1. Introduction

The corporate finance literature recognizes the importance of short-term financial decisions for the firm’s profitability. In a global context, the problematics of working capital management represent an ongoing topic because of its importance in ensuring the optimal route for businesses. Being able to act as a buffer of liquidity (

Baños-Caballero et al. 2020), working capital plays a valuable role during economic turmoil (

Enqvist et al. 2014). In a recent report about all globally listed companies (

PWC Annual Report 2019), PWC Global highlights that improving working capital may release €1.3 trillion of cash, which may boost capital investment by 55%. Moreover, the report highlights new challenges for the financial performance of globally listed companies for the last five years: capital expenditure has declined, cash has become more expensive and harder to convert, and working capital has improved only marginally. Given this backdrop, businesses need to have a working capital culture as support for financial performance.

However, empirical evidence on the relationship between working capital and corporate performance is rather mixed. On the one hand, investments in working capital are supposed to have a positive influence on firm profitability because they support growth in terms of sales and earnings (

Baños-Caballero et al. 2020;

Aktas et al. 2015). Sales are positively influenced by trade credit, improving customer relationships, while holding more inventories secures the business from the perspective of price fluctuations. Moreover, short-term debts used to finance working capital have low-interest rates and are free from inflationary risk (

Mahmood et al. 2019). On the other hand, overinvestment in working capital requires financing and, consequently, supplementary costs, and may also generate adverse effects and financial losses for shareholders (

Chang 2018;

Aktas et al. 2015). Therefore, a rapid increase in the cost of working capital investments relative to the benefits of holding larger inventories or allowing for trade credit to customers lowers the firm’s profitability levels. Recently, a few papers argued that there was a non-linear interrelation between investment in working capital and firm profitability (

Mahmood et al. 2019;

Tsuruta 2018;

Boțoc and Anton 2017;

Aktas et al. 2015;

Mun and Jang 2015;

Baños-Caballero et al. 2014). The non-linear relationship supposes that investments in working capital have a positive influence on corporate profitability until a certain point, called the optimum level of working capital (or the break-even point). Above the optimum, working capital may become a negative determinant of firm performance. The positive and negative combination with a break-even point is called an inverted U-shaped relationship (

Mahmood et al. 2019). Taking into account that “entrepreneurial success can refer to the mere fact of continuing to run the business” (

Staniewski and Awruk 2019), the trade-off between working capital and firm profitability can be acknowledged as of important significance in the context of entrepreneurial success.

This study seeks to examine the profit creating potential of working capital for a sample of firms from Poland over the period of 2007–2016. The first motivation behind the study is represented by market characteristics. The Polish market was developing dynamically and may have different characteristics than the patterns of mature markets (

Mielcarz et al. 2018). Moreover, it is worth to know that according to FTSE Russell Agency, Poland was qualified as a developed country in 2018. Second, Poland’s economic outlook motivates the present research. Over the analyzed period, inflation had an upward trend, leading to an increase in interest rates, which impacts the corporate cost of capital. In light of this threat, businesses may focus on the areas under their control, covering working capital. The third motivation behind this paper is the fact that a large body of recent research studies has investigated the impact of working capital on corporate performance from the perspective of developed economies especially the US, the UK, and China (i.e.,

Dalci et al. 2019;

Ren et al. 2019;

Laghari and Chengang 2019;

Mahmood et al. 2019;

Goncalves et al. 2018;

Tsuruta 2018;

Aktas et al. 2015;

Mun and Jang 2015;

Enqvist et al. 2014;

Baños-Caballero et al. 2014). Specifically, a small number of studies have focused on emerging economies: Uganda (

Kabuye et al. 2019), Egypt (

Moussa 2018), Vietnam (

Le 2019;

Nguyen and Nguyen 2018), Malaysia (

Yusoff et al. 2018), high-growth firms from emerging Europe (

Boțoc and Anton 2017), Pakistan (

Habib and Huang 2016), Ghana (

Amponsah-Kwatiah and Asiamah 2020), Egypt, Kenya, Nigeria, and South Africa (

Ukaegbu 2014).

