1. Introduction

The outbreak of COVID-19 led to quarantine, lockdown, and social distancing measures being imposed across the globe. The rapid increase in the number of people infected and the mortality rate prompted countries to change their basic priorities despite the major negative effects and consequences that these measures would have. This situation motivated researchers to study the major effects of restrictions on different sectors and economies (

Davidescu et al. 2021;

Dimian et al. 2021;

Vasile et al. 2021).

Since the first global announcements of the spread of SARS-CoV-2 in January 2020, there have been undefinable disruptions in supply chains worldwide (

Choi et al. 2020), and economies have been confronted with severe disruption in operational and financial flows linked to the decrease in demand and product segmentation, supply shortages, disorders in inventories and their placement, productivity decrease, etc. The demand for different commodities follows different trends, i.e., the demand and supply for oil decreased, prompting a significantly decreasing the oil price (

Rajput et al. 2020); the demand for consumption goods and medication increased compared with the previous year, prompting a smooth supply of these commodities (

WHO 2020a). We also witnessed the metamorphosis of global supply chains under digitalization, regionalization, de-Sinicization, and renewed protectionism. (

Grillo et al. 2018;

Frazzon et al. 2019;

Kano and Oh 2020;

Belhadi et al. 2021;

Fantazy and Mukerji 2021;

Fekpe and Fiagbey 2021;

Gurtu and Johny 2021).

Furthermore, another substantial decline was observed in FDI flows during the ongoing COVID-19 crisis. Foreign direct investment (FDI) creates a link between a country of origin and destinations that “help” contagious phenomena (

Antonietti et al. 2020). The focus of this study is the correlation of FDI outflows with COVID-19 cases and deaths, investigating if the main determinants of FDI outflows are significant for developed European countries.

Developed countries generate FDI to maintain sustainable development, market competitiveness, and export stimulation (

Matei 2004;

Azzutti 2016), as a financial source of the repatriation of capital and the repayment of loans (

Barauskaite 2012), etc. Developing countries need foreign capital positively effect economic growth and to enrich the opportunities for decent employment, as well as capital and knowledge transfers (

Zaman and Vasile 2012;

Akbar and Akbar 2015;

Panait and Voica 2017;

Comes et al. 2018;

Raluca 2017;

Iacovoiu 2018;

Islam et al. 2020;

Djokoto 2021;

Hysa and Mansi 2021;

Jushi et al. 2021). This has been a topic of interest since Adam Smith, but one of the first studies to stand out regarding this topic is that of

Ohlin (

1933). According to Ohlin, these investments are motivated not only by the opportunity for higher profits, but also to overcome trade barriers and provide resources. The increase in FDI during the 1980s and 1990s motivated more studies on its determinants and the policy measures that make it attractive to developing countries. Although the world suffers from different crises, the impact on FDI causes these studies to focus on special cases for different countries, and different groups of countries.

Researchers such as

Dorneana et al. (

2012) and

Popescu (

2014) investigated the relationship between the 2008 financial crisis and FDI in central and eastern European countries, and concluded that there was a statistically significant negative effect, where other gaps and more opportunities for empirical analyses were introduced and found to be motivating.

Gherghina et al. (

2019) focused their research on 11 central and eastern European countries to analyze the relationship between FDI and economic growth, taking into account the contribution of foreign capital to the achievement of several Sustainable Development Goals. The period of analysis was 2003–2016, and the results of the study demonstrated the existence of a non-linear relationship between FDI and gross domestic product per capita.

The report of

IMF (

2020) on the World Economic Outlook reflected a 4.9% decrease in global growth, projecting a 5.4% decrease for 2021. A worse-than-expected deep downturn was observed among all advanced economies. The labor market took a big hit, when comparing Q1 of 2020 with Q4 of 2019: global working hours showed a loss of 130 million full-time jobs (

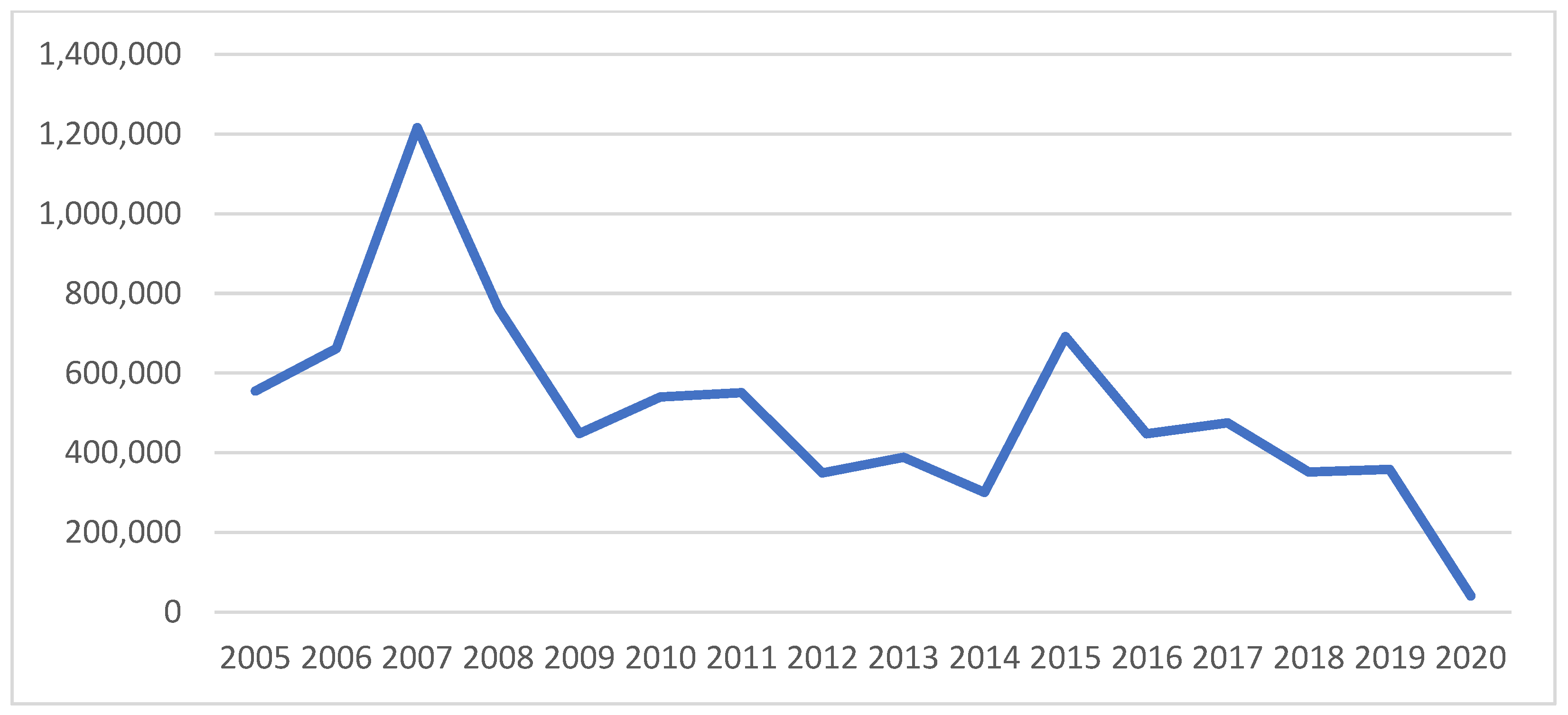

ILO 2020). FDI in 2020 registered a drop of 35% compared with 2019, which represented a more severe fall than the last crisis, i.e., FDI returned “back to the level seen in 2005” (

UNCTAD 2021a). The trend of the FDI flows outward during 2005–2020 can be found in

Figure 1 as below.

