How Do International M&As Affect Rival Firm’s Sustainable Performance? —Empirical Evidence from an Emerging Market

1

School of Economics and Management, Tsinghua University, Beijing 100084, China

2

Research Center for Technological Innovation, Tsinghua University, Beijing 100084, China

*

Authors to whom correspondence should be addressed.

Sustainability 2020, 12(4), 1318; https://0-doi-org.brum.beds.ac.uk/10.3390/su12041318

Submission received: 30 December 2019

/

Revised: 9 February 2020

/

Accepted: 10 February 2020

/

Published: 12 February 2020

(This article belongs to the Special Issue Mergers and Acquisitions Processes and Sustainability)

Abstract

:International mergers and acquisitions (M&As) have been increasingly used by emerging market enterprises (EMEs) as a springboard for strategic assets to overcome latecomer disadvantages and build sustainable competitive advantages. While current literature only focuses on the M&As’ impacts on acquirers, little is known about the impacts of EMEs’ international M&As on their external stakeholders, such as rival firms. Based on the longitudinal data covering 325 large international M&As completed by Chinese public manufacturing firms during 2009–2015, empirical results show that international M&As at the industry level have significant negative influence on the sustainable performance of acquirers’ rivals, and these negative relationship will be accentuated when the international M&As are horizontal M&As, when rivals are carrying out cost leadership strategy, and when those M&As are completed in the high-tech industry. This study enriches the literature of international M&As and the economic pillar of sustainability by pushing current research toward rival’s perspective and denotes that firms need to consider the potential negative impact on the sustainability of their outside stakeholders (e.g., other firms and whole industry). It also generates practical implications for firms to actively deal with potential negative effects of competitors’ international M&As on their sustainable performance, especially those players in the high-tech industry.

1. Introduction

International mergers and acquisitions (M&As) have been increasingly used as a springboard for strategic resources by emerging market enterprises (EMEs) to build up sustainable competitive advantages [1,2], accelerate industry catch-up, and achieve sustainable economic and social development [3] in the past decades. Scholars have investigated multiple dimensions of international M&As completed by EMEs—for example, motivations, post-integration process, and the influence on firms’ financial and innovation performance [4,5,6,7]. However, almost all the previous research focuses on those M&As processes of acquirers and oversees their influence on acquirers’ external stakeholders (e.g., rival firms), especially on the sustainability of those stakeholders. Further studies should shed light on this topic since not all firms are equally aggressive in realizing value from international M&As [1,2,8] and sustainability are playing the role of a prerequisite for success [3].

As González-Torres et al. [3] point out in their latest study, one hot topic on sustainability in M&As is the effects of M&As on firms’ external stakeholders’ performance, which is highly related to the economic pillar of sustainability that emphasizes the value created by firms to their external context supporting future generations of prosperity [3,9]. Considering that rival firms are critical stakeholders of acquirers, and acquirers’ strategies and actions will have a direct influence on them, we focus on the impacts of acquirers’ international M&As on the sustainable performance of their rival firms.

The existing limited research proposed paradoxical theoretical arguments suggesting rivals may benefit or suffer from competitors’ international M&As. The literature on industrial organization posits rivals gain from M&As through collusive synergy [10,11] and utilization of information uncovered in M&A announcements [12,13]. Besides that, some scholars raised the growth probability hypothesis based on signaling theory, suggesting that M&As completed by competitors lead to an increment in rivals’ market evaluation [14]. Some other scholars insist that international M&As may harm rivals by acquiring firms’ stronger competitive advantages, which results from efficiency gains, enabling acquirers to sell their products with cost advantages and increase factors prices for rivals at the same time [15]. The previous literature further elaborates that efficiency gains are attributable to operational and financial synergy, and they are stronger for horizontal M&As than non-horizontal M&As [15,16].

Current studies adopting event analysis examined the effects of acquisition announcements on rivals’ stock market reactions, and almost all of them found positive results [14,17]. However, short-term stock price changes do not mean so much for rival firms’ sustainability, and how those non-aggressive rivals’ sustainable performance will be influenced deserves further investigation. Compared with short-term market reactions, rival firms’ long-term profitability should be taken into consideration to reflect the influence on their sustainable performance. What is more, whether the influence is contingent on contextual factors (e.g., the deal characteristics) remains understudied. Theoretically, existing research findings are mainly justified by the literature on industrial organization, while strategic management perspectives should be also taken into account [16,18]. Drawing on the resource-based view, strategic gains from international M&As for acquirers may place rivals to a disadvantageous position.

Accordingly, in this paper, our main goal is to investigate two related research questions (RQ):

RQ1:

How do competitors’ international M&As affect rival firms’ sustainable performance?

RQ2:

How do the characteristics of the deal, rival firm and industry influence the relationship (i.e., RQ1)?

We use empirical evidence from an emerging market to answer these questions. Specifically, we use a longitudinal dataset covering 325 large international M&As completed by Chinese public manufacturing firms during 2009–2015. Empirical results show that rivals’ sustainable performance will be harmed by the international M&As completed by their competitors. The negative effects will be stronger for horizontal international M&As compared with non-horizontal ones. Besides, the negative relationship will be accentuated by rivals’ cost leadership strategy, which reveals the degree of firm’s dependence on efficiency. The negative moderation of industry relatedness of M&As and cost leadership strategy confirms the efficiency gains mechanism further. What is more, for rivals in the high-tech industry, the negative effects of international M&As on their sustainable performance will be strengthened, providing robust evidence to support our strategic asset gains argument.

Our study contributes to the research and practice of M&As and the economic pillar of sustainability in three ways. First, we shift the pendulum from focusing on M&As’ effects on acquirers to their rivals. Considering the deficiency of the short-term oriented measurement (i.e., stock price changes) for rivals’ sustainable performance in previous research, we take rival firms’ long-term profitability, measured in return on assets (ROA), into consideration. In contrast with the short-term market reactions, our study finds EMEs’ international M&As have negative effects on their rivals’ sustainable performance. By shedding light on rival firms’ sustainable performance, our research may open a new window for scholars to further investigate the impacts of growing international M&As completed by EMEs on other external stakeholders.

Second, we propose a new mechanism from strategic management perspectives to explain the effects of international M&As on rivals’ sustainable performance, namely, the strategic asset gains for acquirers. The new mechanism complements the existing efficiency gains argument based on industrial organization literature and provides a new perspective for future research to understand the impact of a firm’s strategic behaviors on their external stakeholders.

Finally, we found EMEs’ international M&As engender more negative impacts on rivals’ sustainable performance when they implement a cost leadership strategy and when they are from the high-tech industry. This generates important lessons for firms when they are faced with competitors’ international M&As, especially in today’s fierce global competition in high-tech industries. Firms have to adjust their cost structure and develop or source strategic assets in an alternative way to compete with their acquiring competitors for sustainable competitive advantages and long-term performance.

2. Literature Review and Hypotheses

Plenty of research sheds light on the impacts of international M&As on acquiring firms’ performance, especially for EMEs that are facing more pressures to engage in international M&As with the development of globalization [2,8]. Previous literature reveals that M&As create value for acquirers through three kinds of synergy, namely operational synergy, financial synergy and collusive synergy [15]. Operational synergy attributes to economies of scale and scope in production, the realization of technological complementarities, replacement of inefficient management teams, etc. [19]. Financial synergy occurs when an acquired firm can receive cheaper capital for growth [20]. Collusive synergy originates from the increased market power after absorbing competitors. Reduced competition leads to lower monitoring costs of the collusive agreements, therefore, the existing players can charge a higher price for their products [10,11].

Based on the synergy effects, existing research has paid tremendous attention to the effects of M&As on acquiring firms’ performance; however, little is known on the specific mechanisms by which M&As benefit or harm acquiring firms’ rivals [17,18].