Golas (

2020) analyzes the impact of working capital management on firm profitability only for the Polish dairy industry, from the perspective of different elements of working capital. The authors find that inventories and cash conversion cycle relate inversely with Return on Assets (ROA), while days sales outstanding and days payable outstanding have a positive influence on profitability. Therefore, the scarce empirical literature for emerging economies highlights contradictory results. The present paper attempts to fill in this gap in the literature. Therefore, the importance of working capital efficiency and the monetary policy tightening motivate the research on working capital–corporate performance interrelation, to enhance companies’ working capital culture.

The analysis is conducted on 719 firms listed on the Warsaw Stock Exchange and different panel data methodologies are employed. The results indicate an inverted U-shaped (concave) relationship between working capital ratio and firm profitability and the findings are robust for different proxies and methodologies, namely a panel model with fixed effects and the panel-corrected standard errors (PCSE) estimation, respectively.

We identify several arguments to assess the nexus between working capital and firm performance on the example of Polish listed firms. Firstly, the Polish stock market is the most developed in Central and Eastern Europe in terms of listed firms and trading volumes. Secondly, being a developing economy, the cost of capital is higher and the capital market is less developed when compared to Western economies, therefore, firms that hold high working capital on their balance sheet are exposed to higher interest charges and, therefore, to bankruptcy risk. On the other hand, similar to other countries in the region, in Poland, the banking sector represents the largest share of the financial system. Both lending standards and lending terms were tightened since the start of the financial crisis of 2008 and, therefore, the firms may face credit constraints and cannot acquire sufficient credit to invest in working capital (

Tsuruta 2019). Moreover,

Chen and Kieschnick (

2018) demonstrate that the availability of bank credit has a significant impact on firms’ working capital policies.

Our study brings new theoretical and practical contributions to the relationship between working capital management and firm profitability. Firstly, the research extends and complements the literature on the field by highlighting new evidence on the non-linear interrelation between working capital management and corporate performance in Poland. The results reveal a concave working capital–firm profitability relationship, meaning that working capital has a positive effect on profit up to a break-even point (optimum level). After the break-even point, working capital starts to negatively affect the firm profitability. The findings highlight that proactive working capital policies are profit-enhancing. Secondly, the study brings relevant corporate policy implications for an emerging economy framework. The results are suitable for use in business practice. In other words, corporate financial executives should avoid greater net investment in working capital and target its optimal level, while internally-generated funds can be oriented towards more profitable investment opportunities. Therefore, corporate managers should focus on maintaining accounts payable, accounts receivable, and inventory turnover at a certain level, to maximize the effects of working capital, for the benefit of the shareholders. From the practitioner’s perspective, working capital represents a potential tool to optimize financial performance and also indicates the areas requiring improvement and supervision to ensure financial performance. Policymakers can use this knowledge for profit maximization. We consider that the results push forward the understanding of treasury management, a complex and dynamic domain, oriented towards the highest performance and simplification of all treasury activities (

Polak et al. 2018). The research highlights that, above the optimal level, working capital harms business performance. As working capital can be viewed as an adequate forecasting indicator about future economic issues (

Michalski 2014), we consider that our research could offer a macroeconomic signal if most of the public firms hold higher levels of working capital.

The remainder of this article is organized as follows:

Section 2 presents the relevant literature on the working capital management–firm profitability relationship.

Section 3 describes the sample used in the empirical analysis and the considered empirical methods.

Section 4 presents the empirical results and robustness checks.

Section 5 concludes the paper and offers some policy implications.

2. Literature Review

The academic literature proposes different competing views to explain the relationship between working capital and firm performance. On the one hand, most of the previous studies find a positive relationship between the two measures, based on firms from developed economies—the US (

Lyngstadaas 2020), the UK (

Goncalves et al. 2018), Finland (

Enqvist et al. 2014), or from developing economies—Uganda (

Kabuye et al. 2019), Egypt (

Moussa 2018), Vietnam (

Nguyen and Nguyen 2018), Ghana (

Amponsah-Kwatiah and Asiamah 2020).

Kabuye et al. (

2019) analyze the impact of internal control systems and working capital management on the financial performance of 110 supermarkets from Uganda and find that working capital management is a significant predictor of financial performance.

Moussa (

2018) examines the impact of working capital management on the performance of 68 industrial firms from Egypt for the period of 2000–2010 and documents a positive relationship between working capital management (measured by the cash conversion cycle) and firm profitability. The author points out that stock markets in less developed economies do not realize the optimum efficiency of their WCM.