The impact was higher on developed economies, where FDI fell by 58%, and much more moderate for developing countries, with only 8%. The most severe impact was registered in the first half of 2020, followed by a recovered trend based on cross-border mergers and acquisitions and international project finance deals. According to the same report, regional differences were significant, both with decreased levels and recovered dynamics. “FDI flows to Europe fell by 80%. The fall was magnified by large swings in conduit flows, but most large economies in the region saw sizeable declines” (

UNCTAD 2021b).

As mentioned above, this paper provides a study on the FDI outflows in the era of COVID-19, while analyzing the effect of this situation on their determinants and concretely providing evidence on European countries. Policymakers should be motivated to draft policies through economic recovery. Being one of the most studied topics, determinants of FDI remain important to bring it back into focus and to reanalyze their impacts. Through a literature review on the latest scientific studies, this paper aims to find the gap and give a contribution on valuable conclusions and recommendations through an econometric analysis based on a balanced set of panel data (secondary data) for 22 European countries: Austria, Belgium, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, The Netherlands, Poland, Portugal, Slovakia, Slovenia, Spain, and Sweden. Data collected from reliable sources such as “The Organization for Economic Co-operation and Development (OECD)” and “World Health Organization (WHO)” were on FDI outflows, inflation, interest rates, business confidence, coronavirus cases and deaths, unemployment, and GDP during the pandemic year 2020. The detailed analysis focused on the first three quarters of 2020 to identify the determinants and their vulnerability to shocks and to understand to what extent the policy measures promoted in 2020 and beyond have supported the robust recovery and resilience of FDI flows.

2. Literature Review

A large pool of studies focusing on FDI exists, which has been briefly reviewed by

Paul and Feliciano-Cestero (

2021), specifying the theories build on the impacts, determinants, and correlations with the development of their home country, and internationally. FDI theories explain why major companies choose to move production abroad, instead of producing in their home countries and engaging in international trade. Although most of the literature is focused on inward FDI, or inflows, there is a great importance to acknowledge the significance of FDI outflows, their determinants, and the impacts on home countries. Internationalization theory, which was primarily presented by

Hymer (

1976), and later more briefly analyzed by

Buckley and Casson (

2009), analyzes and presents the advantages of FDI outflows of the home country, as well as opening new doors for study.

The literature provides a wide range of studies on the determinants of FDI. Studies even date from 1933, as mentioned above, while other studies have continued the empirical analysis of the determinants, such as those of

Goldsbrough (

1979);

Schneider (

1985);

Tsai (

1994);

Loree and Guisinger (

1995);

Gastanaga et al. (

1998);

UNCTAD (

2002);

Demirhan and Yılmaz (

2015);

Phung (

2016), etc. Through the review of these studies, the general determinants of FDI can be summarized. There are several notable groups of these determinants, such as those presented in the study by

Imeraj (

2018): market size, which includes macroeconomic stability and market openness; labor force factors, including costs and rates; infrastructure of the host country; political stability; natural resources; economic growth, where variables such as GDP growth or GDP per capita are included; and financial development (

Mansi et al. 2020) as another branch of determinants, including policies, taxes, and different rates.

Nevertheless, the literature is still filling the gaps of analysis and evidence regarding the main determinants of FDI outflows, which are intrinsically related to the home country.

The study by

Tolentino (

2008) gave importance to the determinants of FDI outflows of China and India, by specifying them in a more macroeconomic nature. Through econometric analysis, the study aimed to prove that determinants such as income per capita, openness of the economy, interest rates, and technological capacities are significant for the level of FDI outflows. However, the conclusions were not as expected; for the case of China, there was no proven significant cause of FDI outflow levels from macroeconomic determinants, whereas in India, technology was most significant; however, most importantly, there was a Granger causality proven between FDI outflows and interest rates. Another study of FDI determinants has especially tested the inflation rate effect on FDI in Sierra Leone. Based on time-series data,

Faroh and Shen (

2015), through an econometric model, concluded that openness and exchange rates are significant and can determine FDI, whereas variables such as inflation, GDP, and interest rates did not prove to be significant determinants of FDI in Sierra Leone. However,

Hysa and Hodo (

2016) argue that a relationship exists between the FDI-to-GDP ratio and GDP growth, because the FDI-to-GDP ratio and GDP dynamics affect one another, ceteris paribus.

Belaşcu et al. (

2018) focused on the impact of FDI on the economic and social welfare of countries from central and eastern Europe that are members of the European Union. The researchers used a panel methodology and implemented various panel specifications, taking into account the particularities of the relationship between FDI and economic growth among the five countries selected. The conclusions of the study suggested that FDI has “a positive contribution to economic growth, together with capital and, to some extent, international trade size, but also that country and period idiosyncrasies matter for a better understanding of economic growth determination” (

Belaşcu et al. 2018, p. 35).

Rjoub et al. (

2017) focused their scientific research on the determinants of FDI for “landlocked countries” in sub-Saharan Africa over the period 1995–2013. The results of this study demonstrated that variables such as trade (openness), natural resource endowment, market size domestic investment, and human capital have positive and significant impacts on FDI flows received by these countries.

Saini and Singhania (

2018) investigated FDI determinants for 20 countries (11 developed and 9 developing) on panel data and concluded that the main FDI determinants for developed countries were GDP growth, trade-openness, and freedom index, whereas in developing countries, FDI was positively correlated with economic variables such as gross fixed capital formation (GFCF), trade openness, and efficiency variables. Following the comparison study of FDI determinants in developing and developed countries, the later study by

Sabir et al. (

2019) should be mentioned as well, which investigated institutional quality as a key determinant of FDI for different economies with different income levels. Through the GMM system, the study found out that first, the institutional quality positively affects the FDI flows in developed countries and is more important compared with developing countries. Furthermore, the control of corruption, government effectiveness, political stability, regulatory quality, rule of law, and voice and accountability reflect a higher coefficient of FDI.

Developed economies are the first to take advantage and benefit from FDI outflows (

Knoerich 2017), especially regarding their growth (

Herzer 2010) which leads to one of the primary determinants. Macroeconomic determinants are the first to be identified as related to and influencing the FDI outflow. Among the macroeconomic determinants, the growth or GDP, market size, inflation, and the labor force (employment or unemployment) appear to have impacts (

Stoian 2013); (

Buckley et al. 2007); (

Tolentino 2008); (

Kayam 2009). If the growth and GDP per capita of an economy is high or rapidly increasing, this indicates a higher potential and even more attractiveness for FDI inflows, but especially the higher propensities to save and invest motivate FDI outflows as well. However, considering the interest rates, high rates would probably motivate investors to invest in their home countries, whereas the contrary is expected if the rate is low, which would impact the outflow of investments. The labor force is a driving determinant as well, considering the impacts on investment decision making, because it directly deals with its costs and abilities.

