3.1. Methodology for Assessing and Making Strategic Decisions on Managing Sustainable Development of Industrial Enterprises: Current Status

As a methodological base of the research, the following are proposed: a systematic approach to studying the problems of sustainable development, a cultural and logical approach, and the theory and practice of assessing the sustainability indicators of economic facilities. Also considered are the theory of economic and mathematical modeling and works on investment design, strategic management, and the development of managerial decisions.

The analysis of scientific works shows that the problem of sustainable development is considered in the coordinate system: “nature–society–man”. This means that the ecological, economic, and social systems should be presented as three equal, interconnected components of sustainable development that cannot be separated from each other [

21]. The interaction of these guidelines for sustainable development provides a certain synergy and, with the optimal organization of strategic management, can increase the efficiency of the production system.

The enterprise itself, given the specifics of the activity, must be represented in the form of a stochastic dynamic system [

13,

22,

23]. This implies the synthesis and certain integration of complementary approaches to improving the management mechanisms of the mining company. Specifically, this study proposes the integration of three approaches. Firstly, the theory and practice of strategic management of enterprise sustainability; secondly, investment design; thirdly, analysis and assessment of sustainability indicators of industrial enterprises. An honest and correct assessment of the business allows you to choose and implement the optimal investment policy, which affects the equilibrium development of the company and the implementation of selected strategies. At the same time, the success of investment design is determined by the effectiveness of strategic management of the sustainable development of the enterprise and the ability to make adequate management decisions. Thus, this interconnection and complementarity makes it significant to use and clarify modern methods for diagnostics, assessing the safety of investment projects, and developing investment strategies of enterprises in the context of managing sustainable business development.

In Russia, more and more attention is being paid to the environmental status of investment projects, which is associated with global trends in life, the image component of the business, and the outflow of labor from disadvantaged regions of the country. The economic approach, based on the fact that living conditions are a blessing, a limited resource, which is part of the interests of an economic entity, is becoming increasingly important. Economics studies human behavior in terms of the relationship between its goals and limited means that allow alternative use. That is, it is necessary to study not only changes in the quality parameters, but also to assess the value of the environmental good and relations regarding the appropriation of living conditions.

All this should be taken into account when forming the investment policy of industrial enterprises, where the availability of investment is largely determined not only by the economic, but also by the environmental status of the projects.

From the point of view of the safety problems of production systems, it is necessary to prioritize the environmental and economic problems of enterprise sustainability, which allows you to take into account environmental changes depending on the specific situation and plan certain strategic decisions. According to V.V. Krivorotova and A.V. Kalina, the implementation of this procedure requires recognition of the inextricability of the problems associated with economic and environmental risks, which have the same nature of threats and consequences [

24].

When implementing the strategy for sustainable development of an industrial enterprise, forming an investment policy, and assessing risks, according to O. Rostova et al., the primary threats in terms of the magnitude of the consequences are experienced by the following basic properties of the system: the ability to self-development and the ability to counteract destabilization factors [

22,

23]. That is why indicators that characterize the basic properties of the system—adaptability of the control mechanism to environmental influences and sufficiency of resources for reproduction—should be singled out as criteria for assessing the level of the state of the enterprise.

According to the resource approach to assessing the economic and environmental status, one should be guided by general basic quantitative indicators. An indicative approach to risk assessment is aimed at determining the quality of the external and internal environment, the level of environmental safety, and involves the use of indicators and indices to assess the state of the ecosystem and the level of environmental impact of business entities.

Many researchers, in particular, P. Horvath, R. Gleich, and M. Seiter, suggest, evaluating all sorts of risks, to apply balanced indicators that allow you to track the dynamics of development and deviations from planned indicators. They are associated with changes in the production base, updating the product range, the introduction of new technologies, and social reforms [

25].

This study is based on resource and indicative index approaches, which allow to fairly accurately determine environmental and economic risks and assess them. As quantitative characteristics for evaluating projects, according to T.A. Akimova, the indicators of technological intensity, environmental capacity, and enterprise potential should be used [

5].

The well-known approach of J. Forrester was also used, which, when developing a model, suggests considering the company as a set of interacting divisions. This interaction takes into account temporal and spatial factors, where the relationship and interaction of both internal elements of the system and external are traced. This allows you to find the right managerial decisions for both departments and the company as a whole, linking the firm’s strategy with the situation on the market [

26,

27].

