The Market Responses to Super Bowl Advertising: The Role of Product Type and Multiple Executions

Department of Media, Kyung Hee University, Seoul 02447, Korea

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(13), 7127; https://0-doi-org.brum.beds.ac.uk/10.3390/su13137127

Submission received: 21 May 2021

/

Revised: 14 June 2021

/

Accepted: 21 June 2021

/

Published: 25 June 2021

(This article belongs to the Special Issue Strategic Planning of Sports Systems)

Abstract

:This study uses event study analysis to examine the impact of Super Bowl commercials on the stock prices of sponsoring firms by product type and the frequency of ad executions. By examining 272 Super Bowl advertisements from 142 firms that aired from 2010 to 2019, the results show that the execution of Super Bowl advertising was positively associated with excess returns. In particular, the abnormal return for the day after the event represents the largest gain in excess returns over a period of ±10 days around the event day. Further, cumulative average abnormal returns (CAARs) are consistently positive right after the event day. The findings demonstrate that Super Bowl commercials yielded higher returns for low-involvement and hedonic products. The number of ad executions is found to substantially enhance the effectiveness of Super Bowl advertising.

1. Introduction

The Super Bowl, the championship game of the National Football League (NFL) in the U.S., is one of the most popular sports events in the world. In 2020, it recorded 102 million viewers and charged $5.5 million for a 30-second commercial. Fox’s Super Bowl ad revenue in 2020 totaled $525.4 million and ad prices continue to rise every year [1]. While there is anecdotal evidence of the various benefits of Super Bowl advertising such as high reach of various demographics, it is still unclear whether advertising expenditures pay off in terms of return on investment [2]. The event study approach is a useful way to appreciate the financial impact of specific marketing activities of companies by assessing the abnormal returns associated with the announcement of those activities [3]. Since the stock price quickly reflects the future expectation of an event in the market, the abnormal stock return generated by the event can be seen as the reliable indicator of long-term impact on the value of a firm [4].

There have been many attempts to examine the relationship between the announcement of various marketing activities such as celebrity endorsement contracts [5], brand extension announcements [6], awards of product quality [7], product placement [8], and abnormal returns for firms. Although several studies attempted to examine the economic impact of Super Bowl advertising from an event study perspective, the findings are rather mixed and inconclusive [3]. While the majority of studies found a positive impact of Super Bowl ads on stock prices (e.g., [9]), several studies found a negative relationship between Super Bowl ads and stock returns (e.g., [10]). For example, Kim and Morris [10] showed that 22 of 35 Super Bowl advertisers analyzed experienced stock price declines the day after the Super Bowl. We believe that there exist underlying conditions which maximize the effectiveness of the Super Bowl ads.

The primary purpose of this study is twofold. A first goal of this study is to explicate the moderating role of product characteristics in determining the salience of Super Bowl effects. Even if many attempts have been made to understand the financial impact of Super Bowl advertising, little attention has been devoted to issues concerning the ways that product involvement and hedonic/utilitarian attributes of products affect the influence of Super Bowl campaigns. Only a handful of studies examined the impact of product characteristics on the effectiveness of Super Bowl advertising. For instance, Kim and Cheong [11] examined how executional elements affect the likability of Super Bowl advertising. The results indicated that the influence of executional elements was greater when the advertised product was low involvement rather than high involvement. This study posited that the relationship between the Super Bowl advertising and abnormal stock returns would depend on the product involvement and hedonic/utilitarian attributes of products. The results shed light on how the effectiveness of the Super Bowl ads is maximized.

Another intriguing question inspiring this research is whether the number of executions of Super Bowl advertising plays an important role in determining the salience of such effects as well. The effects of multiple exposures to advertising on consumers have been extensively studied [12]. The results of prior research suggest that there is a positive relationship between the number of exposures to an advertisement and the recall of that advertisement [13]. This study postulates that the effectiveness of Super Bowl ads will be enhanced by increasing the number of ad executions. Given the high costs and risks involved in Super Bowl advertising, it is critical for advertisers to consider the optimum level of frequency to generate the desired outcomes.

The remainder of this paper is organized as follows. Section 2 reviews the relevant literature and theoretical background. Section 3 addresses the data, key variables, and research method, while Section 4 represents the empirical findings. Section 5 involves discussion, limitations, and conclusions of the present study.

2. Theoretical Background

2.1. Super Bowl Advertising

The Super Bowl is the most popular sports event in the world; it garnered 102 million viewers and charged $5.5 million for a 30-s commercial in 2020. Firms spent a total of $525.4 million on Super Bowl advertising in 2020, and ad prices continue to rise every year [1]. Many companies spend a substantial part of their advertising budgets on this event because of the exceptionally high level of viewership and the broad demographics of viewers [14]. Watching the commercials during the Super Bowl has become an important part of the Super Bowl experience [2]. Super Bowl commercials are distinct from typical advertisements in several ways. Since viewers watch the new advertisements for the first time, ads have become an interesting topic for online and offline discussions, both before and after the game. It was reported that 52% of Super Bowl viewers talked about the Super Bowl commercials the following day [15]. Further, Super Bowl commercials are probably the only ones evaluated by both viewers and news media [11]. USA Today has reported likeability scores for each Super Bowl advertisement since 1989.

Most studies on Super Bowl advertising have focused on the impact of executional elements by using short-term measures of advertising effectiveness such as ad recall, ad likability, and buzz [16]. For example, in a non-laboratory setting, Newell and Henderson [13] examined the effects of length, frequency, and pod placement on the recall of Super Bowl commercials. Super Bowl viewers were surveyed the day after the game to assess their recall of ads embedded in the game. The findings indicated that advertising recall was positively related to the length and frequency of advertisements.

Some researchers attempted to examine the relationship between Super Bowl advertising and consumer’s online behavior. For example, Lewis and Reiley [17] found the positive influence of 46 Super Bowl commercials on online searches of advertised products within 15 seconds following a Super Bowl ad appearance during the game. Similarly, Chandrasekaran, Srinivasan, and Sihi [18] investigated the influence of Super Bowl ad content on online brand searches. By analyzing the 2004–2012 Super Bowl commercials, the authors found that the informational content of the TV commercial significantly improved consumers’ online brand searches, whereas website prominence and prior media publicity yielded negative results.

Nail [19] emphasized the role of media coverage and word-of-mouth discussion in assessing the persuasiveness of Super Bowl advertisements. The results demonstrate that aggressive promotion activities were the best strategy to boost consumer discussion after the game. In particular, increasing media coverage and word-of-mouth communications before the Super Bowl were found to drive post-game activities such as discussion after the game. More recently, the impact of consumer engagement with Super Bowl ad tweets on engagement with the advertiser’s Twitter account was empirically examined [20]. The authors used Python to collect viewer participation data from the official Twitter accounts of the Super Bowl advertisers. The findings of regression analysis indicated that the number of retweets and favorites on Super Bowl ad tweets positively affected the numbers of followers and favorites on the official Twitter accounts of the Super Bowl advertisers.

