Transparency and Accountability in Sports: Measuring the Social and Financial Performance of Spanish Professional Football

Abstract

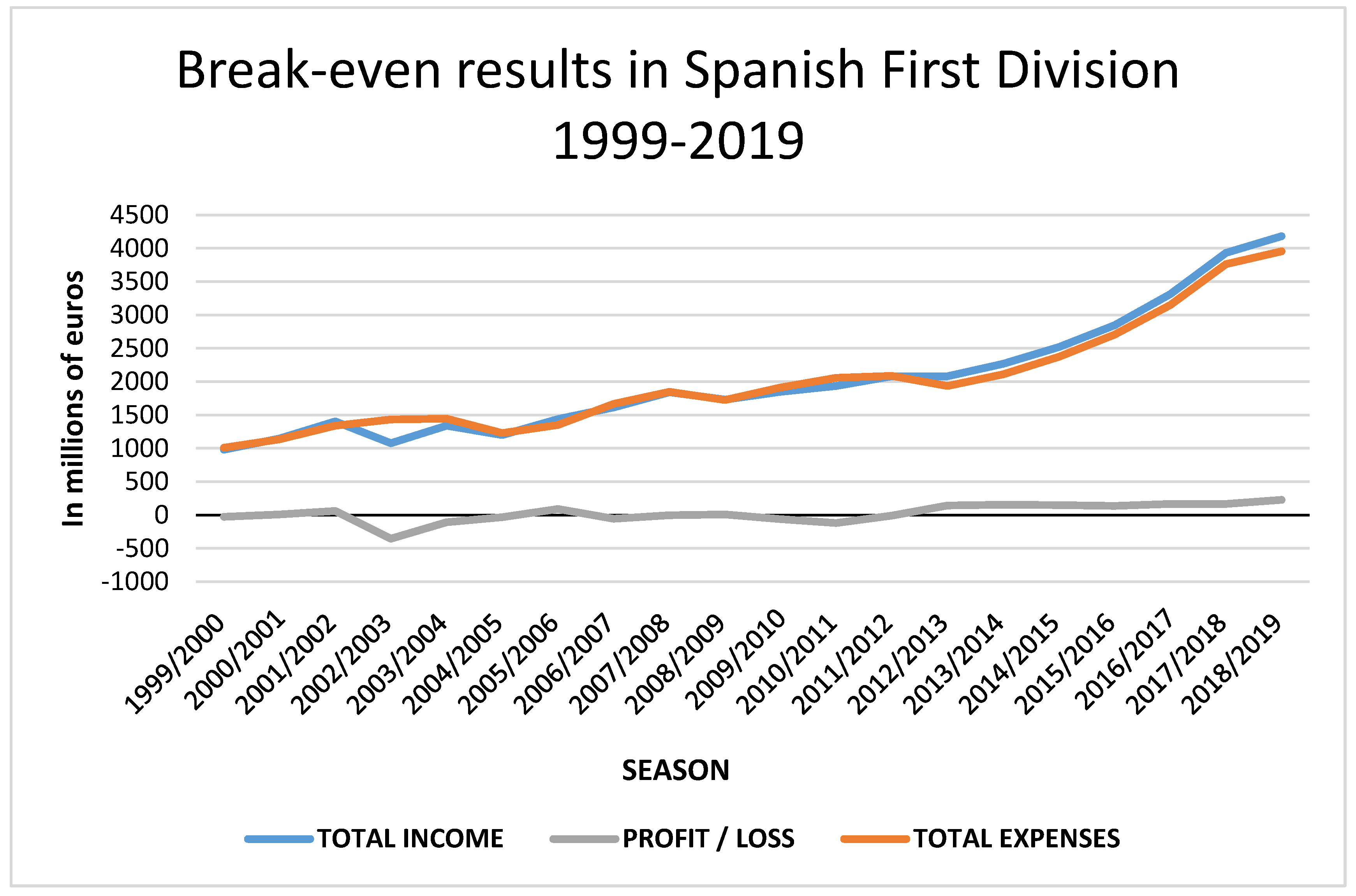

:1. Introduction

2. Previous Literature

2.1. Transparency and Social Performance in Professional Spanish Football

2.2. Accountability and Financial Performance in Professional Football

2.3. Social Performance vs. Financial Performance in Spanish Professional Football

2.4. Formulation of Hypotheses

3. Materials and Methods

3.1. Sample and Data

3.2. Empirical Analysis

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Smith, E.D. The Effect of the Separation of Ownership from Control on Accounting Policy Decisions. Account. Rev. 1976, 51, 707–723. [Google Scholar] [CrossRef]

