Mergers and Acquisitions Risk Modeling

1

Kursk Branch, Financial University under the Government of the Russian Federation, 305016 Kursk, Russia

2

General Economic Theory and History of Economic Thought Department, St. Petersburg State University of Economics, 191023 St. Petersburg, Russia

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(9), 451; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14090451

Submission received: 4 August 2021

/

Revised: 12 September 2021

/

Accepted: 16 September 2021

/

Published: 21 September 2021

(This article belongs to the Special Issue Risk Management in Economics and Finance in the Age of Digital Ecosystems Development)

Abstract

:In the context of the dynamics of the modern external environment, the importance of risk management in general and the risks inherent in the processes of mergers and acquisitions has sharply increased. This is becoming one of the primary challenges in business, the solution of which will contribute to economic growth and development. In this article, based on a broad review of literature, the key risks of mergers and acquisitions are identified and classified, the level of their significance is assessed, the relevant management tools are selected for each risk and a computer program is developed that implements the selection of tools for each specific merger and acquisition transaction. A comprehensive automated methodology for the selection of risk management tools in the implementation of mergers and acquisitions can become an effective risk management tool for companies participating in such transactions. This will allow to identify and track risks in a timely manner, assess their significance, and, among other things, contribute to the adoption of effective management decisions regarding risk management.

1. Introduction

Over time, the economic system becomes more complex. There are more of its elements and their interrelationships become more complex. Increasing complexity makes the economic system more vulnerable to risks. As a result, effective risk management becomes one of the key factors for the success of economic activity. A qualitative review on the scientific risk management literature is provided by Aven (2016). This paper provides an overview of advances in risk management, with a special focus on the fundamental ideas and thinking on which risk management is based.

Various approaches to assessing and analyzing risks, as well as methods for mitigating risks, would be considered by Aven and Nøkland (2010); Fertis et al. (2012); Folch-Calvo et al. (2020); Haugen and Vinnem (2015); Huang et al. (2016); Le Coze et al. (2014); Masys (2012); Nobanee et al. (2021); Rodrigues et al. (2014). Dependency is at work: the more complex the economic process is organized, the more sensitive it is to risk. The nature of this dependence can be described by analogy with Ashby (1956) Law of Requisite Variety. The more complex the economic system (process) is organized, the more diverse the risks affecting it become. Consequently, as the economy evolves, the importance of risk management grows. Over time, risk management can be expected to become a key form of management.

The growing diversity of economic processes leads to an increase in the number of their differences. Effective risk management systems must consider the specifics of the risks. Therefore, they are becoming more and more specialized. Risk management inherent in mergers and acquisitions is of particular interest. Successful completion of this challenge will contribute to economic growth and development. The presence of many risks associated with mergers and acquisitions does not allow making prompt management decisions in the field of implementation of integration interactions in business (Chen et al. 2020). Therefore, it becomes necessary to identify these risks, classify them, and, in the future, neutralize them.

This article aims to develop a model that will support the M&A risk management process. Mergers and acquisitions play an important role in the modern economy. The specificity of their implementation in various industries, institutional conditions and at different phases of the economic cycle has been studied in detail in the literature (Avinadav et al. 2017; Barros and Domínguez 2013; Bruyland et al. 2019; Fischer et al. 2021; Gagnon and Volesky 2017; González-Torres et al. 2020; Hečková et al. 2019; Lewis and Bozos 2019; Loukianova et al. 2017; Rani et al. 2020). However, there are significant practical difficulties in carrying out M&A transactions.

The relevance and significance of the implementation of the development described in the article is due to insufficient scientific and methodological support for the implementation of mergers and acquisitions (Ott 2020). This makes it difficult in practice to implement effective restructuring of the economy and gives rise to systemic problems associated with insufficient competitiveness of business. Managers working in the M&A market cite the speed of making managerial decisions and the unified approach to solving managerial problems as important factors in their activities (Barua and Ioanid 2020). These circumstances determine the relevance of automation of the risk management methodology for mergers and acquisitions. The first step on this path is to formalize this technique.

Currently, the market situation, according to AK&M (2020) estimates, is significantly influenced by the COVID-19 pandemic. The pandemic has led to increased uncertainty (Sharma et al. 2020). The spread of the coronavirus and measures to combat it (social distancing, border closures, stoppages of production, curfews, etc.) are the reason for the increased risk of mergers and acquisitions. Many companies are abandoning previously planned acquisitions, directing their resources to support existing assets. M&A activity has declined. This requires a clearer study of all M&A procedures—in particular, an attentive attitude to risks.

Many studies are devoted to the issues of risk management in the implementation of mergers and acquisitions, but no comprehensive M&A risk management model has been proposed. The task is to consider the most complete list of risks inherent in M&A transactions. The risk management process is multi-stage and is a set of sequential stages. There are many different opinions of researchers about the number and content of these stages. The most complete classification of M&A stages is given by Keshk et al. (2018): «Risk management is one of the most important management, especially in this time, which has many unexpected events. This management means with classification, analyzing, planning, identification, assessment, and response and avoidance strategies of risks».

Boronenko (2017) proposes to consider as stages of risk management: information analysis (monitoring the external and internal environment of the company, identifying possible risks and adjusting known factors), diagnosing the current situation (specifics of the task, identifying and taking into account the reasons that cause a change in risk, their ranking and assessment losses in the event of a change in the situation), development of alternative solutions (for each option, setting the boundaries of a possible negative manifestation of all types of risks), decision-making (comprehensive justification of the decision and acceptance of an acceptable risk), organization and implementation (implementation of a risk solution, operational measures to eliminate new aspects of risk manifestation).

Delakhov and Karataev (2017) highlight such stages of risk management as: planning, risk analysis, identifying problem areas, choosing a solution from possible options, implementing measures to combat risk. Guzhin and Yezhkova (2017) examine the risk planning stage in detail, dividing it into three sub-stages: identifying project risks, assessing the degree of risk hazard, developing a response.

Among all the stages of risk management, Legeida (2018) notes the importance of the stage of risk classification. To predict risk as accurately as possible and take effective measures to reduce the strength of its influence, it is necessary to correctly classify risks according to their functional orientation, since each type of risk has its own management technique. Kiseleva (2017) identifies the types of risks and notes that within the framework of the risk management process for each risk, it is necessary to determine the likelihood of its occurrence and assess the impact of the risk using special methods of assessing and minimizing risks.

Kurmakaeva (2019) proposes a classification system for the stages of risk management, highlighting the stages of identifying risk and assessing the likelihood of its implementation, as well as the scale of the consequences of determining the maximum possible loss, choosing methods and tools for managing the identified risk, developing a risk strategy, implementing a risk strategy, evaluating the results achieved and adjusting the risk strategy.

Kuzmina (2018) notes that there is no single mechanism for implementing an M&A transaction. Therefore, this author formulates and substantiates his own universal transaction algorithm, highlighting seven main stages of its implementation:

- Strategy development. At this stage, the company’s management decides to conduct an M&A transaction;

- Determination of the criteria for the target company. Such criteria can be the possibility of entering a new market, expanding the range of products manufactured, sales volume, the level of profitability, and others;

- Choosing a target company. The search can be carried out in-house or through intermediaries;

- Due diligence and evaluation of the transaction object. This stage involves researching the financial, operational, legal, strategic and cultural aspects of the company’s activities. Based on the analysis, a decision is made on the feasibility of concluding a deal. Additionally, at this stage, the planning and assessment of transaction costs is carried out and the question of financing the transaction is raised;

- The negotiation process. At this stage, agreements are reached on key issues and permission is obtained from the antimonopoly service;

- Legal registration of the transaction;

- Integration of companies. At this stage, a new structure of the merged company is formed, the company’s personnel are determined, the need to attract new employees is assessed, a decision-making scheme is developed and corporate cultures and production processes are integrated.

