1. Introduction

The alarming increase of the consequences of climate change around the world has transformed sustainable growth conditions into a strategic issue for any type of human activity that is unfolding [

1]. The economic field is not an exception, as significant measures for reducing pollution are expected from the business community. In the past decades, it has been globally accepted that the rapid growth of economies has engendered enormous costs of environmental degradation. The ecological damage caused by the global economy is at an unprecedented point, and the efforts to control the damage are at the implementation stage. There is a large number of international agreements and regulations [

2,

3,

4,

5,

6] that attempt to limit the unfavourable impact of companies on the environment, but plenty of work still needs to be done in order to reach a green economy. Although the guidelines for sustainable development are globally widespread, different regions of the world have implemented this concept in their own particular way. The European Union (EU) has assumed the ambitious sustainable development goals (SDG), being fully committed to becoming a global leader in implementing the 2030 Agenda [

6]. Within the Commission priorities, “The European Green Deal” for a climate-neutral economy represents a challenging and critical point to be implemented at the Member States level. Considered as “a road map for making the EU’s economy sustainable” [

7], this green engagement “resets the Commission’s commitment to tackling climate and environmental-related challenges” at the core of its policies ([

8], p. 1). A similar interest in achieving sustainable green growth has also been embraced by the countries within the European Economic Area (EEA), namely, Iceland, Liechtenstein, and Norway [

9]. Together with the EU Member States, these countries have signed up for economic development without compromising the environment. The priority of green investment and the circular economy has been reinforced in all the European regions in the context of the unprecedented pandemic crisis that Europe is currently facing.

With the importance of a clean environment widely accepted, the ecological behaviour of companies has become an important issue for the stakeholders, as well as at the academic level. The increasing demand for responsible, reasonable and green conduct of the companies has deeply transformed the business process, modelling “the current ESG management practices” (see [

10], p. 854) and strengthening the connection between the environmental actions and the financial outputs. “Going green” has become an important issue in contemporary business practice [

11] and a strategic perspective to respond to the pressure of multiple stakeholders’ groups [

12]. In order to achieve competitive advantage and financial benefits, the companies have adopted the stakeholder theory. As a result, they have integrated the concepts capable of meeting the expectations of both internal and external stakeholders into their business system [

13]. Corporate social responsibility (CSR) and environment social governance (ESG) are concepts used to express the overall engagement of a company to the stakeholders’ concerns and to assess the impact of sustainable practices on corporate performance.

In the past decades, the scholars have focused their attention on the relationship between the environmental performance (EP) and the financial performance (FP) of a company, but the results were not conclusive. Following the stakeholder theory, the main body of the literature reveals a positive association between the environmental performance and the financial performance of a company [

14]. The efficient use of natural resources and pollution reduction stands for an effective environmental policy [

15] that improves the profitability of the company [

16]. At the same time, there are scholars that found a negative association between EP–FP variables [

17]. Such studies do not support the stakeholder theory, showing that environmental investments diminish corporate performance. The efforts made to understand the environmental–financial performance relationship are considerable and move the research boundary forward by exploring its implication and determinants from various perspectives. An important research perspective for this paper is based on the distinction made by the previous scholars in assessing environmental performance both through partial metrics (such as carbon emissions, pollution reduction) and global metrics (appreciated by general scores or ranks). The relevance of this viewpoint for the present study relies on the fact that “one of the reasons for the inconclusive results is the different selections of environmental performance indicators” ([

14], p. 1943). Some scholars choose to express EP through a single, explicit dimension of the ecological policy of a company. For example, [

18] explored the impact of carbon emission reduction on the financial and operational performance of a sample of international companies. At the same time, other scholars have used more complex tools to reflect EP, particularly, the qualitative scores provided by comprehensive databases. This is the case for [

19], who analysed the relationship between EP and FP using data on environmental scores published by the ASSET4 database (by Thomson Reuters) for Australian companies. Providing a broader perspective on a company’s environmental behaviour, these metrics are a better criterion for assessing its performance and associated risks. The findings are still inconclusive. However, most of the evidence shows a positive connection between both partial EP–FP [

18,

20,

21,

22] and global EP–FP [

19,

23].

