that dates back to the 1960s, having recently attained the top rank in overall SDG performance (i.e., 84.72/100) out of the 193 UN Member States [24]. Sweden ranks first in the EU regarding organic food consumption and recycling cans and bottles and obtains the highest share of its energy from renewable sources [25]. Additionally, Sweden was ranked by Robecosam Country Sustainability Ranking as the most sustainable country in 2016 [25]. Thus, learning its approach toward sustainability reporting may prove highly beneficial for other stakeholders.

2.3. China

China’s sustainability reporting can be generally divided into five periods, beginning with 1978–1999. A legal environment was established during this period, wherein companies could fulfill their social responsibilities [26].

In the second period (1999–2005), specifically in 2001, China joined the World Trade Organization and was introduced to sustainable standards and policies [26]. Ever since, the Chinese government has promulgated numerous national-level legislations for promoting the sustainable development of Chinese companies [27].

Further, in January 2006, the third period (2006–2011) commenced, with announcement No. 42 of the “Company Law of the People’s Republic of China”, which stated that CSR was mandatory for all companies [28]. Since then, many companies have published their own sustainability management development reports [29].

A paradigm shift defined the fourth period (2012–2018): social responsibility was integrated into China’s ideology, targets, and organizational management methods [30]. The fifth and final period began in 2018, promoting national-level investment policies regarding sustainability and encouraging Chinese companies to fulfill their social responsibilities overseas. As of 2019, more than 2030 Chinese companies had published social responsibility reports, proving the flourishing of CSR in China [31].

2.4. South Korea

Although the first Korean sustainability report was released in 1995, most Korean companies began publishing and disclosing their sustainability reports only after 2005. The name for the reports has also evolved with time: in 2000, they were called “Environmental Social Reports” or “Environmental Reports”. Between 2000 and 2006, they were named “Corporate Social Responsibility Reports”. Post-2007, environment-related reports came to be known as “Sustainability Reports” [16]. Generally serving to inform nonfinancial stakeholders and investors about a company’s environmental and sustainability performance, the contents of these sustainability reports can be divided into three main categories following the GRI guidelines: economic, social, and environmental aspects.

Until 2010, the sustainability report publishing rate in the country was low (56 cumulative publications per year), but as it became compulsory, this rate grew to 115 in 2015. Notably, 122 and 101 reports were published in 2020, respectively. Therefore, the roles of companies have become pivotal in light of the growing importance of issues concerning social responsibility and ESG. Then, in late 2020, owing to the impact of COVID-19, the ESG perspective began to be nationally highlighted, evoking environmental interest as a new crucial national issue. Furthermore, owing to climate change-related issues, corporate risk management became a prerequisite for ESG management.

3. Comparison of the Sustainability Reports

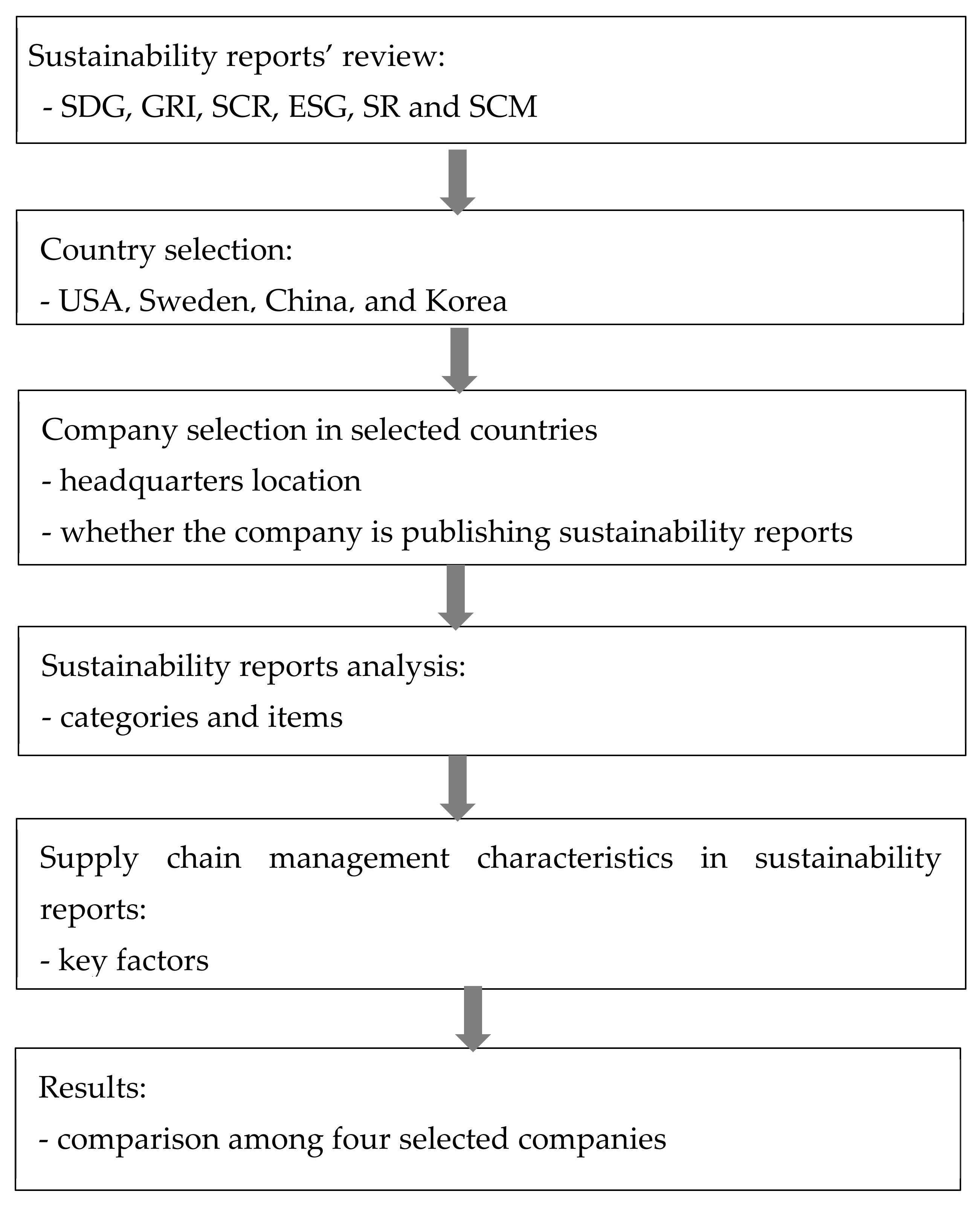

According to Ruiz et al. [15], no significant difference has been found in the sustainability reporting system, as most of the countries follow the same criteria and guides, similar to the GRI. However, analyzing this statement and detailed measurement items relative to published sustainability reports is necessary. Global companies operating in the four countries of interest were selected. The companies were chosen based on the following criteria: the parent entity (i.e., headquarters) is situated in the selected country and the chosen company is considered to be a representative in publishing sustainability reports in the selected country. Since the year and criteria for preparing sustainability reports vary slightly by company, three reports that each company published from 2005 to 2020 were chosen. Each company’s report was investigated based on the selected reports. Particular attention was paid to the assessment items regarding SCM, which were, then, compared and reviewed. SCM was selected for the assessment for three reasons. First, SCM includes many participating parties. Second, it directly affects carbon emissions. Third, considering that all the organizations selected were global companies, their SCM has direct and indirect impacts on society, the economy, and the environment.

Figure 1 shows the design process of the study for comparison of the sustainability reports among four countries.

