Sustainability of the Energy Sector in Jordan: Challenges and Opportunities

1

Department of Logistics, German Jordanian University, Amman Madaba Street, Amman 11180, Jordan

2

Department of Politics and International Relations (DPIR), University of Oxford, Manor Road, Oxford OX1 3UQ, UK

3

Department of Economics, Yarmouk University, Difaa Al Madani Street, Irbid 21163, Jordan

*

Author to whom correspondence should be addressed.

Sustainability 2020, 12(24), 10465; https://0-doi-org.brum.beds.ac.uk/10.3390/su122410465

Submission received: 9 November 2020

/

Revised: 26 November 2020

/

Accepted: 7 December 2020

/

Published: 14 December 2020

(This article belongs to the Special Issue Natural Resources Management and Conflicts in the Context of Sustainability Transformation)

Abstract

:The acceleration of economic development and rising standards of living have made energy security a top priority for policy makers worldwide. The issue of securing energy is particularly challenging for Jordan, which suffers from scarcity of natural resources, combined with the regional instability and conflicts. Based on desk research and on experts’ interviews, this study discusses the status quo of the energy sector in Jordan, its main challenges, and future aspirations. It thus contributes to the debate on how Jordan can ensure environmental, economic, social, and political sustainability of its energy sector. Jordan’s energy security has been historically linked to its relations with the neighboring countries and thus vulnerable to external shocks and outside political events. Notwithstanding reform efforts to reduce dependency from imports and some progress in diversifying the energy mix, energy security remains critical: the country imports around 94% of its energy, which represents approximately 10% of GDP. The growing domestic demand, which increases at a yearly rate of 3%, further adds to the pressure to envision strategies towards a more sustainable energy sector. These strategies will need to include investment in renewable energy, the reduction of energy consumption via increasing energy efficiency, and also synergic agreements with other countries. The interviewed experts highlighted the importance of governance for the successful implementation of these strategies. The creation of an enabling environment should go hand in hand with the involvement of all key stakeholders from energy and related sectors, into the development of a future vision of a sustainable energy sector.

1. Introduction

Securing and ensuring energy is a top priority for governments across the world, as energy is a key driver of economic development, allowing, for instance, water to be pumped throughout a country, industry to operate, transportation to work, and other key services to run. The International Energy Agency (IEA) defines energy security as “the uninterrupted availability of energy sources at an affordable price” [1] (p. 13). The topic has become central to the policy debate since the oil crisis of the 1970s, which revealed the full consequences of “the gradual shift from European coal and American domestic oil to Western reliance on Middle East oil” [2] (p. 112), so that the links between energy, security, and foreign policy became clear. Since then and until recently, the concept of energy security was mostly related to securing access to oil and other fossil fuels [3]. Technological progress, increased diversification of the energy markets, climate change awareness, and modified global equilibria call for a more comprehensive operational definition of energy security. Accordingly, it is now widely agreed in the literature that energy security “is a complex concept with multi-layered dimensions that interconnects different subject areas” [4] (p. 101).

This study investigates energy security with specific reference to the case of Jordan. The issue of securing energy is particularly challenging for Jordan, which suffers from scarcity of fossil fuel, combined with the regional instability. Jordan’s energy mix is dominated by fossil fuel [5]. Domestic demand for energy is increasing at a sustained pace [6] and the country imports around 94% of its energy supply [7]. This also makes the Jordanian energy sector particularly sensitive to regional conflicts [8]. Recently, regional instability has also been causing intermittency of supply and price fluctuations (which was the case of liquified gas imports from Egypt, disrupted since 2011) and has induced the authorities to rethink the approach to energy policy, exploring the feasibility of alternative sources of energy such as oil shale [7] and nuclear energy [9], testing new international agreements (e.g., the construction of an electric transmission line between Jordan and Saudi Arabia), and increasing the focus on renewable energy [7,10].

As discussed in Section 4, the literature on the energy sector in Jordan highlights the potential of Jordan as energy producer for non-conventional and renewable energy [11,12,13], but also highlights that this potential is widely unexploited [6,14,15]. It also discusses international agreements [5] and reflects on their possible implications for the overall political stability of the region [11,16,17]. However, the debate on the energy sector in Jordan is still lacking a full understanding of the factors and the conflicts undermining this potential. This study therefore aims at complementing the literature in this regard, enriching it with an insiders’ view on the energy sector, collected via experts’ interviews.

The present study contributes to the literature on energy security and sustainability in Jordan by contextualizing the concept of energy security within its environmental, economic, social, and political sustainability, and by combining the analysis of energy policies and strategies with interviews of key informants to better understand background stories on how and why certain strategies and decisions have been taken and adopted. This study aims to answer the following overarching research question: how can Jordan move towards a sustainable energy security sector? Hereby, the focus will be put on identifying the main challenges and opportunities towards the transition, but also on understanding potential conflicts hampering the settlement towards a more sustainable security of energy. The study aims at providing answers to this question by reviewing previous studies and existing evidence on the topic, identifying and collecting lessons to achieve sustainable energy security, and testing their feasibility with key experts, also in light of current strategies and policy options envisioned. Therefore, starting from a historic perspective on Jordan’s energy security and linking it with political and regional events, the present study reviews the main trends and challenges of the Jordanian energy market, discusses current energy policy, and addresses the debate on policy options envisioned.

After this introduction, the conceptual framework and the methodology underpinning the study are derived and contextualized within related literature. The conceptual framework will be applied to Jordan’s energy sector status before providing the results of the research in terms of interviews and findings. Main results and concluding remarks are then presented.

2. Sustainable Energy Security: Theoretical Background and Conceptual Framework

Trying to define security in relation to energy, it emerges that “the concept of energy security is inherently slippery because it is polysemic in nature, capable of holding multiple dimensions and taking on different specificities depending on the country (or continent), timeframe or energy source to which it is applied” [18] (p. 887). A basic differentiation of the energy security concept is based on the temporal perspective. Hereby, long-term energy security has to essentially address the investments to grant a supply of energy in line with economic and environmental needs. Short-term energy security is related to promptly reacting to sudden changes in the energy markets. Based on this differentiation, Kisel et al. [19] developed a framework according to which energy security consists of four layers: the layer of short-term operational resilience, which characterizes the short-term dimension of the concept, and the layers of technical vulnerability, economic dependence, and political affectability, characterizing its long-term dimensions. Even though this framework is useful for a technical assessment of energy security, it fails to capture some elements needed to characterize wider social and political implications of energy security. As an example, environmental considerations are only encompassed within the short-term layer of operational resilience. Other definitions are based on the interplay between elements of absolute and relative energy security. In this view, absolute security is linked to availability [20] and adequacy of capacity [21], whereas relative security points to affordability and economic sustainability [18].

Screening the literature, it emerges that the concept of sustainability is very often present when it comes to (long-term) energy security. Sustainability is “the quality of being able to continue over a period of time” [22]. The concept of sustainability has been widely used in environmental sciences, where the first use was documented in 1713 to discuss the danger of wood overconsumption [23]. It then found applications in economic analysis, notably in Malthus’ theories on population growth, first published in 1798. The concept has since then become part of the scientific debate both in environmental and social sciences to denote situations in which the rate of use of a certain resource does not exceed its regeneration rate [23]. It had a surge in fortune after 1987, when it was linked to development by the World Commission for Environmental Development’s report (WCED). Sustainable development is defined as development “that meets the needs of the present without compromising the ability of future generations to meet their own needs” [24] (p. 15). The recognition of ensuring “the access to affordable, reliable, sustainable, and modern energy for all” among the Sustainable Development Goals [25] (p. 18) reveals how interconnected energy security and sustainable development are. To underline these interlinkages, some analysts prefer to speak of sustainable energy security [26,27].

Linking energy security to sustainability clearly points to the fact that energy security has an impact on the overall sustainability of a system: the sustainability of energy security should be assessed in regard to the supply of energy, to its economic impact (affordability, both in terms of cost and of risk), to the technological possibilities and associated risks, to environmental impact (trade-offs and mitigation possibilities), social acceptance, and geopolitical considerations (also in the sense of military security) [3].

Energy security is among the top priorities of governments worldwide, with energy often being the fuel of economic growth and development. Energy policy, which has been defined as ensuring security, diversity, and sustainability of energy supply at a competitive price [28], is at the core of policy making. Interestingly, definitions of energy policy often borrow from the definition of energy security, making the boundaries between the two concepts blurred and mixing means with ends [29]. From the principles of energy policy, it is possible to derive conceptual frameworks useful for defining energy security. This is the case of the principles inspiring the EU energy policy, which are to “ensure the functioning of the internal energy market and the interconnection of energy networks; Ensure security of energy supply in the EU; Promote energy efficiency and energy saving; Decarbonise the economy and move towards a low-carbon economy in line with the Paris Agreement; Promote the development of new and renewable forms of energy to better align and integrate climate change goals into the new market design; Promote research, innovation and competitiveness” [30] (p. 1). Interestingly, the EU principles drive energy policy towards principles of sustainable energy security rather than only energy security. The principles can be strongly related to the definition by von Hippel et al. [3], as it integrates supply, geopolitical considerations, economic impact, environmental considerations, and technological possibilities of energy security.

For the purpose of this study, this paper adopts and builds on the conceptual framework developed by Von Hippel et al. [3]. This framework identifies sustainable energy security as being formed by the following dimensions: “energy supply; economic; technological; environmental; socio-cultural; and military-security (geopolitical)” [3] (p. 6724). Therefore, when envisioning and planning how to ensure energy security—in this case for Jordan—the mentioned dimensions need to be considered in order to ensure the sustainability of the sector.

Table 1 reflects on the dimensions of energy security considered in this study, on related features and assessment criteria that can be used to capture them, and on important considerations that can be addressed if reflecting on sustainability.

This study discusses potential challenges for Jordan’s energy sector in light of the framework of Table 1. In doing that, it aims at adding to the existing literature by providing a holistic picture of the energy sector in Jordan, enriched and complemented by experts’ interviews as specified in the section on Methodology.

3. Methodology

The methodology used for this study—given the guiding research question and the focus on national policies and strategies—focused on one core method of data collection: semi-structured interviews with key figures (experts and key informants), selected among policy makers, representatives of international organizations, and local academics specialized in energy issues. This method helped in complementing and building on the desk-based review that was conducted for this study of Jordanian policies and strategies on energy released by the relevant governmental institutions in Jordan, reports by international organizations and donors, and academic articles and writings on the topic.

More specifically, the desk-based review was very useful for identifying the relevant strategies and policies, donors’ and international organizations’ suggestions on how to reform, and academic analysis and critiques on the sector. In this sense, the semi-structured interviews were used to complement the review to understand why certain changes happened over time, why different policies and strategies were passed, and the key events that pushed governments to support or abandon plans (for instance the nuclear one). To implement the interviews, the authors conducted semi-structured interviews of selected key informants working in Jordan. The selection of participants was based on the “purposeful sampling” method described by Patton [31]. As noted by Patton, this approach is about “strategically selecting information-rich cases to study, cases that by their nature and substance will illuminate the inquiry question being investigated.” This means selecting individuals that are especially knowledgeable about or experienced with a phenomenon of interest [32]. In particular, “heterogeneity sampling” [33] was used in selecting key informants from different categories representing the sectors involved in the field of inquiry: academia, government, international agencies, research institutes, and the private sector.

A total of 11 experts were interviewed. As presented in Table 2, the sample consisted of four academics, two representatives of international institutions and organizations, and four high-level former or current governmental officials from the Jordanian Ministry of Energy and Mineral Resources, Ministry of Planning and International Cooperation, Ministry of Water and Irrigation, Ministry of Agriculture, and Water Authority of Jordan. The sample is complemented by an informant with a managerial position in an electricity company as representative of the private sector.

