1. Introduction

Public sector undertakings (PSUs) are not mere profit-maximizing economic units but a thread that seamlessly ties together the social fabric, forms the cornerstone of economic development, and facilitates self-reliance (

Pollitt 2017). Consequently, the performance measurement and management of PSUs assume paramount importance. However, ambiguous objectives (

Pollanen 2005), lack of robust governance structures (

Almqvist et al. 2013;

Hughes 2017), and ineffective control systems in PSUs (

Burkert et al. 2011) have been causes of concern for researchers and practitioners alike. These chronic causes called for ‘new’ public management practices (

Hood 1991).

New public management (NPM) started to gain currency in Asian markets in the aftermath of the 1997 Asian financial crisis. Widespread reforms in terms of privatization, ‘agencification’, decentralization, and performance management were observed across Asian countries, such as Indonesia, Japan, Malaysia, China, etc. (

Koike 2013).

Though, owing to the limitations of NPM, particularly those related to the effectiveness of governance (

Christensen and Laegreid 2007), post-NPM reforms came into being. Post-NPM reforms improved governance repertoire by providing governance frameworks to govern inter-organizational actions more effectively (

Christensen 2012). It also led to the emergence of ‘New Public Governance’ (NPG) (

Almqvist et al. 2013). Core of these propositions is a greater emphasis on common values, the increased involvement of PSUs, and the provision of general frameworks for self-governance to improve cooperation in regard to public goals (

Ling 2002;

Nabatchi et al. 2010;

Sørensen and Triantafillou 2009). Yet, a few emerging economies (‘unfamiliar diners’) (

Turner 2002) such as India failed to take cues from these reforms and continued to bear the burden of loss-making and inefficient Public Sector Undertakings (PSUs) (

Ramaswamy and Renforth 1996).

After independence, India pursued the path of development in which the public sector would play a vital role. Unfortunately, public sectors manifested themselves into loss-making enterprises with low-capacity utilization, overcapitalization due to severe cost overruns, and an inability to innovate and compete with global players. Rather than augmenting government resources, PSUs started to become a cost center consuming capital resources for their survival (

Khumawala 1997). With increasing constraints on resources and budgets, the Indian government has finally begun to ‘divest’ the so called state-owned ‘assets’, which have become more of a ‘liability’.

The Indian government started disinvestment in the public sector in 1991, and the amount of disinvestment has been steadily increasing. Initially, the private sector did not find it attractive to invest. Between 2001–2004, there was disinvestment worth

$2.8 billion US

$. This was possible due to a change in stance of the government policy by going for strategic sales with either transfer of control or sale of stake to the public, but still retaining control of the management. Companies noteworthy to be mentioned during the period include India Tourism Development Corporation Ltd. (ITDC), New Delhi, India; Modern Food Industries (India) Ltd. (MFIL), Gurgaon, Haryana, India; Paradeep Phosphates Ltd., Bhubaneswar, Odisha, India; Hindustan Zinc Ltd., Udaipur, Rajasthan, India; Bharat Aluminium Co., Ltd., New Delhi, India, etc. The public offer of Life Insurance Corporation (LIC) Ltd. and sale of the ailing national carrier Air India to the Tata Group is one important milestone towards privatization. From 2016 and 2017 and 2020 and 2021, the government of India collected over US

$36 billion from the sale of stake in public sector undertakings (

http://www.bsepsu.com/historical-disinvestment.asp accessed on 24 February 2022).

The importance of PSUs in one of the prominent Asian economies, i.e., India, cannot be overemphasized (

Büge et al. 2013). Indian PSUs have a complete monopoly in nuclear power generation. Indian PSUs also have a major market share in the coal, petroleum, power generation, telecommunication, and fertilizer sectors besides strong international presence (

KPMG 2012). In 2014 and 2015, the PSU sector had a gross turnover of US

$261.62 billion in comparison to US

$270.81 billion in 2013 and 2014, showing a decrease of 3.4%. Along the same lines, the profit of PSUs also showed a fall of 12.9% from US

$19.61 billion in 2013 and 2014 to US

$17.1 billion in 2014 and 2015. Amongst the various sectors, PSUs from petroleum (refinery and marketing), coal, crude oil, steel, electricity (power generation), and trading and marketing services contributed the most to the country’s GDP. In view of the magnitude of PSUs in terms of their overall contribution (not limited to employment and development) to the Indian economy, it seems imperative to take all necessary steps to improve their performance (

Mansi et al. 2017). They are the building blocks of the Indian economy and play a vital role in the country’s socio-economic development (

Mansi et al. 2017). As government-owned enterprises, these organizations have additional commitments for economic and social well-being; these commitments need to be reflected in their risk-taking (

Mishra 2011), decision-making, and governance structures.

