Investor Intention in Equity Crowdfunding. Does Trust Matter?

1

Department of Business, Universitat Autònoma de Barcelona, 08193 Bellaterra, Barcelona, Spain

2

Faculty of Applied Studies, Department of Business Administration, King Abdulaziz University, Jeddah 21589, Saudi Arabia

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(2), 53; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14020053

Submission received: 24 November 2020

/

Revised: 12 January 2021

/

Accepted: 18 January 2021

/

Published: 27 January 2021

(This article belongs to the Special Issue Crowdfunding)

Abstract

:Equity crowdfunding (ECF) is becoming a convenient alternative instrument for investing in entrepreneurs’ projects in many countries. The purpose of this study was to investigate the factors that affect the investor’s intentions toward ECF platforms in Saudi Arabia, where they have not been introduced until very recently. This context offers a unique opportunity to test the role of investors’ perceived trust in the context of ECF. The proposed framework builds on two critical layers: (1) trust in the platform (intermediary) and (2) trust in the fundraiser. Structured equation modelling was applied to examine the factors that affect investors’ trust and intentions. The framework was analysed using survey data from 216 users of Manafa, one of the largest ECF platforms in Saudi Arabia. Our findings showed that both fundraiser and platform trust have a significant effect on the investor’s intentions. In particular, trust in the platform substantially impacts the fundraiser’s trust, showing the importance of the fundraiser’s reliance on trusted institutions. On the other hand, to build investors’ trust, fundraisers must deliver high-quality information for their projects.

1. Introduction

Crowdfunding has emerged as an alternative source of for-profit and non-profit financial aid for entrepreneurs. In 2008, during the economic crises, many small and medium enterprises (SME) and start-ups transformed their traditional practices by seeking funds from the crowd platforms instead of financial institutions such as banks (Tomczak and Brem 2013). Recently, crowdfunding has become an excellent financial recourse for the individuals, business and the public sector. The adoption of Web 2.0 (Bouncken et al. 2015), allows individuals to share their information through websites and applications. Thus, technology helps entrepreneurs connect with millions of potential investors. Project creators on crowdfunding platforms request funds for a particular project, while crowd investors (termed bakers, funders or sponsors, depending on the platform purpose) contribute to for-profit or non-profit projects. Crowdfunding uses mediation by collecting numerous small amounts of money from a vast number of individuals; this approach to fundraising is open to the funder and applied through the internet.

Crowdfunding is considered an element of the internet economy, with many countries issuing policy responses in financial technology (fintech) regulation. According to the Global Crowdfunding Industry Report 2015, 344 million households are expected to use their savings to invest in crowdfunding by 2025 (Massolution 2015). Academic research in the field of crowdfunding has increased. The majority of scholars have been investigating the types and definitions of crowdfunding and the funders’ motivation and geographic character (Alegre and Moleskis 2016).

Crowdfunding emerged after the concept of crowdsourcing, which allows the crowd to solve problems by applying online tasks to the crowd (Paschen 2017). Firms have been using crowdsourcing to solve their internal task sourcing constraints. Moreover, firms can attain new ideas and answers from the crowd (Van der Have and Rubalcaba 2016). Crowdfunding offers a more innovative role in a capital raising and problem-solving paradigm.

The goal of crowdfunding (whether commercial or charitable) is to use the power of the crowd to obtain a small portion of the money that collectively will provide enough capital to establish a proposed project, which may be unlikely to succeed through traditional bank funding (Ullah and Zhou 2020). Based on the literature, scholars have identified different crowdfunding types based on what the funder will be given in exchange for their monetary contribution (Walthoff-Borm et al. 2018). In this study, we investigated equity crowdfunding.

ECF platforms fund new venture entrepreneurs, enabling them to start or develop their projects. In ECF, unlike other types of platforms (reward1, peer-to-peer2 and donation crowdfunding3) the project’s owner offers shares to the funders as a percentage of the company running the project. ECF has become an alternative financial instrument for investors (Hollas 2013).

In developing countries, fintech financial solutions have been challenging the traditional forms of finance. At the Middle East Financial Technology conference (MEFTECH) 2020, Saudi Arabia declared its intent to be a hub of financial technology, a stated goal in the Saudi Vision 2030. According to the Fintech Saudi annual report published in 2020, the fintech industry continues to expand. The value of fintech transactions from 2017 to 2019 increased by 18% annually, achieving more than USD 20 billion in 2019 (Resources—Fintech Saudi n.d.) Moreover, the Saudi fintech market is expected to have over USD 33 billion worth of transactions. Between 2020 and 2024, those transactions will grow by a Compound annual growth rate(CAGR) of 2.4% annually, with an estimated overall amount of USD 3.2 million (Crowdfunding—Saudi Arabia|Statista Market Forecast n.d.). The Saudi Arabia Monetary Authority (SAMA) and Capital Market Authority (CMA) are working to develop regulations and rules for the Saudi financial capital markets, including the primary goal of meeting the objectives of the 2030 vision of Saudi Arabia.

Furthermore, the vision recognised SMEs and their essential role in economic growth. CMA has recognised the need for investment diversification channels from the traditional financial source, reducing unemployment and raising the Saudi gross domestic product (GDP). Hence, the CMA initiated a financial technology lab called FinTech Lab to enhance economic activities through technology applications. Under the authority of Saudi Arabia Capital Market law Royal Decree No. (M/30) (31 July 2003) and The Financial Technology Experimental Permit Instructions (1 October 2018), CMA announced its first batch of FinTech ExPermits in February 2018. One of the first companies to get an experimental permit was the equity crowdfunding platform, Manafa.

To a greater or lesser extent, entrepreneurs know that, in the real world, most of the critical factors affecting success are out of their control. Currently, many cases of fraud in crowdfunding have made building trust a challenging task for entrepreneurs. This effect is evident in reward-based crowdfunding. The delay or inability to deliver the product is considered fraud. In contrast, ECF fraud (that is when entrepreneurs are involved in illegal and unethical activities) is hard to detect (Cumming et al. 2020). When asking about the importance of trust in equity crowdfunding, every practitioner and entrepreneur will answer affirmatively. Nevertheless, being trusted entails taking multiple actions. It is easy to misunderstand what trust is about, and how it can be generated unless rigorous evidence is provided. This shows that different and generally complementary strategies have a real impact on micro investor decisions. In the Saudi business environment, trust is essential in a business relationship (Abosag and Naudé 2014). Recent studies have investigated trust in reward-based and lending crowdfunding and suggest that trust plays a significant role in project success (He et al. 2016; Moysidou and Hausberg 2019). Unlike the traditional investment process, investors who intend to invest in a start-up tend to look at the project owners more than the financial disclosure; investors tend to spend money on people they trust (Moysidou and Hausberg 2019). In donation crowdfunding, trust has a significant effect on the intention to donate (Chen et al. 2019). There is no doubt that the topic of trust and its impact on investors’ intent needs attention, particularly in the context of ECF, where complexity and uncertainty are high, and information asymmetries abound. Unlike P2P crowdfunding, investors in ECF focus on the mid-to-long term.

Thus, a gap in research is found on the need to determine trust and its effect on investors’ intention in the context of ECF. This study aimed to know how trust in the field of ECF is established and the impact of trust of the fundraiser and the platform on the intention of potential investors. We investigated interpersonal and institutional trust in the field of crowdfunding by applying two well-known trust theories, swift trust (Meyerson et al. 1996) and transfer trust (Stewart 2003). These theories fit comfortably in the field of crowdfunding, where trust is original and temporary. Swift trust occurs in short-term organisational structures that include quickly formed teams or groups. According to Meyerson et al. (1996), a group of people engage in trust first, then they verify and confirm trust values accordingly. On the other hand, transfer trust suggests that trust is conveyed from the platform to the vendors (Stewart 2003) and has been employed notably in the context of e-commerce. Online trust does not rely on a long-term relationship, and it does not require previous experience or past behaviour. Therefore, these theories allow us to frame the potential significance that trust may exert on potential investors’ intention in ECF.

Guided by the swift and transfer trust theories (Meyerson et al. 1996; Stewart 2003), this study examined the effect of familiarity, the disposition to trust, project information quality, trust in the fundraisers and confidence in the platform as factors in the investor’s intention in the ECF platform. Our empirical findings showed that, in equity crowdfunding, the most crucial factors that positively affect the investor’s intention were perceived project information quality and perceived trust in the platform. We also found that perceived trust in the platform has a significant impact on the perceived trust in fundraisers. The results are valuable for both entrepreneurs and platforms.

From a theoretical perspective, this study contributed to the crowdfunding literature in several ways. First, we used the swift and transfer theories (Meyerson et al. 1996; Stewart 2003), a framework that fills an essential gap in the ECF literature. To our knowledge, there is no study investigating the effect of trust on the investors’ intention to invest in ECF. This study is the first to examine the impact of trust in ECF in developing countries. From a practical standpoint, this study provided intuitive concepts for entrepreneurs on how to build trust in their relationship with investors. It also offered crowdfunding platform guidance on how to enhance and model the functions of the platform. Second, the study findings will contribute to the literature on information asymmetries and uncertainty in ECF. Likewise, the intention to invest in ECF is an essential factor that empowers a project’s success. Furthermore, ECF is particularly interesting because of the complexity of its contractual process and crowd involvement. Finally, prior studies have focused primarily on developed countries, whose findings may not apply to Saudi or Middle Eastern environments. To provide a greater understanding of investor behaviour in Saudi ECF platforms, further research on one of the developing country’s ECF is needed.