The interviews were conducted from September to November 2020. On average, the length of the interviews was between 60 and 75 min and was guided following guidelines on qualitative interviewing by Patton [31]. The interview guide was prepared to ensure that the same basic lines of inquiry were pursued with each person interviewed. Based on the main research question a list of sub-questions was developed and aimed at exploring different angles of the topic. Aspects elicited in the interviews encompassed an outlook on the energy supply in the sense of future perspectives, potential of the energy sector in Jordan, and main challenges to it (economic, technological, environment, socio-cultural, and geopolitical). Governance of the energy sector, existence, feasibility, and potential of regional cooperation were explored too.

The overarching research question was, “how can Jordan move towards a sustainable energy security sector?,” while the sub-research questions, which guided the design of the interviews, were related to the current status and future outlooks of the energy sector in Jordan, challenges and conflicts hindering the sustainability of the energy sector and energy security, governance, and the role and potential of regional cooperation, as presented by Table 3. The first four topics are the main overarching dimensions that were discussed in interviews, while the remaining five (from 5 to 9) focused on specific questions on domains and options related to the energy sector in Jordan.

4. Energy Security in Jordan: A Review of Its Current Status

As it emerges from a brief review of the literature, the research on energy security in Jordan has explored characteristics of the energy market in the country, adoption of renewable energy [6,17,34,35,36], policies to boost it [37,38], and its potential and challenges [13,14,15]. Several contributions are also dealing with the political implications of energy security [39], recommendations [40], and policy options, in particular in relation to cooperation with neighboring countries [5,11,16]. Given the severe water scarcity of the country and the increasing energy demand of the water sector, addressing the water–energy nexus has been also discussed as an important element in achieving sustainability [41,42]. The reliance on imported energy has historically increased the vulnerability of Jordan towards regional events, as “Jordan’s energy landscape has been impacted by relations between and among its Middle Eastern neighbours” [5]. Thus, geopolitics, Jordanian foreign policy, and energy security have been intertwined and interlinked and can serve as a useful lens to understand energy policy in Jordan [39].

4.1. The Energy Market

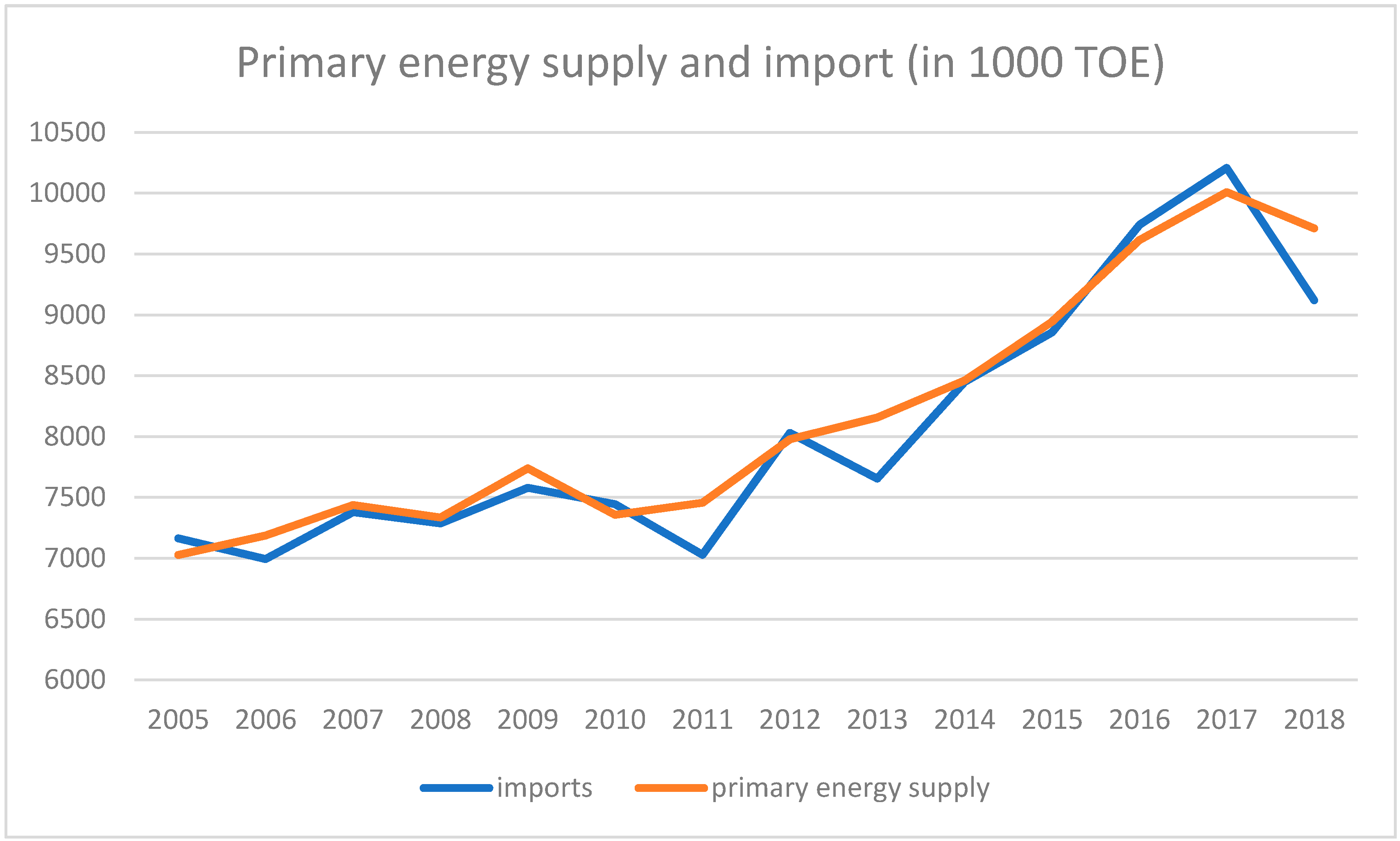

Average real economic growth between 2005 and 2011 was 6% per year and decreased to an average of 2.4% between 2012 and 2018 [43]. Average yearly population growth for the same periods was 4.6% and 3.8%, respectively [43]. On the opposite end, primary energy supply (meaning energy production net of exports, international bunkers, and stock changes) was growing at a moderate rate (1% per year between 2005 and 2011), whereas it registered a clear acceleration after 2012 (average growth between 2012 and 2018 was 3.9% per year) (Figure 1). The consequences of the so-called Arab Spring, the outbreak of the war in Syria, and the inflow of a large number of refugees with their interconnected needs for shelter, electricity, water, and further basic needs have been heavily affecting Jordan and its energy needs. The refugee crisis, together with the interruption of relatively cheap natural gas imports from Egypt, faced Jordan with the urgent need to rethink energy security, and the debate on energy has become one of the top political and economic priorities.

As is evident in Figure 1, most of the energy supply is covered via import. Between 2005 and 2017, the import of energy represented on average 98.7% of primary energy supply. As a result of the efforts in diversifying the sources of energy and of the investment in renewable energy, imports decreased in 2018 to 94% of primary energy supply.

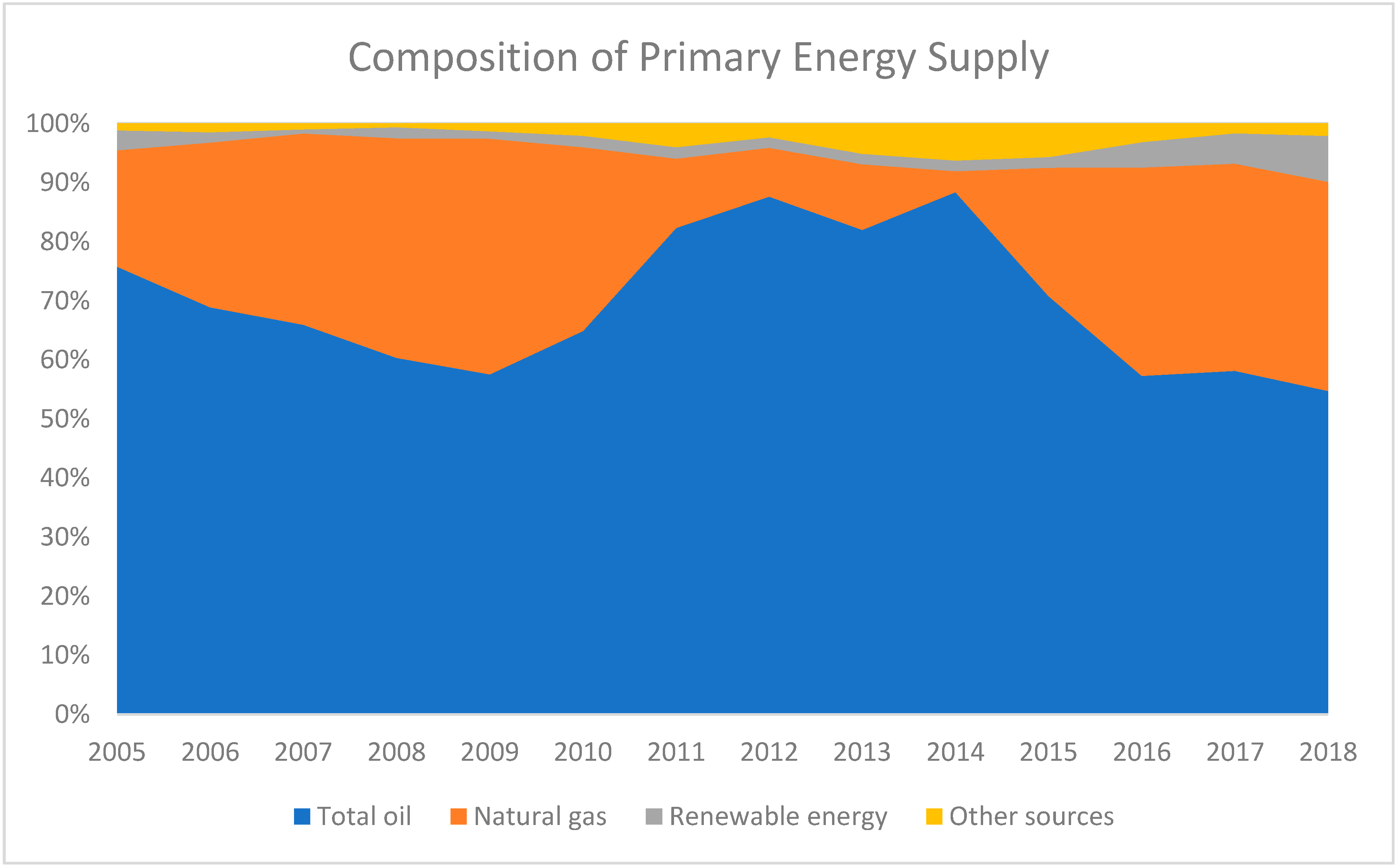

The energy market in Jordan is clearly dominated by oil products, followed by natural gas (Figure 2). Renewable energy, which is mostly represented by solar electricity generation, has been increasing its importance from less than 1% in 2010 [7,44] to reach a share of 7.8% of total primary energy supply in 2018. The exploitation of wind energy is still a new development in Jordan, with the first significant project in this regard launched in 2013 [7,44]. Data from the International Energy Agency (IEA) [3] reveal that since then wind electricity generation has registered a rapid increase (from 2 GWh in 2014 to 449 GWh in 2017). As a comparison, in the same year, solar contributed to electricity production with 897 GWh and hydroelectric generation with only 38 GWh.