The latest research [

24,

25,

26] suggests that environmental performance, as part of the environment social governance (ESG) score, has a complex nature, with both material and immaterial components that vary between companies and industries, and this may be an additional reason for the mixed association. At the same time, due to this material ability to impact the financial performance of a company, the stakeholders have increased the relevance and usefulness given to the environmental and social issues in the context of their decision-making process. Further, the new approach supports the stakeholder theory and concludes that the positive or negative links among EP–FP variables are in connection with the capacity of a company to create value.

The paper goes beyond all these arguments, makes a new supposition, and brings an important empirical contribution. The stakeholder theory suggests there is a connection between ecological expectations and the sustainable success of a company. However, as previously seen, there is a gap in the specialised literature as the stakeholder theory is not always validated by studies in practice. The question of whether stakeholders are constantly concerned with the environmental issues, no matter the financial performance, arises. This topic is to be tackled by our survey. Our assumption is that the stakeholders are not so concerned with environmental issues when companies get negative returns as they are when the companies get positive returns.

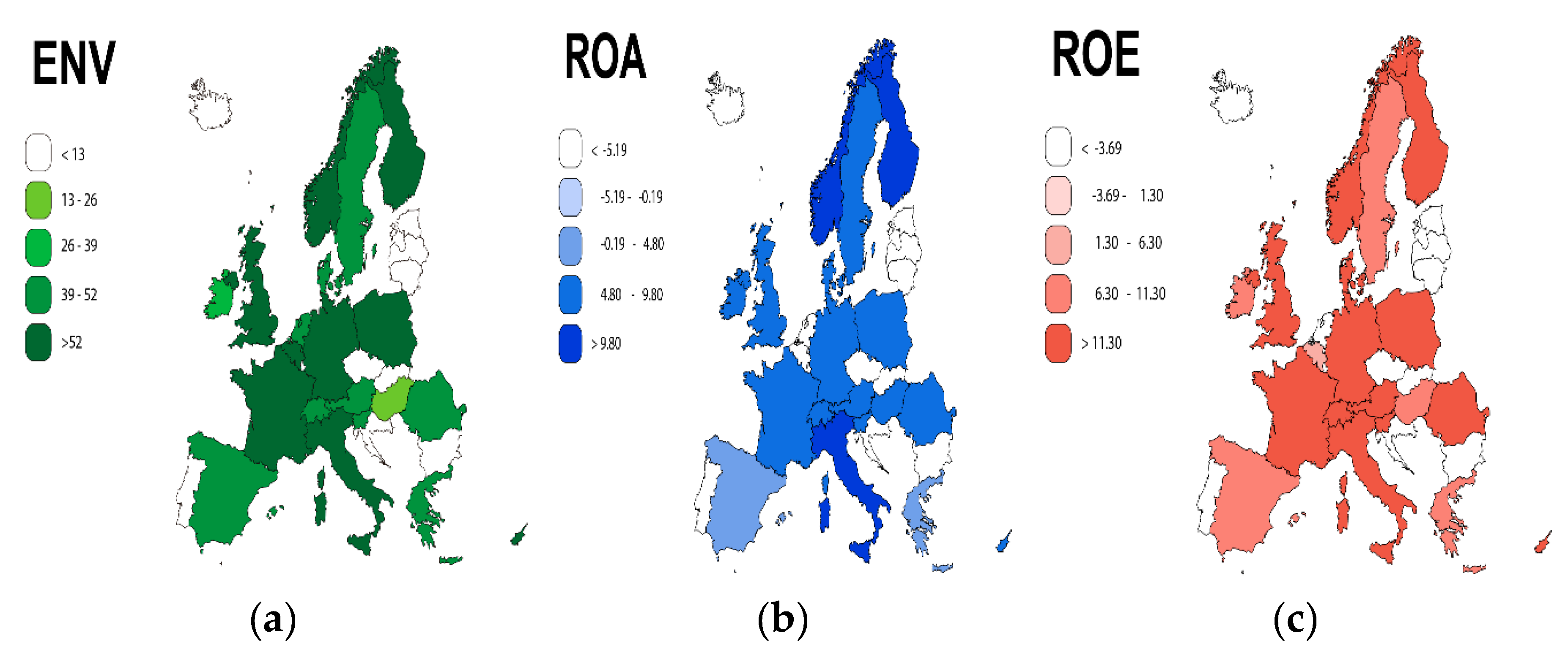

Unlike the previous research that is focused on the assessment of nonfinancial metrics as ESG factors, this particular piece of research is focused on a deeper judgment of the financial performance scenario, engendering a difference between periods of time with positive returns and the periods with negative returns. Using the return on assets (ROA) and return on equity (ROE) scores provided by the Refinitiv Eikon database, as well as the environmental pillar score (ENV) as a robust measure “based on materiality, data availability and industry relevance” ([

27], p. 1), the research aims to find out whether the stakeholders value environmental performance with the same relevance along different profitability scenarios. The paper considers the stakeholder theory in a complementary approach and seeks to integrate into the EP–FP relationship the dynamics of the stakeholders’ decision-making process. The possibility of different profitability scenarios affecting stakeholder decision-making has not been considered before.