What has to be emphasized is the moderately low analysis of home country determinants on FDI outflows rather than host country determinants, as broadly studied and reviewed (

Zhang and Daly 2011); (

Liu et al. 2005); (

Tolentino 2008). Home country institutions and policies also determine the level of FDI outflow to some extent (

Luo et al. 2010); (

Buckley et al. 2007); (

Salehizadeh 2007); institutional and political transparency and economic freedom positively affect the FDI outflows. Outflows and business confidence are considered advantages which present an opportunity for investors or multinational firms to enlarge their investments abroad. The geographical position (

Kang and Jiang 2012), exchange rate (

Goh and Wong 2011); (

Onyeiwu 2011); (

Tolentino 2010) are hypothesized to be significant determinants of the FDI outflow. The exchange rates are related to the interest rate, and as also defined in the macro theories, these are negatively related to the FDI outflow; a higher exchange rate would depreciate the domestic currency, lowering the outflows of FDI as a result (

Onyeiwu 2011).

By the end of 2019, the main focus of researchers was the impact of COVID-19, which has already been studied in some perspectives, even related to FDI determinants (

Horobet et al. 2020;

Khan et al. 2020;

Bilal et al. 2021). The pandemic crisis generated by COVID-19 is a black swan event that has had a dramatic impact on the global economy, generating numerous threats for companies, but also business opportunities, determined by paradigm shifts that affect the activity of different entities on economic, social, and environmental levels. Resetting business and consumer behavior is the new reality generated by this black swan (

Czech et al. 2020;

Gigauri 2021).

The latest studies related to FDI flows and the COVID-19 period focus on the analysis of the impact of this crisis on the determinants and level of FDI flows. During the pandemic, developing and developed economies had to enforce lockdowns and social distancing measures, which had an immediate negative impact on supply chains and unbalanced all economies around the world (

Khan et al. 2020).

Ajide and Osinubi (

2020) studied FDI outflows during the COVID-19 pandemic, gathering preliminary empirical evidence. Their study focused on 43 countries, and through ordinary least squares (OLS) and quantile regression analyses, proved the positive relationship between FDI outflow and the confirmed COVID-19 cases and deaths. However, the propensity to invest was proven to negatively affect most of the economies considered in the study.

The effects of COVID-19 were analyzed from another point of view regarding their relationship to developed economies, as mentioned in the study by

Antonietti et al. (

2020), on countries with a more central position in the global production network. They investigated whether these countries had a higher number of infections and mortality rates through analyzing the data of 28 EU countries. Even though this study did not directly analyze the determinants of FDI, the conclusions provide evidence that countries with a central function in the global production and supply chains had greater susceptibility to the infection and death of their people. This relationship is driven by many sectors, such as business machinery and equipment, business services, real estate, textiles, tourism, and transport industries.

In May 2020, the OECD published a study of FDI flows in times of COVID-19, providing the data and trends; there have even been scenarios published concerning future developments (

OECD 2020). It can be observed that the factors differentiating the economies and FDI motivations provide information on how much COVID-19 affects them. A sure fact is that there will most probably be a diversification of the investment sectors or geographic positions, which might decrease some FDI flows in some countries and increase them in others. The shock of demand of the firms operating in the energy sector may negatively impact FDI which is oriented from sources of the host country, whereas some other promising FDI sectors might be those of knowledge-seeking. Multinational enterprises might diversify their supplier networks to increase flexibility to location-specific shocks.

The prolongation of the pandemic and its manifestation in waves has forced states to adopt; thus, economic recovery started in the second half of 2020, with the business environment adapting to the new conditions of increased uncertainty related to the duration of the pandemic, shifting growth predictions (

UNCTAD 2021b;

Barklie 2021).

Studies in the literature have strongly approved the advantages of FDI outflows from the home countries, also specifying their determinants and analyzing the crises impacts on them, which is important in the analysis of specific cases of the impacts of COVID-19 on FDI outflows and the significance of proven determinants during this period in the more developed EU economies. Analysis of the mechanisms of FDI outflows under specific crisis situations would obviously help inform and guide international trade policymakers. In this regard, this study developed two hypotheses to be tested:

Hypothesis 1 (H1). COVID-19 cases and/or COVID-19 deaths are correlated with the FDI outflows for EU countries.

Hypothesis 2 (H2). Determinants such as GDP growth, unemployment, interest rates, and inflation are still statistically significant for FDI outflows of the selected developed EU economies.

