Ecological Footprint as an Indicator of Corporate Environmental Performance—Empirical Evidence from Hungarian SMEs

Abstract

:1. Introduction

2. Theoretical Framework

2.1. The Concept of Ecological Footprint

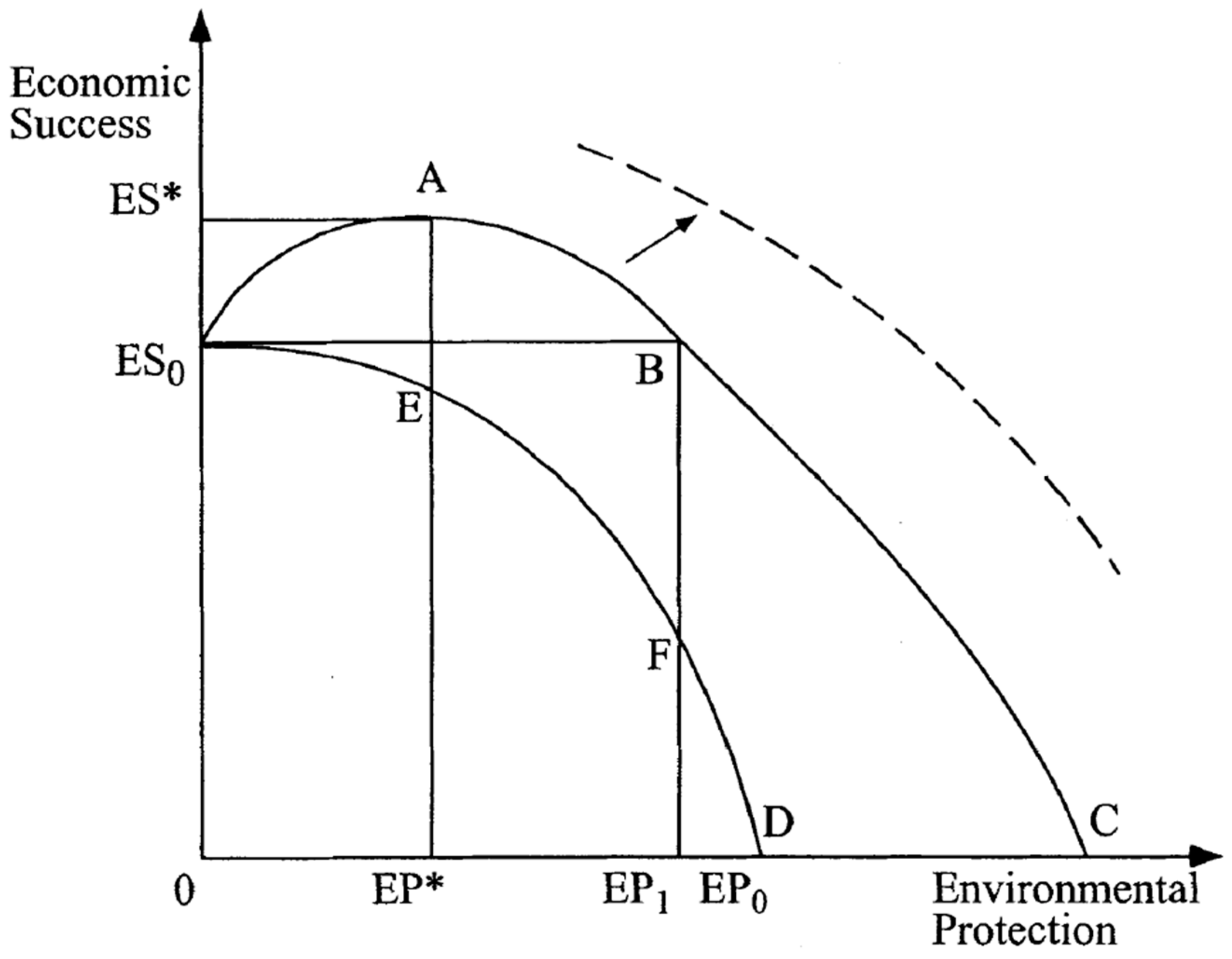

2.2. Ecological Footprint as a Possible Corporate Environmental Performance Indicator

- (1)

- is a well-known and easy-to-understand measure of environmental sustainability;

- (2)

- is a quantitative indicator and is measured on a ratio scale, therefore providing adequate data to create key performance indicators (KPIs);

- (3)

- is a reliable indicator because calculations are based on scientifically proven data, such as carbon emission factors of electricity grid or fossil fuels, local food consumption, etc.; and

- (4)

- calculations can be standardized through online calculators, therefore providing a low-cost solution for small- and medium-sized companies.

