A Win-Win Outcome between Corporate Environmental Performance and Corporate Value: From the Perspective of Stakeholders

Economics and Management School, Wuhan University, Wuhan 430072, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(3), 921; https://0-doi-org.brum.beds.ac.uk/10.3390/su11030921

Submission received: 19 January 2019

/

Revised: 2 February 2019

/

Accepted: 4 February 2019

/

Published: 12 February 2019

(This article belongs to the Special Issue Comparative Corporate Social Responsibility (CSR) and Sustainable Development Goals (SDGs))

Abstract

:This paper combines determinants of corporate environment performance (CEP) and the effect of CEP on corporate value together, namely how to motivate firms to conduct environmental protection from the perspective of enhancing firm value. Using a sample of 204 observations of listed corporations in Chinese pollution-intensive industries over the period of 2013–2014, we observed that: (1) compared to investment in a single stakeholder, combinations of multidimensional stakeholders are more likely to affect CEP, and the path is not unique; (2) employees have a positive role, but investors, the community, suppliers, and customers have negative roles; (3) among three patterns for high CEP, both high investment in employees and low investment in the community, suppliers and customers will not detract from firm value, i.e., a win-win outcome; (4) among three patterns for low CEP, one will enhance firm value; and (5) the investor should be seen as an important breakthrough in corporate environmental protection. Such conclusions have stronger promotional value for other emerging countries where corporate social and environmental responsibility is still in the initial stage and the traditional corporate government mode still has a leading position.

1. Introduction

Global environmental degradation is a side-effect of economic development, which is why achieving a balance between economic development and environmental protection has attracted significant public concern [1,2]. For example, based on the BP Statistical Review of World Energy 2017, mainland China consumed 23% of global primary energy and produced 27.3% of global carbon dioxide emissions in 2016 [3]. However, according to feedback from real-world data, the policies mostly demonstrate a trade-off rather than a win-win [4]. Tang et al. [5] found that the effects of environmental regulations are constrained by economic goals, especially for local government. When we focus on corporate environment practices, only 33% of listed firms in China choose to publish social and environmental reports [6]; most firms doubt that this action will detract from firm value [7]. Herein, the corporate value mainly refers to the corporate market value [8], since it has less discretionary space, compared to the accounting-based variable [9]. Meanwhile, it can better predict firm performance in the long run, therefore testing whether a certain corporate environmental strategy is sustainable [10]. More importantly, the expectation of a win-win situation between corporate environmental performance (CEP) and corporate value is an additional incentive to make headway in the pro-environmental change process [11]. Therefore, our paper is determined to answer how to obtain a win-win outcome between CEP and corporate value.

In view of the increasing importance of corporate environmental protection, relevant theoretical research addresses the issue mainly from two perspectives, i.e., determinants of variation in CEP across firms either from legitimacy theory [12] or stakeholder theory [13] and the effect of CEP on corporate value [7,14]. However, as far as we know, these two representative studies are conducted separately (details discussed below). Actually, they are tightly connected, theoretically and practically speaking, because the determinants of CEP affect the formation of the corporate environmental strategy, which in turn impacts the corporate value restricted to concrete execution. Therefore, the question lies in how we select the appropriate perspective to combine two types of research together. Herein, we choose stakeholders based on two important considerations. According to the definition by Freeman [15], stakeholders can affect the enterprise’s operation while at the same time being affected by it, thus providing us a reasonable research scope with a solid theoretical foundation compared to those with a general reference, such as legitimacy theory [16]. Moreover, stakeholders’ power not only affects the corporate environmental strategy [17], but also helps internalize the concrete effect of CEP due to the stakeholders’ orientation towards CEP [18].

Though stakeholder theory is pivotal, little effort has been made to explore the interaction between stakeholders [19]. In fact, there are complementary and trade-off relations between stakeholders; recently, some scholars have attempted to address this issue from a configurational perspective [20,21,22]. That is to say, instead of employing the linear fashion method, we should turn to the configurational perspective.

As for the effect of corporate environmental protection, numerous studies have failed to reach a consistent conclusion. Evidence from the regional or industrial perspective has used an aggregate index, ignoring firm heterogeneity. Meanwhile, firm-level evidence not only neglects the conditions of CEP that have occurred, but also mainly employs the linear fashion method. Actually, the consequence of CEP should be non-linear [2]. Therefore, we employ the fuzzy-set/qualitative comparative analysis (fs/QCA) method, which can manage multiple interactions and non-symmetric relationships simultaneously by using firm-level data.

To test our hypothesis, we use a sample of 204 observations of listed corporations in Chinese pollution-intensive industries over the period of 2013–2014. We measured the score of each stakeholder from the Hexun Corporate Social Performance (CSP) Database [23], which not only provides relatively authoritative and professional scores for CSP that differ from content analyses by certain authors, but is also more suitable for CSP practices in China (seen Section 4.2). We choose Tobin’s Q as the related output variable. By applying an fs/QCA in view of the fact that complementarity and trade-offs exist between stakeholders [15], the results suggested that both high CEP and low CEP have three patterns. For high CEP, none of the three patterns were able to enhance firm value, but two patterns (~community * (~supplier and customer + employee)) did not detract from corporate value; namely, such environmental protection will be sustainable. For low CEP, high investment in the community with few employees also lowers firm value, but one pattern (investor * supplier and customer * community) will add firm value. This striking contrast in the outcome for different CEP strategies provides us with a clear explanation of why firms are more willing to choose a reactive environmental strategy. As to the effect of a single stakeholder on CEP, high investment in employees and low investment in investors, suppliers, and customers or the community are more likely to result in high CEP, while low investment in employees and high investment in investors, suppliers, and customers or the community are more likely to result in low CEP. Additionally, investment relations are more important for firm value and combinations of stakeholders rather than investment in a single stakeholder in terms of the likelihood of affecting CEP and related outcomes.

By shedding light on corporate environmental strategy selections and related outcomes, our research contributes to the prior research in several ways. First, as stated above, our study combines the effect of CEP with the formation of firms’ environmental strategy. Traditional works directly study the determinants or consequences of CEP, regardless of their combination. In this way, we focus on how to motivate firms to conduct environmental protection from the perspective of enhancing firm value, instead of passively responding to government regulations. Meanwhile, we propose a new understanding for the inconsistent effect of environmental protection. Traditional studies employ linear regression to manage such inconsistencies, but this neglects the conjunction, equifinality, and asymmetry among elements [24]. By using fs/QCA, we argue that the configuration rather than a single element affects CEP and the related outcome, i.e., whether CEP boosts firm value depends on the combinations of stakeholders. Besides, another contribution is that our research provides a comprehensive perspective for stakeholders’ net power with respect to CEP. Traditional research always assumes that firms passively react to stakeholders’ absolute power. Actually, firms have more space and greater chances of counteracting the absolute power of stakeholders, especially for emerging countries (discussed below). Based on this setting, the results found that the employee is in a core position to guarantee high CEP and that the investor is in a core position to guarantee a high firm value, which provides appropriate classifications of stakeholders rather than traditional elements in primary and secondary stakeholders. Such conclusions have stronger promotional value for countries where CSP is still in the initial stage and the traditional corporate government mode still has a leading position.

2. Literature Review

Although scholars have conducted fruitful studies on CEP, these studies can be mainly classified as determinants of CEP and related consequences on firm value, and they are also key research questions in this paper. Therefore, we conduct a thorough literature review from these two aspects and then present comments on the research.

2.1. Determinants of CEP

As one important component of CSP, the determinants of CEP closely resemble those of CSP [25,26], thereby guiding us to follow such logic to conduct a more careful literature review.

When explaining why firms are engaged in corporate environmental protection, two typical theories are used. Legitimacy theory recognizes legitimacy as an important factor that affects firm operations [27]. The firm’s legitimacy will be improved if its value system conforms to that of the social system. Conversely, the firm’s legitimacy will be threatened. Therefore, a firm may use a proactive corporate environmental strategy to improve or repair legitimacy [12]. It must be noted, however, that legitimacy theory provides firms with broader objectives whose expectations should be met. Consequently, scholars introduced stakeholder theory to better explore why firms choose different corporate protection strategies [13]. Previous studies have indicated that various CEP across firms may result from shareholders and creditors, suppliers, and customers [17], employees [28], and the general public [29]. Additionally, a few studies include broader stakeholders in exploring the formation of a corporate environmental strategy. Buysse and Verbeke [30] conducted an empirical analysis of linkages between CEP and stakeholder management, and they found that a more proactive corporate environmental strategy means broader coverage of stakeholders.

