To Rebuild or Relocate? Long-Term Mobility Decisions of Hazard Mitigation Grant Program (HMGP) Recipients

Department of Landscape Architecture and Urban Planning, Texas A&M University, Langford A311, College Station, TX 77843-3137, USA

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(16), 8754; https://0-doi-org.brum.beds.ac.uk/10.3390/su13168754

Submission received: 1 July 2021

/

Revised: 27 July 2021

/

Accepted: 30 July 2021

/

Published: 5 August 2021

(This article belongs to the Special Issue Flood Vulnerability and Resilience in Urban Settings: Perspectives for Sustainability)

Abstract

:Limited funds and the demand for disaster assistance call for a broader understanding of how homeowners decide to either rebuild or relocate from their disaster-affected homes. This study examines the long-term mobility decisions of homeowners in Lumberton, North Carolina, USA, who received federal assistance from the Hazard Mitigation Grant Program (HMGP) for property acquisition, elevation, or reconstruction following Hurricane Matthew in 2016. The authors situate homeowners’ decisions to rebuild or relocate in the context of property attributes and neighborhood characteristics. Logit and probit regressions reveal that homeowners with lower-value properties are less likely to relocate, and those subjected to higher flood and inundation risks are more likely to relocate. Additionally, homeowners in neighborhoods of higher social vulnerability—those with a higher proportion of minorities and mortgaged properties—are more likely to rebuild their disaster-affected homes. The authors discuss homeowners’ mobility decisions in the context of the social vulnerability of neighborhoods. Our results contribute to an ongoing policy discussion that seeks to articulate the housing and neighborhood attributes that affect the long-term mobility decisions of recipients of HMGP assistance. The authors suggest that local governments prioritize the mitigation of properties of homeowners of higher physical and social vulnerability to reduce socioeconomic disparities in hazard mitigation and build equitable community resilience.

1. Introduction

Disasters are commonly defined as “an event concentrated in time and space, in which a society or a relatively self-sufficient subdivision of a society, undergoes severe danger and incurs such losses to its members and physical appurtenances that the social structure is disrupted and the fulfillment of all or some of the essential functions of the society is prevented” [1] (p. 655). The increasing intensity and frequency of disasters prove a growing concern to nations across the globe, but particularly to the United States. In 2017, the number of disasters worldwide (over 700) more than tripled the count in 1980 (slightly over 200) [2]. The Insurance Information Institute estimates over 100 disasters struck the United States in 2018 alone: More than three-fifths were meteorological and hydrological, heightening concern for coastline counties, which house nearly one-third (29.1%) of the nation’s population and are among the fastest-growing counties in the United States [3]. This poses a significant threat not only to individual lives but also to real estate: CoreLogic estimates that in 2019 alone, over 7 million single-family residential homes along the Gulf and Atlantic Coasts had the potential for storm surge damage that could generate nearly $2 trillion in reconstruction costs [4].

The increasing incidence of disasters along the coasts, combined with the growing proportion of the population exposed to potential disasters, exacerbates the threat of property damage and population displacement. Rising levels of property damage will increase the total cost of damage, the share of homeowners who seek disaster assistance, and the amount of assistance requested. Limited funds for disaster assistance, combined with the increasing demand for such funds, dictates a broader understanding of the factors that contribute to the mobility decisions of homeowners who receive funding to either rebuild or relocate. The disaster literature largely focuses on these factors in the context of homeowners who are offered buyouts (i.e., property acquisition), as opposed to homeowners who receive funding for property elevation or reconstruction [5,6,7,8,9]. The purpose of our research is to explore the relationship between property and neighborhood attributes and the mobility decisions of homeowners who receive Hazard Mitigation Grant Program (HMGP) assistance to either rebuild or relocate.

Aiming to decrease the exposure of people and property to disasters, the Federal Emergency Management Agency (FEMA) administers the HMGP, which constitutes the oldest and largest hazard mitigation program for homeowners [10]. The HMGP was founded in the 1980s and has provided various mitigation activities that assist in implementing long-term mitigation planning and projects following a Presidential major disaster declaration, including property acquisition, structure demolition or relocation, structural elevation, mitigation reconstruction, dry floodproofing, structural retrofitting, safe room construction, wind retrofitting, and hazard mitigation planning [11]. However, HMGP assistance is largely directed to home buyouts. From 1989 to 2018, approximately 40,000 properties damaged by hydrological events were bought out by the HMGP, representing nearly 97% of total HMGP activities [12,13].

Following Hurricane Matthew (October 2016), in Lumberton, North Carolina, USA, a city of 20,000 situated approximately 70 miles from the Atlantic Coast, 400 homeowners applied for HMGP funding [14]. The funding ultimately provided 101 homeowners the opportunity to relocate or rebuild their disaster-affected homes through one of three mechanisms: Property acquisition, reconstruction, or elevation. Acquisition—including structure demolition/relocation—involves the purchase of the flood-prone property by the city, which demolishes it and, in return, provides just compensation to the homeowner, which is determined through an appraisal and subsequent review of the appraiser’s recommended fair market value. Mitigation reconstruction entails the demolition of the disaster-affected home, and a home comparable in size is constructed in its wake. Elevation involves raising the home to a sufficient height to allow potential floodwaters to flow underneath, rather than infiltrate, the home [15].

Lumberton offers a unique study site: Its high physical and social vulnerability and the incidence of two hurricanes in less than two years. The Lumber River, which runs through the city, paired with the city’s near sea-level elevation, renders it particularly prone to flooding. Thus, in Lumberton, recurrent disasters prove particularly deleterious. In addition, Lumberton is one of the poorest and most racially diverse cities in North Carolina and the United States [16]. The low socioeconomic status of its residents exacerbates the effects of disasters. As seen in Table 1, over one-third of the city’s population lives in poverty: In 2016, the poverty rate for Lumberton measured 35.1%, more than double that of North Carolina (16.8%) and the United States (15.1%). The city is predominantly minority: In 2016, 37.4% of its population was African American; 13%, Native American (Lumbee tribe); and 36.4%, white (non-Hispanic or Latino). Hurricane Matthew resulted in significant property damage and population displacement: 400 housing units were destroyed, and nearly 1000 residents in south Lumberton, a largely African American area, permanently relocated [17]. In this regard, Lumberton represents an excellent case for this study as the poorest, most diverse, and heavily flood-exposed small towns in the United States face a higher recurrence of disaster events. Thus, investigating the long-term mobility decisions of recipients of HMGP assistance could provide policy implications for the future HMGP design for areas with similar conditions in the United States.

As the distribution of HMGP funding may span several years, and project completion, several more years, Hurricane Matthew (2016) offers a unique opportunity for the researchers to trace the long-term mobility decisions of 101 homeowners in Lumberton. The authors examine the decision-making process—i.e., to rebuild or relocate recipients of HMGP assistance. The authors situate the mobility decisions of HMGP recipients in the context of property and neighborhood attributes to address the question: How do housing and sociodemographic characteristics at the property and neighborhood levels shape the long-term mobility decisions of HMGP recipients? Combining FEMA’s HMGP data, Robeson County appraisal data, Decennial Census, and floodplain and inundation depth data, the authors conducted binomial logit and probit regressions to estimate the impacts of property and neighborhood attributes on the homeowner’s decision to rebuild or relocate. Our study indicates that the HMGP recipients whose properties are physically vulnerable to floods are more likely to relocate, while those whose properties are situated in neighborhoods of higher social vulnerability are less likely to relocate. These homeowners likely face several financial constraints, as well as less information on available resources (i.e., lower social capital), which diminish their ability to adequately mitigate, prepare for, respond to, and recover from disasters, especially in the absence of disaster assistance—as such, ensuring that homeowners in neighborhoods of higher social vulnerability receive adequate funding to rebuild or relocate from their disaster-affected properties should diminish disparities in disaster recovery.

2. Theoretical Framework

It is well-established that the impact of disasters tends to disproportionately affect households and remains a challenge for disadvantaged groups (e.g., low-income households, ethnic minorities, the elderly, or the disabled). Researchers call this condition “vulnerability” and define it as “the characteristics of a person or group and their situation that influence their capacity to anticipate, cope with, resist and recover from the impact of a natural hazard” [18] (p. 9). Scholars have coined two terms—physical and social vulnerability—to encapsulate household (and community) disparities to the exposure and effects of disasters [19,20]. In this study, physical vulnerability is “the susceptibility to damage and loss based on the interaction between exposure and physical characteristics, including structure, critical infrastructure, and the natural environment that protects the community” [20] (p. 83). Meanwhile, social vulnerability refers to “the potential for loss and its complex interaction among risk, mitigation, and the social fabric of a place” [21] (p.8). While physical and social vulnerability are well-established fields in the disaster literature, studies examining the relationship between these concepts and the long-term mobility decisions of homeowners who receive disaster assistance have recently begun to emerge. Although previous research finds such assistance critically shapes recipients’ decisions to relocate from their disaster-affected properties (via buyouts) [5,8,22,23], little research has examined the contribution of federal funding in facilitating hazard mitigation for individual recipients through property elevation or reconstruction. The authors chose the City of Lumberton to explore this relationship as it is of high physical and social vulnerability and experienced severe damage from two hurricanes over the course of less than two years. Physical and social vulnerability recognize that the extent and costs of property damage are not evenly distributed across disaster-affected areas. Disasters disproportionately affect households of higher physical and social vulnerability, which are not only more likely to live in flood-prone areas (as housing costs are generally lower), but also face greater financial constraints and less information on the resources available to them to mitigate and recover from disasters [19,20].

The authors review key factors affecting the homeowner’s decision to relocate or rebuild, including (1) property attributes [6,24,25,26], (2) community factors [6,8,24,26,27], (3) homeowners’ perceptions [28,29,30], (4) sociodemographic characteristics [6,23,26,31,32], and (5) the attributes of grant programs [5,31,33,34]. As this study does not involve surveys or interviews, the authors would face data and methodological limitations with respect to the second, third, and fifth factors. Instead, this study focuses on property attributes and sociodemographic characteristics. Although not yet fully developed, the study provides exploratory findings for these factors.