Three streams of literature are related to the subject. First, competitive dynamics literature examines rivals’ responses to M&As completed by their competitors, but the reason the studies in this field choose to focus on rivals’ responses is to explain acquiring firms’ approximately zero or slight positive returns from M&As [21]. Second, quite a few studies explore the spillover effects of international M&As at the industry level in emerging markets (EMs). Meyer and Sinani [22] conducted a meta-analysis on the spillover effects of foreign direct investment (FDI) to developing countries at the industry level. They found local firms’ performance may benefit from FDI, and it is contingent on the level of development of the host country. Spillover literature does provide insights into how rival firms’ performance or productivity are influenced by competitors’ international M&As. But the scenarios in spillover literature are opposite to our focus in this paper. Spillover literature usually pays attention to the phenomenon that multinational corporations from developed countries acquire or merge EMs’ local firms and examines how those activities will affect the rest of local firms’ performance. However, in our research context, firms in EMs are the acquirers, and firms in developed countries are the targets. Third, literature in the organizational learning field examines the effects of international M&As on rivals’ subsequent decisions on whether to imitate acquiring firms or not. For example, Francis et al. [23] found a significantly positive relationship between a US acquirer’s performance and its predecessors’ acquisition activity.

The aforementioned literature attempts to examine the impacts of international M&As on acquirers’ rivals, however, but it hasn’t directly answered the question of how international M&As influence the sustainable performance of acquiring firms’ rivals. Limited studies directly respond to the issue and propose different theoretical arguments. They test the effects of M&As on the rivals of acquirers and targets respectively, but almost all of them only take rivals’ cumulative abnormal returns (CAR) into consideration.

For the impact on the target’s rivals, information signaling is the main theoretical lens used to justify positive stock price reactions of target firms’ rivals. Song and Walkling [24] developed and tested the acquisition probability hypothesis that asserts that rivals of target firms earn CAR because of the probability to become targets themselves in the future. Follow a similar logic, Akhigbe and Martin [25] found, on average, the US domestic rivals of foreign acquisition targets earn positive and significant CAR.

In terms of the impact on the acquiring firm’s rivals, four theoretical arguments suggest rivals benefit from competitors’ acquisition announcements. The first argument is the collusive synergy hypothesis. Stigler [10,11] is one pioneer attempting to explore the influence of M&As on rivals’ performance, and he suggests rivals can benefit from collusive synergy (i.e., free riding on a higher product price after horizontal M&As). However, empirical results are inconsistent when testing the collusive synergy hypothesis. Eckbo’s [12,13] studies rejected the hypothesis by observing the change patterns of rivals’ CAR after their competitors’ acquisition announcements and after some acquisitions were challenged by antitrust laws. In contrast, Prager [26] found supportive evidence for the hypothesis in the changes of rival firms’ stock prices based on the northern securities company case in 1901. Kim and Singal [27] also detected collusive synergy effects which are manifested in the increment of airfares on routes affected by M&As based on data of airline mergers during 1985–1988. They insist on the reason why the previous studies rejected the collusive synergy hypothesis is that the tests done by them are all based on stock-market prices which are at best indirect but probably weak.

The second argument is the information effect proposed by Eckbo [12,13], and he suggests that the proposal announcements may contain technological innovation information that provides clues for rivals to imitate acquirers’ activities even by initiating a merger to create value.

The third argument is based on the managerial self-interest or value destruction effects of acquisitions [18,28]. Though the priority of M&As should be to improve overall performance [16], the facts are that M&As can be initiated for managers’ compensation or motivated by managerial hubris, and finally, destroy acquirers’ shareholder value. Drawing on the argument, Clougherty and Duso [17] assert that rivals of acquirers benefit from being an outsider to a merger.

The fourth argument is the growth probability hypothesis, which suggests that the acquisitions announced in a growing market signal potential for future growth, resulting in positive changes in rivals’ stock prices [14]. The scholars who proposed the hypothesis further elaborate that differences exist in the signals released by horizontal M&As and non-horizontal M&As. Horizontal M&As signal value creation opportunities from operational synergy, and non-horizonal M&As signal value creation opportunities mainly from financial synergy. Industry relatedness of M&As should cause different impacts on rivals’ CAR. They found evidence to support their argument based on acquisition announcements data during 1993–2008 in China.

In contrast, some other research suggests that international M&As may adversely affect the performance of acquirers’ rivals. The negative influence on rivals mainly results from efficiency gains for acquirers after M&As [15]. The literature indicates that efficiency gains can be obtained through operational and financial synergy [15,16]. Chatterjee [15] further clarifies that rivals can be negatively affected by competitors’ M&As by the stronger cost advantages for acquirers and the higher prices of input factors for rivals. On one hand, efficiency gains enable acquirers to experience cost advantages in the product market, and on the other hand, acquirers need fewer factor inputs because of the higher efficiency resulting in higher factor prices for rivals in the factor market.

After reviewing the existing theoretical arguments, we believe that the efficiency gains for acquirers dominate the post-acquisition process in our research context because collusive synergy hypothesis, information effects, growth probability hypothesis, and value destruction effects seem inappropriate to apply here. First, the collusive synergy hypothesis is not applicable to international M&As [29]. Since targets are from foreign countries (regions), and the number of domestic competitors keeps the same after international M&As, the likelihood for firms to collude has not been improved. Therefore, rivals cannot have the chance to free ride on higher product prices. Second, all the rivals in our sample dataset have not initiated any international M&As over the research periods. Thus, we are skeptical as to how much they can leverage the innovative information in acquisition announcements to realize value since the information is probably all about creating value from M&As. Third, the growth probability hypothesis lacks enough explanation power for rivals during our research periods. The research periods in Gaur et al.’s [14] article are from 1993 to 2008. That was the period when the Chinese government promoted the privatization of state-owned enterprises and large-scale institutional changes, which created tremendous opportunities for firms to grow through M&As. However, after 2008, industry competition in China became much fiercer, and M&As may now be a signal of the decline in market position instead of a signal for growth potential [30]. Finally, most of the studies focusing on EMEs’ international M&As performance have drawn positive conclusions [6,31], which is in contrast with the findings in developed countries, where acquirers generally obtain negative or break-even returns from an acquisition [18]. Thus, we assert that efficiency gains for acquirers dominate the post-acquisition process which leads to negative effects on rivals. Therefore, we propose our baseline hypothesis:

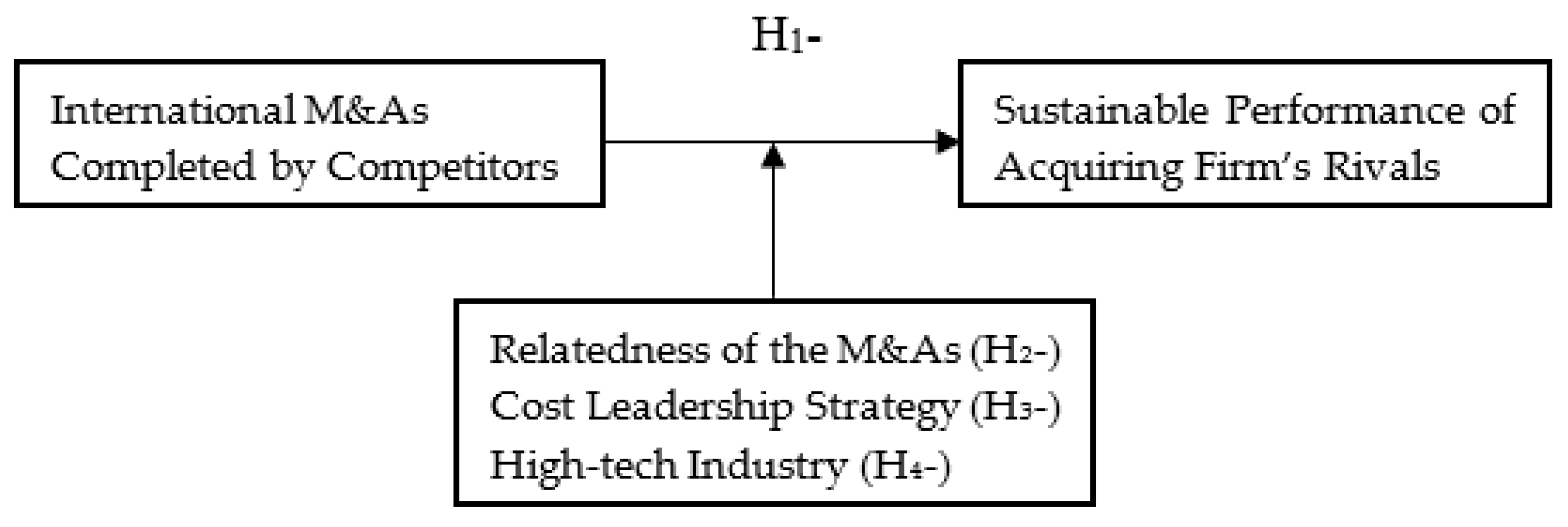

Hypothesis 1.