3.1. Description of the Selected Companies by Country

3.1.1. USA

Founded in 1886, Johnson & Johnson (J&J) is an American multinational corporation that manufactures medical devices, pharmaceuticals, and consumer packaged goods. J&J adopted sustainability reporting quite early, releasing its first intermittent public report in 1993. J&J’s commitment to sustainability reporting appears to be its “ethos” and it started long before most had even heard the term “corporate social responsibility” [32]. In 2020, J&J ranked third on Gartner’s, the world’s largest research and advisory company, annual Supply Chain Top 25 list [33]. J&J was also incorporated into the TIME100 Most Influential Companies List [34] and was named the 2021 World’s Most Admired Company by Fortune Magazine [35]. J&J responded quickly to COVID-19 by manufacturing single-dose vaccines, working tirelessly to supply them internationally. Such responsiveness has made J&J even more influential and increased its market value. In this study, J&J was selected due to its initiative, dedication, contribution, and recognition regarding sustainable development.

3.1.2. Sweden

IKEA (Ingvar Kamprad Elmtaryd Agunnaryd), a value-oriented service provider based in Sweden that retails furniture and home appliances, has gained widespread praise locally and internationally due to its sustainability efforts. IKEA is considered to be one of the most famous places to work in Sweden and one of the country’s most respected and consistent companies [36]. Moreover, according to the Sustainable Brand Index [37], it has been ranked as the second most sustainable Swedish brand. Despite its overtly aggressive cost-cutting strategy, IKEA is a leader in resolving CSR issues [36] by prioritizing the exclusive use of natural renewable resources (e.g., timber). Accordingly, its operations have a direct relationship with both the environment and society [38].

However, customers still inquire about how and where the products are made [39]. To avoid damaging its reputation, IKEA recognizes that it must engage actively with its suppliers regarding their environmental and social conditions [39]. The company has been continuously reaching toward becoming a climate-positive company by 2030. Becoming more sustainable is achieved by implementing a code of conduct and formulating strategies that form better relationships with suppliers while efficiently utilizing recycled resources, renewable energy, and other initiatives [40]. Therefore, IKEA was chosen because of its sustainability practices.

3.1.3. China

In 1984, the Haier Group was founded; it has been dedicated to developing, producing, and selling home appliances (e.g., refrigerators, washing machines, and air conditioners) ever since. Currently, this company is ranked 435th on the Fortune Global 500 [35] and is very competitive. To ensure sustainability, the Haier Group has enforced a “green design, green manufacturing, green management, green recovery” strategy (4G strategy) and innovation ideology [41]. Additionally, it has been publishing environmental reports since 2005, which include sustainability management reports. Despite these qualities regarding sustainability, other Chinese companies have been publishing environmental reports since before the Haier Group, such as China National Petroleum (2000) and Baosan Steel (2003). However, as these are state-owned companies, the Haier Group was chosen because it is from the private sector, thus, facilitating comparisons with the companies in other countries that are privately owned.

3.1.4. South Korea

Samsung SDI (Samsung Digital Interface), Korea’s leading information technology company, was founded in 1970. In its early days, it produced Braun tubes for television sets. However, it eventually grew into a major company involved in producing all sorts of electric and electronic equipment. In 2000, the company started gaining competitiveness in manufacturing electric vehicles and lithium-ion secondary batteries. In 2004, it became the first and only Korean company to be selected for the Dow Jones Sustainability World Index (DJSI World). It has been consistently publishing sustainability reports in Korea. In November 2020, it was included in the DJSI World 16 times, making it the best among all Korean companies regarding sustainability [42].

Samsung SDI’s sustainability management perspective follows the essential preliminary plan that ensures corporate transparency when introducing and implementing new management philosophies [43]. Overall, the company is highly evaluated in the economic, social, and environmental fields, including product environmental responsibility, supply chain social responsibility, ethical management, and employee safety and health. Its established management system accounts for sustainability factors in all sectors, from research and development (R&D) to product and service provision [44]. Accordingly, the company has established itself as a national leader in publishing sustainability reports and has been globally acclaimed for its objectivity in sustainability activities. Accordingly, we chose it as a representative company of Korea.

3.2. Key Elements of the Sustainability Reports

The following section reviews the characteristics of the sustainability reports published by these four companies in 2005/2006, 2013, and 2020. The rationale behind choosing these years is that many companies started preparing their sustainability reports only after 2005. Thus, 2005 was selected as a standard. IKEA is an exception as, in 2005, no sustainability reports were yet published. Therefore, the next year, 2006, was chosen for the analysis; 2013 was selected, as it is midway between 2005 and 2020; 2020 was chosen as the latest reference year. The detailed items and categories of each company’s sustainability report for all the studied years can be found in Table A1, Table A2, Table A3, Table A4, Table A5, Table A6 and Table A7.

3.2.1. Johnson & Johnson, USA

J&J first set its environmental goals in 1990 and published periodic public reports from 1993 onward. In 1998, it shifted to publishing annual sustainability reports. Its early reports primarily concentrated on environmental aspects, and these were termed “Environmental, Health and Safety” (EHS) [32]. Therefore, J&J has set environmental goals and fulfilled its environmental responsibilities to customers, employees, stakeholders, and the community since 1990.

In 2005, the key topics approached by its sustainability reports were selected in response to stakeholder needs and the GRI Sustainability Reporting Guidelines from 2000. Access to health care, carbon dioxide emissions, energy use and conservation, materials and packaging, safety, and governance were crucial. To create environmentally friendly and sustainable products, J&J increased R&D spending and collaborated with international organizations to promote community health and environmental awareness. Its EHS compliance assessment was expanded to incorporate external manufacturers and supplier diversity.

In 2013, a citizenship and sustainability report was prepared following the GRI’s 2013 Sustainability Reporting Guidelines (G4.0 Core) and UN Global Impact Principles. On the basis of the materiality addressed and reported assessment, key factors were classified as extremely high, very high, and high, helping stakeholders and the organization itself identify topics of great interest. Important topics of interest comprised product quality and safety, global health, R&D and clinical trials, SCM, ethical performance, human rights, product ingredients, transparency, and compliance.

The Health for Humanity Report was prepared in 2020 following GRI standards and included the Sustainability Accounting Standards Board index and the UN Global Impact Principles. J&J reported its performance against the GRI’s new framework, the Culture of Health for Business (COH4B) practices and metrics, for the very first time. According to the priority topics assessment process, critical factors for 2020 were product quality, consumer and patient safety, ethics and compliance, access, advancing public health, sustainable products, strengthening health systems, diversity, equity and inclusion, climate, energy use and emissions, R&D investment, pricing, and a responsible supplier base, among others.

Overall, J&J has considered human health as a top priority in all its sustainability reports, followed by environmental and social/business issues. Hence, the company’s core objectives seem to be advancing human health and well-being, protecting the planet, showing responsible leadership, and creating dynamic business growth. Following the SDG, J&J went onto describe its vision for 2030, describing it as “a giant leap towards a world where a healthy mind, body, and environment is within reach for everyone, everywhere”.

3.2.2. IKEA, Sweden

In this study, the sustainability reports published by IKEA in 2006 (Social and Environmental Responsibility Report) [45], 2013 (Sustainability Report) [46], and 2020 (Sustainability Report) [40] were analyzed. Until 2006, IKEA had been addressing and reporting on its sustainability activities as per its internal key performance indicator (KPI) strategy. In the late 1990s, IKEA joined the Forest Stewardship Council (FSC) as well as cooperated with UNICEF and the International Federation of Building and Wood Workers (IFBWW). This resulted in the excellent management of IKEA’s leading resource (i.e., wood). Then, early in the 2000s, IKEA introduced its code of conduct, “IWAY”, and started to engage its social and environmental affairs as a separate function.