2.1. Property Attributes

Economists, policymakers, and disaster researchers argue that homeowners’ mobility decisions are shaped by economic rationality—in essence, seeking to maximize one’s financial benefits while minimizing costs [8]. Although economic rationality is not the sole factor considered in homeowners’ decision-making processes, studies on repetitive property losses from flooding have primarily positioned homeowners’ mobility decisions in the context of economic rationality [8,35]. Particularly, studies on coastal risks and flood hazards find that homeownership and property values are highly important to mobility decisions as homeowners tend to seek comparable homes of prices similar to the pre-disaster assessed values received through buyouts [8,22,26]. However, the relationship between property value and the likelihood of accepting a buyout option is inconclusive. Emphasizing the importance of design decisions of the buyout program conception on homeowners’ experiences during the process, Binder and Greer [31] illustrated a fear among homeowners who rejected the buyout offer that their property values would depreciate as other households in the neighborhood accepted the buyout. These homeowners expressed fear over the potential social and economic impacts that eminent domain would ultimately be used if they decline the buyout offer, and the just compensation awarded to them would amount to less than the buyout offer. Similarly, a post-crisis temporal vulnerability among residents who have historically failed disaster recovery on properties may drive homeowners to accept the buyout when they conclude they have no better alternative [34]. However, others find contradictory results for homeowners of higher socioeconomic status, for whom property values are positively related to place attachment. Homeowners with higher-value properties and who live in affluent neighborhoods may be less likely to accept the buyout offer [8,22,23].

Meanwhile, socially vulnerable homeowners face greater concerns over the financial consequences of relocation. That is, these homeowners carefully weigh the decision to repair their disaster-affected home or accept the buyout and purchase a different property [27,36]. In addition, studies identified that the affordability of comparable homes is a significant consideration of socially vulnerable homeowners, which is likely to be less of a concern to households who do not face similar financial constraints [5,23,26,31].

A large body of literature emphasizes homeowners’ perceptions of flood risk, repetitive losses from flooding, and whether living in a flood-prone area increases the probability of accepting the buyout offer [5,8,37]. Kunreuther [38] and Robinson, Davidson, Trainor, Kruse, and Nozick [5] provide evidence that homeowners with properties located in a floodplain bear a higher likelihood of accepting the buyout offer. In addition, flood frequency and intensity are also considered important factors in the decision to relocate [24]. Researchers also addressed property damage from floods and its significant effect on the homeowner’s propensity to accept the buyout offer [26,39,40].

2.2. Neighborhood-Level Sociodemographic Attributes

Homeowners decide to relocate based on a holistic consideration of both their individual situations and the responses of their neighbors [19,40,41,42,43]. Researchers investigating post-disaster mobility decisions have focused on the relationship between homeowners and their surrounding communities, the physical and social vulnerability of a community, and its environmental characteristics. Prior research found that socially and economically vulnerable communities are less likely to receive disaster assistance due to a lack of bureaucratic and monetary resources.

Family composition is another important factor affecting homeowner’s mobility decisions. Bird, et al. [44] and King, et al. [45] revealed that the households most likely to relocate were primarily young or middle-aged, had vocational qualifications, were of moderate-income, and had children or other dependents. On the other hand, elderly and minority communities are more likely to stay in place—despite repetitive flood risks—because such adults are “aging in place” and have a fear that relocation can severely impact their quality of life by separating them from their daily routines [22,40,46].

Social ties among community members and attachment to a community are strong motivators for homeowners to remain in their pre-disaster properties, but this varies based on demographic, socioeconomic, spatial, and psychosocial determinants [8,22,47,48]. Specifically, researchers find strong social ties among minority homeowners, which significantly affect mobility decisions. Previous studies have demonstrated that race plays a significant role in the homeowner’s decision to reject or accept a buyout offer [5,48,49,50]. Given that, Li, et al. [51], Reeser [26], and Riad and Norris [47] demonstrated that African Americans are less likely to choose to relocate. Minorities and the elderly have been significantly excluded from the post-disaster recovery process [52]. The trajectory and quality of the recovery process vary widely depending on demographic characteristics [53,54,55].

Neighborhood housing characteristics also affect homeowners’ long-term mobility decisions. Cutter, et al. [56] addressed the unequal distribution of disaster assistance in the recovery and mitigation processes, particularly in the aftermath of Hurricane Katrina, and suggested that the funding provisions were unfavorable to socially vulnerable populations, including renters, low-income households, and families below the poverty level, and they are more likely to be excluded from disaster assistance [52]. Specifically, neighborhoods with a higher proportion of renter-occupied units are generally correlated with higher social vulnerability; as such, homeowners in these neighborhoods, on average, face greater financial constraints and less information on the resources available to them, rendering them less likely to relocate. In addition, homeowners with a mortgage have difficulty in participating in the HMGP program, given that the pre-disaster value of the property might prohibit those homeowners from choosing to relocate if it is not enough to purchase a comparable home out of floodplain [31,57].

The literature has largely studied disaster assistance in the context of property acquisition (buyouts), leaving significant limitations in our understanding of disaster assistance in relation to property elevation and reconstruction. As such, while the literature on disaster assistance continues to examine the variety of factors that shape homeowners’ decisions to relocate, there remains a gap in the literature on the factors that motivate homeowners to seek property elevation or reconstruction. Based on the paucity of empirical studies that use hypothesis testing to investigate the relationship between the mobility decisions of HMGP recipients and factors affecting those decisions, the authors adopt an exploratory approach. In short, this paper aims to establish the role of three categories—property attributes and neighborhood sociodemographic and housing characteristics—on the long-term mobility decisions of homeowners. The authors pose the question: How do housing and sociodemographic characteristics at the household and neighborhood levels affect the long-term mobility decisions of homeowners?

3. Research Context and Methodology

3.1. Recipients of HMGP Assistance

In 2017, when homeowners in Lumberton applied for HMGP assistance, applicants faced three options: Property acquisition (buyouts), elevation, or reconstruction. The authors group homeowners into two categories: Those who relocate and those who remain. Homeowners awarded assistance for property acquisition fall into the first category, as they chose to sell their properties to the government and relocate to another housing unit. On the contrary, recipients awarded assistance for property elevation or reconstruction fall into the second category, as they chose to rebuild their damaged homes and remain in their pre-disaster neighborhoods.

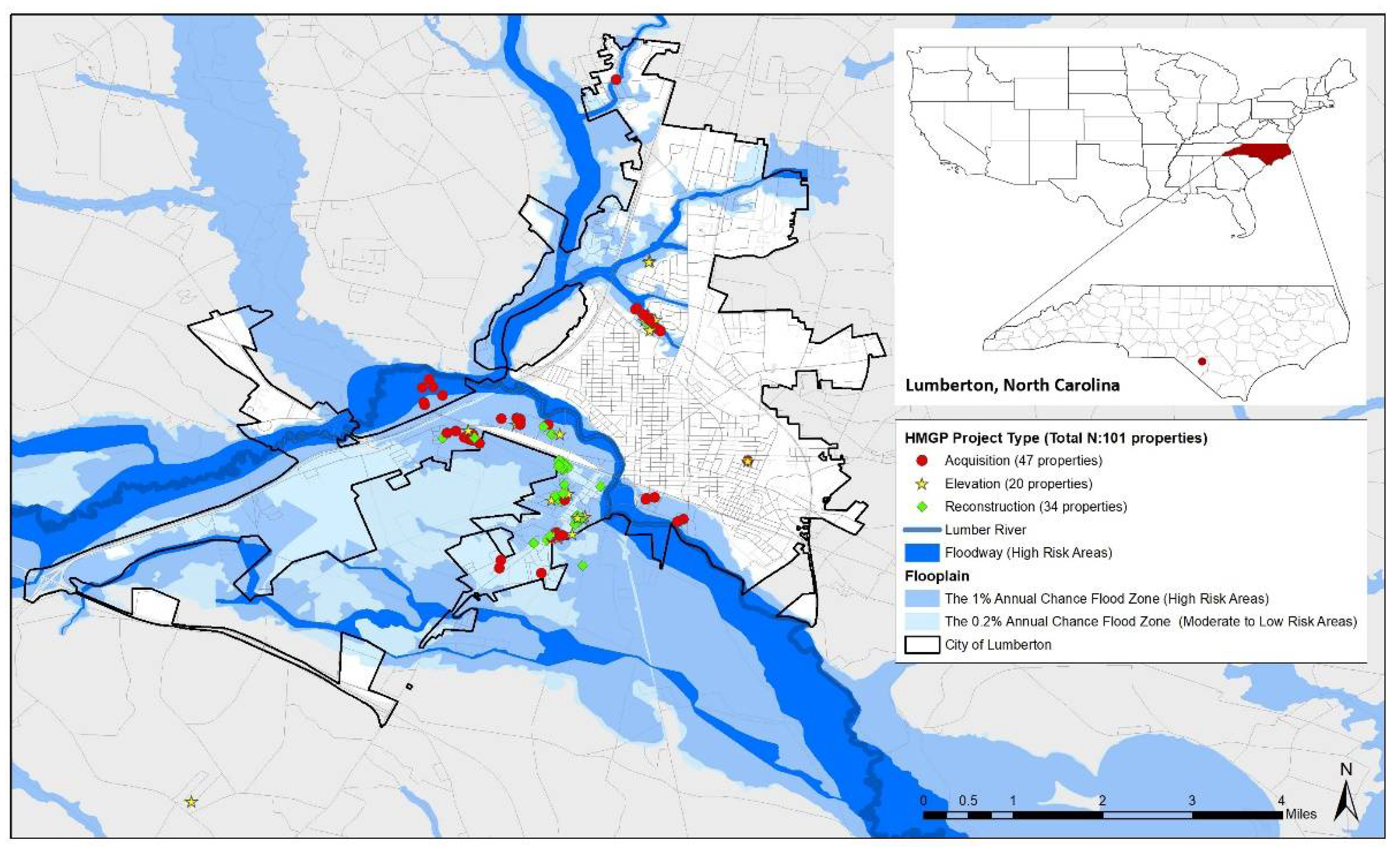

Among the 400 applicants in Lumberton, 101 were awarded a total of $13.5 million in HMGP funding in June 2018 (106 homeowners were initially awarded assistance, but five homeowners dropped out of the program). Households in Lumberton constitute approximately 12.5% of all recipients of HMGP assistance from Hurricane Matthew in North Carolina. By the end of the program (the anticipated completion date was October 2020), 47 properties were acquired, 20 homes were elevated, and 34 homes were reconstructed. The cost of each option was relatively constant: The city spent $127,872 per property acquisition, $124,820 per property elevation, and $129,213 per property reconstruction [58]. Figure 1 depicts the distribution of HMGP recipients’ properties across the city of Lumberton. The Lumber River, which winds through the city, renders a floodplain of significant size. Since the northern portion of the city is of higher elevation, while the southern part of the city is only slightly above the river’s elevation [59], southern and western Lumberton are of higher physical vulnerability: Land in these regions lies within the floodway and the 100-year flood zone (if not also the 500-year flood zone). Southern Lumberton bore a disproportionately high concentration of dislocated households and heavily damaged properties after Hurricane Matthew in 2016. The majority of assisted properties are located in either a floodway or floodplain and lie primarily in the southern and western portions of the city, which experienced the most damage from Hurricane Matthew.