The usefulness of the environmental performance of a company within the decision process will be assessed through the association capacity among EP–FP variables. The empirical analysis is based on Pearson’s correlation and linear regression techniques used to examine the hypothesised relationships, namely, environmental performance is associated with both positive and negative returns (ROA and ROE). The paper is based on a sample of 299 EEA companies operating in two activity sectors, namely, the extractives and minerals processing sector and the healthcare sector. The data sampled were collected from the Refinitiv database for the period 2009–2018.

As far as we know, this is the first research that assesses the environmental performance of a company within such different scenarios of financial returns. Our findings bring important scientific insights about this complex association at the level of companies from two relevant activity sectors in terms of environmental dependency. Company management and policy-makers would like to know if the stakeholders appreciate ecological behaviour regardless of the company reporting profit or loss. The paper provides valuable knowledge on environmental management policy design and provides scholars with a different point of view on the EP–FP relationship. The main limitation of the paper is generated by the applied research techniques. A future direction of research refers to a methodological approach through more advanced techniques.

The paper is structured as follows: after the introduction (

Section 1), the literature review and hypotheses development (

Section 2) and the materials and research methods are presented (

Section 3).

Section 4 contains the empirical results and the main observations and discussions.

Section 5 outlines the conclusions of the research.

2. Literature Review and Hypotheses Development

In the past decades, an impressive body of empirical evidence has been dedicated to the relationship between the environmental performance (EP) and the financial performance (FP) of companies. As the public and private concerns about climate change have increased, scholars have focused their attention on the issue of companies’ ecological impact reduction and its association with core business goals.

The environmental performance of a company is only part of much larger sustainability metrics, such as ESG or CSR, but it has consistently gained attention and utility in the decision-making process. The stakeholders have recognised the importance of environmental and social behaviour of a company by including these issues into their decision process. For this purpose, they require “proper information for analysing the corporate behaviours from various perspectives” ([

28], p. 1). In order to assess the performance and the risk associated with the company’s activity, investors, as an important part of the stakeholder category, “take more factors into consideration in their investment decisions than only financial accounting returns” ([

29], p. 3). This behaviour has gained ground in the past decades and increased the pressure on the companies to work in the interest of all socioeconomic parts while maximising their profits. This is the basic principle of the stakeholder theory, which “has emerged as the dominant paradigm in CSR discussions” ([

13], p. 3) and later, in the ESG framework. According to Freeman’s opinion, the stakeholders are any category of individuals that can affect and are affected by the achievement of a company’s objectives [

30]. These internal (owners, employees) and external individuals (investors, customers, suppliers, community, government) have different interests related to the operating activity of a company. Nevertheless, if their “demands affect firms’ conduct, they should also relate to their economic performance” ([

31], p. 1). Based on this framework, environmental policy has become a key issue of the management area of a company. A change in companies’ strategies has occurred, as the firms do not only pay attention to stakeholders’ demands, but they also make environmental issues a part of their strategy [

32].

The EU principle “an economy must work for the people and the planet” lies in line with the stakeholder theory ([

33], p. 2). By having at the core of its strategies the goal of sustainable development, the European Commission has already taken important steps for increasing the transparency of nonfinancial and diversity information [

34] and for protecting investor interest [

35,

36]. The EU Member States are frontier settlers in adopting regulations regarding the disclosure of information on environmental matters, employees, human right and social matters, as a condition for a sustainable economy. With specific reference to environment protection and a green economy, the EU has assumed ambitious targets [

4,

5,

6,

7,

33]. The other countries of the EEA, namely, Iceland, Liechtenstein, and Norway [

9] share the same vision. The companies from the EEA Member States are encouraged to adopt environmentally sustainable strategies in order to reduce their negative impact and to increase their operational performance.