2.3. Impact of Environmental Performance on Financial Performance

2.4. Sectoral Average of EF

3. Methodology

3.1. Calculation of EF

- (1)

- usage of different fuel types (i.e., petrol, gasoline, LPG), if accurate analytical records are available;

- (2)

- mileage of vehicles of different fuel types (kilometers a year) and average fuel consumption (liters per 100 km);

- (3)

- mileage of different category and fuel type of cars and small vans;

- (4)

- number and average distance of trips in case of taxi and air travel; and

- (5)

- an average of daily distance in case of public transport (underground, tram, bus).

3.2. The Sample

- (1)

- It is a small- or medium-sized company, defined by the Commission of the European Communities [75], namely has less than 250 employees and its turnover is less than €50 million or its balance sheet total is less than €43 million.

- (2)

- Energy consumption of corporate activities can be separated from other activities, e.g., private home of managers and/or owners.

- (3)

- Managers and/or owners are willing to participate in the survey.

- (1)

- The operation of SMEs may differ. For example, the EF will be greater if a retail store transports goods with its own van and/or provides home delivery for costumers, or if an engineering office must make trips for its field works.

- (2)

- Manager’s attitudes towards sustainability may vary significantly. Some managers attempt to engage in environmentally friendly projects (e.g., energy efficient equipment, solar panels, etc.), while others do not.

- (3)

- The organization culture may also be different.

4. Results

4.1. Construction

4.2. White-Collar Jobs

4.3. Production

4.4. Retail and Wholesale Trade

4.5. Transportation

5. Conclusions and Discussions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Lewis, S.L.; Maslin, M.A. Defining the Anthropocene. Nature 2015, 519, 171–180. [Google Scholar] [CrossRef] [PubMed]

- Global Footprint Network Earth Overshoot Day. 2020. Available online: https://www.overshootday.org/ (accessed on 17 November 2020).

- Anciaux, A. “On Holidays, I Forget Everything … Even My Ecological Footprint”: Sustainable Tourism through Daily Practices or Compartmentalisation as a Keyword? Sustainability 2019, 11, 4731. [Google Scholar] [CrossRef] [Green Version]

- Wackernagel, M.; Pearce, F. Day of Reckoning. New Sci. 2018, 239, 20–21. [Google Scholar] [CrossRef]

- European Commission. Europe 2020—Overview. Available online: https://ec.europa.eu/eurostat/web/europe-2020-indicators (accessed on 20 November 2020).

- Eurostat. Statistics on Small and Medium-Sized Enterprises—Statistics Explained. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php/Statistics_on_small_and_medium-sized_enterprises#General_overview (accessed on 26 November 2020).

- Baah, C.; Opoku-Agyeman, D.; Acquah, I.S.K.; Agyabeng-Mensah, Y.; Afum, E.; Faibil, D.; Abdoulaye, F.A.M. Examining the Correlations between Stakeholder Pressures, Green Production Practices, Firm Reputation, Environmental and Financial Performance: Evidence from Manufacturing SMEs. Sustain. Prod. Consum. 2021, 27, 100–114. [Google Scholar] [CrossRef]

- Cariola, A.; Fasano, F.; La Rocca, M.; Skatova, E. Environmental Sustainability Policies and the Value of Debt in EU SMEs: Empirical Evidence from the Energy Sector. J. Clean. Prod. 2020, 275, 123133. [Google Scholar] [CrossRef]

- Rossi, M.; Lombardi, R.; Siggia, D.; Oliva, N. The Impact of Corporate Characteristics on the Financial Decisions of Companies: Evidence on Funding Decisions by Italian SMEs. J. Innov. Entrep. 2016, 5, 2. [Google Scholar] [CrossRef] [Green Version]