International M&As completed by competitors are negatively related to the sustainable performance of acquiring firms’ rivals.

After discussing the relationship between international M&As and the sustainable performance of acquiring firms’ rivals, we tend to find out whether the negative main effects may be accentuated or attenuated by the characteristics of the deal itself, rival firm, and industry. As for the deal characteristics, industry relatedness is one of the most commonly researched dimensions [28]. It is well established that acquirers benefit more in horizontal M&As than non-horizontal M&As [16,19] because acquirers can obtain operational synergy and financial synergy simultaneously, thus, receiving efficiency gains and placing rivals at a competitive disadvantageous position. The preponderance of empirical studies also found a positive association between acquiring firm post-acquisition performance and related M&As [32,33]. Therefore, we propose that,

Hypothesis 2.

The negative effects of international M&As completed by competitors on rivals’ sustainable performance are stronger for horizontal M&As than for non-horizontal M&As.

Besides the influence of industry relatedness at the deal level, we also consider the influence of rivals’ firm competitive strategy in the relationship between competitors’ international M&As and their performance. We focus on the cost leadership competitive strategy, which emphasizes efficiency improvement [34]. It builds up firm competitive advantages through a low-cost position relative to its rivals. To achieve such a position, firms have to minimize their costs for production, operation, advertising, and R&D activities [34]. In other words, firms that pursue superior performance through cost leadership strategy highly depend on efficiency improvements. Considering our conjecture that the main mechanism in our research context through which international M&As completed by competitors affect rivals’ performance is the efficiency gains for those acquirers, we surmise the negative impacts of international M&As on rivals’ performance will become stronger when rivals implement a cost leadership strategy. Because the shock to rivals induced by efficiency gains for acquirers will be amplified when a firm has a higher degree of dependence on efficiency. Therefore, we hypothesize that,

Hypothesis 3.

The negative effects of international M&As completed by competitors on rivals’ sustainable performance are stronger when rivals are implementing the cost leadership strategy.

Besides the efficiency gains mechanism proposed in previous literature, we suggest taking strategic assets gains mechanism into consideration when examining the effects of competitors’ international M&As on rivals’ performance. Because the relative positions of acquirers and their rivals can be changed through strategic assets gains for acquirers. China as a specific representative of EMs provides an ideal research context to test our conjecture. Because the idiosyncratic role played by international M&As to seek strategic assets is more prominent for acquiring firms in EMs. Theoretical perspectives like the springboard view [1,2] and Linkage–leverage–learning framework [35,36] both assert that EMEs use international M&As to access and source superior resources (e.g., advanced technology). Plenty of empirical studies provide supportive evidence for the theoretical arguments. For instance, Awate, Larsen, and Mudambi [31,37] found that the momentum for Indian leading turbine manufacturing firm initiating international M&As is to source knowledge globally Zhu and Zhu [38] review article also revealed that the motivation for Chinese firms conducting international M&As changed from natural resources sourcing in the 1990s to technology seeking in the 2000s.

Consistent with the prediction of the resource-based view, which asserts that acquirers can develop sustainable competitive advantages based on the strategic assets that are valuable, scarce, inimitable, and non-substituted [39], many empirical studies have detected the resource-deepening and resource extension effects of international M&As for acquirers [40,41]. Acquirers can probably leverage strategic assets obtained from international M&As and provide customers with upgraded products with higher added value, thus resulting in adverse impacts on rival firms.

Given technological competencies are more critical for high-tech firms to achieve sustainable competitive advantages than non-high-tech firms, and international M&As function as springboards to compensate and upgrade acquirers’ technological competencies, we surmise that the negative effects of international M&As on rivals’ sustainable performance for the high-tech industry will be stronger than the non-high-tech industry. Namely, high-tech acquirers will place their rivals to a more competitive disadvantageous position after obtaining vital technological resources through international M&As, and high-tech rival firms’ sustainable performance will be more adversely affected by competitors’ international M&As activities. Therefore, we expect,

Hypothesis 4.

The negative effects of international M&As completed by competitors are stronger for high-tech industry than for non-high-tech industry.

Figure 1 shows the overall research framework.

3. Methods

3.1. Data Sources

To test our hypotheses, we use longitudinal panel data with a sample that consisted of Chinese public firms in manufacturing industries where large international M&As have been completed during the years 2009–2015. We limited our sample to large international M&As with transaction value greater than $1 million USD because large M&As have more strategic importance for acquiring firms and are more likely to affect their rivals [14,42]. This criterion resulted in 325 international M&As completed by 205 public manufacturing firms during our research periods. 225 of those M&As are horizontal M&As, and the target firms in 271 of the M&As are from developed countries (regions). From the year 2009 to 2015, 7, 14, 32, 44, 44, 68, and 116 international M&As were completed, respectively.

To identify rivals, we first identified the sub-industries that the acquirers belonged to by applying the sub-industry level of the Global Industry Classification Standard (GICS) and made sure there was at least one more rival firm besides acquiring firms in the same sub-industries. Then, we excluded all firms with experiences of special treatment or backdoor listing to mitigate confounding effects. Finally, our sample contained 5656 firm-year observations from 1126 rival firms in 34 subindustries that had not initiated any international M&As during our research periods. The 34 subindustries included commodity chemicals, electrical components and equipment, industrial machinery, pharmaceuticals, electronic equipment and instruments, etc.

We collected the international M&As data from the Wind Economic Database (supported by a leading provider of financial databases of Chinese listed firms), the Zephyr BvD database, and corporate annual reports. All the firms’ financial and basic information data is gathered from the Wind database.

3.2. Measurements

Dependent variable

Rival firms’ sustainable performance. Following the measurements used for acquiring firms’ long-term performance in existing literature [42,43,44], we used the change in the rival’s return on assets (ROA) from 1 year before the acquisition to n years after the M&A to measure the rival firm’s sustainable performance. Considering scholars usually employ 1–3 year window to examine acquisition effects [45], our dependent variables were calculated from year t-1 to year t+1 (Roa1), year t+2 (Roa2), year t+3 (Roa3) respectively, as well as from year t−1 to the average ROA changes over the period from year t+1 to year t+3 (Roaa).

Independent variable

International M&As completed by competitors. Our independent variable is an industry level variable, and we measured it by the total number of international M&As completed by all firms in the subindustry each year (Qim&a).

Moderators

Industry Relatedness. Scholars generally adopt a binary variable to measure whether acquirers and targets are industry-related based on their primary industry code [14]. However, this is not applicable for our study, instead, we used a continuous variable to measure industry relatedness of the international M&As because our variable is the aggregate amount of international M&As completed by firms in the whole subindustry each year and the number is usually larger than one. Therefore, we measured industry relatedness by two count variables, namely, the number of horizontal (Qhim&a) and non-horizontal (Qnhim&a) international M&As. To detect the moderation effects of industry relatedness, we will compare whether the coefficients for the two variables are significantly different.

Cost Leadership Strategy(CLS). Like Duanmu, Bu, and Pittman [46], we followed the operationalization for the cost leadership strategy of Gao et al. [47] with one modification. In Gao et al.’s [47] research, they measured cost leadership strategy by the ratio of production cost to total sales, and small values indicate stronger cost leadership. In our study, we adopted the ratio of total sales to production cost to measure CLS, and larger values indicate stronger cost leadership. So that our results are more straightforward for interpretation [46].

High-tech industry We used a dummy variable (High-tech) to measure whether rival firms are from high-tech subindustry based on the Classification of High-tech Industry (Manufacturing) (2017) document issued by the National Bureau of Statistics of China. It equals one (zero otherwise) when the rival is from high-tech subindustries, including pharmaceuticals, biotechnology, health care equipment, aerospace and defense, communications equipment, computer hardware, computer storage and peripherals, electronic equipment and instruments, electronic components, semiconductor equipment, and semiconductors.