Each stage of a M&A transaction carries certain risks:

- At the stage of determining the company’s development strategy and choosing an M&A transaction as a tool for implementing the strategy, the most common risk is strategic risk. Ramieva et al. (2016) understands strategic risk as the risk of the wrong choice of the company’s development strategy. Anisimovets (2016), at the stage of deciding to conduct a transaction, highlights the risk of incorrect strategy formation;

- The stage of analyzing the company’s external environment and analyzing candidates for an M&A transaction, in particular, the choice of the target company as the most significant risks is accompanied by the risks of the wrong choice of the target company and the risks of company incompatibility. For example, Warter and Warter (2017) highlights the risk of significant cultural differences between companies;

- At the stage of a comprehensive analysis, the target company most often identifies the risk of a poor-quality study of the business characteristics of the target company;

- At the stage of predicting the results of an M&A transaction, the most significant is the risk of overestimating the potential benefits from the transaction (entrepreneurial risk);

- At the stage of developing the structure of an M&A transaction, the key risks are financing risks and lack of agreement on the parameters of the transaction between companies. Sui and Dumitrescu-Peculea (2016) understand financing risks as the risks associated with various types of financing a transaction, including the risk of insufficient funds to service debt when using debt financing;

- Determining the price of an M&A transaction comes with financial risks. Sui and Dumitrescu-Peculea (2016) focuses on the risks of mispricing. Svetlova and Thielmann (2020) consider financial risks broadly. «Financial risks relate to financial intermediation, execution of payments, financial protection, supply of financial products, and smooth functioning of money. Perception and management of these risks can be distorted by behavioral biases, institutional risk cultures, and interconnectedness within global financial networks. Modern financial technologies such as FinTech, RegTech, blockchain, and digital currencies pose new challenges for risk management»;

- When an M&A transaction is concluded and the documents are legalized, the political risk of opposition from the authorities to the transaction is most likely to materialize. Also important are the risk of conflicts between shareholders of the companies, the risk of losing key employees of the target company who do not agree with the deal.

Duan et al. (2019) separate the M&A risk assessment process to three steps, that is: before M&A, in M&A and after M&A. They assign the greatest importance to the stage of carrying out integration procedures. At this stage, all risks are divided into six types:

- Systemic risk;

- Law risk;

- Financial risk;

- Intermediary risk;

- Integrated risk;

- Information risk.

Evaluation of the effectiveness of the M&A transaction after the integration procedures is accompanied by a large number of risks. Chang and Cho (2017) conduct extensive post-trade risk analysis. They conclude that «post-merger risks tend to persist for firms seeking M&A transactions with a customer-side motive, whereas this does not occur with a production-side motive. While greater post-merger risks are associated with M&As with a customer-side motive, our results suggest that its association with post-merger risks is moderated by industry dynamism. Overall, our study sheds new light on the post-merger risk by addressing its dynamic nature». It also emphasizes the particular importance of risks at the post-integration stage (Li et al. 2021).

The variety of risks implies the need to rank them on a relevant basis. Analysis of the literature showed that studies devoted to the problem of assessing the significance of M&A risks are divided into two areas:

- Studies using expert assessments without statistical confirmation, where the significance of risk is described qualitatively;

- Research using a statistical approach to assessing the importance of risk (for example, a survey among top managers with statistical data).

The first direction is more common. For example, Skitsko proposes to use a rating scale from 1 to 5 points to assess the importance of risk, where points are responsible for the level of significance of risk: 1 point—very low, 2 points—low, 3 points—medium, 4 points—high, 5 points—very high. Each risk is assigned a score based on statistical data or on the basis of expert assessments. In the absence of a qualitative or quantitative assessment, the risk is assigned an average level of significance (3 points). Next, a list of risks of M&A transactions is formed with the corresponding scores of the significance level. The results for each risk are summarized and an overall assessment of the significance of the risk is derived. Higher scores for a particular M&A risk mean that it is more important (Skitsko and Huzenko 2017).

The advantage of this technique is its versatility. Any risk can be assessed using a universal rating scale. However, the Skitsko method has a significant drawback: it evaluates the significance of risks depending on the subjective opinion of experts. The objectivity of the method can be increased by modifying the risk rating. In the overall rating, only those risks that are often mentioned and are equally assessed by many experts remain in the same places. If the risk is not used in other studies, then it is specific to some specific industries, areas, companies or countries. Therefore, he cannot stand in a high place in the universal rating. The overall rating allows you to highlight those risks that are common. These risks can be found in all M&A transactions.

In practice, a wide range of methods are used. For example, qualitative methods such as filling out questionnaires, SWOT analysis, Delphi method, rose and the spiral of risks are more objective than the opinions of individual experts. Further, such quantitative methods, such as the method for calculating the average risk value, interval analysis, scenario analysis, simulation modeling (Monte Carlo method), stress testing are based on mathematical statistics and assess the significance of risks much more accurately, but they require a significant investment of time and other resources.

One simple method to quantify risks is to calculate the average risk by using the minimum, maximum, and expected impacts on the cost or timing of a project. The impact on the timing has a monetary value (additional interest costs, lost revenue due to delays in production, costs for staff that were not downsized in a timely manner, etc.). The team involved in developing the M&A strategy can calculate the cost increases resulting from the delay per unit of time and determine the cost impact of the risks on the project timeline. The final step is to conduct a sensitivity analysis when the key parameters of the M&A deal change.

The Monte Carlo method allows you to determine the overall impact on the project of cost and time risks. The analysis by this method consists of assessing the quantitative value of the probability, the degree of risk impact on the cost and timing, choosing the type of distribution in accordance with the nature of the analyzed risk, and simulating the impact of the overall risk on the cost and timing of the project. The result is the calculation of the total cost of the risks accepted, transferred and divided between the parties to the transaction.

The second line of research on the significance of M&A risks includes such authors as Ott (2020). It identifies its own system for quantitatively assessing the significance of the risks of mergers and acquisitions and distributes risks depending on their level of significance. Another quantitative risk assessment method is proposed by Liu et al. (2019). They proposed a new method to evaluate risks of mergers and acquisitions. The process of their method is to determine the positive and negative ideal solutions of interval-valued intuitional fuzzy uncertain language firstly. Then, calculate grey relational grades of every evaluating value for positive or negative ideal solutions. Third, determine the weights of attributes by a linear programming model if part of attribute information is known. Fourth, calculate grey relational grades of each alternative for the positive or negative ideal solutions. Lastly, calculate relative grey relational grades and sort the alternatives.

The main common drawback of the two approaches to assessing the significance of risk is their subjectivity. Even large consulting companies such as McKenzie, Deloitte and PwC publish reports analyzing the potential M&A risks based on the subjective opinions of experts. Apparently, it is impossible to completely overcome subjectivity. This is due to the subjective nature of the “risk” category itself (Slovic 1999).

Research on M&A risk management tools falls into three areas:

- Search for instruments depending on the type of risk;

- Search for instruments depending on the stage of the deal;

- Search for common instruments for all types of risk and transaction stages.

In the first direction, the most comprehensive research is the work of Sui and Dumitrescu-Peculea (2016) (Table 1).

Within the framework of the second direction, the most complete system of tools is offered by Anisimovets (2016), which uses its own set of management tools for each stage of the transaction:

- The stage of strategy development (involving employees of strategic planning departments);

- The stage of searching and evaluating suitable candidates (creating criteria for searching for candidates, forming a profile of the target company, ranking indicators for evaluating candidates by importance, constant monitoring of the mergers and acquisitions market);

- The stage of negotiations (involvement of mediators during negotiations, drawing up a letter of intent);

- The stage of integration (attracting employees responsible for the transaction to analyze and optimize processes in the target company and develop new processes for the combined company, create internal communications between company employees, overcome cultural differences, develop a new organizational and management structure, develop staff retention measures);

- The stage of control (continuous updating of the business plan by adapting it to the current situation, tracking the indicators of the merger and acquisition transaction, drawing up an aggregate report to identify problematic aspects, clearly delineating responsibility for achieving key indicators of the transaction, reducing the time for making management decisions).

In the third direction, researchers suggest using one instrument regardless of the type of risk and stage of the transaction.

Ramieva et al. (2016) focuses on strategic risks as the most significant in the implementation of mergers and acquisitions. To manage them, a full comprehensive analysis of the target company’s strategy is performed. This analysis includes determining the attractiveness of the industry, target company, region, economic benefits and costs, growth dynamics and structure of the industry, and a forecast for the future. In addition, this tool should also include an analysis of the impact of macroeconomic factors and take into account the uncertainty factor of the company’s external environment.

Warter and Warter (2017) identifies the risks associated with the cultural diversity of the companies participating in the transaction as the main risk, proposing due diligence as the main tool to combat them. It is the process of identifying and assessing the degree of cultural alignment or compatibility between companies that are potential parties to a transaction. This tool allows you to identify potential areas of conflict in company cultures.

Modern mechanisms to reduce risks in international transactions offer Lewis (2019). Acquirers can reduce their risk by trading internal and deal-level risk factors (information asymmetry and moral hazard) off against external and country-level risk factors (“liability of foreignness” and “double-layered acculturation”). Country’s governance quality decreases the likelihood of deal withdrawal, and the risk mitigating effect is even stronger when the selling country has a strong governance mechanism as well, or when the acquiring country has high operational risk, or when the selling country has lower operational risk.

M&A risk mitigation toolkit was offered by Zhang (2017). To reduce risks, Zhang suggests that M&A companies adopt a variety of methods to comprehensively assess the value of the target enterprise, rationally design the financing plan and pay close attention to the target business operation.