- Giacosa, E.; Culasso, F.; Mazzoleni, A.; Rossi, M. A model for the evaluation trends performance in small and medium enterprises. Corp. Ownersh. Control 2016, 13, 389–402. [Google Scholar] [CrossRef]

- Rossi, M. Capital Structure of Small and Medium Enterprises: The Italian Case. IJGSB 2014, 6, 130. [Google Scholar] [CrossRef]

- Rossi, M.; Lombardi, R.; Nappo, F.; Trequattrini, R. The Capital Structure Choices of Agro-Food Firms: Evidence from Italian SMEs. IJMP 2015, 8, 172. [Google Scholar] [CrossRef]

- Kása, R.; Radácsi, L.; Csákné Filep, J. Családi vállalkozások definíciós operacionalizálása és hazai arányuk becslése a kkv-szektoron belül. Statisztikai Szemle 2019, 97, 146–174. [Google Scholar] [CrossRef]

- Sági, J.; Chandler, N.; Lentner, C. Family Businesses and Predictability of Financial Strength: A Hungarian Study. Probl. Perspect. Manag. 2020, 18, 476–489. [Google Scholar] [CrossRef]

- Harangozó, G.; Szigeti, C. Corporate Carbon Footprint Analysis in Practice—With a Special Focus on Validity and Reliability Issues. J. Clean. Prod. 2017, 167, 1177–1183. [Google Scholar] [CrossRef]

- Szigeti, C.; Szennay, Á.; Lisányi Endréné Beke, J.; Polák-Weldon, J.R.; Radácsi, L. Challenges of Corporate Ecological Footprint Calculations in the SME Sector in Hungary: Case Study Evidence from Six Hungarian Small Enterprises. In Agroecological Footprints Management for Sustainable Food System; Banerjee, A., Meena, R.S., Jhariya, M.K., Yadav, D.K., Eds.; Springer: Singapore, 2021; pp. 345–363. ISBN 9789811594960. [Google Scholar]

- Wackernagel, M.; Rees, W. Our Ecological Footprint—Reducing Human Impact on the Earth; New Society Publishers: Gabriola, BC, Canada, 1996; ISBN 978-0-86571-312-3. [Google Scholar]

- Wackernagel, M.; Rees, W.E. Perceptual and Structural Barriers to Investing in Natural Capital: Economics from an Ecological Footprint Perspective. Ecol. Econ. 1997, 20, 3–24. [Google Scholar] [CrossRef]

- Wackernagel, M.; Onisto, L.; Bello, P.; Callejas Linares, A.; Susana López Falfán, I.; Méndez García, J.; Isabel Suárez Guerrero, A.; Guadalupe Suárez Guerrero, M. National Natural Capital Accounting with the Ecological Footprint Concept. Ecol. Econ. 1999, 29, 375–390. [Google Scholar] [CrossRef]

- Van den Bergh, J.C.J.M.; Verbruggen, H. Spatial Sustainability, Trade and Indicators: An Evaluation of the ‘Ecological Footprint’. Ecol. Econ. 1999, 29, 61–72. [Google Scholar] [CrossRef]

- Monfreda, C.; Wackernagel, M.; Deumling, D. Establishing National Natural Capital Accounts Based on Detailed Ecological Footprint and Biological Capacity Assessments. Land Use Policy 2004, 21, 231–246. [Google Scholar] [CrossRef]

- Čuček, L.; Klemeš, J.J.; Kravanja, Z. A Review of Footprint Analysis Tools for Monitoring Impacts on Sustainability. J. Clean. Prod. 2012, 34, 9–20. [Google Scholar] [CrossRef]

- Galli, A.; Wiedmann, T.; Ercin, E.; Knoblauch, D.; Ewing, B.; Giljum, S. Integrating Ecological, Carbon and Water Footprint into a “Footprint Family” of Indicators: Definition and Role in Tracking Human Pressure on the Planet. Ecol. Indic. 2012, 16, 100–112. [Google Scholar] [CrossRef]

