Designation of Origin Distillates in Mexico: Value Chains and Territorial Development

and

and

Abstract

:1. Introduction

2. Designations of Origin: Scope, Limitations and Links with Territorial Development

- (a)

- The unique organoleptic properties found in the territory (terroir) and its traditional production and processing methods, which may be difficult or impossible to reproduce in other regions or countries, thus providing a valuable and lasting competitive advantage.

- (b)

- The institutional structures or agreements inherent in many GIs with their capacity to enhance competitiveness when they can improve collective action and reduce transaction costs along the value chain.

- (c)

- The supply of enough information to reduce asymmetry between producers and consumers, creating a public benefit through improved market transparency and reduced information costs.

- (d)

- The construction of conceptual frameworks to promote an integrated and multifunctional model for rural development that is capable of promoting economic and social interests, as well as local values such as environmental management, culture and tradition.

- Identification: Awareness at the local level and evaluation of productive potential

- Qualification: Establishment of the rules related to the creation of value and the preservation of local resources

- Remuneration through the local system and marketing

- Reproduction of local resources in a way that reinforces sustainability

- Public policy on territorial matters that provides an institutional framework appropriate to the related initiatives, as well as a set of strategies that encourage all phases of the virtuous circle

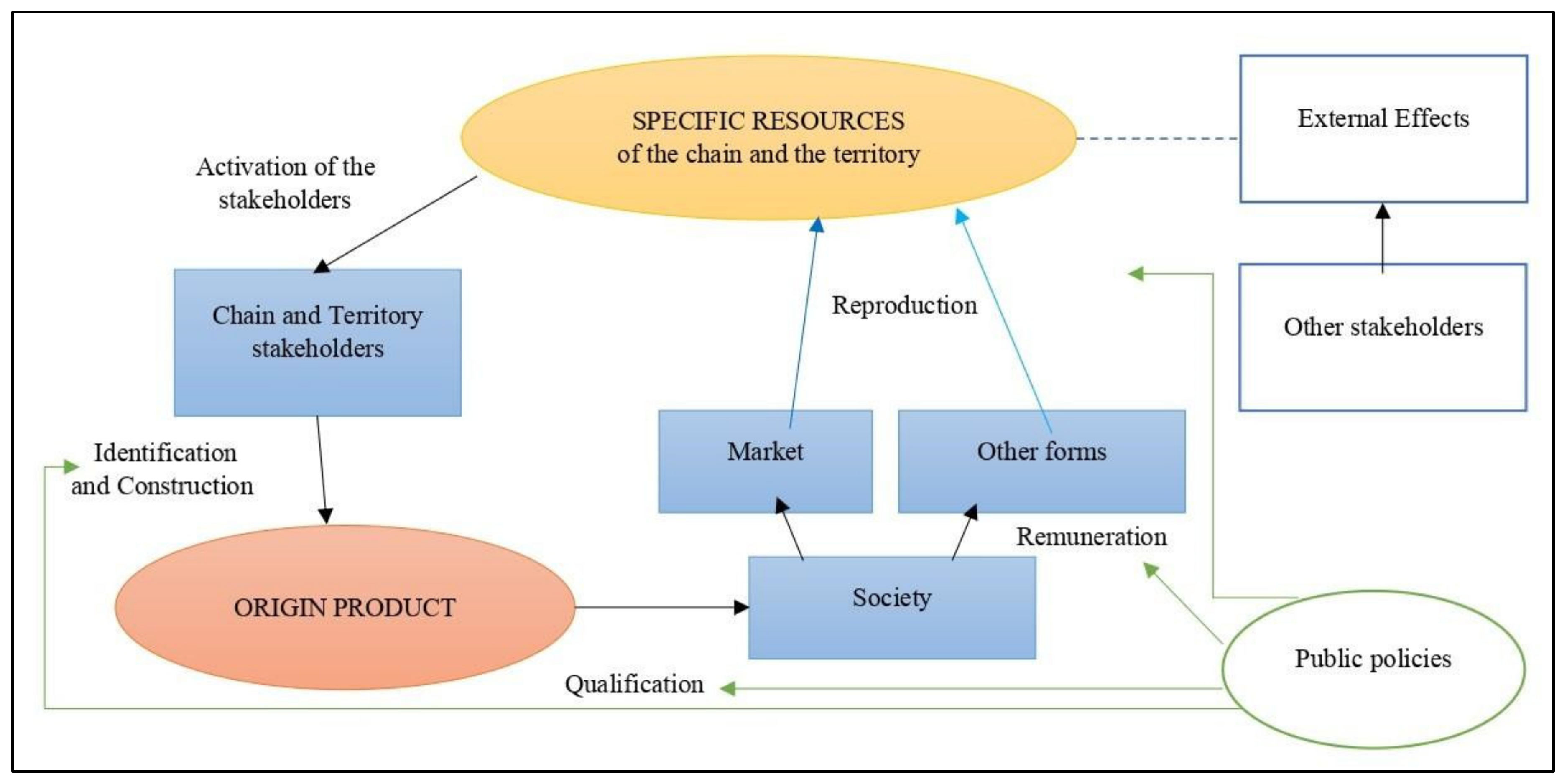

- Actors that are both local to and outside of the territory (production and marketing, public actors, non-governmental organizations, research and development centers) play a fundamental role throughout. Likewise, the institutional framework (i.e., public policy and regulation) plays an important role in the promotion and regulation of quality linked to geographic schemes. Figure 1 summarizes the virtuous circle:

- -

- Organizational structures and strong institutions to maintain, market and monitor the GI. This includes processes associated with virtuous circle identification and appropriate demarcation, organization of practices and existing standards, an adequate protection plan and commercialization of appropriate tools, which always require the creation of local level institutions and management structures that are willing to make a long-term commitment to participatory cooperation methods.

- -

- Equitable sharing between producers and companies in the GI’s protected region. Equity is achieved when local stakeholders who benefit from the GI not only share the costs and benefits, but also control and decision-making over their public goods.

- -

- Solvent commercial partners may commit to promoting and marketing the GI in the long-term. Many commercial successes with GIs are the result of consistent, long-term marketing and promotion efforts by creditworthy business partners.

- -

- Effective legal protection including a strong national protection system for the GI. Carefully chosen protection options will ensure effective monitoring and enforcement in the relevant markets to reduce the chances of fraud threatening its reputation and even its legal validity.