3. Outward FDI during the First Year of the Pandemic

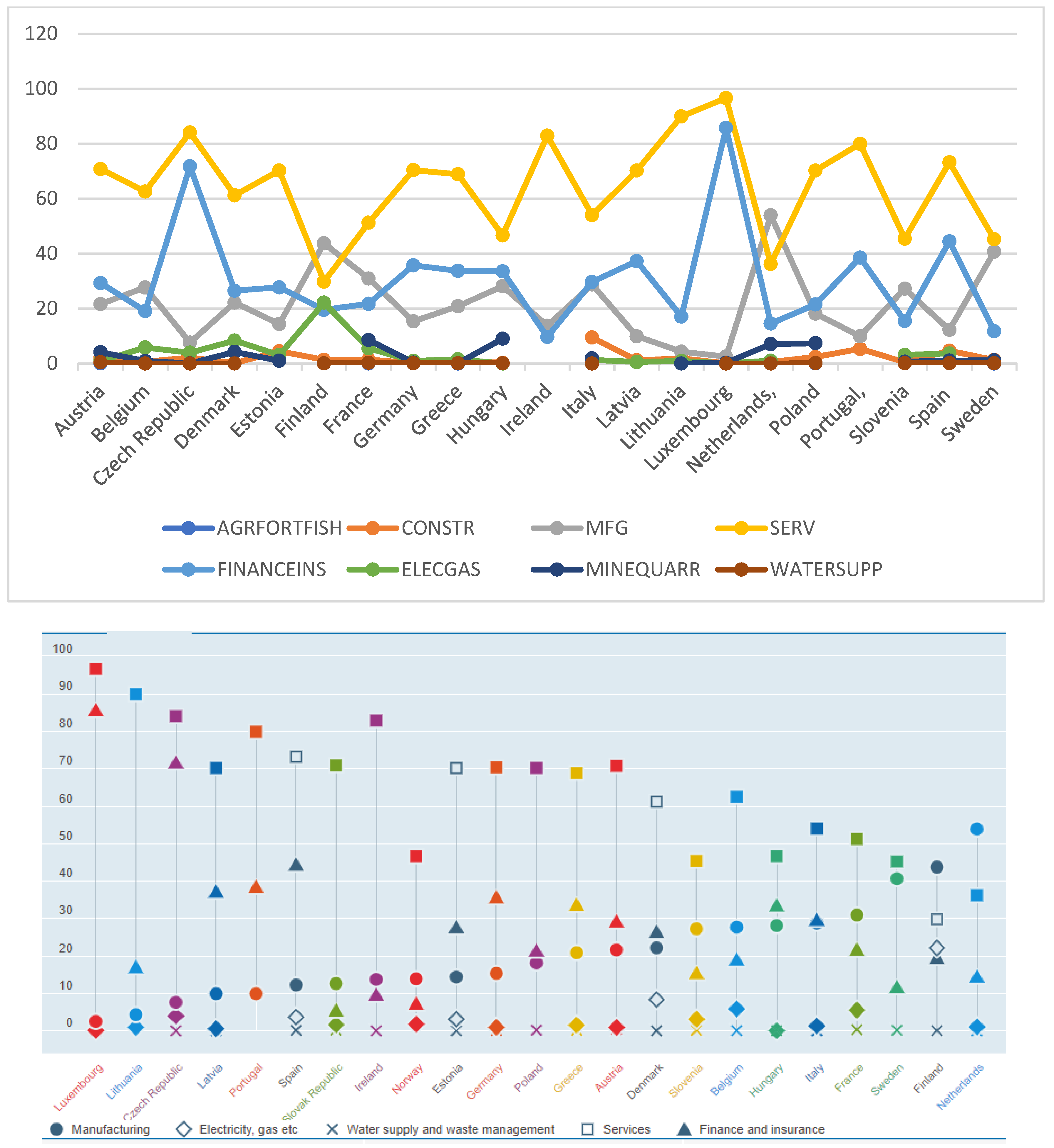

According to the OECD database, the FDI outward stock in the EU is dominated by the service sector, followed by finance and insurance, with significant differences between countries and industries.

Figure 2 shows outward FDI stocks by industry—manufacturing; electricity, gas, etc.; water supply and waste management; services; and finance and insurance—as a percentage of the total FDI, using 2019 data, or the latest available (2018).

From the perspective of the FDI stock, the evolutions are strongly determined by the policy of the countries of origin regarding the capital export, regarding the flows; these are influenced by the conjuncture of the business environment and by the shocks of the globalized economy.

Additionally, the interest of capital-exporting states, regarding the selection of geographical areas and the field of activity is different, with the influencing factors being extremely diverse, both from the perspective of policies but also of the opportunities specific to the host countries. Thus, the impact of the COVID-19 crisis on FDI flows was determined by the ability to adapt in the short term rather than by an investment strategy.

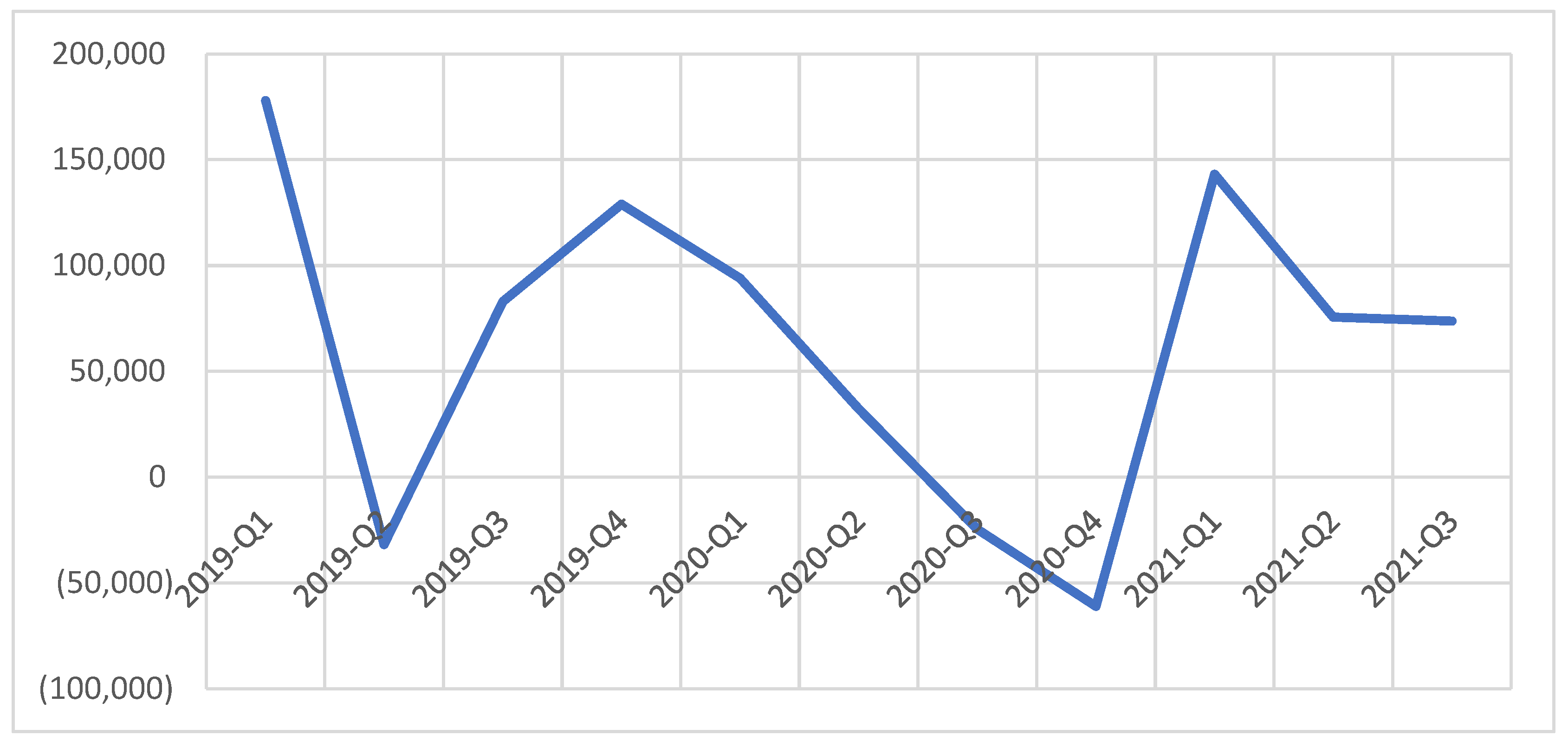

As experts have shown, FDI flows during the pandemic have evolved relatively chaotically, from a short-term protection policy for companies associated with the restrictions imposed by COVID-19, to a risk-taking trend associated with pandemic prolongation and uncertainty over its completion. Therefore, the evolution of flows was different over short time intervals:

- a-

In the first quarters of 2020, we witnessed general reductions in inflows, as a reaction to the period of generalized lockdown and then differentiated returns in different countries, depending on the incidence of COVID-19 and the severity of the effects measured by active cases and deaths;

- b-

The experience of repeating pandemic waves, with increased incidence and different severe effects, and the uncertainty of the end of the COVID-19 crisis, determined different reactions of companies and states, differentiated by industry/activity and from the perspective of resuming/relaunching medium- and long-term investment policies. There was also an “adaptation” and capitalization of opportunities, registering a return of flows after the third quarter, but the severity of the pandemic waves and their specific characteristics (Delta and later Omicron) determined an oscillating quarterly evolution in 2021, “with rebounded strongly, but the recovery is highly uneven” (

UNCTAD 2022). The details are shown in

Figure 3.

