How Does Information Transmission Influence the Value Creation Capability of a Digital Ecosystem? An Empirical Study of the Crypto-Digital Ecosystem Ethereum

Abstract

:1. Introduction

2. Theoretical Background

3. Hypothesis Development

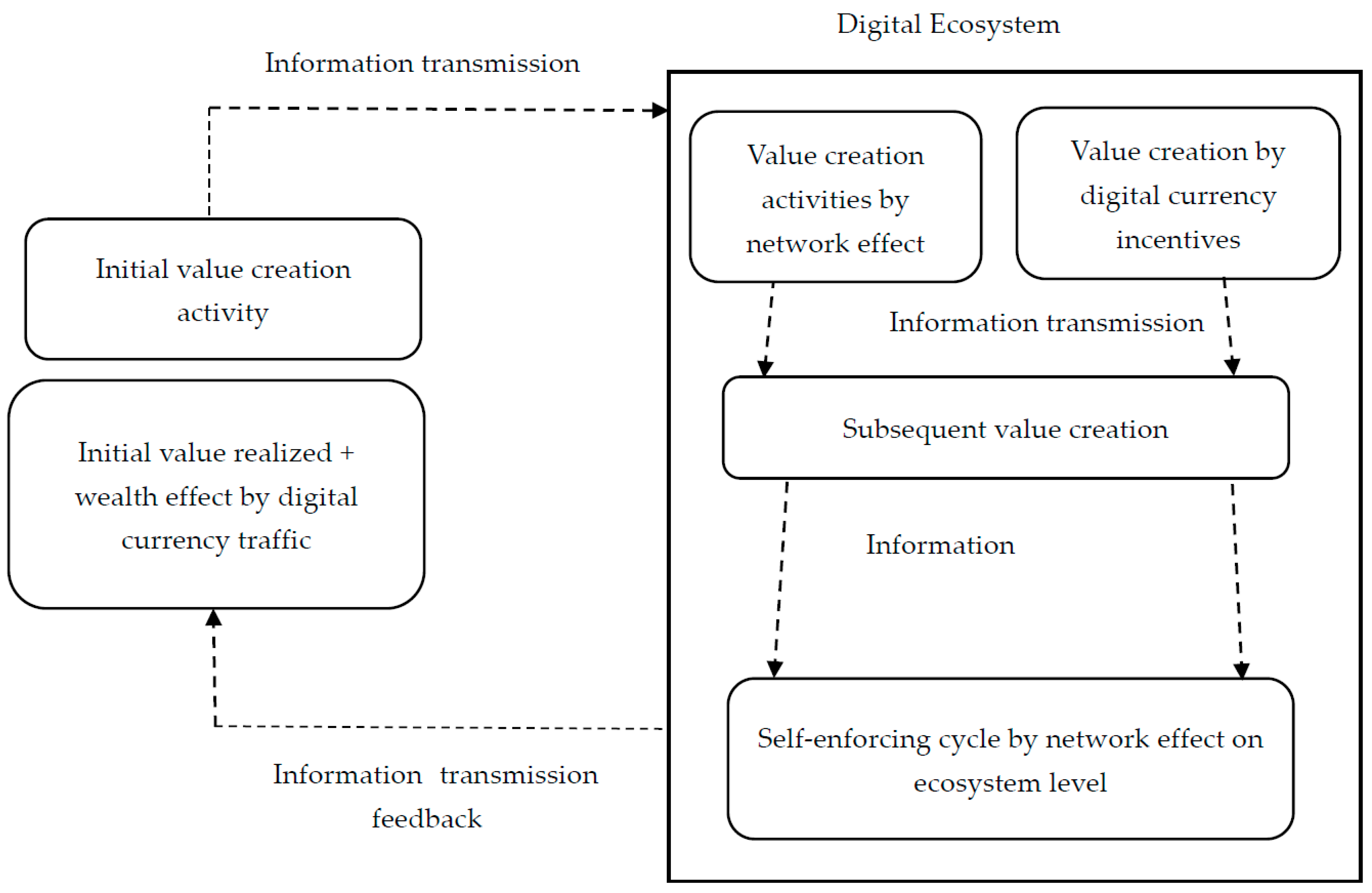

3.1. Value Creation Capability of a Digital Ecosystem

3.2. Critical Factors in Value Creation Scale and Sustainability

4. Methodology

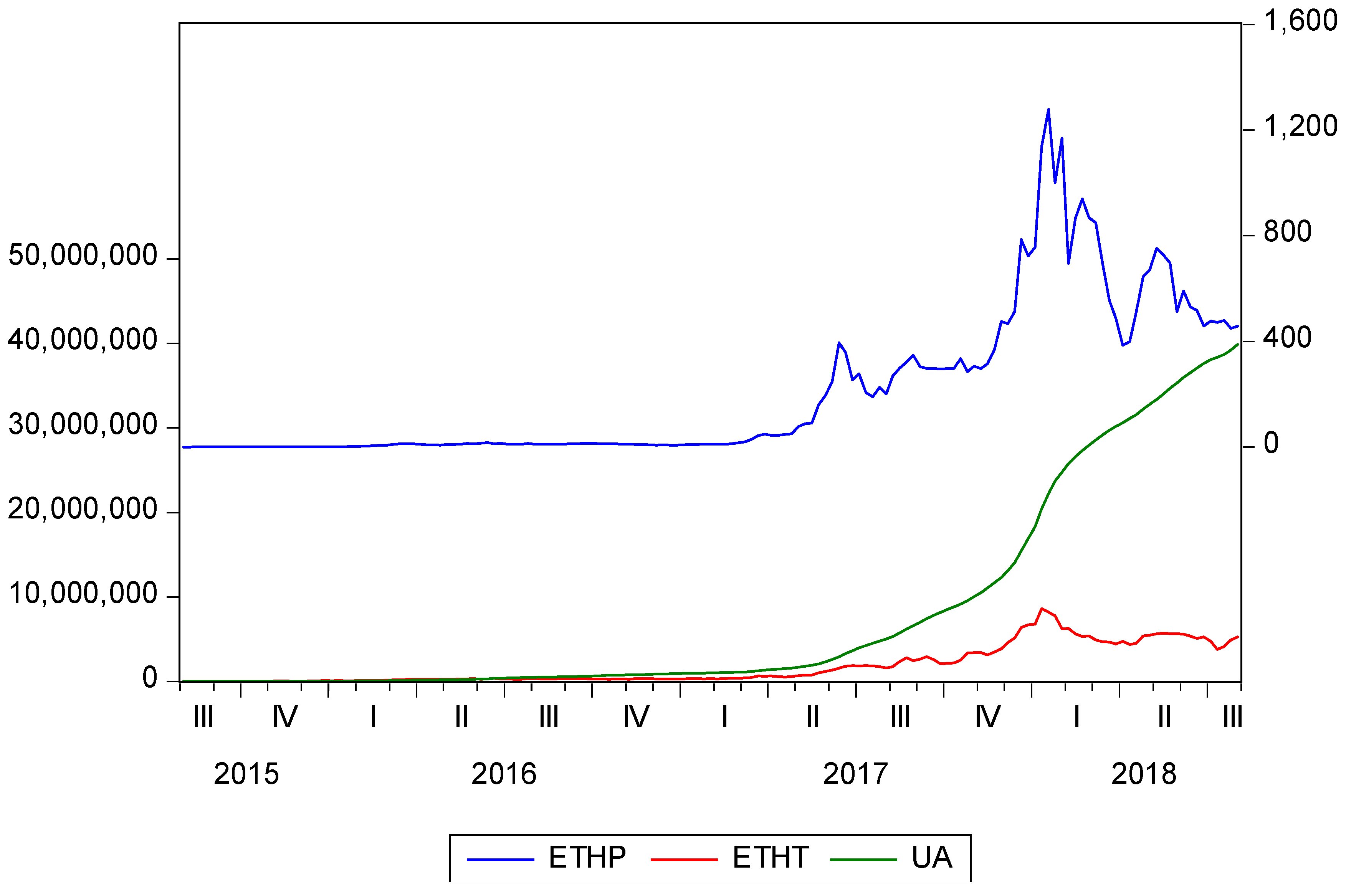

4.1. Sample and Data Collection

4.2. Measures

DPETHT = (ETHT-ETHT−1)/ETHT−1

DPUA = (UA-UA−1)/UA−1

4.3. Model

5. Research Findings

5.1. Regression Results

5.2. Granger Causality Tests

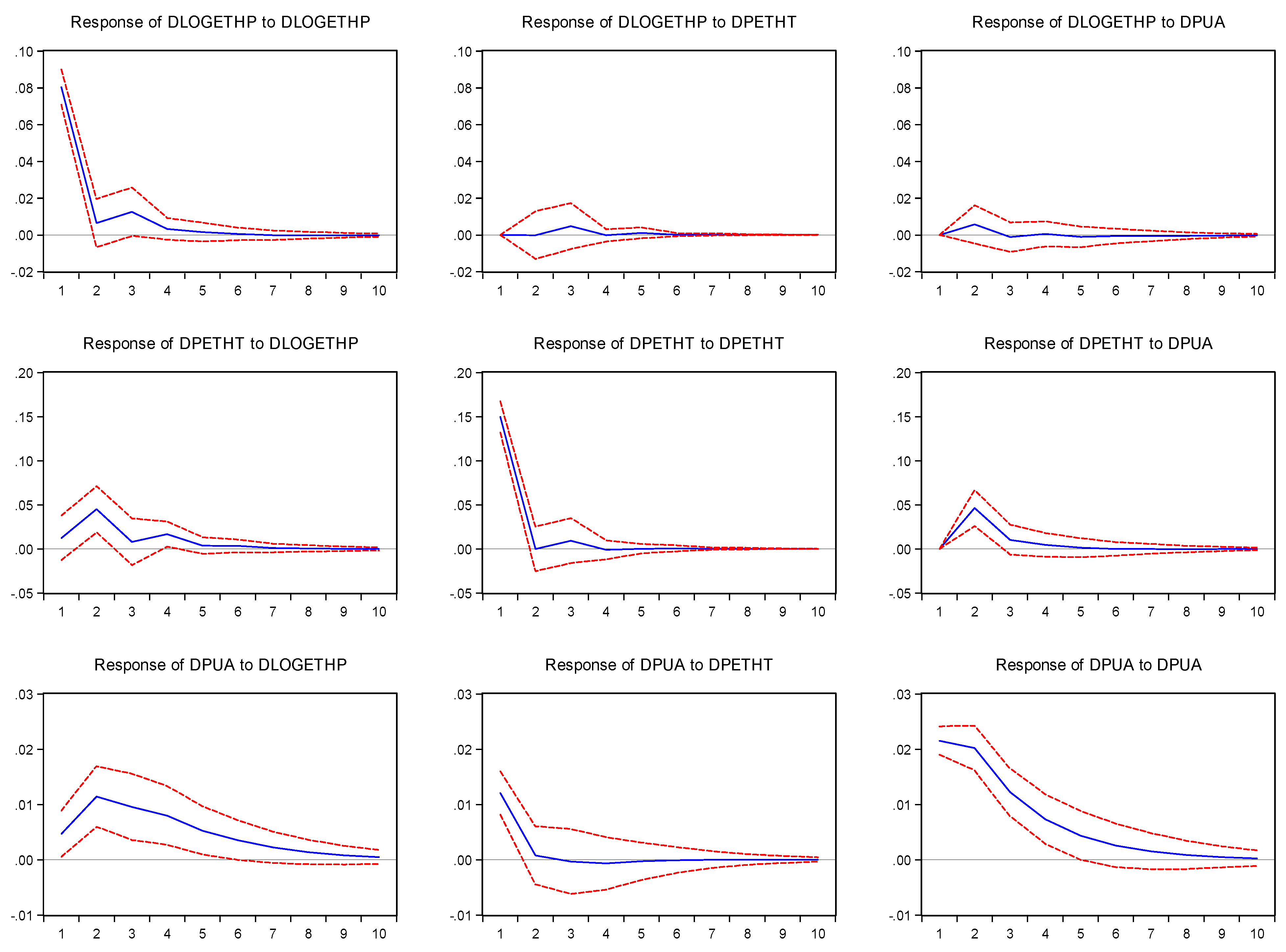

5.3. Impulse Response Functions

5.4. Robustness Test

6. Discussion and Conclusions

Funding

Acknowledgments

Conflicts of Interest

References

- Weill, P.; Woerner, S.L. Thriving in an Increasingly Digital Ecosystem. MIT Sloan Manag. Rev. 2015, 56, 27–34. [Google Scholar]