Control Variables

To confirm that our results are not confounded by other factors, we control the influence of industry, year, and firm characteristics. We introduced 33 dummy variables (Industry) in our regression models for all the 34 subindustries. We also included year dummies (Year) for the seven years of our research periods. In terms of firm level, firm age, firm size, firm ownership, firm financial capabilities, innovation capabilities, and marketing capacities have been added in our models. Firm age is calculated based on the date firm registered. Firm Size is measured by the natural logarithm of the total employees. Three dummy variables are added into the models to measure four types of firm ownership, namely, state-owned ownership (Ownership_1), domestic private ownership (Ownership_2), foreign ownership (Ownership_3), and others (Ownership_4). We used Ownership_2, which dominated our sample, as the reference group. Firm financial capacity is calculated by the ratio of debt to total assets (Dbasst). Innovation capacity is measured by R&D intensity (R&D), which is calculated by R&D expenditures divided by sales each year. Firm marketing capacity (Marketing) is measured by the ratio of marketing expenditure to sales each year.

3.3. Analytical Strategy

We employ a panel data-analysis with the “fixed effects” model to test the relationship between the number of international M&As completed in industry and acquiring firms’ rival sustainable performance. To examine the moderation effects, we follow Hayes’s [48] recommendations to center the independent variables and moderators first, and then enter the interactions between centralized independent variables and moderators (i.e., MCLS, MHigh-tech in our models) into the regression models, respectively. After dropping some cases due to missing values for our control and independent variables, we were left with a sample of 4671 firm-year observations across 34 subindustry groups for the regression analysis.

4. Results

4.1. Descriptive Statistics

Table 1 reports descriptive statistics and correlations. Overall, the magnitude of the correlations suggests that multicollinearity is not a problem in each of our models. The number of international M&As is the sum of the number of horizontal and non-horizontal international M&As. Thus, correlations among the three variables are quite large, but they will be added in different models, respectively, as independent variables. Therefore, the strong correlations among them are not a problem for our analysis. The situation also applies to the large correlations among average Roa1, Roa2, Roa3, and Roaa. Roaa is the mean of Roa1, Roa2, and Roa3 (due to space limitation, we have not listed the correlations among Roa1, Roa2, and Roa3 in Table 1).

4.2. Main Effects

Table 2 presents the results of the ordinary least square (OLS) fixed-effects regressions models where we use the number of international M&As within the industry as the explanatory variable to test hypothesis 1. Model 1 is the baseline model only containing control variables. As for the firm ownership dummies, the domestic private-owned group with the most observations has been used as the reference group. Hypothesis 1 predicts the larger the number of international M&As in an industry, the more negative the sustainable performance of acquiring firms’ rivals will be. The coefficient of the number of international M&As in an industry (Qim&a) is negative and significant (p < 0.01) in model 2, indicating that hypothesis 1 is supported. More specifically, the differences among the coefficients of Oim&a in models 3, 4, and 5 indicate that the influence of Qim&a on rivals’ performance mainly occurs two years after the acquisitions completed. Because it usually takes acquirers two years to integrate targets before they can extract value from acquisition [49]. Thus, the negative influence of the international M&As on rivals’ performance is not significant for the first year after M&As.

4.3.1. Industry Relatedness

To test the moderation effects of industry relatedness of the international M&As, we added the number of horizontal international M&As (Qhim&a) and non-horizontal M&As (Qnhim&a) into different models, respectively, and Table 3 presents the results. The moderation effects can be identified if the coefficients of the two variables are significantly different. In hypothesis 2, we predicted that the negative influence of horizontal international M&As on rivals’ performance will be stronger compared with non-horizontal ones. The coefficient of the number of horizontal international M&As (Qhim&a) in model 6 is negative and significant (β = -0.099, p < 0.01), whereas the coefficient of the number of non-horizontal international M&As (Qnhim&a) in model 10 is negative but nonsignificant (β = −0.061, p = 0.260). Therefore, hypothesis 2 is supported. What is more, interesting results are found in model 7–9 and model 11–12 where rivals’ performance of 1–3 years after the M&As are treated as the dependent variables. Significant differences exist in the coefficients of the number of horizontal (Qhim&a) and non-horizontal M&As (Qnhim&a). It indicates non-horizontal international M&As only will engender negative influence on rivals’ performance in the first year after the M&As, whereas, the impacts of horizontal international M&As on rivals’ performance become significant two years after the M&As. Compared with the impacts of horizontal international M&As on rivals’ performance, non-horizontal M&As’ negative influence occurs earlier but lasts a shorter amount of time.

4.3.2. Cost Leadership Strategy

Table 4 shows the results for the moderation effects test of cost the leadership firm strategy in the high-tech industry. In hypothesis 3, we predicted a negative moderation effect of a firm’s cost leadership strategy on the association between the number of international M&As and rivals’ sustainable performance. The coefficient of the interaction (MCLS) of the firm cost leadership strategy and the independent variable in model 14 is negative and significant (β =-1.328, p < 0.01), suggesting that rivals’ sustainable performance will become more negative in the presence of their cost leadership strategy. Thus, hypothesis 3 is supported. Models 15, 16, and 17 show that the magnitude of negative moderation effects of cost leadership strategy become larger and larger after the acquisition is completed, and the negative effects become significant immediately after the international M&As.

4.3.3. The High-Tech Industry

Hypothesis 4 predicts that the negative influence of international M&As on rivals’ sustainable performance will be stronger for the high-tech industry than the non-high-tech industry. The coefficient of the interaction (MHigh-tech) of the high-tech dummy and independent variable is negative and significant (β = −0.124, p < 0.01) shown in model 18, thus supporting hypothesis 4. In addition, model 19–21 indicate the moderation effects of the high-tech industry start in the second year after the M&As.

In order to test the robustness of our findings, we measured international M&As within the industry by the total transaction value in millions of dollars USD. We did not see qualitative differences compared with our results measuring the independent variable in the number of international M&As (please see the results of the robustness check in Appendix Table A1, Table A2 and Table A3), indicating our results are robust.

5. Discussions

5.1. Contributions

Based on longitudinal data of Chinese public manufacturing firms from the year 2009 to 2015, we empirically examined the effects of international M&As completed by competitors within the industry on rival firms’ sustainable performance. The results of OLS regression with fixed effects indicate that competitors’ international M&As will negatively influence rivals’ sustainable performance for three post-acquisition years. As for individual year effects, the negative effects start being significant two years after competitors’ international M&As and become even stronger in the third year. The conclusions are consistent with the findings in the literature, which discloses that acquirers need several years to integrate and obtain synergies from M&As [50]. Thus, the negative effect on rivals will not immediately become significant, but with the processing of integration, the negative effects and their magnitude will become significant and larger.

Our study also found the negative association between competitors’ international M&As and rivals’ sustainable performance is contingent on the characteristics of the deal, rival firm’s competitive strategy, and the industry. The overall negative effects will become stronger when the international M&As are horizontal rather than non-horizontal. This confirms the conventional wisdom that acquirers generally benefit more from related acquisitions [16]. Rivals’ cost leadership strategy also accentuates the association, providing robust support for industrial organization literature’s argument that acquirers extract value from M&As through efficiency gains, which causes negative product/factor price effects for rivals [15].

In addition, whether rivals are from the high-tech industry or not also makes a difference. For rivals in the high-tech industry, the negative effects of international M&As on their sustainable performance will be strengthened. It is easier to understand the results from the strategic management perspective, and the resource-based view (RBV) is one appropriate theoretical lens to be applied. Acquirers may build up sustainable competitive advantages through strategic assets [39] obtained by international M&As, adversely placing their rivals in a disadvantageous position. The argument is especially true for the high-tech industry, where firms’ competitive advantages rely heavily on strategic technology assets.

Our study makes three contributions to the research on M&As and sustainability. First, we shift the research pendulum from focusing the M&As’ effects on acquirers’ performance to their rivals’, which responds the call to shed light on the influence of M&As on the sustainability of acquirers’ external stakeholders [3]. Our results confirm the conventional wisdom of industrial organization literature that acquirers benefit from operational and financial synergy, which in turn is harmful to rivals’ performance. What is more, our research reveals the effects of competitors’ international M&As on rivals’ sustainable performance measured by long-term profitability, whereas the previous studies only focus on the effects on rivals’ short-term market reactions. Compared with market reactions, profitability is more critical for a firm’s sustainability.

Second, our study complements the existing related research from a strategic management perspective by disclosing other paths of how competitors’ international M&As will influence rivals’ sustainable performance and that strategic assets gain effects that are justified by the resource-based view.

