Regional Inequalities in Flood Insurance Affordability and Uptake under Climate Change

, , and

, , and

Abstract

:1. Introduction

2. Model Description

2.1. Flood Risk Model

2.2. Insurance Sector Model

Voluntary or Semi-Voluntary Market (M2, M3)

2.3. Household Behavior Model

3. Results

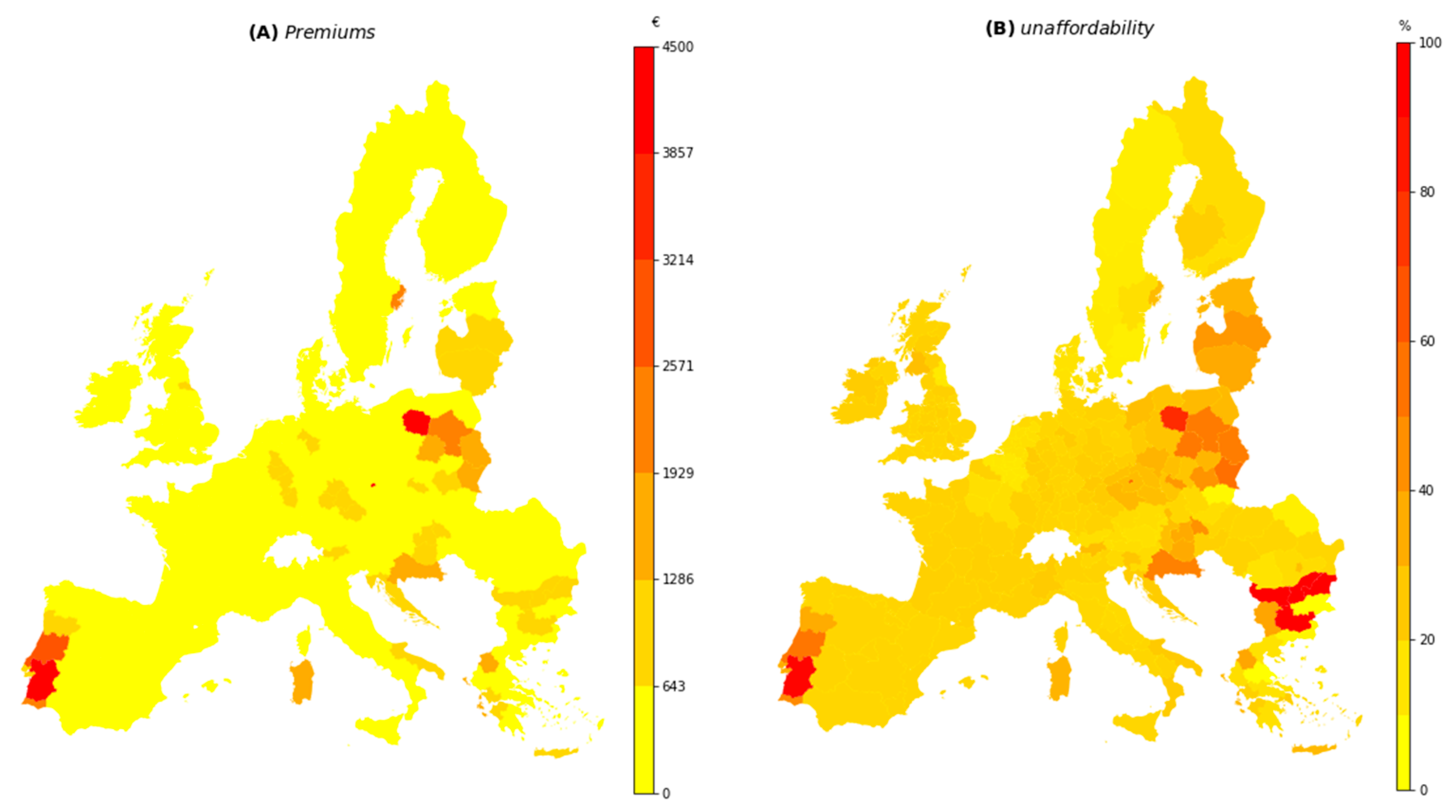

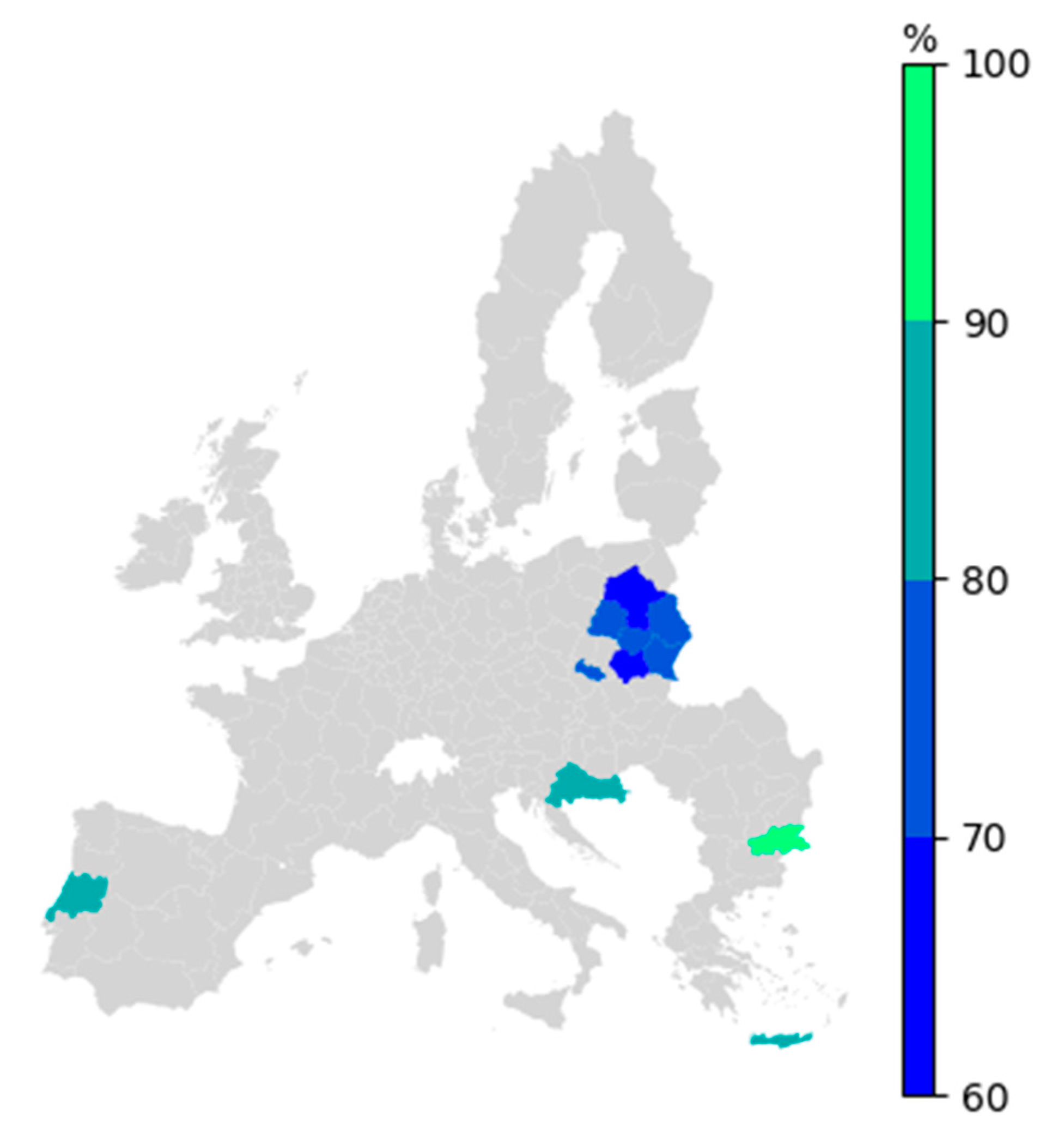

3.1. Unaffordability of Flood Insurance under Current Insurance Arrangements