3. Value Chains for Boosting GIs

4. Materials and Methods

5. Results and Discussion of Mexican Designations of Origin and Marketing Chains

5.1. Institutional Framework

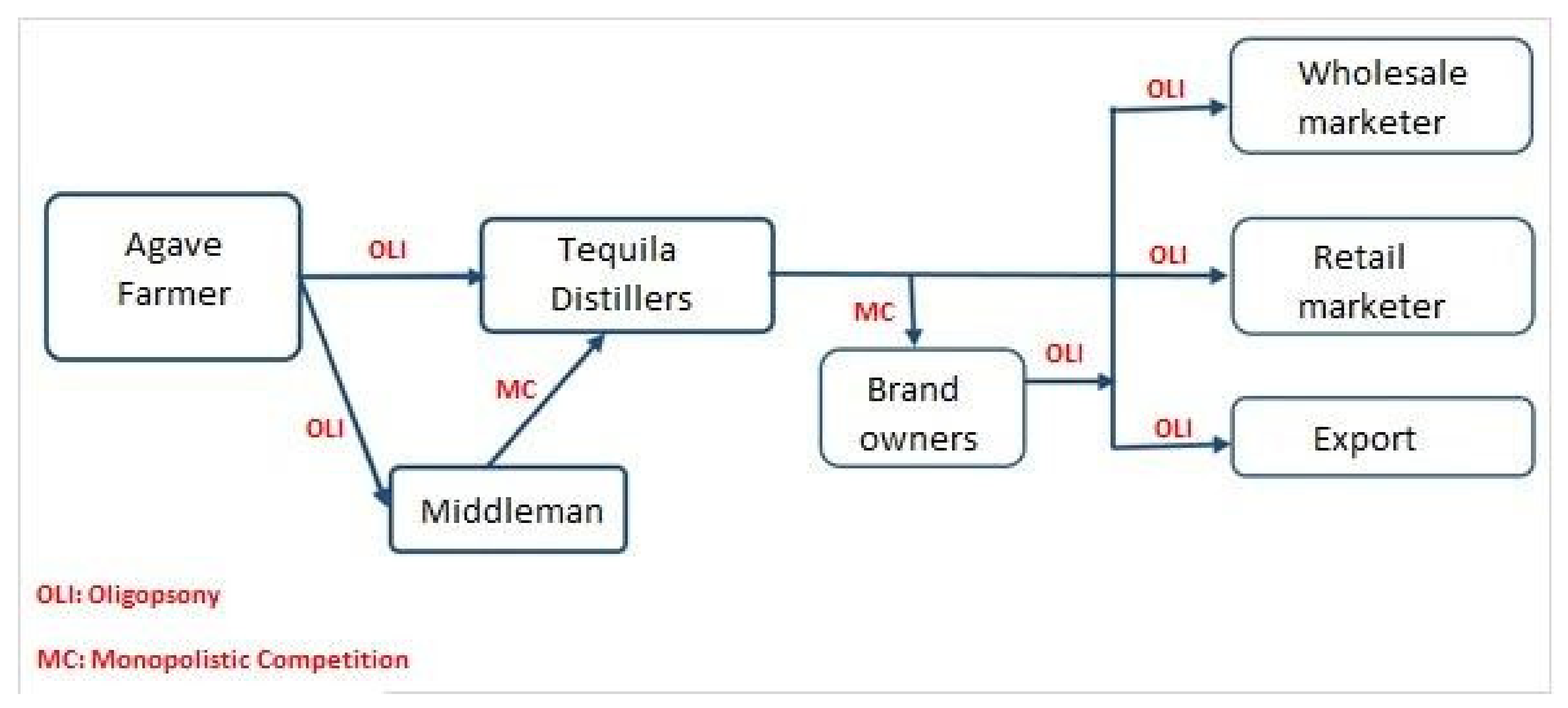

5.2. The Input–Output Dimension

5.3. The Geographic Scale

5.4. Governance

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Vandecandelaere, E.; Arfini, F.; Belletti, G.; Marescotti, A. Uniendo Personas, Territorios y Productos: Guía para Fomentar la Calidad Vinculada al Origen y a las Indicaciones Geográficas Sostenibles; FAO y SINER-GI: Rome, Italy, 2010; p. 194. ISBN 978-92-5-306656-8. [Google Scholar]

- MARCANET. Listado de Indicaciones Geográficas. 2020. Available online: https://marcanet.impi.gob.mx:8181/marcanet/vistas/common/datos/bsqIndicacionGeografica.pgi (accessed on 27 December 2020).

- Instituto Mexicano de Propiedad Industrial-IMPI. Ventajas de Contar con una Marca Colectiva. 2019. Available online: https://www.gob.mx/impi/articulos/ventajas-de-contar-con-una-marca-colectiva?fbclid=IwAR1AgSOeqBjySYLF5Yc8WuLLu4B8pjK57eokNzQgpqPuIQIiqYf-rD7xuwU (accessed on 30 December 2019).

- Renting, H.; Marsden, T.K.; Banks, J. Understanding alternative food networks: Exploring the role of short food supply chains in rural development. Environ. Plan. A Econ. Space 2003, 35, 393–411. [Google Scholar] [CrossRef] [Green Version]

- Ranaboldo, C.; Arosio, M. Vínculos rural-urbano: Cadenas cortas y sistemas alimentarios locales. In Serie Documentos de Trabajo (129); Programa Cohesión Territorial para el Desarrollo, RIMISP: Santiago, Chile, 2014. [Google Scholar]

