Confucius Institute and the Completion of Chinese Cross-Border Acquisitions

School of Economics and Management, Dalian University of Technology, Dalian 116024, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(18), 5088; https://0-doi-org.brum.beds.ac.uk/10.3390/su11185088

Submission received: 29 July 2019

/

Revised: 26 August 2019

/

Accepted: 13 September 2019

/

Published: 17 September 2019

(This article belongs to the Collection Cultural Crossovers and Social Sustainability)

Abstract

:As a global platform for cultural exchange, the Confucius Institute (CI) has effectively promoted sustainable development among countries and regions. However, existing literature has mostly drawn insights from the national macro-level to study the roles played by CIs, whereas the potential of CIs to influence corporate behaviors has not received extensive attention. This study expands the research on CIs from the national macro-level to the enterprise micro-level by exploring the effect of CIs on the likelihood of acquisition completion. Using data from 1695 Chinese cross-border acquisitions from 2006 to 2017, we find that establishment of CIs can significantly increase acquisition completion likelihood. Furthermore, the level of influence of CIs on acquisition completion depends on country- and firm- level factors. At the country level, the positive effect of CIs on completion likelihood intensifies when cultural distance between host countries and China is great. At the firm level, the acquirer’s past cross-border acquisition experience moderates the effects of CIs, which are more beneficial to firms with no previous successes. In addition, we have made some further analyses, and find that the presence of CIs not only helps to increase the likelihood of acquisitions completion, but also helps to shorten the acquisition durations. The role of CIs in cross-border acquisition completion likelihood do not depend on the types of Chinse enterprises, which indicates that CIs, unlike government agencies, do not offer additional help for SOEs.

1. Introduction

The Confucius Institute (CI), launched by Hanban (The Confucius Institute Headquarters), has expended considerable efforts to promote the Chinese language and culture, spread Sinology, and facilitate cultural exchange [1]. It has become a global platform for Chinese teaching and the popularization of Chinese culture, enabling foreigners to gain a deeper and more direct understanding of China [2]. By the end of 2017, 525 CIs and 1113 Confucius Classrooms (mostly satellite facilities associated with CIs) had been established in 146 countries or regions (The regions indicate Special Administrate Region, such as Hong Kong (Hong Kong Special Administrative Region of the People’s Republic of China)) [3]. With the rapid expansion of the CI network, increasing numbers of scholars have started to pay attention to the influence of CIs on international business relationships between China and the rest of world, particularly with regard to foreign direct investment (FDI) [4,5,6,7].

Since China launched its “go global” initiative in 2001, cross-border mergers and acquisitions (hereafter referred to as “acquisitions”) have constituted crucial element of Chinese outward FDI, because nearly half of Chinese outward FDI is delivered through acquisitions [8]. However, a substantial percentage of acquisitions are abandoned in the pre-completion due to differences in culture, language, and business practices among countries [9]. This thus raises the following question: acting as a platform for cultural exchange, could CIs established in a host country affect the likelihood of cross-border acquisition completion by Chinese multinational enterprises (MNEs)?

Recent studies on CIs have focused on investigating their influence on international relationships between China and other countries. Their findings suggest that CIs play an active role in boosting FDI and exports from China [5,7], promoting China’s higher education institutes in other countries [2], and attracting more tourists to China [10,11]. In general, these studies have mostly drawn insights from the national macro-level to study the roles played by CIs, whereas literature on the potential for CIs to influence corporate behaviors is limited. We address this gap in the literature by investigating the possible effects of CIs on Chinese enterprises’ cross-border acquisitions.

Cross-border acquisitions constitute a critical top-level managerial strategy of MNEs [12], and their completion or abandonment is mostly influenced by country-, deal- and firm-level factors, such as bilateral relationship [13], cultural distance [14] and information asymmetry [15,16,17]. However, CIs can play a vital role in these aspects. For example, CIs can shrink the cultural distance between two countries to reduce cultural friction [5], provide Chinese language lessons to senior managers of enterprises in the host countries to reduce negotiation costs, and act as an information exchange platform to alleviate information asymmetry [5]. Thus, we expect that the presence of CIs in host countries promotes the likelihood of success in cross-border acquisitions among Chinese MNEs.

However, some scholars sometimes express suspicion that CIs established in the host countries are the agents of Chinese government, which may be intervened by government. In fact, CIs has a high degree of independence in its establishment and operation. On the one hand, according to its Constitution and by-laws, CI is a non-profit organization dedicated to strengthening educational and cultural exchanges and cooperation between China and other countries, deepening friendly relationships with other nations. On the other hand, from the opening process of CIs, applications are usually submitted by foreign organizations which are interested in opening a CI. Although the start-up funding of CIs is provided by Hanban, it should be hosted by the foreign partner organizations. In addition, Lien and Oh (2014) investigated the factors determining the successful establishment of a CI, and found that sufficient local demand for learning Chinese language and culture is an important factor affecting the establishment of CIs [18]. Akhtaruzzaman et al. (2017) empirically examined the effects of CIs on FDI outflows from China to Africa, and revealed that establishment of CIs in Africa is not motivated by natural resource seeking of Chinese government [7].

In this paper, we use Chinese MNEs’ cross-border acquisitions to demonstrate the influence of CIs and to explain why and how the presence of CIs affects the likelihood of acquisition completion. For a more thorough exploration of the proposed relationship, we further consider some country- and firm- level moderating factors, such as the effect of cultural distance between China and the host country as well as acquirer’s past cross-border acquisition experience. Considering cross-border acquisitions by Chinese MNEs between January 2006 and December 2017, we find that the establishment of CIs significantly increases the likelihood of success in these deals. The positive effect of CIs on completion likelihood is more prominent when the cultural distance is relatively great. The acquirer’s cross-border acquisition experience moderates the effects of CIs: CIs play a greater role for Chinese MNEs that do not have successful cross-border acquisition experience. In addition, the results of the additional analyses demonstrate that the presence of CIs not only helps to increase the likelihood of acquisitions completion, but also helps to shorten the acquisition durations. The role of CIs in cross-border acquisition completion likelihood do not depend on the types of Chinse enterprises, which means that CIs, unlike government agencies, do not offer additional help for SOEs.

This study provides several important contributions. First, our study enriches the literature on CIs. Recently, most studies in this area have focused on the effect of CIs at the national macro-level, such as the influence on FDI, exports, higher education, and tourism [2,5,6,7,10,11], whereas the potential of CIs to influence cross-border acquisition has not received extensive attention. This study enriches the literature on the economic consequences of CIs by focusing on cross-border acquisitions among Chinese MNEs. This extension is essential because it partly explains the mechanism through which CIs promote international business relationships between China and the rest of the world. Second, this study contributes to the literature on the determinants of cross-border acquisition outcomes. When studying the effect of informal institutional factors (e.g., culture) on cross-border acquisition outcomes, most studies have focused on the cultural distance between the home and host countries from a static perspective [14,19,20,21,22]. However, few studies have analyzed the determinants of cross-border acquisitions from the dynamic perspective of cultural convergence. As a representative of China’s active cultural initiatives, CIs are introduced in the current study to investigate the direct influence of cross-cultural exchange on cross-border acquisitions. Thus, this study takes a crucial step in supplementing the cross-border acquisition literature from the perspective of the home country’s cultural output. Third, the finding of this study can help deepen the understanding of the inherent relationship between cultural convergence and economic development. Cultural exchange is the cornerstone of economic cooperation. Reducing cultural obstacles is conducive to sustainable development in the global economy.

The remainder of this paper is organized as follows. First, we examine the development of CI programs. Next, we present a brief literature review, including literature on the determinants of cross-border acquisition completion as well as the influence of CIs. Subsequently, we propose a series of hypotheses. We then introduce the empirical model, present the data, and discuss the empirical analysis and robustness analyses. After that, we make some further analyses. Finally, we summarize our findings.

2. Development of the Confucius Institute Programs

The Confucius Institute Headquarters in Beijing is referred to as Hanban. Adopting an institute development strategy similar to those adopted by Germany’s Goethe-Institut, France’s Alliance Française, and the British Council, Hanban launched the first CI in Korea in 2004. Since then, the number of CIs has grown rapidly. By the end of 2017, a total of 525 CIs and 1113 Confucius Classrooms had been established in 146 countries and regions. CIs now have 46,200 full-time and part-time native Chinese and indigenous teachers and 1.7 million students from all walks of life. Throughout 2017, the institutes held a total of 42,000 diverse cultural events, with 12.72 million people in attendance [3]. According to Xinhua (2006), Hanban aims to open 1000 CIs by 2020.

According to its Constitution and by-laws, the CI is a non-profit organization dedicated to strengthening educational and cultural exchanges and cooperation between China and other countries, deepening friendly relationships with other nations, and promoting the development of multiculturalism in the world. Establishing a CI entails one of the following three methods: with full investment from Hanban, in cooperation with Chinese institutions, or through franchising authorized by Hanban. Presently, most CIs are established through cooperation between China and a foreign organization [6]. Once a CI is established, it offers diverse language and cultural services, such as providing Chinese language lessons for the presidents or senior managers of foreign companies, providing information on and consulting services related to China’s education opportunities, and conducting language and cultural exchange activities between China and other countries.

In December 2013, the concept of CIs was written into the Resolution of the Sixth Plenum of the 17th Chinese Communist Party’s Central Committee, which has encouraged social organizations and Chinese-funded institutions to be involved in the construction of CIs and to engage in programs for cultural and educational exchange. By the end of 2017, Chinese party leaders and government officials had participated in CI activities hundreds of times and had guided the work there. Moreover, the development of CIs is valued by the leaders of other countries. For example, in October 2017, President Gjorge Ivanov of Macedonia attended and addressed the 3rd China Central and Eastern European Forum, held by a CI at Ss. Cyril and Methodius University in Skopje.