In 2013, IKEA dropped its internal KPI system to shift toward following GRI guidelines. Thus, from then on, the company’s sustainability reports were created using global standards rather than internally set guidelines. Additionally, IKEA adopted the UTZ certification program for ensuring the sustainable farming of coffee, tea, cocoa, and hazelnuts. Subsequently, IKEA was inducted into the Marine Stewardship Council, leading it to enhance food sustainability at IKEA. Moreover, the company started to recognize water as a necessary resource for its operations, planning routes to ensure better consumption. It also determined its carbon footprint and considered its importance in the reports. As for social aspects, IKEA added some key indicators related to diversity, equality, sustainability in everyday life, and customer sustainability education. Specifically, it introduced education endeavors on light-emitting diode (LED) lighting and announced two newly developed SCM control systems (i.e., the supplier sustainability index and indirect materials and service suppliers).

After the UN introduced the SDG, IKEA promptly took the initiative, switching its sustainability reporting to the latest SDG standards described in 2020. It also went onto upgrade its IWAY system to the latest 6.0 version. Furthermore, it identified and addressed a problem regarding air quality in the organization. Subsequently, when remote work started to increase, IKEA developed house-working agendas to establish better conditions for those who worked from home. Similarly, numerous initiatives were introduced to address social issues, such as refugee support and financial self-help groups. Moreover, stakeholder engagement was included in the sustainability report. Two new sustainable revenue models were created (i.e., resale program and subscription model); these three topics were non-existent in the 2013 report.

In summary, since the induction of IKEA into sustainability councils (e.g., FSC, UN Global Compact, UNICEF, and IFBWW), it has consistently been following those standards. The company has also adopted the SDG standard, UTZ control, and IWAY 6.0 system in tandem with many social support programs for minorities.

3.2.3. Haier Group, China

To assess the key factors of the Haier Group, the 2005 Environmental Report and the 2013 and 2020 Social Responsibility Reports were analyzed. All these documents were officially announced and published by the company. Contrary to the companies from the other countries, its reports were prepared by referring to GRI standards and the directives of the Chinese Academy of Social Sciences and those of the Shanghai Stock Exchange [41,47,48].

In 2005, the Environmental Report focused only on environmental activities. Its 4G strategy had already been introduced, and it remains in use today. Furthermore, the report presented a green purchasing policy, although it only covered hazardous chemicals. In the stakeholder section of this report, the company included only suppliers, customers, and employees.

Then, in the 2013 report, the company added a low-carbon management agenda to the global warming report. The stakeholder sector was expanded to include shareholders. Compared with 2005, its investment in social activities was shown to have increased significantly.

Moreover, in the 2020 report, the Haier Group added a climate change response agenda, concurring with international interest in climate change response topics during the period. The 2020 report also prominently promoted employees’ welfare, rights, and interests, openly describing them as the company’s intangible assets. Moreover, anti-corruption policies were extended to all stakeholders rather than just specific actors. Additionally, despite the harsh global economic situation owing to the COVID-19 outbreak, the company still ensured employee safety, guaranteed production and shipments, and donated medical supplies. Hence, even amidst challenging economic conditions, the company actively fulfilled its CSR.

In summary, the Haier Group implemented innovation, green design, green manufacturing, green management, green recovery, and green purchasing in 2005. In 2013, the primary focuses were innovation, integrating order and personnel in the business model, establishing an Internet-based platform operation, green design, green manufacturing, green management, green recovery, green purchasing, low-carbon management, establishing win/win partnerships with suppliers, and securing shareholder interests. Finally, in 2020, sustainability management was ensured by emphasizing anti-corruption, sustainable SCM, the interests of all stakeholders, human rights, the integration of order with personnel in the business model, Internet-based platform operation, green design, green manufacturing, green management, green recovery, green purchasing, and the climate change response.

3.2.4. Samsung SDI Corporation, South Korea

The key elements were compared and explored through Samsung SDI’s sustainability reports. Samsung SDI’s sustainability management system established a vision for building a company that contributes to society by developing leadership in sustainable corporate management. The company targets the triple bottom line (TBL), which denotes the economy, the environment, and society (i.e., the three main areas of “sustainable growth”, “win/win partnerships”, and “environmental value creation”) to facilitate balanced development and growth [44].

In 2005, eco-friendliness and environmental value were the primary targets of Samsung SDI’s sustainability management. On the basis of five strategies and an eco-network, the company established sustainability goals for the environment. Moreover, it planned an environmental management system, implementing it through eco-friendly SCM [49]. In 2013, the company declared its shift into prioritizing eco-friendliness and energy solutions. As energy exhaustion and alternative energy became significant issues, it increased its interest in the alternative energy sector [50]. In 2020, despite COVID-19 and uncertain global management, the company’s sustainable management continued to grow in battery business, and it established a sustainable management vision called the “Sustainable Development Innovator”, which has expanded its scope of decarbonization and resource circulation to help resolve environmental crises and issues. Additionally, social responsibility and ethical practices have been established throughout the supply chain [44].

In summary, the 2005 eco-friendly sustainability strategy included elements of environmentally friendly products, production, and communication; green purchasing and partnerships; and eco-friendly SCM. In 2013, elements of “social contributions” were incorporated, including eco-friendly energy solutions, eco-friendly products and services, environmental management system, greenhouse gases, compliance and ethical management, talent management, win/win partnerships, and customer satisfaction management. By 2020, “reinforce product safety and quality management”, “secure future growth drivers”, “generate solid business outcomes”, “support the sustainability of the supply chain”, “ensure responsible mineral sourcing”, “respond to climate change”, “mitigate environmental impact along the product life cycle (production and use)”, and “achieve circular economy through resource circulation” were given precedence. The company ensured continuous progress toward better sustainability management by focusing on these specific core elements.

4. Characteristics of SCM in the Sustainability Reports

With time, a growing awareness of the constant change of the global environment and expanding appreciation for the significance of environmental factors has developed. Companies have also become aware of the prominence of sustainable SCM, which focuses on changes in the understanding of sustainability and its related issues. Sustainable business practices are governed by consumer sustainability awareness, which has been demonstrated by companies’ continued efforts to reduce environmental pollution in their SCM through corporate management. This denotes those global environmental issues require suppliers to be more responsible for their actions. Hence, SCM could and should be used as a corporate strategy to systematically manage risks and achieve economic, environmental, and social performance. The following sections assess the economic, social, and environmental responsibilities of the selected companies regarding their SCM in each country and examine the characteristics for each year.

4.1. Johnson & Johnson

J&J is a global company with manufacturing sites and suppliers worldwide. In 2005, J&J conducted EHS compliance audits for contracted manufacturers and suppliers to improve their sustainability performance. In collaboration with the World Environment Center and the U.S. Agency for International Development, it implemented pilot projects in Mexico and Brazil to promote cleaner production processes in small and medium-sized supplier manufacturing sites. As part of the Supplier Diversity Program, J&J purchased goods and services from small and diverse businesses led by women and minority groups, helping them grow through mentoring programs.

In 2013, J&J introduced responsibility standards for suppliers, including performance factors, human rights, and business ethics based on its EHS document. Further, the company developed the Procurement Sustainability Initiative and Sustainability Toolkit to assist suppliers in understanding J&J’s commitment to sustainability and improve their performance. New and existing suppliers performed the assessment process, and the company continued working with small companies and businesses led by minorities, women, and/or veterans to ensure diversity and inclusion. J&J invested significantly in local suppliers, helping enhance their supplier network, create jobs, and strengthen ties with consumers and the community.