Further, companies’ responsibility for their direction and supervision ultimately vests with the board (

Shleifer and Vishny 1997). Like most Anglo-Saxon countries, India has a system of one-tier boards (

Van Thiel 2015). However, owing to the presence of non-executive members, these boards seem to have a mixed combination (type I and type II) (

Van Thiel 2015). These boards assume greater importance as they are one of the instruments that principals can use to monitor the agent’s performance (

Beasley et al. 2006). In addition, the view based on stewardship theory highlights the role of the board as a partner to help improve the organization’s performance (

Davis et al. 1997). Further, in the democracy perspective, the board represents society and the general interest. Another model based on stakeholder theory assumes that board members represent specific interests. In the most widely acknowledged model, board members are nominated to help the organization by importing knowledge, contacts, and other important resources that the organization can use to further its goals (

Cornforth 2003). Accordingly, the quality of governance structure appears to be a pertinent factor in the performance management of PSUs (

Van Thiel 2015). It is essential to have a governance structure that not only exudes integrity, fairness, impartiality, and expertise (Higgs Report (

Higgs 2003)) but is also diverse, independent, and pragmatic (

Davies Report 2011). Recognizing the significance of robustness of governance for efficient performance management, we suggest a governance index for the quality of governance structure.

Further, in view of the strategic importance of PSUs in the Indian economy, it appears pertinent to have a comprehensive measure of their risk levels, which can serve as a guide in their performance measurement and management (

Power 2004). Therefore, the paper puts a risk index to gauge the exposure levels of companies, which has been tested and validated using the data of Indian PSUs. In the process, it was observed that a few Indian PSUs have contingent liabilities to the tune of 510 million US dollars. Being an off-balance sheet item, they are often neglected, but if materialized, they could jeopardize the operations and endanger the very survival of the firm. As a result, a new ratio has been developed in the paper to deal with contingent liabilities. Similarly, the defensive interval ratio tends to neglect the interest obligations, but Indian PSUs tend to be highly leveraged, and as such, a ‘modified defensive interval ratio’ is warranted and has been put forth in the paper.

Based on diff-GMM regression, the empirical evidence suggests that PSUs that do well in terms of indices perform better and are able to generate higher returns. Specifically, when risky PSUs have better governance structures (as per the governance index), they tend to be more efficient in the use of their resources. Such results lend credence to the indices suggested in the study. Accordingly, these indices may serve as benchmarks for performance evaluation, facilitate identification of critical areas, aid the auditors, and may serve as reference points for regulators to develop a Basel-like framework for PSUs. In addition, the quality of governance structure, as demonstrated by the governance index, may be taken as a signal of efficiency, accountability and transparency exercised in the PSU (

Alexius and Örnber 2015).

In the next section, a theoretical discussion of the performance management of PSUs is presented. In the

Section 3, both indices have been developed, followed by a description of data and methodology. Empirical analysis and discussion have been presented in subsequent sections. Finally, the paper concludes with implications and scope for future research.

2. Theoretical Discussion

The efforts to ‘reinvent the public sector’ led to the emergence of New Public Management (NPM). NPM primarily revolves around performance management practices (

Hood 1991). These practices mainly include goal setting, decision rights allocation, and performance measurement and evaluation. However, the movement to improve the performance of PSUs started to gain momentum in the early 2000s (

Fryer et al. 2009). The effects were apparent across the globe, though in varying degrees. Yet, an emerging economy like India, which was founded on the principles of a mixed economy (

Jain et al. 2014), did not join the movement and is now finding its PSUs in the doldrums (

Gupta et al. 2014) and is awaiting a reform.