- Boucher, F.; Riveros-Cañas, R.A.; Espinoza-Ortega, A. Inclusive and dynamic economic growth in rural areas: Alternatives from localized agri-food systems and short chains. In Proceedings of the 7th International Conference on Localized Agrifood Systems, Challenges for the New Rurality in a Changing World, Stockholm, Sweden, 8–10 May 2016. [Google Scholar]

- Torres-Salcido, G.; Sanz-Cañada, J. Territorial governance. A comparative research of Local Agro-food systems in México. Agriculture 2018, 8, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Delgadillo Macías, J.; Sanz-Cañada, J. Sistemas Agroalimentarios de Proximidad. Contextos Rururbanos en México y España. (Colección: Agenda Pública para el Desarrollo Regional, la Metropolización y la Sostentabilidad: 4); Universidad Nacional Autónoma de México, Instituto de Investigaciones Económicas: Mexico City, México, 2018; p. 277. ISBN UNAM 978-607-30-0872-3. [Google Scholar]

- Gereffi, G. The organization of buyer-driven global commodity chains: How U.S. retailers shape overseas production networks. In Commodity Chains and Global Capitalism; Gereffi, G., Korzeniewicz, M., Eds.; Praeger Publishers: Westport, CT, USA, 1994; pp. 95–122. [Google Scholar]

- Organización Mundial de la Propiedad Intelectual—OMPI. Las indicaciones geográficas: Introducción. Publicación OMPI. 2007, 952, 1–42. Available online: http://www.wipo.int/edocs/pubdocs/es/geographical/952/wipo_pub_952.pdf (accessed on 22 January 2020).