3. Literature Review and Hypothesis Development

3.1. Background Literature on Determinants of Acquisition Completion

Prior literature has investigated various country-, firm-, and deal-level factors that potentially affect the likelihood of deal completion in cross-border acquisitions. At the national level, most studies have focused on formal and informal institutional determinants. Dikova et al. (2010) revealed that a negative relationship exists between institutional distance and the likelihood of acquisition completion; furthermore, they found that differences in national formal and informal institutions can explain part of the variation in the likelihood that an announced cross-border acquisition deal will be completed [14]. Zhang et al. (2011) observed that the success of Chinese overseas acquisitions, measured as the acquisition completion likelihood of Chinese MNEs, is influenced by institutional factors such as the host country’s institutional quality, institutional restrictions in the target industry, and institutional constraints of acquiring firms [23]. Zhou et al. (2016) demonstrated that the larger the country distance, such as differences in laws, regulations, and risk levels, between developed and emerging countries is, the higher the acquisition completion failure rate is [9]. In addition, several researchers have argued that some publicly announced cross-border acquisition deals were abandoned due to differences in national culture between the home and host countries [19,20,21,24]. Consistent with the findings of other empirical studies, Popli et al. (2016) revealed that cultural distance between host and home countries has a negative effect on the likelihood of cross-border acquisition completion, but this negative relationship is mitigated by the cultural experience reserve [25].

At the firm level, previous cross-border acquisition experience becomes a salient factor. Many scholars have revealed that experience can increase the likelihood of acquisition completion, and they have suggested that experience can help MNEs in dealing with the complexity of the pre-acquisition process [14,25,26]. Moreover, state ownership can influence cross-border acquisitions. On the basis of 421 Chinese cross-border acquisitions, Chen and Guo (2016) reported that state-owned enterprises (SOEs) have a higher likelihood of acquisition completion than do other types of firms. They further indicated that compared with other types of enterprises, SOEs receive more support from governments, particularly in terms of low-interest financing, favorable exchange rates, reduced taxation, and subsidized insurance [27]. By contrast, from the perspective of legitimacy concerns, Li et al. (2017) showed that SOEs, which are regarded as agents of their home countries’ governments, experience a lower likelihood of acquisition completion than do other foreign firms [28]. Li et al. (2019) suggested that opaqueness, or the lack of transparency, is the main factor behind this phenomenon. [17].

At the deal level, Lim and Lee (2016) demonstrated that firms targeting related industries that engage in cross-border acquisitions are more likely to complete a deal than do firms targeting unrelated industries [29]. Huang et al. (2016) showed that the use of stock (instead of cash) as the method of payment in cross-border acquisitions is associated with a lower likelihood of acquisition completion [16]. In addition, some studies have revealed that other acquisition deal characteristics, such as acquisitions attitude [30] and the trust between acquirers and targets [31], can affect the likelihood of the acquisition completion.

3.2. Background Literature on Effects of Confucius Institutes

Empirical studies have been conducted on the role of CIs at the macro level. Akhtaruzzaman et al. (2017) suggested that CIs are indeed an effective instrument for increasing China’s soft power, but they indicated that this soft power is not motivated solely (if at all) by resource seeking [7]. Lien et al. (2012) investigated the empirical effects of the presence of CIs on Chinese outward FDI flows and trade. They found that the presence of CIs has a positive effect on FDI from China and Chinese exports to developing countries. Compared with exports, the effect of CIs on FDI is stronger [5]. Lien and Co (2013) showed that CIs help promote U.S. exports to China, which is strong evidence of the direct economic benefits CIs bring to the United State [6]. On the Chinese teaching aspect, Lien (2013) showed that CIs successfully induce more individuals in host countries to learn Chinese; host countries can thus benefit from the establishment of a CI [32]. Moreover, Lien and Miao (2018) examined the effects of a CI on the foreign students of its Chinese partner university in China. They found that Chinese partner universities have a significantly positive effect on non-degree-seeking foreign students [2]. Regarding the tourist flow, Lien et al. (2014) demonstrated that CIs, as a comprehensive platform for China’s foreign cultural exchange, have a significantly positive effect on China’s tourist flows [10].

3.3. Hypothesis Development

In this study, we argue that CIs influence the likelihood of cross-border acquisition completion among Chinese MNEs through three mechanisms. First, CIs established in host countries can shorten the cultural distance between China and the host countries. Cultural differences are likely to be particularly prominent in cross-border acquisitions, where people with possibly conflicting values have to coordinate with one another [14,24]. Similar to geographic distance, a larger cultural distance between acquisition firms can reduce the likelihood of a successful acquisition [24]. However, the establishment of CIs could promote cultural exchange between China and the rest of world. As a comprehensive platform for China’s foreign cultural exchange, CIs enable foreign publics to develop a deeper and more direct understanding of China [2]. Through branded projects and various activities, CIs effectively bridge cultural gaps between China and their host countries [11]. For example, each year, the Confucius Institute Conference and dozens of regional and national conferences are held to showcase China’s diverse culture. Furthermore, in 2017, more than 42,000 activities and performances were organized across 1600 CIs and Confucius Classrooms, attracting more than 12.72 million participants. These activities can increase foreigners’ understanding of Chinese culture, reduce the cultural distance between the host country and China, and improve the likelihood of cross-border acquisition completion among Chinese MNEs.

Second, CIs established in host countries can reduce the negotiation costs associated with merging two firms across borders. Language differences are a major factor hindering cross-border acquisitions [24]. Kim et al. (2015) suggested that language differences between two countries can lead domestic entrepreneurs to communicate ineffectively with their foreign counterparts, which may increase negotiation costs [33]. However, the establishment of CIs can offer substantial educational support for foreigners who wish to learn Chinese in their home countries [5], particularly for senior managers of the host countries’ enterprises. For example, Business Confucius Institutes, providing professional Chinese training for senior managers, have been established in Britain, the United States, Greece, Denmark, and other countries [3]. With the advancement of Chinese language training at CIs, increasing numbers of senior managers of foreign enterprises will become familiar with Chinese. Therefore, the negotiation cost of cross-border acquisitions between Chinese MNEs and foreign enterprises may drop and the likelihood of acquisition completion could correspondingly increase.

Third, the presence of CIs can reduce information asymmetry between Chinese MNEs and foreign enterprises, which may lower the information searching costs of cross-border acquisitions. Boeh (2011) found that information asymmetry for cross-border acquisitions is significantly higher than that for domestic acquisitions due to the differences in cultural, legal, and management norms [34]. In a cross-border acquisition deal, the acquirer must obtain relevant information of the foreign enterprise, industry, and host country to make a reasonable valuation of the target [17]. Information asymmetry between acquirers and targets creates complications and considerable uncertainty, which may lead to the abandonment of the acquisition [14]. However, CIs can serve as an information exchange platform, which could help reduce acquisition information asymmetry between acquirers and targets. Lien et al. (2012) also reported that the presence of CIs could allow the exchange of vital business information for both sides [5]. For example, when preparing to acquire a foreign company, Chinese MNEs can collect some local information, such as host government regulations, market access information, and local customs, by communicating with teachers or students at local CIs. Furthermore, CIs typically organize various business activities in the host country, which can strengthen information sharing between Chinese and foreign parties, thereby reducing the information asymmetry caused by cultural distance. In short, the information asymmetry between acquirers and targets could be reduced through the platform function of CIs.