- Barros, P.S. Portuguese football. J Sport Econ. 2006, 7, 96–104. [Google Scholar] [CrossRef]

- Emery, R.; Weed, M. Fighting for survival? The financial management of football clubs outside the ‘top flight’ in England. Manag. Leis. 2006, 11, 1–21. [Google Scholar]

- Ogbonna, E.; Harris, C.L. Organizational cultural perpetuation: A case study of an English Premier League football club. Br. J. Manag. 2014, 25, 667–686. [Google Scholar] [CrossRef]

- Yeh, C.M.; Taylor, T. Issues of governance in sport organisations: A question of board size, structure and roles. World Leis. J. 2008, 50, 33–45. [Google Scholar] [CrossRef]

- Kennedy, P. ‘Left wing’ supporter movements and the political economy of football. Soccer Soc. 2013, 14, 277–290. [Google Scholar] [CrossRef]

- Storm, K.R.; Nielsen, K. Soft budget constraints in professional football. Eur. Sport Manag. Q. 2012, 12, 183–201. [Google Scholar] [CrossRef]

- Pielke, R., Jr. How can FIFA be held accountable? Sport Manage. Rev. 2013, 16, 255–267. [Google Scholar] [CrossRef]

- Making an Impact: Annual Report 2013, Deloitte, Belgium. Available online: http://www2.deloitte.com/content/dam/Deloitte/be/Documents/about-deloitte/BE_Annual-report_2013_web.pdf (accessed on 16 July 2020).

- Annual Review of Football Finance 2014 Highlights, Sports Business Group. Available online: https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/sports-business-group/deloitte-uk-annual-review-football-finance.pdf (accessed on 18 July 2020).

- Gammelsæter, H. Institutional pluralism and governance in ‘Commercialized’ sport clubs. Eur. Sport Manag. Q. 2010, 10, 569–594. [Google Scholar] [CrossRef]

- Robinson, T.; Simmons, R. Gate-sharing and talent distribution in the English football league. Int. J. Econ. Bus. 2014, 21, 413–429. [Google Scholar] [CrossRef] [Green Version]

- Buchholz, F.; Lopatta, K. Stakeholder salience of economic investors on professional football clubs in Europe. Eur. Sport Manag. Q. 2017, 17, 506–530. [Google Scholar] [CrossRef]

- Buraimo, B.; Simmons, R.; Szymanski, S. English football. J Sport Econ. 2006, 7, 29–46. [Google Scholar] [CrossRef]

- Dimitropoulos, P.E.; Stergios, L.; Emmanouil, D. Managing the European football industry: UEFA’s regulatory intervention and the impact on accounting quality. Eur. Sport Manag. Q. 2016, 4, 459–486. [Google Scholar] [CrossRef]

- Dimitropoulos, P.E. Corporate governance and earnings management in the European football industry. Eur. Sport Manag. Q. 2011, 5, 495–523. [Google Scholar] [CrossRef]

- Nicoliello, M.; Zampatti, D. Football club’s profitability after the Financial Fair Play Regulation: Evidence from Italy. Sports Bus. Manag. 2016, 6, 460–475. [Google Scholar] [CrossRef]

- Wilson, R.; Plumley, D.; Ramchandani, G. The relationship between ownership structure and club performance in the English Premier League. Sports Bus. Manag. 2013, 3, 19–36. [Google Scholar] [CrossRef]

- Urdaneta, R.; Martín, E.; Guevara, J. The Other Side of the Star League: Report on the Transparency and Financial Situation of Spanish Football [Paper presentation], XX AECA International Congress, Málaga, Spain, September 25–27. Available online: https://xxcongreso.aeca.es/wp-content/uploads/2019/09/81c.pdf (accessed on 11 June 2020).