The remainder of this paper is organised as follows: Section 2 introduces the conceptual framework and the literature review results related to our study. Section 3 presents the study hypotheses. In Section 4, we describe the research methodology, including data collection and measurement and the results of structural equation modelling. In Section 5, we discuss the study findings and their implications. In the final Section 6, we consider study limitations and opportunities for future study.

2. Conceptual Framework and Hypothesis

2.1. Conceptual Framework

The concept of social capital is multidimensional (Hazleton and Kennan 2000; Nahapiet and Ghoshal 1998). The dimensions are cognitive, relational and structural social capital. Cognitive, social capital can support people in the association to increase social capital due to the shared narrative and shared language. Structural social capital suggests structural features, for example, network ties, roles and rules. Both cognitive and structural capital relate to the network’s relationship, not to the quality of the relationship. Nevertheless, relational social capital describes the relationship’s quality, meaning trust, trustworthiness, expectations and obligations of the social network (Cabrera and Cabrera 2005).

Trust is considered a relational, social and capital characteristic, introduced into crowdfunding by (Zheng et al. 2014). It encouraged research by involving various aspects of relational social capital. Trust is a vital aspect of entrepreneurial finance (Mochkabadi and Volkmann 2020) and one of the significant impacts on the supporters’ intention in crowdfunding (Strohmaier et al. 2019). Similarly, the decision-making in venture capital is influenced by a trust (Bottazzi et al. 2016). Crowdfunding platforms assume trust among fundraisers and investors when funders are encouraged to support a project’s creator.

Thin trust, which is the trust between strangers and trust in the internet, “the level of confidence assigned in the internet effectiveness a medium to conduct transactions,” has been investigated in the equity-based crowdfunding platforms (Kshetri 2018). A study of a Chinese peer-to-peer platform applied the trust model to understand critical factors that affected investors’ trust in fundraisers (the borrower) and trust in intermediaries (Chen et al. 2014). Chen et al. found that trust in the platform and trust in the borrowers significantly impact the funders’ intention. Trust has further been divided into calculus and relationship trust relating to ECF. We examined the trust effect on the willingness of investors using a research model with three measures: (1) entrepreneur-related, (2) project characteristics and (3) platform-related (Kang et al. 2016). Moreover, individual trust expectations can be distinguished as either competence-based trust or integrity-based trust (Connelly et al. 2018). Competence-based trust is when the trustee has the technical and interpersonal competencies to complete their work. In crowdfunding, competency-based trust is represented by trust in the entrepreneurial capabilities of the fundraiser. In addition, the project creator’s creditworthiness would be measured by their previous successful experience in crowdfunding (He et al. 2016). Integrity-based trust is rooted in the trustee’s experiences, personality, motives and honesty.

Equity crowdfunding entails high levels of information asymmetry between entrepreneurs and potential investors (Ahlers et al. 2015). Thus, trust plays a significant role for those who want to invest in a project presented on the platform. However, distrust can negatively impact potential investors (Lee et al. 2010). Trust requiring a face-to-face bonding relationship between the trustors and the trustee is traditional trust. Moreover, trust must be built through a high degree of communication, which is unlikely to happen in the internet community. The conventional trust model considers trust to be a developing progression (Wang et al. 2016). Trust typically occurs after a dependable relationship history slowly developed through people’s communication of prior behaviour (Gefen 2000).

However, the traditional trust model cannot explain the levels of trust in the geographically dispersed team or virtual team (Robert et al. 2009). This type of trust, called swift trust, was explored by Meyerson et al. in 1996. Swift trust is a type of trust that happens in a temporary group and can involve a quick-starting team (Meyerson et al. 1996). Swift trust is an initial trust that occurs at the beginning of a relationship when there has been no previous communication with the trustee. ECF is a complex type of crowdfunding because the exchange implies not just contributing to a project but owning part of a legal entity (Moysidou and Hausberg 2019). Thus, swift trust theory provides an appropriate approach that could be applied in this study.

The other type of trust used in our study is the transfer trust theory (Stewart 2003). Transfer trust proposes that one person can trust another unfamiliar person based on the level of confidence in a familiar person or object when there is a particular connection between the familiar and unfamiliar person or object (Wang et al. 2013). In our study, the familiar object is the platform, while the unfamiliar object that lacks information is the entrepreneurs.

Though trust is one of the significant elements affecting an investor’s decision relating to online investment, few studies have examined the effect of trust on the project’s success in the field of crowdfunding. A high degree of online trust in the internet community is more important than face-to-face trust (Grabner-Kräuter and Kaluscha 2003). In particular, in the context of ECF, trust is essential, not only because the ECF occurs online but also because the majority of funders are not sophisticated investors (Belleflamme et al. 2014).

Because most information on crowdfunding platforms is unsupported, the relationship between the fundraiser and the crowd is hampered by asymmetries (Moritz et al. 2015). Thus, potential investors focus on identifiable entrepreneur signals; information on the project page is one of the signs that investors receive (Bi et al. 2017). The level of trust varies for each type of crowdfunding because each kind of profit crowdfunding differs in its contribution (Moysidou and Hausberg 2019). As mentioned previously, ECF is the most complex type of crowdfunding, requiring high levels of trust. Thus, trust is essential to surmount the information asymmetries.

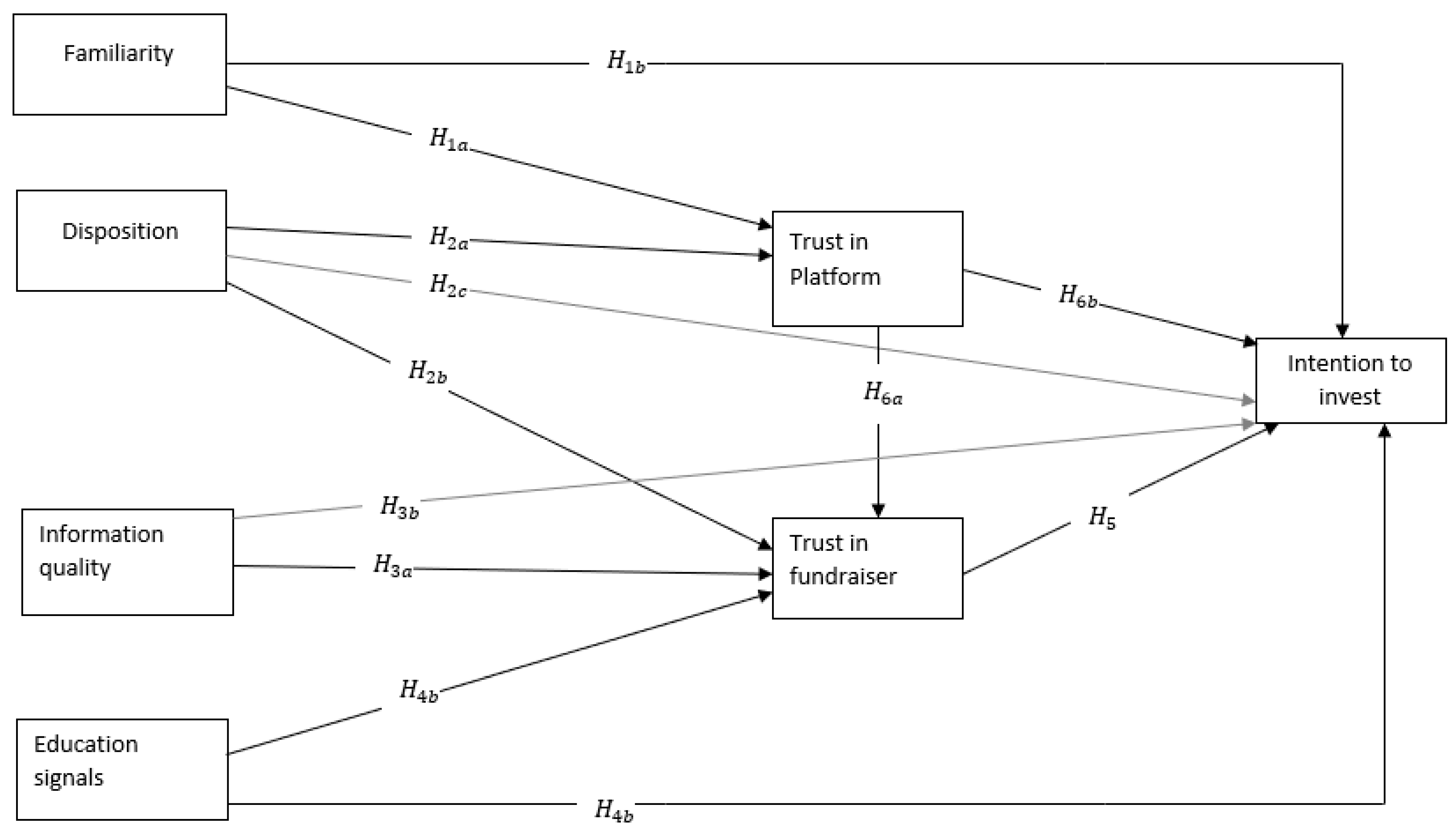

This study examines the effect of familiarity, project quality, disposition to trust, education signals, fundraiser’s trust and platform trust in investors’ intention in the equity crowding platform (Figure 1). Moreover, fundraiser trust and platform trust have been tested as endogenous and mediation variables.