For the practical application of a risk management tool, it is necessary to evaluate it according to predetermined criteria. Most authors refer to such criteria as the degree of risk uncertainty and the magnitude of the consequences of the risk realization. Brocal et al. (2021) believe that frameworks that deal with emerging risk management in industrial contexts are very recent or, even still, in the development and maturation stage. Uncertainty should be considered as the main characteristic of emerging risk in this context. To this end, uncertainty has been integrated, as a combination of knowledge and understanding, in a theoretical framework on emerging risk. An emerging risk classification scheme has been developed with the results obtained. This scheme makes it possible to estimate the level of emerging risk and management strategies based on the combination of uncertainty and the potential consequences of emerging risk.

The uncertainty parameter is of great importance according to Slagmulder and Devoldere (2018). Research shows how leading companies develop a strategic risk management (SRM) capability to increase their resilience and agility in response to deep uncertainty.

2. Materials and Methods

The complexity of risk management determines the complexity of the formulation of its essence. In this article (in relation to M&A), such a definition of risk management is adopted. This is an element of the corporate strategy of mergers and acquisitions, consisting of a set of methods and techniques that allow predicting the occurrence of risks, comprehensively analyzing and assessing them, and taking certain actions to reduce or neutralize the negative consequences of risks in order to maximize the effect of the M&A transaction. As a first approximation, the effect of the M&A transaction is expressed in an increase in the profit of the combined company. This definition takes into account those aspects of risk management that are directly related to this work.

Based on the research results, which are reviewed in the Introduction, the following risk management algorithm is proposed, which is relevant to the objectives of this study:

- Information analysis. Risk management begins with an informational analysis of the external and internal environment in which a merger and acquisition transaction is being implemented. The current state of the companies participating in the transaction is assessed, regulatory and legal restrictions on the transaction are considered. In other words, a complete information base is analyzed, which affects the presence or absence of risks of a merger and acquisition transaction;

- Risk identification. The second stage of risk management is risk identification. At this stage, based on the analysis performed, the risks that are inherent in a particular transaction at this stage of its implementation are identified;

- Risk classification. The identified risks must be classified, since each type of risk has its own management tools. Identification of the type of risk allows faster and more accurate selection of a risk management tool;

- Assessment of the significance of risks. The next stage of risk management is to assess the significance of risks by the number of potential losses, by the strength of the impact on the companies participating in the transaction;

- Risk ranking by level of significance. The assessment of the significance of risks is carried out with the aim of their subsequent ranking according to the level of significance to determine the priority of making management decisions to find tools for managing specific risks;

- Choosing a risk management tool. A ranked number of risks by their level of significance allows for a faster and more accurate selection of the relevant tool for their management;

- Implementation of measures to combat risk. At the conclusion of the risk management algorithm, in accordance with the selected risk management tools, specific practical measures are taken to combat risks, to eliminate them or reduce the negative consequences of their implementation.

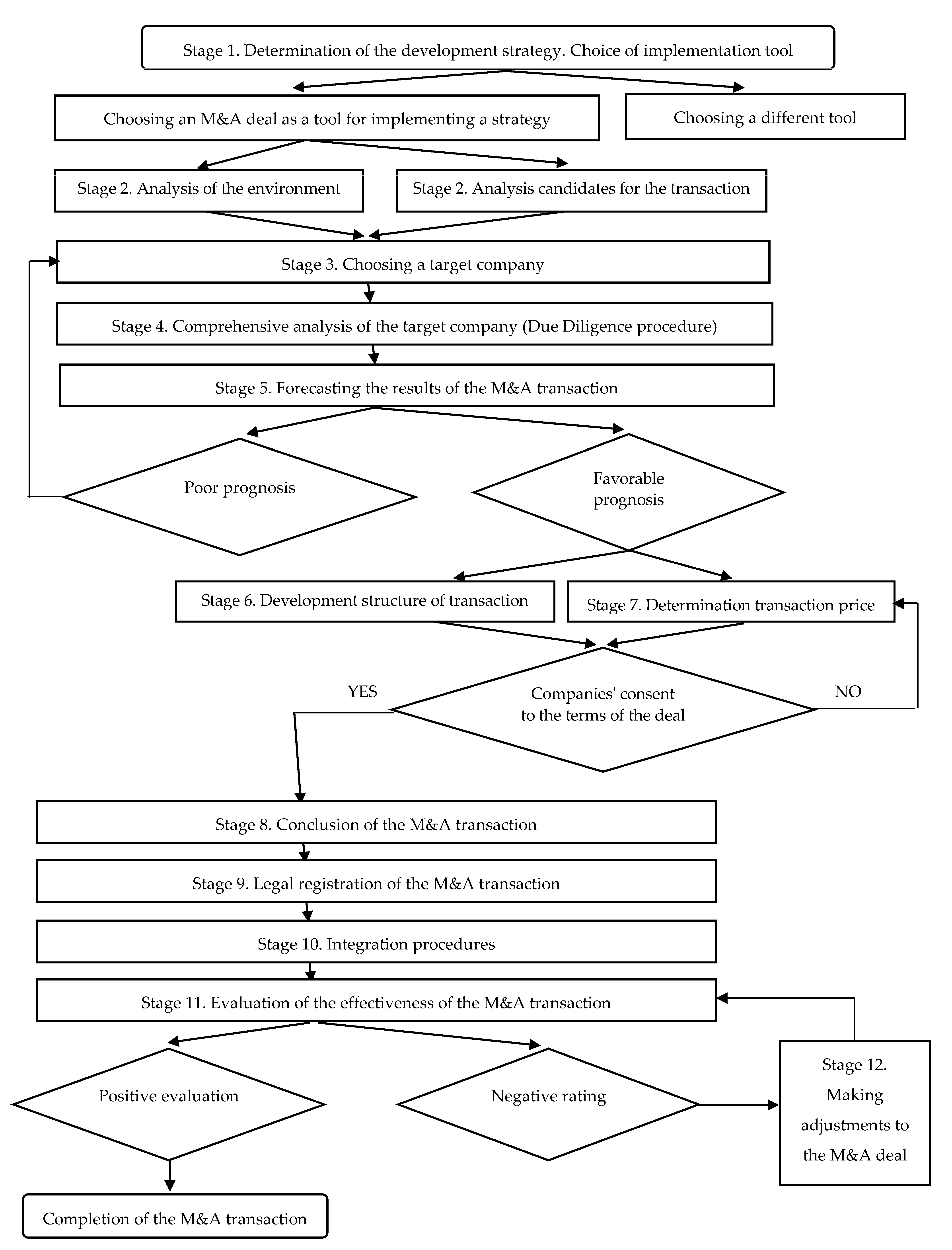

The most general algorithm for the formation and implementation of an M&A transaction was drawn up shown in the Figure 1.

This algorithm is quite general and detailed at the same time, since it was compiled with the aim of further theoretical study of the process of mergers and acquisitions, as well as identifying risks at each of the stages, therefore, the stages should be moderately detailed and moderately generalized. Let us consider each of the stages of planning and implementing an M&A transaction in more detail.

At the first stage, the company determines the basic strategy for its development: an integrated, concentrated, differentiated growth strategy or a reduction strategy. Analyzes the available tools for implementing the strategy: own or debt financing, M&A transactions. If an M&A transaction is chosen as a tool for implementing the chosen basic development strategy, the algorithm continues to be followed.

At the second stage, the company analyzes the external environment: political, economic, legal, and other conditions in which the company will have to implement the chosen strategy. Analyzes candidates for an M&A transaction, evaluates them according to the evaluation criteria developed by the buying company.

At the third stage, in accordance with the selected criteria, the most suitable target company is selected.

At the fourth stage, the company carries out a comprehensive analysis of the selected target company (Due Diligence procedure)—checking the legal, financial, tax and marketing aspects of activities. The value of the Target Company, risks and potential synergistic effects are assessed.

At the fifth stage, the company predicts the potential results of the M&A transaction based on a comprehensive analysis of the Target Company and external conditions for the implementation of the transaction. In case of an unfavorable forecast, the company reconsiders the choice of the target company, and in case of a favorable forecast, the transition to the sixth and seventh stages is carried out.

At the sixth and seventh stages, the structure of the transaction is developed: a phased schedule for its implementation, a scheme and plan for financing the transaction, and a method of payment is selected. An integration plan is being drawn up. The transaction price is also determined based on the projected results of the transaction, the estimated value of the Target Company, risks and potential synergies. If the companies agree with these terms of the transaction, then the transition to the eighth stage is carried out, and if not, then the terms of the transaction are revised, return to the sixth and seventh stages.