2.2. Event Study and Economic Worth of Super Bowl Ads

Since the ultimate goal of marketing activities is to improve the economic worth of stockholders, it is becoming more crucial for marketers to verify the return on investment for their marketing activities [21]. An event study analysis is a statistical method to examine the influence of an event on the stock price of a firm [5]. The event study approach assesses abnormal returns, which are defined as the differences between actual returns around an event of interest and expected returns. An expected return is estimated in terms of a firm’s expected stock performance relative to the market index [22]. The theoretical assumption underlying an event study is ‘efficient market hypothesis’, which postulates that “the price of a security is the present value of future cash flows expected from a firm’s assets and, at any given time, reflects all the available information about the firm’s current and future profit potential” [5] (p. 57). Thus, any news concerning the current and future value or productivity of a company is believed to affect a shift in the stock price by signaling consumers and investors in the market.

Many studies have demonstrated that Super Bowl advertising can exert a significant influence on firm value [16]. While the potential benefits of Super Bowl advertising have been widely accepted in both academia and industry, empirical evidence for the financial reward of Super Bowl advertising has been elusive. Some studies found a positive relationship between Super Bowl ads and stock prices (e.g., [3,9,15]), whereas others reported a negative impact on market reaction [10,23]. For instance, Tomkovick and colleagues [24] reported that Super Bowl stocks outperformed the S&P 500 index by over 1.0 percent in the test period, whereas Kim and Morris [10] (p. 10) found that Super Bowl commercials had a significantly negative influence on firm value in terms of cumulative abnormal returns on the day after the game. The authors lamented, “Super Bowl advertising, from an equity position, could have been seen as an overly expensive rather than an efficient investment.” Similarly, Filbeck and his colleagues [23] showed that Super Bowl advertisers experienced significantly negative returns in the entire event window. Although a relatively small number of studies found a negative relationship between Super Bowl ads and stock prices, the majority of studies support the positive influence of Super Bowl advertising on the value of a firm the day after the event:

Hypothesis 1 (H1).

Executing Super Bowl advertising is positively associated with a change in firm market value.

2.3. Moderating Role of Product Type and Multiple Executions

While many attempts have been made to explain how Super Bowl advertising can influence the effectiveness of advertising, little attention has been paid to the conditions under which such effects become salient. Product involvement has been found to influence the way that consumers process and evaluate advertising messages [25]. Product involvement can be defined as a consumer’s perceived importance or relevance of a product category, which is derived from intrinsic interests, values, and goals [26]. Although various approaches to product involvement have been discussed by different researchers, there is consensus that product involvement is an enduring trait of an individual, and consumers possess fairly stable levels of involvement with a certain product category [25]. In this study, product involvement is operationalized as an ongoing concern with a particular product class based on an individual’s inherent interests and needs across all purchase situations [27]. Prior research on program involvement suggests that an individual’s involvement with a TV program can exert a significant influence on the effectiveness of advertising [28]. Specifically, increasing involvement in a program is likely to generate more thoughts about and attention to the program, which, in turn, interferes with viewers’ ability to process advertising messages [29]. Because a sporting event like the Super Bowl induces high levels of engagement and arousal among viewers, they are considerably involved in watching the program throughout the game. Given the limited resources of processing TV commercials, it is expected that viewers are more likely to easily process advertising messages that require a relatively small amount of cognitive resources such as low-involvement products than high-involvement products. Accordingly, the following hypothesis is postulated:

Hypothesis 2 (H2).

The impact of Super Bowl advertising will be moderated by product involvement in terms of firm market value. In particular, the positive effect of the Super Bowl ads will be more pronounced for low involvement products than high involvement products in terms of stock prices.

Previous research suggests that certain types of products can generate quite different responses than others. The FCB grid model [30] suggests that there are two types of responses to products: “think” and “feel”. According to this paradigm, “think implies the existence of a utilitarian motive and consequent cognitive information processing,” while “feel implies ego-gratification, social acceptance, or sensory pleasure motives and consequent affective information processing” [31] (p. 25). In line with this, some researchers categorize products into hedonic and utilitarian products [32]. Consumers use utilitarian products, such as toothpaste and laundry detergent, to fulfill functional and practical needs. Such consumption is often made to achieve certain goals and tasks. On the other hand, hedonic products such as wine and perfume are used primarily for fulfilling experiential needs, such as sensory pleasure, fun, and excitement [33].

It is predicted that the impact of Super Bowl advertising on stock prices is likely to be higher when advertising hedonic rather than utilitarian products. According to mood congruity framework, the effectiveness of advertising can be improved by matching the affective tone of an advertisement with that of the program in which it is inserted [34]. Since the Super Bowl has become the most exciting and entertaining TV event of the year, its festive and cheerful atmosphere routinely evokes varied emotional responses among viewers [35]. In such an affective environment, the viewers might more favorably respond to commercials for hedonic products that are affectively consistent with the prevailing mood state [36]. Therefore, the following hypothesis is posited:

Hypothesis 3 (H3).

The impact of Super Bowl advertising will be moderated by the characteristic of products (i.e., hedonic/utilitarian products) in terms of the value of a firm. In particular, the positive effect of the Super Bowl ads will be more pronounced for hedonic products than utilitarian products in terms of stock prices.

The effects of multiple exposures to an advertising message on consumers have been extensively examined [12]. Since the influence of advertising on a consumer’s learning process is directly related to the number of times a consumer is exposed to the advertising message, advertising repetition can improve the effectiveness of advertising [37]. Since multiple exposures to an advertisement allow consumers to have more opportunities to elaborate on the message, this increased elaboration time facilitates learning and retaining information contained in the ad [38]. Further, the process by which the repetition of advertising messages enhances the effectiveness of advertising can be explained by a two-stage learning model [39]. According to this paradigm, the learning of advertising messages mediates sales of advertised products when exposures are voluntary.

The positive outcome of advertising repetition has precedence in Zajonc’s [40] mere-exposure effect hypothesis. According to this framework, repeated exposure to an object is a sufficient condition for generating an individual’s favorable attitude toward that object. Mere-exposure effect has been found to be more pronounced for unfamiliar objects than for familiar objects. Since the Super Bowl is the first show case for advertisers to introduce their advertisements, we anticipate a positive effect of multiple exposures to such unfamiliar advertisements on consumer responses.