- Sports Business Group. Football Money League 2019. Available online: https://www2.deloitte.com/cl/es/pages/consumer-business/articles/football-money-league-2019.html# (accessed on 18 July 2020).

- Barajas, A.; Rodríguez, P. Spanish football club’s finances: Crisis and player salaries. Int. J. Sport Finance. 2010, 5, 52–66. Available online: https://ssrn.com/abstract=1569552 (accessed on 14 September 2020).

- Barajas, A.; Rodríguez, P. Spanish Football in need of financial therapy: Cut expenses and inject capital. Int. J. Sport Finance. 2014, 9, 73–90. Available online: https://ssrn.com/abstract=2389293 (accessed on 14 September 2020).

- Leach, S.; Szymanski, S. Making money out of football. Scott. J. Political Econ. 2015, 62, 25–50. [Google Scholar] [CrossRef] [Green Version]

- García, J.; Rodríguez, P. From Sports clubs to stock companies: The financial structure of football in Spain 1992–2001. Eur. Sport Manag. Q. 2003, 3, 235–269. [Google Scholar] [CrossRef]

- Mareque, M.; Barajas, A.; López-Corrales, F. The Impact of Union of European Football Associations (UEFA) Financial Fair Play Regulation on Audit Fees: Evidence from Spanish Football. Int. J. Financ. Studies. 2018, 6, 92. [Google Scholar] [CrossRef] [Green Version]

- Plumley, D.; Ramchandani, G.M.; Wilson, R. The unintended consequence of Financial Fair Play: An examination of competitive balance across five European football leagues. Sports Bus. Manag. 2019, 9, 118–133. [Google Scholar] [CrossRef]

- Gallagher, R.; Quinn, B. Regulatory own goals: The unintended consequences of economic regulation in professional football. Eur. Sport Manag. Q. 2019, 20, 151–170. [Google Scholar] [CrossRef]

- Dimitropoulos, P.; Scafarto, V. The impact of UEFA financial fair play on player expenditures, sporting success and financial performance: Evidence from the Italian top league. Eur. Sport Manag. Q. 2019, 21, 20–38. [Google Scholar] [CrossRef]

- Franck, E. European club football after ‘five treatments’ with financial fair play-time for an assessment. Int. J. Financ. Stud. 2018, 6, 97. [Google Scholar] [CrossRef] [Green Version]

- Peeters, T.; Szymanski, S. Financial fair play in European football. Econ. Policy. 2014, 29, 343–390. [Google Scholar] [CrossRef] [Green Version]

- Ahtiainen, S.; Jarva, H. Has UEFA’s financial fair play regulation increased football clubs’ profitability? Eur. Sport Manag. Q. 2020, 1–19. [Google Scholar] [CrossRef]

- Transparency Law 19/2013 of December 9, on Transparency, Access to Public Information and Good Governance. Available online: https://www.boe.es/eli/es/l/2013/12/09/19/con (accessed on 18 December 2019).

- UEFA. UEFA Club Licensing and Financial Fair Play Regulations, Edition 2010 ed; UEFA: Nyon, Switzerland, 2010. [Google Scholar]

- Professional Football League. General Regulations of the Professional Football League. 2016, 10, pp. 91–125. Available online: https://assets.laliga.com/assets/2020/07/23/originals/80f0a96624c7a9a5df2ff048066a6489.pdf (accessed on 18 December 2019).

- Henry, I.; Lee, P.C. Governance and ethics in sport. In The Business of Sport Management; Beech, J., Chadwick, S., Eds.; Harlow: Pearson Education: London, UK, 2004; pp. 25–41. [Google Scholar]

- Mrkonjic, M. Measuring the Governance of International Sport Organisations: Democracy, Transparency and Responsibility as Key Attributes. 21st Conference of the European Association for Sport Management, Sport Management for Quality of Life, Istanbul, Turkey; 2013. Available online: http://www.easm.net/download/2013/MEASURING%20THE%20GOVERNANCE%20OF%20INTERNATIONAL%20SPORT%20ORGANISATIONS.pdf (accessed on 15 February 2019).