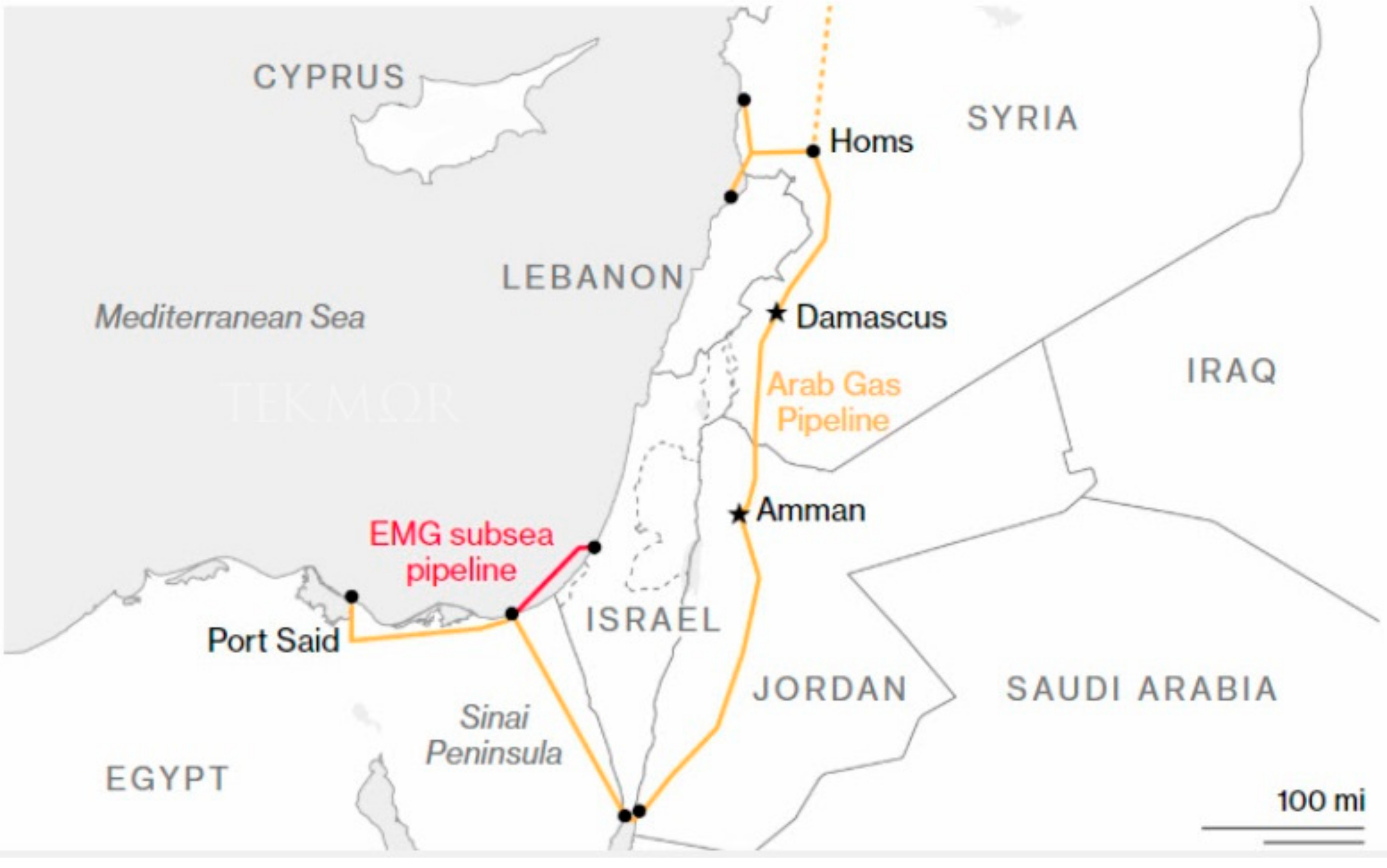

Oil products and natural gas are also the most important components of the energy imports to Jordan. Until 2011, natural gas was mostly imported at a favorable price from Egypt to Jordan through the Arab Gas Pipeline (Figure 3). The construction of the pipeline was initiated in 2001 and the first section connected Arish in the Sinai Peninsula to Aqaba, Jordan [45]. Further sections were then progressively built to connect Aqaba to the Syrian border, and from there throughout Syria to Lebanon and the Turkish border [46].

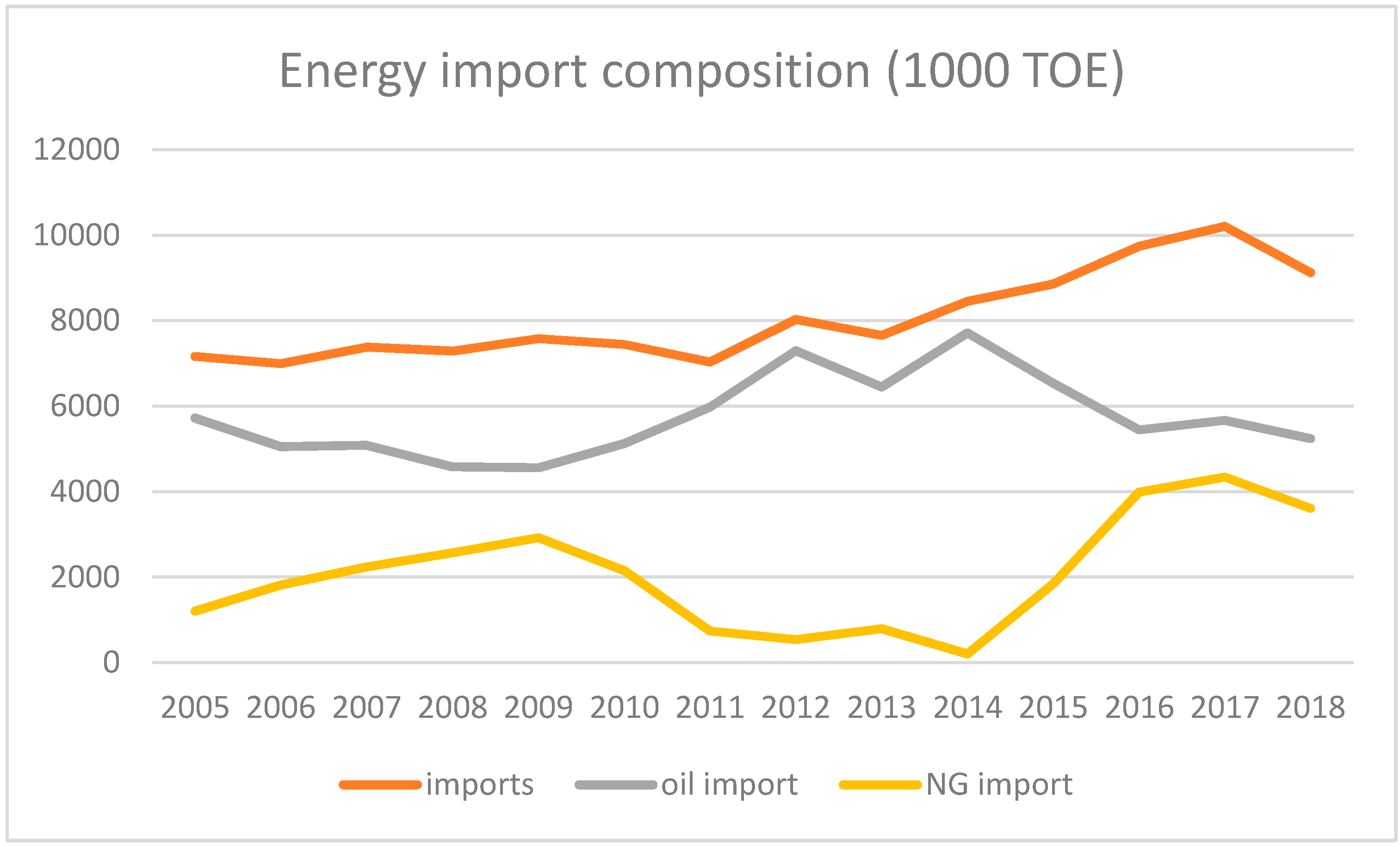

As a consequence of the Arab Spring events in Egypt in 2011, the import of natural gas had a sharp drop and continued to decrease until 2014 (Figure 4). More costly oil imports made up for the gap in the supply. Since 2014, natural gas import has increased and, accordingly, the import of oil has decreased. In 2015, the Sheikh Sabah Liquified Natural Gas port was established in Aqaba to enable the import of natural gas, shipped from different international sources on market basis. This represented an important step in diversifying the sources of imported energy.

It is interesting to note the implications of these international developments for the overall cost of energy: In 2009, the cost of consuming energy represented 12% of GDP. As a result of the substitution of Egyptian natural gas with oil, this cost reached a peak of 21% of GDP in 2012 and was on average 18.9% between 2011 and 2014. Starting to import natural gas through the Aqaba terminal reduced the cost of energy to an average share of 8.8% between 2015 and 2018 (data have been extracted from the respective MEMR Annual Reports). The increase in oil imports was mostly used to substitute natural gas in electricity generation. As a result, between 2011 and 2015, the National Electric Power Company (NEPCO) cumulated a debt of JOD 5 billion (around USD 7 billion).

4.2. Energy Consumption

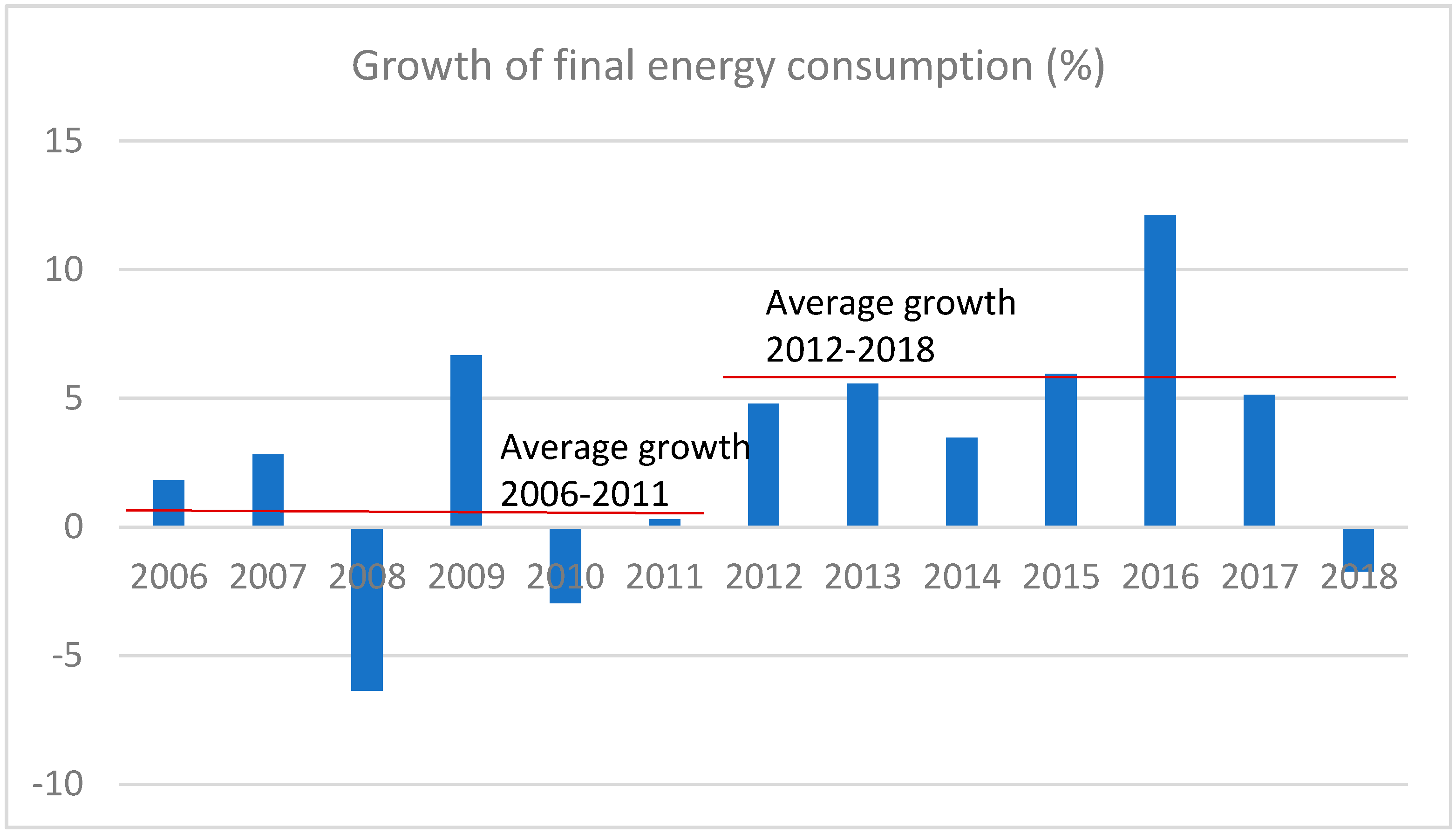

Final energy consumption remained stable between 2005 and 2011, but it has since then considerably increased. This is also evident considering the growth rates of final energy consumption as presented in Figure 5. The average growth was less than 0.38% per year between 2006 and 2011 and it jumped to an average growth of 5% between 2012 and 2018. This rapid and sustained trend could be motivated by the inflow of refugees due to the war in Syria (2.8 million refugees registered with the United Nations High Commissioner for Refugees, UNHCR) [48].