- Goldfarb, A.; Tucker, C. Digital Economics. J. Econ. Lit. 2019, 57, 3–43. [Google Scholar] [CrossRef] [Green Version]

- Rochet, J.C.; Tirole, J. Platform Competition in Two-Sided Markets. J. Eur. Econ. Assoc. 2003, 1, 990–1029. [Google Scholar] [CrossRef] [Green Version]

- Rochet, J.C.; Tirole, J. Two-Sided Markets: A Progress Report. Rand J. Econ. 2006, 37, 645–667. [Google Scholar] [CrossRef]

- Varian, H.R.; Farrell, J.; Shapiro, C. The Economics of Information Technology: An Introduction, 1st ed.; Cambridge University Press: London, UK, 2004; pp. 1–10. [Google Scholar]

- Yoo, Y.; Henfridsson, O.; Lyytinen, K. Research Commentary: The New Organizing Logic of Digital Innovation: An Agenda for Information Systems Research. Inform. Syst. Res. 2010, 21, 724–735. [Google Scholar] [CrossRef]

- Grossman, S.J.; Stiglitz, J.E. On The Impossibility of Informationally Efficient Markets. Am. Econ. Rev. 1980, 70, 393–408. [Google Scholar]

- Alstyne, M.W.; Parker, G.G. Two-Sided Network Effects: A Theory of Information Product Design. Manag. Sci. 2005, 51, 1449–1592. [Google Scholar]

- Armstrong, M. Competition in Two-Sided Markets. Rand J. Econ. 2006, 37, 668–691. [Google Scholar] [CrossRef]

- Boudreau, K.; Hagiu, A. Platform Rules: Multi-Sided Platforms as Regulators. 2008. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1269966 (accessed on 23 August 2019).[Green Version]

- Weyl, G.E. A Price Theory of Multi-Sided Platforms. Am. Econ. Rev. 2010, 100, 1642–1672. [Google Scholar] [CrossRef]

- Ramaswamy, V.; Ozcan, K. Brand Value Co-Creation in a Digitalized World: An Integrative Framework and Research Implications. Int. J. Res. Mark. 2016, 33, 93–106. [Google Scholar] [CrossRef]

- Autio, E.; Thomas, L.D.W. Ecosystems and Value Co-Creation. Acad. Manag. Proceed. 2018. [Google Scholar] [CrossRef]

- Ramaswamy, V. Co-Creation of Value: Towards an Expanded Paradigm of Value Creation. Mark. Rev. 2009, 26, 11–17. [Google Scholar] [CrossRef]

- Pera, R.; Occhiocupo, N.; Clarke, J. Motives and Resources for Value Co-Creation in a Multi-Stakeholder Ecosystem: A Managerial Perspective. J. Bus. Res. 2016, 69, 4033–4041. [Google Scholar] [CrossRef]

- Moore, J.F. Shared Purpose: A Thousand Business Ecosystems, a Connected Community, and the Future, 1st ed.; CreateSpace Independent Publishing Platform: Charleston, SC, USA, 2013; pp. 25–39. [Google Scholar]

- Fumagalli, A.; Lucarelli, S.; Musolino, E.; Rocchi, G. Digital Labour in the Platform Economy: The Case of Facebook. Sustainability 2018, 10, 1757. [Google Scholar] [CrossRef]

- Catalini, C.; Gans, J.S. Some Simple Economics of the Blockchain. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2874598 (accessed on 30 June 2019).