- Král, P.; Cuskelly, G. A model of transparency: Determinants and implications of transparency for national sport organizations, Eur. Sport Manag. Q. 2018, 18, 237–262. [Google Scholar] [CrossRef]

- Cotterrell, R. Transparency, mass media, ideology and community. J. Cult. Res. 1999, 3, 414–426. [Google Scholar] [CrossRef]

- Djokic, D. Corporate governance in Slovenia: Disclosure and transparency of public companies. Int. J. Manag. Cases. 2012, 14, 41–48. [Google Scholar] [CrossRef]

- Rawlins, B. Give the emperor a mirror: Toward developing a stakeholder measurement of organizational transparency. J. Public Relat. Res. 2008, 21, 71–99. [Google Scholar] [CrossRef]

- Strathern, M. The tyranny of transparency. Br. Educ. Res. J. 2000, 26, 309–321. [Google Scholar] [CrossRef]

- Fernández, J.; López, R. Responsabilidad Social y Buen Gobierno en los Clubes de Fútbol españoles. Univ. Bus. Rev. 2015, 2, 38–53. [Google Scholar]

- Transparency International Spain (TIE). Index of Transparency of the Football Club (INFUT). Available online: https://transparencia.org.es/indice-de-los-clubs-de-futbol-infut/ (accessed on 15 February 2020).

- Grant, R.; Keohane, R.O. Accountability and abuses of power in world politics. Am. Political Sci. Rev. 2005, 99, 29–43. [Google Scholar] [CrossRef] [Green Version]

- François, A.; Bayle, E.; Gond, J.P. A multilevel analysis of implicit and explicit CSR in French and UK professional sport. Eur. Sport Manag. Q. 2019, 19, 15–37. [Google Scholar] [CrossRef] [Green Version]

- Edwards, M.; Hulme, D. NGO performance and accountability in the post-cold war world. J. Int. Dev. 1995, 7, 849–856. [Google Scholar] [CrossRef]

- Morrow, S. Football club financial reporting: Time for a new model? Sports Bus. Manag. 2013, 3, 297–311. [Google Scholar] [CrossRef]

- Morrow, S. Financial Fair Play-Implications for Football Club Financial Reporting. The Institute of Chartered Accountants of Scotland. 2014. Available online: http://www.storre.stir.ac.uk/bitstream/1893/21393/1/ICAS%20Financial%20Fair%20Play%20Report%20-%20Stephen%20Morrow.pdf (accessed on 21 September 2019).

- Solberg, H.A.; Haugen, K.K. European club football: Why enormous revenues are not enough? Sport Soc. 2010, 13, 329–343. [Google Scholar] [CrossRef]

- Sánchez, L.C.; Barajas, A.; Sánchez-Fernández, P. Finanzas del deporte: Fuentes de ingreso y regulación financiera en el fútbol europeo. Pap. Econ. Española. 2019, 159, 200–223. Available online: https://dialnet.unirioja.es/servlet/articulo?codigo=6896173 (accessed on 14 September 2020).

- Dimitropoulos, P.E. Audit selection in the European football industry under Union of European Football Associations Financial Fair Play. IJEFI 2016, 6, 901–906. Available online: https://www.econjournals.com/index.php/ijefi/article/view/2229 (accessed on 7 October 2020).

- Balance de la Situación Económico-Financiera del Fútbol Español 1999–2019. Subdirección General de Deporte Profesional y Control Financiero del Consejo Superior de Deportes. 2020. Available online: https://www.csd.gob.es/sites/default/files/media/files/2020-07/Balance%20situaci%C3%B3n%20F%C3%9ATBOL%201999-2019.pdf (accessed on 14 September 2020).