Despite the theoretical and managerial importance of the number of ad executions, empirical evidence concerning how multiple exposures to Super Bowl commercials affect the effectiveness of the Super Bowl advertising is scant. Only one field survey examined the impact of frequency of advertising on the persuasiveness of TV commercials in the Super Bowl context [13]. The authors tested the effects of length, frequency, and pod placement on advertising recall in a non-laboratory setting. Participants were surveyed the day after Super Bowl XXVIII to measure recall of commercials aired during the game. The results indicated that the mean recall of brands with multiple executions was significantly higher than that of brands with a single execution. Based on the foregoing discussion, the following hypothesis is postulated:

Hypothesis 4 (H4).

The impact of Super Bowl advertising will be moderated by the number of advertising execution in terms of firm market value. In particular, the positive effect of the Super Bowl ads will be more pronounced for the advertisers of multiple executions than those of a single execution in terms of stock prices.

3. Methodology

3.1. Sample and Data

This study examines 272 Super Bowl advertisements for 142 firms from 2010 to 2019, calculating anticipated returns over an estimation window of 120 trading days that ended 10 days prior to the event day. Consistent with previous research [5], the event window was set as ±10 days of the event day. Figure 1 shows event windows for this study [41]. The reason for setting event windows prior to the event date is to allow the possibility that information regarding Super Bowl ads may leak before the announcement of the event in the news media [4].

To select firms to be used in this study, a list of companies that have advertised during Super Bowls for the past 10 years (from 2010 to 2019) (Table 1) was created on the basis of the Super Bowl official website (http://superbowl-ads.com, https://www.nfl.com/super-bowl/commercials, accessed on 19 September 2019). Among them, companies listed on the NASDAQ and New York Stock Exchanges were selected for analysis. The reason for the selection of this period is that the period of 10 years can be conceived as a period sufficient to capture the trends and effects of a specific event synchronically [42].

Utilizing the stock price data from Yahoo! Finance (https://finance.yahoo.com, accessed on 1 October 2019), the daily returns for each firm as well as the market index are calculated for the 10 trading days before/after the event day. Because the Super Bowl is held on the first Sunday of February—a day when the stock market is not open—the day after the Super Bowl was set as an ‘event day’ [10].

3.2. Statistical Analysis

Based on Brown and Warner’s study [22], the parameters of the market model for each firm were computed by regressing its actual returns on the returns of a weighted portfolio of securities using an estimation period of 120 days before the event. The most crucial problem in an event study is the estimation of abnormal returns generated by unexpected events such as the Super Bowl. Using the parameter estimates from the ordinary least squares regression (OLS), abnormal returns for every security on a specific date was calculated. The method of calculating the abnormal return using the market model is as follows:

: the abnormal return for each firm on day , : the actual return for each firm on day , , is the intercept, is the regression coefficient for the firm , and : the expected stock return on day for the firm .

In addition to examining abnormal returns, cumulative abnormal returns (CAR) should be calculated for a couple of reasons. Since the effect of an event may be spread over several days surrounding the event day, CAR help researchers to understand the cumulative effect of an event. Further, calculating abnormal returns surrounding the event day enables uncertainty as to the actual date of the event [5]. For each firm, the CAR for the event period is calculated by adding all the abnormal returns in the event period as follows:

To examine the moderating effect of product type such as product involvement and hedonic/utilitarian products, each product or service that appeared in the Super Bowl advertising was classified into four categories based on the FCB grid of 60 common products [31]. First, products were categorized into low-involvement products and high-involvement products based on the FCB grid model, while hedonic/utilitarian product types were generated in accordance with previous studies (e.g., [11,43]). The classification of products is presented in Table 2. Finally, the number of ad executions was measured on the basis of the number of advertisements aired in each year (i.e., single exposure vs. multiple exposures). Advertisers who executed more than two times in each Super Bowl game were coded as multiple exposures [13].

4. Results

Figure 2 shows the average abnormal returns for 142 firms on the event day, as well as for a window of ±10 days around the event day. To examine if abnormal returns were caused by the Super Bowl advertising, the hypothesis that the cross-sectional mean of abnormal return at the event day is different from 0 was statistically tested [5]. Results indicate that, on average, the execution of Super Bowl advertising is positively associated with excess returns. In particular, the average abnormal return for the day after event day is 0.50%, which is statistically significant (t = 3.267, p < 0.05). This period represents the largest gain in excess returns over a period of ±10 days around the event day (Table 3). The results imply that, on average, advertisers employing Super Bowl ads experienced a gain of 0.50% in excess returns. This result is consistent with previous studies supporting the positive impact of Super Bowl ads on stock market reaction [2,9]. Thus, H1 was supported.

Table 4 shows the cumulative abnormal returns (CARs) for various windows surrounding the event day. The evidence of significant positive returns on the +1 day and the cumulative average return over 10 days (+1, +10) suggest that, on average, the market continuously reacts positively to Super Bowl advertising.

Figure 3 demonstrates that cumulative average abnormal returns (CAARs) are consistently positive right after the event day, indicating that Super Bowl advertising substantially enhances a firm’s ROI for 10 days after the Super Bowl. As shown in Table 4 CAARs for the window of (+1; +10) are found to be 2.353% (t = 5.438, p < 0.001), indicating that, on average, advertisers were financially rewarded for 10 days after the Super Bowl. This result implies that the impact of Super Bowl ads may be spread over several days after the event day because of the gradual availability of information and prediction of the event’s influence on future firm profitability [5].