3.2. Data Sources

This study combines multiple datasets to investigate the role of property attributes and neighborhood sociodemographic and housing characteristics on the mobility decisions of HMGP recipients. The authors obtained the list of HMGP recipients from the City of Lumberton. This study uses Robeson County appraisal data for property-level data and 2010 Decennial Census data at the block level from the IPUMS National Historical Geographic Information System (NHGIS) for neighborhood-level data [60]. The Robeson County appraisal data for 2016 and 2017 from NC OneMap includes parcel values (i.e., assessed values), ownership information, the presence of a structure on the property, and site addresses. To calculate the potential effects of Hurricane Matthew (October 2016) on home value, the pre-disaster property values are reflected by the 2016 assessed values published that March; post-disaster property values are the 2017 assessed values published that October. The authors use 2010 Decennial Census data collected from the IPUMS NHGIS at the block level to capture neighborhood sociodemographic and housing characteristics. Given the small size of Lumberton’s population (approximately 20,000 people), the authors use the smallest geographic unit—the block—for which data are publicly available. Compared to block groups or tracts, this unit of analysis introduces more variation into the data, allowing for higher degrees of freedom for the variables that measure neighborhood characteristics. The properties of the 101 HMGP recipients lie within 47 blocks and 10 block groups across the city of Lumberton. If the study used the block group as the unit of analysis, it would increase the likelihood of failing to reject a false null hypothesis (committing a Type II error). The authors also collected FEMA floodplain and floodway GIS maps to determine the exposure of HMGP recipients’ properties to flooding. Finally, inundation depth data following Hurricane Matthew was obtained from the United States Geological Survey (USGS).

3.3. Methods

3.3.1. Variables

The authors use binomial logit and probit regressions to investigate the impacts of property attributes and neighborhood sociodemographic and housing characteristics on the long-term mobility decisions of homeowners who received HMGP assistance. The dependent variable, which represents the homeowner’s decision to rebuild or relocate, equals 1 when the HMGP recipient chooses to relocate. Independent variables consist of three categories: Property attributes and neighborhood sociodemographic and housing characteristics. Table 2 depicts definitions and descriptive statistics for variables used in the logit and probit models.

The first set of independent variables, property attributes, consists of five predictors. To correct the non-normality in the distribution of assessed values, the authors transformed the assessed value into its natural logarithm. Lower-income homeowners are more likely to face financial constraints that reduce the viability of relocation (thereby potentially affecting their mobility decision). The binary variable lowvalueproperty was used: A value of 1 indicates that the pre-disaster assessed value as a percentage of the median assessed value in Lumberton falls below 50%. This variable shows whether and how the lower-value properties in town affect homeowners’ mobility decisions compared to moderate and higher-value properties. In terms of the variable damage, using the change in assessed value as a proxy for housing damage has been well-established in previous studies (e.g., Bin and Kruse [61], De Silva, et al. [62], Zhang and Peacock [54], Peacock, Van Zandt, Zhang, and Highfield [19]). The variable damage reflects the change in each property’s improvement value from 2016 to 2017. The dummy indicator floodplain indicates whether a property is within the 500-year flood zone (0.2% annual chance flood zone) or 100-year flood zone (1% annual chance flood zone), with properties in the floodway acting as the reference group. The variable inundationdepth is obtained from the inundation shapefile created from the high-water mark data provided by the USGS and computed via a spatial join with the HMGP dataset.

The second set of independent variables, neighborhood sociodemographic characteristics, focuses on the age distribution and minority composition of the block. The model includes the percentage of children and the elderly in each block. In addition, as Lumberton is predominantly minority, the authors collected data on the three largest minorities in Lumberton: Non-Hispanic African Americans, non-Hispanic Native Americans, and individuals of Hispanic or Latino origin. The African American population of the blocks in which HMGP recipients’ properties are located (48.9%) exceeds, on average, that of the city (37.4%). Moreover, the Native American population of the blocks in which HMGP recipients’ properties are situated measures, on average, 18.5%, slightly higher than that of the city (approximately 13%).

Finally, the third set of variables, neighborhood housing characteristics, includes two variables: The proportion of renter-occupied units and the proportion of mortgaged owner-occupied properties. Fewer governmental resources are available to renters for disaster recovery and hazard mitigation [63]. Moreover, residents who have a mortgage on their homes are more likely to choose property reconstruction or elevation than property acquisition [31].

To identify the relationship between social vulnerability and the mobility decisions of HMGP recipients, the authors developed an overall social vulnerability score for each block group and created a map to depict the spatial distribution of socioeconomic disparity in Lumberton. The social vulnerability score, the methodology of which proves similar to the CDC’s Social Vulnerability Index, reflects the sum of 16 social vulnerability indicators related to disaster funding, discussed in detail in Appendix B, and ranks each block group in Lumberton. Rankings are based on percentile, with values ranging from 0 to 1. Higher values indicate greater vulnerability [64].

3.3.2. Data Analysis: Logit and Probit Models

Logit and probit models assume that a binary outcome random variable is driven by a latent random variable that ranges from 0 to 1. While probit regression uses the cumulative distribution function of the normal distribution to enforce the assumption, logit regression uses the logit function with the sigmoid form. Logit and probit models follow the equations:

In this paper, P represents the probability Yi = 1 of homeowner i selecting property acquisition, while β indicates the coefficients to be estimated. In the probit model, is the cumulative density function for the standard normal. In addition, βj indicates the change in the probability based on a unit change in the jth variable, holding all other variables constant.

Although the binary probit model has theoretical grounds that are reasonable and robust for its assumptions about the distributions of the disturbance terms, εi and εj, the choice probability of the model is expressed as an integral [65]. This often makes it difficult to interpret and renders the binary logit model the commonly used form in practice because of its computationally simpler technique and easier interpretation [66]. While the logit model is superior in terms of its analytical perspective, the probit model estimates with a more reliable theoretical basis [65]. Thus, this study takes advantage of the benefits of both models by comparing the results of the logit and the probit models.

The authors regressed the mobility decisions of HMGP recipients on three sets of independent variables—property attributes and neighborhood sociodemographic and housing characteristics. In this regard, the authors estimated the models as follows:

Y(relocate)i = β0 + β1X(ln_homevalue)i + β2X(lowvalued)i + β3X(damage)i + β4X(flood_500yr)i +

β5X(flood_100yr)i + β6X(inundationdepth)i + β7X(pop_over65)i + β8X(pop_under18)i + β9X(race_AA)i +

β10X(race_NA)i + β11X(race_HI)i + β12X(renter)i + β13X(ownloan)i

β5X(flood_100yr)i + β6X(inundationdepth)i + β7X(pop_over65)i + β8X(pop_under18)i + β9X(race_AA)i +

β10X(race_NA)i + β11X(race_HI)i + β12X(renter)i + β13X(ownloan)i

As each household is nested in a block, neighborhood characteristics are identical for observations in the same block. The authors clustered standard errors by block to generate a robust variance estimate that corrects for within-cluster correlation. The authors ran alternative estimations for multilevel mixed-effects logistic regression, using a nested framework within a block, but the estimated magnitudes, signs, and significances of coefficients in the model produced essentially the same results. Thus, the authors chose to use the simpler models, the logit and probit regression with clustered robust standard errors, since the mixed effect model does not outperform the reported models.

4. Results and Discussion

4.1. Long-Term Mobility Decisions of HMGP Recipients

Table 3 reports the results of the logit and probit regression models. For each explanatory variable, the estimated coefficients indicate whether the sign of the effects on the probability of the long-term mobility decision is positive or negative. As both models are nonlinear and the coefficients are not marginal effects, the average marginal effects (AME) were estimated to show the impact of a unit change of each explanatory variable on the likelihood of choosing relocation.