At the eighth stage, the company enters into an M&A deal. Agreements are implemented on the terms of the transaction (purchase price of the Target Company, transaction structure, scheme, and method of payment).

At the ninth stage, the legal registration of documents for the M&A transaction takes place.

At the tenth stage, the process of company integration itself takes place. A new organizational structure of the merged company is being formed, the integration of corporate cultures and production processes is taking place.

At the eleventh stage, the results of the M&A transaction are evaluated, compared with the predicted results of the transaction, and conclusions are drawn about the degree of achievement of the set goals as a result of the integration. If a positive assessment is given, then the process of formation and implementation of the M&A transaction is completed, and if a negative assessment is given, then an additional twelfth stage is implemented to adjust the transaction (there is a return to the eleventh stage).

For the most effective, targeted risk management, it is necessary to rank the identified risks within each stage according to the level of significance (Vertakova and Vselenskaya 2020). In order to compile a risk rating for mergers and acquisitions, it is proposed to calculate an integrated assessment of the significance for each risk, based on the Skitsko risk significance assessment methods; Verdiev; Yarina; Sogrina. The choice of specific methods for assessing the significance of risks is due to their effectiveness and the breadth of distribution and application in practice. The integrated assessment will be calculated using the formula:

where R—integrated significance assessment; r1—place in the ranking according to the Skitsko’s method; r2—place in the rating according to the Verdiev’s method; r3—place in the ranking according to Yarin’s method; r4—place in the ranking according to Sogrina’s method.

R = (r1 + r2 + r3 + r4)/4,

The weights of the methods are taken to be equal; the arithmetic mean is taken as a calculation method. The results of the assessment are presented in the Appendix A. Table A1 (Appendix A) compiled by the authors using Equation (1). Estimation by Skitsko, Verdiev, Yarin and Sogrina methods was used. These methods allow for the assessment of risks using a linguistic variable (qualitative assessment). These linguistic variables were then converted into scores (quantification). For these quantitative estimates, the calculation of the arithmetic mean was used. That is, the author’s assessment methodology is based on the integration of risk assessment by the Skitsko, Verdiev, Yarin and Sogrina methods.

In the last column of the Table A1 (Appendix A), in parentheses, there are risk ranking indicators for each stage of the M&A transaction. Arranging the risks of a merger and acquisition transaction in descending order of their level of significance makes it possible to formulate the priorities of risk management. Based on the analysis of the literature and the practice of managing mergers and acquisitions, the relevant tools for managing the risks of mergers and acquisitions at each stage of the transaction were identified (Plotnikov et al. 2019).

These results are presented in Appendix B. The most common risk management tools for mergers and acquisitions, which can be called universal tools, are highlighted at each stage: constant monitoring, engaging a specialized third-party organization or delegating authority to qualified company employees to solve specific problems, conducting a comprehensive analysis and assessment, implementing a mechanism control, identification and assessment of certain aspects of the company’s activities, a clear study of the strategy for the integration of companies.

Specific risk management tools for mergers and acquisitions were identified at most stages of the transaction:

- At the stage of analyzing the external environment and candidates for a deal—this is the creation of criteria, ranking according to the level of significance, the formation of a company profile;

- At the stage of a comprehensive analysis of the target company, development of the structure and conclusion of the transaction—engaging intermediaries to solve specific problems;

- At the stage of predicting the results—develop an effective assessment methodology;

- At the stage of developing the structure of the transaction—a clear distribution of rights, powers and obligations, drawing up a letter of intent, combining various financial instruments, developing an effective capital structure;

- At the stage of determining the price of the transaction—the development of an effective pricing methodology, the choice of a strategically effective method of payment;

- At the stage of concluding an M&A deal and integration procedures—development of measures to retain staff, customers and suppliers, development of a new organizational and management structure;

- At the stage of integration procedures—creation of internal communications between company employees;

- At the stage of evaluating the effectiveness of the transaction—controlling, insurance, a clear delineation of responsibility for the achievement of key indicators of the transaction.

3. Results

Practical application of the developed risk management model for mergers and acquisitions is a multi-stage process.

The first stage in the implementation of the developed risk management model is the identification of the stage of the transaction, since each of the ten stages of the M&A transaction has its own set of characteristic risks. As part of the development of a risk management model, each risk is assigned its own unique number from R1 to R51. In addition, each risk needs its own relevant tools to manage it.

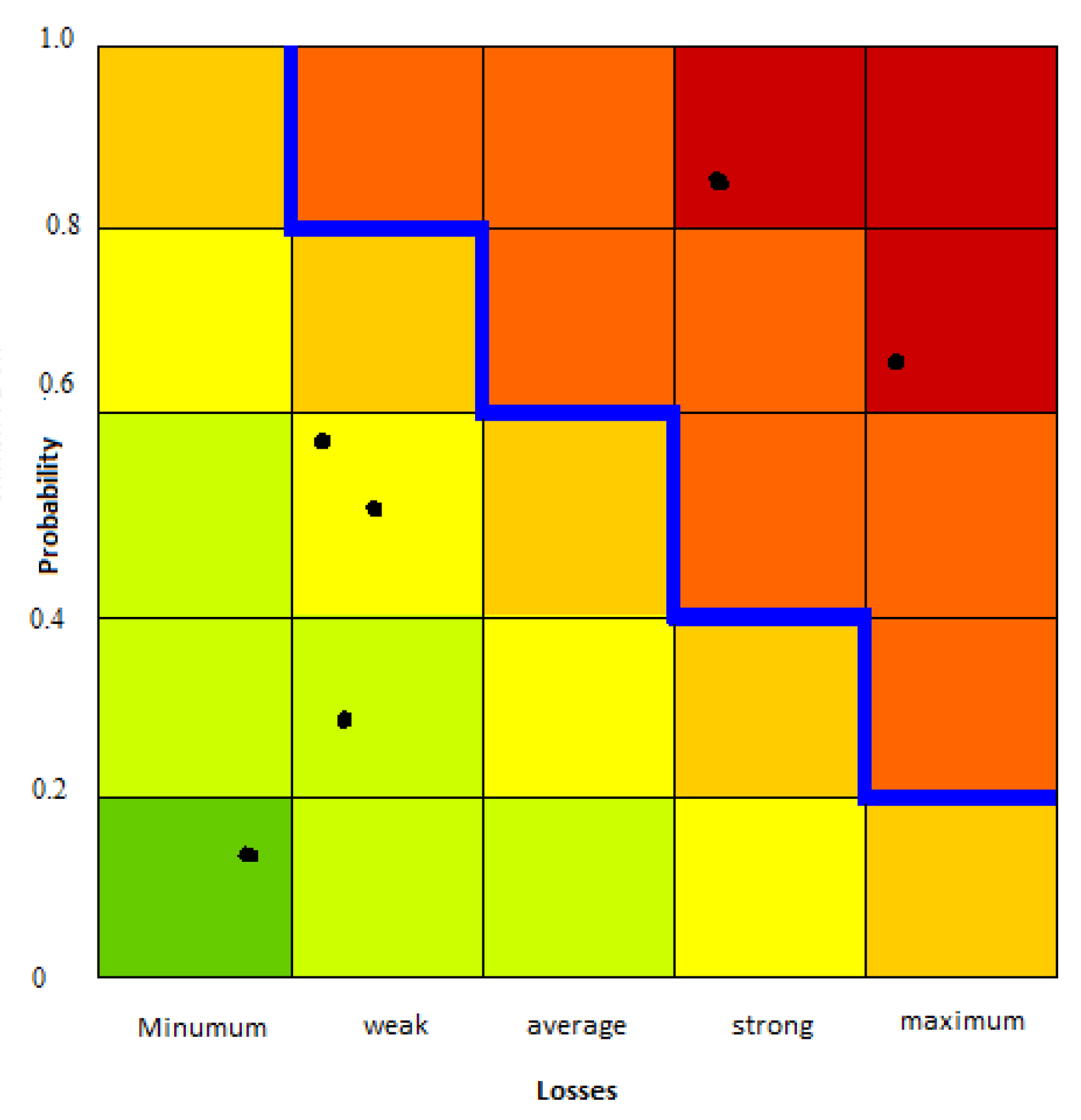

Each risk has two key characteristics: the likelihood of risk occurrence (measured from 0 to 1), loss (measured in conventional units of damage). Within the framework of an automated risk management model, these characteristics are input parameters for each of the 51 risks. That is, the user of a computer program for a specific merger and acquisition transaction, based on the data of the expert assessment, it will be necessary to enter for each risk the probability of its occurrence and potential losses in conventional units.