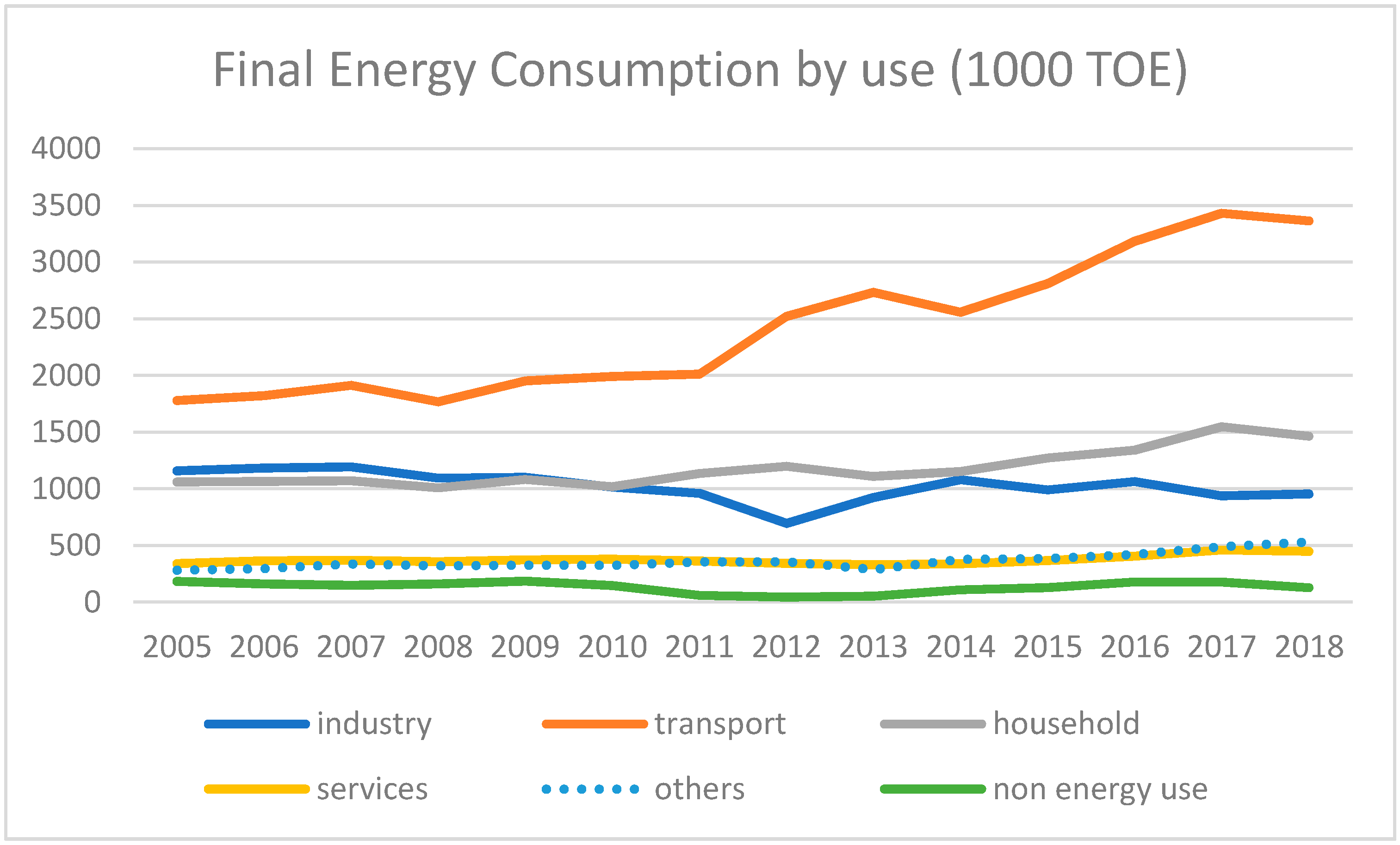

This line of explanation is also supported by disentangling final energy consumption by use (Figure 6). The year 2012 witnessed an increase in final energy consumption by household, vis-à-vis a drop in energy consumption by industry. A further trend, which can be rationalized with the same explanation, is the increase in the share of final energy consumed for transportation. In 2018, half of final energy consumption (49%) was due to transport, 21% to household uses, and 14% to industry.

The high share of final energy used for transportation seems to be a peculiar trait of the Jordanian economy, which has become even more pronounced since 2012. Worldwide, industry consumes the highest share of energy (29.2% according to data by the International Energy Agency (IEA) for the year 2017), followed closely by transportation (28.8%) and household consumption (21%). Also considering the Middle East as aggregate, the rank remains the same, though with slightly different shares (30.5% industry, 27.2% transportation, and 17.6% household according to the IEA for 2017). In Jordan, on the contrary, the share of final energy consumption by industry is less than that of transportation and household, and industrial final energy consumption has been decreasing both in absolute and in relative value. This can be linked to the slow but steady decrease of the value added of industry to GDP. According to the World Development Indicators [45], the value added of industry to Jordanian GDP decreased from 32% in 2008 to reach 27.5% in 2018.

Energy intensity progressively increased from 223 koe/USD 1000 at constant prices in 2013 to 247 koe/USD 1000 in 2017 and 235 koe/USD 1000 in 2018. The increase in energy intensity, not backed up by sustained economic growth, can be attributed to inefficient utilization of energy and increased standards of living. Interviewees also mentioned that the historically low prices of fuel and electricity in Jordan contributed to spreading unsustainable patterns of consumption, similar to those of the oil-rich countries in the region. Even though the situation with the prices has changed, consumption is slow in adapting. The interviewees thus signaled the urgent need to reduce energy demand via energy saving and favored the view that this can be achieved via incentives (currently missing overall in the legislation) and via awareness campaigns.

4.3. Electricity

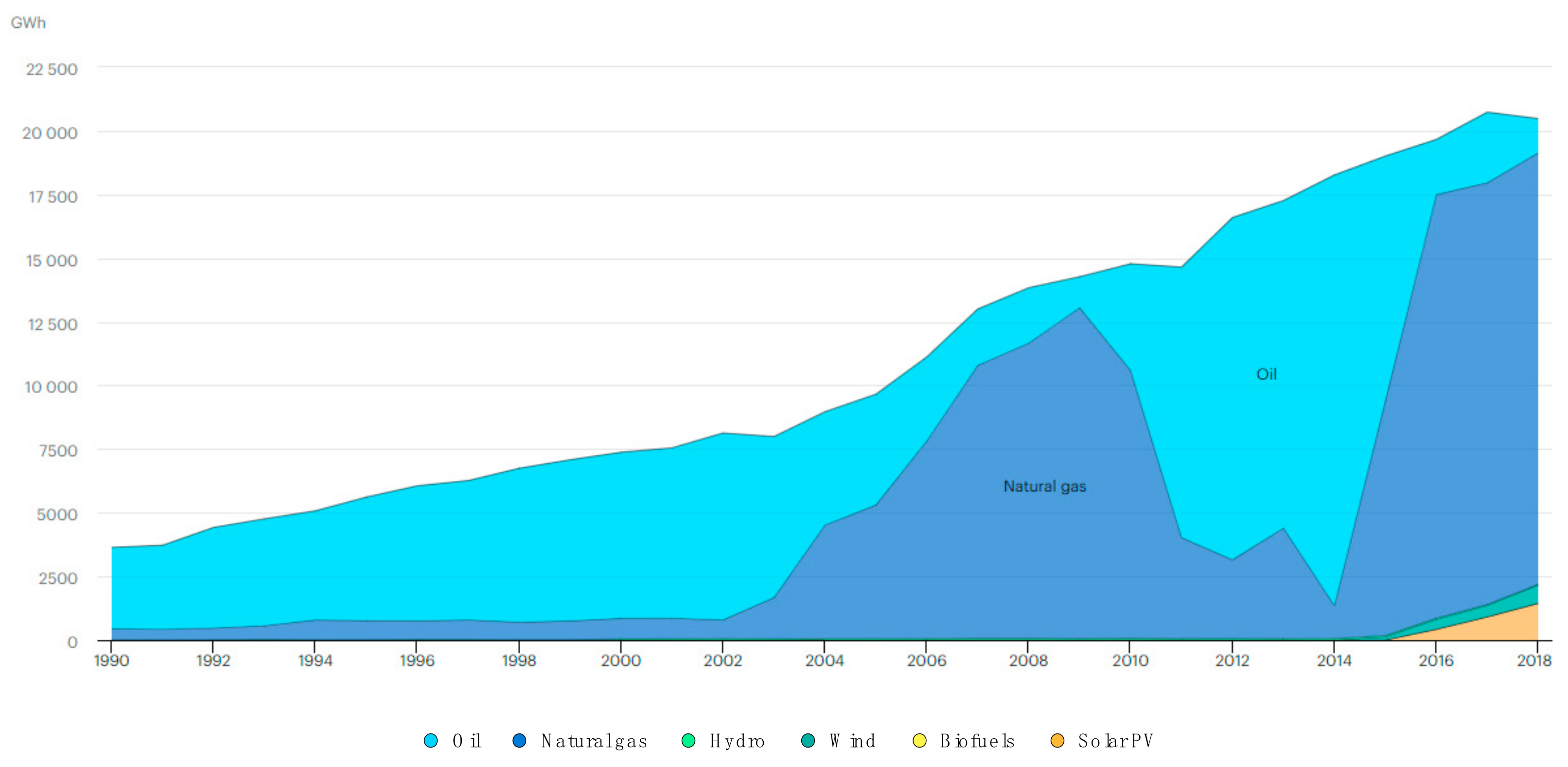

In Jordan, around 39% of primary energy is used for electricity generation and is essentially produced from natural gas and oil [40]. According to a statement by NEPCO, in 2018, imported natural gas contributed to 93% of electricity generation [49]. The remaining share was generated by relying on crude oil, solar, and hydropower (Figure 7). Crude oil imported from Iraq at below market price made up for the big bulk of electricity production until the Iraq War of 2003. Iraqis’ crude oil was then progressively substituted via natural gas from Egypt. The situation continued until 2010, when instabilities in Egypt caused disruption to the flow of natural gas to Jordan, which had to be substituted via crude oil. In 2015, electricity generation went back to the predominance of the cheaper natural gas. Figure 7 also shows an increase in the share of renewable energy power generation.