Finally, we found the moderation effects of industry relatedness of the M&A deal, rivals’ cost leadership strategy, and the high-tech industry. These findings further enrich our understanding of the effects of competitors’ international M&As activities on rivals’ sustainable performance and provide robust support for the efficiency gains and strategic asset gains mechanism.

5.2. Practical Implications

This study also generates several practical implications for firms’ strategic management to deal with rival’s international M&As towards sustainable competitive advantages and sustainable performance.

First, rivals of acquiring firms should embrace the competitive dynamics, be more aware of their competitors’ international M&As activities, and not be deluded by the positive short-term market reactions along with those M&As [14,17]. This is because our study shows that international M&As will create both efficiency gains and strategic gains for acquiring firms, which in turn will lead to competitive disadvantages for rival firms. Especially for horizontal international M&As, the negative influence will not be released immediately. However, with the accomplishment of acquirers’ integration, their negative impacts are stronger and last longer than non-horizontal international M&As.

Second, our study shows that the negative shock from competitors’ international M&As are stronger and even start earlier for firms implementing a cost leadership strategy. This reminds rival firms that they should adjust their cost structure and improve efficiency in order to cope with the potential negative impacts engendered by competitor’s international M&As. Especially for the firms that are competing in emerging markets such as China, India, and Brazil, the industry dynamics and competitive intensity are much higher than that of developed markets. Firms that cannot adjust their management strategy according to the industry dynamics will not only lose the share of the current market but also will risk losing sustainable competitive advantages.

Finally, firms operating in the high-tech industry should pay more attention to build up sustainable competitive advantages from strategic assets as early as possible. As shown in this study, compared with non-high-tech firms, high-tech firms’ sustainable competitive advantages rely more on strategic assets, such as cutting-edge technology [51] and management know-how [52]. Acquirers in the high-tech industry compensate for their strategic assets deficiencies through international M&As. As a result, the negative shock for their rivals will be stronger than firms in the non-high-tech industry. In today’s global context, international M&As are increasingly used as a springboard to obtain strategic assets to compensate acquires’ competitive weakness, and competitors may exceed itself by initiating the aggressive measures. Therefore, it is necessary for firms to develop or nurture their own strategic assets to cope with the potential negative shocks triggered by competitors’ international M&As.

6. Conclusions

One important consideration of the sustainability concept is related to the impact of a firm’s behavior on its outside stakeholders rather than shareholders [9]. The spillover effect of international M&As on the sustainable performance of their external stakeholders, i.e. other firms and the whole industry, is an important but understudied topic of research on sustainability in M&As [3]. Using a longitudinal sample of international M&As completed by public manufacturing firms in China during 2009–2015, our empirical study shows that international M&As completed by emerging market enterprises would adversely affect their rivals’ sustainable performance, and the negative effects will be stronger for horizontal international M&As compared with non-horizontal M&As. Besides, the negative relationship will be accentuated when rivals implement a cost leadership strategy and when rivals are from high-tech industry. Our empirical results confirm that conventional efficiency gains are justified by industrial organization literature and provide supportive evidence for strategic assets gains for acquirers from strategic management perspectives. Theoretical contributions and practical implications for firms’ sustainable development are discussed. Consider the institutional and cultural differences within emerging markets, between emerging markets and developed markets, future research could draw from this study and further look at the impact of EMEs’ international M&As in different institutional contexts and compare the differences between international M&As and domestic M&As completed by firms from emerging markets. In this way, management scholars could contribute more novel knowledge to the research on sustainability in M&As.

Author Contributions

Conceptualization, X.H. and X.Y.; Data curation, X.H.; Formal analysis, X.H.; Funding acquisition, Z.J. and J.L.; Methodology, X.H.; X.Y. and J.L.; Project administration, J.L.; Resources, Z.J. and J.L.; Supervision, Z.J. and J.L.; Writing – original draft, X.H.; X.Y.; Writing—review & editing, X.Y.; X.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by National Natural Science Foundation of China (Grant No.:71941026), and the MOE Project of Key Research Institute of Humanities and Social Sciences at Universities (Grant No.: 16JJD630005).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

International M&As in the following models are measured in the sum transaction value within the industry.

{kind=link}

Table A1.

OLS fixed-effects regression models for rivals’ performance.

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Roaa | Roa1 | Roa2 | Roa3 | |

| Qim&a | −0.001 *** | −0.000 | −0.001 *** | −0.001 *** |

| (−4.00) | (−0.57) | (−4.58) | (−4.29) | |

| Controls | Firm Age, Ownership, Size, Debt to Asset Ratio, R&D Intensity, and Marketing Intensity included | |||

| _cons | 16.077 *** | 9.792 *** | 20.379 *** | 18.061 *** |

| (9.35) | (4.88) | (9.46) | (8.06) | |

| N | 4671 | 4671 | 4671 | 4671 |

| R2 | 0.073 | 0.043 | 0.073 | 0.092 |

Notes: *, ** and *** represent significance levels of 10%, 5% and 1% respectively; T value is shown in brackets in the table.

Table A2.

Moderation effects of industry relatedness.

| Variables | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) |

|---|---|---|---|---|---|---|---|---|

| Roaa | Roa1 | Roa2 | Roa3 | Roaa | Roa1 | Roa2 | Roa3 | |

| Qhim&a | −0.001 *** | −0.000 | −0.001 *** | −0.001 *** | ||||

| (−4.03) | (−0.41) | (−4.72) | (−4.37) | |||||

| Qnhim&a | 0.001 | −0.004 | 0.003 | 0.002 | ||||

| (0.33) | (−1.64) | (1.42) | (0.86) | |||||

| Controls | Firm Age, Ownership, Size, Debt to Asset Ratio, R&D Intensity, and Marketing Intensity included | |||||||

| _cons | 16.118 *** | 9.844 *** | 20.407 *** | 18.102 *** | 17.092 *** | 9.731 *** | 21.989 *** | 19.557 *** |

| (9.38) | (4.91) | (9.48) | (8.08) | (10.00) | (4.89) | (10.26) | (8.77) | |

| N | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 |

| R2 | 0.073 | 0.043 | 0.073 | 0.092 | 0.069 | 0.043 | 0.068 | 0.088 |

Notes: *, ** and *** represent significance levels of 10%, 5% and 1% respectively; T value is shown in brackets in the table.

Table A3.

Moderation effects of cost leadership strategy and high-tech industry.

| Variables | (13) | (14) | (15) | (16) | (17) | (18) | (19) | (20) |

|---|---|---|---|---|---|---|---|---|

| Roaa | Roa1 | Roa2 | Roa3 | Roaa | Roa1 | Roa2 | Roa3 | |

| Qim&a | −0.001 *** | −0.000 | −0.001 *** | −0.001 *** | −0.001 *** | −0.000 | −0.001 *** | −0.001 ** |

| (−3.99) | (−0.54) | (−4.57) | (−4.30) | (−2.70) | (−0.75) | (−3.38) | (−2.28) | |

| CLS | −2.936 *** | 0.156 | −3.410 *** | −5.555 *** | ||||

| (−3.98) | (0.18) | (-3.69) | (−5.79) | |||||

| MCLS | −0.007 *** | −0.004 *** | −0.009 *** | −0.008 *** | ||||

| (−6.30) | (−3.33) | (−6.17) | (−5.58) | |||||

| High-tech | 1.720 | 1.867 | 1.571 | 1.721 | ||||

| (1.49) | (1.39) | (1.09) | (1.15) | |||||

| MHigh-tech | −0.000 | 0.000 | −0.000 | −0.001 ** | ||||

| (−1.04) | (0.44) | (−0.66) | (−2.16) | |||||

| Controls | Firm Age, Ownership, Size, Debt to Asset Ratio, R&D Intensity, and Marketing Intensity included | |||||||

| _cons | 16.453 *** | 9.442 *** | 20.782 *** | 19.134 *** | 15.511 *** | 9.297 *** | 19.871 *** | 17.366 *** |

| (9.55) | (4.68) | (9.62) | (8.53) | (8.86) | (4.55) | (9.05) | (7.61) | |

| N | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 |

| R2 | 0.086 | 0.046 | 0.084 | 0.106 | 0.074 | 0.043 | 0.073 | 0.094 |

Notes: *, ** and *** represent significance levels of 10%, 5% and 1% respectively; T value is shown in brackets in the table.