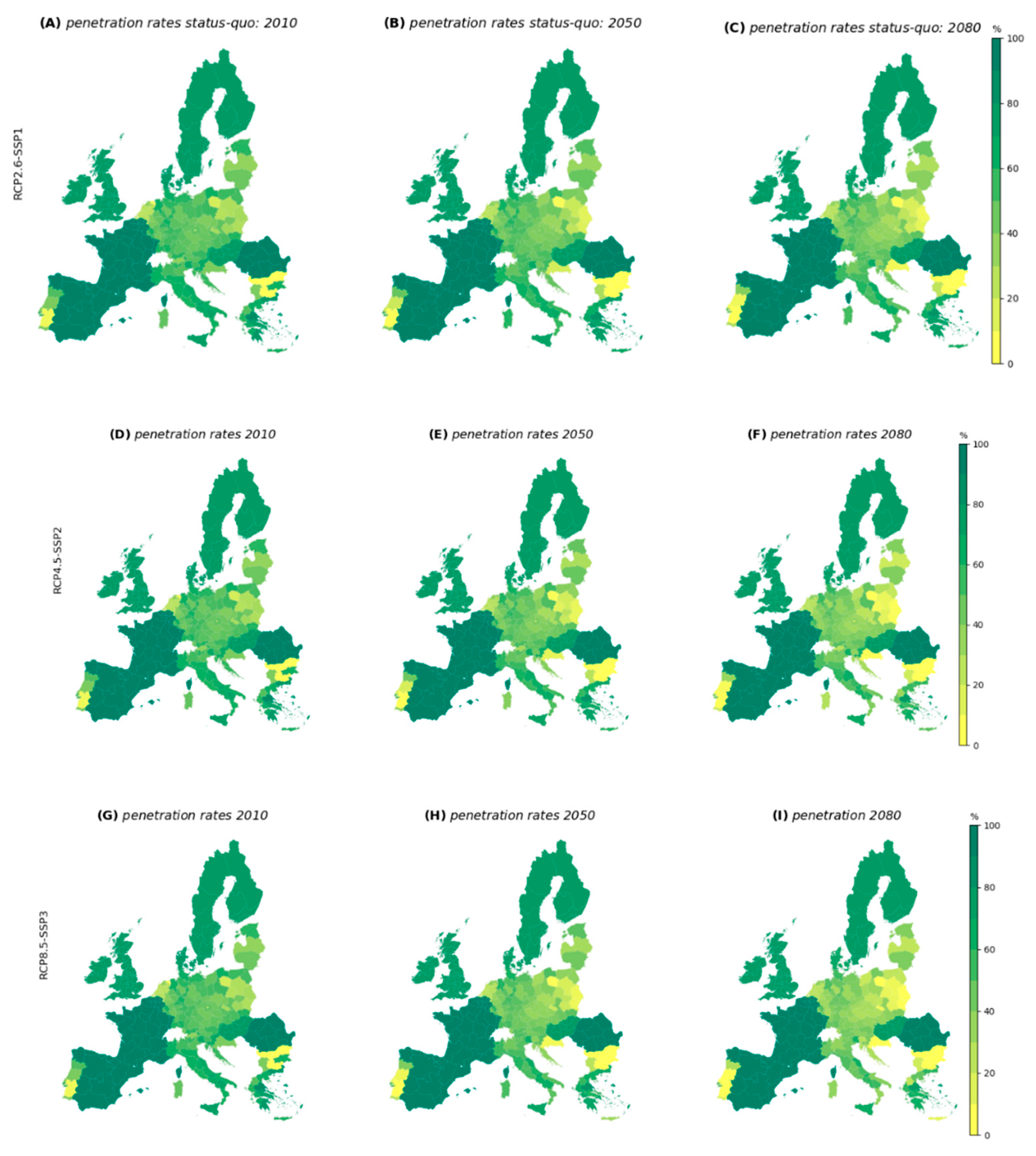

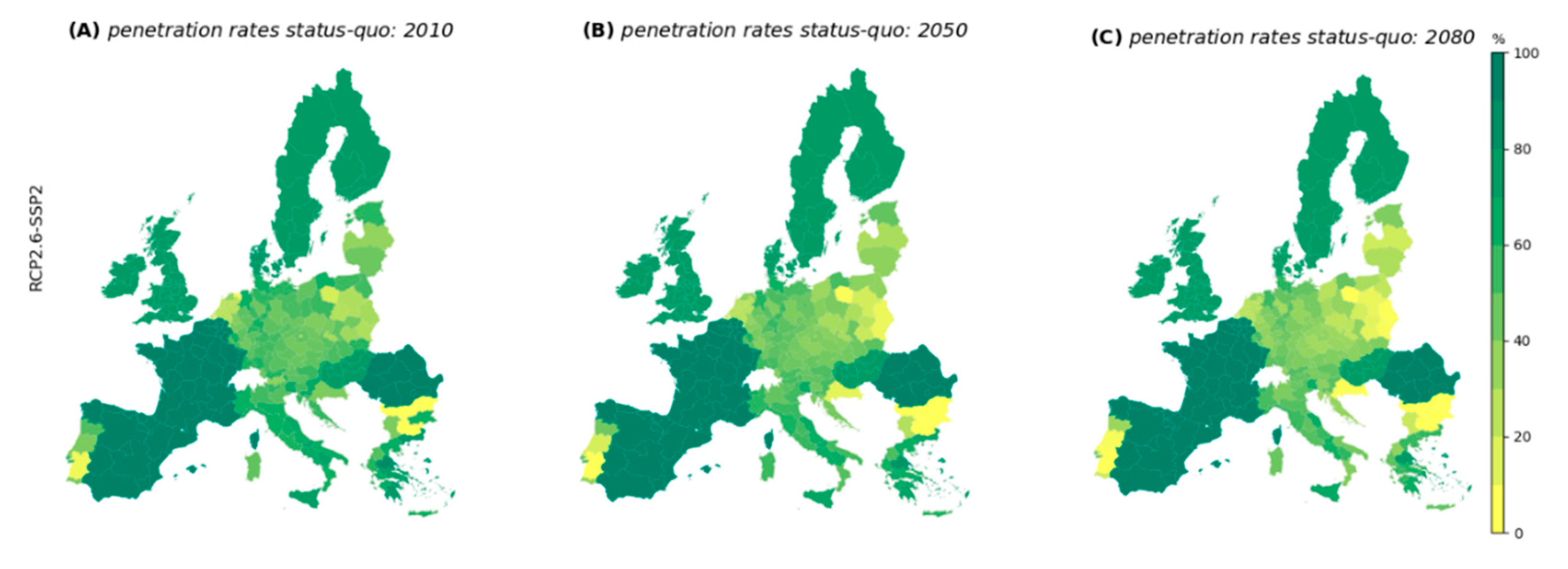

3.2. Insurance Market Penetration

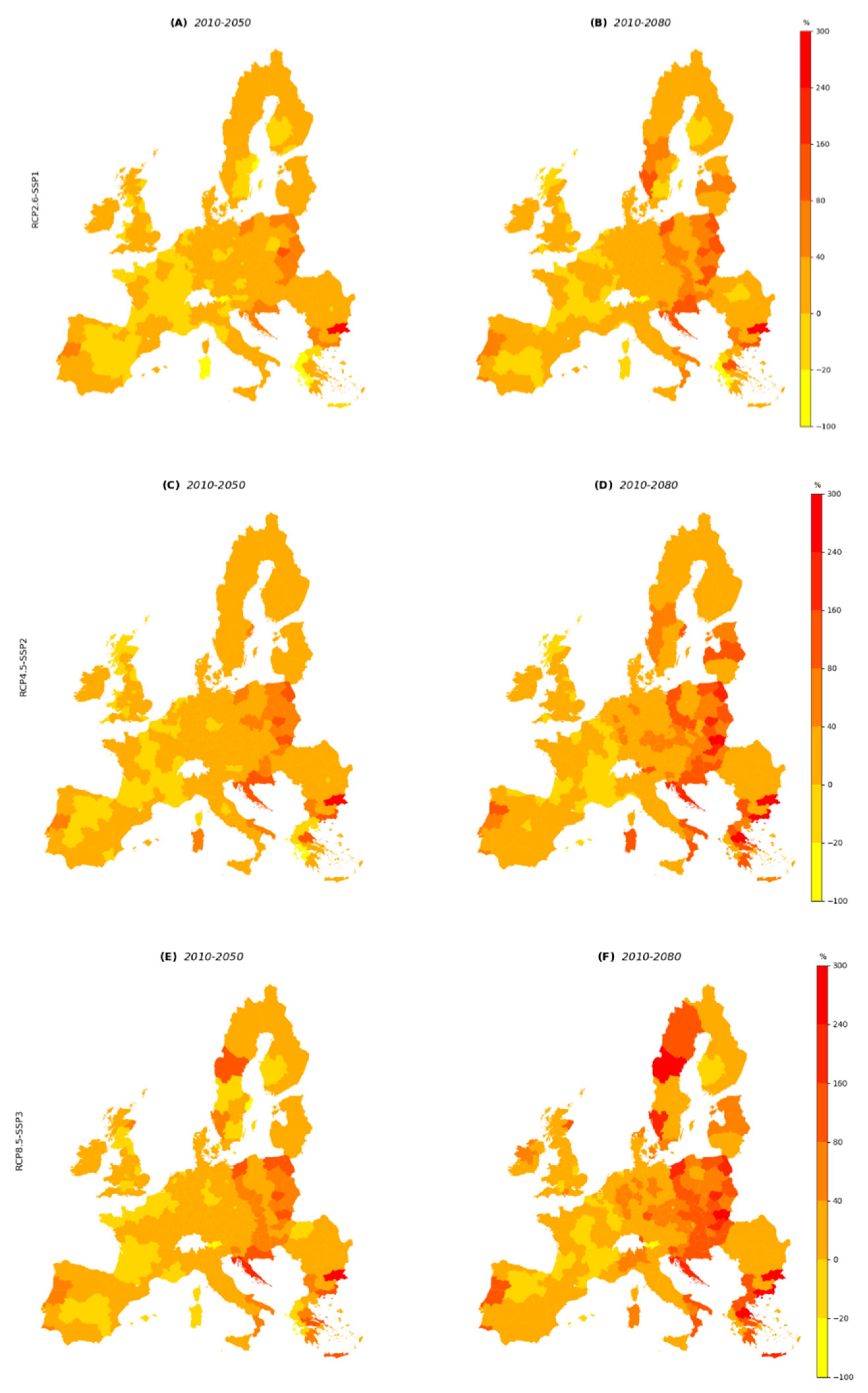

3.3. Unaffordability of Flood Insurance and Penetration Rates under Policy Change

4. Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Premiums in the Solidarity and Public-Private Market Structures

Appendix A.1. Solidarity Market (M1)

Appendix A.2. Public-Private Market (PPP) (M6)