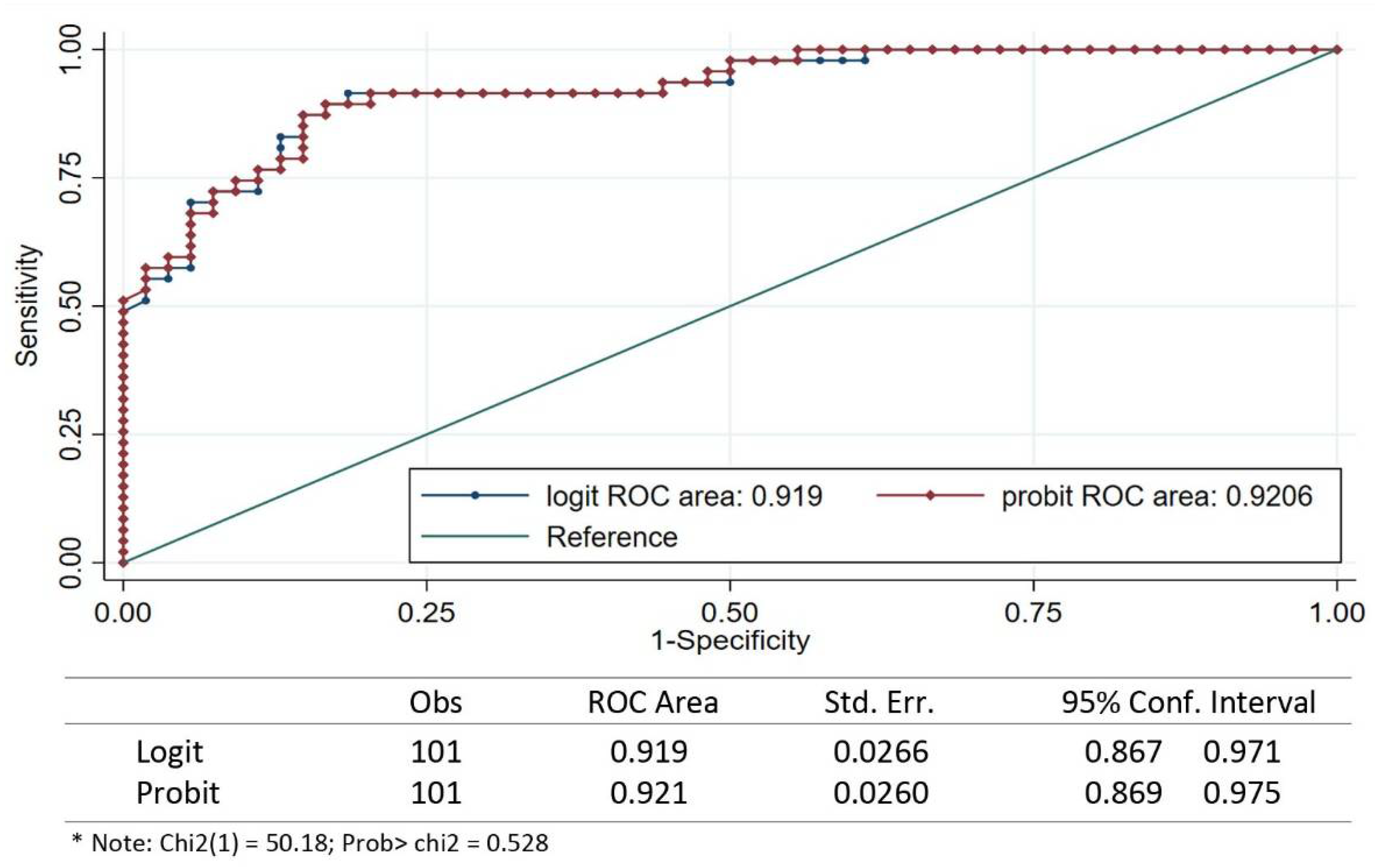

The logit and probit models explain approximately 50% of the variance in the probability that the HMGP recipient chooses relocation (49.92% and 50.31%, respectively). The authors conducted the area under the receiver operating characteristics (ROC) curves for both models to measure and compare the accuracy between the predictive tests [67]. The areas under the ROC curves for both models are above 0.9 (0.919 and 0.921, respectively), representing excellent accuracy. In addition, the result suggests that we cannot reject the hypothesis that the area under the ROC curve for the logit and probit model is equal (Chi2 = 50.18; Prob > Chi2 = 0.528) (See Appendix A).

In both models, homeowners with lower-value properties are less likely to choose relocation. High risks of flood and inundation are significant factors in the mobility decision. Compared to homeowners whose properties lie within the floodway, which is the highest risk area, homeowners of properties located in a 100-year flood zone depict a lower probability of choosing to relocate. Furthermore, HMGP recipients with heavily inundated properties are more likely to relocate.

A variable depicting neighborhood minority composition is statistically significant. Specifically, an increase in the African American, Native American, and Hispanic or Latino populations in a neighborhood decreases the likelihood that HMGP recipients will relocate. Strong social ties and community attachment may affect such a decision. Furthermore, minority homeowners exhibit differing risk perceptions for future disasters and less trust in governmental interventions than non-minority homeowners, reducing the likelihood that minorities will seek relocation [50].

Finally, the proportion of mortgaged properties in neighborhoods is significantly associated with the likelihood that HMGP recipients will choose to remain. The proportion of mortgaged properties exhibited a strong negative association with the probability of choosing to relocate, which follows the results of previous studies.

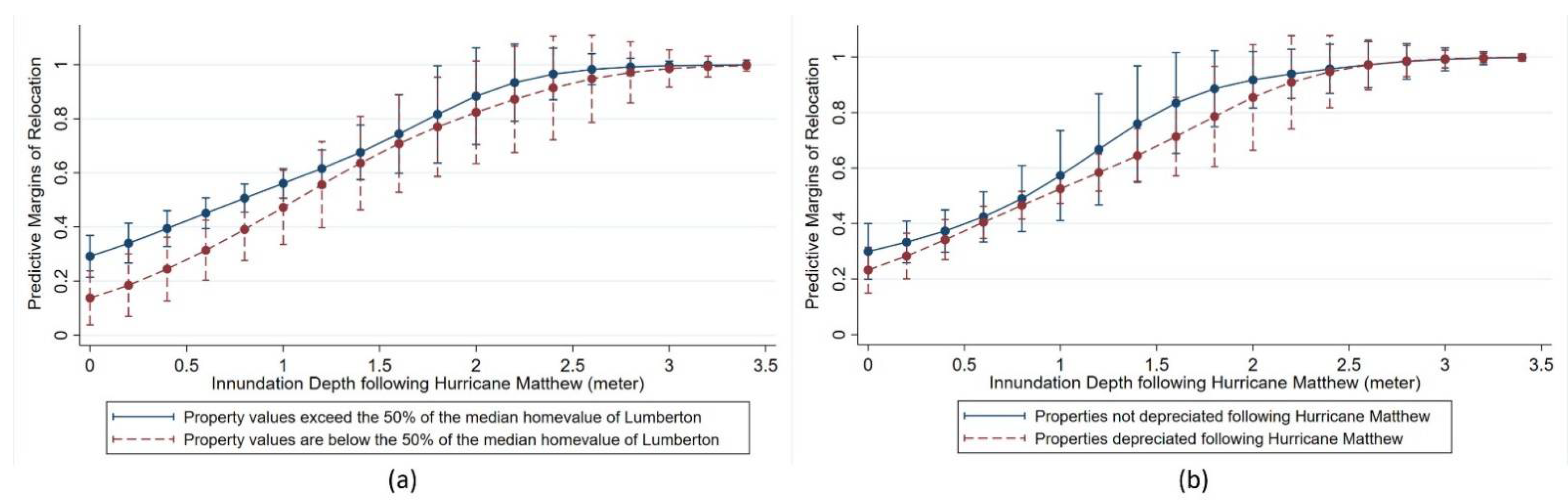

Examining the predictive margins for the probability of relocation sheds light on how homeowners with financial constraints face significant challenges in mobility decisions. Figure 2 exhibits predictive margins for the probability of relocation over inundation depth based on the ratio of the property value to the city’s median property value and depreciation in property value. Controlling for all other explanatory variables, Figure 2a indicates that regardless of the severity of inundation risks, homeowners whose property values are below the median property value of Lumberton are less likely to relocate. Similarly, homeowners whose properties depreciated following Hurricane Matthew are less likely to relocate than those whose properties did not depreciate in the overall range of inundation risk (see Figure 2b).

4.2. Discussion of the Logit and Probit Model Results

The findings from both models suggest that homeowners with lower-value properties are less likely to relocate. Moreover, homeowners whose properties are subjected to higher flood and inundation risks are more likely to relocate. Additionally, homeowners in neighborhoods of higher social vulnerability—those with a higher proportion of minorities and mortgaged properties—are more likely to rebuild their disaster-affected homes.

The results also provide evidence that property value should be carefully interpreted as a factor of the homeowner’s long-term mobility decision among HMGP assistance. Albeit only in the probit model, the greater the home value, the higher the probability the homeowner relocates. Homeowners with higher value properties may have invested more heavily in their properties as well as home upgrades, serving as disincentives for them to choose relocation. Put differently, higher economic dependence on place and property could function as an obstacle to accepting the buyout offer [22]. Kick, Fraser, Fulkerson, McKinney, and De Vries [8] explain this tendency by looking at the effect of “median household income” on the “condition of the property” through structural equation modeling. They conclude that wealthier residents find it more difficult to reach decisions favorable to relocation due to the higher economic value of the property. Given that the value of HMGP assistance awarded is estimated based on the pre-flood market value of the property, introducing “property value” into the models as an economic factor contributes to directly evaluating the impact of financial compensation on homeowners’ mobility decisions in terms of rational economic choice.

Additionally, findings from both the logit and probit models point to the high impact of home value on the mobility decision, specifically among HMGP recipients who have a lower-value property in town, suggesting their lower likelihood of relocation. This is seemingly contradictory to the findings in De Vries [34] that flood victims who experience repetitive property damage may face post-disaster vulnerability and be more likely to accept the buyout offer when they consider the alternative options. In our sample, even though the HMGP recipients are provided funds to either rebuild or relocate, finding a home of equivalent quality in safer areas through relocation may be another challenge to lower-value property owners due to financial constraints. In this regard, our quantitative findings corroborate previous exploratory studies that suggest residents with lower economic status may have fewer perceived options and thereby a reduced willingness to relocate [5,6,26]. In sum, our findings support that housing price is a determinant factor affecting mobility decisions among the HMGP recipients in terms of rational economic choice. Still, home values should be considered in different contexts (i.e., whether it is lower or higher value property) as a matter of choice opportunity.

The findings indicate that HMGP recipients with properties facing higher flood risks and heavily inundated properties are more likely to relocate, confirming the findings of previous studies, which argue that risk perception and direct experience with hazards are significant drivers behind the mobility decision [68,69,70,71,72]. Introducing inundation depth as a property-level attribute affecting the homeowner’s mobility decision has not been attempted yet in the previous research and is notable in that it captures physical vulnerability to floods, which would have been directly increased by Hurricane Matthew and following flood events. The inundation depth is statistically significant in both the logit and probit models, depicting the increased likelihood of relocation. These results are consistent with existing literature suggesting the increased likelihood of relocation of homeowners in higher risks of floodplains [5,71].