2.2. Hypothesis

2.2.1. Familiarity

Familiarity describes investors’ acquaintance with the ECF platform throughout the interaction. Investors can predict the platform behaviour, which is the mediator based on the experience gained from previous communications (Kim et al. 2008). Therefore, the investors acquaint themselves through the platform and develop familiarity with the behaviour of the intermediate. A buyer’s familiarity with the online business party indicates the buyer’s level of acquaintance with the selling unit, including the seller’s knowledge and an understanding of the relevant process, such as looking for products and information and buying through the platform.

According to Luhmann (2018), familiarity is a prerequisite of trust because trust usually deals with the belief in a potential entity’s action, while familiarity deals with understanding the current entity’s action (Gefen 2000). Consumers or investors often return to the platform when they have had a pleasant experience; they will not revisit the platform when they have had an unpleasant experience. Thus, investors will develop a high level of familiarity with the platform where they have had favourable experiences. Investors who have a positive experience with the platform will stick to the platform and project a strong perception of what they expect in the future (Kim et al. 2008). Investor’s loyalty defines the trust that the investors have in the platform. Familiarity represents the investors’ degree of trust in the crowdfunding framework (Moysidou and Hausberg 2019). Moreover, in crowdfunding, investors typically invest in different projects but chose the platform with which they have had a positive experience. Thus, an investor frequently attempts to invest in projects posted on the trusted platform.

Interface complexity is another element of potential investors’ intricacy. For example, how, where and what information does an investor need to do what is required? Familiarity should mitigate this complexity and result in enhanced use of the platform (Luhmann 2018). On the other hand, those affected by the platform’s complexity are more likely to quit investing in the platform, simply because they may not understand what to do and how to do it. Thus, the following hypothesis suggests that familiarity increases trust in the ECF platform and the potential investors’ intention.

Hypothesis 1 (H1).

Familiarity with crowdfunding (H1a) and the crowdfunding platform (H1b) are positively associated with investors’ intention.

2.2.2. Disposition to Trust

Here, we turn to the three types of trust identified by McKnight et al. (1998, 2002): (1) trusting beliefs, (2) trusting intention and (3) disposition to trust. McKnight et al. compressed the disposition to trust into faith in humanity and a trusting stance in the same study. The propensity to trust is an additional attendance of trust. However, that trust has not been built-in gradually through consistent interaction. Moreover, the disposition to trust has been described as a person’s general tendency to trust others (Bélanger and Carter 2008). The propensity to trust is a psychological concept identified by Erikson (1968) and Rotter (1967). This concept rests on the premise that individuals develop general beliefs about people’s reliability throughout the cycle of their lives. Thus, the disposition to trust is not founded on knowledge or experience with another person. In our framework, an investor’s propensity to trust is the extent to which a person shows a willingness to depend on others throughout a wide range of circumstances and players.

The disposition is not built on previous information or experience about a specific trusted group but is autonomous of the particular perspective (Kenning 2008). On the other hand, it is the outcome of ongoing socialisation and lifetime experiences (Fukuyama 1995; Uslaner 2008). A study on leading Chinese crowdfunding found that disposition to trust is essential to initiating trust in the investment process (Chen et al. 2014). Another crowdfunding survey found that backers’ disposition to trust has a positive impact on fundraisers’ perception of trust (Moysidou and Hausberg 2019). In e-commerce, consumers’ propensity to trust was observed to impact online trust (Teo and Liu 2007). Disposition to trust is crucial in the short-term or initial relationship, especially in the virtual environment in which parties are not familiar with each other. Thus, a disposition to trust in an active crowdfunding environment is expected to be evident in an impromptu relationship where information about the fundraiser (trustees) is not clear. Therefore, the disposition to trust will have a significant effect on endogenous variables: fundraiser trust, platform trust and investors’ intent.

Hypothesis 2 (H2).

Disposition to trust is positively associated with (H2a) the equity crowdfunding platform, (H2b) the fundraiser and (H2c) investors’ intention.

2.2.3. Project Quality

In this study, the quality of project information was described as the degree to which an investor accepts that the information that he or she has been given about a project is of high value (Liu et al. 2018). Unlike traditional investors, crowdfunding investors access all of the project information (financial and non-financial) from the project page. Because multiple projects are posted simultaneously and with the same purpose, funders can distinguish projects that are reliable from those not by obtaining specific information such as project goals, project owner and the amount of funding. A recent study on crowdfunding lending found that project quality significantly affects the fundraiser’s trust (Moysidou and Hausberg 2019). Moreover, cognitive trust is defined as the “trustor’s rational expectations that a trustee will have the necessary attributes to be relied upon” (Komiak and Benbasat 2006). Cognitive trust belongs to reasoning activity or, according to Lewis and Weigert, “good rational reasons why the object of trust merits trust” (Lewis and Weigert 1985). Furthermore, in cognitive trust, sophisticated investors’ trust and confidence in the project initiators are based on their knowledge, reliability and competence; while, in crowdfunding, constant communication along with previous experience between the trustors and the trustees has not always existed. Therefore, cognitive trust is founded on” good rational reasons.” Accordingly, we propose that project information quality will significantly impact the fundraiser’s trust and the investors’ intention.

Hypothesis 3 (H3).

Perceived project quality is positively related to trust in (H3a) the project fundraiser and (H3b) the investors’ intention.

2.2.4. Education Signal

Once a project is launched on the platform, investors face enormous uncertainty from the fundraiser. When entrepreneurs lack track records or actual output, such as a source of revenue, the fundraisers’ human capital will be one of the primary signals, particularly the project founder’s education (Grossman 2006). The role of education is a quality signal of human capital (Spence 1978). Various studies have shown positive and sustainable relationships among entrepreneurs’ educational level and project success (Cooper et al. 1994; Wiersema and Bantel 1992). Educated entrepreneurs not only offer greater knowledge; they also have considerably more of the skills needed for a project’s success (Barbi and Mattioli 2019).

Moreover, most of the information on human capital is represented by formal education. In the context of entrepreneurial finance, initiators who have a PhD are expected to receive funds from investors in the early stages (Hsu 2007). Likewise, a new venture capital study found that start-up ventures are more likely to be funded if the owners have “high academic status” (Backes-Gellner and Werner 2007). The same study found that fund-seekers with an academic degree can quickly get a loan and have fewer labour problems. In the field of crowdfunding, one of the first studies on the context of equity-based crowdfunding investigated the impact of entrepreneurs’ education as a signal, choosing an MBA holder as an indicator of a broad education (Ahlers et al. 2015). Thus, the education signal has a high impact on the fundraisers’ trust and investors’ intention.

Hypothesis 4 (H4).

The perceived entrepreneur’s education signal is positively associated with trust in (H4a) the project fundraiser and (H4b) the investors’ intention.

2.2.5. Fundraisers Trust

Investing in ECF is considered to be a high-risk, long-term investment. Trust in the fundraiser was hypothesised in this research as confidence that the fundraiser will perform cooperatively to satisfy the investor’s expectations (McKnight and Chervany 2001). Fundraiser trust is vitally necessary for funding achievements. In the context of crowdfunding, investors can choose to invest in a project offered from multiple entrepreneurs, but many are generally not accustomed to dealing with those fundraisers. Further, investors and project owners do not usually repeat transactions (Lin et al. 2013). Investors in crowdfunding lending are subject to risk, information asymmetry and uncertainty in their investment decisions (Chen et al. 2014). Thus, investors must thoroughly assess the fundraisers in all aspects. The fundraiser assessment can be provided through the information on the project page to indicate the project owner’s honesty and reliability. Investors’ trust in the fundraisers can be effected through the regulation of the transaction because the technical protection of the platform can avoid fundraiser fraud. Furthermore, entrepreneurs who are explicit about their obligations and good standing will reduce the probability of fundraiser failure (Liu et al. 2015). Studies of trust and behavioural intention found that an individual’s personality affects the attitude of trust (Brown et al. 2004; Gefen et al. 2003).

Interpersonal trust has been examined to investigate human behaviour in offline and online environments. This concept is fundamentally crucial in an individual’s behaviour (Jarvenpaa et al. 1998; McKnight et al. 2002; Parks and Floyd 1996). In this study, we applied interpersonal trust and confidence between the investors and fundraisers. Interpersonal trust has been tested in various fields such as economic behaviour, financial decision behaviour and human resources. Rotter (1980) defined interpersonal trust as a “general expectancy, held by a group or individual that the trustor’s written and oral statement can be relied on.” Rotter introduced the interpersonal trust scale (ITS), containing 25 items that evaluate trust in individuals generally and particular groups, such as parents and public officials. Thus, in ECF, the fundraisers play a significant role in trust through the project page’s information. Moreover, a more confident attitude about investing will be built when trust conquers uncertainty (Chen et al. 2014). Previous studies have suggested that vendors’ trust positively affects the intent to purchase (Pavlou and Gefen 2004; Sun 2010). These findings can likewise be supported in virtual environments. Hence, we concluded that the fundraiser’s trust influences an investor’s intention to invest.