2.2. Consequences of CEP

Relevant theoretical studies have addressed the issue of the consequences of CEP from two aspects. The first representative study focused on the effect of environmental regulation from a regional or industrial perspective. Traditional views based on neoclassical economics argue for a negative relationship between environmental protection and economic development. Although environmental regulation may enhance environmentally-friendly innovations, it will crowd out other R&D investment, thus dampening economic development [31]. Evidence from Lee [32] has supported this viewpoint, and the rising cost has decreased the production rate by 12%. Meanwhile, the Porter hypothesis stresses positive outcomes through innovation offsets and learning effects [33]. Testa et al. [34] found that more stringent environmental regulations have acted as a motivation for firms to implement innovations, which in turn enhances competitive performance. Additionally, some scholars pay attention to nonlinearity, i.e., the effect of environmental regulation relies on certain context factors. For example, Zhao and Sun [35] stressed that flexible regulation can offer a stronger motivation for environmental protection. However, what is noteworthy is that evidence from the regional or industrial perspective has overlooked firm heterogeneity, and an important breakthrough point would be to identify the effect of environmental regulation from the firm perspective [36].

Another representative study focuses on the effect of CEP on firm value. Based on Friedman’s classic point that the responsibility of the firm is to increase profits, some scholars argue that CEP will crowd out resources that were originally intended for investment in core competitive business, thus leading to the lack of competitive advantage compared to its rivals. The management opportunism hypothesis also opposes CEP. In addition, some scholars agree with the reputation effect of CEP, but firms have difficulty internalizing the effects to complement the costs [37]. The alternative view argues that firms can cultivate rare, unduplicated, and irreplaceable resources in the process of increasing CEP based on instrument stakeholder theory and resource-based views [38], thus positively affecting firm value [8]. Meanwhile, Singh et al. [39] thought that getting accreditation in environmental programs such as ISO 14000 standards enables firms to achieve legitimacy by signaling to stakeholders their internal emphasis on environmental performance and pressing their supply chain partners to obtain similar accreditation. Other scholars indicated that the effect of CEP is based on certain conditions and that a non-linear relationship may be more appropriate [2].

2.3. Review Comments

With a systematic argument about the drivers and the effects of CEP, it is easy to see that numerous studies have been conducted, particularly on the effect of CEP, thus providing us a theoretical foundation for our research. However, the theoretical evidence fails to provide consistent conclusions to guide firms in balancing corporate environmental protection and firm development. We believe that there are several shortcomings that should be addressed.

Prior studies separate the two, especially studies on the consequences of CEP, which ignore the formation of corporate environmental strategy, while theoretically and intuitively speaking, various strategies result in different outputs via detailed implementation. Here, we address the issue by introducing stakeholders in view of their influence on the formation and implementation of the corporate environmental strategy.

Rooted in CSP, scholars always investigate drivers of CEP based on stakeholder theory. Nevertheless, little effort has been made to explore the interaction between stakeholders [19]. In fact, there are complementary and trade-off relations between stakeholders; recently, some scholars have attempted to address this issue from a configurational perspective [20,21,22]. Here, we still follow this view to understand the interdependence of stakeholders.

As for the effect of corporate environmental protection, numerous studies have failed to reach a consistent conclusion. Evidence from the regional or industrial perspective has used an aggregate index, ignoring firm heterogeneity. Meanwhile, firm-level evidence not only neglects the conditions of CEP that have occurred, but also mainly employs the linear fashion method. Actually, the consequence of CEP should be non-linear [2]. Therefore, we employed the fs/QCA method, which can manage multiple interactions and non-symmetric relationships simultaneously by using firm-level data.

3. Theories and Hypothesis Development

3.1. Multiple Dimensions and Classifications of Stakeholders

CSP has been explained as a corporation taking economic responsibility and having responsibilities in legislation, ethics, and charity. Although this definition from Carroll is widely used in the research, this type of classification is vague in practice, as he noted in 1991 [40]. The stakeholder, another component that is closely associated with CSP, specifies the dimensionality of CSP. According to Freeman, stakeholders can affect the enterprise’s operation, while simultaneously being affected by it. In general, stakeholders include investors, employees, suppliers, customers, the environment, and the community [41,42].

Among these stakeholders is the investor, who, as the funds provider, determines the funding source. If they follow the traditional corporate governance mode stating that corporate environmental protection violates firm development, corporate environmental projects cannot obtain financial support, thus determining the formation of an environmental strategy. Moreover, considering the highly risky and time-consuming traits of these projects, the investor may choose to suspend these projects, thus affecting the consequences of CEP. An employee’s environmental awareness and skills have an important effect on the success of corporate environmental projects. Environmentally-friendly materials from the supplier and the acceptance level of green products from the customer also largely impact the formation and consequences of corporate environmental strategy. Moreover, the general public can exert a certain amount of pressure on firms to force firms to obtain higher CEP.

The stakeholders’ multiple dimensions exhibit diversity, but whether they have the same weight for CEP and firm value is unclear. Kacperczyk [43] found that concern for the environment and the community led to higher firm value compared to other dimensions, which indicates that there are different weights for them. According to the concept of the resource-based view, the primary stakeholders are key factors in influencing the enterprise due to the irreplaceability and social complexity of the connection with enterprises when compared to secondary stakeholders that have a broader definition and connotation. Based on Clarkson [44], the primary stakeholders are dimensions without which an enterprise cannot exist, including the investors, employees, suppliers, and customers. However, secondary stakeholders refer to others without direct engagement in economic transactions, such as the community.

Although the above classification of stakeholders that is based on absolute power has been widely used, firms should not be recognized as passively reacting to stakeholders’ power. Actually, firms can use their power to influence absolute power from stakeholders [45]. Therefore, the power of stakeholders should be the difference between the firm and stakeholder [18]. For instance, both the supplier and customer are always considered primary stakeholders—namely, having absolute power—but certain firms may use product price or contracts to reduce the absolute power. In other words, it is the stakeholder-firm power difference rather than absolute power that determines various CEP and related results.

The stakeholder-firm power difference will be more appropriate for emerging countries. Considering the immature regulatory, industrial, and social environments in these countries, firms have more space and greater chances of counteracting the absolute power of stakeholders [46]. China, as the largest emerging market, provides us with better research materials to investigate the validity of the stakeholder-firm power difference

To sum up, we provide a joint framework for stakeholder theory with a stakeholder-firm power difference. Among them, stakeholder theory provides us with a reasonable research scope; namely, who affects the formation and consequences of the corporate environmental strategy. Meanwhile, we use stakeholder-firm power rather than absolute power to better understand the actor of each stakeholder in CEP. It is possible and helpful to link them to better understand corporate environmental practices in emerging countries.

3.2. Configurational Perspective of Stakeholders

A joint framework of stakeholder theory with the stakeholder-firm power difference only explores the single stakeholder’s role, and the next issue that should be addressed is the clarification of the interdependency among stakeholders. Actually, there are both complementary and trade-off aspects among stakeholders, i.e., a configurational perspective on the interactions of stakeholders.

Investments in two elements are complementary when the returns from an investment in Component A are an increasing function of the investments in Component B, and vice versa. Based on this logic, joint actions among elements tend to perform better than the action of a single element, and this is the key distinction of the traditional regression method. “Complementary” means that stakeholders’ multiple dimensions can have an interactive influence on the CEP, since adding an investment to a certain type of stakeholder does not mean that this must reduce the investment of other stakeholders, and companies will invest in certain types of stakeholders as a whole. They have a strong link to improve the competitive advantage of the company and their own welfare as well. As Freeman [15] argued, the values of each stakeholder group are diverse, but they are consistent with each other.