- Guevara, J.C.; Martín, E.; Arcas, M.J. Financial Sustainability and Earnings Management in the Spanish Sports Federations: A Multi-Theoretical Approach. Sustainability 2021, 13, 2099. [Google Scholar]

- Moskowitz, M. Choosing Socially Responsible Stocks. Bus. Soc. Rev. 1972, 1, 72–75. [Google Scholar]

- Friedman, M. Capitalism and Freeform; University of Chicago Press: Chicago, IL, USA, 1962; Available online: https://press.uchicago.edu/ucp/books/book/chicago/C/bo68666099.html (accessed on 19 February 2020).

- Preston, L.E.; O’Bannon, D.P. The Corporate Social-Financial Performance Relationship: A Tipology and analysis. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Gómez, F. Responsabilidad Social Corporativa y Performance Financiero: Treinta y Cinco Años de Investigación Empírica en Busca de un Consenso. Principios 2008, 11, 5–22. [Google Scholar]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate: Twenty-five years on incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives bry busuness. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef] [Green Version]

- Moneva, J.M.; Ortas, E. Corporate environmental and financial performance: A multivariate approach. Ind. Manag. Data Syst. 2010, 110, 193–210. [Google Scholar] [CrossRef]

- Rodríguez, M. Social responsibility and financial performance: The role of good corporate governance. BRQ Bus. Res. Q. 2016, 19, 137–151. [Google Scholar] [CrossRef] [Green Version]

- Reverte, C. Determinants of corporate social disclosure by Spanish listed firms. J. Bus. Ethics. 2009, 88, 351–366. [Google Scholar] [CrossRef]

- Chand, M.; Fraser, S. The Relationship between Corporate Social Performance and Corporate Financial Performance: Industry Type as a Boundary Condition. Bus. Rev. 2006, 5, 240–245. [Google Scholar]

- Inoue, Y.; Kent, A.; Lee, S. CSR and the bottom line: Analysing the link between CSR and financial performance for professional teams. J. Sport Manag. 2011, 25, 531–549. [Google Scholar] [CrossRef]

- Sánchez, L.C.; Sánchez-Fernández, P.; Barajas, A. Ownership structures and financial profitability in European football, J. Sports Econ. Manage. 2016, 6, 5–17. Available online: https://dialnet.unirioja.es/servlet/articulo?codigo=5583923 (accessed on 14 September 2020).

- Dimitropoulos, P.E.; Tsagkanos, A. Financial performance and corporate governance in the European football industry. Int. J. Sport Finance. 2012, 7, 280–308. Available online: http://fitpublishing.com/journals/international-journal-sport-finance-ijsf-74 (accessed on 7 October 2020).

- Kelly, S. Understanding the role of the football manager in Britain and Ireland: Weberian Approach. Eur. Sport Manag. Q. 2008, 8, 399–419. [Google Scholar] [CrossRef]

- Hamil, S.; Morrow, S. Corporate Social Responsibility in the Scottish Premier League: Context and Motivation. Eur. Sport Manag. Q. 2011, 11, 143–170. [Google Scholar] [CrossRef]

- Dermit-Richard, N.; Scelles, N.; Morrow, S. French DNCG management control versus UEFA Financial Fair Play: A divergent conception of financial regulation objectives. Soccer Soc. 2017, 20, 408–430. [Google Scholar] [CrossRef]

- Orlitzky, M. Does firm size confound the relationship between corporate social performance and firm financial performance? J. Bus. Ethics. 2001, 33, 167–180. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/25074599 (accessed on 21 September 2020). [CrossRef]

- Van Tendeloo, B.; Vanstraelen, A. Earnings management under German GAAP versus IFRS. Eur. Account. Rev. 2005, 14, 155–180. [Google Scholar] [CrossRef]

- Watts, R.; Zimmerman, J. Positive accounting theory: A ten-year perspective. Account. Rev. 1990, 65, 131–156. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/247880 (accessed on 21 September 2020).

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad Manag. J. 1988, 31, 854–872. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/256342 (accessed on 19 February 2020).

