Exploring the Trust Influencing Mechanism of Robo-Advisor Service: A Mixed Method Approach

School of Information Technology & Management, University of International Business and Economics, Beijing 100029, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(18), 4917; https://doi.org/10.3390/su11184917

Submission received: 3 August 2019

/

Revised: 3 September 2019

/

Accepted: 5 September 2019

/

Published: 9 September 2019

(This article belongs to the Special Issue Fintech and Logistics in the Fourth Industrial Revolution Era)

Abstract

:As a typical application of fintech, the robo-advisor has increasingly gained attention over the last decade. However, most research regarding the robo-advisor has focused on its development issues such as performance improvement and regulation, while limited research has paid attention to trust. This research extends the literature by investigating the trust influencing mechanism of robo-advisors by a mixed method approach. Specifically, we identified six salient trust influencing factors by qualitative interviews and proposed the research model based on trust transfer theory. This model was tested via a survey of 230 investors. Our study finds the significant influencing role of supervisory control and validates the relationships among trust influencing factors, trust in technologies, trust in vendor and trust in robo-advisor. Moreover, several differences between junior investors and senior investors are also found in our research. This study examines trust transfer theory in the new context of the robo-advisor and contributes to further development of this increasingly utilized service.

1. Introduction

Fintech developments have receiving increasing attention from customers, vendors, regulators and other social organizations [1]. As a combination of technology and finance service, fintech has great potential in improving financial efficiency. Many traditional financial services, combining their own advantages with modern technologies, have innovated better services such as crowdfunding, online lending and robo-advisors [2]. Taking the advantage of artificial intelligence and other modern technologies, a robo-advisor creates a digital platform to conduct customer self-assessment and portfolio management [3]. Due to the cutting of human labor cost, this service provides a personalized and expenditure saving service to individual investors [4]. It is an innovative service which provides benefits to both social performance and healthy economic growth. To be specific, by developing and optimizing robo-advisor products, modern technologies including big data, customer profiling and cloud computing will be improved and better applied in society, enlightening more technological advances in other relevant industries. Furthermore, financial management and financial markets are linked with sustainability [5], so promoting robo-advisors contributes to promote finance, increase social vitality and sustainably develop the economy. However, since there is no standard criterion in this industry, robo-advisor products are hard to for customers to trust, which further leads to a slow adoption situation [4,6]. Thus, investigating trust and providing actionable suggestions for robo-advisor vendors are of benefit for production optimization, industry standardization and sustainability.

A robo-advisor is an automated service for a customer. From this perspective, we proposed to explore the role of supervisory control in robo-advisors. Supervisory control refers to a human intermittently supervising the performance of automated systems [7,8]. There is limited research on the relationship between supervisory control and trust, so there is a provocative question as to whether supervisory control can be used in robo-advisors to increase initial trust of the customers. Accordingly, this study aims to explore the following questions: (1) Is supervisory control a salient trust influencing factor of robo-advisors? (2) Besides the supervisory control, what other trust influencing factors does a robo-advisor have? (3) What is the trust influencing mechanism in the context of robo-advisors?

Our study explored trust influencing mechanisms of robo-advisors by qualitative investigation and quantitative analysis and proposed actionable development suggestions for the service vendors. The paper is structured as follows. A literature review is given in next section. Section 3 describes the qualitative investigation, following the research model and hypothesis. Quantitative investigation is exhibited in Section 5. The conclusion and contributions are discussed in the last part of this research.

2. Literature Review

2.1. Robo-Advisor

According to Sironi, a robo-advisor is an automated investment service that facilitates wealth management for customers by combining modern technologies and scientific algorithms [9]. The first robo-advisor company launched in America in 2008 and its huge success attracted billions worth of investments in this market [10]. Since then, various companies also stepped into this market including initiative startups, banks, and even high-tech companies [11]. It has been demonstrated that the use of robo-advisors is an opportunity to reshape the investment industry and has a promising future [5,12,13,14]. However, robo-advisors are also faced with challenges [15,16,17]. Previous studies of robo-advisors mainly focus on conceptual works [9,11,17], modification of algorithm and assets allocation method [18,19] and other development issues such as regulation [11,12]. Especially, from the perspective of trust, prior studies have identified some trust influencing factors of a robo-advisor, including security, information quality, interface design and so on [20,21]. Nevertheless, a systematic trust influencing mechanism model of robo-advisor has not been developed yet.

With increasing development of technologies, innovations are expected to take on more responsibilities for sustainability [22]. Sustainability initially refers to economic developments that meet the needs of present generation, later involving more contents of the impacts on future ecosystems, societies, and finance [4,23,24]. Research on the relationship between the financial industry and sustainability mainly concentrates on the strategy formulation [22], while is limited on the issue of how high-tech financial services impact sustainability. However, taking the perspective of fintech industry, many services including online shopping, e-health, and self-driving cars have made our life more sustainable [25,26]. As for the robo-advisor, it provides low cost, low risk and better algorithms for customers, and improves the method of finance. Moreover, some robo-advisor products have also taken environmental and social criteria into their investment recommendation [26].

2.2. Trust and Trust Influencing Factors

With the rapid development of modern technologies, trust plays an increasingly critical role nowadays. Trust has been conceptualized by many prior studies [27,28,29,30], one of the most widely accepted definitions is that trust is a willingness to be vulnerable and abandon right of control based on the expectation of the trustor [29]. Trust is a complex concept and can be explored in various perspectives. For example, interpersonal trust refers to the trust between individuals or groups [31]. It is generally explored based on the feeling of empathy [32,33], which heavily affects individual’s decision and behavior [34]. From the perspective of institution, institutional trust is based on the sense of security from institutions [35]. As institution-based trust often involves multiple unfamiliar parties, it is suitable to explore the e-commerce relatives [36,37,38]. According to McKnight, institution-based trust has two types, which are situational normality and structural assurances [39]. Situational normality is a sense of reassurance that the situation is normal and trustworthy, while structural assurance is a trust feeling gained from safety nets such as regulations, guarantees and contracts. Considering that a robo-advisor has similarities to e-commerce products, we will focus on institutional trust to explore the trust influence mechanism of robo-advisors.

Investigating trust influencing factors is of benefit to understanding trust influencing process. In the field of e-commerce, some trust influencing factors have been identified in previous studies. For example, on the circumstance of online purchase, it has been found that trust can be influenced by customers’ disposition, service quality and privacy protection [40,41,42,43]. Reputation [44], interface design [45] and perceived risk [46] have also been validated in the literature of e-commerce. Furthermore, prior studies also found the connection between trust influencing factors and other users’ behavior, such as technology adoption [47]. In the field of human–robot interaction, it has been examined that factors including human-related characteristics and robot-related characteristics have great impacts on the trust in robots [48]. However, considering there are some differences between robo-advisor and e-commerce businesses, the applicability of these trust influencing factors still needs further exploration.

2.3. Supervisory Control

Automation transitions have great potential in overcoming shortages of human work and improving efficiency [49]. As a specific type of automation, robotic service has some features, such as remote operation, pure online transaction and a high level of automation, to distinguish it from traditional automations and make it harder to be completely trusted by customers [48,50]. To change this situation, previous studies proposed supervisory control to modify the interaction between humans and robotic systems [51,52]. Supervisory control refers to human monitoring of the performance of automation systems in case of emergencies [20,21]. Owing to the efficiency and flexibility of a compromise method, it provides a potential way to save the workload of humans while improving system performance [51]. Accordingly, it is commonly accepted that supervisory control is superior to automatous robots or pure manual operation [20].

The importance of supervisory control has been emphasized and explored under various circumstances. For example, in some military combat systems, where the cognition of operators plays a significant role in decision making, human intervention is essential to change the automation mode [53,54]. From the perspective of civilian systems, such as autonomous navigation systems [50,55], building water cooling systems [56] and other industrial control systems [57], supervisory control is also crucial for safety and correctness. Furthermore, supervisory control can change user’s trust in a human–machine relationship [58]. However, with the rapid development of modern automation technology, it is unknown to us whether this approach can affect the trust in robo-advisors.

2.4. Trust Transfer Theory

We built our trust influencing model of robo-advisors mainly based on the trust transfer theory. With deeper exploration of trust, increasing literature has begun to explore trust transfer process to better understand trust development. This theory was firstly discovered from the fact that if a person trusts a known person, he would trust an unknown person who is trusted by the known one [59]. Namely, trust can transfer from individuals to individuals. Since then, studies also demonstrated that trust can transfer in different entities and contexts. For example, it has been noted that trust in personnel will lead to the trust in the counterpart institution [35]. Taking an online bank as an instance, Lee et al. validated that offline trust can transfer to online trust [60]. Furthermore, the online trust in a website also can transfer to another website through the hypertext links [61].

Traditional trust development models are generally conceptualized based on the change of trust influencing factors [62] but trust transfer theory gives us a clue to investigate the trust influencing process from another perspective. This theory has been explained in several raising e-commerce products. For example, trust towards social commerce members will influence trust towards social commerce apps [63]. In the context of mobile payment, internet payment trust is a determinant of mobile payment service trust [64]. It is demonstrated that the public e-service trust is transferred from trust in public administration and trust in the Internet [65]. Similarly, research has found that trust in a government website is due to trust in government and trust in technology [66]. This research is based on the trust transfer theory, combining with trust influencing factors, to build the trust development model and explore trust transfer process of robo-advisors.