The first and foremost step in performance management is performance measurement (

Swiatczak et al. 2015). Though the use and quality of performance indicators have been evolving (

Kennerley and Neely 2002;

Johnson 2005), ‘devising good indicators of quality is still hard’ (

Zineldin 2006). Initially, financial indicators were more prevalent, but gradually other indicators (e.g., quality) were introduced. This has led to a proliferation of indicators (

Modell 2004;

Carlin et al. 2004) but not always an improvement in the quality of the indicators themselves (

Lemieux-Charles et al. 2003). As a result, there are four types of indicators: output based, welfare based, performance based and composite indicators that combine all three (

Stevens and Zimmerman 2006). Further,

Macpherson (

2001) states that the most useful numbers are those pertaining to planning, prediction, and budget.

Several authors have proposed various frameworks to assess organization’s activity, few being performance prism (

Neely and Adams 2001) or the Balanced Scorecard (

Kaplan and Norton 1996).

Rouse and Putterill (

2003) provide a critique of these frameworks and outlines an alternative framework consisting of multi-dimensional views and evaluation frameworks to reflect the variety of stakeholders. However, there is no single framework that suits all organizations (

Pun and White 2005). Further, choosing an inappropriate measure may lead to goal-incongruence and exploitation of organizational resources (

Alexius et al. 2014).

It is in this context that

Rangan (

2004) and

Kaplan (

2001) advocate that goal clarity and measurability of results are of foremost importance to preventing the diffusion of organizational energy. Effective programs and their efficient implementation could be achieved by focusing on controls, i.e., focusing on either output controls, action controls, or clan controls or a mix of these. Output-based controls or performance measurement have been a subject of great debate, resulting in a shift towards outcome-based measures (

Guthrie and English 1997). Despite this shift, the ambiguity in objectives remains a cause of concern (

Pollanen 2005), and that is what precisely needs to be addressed.

Post-NPM reforms attempted to address a few of these concerns by suggesting different governance modes that are believed to have improved the effectiveness of governance in PSUs. A few of those governance models are ‘Neo-Weberianism’ (

Pollitt and Bouckaert 2011), ‘joined-up government’, and ‘whole of government’ (

Christensen and Laegreid 2007,

2011b;

Stoker 2006). The post-NPM era heralds integration, coordination, and cooperation. New governance mechanisms based on self-governance modes, thus seek to create a strong and unified sense of values and goals to enhance engagement and commitment of all involved parties to contribute to public-task fulfilment (

Frost and Morner 2011;

Sørensen and Triantafillou 2009). Post-NPM approaches create governance frameworks that foster decentralized steering and mutual monitoring. This new approach help the managers of PSUS to foster their problem-solving and self-steering capacities (

Sørensen and Triantafillou 2009;

Wälder and Morner 2013).

Though there is a plethora of literature on boards, most studies relate to boards in private organizations (

Jegers 2009), however, little is known about governance structures in PSUs (

Hinna et al. 2010;

Cornforth 2011). Most of the studies have focused on the composition, size, and diversity of boards and the effects thereof on the performance of the organization (

Huse 2007). The few studies that have examined boards of PSUs have primarily looked at specific aspects like the accountability, particularly in relation to the role of regulatory authorities before and during the financial crisis, the application of governance codes, and the remuneration of board members (

Hinna et al. 2010;

Cornforth 2011). Special aspects like the appointment of politicians are sometimes studied as well, under the heading of patronage (

Van Thiel 2012). However, importance and role of the board or governance for performance management in PSUs remain an under-researched area. It is in this background that few Asian countries have now begun the ‘institutionalization’ of performance management, yet most governments attempt to apply ‘result-based management’ (

Koike 2013).

The problems associated with performance management are more profound in developing economies, such as India, due to lethargic bureaucracy, patrimonial culture (

Koike 2013), red-tapism, and nepotism. Therefore, several researchers have attempted to examine the performance of Indian PSUs, particularly Central PSUs.