- Birkhäuser, S.; Kaserer, C.; Urban, D. Did UEFA’s financial fair play harm competition in European football leagues? Rev. Manag. Sci. RMS. 2017, 1–33. [Google Scholar] [CrossRef] [Green Version]

- Doornik, J.; Hansen, H. An omnibus test for univariate and multivariate normality. Oxf. Bull. Econ. Statistics. 2008, 70, 927–939. [Google Scholar] [CrossRef]

- Pesaran, M.H. General diagnostic tests for cross section dependence in panels. Empir. Econ. 2021, 60, 13–50. Available online: https://0-link-springer-com.brum.beds.ac.uk/article/10.1007%2Fs00181-020-01875-7 (accessed on 15 February 2021). [CrossRef]

- Breusch, T.A. Pagan. The Lagrange multiplier test and its application to model specification in econometrics. Rev. Econ. Stud. 1980, 47, 239–253. [Google Scholar] [CrossRef]

- Blavoukos, S.; Caramanis, C.; Dedoulis, E. Europeanisation, independent bodies and the empowerment of technocracy: The case of the Greek auditing oversight body. South Eur. Soc. Politics. 2013, 18, 139–157. [Google Scholar] [CrossRef]

- Washington, M.; Patterson, K.D. Hostile Takeover or Joint Venture: Connections between Institutional Theory and Sport Management Research. Sport Manag. Rev. 2011, 1, doi. [Google Scholar] [CrossRef]

- Neri, L.; Russo, A.; Di Domizio, M. Giambattista Rossi. Football players and asset manipulation: The management of football transfers in Italian Serie, A. Eur. Sport Manag. Q. 2021, 1–21. [Google Scholar] [CrossRef]

- Torres, L.; Martin, E.; Guevara, J.C. The gold rush: Analysis of the performance of the Spanish Olympic federations. Cogent Soc. Sci. 2018, 4, 1. [Google Scholar] [CrossRef]

- Scafarto, V.; Dimitropoulos, P. Human capital and financial performance in professional football: The role of governance mechanisms. Corp. Gov: Int. J. Bus. Soc. 2018, 18, 289–316. [Google Scholar] [CrossRef]

{kind=link}

| Min | Max | Mean | Std. Dev. | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2015 | 2016 | 2019 | 2015 | 2016 | 2019 | 2015 | 2016 | 2019 | 2015 | 2016 | 2019 | |

| INFUT | 10.00 | 15.80 | 53.13 | 100.00 | 100.00 | 100.00 | 44.21 | 62.81 | 93.63 | 23.23 | 23.39 | 10.68 |

| INCLUB | 22.20 | 16.70 | 65.00 | 100.00 | 100.00 | 100.00 | 51.21 | 75.73 | 94.17 | 23.04 | 23.29 | 9.17 |

| INSOC | 16.70 | 30.60 | 64.29 | 100.00 | 100.00 | 100.00 | 51.34 | 74.11 | 96.68 | 22.91 | 21.89 | 6.94 |

| INEF | 0.00 | 0.00 | 0.00 | 100.00 | 100.00 | 100.00 | 34.24 | 49.64 | 90.60 | 30.60 | 33.84 | 22.64 |

| INCS | 0.00 | 0.00 | 0.00 | 100.00 | 100.00 | 100.00 | 22.44 | 40.73 | 87.62 | 28.00 | 33.94 | 24.18 |

| INT | 0.00 | 0.00 | 0.00 | 100.00 | 100.00 | 100.00 | 52.10 | 64.30 | 94.18 | 27.86 | 24.65 | 16.87 |

| CAUSAL SEQUENCE | SIGN OF THE RELATIONSHIP | ||

|---|---|---|---|

| Positive | Neutral | Negative | |

| SP →FP | Social impact hypothesis | Hypothesis of the “moderator” variables | Trade-off hypothesis |

| FP →SP | Hypothesis of the availability of funds | Hypothesis of opportunism of managers | |

| SP ↔ FP | Positive synergy | Negative synergy | |

| Regulatory Framework | Performance | Variables | Indicators |

|---|---|---|---|

| TL 19/2013 | Social Performance | Transparency | Index INFUT |

| UEFA’s FFP/LFP’s RCE | Financial Performance | Accountability | ROA/Leverage/Solvency/Liquidity/Herfindahl Index |