Detailing the analysis by country and field of activity (OECD, database 2022), the evolution of the data during the pandemic indicates a chaotic evolution rather than one based on measures of support policies for adaptation. We are witnessing changes in the approach to sustaining FDI flows, both from the perspective of countries of origin and those benefiting from FDI; the openness to a long-term and integrated vision of FDI effects, rather than one based on immediate benefits. Moreover, the conducted studies have highlighted not only the volatility of flows in times of crisis, but also the tendency to analyze the extensive and indirect effects of FDI flows on the business environment. In the case of FDI-exporting countries, whether they are more developed or less developed, the extended impact calls for a paradigm shift in public policy. According to previous developments, COVID-19 has affected countries and companies differently, depending on the national/regional context and FDI motivations, and “companies were already rethinking their supply chains in response to demands from consumers and companies for more sustainable and inclusive production methods” (

OECD 2021).

It is premature to estimate the time required for a resilient reconfiguration of FDI flows. The prolongation of the pandemic has reshaped policy measures, both in terms of areas of interest for investment and opportunities to expand digitalization, but also to reconsider analyses of their effects on the business environment, market competitiveness and efficiency, gains, and reinvestment rates.

Based on the experience of the previous financial crisis (2008–2009), but also of the evolutions in the first quarters of the pandemic (from 2020) to respond to the guidelines of robust and resilient recovery (defined by European Union countries’ recovery and resilience plans), the policies promoted by capital-exporting companies, as well as states, must address the main factors and influences of FDI flows. Hence, detailed analyses such as the one followed in our case study are significant. It should be noted that changing the thinking pattern on the complex impact of FDI flows must start from a periodic analysis of the determinants associated with external influences, such as the restrictions imposed by COVID-19. Here, we present the evolution of the first stage—forced adaptation, 2020—and continue the analysis with the addition of the year 2021, in quarterly evolution, when the uncertainty of the duration of the pandemic is associated with adapting the business model and reconsidering policies in the medium term.

4. Data and Methodology

Through the literature review, and especially focusing on the latest investigations, something is definitely needed: a study of the key FDI outflow determinants. Structural change, main sectors in focus, and diversification are occurring, and most probably, this COVID-19 era will once again highlight the determinants which absorb the highest positive possible impact on EU economies and develop resilient responses through redefining and consolidating international investment policies, based on international investment agreements, reform accelerators, and UNCTAD’s reform package. This makes this study important and necessary in the COVID-19 context. The research question of this study explores the main effects of the COVID-19 era on the determinants of FDI. Which of the effects remain statistically significant, and what should policymakers take into consideration for future policy changes or recommendations?

The hypotheses of this study are as follows:

H1. COVID-19 cases and/or COVID-19 deaths are correlated with the FDI outflows for EU countries.

H2. Determinants such as GDP growth, unemployment, interest rates, and inflation are still statistically significant for FDI outflows of the selected developed EU economies.

Determinants of FDI outflow, as studied and continuously analyzed by

Buckley et al. (

2007), are not always significant for selected countries. GDP growth, unemployment, interest rates, and inflation are among the macroeconomic determinants studied to be significant and correlated with national FDI outflows, despite their level of development (

Tolentino 2008;

Stoian 2013;

Liu et al. 2005;

Luo et al. 2010;

Zhang and Daly 2011). Under the situation of a lockdown and demand and supply shocks of all economies, the significance of some determinants of FDI outflows in question and the study of this relationship is important in regard to the policy changes that may apply to the more developed EU countries.

The main objective of this study is to bring back the determinants of FDI in the European countries and to analyze the impacts of the COVID-19 pandemic situation on them. To conduct such an analysis, a balanced set of panel data for 22 European countries, confined due to the availability of data, was created and used. The sample of this paper consisted of secondary data collected from reliable sources such as “The Organization for Economic Co-operation and Development” (

OECD 2021) and the “World Health Organization” (

WHO 2020b) and comprised quantitative data. This study dealt with quarterly data; specifically, its focus was on the first, second, and third quarters of 2020, and there were 66 observations in total. The chosen period was based on the availability of data.

Table 1 describes the data chosen for the empirical analysis of this study.

Based on the definitions provided by the OECD, outward FDI flows, or FDI outflows, are the value of outward direct investment made by the considered economy to external economies. FDI flows are measured in million USD.

Inflation is defined as the change in the prices of a basket of goods and services. Considering 2015 as the base year, inflation was measured by the consumer price index (CPI) in terms of the annual growth rate.

Short-term interest rates are the rates at which short-term borrowing is affected or the rate at which short-term government papers are issued. Short-term interest rates are generally averages of daily rates, measured as percentages.

The business confidence index provides information on future developments, based on opinion surveys on developments in production, orders, and stocks of finished goods in the industrial sector. Numbers above 100 suggest increased confidence in future business performance, and numbers below 100 indicate pessimism towards future performance. Data provided for business confidence are daily; therefore, the authors calculated quarterly data by taking the averages of daily rates.

The numbers of coronavirus cases and deaths have been confirmed and published by the WHO. Based on the daily reports, the authors calculated quarterly values for confirmed cases and deaths.

The unemployment rate is measured as the number of unemployed people as a percentage of the labor force, and is seasonally adjusted. The labor force is defined as the total number of unemployed people plus those in employment.

Quarterly GDP is based on real GDP, and it is measured as a percentage change from the previous quarter. To empirically test the relationships between FDI outflows, inflation, interest rates, business confidence, coronavirus cases and deaths, unemployment, and GDP during the pandemic, multiple regression analysis was used to derive regression equations and conclusions on the effects that the chosen explanatory variables have on the responding variables. The explanatory variables were inflation, interest rates, business confidence, coronavirus cases and deaths, unemployment, and GDP, whereas the responding variable was the FDI outflow. To ensure accurate results, FDI outflows and the numbers of coronavirus cases and death are expressed in logarithmic form, which tends to straighten out exponential growth patterns. White cross-section standard errors and covariance were used to eliminate heteroskedasticity and serial correlations. To avoid the multicollinearity problems that arise due to the strong correlations between coronavirus cases and deaths, two different regression equations were derived: one involving the number of cases, and the other involving the number of deaths. The multiple regression equations can be expressed as follows:

The basis of the regression model of this paper was adopted from

Ajide and Osinubi (

2020), who studied the relationship between FDI outflows and short-term interest rates, inflation, and coronavirus cases and deaths for the first quarter of 2020. However, this study focuses on three quarters of 2020 (Q1, Q2, and Q3), and it incorporates two more variables in the regression analysis: unemployment and quarterly GDP.

Specifically, log (FDIit) is the natural log of foreign direct investment outflows; COVID-19 Cases_i is the log of confirmed COVID-19 cases (CoCasit) or the log of confirmed COVID-19 deaths (CoDeait). Additionally, i is an indicator for each country, whereas ∂_1 is a constant. Furthermore, all other variables present control variables, and eit represents an error term.

Two widely known models can be used when working with panel data—the fixed effects model and the random effects model—which fall under the panel generalized least squares method. To determine which model is more appropriate, the Hausman test was performed. The Hausman test assumes that a random effects model is more appropriate than a fixed effects model, and based on its results, it can be seen whether such an assumption holds or not.