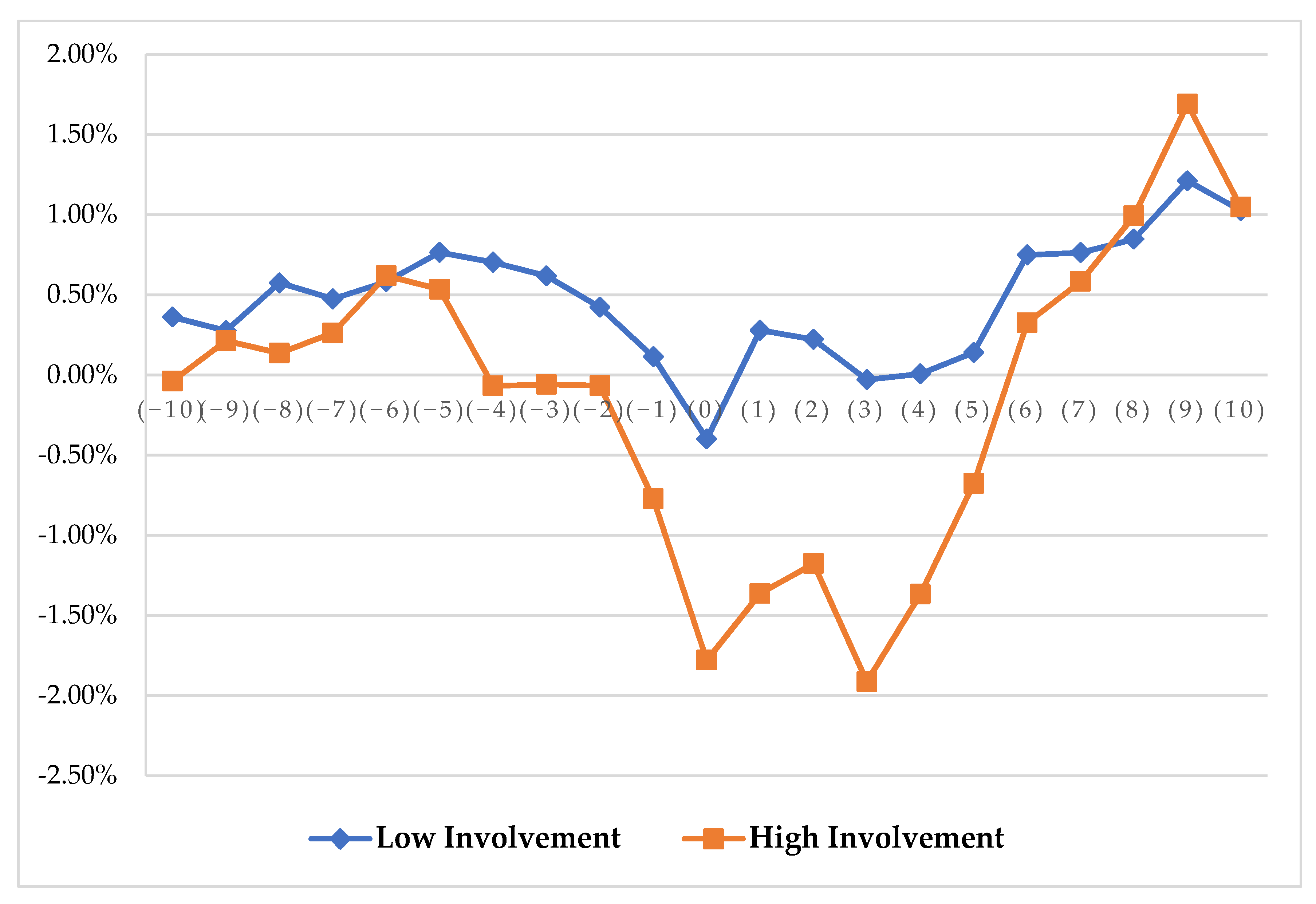

Figure 4 demonstrates differences in the CAAR between low- and high-involvement product groups. While the effects of Super Bowl ads did materialize among both low- and high-involvement product firms, these effects marginally appeared to be more pronounced among low-involvement products than high-involvement products (t = 1.695, p = 0.092 at +1 day, t = 1.825, p = 0.070 at +3 day). A similar pattern of results was observed when the CAAR for the window of (+1; +10) was employed as a dependent variable (t = 1.824, p < 0.070). Thus, H2 was partially supported.

Similarly, the impact of Super Bowl ads was moderated by utilitarian/hedonic product type. As shown in Figure 5, the Super Bowl commercials yielded higher CAARs for hedonic products than for utilitarian products (t = 3.082, p = 0.003 at +1 day). Specifically, the significant impact of product type was consecutively observed from −1 day to +5 day (p < 0.05). Thus, H3 was supported.