3. Qualitative Investigation

3.1. Data Collection

Trust influencing factors are the foundation of our research model. To identify these factors, we conducted semi-structured interviews on 27 valid investors. The sample was selected based on following principles: (1) having acceptance, attention, or having a certain understanding of robo-advisors; (2) having various occupations and investment experience to increase sample diversity. The ages of interviewees ranged from 20 to 50. Each interview lasted over 15 min. Afterwards, the data were recorded and transcribed into text form, numbering from ID1 to ID27.

3.2. Data Analysis

After coding, we extracted keywords from interview data and developed them into constructs. To avoid ambiguity, we conducted this process with two authors. We identified 17 keywords from interview data and exhibit results in Table 1. According to the mentioned frequency, we selected salient keywords with high mentioning frequency, which are reputation, information quality, service quality, attitude toward artificial intelligence (AI), service commitment and government regulation. As the interviewees said,

“I think reputation has great influence on my trust toward robo-advisors. For example, I spent lots of time on choosing a robo-advisor service with good reputation. If there are famous banks or financial companies that support this product, I must prefer to choose their service.”(ID24)

“I think the expertise of provided information is very important. My investment experience is weak, so I am inclined to choose a robo-advisor that can provide authoritative and professional information for me.”(ID6)

“If a robo-advisor service is lacking a certain function or information compared to other products, I would think this service is defective and hard to trust.”(ID25)

“The assurances such as contracts and government regulation will influence my adoption decision on a robo-advisor. The policy of robo-advisors has not been completely established, so I value the service contract more. If there is no contract assurance, I am afraid the service would lose my money.”(ID7)

In order to understand the factors from the perspective of institutional trust, we divided these factors into three groups, which are deposition, situational normality and structural assurance. To be specific, structural assurance requires a service to provide assurance to prevent customers from finance loss, privacy leakage and other risks [39]. Thus, factors such as privacy policy, service commitment and government regulation belong to this type of trust. Meanwhile, situation normality refers to a trustworthy situation, which is a reflection of customer’s expectancy [36]. Consequently, factors including reputation and service quality are categorized into this type. The descriptions and categories of the six salient trust influencing factors are exhibited in Table 2.

4. Research Model and Hypotheses

4.1. Research Model

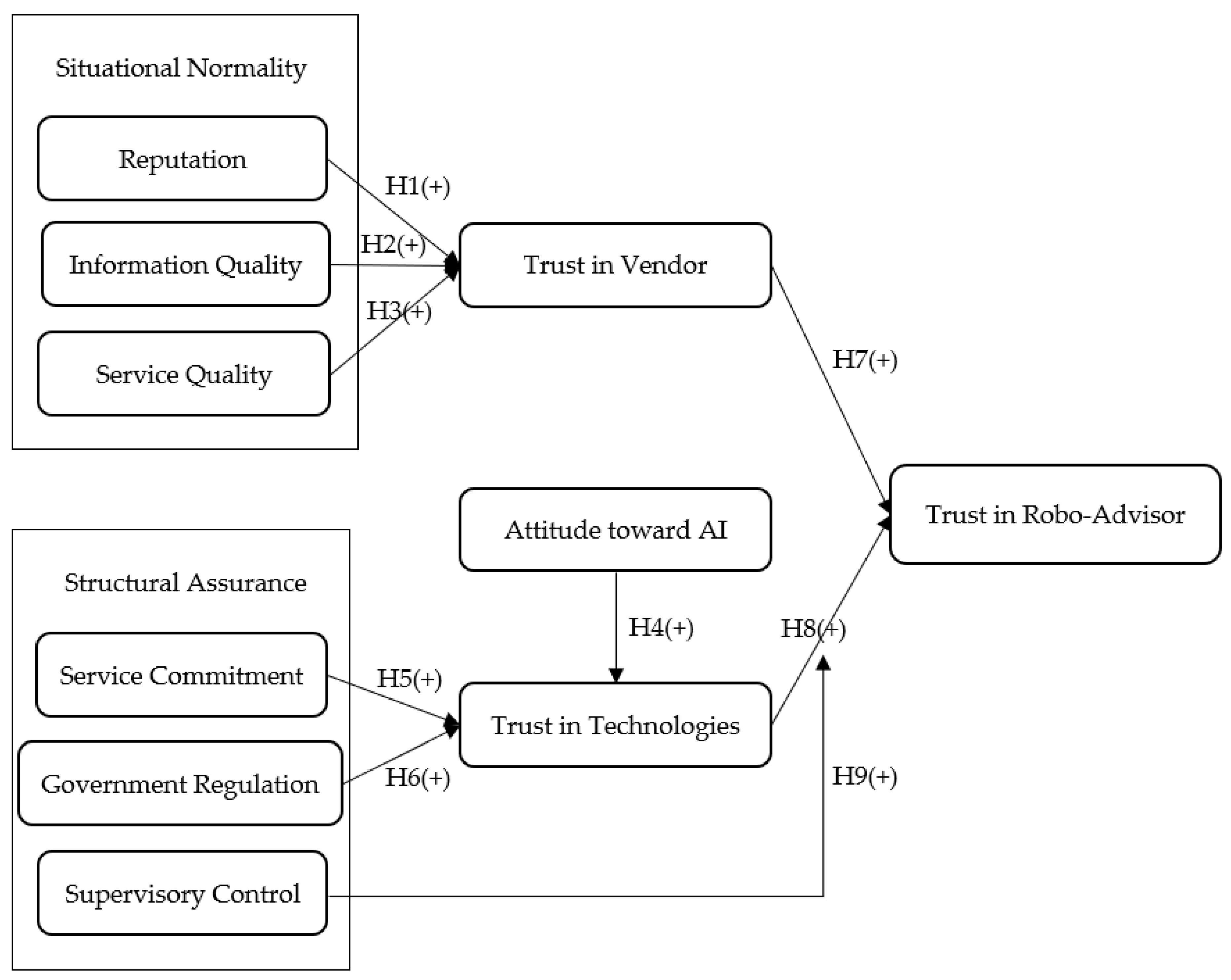

We selected six salient keywords with high mentioning frequency, which are reputation, information quality, service quality, attitude toward artificial intelligence (AI), service commitment and government regulation. Based on trust transfer theory, we incorporated the variables of trust in technologies and trust in vendor to deeper explore the trust development process of robo-advisors. In addition, drawing from the literature on automation, we designed the supervisory control construct to examine the impact on the trust influencing process of robo-advisors. Figure 1 provides an overview of our research model. The details of this conceptual model will be explained in the next section.

4.2. Hypotheses Development

4.2.1. Reputation

Firm reputation is a significant factor in gaining customers’ trust. On one hand, a positive firm reputation indicates a satisfying fulfillment of company’s prior obligation [67]. On the other hand, reputation is the representation of public opinion, which can shape customer’s first impressions of a firm [68]. Consumers tend to conclude that transacting with firms with positive reputation is low-risk, while transacting with firms with negative reputation is uncertain and high-risk [67]. Therefore, positive firm reputation can reduce uncertainty and increase customers’ trust [69]. In the context of e-commerce, reputation is of vital importance because the internet brings lots of unfamiliar entities together [70]. Moreover, it has been proved that reputation affects trust in various e-commerce products such as mobile banking and online retailing [71,72]. Robo-advisors are an increasingly used product on the internet, and reputation is a key factor that impacts trust in robo-advisors [73,74]. Thus, we hypothesize:

Hypothesis 1 (H1).

Reputation positively affects customer’s trust in robo-advisor vendors.

4.2.2. Information Quality

The importance of information quality has been highlighted in trust building, technology acceptance, spreading behavior [75,76,77] and so on. Especially in e-commerce business, high information quality is a promoting factor that influences the decision-making process of customers and facilitates trust generation [77,78]. For example, it has been proved that information quality positively influences customer’s trust in online purchases [79]. While taking mobile banking as an instance, the quality of payment information affects initial trust building process [68]. In our study, the information quality refers to the quality of a recommended portfolio by a robo-advisor, which has been validated as a salient trust influencing factor before [73]. Previous study has illustrated that high information quality can give positive feedback to the source of information and promote the trust effectively [80]. As a consequence, we hypothesize:

Hypothesis 2 (H2).

Information quality positively affects customer’s trust in robo-advisor vendors.

4.2.3. Service Quality

Customer’s behavior can be strongly influenced by service quality [80]. For customers, positive service quality generally results in a favorable behavior, such as trust, adoption and continuous usage [81,82,83]. In an internet environment, where the companies’ competition is getting more severe than before, service quality is a critical factor in choosing a product or service. For example, service quality positively affects trust and further facilitates the relationship commitment between customers and IT service [84]. In other e-commerce products such as e-government and online shopping, the role of service quality is also significant [66,85]. Based on the trust transfer theory, we argue that superior service quality might facilitate commitment to the robo-advisor vendor, finally leading to the trust in robo-advisors. Thus, we hypothesize:

Hypothesis 3 (H3).