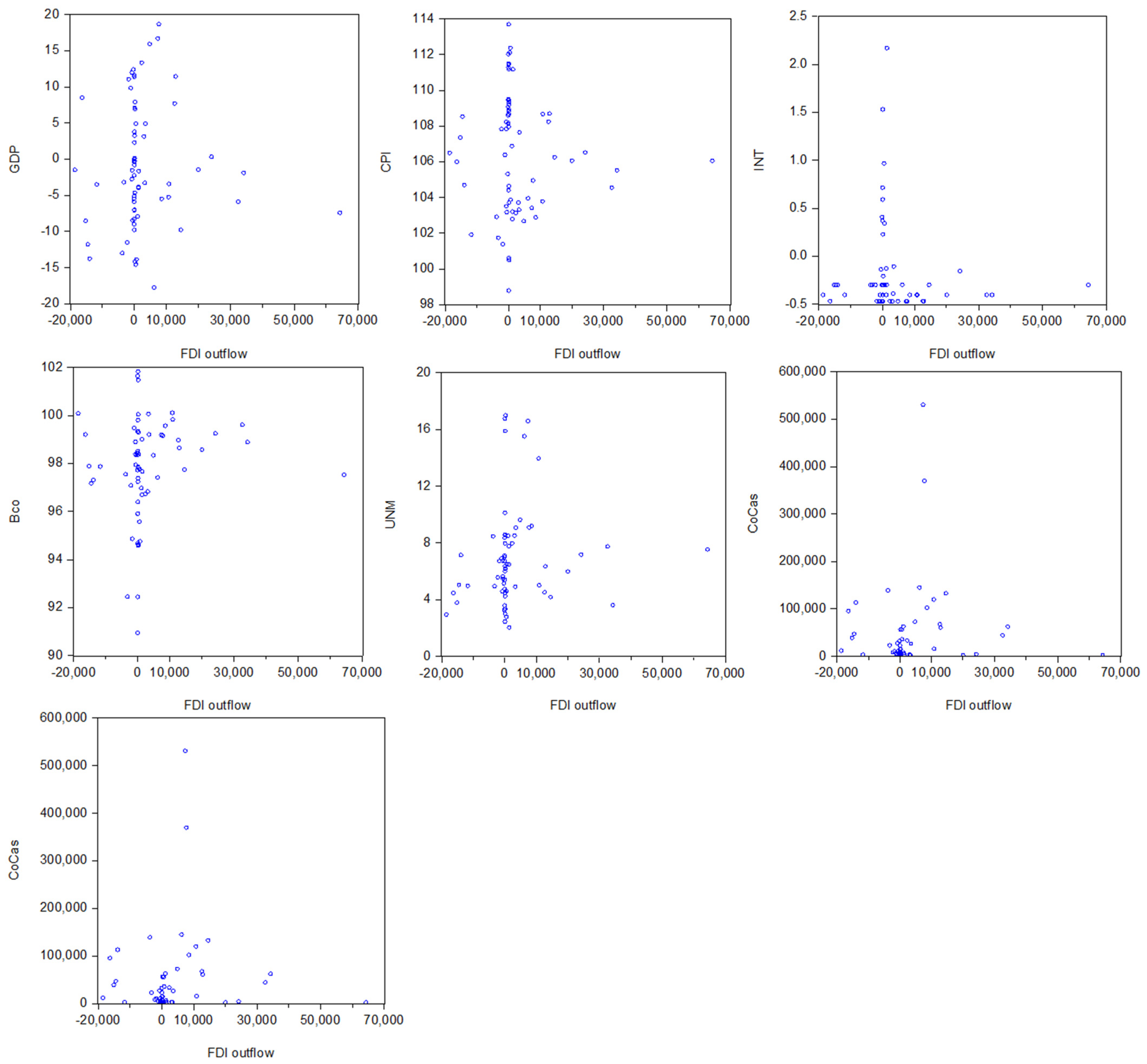

Figure 4 shows the scatterplot of FDI outflows with each variable. As observed, there were concentrated datasets for GDP, CPI, INT, Bco, and UNM. As per the other two variables, COVID-19 cases and COVID-19 deaths, the correlation with the FDI outflow seems to be a horizontal line, which is slightly positive.

5. Empirical Results

Referring to

Table 2, regarding FDI outflows, the chosen European countries had an average of USD 2865.93 million for three quarters of 2020. The highest value of FDI outflows was USD 64,339.98 million from Luxembourg in the second quarter of 2020, whereas the minimum value of FDI outflows was USD −18,529.30, from The Netherlands, recorded in the first quarter of 2020. The standard deviation was quite high, indicating that the data points were spread out over a large range of values. Considering unemployment levels, European countries had an average of 6.92% for the chosen period. The highest unemployment level was 16.96%, recorded in Greece in the second quarter of 2020, whereas the lowest recorded level of unemployment was 2.03%, in the Czech Republic for the first quarter of 2020. Based on the standard deviation, the data points were not clustered around the mean.

Table 2 shows the summary statistics of all variables before the regression analysis. Comparing the median and mean for each component, it can be shown that the values are close to each other. This supports the fact that the selected data for our model followed a normal distribution (