Singh and Chittedi (

2011) observed a significant improvement in the performance of PSUs in the post-liberalization era. Similarly,

Gupta et al. (

2011a) noted a significant improvement in the performance of PSUs that entered a Memorandum of Understanding with the government. In contrast, disinvestment did not lead to desired outcomes (

Gupta et al. 2011b). Interestingly,

Ramamurti (

1987) documents that most Indian PSUs consider commercial profitability as the measure of their success. He observed that the profit motive in India was stronger than in countries with mixed enterprises or which are more right-winged.

Müller (

2000) suggests that the under-performance of PSUs may be attributed, to a marked extent, to the entailing complex governance structure. The complications are intensified with the interference of the government (

Simpson 2014). For instance, the top three Indian PSUs accounted for 74.35% of the total loss of all PSUs in 2011–2012. These companies have been incurring losses consecutively since 2009. A survey by

Gupta et al. (

2011a) leads to a recommendation that directors of PSUs should not involve themselves in the day-to-day functioning of the organization.

In contrast, China has come a long way, considering its experience with privatization. China’s ‘open policy’ of the 1980s to improve the efficiency of state-owned enterprises was based on the twin pillars of privatization and consolidation. Privatization led to productivity gains of over 170 per cent in Chinese firms (

Zhangkai Huang et al. 2020). Apart from this, it is also argued that, apart from privatisation, focus on building core competencies of the Chinese state-owned enterprises also played an effective role (

Barney 1991,

1995;

Cheng and Bennett 2006).

Despite several studies attempting to measure performance measurement, there is no conclusive evidence on the effects of performance measurement (

De Bruijn 2002). On the one hand, it brings transparency (

Osborne and Gaebler 1992) and helps in shaping accountability (

De Bruijn 2001); on the other hand, it prompts game-playing (

De Bruijn 2003) and blocks innovation (

Smith 1993). To overcome these issues,

De Bruijn (

2003) suggests an outcome-based measure of performance instead of an output-based measure and has defined the rules of the game.

Therefore, in view of the above and the state of Indian PSUs, it seems imperative that a framework/model is developed that leads to better utilization of resources of PSUs, resulting in improved firm performance (

Maheshwari and Ahlstrom 2004).

Accordingly, the primary objective of the study is to suggest measures that may lead to improvement in the performance of PSUs. In order to achieve this objective, two normative frameworks (one relating to risk levels and the other relating to governance structure) are being put forth.

4. Data and Methodology

The sample consists of all 39 PSUs in the Nifty 500 Index. As of 31 March 2017, the Nifty 500 Index represents about 95.2% of the free-float market capitalization of the stocks listed on NSE. Further, these PSUs, together with a market capitalization of about INR 10 lakh crores, constitute 8.5% of NIFTY 500 Index

1. The study covers a 10-year period from 1 April 2005 to 31 March 2015. Financial data is collected from a data base called Ace Equity. Further, for Risk disclosure and fields of governance the data are hand collected from individual annual reports of the relevant firms culled from databases such as Bloomberg.

Return on assets (ROA) (

Parthasarathy et al. 2006) and return on equity (ROE) have been used as proxies of firm performance. The control variables used in the model include the age of the firm (

Ahuja and Majumdar 1998), growth rate of the firm, and size of the firm (

Ahuja and Majumdar 1998). A dummy variable has also been used to factor in the effects of recession (though the period of recession has been explicitly defined by NBER for the US, a definite period could not be traced for India).

Singh et al. (

2016) suggest that as per the UNCTAD’s investment brief, worldwide flows came down by nearly 20% towards the second half of 2007–2008; therefore, it appears reasonable to consider the period from 2005–2008 as the pre-recession period and 2008–2015 as the post-recession period for Indian companies. Further, given the panel nature of data and the possibility of endogeneity, dynamic panel data-generalized method of moments (DPD-GMM) regression has been used (

Arellano and Bond 1991;

Wintoki et al. 2010).