Despite the growing importance, the environment issue remains a provocative and complex framework, especially in association with financial performance indicators. The literature is largely fragmented, offering mixed findings regarding the relationship between EP and FP variables.

Ramanathan studied the EP–FP relationship and found that the evidence in this field is inconclusive since some studies showed a positive link between the two variables, others showed a negative link, while some found no link [

37]. However, Orlitzky et al. disagreed with this opinion. So, using the meta-analysis method within their study, they found a positive correlation between corporate social performance and financial performance, as well a bidirectional and simultaneous relationship between them [

38].

On a sample of Chinese listed companies from heavily polluting industries, studied from 2009 to 2014, [

14] analysed the relationship of EP–FP. They concluded that there is a positive relationship between EP and FP, expressed by the authors as a win–win relationship. Mathematically, a concave-down quadratic function links the two variables. However, in 2010, the regulations on environmental disclosure became stricter in China, forcing the companies to invest more money in reducing pollution. As a consequence of these extra costs, the financial performance decreased, which further led to a weaker link between EP and FP.

The link between environmental and economic performance, according to [

31]’s research, can be determined by the stakeholders’ demands on the integration of the principle of sustainability in corporate management. Based on the instrumental value of stakeholder theory, [

39] found a negative impact of country-level sustainability performance on financial performance. The authors argued that, in the case of a country with good social and environmental performance, the stakeholders take for granted the improvements in the field [

39].

Pizzi analysed the relationship between CSR and the financial–economic performance of 118 Italian companies listed on the Milan Stock Exchange. He concluded that the companies with nonfinancial reporting have higher performance, seen as from dividends paid to shareholders. Additionally, the higher the environment risk, the lower the financial performance. He also compared the negative effects due to the environmental risk with the positive effects of nonfinancial reporting, and the results obtained showed that the former are higher than the latter [

40]. Similar results were obtained by [

41]. Using the questionnaire method, they stressed that Romanian companies pay attention to CSR, motivated by the competitive environment, and that CSR is strongly connected with the companies’ performance, both financial and nonfinancial [

41]. The survey method was also used by [

42] in exploring the pressure of external stakeholders on environmental performance. Relying on the stakeholder theory, their findings demonstrated that different human resource management (HRM) practices are mediating the relationship between stakeholders’ pressure and environmental performance.

One of the main reasons that “the EP–FP relationship is inconclusive globally, is the different selections of environmental performance indicators” ([

14], p. 1943). Therefore, during the process of reviewing the representative literature underlying this area, we highlighted the perspective of EP expression through a partial or global metric.

We refer to partial environmental performance as a measure that expresses a singular environment issue of the company, such as emissions/pollution reduction, good management of water, energy, resources or waste, environment information disclosure, or environmental regulation implementation. This represents a one-dimension environmental performance tool. An important number of studies have empirically analysed the impact of abovementioned issues of environmental performance on corporate financial performance [

18,

20,

21,

22,

43]. Background of these research findings can be established as two-way outputs: positive and negative relationships between EP and FP. The evidence of a positive relationship is numerically superior [

18,

20,

21,

22] to those of a negative association [

43], meaning that financial efforts of companies to invest in green technologies or green-actions are appreciated by the key stakeholders, and rewarded through higher financial performance. These conclusions are drawn back by the limited content of environmental measures to just one side of such a complex concept.

We refer to global environmental performance as a metric which has accumulated more than one practical issue in the field of study. On the whole, the most common measurement tools are expressed as a rank score obtained from a large number of theme-indicators or pillars developed by different databases (such as Thomson Reuters/Refinitiv, Morgan Stanley Capital International (MSCI), Vigeo or Bloomberg). The methodologies applied vary from one database to another, and, usually, the environment (E) metric is a part of larger sustainability indicators (ESG, CSR). The literature underpinnings comprising the relationship between multidimensional environmental performance and financial performance [

19,

23,

44] provide a broader perspective of this connection, but their conclusions are portrayed by the same mixed results regarding the direction way and strength of these associations. Thus, environmental performance that is measured by the score of environmental pillars of ESG, which encloses three dimensions, namely, emission reduction, product innovation and resource decline, positively influences the financial performance of companies around the world; this is more emphasised for developing countries than the developed ones [

23]. The same favourable relationship between EP and FP was obtained for the “prefinancial crises period (2001–2007)” of Australian companies ([

19], p. 324); for a long-term horizon, companies can benefit from their environmental strategies [

44].