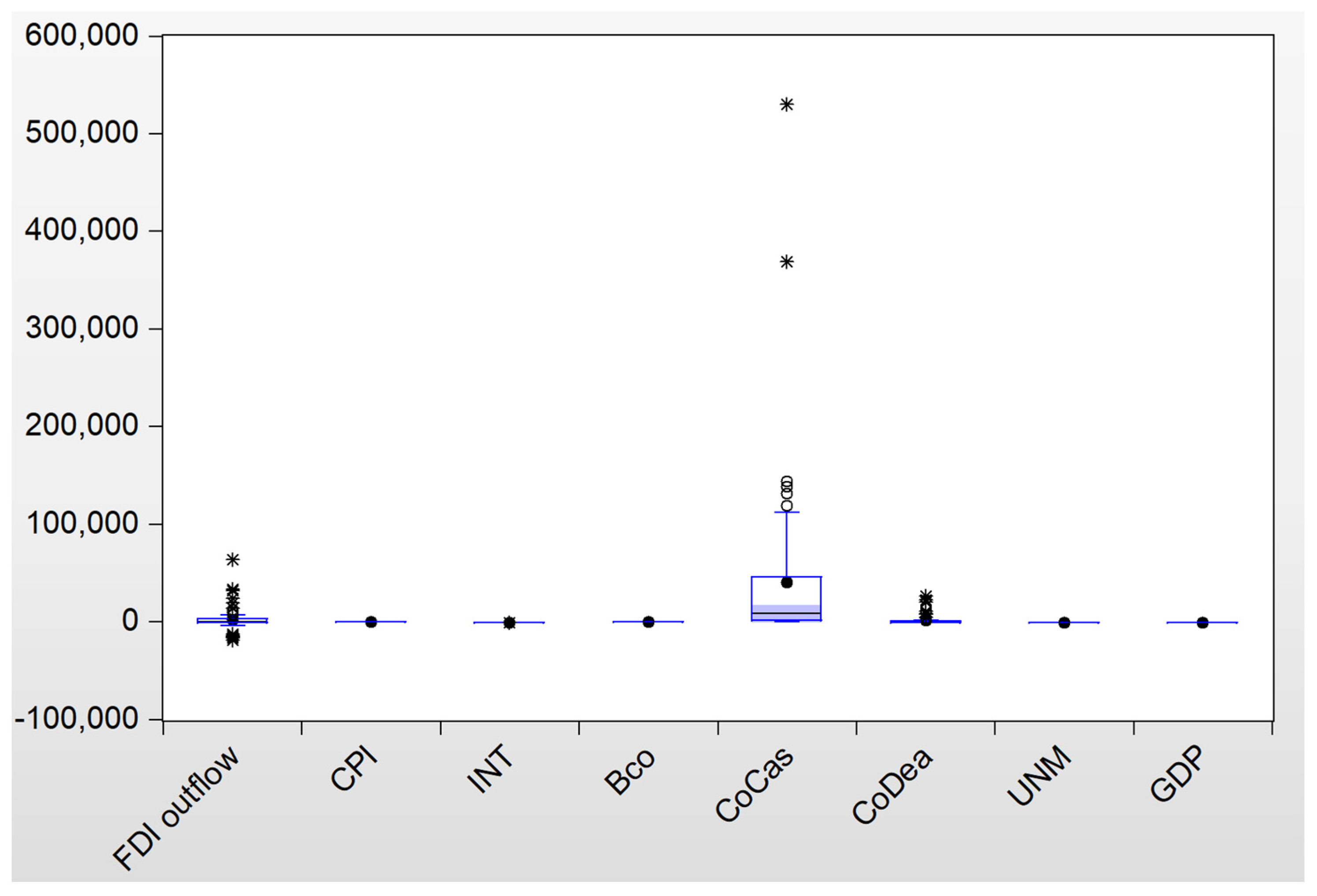

Hozo et al. 2005). For some additional information on the dataset, we have included the complete data in the boxplot (

Figure 5). The variables of FDI outflows, COVID-19 cases, and COVID-19 deaths exhibited outliers in their respective datasets. This is the reason we used logarithmic values for these three variables. As stated above, all these variables were normally distributed.

Regarding short-term interest rates, the average percentage for the chosen period was negative (−0.20%), whereas the highest interest rate was 2.17%, recorded in the Czech Republic in the first quarter. Estonia recorded the lowest interest rates (−0.47%) among European countries, in the third quarter of 2020. The standard deviation indicated that the interest rates were not spread out over a large range of values, but were clustered around the mean. Considering inflation rates, European countries had an average of 106.43% over the three quarters of 2020. The highest value (113.69%) was recorded in Hungary in the third quarter of 2020, whereas the lowest rate was 98.77%, recorded in Greece in the third quarter. The inflation rates were quite high, and the recorded values were clustered around the mean.

The reported numbers of coronavirus cases and deaths were spread out over a large range of values because countries have been hit differently by coronavirus. Spain recorded the highest number of confirmed cases, 530,314 in the third quarter of 2020, whereas the highest number of confirmed deaths was 26,713, recorded in France in the second quarter of 2020. In the first quarter of 2020, Slovakia had 336 confirmed cases, which was the lowest number of confirmed cases during Q1, Q2, and Q3; both Slovakia and Latvia had 0 cases of deaths in the first quarter of 2020.

Referring to the business confidence index, the highest index score was 101.8288, reached by Lithuania in the first quarter, whereas the lowest index score was 90.93180, recorded in the second quarter of 2020 for Estonia. The average score was 97.85150, whereas the standard deviations indicated that index scores were not very spread out, but clustered around the mean. Lastly, regarding the quarterly GDP, the average percentage for the chosen period was negative (−0.94%), whereas the highest GDP growth was 18.66%, recorded in France in the third quarter. In the second quarter of 2020, Spain recorded the lowest interest rates (−17.79%) among European countries. GDP growth rates were spread out over a large range of values.

Table 3 presents some more information on the multicollinearity using the correlation matrix of variables. For a better configuration of the regression model, we used the log for the following variables: LFDI = log (FDI outflows); LCODEA = log (confirmed COVID-19 cases); and LCOCAS = log (confirmed COVID-19 deaths). As expected, there was a strong positive correlation between confirmed coronavirus cases and deaths above the threshold level of 0.8, confirming the multicollinearity problem in this case. For this reason, in this study, two different regression equations were explored, one involving confirmed coronavirus cases and the other one involving confirmed coronavirus deaths. As suggested by the correlation coefficients, the other independent variables were not strongly correlated with each other. It seems there was a positive relationship between confirmed coronavirus cases and FDI outflows as well as between confirmed coronavirus deaths and FDI outflows; however, the regression equations presented more accurate results.

Regression Equations

Based on the results of the Hausman test, whose

p-values > 0.05, the random effects model was deemed more appropriate than the fixed effects model for both regression equations. As shown in

Table 4, the impacts of unemployment, inflation, log (confirmed coronavirus cases), business confidence, and quarterly GDP were significant at the 5% and 10% levels, because their respective

p-values were less than 0.05 and less than 0.1. The t-statistics suggest that each of the independent variables, except interest rates, had a statistically significant impact on the dependent variable. The adjusted R

2 suggests that for the chosen European countries, 19.2% of the variation in log (FDI) was explained by this model, whereas the probability (F-statistic) values were less than the 5% and 10% levels of significance (0.03 < 0.05 and 0.03 < 0.1), meaning that the overall model was statistically significant.

Referring to

Table 5, which shows the regression outcomes when log (confirmed coronavirus deaths) was taken into consideration, it turned out that in this case, along with interest rates, quarterly GDP did not have a statistically significant impact on log (FDI). The t-statistics suggest that the other independent variables had significant impacts on the dependent variable, because their respective

p-values were less than the 10% level of significance. Except for unemployment, whose

p-value = 0.0572, the other independent variables were significant at a 5% level of significance as well. The adjusted R

2 suggests that for the case of the chosen European countries, 19% of the variation in log (FDI) was explained by this model, whereas the probability (F-statistic) values were less than the 5% and 10% levels of significance (0.03 < 0.05 and 0.03 < 0.1), meaning that the overall model was statistically significant. It is important to emphasize that both log (CoCas), used in the previous model, and log (CoDea), used here, were highly significant.

6. Analysis and Discussion

Based on the models presented in the previous section, the multiple regression equations are as follows:

Considering both equations, it seems that unemployment had a positive impact on FDI outflows up to a certain point, and then its impact became negative, meaning that for high levels of unemployment, the impact of unemployment on FDI outflows was negative. Equation (1) indicates that up to a 5.75% level of unemployment, its impact on FDI outflows is positive, whereas above a 5.75% level of unemployment, its impact becomes negative. Equation (2), which takes into consideration the confirmed number of coronavirus of deaths, shows that up to a 7% level of unemployment, its impact on FDI outflows is positive, whereas above a 7% level of unemployment, its impact becomes negative. Specifically, when dealing with quadratic terms and contradictory signs, the turning point can be determined to be β

1/2β

2. In the chosen European countries, when the unemployment increased in low levels, the outflows of FDI increased as well, whereas when the unemployment reached high levels, it tended to decrease the outflows of FDI. In both cases, the impact was significant. These results are in line with other previous studies, such as those by

Kayam (

2009) and

Stoian (

2013). The research by

Crescenzi et al. (

2022) demonstrated that the “link between outward FDI and domestic local employment is generally positive” (

Crescenzi et al. 2022, p. 75).