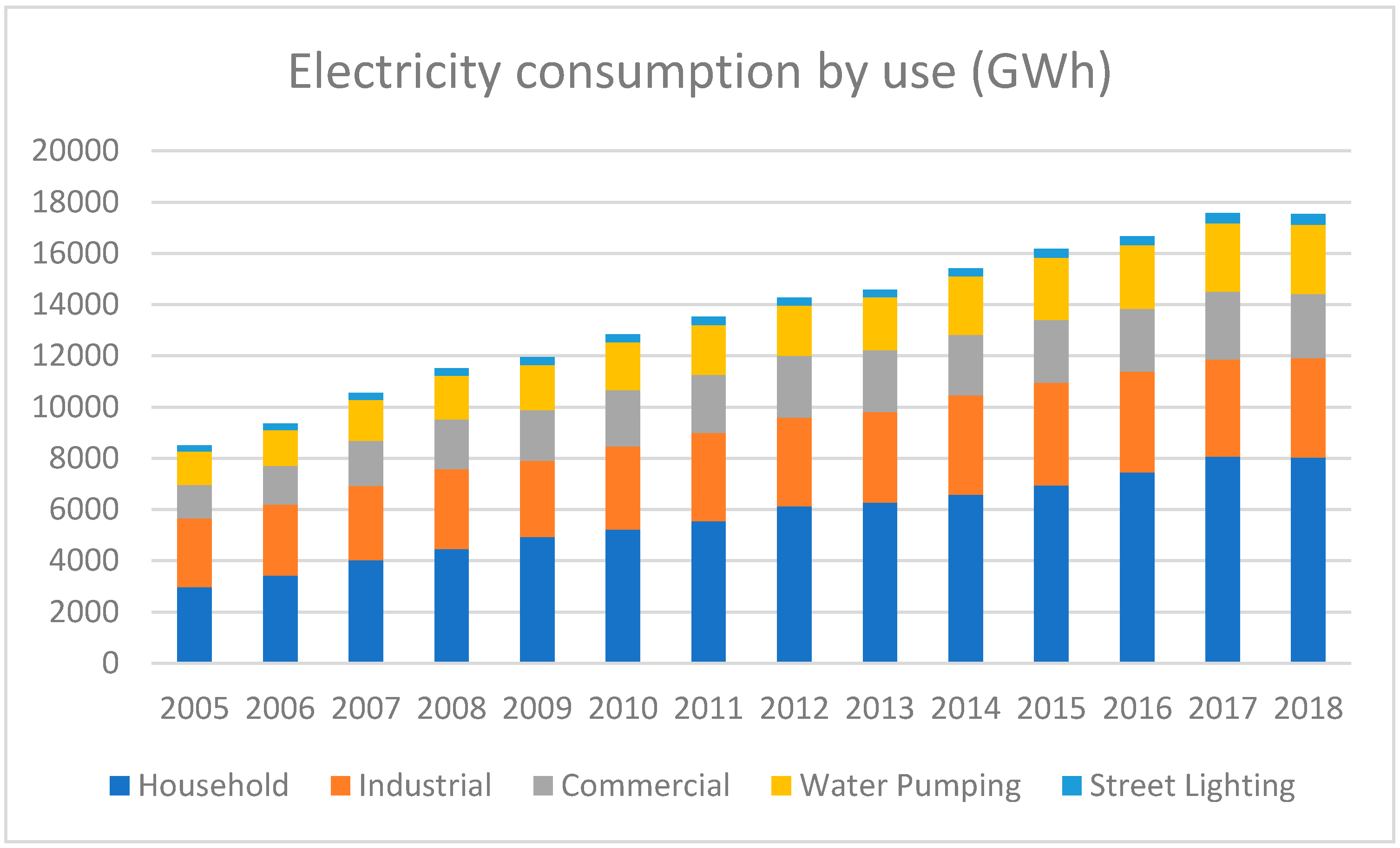

Jordan grants universal access to electricity for its population, as the totality of both rural and urban populations have access to electricity. Electricity consumption has been steadily increasing and the largest share is consumed by households (Figure 8). In 2018, households consumed 46% of electricity, industries 22%, water pumping 16%, commercial activities 14%, and street lighting the remaining 2%.

The cost of electricity is therefore crucial to the Water Authority of Jordan (WAJ), which is the largest electricity customer in the country. From desk research and as confirmed by interviews, renewable energy could definitely be upscaled for water pumping purposes. At present, significant examples of projects for renewable energy production in Jordan are the renewable wind energy plants in Tafileh and the solar plant in Qweider, generating 100 and 70 MW electricity per year, respectively. The interviews also signaled the possibility of investing in other forms of renewable energy to support the energy needs of the water sector. A priority would be to upscale hydropower at water treatment plants. Interviewees also saw some interesting experiences that could be upscaled, such as the As-Samra Waste Water Plant, which was completed in 2008 and is 80% powered by a combination of hydraulic turbines and biogas.

A challenge in this direction seems to be the very limited cooperation between water and energy institutions and stakeholders. This has been highlighted already by very recent research [41], which also supports the view that there are no significant conflicts in the preferences of water and energy stakeholders [42]. Our interviewees labeled the absence of coordination between the two sectors as a missed opportunity to address the nexus. Necessary steps would be to formulate a comprehensive plan for the water–energy nexus and to modify the regulatory framework to make its implementation possible. Other interviewees pointed to the importance of including agriculture in the nexus, adopting a more participatory approach and empowering stakeholders.

While Figure 8 shows that electricity consumption has been steadily increasing in the past decade, it is necessary to consider that per capita electricity consumption has decreased since 2015. It is currently assessed on a level of 1701 KWh [10]. This may be the result of new tariffs driving better efficiency in electricity use and better efficiency of household appliances and machineries, as well as of the increase in small-scale renewable projects, in particular for establishments such as universities, large enterprises, government institutions, schools, and hospitals (for an overview on small-scale renewable projects, see Ministry of Energy and Mineral Resources, MEMR, various annual reports). However, a different line of explanation seems to also be plausible: according to the Jordan National Social Protection Strategy for 2019, poverty increased among Jordanians (not counting refugees) from 14.4% in 2010 to 15.7% in 2018. Notably, socio-economic conditions have pronounced implications on electricity consumption, so reduced electricity consumption may be the sign of growing poverty. An interesting analysis on the relation between income and electricity consumption in Jordan demonstrates that in Amman city, which alone hosts almost one third of the total population in Jordan, densely populated areas have much lower electricity consumption than low-density areas [51]. Moreover, the decrease was registered in the per capita consumption—not the total consumption, which increased. Therefore, this may be caused by a lower per capita consumption by the people who moved to Jordan after 2014.

4.4. Energy Policy and Strategies

As said, energy security is now at the top of the policy debate in Jordan. The scarcity of natural resources in general and the reliance on imports to face energy needs put the country in a vulnerable position. Both authorities and public opinion are aware of the need to envision strategies to reach sustainable energy security, diversify the sources of energy and of imports, and increase the contribution of domestic sources.

Historical developments have been shaping the energy market in Jordan and reviewing them can help to better understand the options and strategies that are currently being envisioned towards securing the growing energy needs of the country. The 1990s reinforced the dependency of Jordan on fossil fuel. Until 2002, Jordan depended almost exclusively on Iraq to import crude oil and oil derivatives at a favorable price [52]. Under Saddam Hussein, Iraq delivered oil to Jordan for roughly one third of its market price and also allowed Jordan to pay in consumer goods [53]. In addition, Jordan met its electricity needs by importing electricity from Egypt and Syria. Even though the 1990s witnessed some progress in the adoption of solar panels for household water heating use, the overall cheap prices of imported energy prevented an upscale of renewable energy projects and investment in related research and development [54].

With the Iraq War in 2003 and the end of Saddam Hussein’s regime, Jordan could no longer secure its oil demand from Iraq and started importing oil mostly from Saudi Arabia at market prices. The energy bill started to grow following the steady increase in international oil prices. To reduce costs, Jordan started importing liquified natural gas from Egypt through the Arab Pipeline, which became operative in 2003. Natural gas was used to operate some power plants in substitution of the previously used oil.

All of these developments induced the authorities to formulate the first National Energy Efficiency Strategy 2005–2020. The strategy was released in 2005 and then updated in 2007 to the Master Strategy for the Energy Sector 2007–2020. The strategy and the master plan were organized over three main chapters, namely, (1) oil, electricity, and natural gas; (2) the renewable energy sector and energy conservation sector; and (3) the alternative and local energy sector. Overall, the guiding principles were the need to rationalize energy consumption and increase efficiency and reliance on renewable resources. Efficiency was to be enhanced via tariffs and pricing mechanisms, as well as via the support of investments in energy-saving techniques and the reduction of customs and duties on electric vehicles. Concerning the promotion of renewable energy resources, the strategy signaled the need to issue a renewable energy law, to attract private sector investment, and to create a fund to support renewable energy projects [55]. The “Renewable Energy and Energy Efficiency Law” (RE & EE) was promulgated in 2012 (Law No. 13 of 2012). Even though the RE & EE Law clearly represented an important and essential first step towards the upscaling of renewable energy projects in the kingdom, it was not clear concerning the cost of interconnecting renewable energy projects to the national grid and in suggesting a pricing reference of feed-in tariffs [54].

A second National Strategy for the Energy Sector was formulated for the 2015–2025 period, followed by another one for the 2020–2030 period. In general, both of these strategies have a strong focus on energy security and share the main objectives of the 2007–2020 document of diversifying the sources of energy to reduce vulnerability from external development and price fluctuations, investing in renewable energy and efficiency, boosting local energy production, and exploring alternative energy options. Both strategies aim at reducing the reliance on (imported) oil fuels in producing electricity. The 2015–2025 strategy envisions that by the end of 2025, 47% of electricity should come from nuclear sources, 26% from oil, 15% from renewable energy, and 11% from oil shales. Taking into consideration the difficulties in implementing the nuclear program, the strategy for 2020–2030 has abandoned nuclear ambitions and is prospecting a share of 53% of electricity to be produced via natural gas, 31% through renewable energy, 15% through oil shales, and only 1% using oil.

In 2008, the Jordan Atomic Energy Commission was established to develop the peaceful use of nuclear energy in the country. The commission was established in place of the Jordan Nuclear Energy Commission, which was founded in 2001. In 2008, the Jordan Nuclear Regulatory Commission—substituted by the Energy and Minerals Regulatory Commission in 2014—was responsible for coordinating feasibility studies of the uranium deposits, for studying regulatory mechanisms and safety procedures for the exploitation of nuclear energy, and for studying the financial feasibility of the program). The option of nuclear energy has been envisioned to generate electricity and to desalinate water, making use of the uranium deposits in Jordan [56]. In 2016, the Jordan Research and Training Reactor was established on the premises of the Jordan University of Science and Technology (JUST). There has been a vivid debate on nuclear energy and implementation strategies (two large reactors versus several smaller modular reactors), and several possible strategic partners have been considered (for a glance at the stand with the nuclear program in Jordan, see the information provided by the World Nuclear Association: https://www.world-nuclear.org/information-library/country-profiles/countries-g-n/jordan.aspx and newspaper sources: https://www.jordantimes.com/news/local/jordan-replace-planned-nuclear-plant-smaller-cheaper-facility; https://www.7iber.com/2014/jo-nuclear-program/). Studies on the uranium deposits, on the financial feasibility of the nuclear program, and on the necessary regulatory mechanisms and safety procedures for the exploitation of nuclear energy have pointed to some key challenges. Amongst these challenges are the critical aspects of water availability for cooling [57] and the quality of the uranium deposits [58]. The nuclear program has also encountered some opposition among civil society and environmental activists. These challenges led the Jordanian government to the 2018 decision to close and liquidate the Jordan Nuclear Power Company (JNPC). Reviewing the National Strategy for the Energy Sector 2020–2030 and its expectations for the 2030 energy mix, it seems that the concerns over possible risks of nuclear energy have prevailed and that the program has therefore been abandoned. Interviews confirmed that while there has been vivid debate in the country about the pros and cons of embarking on nuclear energy production, the plan was not pursued and was abandoned in the end.