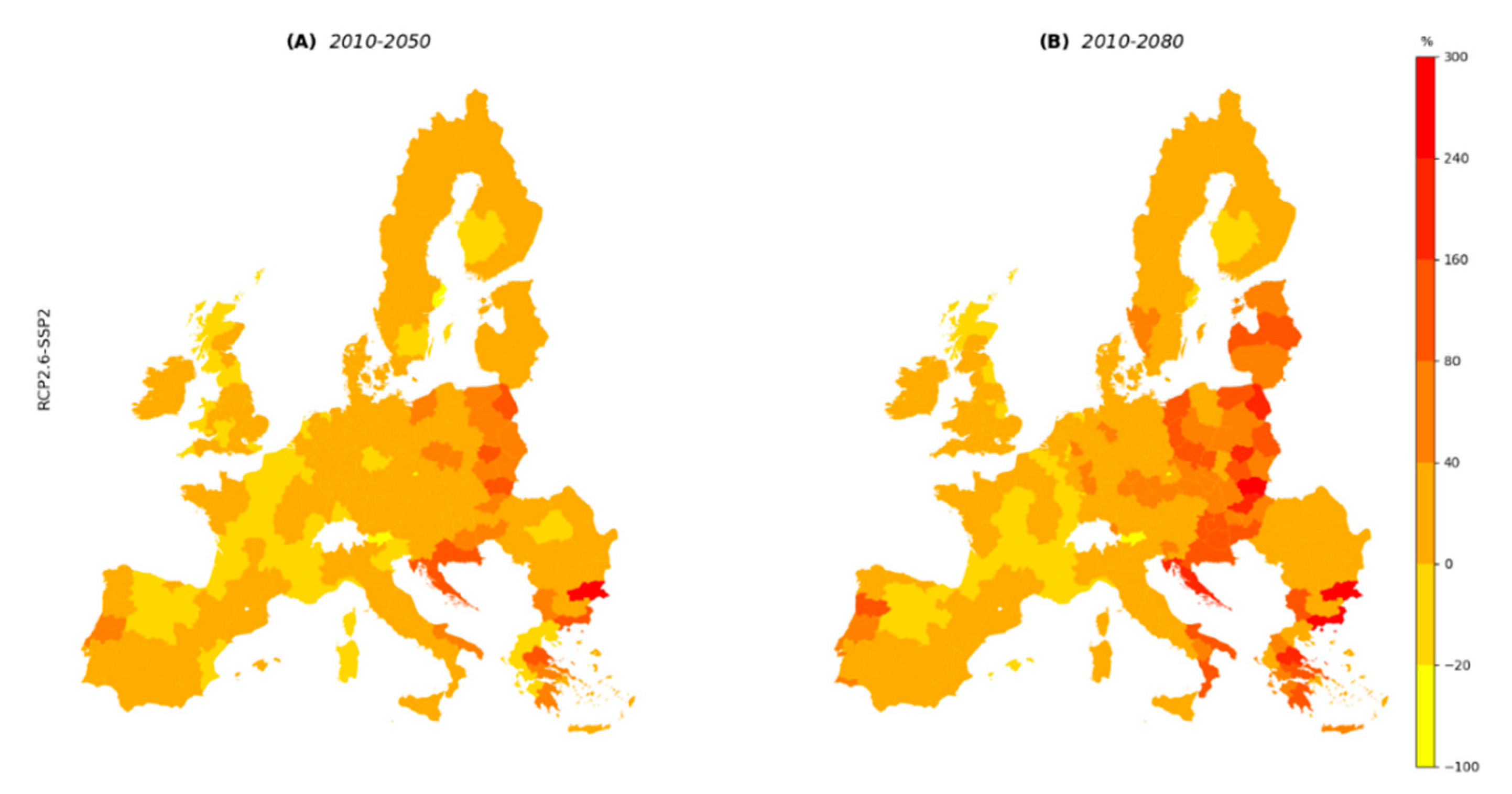

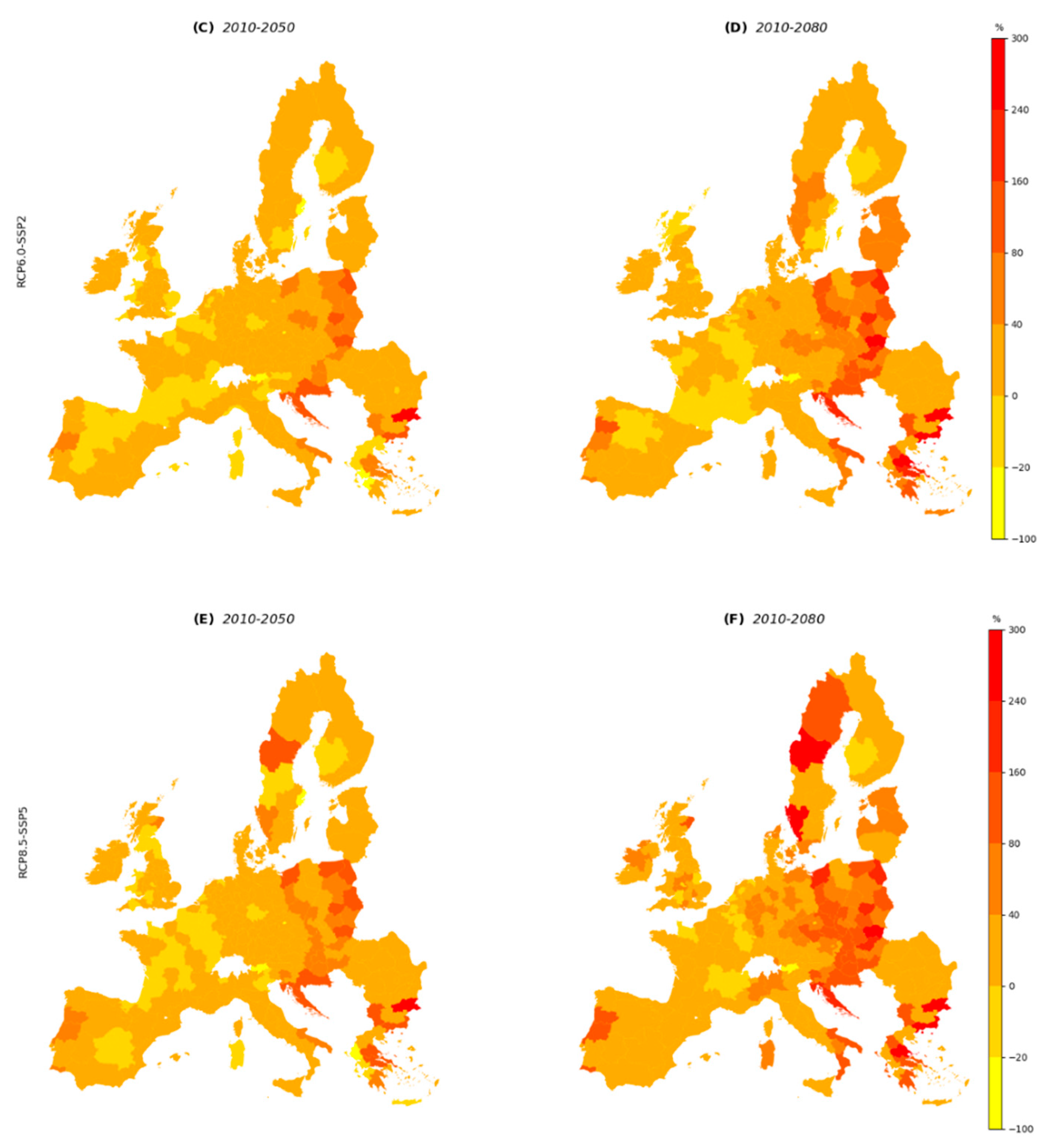

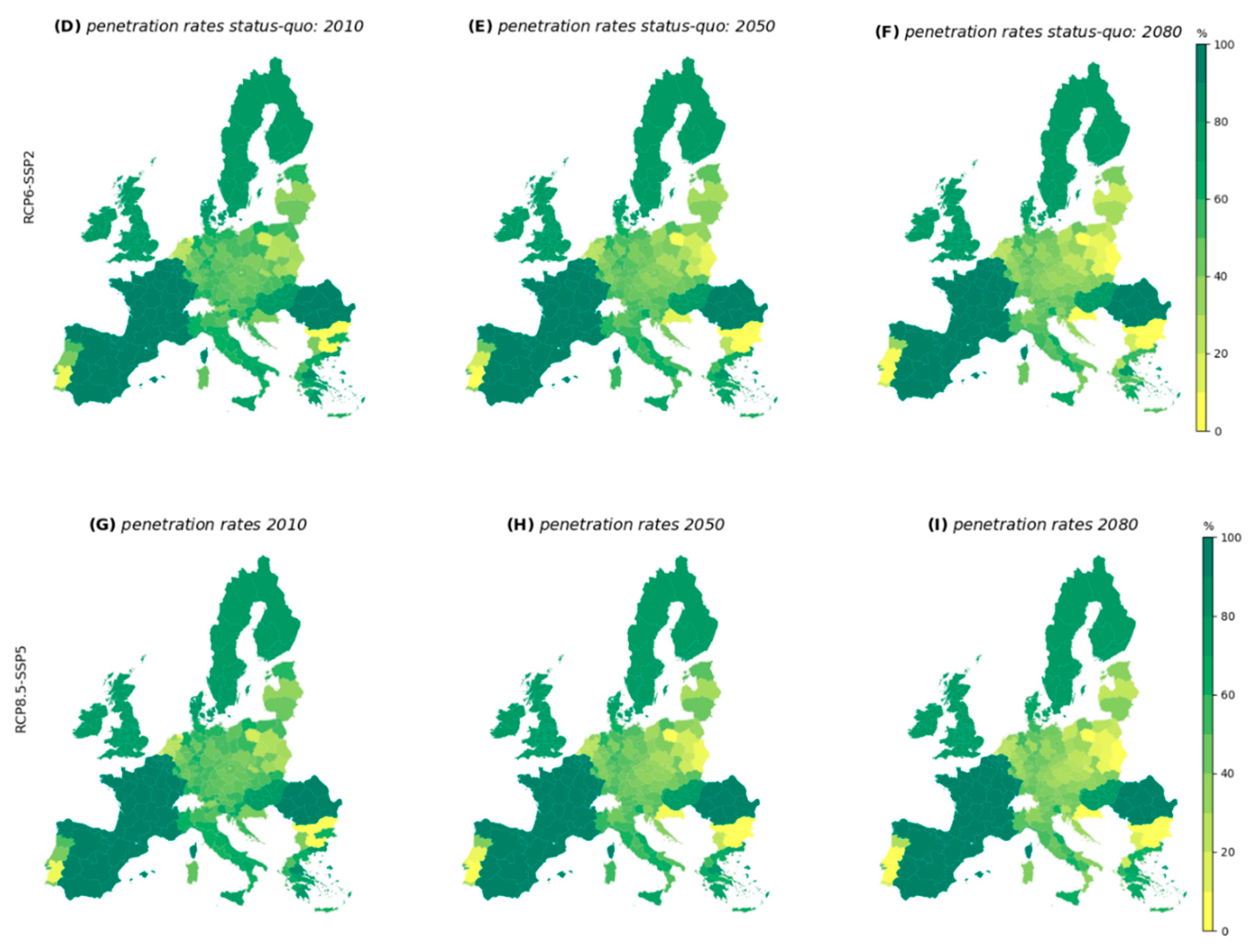

Appendix B. Results of Unaffordability and Market Penetration under Scenarios: RCP2.6-SSP2; RCP6.0-SSP2; RCP8.5-SSP5