The discussions remain largely fragmented while the gap between the academic world and practitioners seems to become deeper within the evolution of these measurement tools [

24]. At the same time, there is widespread pressure from investors on firms to disclose ESG information, as it is a criterion in their investment decision [

45]. Considered as total or individual scores, the environment, social and governance ratings have become an essential part of the decision process. They complete the performance–risk frame of a company through their capacity to financially impact operational activity. This capacity has evolved as materiality theory, and it varies from company to company and from industry to industry. There are “several databases that rate companies by their ESG scores” ([

29], p. 14) in conditions of materiality, and there is a large category of previous studies that have relied on such ESG levels for their findings. Based on these judgements and the access to Refinitiv data, we used the environmental pillar score (ENV) provided by the Refinitiv Eikon database in our research, as well as return on assets (ROA) and return on equity (ROE). Assumed as a relevant metric, ENV offers robustness and relevance to our scientific approach.

Regarding the measurement of financial performance, the specialised literature is more standardised. Traditionally, financial performance is expressed through accountant indicators (ROA, ROE) or market-based indicators (Tobin’s q, market capitalisation; see [

46], p. 343).

Following the stakeholder theory and the growing importance of environmental issues for stakeholders, this research starts from the premise that there is a connection between EP and FP of a company. However, the inconclusive results regarding this type of association reveal the gap in the literature and highlight the fact that not all key factors of the EP–FP relationship have been studied so far [

29]. Based on these considerations, the objective of the research is to assess whether stakeholders are constantly concerned about environmental issues regardless of financial performance.

This study intends to make one step forward from the classical relationship between environmental–financial performance and to take a deeper look at the accounting financial returns of a company as one of the main pillars of the economic decision process. The empirical assumption of the research starts from the point where a company does not generate profitability and becomes a loss-making entity. Consequently, the questions are whether the stakeholders value the environmental performance of the company during the periods of time with negative returns as they value it during the profitable periods.

The following sets of hypotheses were formulated:

The first set:

HA0 Environmental performance is significantly associated with accounting returns, expressed in positive values (positive ROA and ROE)

HA1 Environmental performance is not significantly associated with accounting returns, expressed in positive values (positive ROA and ROE)

The second set:

HB0 Environmental performance is significantly associated with accounting returns, expressed in negative values (negative ROA and ROE)

HB1 Environmental performance is not significantly associated with accounting returns, expressed in negative values (negative ROA and ROE)

In order to assess the decisional usefulness of environmental performance, we have split the accounting indicators ROA and ROE into two categories, namely, positive returns and negative returns. If the stakeholders take environmental performance into account, both in terms of profitability and loss, it is expected that the causal association among EP–FP variables will be statistically relevant.

Furthermore, if the findings support a significant association between variables, the secondary purpose of the research is to investigate the prediction scale, in which the evolution of environmental performance (as an independent variable) can explain the total variation in the company’s returns (as a dependency variable).

To fulfil the research purposes, we have selected two activity sectors that are recommended by the Sustainability Accounting Standards Board (SASB) as being at the top and middle of the materiality capacity in connection with environmental issues. The two activity sectors are (1) extractives and minerals processing, placed at the top of the list regarding the materiality capacity of environmental issues to impact financial performance, and (2) healthcare, situated in the middle area of the same list [

47].

To the best of our knowledge, this is the first research to analyse the link between environmental behaviour and a company’s accounting returns, taken into consideration as both positive and negative values. During the operational cycles of a company, these financial results are the basic point of any decisional process. The introduction of sustainable growth into the judgment criteria of stakeholders has made necessary a multisize estimation of the company’s performance. Therefore, does environmental protection remain constant in the company’s valuation equation, whether it has a positive or negative return? To proper investigate this academic and practical question, we have used the relevant data samples and robust econometrical techniques described below.

4. Results and Discussion

In order to verify the hypotheses and to obtain solid evidence for the research objective (if the stakeholders keep their interest in the environmental issues, regardless the company’s financial returns), we applied the research methodology. Therefore, we performed Pearson’s correlation test and linear regression analysis separately for each business sector and for the two profitability scenarios, namely, positive accounting returns (positive ROA, ROE) and negative accounting returns (negative ROA, ROE), respectively. The main findings are presented in the following paragraphs.