Modeling the management of a complex ecological and economic system, such as an industrial enterprise, requires special attention to the algorithms for implementing these processes, which is thoroughly considered in the works of the Shiryaevs. They proposed very interesting methods of constructing mathematical models that allow us to describe the interaction of structural units of the company and the corresponding financial, material, and communication flows [

27].

This work also offers tools for adapting an industrial enterprise to changing environmental conditions, which logically follows from the recommendations of K. Waren on the formation of an enterprise management mechanism in conditions of uncertainty and instability of economic relations and relations of market entities [

28].

Since the possibility of obtaining affordable investments by industrial companies is most closely linked to the assessment of the environmental and economic status of the enterprise, it is necessary to take the approaches to modeling the strategic management mechanism of the company that V.V. Leontiev and J. Forrester supplemented by the achievements of a number of modern authors [

27,

29]. So, according to B. Sharp, D. Bergh, and L. Ming, the model should include modules of managerial actions based on the basic functions of management-controlling, feedback, social responsibility of the business, motivation system, and elements of reputation capital [

30]. Thus, it is possible to ensure close interaction of the production system with the environment in the external environment and timely identify and respond to possible destructive threats.

The process of modeling the mechanism of strategic management of sustainable development of an enterprise, as indicated by F. Mousavifard, A. Ayoubi, and M. Sanie, must include a component of automated information and communication systems. This allows you to improve the quality of diagnosis and assessment of environmental and economic threats, and to timely plan actions aimed at reducing the possibility of the transition of the economic system to a state of uncertainty [

31].

The stable state of enterprises in modern conditions depends on many factors, but among them, according to a number of researchers, the technological development of the company and the availability of investments for implementing business projects are determining factors [

19].

The presented study, as an important component of the strategic management system, distinguishes precisely investment policy, its close linkage to the enterprise ecosystem, and the security of the territory of operations, which is also associated with the introduction of environmentally friendly or acceptable technologies. At the same time, these advanced and safe technologies provide an economic effect and contribute to the sustainability of the company. The works of S.G. Kalinin, V. Tribushnaya, and other scientists presented approaches and methods for forming investment strategies and optimizing the structure of investment capital [

32]. In particular, when modeling the mechanism of managerial decision-making, it should be possible to pre-identify and correctly respond to emerging gaps in the process of strategy implementation. These gaps appear when an insufficiently accurate risk assessment is made, when the technologies do not meet the environmental requirements, and the investment potential does not meet the needs of the enterprise.

Improving the strategic management of the sustainable development of the enterprise provides for a set of actions with close attention to each component of management [

33]. One of these components is the analysis and assessment of the solvency of the enterprise, taking into account possible risks.

In the international practice of analyzing the sustainable development of an enterprise, including the possible likelihood of bankruptcy, there are various methods: the Altman method, the four-factor forecasting Tuffler model, the Lis model, and others. For Russian companies, a modified five-factor model suggested by G.V. Savitskaya, which takes into account the specifics of domestic enterprises, is often used [

34]. These methods are used to determine financial stability, without taking into account the social and environmental sustainability of the enterprise.

The Altman model allows you to accurately assess and predict the possibility of bankruptcy of large industrial companies using the Z-factor. The coefficient is calculated according to the following Equation (1).

where X11 is working capital/total assets; X12 is retained earnings/amount of assets; X13 is operating profit/amount of assets; X14 is market value of shares/debt; and X15 is revenue/amount of assets.

You can also calculate the insolvency risks of an industrial company using the well-known Lis model. The discriminant model includes four factors and is calculated by Equation (2).

where X21 is working capital/total assets; X22 is profit from sales/total assets; X23 is retained earnings/amount of assets; and X24 is carrying amount of equity/borrowed capital.

Features of the economic activity of industrial enterprises in Russia led to the need to improve the Altman model (Equation (3)).

where X31 is the share of working capital in the formation of current assets, coefficient; X32 is accounts for working capital per ruble of the main; X33 is total capital turnover ratio; X34 is return on assets of the enterprise; and X35 is coefficient of financial independence (share of equity in the total currency of the balance sheet).

Sustainable development of the enterprise involves minimizing the risks of bankruptcy and insolvency of the company. Therefore, it is necessary to pay close attention to the calculation of the corresponding coefficients, trying to apply the most appropriate method for calculating the sustainability of an industrial company, and taking into account the specifics and conditions of activity of industrial enterprises of the Russian Federation.

The above methods used in Russia do not allow to fully take into account all aspects of assessing the sustainable development of enterprises, which requires the introduction of appropriate amendments to existing models for assessing business sustainability.