- Harvey, C.R. Cryptofinance. 2016. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2438299 (accessed on 18 August 2019).

- Abadi, J.; Brunnermeier, M. Blockchain Economics. 2018. Available online: https://scholar.princeton.edu/sites/default/files/markus/files/blockchain_paper_v3g.pdf (accessed on 8 September 2019).[Green Version]

- Amit, R.; Zott, C. Value Creation in E-Business. Strateg. Manag. J. 2001, 22, 493–520. [Google Scholar] [CrossRef]

- Amit, R.; Massa, L.; Zott, C. The Business Model: Recent Developments and Future Research. J. Manag. 2011, 37, 1019–1042. [Google Scholar] [Green Version]

- Katz, M.L.; Shapiro, C. Network Externalities, Competition and Compatibility. Am. Econ. Rev. 1985, 75, 424–440. [Google Scholar]

- Katz, M.L.; Shapiro, C. Systems Competition and Network Effects. J. Econ. Perspect. 1994, 8, 93–115. [Google Scholar] [CrossRef]

- Shapiro, C.; Varian, H.R. Information Rules: A Strategic Guide to the Network Economy, 1st ed.; Harvard Business School Press: Boston, MA, USA, 1998; pp. 173–226. [Google Scholar]

- Clements, M.T. Direct and Indirect Network Effects: Are They Equivalent? Int. J. Ind. Organ. 2004, 22, 633–645. [Google Scholar] [CrossRef]

- Tóth, Z.; Peters, L.D.; Pressey, A.; Johnston, W.J. Tensions in a Value Co-creation Context: A Network Case Study. Ind. Mark. Manag. 2018, 70, 34–45. [Google Scholar] [CrossRef]

- Vargo, S.L.; Maglio, P.P.; Akaka, M.A. On Value and Value Co-Creation: A Service Systems and Service Logic Perspective. Eur. Manag. J. 2008, 26, 145–152. [Google Scholar] [CrossRef]

- Alves, H.; Fernandes, C.; Raposo, R. Value Co-creation: Concept and Contexts of Application and Study. J. Bus. Res. 2016, 69, 1626–1633. [Google Scholar] [CrossRef]

- Galvagno, M.; Dalli, D. Theory of Value Co-Creation: A Systematic Literature Review. Manag. Serv. Qual. 2014, 24, 643–683. [Google Scholar] [CrossRef]

- Mahr, D.; Lievens, A.; Blazevic, V. The Value of Customer Co-Created Knowledge during the Innovation Process. J. Prod. Innov. Manag. 2014, 31, 599–615. [Google Scholar] [CrossRef]

- Autio, E.; Nambisan, S.; Thomas, L.D.W.; Wright, M. Digital Affordances, Spatial Affordances, and the Genesis of Entrepreneurial Ecosystems. Strateg. Entrep. J. 2018, 12, 72–95. [Google Scholar] [CrossRef]

- Zeng, S. Study on the Strategy of Customer Participation in Service Innovation in Virtual Community. Am. J. Ind. Bus. Manag. 2018, 8, 1469–1475. [Google Scholar] [CrossRef] [Green Version]

- Farrell, J.; Katz, M.L. Innovation, Rent Extraction and Integration in Systems Markets. J. Ind. Econ. 2000, 48, 413–432. [Google Scholar] [CrossRef]

- Hoyer, W.D.; Chandy, R.; Dorotic, M.; Krafft, M.; Singh, S.S.; Chandy, R.K. 2010, Customer Co-creation in New Product Development. J. Serv. Res. 2010, 13, 283–296. [Google Scholar] [CrossRef]

- Greenstein, S.; Lerner, J.; Stein, S. Digitization, Innovation, and Copyright: What is the Agenda? Strateg. Organ. 2013, 11, 110–121. [Google Scholar] [CrossRef]