4.1. The Association between Environmental Performance and Accounting Financial Returns at the Extractives and Minerals Processing Companies’ Level

The aggregated environmental pillar score (ENV), provided by the Refinitiv database, is assumed to be connected with the financial performance of the companies operating in the extractives and minerals processing sector (H

A0 and H

B0). This assumption relies on the dependence of this activity sector on natural resources and is meant to offer robustness to the environmental dimension within the stakeholder’s decisional process. The decision-making relevance is pursued in a comparative manner between the periods with positive returns (

Table 2) and periods with negative returns (

Table 3).

Pearson’s correlation coefficients (r) indicate the presence of a moderate association capacity between ENV and both ROA (r = −0.357) and ROE (r = −0.260). The values of the significance tests (Sig.), situated well below the acceptance threshold (p. Sig. < 0.05), validate the linear links between environmental performance (ENV) and positive returns (ROA and ROE) in the case of extractives and minerals processing companies, meaning that the ecological behaviour of these companies is important within the decisional process.

According to linear regression outputs (

Table 2), ENV has a negative influence on both ROA (−0.015) and ROE (−0.032) considered during the period of time with positive returns. The findings support that 12.8% of ROA variation can be explained through environmental performance evolution, while in the case of ROE, only 6.8% of its variation can be attributed to the ENV evolution. Statistically relevant at

p < 0.05, these influences suggest that achieving a superior level of environmental performance puts pressure on the financial results of a company, causing a decrease in ROA and ROE levels. These results are opposite to those achieved by other researchers, as revealed by literature underpinnings [

19,

23,

24].

The linear regression equations are

In conclusion, there is a statistically relevant association between environmental performance and positive ROA and ROE, meaning that our hypothesis (Environmental performance is significantly associated with accounting returns expressed in positive values (positive ROA and ROE)) is validated in the case of the extractives and minerals processing activity sector. The environmental performance metrics, along with the positive returns of the companies, have been taken into consideration by the stakeholders from the analysed activity sector. This evidence marks the additional pressure that links environmentalists’ demands to corporate performance.

The main question of the research is whether the environmental performance of a company also matters in the case of negative returns. In order to validate this hypothesis, we selected for each company the time periods with negative values for ROA and ROE. Furthermore, we investigated the association between ENV and the negative values for ROA and ROE (

Table 3).

The findings summarised in

Table 3 also indicate a moderate capacity of association between the environmental performance of the extractives and minerals processing companies and their negative accounting returns. Pearson’s correlation coefficients (r) support the links between ENV and both negative ROA (r = 0.348) and ROE (r = 0.209) on a smaller scale than in the case of positive returns. The results of the regression technique point out that 12.1% of ROA (negative) variation can be explained by environmental performance variation (ENV) and a smaller percentage of 4.3% from ROE (negative) evolution can be explained through ENV variation. ENV has a positive influence on both the negative values of ROA (0.026) and ROE (0.030), which means that any increase in the environmental performance of companies generates an increase in financial expenses and then a strengthening of their negative returns.

The linear regression equations are

Based on all the above, hypothesis HB0 (Environmental performance is significantly associated with accounting returns expressed in negative values (negative ROA and ROE)) is fulfilled. The issues regarding environmental protection are being checked out by the stakeholders, even in the case of negative returns reported by the companies. Based on these findings, we can assert that the interest of stakeholders in ecological behaviour is maintained, no matter the financial performance reported. Nevertheless, the empirical assumption that the stakeholders may be less concerned about EP when companies get negative returns compared to periods with positive returns is supported by the lower level of r in the case of the negative scenario.

As a final remark, in the case of extractives and minerals processing companies from the EEA, we have noticed a better connection between ENV and ROA (both with positive and negative values), than between ENV and ROE (positive and negative). The higher level of association in the case of environmental performance and ROA can be explained through the fact that companies operating in the analysed sector are large companies with significant total asset values. All the decisions regarding the environmentally sustainable growth of these companies will be reflected in an increase in investments in their tangible asset level.

4.2. The Association between Environmental Performance and Accounting Financial Returns at the Healthcare Companies’ Level

The metrics that indicate the environmental behaviour of the companies active in the healthcare sector are outlined by SASB as having an average capacity to impact the operational activity of these corporations. Given the growing importance of green investment and sustainable growth in the European market, environmental performance can now become a decision-making point in almost all sectors of economic activity. We consider the assessment of the link between environmental performance and accounting returns (positive and negative) in the case of healthcare companies as a mandatory process for the purpose of collecting information on concerns for sustainable growth.