Concerning oil shales, Jordan is the eighth country worldwide in terms of reserves [59]. Challenges hindering the exploitation of oil shales were (and still are) the cost intensity of the extraction process and the difficulty of mitigating environmental effects, with oil shale being an extremely polluting energy source. Interviewees shared in general the opinion that given the abundance of superficial oil shales in Jordan, oil shales definitely represent an interesting option for the energy mix of the country.

Despite the commitment of the authorities to reach a 10% share of energy from renewable sources and the favorable conditions for solar and wind, infrastructure, lack of funds and local financing schemes, and the size of the domestic market are discouraging investments in the sector and are hindering the transition [14]. To unleash the potential of renewable energy in Jordan, some contributions have been exploring the possibility of new transnational agreements, mostly between Jordan and Israel, suggesting, for instance, the exchange between desalinated water from Israel and Palestine and solar energy from Jordan [11,16], or, more in general, the potential of increased transnational cooperation and better connectivity of the national grids with Israel [5], often framing it within the regional project of the Red Sea–Dead Sea Canal. Nevertheless, these regional projects, while promising on a technical level, have and bring up political barriers and considerations that have precluded their realization. Azzuni et al. [12], based on simulation results, posit that “a transition towards a 100% renewable energy system for Jordan would be technically feasible and economically viable.”

Jordan’s potential for renewable energy—specifically solar—is unquestionable, being located in the sun belt and enjoying an average of 316 sunny days per year, having wind speeds ranging between 7 and 8.5 m/s [7,10], and having large desert areas with low population. As the example of Germany teaches, however, getting the maximum benefit out of renewable energy is more a question of political will, coordinated action, and investment, rather than a mere issue of resources and conditions. Jordan has taken important steps concerning the adoption of renewable energy technologies, but the overall achievements are still below the targets. Major obstacles are the high initial cost of producing energy through renewables and the high investments needed. Given the limited financial capabilities of the state, the authorities have been thus relying on private investments and are following the strategy to provide incentives to investors and launch Public–Private Partnerships (PPPs). Among other incentives, industrial renewable energy projects are granted a two-year exemption on income tax and a lifelong exemption on property tax [60].

A competitive bidding mechanism has been developed to select investors through calls for direct proposals. So far, three direct proposals rounds have been announced, in 2011, 2013, and 2016. Any local and international stakeholder was free to submit a technical and financial offer for a specific project defined by the Ministry of Energy and Natural Resources (MEMR). To incentivize the private companies, the Jordanian government committed to buying the electricity generated—at least for the establishment phase—at a negotiated price [40,42]. As elaborated in Section 5, some of the interviewees mentioned that the state is in many cases overly rewarding the private companies in the frame of PPPs. This can be interpreted as a form of weak governance, which seems to have imprinted Jordan’s public–private relationships since the beginning of the industrialization policies of the 1950s. As the International Bank for Reconstruction and Development (IBRD) noted back in 1957, the “degree of security given to its shareholders […] is so excessive as to give rise to a distorted notion of what should be considered reasonable riskbearing in industrial ventures” [61].

Further efforts have been also put into the realization of smaller-scale renewable projects (and connection to the grid) for universities, commercial and industrial enterprises, government institutions, schools, mosques, and hospitals [7,44]. Relatively widespread is also the use of solar panels for water heating by households, as approximately 15% of households make use of solar panels for water heating [62]. In general, international support and grants have been also contributing to the development of the renewable energy sector.

5. Results

The interviews reflected the perspectives of experts, decision-makers, and professionals in the field of energy and thus enabled us to understand the debate underlying the formulation and adoption of strategies, the implementation of policies, and the degree of integration of stakeholders’ perspectives.

The interviewees were coherent in signaling the potential of Jordan as an energy producer and in pointing to substantial challenges in terms of governance and lack of enabling the environment towards the envisioned transition. They also pointed to the existence of vested interests and stakeholders striving towards the maintenance of the status quo. Table 4 presents some selected quotes from the interviews related to issues that we consider to be representative and expressing consensual views among the interviewees.

6. Discussion

In general, the topics that emerged in the interviews could cover the dimensions of sustainable energy security included in the theoretical framework: The interviewees provided elements related to characteristics of energy supply and developed their vision for the sector. They further reflected on affordability and realizability, which related to the economic and technological dimensions as well as the environmental externalities and social impact of the envisioned alternatives. Geopolitical considerations emerged both in regard to the dependency on import and to the challenges and potential of regional and international cooperation.

An essential result is that interviewees unveiled several conflicts that are relevant to the energy sector in Jordan and that hamper the sustainability of energy security at different levels, conflicts that were not evident in the review of policies, governmental reports, and from the desk research. All of the interviewees favored a transition towards a future energy mix dominated by renewable energies, mostly solar and wind, and supported, for a minimum necessary share of conventional sources of energy, by imported natural gas and domestic oil shales. However, they pointed to inherent conflicts and trade-offs the envisioned transition would bring, as well as to conflicting views and interests weakening the political will towards this transition and in the end hampering change.

One of these conflicts is represented by environmental and economic considerations in regard to different energy options. This conflict emerged, among others, in regard to the diversification of the energy mix, with the idea of integrating the energy mix by making use of oil shales, which is notably a highly polluting energy source, but which Jordan could exploit due to its large reserves and which could have positive repercussions on employment. Interviewees in general highlighted that oil shale extraction would provide the geopolitical advantage of reducing dependency on imports and, being a heavy industry, would generate employment. Some of the interviewees also highlighted that due to the increase in oil prices, oil shale extraction is becoming economically more attractive. In addition, part of the polluting externalities from oil shale extraction could be counterbalanced, for example via water filtering of the sulfur dioxide emissions, which could be then converted into marketable sulfuric acid.

Another situation where interviewees saw a mismatch of environmental sustainability of energy security and economic consideration was the expansion of renewable energy opposed by actors in the electricity market, fearing the loss of their monopolistic role. The suggested solution to unpack these conflicts was to promote a more participatory approach to strategy development and the reform of the electricity sector so as to encompass the perspective of the plurality of stakeholders involved.

The expansion of renewable energy adoption may also potentially imply some conflicts at the social level, which would, however, be limited to the short to medium term. Quoting an interviewee, this is the case of “price distortions that would come with any change, until things settle in the long term. And, notably, renewal energy increases the prices in the short term,” so that appropriate mitigation should be put in place to protect the end consumer and more vulnerable groups of society.

Social conflicts may also arise in trying to improve transportation. The interviewees highlighted that the high share of energy used by transport is also associated with the lack of an efficient transportation net, for both goods and persons. Both desk research and interviews corroborate the idea that there are no plans to find alternatives to road transportation, in general. All of the interviewees noted that the current inefficient transportation mode is generating much employment and a solution would need to take into consideration and try to reduce the social cost of the transition. Concerning person mobility, public transportation is highly inefficient and the timid attempts to improve the bus network in the capital city Amman are based, according to interviewees, on an “outdated model, fostering non-optimal public transportation.” Road transport is also the only modality of transportation for goods, too. In this regard, some of the interviewees noted that the reliance on imports and the predominance of small and medium enterprises, which are served by a huge number of small trucks, contribute to the bloated energy consumption of the transport sector. A further issue that was raised in the interviews was the absence of a pipeline to transport crude oil from the port of Aqaba to the refinery in Zarqa. The cost of transporting crude oil via trucks is considerable, in addition to the negative environmental externalities and the congestion of the road infrastructure. According to our interviewees, the need to build a pipeline to serve the refinery would be a strategic priority for the country and has been under discussion for a long time. The interviewees highlighted that in 2007, a very prominent case of corruption emerged, involving, among others, the pipeline, and plans were put aside. To the best of our knowledge and as confirmed in the interviews, there are currently no concrete plans in this direction.

A further interesting point that was confirmed in interviews is that political instability and frictions are obstacles towards exploiting the existing potential of regional cooperation in the field of energy, which could definitely contribute to the sustainability of energy security and to regional stability. In this regard, some of our interviewees would like to see increased involvement by the international community in supporting the development and implementation of a comprehensive strategy for a more sustainable energy sector in Jordan. In their opinion, it could build on the existing dialogue with the European Union and with European agencies towards the development of a modern and supportive regulatory framework and the involvement of the Japan International Cooperation Agency (JICA) towards the modernization of the electricity sector (inspired by the 3-L principles of energy supply at low cost, low carbon, and low risk) [63]. In their view, these experiences should be upscaled and should start targeting regional cooperation in the electricity sector, too, which cannot be possible without supportive international mediation.

Steps towards the Modernization of the Energy Sector

Several important steps have been taken to restructure the energy sector in Jordan. First of all, the market for oil and petroleum derivatives has been progressively restructured and liberalized. Three companies were licensed in 2013 and started to operate in 2016, importing an increasing share and portfolio of oil products. Since 2018, these three companies have been able to import all of their needs through petroleum derivatives. In 2015, the government also founded the Jordan Oil Terminals Company (JOTC), a private shareholding company fully owned by the government, which is responsible for the storage and handling of all petroleum products, as well as for securing oil supply and ensuring competition.

Before, the only company operating in the market for petroleum derivatives and holding the exclusive right to refine crude oil and trade and market petroleum products in Jordan was the Jordan Petroleum Refinery Company, founded in 1956. The Jordan Petroleum Refinery Company is still the only refinery in the country and is currently planning, with the support of foreign partners, an ambitious expansion project [64].

The authorities also signed a draft agreement in 2013 for the construction of an oil pipeline to deliver oil from Iraq. The pipeline would extend over a total of 1300 km, 900 km of which are in Jordan. The total cost of construction is estimated to be around USD 8 billion (USD 5.6 billion for the Jordanian part). By the end of 2020, the tender process for the project implementation should be completed and construction would start soon after (MEMR, homepage) [7,44].

With the aim of increasing the competitiveness of domestic industry, efforts have been undertaken to encourage industries to switch to gas in substitution of various more expensive fuels. Incentives have been set up for this purpose in the form of a tax exemption for the first three years after the switch to natural gas, among others [65].

Concerning the aim of diversifying the sources of natural gas import to reduce vulnerability and cost, the authorities plan to progressively reduce shipped imports from the terminal in Aqaba. Since September 2018, imports from Egypt through the Arab Pipeline have resumed [66]. In 2016, Jordan signed a 15-year agreement with Noble Energy to import natural gas from Israel through a pipeline located in the north of the country. While this was seen in Jordan as a controversial agreement, as it would strengthen relations and trade with Israel and rely on Israel for part of Jordan’s energy security—confirmed by the position of the Jordanian Parliament, which voted against it—the project has gone ahead [67,68,69]. In fact, operations started in 2020 and Noble Energy is expected to cover 40% of total gas needs for Jordan [70]. Israel and Egypt are thus expected to become the main suppliers of natural gas.

The electricity sector has also progressively opened to market competition. A first restructuring of the electricity sector was achieved in 1996, when the National Electric Power Company (NEPCO) was established and nominated as successor of the Jordan Electricity Authority. In 1997, NEPCO was split into three different independent companies responsible for generation, transmission, and distribution activities. In 2014, the Energy and Minerals Regulatory Commission was established to regulate and supervise the whole energy and electricity sector in a unified framework. According to Law No. 17 for the year 2014, the commission is the legal successor of the Electricity Regulatory Commission, of the Jordan Nuclear Regulatory Commission, and of the Natural Resources Authority. After this restructuring, the Ministry of Energy and Mineral Resources and the Energy and Minerals Regulatory Commission are the only authorities responsible for the energy and mineral resources sector). The commission currently licenses nine electricity-generating companies. Construction, operation, and maintenance of the transmission system within the country are the exclusive responsibility of NEPCO, which is a public shareholding company fully owned by the state. Distribution is operated via three further shareholding companies: Jordan Electric Power Company—JEPCO, Irbid District Distribution Company—IDECO, and Electricity Distribution Company—EDCO.