The automated risk management model for mergers and acquisitions is based on a “risk map”, which serves to visually illustrate the risks inherent in each particular transaction. After entering the probability of occurrence of risks and potential losses from them, the user will need to enter the maximum value of potential losses, which will be located along the horizontal axis on the “risk map” (Figure 2). The program will automatically divide the horizontal axis into five equal parts (by analogy with the vertical axis, which indicates the likelihood of a risk). After entering all the parameters, the user generates a risk map, on which the entered risks are marked.

The green area on the “risk map” denotes an area of insignificant risks. The red zone is the zone of critical risks, which corresponds to the highest values along the axes. There are intermediate levels of risk between these extreme zones. When the user hovers over any point that denotes a particular risk, the user is presented with the following information: risk number (from R1 to R51), risk name, risk probability (from 0 to 1), losses and relevant management tool.

The automated risk management model for mergers and acquisitions is based on the consideration of risk situations, which are described by a tuple of two characteristics. These characteristics are the likelihood of risk occurrence and loss. In the general case, more complex situations are also possible. M&A risks may follow discrete or continuous stochastic distributions with more than only two outcomes. For example, several outcomes are possible (discrete distribution), each of these outcomes has different losses and probabilities. This may be due to the activity and effectiveness of risk management measures.

If the risks follow a discrete or continuous stochastic distribution with more than two outcomes, the proposed model and risk map should be modified. Two main directions of such modification are proposed:

- Conducting stochastic modeling considering the possible ambiguity of the consequences of each of the risks. In this case, each step of modeling will lead to the appearance of a new point on the risk map. Based on the simulation results, not “points”, but “areas” will be built on the risk map. The presence of risk areas increases uncertainty and complicates management decisions. At the same time, it allows for a more objective assessment of the consequences of the M&A deal;

- Conducting preprocessing (normalization) of distribution functions that characterize risks. The goal of this normalization is to move from multiple loss / probability pairs to describing each risk with one pair of these characteristics. In this case, it will be possible to use the proposed risk map. However, this approach simplifies the situation, does not allow considering all the variety of possible outcomes when making an M&A transaction. That is, the simplification of the model is achieved by reducing the accuracy of the risk assessment.

Other approaches to solving this problem are also possible. They require further research.

A serious problem of the proposed model is subjectivity in assessing the likelihood of risks and losses. The risks of mergers and acquisitions can be assessed by business owners, managing directors, analysts and other professionals. The problem of subjectivity in risk assessment is fundamental. It is inherent not only in the process of assessing the risks of mergers and acquisitions, but also in the assessment of any risks in general. To solve it, various expert assessment methodologies are used. Some of them are formalized in the format of official documents (EFSA 2014). Several valuable recommendations are outlined in the literature (Cooke and Goossens 2004; Tian et al. 2018; Turisová et al. 2012). These guidelines look at risk assessment cases. Appropriate tools can be used to assess the risks of mergers and acquisitions. It is recommended to use the Expert System for Risk Assessment of M&A-projects developed by Karelina et al. (2015).

4. Discussion

By applying a comprehensive automated methodology for risk management of mergers and acquisitions, one can analyze the current situation, recognize problem areas and the most significant risks, and form a system for assessing and leveling risks inherent in mergers and acquisitions. The model has several disadvantages and reserves for expansion.

As extensions to the automation of the developed model of risk management of mergers and acquisitions, the following can be proposed:

- Split data entry and output of results for each of the ten stages of the transaction separately. This extension will allow you to analyze data both for each individual stage, and for the entire set of 51 risks as a whole;

- At the time of data entry, do not enter stages, displaying only a general “risk map”. However, when analyzing, add the name of the stage of the M&A transaction.

The model has some shortcomings, identified because of practical testing of the risk management model for mergers and acquisitions.

First, the model does not provide the ability to perform a comparative analysis of risks that are in the same area. It is not always possible to clearly determine the proximity to the next most critical risk zone. The accuracy of this definition is insufficient. Therefore, in the process of deciding on the priority of risk management measures that are in the same area, it is necessary to take into account the level of their significance. In other words, in each zone, first, take measures to manage the most significant risk, regardless of the place it occupies in the zone. This fact suggests that the level of significance must be considered when determining the measures necessary to carry out within the framework of risk management in the implementation of a merger and acquisition transaction.

Secondly, the disadvantage of the model is the subjectivity of assessing the likelihood of risks and losses from them, which entails the need to attract qualified professional experts in the field of mergers and acquisitions to assess them. This is associated with additional financial costs.

Third, the model needs to take into account the specifics of the industry. So, for example, in the considered case we are talking about the banking sector, in which there are no providers of banking services and contracts with them, which makes it difficult to assess risks.

The validation of the model has proven its effectiveness when comparing the theoretical results of applying the risk management model and the actual results of a M&A transaction in practice. In general, taking into account the listed shortcomings and the proposed improvements, the risk management model can be considered effective. The risk management model with the selection of the most adequate risk management tools for each stage of the implementation of the merger and acquisition transaction creates a theoretical foundation for further research on this issue. The model can serve as a basis for the formation or improvement of the management of the company participating in the transaction, a new or existing model of an effective risk management process, which reduces time and labor costs, as well as obtain other positive effects, which will lead to an increase in the efficiency of management of mergers and acquisitions.

5. Conclusions

The developed model of risk management in the implementation of mergers and acquisitions is an almost universal tool for managing risks arising in integration processes. To ensure the efficiency and success of the implementation of mergers and acquisitions, it is very important to manage risks using selected tools at each stage of the transaction by consistently applying risk management techniques when planning mergers and acquisitions, which can prevent and reduce the impact of most of the factors that negatively affect the integration of companies. It is necessary to take into account the level of significance of a particular risk at each stage by comparing the costs of the risk management tool and the significance of the benefits from its use.

The developed system of tools for dealing with the risks of mergers and acquisitions can form the basis for the creation of a comprehensive risk management methodology in the implementation of mergers and acquisitions, which will allow identifying, analyzing, assessing risks, choosing the most effective management tools, determining the acceptable risk of mergers and acquisitions, researching its economic efficiency, develop plans to improve the transaction and actions in case of adverse events.

Author Contributions

Conceptualization, Y.V.; methodology, I.V.; software, I.V. and V.P.; validation, V.P.; formal analysis, Y.V., I.V. and V.P.; investigation, Y.V., I.V. and V.P.; writing—original draft preparation, I.V. and V.P.; writing—review and editing, Y.V. and V.P.; supervision, V.P.; project administration, Y.V. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Acknowledgments

The study was supported by a Grant from the President of the Russian Federation for state support of leading scientific schools of the Russian Federation NSh-2702.2020.6 “Conceptual foundations of a new paradigm of economic development in an era of technological and social transformation”.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

Table A1.

Assessment of the significance of the risks of mergers and acquisitions 1.

| Risks | Skitsko Method | Verdiev Method | Yarin Method | Sogrina Method | Integrated Significance Assessment |

|---|---|---|---|---|---|

| Determination of the company’s development strategy. Choosing an M&A deal as a tool for implementing a strategy | |||||

| The risk of the wrong choice of the company’s development strategy | medium (3) | low (4) | insignificant risk (4) | high (2) | 3.5 (3) |

| The risk of mismatching the M&A strategy with the general strategy of the company | high (2) | very high (1) | significant likelihood of risk manifestation (1) | very high (1) | 1.25 (1) |

| The risk of incorrect strategy formation | very high (1) | high (2) | uncertainty in the manifestation of risk (2) | medium (3) | 2 (2) |

| The risk of choosing the wrong form of integration | low (4) | medium (3) | unrealizable risk (3) | low (4) | 3.5 (4) |

| Analysis of the company’s external environment. Analysis of candidates for an M&A transaction | |||||

| The risk of incorrect selection of candidates for the deal | high (2) | high (2) | significant likelihood of risk manifestation (2) | very high (1) | 1.75 (2) |

| The risk of unfavorable changes in the economy | medium (3) | medium (3) | uncertainty in the manifestation of risk (3) | medium (3) | 3 (4) |

| The risk of non-reflection of changes in the market on the M&A strategy | medium (3) | high (2) | significant likelihood of risk manifestation (2) | high (2) | 2.25 (3) |

| Risk of adverse changes in legislation | very low (5) | very low (5) | unrealizable risk (4) | low (4) | 4.5 (6) |

| Risk of incomplete list of criteria for candidates | very high (1) | very high (1) | full probability of risk manifestation (1) | very high (1) | 1 (1) |

| Risk of non-reflection of changes in legislation on M&A strategies | low (4) | low (4) | uncertainty in the manifestation of risk (3) | medium (3) | 3.5 (5) |

| Choosing a target company | |||||

| The risk of incompatibility of corporate cultures of companies | very high (1) | very high (1) | significant likelihood of risk manifestation (2) | high (2) | 1.5 (2) |