The trade-off between stakeholders’ multiple dimensions is the optimal input ratio among various stakeholders, which is rooted in the high cost of CSP and the scarcity of corporate slack resources [47]. There may be an optimal investment level in stakeholders and a centralized investment strategy with a better effect. In fact, an important view for criticizing CSP is that the lack of a clear balance among stakeholders leads to the lack of an obvious boundary level [48]. Meanwhile, according to Godfrey et al. [49], the feedback of stakeholders is based on a certain level of investment; namely focusing the resources for certain stakeholders is more likely to reach the corresponding perception level and improve corporate value more quickly.

To conclude, given the multiple dimensions of stakeholders, the analysis of the stakeholder-firm power difference on CEP is not suitable for adopting a unitary or aggregate index; the configurations should be a combination of various stakeholders in view of the complementarity. Moreover, regarding the trade-off between the multiple dimensions of stakeholders, the configurations that companies can choose possess strong heterogeneity. In light of these arguments, we propose our first hypothesis:

Hypothesis 1.

Compared to a single stakeholder, configurations are more likely to result in high or low CEP, but there is no unique optional configuration for pollution-intensive industries.

3.3. Each Stakeholder Role in the Configurations

Investors, as the funding provider, have more influence on CEP according to the empirical evidence [50], which demonstrates their absolute power. However, in China, where the indirect financing channel has a dominant position, it is hard for firms to exert an effective influence on this group to counter the absolute power; i.e., the investor has essentiality and exclusivity. However, this high net power does not match the willingness towards CEP. Although the green-credit policy and equator principles have been brought to China, fewer banks adopt this principle: they are more concerned with liquidity, profitability, and security than CEP. Related empirical evidence has found that both the shareholder [13] and creditor [51] have a negative effect on CEP. It is therefore hypothesized that:

Hypothesis 2.

There is a negative effect of investors on CEP for pollution-intensive industries.

According to the traditional classifications of stakeholders, the employee is among the primary stakeholders, and they have stronger absolute power with respect to corporate development. However, different from the Western background, trade unions are relatively weaker in China, especially for private firms, and it is difficult for a single employee to conduct effective negotiations with firms. Firms can use timely and accurate payroll delivery to avoid other employee responsibilities, thus allowing for the possibility of reducing this absolute power.

However, for pollution-intensive industries, environment pollution is accompanied by employee safety, so it may be best to implement an interdependent combination of environmental and occupational health and safety systems [28]. During the corporate practice process, firms always try to adopt an environment, health, and safety (EHS) management system following the instructions of the ISO14001 environment management system and the OHSAS18001 professional health safety control system. Additionally, being among the internal stakeholders, both the skills and participation of employees are key to implementing a proactive environmental strategy [30]. Following this logic, we can infer that firms will not counter the absolute power, and they are more likely to include employees in the process of implementing corporate environmental protection. Therefore, this study proposes the following hypothesis:

Hypothesis 3.

There is positive effect of employees on CEP for pollution-intensive industries.

Both the supplier and customer, as the material provider and product buyer, are essential stakeholders of firms. Related evidence found that customers are willing to buy environmentally-friendly products, and powerful suppliers also refuse to provide materials for firms producing environmentally unfriendly products [52]. However, in China, the extensive growth mode from decades of the economic developmental process has led to ignorance of the CEP from the supplier and customer. For example, firms can take advantage of customers’ low purchasing power and suppliers’ payment terms and conditions to reduce this absolute power. Tang and Tang [18] also found that high CSP cannot lead to equivalent firm performance compared to Western countries, where suppliers and customers are willing to participate in these business strategies. In conclusion, the supplier and customer have essentiality, but lack exclusivity, and it is hypothesized that:

Hypothesis 4.

There is negative effect of the supplier and the customer on CEP for pollution-intensive industries.

The community, as the secondary stakeholder, has less absolute power with respect to firms, and this weak position will be magnified by weak CSP in China. Although the community lacks essentiality and exclusivity in China, it could produce a strong reputation effect. For example, during the Sichuan earthquake in China, Wong Lo Kat became the first company to donate 100 million Yuan, thus acquiring a formidable reputation [53]. Additionally, firms are the main donors compared to individuals. Du et al. [29] found that CEP weakness is positively associated with this community feedback in conducting green-washing due to its relatively lower costs compared to other dimensions, i.e., window-dressing [54]. For this reason, it is hypothesized that:

Hypothesis 5.

There is negative effect of community on CEP for pollution-intensive industries.

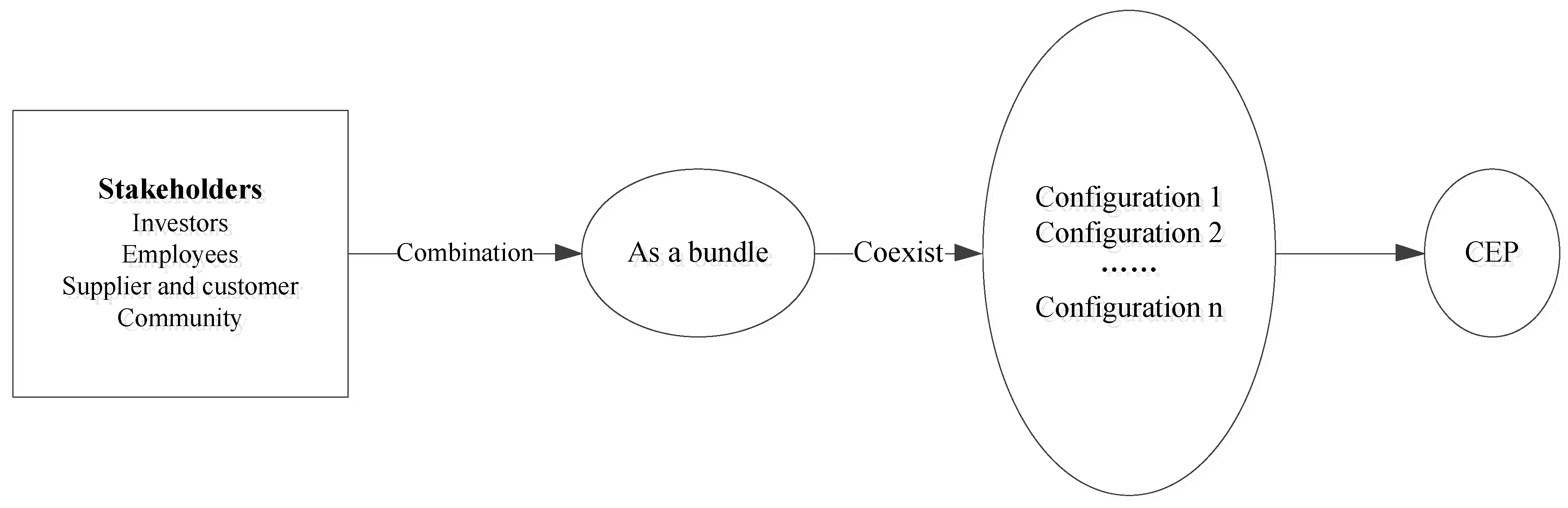

Figure 1 summarizes how these stakeholders work together to affect CEP, which serves as a starting point of our empirical analysis. Herein, stakeholders, including investors, employees, suppliers, and customers, as well as the community, combine as a bundle, and then form configurations to affect CEP.

4. Research Design

4.1. Data and Sample

Our main data sources included the Hexun CSP Database and CSMAR Database. The Hexun CSP Database measures CSP in the dimensions of the investor, employee, supplier, customer, environment, and community, and it is the most widely-used CSP measurement in current studies (discussed below). The CSMAR Database provides other financial information, and it is generally accepted by scholars who study listed firms in China [6].

To control the lag effect of CSP, we chose CSP dimensions in 2013 and firm value in 2014 from listed A-share firms in Chinese pollution-intensive industries, which include the industries of mining, food and beverages, petroleum, chemistry and plastic, and others that are defined by the China Securities Regulatory Commission [35]. Considering the Chinese stock market turbulence in 2015 and 2016, the end of our sample is in 2014, since the corporate value is computed based on stock price (discussed below). In the first half of 2015, China’s Shanghai composite index increased by 60%, and reached the peak point of 5178.19 on 12 June 2015, but suddenly dropped to the point of 2850.71 in the next two months.