Nguyen and Nguyen (

2018) analyze the relationship between working capital management and corporate profitability and document a positive nexus between working capital management and the performance of Vietnamese listed firms over the period of 2008–2014. Listed manufacturing firms in Ghana exhibit a positive relationship between different components of working capital and profitability, as reported by

Amponsah-Kwatiah and Asiamah (

2020). Moreover,

Goncalves et al. (

2018) confirm that WCM efficiency increases profitability on the example of UK unlisted companies between 2006 and 2014. For the US, effective working capital management is found to be associated with the higher financial performance of listed manufacturing firms, as reported by

Lyngstadaas (

2020).

Enqvist et al. (

2014) examine the impact of working capital management on firm profitability in different business cycles, on the example of Finland between 1990 and 2008, and highlight that firms can enhance their profitability by improving working capital efficiency. This first point of view is explained by the fact that working capital offers the firms the opportunity to grow by increasing sales and revenues. There are firms with large exposure to risk connected to small levels of inventory (

Michalski 2016). Therefore, in the case of those firms, holding a low level of inventory leads to negative modifications of sale levels and weaker profits (

Michalski 2016).

On the other hand, an alternative strand of research reports that WCM negatively influences profitability, using samples for developed economies (

Fernandez-Lopez et al. 2020;

Ren et al. 2019;

Dalci et al. 2019), European Union (

Akgun and Karatas 2020), or for developing economies (

Pham et al. 2020;

Wang et al. 2020;

Le 2019;

Yusoff et al. 2018;

Habib and Huang 2016;

Ukaegbu 2014).

Fernandez-Lopez et al. (

2020) report a negative relationship between different components of working capital and firm performance for a sample of Spanish manufacturing companies during the period of 2010–2016.

Dalci et al. (

2019) analyze the relationship between cash conversion cycle and profitability over 2006–2013 for 285 German non-financial firms and found that shortening the length of cash conversion cycle has a positive effect on the profitability of small and medium-sized firms, based on different methodologies: pooled ordinary least squares (OLS), fixed effects, random effects, and generalized method of moments (GMM). A negative relationship between working capital and business performance is found by

Akgun and Karatas (

2020) for a sample of European Union-28 listed firms during the 2008 financial crisis. Moreover, an inverse link between the cash conversion cycle and profitability of Chinese non-state-owned enterprises is found by

Ren et al. (

2019).

Le (

2019) reports a negative impact of working capital management on firm valuation, profitability, and risk for a sample of 497 firms from Vietnam over the period of 2007–2016. The same negative relationship for Vietnamese steel companies is also reported by

Pham et al. (

2020).

Yusoff et al. (

2018) investigate the relationship between working capital management and firm performance for 100 selected manufacturing companies in Malaysia. The authors show that the inventory conversion period, average collection period, and cash conversion cycle are significantly and negatively correlated with profitability. Improving firm performance by a conservative working capital management policy is also confirmed by

Chang (

2018), based on a sample of 31,612 companies from 46 countries over the period of 1994–2011. A detrimental influence of a longer cash conversion period on profitability is reported also for India by

Shrivastava et al. (

2017) based on both classical panel analysis and Bayesian techniques.

Habib and Huang (

2016) find that positive working capital harms profitability, while a negative working capital affects profitability positively, on the example of Pakistan, by employing panel least squares estimation, panel fixed effect, and panel generalized method of movement. A negative association between WCM and performance of non-financial listed firms in Pakistan is also highlighted by

Wang et al. (

2020). Using data on Brazilian public companies over the period of 1995–2009,

De Almeida and Eid (

2014) find that increasing the level of working capital at the beginning of a fiscal year diminishes company value. Moreover, a negative effect of cash conversion cycles on firm profitability, measured as net operating profit, is documented by

Ukaegbu (

2014), based on a panel of manufacturing firms in Egypt, Kenya, Nigeria, and South Africa for the period of 2005–2009. The second point of view is explained by the fact that higher investments in working capital involve more financing and, therefore, the interest expenses of firms might increase, being more exposed to bankruptcy risk. It is appreciated that an increase in the level of working capital generates higher costs of holding and managing working capital, with a negative effect on firm value (

Michalski 2014). However, the relationship of working capital components with the firm value depends on the risk-sensitivity level of firms (

Michalski 2014). Before, during, and after a financial crisis,

Michalski (

2016) demonstrates that the level of working capital is higher and acts as a hedging instrument against the cost of disruptive productivity.