Hypothesis 5 (H5).

Trust in the project fundraiser is positively associated with the investors’ intention.

2.2.6. Platform Trust

Similar to e-commerce, crowdfunding requires not only a seller (fundraiser) and a purchaser (investor), but a platform (intermediary) (Pavlou and Gefen 2004). The ECF intermediary is the platform or, in other words, the marketplace. The platform utilises the internet structure to expedite investing operations through investors and potential entrepreneurs by managing, collecting and distributing information (Moysidou and Hausberg 2019). Therefore, investors should trust both the fundraisers and the platforms. Trust in a crowdfunding platform (intermediary) has been defined as an individual investor’s confidence in the belief that the platform will organise and apply policies, rules and outcomes efficiently and honesty (Bansal et al. 2016).

Furthermore, the platform’s technical protection leads investors to trust the fundraisers. Because of investors’ high risk, the security and safety of investors, such as authentication, fraud safeguard and escrow services, are the platform’s primary concern. In addition to protection and security, investors assume that the platform will provide high-quality services to aid the transaction (Liu et al. 2015). Furthermore, platforms (profit or non-profit) that collect money from the crowd without permission from the Capital Markets Authority of Saudi Arabia are prohibited; this should add credibility to the intermediary. Both formal and informal institutions can affect investor’s trust. Institutional trust has been defined as the relationship between an individual (investor) and an institution (equity crowdfunding platform). In the absence of an institutional perspective, crowdfunding platforms sometimes substitute that absence by providing the necessary institutional safety net. Usually, crowdfunding platforms have their own internal processes that allow honest and trustworthy fundraisers to launch their project on the platform to protect their investors.

In this study, we adopted the theory by Stewart (2003) on trust transfer, arguing that trust in the platform is a crucial factor that builds confidence for the potential investor’s trust in the fundraiser. That trust can affect the willingness to invest. Nevertheless, goodwill and skills cannot be detected by potential investors in the absence of frequent communication. As an alternative, investors rely on platform signals by viewing the pre-launch procedures. Hence, in this study, we suggest that trust in the platform positively affects trust in the fundraiser and the investors’ intention.

Hypothesis 6 (H6).

Trust in the platform positively affects trust (H6a) in the project fundraiser and (H6b) the investors’ intention.

3. Methodology

3.1. Context of the Research

An online survey was administered to the users of Manafa, one of the ECF platforms in Saudi Arabia. Manafa is authorised by the Saudi CMA, which makes it trustworthy (Gazzaz 2019). According to available platform statistics (https://www.manafa.sa/), Manafa has more than 25,000 active investors. During 2019, more than 1.5 million people visited the platform. Females hold 12% of the currently active accounts, while less than 1% are professional investors; the rest are laypeople. To register on this platform, the investor must be a resident of Saudi Arabia. The investor’s identity is confirmed through a government-issued ID, which affects the ease of use of the platform and dramatically enhances trust.

Each investor registered on the platform can independently decide where to invest after reviewing the project’s information and the risks it entails. The standard information provided about a project includes its description, financial information, market information, management team, sometimes a short video presentation, fundraiser profile and risk. Apart from that, information about the equity price and minimum shares that investors can pledge is provided, along with the project evaluation.

3.2. Sample

The study data were gathered through an online survey. We distributed the survey through email and social networks, targeting those registered on Manafa and had who visited the platform. The survey was distributed between 1 February and 20 March 2019. Because the study examined the investor’s intention, the target participants were those who had an account on the platform, not just those who have already invested through it. A total of 267 people participated in the study, of which 216 completed the survey. The average time required to complete the survey was 8.4 min.

Table 1 shows the breakdown of the survey sample by primary demographic variables. As shown in the table, most of the study participants were between 35 and 44 years of age, while a significant portion was aged 25 to 34. Although males dominated the sample, there were more females than indicated in the official report by Manafa (compare 20.8% female respondents in this survey to 12% female account holders reported by Manafa). Most of the respondents had a bachelor’s degree, while a considerable proportion had a master’s degree. Most of the respondents were married.

Apart from the demographics presented in Table 1, there were other significant characteristics of the sample. A total of 173 participants (80.1%) reported they had invested in the stock market before; while a total 134 (62%) reported that they had made some other type of investment. Interestingly, only 31.9% (69 participants) said that they had previously invested in cryptocurrencies.

3.3. Measurement

The scale used for the measurement was based on sources in the literature. All items were modified to adjust to the context of ECF. Five-point Likert scales ranging from 1 (strongly disagree) to 5 (strongly agree) were used to rate each item’s level of agreement. The scale was constructed to cover several domains. First, participants’ familiarity with ECF was assessed with items adapted from Gefen’s scale (Gefen 2000). That section was followed by assessments of project information quality (Kim et al. 2008; and Xu et al. 2013) and the disposition to trust (Gefen 2000). Platform trust items were adopted from McKnight et al. (2002), as were fundraiser trust items. We constructed items ourselves to measure the fundraiser education signal domain, as they were not present in the available literature. Finally, items related to investor’s intention were modified and applied from a study by Dodds et al. (1991).

The survey items were initially developed and modified in English, then translated to Arabic. The questionnaire was distributed in both English and Arabic. To minimise potential errors and ensure that the translation was accurate, a pilot test was conducted. For this evaluation, ten PhD students reviewed the questionnaire and identified potential problems. Minor changes were made to the survey to ensure clarity, readability, completeness and validity. Table 2 shows all of the survey items and their coding in the database and place of origin.

4. Results

4.1. Model Measurement

4.1.1. Common Method Bias (CMB)

Single-factor analysis was used because it is most used to identify CMB. This analysis was done to test the real preferences of the respondents. This method uses exploratory factor analysis (EFA) to test for CMB. When testing for CMB with EFA, all variables were loaded onto a single common factor. Because only one factor was relevant, no rotation was applied (Podsakoff et al. 2003). The logic of Harman’s single factor test (Harman 1976) is that the single factor on which all items are loaded would not explain more than 50% of the total variance (Podsakoff et al. 2003). When we followed that procedure in this study, the variance explained by the single factor was 18.924%, far below the problematic 50%. We concluded that CMB did not influence this study’s results.

4.1.2. KMO and Bartlett’s Test

Both the KMO test and Bartlett’s test must be sound to conduct exploratory (EFA) or confirmatory (CFA) factor analysis (Kline 2014). In this study, both conditions were satisfied with the p-value associated with Bartlett’s test being significant (p < 0.05) and the KMO test equal to 0.746. The results were higher than the necessary recommended values and supported the notion of conducting EFA and CFA on the data.

4.1.3. Reliability, Validity Analysis and Model Fit

The reliability of measurement is the constancy of the measured concept (Bell and Bryman 2007). Internal reliability, stability and inter-observer consistency are the three critical factors involved when considering whether a measurement is reliable. Through time, the stability of measurement is under the influence of whether it is balanced. Internal reliability can be viewed as the extent to which all items of a compound measurement provide reliable estimates. Inter-observer constancy is described as a lack of differences in subjective judgment, in which more than one observer evaluates the scale.

In this study, internal consistency was used to assess the scale’s reliability. Because the scale was comprised of different domains and its score was summative (implying that all items have the same importance), it is understandable if the reliability measure is somewhat lower. To calculate the reliability measure based on internal consistency, Cronbach’s alpha index was used. While this index ranges from 0 to 1, guidelines for its interpretation are that values lower than 0.5 is considered low, those between 0.5 and 0.7 are considered moderate, values between 0.7 and 0.9 are deemed very reliable, and those higher than 0.9 are considered to be very high or to have outstanding reliability (Spicer 2005). Table 3 displays the reliability measurements for every scale domain, reflecting that if all values surpass the value of 0.7, we can conclude that the administered scale was exceptionally reliable.

4.1.4. Confirmatory Factor Analysis (CFA)

The CFA was conducted using the AMOS 22.0 software package. Hair et al. (2010) suggested that the validity of the CFA model can be evaluated through two major prisms: fit indices and overall construct validity. The constructed measurement model is comprised of seven latent variables with three items loading onto each of them. The item-latent variable correspondence is shown in Table 3.

The indices known to provide the most stable and accurate results were used to evaluate Hair’s recommendation for evaluating the model fit using at least four indices. χ2/df is a commonly employed index of model fit; in this study, it was 1.753. Apart from this index, the values of several more are reported: IFL was 0.928, TLI was 0.908, while CFI was 0.981. As Hair et al. (2010) noted, all of these indexes should be equal to or above 0.9 to be considered acceptable. Additionally, an RMSEA of 0.059 was observed.

Apart from the fit indices presented above and noted by Hair et al. (2010), it was essential to validate the CFA outcomes by examining the construct validity (Hair et al. 2010). Although the validity of a scale can be operationalised in many ways, one of the most frequently used is the convergent validity approach. If a scale is unidimensional, consistent with the original definition (that is, it measures what it was intended to measure) and sufficiently reliable, it can be deemed valid. This study examined the extent to which validity was met through the examination of convergent validity.