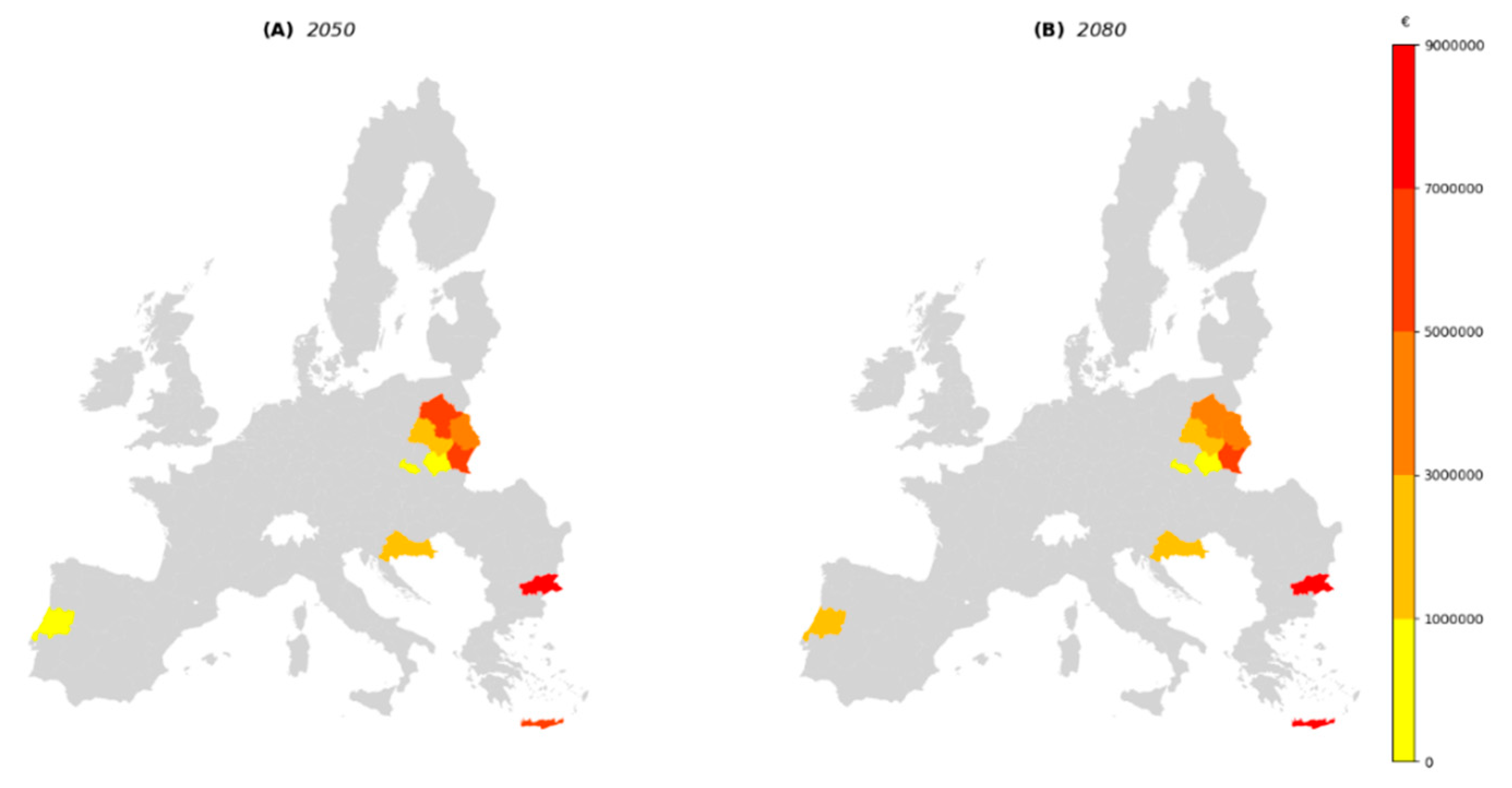

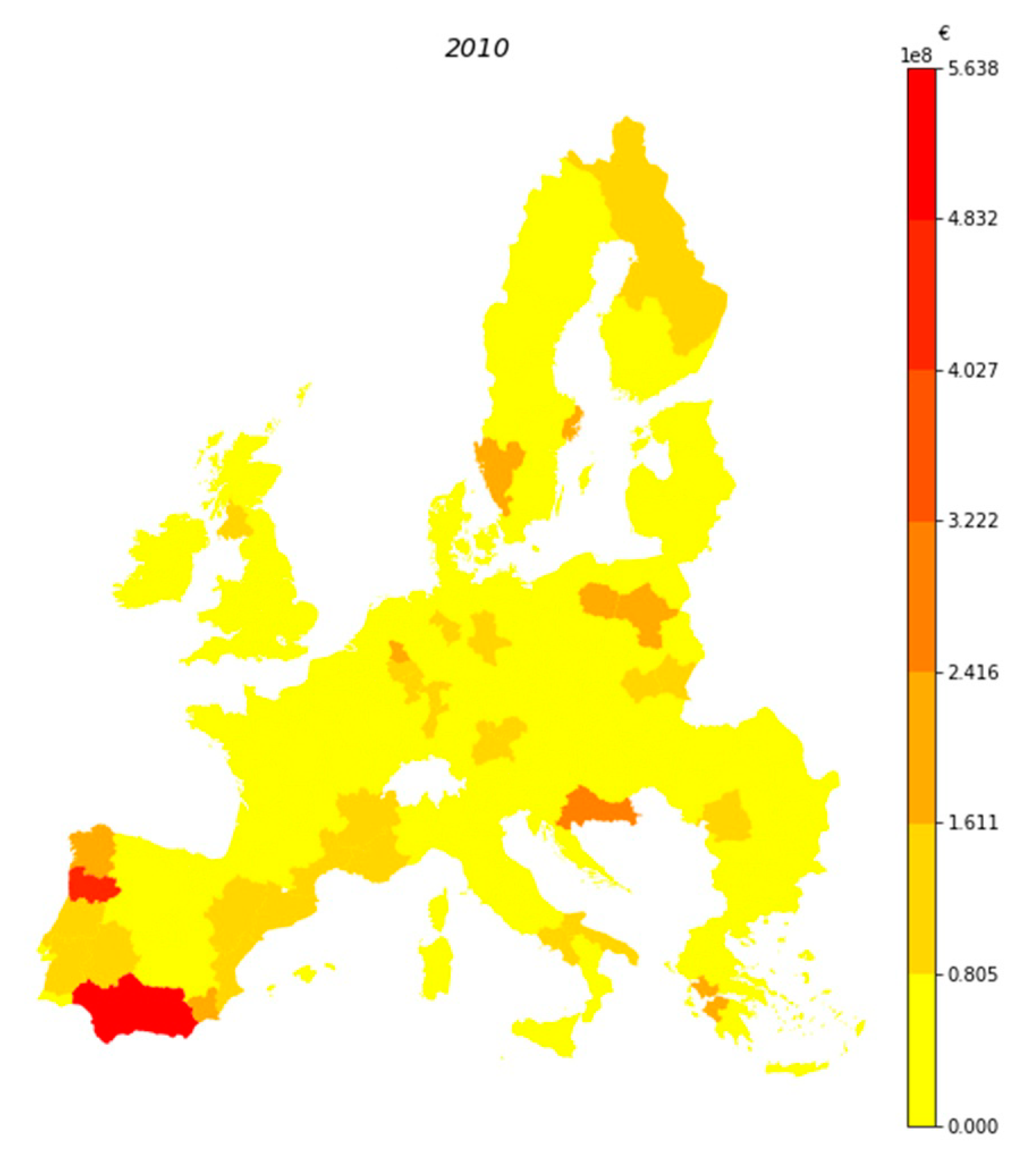

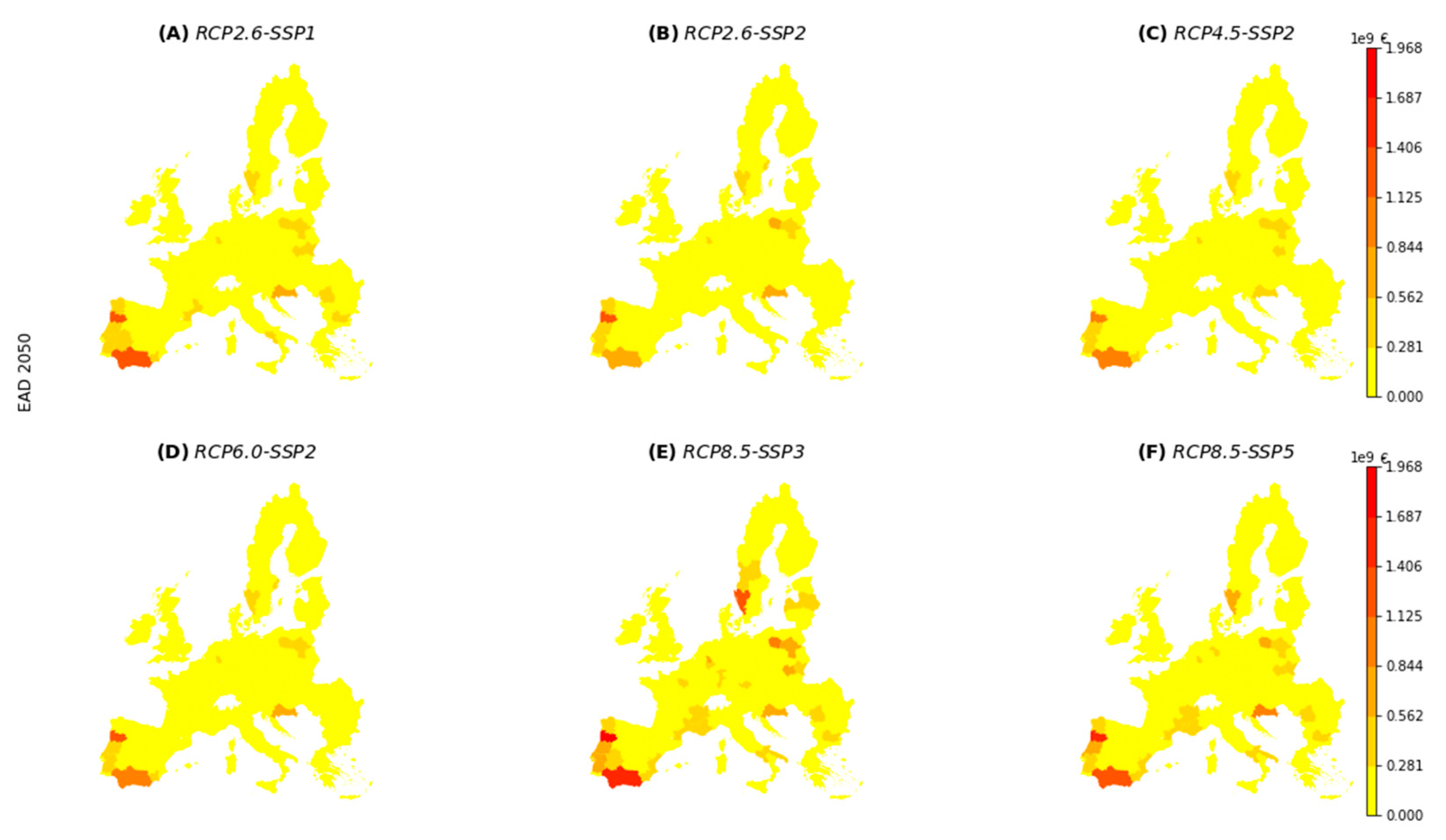

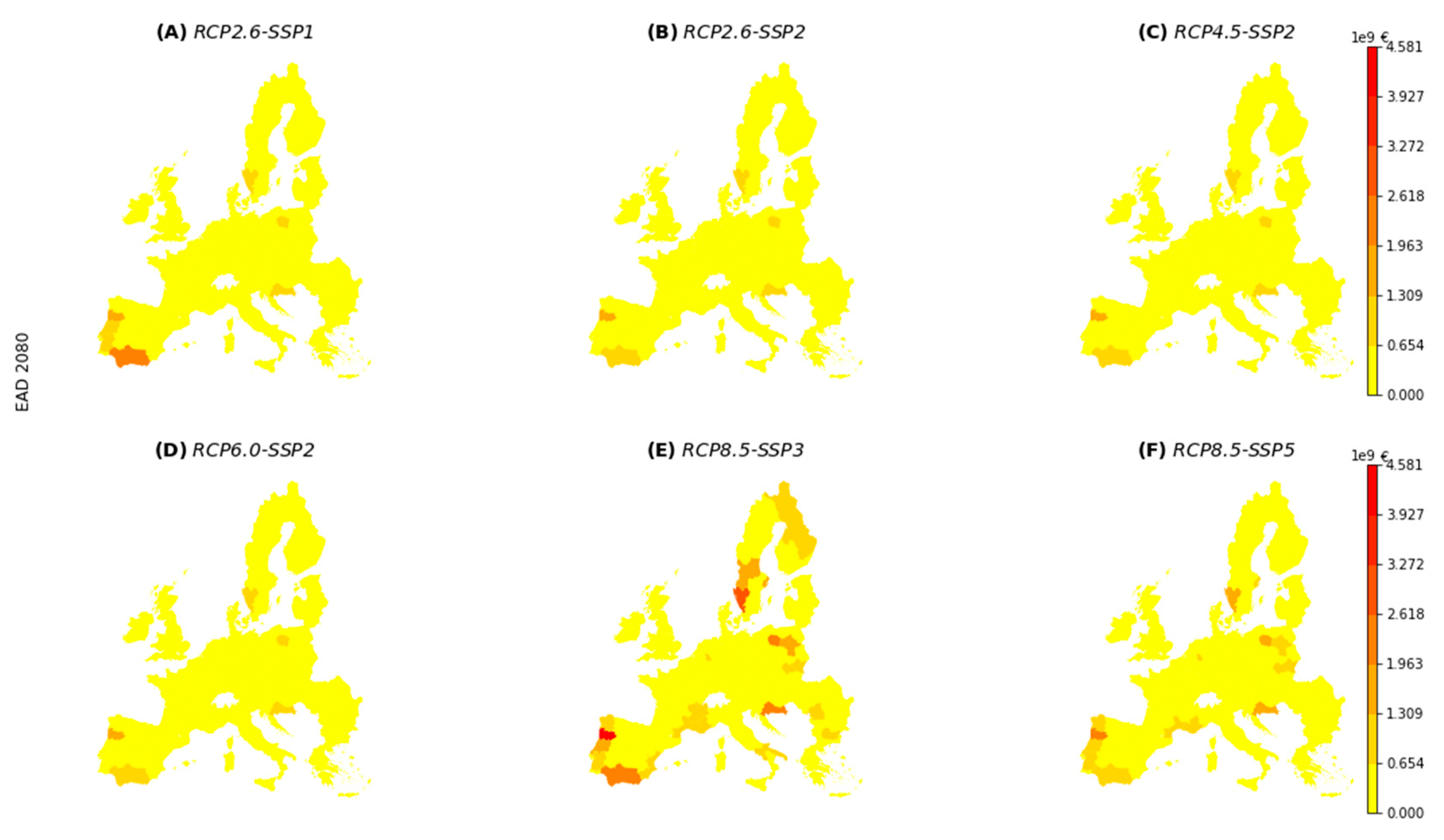

Appendix C. Expected Annual Damage (EAD) in the Baseline and for Future Projections under Multiple Scenarios