Recently, the third point of view emerged and focused on the functional form of the relationship between working capital and firm profitability. A few studies report a concave relationship between the two measures, most of them on the example of firms from developed economies (

Mahmood et al. 2019;

Tsuruta 2018;

Aktas et al. 2015;

Baños-Caballero et al. 2014) followed by a sample of firms from emerging European countries (

Boțoc and Anton 2017) or firms from a certain sector (

Mun and Jang 2015).

Mahmood et al. (

2019) report an inverted U-shaped working capital–profitability relationship using GMM as methodology, for a sample of Chinese companies over the period of 2000–2017. Empirical evidence of inverted U-shaped relationship between working capital and profitability of Chinese listed companies is also reported by

Laghari and Chengang (

2019), based on the same GMM methodology. Using data from over 100,000 small businesses in Japan,

Tsuruta (

2018) reports a negative impact of working capital on firm performance in the short run, but positive over longer periods.

Altaf and Shah (

2018) provide evidence of the inverted U-shape relationship between WCM and firm profitability for a sample of 437 non-financial Indian companies, based on GMM methodology.

Boțoc and Anton (

2017) report an inverted U-shape relationship between working capital level and firm profitability, based on a panel of high-growth firms from Central, Eastern, and South-Eastern Europe over the period of 2006–2015. The concave relationship between working capital level (measured by the cash conversion cycle) and firm profitability is also reported by

Afrifa and Padachi (

2016), using panel data regression methods, for a sample of 160 listed firms during the period of 2005–2010.

Aktas et al. (

2015) document the relationship between WCM and firm performance on a sample of firms from the US over the period of 1982–2011 using fixed-effects regressions. The authors highlight an optimal point of working capital investment, towards which firms may converge to improve their overall performance. Moreover,

Mun and Jang (

2015) report a concave impact of working capital on firm value, which supports the idea of an optimal working capital level for US firms from a specific industry (restaurants), over the period of 1963–2012, based on static and dynamic panel data methodologies. For a sample of firms from the UK,

Baños-Caballero et al. (

2014) point out a non-linear relationship between working capital and firm value, meaning that there is an optimal level of working capital that maximizes firm revenues. Additionally, the optimal level depends on the financing constraints, the authors indicating that the optimal working capital level is lower for firms under financial constraints.

As can be noticed, corporate finance literature does not provide a general agreement on how working capital affects firm performance. The divergence can be explained by different measures used for working capital: cash conversion cycle (

Dalci et al. 2019;

Shrivastava et al. 2017;

Ukaegbu 2014), most popular indicator used as proxy, net trade cycle (

Baños-Caballero et al. 2014) or other measures (Inventory Turnover Ratio, Working Capital Turnover Ratio). Using these measures, in most of the studies, working capital is expressed as a composite measure (

Prasad et al. 2019), but there are also a few studies that have examined the impact of working capital on profit, at the level of individual components of cash conversion cycle or net trade cycle (

Enqvist et al. 2014). Moreover,

Mahmood et al. (

2019) provide several reasons to explain why companies may exhibit a different working capital–profitability: ownership structures, financial flexibility, tax provisions, and leverage. Moreover, the mixed results highlight that the relationship between working capital components and firm profitability may be more complex, and the empirical studies have not found the underlying mechanisms (

Peng and Zhou 2019). In a recent paper,

Peng and Zhou (

2019) propose to consider different discount rates of companies to encounter the inconsistency in the relationship between working capital components and corporate profitability.

Maximization of the business profitability is an effect of working capital management, but also the reverse causality is plausible when firms are profitable, they have more cash to invest in working capital. Moreover, both firm profitability and working capital are determined by multiple factors. From the perspective of potential endogeneity issue, the study of

Seth et al. (

2020) is probably among the first that evaluates the impact of several exogenous variables on the WCM efficiency and firms’ performance. Based on data envelopment analysis and structural equation modeling, the authors find that the following variables have a direct effect on WCM efficiency, and, therefore, on firms’ performance: interest coverage, leverage, net fixed asset ratio, and asset turnover ratio. The literature recognizes some relevant channels that moderates the relationship between working capital and firm performance. One relevant channel is corporate governance.