Regarding neighborhood minority composition, the findings indicate that an increase in the African American, Native American, and Hispanic or Latino populations in a neighborhood decreases the likelihood that HMGP recipients will relocate. The existing literature found that minorities are more likely to remain in their homes following disasters [5,47,48,50,51]. Unlike other cases, a relatively higher proportion of the Lumbee Tribe resides in Lumberton (12.6%). The findings suggest a statistical association between the higher proportion of Native Americans in neighborhoods and a lower likelihood of relocation. It is possible that minority homeowners have lower risk perceptions for future disasters and less trust in government implementation than non-minority residents, and thereby are less confident that choosing relocation would be a viable option for them.

Moreover, the higher proportion of mortgaged properties in neighborhoods is statistically associated with the lower likelihood of relocation among the HMGP recipients. The findings corroborate De Vries [57] arguing that homeowners with a mortgage face greater difficulty in deciding to participate in the HMGP buyout program. The pre-disaster value of the property (the amount offered in the buyout), should it be insufficient to purchase a comparable home, might preclude homeowners, particularly those who carry mortgage debt, from choosing to relocate. Particularly, when coupled with their relatively lower economic status, homeowners with bad credit having paid off a mortgage may be precluded from relocation as they cannot secure a new mortgage when choosing to relocate.

Overall, this study expands the discussion on equitable hazard mitigation by introducing community-level sociodemographic and housing characteristics into empirical literature. In addition to prior literature examining the property level attributes through surveys and interviews, social and physical characteristics of communities are important in homeowners’ mobility decisions as its tendency eventually shapes collective and equitable community resilience [73,74]. Moreover, this study introduces factors that are little explored in the existing literature (i.e., home value, low-value property, inundation depth, mortgage status) and adds to the new empirical findings of the long-term mobility decisions of HMGP recipients.

4.3. Socioeconomic Disparities among HMGP Recipients

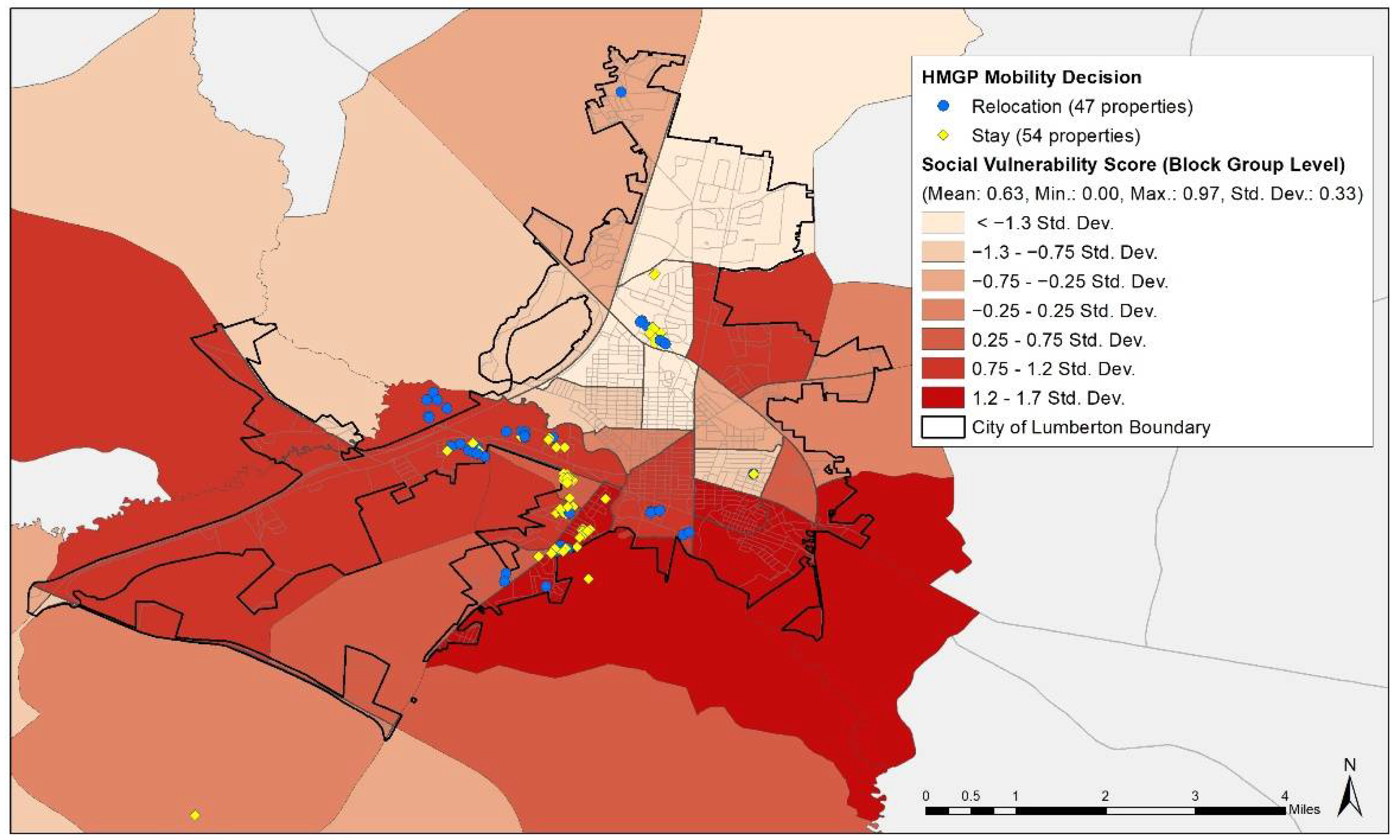

As discussed in the previous section, social vulnerability relates to a fundamental underlying phenomenon in disasters: Low-income and minority households are more likely to be sited in neighborhoods with high physical exposure to disasters. Coupled with the reduced ability of such households to mitigate and recover from disasters (i.e., less financial capital and political clout), disasters have a much greater effect on this particular group, who not only face greater exposure to disasters, but also a prolonged recovery period. Figure 3 shows the relationship between social vulnerability and homeowners’ mobility decisions; HMGP recipients who chose to remain are largely located in the southern and western portions of the city, the most socially vulnerable neighborhoods in Lumberton.

The authors also conducted a t-test to statistically identify the differences in social vulnerability between the two HMGP groups: Those who chose to relocate and those who chose to remain. Table 4 depicts the results of the t-test—among the 101 HMGP recipients, there was a significant difference between the social vulnerability score for recipients who chose to relocate (M = 0.563, SD = 0.049) versus those who opted to remain (M = 0.683, SD = 0.044), with a t-value of 1.812 and p-value of 0.073. The authors find that the social vulnerability score for the homeowners who chose to remain is statistically higher than the score for homeowners who chose to relocate.

Although both groups receive disaster assistance, socially vulnerable homeowners are likely to have fewer options to relocate due to financial constraints and less information on available resources, despite higher flood risks. Our statistical results in Table 3 depict that HMGP recipients with heavily inundated properties are more likely to relocate. Perhaps the governmental agencies may be more aggressive in acquiring these properties than others with less flood history to reduce future flood damages [34]. Many studies have demonstrated that socially disadvantaged populations are likely to live in neighborhoods with higher physical vulnerability. That is, they are located in floodplains and thereby have a higher chance of being exposed to floods [75,76,77]. Nevertheless, Table 4 shows an association between social vulnerability and the mobility decisions of HMGP recipients. In other words, despite higher flood risks, socially vulnerable residents may have a reduced chance of relocating out of floodplains. Multiple reasons may explain this phenomenon. The pre-disaster assessed value of properties in more socially vulnerable neighborhoods is likely depressed before the disaster even strikes; as such, even homeowners who receive disaster assistance may not be able to find an affordable home to which to relocate.

Moreover, social capital, which entails social embeddedness, networks, and resources, could be central to the decision-making process of disaster-affected homeowners to either relocate or rebuild [73,78,79,80]. In this regard, social capital often provides resources that offset the vulnerabilities introduced by demographic characteristics (i.e., age, race, etc.). Some households even highly value social capital, prioritizing it over reducing their physical vulnerability, and decide to remain in their homes. Given that no investment in physical infrastructure can completely reduce physical vulnerability, decision-makers should carefully consider the tradeoffs between physical and social capital. Moreover, social capital should be spotlighted in a lens of community-level disparities in resilience and relocation decisions. That is, an alternative approach to disaster mitigation should be based on reinforcing social infrastructure, such as social capital, which eventually strengthens community resilience.

Additionally, Mobley, et al. [81] assessed and compared the economic benefits of two different hazard mitigation strategies—property acquisition and elevation—to suggest a framework by which policymakers and homeowners consider the most economically viable mitigation practices. Incorporating homeowner and neighborhood characteristics into this framework will contribute to the growing need for identifying better implementation of mitigation measures for communities. Given that HMGP is a voluntary process in which homeowners choose to either relocate or rebuild, providing them an optimal option to make evidence-based decisions should be encouraged to enhance community resilience.

5. Conclusions and Future Outlook

The increasing incidence of disasters along the coasts, combined with the growing proportion of the population exposed to potential disasters, exacerbates the threat of property damage and population displacement. Rising levels of property damage will increase the total cost of damage, the share of homeowners who seek disaster assistance, and the amount of assistance requested. This necessitates a deeper understanding of the decision-making process of homeowners who receive disaster assistance to rebuild or relocate. This paper contributes to the literature by exploring the relationship between physical and social vulnerability and the long-term mobility decisions of homeowners who receive disaster assistance (i.e., property acquisition, elevation, or reconstruction). There is a paucity of literature that positions disaster assistance for property elevation and reconstruction in the context of physical and social vulnerability.

The authors use the logit and probit regressions to determine the differences in the characteristics of individual properties and neighborhood sociodemographic and housing characteristics by the homeowners’ mobility decision (i.e., whether to remain or relocate). The authors find that homeowners with lower-value properties are less likely to relocate and those who are subjected to higher flood and inundation risks are more likely to relocate. In addition, homeowners in neighborhoods of higher social vulnerability—those with a higher minority composition and mortgaged properties—are more likely to rebuild their disaster-affected homes. Our results are consistent with the literature, which finds that homeowners of lower socioeconomic status face greater financial constraints to relocation and are therefore more likely to remain in their disaster-affected properties.