Service quality positively affects customer’s trust in robo-advisor vendors.

4.2.4. Attitude toward AI

Personal characteristics are an important trust influencing factor in e-commerce [36]. Generally speaking, a person who is incline to trust others is easier to trust an unfamiliar product or service. From the perspective of information systems, personal traits also significantly influence the technology acceptance process in the context of online shopping, e-business, ERP and so on [86]. Several concepts have been proposed to demonstrate this feature, such as personal innovativeness and technology readiness [87], commonly referring to the willingness of customer to try out new innovations [88,89]. The specific trait of customer’s innovativeness varies in different technical innovations [86]. As robo-advisors are famous for the application of artificial intelligence to their potential customers, prior study has found that the attitude towards AI is a key trust influencing factor for robo-advisors. However, considering extensive technologies are also used in this disruptive service, such as machine learning and big data [90], the relationship between trust in AI and trust in the technologies used by robo-advisors is unknown. Therefore, we hypothesize:

Hypothesis 4 (H4).

Attitude toward AI positively affects customer’s trust in the technologies used by robo-advisors.

4.2.5. Service Commitment

Service commitments refer to valid contracts, agreements and guarantees from the vendor to pledge the relationship between customers and vendors [91]. In order to reduce transaction uncertainty, service commitment is designed to clarify service duty of the vendor and revise customer’s expectancy [92]. Accordingly, service commitment is expected to influence trust of customers [93]. In other words, contracts and agreements provide a measurement of actual completion of the promised items and compensate for distrust of consumer by enhancing control feelings [94]. When customers do not know enough about a technology, investigating service commitment is one of references to determine whether to trust a new service [95]. Meanwhile, it has been proven that service commitment affects customers’ trust in the context of e-commerce, e-service, online community and so on [92,96]. Therefore, we hypothesize:

Hypothesis 5 (H5).

Service commitment positively affects customer’s trust in the technologies used by robo-advisors.

4.2.6. Government Regulation

Government regulation can shape customer’s behavior remarkably, especially for some rising technologies [97]. It can lower perceived risk and enhance trust of customers [98]. For example, legislation is a salient external factor that positively influences use intention in online environment [97]. To be exact, government regulation indicates a supportive attitude in the condition of new technology emergence, which can increase customers’ faith and provide a favorable environment for the novelty. According to this view, we hypothesize:

Hypothesis 6 (H6).

Government regulation positively affects customer’s trust in the technologies used by robo-advisors.

4.2.7. Trust in Vendors, Trust in Technologies and Trust in Robo-Advisors

Trust in vendor and trust in technology are two equally important components of customer’s trust in e-commerce [99]. On the on hand, trust in vendor is one of the determinants to engage in online business, especially in internet activities filling with uncertainties. Higher trust in the vendor can further lead to higher following intention, sharing intention and higher purchasing intention [40,100]. On the other hand, there is lots of evidence that trust in technologies also plays a significant role in the adoption of high-tech products, such as online purchases [101] and information systems [102]. If a customer distrusts the technology, he might think the product can easily result in misleading, information leakage and business malpractice. There are studies that have explored trust from the two dimensions before. For example, trust in e-government is positively associated with trust in government and trust in technology in the context of a government website [66]. As for robo-advisors, with massive involvement of modern technologies [90], trust in technologies seems to be more crucial to customer’s trust. To explore the trust development of robo-advisors from a systematic way, we designed our research model from the two dimensions simultaneously. Thus, we hypothesize:

Hypothesis 7 (H7).

Trust in vendor positively affects customer’s trust in robo-advisors.

Hypothesis 8 (H8).

Trust in technologies positively affects customer’s trust in robo-advisors.

4.2.8. Supervisory Control

Supervisory control is a main determinant of trust in automation service [103]. Previous study has showed that supervisory control can shape the human–machine relationship and increase human’s faith in machines [104]. From the perspective of high-tech service, trust in technology highly correlates with trust in service. For instance, with the rapid development of public e-service [65] and e-government service [66], trust in technology positively influences trust in the service. Robo-advisor service aims to provide a set of automated personalized investment recommendations to customers. It is hard for pure automation to gain initial trust from customers [6]. Considering many investors prefer to choose their investment portfolio by themselves [105], a supervisory control function may seem friendly to these people and make robo-advisors easier to be trusted. Hence, we hypothesize:

Hypothesis 9 (H9).

Supervisory control strengthens the positive relationship between trust in technologies and trust in robo-advisors.

5. Quantitative Investigation

Following the exploratory qualitative research method, we have proposed hypotheses and built a research model. In this section, we used surveys to collect data and quantitatively examined the model. SPSS and Smart PLS 3.0 were used to conduct data analysis. The data collection and data analysis process are introduced as follows.

5.1. Data Collection

An online survey on a sample of 240 investors was conducted in our study. The questionnaires were all collected online. To assure the quality of questionnaires, a pilot test was conducted on 40 investors before the formal survey. After modification of the questionnaire, 33 valid items were finally accepted. All the measurement items used the seven-point Likert scale ranging from 1 (strongly disagree) to 7 (strongly agree). The items and their sources are shown in Appendix A.

After data collection, we used SPSS to conduct descriptive statistical analysis. Specifically, we selected the collected data mainly based on following criteria. Firstly, since the online survey had a timing function, we removed the samples that finished survey within 1 min for fear of meaningless information. Secondly, we excluded the questionnaires with incomplete data. A number of 230 valid surveys were successfully collected. Information related to investment experience, age and gender were collected and the demographic portrait of our sample is exhibited in Table 3.

5.2. Data Analysis

5.2.1. Measurement

Smart PLS 3.0 was used to conduct further data analysis. Validity and reliability were examined before formal hypotheses test. Our preliminary measurement had three steps. First of all, the scales for our constructs were tested by cross loading. All factors had a loading above 0.7, suggesting that each item was in accordance with their latent construct. Then, Cronbach’s alpha (CA), composite reliability (CR) and average variance extracted (AVE) were examined, which are shown in Table 4. At last, we calculated the square root of the AVE (SQAVE) by referring to latent variable correlations in order to check the discriminant validity. As Table 5 shows, for each construct, the diagonal values were larger than all the values below, which means no dominant construct. Based on the above analysis, it can be concluded that our questionnaire is reliable and valid.

5.2.2. Hypotheses Test

To test the research hypotheses, the partial least squares structural equation modeling (PLS-SEM) analysis method was used in our analysis. After reliability and validity assessment, we utilized standard bootstrapping procedure to output path coefficients. Indicators including mean (M), standard deviation value (STDEV), path coefficient, t-value and p-value were calculated to test the significance and relevance of hypothesized relationships. We exhibited the testing results in Table 6.