In 2020, J&J expected its responsibility standards to be followed by all its suppliers enrolled in the Supplier Sustainability Program to supplement social and environmental improvements. It also encouraged all its suppliers to disclose their environmental performance to CDP. As a part of enhancing supplier diversity and inclusion programs, J&J continued to support women-owned, minority-owned, veteran- and disabled-owned businesses and helped them grow through mentoring programs. Additionally, J&J partnered with the Earthworm Foundation for palm oil product sourcing and the Rainforest Alliance for wood-fiber product sourcing. The company also became a member of the Responsible Mineral Initiative, a cross-industry organization that now helps J&J source conflict minerals responsibly. During the pandemic, J&J ensured its supply chain continuity by working closely with its suppliers, distributors, local government, and regulators.

To sum up, J&J is attentive toward its SCM, with the key factors being human rights, environmental assessment, compliance, supplier diversity and inclusion, transparency and disclosure, and responsible sourcing, among others. Table 1 compares the accomplishments of J&J in 2005, 2013, and 2020 regarding SCM sustainability, highlighting the core changes based on its sustainability reports.

4.2. IKEA

Until 2006, IKEA had practiced its code of conduct, “IWAY”, for responsibly sourcing goods, services, and materials. IWAY established specific standards regarding environmental, social, and working conditions and animal welfare that were to be followed by all suppliers and service providers working with IKEA. The company eventually deployed an “e-Wheel” system to examine the environmental impact of IKEA’s products. The e-Wheel is segmented into four phases: raw materials, manufacturing, product use, and end of life. Furthermore, IKEA’s “WEEE” (Waste Electrical and Electronic Equipment) system ensures that its stores accept and recycle manufactured electrical and electronic equipment. IKEA has also developed an energy usage checklist and established a “WebEss” system, which helps keep track of and report on energy consumption and emissions across IKEA’s buildings. A “smart” way partnership also integrated wooden merchandise and auditing systems into the transportation section.

From 2006 to 2013, the company introduced two newly developed SCM control systems: (1) the Supplier Sustainability Index (the results of this index are used as part of IKEA’s Product Sustainability Scorecard), which enhances product development; and (2) the Indirect Material and Services, which sources high-quality, low-cost products and services while integrating sustainability into purchasing decisions. IKEA has also adopted a strategy of going from “trading to purchasing”, implying that it prefers to engage in long-term relationships with fewer suppliers instead of forming short-term relationships with multiple smaller suppliers. Additionally, IKEA has introduced effective business ethics policies in the last seven years (e.g., related to anti-corruption, transparency, reliable documents, regulations, and permits for IWAY).

In 2020, IKEA expanded the IWAY system to include requirements regarding general forestry, animal welfare, and transport sections for suppliers. Additionally, it went on to add another two novel SCM control entities. The first is the Strategic Sustainability Council, founded in February 2017, which ensures that the same roles are shared across the IKEA franchise system, laying out specific guidelines for IKEA’s role in society, strategic directions, ambitions, and sustainability requirements. The second entity is the “IConduct” system-IKEA’s franchisee code of conduct. Further, the company introduced five dimensions of demographic design, which serve to enhance product and material usage.

Therefore, the characteristics of SCM among IKEA’s sustainability reports can be summarized by the implementation of the IWAY code of conduct, its business ethics, human rights, energy-saving, and sustainable procurement programs (Table 2). Table 2 shows a comparison of IKEA’s accomplishments in terms of sustainable SCM in 2006, 2013, and 2020, highlighting fundamental changes based on its sustainability reports.

4.3. Haier Group Corporation

In its 2005 Environmental Report, the Haier Group presented a strategy of green design, manufacturing, management, and recovery and a green purchasing policy. This policy mandates raw material suppliers to be familiar with the Haier Group’s environmental and chemical management policies, inciting them to adopt measures for preventing environmental pollution during transportation [47]. During this time, the green purchase policy was still limited to hazardous chemical management, but the Haier Group was aware that SCM would play a pivotal role in its sustainable development. Thus, it actively worked toward its implementation.

Accordingly, in 2013, the Haier Group instituted its green procurement policy, with a strong emphasis on information sharing, supply chain transparency, fair competition, and anti-corruption. Using its “win/win partnership” policy, the Haier Group established long-term associations with suppliers to meet its customer demands.

By 2020, all measures related to SCM were different from those found in 2005 and 2013. Nonetheless, they were developed based on existing sustainability management measures, which had been methodically applied to SCM. Owing to the importance of global SCM, the Haier Group is implementing the Global Synergy policy to link regional prices by sharing cases with optimal global suppliers and operating a global bidding system. Additionally, human rights issues are garnering attention internationally and many companies, including the Haier Group, have begun concentrating on such issues in their SCM. The company’s 2020 report presented an agenda related to human rights issues, such as addressing conflict minerals and managing and reviewing supply chain workers.

In the era of the fourth industrial revolution, information technology such as big data is being widely used to strengthen business operations. Therefore, the Haier Group is operating a supply chain technology platform to manage information sharing, supply chain transparency, fair competition, supply chain risk, and green procurement. To ensure effective anti-corruption measures, both the supply chain and stakeholders are scrutinized. Thus, the SCM characteristic that becomes evident in the Haier Group’s sustainable report categories is the operability of a sustainable supply chain, one that allows its users to manage information sharing, transparency, fair competition, and supply chain risk through a supply platform based on information technology. The characteristics of the Haier Group’s SCM are shown in Table 3.

4.4. Samsung SDI Corporation

On the basis of established fair-trade practices, Samsung actively engages in support activities to strengthen the capabilities of its partners. Since social fulfillment has emerged as a significant risk to the competitiveness of a supply chain, the company has developed the S-Partner system, which can detect and mitigate risks regarding the human rights, labor, ethics, environment, and health and safety aspects of the supply chain [44]. The S-Partner certification system—a representative win/win relationship program developed independently of the other studied companies—was created by Samsung to systematically manage partner companies and attain holistic growth through self-diagnosis, checklists, and visit screening.

In 2005, Samsung SDI included eco-friendliness in its overall strategy and SCM. The company suggested the inclusion of environmental management based on green purchases between partner companies. The significance of its SCM was emphasized by investigating the status of the hazardous substances related to its operations and providing supplier education.

In 2013, specific measures and training were provided for stakeholders to evaluate the S-Partner certification program. They were operationalized by strengthening the capacity building between supporting systems and subcontractors. Concomitantly, this initiative imbued social responsibility throughout its supply chain. Consequently, Samsung SDI has continued to develop its SCM through the global spread of green partnerships.

By 2020, Samsung SDI had established codes of conduct for managing social and environmental risks in the supply chain by requiring full compliance from business partners. These codes provide measures that can improve behavioral standards in partner companies and impose restrictions on trading relationships, hence, helping prevent violations to the code. To ensure transparency and fairness among suppliers; manage nonfinancial risks (e.g., workplace safety), the environment, and human rights; and establish responsible practices for ethical mineral procurement in supply chains (Table 4), the company administers written evaluations during on-site inspections.

In 2005, 2013, and 2020, Samsung SDI supported the implementation of social responsibility in the SCM by providing education and screening for, as well as sharing information on human rights, labor, safety, health, environment, and ethics with its supply chain partners. Further, in its 2020 implementation plan, to aim for shared growth with its business partners, Samsung SDI is strengthening social responsibility in the SCM by ensuring stringent compliance with fair trade, developing technical integration, and establishing open communication channels.

4.5. Results

As shown in Table 1, Table 2, Table 3 and Table 4, in the mid-2000s, companies prioritized item and system development for SCM and green policies. In the early 2010s, the focus shifted toward the sustainable supply of raw materials and compliance with laws and regulations such as environmental protection, business ethics, evaluation process, and establishing a safe workplace environment. In the late 2010s, SCM was characterized by collaboration and cooperation with partner companies, environmentally friendly production and development, human-centered operation plans, and risk management.