- Raustiala, K.; Munzer, S.R. The global struggle over geographical indications. Eur. J. Int. Law 2007, 18, 337–365. [Google Scholar] [CrossRef] [Green Version]

- Organización Mundial de la Propiedad Intelectual—OMPI. Arreglo de Lisboa relativo a la Protección de las Denominaciones de Origen y su Registro Internacional, México. 2017. Available online: http://www.wipo.int/export/sites/www/lisbon/es/legal_texts/lisbon_agreement.pdf (accessed on 22 January 2020).

- Giovannucci, D.; Josling, T.; Kerr, W.; O’Connor, B.; Yeung, M.T. Guía de Indicaciones Geográficas: Vinculación de los Productos con su Origen; Centro de Comercio Internacional: Geneva, Switzerland, 2009; p. 221. [Google Scholar]

- Rangnekar, D. The socio-economics of geographical indications: A review of empirical evidence from Europe. UNCTAD-ICTSD Proj. IPRs Sustain. Dev. Issue Pap. 2004, 8, 13–15. [Google Scholar]

- Barham, E. Towards a theory of values-based labeling. Agric. Hum. Values 2002, 19, 349–360. [Google Scholar] [CrossRef]

- Belleti, G.; Scaramuzzi, S. Valorización del territorio desde los productos locales típicos, los circuitos cortos y el turismo rural. In Curso de Valorización del Patrimonio Biocultural y Resiliencia para el Desarrollo Territorial Sostenible; Universidad de Caldas: Mazinales, Colombia, 2017. [Google Scholar]

- Centro de Comercio Internacional-ITC. Indicaciones Geográficas. 2019. Available online: http://www.intracen.org/itc/analisis-mercados/indicaciones-geograficas/ (accessed on 7 August 2019).

- Champredonde, M. Las Indicaciones Geográficas (IG) en América Latina: Balance actual y desafíos. In Desenvolvimiento Territorial: Políticas Públicas Brasileiras, Experiencias Internacionais e Indicaçao Geográficas Como Referenciai; Dallabrida, V.R., Ed.; Editora LiberArs: São Paulo, Brasil, 2014; pp. 265–275. [Google Scholar]

- Díaz, R.; Pelupessy, W.; Sáenz, F. La economía política de las cadenas globales de mercancías: Un marco de análisis. In Cadenas Globales: Enfoque y Aplicaciones para Agroindustrias de Países en Desarrollo; Díaz, R., Pelupessy, W., Sáenz, F., Eds.; EUNA: Heredia, Costa Rica, 2009; pp. 49–66. [Google Scholar]

- Dussel, E. Cadenas globales de valor. Metodología, contenidos e implicaciones para el caso de la atracción de inversión extranjera directa desde una perspectiva regional. In Cadenas Globales de Valor. Metodología, Teoría y Debates; Dussel, E.C., Ed.; Universidad Nacional Autónoma de México: Mexico City, México, 2018; pp. 45–66. [Google Scholar]

- Gibbon, P.; Ponte, S. Trading Down: Africa, Value Chains and the Global Economy; Temple University Press Policy: Philadelphia, PA, USA, 2005; p. 272. [Google Scholar]

- Werner, M.; Bair, J.; Fernández, V. Linking up to development? Global value chains and the making of a post-washington consensus. Dev. Chang. 2014, 45, 1219–1247. [Google Scholar] [CrossRef]

- Bolwig, S.; Ponte, S.; Toit, A.; Riisgaard, L.; Halberg, N. Integrating poverty and environmental concerns into value-chain analysis: A conceptual framework. Dev. Policy Rev. 2010, 28, 173–194. [Google Scholar] [CrossRef]

- Riisgaar, L.; Bolwig, S.; Ponte, S.; Toit, A.; Halberg, N.; Matose, F. Integrating poverty and environmental concerns into value-chain analysis: A strategic framework and practical guide. Dev. Policy Rev. 2010, 28, 195–216. [Google Scholar] [CrossRef]

- Trejo, B.; De los Ríos, I.; Figueroa, B.; Gallego, F.; Morales, F. Análisis de la cadena de valor del queso manchego en Cuenca, España. Rev. Mex. Cienc. Agrícolas 2011, 2, 545–557. [Google Scholar] [CrossRef] [Green Version]