- Zhu, Y.; Jiang, S.; Han, X.; Gao, X.; He, G.; Zhao, Y.; Li, H. A Bibliometrics Review of Water Footprint Research in China: 2003–2018. Sustainability 2019, 11, 5082. [Google Scholar] [CrossRef] [Green Version]

- Helka, J.; Ostrowski, J.; Abdel-Razek, M.; Hawighorst, P.; Henke, J.; Majer, S.; Thrän, D. Combining Environmental Footprint Models, Remote Sensing Data, and Certification Data towards an Integrated Sustainability Risk Analysis for Certification in the Case of Palm Oil. Sustainability 2020, 12, 8273. [Google Scholar] [CrossRef]

- Toth, G.; Szigeti, C. The Historical Ecological Footprint: From over-Population to over-Consumption. Ecol. Indic. 2016, 60, 283–291. [Google Scholar] [CrossRef]

- Borucke, M.; Moore, D.; Cranston, G.; Gracey, K.; Iha, K.; Larson, J.; Lazarus, E.; Morales, J.C.; Wackernagel, M.; Galli, A. Accounting for Demand and Supply of the Biosphere’s Regenerative Capacity: The National Footprint Accounts’ Underlying Methodology and Framework. Ecol. Indic. 2013, 24, 518–533. [Google Scholar] [CrossRef]

- Getting to Know the National Footprint and Biocapacity Accounts—Global Footprint Network. Global Footprint Network. Available online: https://www.footprintnetwork.org/) (accessed on 20 October 2020).

- Lin, D.; Hanscom, L.; Murthy, A.; Galli, A.; Evans, M.; Neill, E.; Mancini, M.S.; Martindill, J.; Medouar, F.-Z.; Huang, S.; et al. Ecological Footprint Accounting for Countries: Updates and Results of the National Footprint Accounts, 2012–2018. Resources 2018, 7, 58. [Google Scholar] [CrossRef] [Green Version]

- Liu, P. Investigación sobre la huella ecológica del turismo: El caso de Langzhong en China. Obs. Medioambient. 2019, 22, 245–263. [Google Scholar] [CrossRef]

- Danish; Ulucak, R.; Khan, S.U.-D. Determinants of the Ecological Footprint: Role of Renewable Energy, Natural Resources, and Urbanization. Sustain. Cities Soc. 2020, 54, 101996. [Google Scholar] [CrossRef]

- Kovács, Z.; Harangozó, G.; Szigeti, C.; Koppány, K.; Kondor, A.C.; Szabó, B. Measuring the Impacts of Suburbanization with Ecological Footprint Calculations. Cities 2020, 101, 102715. [Google Scholar] [CrossRef]

- Lu, W.-C. The Interplay among Ecological Footprint, Real Income, Energy Consumption, and Trade Openness in 13 Asian Countries. Environ. Sci. Pollut. Res. 2020, 27, 45148–45160. [Google Scholar] [CrossRef]

- Zambrano-Monserrate, M.A.; Ruano, M.A.; Ormeño-Candelario, V.; Sanchez-Loor, D.A. Global Ecological Footprint and Spatial Dependence between Countries. J. Environ. Manag. 2020, 272, 111069. [Google Scholar] [CrossRef]

- Chambers, N.; Simmons, C.; Wackernagel, M.; Simmons, C.; Wackernagel, M. Sharing Nature’s Interest: Ecological Footprints as an Indicator of Sustainability; Routledge: London, UK, 2000; ISBN 978-1-315-87026-7. [Google Scholar]

- Tóth, G.; Szigeti, C.; Harangozó, G.; Szabó, D.R. Ecological Footprint at the Micro-Scale—How It Can Save Costs: The Case of ENPRO. Resources 2018, 7, 45. [Google Scholar] [CrossRef] [Green Version]

- Global Footprint Network. Open Data Platform. Available online: http://data.footprintnetwork.org/#/analyzeTrends?type=EFCtot&cn=5001 (accessed on 20 October 2020).