| The risk of choosing the wrong target company | medium (3) | low (4) | negligible risk (5) | low (4) | 4 (5) |

| The risk of company cultural differences | high (2) | medium (3) | uncertainty in the manifestation of risk (3) | high (2) | 2.5 (3) |

| The risk of technological incompatibility of information systems of companies | very high (1) | high (2) | full probability of risk manifestation (1) | very high (1) | 1.25 (1) |

| Risk of brand incompatibility | very low (4) | medium (3) | unrealizable risk (4) | medium (3) | 3.5 (4) |

| Comprehensive analysis of the target company (Due Diligence procedure) | |||||

| The risk of poor-quality study of the business characteristics of the target company | very high (1) | high (2) | full probability of risk manifestation (1) | very high (1) | 1.25 (1) |

| The risk of inability to establish effective contact with the management of the target company | medium (3) | medium (3) | uncertainty in the manifestation of risk (2) | medium (3) | 2.75 (3) |

| The risk of the target company being liable | high (2) | very high (1) | full probability of risk manifestation (1) | high (2) | 1.5 (2) |

| Risk of unknown violations of legal requirements | low (4) | medium (3) | unrealizable risk (3) | low (4) | 3.5 (4) |

| Risk of Differences in Financial Reporting Standards | very low (5) | low (4) | insignificant risk (4) | medium (3) | 4 (5) |

| Forecasting the results of an M&A transaction | |||||

| Risk of incorrect assessment of future synergies from the transaction | high (2) | very high (1) | uncertainty in the manifestation of risk (2) | high (2) | 1.75 (2) |

| The risk of overestimating the potential benefits of the transaction | very high (1) | high (2) | full probability of risk manifestation (1) | very high (1) | 1.25 (1) |

| The risk of underestimating the additional investment required for the transaction | very low (4) | medium (3) | insignificant risk (4) | medium (3) | 3.5 (4) |

| Risk of overestimating future cost savings of the combined company | low (3) | low (4) | uncertainty in the manifestation of risk (3) | medium (3) | 3.25 (3) |

| M&A deal structure development | |||||

| Risk of misunderstanding regarding the parameters of the transaction between the companies | high (2) | medium (2) | uncertainty in the manifestation of risk (2) | Low (3) | 2.25 (2) |

| Funding risks associated with various types of transaction financing | low (3) | low (3) | unrealizable risk (3) | medium (2) | 2.75 (3) |

| The risk of insufficient funds to service debt when using debt financing | very high (1) | high (1) | significant likelihood of risk manifestation (1) | high (1) | 1 (1) |

| Determining the price of an M&A transaction | |||||

| The risk of incorrect pricing | medium (3) | medium (3) | uncertainty in the manifestation of risk (3) | high (2) | 2.75 (3) |

| Risk of incorrect estimation of transaction costs | very high (1) | high (2) | full probability of risk manifestation (1) | very high (1) | 1.25 (1) |

| Risk of administrative miscalculations | low (4) | medium (3) | negligible risk (5) | low (4) | 4 (4) |

| The risk of overestimating the amount of the premium paid when making a deal | very low (5) | low (4) | insignificant risk (4) | low (4) | 4.25 (5) |

| The risk of overestimating the investment potential of the company initiating the transaction | high (2) | very high (1) | uncertainty in the manifestation of risk (2) | very high (1) | 1.5 (2) |

| Closing an M&A transaction. Legal registration of documents | |||||

| The risk of conflicts between shareholders of companies | high (2) | medium (3) | uncertainty in the manifestation of risk (2) | very high (1) | 2 (2) |

| The risk of opposition from the authorities to the transaction | very high (1) | very high (1) | significant likelihood of risk manifestation (1) | high (2) | 1.25 (1) |

| The risk of losing key employees of the target company who do not agree with the deal | medium (3) | high (2) | unrealizable risk (3) | medium (3) | 2.75 (3) |

| Integration procedures | |||||

| The risk associated with a lack of resources for the transaction | high (2) | medium (3) | uncertainty in the manifestation of risk (3) | medium (3) | 2.75 (4) |

| The risk of slowing down the integration process and failure to fulfill its plan | medium (3) | medium (3) | uncertainty in the manifestation of risk (3) | medium (3) | 3 (5) |

| The risk of a decrease in the productivity of employees of the target company, a fall in work discipline | high (2) | high (2) | significant likelihood of risk manifestation (2) | high (2) | 2 (3) |

| Risk of rupture of relationships with counterparties: customers and suppliers | very high (1) | high (2) | full probability of risk manifestation (1) | high (2) | 1.5 (2) |

| The risk of underestimating the complexity of building an effective corporate governance system in the merged company | very high (1) | very high (1) | significant likelihood of risk manifestation (2) | very high (1) | 1.25 (1) |

| The risk of failure to achieve integration goals due to the dependence of the target company on large customers | very low (5) | low (4) | unrealizable risk (4) | medium (3) | 4 (6) |

| Risks of having duplicate contracts with suppliers | low (4) | low (4) | negligible risk (5) | low (4) | 4.25 (7) |

| Evaluation of the effectiveness of the M&A transaction | |||||

| Risk of failure to achieve integration goals | very high (1) | very high (1) | full probability of risk manifestation (1) | high (2) | 1.25 (2) |

| Risk of ineffective post-transaction merger | low (4) | medium (3) | uncertainty in the manifestation of risk (3) | medium (3) | 3.25 (7) |

| The risk of failure to increase the efficiency of asset management of the combined company | medium (3) | high (2) | unrealizable risk (4) | medium (3) | 3 (6) |

| The risk of a decrease in the market value of the combined company | medium (3) | medium (3) | unrealizable risk (4) | low (4) | 3.5 (8) |

| Risk of negative economies of scale | high (2) | very high (1) | significant likelihood of risk manifestation (2) | very high (1) | 1.5 (3) |

| The risk of non-fulfillment of the business plan by the acquiring company | medium (3) | low (4) | significant likelihood of risk manifestation (2) | high (2) | 2.75 (5) |

| The risk of the appearance of direct competitors in the face of the previous owners | very low (5) | very low (5) | negligible risk (5) | low (4) | 4.75 (9) |

| Risk of reduction in cash flows as a result of changes in the company’s development plan | very high (1) | high (2) | significant likelihood of risk manifestation (2) | high (2) | 1.75 (4) |

| The risk of technological changes in the industry | very high (1) | very high (1) | full probability of risk manifestation (1) | very high (1) | 1 (1) |

1 Values in the cells without brackets characterize the calculated value of the significance level by the methodology, and in parentheses—the place in the rating by the corresponding methodology. The same calculated values—the same places in the rating. According to the Skitsko method, 1 point—very low, 2 points—low, 3 points—medium, 4 points—high, 5 points—very high risk. According to the Verdiev method, there are very high, high, medium, low, very low risk significance. According to the Yarin method, insignificant risk, unrealizability of risk, uncertainty of risk manifestation, significant probability of risk manifestation, full probability of risk manifestation. According to the Sogrina method, low, medium, high and very high risk.

Appendix B

Table A2.

Relevant tools for risk management of mergers and acquisitions at each stage of the transaction.

Table A2.

Relevant tools for risk management of mergers and acquisitions at each stage of the transaction.

| Stage | Risks | Risk Management Tools |

|---|---|---|

| Determination of the company’s development strategy. Choosing an M&A deal as a tool for implementing a strategy | The risk of the wrong choice of the company’s development strategy | Attracting specialists from the strategic planning department to clearly develop a company’s development strategy using an M&A transaction |

| The risk of mismatching the M&A strategy with the general strategy of the company | Constant monitoring of the compliance of the M&A strategy with the general development strategy | |

| The risk of incorrect strategy formation | Comprehensive analysis of the strategic goals and objectives of the company’s development with the involvement of specialists from the strategic planning department | |

| The risk of choosing the wrong form of integration | Involvement of specialists from the strategic planning department for a comprehensive assessment of the forms of integration | |

| Analysis of the company’s external environment. Analysis of candidates for an M&A transaction | The risk of incorrect selection of candidates for the deal | Creation of criteria for the search for candidates, formation of a profile of the target company, ranking of indicators for evaluating candidates by importance |

| The risk of unfavorable changes in the economy | Continuous monitoring of the M&A market, implementation of a mechanism to control macroeconomic changes | |

| The risk of non-reflection of changes in the market on the M&A strategy | Constant revision of the company’s strategy to adjust it | |

| Risk of adverse changes in legislation | Constant monitoring of legislation related to the M&A market, implementation of a mechanism for monitoring regulatory changes | |

| Risk of incomplete list of criteria for candidates | Engaging a specialized third-party organization to create a complete list of criteria, delegate authority to create a complete list of criteria to qualified employees of the company | |