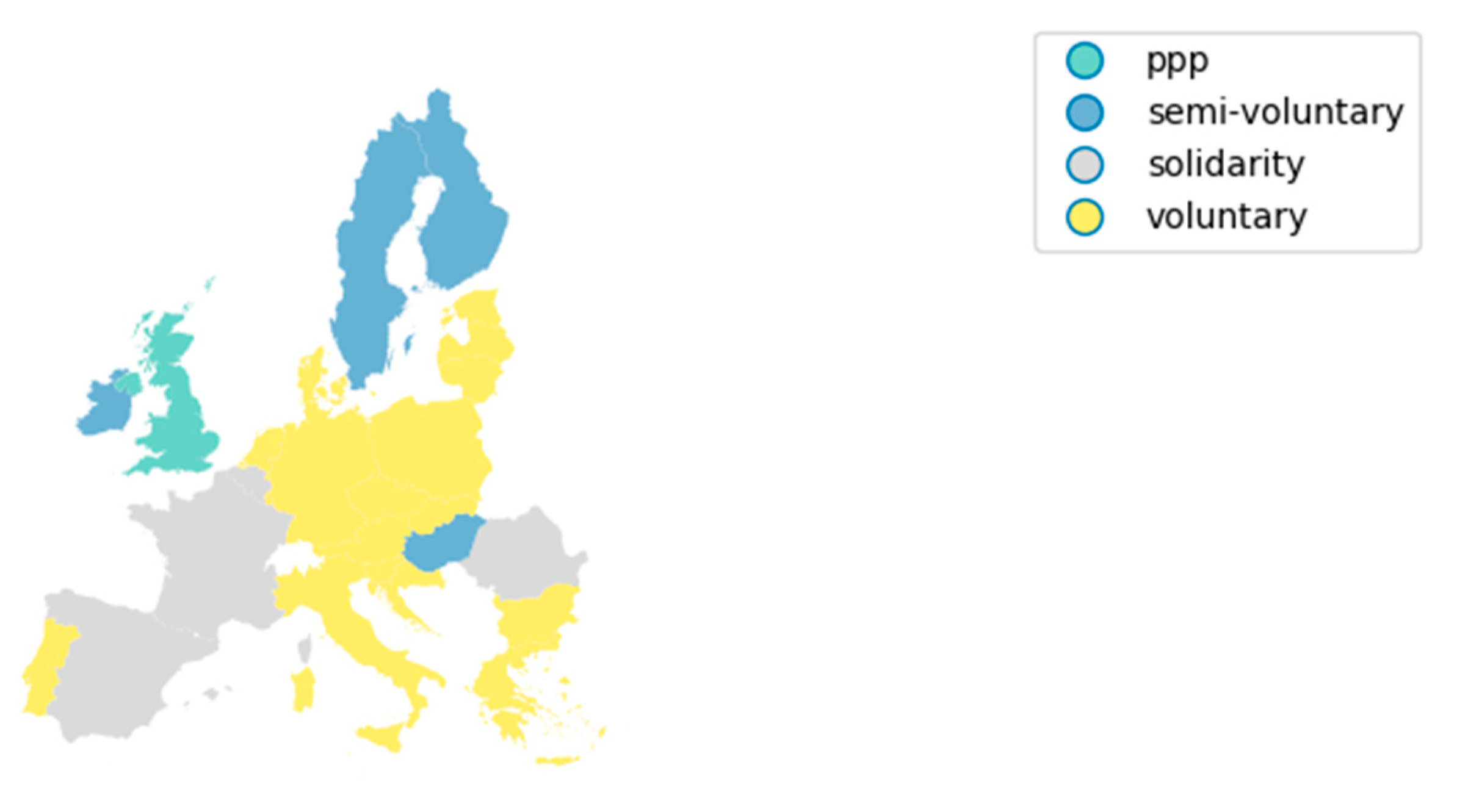

Appendix D. Categorization of Current Insurance Market Structures in the EU

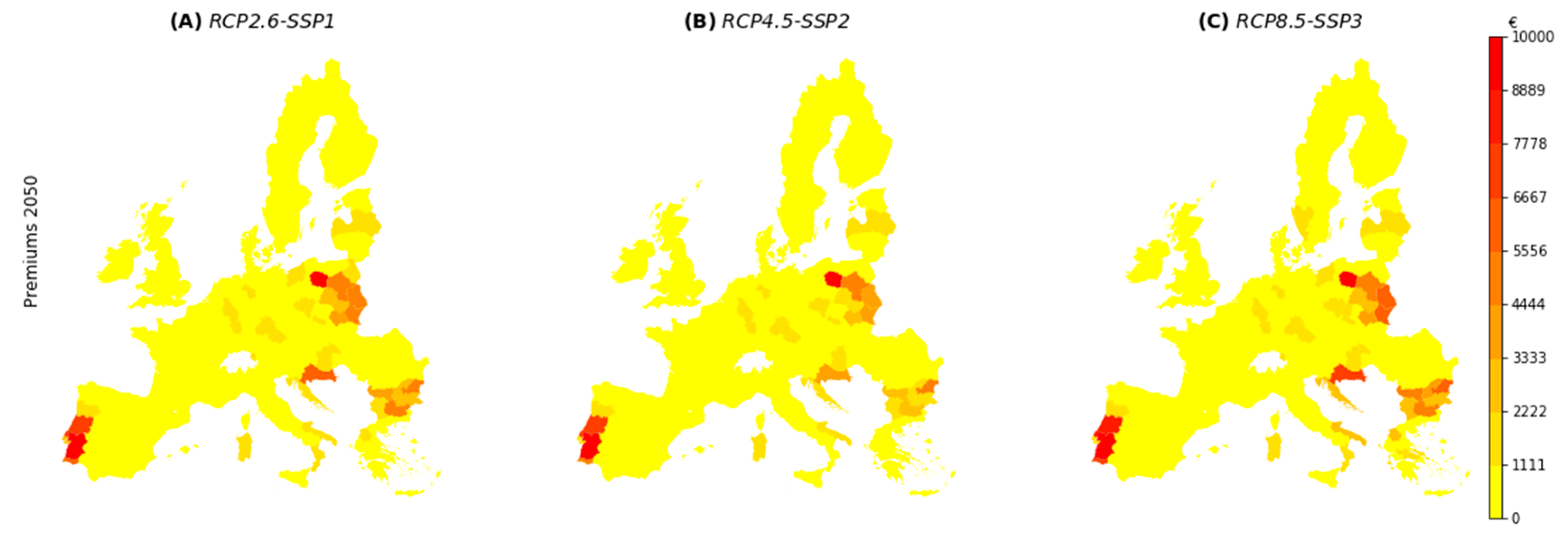

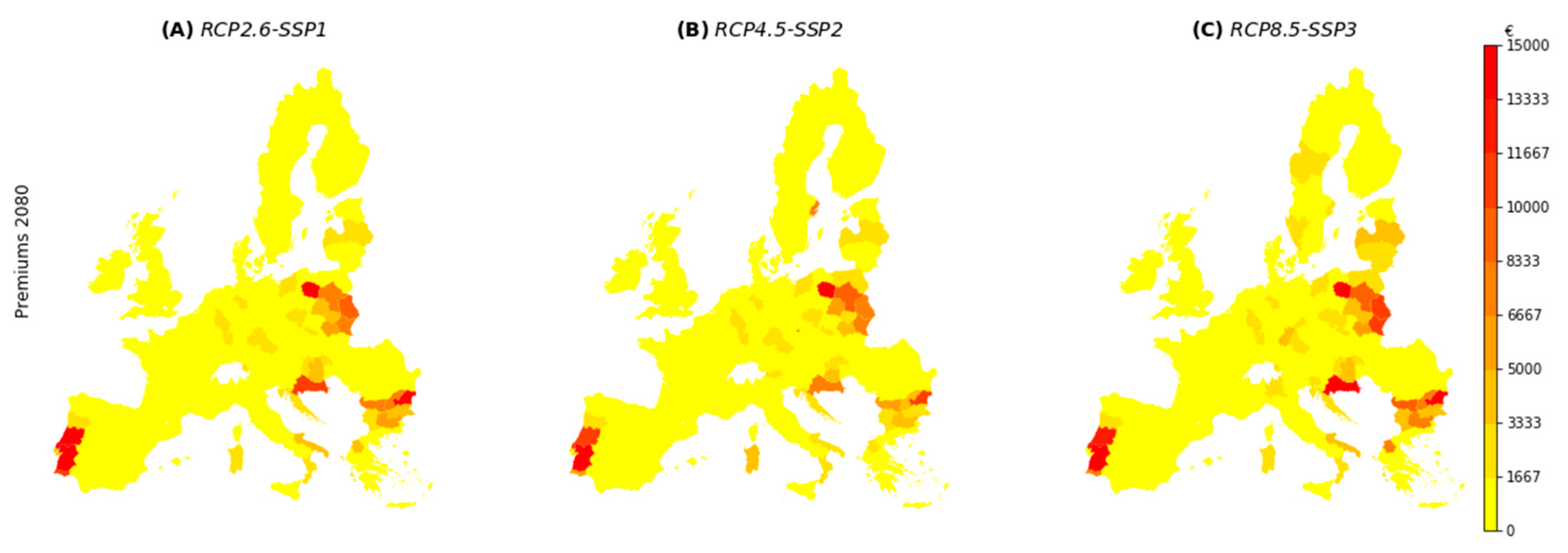

Appendix E. Flood Insurance Premiums in the Baseline and Future Projections Using Multiple Scenarios

Appendix F. Map of EU Countries and the UK

Appendix G. List of Variables and Their Definitions

| - Final premium faced by individual household i in region j at time t. | |

| - Flood occurrence probability. | |

| - Expected flood damage. | |

| - Deductible. | |

| - Cost-loading factor for the primary insurer. | |

| - Risk aversion coefficient of the primary insurers and reinsurers. | |

| - The volatility of flood damage within a quantile range that is considered insurable. | |

| - Cost-loading factor for private reinsurers. | |

| - Expected flood damage that is transferred from insurers to reinsurers. | |

| - Deductible set by reinsurers for primary insurers. | |

| - Premium discount that is determined by the implementation of risk reduction measures. | |

| - Maximum flood occurrence probability considered by households. This is determined by where is the regional flood protection standard, and is a distribution of subjective flood occurrence probabilities. | |

| - Wealth of individual i in region j at time t. | |

| - Flood impact misperception parameter. |

References

- Field, C.B.; Barros, V.; Stocker, T.F.; Dahe, Q.; Jon Dokken, D.; Ebi, K.L.; Mastrandrea, M.D.; Mach, K.J.; Plattner, G.K.; Allen, S.K.; et al. Managing the Risks of Extreme Events and Disasters to Advance Climate Change Adaptation: Special Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK, 2012; ISBN 9781139177245. [Google Scholar]

- AON. Weather, Climate & Catastrophe Insight: 2019 Annual Report. 2020. Available online: https://www.aon.com/global-weather-catastrophe-natural-disasters-costs-climate-change-2019-annual-report/index.html (accessed on 11 May 2020).

- UNISDR; CRED. The Human Cost of Weather-Related Disasters 1995–2015; UNISDR: Geneva, Switzerland, 2015. [Google Scholar] [CrossRef]

- Mirza, M.M.Q. Climate change and extreme weather events: Can developing countries adapt? Clim. Policy 2003, 3, 233–248. [Google Scholar] [CrossRef]

- Kammerbauer, M.; Wamsler, C. Social inequality and marginalization in post-disaster recovery: Challenging the consensus? Int. J. Disaster Risk Reduct. 2017, 24, 411–418. [Google Scholar] [CrossRef]

- Botzen, W.J.W.; van den Bergh, J.C.J.M. Insurance against climate change and flooding in the Netherlands: Present, future, and comparison with other countries. Risk Anal. 2008, 28, 413–426. [Google Scholar] [CrossRef] [PubMed]

- Kousky, C.; Kunreuther, H. Addressing Affordability in the National Flood Insurance Program. J. Extrem. Events 2014, 1, 1450001. [Google Scholar] [CrossRef]

- Yiannakoulias, N.; Darlington, J.C.; Elshorbagy, A.; Raja, B. Meta-analysis based predictions of flood insurance and flood vulnerability patterns in Calgary, Alberta. Appl. Geogr. 2018, 96, 41–50. [Google Scholar] [CrossRef]