Convergent validity, as defined in the literature, implies that the items on the same topic or belonging on the same scale domain share a considerable proportion of the common variance (Hair et al. 2010). This study assessed this variance through several indices: factor loadings, average variance extracted (AVE) and composite reliability. Drawing from the literature (Hair et al. 2010), criteria for considering a measurement valid in the convergent sense were standardised regression weights above the value of 0.5. They were accompanied by a t-value greater than 1.96, AVE greater than 0.5 and a composite reliability index greater than 0.7. Table 3 shows all three measures of convergent validity, along with the Cronbach’s alpha measure discussed in the previous section.

4.1.5. Discriminant Validity

Discriminant validity is “the degree to which two conceptually similar concepts are distinct” (Hair et al. 2010). This idea’s mathematical operationalisation can be achieved by comparing the square root of the AVE with the correlations of a given construct with others. For a pair of constructs, if AVE’s square root is more than their inter-correlation, they are considered different constructs. The values provided in Table 4 can be used to gauge whether that condition is fulfilled for any variable pair. The table’s primary diagonal presents the square roots of AVE, while other non-diagonal elements represent inter-correlations.

In addition to the described analyses, multicollinearity diagnostics was applied to the data. As noted in the literature, a reasonable estimate of multicollinearity is the variance inflation factor (VIF), which should remain lower than 3.3 to establish a conservative inflation limit (Diamantopoulos and Siguaw 2006). Calculation of the VIF for all variables of relevance for the research showed that the results spanned the range between 1.01 and 2.02, far below the suggested upper bound. Based on those findings, we concluded there was no multicollinearity in the data.

4.2. Structural Equation Model

For research, a structural equation model was developed to thoroughly test the hypotheses and understand the relationships between the variables of interest. Moreover, the SEM is known to be applied for both theory testing and analytical applications. This technique combines CFA, path analysis and regression in a theoretical framework to examine the latent variables that simultaneously evaluate the measurement model for the constructs and the structural model (Jöreskog 1993). The overall model achieved an acceptable fit, based on the indices suggested by Hair et al. (2010). The model had a χ2/df of 2.60, while the CFI was 0.91, the NFI was 0.98, and the TLI was 0.90. The RMSEA was 0.08. Together, these indices suggest that the model showed an acceptable fit. The model reported the three endogenous variables’ values as percentages of the variances as follows: trust in the platform 42%, trust in the fundraiser 28% and investor’s intention 44%.

After assessment of the complete model, each of the relationships was evaluated separately. Because each path in the model corresponded to a single hypothesis, the research hypotheses were simultaneously assessed by evaluating the significance of the model path. For a path to be deemed significant, the p-value associated with it would have to be lower than 0.05. The p-value was derived from a t-test of a single path coefficient. Each regression weight was divided by the corresponding standard error of the estimate (SEE) and compared to the critical values of ±1.96. Table 5 shows the results of each hypothesis/path test. For easier comprehension, Figure 2 visually displays the model and the relationships within it.

We started with the direct effect of familiarity on trust in the platform, shown by H1a. The results showed that familiarity significantly influenced trust in the platform (b = 0.29, p < 0. 001). Similarly, familiarity had a significant impact on investor’s intention as shown by H1b (b = −0.107, p = 0.03). The impact of disposition to trust on both trust in the platform (b = 0.08, p = 0.10) and fundraiser trust (b = 0.009, p = 0.85) was not significant; therefore, we considered H2a and H2b to be unsupported by the collected data. We also observed positive support of H3, indicating that the information quality had a direct positive influence on both fundraiser trust (b = 0.162, p = 0.004) and investor’s intention (b = 0.325, p < 0. 001). The effect of education signals on both the trust in the fundraiser (described by H4a; b = 0.067, p = 0.386) and investor’s intention (H4b; b = −0.079, p = 0.284) were not significant, implying that the hypotheses H4a and H4b were not supported.

Additionally, we analysed the effect of interpersonal and institutional trust. In support of H5, there was a significant effect of trust in the fundraiser on the investor’s intention (b = 0.167, p = 0.010). Moreover, we found evidence in support of H6a, in which there was a strong effect of trust in the platform on the trust in the fundraiser (b = 0.411, p < 0.001). After H6a was examined, we found evidence in support of H6b, which was the direct effect of platform trust on the investor’s intention and was somewhat higher than all other paths examined in the model (b = 0.286, p < 0.001). The effect of trust in the platform on investor intention was higher than the impact of fundraiser trust. These findings support the previously published results of McKnight et al. (1998) regarding the fundamental relationship between interpersonal trust and institutional trust. The findings of this study further suggest that such a link also exists in the field of ECF.

On the other hand, although the direct effect of disposition to trust on fundraiser trust was not significant (b = 0.009, p = 0.859), it may affect the platform’s variable trust. This is because the platform trust had a significant effect on fundraiser trust (b = 0.411, p < 0.001), and the fundraiser trust had a significant influence on investor intention (b = 0.167, p = 0.010). To test for this possibility, a mediation analysis was performed to check whether trust in the platform carried the effect of disposition of trust on the trust of the fundraiser. The indirect effect was low but significant (b = 0.035, p = 0.030). This result showed that, although the direct effect of disposition to trust on fundraiser trust was not significant, the indirect effect through platform trust was significant, with the total effect of [0.009 + 0.035 = 0.044]. The influence of the disposition to trust in the investor intention was significant (b = 0.197, p = 0.030); therefore, H2c was supported by the data.

5. Discussion and Implications

In this study, we introduced a trust model to investigate investor’s perceived trust in the intermediary and fundraiser and its effect on the investor’s intention. The study examined how trust transitions from institutional to interpersonal by applying two well-known theories: swift trust (Meyerson et al. 1996) and transfer trust (Stewart 2003). Investors’ trust was analysed from the perspective of both fundraiser and platform. Direct and indirect effect precursors were included for the platform and fundraiser trust. The SEM was employed on data gathered from 216 users of Manafa, one of the largest and best-known Saudi ECF platforms. As illustrated in Table 5, eight of the initial 12 hypotheses were supported. As proposed, we provided evidence that intent to invest was influenced by trust in the platform and trust in the fundraiser; we also supplied additional details regarding the roles of familiarity, disposition, information quality and education signals on the intent to invest.

Mediation effects were examined where deemed necessary. This finding was consistent with previous literature (Gefen 2000; Kim et al. 2008; Liu et al. 2018; McKnight et al. 2002; Moysidou and Hausberg 2019; Pavlou 2003). Interestingly, entrepreneurs’ education signals did not affect platform trust, nor investor intention; this finding is not consistent with the previous literature (Backes-Gellner and Werner 2007; Hsu 2007). A possible explanation for the unsupported result on the educational signal was that the ECF investors were considered unsophisticated. As a result, they might not spend much time investigating entrepreneurs like business angels and venture capital investors.

This study contributes to the crowdfunding literature by focusing on the effect of fundraiser and platform trust on investors’ intention in several ways. First, it contributes to the swift and transfer theories (Meyerson et al. 1996; Stewart 2003) by introducing interpersonal and institutional trust and validating and adopting it in the ECF framework. Second, the study contributes to the behaviour intention literature by showing that trust in both platform and entrepreneurs positively affects investor intention. This study provides valuable insight into the working of trust mechanisms in the crowdfunding domain and sheds light on the interrelationships between the variables of interest.

From a practical point of view, our findings have significant implications for ECF platform practitioners and entrepreneurs. To increase investment intent, entrepreneurs should consider two crucial aspects. First, make sure the platform strictly follows governmental regulations and shows trustworthiness. Second, fundraisers must pay as much attention as possible to the project contents by providing soft (e.g., future plans) and hard (e.g., financial statements) information to enhance the investor’s trust on entrepreneurs and positively affect the investor’s intention. Our results can be utilised to enhance a trust-building model in ECF platforms.

Trust must be considered from a holistic perspective: a trustworthy environment that encompasses all participants and mediators on the supply side. Given that trust affects the potential investors’ ability to overcome uncertainty and information asymmetry, institutional and interpersonal-based trust will, as a result, impacts investors’ intention. Moreover, investor’s trust perception is essential not only for the fundraiser but for the platform itself, by screening honest and competent entrepreneurs. Although the study focused on Manafa platform users with the necessary caution, we believe it can be generalised to similar platforms in developing countries. However, consistent with the study’s primary goal, the results obtained were most useful in the context of Manafa.

6. Conclusions, Limitations and Future Study

This study focused on the effect of investor trust on investor behaviours. Our research improves our knowledge about the role of trust in both fundraisers and platforms in investors’ intention. The study proposed a conceptual framework for assessing the mediating the impact of trust in the platform and the fundraiser concerning investors’ intention. Hence, this research revealed a new position in establishing empirical evidence inside the context of crowdfunding. Although ECF has been growing as a financial resource, we still do not know much about how trust is established in ECF.