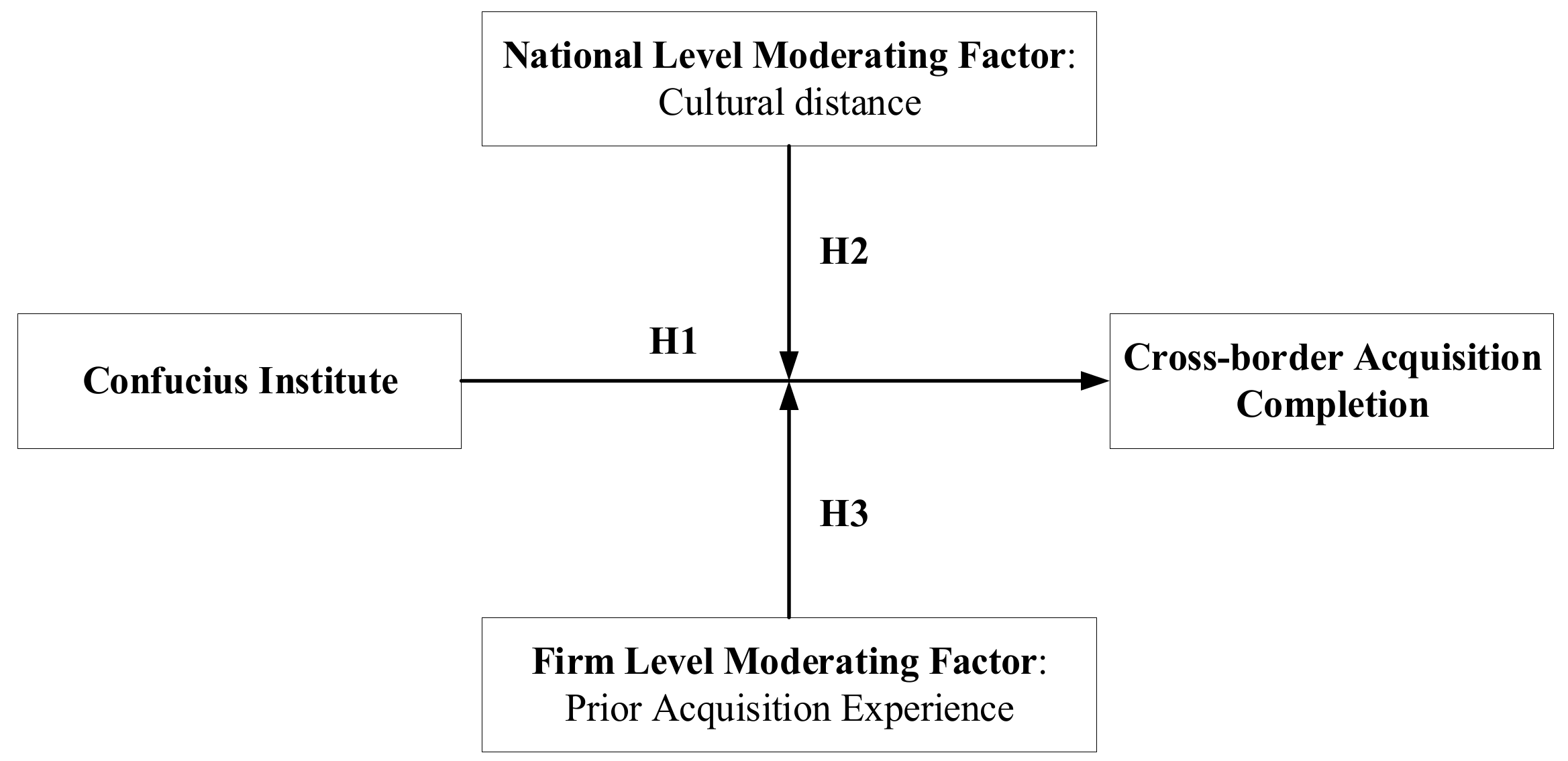

In summary, we suggest that the establishment of CIs in host countries could increase the likelihood of Chinese cross-border acquisition completion. Accordingly, we propose the following hypothesis:

Hypothesis 1:

A positive relationship exists between the presence of CIs and the likelihood of cross-border acquisition completion among Chinese MNEs.

Although CIs has made efforts to promote cultural exchange between China and the rest of world, the role of CIs may vary from country to country because of the inherent similarities between Chinese culture and some other countries’ cultures (such as Singapore). Given the importance of cultural differences in cross-border acquisition activities, we argue that the effect of CIs on acquisition completion could be contingent on the extent of cultural similarity between China and host country.

Countries have their own cultural identities. People in different countries often speak different languages, have different religions [35]. In a cross-border setting, Ahern et al. (2015) noted that cultural distance between acquisition firms could reduce the acquisition completion likelihood [24]. Larger cultural difference would lead to greater difficulties during the acquisition and result in conflict [36]. Compared with cross-border acquisitions in a culturally similar environment, acquisitions occurring in a culturally dissimilar environment may face more cultural friction. For example, Popli et al. (2016) revealed that cross-cultural acquisitions would be more complex due to unconscious cultural blindness and a lack of cultural knowledge [25]. However, as an institution that promotes Chinese culture, CIs established in culturally dissimilar countries may effectively bridge cultural gaps, which can weaken the negative effect of cultural distance in acquisitions.

In contrast, when cross-border acquisitions take place in culturally similar countries, cultural difference may not be the key factor affecting the acquisition completion likelihood because the target firms are familiar with Chinese culture [37]. In this context, the marginal effect of CIs to promote acquisition completion likelihood may be relatively low. Hence, we suppose that the benefits of CIs may be greater in cross-border acquisitions undertaken in culturally dissimilar countries. Accordingly, we propose the following hypothesis:

Hypothesis 2:

Cultural distance moderates the effect of the presence of CIs on the likelihood of cross-border acquisition completion among Chinese MNEs, where the positive relationship becomes stronger when cultural distance is relatively high.

A rich body of acquisition literature has demonstrated that prior experience helps firms learn from and overcome international challenges, increasing their odds of success in subsequent and similar international initiatives [38,39,40]. Therefore, we argue that the effect of CIs on acquisition completion could depend on prior cross-border acquisition experience.

Compared with MNEs that have prior cross-border acquisition experience, MNEs without this experience face more cultural friction in their host countries [14,25,26,28]. For example, they may have more difficulty in dealing with the different languages and religions and may not be able to establish effective communications with the senior managers of target firms [14]. However, CIs can provide professional Chinese training to senior managers, which can weaken the negative effect of inexperience in acquisition negotiations. Additionally, previous acquisition experience enables MNEs to collect information and adapt to the host institutional environment more rapidly [9]. By contrast, MNEs without experience may not possess sufficient capacity to handle issues, leading to legitimacy concerns in their subsequent acquisition activities [28]. As an information exchange platform, CIs can offer valuable information to Chinese MNEs, such as relevant government regulations, market access information, and details of the local customs [5]. This information may help inexperienced Chinese MNEs reduce the number of errors they make and enable them to make appropriate choices in response to local challenges. Hence, we expect that Chinese MNEs’ prior cross-border acquisition experience has a stronger substitution effect for the role of CIs. Specifically, CIs play a greater role for Chinese MNEs without previous cross-border acquisition experience in promoting the likelihood of acquisition completion. Accordingly, we propose the following hypothesis:

Hypothesis 3:

The acquirer’s prior cross-border acquisition experience moderates the effect of the presence of CIs on the likelihood of cross-border acquisition completion, where the positive relationship intensifies when the Chinese MNEs have no cross-border acquisition experience.

Figure 1 shows the conceptual model of this paper. We explore the effect of CIs on the likelihood of acquisition completion (H1). We further test the moderating effects of cultural distance (H2) and acquirer’s prior cross-border acquisition experience (H3).

4. Data and Methodology

4.1. Data and Sample

We derive a sample of cross-border acquisition activities in China that occurred between January 2006 and December 2017 from the Zephyr by Bureau Van Dijk (BvD) database, which has been used in earlier studies [26,41,42,43]. This database offers information on acquisition deal status; deal value; dates of the announcement and completion of the acquisition; and some information on the acquirers and targets, such as the company’s name, ownership, and industry. The number of CIs acting in these areas is collected from the official website of Hanban (http://www.hanban.edu.cn). The GDP growth rate, the host country population and information on the institutional environment of the host country are obtained from the World Bank database. Data on exchange rate for each country are retrieved from the International Monetary Fund. The BIT data are gathered from the website of the Ministry of Commerce of China (http://www.mofcom.gov.cn). The data of geography are from the CEPII database. We set our observation window to span the 12-year period from 2006 to 2017 because Hanban began releasing an annual report on CIs in 2006.

The sample meets the following criteria:

- (1)

- The acquirer must be a Chinese firm, and the target must be a non-Chinese firm.

- (2)

- Deal status should include “announced”, “completed”, “pending” and “withdrawn”, whereas “rumor” should be excluded.

- (3)

- Cross-border acquisitions in tax havens (Bermuda, Cayman Islands and British Virgin Islands) must be excluded.

- (4)

- Samples with missing data must be excluded.

The screening of the Zephyr database for criteria (1) through (4) yields 1695 observations across 39 target countries and regions.

4.2. Measurement

4.2.1. Dependent Variable

4.2.2. Independent and Moderating Variables

Following previous research [5], CI is considered as an independent variable, measured by the number of CIs per capita in each host country. Specifically, CI is defined as the number of CIs divided by country population (hundred million). The information on the number of CIs is obtained from the official website of Hanban.

Cultural distance is measured through the Kogut and Singh (1988) index [44], which is based on Hofstede’ s four cultural dimensions [45]: power distance, individualism, masculinity, and uncertainty avoidance. The variance of each dimension is taken into consideration in the calculation, as follows: , where

and

denote the cultural scores of both the home and host countries on cultural dimension i.

is the variance of each dimension across the whole sample.

Non-experience, the other moderating variable, is used to control for the effect of learning experience. Consistent with prior research [23], it is operationalized as a dummy variable with a value of 1 if the Chinese MNE does not have past successful cross-border acquisition(s) and a value of 0 otherwise.

4.2.3. Control Variables

Following the literature, we introduce a set of control variables into our model to rule out alternative explanations. We control for some country-, deal-, and firm-level factors that could influence the likelihood of acquisition completion, as outlined subsequently.

BIT, one of the moderating variables, presents whether the Chinese government has signed a BIT with the host country in the year t. Consistent with prior research [46,47], BIT is measured as a dummy variable, which takes a value of 1 after the date of signing a BIT between Chinese government and the host country and is 0 otherwise.

Population is used to capture the size of countries. Consistent with prior research [5], it is measured by the log value of the host country population.

GDP growth indicates the economic condition of the target country, which is measured by the annual GDP growth rate of the host country [16]. Erel et al. (2012) argued that firms from weaker-performing economies tend to be acquired effectively [35].

Institutional environment is used to capture the institutional quality of the host country, which forms a crucial basis for the cross-border acquisition deal [48]. Following earlier research [49], we measure Institutional environment by averaging the six indicators into a single index. The higher that score is, the better the institutional environment is. These six indicators, derived from the World Bank’s Worldwide Governance Indicators, are voice and accountability, political stability, government effectiveness, regulatory quality, rule of law, and control of corruption [50].

Neighbor indicates whether the acquirer and target country or region are neighbors (coded as 1) or not (0), to control for the geography differences. Because geography differences are considered as one of factors that potentially affect the cost of cross-border acquisitions [35,51].

Exchange rate risk indicates the uncertainty about the value of exchange rate between home and host countries. Exchange rate volatility is likely to have an impact on the choice of FDI, and hence to affect cross-border acquisition decisions [52]. We therefore include exchange rate volatility as a factor that can play a role in determining the success of a cross-border acquisition. Consistent with earlier research [52], Exchange rate risk is measured by the standard deviation of exchange rate within 12 months of a year.