- Kunreuther, H. The Role of Insurance in Reducing Losses from Extreme Events: The Need for Public-Private Partnerships. Geneva Pap. Risk Insur. Issues Pract. 2015, 40, 741–762. [Google Scholar] [CrossRef]

- Hudson, P.; Botzen, W.J.W.; Czajkowski, J.; Kreibich, H. Moral hazard in natural disaster insurance markets: Empirical evidence from Germany and the United States. Land Econ. 2017, 93, 179–208. [Google Scholar] [CrossRef]

- Grossi, P.; Kunreuther, H.; Windeler, D. An Introduction to Catastrophe Models and Insurance. In Catastrophe Modeling: A New Approach to Managing Risk; Springer: Boston, MA, USA, 2006. [Google Scholar] [CrossRef]

- Kousky, C. Financing Flood Losses: A Discussion of the National Flood Insurance Program. Risk Manag. Insur. Rev. 2018, 21, 11–32. [Google Scholar] [CrossRef]

- Nance, E. Exploring the impacts of flood insurance reform on vulnerable communities. Int. J. Disaster Risk Reduct. 2015, 13, 20–36. [Google Scholar] [CrossRef]

- Roder, G.; Hudson, P.; Tarolli, P. Flood risk perceptions and the willingness to pay for flood insurance in the Veneto region of Italy. Int. J. Disaster Risk Reduct. 2019, 37, 101172. [Google Scholar] [CrossRef]

- Kunreuther, H.; Pauly, M. Neglecting disaster: Why don’t people insure against large losses? J. Risk Uncertain. 2004, 28, 5–21. [Google Scholar] [CrossRef]

- Unterberger, C.; Hudson, P.; Botzen, W.J.W.; Schroeer, K.; Steininger, K.W. Future Public Sector Flood Risk and Risk Sharing Arrangements: An Assessment for Austria. Ecol. Econ. 2019, 156, 153–163. [Google Scholar] [CrossRef]

- Botzen, W.J.W.; Van Den Bergh, J.C.J.M. Monetary valuation of insurance against flood risk under climate change. Int. Econ. Rev. 2012, 53, 1005–1026. [Google Scholar] [CrossRef]

- Cremades, R.; Surminski, S.; Máñez Costa, M.; Hudson, P.; Shrivastava, P.; Gascoigne, J. Using the adaptive cycle in climate-risk insurance to design resilient futures. Nat. Clim. Chang. 2018, 8, 4–7. [Google Scholar] [CrossRef]

- Van Ginkel, K.C.H.; Botzen, W.J.W.; Haasnoot, M.; Bachner, G.; Steininger, K.W.; Hinkel, J.; Watkiss, P.; Boere, E.; Jeuken, A.; De Murieta, E.S.; et al. Climate change induced socio-economic tipping points: Review and stakeholder consultation for policy relevant research. Environ. Res. Lett. 2020, 15, 023001. [Google Scholar] [CrossRef] [Green Version]

- Polhill, J.G.; Filatova, T.; Schlüter, M.; Voinov, A. Modelling systemic change in coupled socio-environmental systems. Environ. Model. Softw. 2016, 75, 318–332. [Google Scholar] [CrossRef]

- Penning-Rowsell, E.C.; Priest, S.; Johnson, C. The evolution of UK flood insurance: Incremental change over six decades. Int. J. Water Resour. Dev. 2014, 30, 694–713. [Google Scholar] [CrossRef]

- Kessler, R.C.; Galea, S.; Gruber, M.J.; Sampson, N.A.; Ursano, R.J.; Wessely, S. Trends in mental illness and suicidality after Hurricane Katrina. Mol. Psychiatry 2008, 13, 374–384. [Google Scholar] [CrossRef] [Green Version]

- Cashell, B.; Labonte, M. The Macroeconomic Effects of Hurricane Katrina. Available online: https://digital.library.unt.edu/ark:/67531/metacrs7648/m1/1/high_res_d/RS22260_2005Sep13.pdf (accessed on 25 August 2020).