- Hobbs, J.; Cooney, A.; Fulton, M. Value Chains in the Agri-Food Sector. Specialized Livestock. Market Research Group; College of agriculture, Department of Agricultural Economics, University of Saskatchewan: Saskatoon, SK, Canada, 2000; p. 32. [Google Scholar]

- Buck, L.; Wollenberg, E.; Edmunds, D. Social learning in the collaborative management of community forests: Lessons from the field. In Social Learning in Community Forests; Wollenberg, E., Edmunds, D., Buck, L., Fox, J., Brodt, S., Eds.; SMK Grafika: Jakarta, Indonesia, 2001; pp. 13–34. ISBN 979-8764-77-3. [Google Scholar]

- Gereffi, G.; Kapaplinsky, R. The value of value chains: Spreading the gains from globalisation. Boletín IDS 2001, 32, 93. [Google Scholar]

- Gereffi, G.; Humpmphrey, J.; Kapaplinsky, R.; Sturgeon, T. Introduction: Globalisation, value chains and development. Boletín IDS 2001, 32, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Vázquez, A. Las nuevas Fuerzas del Desarrollo; Antoni Bosh Editor: Madrid, Spain, 2005; p. 192. ISBN 978-84-95348-16-6. [Google Scholar]

- Dussel, E. GCCS and development: A conceptual and empirical review. Compet. Chang. 2008, 12, 11–27. [Google Scholar]

- Azevedo da Silva, C. La configuración de los circuitos ‘de proximidad’ en el sistema alimentario: Tendencias evolutivas. Doc. Anàlisi Geogr. 2009, 54, 11–32. [Google Scholar]

- Riveros, R.; Boucher, F. SIAL, Circuitos cortos de comercialización y dinamización económica incluyente de los territorios rurales. In Sistemas Agroalimentarios Localizados y Prácticas Agrícolas Tradicionales. Hacia una Propuesta de Política Pública para el Desarrollo Rural; Tolentino, J., Larroa, R.M., Renard, M., Del Valle, M., Eds.; CONACYT-Red SIAL-México-Yod Estudio: Mexico City, México, 2018; pp. 43–65. [Google Scholar]

- Roldán, H.; Gracia, M.; Santana, M.; Horbath, J. Los mercados orgánicos en México como escenarios de construcción social de alternativas. POLIS. Rev. Latinoam. 2016, 43, 1–23. [Google Scholar] [CrossRef] [Green Version]

- Mastronardi, L.; Marino, D.; Aurora, C.; Giannelli, A.I. Exploring the role of farmers in short food supply chains: The case of Italy. Int. Food Agribus. Manag. Rev. 2015, 18, 109–130. [Google Scholar]

- Santini, F.; Gómez, Y.; Paloma, S. Short Food Supply Chains and Local Food Systems in the EU. A State of Play of Their Socio-Economic Characteristics; Publications Office of the European Union: Luxembourg, Luxembourg, 2013; p. 154. ISBN 978-92-79-29288-0. [Google Scholar]

- Gracia, M.; Horbath, J. Un recorrido por las experiencias de trabajo asociativo autogestionado en el sur de México. Cuadernos Desarro. Rural 2014, 11, 171–190. [Google Scholar] [CrossRef] [Green Version]

- Chiffoleau, Y.; Prevost, B. Les circuits courts, des innovations sociales pour une alimentation durable dans le territories. Norois Environ. Aménagement Société 2012, 224, 7–20. [Google Scholar]

- Malak-Rawlikowska, A.; Majewski, E.; Wąs, A.; Borgen, S.O.; Csillag, P.; Donati, M.; Freeman, R.; Hoàng, V.; Lecoeur, J.-L.; Mancini, M.C.; et al. Measuring the economic, environmental and social sustainability of short food supply chains. Sustainability 2019, 11, 4004. [Google Scholar] [CrossRef] [Green Version]

- Parker, G. Sustainable food? Teikei, co-operatives and food citizenship in Japan and the UK. In Working Papers in Real Estate & Planning; Working Paper; University of Reading: Reading, UK, 2005. [Google Scholar]

- Cusolito, A.; Safadi, R.; Taglioni, D. Inclusive Global Value Chains Policy Options for Small and Medium Enterprises and Low-Income Countries; International Bank for Reconstruction and Development/The World Bank and OECD: Washington, DC, USA, 2016; p. 114. ISBN 978-1-4648-0842-5. [Google Scholar]

- Ravenhill, J. Global value chains and development. Rev. Int. Political Econ. 2014, 21, 264–274. [Google Scholar] [CrossRef]

- Santana, M. Los mercados alternativos y la economía solidaria. Electrón. Cienc. Soc. 2011, 16, 136–146. [Google Scholar]

- Draper, P.; Freytag, A. Who Captures the Value in the Global Value Chain? High Level Implications for the World Trade Organization; E15Initiative; International Centre for Trade and Sustainable Development (ICTSD) and World Economic Forum: Geneva, Switzerland, 2014; Available online: http://e15initiative.org/wp-content/uploads/2015/09/E15-Global-Value-Chains-DraperFreytag-FINAL.pdf (accessed on 11 February 2020).