Deal size is used to capture the size of the deal, which is measured by the log value of the cross-border acquisition deal [53,54]. Muehlfeld et al. (2007) revealed that high-value deals fall under regulatory scrutiny, which influences acquisition outcomes [30]. A log transformation is used to ensure that the results are not unduly affected by extreme values.

Same industry indicates whether the target and acquirer in an acquisition deal are operating in the same industry. When acquisitions take place across related business, the announced acquisition attempts may engender positive reactions from investors and the market [23]. The variable is a dummy measure with a value of 1 if the target and acquirer belong to the same industry at the two-digit Standard Industrial Classification level and 0 otherwise [28].

Public acquirer is equal to 1 if the Chinese MNE is listed on either the Shanghai Stock Exchange or Shenzhen Stock Exchange [17]. Trang Thu et al. (2018) argued that public firms are more likely to be subject to a greater number of rules and regulations, which may cause difficulties in consummating the deal [53].

Cash payment is equal to 1 if the acquirer offers to pay in cash and 0 otherwise [14,17]. Li et al. revealed that paying in cash may decrease the resistance of the target firm’s shareholders [17].

SOE is coded as a dummy and refers to the ownership of the Chinese MNEs. SOE has a value of 1 if the acquirer is an SOE and 0 otherwise [13]. Li et al. (2017) argued that SOEs regarded as agents of their home countries’ governments experience a lower likelihood of acquisition completion than other foreign firms [28].

Sought percentage is the percentage of ownership stake of a target sought by the acquirer in a transaction [23]. The higher this factor is, the more likely it is at stake for the acquirer’s and target shareholders, which may affect approval procedures and make it more difficult to complete [14].

We also include year and industry dummies to capture any other unobserved effects. Table 1 presents the variables, short explanations, sources of data, and previous studies that have used the respective measures.

4.3. Methods

In this study, we apply a binary logistic regression model to estimate how the likelihood of cross-border acquisition completion among Chinese MNEs is affected by the presence of CIs in the host country [14,17,28]. In addition, to test the moderating effects of Cultural distance and Non-experience, we set two interaction terms. As the sample consists of 1695 deal originating from 1086 firms and including 39 countries and regions, the assumption of lack of independence among the observations may be violated. To control for these within-country and within-firm correlations, we follow prior research [24,55,56], and apply double-cluster standard errors both at country and acquisition firm levels. The basic model is specified as follows:

where i represents the acquisition deal i of Chinese MNEs, j represents the host country j, and t represents the year t.

5. Empirical Results and Discussion

5.1. Descriptive Statistics and Correlation Analyses

Table 2 presents the means, standard deviations, and correlations between key variables. Approximately 42.8% of Chinese MNEs’ cross-border acquisition deals have been completed. The mean of number of CIs per hundred million people is 20.792. In 2017, the United States is shown to have the highest number of CIs (110 in total), whereas Singapore, Sweden, and Norway are revealed to have only one CI established each. Approximately 20.4% of the Chinese MNEs in the sample have at least one prior experience of cross-border acquisition completion. Moreover, the distribution of CIs and the list of destination countries are shown in the Appendix A.

Table 2 also reveals that all of the correlation coefficients are well below the normal cut-off |0.7|. Variance inflation factor (VIF) values are calculated for each independent variable. All VIF values range between 1.03 and 5.32, which are far below the standard threshold of 10. Therefore, the correlation coefficients do not cause major multicollinearity problems [57]. In addition, the correlation between acquisition completion and CI is 0.29, and the p value is less than 0.01, suggesting a positive correlation between the presence of CIs and the likelihood of acquisition completion. The results thus preliminarily support Hypothesis 1.

5.2. Multivariate Regression Analyses

Table 3 presents the results of the logistic regression model for cross-border acquisition completion. Model 1 examines the effects of the presence of CIs (Hypothesis 1) on the likelihood of cross-border acquisition completion. Models 2 and 3 examine the moderating effects between CI and Cultural distance (Hypothesis 2), and between CI and Non-experience (Hypothesis 3) respectively.

In Model 1, the number of CIs per capita is used as the main variable (CI). The coefficient estimate of CI is positive and significant (β = 0.052, p = 0.000). The estimated coefficient of 0.052 means that one unit increase in CI increases the odds ratio of acquisition completion by 5.34% (e0.052 − 1). Translating this into average marginal effect, it means that the acquisition completion likelihood increases average 0.827% when CI increases one unit. In other words, the acquisition completion likelihood increases by 0.827% if one additional CI is established for every hundred million population in the host country. In percentage terms, the acquisition completion likelihood increases average 0.172% when CI per capita increases by one percentage point. It indicates that the presence of CIs established in the host country can increase the likelihood of cross-border acquisition completion among Chinese MNEs. Thus, Hypothesis 1 is supported. In addition, some control variables have significant effects on acquisition completion. Non-experience (β = −1.267, p = 0.000), Public acquirer (β = −0.340, p = 0.002) and Percentage sought (β = −0.584, p = 0.036) exhibit a significant negative correlation with the likelihood of acquisition completion. By contrast, the coefficient estimates for Same industry (β = 0.264, p = 0.018) and Cash payment (β = 0.759, p = 0.000) are significantly positive. These results are consistent with those from previous studies [14,23,25,26,29,53].

In Models 2 and 3 of Table 3, the interaction terms (CI × Cultural distance, CI × Non-experience) are added to test Hypotheses 2 and 3. As presented in Table 3, Models 2 and 3 exhibit better fit than does Model 1. The coefficient of interaction between CI and Cultural distance is positive and significant (β = 0.023, p = 0.003) in Model 2. To facilitate interpretation of the interaction term, the marginal effect of CI is computed with different cultural distance levels separately, following Li et al. (2019) [17]. Among lower cultural distance (when Cultural distance is one standard deviation below the mean), the marginal effect of CI is 0.470% (p = 0.010). It means that one unit increase in CI increases the acquisition completion likelihood by 0.470% (one percent increase in CI per capita increases the likelihood by 0.098%) when cultural distance is relatively low. Among higher cultural distance (when Cultural distance is one standard deviation above the mean), the marginal effect of CI is 1.236% (p = 0.000). It means that one unit increase in CI increases the acquisition completion likelihood by 1.236% (>0.470%) when cultural distance is relatively high. It signifies that the effect of CI on the completion probability depends on the cultural distance between China and the host country, where the positive relationship between CI and completion probability becomes stronger when cultural distance is relatively high. Thus, Hypothesis 2 is supported.

In Model 3 of Table 3, the coefficient of the interaction term between CI and Non-experience is also positive and significant (β = 0.042, p = 0.016). Similar to Model 2, we separately compute the marginal effect of CI with and without cross-border acquisition experience. When the Chinese MNEs have no cross-border acquisition experience, the marginal effect of CI is 1.046% (p = 0.000). However, when the Chinese MNEs have cross-border acquisition experience, the marginal effect of CI is 0.390% (p = 0.246), which is smaller than 1.046%. Moreover, due to the non-significant marginal effect (p = 0.246), the effect of CIs on completion likelihood may not exist when the MNEs have previous experience. It indicates that the effect of CI on the completion probability depends on prior cross-border acquisition experience as well. Specifically, CIs play a greater role for Chinese MNEs that have no previous cross-border acquisition experience. When the Chinese MNEs have no cross-border acquisition experience, the CIs can help them more in overcoming international challenges among the cross-border acquisitions, including weakening the negative effect of inexperience in acquisition negotiations and offering valuable information, such as relevant government regulations, market access information, and details of the local customs. This result strongly supports Hypothesis 3.

5.3. Robustness Analyses

To examine the robustness of our results, we perform several additional analyses. First, a long gestation period is required to establish a CI in a host country. Using the current year CI as the independent variable may lead to endogenous problems [5]. Following previous studies [5,11], we rerun the analyses using 1-year lagged CI as the independent variable to reduce endogenous influence. The results are reported in Table 4. As demonstrated, the key results still hold when this alternative measure is used.

Second, similar to estimating model using clustered standard errors, the random effects estimation also addresses the issue of lack of independence due to multiple acquisitions by the same firm [26,58]. Therefore, we adopt a panel logistic regression model with random effects as an alternative approach. Consistent with previous study [14,26,58], we estimate a panel logistic regression model with random effects to correct for unobserved effects. The results are presented in Table 5. As demonstrated, the key results still hold when an alternative model is used.

Third, Hong Kong (Hong Kong Special Administrative Region of the People’s Republic of China) is a special case because its political and economic policies are affected by mainland China [17]. We rerun the analyses by excluding Hong Kong from the samples. Thus, we remove 603 observations to yield 1092 observations. The results in Table 6 are still robust.

6. Additional Tests

6.1. The Effect of CIs on the Acquisition Duration

Although MNEs have completed cross-border acquisitions, their acquisitions may take long durations in the processes [28]. This situation has given rise to another question: could the presence of CIs in the host countries shorten acquisition duration as well? In order to explore the effect of CIs on the acquisition durations among Chinese MNEs, we follow prior research [14,28], and set up a dependent variable—Acquisition duration, which is calculated as the difference (equals to the number of days divided by 365) between the dates of completion and announcement of an acquisition. In addition, to test the moderating effects of Cultural distance and Non-experience on Acquisition duration as well, we set two interaction terms. We also apply double-cluster standard errors both at country and acquisition firm levels. The new equation described as follow:

where i represents the acquisition deal i of Chinese MNEs, j represents the host country j, and t represents the year t.