J&J, in the USA, divided its sustainability report into three sections: the environment, society, and suppliers. In Sweden, IKEA split the report into ecology, society, suppliers, and the economy. The Haier Group in China and Korea’s Samsung SDI classified the report into economic, environmental, and societal aspects. Each segment had in-depth submeasurement items, all based on the particular criteria decided by the companies. Although sustainability reports should be prepared based on GRI guidelines, the four companies selected in this study issued their sustainability reports using their own methods. However, they had common factors, including environmental and social aspects. For example, while J&J and IKEA included suppliers in their report sections, IKEA and Samsung SDI both designated sections to discuss the economy. Indeed, prior research shows that environmental protection and coexistence with local communities are classified as common evaluation factors since they are the primary targets of sustainability reports [2]. Despite these similarities, it would be helpful to develop global standards on devising sustainability reports. Furthermore, they will ensure greater comparability between the reports across the different countries.

J&J and IKEA included the supplier factor as a section in their sustainability reports; both companies are attempting to build global networks for their production and SCM. This makes cooperation with suppliers an integral part of their work and may have led them to include this factor in the report. Moreover, as IKEA simultaneously pursues a low-cost and high-quality strategy, the competence of its suppliers is imperative for its production. In Gartner’s [33] ranking of the Top 25 Supply Chains of 2020, J&J ranked third, with its supply chain improvements receiving the best performance award. J&J is known for working with many of its partners to solve social problems and achieve public interest goals. Notably, logistics simplification is a requirement for increasing supply chain efficiency [33].

Upon analyzing the SCM-related factors among the evaluation items in the companies’ sustainability reports, the authors observed that J&J classified them as part of the supply chain and supplier management. In 2005, only five evaluation items were included by J&J, whereas this number had grown to 10 by 2020 (see Table 1). Meanwhile, IKEA classified suppliers into 13 subcategories, including 10 evaluation items in 2006 and 13 in 2020 (see Table 2). The Haier Group had nine subcategories in the SCM category. In 2005, the company included one evaluation item on SCM in the green purchasing policy section. By 2020, four evaluation items were included (see Table 3). Samsung SDI had 16 subcategories for supply chain and supplier management, which were evaluated by 12 items in 2005 and 2013 and 11 items in 2020 (see Table 4). Accordingly, the SCM characteristics in the reports of the four companies analyzed in this study were added as evaluation items in the supply chain sector, and items that were considered to have a low proportion of existing evaluation items were excluded. Although the overall category exhibited little change, the analysis of comprehensive items reflected a change in the trend toward ESG [54].

Additionally, recently, most countries have also been underlining environmental concerns owing to the spreading awareness that human existence is at risk without a sustainable environment. Thus, global warming; climate change; greenhouse gas emissions; pollution; and the excessive use of energy, water, and land represent areas that can only be improved once the global community unites. Therefore, the interrelationship between the environment and SCM builds upon observing how several supply chain networks are involved in manufacturing, packaging, and transportation worldwide. Exemplifying this interrelationship, the National Health Service in England reported that 62% of the healthcare industry’s carbon footprint in 2019 came from its supply chain [55]. Internal and external SCM frameworks both affect a supply chain’s social and environmental performance and a firm’s sustainability performance. Therefore, to build a sustainable environment, this study discusses the need for the development and implementation of environmental measures within SCM.

Hence, the countries analyzed in this study, including the international and national organizations, are working actively toward a more sustainable world. However, to ensure operational efficiency, sustainable approaches in SCM are necessary, as these may help shape a world where all living beings can exist harmoniously. Moreover, this sustainability must be maintained in the long term, which may only be accomplished by gradually increasing the scale of environmental investment in SCM at the national and corporate levels.

5. Conclusions and Discussion

The World Bank reported that the global economic growth rate has declined by 8% owing to the prolonged COVID-19 crisis [56]. Hence, although demand for corporate sustainability continues to grow, the business environment has been experiencing significant changes. In such a scenario, this study selected four companies from four representative countries that continue to publish sustainability reports. After that, the study analyzed vital categories within their sustainability reports issued in 2005/2006, 2013, and 2020. Key factors were examined to find the sections in the reports that addressed the company’s SCM. Herein, the study explains the reasons for targeting SCM. First, global supply chains have experienced massive disruptions and even collapsed owing to the COVID-19 pandemic. Second, each of the countries studied emphasized creating sustainable ecosystems, such as ESG, and even injected public funds to ensure that such systems are created and maintained. Finally, supply chains have a significant environmental impact because they interrelate with most activities within the business, such as raw material procurement, supply to final consumers, and reverse logistics. There is a need to compare and benchmark the key factors in the SCM of countries representing sustainable management. Hence, this study provides insights for enhancing sustainability reporting at the international level by benchmarking several countries and defining the critical perspectives through which sustainability reports should be generated. Noting both the similarities and the differences in organizations as well as the changes in their homogeneity or diversity over time is important [14]. Our results showed that the sustainability report categories for each of the four companies were both somewhat different and similar.

This analysis was based on institutional theory [14], which states that in uncertain fields such as sustainability, new adopters that could bring innovation and variation will endeavor to eliminate the liability of innovation and unfamiliarity by proceeding with the existing practices within the field. Hence, this study aimed to find both the similarities and the differences in the sustainability reports in different countries. Furthermore, Elkington [57] proposed the TBL of the economy, the environment, and society, and this study aimed to expand upon and evaluate those aspects.

Since ESG has recently become a trend among organizations worldwide that care for sustainability, the SCM evaluation items are expected to need to change accordingly. Hence, in sustainability reports, there is a need for creating, managing, and facilitating systematic directions and action items for evaluating SCM in the long term. This is because SCM’s ESG changes cannot be easily managed if they only aim to achieve short-term goals. Additionally, global systems and standards for building an international sustainable ecosystem are needed. As shown by analyses, even if a generally accepted guideline is available, it is difficult to compare the reports of companies from different countries, as firms in a field may be highly diverse on some dimensions, but remarkably homogeneous on others [15]. Thus, to establish global standards in sustainability reporting, a single integrated set of sustainability report assessment items is necessary.

According to results of study of DiMaggio and Powell [14], we analyzed the company reports. Hence, although no significant difference was found in the categories, differences in the detailed measurement items were found, depending on the company and period. Therefore, this study has practical value, as it shows that while the detailed measurement items differed in the sustainability reports, their basic categories were similar. This difference in details demonstrates that they differ substantially by company depending on the company characteristics. Thus, this research may be used to improve the measurement items of sustainability reporting systems. Moreover, when comparing countries, this study can be used.

This study has the following limitations and potential future research avenues. First, from the four countries selected, four companies were chosen to represent the sustainability reports of their respective nations. The countries were determined based on the subjective viewpoints of researchers. However, more countries and companies should be analyzed in future research to allow researchers to draw more objective comparisons. For example, future research should include an analysis of countries in South America or Middle East, as a major portion of global petroleum exports is from these regions. If supply chain disruptions were to occur in these regions, there will be major snowballing effects that can cause a global energy crisis. Second, the study analyzed only the items related to SCM in the sustainability report, and thus all other items need to be evaluated in detail in future research. Third, the study selectively analyzed three years and their respective sustainability reports. Therefore, future research should follow up by analyzing reports from a broader range of years.