The difficulties of the electricity sector essentially reflect as losses for state-owned NEPCO. As a result of increased and progressive electricity tariffs, cheaper import, and decrease in oil prices, NEPCO has managed to reduce (but not to eliminate) its operational losses [71]. Since 2017, electricity bills have encompassed an additional fee to be added in adjustment to eventual oil price increases. In general, reforming the electricity sector to make it more sustainable and financially viable, while considering the social cost of shifting the burden of high generation costs to the final customers, is an issue that needs to be addressed.

The interviewees were unanimously convinced of the need to reform the electricity sector, set more ambitious targets for the share of renewable energy, and review regulations to address the existing bureaucratic challenges. In this regard, interviewees suggested that a priority would be to review the monopolistic role of state-owned NEPCO. The argument is that given its current role, NEPCO sees renewable energy as a threat to its revenues. Quoting one of the interviewees, this fear is aggravated for NEPCO by “being stuck in take-or-pay contracts,” which implies a systematic excess of electricity generation and waste in Jordan.

The analysis of the Jordanian energy sector has highlighted that Jordan relies on a conventional energy mix, mostly based on (imported) crude oil and natural gas. Increasing international prices, regional instability, and sustained growth of energy demand point to the urgency of formulating a new vision for the energy sector.

The regional developments of the last few years, with the Iraq War in 2003 and the disruption of the gas supply from Egypt, reveal that the reliance of imported sources of energy increases the vulnerability of the country to external events and jeopardizes its economic growth perspectives. As such, energy security is challenging also in regard to geopolitical considerations, given the existing tensions and conflicts among and within the neighboring countries. Considering the excellent conditions for the exploitation of renewable energy, mostly in the form of solar and wind, the country has the potential to exploit existing technological possibilities towards a green energy mix, which would bring together technological and environmental aspects of more sustainable energy security.

The experts interviewed for this study were also coherent in highlighting the need to move Jordan towards a more sustainable energy sector. Interestingly, despite the non-availability of conventional energy sources, interviewees signaled the potential of Jordan as an energy producer. The interviewed experts shared a vision to drive sustainable energy policy in Jordan, in which renewable energy makes for the big bulk of energy supply. Being located in the sun belt, endowed with appropriate wind speed, and having large desert area, the country has undoubtedly the right conditions for that. The remaining part of the energy mix should consist of conventional energy sources, such as domestically extracted fuel from oil shales, to generate employment, reduce import dependency and imported clean natural gas. This vision should go hand in hand, according to the experts, with the progressive electrification of the economy.

The interviewees were again consistent in highlighting technical challenges to the transition, due to the need to upscale the infrastructure to enable the integration of non-conventional energy sources into the national electricity grid (green corridor), and economic challenges, in the sense of the large investments needed, which would need increased participation by private companies. The small size of the domestic market seems to be one of the factors discouraging investment. The regional integration of electricity grids would help in overcoming this issue. The interviewees highlighted that this entails modernized infrastructure at the regional level to facilitate the collaboration and connection between Jordan and other countries in the region and beyond (especially that Jordan be connected via electricity network with so many countries), which should not be confused with local infrastructure modernization, the need to raise sufficient funding from international and local institutions, and the importance of a strong political arrangements and coordination that would foster or hamper development in this regard, which need to be considered by policy makers at the highest level.

There was a further substantial consensus among the interviewed experts about weak governance being the most important factor truly hampering the transition to a more sustainable energy sector. Some experts spoke, in addition to weak governance, of a “lack of enabling environment,” “bureaucratic thinking,” and a “lack of implementation capability.” Quoting an interviewee, “for long term strategies, you need to be sure that what you start will be further implemented by future governments.” This is echoed by a further expert, stating that, “there is much speaking of strategies, but there is no real implementation in place.” Weak governance thus hampers the implementation of strategies, which would also require coordination and trust among stakeholders [72]. According another interviewee, “institutions are there, but they do not really coordinate. Coordination is weak and there are different perspectives. Every entity has its own interests and targets, since in the end, each one wants to present a better balance sheet.” Some interviewees even alluded to the lack of trust between institutional stakeholders, pointing to the lack of a real exchange of information between different governmental agencies and authorities.

This lack of coordination and trust between the energy sector and related sectors’ stakeholders is proof of the weak governance and a result of the missing exploitation of the natural synergies between these sectors. The interviewees were all convinced of the necessity to strengthen the institutional framework and formulate a comprehensive strategy to address the water–energy nexus, but also to address synergies with the agricultural and transportation sectors. Based on the failure of top-down approaches to solve natural resources conflicts [72], a participatory approach involving all stakeholders would be mostly needed. Weak governance typically amplifies the bargaining power of vested interests [73] and, in the case of Jordan’s energy sector, seems to strengthen resistance to change. It is interesting that all of the sampled experts commented on the prominent role of NEPCO in hindering the transformation towards a more sustainable and environmentally friendly electricity sector.

The water sector is an important electricity consumer in Jordan and it should therefore participate in the formulation of a comprehensive energy and energy conservation strategy. The systematic implementation of small-scale renewable energy projects, including solar, water, and hydropower in conjunction with dams, water pumping stations, and water treatment plants could be one of the first and most promising steps towards addressing the water–energy nexus.

With almost half of the energy being used for transportation, a round table on how to address the transport–energy issue would be a further priority. In this regard, interviewees shared the vision of incentivizing the electrification of transport, which could also fit well into the auspicated renewable energy ambition of the country. Interviewees highlighted that public transportation and more efficient and environmentally friendly goods transport would be needed, too (e.g., e-cars). Interviewees were, however, aware that addressing the complex issue goes beyond mere infrastructure development. It also needs to take into consideration the characteristics of the Jordanian economy, with the predominance of micro, small, and medium enterprises, as well as socio-economic aspects, the first being the large share of the workforce employed by the transportation sector. In 2019, the transportation sector employed 5% of the workforce. Therefore, it would be crucial to strike a balance when modernizing the transportation system, creating the infrastructure for a more efficient and green transportation of persons and goods while taking into consideration the repercussions of new equilibria on the economy as a whole. Again, a participatory process would be needed.

7. Conclusions

Despite the favorable conditions for solar and wind, Jordan’s energy mix is still dominated by imported fossil fuels and natural gas. As such, the country’s energy security is vulnerable to international and regional developments, as well as to fluctuations in energy prices. Redefining strategies towards a more sustainable energy sector is at the top of the political agenda in Jordan and the authorities have been envisioning alternative options, but progress has been moderate so far. With this background in mind, this study aimed at identifying the main challenges and opportunities towards more sustainable energy security in Jordan and at validating them by means of interviews with Jordanian policy makers and key energy experts. The analysis has revealed that to ensure the transition to a sustainable energy sector, it is necessary to reflect in a synergic manner both energy demand and supply. Concerning energy demand, the priority should be dedicated to improving energy efficiency and optimizing energy demand management, starting with transportation (which alone deploys almost half of total energy consumption), the water sector (where the potential for energy conservation is evident but unexploited), and households (where incentives and awareness should target a change in unsustainable consumption patterns). Concerning energy supply, the analysis has confirmed the need to target the diversification and reduction of imports, as well as the increased reliance on domestic sources of energy (renewables, in primis, and other non-conventional sources to complement the mix).

All of this would require existing conflicts between stakeholders to be addressed through a more participatory approach to reform, which could increase the consensus about reforms and strategies and improve energy sector governance.

Author Contributions

All authors have contributed to the conceptualization, design, methodology, data collection, analysis, and writing of this article. All authors have read and agreed to the published version of the manuscript.

Funding

This publication was also made possible in part through the support received by Hussam Hussein from the Oxford Martin School Programme on Transboundary Resource Management, University of Oxford. The views expressed in this paper are the sole responsibility of the authors.

Acknowledgments

The authors are grateful to Michael Gilmont (University of Oxford), Gokhan Cuceloglu (University of Oxford), and Raya A. Al-Masri (University of Surrey) for their constructive feedback on previous drafts of this article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- IEA. Energy Supply Security: Emergency Response of IEA Countries. 2014. Available online: https://www.iea.org/publications/freepublications/publication/ENERGYSUPPLYSECURITY2014.pdf (accessed on 10 November 2020).

- Miller, L. Energy, Security and Foreign Policy: A Review Essay. Int. Secur. 1977, 1, 111–123. [Google Scholar] [CrossRef]

- Von Hippel, D.; Suzuki, T.; Williams, J.H.; Savage, T.; Hayes, P. Energy security and sustainability in Northeast Asia. Energy Policy 2011, 39, 6719–6730. [Google Scholar] [CrossRef]

- Jakstas, T. What does energy security mean? In Energy Transformation towards Sustainability; Tvaronavičienė, M., Ślusarczyk, B., Eds.; Elsevier: Amsterdam, The Netherlands, 2020; pp. 99–112. [Google Scholar]

- Hamed, T.A.; Bressler, L. Energy security in Israel and Jordan: The role of renewable energy sources. Renew. Energy 2019, 135, 378–389. [Google Scholar] [CrossRef]

- Abu-Rumman, G.; Khdair, A.I.; Khdair, S.I. Current status and future investment potential in renewable energy in Jordan: An overview. Heliyon 2020, 6, e03346. [Google Scholar] [CrossRef] [PubMed]

- Ministry of Energy and Mineral Resources (MEMR). Annual Report 2017; Ministry of Energy and Natural Resources: Amman, Jordan, 2018.

- Alshwawra, A.; Almuhtady, A. Impact of Regional Conflicts on Energy Security in Jordan. Int. J. Energy Econ. Policy 2020, 10, 45–50. [Google Scholar] [CrossRef]

- Wardam, B.M. Five Reasons for Jordanian Nuclear Program Failure. 2014. Available online: https://www.7iber.com/2014/jo-nuclear-program/ (accessed on 30 August 2020).

- Ministry of Energy and Mineral Resources (MEMR), Updated Master Strategy of Energy Sector in Jordan for the Period (2007–2020), Amman, Jordan. Available online: http://www.memr.gov.jo/Portals/0/energystrategy.pdf (accessed on 10 November 2020).

- Katz, D.; Shafran, A. Transboundary exchanges of renewable energy and desalinated water in the Middle East. Energies 2019, 12, 1455. [Google Scholar] [CrossRef] [Green Version]

- Azzuni, A.; Aghahosseini, A.; Ram, M.; Bogdanov, D.; Caldera, U.; Breyer, C. Energy Security Analysis for a 100% Renewable Energy Transition in Jordan by 2050. Sustainability 2020, 12, 4921. [Google Scholar] [CrossRef]

- Baniyounes, A.M. Renewable energy potential in Jordan. Int. J. Appl. Eng. Res. 2017, 12, 8323–8331. [Google Scholar]

- Jaber, J.O.; Elkarmi, F.; Alasis, E.; Kostas, A. Employment of renewable energy in Jordan: Current status, SWOT and problem analysis. Renew. Sustain. Energy Rev. 2015, 49, 490–499. [Google Scholar] [CrossRef]

- Yaser, A.; Ahmad, B. Renewable energy assessment in Jordan. Renew. Sustain. Energy Rev. 2007, 15, 2232–2239. [Google Scholar]

- Katz, D.; Shafran, A. Energizing Mid–East water diplomacy: The potential for regional water–energy exchanges. Water Int. 2020, 45, 1–19. [Google Scholar] [CrossRef]

- Al Zou’bi, M. Renewable energy potential and characteristics in Jordan. J. Mech. Ind. Eng. Res. 2010, 4, 45–48. [Google Scholar]

- Chester, L. Conceptualising energy security and making explicit its polysemic nature. Energy Policy 2010, 38, 887–895. [Google Scholar] [CrossRef]

- Kisel, E.; Hamburg, A.; Härm, M.; Leppiman, A.; Ots, M. Concept for Energy Security Matrix. Energy Policy 2016, 95, 1–9. [Google Scholar] [CrossRef]

- Stern, J. European gas security: What does it mean and what are the most important issues. In Proceedings of the Presentation to CESSA Conference, Cambridge, UK, 14 December 2007. [Google Scholar]

- Scheepers, M.; Seebregts, A.; de Jong, J.; Maters, H. EU Standards for Energy Security of Supply: Updates on the Crisis Capability Index and the Supply/Demand Index Quantification for EU-27; ECN-C-06-039/CIEP; ECN Clingendael International Energy Programme: The Hague, The Netherlands, 2007. [Google Scholar]

- Cambridge Advanced Learner’s Dictionary & Thesaurus; Cambridge University Press: Cambridge, UK, 2008.