Even though we found that the impact of short-term interest rates on FDI outflows was positive, meaning that an increase in short-term interest rates tended to increase the outflows of FDI, this variable was found to be insignificant. The study by

Hsieh et al. (

2019), analyzing a period back to 1994, focusing on the U.S. economy, revealed that “GDP growth and the interest rate, however, do not produce significant results” (

Hsieh et al. 2019, p. 386) on outward FDI.

The impact of inflation on FDI outflows was negative in both equations, meaning that an increase in inflation rates tends to decrease the outflows of FDI, supporting the findings of other researchers (

Buckley et al. 2007;

Kayam 2009;

Stoian 2013). In the first case, a 1% increase in inflation rates, ceteris paribus, tended to decrease the outflows of FDI by 28%, whereas the second equation showed that a 1% increase in inflation rates, ceteris paribus, tended to decrease the outflows of FDI by 24%. In both equations, the impact of inflation on FDI outflows was significant; however, the impact appears to be higher in the first equation.

The coefficients of log (CoCas) and log (CoDea) showed positive and significant impacts on FDI outflows. A 1% increase in confirmed coronavirus cases, ceteris paribus, tended to increase the outflows of FDI by 0.43%, whereas a 1% increase in confirmed coronavirus deaths, ceteris paribus, tended to increase the outflows of FDI by 0.26%. Thus, in the chosen European countries, the coronavirus pandemic has increased FDI outflows. The impact of confirmed coronavirus cases appeared to be higher than the impact of confirmed coronavirus deaths.

In both equations, the coefficient of business confidence showed a positive impact on FDI outflows, meaning that the higher the business confidence level, the higher the outflows of FDI. Equation (1) indicates that a 1 unit increase in business confidence, ceteris paribus, tended to increase FDI outflows by 31%, whereas according to the second equation, a 1 unit increase in business confidence, ceteris paribus, tended to increase the outflows of FDI by 36%. In both cases, the positive impact of the level of business confidence on FDI outflows was significant; however, this impact appears to be higher in the second case.

Considering both equations, the outcomes related to the impact of GDP growth on FDI outflows are contradictory. In the first equation, the impact of GDP growth on FDI outflows appeared to be negative, whereas in the second equation, this impact was positive. In the first case, a 1% increase in GDP growth, ceteris paribus, tended to decrease FDI outflows by 2%, whereas the second equation suggested that a 1% increase in GDP growth, ceteris paribus, tended to increase FDI outflows by 0.7%. In the first equation, the negative impact was statistically significant, whereas in the second equation, the positive impact was not statistically significant.

Both regression models had nearly the same explanatory power and they were statistically significant. The chosen independent variables had the same impact directions, except for GDP growth, whereas the magnitude of these impacts was different in these regression equations. In general, the independent variables in the first equation had higher impacts compared with the second equation.

The empirical analysis showed that both COVID-19 cases and COVID-19 deaths were correlated with the FDI outflows for EU countries; hence, the first hypothesis stated in this paper can be accepted. The results of this study are in line with the work of

Ajide and Osinubi (

2020).

Ajide and Osinubi (

2020), who analyzed 43 countries from 1 January to 31 March 2020, demonstrated that “there is a positive impact of COVID-19-related confirmed deaths on FDI outflows” (

Ajide and Osinubi 2020, p. 79). The second hypothesis was partially accepted, because the empirical analysis suggested that determinants such as unemployment and inflation were statistically significant for the FDI outflow of the selected EU economies, whereas interest rates were not statistically significant. Although the GDP growth was statistically significant from the first equation, it was not from the second one.

7. Conclusions and Recommendations

Foreign direct investment has been widely studied as an element impacting economic growth and dramatically affecting every market economy. Initially seen as a panacea that could fuel the process of economic development, foreign direct investment generates negative externalities in host countries, which is why public authorities must develop and promote specific tools to capitalize on the potential of foreign companies. Foreign direct investment is a positive source of economic growth for countries, but also creates a link between the country of the origin and destinations, which “helped” develop the contagious phenomenon of COVID-19. This paper aimed to provide a study on FDI in the era of COVID-19 and concretely provide evidence on European countries; thus, the econometrical analysis used random effects models to study the relationships between FDI, its known determinants, and COVID-19.

Overall, based on the empirical results, it appears that COVID-19 has fueled FDI outflows. Unemployment had a positive impact on FDI outflows up to a point, and then its impact became negative. Additionally, increases in short-term interest rates tended to increase the outflows of FDI, whereas higher business confidence increased FDI outflows as well. GDP growth appears to have had a positive impact on FDI outflows; however, when considering coronavirus deaths instead of cases, this impact became negative. Finally, an increase in inflation rates tended to decrease the outflows of FDI. Based on the outcomes of the empirical results and analysis, the first hypothesis of this paper can be accepted, whereas the second hypothesis is only partially accepted because the impact of short-term interest rates was not statistically significant. The results are similar to those of

Ajide and Osinubi (

2020), who argued that COVID-19 has affected the attractiveness of most economies, forcing multinational companies to relocate their investments. Additionally, the reduction in financial resources and the short supply of manpower has boosted FDI outflows.

The enforced lockdowns for COVID-19 induced aggregate demand and supply shock, which has generated a domino effect on all sectors of the economy, including FDI. FDI outflows are “both a cause and a consequence of economic growth and the long-run causality is bidirectional”. According to

Herzer (

2010), governments should take the necessary measures to uplift the confidence of foreign investors during difficult times. The positive effects of firms’ foreign investing spread to the whole economy through their supply chains, with a wider effect both at micro and micro levels. Moreover, “policies that increase outward FDI will contribute to enhancing economic growth both abroad and at home” (

Hayakawa and Matsuura 2017). Even this study showed that increasing business confidence by 1%, ceteris paribus, tends to increase FDI flows by 31%. Based on the availability of data, this paper dealt with 22 European countries for Q1, Q2, and Q3 of 2020. Data for all chosen variables were not available for the fourth quarter (Q4); therefore, this period was not taken into consideration, which represents a limitation of this study.

The COVID-19 pandemic has caused a reconfiguration of financial flows, but also of international supply chains, with more and more companies being in a complex process of rethinking their business strategies in the context of intensifying digitalization and increasing regionalization. In this way, transnational corporations will seek to bring vulnerabilities back to external shocks generated by black swan events.

This study had some limitations. We tried to assess the first impacts of COVID-19; therefore, we wanted to address the issues for Q1, Q2, and Q3 of 2020. As such, there is a limitation of the number of observations, and also in the inclusion of all EU countries, due to the limited data available for that period. Another limitation might be the exclusion of FDI inflows from the model. The main reason was to be focused on outflows and to find the barriers and the supporting variables for FDI. Nevertheless, for future studies, we suggest expanding the dataset and adding some more control variables that will help to highlight the impact on FDI.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}