To fill the gap in the existing literature, this study contributed to expanding the swift and transfer theories (Meyerson et al. 1996; Stewart 2003) in a context that has not been studied before, ECF. The results indicate that familiarity, the disposition to trust and information quality positively impact investors’ intention; while education signals were found to have no significant effect. Moreover, trust in the platform and the fundraiser, which were the focal points of our study, significantly affected the investor’s intention. Furthermore, trust in the platform significantly affects the investor’s trust in fundraisers. Both fundraiser trust and platform trust were tested as mediation. No mediation effect was found, except for disposition to trust; trust in the platform carries the effect of disposition of trust on the trust of the fundraiser.

This study represents a step forward in understanding the formation of trust in ECF, though it has limitations. First, data were collected from only one ECF platform in Saudi Arabia, exclusive to its citizens. Thus, the findings can only be generalised to ECF platforms in Saudi Arabia and those who share the same culture, such as the Gulf countries. Therefore, future studies can build on our research by applying it to different crowdfunding platforms or in a different culture.

Second, the study examined the intention of potential investors instead of the behaviour of actual investors. We evaluated ECF investors’ intention rather than real investment by dragging data from the ECF crowdfunding platform; the effectiveness of the framework can be tested. This study showed that perceived trust is one of the most crucial elements affecting potential investors in ECF. Prior studies found that investor trust is a critical factor affecting investor intention. An in-depth understanding of the impact of ECF investor intention relating to trust investment is vital.

Previous studies have investigated the impact of trust on the willingness of peer-to-peer lending crowdfunding (Moysidou and Hausberg 2019). Lenders in crowdfunding are looking for a short-term return, while investors in ECF are looking for a long-term investment. Thus, a comparative study could be performed to determine and quantify the trust between these two crowdfunding types. Furthermore, it is not easy to investigate all of the potential variables influencing our model in one study. Additional variables, such as governance, risk and platform quality, may affect behavioural intention along with the trust factors that we have established in our framework.

The sample size was neither too small nor too big to run SEM. Because ECF is still new in Saudi Arabia, future researchers are encouraged to collect larger samples for similar quantitative studies. Finally, qualitative research in this domain is essential, and we recommend that future researchers turn toward such endeavours.

Author Contributions

Authors have contributed equally to the article. All authors have read and agreed to the published version of the manuscript.

Funding

The research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

Mohammed Alharbey appreciates his employer King Abdulaziz University and the Saudi government for funding his Ph.D. studies. He is also grateful to his supervisor for providing continuous guidance. Stefan Van Hemmen acknowledges the financial support from the Spanish Ministerio de Economía, Industria y Competitividad, project number ECO2017-86305-C4-2-R and also from AGAUR (Generalitat de Catalunya), project 2017SGR1036.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abosag, Ibrahim, and Peter Naudé. 2014. Development of Special Forms of B2B Relationships: Examining the Role of Interpersonal Liking in Developing Guanxi and Et-Moone Relationships. Industrial Marketing Management 43: 887–96. [Google Scholar] [CrossRef]

- Ahlers, Gerrit K. C., Douglas Cumming, Christina Günther, and Denis Schweizer. 2015. Signaling in Equity Crowdfunding. Entrepreneurship Theory and Practice 39: 955–80. [Google Scholar] [CrossRef]

- Alegre, Inés, and Melina Moleskis. 2016. Crowdfunding: A Review and Research Agenda. Available online: https://ssrn.com/abstract=2900921 (accessed on 7 October 2016).

- Backes-Gellner, Uschi, and Arndt Werner. 2007. Entrepreneurial Signaling via Education: A Success Factor in Innovative Start-Ups. Small Business Economics 29: 173–90. [Google Scholar] [CrossRef]

- Bansal, Gaurav, Fatemeh Mariam Zahedi, and David Gefen. 2016. Do Context and Personality Matter? Trust and Privacy Concerns in Disclosing Private Information Online. Information & Management 53: 1–21. [Google Scholar]

- Barbi, Massimiliano, and Sara Mattioli. 2019. Human Capital, Investor Trust, and Equity Crowdfunding. Research in International Business and Finance 49: 1–12. [Google Scholar] [CrossRef]

- Bélanger, France, and Lemuria Carter. 2008. Trust and Risk in E-Government Adoption. The Journal of Strategic Information Systems 17: 165–76. [Google Scholar] [CrossRef] [Green Version]

- Bell, Emma, and Alan Bryman. 2007. The Ethics of Management Research: An Exploratory Content Analysis. British Journal of Management 18: 63–77. [Google Scholar] [CrossRef]

- Belleflamme, Paul, Thomas Lambert, and Armin Schwienbacher. 2014. Crowdfunding: Tapping the Right Crowd. Journal of Business Venturing 29: 585–609. [Google Scholar] [CrossRef] [Green Version]

- Bi, Sheng, Zhiying Liu, and Khalid Usman. 2017. The Influence of Online Information on Investing Decisions of Reward-Based Crowdfunding. Journal of Business Research 71: 10–18. [Google Scholar] [CrossRef]

- Bottazzi, Laura, Marco Da Rin, and Thomas Hellmann. 2016. The Importance of Trust for Investment: Evidence from Venture Capital. The Review of Financial Studies 29: 2283–318. [Google Scholar] [CrossRef] [Green Version]

- Bouncken, Ricarda B., Malvine Komorek, and Sascha Kraus. 2015. Crowdfunding: The Current State of Research. International Business & Economics Research Journal (IBER) 14: 407–16. [Google Scholar]

- Brown, Houghton G., Marshall Scott Poole, and Thomas L. Rodgers. 2004. Interpersonal Traits, Complementarity, and Trust in Virtual Collaboration. Journal of Management Information Systems 20: 115–38. [Google Scholar] [CrossRef]

- Cabrera, Elizabeth F., and Angel Cabrera. 2005. Fostering Knowledge Sharing through People Management Practices. The International Journal of Human Resource Management 16: 720–35. [Google Scholar] [CrossRef] [Green Version]

- Chen, Dongyu, Fujun Lai, and Zhangxi Lin. 2014. A Trust Model for Online Peer-to-Peer Lending: A Lender’s Perspective. Information Technology and Management 15: 239–54. [Google Scholar] [CrossRef]

- Chen, Yuangao, Ruyi Dai, Jianrong Yao, and Yixiao Li. 2019. Donate Time or Money? The Determinants of Donation Intention in Online Crowdfunding. Sustainability 11: 4269. [Google Scholar] [CrossRef] [Green Version]

- Connelly, Brian L., T. Russell Crook, James G. Combs, David J. Ketchen Jr., and Herman Aguinis. 2018. Competence-and Integrity-Based Trust in Interorganizational Relationships: Which Matters More? Journal of Management 44: 919–45. [Google Scholar] [CrossRef] [Green Version]

- Cooper, Arnold C., F. Javier Gimeno-Gascon, and Carolyn Y. Woo. 1994. Initial Human and Financial Capital as Predictors of New Venture Performance. Journal of Business Venturing 9: 371–95. [Google Scholar] [CrossRef]

- Crowdfunding—Saudi Arabia|Statista Market Forecast. n.d. Statista. Available online: https://0-www-statista-com.brum.beds.ac.uk/outlook/335/110/crowdfunding/saudi-arabia (accessed on 21 September 2020).

- Cumming, Douglas J., Lars Hornuf, Moein Karami, and Denis Schweizer. 2020. Disentangling Crowdfunding from Fraudfunding. Max Planck Institute for Innovation & Competition Research Paper No. 16-09. Available online: https://ssrn.com/abstract=2828919 (accessed on 4 January 2020).

- Diamantopoulos, Adamantios, and Judy A. Siguaw. 2006. Formative versus Reflective Indicators in Organizational Measure Development: A Comparison and Empirical Illustration. British Journal of Management 17: 263–82. [Google Scholar] [CrossRef]

- Dodds, William B., Kent B. Monroe, and Dhruv Grewal. 1991. Effects of Price, Brand, and Store Information on Buyers’ Product Evaluations. Journal of Marketing Research 28: 307–19. [Google Scholar]

- Erikson, Erik H. 1968. Identity: Youth and Crisis. New York: WW Norton & Company. [Google Scholar]

- Fukuyama, Francis. 1995. Trust: The Social Virtues and the Creation of Prosperity. New York: Free Press, vol. 99. [Google Scholar]

- Gazzaz, Heba. 2019. Crowdfunding in Saudi Arabia: A Case Study of the Manafa Platform. International Journal of Economics and Finance 11: 1–72. [Google Scholar] [CrossRef]

- Gefen, David. 2000. E-Commerce: The Role of Familiarity and Trust. Omega 28: 725–37. [Google Scholar] [CrossRef] [Green Version]

- Gefen, David, Elena Karahanna, and Detmar W. Straub. 2003. Trust and TAM in Online Shopping: An Integrated Model. MIS Quarterly 27: 51–90. [Google Scholar] [CrossRef]

- Grabner-Kräuter, Sonja, and Ewald A. Kaluscha. 2003. Empirical Research in On-Line Trust: A Review and Critical Assessment. International Journal of Human-Computer Studies 58: 783–812. [Google Scholar] [CrossRef]

- Grossman, Michael. 2006. Education and Nonmarket Outcomes. In Handbook of the Economics of Education. Amsterdam: Elsevier, vol. 1, pp. 577–633. [Google Scholar]