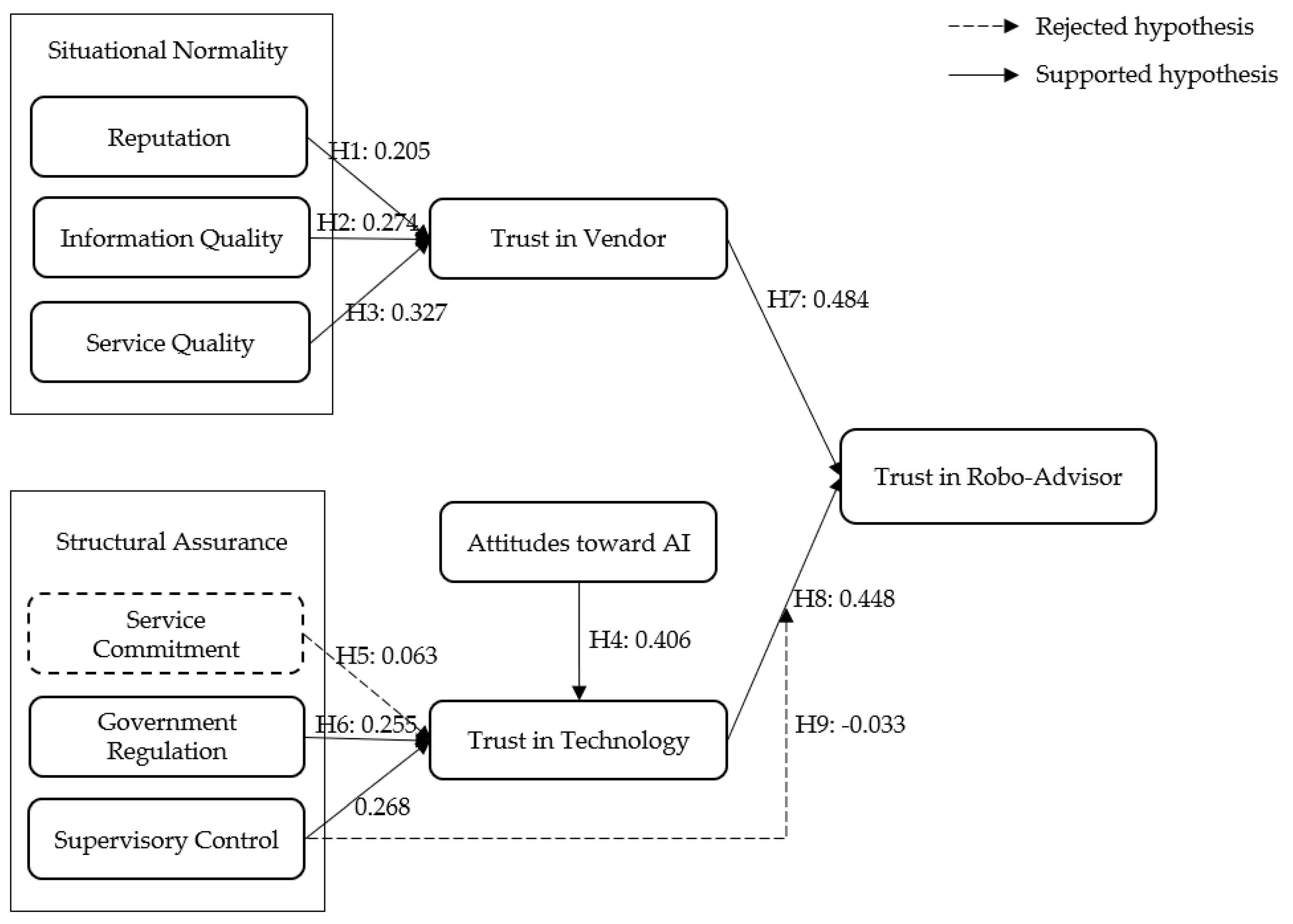

As Table 6 shows, almost all the hypotheses were validated except Hypothesis 5 and Hypothesis 9. The statistics show that reputation had an apparently positive correlation with trust in vendor (t-value = 2.53, p = 0.012). Information quality and service quality also had significant impacts on trust in vendor with t-values of 4.01 and 3.53, respectively (p < 0.005). Meanwhile, government regulation had significant influences on trust in technologies (t-value = 4.04, p < 0.005), which means that trust in technologies was heavily affected by policies. Moreover, attitude to AI had the most powerful impact on trust in technologies (t-value = 6.26, p < 0.005). Furthermore, we have found the trust transfer mechanism of robo-advisor. Results showed that trust in vendor and trust in technologies had significant impacts on trust in robo-advisor (t-values = 7.84 and 6.36 respectively, p < 0.005). However, the results showed a negative support to the moderating effect of supervisory control, namely H9 was rejected. Instead, we found that supervisory control had a significant influence on trust in technologies (t-value = 3.66, p < 0.005). According to the results of our quantitative data analysis, we updated our conceptual model and proposed a revised version (see Figure 2).

5.2.3. Control Variables

Taking gender, age and investment experience as control variables, we found that gender had little influence on our research model while the effects under different age groups were also insignificant. However, we found that investment experience significantly affected the relationships of our model. Previous research has found that investment experience indeed has effects on investment behavior [64]. To further explore whether investment experience leads to different opinions in customers, we partitioned our sample into two groups, which were junior investors and senior investors. The mean value of investment years in our sample was 2.06 years. Accordingly, we classified investors with less than 2 investment years as junior investors and the rest as senior investors. We re-ran the data and the result is depicted in Table 7.

As Table 7 shows, junior investors and senior investors obviously had distinct opinions on the relationships among service quality, attitude to AI and trust in vendor. Firstly, junior investors valued the overall service quality more, they expected convenient and comprehensive financial service from robo-advisor. When more satisfying service quality was offered, they would put more trust in the service vendor. Secondly, attitude toward AI played an important role in trust in technologies, yet it had less impacts on senior investors. We reckoned that experienced investors usually have strong faith in their own judgement rather than an automated service. Moreover, senior investors have higher scores of trust in vendor, which means that experienced investors have less suspicion of their chosen vendors.

6. Discussion and Conclusions

As a typical service of fintech, investigating robo-advisors contributes to sustainability from three aspects. From the perspective of society, on one hand, a robo-advisor improves customer’s efficiency and reshapes the style of investment. On other hand, it is beneficial for sustainable development by driving modern technologies in continuously advancing and facilitating the development of other relevant industries. From the perspective of economy, the new fin-tech innovation will enlarge investment and contribute to more robust economic growth and prosperity.

One of the challenges faced by robo-advisor is difficulty in being trusted by customers. Accordingly, the objective of our study is exploring the trust influencing mechanism of robo-advisors based on trust transfer theory. Mixed methods including interviews and surveys were used in our research. Specifically, we identified six salient trust influencing factors of robo-advisors by analyzing interview data, which are reputation, information quality, service quality, service commitment, government regulation and attitude toward AI. Then, according to the automated feature of robo-advisors, we have drawn a construct of supervisory control from previous literature and developed an integrated trust influencing mechanism model. Finally, by quantitatively analyzing 230 questionnaires, we examined the model and proposed a revised version (see Figure 2). The findings, contributions and future work will be described in this section.

6.1. Findings

6.1.1. Supervisory Control is a Salient Trust Influencing Factor of Robo-Advisors

According to the automation feature of robo-advisors, we have drawn a construct from the literature, namely supervisory control, to explore its impacts on the trust development process of robo-advisors. We found that supervisory control has a directly positive correlation to trust in a robo-advisor.

Supervisory control refers to moderate human intervention to the automated settings [20,21]. As automation technology has not been widely accepted, customers are unfamiliar with automated services. When facing a novel high-tech investment tool, namely a robo-advisor, customers generally hold a cautious attitude and want more autonomy of their own. It gives us the clue that robo-advisors will be more easily trusted by customers with supervisory control. We suggest that the robo-advisor vendors should add more flexible functions such as replacing stocks according to a customer’s preference, to attract more conservative investors. As an interviewee says:

“I think robo-advisor service needs more improvements. One question is, I knew several robo-advisor products, they all provide me with a set of portfolios that I can’t change. I think it should let me change one item or something, making this service more personalized.”(ID6)

6.1.2. Six Trust Influencing Factors of Robo-Advisors

According to our analysis, there are seven salient trust influencing factors in the context of robo-advisors. Firstly, six salient factors including reputation, information quality, service quality, service commitment, government regulation and attitude toward AI are identified by qualitative interviews. Secondly, the role of supervisory control is validated by quantitative analysis. In conclusion, reputation, information quality and service quality have positive correlations with trust in vendor, while factors including government regulation, attitude toward AI and supervisory control positively affect trust in technologies used by robo-advisors. Additionally, the quantitative analysis shows that service commitment has an insignificant impact on trust in technologies. We reckon that the customers that barely expect service commitment to provide trust-worthy information for the technologies account for a large proportion. As an interviewee puts,

“I believe that the service commitments are the constraints in principle and bottom line. It must protect customer’s benefits based on the legislation. So, I will read the items before my adoption but I do believe it won’t harm my interests.”(ID21)

6.1.3. The Trust Influencing Mechanism of Robo-Advisors

We investigated the trust influencing mechanism and built a trust influencing model in the context of robo-advisors. The relationships among trust influencing factors, trust in vendor, trust in technologies and trust in robo-advisor were validated by quantitative analysis. Apart from the trust influencing factors closely correlate with trust in trust in vendor or trust in technologies, we demonstrated that these trusts can transfer into the trust in robo-advisor service. The modified trust influencing model of robo-advisor is exhibited in Figure 2. Moreover, the relationships in our research model can be affected by customer’s investment experience.

6.2. Contribution and Future Research

6.2.1. Theoretical Contribution

Our research has several theoretical and practical contributions. First of all, previous research of trust in robo-advisors mainly focused on the regulation issue [11,15]. This research extends the literature of trust in robo-advisors by exploring the trust influencing mechanism of robo-advisors. We identified a total number of seven trust influencing factors of robo-advisors, which are reputation, information quality, service quality, service commitment, government regulation and attitude toward AI. Besides, due to the automation feature of robo-advisor, a novel factor named supervisory control is discovered from literature and validated by quantitative analysis.

Secondly, previous research of trust in robo-advisors generally concentrates on exploring the relationship between trust influencing factors and other customer behaviors such as adoption [18,19], rarely deeply investigating the trust developing mechanism of robo-advisors. Our study proposed an integrated trust building model and examined the relationship between trust influencing factors and trust in entities. This research provides clues to explore how trust develops in similar contexts.

Moreover, this study enriched the literature on trust transfer theory. Trust transfer theory has been utilized in several e-commerce service such as online shopping, online banking, online government service and so on [60,61,66]. Our study tests the applicability of this theory and extends it in the new context of robo-advisors.

6.2.2. Practical Contribution

This research also has several practical implications. First, the research model we proposed is helpful to vendors to understand the needs of customers and design better robo-advisor systems. Second, by investigating trust in robo-advisors, we promote this service and contribute to more positive customer behaviors, facilitate further technological testing and improvement. Furthermore, with deeper investigation of robo-advisors, this study promotes the transition from traditional financial service to modern high-tech service, helping sustainable development for a better society in the fourth industrial revolution era.

In summary, there are several suggestions that we concluded for robo-advisor service vendors. To begin with, the vendors are encouraged to advertise themselves and enhance their reputation. Trust in vendor is a powerful factor in gaining customer’s initial trust in their product. Moreover, from the perspective of trust in technologies, it is provocative that technical companies have natural advantages to develop this service. Furthermore, it is suggested that vendors should provide more clear and readable commitments to customers and advertise their product more to gain customers’ trust. Our findings on the differences between senior investors and junior investors provide a reference for vendors’ self-positionings. Specifically, a well-known company is encouraged to improve their performance on information recommendations while new startups are suggested to focus more on their service quality to attract new investors.