| Risk of non-reflection of changes in legislation on M&A strategies | Constant revision of the company’s strategy to adjust it | |

| Choosing a target company | The risk of incompatibility of corporate cultures of companies | Implementation of a mechanism for identifying and assessing the degree of compatibility between corporate cultures of companies, a clear study of a strategy for the integration of corporate cultures |

| The risk of choosing the wrong target company | Formation of a comprehensive detailed profile of the target company | |

| The risk of company cultural differences | Implementation of a mechanism for identifying and assessing the cultural differences of companies, a clear study of the strategy of cultural integration | |

| The risk of technological incompatibility of information systems of companies | Implementation of a mechanism for identifying and assessing the degree of technological compatibility of information systems of companies, a clear study of the strategy for integrating information systems | |

| Risk of brand incompatibility | Implementation of a mechanism for identifying and assessing the degree of compatibility of brands of companies, a clear study of the strategy of “brand” integration | |

| Comprehensive analysis of the target company (Due Diligence procedure) | The risk of poor-quality study of the business characteristics of the target company | Engaging a specialized third-party organization for a detailed comprehensive analysis of the target company, delegation of authority for a detailed comprehensive analysis of the target company to qualified employees of the company |

| The risk of inability to establish effective contact with the management of the target company | Involvement of intermediaries in the initial negotiations | |

| The risk of the target company being liable | Implementation of a mechanism for control over the documentation of the target company (checking the target company in terms of the availability of obligations) | |

| Risk of unknown violations of legal requirements | Implementation of a control mechanism over the activities of the target company (verification of the target company in terms of compliance with legal requirements) | |

| Risk of Differences in Financial Reporting Standards | Implementation of a control mechanism over the financial reporting of the target company (checking the target company in terms of financial reporting standards) | |

| Forecasting the results of an M&A transaction | Risk of incorrect assessment of future synergies from the transaction | Development of an effective methodology for assessing the financial result of the transaction, engaging a specialized third-party organization to assess the future synergistic effect of the transaction, delegating the authority to assess the future synergistic effect of the transaction to qualified employees of the company |

| The risk of overestimating the potential benefits of the transaction | Development of an effective methodology for assessing the financial result of the transaction, engaging a specialized third-party organization to assess the potential benefits of the transaction, delegating the authority to assess the potential benefits of the transaction to qualified employees of the company | |

| The risk of underestimating the additional investment required for the transaction | Engaging a specialized third-party organization to evaluate the additional investment required for the transaction, delegating the authority to assess the additional investment required for the transaction to qualified employees of the company | |

| Risk of overestimating future cost savings of the combined company | Development of an effective methodology for assessing the financial result of the transaction, engaging a specialized third-party organization to assess the future cost savings of the combined company, delegating the authority to assess the future cost savings of the combined company to qualified employees of the company | |

| M&A deal structure development | Risk of misunderstanding regarding the parameters of the transaction between the companies | A clear distribution of the rights, powers and obligations of the companies involved in the transaction, the involvement of intermediaries in the negotiations, drawing up a letter of intent |

| Funding risks associated with various types of transaction financing | Combining various financial instruments to finance M&A transactions, developing an efficient capital structure | |

| The risk of insufficient funds to service debt when using debt financing | Combining various financial instruments to finance M&A transactions, developing an efficient capital structure | |

| Determining the price of an M&A transaction | The risk of incorrect pricing | Development of an effective methodology for pricing the transaction, engaging a specialized third-party organization to calculate the price of the transaction, delegating the authority to calculate the price of the transaction to qualified employees of the company |

| Risk of incorrect estimation of transaction costs | Selection of a strategically effective payment method, development of an effective methodology for assessing the costs of completing a transaction | |

| Risk of administrative miscalculations | Involvement of a specialized third-party organization to carry out settlements for the transaction, delegation of authority to perform settlements for the transaction to qualified employees of the company, insurance against administrative settlements | |

| The risk of overestimating the amount of the premium paid when making a deal | Involvement of a specialized third-party organization to assess the amount of the bonus paid upon the completion of the transaction, delegation of authority to assess the amount of the bonus paid upon the completion of the transaction to qualified employees of the company | |

| The risk of overestimating the investment potential of the company initiating the transaction | Engaging a specialized third-party organization to assess the investment potential of the initiator of the transaction, delegating the authority to assess the investment potential of the initiator of the transaction to qualified employees of the company | |

| Closing an M&A transaction. Legal registration of documents | The risk of conflicts between shareholders of companies | Engaging intermediaries in negotiations, drafting an agreement between shareholders on the business plan of the combined company, developing a new organizational and management structure, creating a system of internal communications between shareholders |

| The risk of opposition from the authorities to the transaction | Engaging intermediaries in negotiations with government agencies | |

| The risk of losing key employees of the target company who do not agree with the deal | Development of staff retention measures, involvement of intermediaries in negotiations with staff, development of a new organizational and management structure | |

| Integration procedures | The risk associated with a lack of resources for the transaction | Development of an effective methodology for assessing the number of resources required to complete a transaction, engaging a specialized third-party organization to assess the amount of resources required to conduct a transaction, delegating authority to assess the amount of resources required to conduct a transaction |

| The risk of slowing down the integration process and failure to fulfill its plan | Constant monitoring of the calendar fee of the integration process in terms of meeting deadlines and fulfilling planned targets | |

| The risk of a decrease in the productivity of employees of the target company, a fall in work discipline | Development of personnel retention measures, development of a new organizational and management structure, creation of internal communications between company employees | |

| Risk of rupture of relationships with counterparties: customers and suppliers | Development of measures to retain customers and suppliers | |

| The risk of underestimating the complexity of building an effective corporate governance system in the merged company | Engaging a specialized third-party organization to build an effective corporate governance system in the merged company, delegating the authority to build an effective corporate governance system in the merged company to qualified employees of the company, developing a new organizational and management structure | |

| The risk of failure to achieve integration goals due to the dependence of the target company on large customers | Implementation of a control mechanism over the activities of the target company (checking the target company in terms of the company’s dependence on large customers), development of measures to retain large customers | |

| Risks of having duplicate contracts with suppliers | Implementation of a control mechanism over the activities of the target company (checking the target company in terms of duplicate contracts with suppliers) | |

| Evaluation of the effectiveness of the M&A transaction | Risk of failure to achieve integration goals | Insurance, constant monitoring and controlling of the implementation of integration goals, a clear delineation of responsibility for the achievement of key transaction indicators |

| Risk of ineffective post-transaction merger | Conducting a comprehensive assessment of the effectiveness of the transaction at each of its stages, a clear delineation of responsibility for the achievement of key indicators of the transaction | |

| The risk of failure to increase the efficiency of asset management of the combined company | Involvement of a specialized third-party organization for the effective management of the assets of the combined company, delegation of powers for the effective management of the assets of the combined company to qualified employees of the company | |

| The risk of a decrease in the market value of the combined company | Continuous monitoring of the financial and economic activities of the merged company in terms of the market value of the company | |

| Risk of negative economies of scale | Continuous monitoring of the financial and economic activities of the combined company as part of the economies of scale | |

| The risk of non-fulfillment of the business plan by the acquiring company | A clear delineation of responsibility for the achievement of key indicators of the transaction, constant monitoring of the implementation of the business plan | |

| The risk of the appearance of direct competitors in the face of the previous owners | Involvement of intermediaries in negotiations with the former owners of the target company | |

| Risk of reduction in cash flows as a result of changes in the company’s development plan | Continuous monitoring of the financial and economic activities of the merged company in terms of the company’s cash flows | |

| The risk of technological changes in the industry | Continuous updating of the business plan by adapting it to the current situation, introducing a mechanism for monitoring technological changes in the industry |

References

- AK&M. 2020. Mergers and Acquisitions M&A. Available online: https://www.tadviser.ru/index.php/Article:Mergers and acquisitions_M&A#.2A2020 (accessed on 6 March 2021).