Author Contributions

D.M. analyzed Johnson & Johnson case; V.L. prepared the IKEA case; W.D. analyzed the case of the Haier Group; H.-J.L. prepared Samsung SDI on sustainability reports; D.L. presented the overall results of four cases on sustainability reports. All authors have conceptualization, writing, and read of the manuscript. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by INHA UNIVERSITY Research Grant.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Sustainability report categories and items for Johnson & Johnson in the USA.

| Sections | Contents | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Environment | Environment management | Product stewardship (earthwards approach) | ✓ | ✓ | ✓ |

| Packaging and recycling | ✓ | ✓ | ✓ | ||

| Ingredients and sourcing of raw materials | ✓ | ✓ | ✓ | ||

| Waste management | ✓ | ✓ | ✓ | ||

| Biodiversity conservation | ✓ | ✓ | |||

| Water | Water usage amd discharge | ✓ | ✓ | ✓ | |

| Water conservation | ✓ | ✓ | ✓ | ||

| Greenhouse gas emissions/ climate change | Climate policy and initiatives/(climate resilience) | ✓ | ✓ | ✓ | |

| Energy use | ✓ | ✓ | ✓ | ||

| Facility CO2 emissions | ✓ | ✓ | ✓ | ||

| Air emissions | ✓ | ✓ | ✓ | ||

| Green buildings | ✓ | ✓ | |||

| Green chemistry | ✓ | ||||

| Society | Employee | Safety | ✓ | ✓ | ✓ |

| Health | ✓ | ✓ | ✓ | ||

| Employment policies and practices | ✓ | ✓ | ✓ | ||

| Ergonomics | ✓ | ||||

| Diversity and inclusion | ✓ | ✓ | ✓ | ||

| Labor practices and workforce | ✓ | ✓ | ✓ | ||

| Employee retention, development, and recruitment | ✓ | ✓ | |||

| Compensation | ✓ | ✓ | ✓ | ||

| Community (human health and well-being) | Disaster relief, volunteerism | ✓ | ✓ | ✓ | |

| Global public health | ✓ | ✓ | ✓ | ||

| Access to, and affordability of, healthcare (HIV, TB) | ✓ | ✓ | ✓ | ||

| Product pipeline/(innovation) | ✓ | ✓ | ✓ | ||

| R&D and clinical trials | ✓ | ✓ | ✓ | ||

| Market access | ✓ | ✓ | |||

| Preventing disease and promoting wellness | ✓ | ✓ | |||

| Preventing and responding to pandemic threats (United in defeating COVID-19) | ✓ | ||||

| Community involvement and engagement | ✓ | ✓ | ✓ | ||

| Customers | Assuring product quality and safety | ✓ | ✓ | ✓ | |

| Meeting customers’ needs/satisfaction | ✓ | ✓ | ✓ | ||

| Marketing communication/direct to consumer advertising | ✓ | ✓ | |||

| Share holders | Financial performance | ✓ | ✓ | ✓ | |

| Corporate governance | ✓ | ✓ | ✓ | ||

| Business conduct | ✓ | ✓ | ✓ | ||

| Political contribution | ✓ | ✓ | ✓ | ||

| Supplier | Ethics amd compliance | Ethics and integrity | ✓ | ✓ | ✓ |

| Anti-corruption/transparency | ✓ | ✓ | |||

| Ethical marketing | ✓ | ✓ | ✓ | ||

| Human rights | ✓ | ✓ | ✓ | ||

| Environmental and safety compliance | ✓ | ✓ | ✓ | ||

| Supply chain and supplier management | Procurement practices DMA | ✓ | ✓ | ✓ | |

| Freedom of association | ✓ | ✓ | ✓ | ||

| Labor practice and workforce | ✓ | ✓ | ✓ | ||

| Human rights | ✓ | ✓ | ✓ | ||

| Environmental assessment | ✓ | ✓ | ✓ | ||

| Information security and data privacy | ✓ | ✓ | ✓ | ||

| Enhancing supplier diversity and inclusion | ✓ | ✓ | ✓ | ||

| Intellectual property | ✓ | ✓ |

Table A2.

Sustainability report categories and items for IKEA in Sweden (1).

| Sections | Contents | Key Factors | 2006 | 2013 | 2020 |

|---|---|---|---|---|---|

| Ecology | Products and materials (2006): A more sustainable life at home (2013) | e-Wheel system | ✓ | ||

| Renewable materials used in products | ✓ | ✓ | ✓ | ||

| Waste recycling, reclaiming, or use in energy production. | ✓ | ✓ | ✓ | ||

| Recall management | ✓ | ||||

| WEEE system | ✓ | ||||

| Circular products (reuse, refurbish, remanufacture, and recycle) | ✓ | ||||

| The five dimensions of democratic design | ✓ | ||||

| Product innovations (evaluation system to check how green a product is) | ✓ | ||||

| Inorganic raw materials and virgin fossil materials | ✓ | ||||

| IKEA Food | Aquaculture Stewardship Council (ASC, 2013) + Marine Stewardship Council | ✓ | |||

| UTZ certification | ✓ | ✓ | |||

| Organic products | ✓ | ✓ | ✓ | ||

| Organic dish served | ✓ | ✓ | ✓ | ||

| Agriculture and animals | ✓ | ✓ | ✓ | ||

| Forestry | FSC certification scheme | ✓ | ✓ | ✓ | |

| WWF and IKEA | ✓ | ✓ | ✓ | ||

| Rainforest Alliance | ✓ | ✓ | ✓ | ||

| Reducing wood waste | |||||

| Energy | Renewable energy/Renewable Electricity Certificates/“Bundled” renewable power | ✓ | ✓ | ✓ | |

| IKEA introduced a mandatory energy usage checklist | ✓ | ||||

| WebEss system | ✓ | ||||

| Reduced energy use/effective energy consumption/energy efficient construction/motion detectors to save electricity | ✓ | ✓ | ✓ | ||

| Air quality | ✓ | ||||

| Save, reuse, or purify water | ✓ | ✓ | |||

| Transport | Environmental Protection Agency Smart Way Partnership | ✓ | |||

| Customer carbon footprint | ✓ | ✓ | ✓ | ||

| Supplier carbon footprint | ✓ | ✓ | ✓ | ||

| Employee carbon footprint | ✓ | ✓ | |||

| Product transport carbon footprint | ✓ | ✓ | |||

| Packing flat and filling space | ✓ | ✓ | |||

| Space-saving packages | ✓ | ✓ | |||

| GLES 3-pack plastic box | ✓ | ||||

| Rail initiatives | ✓ | ||||

| Delivery | ✓ | ✓ | ✓ | ||

| Green company cars | ✓ | ✓ |

Table A3.