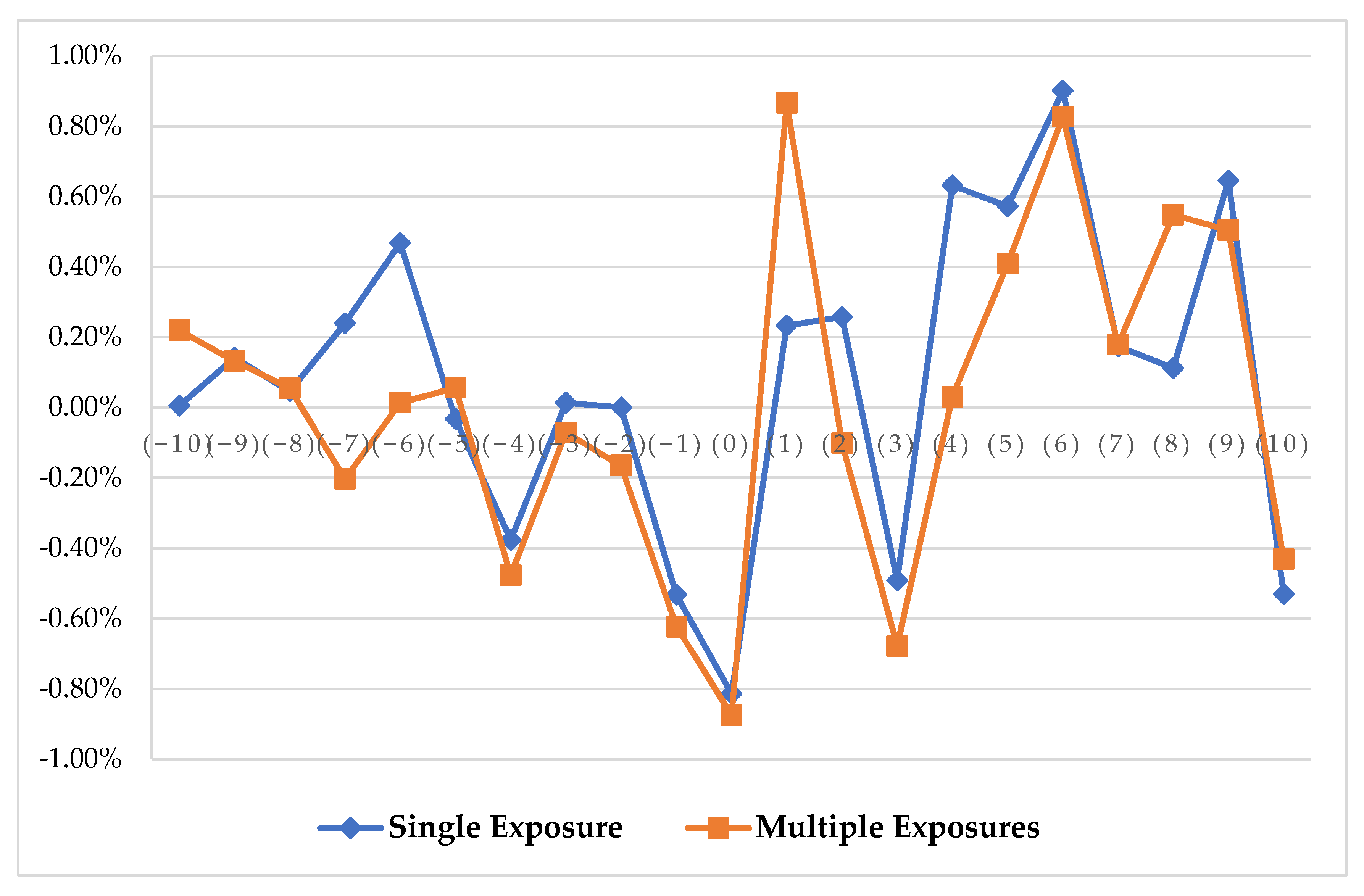

Finally, no significant interaction between multiple executions and the Super Bowl effect was observed in terms of cumulative abnormal returns. However, the results show that there was a marginally significant interaction between multiple executions and the Super Bowl effect for a short-term period. Specifically, as shown in Figure 6, the impact of Super Bowl ads was found to be more pronounced among firms with multiple ad executions than those with a single ad execution in terms of AARs (t = 2.051, p = 0.042 at +1 day, t = 1.907, p = 0.059 at +4 day). Thus, H4 was partially supported.

5. Discussion

The present study attempted to provide further insight into the effectiveness of Super Bowl advertising by examining the economic worth of Super Bowl longitudinally. By analyzing Super Bowl advertisements and stock prices for 142 firms for 10 years, results indicate that the execution of Super Bowl advertising is positively associated with excess returns for Super Bowl advertisers. Compared to the results of previous studies examining the Super Bowl ads at the short-term level (e.g., [10]), the present study corroborated the robust influence of Super Bowl commercials on firm value. The finding shows that Super Bowl advertising substantially enhances a firm’s ROI for 10 days after the Super Bowl game. This result implies that the impact of Super Bowl ads may be spread over several days after the event day. This result is consistent with previous studies supporting the positive impact of Super Bowl ads on stock prices [2,9]. Previous research suggests that advertising can affect opinions of stakeholders and values of companies through signaling and the spillover effect [44]. It stands to reason that media exposure to Super Bowl advertising not only heightens consumer attention to advertised products but also boosts the profile of Super Bowl advertisers with investors, which, in turn, makes their stocks more appealing options for investment [24].

Another contribution of the present study is in the discovery of the boundary conditions under which the salience of Super Bowl ad effects become evident. This study posited that the relationship between the Super Bowl advertising and abnormal stock returns would depend on the characteristics of products. As predicted, the magnitude of the effect (posited in Hypothesis 1) was found to be more pronounced among low-involvement products than among high-involvement products in terms of abnormal returns. The observation that the effect of Super Bowl advertising does not manifest itself in the same way under varying levels of product involvement is consistent with previous studies. For example, Kim and Cheong [45] found that the influences of latent factors in Super Bowl commercials (i.e., female, affective, time-elapse, divergent, and music factors) on ad likability were greater when the advertised product was a low- rather than high-involvement product. It may be that the advantage of Super Bowl advertising is most beneficial for low-involvement product categories.

This result makes sense from the prior research examining the relationship between Super Bowl ad likability and product categories. For instance, Tomkovick et al. [15] found that the likability for Super Bowl ads in the food and beverage categories were significantly higher than that for ads in the other eight categories. Usually, low-involvement products such as snacks, soft drinks, and beer are the products that audiences are typically consuming while they watch the game. Given the low-involvement and light-hearted nature of the TV watching environment [46], viewers of the Super Bowl might be more likely to enjoy commercials that do not require enormous cognitive efforts and elaboration of information.

In addition to product involvement, the hedonic/utilitarian nature of a product was found to play an important role in determining the impact of Super Bowl advertising. The findings demonstrate that Super Bowl commercials yielded higher returns for hedonic products than utilitarian products in terms of cumulative abnormal returns. This pattern of results aligns with the literature on mood congruity, which suggests that the persuasiveness of advertising can be enhanced by matching the affective tone of a commercial with that of the program in which it is embedded because “greater availability of mood-consistent information in memory facilitates the encoding of information that is affectively consistent with the prevailing mood state” [36] (p. 4).

Because the experience of watching sporting events such as the Super Bowl is likely to cause emotional reactions in viewers such as excitement, fun, or pleasure, the viewers might prefer TV commercials that match the affective tone of the program to maintain the current mood induced by the program. In the case of this study, consumers might perceive commercials featuring hedonic products as more congruent with the moods induced by the program than those featuring utilitarian products, which, in turn, yielded more favorable responses to the commercials [34]. The implication for advertisers is that it seems to be imperative to appreciate the characteristics of products advertised when they intend to execute Super Bowl commercials.

Finally, the results of this study suggest that the number of ad executions itself can substantially enhance the effectiveness of Super Bowl advertising for a short-term period. Although the moderating effect of multiple executions did not reach the statistical significance in terms of cumulative abnormal returns, the impact was found to be more pronounced among firms with repetitive ad execution in terms of average abnormal returns. These results are consistent with the notion that the effect of advertising on a consumer’s learning process is directly related to the number of times the consumer is exposed to the advertising message [37]. Specifically, the two-stage learning model suggests that the learning of advertising messages can mediate sales of advertised products when viewers are voluntarily exposed to the ads [39]. Since multiple exposures to a TV commercial facilitates consumer processing and retention of advertising messages, the advertisers who repeated their advertisements might benefit more from Super Bowl advertising.

This study had several limitations. First, the time periods employed for the event analysis (i.e., 2010–2019) were arbitrarily selected. Replication of this study with samples spanning a different time frame might produce slightly different results due to different social, cultural, and economic environments. Another limitation of this study was the use of the market model [22]. Although the market model is the most frequently used approach to estimate expected returns, there are other methods such as mean adjusted returns, market adjusted returns, and conditional risk adjusted returns [47]. Although the findings reported in this study might provide some insight into understanding how Super Bowl advertising interacts with executional factors such as product category and number of ad executions, the generalizability of the findings seems to be limited to the firms, commercials, and stock prices examined here. In subsequent studies, it would be valuable to test the hypotheses posited here by employing different analytical models and sample frames so that we could be more assured of the validity of the results. Finally, as growing numbers of Super Bowl advertisers (e.g., Anheuser-Busch) are looking to emphasize their commitment to sustainability in order to differentiate their brand image and to enhance their corporate reputation, it would be critical for companies to assess the effectiveness of their Super Bowl commercials depicting sustainability. Additional research is called for on the persuasive impact of various sustainability commitments claimed by Super Bowl advertisers (e.g., environmental initiatives).