- Anisimovets, Victoria Alexandrovna. 2016. Risks in mergers and acquisitions. Young Scientist 9: 465–67. [Google Scholar]

- Ashby, William Ross. 1956. An Introduction to Cybernetics. London: Chapman and Hall, p. 295. [Google Scholar]

- Aven, Terje, and Thor Erik Nøkland. 2010. On the use of uncertainty importance measures in reliability and risk analysis. Reliability Engineering and System Safety 95: 127–33. [Google Scholar] [CrossRef]

- Aven, Terje. 2016. Risk assessment and risk management: Review of recent advances on their foundation. European Journal of Operational Research 253: 1–13. [Google Scholar] [CrossRef] [Green Version]

- Avinadav, Tal, Tatyana Chernonog, and Yael Perlman. 2017. Mergers and acquisitions between risk-averse parties. European Journal of Operational Research 259: 926–34. [Google Scholar] [CrossRef]

- Barros, Rafael Hernandez, and Ignacio López Domínguez. 2013. Integration strategies for the success of mergers and acquisitions in financial services companies. Journal of Business Economics and Management 14: 979–92. [Google Scholar] [CrossRef] [Green Version]

- Barua, Arup, and Alexandra Ioanid. 2020. Country Brand Equity: The Decision Making of Corporate Brand Architecture in Cross-Border Mergers and Acquisitions. Sustainability 12: 7373. [Google Scholar] [CrossRef]

- Boronenko, Marina Vladimirovna. 2017. Formation of the risk management system at the enterprise. International Journal of the Humanities and Natural Sciences 10: 109–12. [Google Scholar]

- Brocal, Francisco, Nicola Paltrinieri, Cristina González-Gaya, Miguel Sebastián, and Genseric Reniers. 2021. Approach to the selection of strategies for emerging risk management considering uncertainty as the main decision variable in occupational contexts. Safety Science 134: 105041. [Google Scholar] [CrossRef]

- Bruyland, Evy, Meziane Lasfer, Wouter De Maeseneire, and Wei Song. 2019. The performance of acquisitions by high default risk bidders. Journal of Banking & Finance 101: 37–58. [Google Scholar]

- Chang, Young Bong, and Wooje Cho. 2017. The Risk Implications of Mergers and Acquisitions with Information Technology Firms. Journal of Management Information Systems 34: 232–67. [Google Scholar] [CrossRef]

- Chen, An-Sing, Hsiang-Hui Chu, Pi-Hsia Hung, and Miao-Sih Cheng. 2020. Financial risk and acquirers’ stockholder wealth in mergers and acquisitions. North American Journal of Economics and Finance 54: 100815. [Google Scholar] [CrossRef]

- Cooke, Roger, and Louis Goossens. 2004. Expert judgement elicitation for risk assessments of critical infrastructures. Journal of Risk Research 7: 643–56. [Google Scholar] [CrossRef]

- Delakhov, Dmitry Afanasievich, and Nikolay Dorofeevich Karataev. 2017. Risk management in entrepreneurial activity. Discussion 5: 31–34. [Google Scholar]

- Duan, Yinying, Yong Ye, and Zhichao Liu. 2019. Risk assessment for enterprise merger and acquisition via multiple classifier fusion. Discrete & Continuous Dynamical Systems-S 12: 747–59. [Google Scholar]

- European Food Safety Authority (EFSA). 2014. Guidance on Expert Knowledge Elicitation in Food and Feed Safety Risk Assessment. EFSA Journal 12: 3734. [Google Scholar] [CrossRef]

- Fertis, Apostolos, Michel Baes, and Hans-Jakob Lüthi. 2012. Robust risk management. European Journal of Operational Research 222: 663–72. [Google Scholar] [CrossRef]

- Fischer, Sophie, John Rodwell, and Mark Pickering. 2021. A Configurational Approach to Mergers and Acquisitions. Sustainability 13: 1020. [Google Scholar] [CrossRef]

- Folch-Calvo, Martin, Francisco Brocal-Fernández, Cristina González-Gaya, and Miguel Sebastián. 2020. Analysis and Characterization of Risk Methodologies Applied to Industrial Parks. Sustainability 12: 7294. [Google Scholar] [CrossRef]

- Gagnon, Marc-André, and Karena Volesky. 2017. Merger mania: Mergers and acquisitions in the generic drug sector from 1995 to 2016. Global Health 13: 62. [Google Scholar] [CrossRef] [Green Version]

- González-Torres, Thais, José-Luis Rodríguez-Sánchez, Eva Pelechano-Barahona, and Fernando García-Muiña. 2020. A Systematic Review of Research on Sustainability in Mergers and Acquisitions. Sustainability 12: 513. [Google Scholar] [CrossRef] [Green Version]

- Guzhin, Aleksandr Aleksandrovich, and Valentina Gennadievna Ezhkova. 2017. Risk management and risk management methods. Innovations and Investments 2: 185–89. [Google Scholar]

- Haugen, Stein, and Jan Erik Vinnem. 2015. Perspectives on risk and the unforeseen. Reliability Engineering and System Safety 137: 1–5. [Google Scholar] [CrossRef]

- Hečková, Jaroslava, Róbert Štefko, Miroslav Frankovský, Zuzana Birknerová, Alexandra Chapčáková, and Lucia Zbihlejová. 2019. Cross-Border Mergers and Acquisitions as a Challenge for Sustainable Business. Sustainability 11: 3130. [Google Scholar] [CrossRef] [Green Version]

- Huang, Peng, Micah Officer, and Ronan Powell. 2016. Method of payment and risk mitigation in cross-border mergers and acquisitions. Journal of Corporate Finance 40: 216–34. [Google Scholar] [CrossRef] [Green Version]

- Karelina, Mariia, Tatiana Ivanova, and Violetta Trofimova. 2015. Expert system for risk assessment of M&A-projects. International Business Management 9: 762–70. [Google Scholar]

- Keshk, Ahmed Mohamed, Ibrahim Maarouf, and Ysory Annany. 2018. Special studies in management of construction project risks, risk concept, plan building, risk quantitative and qualitative analysis, risk response strategies. Alexandria Engineering Journal 57: 3179–87. [Google Scholar] [CrossRef]

- Kiseleva, Irina Anatolievna. 2017. Risk management in business. Problems of Science 13: 62–65. [Google Scholar]

- Kurmakaeva, Diana Damirovna. 2019. Topical issues of risk management in the organization. Contentus 11: 39–44. [Google Scholar]

- Kuzmina, Yulia Vyacheslavovna. 2018. Theoretical aspects of mergers and acquisitions. NovaInfo 77: 146–50. [Google Scholar]

- Le Coze, Jean-Christophe, Kenneth Pettersen, and Teemu Reiman. 2014. The foundations of safety science. Safety Science 67: 1–5. [Google Scholar] [CrossRef]

- Legeida, Vladimir Sergeevich. 2018. The essence and content of risk management. Problems of Science and Education 7: 114–17. [Google Scholar]

- Lewis, Yimai. 2019. Risk Mitigation in International Mergers and Acquisitions. Ph.D. Thesis, Georgia State University, Atlanta, GA, USA. Available online: https://scholarworks.gsu.edu/marketing_diss/49 (accessed on 6 March 2021).

- Lewis, Yimai, and Konstantinos Bozos. 2019. Mitigating post-acquisition risk: The interplay of cross-border uncertainties. Journal of World Business 54: 100996. [Google Scholar] [CrossRef]

- Li, Shi, James Ang, Chaopeng Wu, and Shijie Yang. 2021. Valuing technological synergies in mergers. The North American Journal of Economics and Finance 58: 101464. [Google Scholar] [CrossRef]

- Hongjiu, Liu, Liu Qingyang, and Hu Yanrong. 2019. Evaluating Risks of Mergers & Acquisitions by Gray Relational Analysis Based on Interval-Valued Intuitionistic Fuzzy Information. Mathematical Problems in Engineering 2019: 3728029. [Google Scholar]

- Loukianova, Anna, Egor Nikulin, and Andrey Vedernikov. 2017. Valuing synergies in strategic mergers and acquisitions using the real options approach. Investment Management and Financial Innovations 14: 236–47. [Google Scholar] [CrossRef] [Green Version]

- Masys, Anthony. 2012. Black swans to grey swans: Revealing the uncertainty. Disaster Prevention and Management 21: 320–35. [Google Scholar] [CrossRef]

- Nobanee, Haitham, Fatima Youssef Al Hamadi, Fatma Ali Abdulaziz, Lina Subhi Abukarsh, Aysha Falah Alqahtani, Shayma Khalifa AlSubaey, Sara Mohamed Alqahtani, and Hamama Abdulla Almansoori. 2021. A Bibliometric Analysis of Sustainability and Risk Management. Sustainability 13: 3277. [Google Scholar] [CrossRef]

- Ott, Christian. 2020. The risks of mergers and acquisitions—Analyzing the incentives for risk reporting in Item 1A of 10-K filings. Journal of Business Research 106: 158–81. [Google Scholar] [CrossRef]

- Plotnikov, Vladimir, Yulia Vertakova, and Inga Vselenskaya. 2019. Risk Management Instruments for Mergers and Acquisitions. Paper presented at 34th International Business Information Management Association Conference (IBIMA)—Vision 2025: Education Excellence and Management of Innovations through Sustainable Economic Competitive Advantage, Madrid, Spain, November 13–14; pp. 1748–58. [Google Scholar]