- Rysman, M.; Schuh, S. New Innovations in Payments. Innov. Policy Econ. 2017, 17, 27–48. [Google Scholar] [CrossRef]

- Cong, L.W.; Li, Y.; Wang, N. Tokenomics: Dynamic Adoption and Valuation. 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3153860 (accessed on 25 August 2019).[Green Version]

- Athey, S.; Parashkevov, I.; Sarukkai, V.; Xia, J. Bitcoin Pricing, Adoption and Usage: Theory and Evidence. 2017. Available online: https://siepr.stanford.edu/sites/default/files/publications/17-033_0.pdf (accessed on 5 September 2019).

- Budish, E. The Economic Limits of Bitcoin and the Blockchain. 2018. Available online: https://www.nber.org/papers/w24717 (accessed on 3 September 2019).

- Buterin, V. Ethereum: A Next Generation Smart Contract and Decentralized Application Platform. 2014. Available online: https://cryptorating.eu/whitepapers/ethereum/ethereum_white_paper.pdf (accessed on 8 July 2019).

- Seretakis, A. Blockchain, Securities Markets and Central Banking. 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3007402 (accessed on 30 August 2019).

- Cong, L.W.; He, Z.G. Blockchain Disruption and Smart Contracts. Rev. Financ. Stud. 2019, 32, 1754–1797. [Google Scholar] [CrossRef]

- Bordo, M.D.; Levin, A.T. Central Bank Digital Currency and the Future of Monetary Policy. 2017. Available online: https://www.nber.org/papers/w23711.pdf (accessed on 8 September 2019).

- Raskin, M.; Yermack, D. Digital Currencies, Decentralized Ledgers, and the Future of Central Banking. 2016. Available online: https://www.nber.org/papers/w22238.pdf (accessed on 22 August 2019).

- Chiu, J.; Davoodalhosseini, M.; Jiang, J.; Zhu, Y. Central Bank Digital Currency and Banking. 2019. Available online: http://ssrn.com/abstract=3331135 (accessed on 8 September 2019).[Green Version]

- Diniz, E.H.; Siqueira, E.; Heck, E.V. Taxonomy of Digital Community Currency Platforms. Inform. Technol. Dev. 2019, 25, 69–91. [Google Scholar] [CrossRef]

- Albuquerque, R.; Miao, J.J. Advance Information and Asset Prices. J. Econ. Theory 2014, 149, 236–275. [Google Scholar] [CrossRef]

- Banerjee, S. Learning from Prices and the Dispersion in Beliefs. Rev. Financ. Stud. 2011, 24, 3025–3068. [Google Scholar] [CrossRef]

- Normann, R.; Ramirez, R. From Value Chain to Value Constellation: Designing Interactive Strategy. Harv. Bus. Rev. 1993, 71, 65–77. [Google Scholar]

- Etgar, M. A Descriptive Model of the Consumer Co-Production Process. J. Acad. Mark. Sci. 2008, 36, 97–108. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F. Institutions and Axioms: An Extension and Update of Service- Dominant Logic. J. Acad. Mark. Sci. 2016, 55, 5–23. [Google Scholar] [CrossRef]

- Cova, B.; Dalli, D. Working Consumers: The Next Step in Marketing Theory? Mark. Theory 2009, 9, 315–339. [Google Scholar] [CrossRef]

- Ramaswamy, V.; Ozcan, K. What Is Co-Creation? An Interactional Creation Framework and Its Implications for Value Creation. J. Bus. Res. 2018, 84, 196–205. [Google Scholar] [CrossRef]

- Saarijärvi, H. The Mechanisms of Value Co-creation. J. Strateg. Mark. 2012, 20, 381–391. [Google Scholar] [CrossRef]

- Saarijärvi, H.; Kannan, P.K.; Kuusela, H. Value Co-creation: Theoretical Approaches and Practical Implications. Eur. Bus. Rev. 2013, 25, 6–19. [Google Scholar] [CrossRef]