We present the finding in Models 1–3 of Table 7. As reported in Model 1, the coefficient of CI is negative and significant (β = −0.003, p = 0.022), which means that the time to complete an acquisition reduces average 0.003 year (about 1 day) when CI increases one unit. In percentage terms, the acquisition duration reduces average 0.2 day when CI increases by one percentage point. It indicates that the presence of CIs established in the host country not only helps to increase the likelihood of acquisitions completion, but also helps to shorten the acquisition durations. In addition, as presented in Model 2, the coefficient of the interaction term between CI and Cultural distance is negative and significant (β = −0.001, p = 0.049), which means that CIs may be more conducive to shorten the acquisition durations when acquisition deals undertake in culturally dissimilar countries. The coefficient of interaction between CI and Non-experience is also negative and significant (β = −0.002, p = 0.083) in Model 3. It indicates that CIs can shorten more acquisition durations when the MNEs have no cross-border acquisition experience. As a result, CIs may help to promote the comprehensive efficiency of the whole acquisition process.

6.2. The Moderating Effect of SOE

Prior literature has revealed that in cross-border acquisition activities, SOEs receive more support from governments relatively to other types of enterprises, particularly in terms of low-interest financing, favorable exchange rates, reduced taxation, and subsidized insurance [27]. As an institution owned by Hanban, do CIs play a different role in the likelihood of cross-border acquisition completion between SOEs and non–SOEs? In order to examine this issue, we set an interaction term (CI × SOE) to test the moderating effects of SOE. We also apply double-cluster standard errors both at country and acquisition firm levels. The equation is described as:

where i represents the acquisition deal i of Chinese MNEs, j represents the host country j, and t represents the year t.

The result is presented in Model 4 of Table 7. As demonstrated, the coefficient of interaction between CI and SOE is not significant (β = −0.022, p = 0.266), signifying the role of CIs in cross-border acquisition completion likelihood do not depend on the types of Chinse enterprises. It further indicates that CIs, unlike government agencies, do not offer additional help for SOEs.

7. Conclusions

With the rapid growth of CIs, the effect of CIs on FDI and trade has been discussed extensively [5,6,7]. Following previous studies, we use data on 1695 Chinese cross-border acquisitions that took place between 2006 and 2017 to analyze CIs’ influence on the likelihood of cross-border acquisition completion among Chinese MNEs. We observe that the establishment of CIs in host countries significantly improves the likelihood that Chinese MNEs will succeed at cross-border acquisitions. Moreover, we consider several moderating effects. At the national level, the positive effect of CIs on completion likelihood is more prominent when the cultural distance between China and the host country is great. At the firm level, the acquirer’s past experience with cross-border acquisition moderates the effect of CIs on completion likelihood, signifying that CIs play a greater role for Chinese MNEs without cross-border acquisition experience. In addition, we find that the presence of CIs not only helps to increase the likelihood of acquisitions completion, but also helps to shorten the acquisition durations. The role of CIs in cross-border acquisition completion likelihood do not depend on the types of Chinse enterprises, which indicates that CIs, unlike government agencies, do not offer additional help for SOEs.

Our findings provide some practical significance. From a global perspective, cultural and language institutes, such as CIs, have played an active and integral role in the sustainable development of the global economy. In particular, these institutes can accelerate cultural exchange and fusion among all cultures of the world, which can in turn reduce cultural obstacles to global economic cooperation. From the perspective of China, as a global platform for cultural exchange, CIs can accelerate the globalization process of Chinese enterprises, especially for enterprises with less experience in cross-border acquisitions. The presence of CIs also offers significant educational support for foreigners who wish to learn the Chinese culture and language. With familiarity with Chinese culture, the foreign public may gain a deeper understanding of China. Thus, the resistance to globalization among Chinese MNEs will be reduced. Furthermore, CIs provide vital business information to Chinese MNEs, such as the host government’s regulations, market access information, and details of local customs. Therefore, the transaction costs of cross-border acquisitions may be lowered.

Although our empirical results support the proposed hypotheses, our study has some limitations. First, we merge several databases to obtain 1695 observations from 39 countries and regions for this study. As mentioned, the merged dataset covers cross-border acquisition data from 39 countries and regions due to the data availability of some of the explanatory variables. Additional observations from more countries may expand the empirical findings. Second, the differences between each CI are not taken into account in this study. There may be an empirical bias in considering each CI as homogeneous. Thus, we attempt to replace the number of CIs with the number of registered students at each CI to represent the local influence of CIs. However, the number of registered students at each CI cannot be obtained due to data limitations.

Our results suggest several directions for future research. First, we test only the role of China’s CIs in promoting the globalization process of Chinese MNEs. However, CIs should also be compared with other similar programs, such as Germany’s Goethe-Institut, France’s Alliance Française and the British Council, in terms of cross-border acquisition completion. Second, apart from focusing on pre-acquisition activities, future research could examine the effect of CIs on post-acquisition performance. A study on whether the establishment of CIs in host countries influences the integration process of cross-border acquisitions by shortening the cultural distance may be beneficial.

Author Contributions

Y.L. and S.O. conceived and designed the research; S.O. collected and analyzed the data; S.O. wrote the paper in consultation with Y.L.; all authors discussed the results and contributed to the final manuscript.

Funding

This research was funded by the National Social Science Fund Major Project of China (Grant Number:18ZDA095).

Acknowledgments

We appreciate the constructive comments of the editors and reviewers on this manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Distribution of CIs and List of destination countries.

| Country/Region | Confucius Institute 1 | Attempted Acquisitions | Completed Acquisitions |

|---|---|---|---|

| United States | 110 | 218 | 87 |

| United Kingdom | 29 | 44 | 39 |

| South Korea | 23 | 25 | 15 |

| Germany | 19 | 77 | 35 |

| Russian | 17 | 19 | 12 |

| France | 17 | 28 | 17 |

| Thailand | 16 | 14 | 5 |

| Australia | 14 | 130 | 91 |

| Japan | 14 | 44 | 15 |

| Canada | 12 | 71 | 45 |

| Italy | 12 | 65 | 45 |

| Brazil | 10 | 27 | 14 |

| Spain | 8 | 14 | 12 |

| Belgium | 6 | 9 | 8 |

| Indonesia | 6 | 16 | 8 |

| Poland | 5 | 4 | 1 |

| Mexico | 5 | 5 | 2 |

| South Africa | 5 | 8 | 3 |

| Portugal | 4 | 3 | 2 |

| Turkey | 4 | 2 | 2 |

| Pakistan | 4 | 5 | 2 |

| Denmark | 3 | 2 | 1 |

| New Zealand | 3 | 9 | 6 |

| Netherlands | 3 | 28 | 14 |

| Colombia | 3 | 4 | 2 |

| Argentina | 2 | 5 | 3 |

| Switzerland | 2 | 12 | 4 |

| Chile | 2 | 13 | 5 |

| Malaysia | 2 | 18 | 8 |

| Israel | 2 | 19 | 14 |

| India | 2 | 34 | 11 |

| Sweden | 1 | 6 | 4 |

| Hong Kong | 1 | 603 | 135 |

| Czech Republic | 1 | 4 | 2 |

| Finland | 1 | 5 | 2 |

| Norway | 1 | 4 | 3 |

| Vietnam | 1 | 6 | 1 |

| Luxembourg | 1 | 8 | 6 |

| Singapore | 1 | 87 | 44 |

| Total | 372 | 1695 | 725 |

1 Number of Confucius Institutes at the end of 2017.

References

- Theo, R.; Leung, M.W.H. China’s Confucius Institute in Indonesia: Mobility, Frictions and Local Surprises. Sustainability 2018, 10, 530. [Google Scholar] [CrossRef]

- Lien, D.; Miao, L. Effects of Confucius Institutes on China’s higher education exports: Evidence from Chinese Partner Universities. Int. Rev. Econ. Financ. 2018, 57, 134–143. [Google Scholar] [CrossRef]

- Xu, L. Confucius Institute Annual Development Report 2017; Confucius Institute: Beijing, China, 2017. [Google Scholar]

- Oh, C.H.; Selmier, W.T.; Lien, D. International trade, foreign direct investment, and transaction costs in languages. J. Socio-Econ. 2011, 40, 732–735. [Google Scholar] [CrossRef]

- Lien, D.; Oh, C.H.; Selmier, W.T. Confucius institute effects on China’s trade and FDI: Isn’t it delightful when folks afar study Hanyu? Int. Rev. Econ. Financ. 2012, 21, 147–155. [Google Scholar] [CrossRef]

- Lien, D.; Co, C.Y. The effect of Confucius Institutes on US Exports to China: A state level analysis. Int. Rev. Econ. Financ. 2013, 27, 566–571. [Google Scholar] [CrossRef]

- Akhtaruzzaman, M.; Berg, N.; Lien, D. Confucius Institutes and FDI flows from China to Africa. China Econ. Rev. 2017, 44, 241–252. [Google Scholar] [CrossRef]

- Deng, P. Why do Chinese firms tend to acquire strategic assets in international expansion? J. World Bus. 2009, 44, 74–84. [Google Scholar] [CrossRef]

- Zhou, C.; Xie, J.; Wang, Q. Failure to Complete Cross-Border M&As: “To” vs. “From” Emerging Markets. J. Int. Bus. Stud. 2016, 47, 1077–1105. [Google Scholar]

- Lien, D.; Ghosh, S.; Yamarik, S. Does the Confucius institute impact international travel to China? A panel data analysis. Appl. Econ. 2014, 46, 1985–1995. [Google Scholar] [CrossRef]

- Lien, D.; Yao, F.; Zhang, F. Confucius Institute’s effects on international travel to China: Do cultural difference or institutional quality matter? Appl. Econ. 2017, 49, 3669–3683. [Google Scholar] [CrossRef]