Beginning with the initial sample, we exclude (1) cross-listed corporations given the special regulatory system, (2) observations belonging to the IPO year due to the IPO effect, (3) ST/PT corporations due to abnormal financial conditions, and (4) observations with missing values. We ultimately obtained 204 observations for our primary tests.

4.2. Variable Definitions

The metric for the firm value is Tobin’s Q, defined as the market value divided by the book value, and it has several advantages. Compared to the accounting-based variable, it has less discretionary space [9]. Meanwhile, it can better predict firm performance in the long run, therefore testing whether a certain corporate environmental strategy is sustainable [10]. Moreover, numerous prior studies have adopted this index based on China’s setting, similar to Kong et al. [55], Singh et al. [39], etc.

We measure multiple dimensions of CSP according to the Hexun CSP Evaluation System, which measures the CSP of listed A-share firms in China from the following aspects: investors, employees, suppliers, customers, the environment, and the community. These five dimensions include 13 second indexes and 37 third indexes [56], with a potential maximum score of 100 to aggregate the extent of each firm’s overall CSP. Similar samples drawn from the Hexun CSP Database, such as Xiong et al. [57], Li et al. [58], Tang et al. [6], etc., have also been published in prestigious academic journals.

The sample distribution, definitions, and descriptive statistics of the variables are listed in Table 1. According to Table 1, the metal and non-metal materials industry and the petroleum, chemistry, and plastics industry account for the two largest sample proportions. Compared to the employee, supplier, and customer, the other dimensions had more fluctuations, and the mean value of Tobin’s Q for the sample firms was 1.733.

4.3. Research Method

Unlike the traditional linear fashion, we study this relationship from a configurational perspective. We implement fs/QCA. This method makes it possible to investigate multiple-factor interactions, while the traditional regression method fails to achieve this. Additionally, this method stresses asymmetries from the conditions to outcome, which can help explain why firms choose different environmental strategies. This method also thinks configurations are equifinal, which means that firms can implement proactive strategies in either customer relations, employee relations, or other stakeholders’ relations.

As a method of set-theory, fs/QCA uses set-subset connections rather than correlations to depict the relations between conditions. If Set A is contained in Set B, then A is the sufficient condition for B. On the contrary, B is a necessary condition for A. In the extreme case, the two variables are totally uncorrelated and still have better set-subset connections [20]. To compute the empirical strength of the necessary and sufficient conditions, we rely on consistency and coverage measures in the next two equations.

Consistency (X ≤ Y) = ∑min (xi, yi)/∑xi

Coverage (X ≤ Y) = ∑min (xi, yi)/∑yi

Among them, Xi is the degree of membership of individual i in configuration X, and Yi is its degree of membership in outcome Y.

Although both the consistency and coverage range from 0–1, they have different meanings. Consistency indicates how closely a perfect subset relationship is approximated, and the larger the consistency is, the more perfect the relationship is. For instance, a consistency score of one demonstrates that X is completely contained in Y. We generally accept a consistency value when it is above 0.75 [59], and it is roughly similar to a significance score in a regression analysis, while coverage evaluates the degree to which a cause or a causal combination leads to the instance of a certain result. It is roughly akin to R-squared in a regression analysis, and it does not have this benchmark value.

To demonstrate the combination of conditions, Boolean algebra has been used. Among them, * denotes “AND”, + denotes “OR”, ~ denotes “ABSENCE”, and → denotes the logical implication operator.

To complete the transformation of a variable to a fuzzy set, we follow Garcia-Castro and Francoeur [20] and chose the 25th, 50th, and 75th percentiles as the minimum threshold, crossover point, and maximum threshold. At the same time, we used the direct method based on the fuzzy package by Longest and Vaisey [60] in Stata to complete the calibrations, and all results reported below are also based on this package. Table 2 lists the relative fuzzy sets’ calibration.

5. Empirical Analysis

According to Sharma and Vredenburg [61], both a proactive environmental strategy and a reactive environmental strategy can be observed as continuous variables, and their difference will be reflected in CEP scores. Thus, it is natural for us to classify high CEP as a proactive environmental strategy and low CEP as a reactive environmental strategy. On this basis, the patterns for high CEP are equivalent to a proactive environmental strategy, and the patterns for low CEP are equivalent to a reactive environmental strategy. Marquis and Qian [62] conducted similar actions to differentiate the symbolic CSP from substantial CSP.

5.1. Results for Proactive Environmental Strategy

Table 3 lists the sufficiency and necessity matrix. Given the benchmark value of 0.75, we found that the employee constitutes a necessary condition of superior CEP, and necessary scores of other stakeholders ranged from 0.325–0.473, below 0.75. The sufficiency scores ranged from 0.286–0.702, all of which are below 0.75, which indicates that none can be observed as a sufficient condition for CEP. Therefore, we can infer that a single stakeholder cannot lead to high CEP, and this conforms to Hypothesis 1: namely, a single stakeholder cannot result in the formation of a corporate environmental strategy.

Table 4 lists patterns for high CEP and related outcomes for Tobin’s Q. Three patterns resulted in a proactive environmental strategy, and the total coverage was 0.803, which accounted for larger proportions of related samples. Although the total consistency was 0.725, the consistency of each pattern was above the benchmark value. The expression of C1 is ~investor * employee * ~ supplier and customer → high CEP, which shows low investment in the investor, supplier and customer, and high investment in employees leads to high CEP, thus supporting Hypotheses 2–4. Given the combination of these stakeholders, the consistency of C1 with a high CEP to a high Tobin’s Q was 0.374, below the benchmark value of 0.75, indicating that it cannot enhance firm value. However, its consistency with a low Tobin’s Q was 0.79, thus demonstrating the eroding of the firm value in the long run.

Configurations of C2 and C3 not only have higher unique coverage, but also maintain the present status, namely without increasing or decreasing the firm value. The expression is ~community * (~supplier and customer + employee) → high CEP, and both patterns consider investors as being unaffected regarding the result, thus supporting Hypotheses 3–5. The employee, supplier, and customer do not possess high net power, but an employee has natural a relationship that the supplier and customer do not have in relation to the corporate environmental strategy. Moreover, firms with a high CEP decrease unnecessary green-washing to save scarce resources.

Among these three patterns, the different consequences of corporate value should draw our attention. Compared to C2 and C3, the key difference lies in low investment relations. Just as we noted that the investor had the highest net power with respect to firms in China, it is difficult to enhance corporate performance without decreasing investment in this group, and the results for a reactive environmental strategy in the following section also support this viewpoint.

5.2. Results for a Reactive Environmental Strategy

Table 5 lists the sufficiency and necessity matrix. Given the benchmark value of 0.75, we found that no single stakeholder constitutes the necessary condition, but the community, supplier, and customer constitute a sufficient condition for a reactive environmental strategy, thus supporting Hypotheses 4 and 5.

Table 6 lists patterns for low CEP and related outcomes for Tobin’s Q. There are also three patterns that result in a reactive environmental strategy. The total coverage was 0.722, which accounts for larger proportions of related samples, while the total consistency is 0.860, which is far better than 0.75. The expression of C4 is investor * supplier and customer * community → low CEP, which shows significant investment in the investor, supplier, customer, and community leads to low CEP, thus supporting Hypotheses 2, 4, and 5. For C5 and C6, they had a higher unique coverage, and the expression is ~employee * (supplier and customer + community), indicating the positive effect of the employee and the negative effect of the community, supplier, and customer, i.e., Hypotheses 3–5.

Among these three patterns, the related outcome varies greatly. The consistency of C4 for a high Tobin’s Q was 0.819, indicating enhancing firm value. Meanwhile, the consistency of C5 for a low Tobin’s Q was 0.773, demonstrating an eroding of the firm value. Moreover, the consistency of C6 with either type of Tobin’s Q was below 0.75, which means unchanged firm value. When conducting a closer analysis of these patterns’ formation, this finding still supports the argument that the investor plays a significant role in enhancing firm value. However, the new finding was that in C5, high investment in the community with weak CEP, will detract from firm value, which means that although green-washing can cover poor corporate environmental protection [29], this masking tactic should be controlled to a certain extent.