Given the high costs involved in Super Bowl advertising, how to measure the economic worth of Super Bowl advertising is a critical decision for advertisers. Although many practitioners have recognized the potential benefits of Super Bowl advertising, to date there has not been much beyond conventional wisdom and intuitive notion to guide companies in executing Super Bowl commercials. An even study methodology can be a useful tool for assessing whether advertising expenditures reward in terms of return on investment.

Author Contributions

Conceptualization: J.-G.L. data collection: K.-A.K., analysis: J.-G.L. and K.-A.K. Discussion: J.-G.L. All authors wrote, reviewed and commented on the manuscript. All authors have read and agreed to the published version of the manuscript.

Funding

This research is supported by a grant from Kyung Hee University in 2016 (KHU-20161704).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable. The research has adhered to ethical practices that include, fundamentally, the informed consent of the participants and adherence to the guidelines for the practice of good publications, developed by the Publications Ethics Committee (COPE, 1997).

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Alexandra, B. Viacom CBS Seeks About $5.5 Million for 30-Second Commercial Spots in 2021 Super Bowl. Wall Str. J. 2020. Available online: https://www.wsj.com/articles/viacomcbs-seeks-about-5-5-million-for-30-second-commercial-spots-in-2021-super-bowl-11597956492 (accessed on 21 August 2020).

- Choong, P.; Filbeck, G.; Tompkins, D.L.; Ashman, T.D. An event study approach to evaluating the economic returns of advertising in the Super Bowl. Acad. Mark. Stud. J. 2003, 7, 89–99. [Google Scholar]

- Kim, J.-W.; Denton, L.T.; Wang, T. Assessing Stock Market Response to the Release of Ad Meter Rankings of Super Bowl TV Commercials. Int. J. Integr. Mark. Commun. 2015, 7, 15. [Google Scholar]

- Louie, T.A.; Kulik, R.L.; Jacobson, R. When bad things happen to the endorsers of good products. Mark. Lett. 2001, 12, 13–23. [Google Scholar] [CrossRef]

- Agrawal, J.; Kamakura, W.A. The economic worth of celebrity endorsers: An event study analysis. J. Mark. 1995, 59, 56–62. [Google Scholar] [CrossRef]

- Lane, V.; Jacobson, R. Stock market reactions to brand extension announcements: The effects of brand attitude and familiarity. J. Mark. 1995, 59, 63–77. [Google Scholar] [CrossRef]

- Tellis, G.J.; Johnson, J. The value of quality. Mark. Sci. 2007, 26, 758–773. [Google Scholar] [CrossRef] [Green Version]

- Wiles, M.A.; Danielova, A. The worth of product placement in successful films: An event study analysis. J. Mark. 2009, 73, 44–63. [Google Scholar] [CrossRef]

- Fehle, F.; Tsyplakov, S.; Zdorovtsov, V. Can companies influence investor behaviour through advertising? Super bowl commercials and stock returns. Eur. Financ. Manag. 2005, 11, 625–647. [Google Scholar] [CrossRef]

- Kim, J.; Morris, J.D. The effect of advertising on the market value of firms: Empirical evidence from the super bowl ads. J. Target. Meas. Anal. Mark. 2003, 12, 53–65. [Google Scholar] [CrossRef] [Green Version]

- Kim, K.; Cheong, Y.; Kim, H. Information content of Super Bowl commercials 2001–2009. J. Mark. Commun. 2012, 18, 249–264. [Google Scholar] [CrossRef]

- Schmidt, S.; Eisend, M. Advertising repetition: A meta-analysis on effective frequency in advertising. J. Advert. 2015, 44, 415–428. [Google Scholar] [CrossRef]

- Newell, S.J.; Henderson, K.V. Super Bowl advertising: Field testing the importance of advertisement frequency, length and placement on recall. J. Mark. Commun. 1998, 4, 237–248. [Google Scholar] [CrossRef]

- Kanner, B. The Super Bowl of Advertising: How the Commercials Won the Game; UNC Press Books: Chapel Hill, NC, USA, 2004; Volume 77. [Google Scholar]

- Tomkovick, C.; Yelkur, R.; Christians, L. The USA’s biggest marketing event keeps getting bigger: An in-depth look at Super Bowl advertising in the 1990s. J. Mark. Commun. 2001, 7, 89–108. [Google Scholar] [CrossRef]

- Raithel, S.; Taylor, C.R.; Hock, S.J. Are Super Bowl ads a super waste of money? Examining the intermediary roles of customer-based brand equity and customer equity effects. J. Bus. Res. 2016, 69, 3788–3794. [Google Scholar] [CrossRef]

- Lewis, R.A.; Reiley, D.H. Down-to-the-minute effects of super bowl advertising on online search behavior. In Proceedings of the Fourteenth ACM Conference on Electronic Commerce, Philadelphia, PA, USA, 16–20 June 2013; pp. 639–656. [Google Scholar]

- Chandrasekaran, D.; Srinivasan, R.; Sihi, D. Effects of offline ad content on online brand search: Insights from super bowl advertising. J. Acad. Mark. Sci. 2018, 46, 403–430. [Google Scholar] [CrossRef]

- Nail, J. Visibility versus surprise: Which drives the greatest discussion of Super Bowl advertisements? J. Advert. Res. 2007, 47, 412–419. [Google Scholar] [CrossRef]

- Noh, Y.; Kim, H.; Kim, K.; Cheong, Y. The relationship between consumer engagements with Super Bowl ad tweets and the advertisers’ official Twitter accounts: A panel data analysis of 2019 Super Bowl advertisers. Int. J. Advert. 2020, 1–18. [Google Scholar] [CrossRef]

- Eastman, J.K.; Iyer, R.; Wiggenhorn, J.M. The short-term impact of Super Bowl advertising on stock prices: An exploratory event study. J. Appl. Bus. Res. (JABR) 2010, 26. [Google Scholar] [CrossRef] [Green Version]

- Brown, S.J.; Warner, J.B. Using daily stock returns: The case of event studies. J. Financ. Econ. 1985, 14, 3–31. [Google Scholar] [CrossRef]

- Filbeck, G.; Zhao, X.; Tompkins, D.; Chong, P. Share price reactions to advertising announcements and broadcast of media events. Manag. Decis. Econ. 2009, 30, 253–264. [Google Scholar] [CrossRef]

- Tomkovick, C.; Yelkur, R.; Rozumalski, D.; Hofer, A.; Coulombe, C.J. Super Bowl Ads Linked to Firm Value Enhancement. J. Mark. Dev. Compet. 2011, 5, 29–43. [Google Scholar]

- Celsi, R.L.; Olson, J.C. The role of involvement in attention and comprehension processes. J. Consum. Res. 1988, 15, 210–224. [Google Scholar] [CrossRef]