References

- Luo, Y.; Tung, R.L. International expansion of emerging market enterprises: A springboard perspective. J. Int. Bus. Stud. 2007, 38, 481–498. [Google Scholar] [CrossRef]

- Luo, Y.; Tung, R.L. A general theory of springboard MNEs. J. Int. Bus. Stud. 2018, 49, 129–152. [Google Scholar] [CrossRef]

- González-Torres, T.; Rodríguez-Sánchez, J.-L.; Pelechano-Barahona, E.; García-Muiña, F.E. A Systematic Review of Research on Sustainability in Mergers and Acquisitions. Sustainability 2020, 12, 513. [Google Scholar] [CrossRef] [Green Version]

- Ai, Q.; Tan, H. Uncovering neglected success factors in post-acquisition reverse capability transfer: Evidence from Chinese multinational corporations in Europe. J. World Bus. 2020, 55, 101053. [Google Scholar] [CrossRef]

- Deng, P.; Yang, M. Cross-border mergers and acquisitions by emerging market firms: A comparative investigation. Int. Bus. Rev. 2015, 24, 157–172. [Google Scholar] [CrossRef] [Green Version]

- Gubbi, S.R.; Aulakh, P.S.; Ray, S.; Sarkar, M.B.; Chittoor, R. Do international acquisitions by emerging-economy firms create shareholder value? The case of Indian firms. J Int Bus Stud. 2010, 41, 397–418. [Google Scholar] [CrossRef]

- Rodríguez-Sánchez, J.-L.; Mora-Valentín, E.-M.; Ortiz-de-Urbina-Criado, M. Successful Human Resources Management Factors in International Mergers and Acquisitions. Adm. Sci. 2018, 8, 45. [Google Scholar] [CrossRef] [Green Version]

- Kumar, V.; Singh, D.; Purkayastha, A.; Popli, M.; Gaur, A. Springboard internationalization by emerging market firms: Speed of first cross-border acquisition. J. Int. Bus. Stud. 2019. [Google Scholar] [CrossRef]

- Purvis, B.; Mao, Y.; Robinson, D. Three pillars of sustainability: in search of conceptual origins. Sustain. Sci. 2019, 14, 681–695. [Google Scholar] [CrossRef] [Green Version]

- Stigler, G.J. Monopoly and oligopoly by merger. Am. Econ. Rev. 1950, 40, 23–34. [Google Scholar]

- Stigler, G.J. A theory of oligopoly. J. Polit. Econ. 1964, 72, 44–61. [Google Scholar] [CrossRef]

- Eckbo, B.E. Horizontal mergers, collusion, and stockholder wealth. J. Financ. Econ. 1983, 11, 241–273. [Google Scholar] [CrossRef]

- Eckbo, B.E. Mergers and the market concentration doctrine: Evidence from the capital market. J. Bus. 1985, 58, 325–349. [Google Scholar] [CrossRef]

- Gaur, A.S.; Malhotra, S.; Zhu, P. Acquisition announcements and stock market valuations of acquiring firms’ rivals: A test of the growth probability hypothesis in China. Strateg. Manag. J. 2013, 34, 215–232. [Google Scholar] [CrossRef]

- Chatterjee, S. Types of Synergy and Economic Value: The Impact of Acquisitions on Merging and Rival Firms. Strateg. Manag. J. 1986, 7, 119–139. [Google Scholar] [CrossRef]

- Lubatkin, M. Mergers and the Performance of the Acquiring Firm. Acad. Manage. Rev. 1983, 8, 218. [Google Scholar]

- Clougherty, J.A.; Duso, T. The impact of horizontal mergers on rivals: gains to being left outside a merger. J. Manag. Stud. 2009, 46, 1365–1395. [Google Scholar] [CrossRef] [Green Version]

- Haleblian, J.; Devers, C.E.; McNamara, G.; Carpenter, M.A.; Davison, R.B. Taking Stock of What We Know About Mergers and Acquisitions: A Review and Research Agenda. J. Manage. 2009, 35, 469–502. [Google Scholar] [CrossRef]

- Steiner, P.O. Mergers: Motives, Effects, Policies; University of Michigan Press: Ann Arbor, MI, USA, 1975. [Google Scholar]

- Valentini, G. Measuring the effect of M&A on patenting quantity and quality. Strateg. Manag. J. 2012, 33, 336–346. [Google Scholar]

- Uhlenbruck, K.; Hughes-Morgan, M.; Hitt, M.A.; Ferrier, W.J.; Brymer, R. Rivals’ reactions to mergers and acquisitions. Strateg. Organ. 2017, 15, 40–66. [Google Scholar] [CrossRef]

- Meyer, K.E.; Sinani, E. When and where does foreign direct investment generate positive spillovers? A meta-analysis. J. Int. Bus. Stud. 2009, 40, 1075–1094. [Google Scholar] [CrossRef]

- Francis, B.B.; Hasan, I.; Sun, X.; Waisman, M. Can firms learn by observing? Evidence from cross-border M&As. J. Corp. Finance. 2014, 25, 202–215. [Google Scholar]

- Song, M.H.; Walkling, R.A. Abnormal returns to rivals of acquisition targets: A test of the acquisition probability hypothesis’. J. Financ. Econ. 2000, 55, 143–171. [Google Scholar] [CrossRef]

- Akhigbe, A.; Martin, A.D. Information-signaling and competitive effects of foreign acquisitions in the US. J. Bank. Financ. 2000, 24, 1307–1321. [Google Scholar] [CrossRef]

- Prager, R.A. The effects of horizontal mergers on competition: The case of the Northern Securities Company. RAND J. Econ. 1992, 23, 123–133. [Google Scholar] [CrossRef]

- Kim, E.H.; Singal, V. Mergers and market power: Evidence from the airline industry. Am. Econ. Rev. 1993, 83, 549–569. [Google Scholar]

- King, D.R.; Dalton, D.R.; Daily, C.M.; Covin, J.G. Meta-analyses of post-acquisition performance: Indications of unidentified moderators. Strateg. Manag. J. 2004, 25, 187–200. [Google Scholar] [CrossRef] [Green Version]

- Elango, B.; Dhandapani, K.; Giachetti, C. Impact of institutional reforms and industry structural factors on market returns of emerging market rivals during acquisitions by foreign firms. Int. Bus. Rev. 2019, 28, 101493. [Google Scholar] [CrossRef]

- Hopkins, H.D. Acquisition strategy and the market position of acquiring firms. Strateg. Manag. J. 1987, 8, 535–547. [Google Scholar] [CrossRef]

- Awate, S.; Larsen, M.M.; Mudambi, R. EMNE catch-up strategies in the wind turbine industry: Is there a trade-off between output and innovation capabilities? Glob. Strategy J. 2012, 2, 205–223. [Google Scholar] [CrossRef]

- Haleblian, J.; Finkelstein, S. The Influence of Organizational Acquisition Experience on Acquisition Performance: A Behavioral Learning Perspective. Adm. Sci. Q. 1999, 44, 29–56. [Google Scholar] [CrossRef]

- King, D.R.; Slotegraaf, R.J.; Kesner, I. Performance Implications of Firm Resource Interactions in the Acquisition of R&D-Intensive Firms. Organ. Sci. 2008, 19, 327–340. [Google Scholar]

- Porter, M. Creating and Sustaining Superior Performance; The Free Press: Glencoe, IL, USA, 1985. [Google Scholar]

- Mathews, J.A. Dragon Multinational: A New Model for Global Growth; Oxford University Press: Oxford, NY, USA, 2002. [Google Scholar]

- Mathews, J.A. Dragon multinationals: New players in 21st century globalization. Asia Pac. J. Manag. 2006, 23, 5–27. [Google Scholar] [CrossRef]

- Awate, S.; Larsen, M.M.; Mudambi, R. Accessing vs sourcing knowledge: A comparative study of R&D internationalization between emerging and advanced economy firms. J. Int. Bus. Stud. 2015, 46, 63–86. [Google Scholar]

- Zhu, H.; Zhu, Q. Mergers and acquisitions by Chinese firms: A review and comparison with other mergers and acquisitions research in the leading journals. Asia Pac. J. Manag. 2016, 33, 1107–1149. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Gubbi, S.R.; Elango, B. Resource deepening vs. resource extension: Impact on asset-seeking acquisition performance. Manag. Int. Rev. 2016, 56, 353–384. [Google Scholar] [CrossRef]