5.3. Robust Tests

We conducted a series of robust tests to verify that the results shown hold under different sample years, different classification methods, and different calibrations.

(1) Since the fs/QCA method could not work with the panel data, we attempted to present the results of a proactive and reactive environmental strategy in each years from 2010–2012. The beginning year of 2010 was because Hexun evaluates CSP from this year, and the calculation procedures remained unchanged.

Table 7 lists configurations for high CEP from 2010–2012. Among them, there are respectively three patterns, two patterns and three patterns for 2010, 2011, and 2012, which resemble the number from 2013. The solution consistency varied from 0.75–0.794, and the total coverage ranged from 0.574–0.697, indicating higher coverage of related samples.

As for each stakeholder role in the configurations, the employee has a positive effect on CEP, while the community, supplier, and customer have a negative influence on CEP, thus supporting H Hypotheses 3–5. However, the results of C7 and C13 violated the results of C10 and C12 regarding the role of investor, which seemingly demonstrates a rejection of Hypothesis 2. Upon closer examination, these results confirm Hypothesis 1: namely, there is no unique mode. Moreover, the unique coverage of C7 and C13 accounted for a small proportion of the total coverage.

None of the related consequences can enhance firm value, but both C10 and C12 eroded firm value, which again supports the key role of the investor in affecting firm value.

Table 8 depicts patterns for low CEP from 2010–2012. A low employee effect emerged in all of these patterns, thus entirely supporting Hypothesis 3. Meanwhile, Hypotheses 2, 4, and 5 have also been supported overwhelmingly. As for the related consequences, C15, C17, C20, and C21 can enhance firm value, and none detract from firm value. The striking contrast between Table 7 and Table 8 helps explain why firms always try to meet the basic requirements of environmental regulation from the government in China.

(2) Following the procedure of Fiss [59], we employed a traditional cluster method to conduct mode classification. Before the cluster analysis, we standardized all variables. In the first step, a hierarchical cluster analysis was used to find an appropriate cluster and then adopt a K-means cluster analysis.

Table 9 lists the result of the K-means cluster analysis, and it demonstrates that four clusters were better. Among them, C25 and C23 had high CEP, while C22 and C24 had low CEP. All results basically support the negative influence of employees and the positive effect of the community, supplier, and customer on CEP, i.e., Hypotheses 3–5. However, the investor serves as a mixed role in C22 and C25, seemingly rejecting Hypothesis 2. We can explain the result from the following aspects. First, unlike the community, supplier, and customer, the necessity scores and sufficiency scores in Table 3; Table 5 are in the middle, which indicates the possibility of introducing the investor in a proactive environmental strategy. Second, after synthesizing all results from Table 3, Table 4, Table 5, Table 6, Table 7, Table 8 and Table 9, we can overwhelmingly support Hypothesis 2. Third, just as Fiss [59] indicated, the results from the cluster method should be mere reference points compared to those of fs/QCA.

(3) We also change the calibrations with ±10 percentile points, and the results suggested no substantial change in our main results except for the different coverage scores and consistency scores. Additionally, we used the contemporary variable for output variables and changed it into a return on assets (ROA), and the main conclusions still hold.

6. Discussion

Our study links the determinants of CEP and its corresponding effect from the perspective of stakeholders. Compared with previous studies, we drop the traditional linear regression, which neglects the conjunction, equifinality, and asymmetry among elements. Though previous studies, such as Ni et al. [41], Garcia-Castro, and Francoeur [20], have adopted the fs/QCA method to consider the conjunction, equifinality, and asymmetry among stakeholders in the corporate sustainability field, these papers mainly focus on how these stakeholders interact with each other to affect corporate value. While, in our paper, we set the corporate environment performance as the outcome and then how these stakeholders work together to affect firm value when environment performance is low or high.

Meanwhile, our study also relates to those papers mainly because it employs the linear regression method in studying determinants of CEP. Our results found that investors have a negative effect on CEP, similar to Lu and Abeysekera [13], while employees are positively related to a proactive environmental strategy [30]. Similar to Tang and Tang [18], our results found that suppliers and customers are also negatively related to CEP, while community donation acting as window-dressing in CEP [29]. However, by employing the fs/QCA method, we found that the employee is in a core position to guarantee high CEP and that the investor is in a core position to guarantee a high firm value.

Lastly, our study also denotes that whether CEP enhances firm value depends on how these stakeholders work together. However, as stated above, prior studies mainly employed the linear fashion method. Against the backdrop, we also make a beneficial supplement by employing a non-linear method.

7. Conclusions and Limitations

This paper presents how multiple dimensions of stakeholders can act as a whole to influence corporate environmental strategy and, given certain pattern, what the related performance will be. Using a sample of 204 observations of listed corporations in Chinese pollution-intensive industries over the period of 2013–2014, we found that compared to a single dimension of stakeholders, the configurations are more likely to affect CEP, but there are no uniform combinations of stakeholders. Whether stakeholders lead to higher CEP depends on combinations of stakeholders, and among these patterns, the employee has a positive role, but the investor, supplier, customer, and community have negative roles, which can be seen as an amendment for traditional stakeholder classification.

Three patterns result in proactive and reactive environmental strategies. For high CEP, all three patterns are not able to lead to high firm value, but for both C2 and C3, ~community * (~supplier and customer + employee) will not erode firm value, thus providing us appropriate modes in the long run. For low CEP, C4 can lead to high firm value, and C5 would lower firm value. These results provide new evidence for the relationship between economic development and environmental protection that the investment relationship should be an appropriate combination with CEP for a win-win outcome.

As the largest emerging country, empirical evidence from China not only provides support for relatively fewer studies from the configurational perspective of stakeholders’ net power with respect to CEP and related consequences, but also has important policy implications for other countries where CSP is still in the initial stage and the traditional corporate government mode still has a leading position.

First, firms can adopt a proactive environmental strategy that does not necessarily erode firm value. In China or other emerging countries, CEP is still in its early stage, and firms are driven by administrative laws and regulations, thus leading to a passive environmental strategy; firms hesitate to implement CEP due to it resulting in a low firm value. Our results suggest that the effect of CEP depends on configurations of stakeholders, so firms should change their attitudes toward CEP for strategic use.

Second, whether a corporate environmental strategy enhances firm value depends on the configuration, but neither a single dimension, nor all dimensions can achieve this goal. During this process, better employee relations and low investment in the community, suppliers, and customers will be the best choice. More importantly, investor relations should be intensified because for CEP, the investor has relatively higher sufficiency and necessity scores compared to the community, suppliers, and customers, thus supporting this viewpoint that the investor can be incorporated into a proactive environmental strategy to enhance firm value.

Furthermore, although these two patterns cannot enhance firm value, it does not lower firm value. In view of the conditions that CSP is still in an early stage, along with economic development, stakeholders will be more strongly orientated towards CEP. Therefore, firms can conduct a proactive environmental strategy early by following the pattern of C2 and C3. During this process, firms can accumulate enough management experience compared to their followers. Finally, the forerunners will enjoy significant rewards.

This paper also has limitations. Our results are acquired from listed firms, so we should carefully expand these explanations to non-listed firms. In the next steps, we should collect more non-listed firms’ data to conduct an analysis. In addition, fs/QCA only supplies the elements in each configuration, and we have little knowledge about the optimal level of each element, which will be important work in the next step. Finally, we hope future studies can employ the recent database after eliminating the effect of market turbulence.

Author Contributions

Conceptualization, C.J. and Q.F.; data curation, Q.F.; formal analysis, C.J. and Q.F.; funding acquisition, C.J. and Q.F.; investigation, Q.F.; methodology, C.J. and Q.F.; project administration, C.J. and Q.F.; resources, Q.F.; software, Q.F.; supervision, C.J. and Q.F.; validation, Q.F.; visualization, Q.F.; writing, original draft, Q.F.; writing, review and editing, C.J. and Q.F.

Funding

This research was funded by The National Social Science Fund of China, Grant Number 15ZDC020, The APC was funded by The National Social Science Fund of China, Grant Number 15ZDC020.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of the data; in the writing of the manuscript; nor in the decision to publish the results.