- Diario Oficial de la Federación—DOF. Ley de Propiedad Industrial; Gobierno de México: Mexico City, Mexico, 1942.

- Diario Oficial de la Federación—DOF. Decreto por el que se Reforma y Adiciona la Ley de Propiedad Industrial; Gobierno de México: Mexico, 1973.

- Diario Oficial de la Federación—DOF. Ley de Invenciones y Marcas; Gobierno de México: Mexico City, Mexico, 1976.

- Diario Oficial de la Federación—DOF. Ley Orgánica de la Administración Pública Federal; Gobierno de México: Mexico, 1976.

- Diario Oficial de la Federación—DOF. Declaración General de Protección a la Denominación de Origen “Tequila”; Gobierno de México: Mexico City, Mexico, 1977.

- Bowen, S.; Valenzuela, A. Geographical indications, terroir, and socioeconomic and ecological sustainability: The case of tequila. J. Rural Stud. 2009, 25, 108–119. [Google Scholar] [CrossRef]

- Macías, A.; Valenzuela, A.G. El tequila en tiempos de la mundialización. Comer. Exter. 2009, 59, 459–472. [Google Scholar]

- Hernández, J. Tequila: Centro mágico, pueblo tradicional. ¿Patrimonio o privatización? Andamios 2009, 6, 41–67. [Google Scholar] [CrossRef]

- Cabrales, L.F. La valorización del patrimonio agroindustrial del Tequila: ¿Desarrollo local o secuestro corporativo de un paisaje singular? In Investig. Rural; Baena, R., Foronda-Robles, C., Galindo, L., García, A., García, A.M., García, B., Guerrero, I., Navarro, J., Prados, M.J., Posad, J.C., Eds.; Ulzama ediciones: Navarra, Spain, 2012; pp. 17–42. [Google Scholar]

- Consejo Regulador del Mezcal—CRM. Informe Estadístico 2016; CRM: México City, Mexico, 2016; Available online: http://www.crm.org.mx/informes.php (accessed on 22 May 2017).

- Huerta, R.; Luna, R. Los caminos del mezcal y del tequila. In Agua de las Verdes Matas. Tequila y Mezcal; Vera, J., Fernández, R.C., Eds.; Artes de México y del Mundo: México City, Mexico, 2015; pp. 43–63. [Google Scholar]

- Cortés, L.; Basurto, F.; Agave salmiana Otto ex Salm. Jardín Botánico, Instituto de Biología. Universidad Nacional Autónoma de México. 2017. Available online: http://www.ibiologia.unam.mx/gela/pp-1.html (accessed on 20 November 2019).

- Diario Oficial de la Federación—DOF. NORMA Oficial Mexicana NOM-070-SFCI-2016, Bebidas alcohólicas-Mezcal-Especificaciones. 23 de Febrero de 2017. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5472787&fecha=23/02/2017 (accessed on 5 March 2020).

- Consejo Regulador de la Denominación de Origen Calificada Rioja. 2018. Available online: https://www.riojawine.com/doca-rioja/denominacion-de-origen-calificada/ (accessed on 20 October 2020).

- Consejo Regulador del Mezcal—CRM. Informe Estadístico 2017; CRM: México City, Mexico, 2017; Available online: http://www.crm.org.mx/informes.php (accessed on 8 September 2018).

- Diario Oficial de la Federación—DOF. PROYECTO de Norma Oficial Mexicana PROY-NOM-199-SCFI-2015, Bebidas Alcohólicas-Denominación, Especificaciones Fisicoquímicas, Información Comercial y Métodos de Prueba. 29 de Febrero de 2016. Available online: http://dof.gob.mx/nota_detalle.php?codigo=5428197&fecha=29/02/2016 (accessed on 17 March 2020).