The research findings are summarised separately in the case of the association between ENV and positive returns (

Table 4) and between ENV and negative returns (

Table 5).

In the case of companies operating in the healthcare sector, statistical outputs (see

Table 4) suggest that there is no relevant association between environmental performance and positive ROA, while between ENV and ROE, the association capacity is quite low.

Pearson’s correlation coefficients (r) revealed a lack of linear correlation between ENV and ROA (r = 0.027, with a p-value of Sig. > 0.05) and a low, statistically significant, correlation between ENV and ROE (r = 0.178, with a p-value of Sig. < 0.05). Thus, we can assert that the hypothesis HA0 (Environmental performance is significantly associated with accounting returns expressed in positive values (positive ROA and ROE)) is partially validated in the case of healthcare companies.

Since the link between ROA and ENV is not statistically significant, we can write the linear regression equation only for the relationship between ROE and ENV as

During the periods with positive returns, the stakeholders are not too concerned about corporate environmental performance. The stakeholder theory is weakly supported by these results. There is no pressure on the management of healthcare companies to increase their ecological actions.

Table 5 presents the findings regarding the association capacity between ENV and negative returns (ROA, Model 3 and ROE, Model 4) in the case of healthcare companies from EEA Member States.

Regarding the time periods marked by negative returns reported by the healthcare companies, Pearson’s correlation coefficient (r) shows a moderate capacity of association only in the case of ENV and ROA (r = 0.249, with p-value for Sig. < 0.05). According to the deeper regression analysis, in the case of this pair of variables, 6.2% of the ROA total variation can be explained by the evolution of environmental performance (ENV). Regarding the ENV and ROE association, Pearson’s correlation coefficient indicates a null linear correlation (r = 0.051, with p-value for Sig. > 0.05).

Only the link between ROA and ENV is statistically significant. For this reason, we can write the linear regression equation only for this relationship:

Consequently, our research hypothesis HB0 (Environmental performance is significantly associated with accounting returns expressed in negative values (negative ROA and ROE)) is only partially validated. The observation made in the case of the positive returns scenario remains valid in the case of negative scenarios. The stakeholders are not very interested in the environmental performance of the companies. The attention paid to these issues remains constantly low, whether the company has reported a profit or a loss.

Based on all the observations made, in the case of healthcare companies, we can conclude that the ecological actions of these companies are rather weak benchmarks in the decision-making process of stakeholders.

5. Conclusions

A key step in the fight to reduce pollution and achieve sustainable growth for EEA companies can be seen as raising public expectations and pushing for high transparency in companies, especially those with a significant impact on natural resources. There is a widespread demand from stakeholders for qualitative data on a company’s ecological behaviour as part of the overall ESG score. In addition to financial performance, equally pursued by managers and shareholders, managers must take into account the interests of stakeholders, often divergent. One of these interests, the improvement of environmental behaviour, puts additional pressure on the company’s management. The paradox is that caring for the environment of shareholders is a means of harmonising the interests of the multitude of stakeholders, and the task of managers becomes easier. Therefore, CSR and ESG seem to be links between the interests of stakeholders and managers, and through their implementation, everyone wins. However, the scientific literature on the ability of such metrics to connect with financial indicators is still being debated, and more investigations are needed.

Based on these academic and practical considerations, the research approached, in an innovative and new light, the complex relationship between the environmental performance and the financial performance of a company (expressed through the accounting measures ROA and ROE). Within this framework, the paper brings the perspective of analysing the association of EP–FP variables in a comparative approach between periods with positive returns and periods with negative returns. Relying on the stakeholder theory in a complementary way, the research addresses the empirical supposition whether the stakeholders are constantly concerned about environmental issues, regardless of the financial performance. The stipulation of this hypothesis as an objective of the research aimed to assess the possibility that the inconclusive association between EP–FP could be caused by the variation of environmental concerns of stakeholders. The integration of nonfinancial information related to the environmental behaviour of a company in the decision-making process has evolved closely towards mandatory business conduct. However, a nonfinancial metric is useful within the decision process as long as it manages to be related to financial data and upgrades the company’s performance–risk profile. By adding to this knowledge of the high-priority given to reducing the negative impact of EEA economies on the environment, a new question arose: does the decision-making relevance for environmental metrics remain the same during the periods with negative returns? Do stakeholders value the environmental performance of companies at the same scale whether the financial outputs are positive or negative, or is the sustainable growth pursued only during the profitable periods of time? The conclusions related to these questions not only provide managerial support in the design of corporate environmental policy but also help academics to focus, in the future, on a deeper and more comprehensive approach to the PE–FP relationship.