3.2. Methodology of Enterprise Development Management in the Context of Social, Environmental, and Economic Sustainability

Traditional methods of analyzing the state of an industrial enterprise, unfortunately, do not fully reflect the fundamental directions of the concept of sustainable development within the framework of decisions and recommendations of the UN. In Russia, whose economy has been characterized in recent decades by serious fluctuations from growth to recession and is characterized by a high degree of instability, they did not pay enough attention to the triad of sustainable development in the coordinate system: nature–society–people. According to this approach, reflected in the United Nations Millennium Declaration in 2000, sustainable development can be represented as a process of large-scale changes of a global nature. This process involves the coordination of scientific and technological transformations, business projects, the exploitation of natural resources, personality development, and changing public institutions in order to strengthen existing and future development potentials to meet social needs and harmonize relations. Based on this, there are three equal components of sustainable development: economic, environmental, and social. The interaction of these systems ensures the progressive development of the world economy and its individual representatives. In order to achieve optimal interaction of these three components, new, modern methods of a comprehensive assessment of stability are needed. This study proposes the development of additional indicators of sustainable development, which are typical for enterprises of a particular selected industry. As part of the reporting, three groups of indicators of sustainable development are identified, which represent three aspects: economic, environmental, and social (

Table 1,

Figure 1).

Given the insufficient data and the confidentiality of corporate information in each dimension, a number of indicators were identified, the values of which were taken from company reports or estimated by experts [

35]. Thus, based on the analysis of the above works, as well as the works of T.A. Khudyakova, A.V. Shmidt, S.A. Shmidt, [

19], V.I. Shiryaev, I.A. Baev, and E.V. Shiryaev [

27], we proposed the following scheme for assessing the environmental and economic status of an economic entity.

Estimated indicators of the respective components are combined on the basis of the above criteria for the availability of adaptation mechanisms to environmental influences and the adequacy of resources for the reproduction of the company’s activities in the relevant territory.

A comprehensive risk assessment allows you to start the process of making managerial decisions related to the further development of the company and the implementation of investment projects. Here, one should strictly observe the procedural aspects, the sequence of stages and steps of development and decision making, and their adequacy to the firm’s strategy, as V.A. Barinov points out in his work [

36].

The model of V.V. Leontiev reflects the main parameters of the activities of industrial companies [

29]. This model is simple and allows you to make additions to it to reflect the specific characteristics of the activity of the object of study.

The management system should ensure timely response to possible gaps and close interaction of the strategic management components of sustainable development. For this, it is necessary to provide components, algorithms of actions, common to different control subsystems, in an improved model for making managerial decisions [

37].

When developing the appropriate strategic management algorithm for the sustainable development of an industrial enterprise, one should focus on the works of the authors, which give a thorough analysis of the activities of industrial companies in Russia over the past 5–6 years of activity. They take into account the specifics of the functioning of Russian business in a crisis state of the economy. Such an algorithm is presented in the works of N. Yu. Varkova, A.V. Aliukov, T.A. Khudyakova, and V.V. Zhuravlev, devoted to optimizing the mechanisms of assessment, development, adjustment, and control of strategic management decisions [

38].

Having analyzed the practice of managing industrial enterprises of the Urals and the scientific works of a number of foreign and Russian researchers, it is proposed to make certain improvements to the methodological tools, process, and strategic management mechanisms of an industrial enterprise.