- Hair, Joseph F., Rolph E. Anderson, Barry J. Babin, and Wiiliam C. Black. 2010. Multivariate Data Analysis: A Global Perspective. Upper Saddle River: Pearson, vol. 7. [Google Scholar]

- Harman, Harry H. 1976. Modern Factor Analysis. Chicago: University of Chicago Press. [Google Scholar]

- Hazleton, Vincent, and William Kennan. 2000. Social Capital: Reconceptualizing the Bottom Line. Corporate Communications: An International Journal 5: 81–87. [Google Scholar] [CrossRef]

- He, Wu, Guandong Xu, Haichao Zheng, Jui-Long Hung, Zihao Qi, and Bo Xu. 2016. The Role of Trust Management in Reward-Based Crowdfunding. Online Information Review 40: 97–118. [Google Scholar]

- Hollas, Judd. 2013. Is Crowdfunding Now a Threat to Traditional Finance? Corporate Finance Review 18: 27. [Google Scholar]

- Hsu, David H. 2007. Experienced Entrepreneurial Founders, Organizational Capital, and Venture Capital Funding. Research Policy 36: 722–41. [Google Scholar] [CrossRef]

- Jarvenpaa, Sirkka L., Kathleen Knoll, and Dorothy E. Leidner. 1998. Is Anybody out There? Antecedents of Trust in Global Virtual Teams. Journal of Management Information Systems 14: 29–64. [Google Scholar] [CrossRef]

- Jöreskog, Karl G. 1993. Testing Structural Equation Models. Sage Focus Editions 154: 294–94. [Google Scholar]

- Kang, Minghui, Yiwen Gao, Tao Wang, and Haichao Zheng. 2016. Understanding the Determinants of Funders’ Investment Intentions on Crowdfunding Platforms. Industrial Management & Data Systems 116: 1800–19. [Google Scholar] [CrossRef]

- Kenning, Peter. 2008. The Influence of General Trust and Specific Trust on Buying Behaviour. International Journal of Retail & Distribution Management 36: 461–76. [Google Scholar] [CrossRef]

- Kim, Dan J., Donald L. Ferrin, and H. Raghav Rao. 2008. A Trust-Based Consumer Decision-Making Model in Electronic Commerce: The Role of Trust, Perceived Risk, and Their Antecedents. Decision Support Systems 44: 544–64. [Google Scholar] [CrossRef]

- Kline, Paul. 2014. An Easy Guide to Factor Analysis. Abingdon-on-Thames: Routledge. [Google Scholar]

- Komiak, Sherrie Y. X., and Izak Benbasat. 2006. The Effects of Personalization and Familiarity on Trust and Adoption of Recommendation Agents. MIS Quarterly 30: 941–60. [Google Scholar] [CrossRef]

- Kshetri, Nir. 2018. Informal Institutions and Internet-Based Equity Crowdfunding. Journal of International Management 24: 33–51. [Google Scholar] [CrossRef] [Green Version]

- Lee, Jung, Jae-Nam Lee, and Bernard CY Tan. 2010. Emotional Trust and Cognitive Distrust: From A Cognitive-Affective Personality System Theory Perspective. Paper presented at the PACIS 2010, Taipei, Taiwan, July 9–12; p. 114. [Google Scholar]

- Lewis, J. David, and Andrew Weigert. 1985. Trust as a Social Reality. Social Forces 63: 967–85. [Google Scholar] [CrossRef]

- Lin, Mingfeng, Nagpurnanand R. Prabhala, and Siva Viswanathan. 2013. Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-to-Peer Lending. Management Science 59: 17–35. [Google Scholar] [CrossRef]

- Liu, De, Daniel Brass, Yong Lu, and Dongyu Chen. 2015. Friendships in Online Peer-to-Peer Lending: Pipes, Prisms, and Relational Herding. Mis Quarterly 39: 729–42. [Google Scholar] [CrossRef]

- Liu, Lili, Ayoung Suh, and Christian Wagner. 2018. Empathy or perceived credibility? An empirical studyon individual donation behavior in charitable crowdfunding. Internet Research 28: 623–65. [Google Scholar] [CrossRef]

- Luhmann, Niklas. 2018. Trust and Power. Hoboken: John Wiley & Sons. [Google Scholar]

- Massolution, C. L. 2015. Crowdfunding Industry Report. Available online: http://Reports.Crowdsourcing.Org/Index.Php (accessed on 20 January 2020).

- McKnight, D. Harrison, and Norman L. Chervany. 2001. What Trust Means in E-Commerce Customer Relationships: An Interdisciplinary Conceptual Typology. International Journal of Electronic Commerce 6: 35–59. [Google Scholar] [CrossRef]

- McKnight, D. Harrison, Vivek Choudhury, and Charles Kacmar. 2002. Developing and Validating Trust Measures for E-Commerce: An Integrative Typology. Information Systems Research 13: 334–59. [Google Scholar] [CrossRef] [Green Version]

- McKnight, D. Harrison, Larry L. Cummings, and Norman L. Chervany. 1998. Initial Trust Formation in New Organizational Relationships. Academy of Management Review 23: 473–90. [Google Scholar] [CrossRef] [Green Version]

- Meyerson, Debra, Karl E. Weick, and Roderick M. Kramer. 1996. Swift Trust and Temporary Groups. Trust in Organizations: Frontiers of Theory and Research 166: 195. [Google Scholar]

- Mochkabadi, Kazem, and Christine K. Volkmann. 2020. Equity Crowdfunding: A Systematic Review of the Literature. Small Business Economics 54: 75–118. [Google Scholar] [CrossRef]

- Moritz, Alexandra, and Joern H. Block. 2016. Crowdfunding: A Literature Review and Research Directions. In Crowdfunding in Europe. Berlin/Heidelberg: Springer, pp. 25–53. [Google Scholar]

- Moritz, Alexandra, Joern Block, and Eva Lutz. 2015. Investor Communication in Equity-Based Crowdfunding: A Qualitative-Empirical Study. Qualitative Research in Financial Markets 7: 309–42. [Google Scholar] [CrossRef] [Green Version]

- Moysidou, Krystallia, and J. Piet Hausberg. 2019. In Crowdfunding We Trust: A Trust-Building Model in Lending Crowdfunding. Journal of Small Business Management 58: 511–43. [Google Scholar] [CrossRef]

- Nahapiet, Janine, and Sumantra Ghoshal. 1998. Social Capital, Intellectual Capital, and the Organizational Advantage. Academy of Management Review 23: 242–66. [Google Scholar] [CrossRef]

- Parks, Malcolm R., and Kory Floyd. 1996. Making Friends in Cyberspace. Journal of Computer-Mediated Communication 1: JCMC144. [Google Scholar]

- Paschen, Jeannette. 2017. Choose Wisely: Crowdfunding through the Stages of the Startup Life Cycle. Business Horizons 60: 179–88. [Google Scholar] [CrossRef]

- Pavlou, Paul A. 2003. Consumer Acceptance of Electronic Commerce: Integrating Trust and Risk with the Technology Acceptance Model. International Journal of Electronic Commerce 7: 101–34. [Google Scholar]

- Pavlou, Paul A., and David Gefen. 2004. Building Effective Online Marketplaces with Institution-Based Trust. Information Systems Research 15: 37–59. [Google Scholar] [CrossRef] [Green Version]

- Podsakoff, Philip M., Scott B. MacKenzie, Jeong-Yeon Lee, and Nathan P. Podsakoff. 2003. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. Journal of Applied Psychology 88: 879. [Google Scholar] [CrossRef] [PubMed]

- Resources—Fintech Saudi. n.d. Available online: https://fintechsaudi.com/resources/ (accessed on 21 September 2020).

- Robert, Lionel P., Alan R. Denis, and Yu-Ting Caisy Hung. 2009. Individual Swift Trust and Knowledge-Based Trust in Face-to-Face and Virtual Team Members. Journal of Management Information Systems 26: 241–79. [Google Scholar] [CrossRef]

- Rotter, Julian B. 1967. A New Scale for the Measurement of Interpersonal Trust 1. Journal of Personality 35: 651–65. [Google Scholar] [CrossRef] [PubMed]

- Rotter, Julian B. 1980. Interpersonal Trust, Trustworthiness, and Gullibility. American Psychologist 35: 1. [Google Scholar] [CrossRef]

- Spence, Michael. 1978. Job Market Signaling. In Uncertainty in Economics. Amsterdam: Elsevier, pp. 281–306. [Google Scholar]

- Spicer, John. 2005. Making Sense of Multivariate Data Analysis: An Intuitive Approach. Thousand Oaks, London and New Delhi: Sage. [Google Scholar]

- Stewart, Katherine J. 2003. Trust Transfer on the World Wide Web. Organization Science 14: 5–17. [Google Scholar] [CrossRef]

- Strohmaier, David, Jianqiu Zeng, and Muhammad Hafeez. 2019. Trust, Distrust, and Crowdfunding: A Study on Perceptions of Institutional Mechanisms. Telematics and Informatics 43: 101252. [Google Scholar] [CrossRef]

- Sun, Heshan. 2010. Sellers’ Trust and Continued Use of Online Marketplaces. Journal of the Association for Information Systems 11: 2. [Google Scholar] [CrossRef]