The authors acknowledge that there may be other factors involved in residents’ mobility decisions to rebuild that were not captured in this study. For instance, household-level attributes, such as emotional ties to one’s home or offers proposed by the municipality for property acquisition perceived by the homeowner to be low, might motivate homeowners to rebuild. The authors also acknowledge that the multiple layers and dynamics in the decision-making process may not be captured in our findings. Residential mobility decisions regarding HMGP assistance and its outcomes are made through the following process: (1) The homeowner’s decision whether to apply for HMGP assistance; (2) both the homeowner’s and the municipality’s combined decision as to which type of HMGP assistance to apply for; and (3) the federal agency’s selection of HMGP recipients. Due to our limitation in data collection regarding HMGP applications, these dynamic layers of the decision-making process were simplified. This should be further investigated in future research.

The findings of this study may not be generalizable given the small sample size. Solely including the HMGP recipients in the sample and excluding households who have applied but not received or who did not apply for the program may increase the potential for sample selection bias. Based on findings from the literature, which suggest that disaster assistance is unfavorable to socially vulnerable populations (i.e., minorities, low-income households, the elderly, renters, female-headed households, etc.) [19,52,55,56], the authors assume the proportion of socially vulnerable homeowners to be higher than the proportion homeowners in affluent neighborhoods among households underfunded or ineligible for the HMGP assistance in Lumberton. Hence, the authors expect estimated coefficients in the models would be accentuated if the data on these households are included in the sample.

However, residential mobility decisions regarding HMGP assistance and its outcomes in small urban areas result from the decision-making process between homeowners and the municipality. In this respect, the authors argue that this research contributes to the literature as a case study by addressing the role of the municipality during the decision-making process in small-town hazard mitigation and suggesting how to guide and assist homeowners for equitable distribution of hazard mitigation outcomes. Rare cases have investigated the HMGP assistance outcomes from the viewpoint of both the homeowner’s and the municipality’s combined decision on which type of HMGP assistance to apply for. Choosing a mitigation action is initially a voluntary process for all participants. However, in small urban areas like Lumberton, individuals generally interact with city officials in the process of applying for HMGP, and, as such, they sometimes may be encouraged to pursue a particular mitigation action based on the city’s long-term recovery or hazard mitigation plan. In this regard, residential mobility decisions are not solely voluntary but, rather, can be seen as the outcomes of communication between individuals and the local government.

By considering the entire population of HMGP recipients in Lumberton, NC, USA, this study allows us to deepen our understanding of the mobility decisions of such recipients. Thus, the roles of local officials in the process of HMGP application and implementation should include consulting with and guiding HMGP applicants to choose the option that best optimizes their outcomes.

In Lumberton, city officials have facilitated resilient housing development strategies by including a post-disaster housing relocation plan. The city’s recovery plan entails a community vision in which the entire community repairs physical infrastructure and conducts relevant initiatives to become a resilient city. For example, concerning the loss in tax revenues from those who relocate through HMGP, the recent Lumberton Recovery Plan suggested abandoned properties outside the floodplain be reconstructed into affordable housing units by 2020 [82]. For equitable mitigation outcomes, such municipal efforts could prioritize socially and economically vulnerable populations with fewer viable relocation options.

Although our findings have important implications, there are limitations to the study. First, the small sample size poses a significant limitation to our research. Even though the authors used the total population that received HMGP assistance in Lumberton, the small population size may decrease the power of the study’s results. It may cause the overestimation of the odds ratios and sampling bias in the regressions. With only 101 observations, our results are not generalizable to the population that makes mobility decisions after disasters. However, the uniqueness of the Lumberton case (due to its high physical and social vulnerability and the incidence of two hurricanes in less than two years) sheds light on how the allocation and prioritization of federal funding assistance in small towns should be, particularly in areas that lack bureaucratic and financial resources. Previous studies that illustrate the property attributes and sociodemographic characteristics of households that seek buyouts also use small samples [6,25,41]. By illustrating the allocation of federally funded disaster assistance in a small town, this exploratory study offers a unique case study. Given that the HMGP is a mitigation tool that provides homeowners the opportunity to relocate or rebuild, investigating how those physical and sociodemographic characteristics of homeowners may result in different outcomes offers a thought-provoking question to both scholars and practitioners.

Another limitation is the availability of household-level data on HMGP recipients. Although the literature demonstrates that property- and household-level factors affect homeowners’ post-disaster mobility decisions, this research was not able to control for individual-level information due to limited access to data, increasing the potential for omitted variables bias or selection bias. Additionally, as a result of data limitations, this study cannot capture the characteristics of all 400 applicants to the program, which would have provided a greater understanding of potential differences in the housing and demographic characteristics of HMGP applicants and recipients. Further studies (i.e., individual-level surveys that capture homeowners’ perception of the decision to rebuild or relocate, comparisons of property and demographic characteristics between HMGP applicants and recipients) should be examined to supplement the current data limitations.

Our overall findings reveal that more socially vulnerable homeowners tend to rebuild (i.e., remain in) their disaster-affected properties. The authors recommend that cities prioritize the mitigation of properties of homeowners of lower socioeconomic status to reduce socioeconomic disparities in disaster recovery. Furthermore, homeowners of lower socioeconomic status should be equipped with the resources necessary to ensure diverse mobility choices are feasible. Based on the small observation count and uniqueness of the geographic setting, future research should continue to explore the mobility decisions of recipients of HMGP assistance, particularly with respect to property elevation and reconstruction, whose disaster-affected homes are situated in areas of higher physical and social vulnerability.

Author Contributions

Conceptualization, K.S., C.L. and S.V.Z.; methodology, K.S. and C.L.; software, K.S.; validation, K.S., C.L. and S.V.Z.; formal analysis, K.S.; investigation, K.S., C.L. and S.V.Z.; data curation, K.S.; writing—original draft preparation, K.S. and C.L.; writing—review and editing, K.S., C.L. and S.V.Z.; visualization, K.S.; supervision, K.S.; project administration, K.S. and C.L.; funding acquisition, K.S. and C.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Natural Hazards Center Quick Response Research Grant Program, grant number NSF Award 1635593, and additional financial support by the Center for Risk-Based Community Resilience Planning at Colorado State University through a cooperative agreement with the U.S. National Institute of Standards and Technology, grant number 70NANB15H044.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

The authors would like to thank the editor and the reviewers for their helpful comments. Special thanks to Brian Nolley, Community Development Administrator in the City of Lumberton, for sharing the Hazard Mitigation Grant Program (HMGP) data.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Figure A1.

The area under receiver operating characteristics (ROC) curves for logit and probit models.

Figure A1.

The area under receiver operating characteristics (ROC) curves for logit and probit models.

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Social vulnerability indicators.

| Category | Construct | Measurement | Rationale |

|---|---|---|---|

| Socio-Economic Status | Below Poverty | The percent of the population below the poverty level | Lower savings and insurance, home repair difficulties, negative physical and mental health outcomes, greater displacement |

| Unemployed | The percent of the civilian (age 16+) population that is unemployed | Difficulty returning home after disaster displacement, limited resources to apply for disaster assistance | |

| Less Education | The percent of the population (age 25+) with no high school diploma | Increased difficulties with insurance and assistance claims | |

| Service Sector Employment | The percent of the population employed in the service sector | Decrease in the need for low-paid service sector jobs following disasters; less likely to carry flood insurance and greater difficulty in the application process | |

| Household Composition/Disability | Elderly | The percent of the population aged 65 and older | Negative health outcomes, lower ability to navigate insurance claims, increased social isolation |

| Children | The percent of the population aged 17 and younger | Negative psychological outcomes, health impacts | |

| Disability | The percent of the civilian noninstitutionalized population with a disability | Social isolation | |

| Female-headed Households | The percent of female-headed households | Less emotional support, additional care responsibilities | |

| Single-parent Households | The percent of single parent households with children under 18 | Additional care responsibilities; less likely to carry flood insurance and apply for assistance | |

| Minority Status/Language | African American | The percent of the non-Hispanic African American population | Higher death and injury rates; negative post-flood health outcomes; less likely to carry flood insurance and application; lower trust in authority for post-flood assistance; higher employment loss, lower social capital, lack of trust in government |

| Native American | The percent of the non-Hispanic Native American population | Lower assistance-to-damage ratios; less likely to carry flood insurance and application; less trust in authority/government; discrimination | |

| Hispanic | The percent of the Hispanic population | Lower assistance-to-damage ratios; likely to carry flood insurance and application; language barrier; discrimination | |

| Language | The percent of the population (age 5+) that speaks English “less than well” | Limited access to information and assistance | |

| Housing Type and Status | Mobile-Homes | The percent of mobile homes | Lack of control over home repairs, less insurance, mitigation policies favor homeowners |

| Renter | The percent of renter-occupied housing units | Complicated decision-making process with respect to assistance; fewer resources and less control; dependence on property owners for mitigation | |

| Vacancy | The percent of vacant housing units | Lack of maintenance and less control |

Notes: The Cronbach’s alpha (scale reliability coefficient) computed in STATA revealed good internal reliability for the 16 measures (α = 0.788), suggesting Social Vulnerability Indicators have relatively high internal consistency.

References

- Fritz, C.E. Disaster, contemporary social problems. Harcourt N. Y. 1961, 65, 1–694. [Google Scholar]

- The Economist. Weather-Related Disasters are Increasing. 2017. Available online: https://www.economist.com/graphic-detail/2017/08/29/weather-related-disasters-are-increasing (accessed on 1 December 2019).

- III. Facts + Statistics: U.S. Catastrophes; Insurance Information Institute: New York, NY, USA, 2019. [Google Scholar]

- CoreLogic. 7.3 Million Homes at Risk of 2019 Hurricane Storm Surge Damage with $1.8 Trillion in Potential Reconstruction Costs, According to CoreLogic Report. Available online: https://www.corelogic.com/news/7.3-million-homes-at-risk-of-2019-hurricane-storm-surge-damage-with-1.8-trillion-in-potential-reconstruction-costs.aspx (accessed on 15 November 2019).