Kayani et al. (

2019) provide evidence on the collective empirical impact of WCM and corporate governance on financial performance for the US listed firms. The authors recommend considering the collective effects of short-term (WCM) and long-term (corporate governance) indicators, on financial performance.

Giroud and Mueller (

2011) take into account market competition and highlight, that, weak corporate governance lowers firm value in non-competitive industries. Moreover, the endogeneity problem can be driven by CEO characteristics. The firm’s chief executives are more focused on achieving short-term profitability, rather than long-term performance (

Kayani et al. 2019).

From the methodology perspective, the empirical findings are, mostly, documented on static panel data methods (regression analysis) and correlation analysis. Recently, some studies use methods, like GMM to control for endogeneity challenges (

Dalci et al. 2019;

Mahmood et al. 2019;

Laghari and Chengang 2019;

Altaf and Shah 2018;

Boțoc and Anton 2017). Endogeneity is recognized as being a challenge in corporate finance, and thus

Li (

2016) proposes several methods to deal with it, as follows: GMM, instrumental variables, fixed effects models, lagged dependent variables, and control variables. The current econometric analysis is performed using, behind ordinary least squares, two additional panel data techniques, the fixed-effects, and panel-corrected standard errors models. The justification is represented by the advantages of fixed-effects regression analysis, which takes full account of factors that might influence firm profitability in a certain year, and respectively of panel-corrected standard errors model, which accounts for firm-level heteroscedasticity and contemporaneous correlations across firms. Moreover, the combination of the methods (fixed effects and meaningful control variables) appears to work in mitigating endogeneity issues, according to

Li (

2016).

The mixed results regarding the effects of working capital indicate that short-term financial decisions should recognize working capital as a determining factor of financial performance. Therefore, the current research assumes the existence of an optimal working capital level for firms in Poland that maximizes their benefits.