6.2.3. Limitation and Future Research

There are some limitations that have to be considered in our study. First of all, we identified the salient trust influencing factors through interviews. Due to the limited interview data, the qualitative analysis result may be not comprehensive enough. Future research can enlarge the sample and find more important trust influencing factors to enrich this research.

Second, our sample was mainly composed of young people with limited investment experience. Accordingly, the results of our study may not universally applicable to all groups, especially to elder customers who have more investment experience. Thus, we suggest future researchers increase the diversity of their sample, so that the data volume of all age groups is balanced and people with various investment experience are involved.

Last but not least, our sample was collected in China. Because the development of robo-advisors has various situations in different countries, our research results may not be universally applicable to other contexts. As a consequence, we encourage future research that includes samples from various countries to examine the generalizability of our study. We are interested in research to analyze more diverse data and conduct comparative study in the future.

Author Contributions

Conceptualization, X.C.; J.C.; F.G.; methodology, X.C.; J.C.; software, K.L.; validation, X.C., F.G.; formal analysis, K.L.; investigation, F.G., Y.Z., P.G.; data curation, K.L.; writing—original draft preparation, F.G.; writing—review and editing, X.C., Y.Z., P.G.; supervision, X.C.; J.C.; funding acquisition, X.C; J.C.

Funding

This research was funded in part by the National Key R&D Program of China under Grant No.2017YFB1400700, the Fundamental Research Funds for the Central Universities in UIBE (CXTD10-06), Program for Excellent Talents in UIBE (Grant No.18JQ04), and the Foundation for Disciplinary Development of SITM in UIBE.

Acknowledgments

We thank all the participants who attended the interviews and helped this research.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

Table A1.

Measurement items for variables.

| Variables | Measurement Items | Sources |

|---|---|---|

| Reputation (RE) | Other products or services offered by this vendor are also well received. (RE1) | [106] |

| The vendor have reliable operation ability, stable profitability and ability to deal with risks. (RE2) | ||

| The vendor has good service level. (RE3) | ||

| Information Quality (IQ) | The robo-advisor can provide me with high-yield information. (IQ1) | [57] |

| The robo-advisor can provide timely information for me. (IQ2) | ||

| The robo-advisor can accurately provide customized investment information for me. (IQ3) | ||

| Service Quality (SQ) | The robo-advisor can provide me with a convenient and smooth experience. (SQ1) | [107] |

| The robo-advisor can meet my financial needs. (SQ2) | ||

| The robo-advisor can provide staff service access and help me deal with problems through staff when necessary. (SQ3) | ||

| Attitude toward AI (AA) | I think the application of AI technology will improve our quality of life. (AA1) | [90] |

| I would like to try to use the products and services using AI technology. (AA2) | ||

| I think intelligent products are relatively mature and rarely make serious mistakes. (AA3) | ||

| Service Commitment (SC) | The service agreement of this robo-advisor guarantees user privacy, capital security and so on. (SC1) | [27,57] |

| The service agreement of this robo-advisor guarantees the technical basis. (SC2) | ||

| Overall, the service agreement of this robo-advisor convinces me that they can provide a secure transaction environment. (SC3) | ||

| Government Regulation (GR) | I think the government supports customers to use smart robo-advisors. (GR1) | [108] |

| As far as I know, to promote the healthy development of robo-advisor, the government has issued relevant policies to support the industry. (GR2) | ||

| As far as I know, to prevent chaos of robo-advisor industry, the government has promulgated relevant laws and regulations to protect customers. (GR3) | ||

| Trust in Vendor (TV) | The vendor can safeguard the interests of consumers. (TV1) | [109] |

| The vendor hopes to maintain a good reputation. (TV2) | ||

| Overall, the vendor is credible. (TV3) | ||

| Trust in Technologies (TT) | I think the application of big data, cloud computing and AI technology in financial products will improve my investment and financial management effect. (TT1) | [62] |

| I’d like to try financial products using big data, cloud computing and AI technology. (TT2) | ||

| I think there is no technical risk in applying big data, cloud computing and AI technology to financial products. (TT3) | ||

| Supervisory Control (SCO) | If I can adjust and delete the contents according to my preferences in a system-recommended purchase portfolio, I will be more satisfied. (SCO1) | |

| If I can adjust and delete the contents according to my preferences in a recommended purchasing portfolio, I will trust more in the system. (SCO2) | ||

| If a service recommends a portfolio that suitable for me but I am not satisfied with one of the components, I think my investment will be efficient and profitable only if I can adjust the content of the portfolio. (SCO3) |

References

- Geranio, M. Fintech in the exchange industry: Potential for disruption? Masaryk Univ. J. Law Technol. 2017, 11, 245–266. [Google Scholar] [CrossRef]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Jung, D.; Dorner, V.; Glaser, F.; Morana, S. Robo-advisory. Bus. Inform. Syst. Eng. 2018, 60, 81–86. [Google Scholar] [CrossRef]

- Jung, D.; Dorner, V.; Weinhardt, C.; Pusmaz, H. Designing a robo-advisor for risk-averse, low-budget consumers. Electron. Mark. 2018, 28, 367–380. [Google Scholar] [CrossRef]

- Castro, N.R.; Chousa, J.P. An integrated framework for the financial analysis of sustainability. Bus. Strategy Environ. 2006, 15, 322–333. [Google Scholar] [CrossRef]

- Mallat, N. Exploring consumer adoption of mobile payments—A qualitative study. J. Strateg. Inform. Syst. 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Sheridan, T. Human supervisory control of robot systems. In Proceedings of the 1986 IEEE International Conference on Robotics and Automation, San Francisco, CA, USA, 7–10 April 1986. [Google Scholar]

- Ferrell, W.R.; Sheridan, T.B. Supervisory control of remote manipulation. IEEE Spectr. 1969, 4, 81–88. [Google Scholar] [CrossRef]

- Sironi, P. Personalize personal finance. In FinTech Innovation: From Robo-Advisors to Goal Based Investing and Gamification; John Wiley & Sons: Hoboken, NJ, USA, 2016; pp. 8–11. [Google Scholar]

- Epperson, T.; Hedges, B.; Singh, U.; Gabel, M. AT Kearney 2015 Robo-Advisory Services Study; AT Kearney: București, Romania, 2015. [Google Scholar]

- Fisch, J.E.; Labouré, M.; Turner, J.A. The Emergence of the Robo-Advisor. Pension Research Council Working Papers, Wharton School Pension Research Council, University of Pennsylvania. Available online: https://repository.upenn.edu/prc_papers/10 (accessed on 1 December 2018).

- Lopez, J.C.; Babcic, S.; Andres, D.L.O. Advice goes virtual: How new digital investment services are changing the wealth management landscape. J. Financ. Perspect. 2015, 3, 156–164. [Google Scholar]

- Callaway, J. Fintech Disruption: Opportunities to Encourage Financial Responsibility. Pension Research Council Working Papers, Wharton School Pension Research Council, University of Pennsylvania. Available online: https://repository.upenn.edu/prc_papers/8 (accessed on 1 December 2018).

- Bussmann, O. The future of finance: Fintech, tech disruption, and orchestrating innovation. In Equity Markets in Transition; Springer: Cham, Switzerland, 2017; pp. 473–486. [Google Scholar]

- Ji, M. Are robots’ good fiduciaries? Regulating robo-advisors under the investment advisers act of 1940. Colum. L. Rev. 2017, 117, 1543–1583. [Google Scholar] [CrossRef]

- Baker, T.; Dellaert, B. Regulating robo advice across the financial services industry. Iowa L. Rev. 2018, 103, 713–749. [Google Scholar] [CrossRef]

- Jung, D.; Glaser, F.; Köpplin, W. Robo-advisory: Opportunities and risks for the future of financial advisory. In Advances in Consulting Research; Springer: Cham, Switzerland, 2019; pp. 405–427. [Google Scholar]

- Beketov, M.; Lehmann, K.; Wittke, M. Robo advisors: Quantitative methods inside the robots. J. Asset Manag. 2018, 19, 363–370. [Google Scholar] [CrossRef]

- Xue, J.; Liu, Q.; Li, M.; Liu, X.; Ye, Y.; Wang, S.; Yin, J. Incremental multiple kernel extreme learning machine and its application in Robo-advisors. Soft Comput. 2018, 22, 3507–3517. [Google Scholar] [CrossRef]

- Lee, S.; Choi, J.; Ngo-Ye, T.L.; Cummings, M. Modeling trust in the adoption decision process of robo-advisors: An agent-based simulation approach. In Proceedings of the Tenth Midwest Association for Information Systems Conference, Saint Louis, MO, USA, 17–18 May 2018. [Google Scholar]

- Ngo-Ye, T.L.; Choi, J.J.; Cummings, M. Modeling the robo-advisor ecosystem: Insights from a simulation study. Issues Inform. Syst. 2018, 19, 128–138. [Google Scholar]