The answers to these questions were obtained based on the statistical techniques of Pearson’s correlation and linear regression. In order to provide solid evidence on the usefulness of environmental performance during different profitability scenarios, we applied the methodological techniques at the level of companies operating in two environmentally closely related sectors of activity. The two sectors are extractives and minerals processing, considered by SASB [

47] as the sector with the highest capacity of environmental issues impacting operational and financial results, and the healthcare sector, placed by the SASB at the middle of such a material capacity. The research findings provide important insights into the association between environmental performance and both positive and negative returns at the level of each sector of activity and among the sectors.

In the case of extractives and minerals processing companies, the statistical results point out a moderate capacity of association between environmental performance (ENV) and both the positive returns (positive ROA and ROE) and the negative returns (negative ROA and ROE). Based on these findings, we concluded that in the case of companies operating in a sector highly dependent on natural resources, the environmental actions and reduction of the environmental footprint represent relevant data for the decision-making process, regardless of whether the companies have reported positive or negative returns. Stakeholders are aware of the implications that environmental issues have on the sustainable development of these companies and, therefore, give them increased importance in risk assessment, no matter the level of accounting profitability. However, their concern is not constantly maintained at the same intensity. The lower capacity of association between EP and negative returns supports the assumption that the stakeholders may adopt a different ecological concern in the case of positive returns compared to negative returns. The percentage of total ROA variation explained by the evolution of ENV was consistently higher than the percentage in total ROE variation. The results are consistent with the economic causality between environmental investment and the value of tangible assets. Regarding the direction of the association between variables, the environmental performance metric was a factor of decreasing positive returns (positive ROA and ROE), and a factor of increasing negative returns (negative ROA and ROE). Therefore, investments in extractives and minerals processing companies with superior ecological behaviour reduce their financial performance, expressed by positive ROA and ROE, and contribute to the intensification of the negative level of accounting returns (negative ROA and ROE).

In the case of the healthcare sector, where companies with a lower impact on the environment operate, the statistical outputs support a moderate capacity of association only between environmental performance (ENV) and negative values of ROA. The association between ENV and positive values of ROA was statistically null, as well as the association between ENV and negative values of ROE. For the pair of variables ENV–positive ROE, Pearson’s correlation coefficient produced a low capacity of linear association, but it was relevant from a statistical point of view. The low capacity of association between environmental performance and both positive and negative values of ROA and ROE has partially validated our hypotheses for healthcare companies, confirming our previous conclusion that not every type of nonfinancial information is relevant in the decision-making process. In this case, environmental issues are not one of the main factors in stakeholders’ judgment. The usefulness is rather related to framing the specific background of the activity–performance–risk profile. In poor accordance with the stakeholder theory, ecological concerns do not seem to put pressure on the financial performance of these companies.

The findings suggest that environmental concerns and stakeholders’ requirements vary across industries. However, their relevance during the decision-making process and their impact on financial performance slightly depend on the scenario of positive and negative results. Only in the case of the extractives and minerals processing companies does the level of Pearson’s coefficient supported a slow variation of the relevance of EP in the case of positive returns compared to the case of negative returns. The limits of the research are related to the applied methodological techniques, and a future research direction may be the assessment of this comparative approach based on advanced techniques.

Our results provide a particularly important perspective, both for the decision-makers of a company and for researchers, that environmental responsibility remains a standing point in the case of companies with a high impact on the environment, whether the company has reported positive or negative returns. The scientific and practical contributions of the findings are even more relevant in the context of the European Green Deal and the “striving to be the first climate-neutral continent” [

7]. To become an environmentally sustainable economy, European companies need to understand the complex but vital link between the economy and the planet and to implement adequate strategies to enable them to become resource-efficient and globally competitive. In the real economy, the cycles of upward and downward movements in companies’ profitability follow naturally, one after the other. Therefore, in the authors’ opinion, the research addressing this topic, in the case of European industries, can enrich the body of knowledge in this field and can contribute to achieving the European Green Deal goals.

{kind=link}

{kind=link}