Due to the use of panel data methodology in the study, the method can control for unobservable heterogeneity (

Hsiao 2003), with significant reduction or elimination of estimation bias and potential problems of data multicollinearity (

Hsiao 2003). The main advantage of using the panel data is mainly to control for unobservable firm-specific effects (

Baltagi 1995). Despite these various advantages, the presence of autocorrelation might exist with data considered for longer periods (

Simon 2015). However, the study considers short panel data, which makes it less exposed to the problem of autocorrelation (

Simon 2015). Seminal studies by

Wintoki et al. (

2010) suggested that endogeneity could arise on account of (i) simultaneity, (ii) unobservable heterogeneity, and (iii) dynamic endogeneity. In this study,

Arellano and Bond’s (

1991) two-step generalized method of moments (GMM) approach with lagged variables of the dependent variable is thus used to nullify the potential problem of endogeneity and multicollinearity of the study variables (

Arellano and Bond 1991;

Arellano and Bover 1995;

Windmeijer 2005).

Thus, the following model has been used:

where ROA

it is the return on assets in company i at time t; β

1 is the growth elasticity of ROA. Similarly, ROE

it is the return on equity in company i at time t; β

1 is the growth elasticity of ROE. Descriptions of other variables are provided in

Table 3. e

it is the idiosyncratic error term. In order to examine the time-varying nature of CGI and risk index across the industries considered, panel plots were obtained using the Grammar of Graphics (ggplot) library using R-programming. A first generation panel stationarity test was conducted on the individual variables considered using the Levin, Lin, Chu (LLC) as proposed by

Levin et al. (

2002), which is based on the assumption of independent cross-sectional units. Based on the tests conducted, all the variables were considered to be stationary at level except for the size variable. The size variable depicting net total assets of the company was found to be stationary at the first difference, and thus log of the size variable was considered for the study.

5. Empirical Analysis

The descriptive statistics in

Table 4 suggest that the average ROA of the sample companies is around 11.5%, and the average ROE is around 15%. Given the fact that the period of study includes the period of recession as well, such returns seem satisfactory. Similarly, an average risk index of around 45 per cent is worth mentioning. It highlights the fact that implementation of hybrid regulatory models through Public-Private Partnership (PPP) may provide a strong incentive for managers to bring more efficiency. Irrespective of these companies being present for a longer period on average, state ownership of the firms has continued to make these firms incompetent and incapable of competition. However, the objective with which the PSUs were envisioned still seems a far-fetched dream. The much-needed improvement in governance structures of PSUs is evident from the low mean CGI score of around 62 per cent. Risk index and CGI values point towards the underutilized institutional capacity and weaker regulatory commitments. An in-depth analysis revealed it is primarily on account of non-compliance with even the basic governance parameters, such as a minimum number of independent or non-executive directors.

Further, the results in

Table 5 indicate that both ROA and ROE of the current year are significantly and positively associated with the ROA and ROE of the immediately preceding year, respectively.

The corporate governance index is positively related to both ROA and ROE, indicating that with the improvement in governance structure, PSUs tend to perform better. Considering the components of CGI, it may be suggested that (i) PSUs appoint separate a CEO and chairperson, (ii) ensure adequate representation of women on boards, (iii) appoint a Chief Risk Officer, and (iv) constitute a risk management committee.

The results also indicate that there is a negative association between risk index and returns. In other words, those PSUs which have lower risk in terms of the normative framework (developed in the paper) can generate higher returns. A recession dummy is negatively related to ROA and ROE at 1% significance level, indicating returns are negatively impacted during a recession. The null of the Wald test was rejected in all estimated models, so all coefficients are different from zero. These results not only validate the framework used to develop the risk index but also provide a yardstick for PSUs to benchmark their risk-taking if they want to maximize their ROA and ROE.

6. Additional Analysis and Tests of Robustness

The results above primarily indicate the effect of CGI when RI is zero and vice-versa. However, such a model seems unrealistic as both the forces, quality of governance structure, and risk levels are operational at any given point in time. Therefore, it seems reasonable to examine the effects of possible interaction between the two variables. A preliminary graphical investigation of CGI and RI with respect to returns revealed distinctly non-parallel lines, suggesting interaction effects amongst the variable of interest. Accordingly, an interaction variable (RI*CGI) has been introduced, and the modified model is as follows:

where

denotes ROA, ROE, standard deviation of return (risk), and average return (equity) of the company. Columns (1) and (2) of

Table 5 clearly highlight the interaction effects of RI and CGI on returns. The RI continues to be negatively associated with returns, but in the presence of interaction terms, the coefficient of CGI terms is also negative. When viewed in conjunction with a positive coefficient of interaction, the results suggest that firms with higher risk can improve their returns by having a better-quality governance structure. However, for firms with lower risk levels, quality governance structure comes at a cost, as they tend to have lower returns. In other words, risk levels (RI) act as moderating variables, influencing the relation between the quality of governance structure and returns.