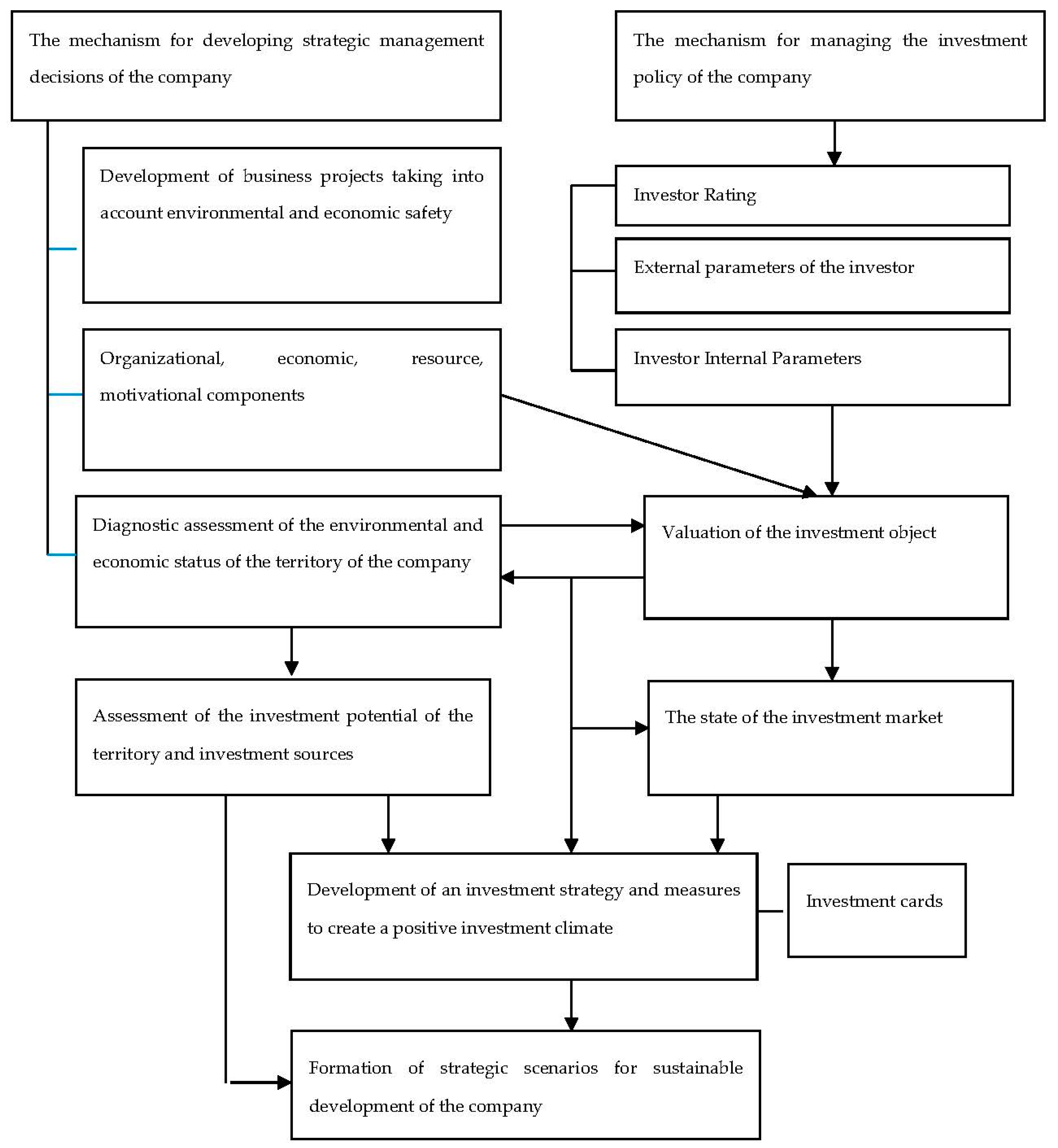

Strategic management should be based on the close interaction of two subsystems: the subsystem of managerial decision-making and the formation of investment policy. Synergy will be achieved by identifying the connecting components of this process, which include a diagnostic assessment of the environmental and economic condition of the territory of the company and the investment opportunities of the enterprise.

The main elements of the improved mechanism are presented below. A graphical model and proposals for economic and mathematical modeling are also presented, which reflect the relevant processes for managing the sustainable development of industrial companies in Russia.

Strategic management of the sustainable development process is considered from the point of view of efficiency for all functional aspects of the enterprise, that is, social, economic, environmental. Management of complex systems involves fine-tuning the control mechanism, taking into account the whole variety of environmental factors, detailing plans, optimal selection of methods and technologies, proactive management of the company, and the ability to timely adapt the company’s strategy to possible changes in operating conditions [

39]. So, in order to achieve the sustainability of the functioning of the coal mining company, an algorithm is proposed for improving the strategic management of the investment activity of the enterprise, which consists of the following steps.

Proactive-analytical phase. This stage is characterized by the search for points of contact of the company with environmental elements, the establishment of positive interaction with the socio-economic and environmental environment of the enterprise, and the formation of peculiar “islands” of the future close integration of the company with all subjects of economic, environmental and socio-political interaction. Accordingly, at this stage, an analysis of environmental factors is also carried out, where the main development trends, problems, opportunities, threats are identified. This will determine the set of indicators of sustainable development and determine the contours of the interactions of the enterprise, as an economic and environmental system, in the external and internal environment.