- Du Pisani, J.A. Sustainable development–historical roots of the concept. Environ. Sci. 2006, 3, 83–96. [Google Scholar] [CrossRef]

- World Commission on Environment and Development. Our Common Future; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development; Division for Sustainable Development Goals: New York, NY, USA, 2015. [Google Scholar]

- Fang, D.; Shi, S.; Yu, Q. Evaluation of Sustainable Energy Security and an Empirical Analysis of China. Sustainability 2018, 10, 1685. [Google Scholar] [CrossRef] [Green Version]

- Kapil, N.B.; Sudhakara, R.; Shonali, P.; Mahendra, D. Sustainable energy security for India: An assessment of the energy supply sub-system. Energy Policy 2017, 103, 127–144. [Google Scholar]

- Department of Trade and Industry. Conclusions of the Review of Energy Sources for Power Generation; The Stationary Office: London, UK, 1998. [Google Scholar]

- Helm, D. Energy policy: Security of supply, sustainability and competition. Energy Policy 2002, 30, 173–184. [Google Scholar] [CrossRef]

- European Parliament. Energy Policy: General Principles. Available online: https://www.europarl.europa.eu/factsheets/en/sheet/68/energy-policy-general-principles (accessed on 5 November 2020).

- Patton, M.Q. Qualitative Research & Evaluation Methods Integrating Theory and Practice, 4th ed.; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2014. [Google Scholar]

- Creswell, J.W.; Clark, V.L.P. Designing and Conducting Mixed Methods Research; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2011. [Google Scholar]

- Palinkas, L.A.; Horwitz, S.M.; Green, C.A.; Wisdom, J.P.; Duan, N.; Hoagwood, K. Purposeful Sampling for Qualitative Data Collection and Analysis in Mixed Method Implementation Research. Adm. Policy Ment. Health Ment. Health Serv. Res. 2015, 42, 533–544. [Google Scholar] [CrossRef] [Green Version]

- EDAMA. Renewable Energy Sector Development in Jordan; EDAMA Association for Energy, Water and Environment: Ammam, Jordan, 2019. [Google Scholar]

- Kiwan, S.; Al-Gharibeh, E. Jordan toward a 100% renewable electricity system. Renew. Energy 2020, 147, 423–436. [Google Scholar] [CrossRef]

- Hrayshat, E.S. Analysis of the renewable energy situation in Jordan. Renew. Sustain. Energy Rev. 2007, 11, 1873–1887. [Google Scholar] [CrossRef]

- Fawwaz, Z.E.; Nazih, M.A. The role of financial incentives in promoting renewable energy in Jordan. Renew. Sustain. Energy Rev. 2013, 57, 620–625. [Google Scholar]

- Saidan, M. Sustainable Energy Mix and Policy Framework for Jordan; Friedrich-Ebert-Stiftung: Amman, Jordan, 2011. [Google Scholar]

- Ayasreh, E.A.; Bin Abu Bakar, M.Z.; Khosravi, R. Dirasat, The Political Concept of Energy Security: The Case of Jordan. Hum. Soc. Sci. 2017, 44, 199–218. [Google Scholar]

- EDAMA. Recommendations for the Energy Sector Strategy; EDAMA: Ammam, Jordan, 2019. [Google Scholar]

- Al-Masri, R.A.; Chenoweth, J.; Murphy, R.J. Exploring the Status Quo of Water-Energy Nexus Policies and Governance in Jordan. Environ. Sci. Policy 2019, 100, 192–204. [Google Scholar] [CrossRef] [Green Version]

- Komendantova, N.; Marashdeh, L.; Ekenberg, L.; Danielson, M.; Dettner, F.; Hilpert, S.; Wingenbach, C.; Hassouneh, K.; Al-Salaymeh, A. Water–Energy Nexus: Addressing Stakeholder Preferences in Jordan. Sustainability 2020, 12, 6168. [Google Scholar] [CrossRef]

- World Bank. World Development Indicators; World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Ministry of Energy and Mineral Resources (MEMR). Annual Report 2018; Ministry of Energy and Mineral Resources (MEMR): Amman, Jordan, 2019.

- Stonaker, M. Energy Infrastructure as a Diplomatic Tool: The Arab Gas Pipeline. J. Energy Secur. 2010, 3. [Google Scholar]

- Leal-Arcas, R.; Akondo, N.; Rios, J. Energy trade in the MENA region: Looking beyond the Pan-Arab electricity market. J. World Energy Law Bus. 2017, 10, 520–549. [Google Scholar] [CrossRef] [Green Version]

- Scheer, S. Thekmor Monitor, Oil and Gas Development in the Eastern Mediterranean. Israel-Egypt gas pipeline deal seen imminent. Available online: http://tekmormonitor.blogspot.com/2019/11/israel-egypt-gas-pipeline-deal-seen.html (accessed on 10 December 2020).

- Government of Jordan (GoJ). Jordan Economic Growth Plan. 2018–2022; Government of Jordan: Amman, Jordan, 2017.

- The Jordan Times. Available online: https://www.jordantimes.com/news/local/93-cent-jordan’s-electricity-generated-natural-gas (accessed on 10 November 2020).

- IEA, Database. Available online: https://www.iea.org/data-and-statistics (accessed on 10 November 2020).

- Dar-Mousa, R.N.; Makhamreh, Z. Analysis of the pattern of energy consumptions and its impact on urban environmental sustainability in Jordan: Amman City as a case study. Energy Sustain. Soc. 2019, 9, 15. [Google Scholar] [CrossRef] [Green Version]

- Khresat, A. The Energy Sector of Jordan; Abdulhameed Shoman Foundation: Amman, Jordan, 2008. (In Arabic) [Google Scholar]

- Lasensky, S. Jordan and Iraq: Between Cooperation and Crisis; US Institute of Peace: Washington, DC, USA, 2006. [Google Scholar]

- Seedan, M. Sustainable Energy Mix and Policy Framework for Jordan; Friedrich Ebert Foundation: Washington, DC, USA, 2011. [Google Scholar]

- Hashemite Kingdom of Jordan. Updated Master Strategy of Energy Sector in Jordan 2007–2020; Jordan Atomic Energy Commission: Amman, Jordan, 2007. [Google Scholar]

- Jordan Atomic Energy Commission. Available online: https://www.google.com/search?client=safari&rls=en&q=Jordan+Atomic+Energy+Commission&ie=UTF-8&oe=UTF-8 (accessed on 6 November 2020).

- Magid, A. Time to Reconsider Jordan’s Nuclear Program. Middle East Institute. 2016. Available online: https://www.mei.edu/publications/time-reconsider-jordans-nuclear-program (accessed on 26 August 2020).

- Xoubi, N. Evaluation of Uranium Concentration in Soil Samples of Central Jordan. Minerals 2015, 5, 133–141. [Google Scholar] [CrossRef] [Green Version]

- Based on data by the World Energy Council. Available online: https://www.worldenergy.org (accessed on 10 November 2020).

- IRENA. Evaluating renewable energy manufacturing potential in the Arab region: Jordan, Lebanon, United Arab Emirates. Energy Strategy Rev. 2018, 9, 1–7. [Google Scholar]

- International Bank for Reconstruction and Development (IBRD), The Economic Development of Jordan. Report of a Mission Organized by the International Bank for Reconstruction and Development at the Request of the Government of Jordan; Johns Hopkins Press: Baltimore, MD, USA, 1957. [Google Scholar]

- Jordan Investment Commission. Energy Sector Profile. 2018. Available online: https://www.jic.gov.jo/wp-content/uploads/2019/07/Energy-Sector-Profile-7-5.pdf (accessed on 26 August 2020).

- Japan International Cooperation Agency (JICA). JICA’s Cooperation for Electricity Sector in Jordan. 2014. Available online: www.jica.go.jp/jordan/english/index.html (accessed on 10 November 2020).

- Jordanian Petroleum Website. Available online: http://www.jopetrol.com.jo/Pages/viewpage.aspx?pageID=16 (accessed on 10 November 2020).

- Ministry of Energy and Mineral Resources (MEMR). National Strategy for the Energy Sector 2020–2030 (Translated); Ministry of Energy and Mineral Resources (MEMR): Amman, Jordan, 2019.

- Ministry of Energy and Mineral Resources. National Strategy for the Energy Sector 2015–2025; Ministry of Energy and Mineral Resources (MEMR): Amman, Jordan, 2014.

- Jordan Parliament Passes Draft Law to Ban Gas Imports from Israel, By Suleiman Al-Khalidi, Reuters. Available online: https://www.reuters.com/article/us-jordan-israel-gas-idUSKBN1ZI0H2 (accessed on 10 November 2020).

- Jordan Court: Gas Deal with Israel Cannot Be Cancelled. Available online: https://www.middleeastmonitor.com/20200514-jordan-court-gas-deal-with-israel-cannot-be-cancelled/ (accessed on 5 November 2020).

- Jordanians Voice Concerns over Imports of Israeli Gas, Al Jazeera. Available online: https://www.aljazeera.com/ajimpact/jordanians-voice-concerns-imports-israeli-gas-200129171830169.html (accessed on 5 November 2020).

- Al Khalili, S. Jordan Gets First Natural Gas Supplies from Israel, Reuters. Available online: https://www.reuters.com/article/jordan-israel-gas/jordan-gets-first-natural-gas-supplies-from-israel-idUSL8N2960Q9 (accessed on 26 August 2020).

- NEPCO. Amman, Jordan, Various Annual Reports; NEPCO: Amman, Jordan.

- Zikos, D. Revisiting the Role of Institutions in Transformative Contexts: Institutional Change and Conflicts. Sustainability 2020, 12, 9036. [Google Scholar] [CrossRef]

- Moe, T. Vested Interests and Political Institutions. Political Sci. Q. 2015, 130, 277–318. [Google Scholar] [CrossRef]

Figure 1.

Jordan’s primary energy supply and energy import between 2005 and 2018 (Data from the Ministry of Energy and Mineral Resources, MEMR]).

Figure 1.

Jordan’s primary energy supply and energy import between 2005 and 2018 (Data from the Ministry of Energy and Mineral Resources, MEMR]).

Figure 2.

Composition of primary energy supply in Jordan between 2005 and 2018 (Data from the MEMR).

Figure 2.

Composition of primary energy supply in Jordan between 2005 and 2018 (Data from the MEMR).

Figure 3.

Map of the Arab Gas Pipeline (Source: Scheer, 2019) [47].

Figure 3.

Map of the Arab Gas Pipeline (Source: Scheer, 2019) [47].

Figure 4.

Energy import composition in Jordan between 2005 and 2018 (Data from the MEMR).

Figure 5.

Growth of final energy consumption in Jordan between 2006 and 2018 (Data from the MEMR).

Figure 6.

Final energy consumption by use between 2005 and 2018 (Data from the MEMR).

Figure 7.

Electricity generation in Jordan by source between 1990 and 2018 (Data source: IEA, 2020) [50].

Figure 7.

Electricity generation in Jordan by source between 1990 and 2018 (Data source: IEA, 2020) [50].

Figure 8.

Jordan’s electricity consumption by use between 2005 and 2018 (Data from MEMR).

{kind=link}

{kind=link}