- Martijn, H. Exporting Protection: EU Trade Agreements, Geographical Indications, and Gastronationalism. Rev. Int. Political Econ. 2020. [Google Scholar] [CrossRef]

- Orozco-Martínez, J.L. Las Relaciones de Poder en los Intercambios Comerciales de la Cadena Productiva del Tequila y su Incidencia en la Competitividad de la Rama industrial. Ph.D. Thesis, ITESO, Tlaquepaque, Jalisco, México, November 2011. [Google Scholar]

- Palma, F.; Pérez, P.; Meza, V. Diagnóstico de la Cadena de Valor Mezcal en las Regiones de Oaxaca; Gobierno de Oaxaca: Oaxaca de Juárez City, México, 2016; p. 83. Available online: http://www.coplade.oaxaca.gob.mx/wp-content/uploads/2017/04/Perfiles/AnexosPerfiles/6.%20CV%20MEZCAL.pdf (accessed on 25 June 2020).

- Sistema Producto Agave Tequilana. Plan rector: Sistema Producto Nacional Agave Tequilana. 2012. Available online: http://dev.pue.itesm.mx/sagarpa/nacionales/EXP_CNSP_AGAVE_TEQUILA/PLAN%20RECTOR%20QUE%20CONTIENE%20PROGRAMA%20DE%20TRABAJO%202012/PR_AGAVE%20TEQUILA_NACIONAL_2012.pdf (accessed on 12 May 2020).

- Consejo Regulador del Mezcal—CRM. Informe Estadístico 2019. El Mezcal, la Cultura Líquida de México; CRM: México City, Mexico, 2019; Available online: http://www.crm.org.mx/informes.php (accessed on 1 May 2020).

- Consejo Regulador del Tequila—CRT. Estadísticas en Línea del CRT. Available online: https://www.crt.org.mx/EstadisticasCRTweb/ (accessed on 11 August 2020).

- Luna, R. Análisis del mercado nacional y norteamericano del Tequila. Continuidades y tendencias recientes. Carta Económica Reg. 2012, 23, 37–58. [Google Scholar]

- Consejo Regulador del Mezcal—CRM. Informe de Actividades Consejo Directivo 2012–2015; CRM: Oaxaca de Juárez City, Mexico, 2013; p. 13. [Google Scholar]

- El Financiero. Tequila… ¿100% Mexicano? El Financiero. 2017. Available online: https://www.elfinanciero.com.mx/empresas/tequila-100-mexicano (accessed on 23 June 2017).

- Bowen, S.; Gaytan, M.S. The paradox of protection: National identity, global commodity chains, and the tequila industry. Soc. Probl. 2012, 59, 70–93. [Google Scholar]

- Aguilar, A. DIAGEO Ataca Nuevo Negocio Alianza con Mezcal Unión y Viene Otra, Apresura Planes con Don Julio, Crece 20% y ya es Líder. El Universal. 2016. Available online: https://www.eluniversal.com.mx/entrada-de-opinion/columna/alberto-aguilar/cartera/2016/02/10/diageo-ataca-nuevo-negocio-alianza-con (accessed on 25 June 2019).

- Sánchez, S.; Diageo Apuesta por el Mezcal ‘de lujo’ con Pierde Almas. Expansión, Sección Empresas. 2018. Available online: https://expansion.mx/empresas/2018/08/24/el-mezcal-una-apuesta-ultra-premium-para-diageo (accessed on 10 January 2019).

- El Financiero. Productor de Absolut Adquiere Mezcalera Mexicana. El Financiero. 2017. Available online: https://www.elfinanciero.com.mx/empresas/pernod-ricard-compra-mezcal-del-maguey (accessed on 8 June 2017).

- Economía Hoy. Casa Pedro Domeq Distribuirá Mezcales de Casa Armando Prieto. Economía Hoy. 2018. Available online: www.economiahoy.mx/empresas-eAm-mexico/noticias/9348351/08/18/Casa-Pedro-Domecq-distribuira-mezcales-de-Casa-Armando-Guillermo-Prieto.html (accessed on 1 December 2019).

- Altonivel. La Transformación de Casa Cuervo que Destila Tradición. Altonivel. 2018. Available online: https://www.altonivel.com.mx/lideres/la-transformacion-de-casa-cuervo-que-destila-tradicion (accessed on 31 July 2019).