The forecast stage. At this stage, you should understand how to integrate management tools into the planning system of business processes necessary to implement the appropriate company strategy. Here, the possibility of sustainable development will be assessed for each component of the strategy—economic, social, environmental—as well as identification of possible problems. The priorities of solving the identified problems are determined on the basis of the methodological tools available to the enterprise management. Based on this, a hierarchical system of goals and objectives is built. As a result, the company’s management determines the direction of investment policy and the structure of investment capital.

Integrated phase. This stage involves the most accurate use of existing tools and the full inclusion of the mechanism for making and implementing managerial decisions in the process of economic activity of the company. Additional opportunities for business development should be given by the synergy of the relations of the enterprise with the elements of the environment. The result of this stage should be to increase the level of sustainability of the company as a single environmental and economic system.

The control and adaptation phase. At this stage, we compare the planned results with the normative indicators of the implementation of the firm’s strategy, adjust the investment policy, and form a system of adaptation measures for the implemented sustainable development strategy. The process of adaptation of an enterprise to changing operating conditions should be considered as an investment process at the micro level in the short and medium term. This means the possibility of using different methodological approaches to company management.

A model for the development of strategic decisions on managing the sustainable development of an industrial enterprise and forming investment strategies should take into account the fact that these enterprises are business entities operating in resource-type territories. They use reproducible and non-reproducible natural resources. Therefore, an important condition for their functioning is the implementation of a system of measures that contributes to the reproduction of the natural resource subsystem. This necessitates a thorough assessment of environmental and economic risks. Also, establishing close ties and interactions between the mechanisms of making managerial decisions and shaping the investment policy of an industrial company [

40].

In Russia, as in many industrialized countries, various regulatory instruments of a compulsory, exacting, and stimulating orientation are used to preserve the environment and ensure safe economic development. In the framework of economic incentives for enterprises in order to prevent the impact of anthropogenic character on the ecological and social environment, limits and quotas on the use of natural resources are used. The framework also applies payments and fines for environmental pollution, environmental insurance, and more. Unfortunately, the size of such payments and deductions is not so large as to have a serious impact on the economic policies of Russian enterprises.

However, due to the fact that, in the last 4–5 years, Russia has encountered problems with the availability of investments, which was mentioned at the beginning of the article, new opportunities have appeared for implementing the strategy of sustainable development of enterprises [

38]. In this case, the condition for ensuring environmental and economic protection of the territory of activity and improving the investment policy of the company should be implemented. Let us highlight these features.

First, the Government of the Russian Federation, in order to stimulate business development and improve the social situation, identifies special development zones in hard-to-reach and disadvantaged territories. It is in these zones that companies that are the subject of our attention carry out their activities. These companies are provided with substantial benefits and certain preferences in the field of financing investment projects but while ensuring environmental protection.

Secondly, there was a reorientation of Russian industrial enterprises to that of East China, India, Japan, Turkey, and other countries. This led to a rethinking of investment policy, which required a serious change in approaches to assessing the ecological and economic state of the environment. It is also necessary to improve the process of making managerial decisions. In modern conditions, decisions require the development of measures and the use of tools to ensure the preservation of the ecosystem and the reproduction of natural resources.

All of the above had an impact on proposals for improving the strategic management model for the sustainable development of an industrial enterprise, as shown in

Figure 2.

System management of enterprise development, according to J. Sterman, means achieving close and well-developed interaction between the main subsystems and elements of the company. Business dynamics aims for management to achieve a synergistic effect, taking into account the influence of the external environment [

41]. That is why, and also based on the development trends in the coal mining industry of the Russian Federation, the main focus of this study was targeted on the two most important subsystems of strategic management of the company. This is a mechanism for developing strategic decisions and a mechanism for managing the company’s investment activities. Both subsystems should closely interact with each other, ensuring a minimum of errors in the development and implementation of the enterprise strategy.

The connecting component of this process is a diagnostic assessment of the environmental and economic state of the territory of the company and an assessment of the investment opportunities of the enterprise. The mechanisms for developing strategic decisions and managing investment policies are set up in such a way that, when implementing the corresponding management functions and assessing various risks, they allow taking into account the effect of various aggressive negative effects on the stability of the enterprise.

Great attention is paid to assessing investors, internal and external parameters of investment policy, and the state of the subjects of the investment market.

The result of optimally debugged mechanisms is the development of an investment strategy and a set of measures to create a positive investment climate for the company [

40]. It is at this stage, in our opinion, that the mutual effect of the work of mechanisms for making strategic decisions and managing the investment activity of the company is manifested. It is expressed in the development of investment maps, which include matrices for assessing environmental safety, the likelihood of a crisis and the occurrence of possible losses at the end of a given period of activity of the enterprise, taking into account changes in environmental parameters. At the same stage, investment strategies are proposed for implementation on the basis of improving the social, environmental, and economic status of business.