- Frias-Aceituno, J.V.; Rodríguez-Ariza, L.; Garcia-Sánchez, I.M. Explanatory factors of integrated sustainability and financial reporting. Bus. Strategy Environ. 2014, 23, 56–72. [Google Scholar] [CrossRef]

- WCED, S.W.S. World commission on environment and development. Our Common Future 1987, 17, 1–91. [Google Scholar]

- Othman, A.R. Sustainability practices and corporate financial performance: A study based on the top global corporations. J. Bus. Ethics 2012, 108, 61–79. [Google Scholar]

- Anshari, M.; Almunawar, M.N.; Masri, M.; Hamdan, M. Digital marketplace and fintech to support agriculture sustainability. Energy Procedia 2019, 156, 234–238. [Google Scholar] [CrossRef]

- Rappitsch, C. Digital Economy and Sustainability; OIKOS: St. Gallen, Switzerland, 2017; pp. 1–30. [Google Scholar]

- McKnight, D.H.; Chervany, N.L. What trust means in e-commerce customer relationships: An interdisciplinary conceptual typology. Int. J. Electron. Commer. 2001, 6, 35–59. [Google Scholar] [CrossRef]

- Gefen, D.; Straub, D.W. Consumer trust in B2C e-commerce and the importance of social presence: Experiments in e-products and e-services. Omega 2004, 32, 407–424. [Google Scholar] [CrossRef]

- Mayer, R.C.; Davis, J.H.; Schoorman, F.D. An integrative model of organizational trust. Acad. Manag. Rev. 1995, 20, 709–734. [Google Scholar] [CrossRef]

- Rousseau, D.M.; Sitkin, S.B.; Burt, R.S.; Camerer, C. Not so different after all: A cross-discipline view of trust. Acad. Manag. Rev. 1998, 23, 393–404. [Google Scholar] [CrossRef]

- Rotter, J.B. A new scale for the measurement of interpersonal trust. J. Personal. 1967, 35, 651–665. [Google Scholar] [CrossRef]

- Paul, D.L.; McDaniel, J.R. A field study of the effect of interpersonal trust on virtual collaborative relationship performance. MIS Q. 2004, 28, 183–227. [Google Scholar] [CrossRef]

- Feng, J.; Lazar, J.; Preece, J. Empathy and online interpersonal trust: A fragile relationship. Behav. Inform. Technol. 2004, 23, 97–106. [Google Scholar] [CrossRef]

- Karbowski, A.; Ramsza, M. Imagine-self perspective-taking and rational self-interested behavior in a simple experimental normal-form game. Front. Psychol. 2017, 8, 1557. [Google Scholar] [CrossRef] [PubMed]

- Zucker, L.G. Production of trust: Institutional sources of economic structure, 1840–1920. Res. Organ. Behav. 1986, 8, 53–111. [Google Scholar]

- Gefen, D.; Karahanna, E.; Straub, D.W. Trust and tam in online shopping: An integrated model. MIS Q. 2003, 27, 51–90. [Google Scholar] [CrossRef]

- Walczuch, R.; Lundgren, H. Psychological antecedents of institution-based consumer trust in e-retailing. Inform. Manag. 2004, 42, 159–177. [Google Scholar] [CrossRef] [Green Version]

- Pavlou, P.A.; Gefen, D. Building effective online marketplaces with institution-based trust. Inform. Syst. Res. 2004, 15, 37–59. [Google Scholar] [CrossRef]

- McKnight, D.H.; Cummings, L.L.; Chervany, N.L. Initial trust formation in new organizational relationships. Acad. Manag. Rev. 1998, 23, 473–490. [Google Scholar] [CrossRef]

- Gefen, D. E-commerce: The role of familiarity and trust. Omega 2000, 28, 725–737. [Google Scholar] [CrossRef]

- Lowry, P.B.; Vance, A.; Moody, G.; Beckman, B.; Read, A. Explaining and predicting the impact of branding alliances and web site quality on initial consumer trust of e-commerce web sites. J. Manag. Inform. Syst. 2008, 24, 199–224. [Google Scholar] [CrossRef]

- Al-Debei, M.M.; Akroush, M.N.; Ashouri, M.I. Consumer attitudes towards online shopping: The effects of trust, perceived benefits, and perceived web quality. Internet Res. 2015, 25, 707–733. [Google Scholar] [CrossRef]

- Yoon, H.S.; Occeña, L.G. Influencing factors of trust in consumer-to-consumer electronic commerce with gender and age. Int. J. Inform. Manag. 2015, 35, 352–363. [Google Scholar] [CrossRef]

- Xiong, L.; Liu, L. A reputation-based trust model for peer-to-peer e-commerce communities. In Proceedings of the IEEE International Conference on E-Commerce, Newport Beach, CA, USA, 24–27 June 2003; pp. 275–281. [Google Scholar]

- Wang, Y.D.; Emurian, H.H. Trust in e-commerce: Consideration of interface design factors. J. Electron. Commer. Organ. 2005, 3, 42–60. [Google Scholar] [CrossRef]

- Pavlou, P.A. Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model. Int. J. Electron. Commer. 2003, 7, 101–134. [Google Scholar]

- Alzahrani, L.; Al-Karaghouli, W.; Weerakkody, V. Analysing the critical factors influencing trust in e-government adoption from citizens’ perspective: A systematic review and a conceptual framework. Int. Bus. Rev. 2017, 26, 164–175. [Google Scholar] [CrossRef]

- Hancock, P.A.; Billings, D.R.; Schaefer, K.E.; Chen, J.Y.; De Visser, E.J.; Parasuraman, R. A meta-analysis of factors affecting trust in human-robot interaction. Hum. Factors. 2011, 53, 517–527. [Google Scholar] [CrossRef]

- Groover, M.P. Automation, Production Systems, and Computer-Integrated Manufacturing; Prentice Hall Press: Upper Saddle River, NJ, USA, 2007. [Google Scholar]

- Lee, J.D.; See, K.A. Trust in automation: Designing for appropriate reliance. Hum. Factors 2004, 46, 50–80. [Google Scholar] [CrossRef]

- Miller, C.A.; Parasuraman, R. Designing for flexible interaction between humans and automation: Delegation interfaces for supervisory control. Hum. Factors. 2007, 49, 57–75. [Google Scholar] [CrossRef]

- Sheridan, T.B. Man-vehicle control. In Monitoring Behavior and Supervisory Control; Springer Science & Business Media: Berlin, Germany, 2013; pp. 3–12. [Google Scholar]

- Cummings, M.L.; Guerlain, S. Developing operator capacity estimates for supervisory control of autonomous vehicles. Hum. Factors 2007, 49, 1–15. [Google Scholar] [CrossRef] [PubMed]

- Chen, J.Y.; Barnes, M.J. Supervisory control of multiple robots: Effects of imperfect automation and individual differences. Hum. Factors 2012, 54, 157–174. [Google Scholar] [CrossRef] [PubMed]

- Nakhaeinia, D.; Tang, S.H.; Noor, S.M.; Motlagh, O. A review of control architectures for autonomous navigation of mobile robots. Hum. Factors 2011, 6, 169–174. [Google Scholar]

- Ma, Z.; Wang, S.; Xu, X.; Xiao, F. A supervisory control strategy for building cooling water systems for practical and real time applications. Energy Convers. Manag. 2008, 49, 2324–2336. [Google Scholar] [CrossRef]

- Stouffer, K.; Falco, J. Guide to Supervisory Control and Data Acquisition (SCADA) and Industrial Control Systems Security; NIST: Gaithersburg, MD, USA, 2006. [Google Scholar]

- Muir, B.M. Trust in automation: Part, I. Theoretical issues in the study of trust and human intervention in automated systems. Ergonomics 1994, 37, 1905–1922. [Google Scholar] [CrossRef]

- Strub, P.J.; Priest, T.B. Two patterns of establishing trust: The marijuana user. Soc. Focus 1976, 9, 399–411. [Google Scholar] [CrossRef]

- Lee, K.C.; Kang, I.; Mcknight, D.H. Transfer from offline trust to key online perceptions: An empirical study. IEEE Trans. Eng. Manag. 2007, 54, 729–741. [Google Scholar] [CrossRef]

- Stewart, K.J. Trust transfer on the world wide web. Organ. Sci. 2003, 14, 5–17. [Google Scholar] [CrossRef]

- Cheng, X.; Macaulay, L. Exploring individual trust factors in computer mediated group collaboration: A case study approach. Group Decis. Negotiat. 2014, 23, 533–560. [Google Scholar] [CrossRef]

- Cheng, X.; Gu, Y.; Shen, J. An integrated view of particularized trust in social commerce: An empirical investigation. Int. J. Inform. Manag. 2019, 45, 1–12. [Google Scholar] [CrossRef]

- Lu, Y.; Yang, S.; Chau, P.Y.K.; Cao, Y. Dynamics between the trust transfer process and intention to use mobile payment services: A cross-environment perspective. Inform. Manag. 2011, 48, 393–403. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló Luis, V.; Flavián, C.; Schepers, J. Trust transfer in the continued usage of public e-services. Inform. Manag. 2014, 51, 627–640. [Google Scholar] [CrossRef] [Green Version]