Sustainability report categories and items for IKEA in Sweden (2).

| Sections | Contents | Key Factors | 2006 | 2013 | 2020 |

|---|---|---|---|---|---|

| Social | Governance and Ethics (since 2013) | People and Planet Positive strategy (introduced in 2012) | ✓ | ||

| Inequality | ✓ | ||||

| Moral leadership | ✓ | ||||

| Green growth | ✓ | ||||

| Customer communications | ✓ | ✓ | |||

| Human rights | ✓ | ||||

| International Recruitment Integrity System (IRIS) | |||||

| International Labor Organization (ILO), | |||||

| Employees | Homeworker agenda | ✓ | |||

| Ensure sustainability is part of our everyday work | ✓ | ||||

| Diversity and inclusion | ✓ | ||||

| Learning and development | ✓ | ||||

| Health and safety | ✓ | ||||

| Communication and engagement | |||||

| Survey to hear the voice of co-workers | ✓ | ||||

| Community involvement | Financial self-help groups | ✓ | ✓ | ||

| Alternative learning centers | ✓ | ✓ | |||

| Income generation initiative | ✓ | ✓ | |||

| Refugees | ✓ | ||||

| Immunization project | ✓ | ||||

| Children | Preventing child labor | ✓ | ✓ | ✓ | |

| Annual donation to improve children’s lives | ✓ | ||||

| Responsible marketing | |||||

| Ensuring children rights | ✓ | ✓ | ✓ | ||

| Education | Scholarships to study responsible forest management | ✓ | |||

| Developing forestry education in Russian schools | ✓ | ||||

| Developing LED lighting education | ✓ | ✓ | |||

| Customer education provision about sustainability | ✓ | ✓ | |||

| Suppliers | Control systems | Supplier Sustainability Index | ✓ | ✓ | |

| Indirect materials and services suppliers | ✓ | ||||

| Strategic Sustainability Council | ✓ | ||||

| IWAY supplier evaluation system (IWAY 6.0, since 2019) | ✓ | ✓ | ✓ | ||

| IConduct | ✓ | ||||

| Wood suppliers | Long-term relationship | ✓ | ✓ | ||

| Must not originate from intact natural forests (INF) | ✓ | ✓ | ✓ | ||

| 4Wood transportation | ✓ | ||||

| Tracing | ✓ | ||||

| Wood supply chain audits/third party auditor | ✓ | ✓ | ✓ | ||

| Economic | Stakeholders | Stakeholder engagement | ✓ | ✓ | |

| New sustainable revenue | Resale program | ✓ | |||

| Furniture as a service (subscription model) | ✓ |

Table A4.

Sustainability report categories and items for the Haier Group in China.

| Sections | Contents | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Economy | Business model and Strategy | Improving performance through innovation | ✓ | ✓ | ✓ |

| Integrating order and personnel in the business model | ✓ | ✓ | |||

| Strategic transition to an Internet-based platform company | ✓ | ✓ | |||

| Environment | Environment management | Environmental management system | ✓ | ✓ | ✓ |

| Green purchasing (raw materials purchasing) | ✓ | ✓ | ✓ | ||

| Green innovation (energy-saving); environmental protection technology and equipment development | ✓ | ✓ | |||

| Training on environmental protection | ✓ | ||||

| Environmental protection public welfare activities | ✓ | ||||

| Hazardous chemical management | ✓ | ✓ | |||

| Energy saving | Energy consumption management | ✓ | ✓ | ||

| Water usage and conservation | ✓ | ||||

| Renewable energy usage | ✓ | ✓ | ✓ | ||

| Waste | Pollutants and waste management | ✓ | ✓ | ||

| Gas emissions/ climate change | Low-carbon management and carbon emissions | ✓ | ✓ | ||

| Climate policy and initiatives | ✓ | ||||

| Social | Community | Community Investment | ✓ | ||

| Employee | Employee recruitment and development | ✓ | ✓ | ✓ | |

| Employee benefits | ✓ | ✓ | |||

| Health | ✓ | ||||

| Managing employee working conditions | ✓ | ||||

| Talent development | ✓ | ✓ | |||

| Labor standards | ✓ | ||||

| Employee rights | ✓ | ✓ | |||

| Diversity and equality for opportunities | ✓ | ||||

| Suppliers | Information shared system | ✓ | |||

| Green purchasing policy | ✓ | ✓ | |||

| Supply chain transparency | ✓ | ||||

| Fair competition | ✓ | ||||

| Anti-corruption | ✓ | ||||

| Global synergy | ✓ | ||||

| Conflict minerals | ✓ | ||||

| Supplier audit | ✓ | ||||

| Supply chain platform (risk management, win-win relationship, transparency, information sharing, long-term trust relationship, etc.) | ✓ | ||||

| Customers | Quality management | ✓ | ✓ | ||

| After-sales service | ✓ | ||||

| Customer satisfaction management | ✓ | ✓ | |||

| Shareholders | Standardization of enterprise management | ✓ | |||

| Strengthening the internal supervision of enterprises | ✓ | ||||

| Information disclosure | ✓ | ||||

| Social activities | Social public welfare activities | ✓ | ✓ | ✓ | |

| Ethics amd compliance | Advertisement compliance | ✓ | |||

| Anti-corruption | ✓ | ||||

| Governance | Products innovation | ✓ | |||

| Intellectual property | ✓ | ||||

| Information security and data privacy | ✓ | ||||

| Enterprise management | ✓ | ||||

| Safe production | ✓ | ✓ |

Table A5.

Sustainability report categories and items for Samsung SDI in South Korea (1).

| Section | Content | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Environmental | Materials | Total materials use other than water, by type | ✓ | ||

| Materials used by weight or volume | ✓ | ||||

| Percentage of materials used that are recycled input materials | ✓ | ||||

| Materials used by weight or volume | ✓ | ||||

| Energy | Direct energy use | ✓ | ✓ | ✓ | |

| Indirect energy use | ✓ | ✓ | ✓ | ||

| Initiatives to use renewable energy sources and to increase energy efficiency | ✓ | ✓ | |||

| Energy saved due to conservation and efficiency improvements | ✓ | ||||

| Initiatives to provide energy-efficient products and the results | ✓ | ||||

| Energy consumption within the organization | ✓ | ||||

| Energy intensity | ✓ | ||||

| Reduction of energy consumption | ✓ | ||||

| Water and effluents | Total water use | ✓ | ✓ | ✓ | |

| Water sources and related ecosystems/habitats affected by use of water | ✓ | ||||

| Annual withdrawals of ground and surface water | ✓ | ||||

| Total water withdrawal by source | ✓ | ||||

| Percentage and total amount of reusable water | ✓ | ||||

| Interactions with water as a shared resource | ✓ | ||||

| Management of water discharge-related impacts | ✓ | ||||

| Water consumption | ✓ | ||||

| Biodiversity | Total amount of land for production activities | ✓ | |||

| Amount of impermeable surface | ✓ | ||||

| Objectives and programs for protecting biodiversity and species | ✓ | ||||

| Locations and size of land owned, leased and managed in protected areas | ✓ | ||||

| Impact of SDI’s activities, products, and services | ✓ | ||||

|

Emissions and waste | Greenhouse gas emissions | ✓ | ✓ | ||

| Use and emissions of ozone-depleting substances | ✓ | ✓ | |||

| NOx, SOx, and other significant air emissions by type | ✓ | ✓ | |||

| Total amount of waste by type and destination | ✓ | ✓ | |||

| Climate change mitigation and adaptation | ✓ | ||||

| International environmental compliance | ✓ | ✓ | |||

| Significant discharges to water | ✓ | ✓ | |||

| Activities to curb greenhouse gas emission and reduced amount | ✓ | ||||

| Total weight discharge by quality and destination | ✓ | ||||

| Total weight of waste by type and disposal method | ✓ | ||||

| Total number and volume of significant spills | |||||

| Waste generation and significant waste-related impacts | ✓ | ||||

| Management of significant waste-related impacts | ✓ | ||||

| Waste generated | ✓ | ||||

| Waste diverted from disposal | ✓ | ||||

| Waste directed to disposal | ✓ | ||||

| Products and services | Significant environmental impacts of major products and services | ✓ | |||

| Percentage of the weight of products | ✓ | ||||

| Initiatives to mitigate environmental impacts of products and services | ✓ | ||||

| Reclaiming rate of products sold and their package materials | ✓ | ||||

| Compliance | Incidents of and fines for non-compliance | ✓ | |||

| Amount of fines and total number of non-monetary sanctions | ✓ | ||||

| Non-compliance with environmental laws and regulations | ✓ | ||||

| Overall | Total environmental expenditures by type | ✓ | |||

| Total environmental protection expenditures and investment by type | ✓ | ||||

| New suppliers that were screened using environmental criteria | ✓ | ||||

| Negative environmental impacts in the supply chain and actions taken | ✓ |

Table A6.