- Zaichkowsky, J.L. Measuring the involvement construct. J. Consum. Res. 1985, 12, 341–352. [Google Scholar] [CrossRef]

- Bloch, P.H. An exploration into the scaling of consumers’ involvement with a product class. ACR N. Am. Adv. 1981, 8, 61–65. [Google Scholar]

- Tavassoli, N.I.; Fitzsimons, G. Program involvement. J. Advert. Res. 1995, 35, 61–72. [Google Scholar]

- Anand, P.; Sternthal, B. The effects of program involvement and ease of message counterarguing on advertising persuasiveness. J. Consum. Psychol. 1992, 1, 225–238. [Google Scholar] [CrossRef]

- Vaugn, R. How advertising works: A planning model revisited. J. Advert. Res. 1986, 26, 57–66. [Google Scholar]

- Ratchford, B.T. New insights about the FCB grid. J. Advert. Res. 1987, 27, 24–38. [Google Scholar]

- Hirschman, E.C.; Holbrook, M.B. Hedonic consumption: Emerging concepts, methods and propositions. J. Mark. 1982, 46, 92–101. [Google Scholar] [CrossRef] [Green Version]

- Strahilevitz, M.; Myers, J.G. Donations to charity as purchase incentives: How well they work may depend on what you are trying to sell. J. Consum. Res. 1998, 24, 434–446. [Google Scholar] [CrossRef]

- Kamins, M.A.; Marks, L.J.; Skinner, D. Television commercial evaluation in the context of program induced mood: Congruency versus consistency effects. J. Advert. 1991, 20, 1–14. [Google Scholar] [CrossRef]

- Kim, J.-W.; Freling, T.H.; Grisaffe, D.B. The Secret Sauce for Super Bowl Advertising: What Makes Marketing Work in the World’s Most Watched Event? J. Advert. Res. 2013, 53, 134–149. [Google Scholar] [CrossRef]

- Lord, K.R.; Burnkrant, R.E.; Unnava, H.R. The effects of program-induced mood states on memory for commercial information. J. Curr. Issues Res. Advert. 2001, 23, 1–15. [Google Scholar] [CrossRef]

- Tellis, G.J. Effective frequency: One exposure or three factors? J. Advert. Res. 1997, 37, 75–80. [Google Scholar]

- Cacioppo, J.T.; Petty, R.E. Effects of message repetition and position on cognitive response, recall, and persuasion. J. Personal. Soc. Psychol. 1979, 37, 97. [Google Scholar] [CrossRef]

- Pechmann, C.; Stewart, D.W. Advertising repetition: A critical review of wearin and wearout. Curr. Issues Res. Advert. 1988, 11, 285–329. [Google Scholar]

- Zajonc, R.B. Attitudinal effects of mere exposure. J. Personal. Soc. Psychol. 1968, 9, 1. [Google Scholar] [CrossRef] [Green Version]

- Benninga, S. Financial modeling. In Massachusetts Institute of Technology, 3rd ed.; MIT Press: Cambridge, MA, USA, 2008. [Google Scholar]

- Strieter, J.; Weaver, J. A longitudinal study of the depiction of women in a United States business publication. J. Am. Acad. Bus. 2005, 7, 229–235. [Google Scholar]

- Choi, H.; Yoon, H.J.; Paek, H.-J.; Reid, L.N. ‘Thinking and feeling’products and ‘utilitarian and value-expressive’appeals in contemporary TV advertising: A content analytic test of functional matching and the FCB model. J. Mark. Commun. 2012, 18, 91–111. [Google Scholar] [CrossRef]

- Joshi, A.; Hanssens, D.M. The direct and indirect effects of advertising spending on firm value. J. Mark. 2010, 74, 20–33. [Google Scholar] [CrossRef] [Green Version]

- Kim, K.; Cheong, Y. Latent factors of executional elements influencing commercial likeability: An exploratory study of super bowl commercials. J. Glob. Acad. Mark. 2011, 21, 83–93. [Google Scholar] [CrossRef]

- Krugman, H.E. The impact of television advertising: Learning without involvement. Public Opin. Q. 1965, 29, 349–356. [Google Scholar] [CrossRef]

- MacKinlay, A.C. Event studies in economics and finance. J. Econ. Lit. 1997, 35, 13–39. [Google Scholar]

Figure 1.

Event Study Period.

Figure 2.

Average Abnormal Returns around Event Date.

Figure 3.

Distribution of AAR and CAAR.

Figure 4.

Distribution of CAAR by Product Involvement.

Figure 5.

Distribution of CAAR by Utilitarian/Hedonic Product.

Figure 6.

Distribution of AAR by the number of Ad Executions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Samples of the Present Study.

| Year | # of Firms | # of Ads | Advertisers (# of Executions) |

|---|---|---|---|

| 2010 | 11 | 21 | Anheuser-Busch (5), Campbell soup, Comcast (2), Denny’s (2), Disney (2), Dr. pepper, Electronic Arts, Google, Pepsi (4), Qualcomm, Unilever |

| 2011 | 8 | 20 | Anheuser-Busch (5), Best buy, CarMax (2), Coca-Cola (2), Disney, Fiat Chrysler, Pepsi (7), Skechers |

| 2012 | 10 | 22 | Anheuser-Busch (4), Blucora, Coca-Cola (2), Disney (2), General Motors (4), Honda motors (2), Met life, Pepsi (2), Skechers, Toyota (2) |

| 2013 | 13 | 23 | Anheuser-Busch (5), Best buy, Colgate, Comcast, Disney, E-Trade, Fiat Chrysler (2), Ford motors (2), Gill, Mondelez, P&G, PVH, Pepsi (5) |

| 2014 | 12 | 25 | Anheuser-Busch (6), CarMax, Charter, Coca-Cola (2), Ford, Fiat Chrysler (2), General Mills, General Motors (2), Intuit (2), Microsoft, Pepsi (3), T-Mobile (3) |

| 2015 | 16 | 35 | Anheuser-Busch (3), Comcast (9), Fiat Chrysler (2), General Motors (2), Gruphub, Intuit, McDonald’s, Microsoft (2), Pepsi (4), P&G, Skechers, T-Mobile (2), Toyota (2), Unilever, Wix.com, WW international |

| 2016 | 22 | 36 | Adgewell, Amazon, Anheuser-Busch (5), AstraZeneca, Coca-Cola, Colgate, Comcast (2), Disney (2), Fiat Chrysler (2), Fitbit, General Motors, Honda (2), Intuit, Kraft, Newell brands, Paypal, Pepsi (4), Pfizer, T-Mobile (2), Toyota, Unilever (2), Wix.com |

| 2017 | 16 | 21 | Anheuser-Busch (2), Apple, Comcast, Disney (3), Dr. pepper, Fiat chrysler, General Motors, H&R block, Intuit, McDonald’s, Netflix, Pepsi, P&G (2), T-Mobile, Toyota, Wendy’s |

| 2018 | 14 | 30 | Anheuser-Busch (6), Amazon (2), Coca-Cola (3), Comcast (3), Disney, E-Trade, Fiat Chrysler (4), Groupon, Intuit, Netflix, Pepsi, P&G (2), Toyota (3), Wix.com |

| 2019 | 20 | 39 | ADT, Anheuser-Busch (9), Amazon (2), Colgate, Comcast, Disney (2), Google (2), Intuit, Kraft (2), Kellogg, Microsoft, Netflix, Norwegian cruise, Pepsi (3), P&G, Skechers, T-Mobile (3), Toyota (2), Verizon (2), Wix.com |

| Total | 142 | 272 |

# represents number.

Table 2.