- Karim, S.; Mitchell, W. Path-dependent and path-breaking change: reconfiguring business resources following acquisitions in the U.S. medical sector, 1978–1995. Strateg. Manag. J. 2000, 21, 1061–1081. [Google Scholar] [CrossRef]

- Meyer-Doyle, P.; Lee, S.; Helfat, C.E. Disentangling the microfoundations of acquisition behavior and performance. Strateg. Manag. J. 2019, 41, 1733–1756. [Google Scholar] [CrossRef]

- Ellis, K.M.; Reus, T.H.; Lamont, B.T.; Ranft, A.L. Transfer effects in large acquisitions: How size-specific experience matters. Acad. Manage. J. 2011, 54, 1261–1276. [Google Scholar] [CrossRef]

- Zollo, M.; Singh, H. Deliberate learning in corporate acquisitions: post-acquisition strategies and integration capability in US bank mergers. Strateg. Manag. J. 2004, 25, 1233–1256. [Google Scholar] [CrossRef]

- Desyllas, P.; Hughes, A. Do high technology acquirers become more innovative? Res. Policy 2010, 39, 1105–1121. [Google Scholar] [CrossRef]

- Duanmu, J.-L.; Bu, M.; Pittman, R. Does market competition dampen environmental performance? Evidence from China. Strat. Mgmt. J. 2018, 39, 3006–3030. [Google Scholar] [CrossRef] [Green Version]

- Gao, G.Y.; Murray, J.Y.; Kotabe, M.; Lu, J. A “strategy tripod” perspective on export behaviors: Evidence from domestic and foreign firms based in an emerging economy. J. Int. Bus. Stud. 2010, 41, 377–396. [Google Scholar] [CrossRef] [Green Version]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach; Guilford Publications: New York, NY, USA, 2017. [Google Scholar]

- Morosini, P.; Shane, S.; Singh, H. National Cultural Distance and Cross-Border Acquisition Performance. J. Int. Bus. Stud. 1998, 29, 137–158. [Google Scholar] [CrossRef]

- Graebner, M.E.; Heimeriks, K.H.; Huy, Q.N.; Vaara, E. The Process of Postmerger Integration: A Review and Agenda for Future Research. Acad. Manag. Ann. 2017, 11, 1–32. [Google Scholar] [CrossRef] [Green Version]

- Romero-Martínez, A.M.; García-Muiña, F.E.; Ghauri, P.N. International Inbound Open Innovation and International Performance. Can. J. Adm. Sci. 2017, 34, 401–415. [Google Scholar] [CrossRef]

- Yin, X.; Chen, J.; Zhao, C. Double Screen Innovation: Building sustainable core competence through knowledge management. Sustainability 2019, 11, 4266. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Research framework.

Table 1.

Descriptive statistics and correlations for rival firms of acquiring firms.

| Variables | N | Mean | S.d. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.Firmage | 5656 | 14.935 | 5.134 | 1.000 | |||||||||||||

| 2.Ownership_1 | 5656 | 0.046 | 0.209 | 0.090 * | 1.000 | ||||||||||||

| 3.Ownership_3 | 5656 | 0.350 | 0.477 | 0.054 * | −0.161 * | 1.000 | |||||||||||

| 4.Ownership_4 | 5656 | 0.035 | 0.183 | 0.031 * | −0.042 * | −0.139 * | 1.000 | ||||||||||

| 5.Firmsize | 5656 | 7.703 | 1.132 | 0.170 * | 0.014 | 0.385 * | −0.022 | ||||||||||

| 6.Dbasst | 5656 | 0.378 | 0.202 | 0.171 * | −0.029 * | 0.394 * | −0.091 * | 0.540 * | 1.000 | ||||||||

| 7.R&D | 5163 | 3.933 | 4.124 | −0.109 * | 0.128 * | 0.170 * | 0.012 | −0.288 * | −0.316 * | 1.000 | |||||||

| 8.Marketing | 5656 | 7.901 | 8.866 | 0.000 | 0.000 | 0.130 * | 0.022 | −0.073 * | −0.240 * | 0.120 * | 1.000 | ||||||

| 9.Qim&a | 5656 | 2.936 | 4.127 | 0.096 * | −0.014 | 0.133 * | 0.011 | −0.086 * | −0.142 * | 0.141 * | 0.167 * | 1.000 | |||||

| 10.Qhim&a | 5656 | 1.796 | 2.784 | 0.096 * | −0.017 | 0.124 * | 0.011 | −0.072 * | −0.136 * | 0.144 * | 0.182 * | 0.950 * | 1.000 | ||||

| 11.Qnhim&a | 5656 | 1.140 | 1.715 | 0.074 * | −0.006 | 0.120 * | 0.008 | −0.089 * | −0.120 * | 0.105 * | 0.106 * | 0.864 * | 0.664 * | 1.000 | |||

| 12.High-tech | 5656 | 0.268 | 0.443 | −0.011 | 0.049 * | 0.034 * | −0.030 * | −0.086 * | −0.215 * | 0.293 * | 0.304 * | 0.220 * | 0.259 * | 0.111 * | 0.243 * | 1.000 | |

| 13.CLS | 5656 | 0.063 | 0.213 | −0.155 * | 0.046 * | 0.211 * | 0.030 * | −0.200 * | −0.372 * | 0.283 * | 0.403 * | −0.012 | −0.011 | −0.010 * | −0.011 | 0.055 * | 1.000 |

| 14.Roaa | 5145 | −1.590 | 4.246 | 0.008 | 0.015 | 0.081 * | 0.002 | 0.022 | 0.162 * | −0.070 * | −0.036 * | −0.129 * | −0.123 * | −0.111 * | −0.127 * | −0.014 | −0.133 * |

| 15.Roa1 | 5145 | −0.738 | 4.599 | 0.018 | 0.013 | 0.035 * | 0.014 | 0.023 | 0.066 * | −0.056 * | 0.006 | −0.033 * | −0.018 | −0.051 * | −0.030 * | 0.008 | −0.025 |

| 16.Roa2 | 5145 | −1.590 | 5.115 | 0.011 | 0.015 | 0.075 * | 0.002 | 0.021 | 0.140 * | −0.047 * | −0.030 * | −0.125 * | −0.121 * | −0.105 * | −0.125 * | −0.010 | −0.118 * |

| 17.Roa3 | 5145 | −2.443 | 5.448 | −0.006 | 0.010 | 0.090 * | −0.010 | 0.012 | 0.191 * | −0.071 * | −0.060 * | −0.156 * | −0.159 * | −0.119 * | −0.155 * | −0.031 * | −0.178 * |

Notes: * shows significance at the 0.05 level.

Table 2.

Results for OLS fixed-effects regression models for rivals’ performance.

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Roaa | Roaa | Roa1 | Roa2 | Roa3 | |

| Firmage | −0.256 *** | −0.187 *** | −0.143 ** | −0.290 *** | −0.127 |

| (−4.63) | (−3.08) | (−2.02) | (−3.81) | (−1.61) | |

| Ownership_1 | 0.614 | 0.582 | 0.586 | 0.564 | 0.596 |

| (0.75) | (0.71) | (0.61) | (0.55) | (0.56) | |

| Ownership_3 | −0.472 | −0.530 | −0.317 | −0.648 | −0.627 |

| (−0.60) | (−0.67) | (−0.34) | (−0.65) | (−0.61) | |

| Ownership_4 | −0.588 | −0.613 | 0.805 | −0.469 | −2.177 |

| (−0.47) | (−0.50) | (0.56) | (−0.30) | (−1.35) | |

| Firmsize | −2.270 *** | −2.211 *** | −1.107 *** | −2.665 *** | −2.862 *** |

| (−9.84) | (−9.55) | (−4.11) | (−9.18) | (−9.48) | |

| Dbasst | 7.526 *** | 7.594 *** | 5.721 *** | 8.251 *** | 8.811 *** |

| (8.30) | (8.38) | (5.42) | (7.26) | (7.45) | |

| R&D | −0.013 | −0.011 | −0.057 | 0.054 | −0.031 |

| (−0.44) | (−0.38) | (−1.64) | (1.44) | (−0.80) | |

| Marketing | 0.012 | 0.011 | −0.018 | −0.014 | 0.067 * |

| (0.38) | (0.37) | (−0.51) | (−0.38) | (1.67) | |

| Qim&a | −0.071 *** | −0.038 | −0.078 ** | −0.097 *** | |

| (−2.72) | (−1.26) | (−2.38) | (−2.84) | ||

| _cons | 17.053 *** | 15.849 *** | 9.306 *** | 20.459 *** | 17.782 *** |

| (10.00) | (9.00) | (4.54) | (9.26) | (7.74) | |

| Year | Yes | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes | Yes |

| N | 4671 | 4671 | 4671 | 4671 | 4671 |

| Model F | 21.25 *** | 20.29 *** | 11.92 *** | 19.62 *** | 26.05 *** |

| R2 | 0.069 | 0.071 | 0.043 | 0.069 | 0.090 |

Notes: *, ** and *** represent significance levels of 10%, 5%, and 1% respectively; T value is shown in brackets in the table.