References

- Cao, Y.-H.; You, J.-X.; Liu, H.-C. Optimal environmental regulation intensity of manufacturing technology innovation in view of pollution heterogeneity. Sustainability 2017, 9, 1240. [Google Scholar] [CrossRef]

- Trumpp, C.; Guenther, T. Too Little or too much? Exploring U-shaped Relationships between Corporate Environmental Performance and Corporate Financial Performance. Bus. Strategy Environ. 2017, 26, 49–68. [Google Scholar] [CrossRef]

- BP BP Statistical Review of World Energy 2017. Available online: https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html (accessed on 19 January 2019).

- Wang, R.; Wijen, F.; Heugens, P.P. Government’s green grip: Multifaceted state influence on corporate environmental actions in China. Strat. Mgmt. J. 2018, 39, 403–428. [Google Scholar] [CrossRef]

- Tang, P.; Yang, S.; Shen, J.; Fu, S. Does China’s low-carbon pilot programme really take off? Evidence from land transfer of energy-intensive industry. Energy Policy 2018, 114, 482–491. [Google Scholar] [CrossRef]

- Tang, P.; Yang, S.; Boehe, D. Ownership and Corporate Social Performance in China: Why geographic remoteness matters. J. Clean. Prod. 2018, 197, 1284–1295. [Google Scholar] [CrossRef]

- Jiang, Y.; Xue, X.; Xue, W. Proactive Corporate Environmental Responsibility and Financial Performance: Evidence from Chinese Energy Enterprises. Sustainability 2018, 10, 964. [Google Scholar] [CrossRef]

- Hu, Y.; Chen, S.; Shao, Y.; Gao, S. CSR and Firm Value: Evidence from China. Sustainability 2018, 10, 4597. [Google Scholar] [CrossRef]

- David, P.; O’Brien, J.P.; Yoshikawa, T.; Delios, A. Do Shareholders or Stakeholders Appropriate the Rents from Corporate Diversification? The Influence of Ownership Structure. Acad. Manag. J. 2010, 53, 636–654. [Google Scholar] [CrossRef]

- Inoue, Y.; Lee, S. Effects of different dimensions of corporate social responsibility on corporate financial performance in tourism-related industries. Tour. Manag. 2011, 32, 790–804. [Google Scholar] [CrossRef]

- Valero-Gil, J.; Rivera-Torres, P.; Garcés-Ayerbe, C. How Is Environmental Proactivity Accomplished? Drivers and Barriers in Firms’ Pro-Environmental Change Process. Sustainability 2017, 9, 1327. [Google Scholar] [CrossRef]

- Shaukat, A.; Qiu, Y.; Trojanowski, G. Board attributes, corporate social responsibility strategy, and corporate environmental and social performance. J. Bus. Ethics 2016, 135, 569–585. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I. Stakeholders’ power, corporate characteristics, and social and environmental disclosure: evidence from China. J. Clean. Prod. 2014, 64, 426–436. [Google Scholar] [CrossRef]

- Fijałkowska, J.; Zyznarska-Dworczak, B.; Garsztka, P. Corporate Social-Environmental Performance versus Financial Performance of Banks in Central and Eastern European Countries. Sustainability 2018, 10, 772. [Google Scholar] [CrossRef]

- Freeman, R.E. Managing for Stakeholders: Trade-offs or Value Creation. J. Bus. Ethics 2011, 96, 7–9. [Google Scholar] [CrossRef]

- Zheng, Q.Q.; Luo, Y.D.; Maksimov, V. Achieving legitimacy through corporate social responsibility: The case of emerging economy firms. J. World Bus. 2015, 50, 389–403. [Google Scholar] [CrossRef]

- Afshar Jahanshahi, A.; Brem, A. Antecedents of Corporate Environmental Commitments: The Role of Customers. Int. J. Environ. Res. Pub. Health 2018, 15, 1191. [Google Scholar] [CrossRef] [PubMed]

- Tang, Z.; Tang, J. Stakeholder-firm power difference, stakeholders’ CSR orientation, and SMEs’ environmental performance in China. J. Bus. Venturing 2012, 27, 436–455. [Google Scholar] [CrossRef]

- Liu, N.; Tang, S.Y.; Lo, C.W.H.; Zhan, X.Y. Stakeholder demands and corporate environmental coping strategies in China. J. Environ. Manag. 2016, 165, 140–149. [Google Scholar] [CrossRef]

- Garcia-Castro, R.; Francoeur, C. When more is not better: Complementarities, costs and contingencies in stakeholder management. Strat. Mgmt. J. 2016, 37, 406–424. [Google Scholar] [CrossRef]

- Lassala, C.; Apetrei, A.; Sapena, J. Sustainability Matter and Financial Performance of Companies. Sustainability 2017, 9, 1498. [Google Scholar] [CrossRef]

- Lee, L.; Chen, L.F. Boosting employee retention through CSR: A configurational analysis. Corp. Soc. Resp. Environ. Manag. 2018, 25, 948–960. [Google Scholar] [CrossRef]

- Hexun CSR Report Rank of Listed Firms. Available online: http://stockdata.stock.hexun.com/zrbg/Plate.aspx?date=2013-12-31 (accessed on 19 January 2019).

- Misangyi, V.F.; Greckhamer, T.; Furnari, S.; Fiss, P.C.; Crilly, D.; Aguilera, R. Embracing Causal Complexity: The Emergence of a Neo-Configurational Perspective. J. Manag. 2017, 43, 255–282. [Google Scholar]

- Kim, H.; Park, K.; Ryu, D. Corporate Environmental Responsibility: A Legal Origins Perspective. J. Bus. Ethics 2017, 140, 381–402. [Google Scholar] [CrossRef]

- Meng, X.H.; Zeng, S.X.; Xie, X.M.; Qi, G.Y. The impact of product market competition on corporate environmental responsibility. Asia Pac. J. Manag. 2016, 33, 267–291. [Google Scholar] [CrossRef]

- Aragon-Correa, J.A.; Marcus, A.; Hurtado-Torres, N. The Natural Environmental Strategies of International Firms: Old Controversies and New Evidence on Performance and Disclosure. Acad. Manag. Perspect. 2016, 30, 24–39. [Google Scholar] [CrossRef]

- Ahsen, A.V. The Integration of Quality, Environmental and Health and Safety Management by Car Manufacturers—A Long-Term Empirical Study. Bus. Strateg. Environ. 2014, 23, 395–416. [Google Scholar] [CrossRef]

- Du, X.; Chang, Y.; Zeng, Q.; Du, Y.; Pei, H. Corporate environmental responsibility (CER) weakness, media coverage, and corporate philanthropy: Evidence from China. Asia. Pac. J. Manag. 2016, 33, 551–581. [Google Scholar] [CrossRef]

- Buysse, K.; Verbeke, A. Proactive environmental strategies: a stakeholder management perspective. Strat. Mgmt. J. 2003, 24, 453–470. [Google Scholar] [CrossRef]

- Popp, D.; Newell, R. Where does energy R&D come from? Examining crowding out from energy R&D. Energy Econ. 2012, 34, 980–991. [Google Scholar]

- Lee, M. The effect of environmental regulations: a restricted cost function for Korean manufacturing industries. Environ. Dev. Econ. 2007, 12, 91–104. [Google Scholar] [CrossRef]

- Porter, M.E.; van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Testa, F.; Iraldo, F.; Frey, M. The effect of environmental regulation on firms’ competitive performance: The case of the building & construction sector in some EU regions. J. Environ. Manag. 2011, 92, 2136–2144. [Google Scholar]

- Zhao, X.; Sun, B. The influence of Chinese environmental regulation on corporation innovation and competitiveness. J. Clean. Prod. 2016, 112, 1528–1536. [Google Scholar] [CrossRef]

- Sen, S. Corporate governance, environmental regulations, and technological change. Europ. Econ. Reviron. 2015, 80, 36–61. [Google Scholar] [CrossRef]

- Lankoski, L. Corporate responsibility activities and economic performance: A theory of why and how they are connected. Bus. Strateg. Environ. 2008, 17, 536–547. [Google Scholar] [CrossRef]