- Teo, Thompson S. H., and Jing Liu. 2007. Consumer Trust in E-Commerce in the United States, Singapore and China. Omega 35: 22–38. [Google Scholar] [CrossRef]

- Tomczak, Alan, and Alexander Brem. 2013. A Conceptualized Investment Model of Crowdfunding. Venture Capital 15: 335–59. [Google Scholar] [CrossRef]

- Ullah, Saif, and Yulin Zhou. 2020. Gender, Anonymity and Team: What Determines Crowdfunding Success on Kickstarter. Journal of Risk and Financial Management 13: 80. [Google Scholar] [CrossRef]

- Uslaner, Eric M. 2008. Where You Stand Depends upon Where Your Grandparents Sat: The Inheritability of Generalized Trust. Public Opinion Quarterly 72: 725–40. [Google Scholar] [CrossRef] [Green Version]

- Van der Have, Robert P., and Luis Rubalcaba. 2016. Social Innovation Research: An Emerging Area of Innovation Studies? Research Policy 45: 1923–35. [Google Scholar] [CrossRef]

- Walthoff-Borm, Xavier, Armin Schwienbacher, and Tom Vanacker. 2018. Equity Crowdfunding: First Resort or Last Resort? Journal of Business Venturing 33: 513–33. [Google Scholar] [CrossRef]

- Wang, Nan, Xiao-Liang Shen, and Yongqiang Sun. 2013. Transition of Electronic Word-of-Mouth Services from Web to Mobile Context: A Trust Transfer Perspective. Decision Support Systems 54: 1394–403. [Google Scholar] [CrossRef]

- Wang, Wei-Tsong, Yi-Shun Wang, and En-Ru Liu. 2016. The Stickiness Intention of Group-Buying Websites: The Integration of the Commitment–Trust Theory and e-Commerce Success Model. Information & Management 53: 625–42. [Google Scholar]

- Wiersema, Margarethe F., and Karen A. Bantel. 1992. Top Management Team Demography and Corporate Strategic Change. Academy of Management Journal 35: 91–121. [Google Scholar]

- Xu, Jingjun, Izak Benbasat, and Ronald T. Cenfetelli. 2013. Integrating Service Quality with System and Information Quality: An Empirical Test in the e-Service Context. MIS Quarterly 37: 777–94. [Google Scholar] [CrossRef]

- Zheng, Haichao, Dahui Li, Jing Wu, and Yun Xu. 2014. The Role of Multidimensional Social Capital in Crowdfunding: A Comparative Study in China and US. Information & Management 51: 488–96. [Google Scholar]

| 1 | Reward-based, seed, or pre-ordering crowdfunding is when the crowd fund’s entrepreneurs or artists give products or services in return for funding, such as membership in a fan rewards club or a ticket for an event (Moritz and Block 2016). Nevertheless, social capital has a significant impact on the success of reward-based crowdfunding campaigns. |

| 2 | The peer-to-peer or lending crowdfunding platform works like a bank by giving loans to borrowers, but at interest rates lower than banks. The platform links lenders or investors with borrowers. Some platforms link the lenders directly to individual borrowers, while other platforms connect the individual to small businesses indirectly by collecting the funds from individuals on the businesses’ behalf (Massolution 2015). |

| 3 | Donation crowdfunding is the donation of funds to non-profit projects. The funders of donation crowdfunding donate through the platform for no tangible return (Moritz and Block 2016). |

Figure 1.

Proposed model.

Figure 2.

Visual representation of the tested SEM model. Note: n.s., not significant. p < 0.05 *; p < 0.01 **; p < 0.001 ***.

Figure 2.

Visual representation of the tested SEM model. Note: n.s., not significant. p < 0.05 *; p < 0.01 **; p < 0.001 ***.

{kind=link}

{kind=link}

Table 1.

Demographics of the collected sample (N = 216).

| Variable | Frequency | Percent [%] |

|---|---|---|

| Age | ||

| 18 to 24 | 3 | 1.4% |

| 25 to 34 | 84 | 38.9% |

| 35 to 44 | 104 | 48.1% |

| 45 to 54 | 19 | 8.8% |

| 55 and older | 6 | 2.8% |

| Gender | ||

| Male | 171 | 79.2% |

| Female | 45 | 20.8% |

| Occupation | ||

| Student | 40 | 18.5% |

| Employed | 148 | 68.5% |

| Retired | 15 | 6.9% |

| Unemployment | 10 | 4.6% |

| Other | 3 | 1.4% |

| Education | ||

| High school or equivalent | 26 | 12% |

| Bachelor’s degree | 102 | 47.2% |

| Master’s degree | 83 | 38.4% |

| Doctoral degree | 5 | 2.3% |

| Marital status | ||

| Married | 134 | 62% |

| Single | 75 | 34.7% |

| Widowed | 0 | 0% |

| Divorced | 7 | 3.2% |

Table 2.

Survey items, database codes and reference source.

| Code | Item | Source |

|---|---|---|

| FAM1 | I am generally familiar with crowdfunding. | |

| FAM2 | I am familiar with conducting online investments in crowdfunding projects. | (Gefen 2000) |

| FAM3 | The process of supporting crowdfunding projects is known to me. | |

| DIS1 | In general, I trust other people. | |

| DIS2 | I tend to count on other people. | (Gefen 2000) |

| DIS3 | In general, I trust other people unless they give me a reason not to trust them. | |

| PROJQ1 | I am satisfied with the information on this project page. | |

| PROJQ2 | Overall, I would give the content quality of the project a high mark. | (Kim et al. 2008; Xu et al. 2013) |

| PROJQ3 | Overall, I would give a high rating in terms of the content quality for the crowdfunding project. | |

| EDU1 | A fundraiser’s education is important to me. | Now developed |

| EDU2 | A fundraiser’s heavy investment in education gives me a signal that the project will succeed in equity crowdfunding. | |

| EDU3 | A fundraiser who has spent heavily on higher education is important to me. | |

| PTRUST1 | I believe that the platform is trustworthy. | |

| PTRUST2 | I believe (the platform) keeps its promises. | (McKnight et al. 2002) |

| PTRUST3 | (The platform) can be trusted at all times. | |

| FTRUST1 | I am convinced that the project creator(s) will fulfil his/her/their obligations. | |

| FTRUST2 | I would call the project creator(s) honest. | (McKnight et al. 2002) |

| FTRUST3 | I believe that the project creator(s) has the competence and efficiency to successfully achieve the goals and keep all promises made to me. | |

| IN1 | The probability that I would fund the crowdfunding project is high. | |

| IN2 | My willingness to invest in the crowdfunding project is high. | (Dodds et al. 1991) |

| IN3 | I intend to contribute financially to crowdfunding campaigns. |

Note: FAM = Familiarity, DIS = Disposition to trust, PROJQ = Project quality, EDU = Education signals, PTRUST = Platform trust, FTRUST = Fundraise trust and IN = Intention.

Table 3.

Convergent validity indices and reliability measures.

| Items | Factor Loading | Composite Reliability | AVE | α |

|---|---|---|---|---|

| Familiarity | 0.893 | 0.736 | 0.888 | |

| FAM1 | 0.870 | |||

| FAM2 | 0.929 | |||

| FAM3 | 0.767 | |||

| Disposition to trust | 0.822 | 0.608 | 0.822 | |

| DIS1 | 0.789 | |||

| DIS2 | 0.854 | |||

| DIS3 | 0.688 | |||

| Education | 0.767 | 0.525 | 0.765 | |

| EDU1 | 0.765 | |||

| EDU2 | 0.759 | |||

| EDU3 | 0.643 | |||

| Project quality | 0.823 | 0.607 | 0.820 | |

| PROJQ1 | 0.751 | |||

| PROJQ2 | 0.796 | |||

| PROJQ3 | 0.790 | |||

| Platform trust | 0.764 | 0.522 | 0.757 | |

| PTRUST2 | 0.666 | |||

| PTRUST3 | 0.828 | |||

| PTRUST4 | 0.660 | |||

| Fundraise trust | 0.772 | 0.540 | 0.713 | |

| FTRUST1 | 0.906 | |||

| FTRUST2 | 0.552 | |||

| FTRUST3 | 0.703 | |||

| Intention | 0.747 | 0.497 | 0.746 | |

| IN1 | 00.769 | |||

| IN2 | 0.657 | |||

| IN3 | 0.685 |

Table 4.

Comparison of the square root of AVE to correlations for each variable pair.

| Variable | [1] | [2] | [3] | [4] | [5] | [6] | [7] |

|---|---|---|---|---|---|---|---|

| Project quality [1] | 0.779 | ||||||

| Platform trust [2] | 0.501 | 0.722 | |||||

| Familiarity [3] | 0.252 | 0.363 | 0.858 | ||||

| Fundraiser trust [4] | 0.374 | 0.438 | 0.087 | 0.735 | |||

| Disposition to trust [5] | 0.015 | 0.089 | 0.006 | 0.045 | 0.780 | ||

| Intention [6] | 0.469 | 0.462 | 0.302 | 0.358 | −0.059 | 0.705 | |

| Education [7] | 0.251 | 0.078 | −0.042 | 0.122 | −0.052 | 0.066 | 0.725 |

Notes. Bold values indicate the square root values of AVE.

Table 5.