- Xie, E.; Reddy, K.S.; Liang, J. Country-specific determinants of cross-border mergers and acquisitions: A comprehensive review and future research directions. J. World Bus. 2017, 52, 127–183. [Google Scholar] [CrossRef]

- Zhang, J.; He, X. Economic nationalism and foreign acquisition completion: The case of China. Int. Bus. Rev. 2014, 23, 212–227. [Google Scholar] [CrossRef] [Green Version]

- Dikova, D.; Sahib, P.R.; van Witteloostuijn, A. Cross-border acquisition abandonment and completion: The effect of institutional differences and organizational learning in the international business service industry, 1981–2001. J. Int. Bus. Stud. 2010, 41, 223–245. [Google Scholar] [CrossRef]

- Faccio, M.; Masulis, R.W. The choice of payment method in European mergers and acquisitions. J. Financ. 2005, 60, 1345–1388. [Google Scholar] [CrossRef]

- Huang, P.; Officer, M.S.; Powell, R. Method of payment and risk mitigation in cross-border mergers and acquisitions. J. Corp. Financ. 2016, 40, 216–234. [Google Scholar] [CrossRef] [Green Version]

- Li, J.; Li, P.; Wang, B. The liability of opaqueness: State ownership and the likelihood of deal completion in international acquisitions by Chinese firms. Strateg. Manag. J. 2019, 40, 303–327. [Google Scholar] [CrossRef]

- Lien, D.; Oh, C.H. Determinants of the Confucius Institute establishment. Q. Rev. Econ. Financ. 2014, 54, 437–441. [Google Scholar] [CrossRef]

- Fang, T.; Fridh, C.; Schultzberg, S. Why did the Telia–Telenor merger fail? Int. Bus. Rev. 2004, 13, 573–594. [Google Scholar] [CrossRef]

- Schmid, S.; Daniel, A. Telia—A Swedish-Finnish marriage after a failed Norwegian courtship. Thunderbird Int. Bus. Rev. 2010, 51, 297–310. [Google Scholar] [CrossRef]

- Angwin, D. Mergers and Acquisitions across European Borders: National Perspectives on Preacquisition Due Diligence and the Use of Professional Advisers. J. World Bus. 2001, 36, 32–57. [Google Scholar] [CrossRef]

- Ahammad, M.F.; Tarba, S.Y.; Liu, Y.; Glaister, K.W.; Cooper, C.L. Exploring the factors influencing the negotiation process in cross-border M&A. Int. Bus. Rev. 2016, 25, 445–457. [Google Scholar]

- Zhang, J.; Zhou, C.; Ebbers, H. Completion of Chinese overseas acquisitions: Institutional perspectives and evidence. Int. Bus. Rev. 2011, 20, 226–238. [Google Scholar] [CrossRef]

- Ahern, K.R.; Daminelli, D.; Fracassi, C. Lost in translation? The effect of cultural values on mergers around the world. J. Financ. Econ. 2015, 117, 165–189. [Google Scholar] [CrossRef]

- Popli, M.; Akbar, M.; Kumar, V.; Gaur, A. Reconceptualizing cultural distance: The role of cultural experience reserve in cross-border acquisitions. J. World Bus. 2016, 51, 404–412. [Google Scholar] [CrossRef]

- Muehlfeld, K.; Sahib, P.R.; Van Witteloostuijn, A. A contextual theory of organizational learning from failures and successes: A study of acquisition completion in the global newspaper industry, 1981–2008. Strateg. Manag. J. 2012, 33, 938–964. [Google Scholar] [CrossRef]

- Chen, Y.; Guo, W. Institutional Risks and Success of Chinese Cross-border Acquisitions: Moderating Role of Diplomatic relations and Economic ‘Soft Power’. World Econ. Stud. 2018, 5, 51–64. [Google Scholar]

- Li, J.; Xia, J.; Lin, Z. Cross-border acquisitions by state-owned firms: How do legitimacy concerns affect the completion and duration of their acquisitions. Strateg. Manag. J. 2017, 38, 1915–1934. [Google Scholar] [CrossRef]

- Lim, M.-H.; Lee, J.-H. The effects of industry relatedness and takeover motives on cross-border acquisition completion. J. Bus. Res. 2016, 69, 4787–4792. [Google Scholar] [CrossRef]

- Muehlfeld, K.; Sahib, P.R.; van Witteloostuijn, A. Completion or Abandonment of Mergers and Acquisitions: Evidence from the Newspaper Industry, 1981–2000. J. Media Econ. 2007, 20, 107–137. [Google Scholar] [CrossRef]

- Trapczynski, P.; Zaks, O.; Polowczyk, J. The Effect of Trust on Acquisition Success: The Case of Israeli Start-Up M&A. Sustainability 2018, 10, 2499. [Google Scholar]

- Lien, D. Financial effects of the Confucius Institute on Chinese language acquisition: Isn’t it delightful that friends come from afar to teach you Hanyu? N. Am. J. Econ. Financ. 2013, 24, 87–100. [Google Scholar] [CrossRef]

- Kim, M.; Liu, A.H.; Tuxhorn, K.-L.; Brown, D.S.; Leblang, D. Lingua Mercatoria: Language and Foreign Direct Investment. Int. Stud. Q. 2015, 59, 330–343. [Google Scholar] [CrossRef]

- Boeh, K.K. Contracting Costs and Information Asymmetry Reduction in Cross-Border M&A. J. Manag. Stud. 2011, 48, 568–590. [Google Scholar]

- Erel, I.; Liao, R.C.; Weisbach, M.S. Determinants of Cross-Border Mergers and Acquisitions. J. Financ. 2012, 67, 1045–1082. [Google Scholar] [CrossRef]

- David, K.T.; Francis, J.; Walls, J. Cultural differences in conducting intra-and inter-cultural negotiations: A Sino-Canadian comparison. J. Int. Bus. Stud. 1994, 25, 537–555. [Google Scholar]

- Chung, G.H.; Du, J.; Choi, J.N. How do employees adapt to organizational change driven by cross-border M&As? A case in China. J. World Bus. 2014, 49, 78–86. [Google Scholar]

- Barkema, H.G.; Bell, J.H.J.; Pennings, J.M. Foreign entry, cultural barriers, and learning. Strateg. Manag. J. 1996, 17, 151–166. [Google Scholar] [CrossRef]

- Barkema, H.G.; Vermeulen, F. International expansion through start-up or acquisition: A learning perspective. Acad. Manag. J. 1998, 41, 7–26. [Google Scholar]

- Haleblian, J.; Finkelstein, S. The influence of organizational acquisition experience on acquisition performance: A behavioral learning perspective. Adm. Sci. Q. 1999, 44, 29–56. [Google Scholar] [CrossRef]

- Huyghebaert, N.; Luypaert, M. Antecedents of growth through mergers and acquisitions: Empirical results from Belgium. J. Bus. Res. 2010, 63, 392–403. [Google Scholar] [CrossRef]

- Von Eije, H.; Wiegerinck, H. Shareholders’ reactions to announcements of acquisitions of private firms: Do target and bidder markets make a difference? Int. Bus. Rev. 2010, 19, 360–377. [Google Scholar] [CrossRef]

- Gu, L.; Reed, W.R. Does financing of Chinese mergers and acquisitions have “Chinese characteristics”? Econ. Lett. 2016, 139, 11–14. [Google Scholar] [CrossRef]

- Kogut, B.; Singh, H. The effect of national culture on the choice of entry mode. J. Int. Bus. Stud. 1988, 19, 411–432. [Google Scholar] [CrossRef]

- Lonner, W.J.; Berry, J.W.; Hofstede, G.H. Culture’s Consequences: International Differences in Work-Related Values. by Geert Hofstede. Soc. Sci. Electron. Publ. 1981, 36, 129–130. [Google Scholar]

- Gamberger, D. The Impact of Bilateral Investment Treaties on Foreign Direct Investment in Switzerland. J. Comp. Econ. 2004, 32, 788–804. [Google Scholar]

- Neumayer, E.; Spess, L. Do bilateral investment treaties increase foreign direct investment to developing countries? World Dev. 2005, 33, 1567–1585. [Google Scholar] [CrossRef] [Green Version]

- Luo, Y.; Tung, R.L. International expansion of emerging market enterprises: A springboard perspective. J. Int. Bus. Stud. 2007, 38, 481–498. [Google Scholar] [CrossRef]

- Brockman, P.; Rui, O.M.; Zou, H. Institutions and the performance of politically connected M&As. J. Int. Bus. Stud. 2013, 44, 833–852. [Google Scholar]

- Kaufmann, D.; Kraay, A.; Mastruzzi, M. The Worldwide Governance Indicators: Methodology and Analytical Issues. Hague J. Rule Law 2011, 3, 220–246. [Google Scholar] [CrossRef]

- Chakrabarti, A.; Mitchell, W. The role of geographic distance in completing related acquisitions: Evidence from US chemical manufacturers. Strateg. Manag. J. 2016, 37, 673–694. [Google Scholar] [CrossRef]

- Chakrabarti, R.; Gupta-Mukherjee, S.; Jayaraman, N. Mars–Venus marriages: Culture and cross-border M&A. J. Int. Bus. Stud. 2009, 40, 216–236. [Google Scholar]

- Trang Thu, D.; Sahib, P.R.; van Witteloostuijn, A. Lessons from the flipside: How do acquirers learn from divestitures to complete acquisitions? Long Range Plan. 2018, 51, 252–266. [Google Scholar] [Green Version]

- Basuil, D.A.; Datta, D.K. Effects of Industry- and Region-Specific Acquisition Experience on Value Creation in Cross-Border Acquisitions: The Moderating Role of Cultural Similarity. J. Manag. Stud. 2015, 52, 766–795. [Google Scholar] [CrossRef]

- Bae, S.C.; Chang, K.; Kim, D. Determinants of target selection and acquirer returns: Evidence from cross-border acquisitions. Int. Rev. Econ. Financ. 2013, 27, 552–565. [Google Scholar] [CrossRef]

- Kim, E.H.; Lu, Y. Corporate governance reforms around the world and cross-border acquisitions. J. Corp. Financ. 2013, 22, 236–253. [Google Scholar] [CrossRef] [Green Version]

- Chatterjee, S.; Price, B. Regression Analysis by Example; Wiley: Hoboken, NJ, USA, 2006; p. 286. [Google Scholar]

- Cameron, A.C.; Trivedi, P.K. Microeconometrics Using Stata; Stata press: College Station, TX, USA, 2010; Volume 2. [Google Scholar]

Figure 1.