- Dixon-Fowler, H.R.; Slater, D.J.; Johnson, J.L.; Ellstrand, A.E.; Romi, A.M. Beyond “Does it Pay to be Green?” A Meta-Analysis of Moderators of the CEP-CFP Relationship. J. Bus. Ethics 2013, 112, 353–366. [Google Scholar] [CrossRef]

- Singh, P.J.; Sethuraman, K.; Lam, J.Y. Impact of Corporate Social Responsibility Dimensions on Firm Value: Some Evidence from Hong Kong and China. Sustainability 2017, 9, 1532. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horizons 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Ni, N.; Egri, C.; Lo, C.; Lin, Y.Y. Patterns of Corporate Responsibility Practices for High Financial Performance: Evidence from Three Chinese Societies. J. Bus. Ethics 2015, 126, 169–183. [Google Scholar] [CrossRef]

- Orlitzky, M.; Louche, C.; Gond, J.-P.; Chapple, W. Unpacking the Drivers of Corporate Social Performance: A Multilevel, Multistakeholder, and Multimethod Analysis. J. Bus. Ethics 2017, 144, 21–40. [Google Scholar] [CrossRef]

- Kacperczyk, A. With greater power comes greater responsibility? Takeover protection and corporate attention to stakeholders. Strat. Mgmt. J. 2009, 30, 261–285. [Google Scholar] [CrossRef]

- Clarkson, M.B.E. A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Eesley, C.; Lenox, M.J. Firm responses to secondary stakeholder action. Strat. Mgmt. J. 2006, 27, 765–781. [Google Scholar] [CrossRef]

- Li, W.; Zhang, R. Corporate Social Responsibility, Ownership Structure, and Political Interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Xu, E.; Yang, H.; Quan, J.M.; Lu, Y. Organizational slack and corporate social performance: Empirical evidence from China’s public firms. Asia. Pac. J. Manag. 2015, 32, 181–198. [Google Scholar] [CrossRef]

- Jensen, M.C. Value Maximization, Stakeholder Theory, and the Corporate Objective Function. J. Appl. Corp. Financ. 2010, 22, 32–42. [Google Scholar] [CrossRef]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strat. Mgmt. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Liu, X.; Anbumozhi, V. Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 2009, 17, 593–600. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. The Causal Effect of Corporate Governance on Corporate Social Responsibility. J. Bus. Ethics 2012, 106, 53–72. [Google Scholar] [CrossRef]

- Murillo-Luna, J.L.; Garcés-Ayerbe, C.; Rivera-Torres, P. Why do patterns of environmental response differ? A stakeholders’ pressure approach. Strat. Mgmt. J. 2008, 29, 1225–1240. [Google Scholar] [CrossRef]

- Xu, Y. Understanding CSR from the perspective of Chinese diners: the case of McDonald’s. Int. J. Contemp. Hosp. Manag. 2014, 26, 1002–1020. [Google Scholar] [CrossRef]

- Liu, W.; Wei, Q.; Huang, S.-Q.; Tsai, S.-B. Doing Good Again? A Multilevel Institutional Perspective on Corporate Environmental Responsibility and Philanthropic Strategy. Int. J. Environ. Res. Pub. Health 2017, 14, 1283. [Google Scholar] [CrossRef] [PubMed]

- Kong, D.; Liu, S.; Dai, Y. Environmental Policy, Company Environment Protection, and Stock Market Performance: Evidence from China. Corp. Soc. Resp. Environ. Manag. 2014, 21, 100–112. [Google Scholar] [CrossRef]

- Hexun Hexun CSP Evaluation System. Available online: http://stock.hexun.com/2013/gsshzr/index.html (accessed on 19 January 2019).

- Xiong, B.; Lu, W.; Skitmore, M.; Chau, K.W.; Ye, M. Virtuous nexus between corporate social performance and financial performance: a study of construction enterprises in China. J. Clean. Prod. 2016, 129, 223–233. [Google Scholar] [CrossRef]

- Li, D.Y.; Xin, L.N.; Chen, X.H.; Ren, S.G. Corporate social responsibility, media attention and firm value: Empirical research on Chinese manufacturing firms. Qual. Quant. 2017, 51, 1563–1577. [Google Scholar] [CrossRef]

- Fiss, P.C. Building better causal theories: A fuzzy set approach to typologies in organization research. Acad. Manag. J. 2011, 54, 393–420. [Google Scholar] [CrossRef]

- Longest, K.C.; Vaisey, S. Fuzzy: A Program for Performing Qualitative Comparative Analyses (QCA) in Stata. Stat. J. 2008, 8, 79–104. [Google Scholar] [CrossRef]

- Sharma, S.; Vredenburg, H. Proactive corporate environmental strategy and the development of competitively valuable organizational capabilities. Strat. Mgmt. J. 1998, 19, 729–753. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate Social Responsibility Reporting in China: Symbol or Substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Theoretical framework. CEP, corporate environmental performance.

{kind=link}

Table 1.

Sample distribution and variable description statistics. CSP, Corporate Social Performance.

Table 1.

Sample distribution and variable description statistics. CSP, Corporate Social Performance.

| Industry Type | Frequency | Variable Name | Definitions | Mean | Std. |

|---|---|---|---|---|---|

| Mining | 21 | Investor | Hexun CSP Evaluation system | 14.597 | 4.018 |

| Food and beverages | 23 | Employee | 9.339 | 2.374 | |

| Textiles, garments, and leather | 17 | Supplier and customer | 15.289 | 2.887 | |

| Paper mills and printing | 10 | Environment | 15.684 | 3.964 | |

| Petroleum, chemistry, and plastics | 38 | Community | 8.007 | 4.487 | |

| Metal and non-metal materials | 43 | Tobin’s Q | Market value/book value | 1.733 | 1.425 |

| Medicine and bio-products | 27 | ||||

| Electricity, gas, and water, production and supply | 25 | ||||

| Total | 204 | ||||

Note: The first two columns list a sample distribution based on industry, and the last three columns demonstrate the definitions and basic description statistics.

Table 2.

Fuzzy sets’ calibration.

| Variable | Calibration | Member Value | Variable | Calibration | Member Value |

|---|---|---|---|---|---|

| Investor | Minimum threshold | 11.835 | Environment | Minimum threshold | 12.500 |

| Crossover point | 14.535 | Crossover point | 17.000 | ||

| Maximum threshold | 18.010 | Maximum threshold | 19.500 | ||

| Employee | Minimum threshold | 7.240 | Community | Minimum threshold | 4.545 |

| Crossover point | 9.095 | Crossover point | 6.500 | ||

| Maximum threshold | 11.255 | Maximum threshold | 12.040 | ||

| Supplier and Customer | Minimum threshold | 12.000 | Tobin’s Q | Minimum threshold | 0.782 |

| Crossover point | 15.000 | Crossover point | 1.322 | ||

| Maximum threshold | 18.000 | Maximum threshold | 2.269 |

Note: The definitions of variables can be observed in Table 1. The minimum threshold, crossover point, and maximum threshold are the 25th, 50th, and 75th percentiles, respectively.

Table 3.

Sufficiency and necessity matrix for a proactive environmental strategy.

| Environment | Investor | Employee | Supplier and Customer | Community | |

|---|---|---|---|---|---|

| Environment | 1.000 | 0.473 | 0.828 | 0.350 | 0.325 |

| Investor | 0.404 | 1.000 | 0.484 | 0.675 | 0.601 |

| Employee | 0.702 | 0.480 | 1.000 | 0.341 | 0.328 |

| Supplier and Customer | 0.288 | 0.649 | 0.330 | 1.000 | 0.768 |

| Community | 0.286 | 0.619 | 0.340 | 0.823 | 1.000 |

Note: The definitions of variables can be observed in Table 1. The necessity scores are displayed in the upper right corner, and the sufficiency scores are in the lower left corner.

Table 4.