| Variable | Min | Max | Mean | Std. Dev. |

|---|---|---|---|---|

| INFUT | 10.000 | 100.000 | 70.436 | 28.594 |

| ROA | −35.276 | 45.625 | 6.884 | 13.945 |

| LEV | −26.344 | 22.703 | 2.816 | 6.697 |

| SOLV | 0.222 | 8.361 | 1.749 | 1.378 |

| LIQ | 0.057 | 6.761 | 0.977 | 0.984 |

| INDICE H t-1 | 0.253 | 1.000 | 0.475 | 0.176 |

| LOG ACT | 15.291 | 21.030 | 18.018 | 1.380 |

| TIME | 1.000 | 3.000 | 2.000 | 0.821 |

| Variables | INFUT | ROA | LEV | SOLV | LIQ | IH t-1 | SIZE | TIME |

|---|---|---|---|---|---|---|---|---|

| INFUT | 1 | |||||||

| ROA | 0.135 | 1 | ||||||

| LEV | −0.068 | −0.057 | 1 | |||||

| SOLV | 0.179 | −0.048 | −0.123 | 1 | ||||

| LIQ | 0.155 | −0.09 | −0.127 | 0.728 | 1 | |||

| IH t-1 | −0.029 | −0.144 | −0.101 | 0.276 | 0.416 | 1 | ||

| SIZE | 0.153 | −0.035 | 0.31 | −0.321 | −0.302 | −0.295 | 1 | |

| TIME | 0.725 | −0.023 | 0.007 | 0.09 | 0.113 | 0.076 | 0.143 | 1 |

| MODEL 1 Random-Effects GLS Regression | MODEL 2 FGLS Regression | |||||

|---|---|---|---|---|---|---|

| Coefficient | z | Significance | Coefficient | z | Significance | |

| ROAit | 0.3182122 | 2.01 | 0.044 ** | 0.361393 | 7.59 | 0.000 *** |

| LEVit | −0.3610613 | −1.09 | 0.275 | −0.485518 | −3.49 | 0.000 *** |

| SOLVit | 3.513109 | 1.47 | 0.142 | 2.755744 | 3.69 | 0.000 *** |

| LIQit | 0.0089839 | 0.00 | 0.998 | 2.173572 | 2.03 | 0.043 ** |

| IHit-1 | −10.72099 | −0.79 | 0.428 | −16.40291 | −4.42 | 0.000 *** |

| SIZEit | 2.519967 | 1.25 | 0.213 | 2.160404 | 2.77 | 0.006 ** |

| TIMEit | 24.43574 | 10.23 | 0.000 *** | 24.03663 | 21.65 | 0.000 *** |

| Constant | −26.06973 | −0.69 | 0.493 | −17.98682 | −1.43 | 0.152 |

| R-sq = | 0.5869 | Time periods = | 3 | |||

| Number Observations = | 84 | Number Observations = | 84 | |||

| Number of groups = | 28 | Number of groups = | 28 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Urdaneta, R.; Guevara-Pérez, J.C.; Llena-Macarulla, F.; Moneva, J.M. Transparency and Accountability in Sports: Measuring the Social and Financial Performance of Spanish Professional Football. Sustainability 2021, 13, 8663. https://0-doi-org.brum.beds.ac.uk/10.3390/su13158663

Urdaneta R, Guevara-Pérez JC, Llena-Macarulla F, Moneva JM. Transparency and Accountability in Sports: Measuring the Social and Financial Performance of Spanish Professional Football. Sustainability. 2021; 13(15):8663. https://0-doi-org.brum.beds.ac.uk/10.3390/su13158663

Chicago/Turabian StyleUrdaneta, Rudemarlyn, Juan C. Guevara-Pérez, Fernando Llena-Macarulla, and José M. Moneva. 2021. "Transparency and Accountability in Sports: Measuring the Social and Financial Performance of Spanish Professional Football" Sustainability 13, no. 15: 8663. https://0-doi-org.brum.beds.ac.uk/10.3390/su13158663