Thus, the presented mechanism for managing the strategic activities of a coal mining company makes it possible to link together the whole range of strategic actions:

- -

the process of developing and making management decisions;

- -

investment design;

- -

strategic control;

- -

diagnosis of possible risks;

- -

assessment of environmental and economic parameters of the implemented investment strategies;

- -

adjustment of management decisions in the framework of achieving the course on sustainable development of the company.

One of the main components of the decision-making mechanism for strategic management of sustainable development of an industrial enterprise is the assessment of environmental and economic risks. This is due to the fact that industrial enterprises are the main consumers of natural resources and most often operate on land spaces, where the main activity is the extraction and processing of these natural resources. For such companies, the principle that takes into account the formation of investment policies and development strategies should be the principle of high-quality reproduction of resources and reduction of risks to the ecosystem of the company. Based on the assessment, decisions are made to develop an investment policy and adjust the basic strategy of the company. The evaluation procedure was schematically presented earlier.

A comprehensive assessment allows you to monitor the state of the environment and determine the parameters of the respective components of the enterprise strategy, and form the company’s investment policy based on the assessment.

Further, in the framework of assessing the social and environmental component of the sustainable development of an industrial enterprise, we turned to the calculation of indicators of sustainable development (Equation (4)).

where Ufa is an indicator of financial and economic stability; Usr is indicator of social sustainability; and Uak is an indicator of environmental sustainability.

To determine the integral indicator of the financial and economic stability of the enterprise, which takes into account the coefficient of total liquidity

, the percentage of the plan

, and the coefficient of the plan for cash flows

, we turn to the formula

The integral indicator of the social stability of the enterprise, taking into account the coefficient of personnel stability

and the ratio of the average wage in the enterprise to the industry average

, the coefficient of the absence of wage arrears

is determined by the formula:

The integral indicator of the environmental sustainability of the enterprise, including the non-waste production coefficient

, the utilization rate of production waste

, and the coefficient of the industrial enterprise’s impact on the air

, is determined by the formula:

To interpret the result of the integral coefficient of sustainable development, we use the class-by-class classification of the enterprise sustainability level—Harrington’s scale of desirability level (

Table 2). One of the main objectives of the study was the development of an integral indicator for assessing the level of sustainability of the enterprise. This indicator is reflected in formula (7). The criteria for its assessment are given in

Table 2. Also, the criteria from

Table 2 can be applied to assess separately the social and environmental component of the sustainable development of an industrial enterprise, financial and economic stability of the enterprise, or the social stability (Equations (4)–(6)).

In general, the graphical model for developing strategic decisions presented in the article is based on the possibility of achieving synergy by closely interconnecting the mechanism for forming managerial decisions of an industrial enterprise and the mechanism for managing investment policies, creating a favorable investment climate, and an appropriate reputation for the enterprise. The appropriate investment atmosphere can be created and maintained solely on the basis of the priority environmental and economic status of the company.

According to the proposed model, close interaction between the strategic decision-making subsystem and the investment policy management subsystem provides:

- -

assessment of the environmental and economic status and investment component;

- -

the presence of a connecting stage common to both strategic management subsystems, which is the development of an investment strategy and measures to form a positive investment climate.

These measures necessarily include measures to protect and restore the ecosystem of the territory of the company.

In order to develop and strengthen ties and interaction between the components of the mechanism of strategic management of the development of the company, it is proposed to develop investment maps. These cards include a matrix of values of the parameters of the ecological and economic system, priorities of investment design, and investment strategies developed on the basis of an assessment of the ecological and economic condition of the territory of the company’s activity. Cards help management make decisions on the formation of investment policies and develop alternative development scenarios.

Thus, optimally established managerial interaction within the framework of the proposed model for strategic decision-making and investment policy management, the process and procedures for evaluating, analyzing, recording, and transmitting data on the state of the ecological and economic system of the company is an important mechanism in the formation of a sustainable development strategy for the mining company.

The proposed recommendations for improving the strategic management model should help enterprise management reduce the number of possible losses in the formation of the company’s strategy, taking into account various aspects of environmental, social, business and economic risks. These recommendations are still far from perfect and raise certain questions; nevertheless, they indicate directions for further research in the field of improving the mechanisms for evaluating and implementing the strategic management of an industrial enterprise.

,

,

{kind=link}

{kind=link}