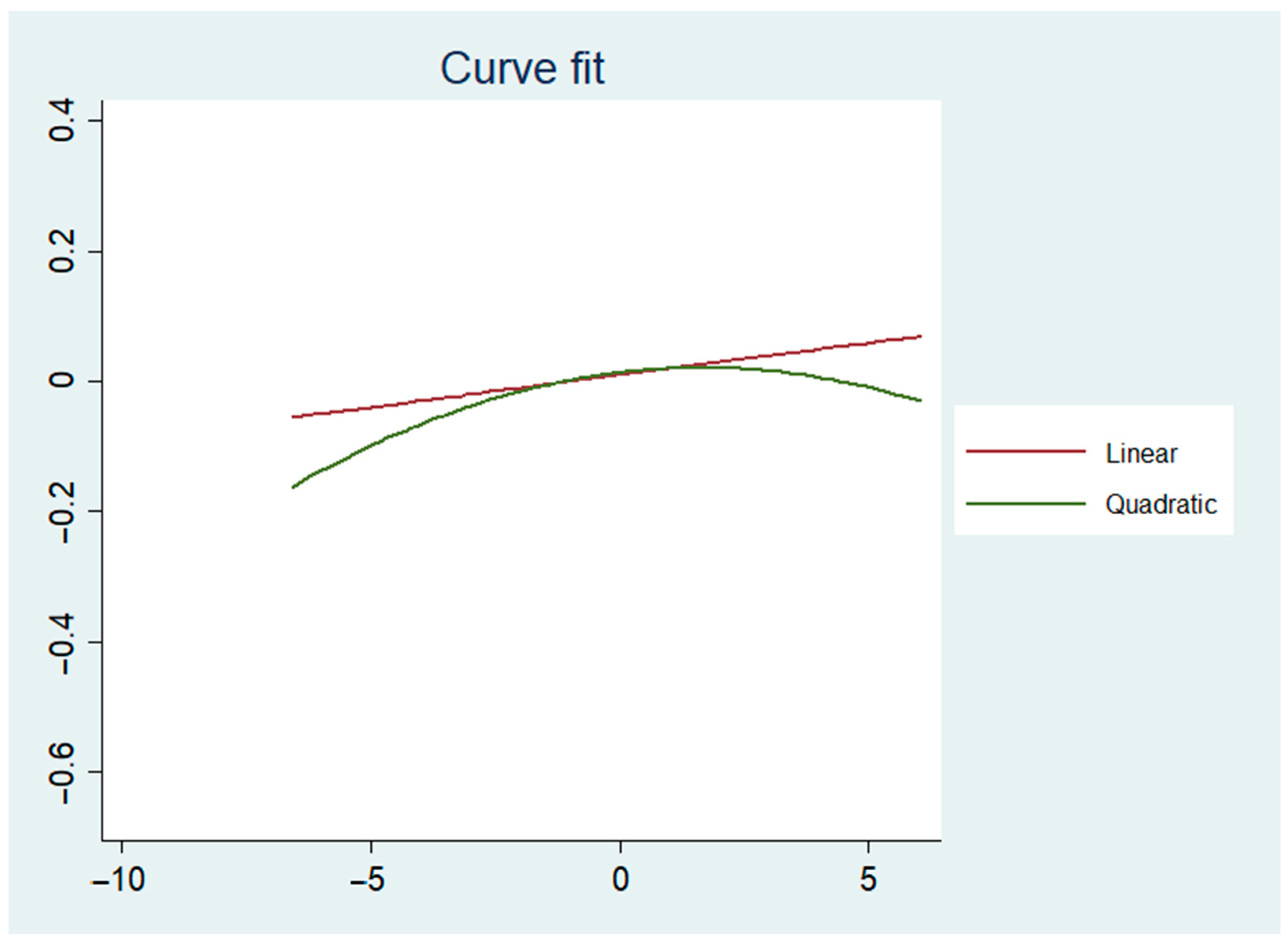

Figure 1 displays the relationship between the level of working capital (WKCR) and profitability (ROA). We notice a non-linear relationship (inverted U-shape) between WKCR and ROA suggesting that the inclusion of WKCR square in the model is necessary. Specifically, in line with the previous studies (

Boțoc and Anton 2017), the authors propose the following hypothesis:

Hypothesis 1. There is a non-linear relationship between working capital and financial performance, with an optimal working capital level that maximizes firm profitability.

3. Data and Methodology

Data were collected from the Amadeus database and the final sample comprised 719 listed firms on the Warsaw Stock Exchange for the period of 2007–2016, which corresponds to 3043 firm-year observations. We exclude from the initial sample financial firms and firms with missing observations for our variables of interest.

The econometric analysis regresses firm profitability against the working capital ratio (WKCR) and its square (WKCR

2). Firm performance is measured by return on assets (ROA), an overall indicator of profitability, calculated as net income to total assets, consistent with the previous studies (

Dalci et al. 2019;

Enqvist et al. 2014). For the robustness purpose, operating return on assets (OROA) has been considered as an alternative measure for profitability, defined as earnings before interest and taxes (EBIT) to total assets ratio. Supplementary independent variables are also considered in the regression model to account for additional determinants of corporate performance, as follows: debt ratio (DEBTR) calculated as the sum of non-current liabilities and loans over total assets; cash ratio (CASHR) computed as cash and cash equivalents divided to total assets; the one-year growth rate in sales (SALESGR), computed as (Sales

1 − Sales

0)/Sales

0, as a proxy for growth opportunities; firm size (SIZE), measured as the logarithm of total assets. The independent variables are described in

Table 1.

Table 2 displays the descriptive statistics for firm profitability, working capital ratio, and the control variables.

Table 2 shows that for Polish firms under the analyzed period, return on assets is, on average, around 1%, while the working capital ratio represents, on average, 19.71% of sales. The value for ROA is comparable with those reported for the German non-financial firms (1.1% reported by Dalci et al. 2019) but considerably lower than those reported for the Finnish firms (8.4% reported by Enqvist et al. 2014) or for the Spanish SMEs (7.9% reported by Garcia-Teruel and Martinez-Solano 2007). The sales of Polish firms on average increased by almost 13% annually and debt represents 23.46% of total assets.