- Ranjan, K.R.; Read, S. Value Co-Creation: Concept and Measurement. J. Acad. Mark. Sci. 2016, 44, 290–315. [Google Scholar] [CrossRef]

- Kohtamäki, M.; Rajala, R. Theory and Practice of Value Co-creation in B2B Systems. Ind. Mark. Manag. 2016, 56, 4–13. [Google Scholar] [CrossRef]

- Prahalad, C.K.; Ramaswamy, V. Co-Creation Experiences: The Next Practice in Value Creation. J. Interact. Mark. 2004, 18, 5–14. [Google Scholar] [CrossRef]

- Ceccagnoli, M.; Forman, C.; Huang, P.; Wu, D.J. Co-Creation of Value in a Platform Ecosystem: The Case of Enterprise Software. MIS Q. 2012, 36, 263–290. [Google Scholar] [CrossRef]

- Breidbach, C.F.; Maglio, P.P. Technology-Enabled Value Co-Creation: An Empirical Analysis of Actors, Resources and Practices. Ind. Mark. Manag. 2016, 56, 73–85. [Google Scholar] [CrossRef]

- Caillaud, B.; Jullien, B. Chicken And Egg: Competing Match-Makers. Rand J. Econ. 2003, 34, 309–328. [Google Scholar] [CrossRef]

- Masiak, C.; Block, J.H.; Masiak, T.; Neuenkirch, M.; Pielen, K.N. The Market Cycles of ICOs, Bitcoin and Ether. 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3198694 (accessed on 2 September 2019).

- Zittrain, J.L. The Generative Internet. Harv. Law Rev. 2006, 119, 1974–2040. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| 2007 | 2017 | ||