- Robinson, C.S.; Davidson, R.A.; Trainor, J.E.; Kruse, J.L.; Nozick, L.K. Homeowner acceptance of voluntary property acquisition offers. Int. J. Disaster Risk Reduct. 2018, 31, 234–242. [Google Scholar] [CrossRef]

- Kirschenbaum, A. Residential Ambiguity and Relocation Decisions: Population and Areas at Risk. Int. J. Mass Emergencies Disasters 1996, 14, 79–96. [Google Scholar]

- Fraser, J.; DeVries, D.; Young, H. Mitigating Repetitive Loss Properties; The Center for Urban and Regional Studies: Chapel Hill, NC, USA, 2006. [Google Scholar]

- Kick, E.L.; Fraser, J.C.; Fulkerson, G.M.; McKinney, L.A.; De Vries, D.H. Repetitive flood victims and acceptance of FEMA mitigation offers: An analysis with community–system policy implications. Disasters 2011, 35, 510–539. [Google Scholar] [CrossRef] [PubMed]

- Bukvic, A.; Smith, A.; Zhang, A. Evaluating drivers of coastal relocation in Hurricane Sandy affected communities. Int. J. Disaster Risk Reduct. 2015, 13, 215–228. [Google Scholar] [CrossRef]

- U.S. Government Accountability Office. Hazard Mitigation: Proposed Changes to FEMA’s Multihazard Mitigation Programs Present Challenges. Available online: https://www.gao.gov/products/gao-02-1035 (accessed on 30 September 2002).

- Federal Emergency Management Agency (FEMA). The Hazard Mitigation Assistance Grant Programs. Available online: https://www.fema.gov/grants/mitigation/hazard-mitigation-assistance-guidance (accessed on 21 November 2019).

- U.S. Department of Homeland Security, Federal Emergency Management Agency (FEMA). The 1993 Great Midwest Flood: Voices 10 Years Later; U.S. Department of Homeland Security Federal Emergency Management Agency: Washington, DC, USA, 2003.

- FEMA. FEMA HMGP Property Acquisitions. Available online: https://www.fema.gov/media-library/assets/documents/85455 (accessed on 21 November 2019).

- NCEM. State of Nrth Carolina CDBG-DR Action Plan: CDBG-DR Grants under Public Law 114-223/254. Available online: https://files.nc.gov/rebuildnc/documents/files/nc_cdbg_dr_non-substantial_amendment_2.pdf (accessed on 9 April 2018).

- Federal Emergency Management Agency (FEMA). Hazard Mitigation Grants. Available online: https://www.fema.gov/grants/mitigation (accessed on 21 November 2019).

- Keyssar, N.; Brown, A. Devastated by One Hurricane, and Then Another, A Community Confronts the Company That Refused to Block the Floodwaters. The Intercept 2019. Available online: https://theintercept.com/2019/06/02/lumberton-north-carolina-hurricane-matthew-florence-flooding-csx (accessed on 24 March 2020).

- CRC. Hurricane Matthew Recovery—Lumberton. Available online: https://coastalresiliencecenter.unc.edu/crc-projects/hurricane-matthew-recovery/hurricane-matthew-recovery-engagement/hurricane-matthew-recovery-lumberton/ (accessed on 24 March 2020).

- Blaikie, P.; Cannon, T.; Davis, I.; Wisner, B. At Risk: Natural Hazards, People’s Vulnerability and Disasters; Routledge: London, UK; New York, NY, USA, 1994. [Google Scholar]

- Peacock, W.G.; Van Zandt, S.; Zhang, Y.; Highfield, W.E. Inequities in long-term housing recovery after disasters. J. Am. Plan. Assoc. 2014, 80, 356–371. [Google Scholar] [CrossRef]

- Masterson, J.; Peacock, W.; Van Zandt, S.; Grover, H.; Schwarz, L.; Cooper, J., Jr. Planning for Community Resilience: A Handbook for Reducing Vulnerability to Disasters; Island Press: Washington, DC, USA, 2014. [Google Scholar]

- Schmidlin, T.W. Risk factors and social vulnerability. In Proceedings of the International Forum on Tornado Disaster Risk Reduction in Bangladesh, Dhaka, Bangladesh, 13–14 December 2009; Wind Engineering Research Center, Tokyo Polytechnic University: Tokyo, Japan, 2009. [Google Scholar]

- De Vries, D.; Fraser, J. Citizenship rights and voluntary decision making in post-disaster US. Int. J. Mass Emerg. Disasters. 2012, 30, 1–33. [Google Scholar]

- Fraser, J.C.; Doyle, M.W.; Young, H. Creating effective flood mitigation policies. Eos. Trans. Am. Geophys. Union 2006, 87, 265–270. [Google Scholar] [CrossRef]

- Handmer, J.; Ord, K. Flood warning and response. In Flood warning in Australia; CRES, Australian National University: Canberra, Austrlian, 1986; pp. 235–257. [Google Scholar]

- Zavar, E.; Hagelman, R.; Rugeley, W. Site, Situation, and Property Owner Decision-making after the 2002 Guadalupe River Flood. In Proceedings of the Applied Geography Conferences, Minneapolis, MN, USA, 10–12 October 2012; pp. 249–257. [Google Scholar]

- Reeser, C.M. Homeowner Willingness to Pay for a Pre-Flood Buyout Agreement; University of Illinois at Urbana-Champaign: Urbana, IL, USA, 2016. [Google Scholar]

- Bukvic, A.; Owen, G. Attitudes towards relocation following Hurricane Sandy: Should we stay or should we go? Disasters 2017, 41, 101–123. [Google Scholar] [CrossRef]

- Bubeck, P.; Botzen, W.J.W.; Aerts, J.C. A review of risk perceptions and other factors that influence flood mitigation behavior. Risk Anal. An. Int. J. 2012, 32, 1481–1495. [Google Scholar] [CrossRef] [Green Version]

- Lindell, M.K.; Hwang, S.N. Households’ perceived personal risk and responses in a multihazard environment. Risk Anal. An. Int. J. 2008, 28, 539–556. [Google Scholar] [CrossRef] [PubMed]

- Ge, Y.; Peacock, W.G.; Lindell, M.K. Florida households’ expected responses to hurricane hazard mitigation incentives. Risk Anal. An. Int. J. 2011, 31, 1676–1691. [Google Scholar] [CrossRef]

- Binder, S.B.; Greer, A. The devil is in the details: Linking home buyout policy, practice, and experience after hurricane Sandy. Politics Gov. 2016, 4, 97–106. [Google Scholar] [CrossRef]

- Smith, G.P. Applying hurricane recovery lessons in the United States to climate change adaptation: Hurricanes Fran and Floyd in North Carolina, USA. In Adapting to Climate Change; Springer: Dordrecht, Netherlands, 2014; pp. 193–229. [Google Scholar]

- Lewis, D.A. The relocation of development from coastal hazards through publicly funded acquisition programs: Examples and lessons from the Gulf Coast. Sea Grant L. Pol’y J. 2012, 5, 98. [Google Scholar]

- De Vries, D.H. Temporal vulnerability and the post-disaster ‘Window of Opportunity to Woo:’a case study of an African-American floodplain neighborhood after Hurricane Floyd in North Carolina. Hum. Ecol. 2017, 45, 437–448. [Google Scholar] [CrossRef] [Green Version]

- Viscusi, W.K. Valuing risks of death from terrorism and natural disasters. J. Risk Uncertain. 2009, 38, 191–213. [Google Scholar] [CrossRef]

- Cole, W.D.; Shore, M.E. Sea Level Rise: Technical Guidance for Dorchester County; Maryland Eastern Shore Resource Conservation & Development Council: Annapolis, MD, USA, 2008. [Google Scholar]

- Burningham, K.; Fielding, J.; Thrush, D. ‘It’ll never happen to me’: Understanding public awareness of local flood risk. Disasters 2008, 32, 216–238. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kunreuther, H. Disaster mitigation and insurance: Learning from Katrina. Ann. Am. Acad. Political Soc. Sci. 2006, 604, 208–227. [Google Scholar] [CrossRef] [Green Version]

- Landry, C.E.; Bin, O.; Hindsley, P.; Whitehead, J.C.; Wilson, K. Going home: Evacuation-migration decisions of Hurricane Katrina survivors. South. Econ. J. 2007, 326–343. [Google Scholar] [CrossRef]

- Bukvic, A. Integrated framework for the Relocation Potential Assessment of Coastal Communities (RPACC): Application to Hurricane Sandy-affected areas. Environ. Syst. Decis. 2015, 35, 264–278. [Google Scholar] [CrossRef]

- Loughran, K.; Elliott, J.R. Residential buyouts as environmental mobility: Examining where homeowners move to illuminate social inequities in climate adaptation. Popul. Environ. 2019, 41, 52–70. [Google Scholar] [CrossRef]

- Loughran, K.; Elliott, J.R.; Kennedy, S.W. Urban ecology in the time of climate change: Houston, flooding, and the case of federal buyouts. Soc. Curr. 2019, 6, 121–140. [Google Scholar] [CrossRef]

- Elliott, J.R.; Brown, P.L.; Loughran, K. Racial inequities in the federal buyout of flood-prone homes: A nationwide assessment of environmental adaptation. Socius 2020, 6, 2378023120905439. [Google Scholar] [CrossRef] [Green Version]

- Bird, D.; King, D.; Haynes, K.; Box, P.; Okada, T.; Nairn, K. Impact of the 2010-11 Floods and the Factors that Inhibit and Enable Household Adaptation Strategies; National Climate Change Adaptation Research Facility Gold Coast: Southport, Australia, 2013. [Google Scholar]

- King, D.; Bird, D.; Haynes, K.; Boon, H.; Cottrell, A.; Millar, J.; Okada, T.; Box, P.; Keogh, D.; Thomas, M. Voluntary relocation as an adaptation strategy to extreme weather events. Int. J. Disaster Risk Reduct. 2014, 8, 83–90. [Google Scholar] [CrossRef]