It is pertinent to note that as the study is exploratory in nature, it is imperative to ensure the robustness of the models and results. For that reason, equity returns of a firm as well as the most widely accepted measure of risk, standard deviation, have been taken to corroborate the results. Clearly, the results presented in columns (3) and (4) are in line with the results of columns (1) and (2), thus, making the suggested normative frameworks warranting implementation.

7. Analysis of PSU Performance over Time Using Panel Data

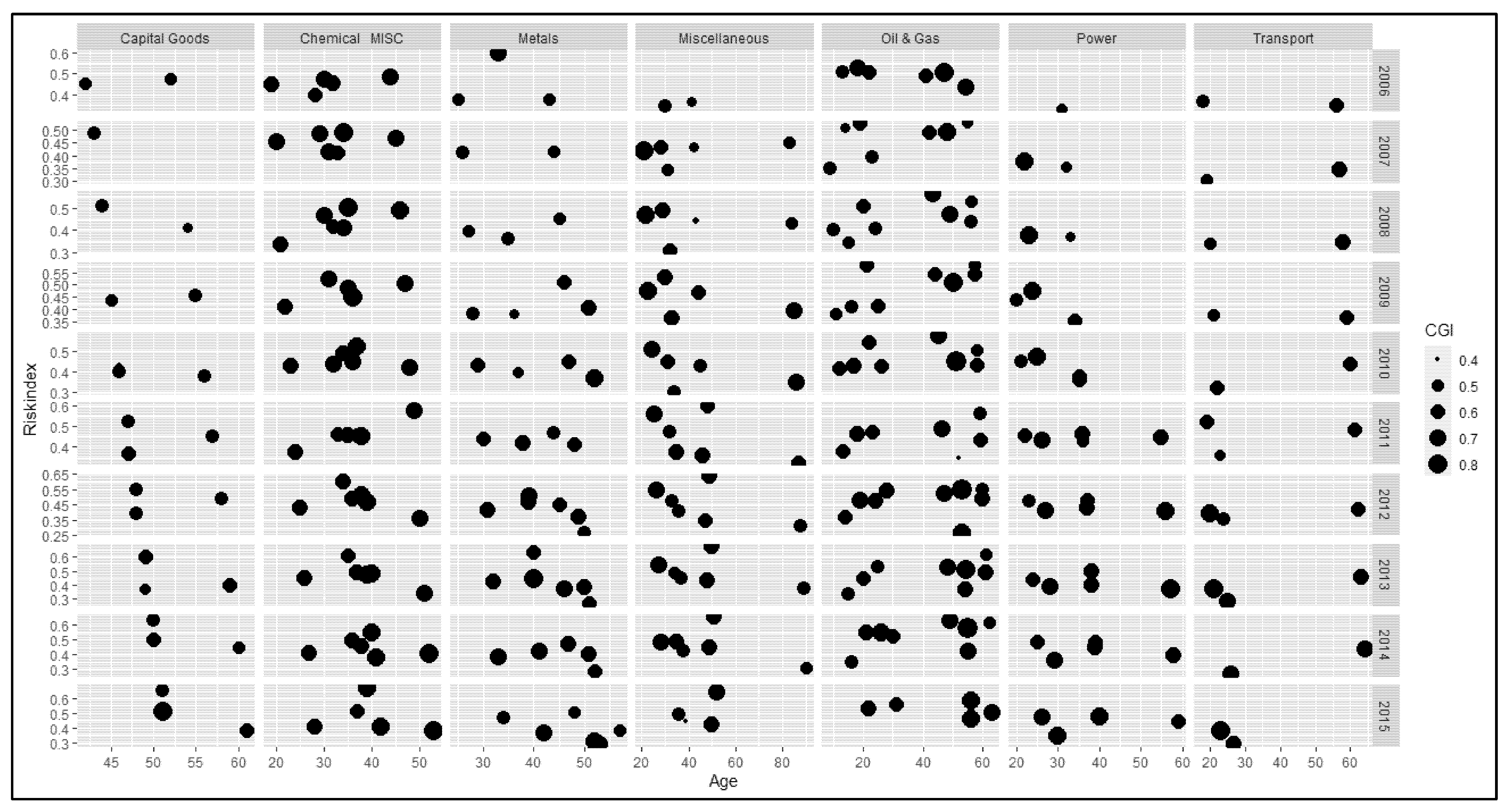

Figure 1 shows a panel plot of the age of the companies within each sector compared with the risk index over time. The size of the bubbles represents the CGI index values.

Figure 1 shows the interaction effects of the risk index and CGI as observed in

Table 5 and

Table 6, with age being the independent variable. It is evident from

Figure 1 that, except for the transport sector, most of the companies in other sectors were incorporated more than 30 years ago, on average. Despite doing business for so long and being the pioneers in their fields, the risk index seems to have changed insignificantly over time. Thus, the age of the companies is not in conjunction with the reduction in risk index across all sectors, thereby highlighting inefficiencies prevailing in the companies across the sectors. PSUs play a critical role in organized industrial activity of emerging economies and are expected to deploy their resources efficiently to accelerate the rate of expansion (

Ramamurti 1987). However, their performance has been largely dismal, with panel plots showing the risk index remained high with no significant change over the years. As a result, there is an urgent need to develop frameworks for the performance management of these inefficient and ineffective PSUs (

Nakamura and Warburton 1998). Inefficiencies of the companies prevail over time with no significant improvements in the risk index. One positive aspect seems to be a slight improvement in the CGI over the years across the following sectors: capital goods, metals, oil and gas, power, and transport. However, worrisome development is that, irrespective of the governance structure put in place as reflected by CGI, there seems to be no role of the structure in effective and efficient risk management as reflected by the risk index. From 2006 to 2015, a significant number of disinvestments took place in India. Irrespective of the government’s ambitions towards privatization, the issue of PSU disinvestments remained a contentious issue due to a lack of focus on core competencies and the government still retaining control of the management irrespective of higher CGI observed