- García-Barrón, E.; Hernández, J.; Gutiérrez-Salomón, A.L.; Escalona-Buendía, H.B.; Villanueva-Rodríguez, S. Mezcal y Tequila: Análisis conceptual de dos bebidas típicas de México. Rev. Iberoam. de Vitic. Agroind. y Rural. 2017, 4, 138–162. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Costs |

|---|

| • Establish a national legal structure |

| • Define exact physical limits |

| • Establish criteria and norms |

| • Provide local or national information and education |

| • Control certification fees |

| • Marketing and promotion |

| • Assessment and application for protection abroad |

| • Investments in infrastructure and production |

| • Adaptation to standards, methods and specifications |

| • In a GI cluster, expenses may be incurred when adapting, working collaboratively, and sustaining collective action |

| • Business or technological limitations |

| • Increased cost of raw materials |

| • Monitoring and maintaining protection |

| • Administrative and bureaucratic costs |

| Category | Characteristics | |

|---|---|---|

| Stages | Equipment | |

| Mezcal | Cooking | Pit, masonry or autoclave furnaces |

| Grinding | Tahona, Chilean or Egyptian mill, trapiche, harrowing machine, mill train or diffuser | |

| Fermentation | Wooden containers, masonry sinks or stainless-steel tanks | |

| Distillation | Alembics, continuous stills or columns of copper or stainless steel | |

| Artisan Mezcal | Cooking | Masonry raised or pit furnaces |

| Grinding | Mallet, tahona, Chilean or Egyptian mill, trapiche or harrowing | |

| Fermentation | Holes in stone, ground or trunks, masonry basins, wooden or clay containers, animal skins; the process includes the fiber of maguey or agave (bagasse) | |

| Distillation | With direct fire in copper boiler stills or clay pot and clay, wood, copper or stainless steel montera; this process can include the fiber of maguey or agave (bagasse) | |

| Ancestral Mezcal | Cooking | Well furnaces |

| Grinding | Mazo, tahona, Chilean or Egyptian mill | |

| Fermentation | Holes in stone, ground or trunk, masonry sinks, wooden or clay containers, animal leather; this process can include the fiber of maguey or agave (bagasse) | |

| Distillation | With direct fire in a clay pot and clay or wood hat; this process may include the fiber of maguey or agave (bagasse). | |

| Distillate | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|---|---|---|

| Cognac | $574 | $642 | $654 | $681 | $689 | $756 | $746 | $819 |

| Armagnac | $585 | $622 | $578 | $563 | $63 2 | $848 | $774 | $844 |

| Mezcal | $241 | $279 | $304 | $354 | $367 | $382 | $392 | $413 |

| Port | $284 | $302 | $323 | $315 | $338 | $359 | $395 | $399 |

| Whiskey | $285 | $283 | $281 | $270 | $305 | $307 | $278 | $302 |

| Geneva | $150 | $169 | $186 | $254 | $239 | $298 | $306 | $299 |

| Tequila | $127 | $132 | $138 | $155 | $163 | $204 | $219 | $246 |

| Brandy | $135 | $136 | $136 | $134 | $152 | $152 | $143 | $146 |

| Vodka | $125 | $126 | $126 | $127 | $140 | $151 | $143 | $138 |

| Ron | $107 | $108 | $108 | $108 | $118 | $132 | $130 | $131 |

| Schnapps | $25 | $25 | $25 | $26 | $27 | $27 | $27 | $28 |

| Equivalent prices for kg of agave | ||||||||

| Mezcal | $30.13 | $34.88 | $38.00 | $44.25 | $45.88 | $47.75 | $49.00 | $51.63 |

| Tequila | $15.88 | $16.50 | $17.25 | $19.38 | $20.38 | $25.50 | $27.38 | $30.75 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pérez-Akaki, P.; Vega-Vera, N.V.; Enríquez-Caballero, Y.P.; Velázquez-Salazar, M. Designation of Origin Distillates in Mexico: Value Chains and Territorial Development. Sustainability 2021, 13, 5496. https://0-doi-org.brum.beds.ac.uk/10.3390/su13105496

Pérez-Akaki P, Vega-Vera NV, Enríquez-Caballero YP, Velázquez-Salazar M. Designation of Origin Distillates in Mexico: Value Chains and Territorial Development. Sustainability. 2021; 13(10):5496. https://0-doi-org.brum.beds.ac.uk/10.3390/su13105496

Chicago/Turabian StylePérez-Akaki, Pablo, Nadia Viridiana Vega-Vera, Yuritzi Paola Enríquez-Caballero, and Marisol Velázquez-Salazar. 2021. "Designation of Origin Distillates in Mexico: Value Chains and Territorial Development" Sustainability 13, no. 10: 5496. https://0-doi-org.brum.beds.ac.uk/10.3390/su13105496