- Teo, T.S.H.; Srivastava, S.C.; Jiang, L. Trust and electronic government success: An empirical study. J. Manag. Inform. Syst. 2008, 25, 99–132. [Google Scholar] [CrossRef]

- Campbell, Y.; Ramadorai, T.; Ranish, B. Getting Better or Feeling Better? How Equity Investors Respond to Investment Experiences; National Bureau of Economic Research, Inc.: Cambridge, MA, USA, 2014. [Google Scholar]

- Kim, D.J.; Ferrin, D.L.; Rao, H.R. A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decis. Support Syst. 2008, 44, 544–564. [Google Scholar] [CrossRef]

- Kim, H.W.; Xu, Y.; Koh, J. A comparison of online trust building factors between potential customers and repeat customers. J. Assoc. Inf. Syst. 2004, 5, 392–420. [Google Scholar] [CrossRef]

- Chen, S.C.; Dhillon, G.S. Interpreting dimensions of consumer trust in e-commerce. Inform. Technol. Manag. 2003, 4, 303–318. [Google Scholar] [CrossRef]

- Greiner, M.E.; Wang, H. Building consumer-to-consumer trust in e-finance marketplaces: An empirical analysis. Int. J. Electron. Commer. 2010, 15, 105–136. [Google Scholar] [CrossRef]

- Kim, G.M.; Shin, B.; Lee, H.G. Understanding dynamics between initial trust and usage intentions of mobile banking. Inform. Syst. J. 2009, 19, 283–311. [Google Scholar] [CrossRef]

- Guo, F.; Cheng, X.; Zhang, Y. A conceptual model of trust influencing factors in robo-advisor products: A qualitative study. In Proceedings of the WHICB 2019 Conference, Wuhan, China, 25–26 May 2019. [Google Scholar]

- Eastlick, M.A.; Lotz, S.L.; Warrington, P. Understanding online B-to-C relationships: An integrated model of privacy concerns, trust, and commitment. J. Bus. Res. 2006, 59, 877–886. [Google Scholar] [CrossRef]

- Salo, A. Robo Advisor, Your Reliable Partner? Building a Trustworthy Digital Investment Management Service. Master’s Thesis, University of Tampere, Tampere, Finland, 2017. [Google Scholar]

- Oliveira, D.F.; Chan, K.S. The effects of trust and influence on the spreading of low and high quality information. Physica A 2019, 525, 657–663. [Google Scholar] [CrossRef] [Green Version]

- Delone, W.H.; McLean, E.R. The DeLone and McLean model of information systems success: A ten-year update. J. Manag. Inform. Syst. 2003, 19, 9–30. [Google Scholar]

- McKnight, D.H.; Lankton, N.K.; Nicolaou, A.; Price, J. Distinguishing the effects of B2B information quality, system quality, and service outcome quality on trust and distrust. J. Strateg. Inform. Syst. 2017, 26, 118–141. [Google Scholar] [CrossRef]

- Zhang, Z.; Gu, C. Effects of consumer social interaction on trust in online group-buying contexts: An empirical study in China. J. Electron. Commer. Res. 2015, 16, 1. [Google Scholar]

- Zhou, T. An empirical examination of initial trust in mobile banking. Internet Res. 2011, 21, 527–540. [Google Scholar] [CrossRef]

- Paglieri, F.; Castelfranchi, C.; da Costa Pereira, C.; Falcone, R.; Tettamanzi, A.; Villata, S. Trusting the messenger because of the message: Feedback dynamics from information quality to source evaluation. Comput. Math. Organ. Theory 2014, 20, 176–194. [Google Scholar] [CrossRef]

- Zeithaml, V.A.; Berry, L.L.; Parasuraman, A. The behavioral consequences of service quality. J. Market. 1996, 60, 31–46. [Google Scholar] [CrossRef]

- De Ruyter, K.; Wetzels, M.; Kleijnen, M. Customer adoption of e-service: An experimental study. Int. J. Serv. Ind. Manag. 2001, 12, 184–207. [Google Scholar] [CrossRef]

- Wang, E.S.T.; Lin, R.L. Perceived quality factors of location-based apps on trust, perceived privacy risk, and continuous usage intention. Behav. Inform. Technol. 2017, 36, 2–10. [Google Scholar] [CrossRef]

- Park, J.; Lee, J.; Lee, H.; Truex, D. Exploring the impact of communication effectiveness on service quality, trust and relationship commitment in IT services. Int. J. Inform. Manag. 2012, 32, 459–468. [Google Scholar] [CrossRef]

- Chang, M.K.; Cheung, W.; Lai, V.S. Literature derived reference models for the adoption of online shopping. Inform. Manag. 2005, 42, 543–559. [Google Scholar] [CrossRef]

- Oliveira, T.; Martins, M.F. Literature review of information technology adoption models at firm level. Electron. J. Inform. Syst. Eval. 2011, 14, 110. [Google Scholar]

- Lin, J.S.C.; Chang, H.C. The role of technology readiness in self-service technology acceptance. Manag. Serv. Quality Int. J. 2011, 21, 424–444. [Google Scholar] [CrossRef]

- Goldsmith, R.E.; Hofacker, C.F. Measuring consumer innovativeness. J. Acad. Market. Sci. 1991, 19, 209–221. [Google Scholar] [CrossRef]

- Parasuraman, A. Technology Readiness Index (TRI) a multiple-item scale to measure readiness to embrace new technologies. J. Serv. Res. 2000, 2, 307–320. [Google Scholar] [CrossRef]

- Leong, K.; Sung, A. FinTech (Financial Technology): What is it and how to use Technologies to create business value in fintech way? Int. J. Innov. Manag.Technol. 2018, 9, 74–78. [Google Scholar] [CrossRef]

- Wetzels, M.; De Ruyter, K.; Van Birgelen, M. Marketing service relationships: The role of commitment. J. Bus. Ind. Mark. 1998, 13, 406–423. [Google Scholar] [CrossRef]

- Shneiderman, B. Designing trust into online experiences. Commun. ACM 2000, 43, 57–59. [Google Scholar] [CrossRef]

- Jøsang, A.; Keser, C.; Dimitrakos, T. Can we manage trust? In International Conference on Trust Management; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Wu, J.J.; Chang, Y.S. Effect of transaction trust on e-commerce relationships between travel agencies. Tourism Manag. 2006, 27, 1253–1261. [Google Scholar] [CrossRef]

- Munoz-Leiva, F.; Luque-Martínez, T.; Sanchez-Fernandez, J. How to improve trust toward electronic banking. Online Inform. Rev. 2010, 34, 907–934. [Google Scholar] [CrossRef]

- Salo, J.; Karjaluoto, H. A conceptual model of trust in the online environment. Online Inform. Rev. 2007, 31, 604–621. [Google Scholar] [CrossRef]

- Poortinga, W.; Pidgeon, N.F. Exploring the dimensionality of trust in risk regulation. Risk Anal. Int. J. 2003, 23, 961–972. [Google Scholar] [CrossRef]

- Siau, K.; Shen, Z. Building customer trust in mobile commerce. Commun. ACM 2003, 46, 91–94. [Google Scholar] [CrossRef]

- McKnight, D.H.; Choudhury, V.; Kacmar, C. The impact of initial consumer trust on intentions to transact with a web site: A trust building model. J. Strategic Inf. Syst. 2002, 11, 297–323. [Google Scholar] [CrossRef]

- Van der Heijden, H.; Verhagen, T.; Creemers, M. Understanding online purchase intentions: Contributions from technology and trust perspectives. Eur. J. Inform. Syst. 2003, 12, 41–48. [Google Scholar] [CrossRef]

- Li, X.; Hess, T.J.; Valacich, J.S. Why do we trust new technology? A study of initial trust formation with organizational information systems. J. Strateg. Inf. Syst. 2008, 17, 39–71. [Google Scholar] [CrossRef]

- Parasuraman, R.; Sheridan, T.B.; Wickens, C.D. Situationawareness, mental workload, and trust in automation: Viable, empirically supported cognitive engineering constructs. J. Cognit. Engin. Decis. Making 2008, 2, 140–160. [Google Scholar] [CrossRef]

- Muir, B.M. Trust between humans and machines, and the design of decision aids. Int. J. Man Mach. Stud. 1987, 27, 527–539. [Google Scholar] [CrossRef]

- Benartzi, S.; Thaler, R.H. How much is investor autonomy worth? J. Financ. 2002, 57, 1593–1616. [Google Scholar] [CrossRef]

- Walsh, G.; Beatty, S.E. Customer-based corporate reputation of a service firm: Scale development and validation. J. Acad. Market. Sci. 2007, 35, 127–143. [Google Scholar] [CrossRef]

- Ding, D.X.; Hu, P.J.H.; Sheng, O.R.L. E-SELFQUAL: A scale for measuring online self-service quality. J. Bus. Res. 2011, 64, 508–515. [Google Scholar] [CrossRef]

- Zhu, K.; Kraemer, K.L.; Dedrick, J. Information technology payoff in e-business environments: An international perspective on value creation of e-business in the financial services industry. J. Manag. Syst. 2004, 21, 17–54. [Google Scholar] [CrossRef]

- Fang, Y.; Qureshi, I.; Sun, H.; McCole, P.; Ramsey, E.; Lim, K.H. Trust, satisfaction, and online repurchase intention: The moderating role of perceived effectiveness of e-commerce institutional mechanisms. MIS Q. 2014, 38, 407–427. [Google Scholar] [CrossRef]

Figure 1.