Sustainability report categories and items for Samsung SDI in South Korea (2).

| Section | Content | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Social | Employment | Total workforce by employment type, contract, and region | ✓ | ✓ | ✓ |

| Total number and rate of employee turnover | ✓ | ✓ | |||

| Net employment creation and average turnover segmented | ✓ | ✓ | |||

| Employee benefits beyond those legally mandated | ✓ | ✓ | |||

| Parental leave | ✓ | ||||

| Labor/management relations | Percentage of employees covered by collective bargaining agreements | ✓ | ✓ | ✓ | |

| Minimum notice period regarding operational change | ✓ | ||||

| Health and safety | Official labor and management health and safety committee | ✓ | ✓ | ||

| Rates of injury, occupational diseases, lost days, and absenteeism, and number of work-related fatalities | ✓ | ✓ | |||

| Disease control programs for employees, families, community members | ✓ | ||||

| Compliance with ILO guidelines | ✓ | ✓ | |||

| Occupational health and safety management system | ✓ | ||||

| Hazard identification, risk assessment, and incident investigation | ✓ | ||||

| Promotion of worker health | ✓ | ||||

| Work-related injuries | ✓ | ||||

| Work-related ill health | ✓ | ||||

| Training | Average hours of training per employee | ✓ | ✓ | ||

| Programs to support continued employability of employees and to manage career | ✓ | ||||

| Policies and programs for skills management or for lifelong learning | ✓ | ||||

| Average hours of training per year per employee | ✓ | ||||

| Programs for upgrading employee skills/transition assistance programs | ✓ | ||||

| Diversity and equal opportunity | Diversity in BOD composition and employees. | ✓ | ✓ | ✓ | |

| Equal opportunity policies or programs, systems to ensure compliance | ✓ | ||||

| Ratio of basic salary of men to women by employee category | ✓ | ✓ | |||

| Strategy and management | Human rights policy, guidelines, and monitoring systems | ✓ | |||

| Evidence of consideration of human rights | ✓ | ||||

| Policies and procedures | ✓ | ||||

| Employee training on human rights | ✓ | ||||

| Investment and procurement practices | Percentage and total number of investment agreements | ✓ | |||

| Rates of significant suppliers and contractors | ✓ | ||||

| Non-discrimination | Total number of incidents of discrimination and actions taken | ✓ | ✓ | ✓ | |

|

Human rights assessment | Operations: human rights reviews or impact assessments | ✓ | |||

| Employee training on human rights policies or procedures | ✓ | ||||

| Collective bargaining | Operations identified: freedom of association and collective bargaining | ✓ | |||

| Child labor | Operations that are likely to have child labor and measures taken | ✓ | |||

| Forced labor | Operations that are likely to have forced labor and measures taken | ✓ | |||

| Disciplinary practices | Description of appeal practices | ✓ | |||

| Non-retaliation policy, confidential employee grievance system | ✓ | ||||

| Indigenous rights | Share of revenues from the area of operations | ✓ | |||

| Policies, guidelines, and procedures | ✓ | ||||

| Community | Programs that evaluate and manage operations on communities | ✓ | ✓ | ||

| Operations: engagement, assessments, and development programs | ✓ | ||||

| Supplier social assessment | New suppliers that were screened using social criteria | ✓ | |||

| Negative social impacts in the supply chain and actions taken | ✓ | ||||

| Corruption | Percentage and total number of business units prone to corruption | ✓ | ✓ | ||

| Percentage of employees trained in anti-corruption policies and procedures | ✓ | ||||

| Actions taken in response to incidents of corruption | ✓ | ||||

| Public policy | Public policy positions and participation | ✓ | |||

| Policies, management systems, and compliance mechanism | ✓ | ||||

| Political contributions | ✓ | ||||

| Competition and pricing | Policies, management systems, and compliance mechanism | ✓ | |||

| Compliance | Monetary values of significant fines for non-compliance | ✓ | |||

|

Customer health and safety | Percentage of products in compliance with procedures | ✓ | |||

| Voluntary code compliance, product labels or awards | ✓ | ||||

|

Product and service labeling | Type of products required by procedures, and percentage of products subject | ✓ | |||

| Policies on product information and labeling, compliance mechanism | ✓ | ✓ | |||

| Policies on customer satisfaction, compliance mechanism | ✓ | ✓ | |||

| Advertising | Policies on standards | ✓ | |||

| Respect for privacy | Policies, management system, and compliance mechanism | ✓ | ✓ | ||

| Marketing communications | Programs to be compliant with marketing communications | ✓ | ✓ | ||

| Compliance | Monetary values of significant fines for non-compliance | ✓ | ✓ |

Table A7.

Sustainability report categories and items for Samsung SDI in South Korea (3).

| Section | Content | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Economic |

Economic performance | Direct economic value generated and distributed | ✓ | ✓ | ✓ |

| Financial implications and other risks and opportunities due to climate change | ✓ | ✓ | |||

| Defined benefit plan obligations and other retirement plans | ✓ | ✓ | ✓ | ||

| Significant financial assistance received from government | ✓ | ||||

| Market presence | Policy, practices, and proportion of local sourcing in major sites | ✓ | |||

| Proportion of senior management hired from the local community | ✓ | ||||

|

Indirect economic impacts | Local hiring procedures and proportion of managed seniors | ✓ | ✓ | ||

| Development and impact of community service activities and social investment | ✓ | ✓ | |||

| Understanding and describing significant, indirect economic impact | ✓ | ||||

| Significant indirect economic impacts | ✓ | ✓ | |||

| Procurement practices | Proportion of spending on local suppliers | ✓ | |||

| Anti-corruption | Operations assessed for risks related to corruption | ✓ | |||

| Communication and training about anti-corruption policies and procedures | ✓ | ||||

| Confirmed incidents of corruption and actions taken | ✓ | ||||

| Anti-competitive behavior | Legal actions for anti-competitive behavior, anti-trust, and monopoly practices | ✓ | |||

| Tax | Approach to tax | ✓ | |||

| Country-by-country reporting | ✓ |

References

- Adams, C.A.; Frost, G.R. Integrating sustainability reporting into management practices. Account. Forum 2008, 32, 288–302. Available online: https://0-www-sciencedirect-com.brum.beds.ac.uk/science/article/pii/S0155998208000306?casa_token=n7W9j157YrQAAAAA:oYq4x6wiGqwnlWHWMl05RX7ClZkBHQIQ4THwzTJEbAOOwHy37Eca9VwXLosjCvM6lB9QeUB4uc (accessed on 24 May 2021). [CrossRef]

- Lee, D.; Schniederjans, M. How corporate social responsibility commitment influences sustainable supply chain management performance within the social capital framework: A propositional framework. Int. J. Corp. Strateg. Soc. Responsib. 2017, 1, 208–233. [Google Scholar]

- Xie, Z. China’s historical evolution of environmental protection along with the forty years’ reform and opening-up. Environ. Sci. Ecotechnol. 2020, 1, 100001. Available online: https://0-www-sciencedirect-com.brum.beds.ac.uk/science/article/pii/S2666498419300018 (accessed on 10 July 2021). [CrossRef]

- A Practical Guide to Sustainability Reporting Using GRI and SASB Standards; Global Reporting Initiative and Sustainability Accounting Standards Board. 2021. Available online: https://www.globalreporting.org/media/mlkjpn1i/gri-sasb-joint-publication-april-2021.pdf (accessed on 10 July 2021).