- Fussell, E.; Sastry, N.; Vanlandingham, M. Race, socioeconomic status, and return migration to New Orleans after Hurricane Katrina. Popul. Environ. 2010, 31, 20–42. [Google Scholar] [CrossRef] [Green Version]

- Paudel, Y.; Botzen, W.J.W.; Aerts, J.C.J.H.; Dijkstra, T.K. Risk allocation in a public-private catastrophe insurance system: An actuarial analysis of deductibles, stop-loss, and premiums. J. Flood Risk Manag. 2015, 8, 116–134. [Google Scholar] [CrossRef]

- Hudson, P.; Botzen, W.J.W.; Aerts, J.C.J.H. Flood insurance arrangements in the European Union for future flood risk under climate and socioeconomic change. Glob. Environ. Chang. 2019, 58, 101966. [Google Scholar] [CrossRef] [Green Version]

- Ward, P.J.; Jongman, B.; Aerts, J.C.J.H.; Bates, P.D.; Botzen, W.J.W.; DIaz Loaiza, A.; Hallegatte, S.; Kind, J.M.; Kwadijk, J.; Scussolini, P.; et al. A global framework for future costs and benefits of river-flood protection in urban areas. Nat. Clim. Chang. 2017, 7, 642–646. [Google Scholar] [CrossRef]

- Winsemius, H.C.; Aerts, J.C.J.H.; Van Beek, L.P.H.; Bierkens, M.F.P.; Bouwman, A.; Jongman, B.; Kwadijk, J.C.J.; Ligtvoet, W.; Lucas, P.L.; Van Vuuren, D.P.; et al. Global drivers of future river flood risk. Nat. Clim. Chang. 2016, 6, 381–385. [Google Scholar] [CrossRef]

- Van der Knijff, J.M.; Younis, J.; de Roo, A.P.J. LISFLOOD: A GIS-based distributed model for river basin scale water balance and flood simulation. Int. J. Geogr. Inf. Sci. 2010, 24, 189–212. [Google Scholar] [CrossRef]

- Van Vuuren, D.P.; Edmonds, J.; Kainuma, M.; Riahi, K.; Thomson, A.; Hibbard, K.; Hurtt, G.C.; Kram, T.; Krey, V.; Lamarque, J.F.; et al. The representative concentration pathways: An overview. Clim. Chang. 2011, 109, 5. [Google Scholar] [CrossRef]

- Van Beek, L.P.H.; Wada, Y.; Bierkens, M.F.P. Global monthly water stress: 1. Water balance and water availability. Water Resour. Res. 2011, 47. [Google Scholar] [CrossRef]

- Van Beek, L.P.H.; Bierkens, M.F.P. The Global Hydrological Model PCR-GLOBWB: Conceptualization, Parameterization and Verification; Report Department of Physical Geography, Utrecht University: Utrecht, The Netherlands, 2009; Available online: http://vanbeek.geo.uu.nl/suppinfo/vanbeekbierkens2009.pdf (accessed on 11 May 2020).

- Weedon, G.P.; Gomes, S.; Viterbo, P.; Shuttleworth, W.J.; Blyth, E.; Österle, H.; Adam, J.C.; Bellouin, N.; Boucher, O.; Best, M. Creation of the WATCH Forcing Data and Its Use to Assess Global and Regional Reference Crop Evaporation over Land during the Twentieth Century. J. Hydrometeorol. 2011, 12, 823–848. [Google Scholar] [CrossRef] [Green Version]

- Taylor, K.E.; Stouffer, R.J.; Meehl, G.A. An overview of CMIP5 and the experiment design. Bull. Am. Meteorol. Soc. 2012, 93, 485–498. [Google Scholar] [CrossRef] [Green Version]

- Hempel, S.; Frieler, K.; Warszawski, L.; Schewe, J.; Piontek, F. A trend-preserving bias correction—The ISI-MIP approach. Earth Syst. Dyn. 2013, 4, 49–92. [Google Scholar] [CrossRef]

- UNISDR Proposed Updated Terminology on Disaster Risk Reduction: A Technical Review. Community Environ. Disaster Risk Manag. 2015. [CrossRef]

- Klein Goldewijk, K.; Beusen, A.; Van Drecht, G.; De Vos, M. The HYDE 3.1 spatially explicit database of human-induced global land-use change over the past 12,000 years. Glob. Ecol. Biogeogr. 2011, 20, 73–86. [Google Scholar] [CrossRef]

- Van Huijstee, J.; Van Bemmel, B.; Bouwman, A.; Van Rijn, F. Towards an Urban Preview: Modelling Future Urban Growth with 2UP Background Report. 2018. Available online: https://www.pbl.nl/en/publications/towards-an-urban-preview (accessed on 11 May 2020).

- Eurostat Household Composition Statistics. Available online: https://ec.europa.eu/eurostat/statistics-explained/pdfscache/29071.pdf (accessed on 5 October 2020).

- Van Vuuren, D.P.; Lucas, P.L.; Hilderink, H. Downscaling drivers of global environmental change: Enabling use of global SRES scenarios at the national and grid levels. Glob. Environ. Chang. 2007, 17, 114–130. [Google Scholar] [CrossRef] [Green Version]

- Riahi, K.; van Vuuren, D.P.; Kriegler, E.; Edmonds, J.; O’Neill, B.C.; Fujimori, S.; Bauer, N.; Calvin, K.; Dellink, R.; Fricko, O.; et al. The Shared Socioeconomic Pathways and their energy, land use, and greenhouse gas emissions implications: An overview. Glob. Environ. Chang. 2017, 42, 153–168. [Google Scholar] [CrossRef] [Green Version]

- Huizinga, J.; de Meol, H.; Szewczyk, W. Global Flood Depth-Damage Functions: Methodology and the Database with Guidelines; EU Publications Office of the European Union: Luxembourg, 2017; ISBN 9789279677816. [Google Scholar] [CrossRef]

- Rojas, R.; Feyen, L.; Bianchi, A.; Dosio, A. Assessment of future flood hazard in Europe using a large ensemble of bias-corrected regional climate simulations. J. Geophys. Res. Atmos. 2012, 117. [Google Scholar] [CrossRef]

- Scussolini, P.; Aerts, J.C.J.H.; Jongman, B.; Bouwer, L.M.; Winsemius, H.C.; De Moel, H.; Ward, P.J. FLOPROS: An evolving global database of flood protection standards. Nat. Hazards Earth Syst. Sci. 2016, 16. [Google Scholar] [CrossRef] [Green Version]

- Dixon, L.; Clancy, N.; Seabury, S.; Overton, A. The National Flood Insurance Program’s Market Penetration Rate: Estimates and Policy Implications; RAND Corporation: Santa Monica, CA, USA, 2018. [Google Scholar] [CrossRef] [Green Version]

- Kriegler, E.; Bauer, N.; Popp, A.; Humpenöder, F.; Leimbach, M.; Strefler, J.; Baumstark, L.; Bodirsky, B.L.; Hilaire, J.; Klein, D.; et al. Fossil-fueled development (SSP5): An energy and resource intensive scenario for the 21st century. Glob. Environ. Chang. 2017, 42, 297–315. [Google Scholar] [CrossRef] [Green Version]

- Hope, A.P.; Salawitch, R.J.; Canty, T.P.; Tribett, W.R.; Bennett, B.F. Paris INDCs. In Paris Climate Agreement: Beacon of Hope; Springer International Publishing: New York, NY, USA, 2017. [Google Scholar] [CrossRef] [Green Version]

- Paudel, Y.; Botzen, W.J.W.; Aerts, J.C.J.H. Estimation of insurance premiums for coverage against natural disaster risk: An application of Bayesian Inference. Nat. Hazards Earth Syst. Sci. 2013, 13. [Google Scholar] [CrossRef] [Green Version]

- Mysiak, J.; Dionisio Pérez-Blanco, C. Partnerships for disaster risk insurance in the EU. Nat. Hazards Earth Syst. Sci. 2016, 16, 2403. [Google Scholar] [CrossRef] [Green Version]

- Kunreuther, H.; Michel-Kerjan, E.; Ranger, N. Insuring future climate catastrophes. Clim. Chang. 2013, 118, 339–354. [Google Scholar] [CrossRef] [Green Version]

- Hudson, P.; Botzen, W.J.W.; Feyen, L.; Aerts, J.C.J.H. Incentivising flood risk adaptation through risk based insurance premiums: Trade-offs between affordability and risk reduction. Ecol. Econ. 2016, 125, 1–13. [Google Scholar] [CrossRef]

- Savage, L.J. The Foundation of Statistics; John Wiley: New York, NY, USA, 1954. [Google Scholar]

- Eurostat Net Financial Wealth of Households Fell during the Opening Phase of the Financial Crisis in the EU. Available online: https://ec.europa.eu/eurostat/documents/3433488/5565228/KS-SF-10-033-EN.PDF/9b1042cd-4f2d-4984-9afe-aef8e5be3a5c?version=1.0 (accessed on 5 October 2020).