Table 3.

Results for OLS fixed-effects regression models for rivals’ performance and moderation effects of industry relatedness.

Table 3.

Results for OLS fixed-effects regression models for rivals’ performance and moderation effects of industry relatedness.

| Variables | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) |

|---|---|---|---|---|---|---|---|---|

| Roaa | Roa1 | Roa2 | Roa3 | Roaa | Roa1 | Roa2 | Roa3 | |

| Firmage | −0.200 *** | −0.176 *** | −0.291 *** | −0.133 * | −0.231 *** | −0.121 * | −0.363 *** | −0.209 *** |

| (−3.42) | (−2.58) | (−3.97) | (−1.74) | (−3.89) | (−1.75) | (−4.88) | (−2.70) | |

| Firmsize | −2.195 *** | −1.134 *** | −2.628 *** | −2.822 *** | −2.266 *** | −1.130 *** | −2.729 *** | −2.940 *** |

| (−9.46) | (−4.20) | (−9.04) | (−9.33) | (−9.82) | (−4.21) | (−9.43) | (−9.77) | |

| Dbasst | 7.632 *** | 5.691 *** | 8.318 *** | 8.886 *** | 7.519 *** | 5.668 *** | 8.175 *** | 8.714 *** |

| (8.42) | (5.39) | (7.32) | (7.52) | (8.29) | (5.37) | (7.19) | (7.37) | |

| R&D | -0.012 | −0.058 * | 0.053 | −0.032 | −0.012 | −0.056 | 0.052 | −0.033 |

| (-0.41) | (-1.66) | (1.43) | (−0.82) | (−0.41) | (−1.61) | (1.39) | (−0.85) | |

| Marketing | 0.012 | −0.018 | −0.014 | 0.068 * | 0.011 | −0.019 | −0.014 | 0.067 * |

| (0.40) | (−0.51) | (−0.35) | (1.70) | (0.36) | (−0.54) | (−0.37) | (1.67) | |

| Qhim&a | -0.099*** | −0.006 | −0.133 *** | −0.157 *** | ||||

| (-2.86) | (−0.16) | (−3.07) | (−3.48) | |||||

| Qnhim&a | −0.061 | −0.146 ** | −0.007 | −0.029 | ||||

| (−1.13) | (−2.33) | (−0.10) | (−0.42) | |||||

| _cons | 15.865*** | 9.878 *** | 20.181 *** | 17.538 *** | 16.758 *** | 9.245 *** | 21.746 *** | 19.283 *** |

| (9.05) | (4.83) | (9.18) | (7.67) | (9.71) | (4.61) | (10.05) | (8.57) | |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 |

| Model F | 20.35*** | 11.81*** | 19.91*** | 26.37 *** | 19.82 *** | 12.21 *** | 19.19 *** | 25.43 *** |

| R2 | 0.071 | 0.043 | 0.070 | 0.091 | 0.070 | 0.044 | 0.068 | 0.088 |

Notes: *, ** and *** represent significance levels of 10%, 5%, and 1% respectively; T value is shown in brackets in the table; Due to space limitation, regression results of firm ownership are omitted from the table.

Table 4.

Results for OLS fixed-effects regression models for rivals’ performance and moderation effects of firm strategy and high-tech industry.

Table 4.

Results for OLS fixed-effects regression models for rivals’ performance and moderation effects of firm strategy and high-tech industry.

| Variables | (14) | (15) | (16) | (17) | (18) | (19) | (20) | (21) |

|---|---|---|---|---|---|---|---|---|

| Roaa | Roa1 | Roa2 | Roa3 | Roaa | Roa1 | Roa2 | Roa3 | |

| Firmage | −0.233 *** | −0.148 ** | −0.344 *** | −0.208 *** | −0.215 *** | −0.139 * | −0.324 *** | −0.182 ** |

| (−3.86) | (−2.08) | (−4.54) | (−2.64) | (−3.50) | (−1.94) | (−4.21) | (−2.27) | |

| Firmsize | −2.093 *** | −1.031 *** | −2.525 *** | −2.724 *** | −2.177 *** | −1.107 *** | −2.625 *** | −2.799 *** |

| (−9.17) | (−3.83) | (−8.80) | (−9.15) | (−9.41) | (−4.10) | (−9.04) | (−9.28) | |

| Dbasst | 7.465 *** | 5.832 *** | 8.108 *** | 8.455 *** | 7.610 *** | 5.679 *** | 8.280 *** | 8.871 *** |

| (8.33) | (5.52) | (7.20) | (7.25) | (8.40) | (5.38) | (7.29) | (7.52) | |

| R&D | −0.004 | −0.055 | 0.063 * | −0.019 | −0.012 | −0.057 * | 0.053 | −0.032 |

| (−0.12) | (−1.59) | (1.71) | (−0.49) | (−0.41) | (−1.65) | (1.42) | (−0.83) | |

| Marketing | 0.057* | 0.000 | 0.040 | 0.132*** | 0.013 | −0.019 | −0.013 | 0.070 * |

| (1.88) | (0.01) | (1.03) | (3.32) | (0.42) | (−0.53) | (−0.33) | (1.76) | |

| Qim&a | −0.102 *** | −0.054 * | −0.115 *** | −0.138 *** | −0.023 | −0.044 | −0.021 | −0.005 |

| (−3.93) | (−1.78) | (−3.51) | (−4.06) | (-0.75) | (−1.21) | (−0.54) | (−0.13) | |

| CLS | −4.011 *** | −0.420 | −4.648 *** | −6.965 *** | ||||

| (−5.40) | (−0.48) | (−4.98) | (−7.20) | |||||

| MCLS | −1.328 *** | −0.750 *** | −1.572 *** | −1.662 *** | ||||

| (−10.27) | (−4.92) | (−9.67) | (−9.86) | |||||

| High-tech | 1.710 | 1.859 | 1.521 | 1.751 | ||||

| (1.49) | (1.38) | (1.05) | (1.17) | |||||

| MHigh-tech | −0.124 *** | 0.012 | −0.148 *** | −0.237 *** | ||||

| (−2.99) | (0.24) | (−2.83) | (−4.38) | |||||

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 | 4671 |

| R2 | 0.099 | 0.049 | 0.094 | 0.119 | 0.074 | 0.044 | 0.071 | 0.095 |

Notes: *, ** and *** represent significance levels of 10%, 5%, and 1% respectively; T value is shown in brackets in the table; regression results of firm ownership and constant terms are omitted from the table.

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hu, X.; Yin, X.; Jin, Z.; Li, J. How Do International M&As Affect Rival Firm’s Sustainable Performance? —Empirical Evidence from an Emerging Market. Sustainability 2020, 12, 1318. https://0-doi-org.brum.beds.ac.uk/10.3390/su12041318

AMA Style

Hu X, Yin X, Jin Z, Li J. How Do International M&As Affect Rival Firm’s Sustainable Performance? —Empirical Evidence from an Emerging Market. Sustainability. 2020; 12(4):1318. https://0-doi-org.brum.beds.ac.uk/10.3390/su12041318

Chicago/Turabian StyleHu, Xiaoting, Ximing Yin, Zhanming Jin, and Jizhen Li. 2020. "How Do International M&As Affect Rival Firm’s Sustainable Performance? —Empirical Evidence from an Emerging Market" Sustainability 12, no. 4: 1318. https://0-doi-org.brum.beds.ac.uk/10.3390/su12041318

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.