in key sectors where disinvestments were proposed. In the case of the following three sectors: chemical miscellaneous, oil and gas, and miscellaneous, though CGI index values have been high from the beginning of the study period, there seems to be no reduction in the risk index with the age of the companies in the sectors. This points towards poor quality of governance and lack of robustness in these sectors.

This paper thus provides evidence that the companies that do well in terms of the risk index and governance index developed in the paper are able to demonstrate better performance. Such benchmarks/models/frameworks may be prescribed for PSUs to ensure effective and efficient work on their part. Though the frameworks seem to be practical, caution needs to be taken while implementing them.

8. Concluding Observations

PSUs are the catalyst in the socio-economic development of emerging economies, such as India. Yet, the mere incorporation of PSUs is not a guarantee for social and economic returns. This paper shows that maintaining a high-quality governance structure in the face of high risk is the key to generating higher returns. The governance- and risk-related dimensions dealt with in the paper are, in fact, complementary to the perspective set out by new public management. In this light, the paper is perhaps the first of its kind in general and in the context of a prominent emerging economy (India) that provides and validates a risk index and governance index. While constructing the CGI, certain non-compliances were observed, even in terms of mandatory requirements, such as the proportion of independent directors. Such infringements call for stringent penal provisions and better monitoring of PSUs. Further, if the normative frameworks are adhered to as per the study by the Securities and Exchange Board of India (SEBI) and Ministry of Corporate Affairs (MCA), PSUs may take more effective and efficient decisions with lower risks, and hassle-free management resulting in better return on assets and return on equity.

Finally, we would like to mention the primarily empirical limitations of this research. Risks, such as risks related to innovation and technological changes, could not be considered due to the unavailability of data. Though the data set may appear old, it has only been used to test the risk index and analyze the results. Further, being exploratory in nature, the indices have scope for improvement. The new datasets may further check for compliance and its effect on the results. We strongly believe that cross-country analysis based on these indices may help evolve these frameworks and would make a tangible contribution to the paradigm of new public management.

{kind=link}