Description of Samples by Product Type.

| Year | Low Involvement n (%) | High Involvement n (%) | Utilitarian n (%) | Hedonic n (%) |

|---|---|---|---|---|

| 2010 | 5 (45.5) | 6 (54.5) | 6 (54.5) | 5 (45.5) |

| 2011 | 3 (37.5) | 5 (62.5) | 3 (37.5) | 5 (62.5) |

| 2012 | 3 (30.0) | 7 (70.0) | 5 (50.0) | 5 (50.0) |

| 2013 | 5 (38.5) | 8 (61.5) | 9 (69.2) | 4 (30.8) |

| 2014 | 4 (33.3) | 8 (66.7) | 9 (75.0) | 3 (25.0) |

| 2015 | 6 (37.5) | 10 (62.5) | 12 (75.0) | 4 (25.0) |

| 2016 | 6 (27.3) | 16 (72.7) | 18 (81.8) | 4 (18.2) |

| 2017 | 6 (37.5) | 10 (62.5) | 9 (56.3) | 7 (43.8) |

| 2018 | 4 (28.6) | 10 (71.4) | 9 (64.3) | 5 (35.7) |

| 2019 | 6 (30.0) | 14 (70.0) | 14 (70.0) | 6 (30.0) |

| Total | 48 (33.8) | 94 (66.2) | 94 (66.2) | 48 (33.8) |

Table 3.

Statistical Significance of AAR and CAAR.

| Event Day | Average Abnormal Return (%) | T-Statistic | p-Value | Cumulative Average Abnormal Return (%) | T-Statistic | p-Value |

|---|---|---|---|---|---|---|

| (−10) | 0.097% | 0.832 | 0.407 | 0.097% | 0.832 | 0.407 |

| (−9) | 0.137% | 0.877 | 0.382 | 0.234% | 1.145 | 0.254 |

| (−8) | 0.050% | 0.421 | 0.674 | 0.284% | 1.203 | 0.231 |

| (−7) | 0.049% | 0.276 | 0.783 | 0.334% | 1.152 | 0.251 |

| (−6) | 0.273% | 1.591 | 0.114 | 0.607% | 1.862 | 0.065 |

| (−5) | 0.006% | 0.047 | 0.963 | 0.612% | 1.690 | 0.093 |

| (−4) | −0.419% | −2.811 | 0.006 ** | 0.193% | 0.518 | 0.606 |

| (−3) | −0.023% | −0.122 | 0.903 | 0.170% | 0.428 | 0.669 |

| (−2) | −0.071% | −0.393 | 0.695 | 0.099% | 0.245 | 0.806 |

| (−1) | −0.572% | −3.029 | 0.003 ** | −0.473% | −1.041 | 0.300 |

| (0) | −0.840% | −4.253 | 0.000 ** | −1.313% | −2.471 | 0.015 * |

| (1) | 0.505% | 3.267 | 0.001 ** | −0.808% | −1.478 | 0.142 |

| (2) | 0.103% | 0.667 | 0.506 | −0.705% | −1.363 | 0.175 |

| (3) | −0.572% | −3.370 | 0.001 ** | −1.277% | −2.275 | 0.024 * |

| (4) | 0.374% | 2.202 | 0.029 * | −0.903% | −1.680 | 0.095 |

| (5) | 0.502% | 3.603 | 0.000 ** | −0.401% | −0.759 | 0.449 |

| (6) | 0.869% | 6.639 | 0.000 ** | 0.468% | 0.871 | 0.385 |

| (7) | 0.176% | 1.210 | 0.228 | 0.644% | 1.127 | 0.262 |

| (8) | 0.300% | 1.866 | 0.064 | 0.944% | 1.560 | 0.121 |

| (9) | 0.585% | 4.554 | 0.000 ** | 1.529% | 2.470 | 0.015 * |

| (10) | −0.488% | −2.714 | 0.007 ** | 1.040% | 1.576 | 0.117 |

* p ≤ 0.05, ** p ≤ 0.01.

Table 4.

CAARs for Windows Surrounding the Event Day.

| Event Window | CAARs (%) | T-Statistic | p-Value |

|---|---|---|---|

| (−10, +10) | 1.040% | 1.576 | 0.117 |

| (−10, −2) | 0.099% | 0.245 | 0.806 |

| (−5, +5) | −1.007% | −2.173 | 0.031 |

| (−5, −2) | −0.508% | −1.929 | 0.056 |

| (−1, 0) | −1.412% | −4.477 | 0.000 |

| (0, +1) | −0.335% | −1.315 | 0.190 |

| (−1, +1) | −0.907% | −2.603 | 0.010 |

| (+1, +2) | 0.609% | 3.272 | 0.001 |

| (+1, +5) | 0.912% | 3.083 | 0.002 |

| (+1, +10) | 2.353% | 5.438 | 0.000 |

| (−1, +10) | 0.941% | 1.924 | 0.056 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Lee, J.-G.; Ko, K.-A. The Market Responses to Super Bowl Advertising: The Role of Product Type and Multiple Executions. Sustainability 2021, 13, 7127. https://0-doi-org.brum.beds.ac.uk/10.3390/su13137127

AMA Style

Lee J-G, Ko K-A. The Market Responses to Super Bowl Advertising: The Role of Product Type and Multiple Executions. Sustainability. 2021; 13(13):7127. https://0-doi-org.brum.beds.ac.uk/10.3390/su13137127

Chicago/Turabian StyleLee, Jung-Gyo, and Kyung-A Ko. 2021. "The Market Responses to Super Bowl Advertising: The Role of Product Type and Multiple Executions" Sustainability 13, no. 13: 7127. https://0-doi-org.brum.beds.ac.uk/10.3390/su13137127

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.