Conceptual model.

Table 1.

Variables, short explanations and sources.

| Variables | Definition | Source(s) of Data | Measure Adopted From |

|---|---|---|---|

| Acquisition completion | Dummy variable equaling 1 if the announced acquisition is completed and 0 otherwise | Zephyr by Bureau Van Dijk (BvD) | Dikova et al. 2010; Muehlfeld et al. 2012 |

| Confucius Institute (CI) | Measured by the number of CIs per capita in the host country | Website of Hanban | Lien et al. 2012 |

| Bilateral investment treaty (BIT) | Dummy variable equaling 1 after the date of signing a BIT and 0 otherwise | Website of the Ministry of Commerce of China | Gamberger 2004; Neumayer et al. 2005 |

| Non-experience | Dummy variable equaling 1 if an acquirer has no past successful international acquisition(s) and 0 otherwise | Zephyr by BvD | Zhang et al. 2011 |

| Population | Measured by the log value of the host country population | World Bank | Lien et al. 2012 |

| GDP growth | The annual GDP growth rate of the host country | World Bank | Erel et al. 2012 |

| Institutional environment | Averaging the six indicators (voice and accountability, political stability, government effectiveness, regulatory quality, rule of law, and control of corruption) into a single index | World Bank | Brockman et al. 2013 |

| Neighbor | Dummy variable equaling 1 if the acquirer and target country or region are neighbors and 0 otherwise | CEPII | Martynova M and Renneboog L 2008 |

| Cultural distance | Measured through the Kogut and Singh (1988) index, which is based on Hofstede’ s four cultural dimensions | The Hofstede Centre | Kogut and Singh 1988 |

| Exchange rate risk | Measured by the volatility of exchange rate between China and the host country | International Monetary Fund | Chakrabarti et al. 2009 |

| Deal size | Measured by the log value of the cross-border acquisition deal | Zephyr by BvD | Trang Thu et al. 2018 |

| Same industry | Dummy variable equaling 1 if the acquirer’s industry is the same as the target’s industry and 0 otherwise | Zephyr by BvD | Li et al. 2017 |

| Public acquirer | Dummy variable equaling 1 if the acquirer is listed on either the Shanghai or Shenzhen stock exchange and 0 otherwise | Zephyr by BvD | Li et al. 2019 |

| Cash payment | Dummy variable equaling 1 if an acquirer offers to pay in cash and 0 otherwise | Zephyr by BvD | Li et al. 2019 |

| Percentage sought | Measured by percentage of ownership stake of a target sought by an acquirer | Zephyr by BvD | Zhang et al. 2011 |

| State-owned enterprise (SOE) | Dummy variable equaling 1 if an acquirer is an SOE and 0 otherwise | Zephyr by BvD | Zhang and He 2014 |

Table 2.

Descriptive statistics and correlations (N = 1695).

| Variable | Mean | S.D. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.Acquisition completion | 0.428 | 0.495 | |||||||||||||||

| 2.Confucius Institutes | 20.792 | 13.046 | 0.290 *** | ||||||||||||||

| 3.BIT | 0.811 | 0.391 | −0.013 | −0.234 *** | |||||||||||||

| 4.GDP growth | 2.568 | 2.075 | −0.069 *** | −0.121 *** | 0.187 *** | ||||||||||||

| 5.Population | 17.157 | 1.558 | 0.094 *** | 0.101 *** | −0.577 *** | −0.117 *** | |||||||||||

| 6.Institutional environment | 1.227 | 0.548 | −0.026 | 0.354 *** | 0.084 *** | −0.138 *** | −0.512 *** | ||||||||||

| 7.Neighbor | 0.395 | 0.489 | −0.305 *** | −0.496 *** | 0.380 *** | 0.225 *** | −0.497 *** | 0.041 * | |||||||||

| 8.Cultural distance | 1.940 | 1.585 | 0.280 *** | 0.647 *** | −0.540 *** | −0.245 *** | 0.557 *** | 0.047 * | −0.678 *** | ||||||||

| 9.Exchange rate risk | 0.026 | 0.023 | 0.156 *** | 0.124 *** | 0.009 | −0.127 *** | 0.102 *** | −0.140 *** | −0.269 *** | 0.302 *** | |||||||

| 10.Deal size | 9.666 | 2.500 | 0.186 *** | 0.052 ** | −0.029 | −0.082 *** | −0.007 | −0.042 * | −0.044 * | 0.079 *** | 0.093 *** | ||||||

| 11.Same industry acquisition | 0.342 | 0.475 | 0.043 * | −0.008 | −0.027 | 0.049 ** | 0.043 * | −0.038 | −0.074 *** | 0.064 *** | 0.067 *** | 0.065 *** | |||||

| 12.Non-experience | 0.796 | 0.403 | −0.361 *** | −0.116 *** | −0.054 ** | 0.016 | −0.039 | 0.087 *** | 0.190 *** | −0.140 *** | −0.145 *** | −0.288 *** | −0.03 | ||||

| 13.SOE | 0.127 | 0.334 | 0.174 *** | 0.037 | 0.062 ** | −0.052 ** | 0.009 | −0.117 *** | −0.052 ** | 0.067 *** | 0.203 *** | 0.298 *** | 0.056 ** | −0.263 *** | |||

| 14.Public acquirer | 0.461 | 0.499 | −0.248 *** | −0.152 *** | 0.011 | 0.031 | −0.064 *** | 0.009 | 0.158 *** | −0.171 *** | −0.128 *** | 0.045 * | 0.066 *** | 0.178 *** | −0.155 *** | ||

| 15.Cash payment | 0.301 | 0.459 | 0.228 *** | 0.036 | 0.037 | −0.090 *** | 0.079 *** | −0.150 *** | −0.167 *** | 0.091 *** | 0.061 ** | 0.191 *** | 0.053 ** | −0.131 *** | 0.177 *** | −0.096 *** | |

| 16.Percentage sought | 0.720 | 0.356 | −0.338 *** | −0.279 *** | 0.054 ** | 0.153 *** | −0.163 *** | 0.042 * | 0.369 *** | −0.369 *** | −0.246 *** | −0.094 *** | −0.003 | 0.258 *** | −0.207 *** | 0.296 *** | −0.076 *** |

* p < 0.1, ** p < 0.05, *** p < 0.01.

Table 3.

Results of logit models predicting acquisition completion.

| Variables | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| CI | 0.052 *** | 0.024 * | 0.021 |

| (3.122) | (1.651) | (1.126) | |

| CI × Cultural distance | 0.023 *** | ||

| (2.971) | |||

| CI × Non-experience | 0.042 ** | ||

| (2.402) | |||

| BIT | 0.465 * | 0.353 | 0.471 * |

| (1.957) | (1.385) | (1.853) | |

| GDP growth | −0.065 | −0.114 ** | −0.078 |

| (−1.218) | (−2.291) | (−1.340) | |

| Population | −0.038 | −0.110 | −0.038 |

| (−0.502) | (−1.364) | (−0.481) | |

| Institutional environment | −0.447 * | −0.448 ** | −0.432 |

| (−1.782) | (−2.204) | (−1.636) | |

| Neighbor | −0.202 | −0.683 * | −0.170 |

| (−0.425) | (−1.662) | (−0.307) | |

| Cultural distance | −0.084 | −0.127 | −0.109 |

| (−0.685) | (−1.177) | (−0.841) | |

| Exchange rate risk | −1.359 | −3.907 | −0.709 |

| (−0.260) | (−0.862) | (−0.129) | |

| Deal size | 0.066 ** | 0.073 ** | 0.068 ** |

| (2.067) | (2.229) | (2.092) | |

| Same industry | 0.264 ** | 0.265 ** | 0.256 ** |

| (2.364) | (2.315) | (2.137) | |

| Non-experience | −1.267 *** | −1.300 *** | −1.309 *** |

| (−2.975) | (−2.996) | (−3.689) | |

| SOE | −0.035 | −0.029 | −0.027 |

| (−0.147) | (−0.126) | (−0.118) | |

| Public acquirer | −0.340 *** | −0.348 *** | −0.340 *** |

| (−3.157) | (−3.094) | (−3.139) | |

| Cash payment | 0.753 *** | 0.788 *** | 0.737 *** |

| (5.662) | (5.822) | (5.595) | |

| Percentage sought | −0.584 ** | −0.604 ** | −0.553 * |

| (−2.099) | (−2.155) | (−1.949) | |

| Cons | 4.409 *** | 6.156 *** | 4.506 *** |

| (3.535) | (4.369) | (3.251) | |

| Industry | YES | YES | YES |

| Year | YES | YES | YES |

| Observations | 1695 | 1695 | 1695 |

| Log-likelihood | −824.448 | −816.427 | −818.649 |

| Pseudo R2 | 0.287 | 0.294 | 0.293 |

* p < 0.1, ** p < 0.05, *** p < 0.01 (z-values are in parentheses; double clustered standard errors at acquirer and target country levels, 39 clusters in country level and 1086 clusters in acquirer level).