- GdV Naturgefahrenreport 2013: Die Schaden-Chronik der Deutschen Versicherer [Natural Hazard Report 2013: Chronicle of Damages by the German Insurance Companies]. 2013. Available online: https://www.flussgebiete.nrw.de/naturgefahrenreport-2013-die-schaden-chronik-der-deutschen-versicherer-mit-zahlen-stimmen-und-7211 (accessed on 11 May 2020).

- Maslow, A.H. A Theory of Human Motivation Theory. Psychol. Rev. 1943, 50, 370–396. [Google Scholar] [CrossRef] [Green Version]

- Bundorf, M.K.; Pauly, M.V. Is health insurance affordable for the uninsured? J. Health Econ. 2006, 25, 650–673. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Saenz, C. What is Affordable Health Insurance?: The Reasonable Tradeoff Account of Affordability. Kennedy Inst. Ethics J. 2009, 19, 401–414. [Google Scholar] [CrossRef] [PubMed]

- Hudson, P. A comparison of definitions of affordability for flood risk adaption measures: A case study of current and future risk-based flood insurance premiums in Europe. Mitig. Adapt. Strateg. Glob. Chang. 2018, 23, 1019–1038. [Google Scholar] [CrossRef]

- Zhao, W.; Kunreuther, H.; Czajkowski, J. Affordability of the National Flood Insurance Program: Application to Charleston County, South Carolina. Nat. Hazards Rev. 2015, 17, 04015020. [Google Scholar] [CrossRef] [Green Version]

- Eurostat Smarter, Greener, More Inclusive?—Indicators to support the Europe 2020 Strategy; Publications Office of the European Union: Luxembourg, 2016. [CrossRef]

- UNISDR. Chart of the Sendai Framework for Disaster Risk Reduction. Available online: https://www.unisdr.org/files/44983_sendaiframeworksimplifiedchart.pdf (accessed on 11 May 2020).

- Alfieri, L.; Feyen, L.; Dottori, F.; Bianchi, A. Ensemble flood risk assessment in Europe under high end climate scenarios. Glob. Environ. Chang. 2015, 35, 199–212. [Google Scholar] [CrossRef]

- Maccaferri, S.; Cariboni, F.; Campolongo, F. Natural Catastrophes: Risk relevance and Insurance Coverage in the EU; Publications Office of the European Union: Luxembourg, 2012; ISBN 9789279218439. [Google Scholar] [CrossRef]

- Michel-Kerjan, E.; Kunreuther, H. Redesigning flood insurance. Science 2011, 333, 408–409. [Google Scholar] [CrossRef]

- Arnell, N.W.; Lloyd-Hughes, B. The global-scale impacts of climate change on water resources and flooding under new climate and socio-economic scenarios. Clim. Chang. 2014, 122, 127–140. [Google Scholar] [CrossRef] [Green Version]

- Hirabayashi, Y.; Mahendran, R.; Koirala, S.; Konoshima, L.; Yamazaki, D.; Watanabe, S.; Kim, H.; Kanae, S. Global flood risk under climate change. Nat. Clim. Chang. 2013, 3, 816–821. [Google Scholar] [CrossRef]

- Haer, T.; Botzen, W.J.W.; de Moel, H.; Aerts, J.C.J.H. Integrating Household Risk Mitigation Behavior in Flood Risk Analysis: An Agent-Based Model Approach. Risk Anal. 2017, 37, 1977–1992. [Google Scholar] [CrossRef] [Green Version]

- Yang, S.; Zhao, Y.; Erdem, T.; Zhao, Y. Modeling the intrahousehold behavioral interaction. J. Mark. Res. 2010, 47, 470–484. [Google Scholar] [CrossRef] [Green Version]

- Paudel, Y. A Comparative study of public-private catastrophe insurance systems: Lessons from current practices. Geneva Pap. Risk Insur. Issues Pract. 2012, 37, 257–285. [Google Scholar] [CrossRef] [Green Version]

- Florida Hurricane Catastrophe Fund: Fiscal Year 2013–2014 Annual Report. 2014. Available online: https://www.sbafla.com/fhcf/Portals/FHCF/Content/Reports/Annual/2013_2014_FHCF_AnnualReportFinal.pdf?ver=2016-06-08-121815-567 (accessed on 11 May 2020).

- FLOOD RE. Annual Report and Financial Statements. 2019. Available online: https://www.floodre.co.uk/wp-content/uploads/Flood-Re-Annual-Report-2019.pdf (accessed on 10 August 2019).

- Le Den, X.; Persson, M.; Benoist, A.; Hudson, P.; de Ruiter, M.; de Ruig, L.; Kuik, O. Insurance of Weather and Climate-Related Disaster Risk: Inventory and Analysis of Mechanism to Support Damage Prevention in the EU; Publications Office of the European Union: Luxembourg, 2017; ISBN 9789279731730. [Google Scholar] [CrossRef]

- Atreya, A.; Hanger, S.; Kunreuther, H.; Linnerooth-Bayer, J.; Michel-Kerjan, E. A Comparison of Residential Flood Insurance Markets in 25 Countries. 2015. Available online: https://riskcenter.wharton.upenn.edu/wp-content/uploads/2020/03/WP2015_FloodInsurancePrograms-25Countries_2015-06-28.pdf (accessed on 25 August 2020).

- Thieken, A.H.; Bessel, T.; Kienzler, S.; Kreibich, H.; Müller, M.; Pisi, S.; Schröter, K. The flood of June 2013 in Germany: How much do we know about its impacts? Nat. Hazards Earth Syst. Sci. 2016, 16, 1519–1540. [Google Scholar] [CrossRef] [Green Version]

- FEMA. An Affordability Framework for the National Flood Insurance Program; 2018. Available online: https://www.fema.gov/media-library/assets/documents/163171 (accessed on 11 May 2020).

- Kousky, C.; Cooke, R. Explaining the failure to insure catastrophic risks. Geneva Pap. Risk Insur. Issues Pract. 2012, 37, 206–227. [Google Scholar] [CrossRef] [Green Version]

- Noonan, D.S.; Sadiq, A.A.A. Flood Risk Management: Exploring the Impacts of the Community Rating System Program on Poverty and Income Inequality. Risk Anal. 2018, 38, 489–503. [Google Scholar] [CrossRef] [Green Version]

- Aerts, J.C.J.H.; Botzen, W.J.W.; Emanuel, K.; Lin, N.; De Moel, H.; Michel-Kerjan, E.O. Evaluating flood resilience strategies for coastal megacities. Science 2014, 344, 473–475. [Google Scholar] [CrossRef]

- Hoffmann, R.; Dimitrova, A.; Muttarak, R.; Crespo Cuaresma, J.; Peisker, J. A meta-analysis of country-level studies on environmental change and migration. Nat. Clim. Chang. 2020, 1–9. [Google Scholar] [CrossRef]

- Alfieri, L.; Feyen, L.; Di Baldassarre, G. Increasing flood risk under climate change: A pan-European assessment of the benefits of four adaptation strategies. Clim. Chang. 2016, 136, 507–521. [Google Scholar] [CrossRef] [Green Version]

- Tesselaar, M.; Botzen, W.J.W.; Aerts, J.C.J.H. Impacts of climate change and remote natural catastrophes on EU flood insurance markets: An analysis of soft and hard reinsurance markets for flood coverage. Atmosphere 2020, 11, 146. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Structure Group | Sector Covering Flood Risk | Common Market Features | Countries Allocated |

|---|---|---|---|

| M1. Solidarity public structure | Public |

| France; Belgium; Spain; Romania |

| M2. Semi-voluntary private market | Private |

| Sweden; Ireland; Hungary; Finland |

| M3. Voluntary private market | Private |

| Austria; Netherlands; Germany; Italy; Portugal; Luxembourg; Greece; Poland; Czech Republic; Slovakia; Slovenia; Croatia; Bulgaria; Latvia; Estonia; Lithuania |

| M4. Voluntary PPP market | Public-Private |

| Hypothetical market structure |

| M5. Semi-voluntary PPP market | Public-Private |

| Hypothetical market structure |

| M6. Public-Private Partnership (PPP) market | Public-Private |

| UK |

| RCP4.5-SSP2 | RCP8.5-SSP3 | RCP2.6-SSP1 | RCP8.5-SSP5 | RCP6-SSP2 | RCP2.6-SSP2 |

|---|---|---|---|---|---|

| Croatia (1/2) | Croatia (1/2) | Croatia (1/2) | Croatia (1/2) | Croatia (1/2) | Croatia (1/2) |

| Bulgaria (1/6) | Bulgaria (1/6) | Bulgaria (1/6) | Bulgaria (1/6) | Bulgaria (1/6) | Bulgaria (1/6) |

| Poland (6/16) | Poland (6/16) | Poland (2/16) | Poland (6/16) | Poland (5/16) | Poland (5/16) |

| Portugal (1/5) | Portugal (1/5) | Portugal (1/5) | Portugal (1/5) | Portugal (1/5) | Portugal (1/5) |

| Czech (1/8) | Czech (1/8) | ||||

| Greece (1/13) | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tesselaar, M.; Botzen, W.J.W.; Haer, T.; Hudson, P.; Tiggeloven, T.; Aerts, J.C.J.H. Regional Inequalities in Flood Insurance Affordability and Uptake under Climate Change. Sustainability 2020, 12, 8734. https://0-doi-org.brum.beds.ac.uk/10.3390/su12208734

Tesselaar M, Botzen WJW, Haer T, Hudson P, Tiggeloven T, Aerts JCJH. Regional Inequalities in Flood Insurance Affordability and Uptake under Climate Change. Sustainability. 2020; 12(20):8734. https://0-doi-org.brum.beds.ac.uk/10.3390/su12208734

Chicago/Turabian StyleTesselaar, Max, W. J. Wouter Botzen, Toon Haer, Paul Hudson, Timothy Tiggeloven, and Jeroen C. J. H. Aerts. 2020. "Regional Inequalities in Flood Insurance Affordability and Uptake under Climate Change" Sustainability 12, no. 20: 8734. https://0-doi-org.brum.beds.ac.uk/10.3390/su12208734