|---|---|---|---|

| Enterprise | MC(Billion $) | Enterprise | MC(Billion $) |

| Exxon Mobil | 467 | Apple | 815 |

| G.E. | 394 | Alphabet | 637 |

| Microsoft | 265 | Microsoft | 558 |

| ICBC | 259 | 485 | |

| Citi | 243 | Amazon | 461 |

| AT&T | 238 | Berkshire Hathaway | 438 |

| Royal Dutch | 232 | Alibaba | 415 |

| BoA | 230 | Tencent | 394 |

| Petro China | 225 | Johnson & Johnson | 357 |

| China Mobile | 207 | Exxon Mobil | 323 |

| ETHP | ETHT | UA | |

|---|---|---|---|

| Mean | 209.147 | 1796289 | 8048799 |

| Median | 13.84 | 348472 | 1022347 |

| Maximum | 1278.69 | 8608045 | 39866900 |

| Minimum | 0 | 8297 | 9639 |

| Std. Dev. | 291.25 | 2224362 | 12331958 |

| Skewness | 1.472 | 1.15 | 1.442 |

| Kurtosis | 4.544 | 3.042 | 3.524 |

| Jarque-Bera | 72.326 | 34.64 | 56.18 |

| Probability | 0 | 0 | 0 |

| Observations | 157 | 157 | 157 |

| Variables | DLOGETHP | DPETHT | DPUA |

|---|---|---|---|

| DLOGETHP | 1.000 | 0.136 | 0.198 |

| DPETHT | 1.000 | 0.539 | |

| DPUA | 1.000 |

| DLOGETHP | DPETHT | DPUA | |

|---|---|---|---|

| Mean | 0.016 | 0.052 | 0.055 |

| Median | 0.005 | 0.018 | 0.045 |

| Maximum | 0.249 | 1.441 | 0.344 |

| Minimum | −0.266 | −0.288 | 0 |

| Std. Dev. | 0.082 | 0.169 | 0.045 |

| Skewness | 0.222 | 3.700 | 2.476 |

| Kurtosis | 3.647 | 30.615 | 13.502 |

| Jarque-Bera | 4.029 | 5346.961 | 881.91 |

| Probability | 0.133 | 0 | 0 |

| Observations | 156 | 156 | 156 |

| Variables | DLOGETHP | DPETHT | DPUA |

|---|---|---|---|

| DLOGETHP(−1) | −0.045 | 0.656 *** | 0.092 *** |

| (0.088) | (0.132) | (0.023) | |

| DLOGETHP(−2) | 0.095 | 0.263 * | 0.041 |

| (0.095) | (0.144) | (0.025) | |

| DLOGETHP(−3) | 0.259 *** | 0.082 | 0.046 * |

| (0.091) | (0.136) | (0.024) | |

| DLOGETHP(−4) | −0.157 * | −0.042 | 0.02 |

| (0.087) | (0.131) | (0.023) | |

| DLOGETHP(−5) | −0.205** | −0.262 ** | −0.054 ** |

| (0.089) | (0.133) | (0.023) | |

| DPETHT(−1) | −0.0319 | −0.031 | −0.02 |

| (0.058) | (0.088) | (0.016) | |

| DPETHT(−2) | −0.008 | −0.094 | −0.01 |

| (0.059) | (0.089) | (0.016) | |

| DPETHT(−3) | −0.015 | 0.037 | −0.021 |

| (0.049) | (0.074) | (0.013) | |

| DPETHT(−4) | 0.060 | −0.029 | 0.003 |

| (0.049) | (0.074) | (0.013) | |

| DPETHT(−5) | 0.059 | −0.019 | 0.036 *** |

| (0.047) | (0.071) | (0.013) | |

| DPUA(−1) | 0.935*** | −0.517 | 0.653 *** |

| (0.336) | (0.505) | (0.089) | |

| DPUA(−2) | −0.291 | 0.568 | −0.081 |

| (0.399) | (0.599) | (0.106) | |

| DPUA(−3) | 0.134 | −0.364 | 0.233** |

| (0.367) | (0.551) | (0.097) | |

| DPUA(−4) | −0.511 | 0.319 | −0.007 |

| (0.347) | (0.521) | (0.092) | |

| DPUA(−5) | −0.254 | 0.313 | −0.059 |

| (0.264) | (0.397) | (0.07) | |

| C | 0.016 | 0.0168 | 0.011 *** |

| (0.013) | (0.02) | (0.003) | |

| Observations | 152 | 152 | 152 |

| R-squared | 0.223 | 0.224 | 0.712 |

| Adj. R-squared | 0.138 | 0.138 | 0.68 |

| Dependent Variable: DLOGETHP | |||

| Excluded | Chi-sq | Df | Prob. |

| DPETHT | 3.224 | 5 | 0.666 |

| DPUA | 12.134 | 5 | 0.033 ** |

| All | 13.52 | 10 | 0.196 |

| Dependent variable: DPETHT | |||

| Excluded | Chi-sq | Df | Prob. |

| DLOGETHP | 33.82 | 5 | 0.000 *** |

| DPUA | 3.741 | 5 | 0.587 |

| All | 37.494 | 10 | 0.000 *** |

| Dependent variable: DPUA | |||

| Excluded | Chi-sq | Df | Prob. |

| DLOGETHP | 31.3 | 5 | 0.000 *** |

| DPETHT | 12.208 | 5 | 0.032 ** |

| All | 41.777 | 10 | 0.000 *** |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huang, H. How Does Information Transmission Influence the Value Creation Capability of a Digital Ecosystem? An Empirical Study of the Crypto-Digital Ecosystem Ethereum. Sustainability 2019, 11, 5345. https://0-doi-org.brum.beds.ac.uk/10.3390/su11195345

Huang H. How Does Information Transmission Influence the Value Creation Capability of a Digital Ecosystem? An Empirical Study of the Crypto-Digital Ecosystem Ethereum. Sustainability. 2019; 11(19):5345. https://0-doi-org.brum.beds.ac.uk/10.3390/su11195345

Chicago/Turabian StyleHuang, He. 2019. "How Does Information Transmission Influence the Value Creation Capability of a Digital Ecosystem? An Empirical Study of the Crypto-Digital Ecosystem Ethereum" Sustainability 11, no. 19: 5345. https://0-doi-org.brum.beds.ac.uk/10.3390/su11195345