Table 4.

Results of logit models with 1-year lagged CI.

| Variables | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| CI | 0.043 ** | 0.010 | 0.006 |

| (2.571) | (0.884) | (0.270) | |

| CI × Cultural distance | 0.027 *** | ||

| (3.596) | |||

| CI × Non-experience | 0.048 ** | ||

| (2.410) | |||

| BIT | 0.417 | 0.373 | 0.463 |

| (1.429) | (1.420) | (1.514) | |

| GDP growth | −0.057 | −0.116 ** | −0.069 |

| (−0.943) | (−2.024) | (−1.052) | |

| Population | −0.138 | −0.200 ** | −0.123 |

| (−1.435) | (−2.067) | (−1.310) | |

| Institutional environment | −0.478 * | −0.481 ** | −0.465 * |

| (−1.847) | (−2.230) | (−1.720) | |

| Neighbor | −0.062 | −0.646 | −0.072 |

| (−0.122) | (−1.489) | (−0.124) | |

| Cultural distance | 0.041 | −0.020 | 0.023 |

| (0.348) | (−0.195) | (0.187) | |

| Exchange rate risk | −3.006 | −5.885 | −2.387 |

| (−0.540) | (−1.219) | (−0.398) | |

| Deal size | 0.061 * | 0.067 ** | 0.063 * |

| (1.824) | (1.993) | (1.866) | |

| Same industry | 0.201 * | 0.216 * | 0.197 |

| (1.740) | (1.809) | (1.621) | |

| Non-experience | −1.267 *** | −1.295 *** | −1.328 *** |

| (−2.853) | (−2.875) | (−3.673) | |

| SOE | 0.025 | 0.039 | 0.038 |

| (0.102) | (0.158) | (0.155) | |

| Public acquirer | −0.306 *** | −0.319 *** | −0.308 *** |

| (−2.634) | (−2.641) | (−2.627) | |

| Cash payment | 0.762 *** | 0.786 *** | 0.750 *** |

| (5.356) | (5.557) | (5.309) | |

| Percentage sought | −0.553 ** | −0.587 ** | −0.535 ** |

| (−2.042) | (−2.131) | (−1.961) | |

| Cons | 6.642 *** | 8.309 *** | 6.491 *** |

| (3.660) | (4.345) | (3.547) | |

| Industry | YES | YES | YES |

| Year | YES | YES | YES |

| Observations | 1661 | 1661 | 1661 |

| Log-likelihood | −809.588 | −799.710 | −803.070 |

| Pseudo R2 | 0.286 | 0.294 | 0.291 |

* p < 0.1, ** p < 0.05, *** p < 0.01 (z-values are in parentheses; double clustered standard errors at acquirer and target country levels, 39 clusters in country level and 1074 clusters in acquirer level).

Table 5.

Results of logit models with random effects.

| Variables | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| CI | 0.057 *** | 0.026 ** | 0.024 * |

| (6.178) | (2.190) | (1.793) | |

| CI × Cultural distance | 0.026 *** | ||

| (3.850) | |||

| CI × Non-experience | 0.045 *** | ||

| (3.352) | |||

| BIT | 0.517 ** | 0.395 | 0.529 ** |

| (2.089) | (1.604) | (2.144) | |

| GDP growth | −0.080 * | −0.132 *** | −0.091 * |

| (−1.655) | (−2.620) | (−1.837) | |

| Population | −0.028 | −0.109 | −0.027 |

| (−0.325) | (−1.233) | (−0.302) | |

| Institutional environment | −0.420 ** | −0.434 ** | −0.409 * |

| (−2.034) | (−2.105) | (−1.953) | |

| Neighbor | −0.146 | −0.694 | −0.135 |

| (−0.287) | (−1.336) | (−0.255) | |

| Cultural distance | −0.110 | −0.154 | −0.134 |

| (−1.025) | (−1.428) | (−1.238) | |

| Exchange rate risk | −1.181 | −4.021 | −0.415 |

| (−0.292) | (−0.986) | (−0.102) | |

| Deal size | 0.080 ** | 0.086 ** | 0.081 ** |

| (2.388) | (2.550) | (2.397) | |

| Same industry acquisition | 0.314 * | 0.314 * | 0.309 * |

| (1.935) | (1.931) | (1.895) | |

| Non-experience | −1.324 *** | −1.360 *** | −1.389 *** |

| (−6.348) | (−6.494) | (−6.584) | |

| SOE | −0.053 | −0.052 | −0.043 |

| (−0.202) | (−0.195) | (−0.162) | |

| Public acquirer | −0.389 ** | −0.393 ** | −0.390 ** |

| (−2.315) | (−2.336) | (−2.305) | |

| Cash payment | 0.857 *** | 0.888 *** | 0.834 *** |

| (5.264) | (5.436) | (5.104) | |

| Percentage sought | −0.709 *** | −0.730 *** | −0.674 *** |

| (−2.984) | (−3.058) | (−2.828) | |

| Cons | 4.773 * | 6.734 *** | 4.882 ** |

| (1.947) | (2.692) | (1.985) | |

| Observations | 1695 | 1695 | 1695 |

| Log-likelihood | −820.202 | −812.388 | −814.717 |

| Wald Chi-squared | 233.106 | 236.856 | 229.656 |

* p < 0.1, ** p < 0.05, *** p < 0.01 (z-values are in parentheses).

Table 6.

Results of logit models excluding Hong Kong.

| Variables | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| CI | 0.044 *** | 0.016 | 0.018 |

| (3.039) | (1.195) | (1.036) | |

| CI × Cultural distance | 0.023 *** | ||

| (2.978) | |||

| CI × Non-experience | 0.035 ** | ||

| (2.209) | |||

| BIT | 0.463 * | 0.359 | 0.472 * |

| (1.854) | (1.369) | (1.805) | |

| GDP growth | −0.078 | −0.133 *** | −0.089 |

| (−1.533) | (−2.649) | (−1.582) | |

| Population | −0.089 | −0.163 * | −0.083 |

| (−1.168) | (−1.952) | (−1.056) | |

| Institutional environment | −0.432 * | −0.444 ** | −0.419 * |

| (−1.895) | (−2.293) | (−1.762) | |

| Neighbor | −0.128 | −0.573 | −0.110 |

| (−0.295) | (−1.433) | (−0.219) | |

| Cultural distance | −0.031 | −0.071 | −0.054 |

| (−0.296) | (−0.815) | (−0.493) | |

| Exchange rate risk | 1.126 | −2.289 | 1.391 |

| (0.200) | (−0.450) | (0.227) | |

| Deal size | 0.094 ** | 0.102 ** | 0.094 ** |

| (2.146) | (2.224) | (2.192) | |

| Same industry acquisition | 0.258 | 0.270 | 0.240 |

| (1.628) | (1.621) | (1.502) | |

| Non-experience | −1.062 ** | −1.100 ** | −1.167 *** |

| (−2.185) | (−2.207) | (−2.696) | |

| SOE | −0.161 | −0.136 | −0.155 |

| (−0.582) | (−0.492) | (−0.570) | |

| Public acquirer | −0.298 ** | −0.294 ** | −0.297 ** |

| (−2.473) | (−2.327) | (−2.367) | |

| Cash payment | 0.642 *** | 0.682 *** | 0.630 *** |

| (4.281) | (4.380) | (4.155) | |

| Percentage sought | −0.467 | −0.482 | −0.424 |

| (−1.481) | (−1.503) | (−1.362) | |

| Cons | 1.823 | 3.487 ** | 1.942 |

| (1.280) | (2.182) | (1.283) | |

| Industry | YES | YES | YES |

| Year | YES | YES | YES |

| Observations | 1092 | 1092 | 1092 |

| Log-likelihood | −582.793 | −575.181 | −579.012 |

| Pseudo R2 | 0.226 | 0.237 | 0.231 |

* p < 0.1, ** p < 0.05, *** p < 0.01 (z-values are in parentheses; double clustered standard errors at acquirer and target country levels, 38 clusters in country level and 716 clusters in acquirer level).

Table 7.

Result of additional tests.

| Variables | Model 1 | Model 2 | Model 3 | Model 4 |

|---|---|---|---|---|

| Acquisition Duration | Deal Completion | |||

| CI | −0.003 ** | −0.002 | −0.002 | 0.055 *** |

| (−2.292) | (−1.286) | (−1.150) | (3.080) | |

| CI × Cultural distance | −0.001 ** | |||

| (−1.971) | ||||

| CI × Non-experience | −0.002 * | |||

| (−1.734) | ||||

| CI × SOE | −0.022 | |||

| (−1.113) | ||||

| BIT | 0.048 | 0.030 | 0.050 | 0.484 ** |

| (1.513) | (0.918) | (1.565) | (2.015) | |

| GDP growth | −0.001 | −0.004 | 0.000 | −0.066 |

| (−0.111) | (−0.496) | (0.040) | (−1.156) | |

| Population | 0.002 | −0.003 | 0.001 | −0.034 |

| (0.170) | (−0.201) | (0.110) | (−0.447) | |

| Institutional environment | −0.046 | −0.044 | −0.049 | −0.418 |

| (−1.332) | (−1.241) | (−1.436) | (−1.617) | |

| Neighbor | −0.101 | −0.131 | −0.102 | −0.160 |

| (−1.127) | (−1.483) | (−1.195) | (−0.319) | |

| Cultural distance | 0.033 * | 0.026 | 0.036 * | −0.088 |

| (1.739) | (1.316) | (1.829) | (−0.701) | |