Patterns for high CEP and related consequences.

| Configurations | Effects on Tobin’s Q | |||||

|---|---|---|---|---|---|---|

| C1 | C2 | C3 | High Tobin’s Q | Low Tobin’s Q | ||

| Investor | ⊗ | Pattern | Consistency | Consistency | ||

| Employee | ● | ● | ||||

| Supplier and Customer | ⊗ | ⊗ | ||||

| Community | ⊗ | ⊗ | C1 | 0.374 | 0.790 | |

| Consistency | 0.787 | 0.780 | 0.778 | |||

| Raw Coverage | 0.488 | 0.702 | 0.709 | C2 | 0.482 | 0.659 |

| Unique Coverage | 0.033 | 0.060 | 0.067 | |||

| Solution Consistency | 0.725 | C3 | 0.504 | 0.631 | ||

| Total Coverage | 0.803 | |||||

Note: The first four columns list related patterns for proactive environmental strategy, and the last three columns are the related consequences corresponding to high and low Tobin’s Q. The definitions of variables can be observed in Table 1. ● indicates the presence of a condition; ⊗ indicates the absence of a condition; while the blank space indicates “does not matter for the outcome”.

Table 5.

Sufficiency and necessity matrix for a reactive environmental strategy.

| Environment | Investor | Employee | Supplier and Customer | Community | |

|---|---|---|---|---|---|

| Environment | 1.000 | 0.609 | 0.377 | 0.745 | 0.716 |

| Investor | 0.686 | 1.000 | 0.484 | 0.675 | 0.601 |

| Employee | 0.421 | 0.480 | 1.000 | 0.341 | 0.328 |

| Supplier and Customer | 0.807 | 0.649 | 0.330 | 1.000 | 0.768 |

| Community | 0.831 | 0.619 | 0.340 | 0.823 | 1.000 |

Note: Definitions of variables can be seen in Table 1. The necessity scores are displayed in the upper right corner and the sufficiency scores are in the lower left corner.

Table 6.

Patterns for low CEP and related consequences.

| Configurations | Effects on Tobin’s Q | |||||

|---|---|---|---|---|---|---|

| C4 | C5 | C6 | High Tobin’s Q | Low Tobin’s Q | ||

| Investor | ● | Pattern | Consistency | Consistency | ||

| Employee | ⊗ | ⊗ | ||||

| Supplier and Customer | ● | ● | ||||

| Community | ● | ● | C4 | 0.819 | 0.590 | |

| Consistency | 0.888 | 0.916 | 0.891 | |||

| Raw Coverage | 0.418 | 0.604 | 0.648 | C5 | 0.545 | 0.773 |

| Unique Coverage | 0.027 | 0.048 | 0.092 | |||

| Solution Consistency | 0.860 | C6 | 0.686 | 0.680 | ||

| Total Coverage | 0.722 | |||||

Note: The first four columns list related patterns for a reactive environmental strategy, and the last three columns are related consequences corresponding to high and low Tobin’s Q. The definitions of variables can be seen in Table 1. ● indicates the presence of condition; ⊗ indicates the absence of condition; while blank space indicates “does not matter for the outcome”.

Table 7.

Patterns for high CEP from 2010–2012.

| C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | |

|---|---|---|---|---|---|---|---|---|

| Investor | ● | ⊗ | ⊗ | ● | ||||

| Employee | ● | ● | ● | ● | ● | ● | ||

| Supplier and Customer | ⊗ | ⊗ | ⊗ | ⊗ | ⊗ | |||

| Community | ⊗ | ⊗ | ⊗ | ⊗ | ⊗ | |||

| Consistency | 0.865 | 0.842 | 0.792 | 0.779 | 0.759 | 0.780 | 0.787 | 0.787 |

| Raw Coverage | 0.271 | 0.536 | 0.499 | 0.322 | 0.523 | 0.333 | 0.279 | 0.600 |

| Unique Coverage | 0.061 | 0.138 | 0.101 | 0.051 | 0.253 | 0.020 | 0.049 | 0.164 |

| Consistency_ High Tobin’s Q | 0.632 | 0.438 | 0.493 | 0.404 | 0.441 | 0.433 | 0.707 | 0.458 |

| Consistency_ Low Tobin’s Q | 0.604 | 0.717 | 0.675 | 0.843 | 0.719 | 0.794 | 0.575 | 0.707 |

| Solution Consistency | 0.794 | 0.753 | 0.750 | |||||

| Total Coverage | 0.697 | 0.574 | 0.668 | |||||

Note: The patterns from C7–C9 are for 2010; the patterns of C10 and C11 are for 2011; and the last three are for 2012. Consistency_ High Tobin’s Q signifies the related value for a high Tobin’s Q, which is the same as the second to last column in both Table 4 and Table 6, while consistency_ Low Tobin’s Q also follows this explanation. The definitions of variables can be observed in Table 1. ● indicates the presence of a condition; ⊗ indicates the absence of a condition; while a blank space indicates “does not matter for the outcome”.

Table 8.

Patterns for low CEP from 2010–2012.

| C15 | C16 | C17 | C18 | C19 | C20 | C21 | |

|---|---|---|---|---|---|---|---|

| Investor | ● | ● | ● | ● | |||

| Employee | ⊗ | ⊗ | ⊗ | ⊗ | ⊗ | ⊗ | ⊗ |

| Supplier and Customer | ● | ● | ● | ● | |||

| Community | ● | ● | ● | ● | |||

| Consistency | 0.855 | 0.853 | 0.807 | 0.803 | 0.795 | 0.829 | 0.801 |

| Raw Coverage | 0.322 | 0.576 | 0.329 | 0.525 | 0.413 | 0.383 | 0.385 |

| Unique Coverage | 0.052 | 0.306 | 0.067 | 0.263 | 0.097 | 0.067 | 0.070 |

| Consistency_ High Tobin’s Q | 0.815 | 0.734 | 0.807 | 0.631 | 0.702 | 0.855 | 0.842 |

| Consistency_ Low Tobin’s Q | 0.528 | 0.582 | 0.543 | 0.667 | 0.525 | 0.456 | 0.452 |

| Solution Consistency | 0.844 | 0.784 | 0.766 | ||||

| Total Coverage | 0.628 | 0.592 | 0.550 | ||||

Note: The patterns of C15 and C16 are for 2010; the patterns of C17 and C18 are for 2011; and the last three are for 2012. Consistency_ High Tobin’s Q signifies the related value for a high Tobin’s Q, which is the same as the second to last column in Table 4 and Table 6, while consistency_ Low Tobin’s Q also follows this explanation. The definitions of variables can be observed in Table 1. ● indicates the presence of a condition; ⊗ indicates the absence of a condition; while a blank space indicates “does not matter for the outcome”.

Table 9.

Cluster analysis results.

| Mean of Final Cluster Centre | Two-Sample t-Test | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| C22 | C23 | C24 | C25 | C22 | C23 | C24 | C25 | ||

| Investor | 0.911 | 0.096 | 0.165 | 0.893 | C22 | 0.000 | −0.602 a | −0.020 | −0.643 a |

| Employee | 0.167 | 0.808 | 0.143 | 0.858 | C23 | 0.602 a | 0.000 | 0.581 a | −0.042 |

| Supplier and Customer | 0.871 | 0.168 | 0.912 | 0.248 | C24 | 0.020 | −0.581 a | 0.000 | −0.623 a |

| Community | 0.821 | 0.194 | 0.838 | 0.165 | C25 | 0.643 a | 0.042 | 0.623 a | 0.000 |

Note: The first five columns list the mean of the final cluster center based on standardized variables, and the last five columns provide a two-sample t-test on the standardized CEP. For example, −0.602 a shows that a standardized CEP of pattern C22 minus that of C23 equals −0.602, and the superscript denotes that this value is statistically significant at the 5% level.

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Jiang, C.; Fu, Q. A Win-Win Outcome between Corporate Environmental Performance and Corporate Value: From the Perspective of Stakeholders. Sustainability 2019, 11, 921. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030921

AMA Style

Jiang C, Fu Q. A Win-Win Outcome between Corporate Environmental Performance and Corporate Value: From the Perspective of Stakeholders. Sustainability. 2019; 11(3):921. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030921

Chicago/Turabian StyleJiang, Chun, and Qiang Fu. 2019. "A Win-Win Outcome between Corporate Environmental Performance and Corporate Value: From the Perspective of Stakeholders" Sustainability 11, no. 3: 921. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030921

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.