Research model.

Figure 2.

Revised model of trust influencing mechanism of robo-advisors.

Table 1.

Keywords extracted from interviews.

| Keywords | Frequency | Keywords | Frequency | Keywords | Frequency |

|---|---|---|---|---|---|

| Attitude toward AI | 24 | Rate of return | 14 | Privacy policy | 5 |

| Reputation | 25 | Ease of use | 14 | Interface design | 4 |

| Government regulation | 21 | Integrity | 13 | Technological capability | 4 |

| Information quality | 18 | Competence | 8 | Financial transparency | 4 |

| Service commitment | 18 | Convenience | 7 | Investment environment | 3 |

| Habitual behavior | 6 | Benevolence | 3 |

Table 2.

Six salient trust influencing factors of robo-advisors.

| Categories | Factors | Descriptions |

|---|---|---|

| Deposition | Attitude toward AI | Tendency to believe or suspect based on artificial intelligence (AI). |

| Situational normality | Reputation | Positive feedback from peer customers and social media. |

| Information quality | Accuracy and completeness of customized investment information. | |

| Service quality | Service accessibility, security and reliability. | |

| Structural assurance | Service commitment | Readability of the service provisions. |

| Government regulation | Establishing regulatory policy for robo-advisors from the government. |

Table 3.

Demographic information of research sample.

| Items | Category | Frequency | Ratio |

|---|---|---|---|

| Gender | Female | 148 | 64.35% |

| Male | 82 | 35.65% | |

| Age | Below 20 | 37 | 16.09% |

| 20–30 | 118 | 51.3% | |

| 30–40 | 22 | 9.57% | |

| Above 40 | 53 | 23.04% | |

| Investment Experience | 0–2 years | 167 | 72.61% |

| 2–4 years | 19 | 8.26% | |

| 4–6 years | 13 | 5.65% | |

| Above 6 years | 31 | 13.48% |

Table 4.

Results of reliability analysis and convergent validity.

| Latent Variables | Indicators | Loadings | CA | CR | AVE |

|---|---|---|---|---|---|

| Reputation (RE) | RE1 | 0.89 | 0.876 | 0.924 | 0.802 |

| RE2 | 0.911 | ||||

| RE3 | 0.885 | ||||

| Information Quality (IQ) | IQ1 | 0.925 | 0.906 | 0.941 | 0.842 |

| IQ2 | 0.93 | ||||

| IQ3 | 0.898 | ||||

| Service Quality (SQ) | SQ1 | 0.906 | 0.901 | 0.938 | 0.835 |

| SQ2 | 0.936 | ||||

| SQ3 | 0.899 | ||||

| Attitudes to AI (AA) | AA1 | 0.892 | 0.803 | 0.884 | 0.717 |

| AA2 | 0.797 | ||||

| AA3 | 0.849 | ||||

| Service Commitment (SC) | SC1 | 0.924 | 0.924 | 0.952 | 0.868 |

| SC2 | 0.945 | ||||

| SC3 | 0.926 | ||||

| Government Regulation (GR) | GR1 | 0.873 | 0.813 | 0.887 | 0.724 |

| GR2 | 0.883 | ||||

| GR3 | 0.794 | ||||

| Trust in Vendor (TV) | TV1 | 0.931 | 0.897 | 0.936 | 0.83 |

| TV2 | 0.892 | ||||

| TV3 | 0.909 | ||||

| Trust in Technologies (TT) | TT1 | 0.91 | 0.781 | 0.874 | 0.703 |

| TT2 | 0.657 | ||||

| TT3 | 0.921 | ||||

| Supervisory Control (SCO) | SCO1 | 0.918 | 0.887 | 0.93 | 0.816 |

| SCO2 | 0.89 | ||||

| SCO3 | 0.901 | ||||

| Trust in Robo-Advisor (TR) | TR1 | 0.905 | 0.887 | 0.93 | 0.816 |

| TR2 | 0.938 | ||||

| TR3 | 0.864 |

Table 5.

Results of discriminant validity.

| RE | IQ | SQ | AA | SC | GR | TV | TT | SCO | TR | SQAVE | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| RE | 0.846 | 0.846 | |||||||||

| IQ | 0.615 | 0.850 | 0.850 | ||||||||

| SQ | 0.564 | 0.638 | 0.917 | 0.917 | |||||||

| AA | 0.545 | 0.645 | 0.8 | 0.895 | 0.895 | ||||||

| SC | 0.451 | 0.508 | 0.809 | 0.777 | 0.931 | 0.931 | |||||

| GR | 0.567 | 0.634 | 0.856 | 0.804 | 0.8 | 0.913 | 0.913 | ||||

| TV | 0.677 | 0.616 | 0.593 | 0.56 | 0.501 | 0.575 | 0.903 | 0.903 | |||

| TT | 0.574 | 0.628 | 0.693 | 0.673 | 0.686 | 0.694 | 0.62 | 0.903 | 0.903 | ||

| SCO | 0.752 | 0.686 | 0.592 | 0.54 | 0.479 | 0.578 | 0.713 | 0.7 | 0.838 | 0.519 | 0.838 |

| TR | 0.496 | 0.541 | 0.817 | 0.766 | 0.893 | 0.811 | 0.567 | 0.717 | 0.519 | 0.911 | 0.911 |

Table 6.

Results of hypotheses testing.

| Hypotheses | Casual Path (CP) | Mean (M) | Standard Deviation Value (STDEV) | Path Coefficient (β) | t-Values | p-Values |

|---|---|---|---|---|---|---|

| H1 | RE→TV | 0.210 | 0.081 | 0.205 | 2.535 | 0.012 |

| H2 | IQ→TV | 0.370 | 0.093 | 0.374 | 4.017 | 0.000 |

| H3 | SQ→TV | 0.326 | 0.092 | 0.327 | 3.535 | 0.000 |

| H4 | AA→TT | 0.405 | 0.065 | 0.406 | 6.262 | 0.000 |

| H5 | SC→TT | 0.059 | 0.062 | 0.063 | 1.016 | 0.310 |

| H6 | GR→TT | 0.254 | 0.063 | 0.255 | 4.047 | 0.000 |

| H7 | TV→TR | 0.481 | 0.062 | 0.484 | 7.846 | 0.000 |

| H8 | TT→TR | 0.451 | 0.070 | 0.448 | 6.368 | 0.000 |

| H9 | SCO→TR | -0.021 | 0.061 | −0.033 | 0.542 | 0.588 |

| SCO→TT | 0.274 | 0.073 | 0.268 | 3.663 | 0.000 |

Table 7.

Comparison of junior investors and senior investors.

| Category | CP | M | STDEV | t-Values | Category | M | STDEV | t-Values |

|---|---|---|---|---|---|---|---|---|

| Junior investors | RE→TV | 0.238 | 0.099 | 2.443 | Senior investors | 0.189 | 0.114 | 1.729 |

| IQ→TV | 0.322 | 0.096 | 3.300 | 0.469 | 0.243 | 2.019 | ||

| SQ→TV | 0.355 | 0.096 | 3.752 | 0.234 | 0.262 | 0.772 | ||

| SC->TT | 0.059 | 0.062 | 0.929 | 0.063 | 0.107 | 0.667 | ||

| GR→TT | 0.301 | 0.060 | 4.965 | 0.479 | 0.139 | 3.310 | ||

| AA→TT | 0.580 | 0.077 | 7.540 | 0.339 | 0.131 | 2.617 | ||

| TV→TR | 0.408 | 0.090 | 4.494 | 0.547 | 0.072 | 7.818 | ||

| TT→TR | 0.431 | 0.103 | 4.184 | 0.331 | 0.118 | 2.788 | ||

| SCO→TT | 0.051 | 0.121 | 0.412 | 0.112 | 0.100 | 1.115 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Cheng, X.; Guo, F.; Chen, J.; Li, K.; Zhang, Y.; Gao, P. Exploring the Trust Influencing Mechanism of Robo-Advisor Service: A Mixed Method Approach. Sustainability 2019, 11, 4917. https://0-doi-org.brum.beds.ac.uk/10.3390/su11184917

AMA Style

Cheng X, Guo F, Chen J, Li K, Zhang Y, Gao P. Exploring the Trust Influencing Mechanism of Robo-Advisor Service: A Mixed Method Approach. Sustainability. 2019; 11(18):4917. https://0-doi-org.brum.beds.ac.uk/10.3390/su11184917

Chicago/Turabian StyleCheng, Xusen, Fei Guo, Jin Chen, Kejiang Li, Yihui Zhang, and Peng Gao. 2019. "Exploring the Trust Influencing Mechanism of Robo-Advisor Service: A Mixed Method Approach" Sustainability 11, no. 18: 4917. https://0-doi-org.brum.beds.ac.uk/10.3390/su11184917

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.