Table 3 shows correlations among the dependent and independent variables of the econometric model. It can be noticed that the coefficient between ROA and WKCR is positive, while the coefficient between ROA and WKCR

2 is negative, which shows that working capital management, above its optimal level, has a less efficient effect on corporate profitability. The results also indicate a negative effect of debt ratio on the working capital level. Growth opportunities relate positively to working capital. The correlation matrix highlights low correlations between independent regressors, therefore the analysis does not suffer because of multicollinearity.

The following econometric specification is used to test the hypothesis regarding the impact of working capital management on firm profitability:

where the dependent variable ROA is the return on assets; the independent variables of interest are WKCR

i,t, measured as (inventories + debtors − creditors)/sales for the firm i at time t, and its square term (WKCR

2i,t) used to test for the non-linearity of our model; as control variables, we employ DEBTR

i,t (debt ratio), CASHR

i,t (cash ratio) and SALESGR

i,t (one-year growth rate in sales); μ

i,t denotes the unobservable firm and time effects; λ

j is an industry unobservable effect; ε

i,t represents the error term.

The study employs three different panel data techniques to estimate Equation (1). Firstly, a pooled ordinary least-squares regression model (OLS) with robust standard errors is estimated to get heteroscedasticity-robust estimators. Secondly, a static panel model with fixed-effects (FE) is defined. The Hausman test was employed to detect the endogenous predictor variables and to choose between fixed-effects or random-effects models. The null hypothesis states that there is no correlation between the error term and the regressors, and, therefore, the preferred model is random effects. In our case, the test rejects the random-effects specification so fixed-effects estimations are employed. Thirdly, in line with

Beck and Katz (

1995), the research also employs a panel-corrected standard errors (PCSE) to account for firm-level heteroscedasticity and contemporaneous correlations across firms. Following

Petersen (

2009), the robust standard errors clustered at the firm level were used to simultaneously relax both the assumption of homoscedasticity and the assumption of no autocorrelation in the panel dataset. Time fixed effects are included to control for macroeconomic shocks that might influence firm profitability in a certain year.

5. Conclusions

Our paper provides empirical evidence on the working capital-profitability relationship for a sample of 719 listed firms from Poland over the period of 2007–2016. Based on different panel data techniques, the relationship proved to be inverted U-shaped. The empirical results highlight that, at a low level of working capital, increasing sales and discounts on early payments significantly influence positively corporate profitability. However, a further increase in working capital above its optimum level establishes a negative working capital–profitability trend, which indicates the disadvantages of working capital financing, respectively opportunity cost and high-interest charges. Firm-specific variables were considered. The findings show that the debt ratio and cash ratio are statistically significant determinants of profitability. In line with the Pecking Order Theory of capital structure, firm profitability is negatively associated with debt. Other control variables (sales growth, cash ratio, and firm size) are found to be important determinants of firm profitability. The empirical findings proved to be robust while using an alternative proxy for the dependent variable–operating return on assets (OROA), and when additional firm-related control variables were considered.

The current study brings theoretical and practical implications. For researchers, our results suggest that a quadratic model needs to be tested for any sample of firms. In terms of practical implications, Polish firms exhibit an inverted U-shaped relationship between working capital and corporate performance, meaning that managers should avoid negative effects on firm profitability through lost sales, lost discounts for early payments, or supplementary financing expenses. The results suggest that corporate financial executives should avoid greater net investment in working capital and target its optimal level, while internally-generated funds can be oriented towards more profitable investment opportunities. Reducing unnecessary working capital releases unnecessary cash invested to fund daily operating activities and increases the firm financial flexibility. Therefore, corporate managers should focus on maintaining accounts payable, accounts receivable, and inventory turnover at a certain level, to maximize the effects of working capital for the benefit of the shareholders. Our results highlight the importance of WCM for profit maximization. The results are suitable for use in business practice, highlighting the importance of finding and attaining the optimal level of working capital.

The study is not without limitations. Firstly, the empirical findings are limited to the listed firms from one emerging country (Poland). Moreover, from the endogeneity perspective, most of the financial variables at the firm level are determined in a network of relationships. Future research extending the sample of countries and controlling for macroeconomic factors and endogeneity issues could bring a valuable contribution to the field. New directions of research should include the role of corporate governance and compensation incentives in mediating the relationship between working capital management and firm profitability (

Coles and Li 2019;

Coles and Li 2020).

{kind=link}