- Sanders, S.; Bowie, S.L.; Bowie, Y.D. Chapter 2 lessons learned on forced relocation of older adults: The impact of Hurricane Andrew on health, mental health, and social support of public housing residents. J. Gerontol. Soc. Work. 2004, 40, 23–35. [Google Scholar] [CrossRef]

- Riad, J.K.; Norris, F.H. The influence of relocation on the environmental, social, and psychological stress experienced by disaster victims. Environ. Behav. 1996, 28, 163–182. [Google Scholar] [CrossRef]

- Binder, S.B.; Baker, C.K.; Barile, J.P. Rebuild or relocate? Resilience and postdisaster decision-making after Hurricane Sandy. Am. J. Community Psychol. 2015, 56, 180–196. [Google Scholar] [CrossRef] [PubMed]

- Mach, K.J.; Kraan, C.M.; Hino, M.; Siders, A.; Johnston, E.M.; Field, C.B. Managed retreat through voluntary buyouts of flood-prone properties. Sci. Adv. 2019, 5, eaax8995. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- DeYoung, S.; Wachtendorf, T.; Davidson, R.; Xu, K.; Nozick, L.; Farmer, A.; Zelewicz, L. A mixed method study of hurricane evacuation: Demographic predictors for stated compliance to voluntary and mandatory orders. Environ. Hazards 2016, 15, 95–112. [Google Scholar] [CrossRef]

- Li, W.; Airriess, C.A.; Chen, A.C.-C.; Leong, K.J.; Keith, V. Katrina and migration: Evacuation and return by African Americans and Vietnamese Americans in an eastern New Orleans suburb. Prof. Geogr. 2010, 62, 103–118. [Google Scholar] [CrossRef]

- Muñoz, C.; Tate, E. Unequal recovery? Federal resource distribution after a Midwest flood disaster. Int. J. Environ. Res. Public Health 2016, 13, 507. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Elliott, J.R.; Pais, J. Race, class, and Hurricane Katrina: Social differences in human responses to disaster. Soc. Sci. Res. 2006, 35, 295–321. [Google Scholar] [CrossRef]

- Zhang, Y.; Peacock, W.G. Planning for housing recovery? Lessons learned from Hurricane Andrew. J. Am. Plan. Assoc. 2009, 76, 5–24. [Google Scholar] [CrossRef]

- Finch, C.; Emrich, C.T.; Cutter, S.L. Disaster disparities and differential recovery in New Orleans. Popul. Environ. 2010, 31, 179–202. [Google Scholar] [CrossRef]

- Cutter, S.L.; Emrich, C.T.; Mitchell, J.T.; Piegorsch, W.W.; Smith, M.M.; Weber, L. Hurricane Katrina and the Forgotten Coast of Mississippi; Cambridge University Press: Cambridge, UK, 2014. [Google Scholar]

- De Vries, D. Internal Migration through Buyouts after Natural Disasters: Hurricane Floyd in Eastern North Carolina (1999). In Proceedings of the Population Association of America 2007 Annual Meeting, New York, NY, USA, 29–31 March 2007. [Google Scholar]

- Seong, K.; Losey, C. To Remain or Relocate? Mobility Decisions of Homeowners Exposed to Recurrent Hurricanes; Natural Hazards Center Quick Response Grant Report Series, 303; Natural Hazards Center; University of Colorado Boulder: Boulder, CO, USA, 2020; Available online: https://hazards.colorado.edu/quick-response-report/to-remain-or-relocate-mobility-decisions-of-homeowners-exposed-to-recurrent-hurricanes (accessed on 20 November 2020).

- van de Lindt, J.W.; Peacock, W.G.; Mitrani-Reiser, J.; Rosenheim, N.; Deniz, D.; Dillard, M.; Tomiczek, T.; Koliou, M.; Graettinger, A.; Crawford, P.S. Community Resilience-Focused Technical Investigation of the 2016 Lumberton, North Carolina, Flood: An Interdisciplinary Approach. Nat. Hazards Rev. 2020, 21, 04020029. [Google Scholar] [CrossRef]

- Manson, S.; Schroeder, J.; Van Riper, D.; Ruggles, S. IPUMS National Historical Geographic Information System: Version 14.0; The University of Minnesota: Minneapolis, MN, USA, 2019. [Google Scholar] [CrossRef]

- Bin, O.; Kruse, J.B. Real estate market response to coastal flood hazards. Nat. Hazards Rev. 2006, 7, 137–144. [Google Scholar] [CrossRef]

- De Silva, D.G.; Kruse, J.B.; Wang, Y. Catastrophe-induced destruction and reconstruction. Nat. Hazards Rev. 2006, 7, 19–25. [Google Scholar] [CrossRef]

- Nelson, K.; Molloy, M. Differential disadvantages in the distribution of federal aid across three decades of voluntary buyouts in the United States. Glob. Environ. Chang. 2021, 68, 102278. [Google Scholar] [CrossRef]

- CDC. Social Vulnerability Index 2018 Database; Agency for Toxic Substances and Disease Registry: Atlanta, GA, USA, 2018. [Google Scholar]

- Ghareib, A.H. Evaluation of logit and probit models in mode-choice situation. J. Transp. Eng. 1996, 122, 282–290. [Google Scholar] [CrossRef]

- Golob, T.F.; Recker, W.W. Mode choice prediction using attitudinal data: A procedure and some results. Transportation 1977, 6, 265–286. [Google Scholar] [CrossRef]

- Zou, K.H.; O’Malley, A.J.; Mauri, L. Receiver-operating characteristic analysis for evaluating diagnostic tests and predictive models. Circulation 2007, 115, 654–657. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Wachinger, G.; Renn, O.; Begg, C.; Kuhlicke, C. The risk perception paradox—implications for governance and communication of natural hazards. Risk Anal. 2013, 33, 1049–1065. [Google Scholar] [CrossRef]

- Keller, C.; Siegrist, M.; Gutscher, H. The role of the affect and availability heuristics in risk communication. Risk Anal. 2006, 26, 631–639. [Google Scholar] [CrossRef] [PubMed]

- Paton, D.; Smith, L.; Johnston, D.M. Volcanic hazards: Risk perception and preparedness. N. Z. J. Psychol. 2000, 29, 86. [Google Scholar]

- Binder, S.B.; Barile, J.P.; Baker, C.K.; Kulp, B. Home buyouts and household recovery: Neighborhood differences three years after Hurricane Sandy. Environ. Hazards 2019, 18, 127–145. [Google Scholar] [CrossRef]

- McGhee, D. Were the Post-Sandy Staten Island Buyouts Successful in Reducing National Vulnerability; Duke University: Durham, NC, USA, 2017. [Google Scholar]

- Norris, F.H.; Stevens, S.P.; Pfefferbaum, B.; Wyche, K.F.; Pfefferbaum, R.L. Community resilience as a metaphor, theory, set of capacities, and strategy for disaster readiness. Am. J. Community Psychol. 2008, 41, 127–150. [Google Scholar] [CrossRef]

- Tobin, G.A. Sustainability and community resilience: The holy grail of hazards planning? Glob. Environ. Chang. Part B Environ. Hazards 1999, 1, 13–25. [Google Scholar] [CrossRef]

- Alderman, K.; Turner, L.R.; Tong, S. Floods and human health: A systematic review. Environ. Int. 2012, 47, 37–47. [Google Scholar] [CrossRef] [Green Version]

- Rufat, S.; Tate, E.; Burton, C.G.; Maroof, A.S. Social vulnerability to floods: Review of case studies and implications for measurement. Int. J. Disaster Risk Reduct. 2015, 14, 470–486. [Google Scholar] [CrossRef] [Green Version]

- Chomsri, J.; Sherer, P. Social vulnerability and suffering of flood-affected people: Case study of 2011 mega flood in Thailand. Kasetsart J. Soc. Sci. 2013, 34, 491–499. [Google Scholar]

- Adeola, F.O.; Picou, J.S. Social capital and the mental health impacts of Hurricane Katrina: Assessing long-term patterns of psychosocial distress. Int. J. Mass Emergencies Disasters 2014, 32, 121–156. [Google Scholar]

- Aldrich, D.P.; Meyer, M.A. Social capital and community resilience. Am. Behav. Sci. 2015, 59, 254–269. [Google Scholar] [CrossRef]

- Cong, Z.; Nejat, A.; Liang, D.; Pei, Y.; Javid, R.J. Individual relocation decisions after tornadoes: A multi-level analysis. Disasters 2018, 42, 233–250. [Google Scholar] [CrossRef] [PubMed]

- Mobley, W.; Atoba, K.O.; Highfield, W.E. Uncertainty in Flood Mitigation Practices: Assessing the Economic Benefits of Property Acquisition and Elevation in Flood-Prone Communities. Sustainability 2020, 12, 2098. [Google Scholar] [CrossRef] [Green Version]

- HMDRRI. 2018 Lumberton Recovery Plan; Hurricane Matthew Disaster Recovery and Resilience Initiative: Lumberton, NC, USA, 2018. [Google Scholar]

Figure 1.

Distribution of HMGP recipients in Lumberton, North Carolina, USA, by project type (Source: Data obtained from the city of Lumberton, North Carolina; NC OneMap; OpenFEMA).

Figure 1.

Distribution of HMGP recipients in Lumberton, North Carolina, USA, by project type (Source: Data obtained from the city of Lumberton, North Carolina; NC OneMap; OpenFEMA).

Figure 2.

Predictive margins for the probability of relocation over inundation depth following Hurricane Matthew based on (a) the ratio of the property value to the median property value of Lumberton and (b) the depreciation in property value.

Figure 2.

Predictive margins for the probability of relocation over inundation depth following Hurricane Matthew based on (a) the ratio of the property value to the median property value of Lumberton and (b) the depreciation in property value.

Figure 3.

Social vulnerability score and location of HMGP recipients’ properties.

Table 1.

Socioeconomic and housing characteristics of North Carolina, Robeson County, and Lumberton (Source: American Community Survey, 2016 5-Year Estimates).

Table 1.