- Trumpp, C.; Endrikat, J.; Zopf, C.; Guenther, E. Definition, Conceptualization, and Measurement of Corporate Environmental Performance: A Critical Examination of a Multidimensional Construct. J. Bus. Ethics 2015, 126, 185–204. [Google Scholar] [CrossRef]

- ISO 14031:2013(En), Environmental Management—Environmental Performance Evaluation—Guidelines. Available online: https://www.iso.org/obp/ui/#iso:std:iso:14031:ed-2:v1:en (accessed on 21 October 2020).

- Dragomir, V.D. How Do We Measure Corporate Environmental Performance? A Critical Review. J. Clean. Prod. 2018, 196, 1124–1157. [Google Scholar] [CrossRef]

- Jung, E.J.; Kim, J.S.; Rhee, S.K. The Measurement of Corporate Environmental Performance and Its Application to the Analysis of Efficiency in Oil Industry. J. Clean. Product. 2001, 9, 551–563. [Google Scholar] [CrossRef]

- Schultze, W.; Trommer, R. The Concept of Environmental Performance and Its Measurement in Empirical Studies. J. Manag. Control 2012, 22, 375–412. [Google Scholar] [CrossRef]

- Csutora, M.; Harangozó, G. Twenty Years of Carbon Accounting and Auditing—A Review and Outlook. Soc. Econ. 2017, 39, 459–480. [Google Scholar] [CrossRef]

- Wackernagel, M.; Beyers, B. Ecological Footprint—Managing Our Biocapacity Budget; New Society Publishers: Gabriola, BC, Canada, 2019; ISBN 978-0-86571-911-8. [Google Scholar]

- Stanwick, P.A.; Stanwick, S.D. The Relationship between Corporate Social Performance, and Organizational Size, Financial Performance, and Environmental Performance: An Empirical Examination. J. Bus. Ethics 1998, 17, 195–204. [Google Scholar] [CrossRef]

- Tsoutsoura, M. Corporate Social Responsibility and Financial Performance; University of California at Berkeley: Berkeley, CA, USA, 2004. [Google Scholar]

- Santis, P.; Albuquerque, A.; Lizarelli, F. Do Sustainable Companies Have a Better Financial Performance? A Study on Brazilian Public Companies. J. Clean. Product. 2016, 133, 735–745. [Google Scholar] [CrossRef]

- Crifo, P.; Diaye, M.-A.; Pekovic, S. CSR Related Management Practices and Firm Performance: An Empirical Analysis of the Quantity–Quality Trade-off on French Data. Int. J. Product. Econ. 2016, 171, 405–416. [Google Scholar] [CrossRef] [Green Version]

- Rokhmawati, A.; Gunardi, A.; Rossi, M. How Powerful Is Your Customers’ Reaction to Carbon Performance? Linking Carbon and Firm Financial Performance. Int. J. Energy Econ. Policy 2017, 7, 85–95. [Google Scholar]

- Chen, Y.-C.; Hung, M.; Wang, Y. The Effect of Mandatory CSR Disclosure on Firm Profitability and Social Externalities: Evidence from China. J. Account. Econ. 2018, 65, 169–190. [Google Scholar] [CrossRef]

- La Rosa, F.; Liberatore, G.; Mazzi, F.; Terzani, S. The Impact of Corporate Social Performance on the Cost of Debt and Access to Debt Financing for Listed European Non-Financial Firms. Eur. Manag. J. 2018, 36, 519–529. [Google Scholar] [CrossRef]

- Taliento, M.; Favino, C.; Netti, A. Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe. Sustainability 2019, 11, 1738. [Google Scholar] [CrossRef] [Green Version]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Van Beurden, P.; Gössling, T. The Worth of Values—A Literature Review on the Relation between Corporate Social and Financial Performance. J. Bus. Ethics 2008, 82, 407. [Google Scholar] [CrossRef] [Green Version]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does It Pay to Be Good... And Does It Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial Performance; Social Science Research Network: Rochester, NY, USA, 2009. [Google Scholar]

- Schaltegger, S.; Synnestvedt, T. The Link between ‘Green’ and Economic Success: Environmental Management as the Crucial Trigger between Environmental and Economic Performance. J. Environ. Manag. 2002, 65, 339–346. [Google Scholar] [CrossRef]

- Harangozó, G.; Kerekes, S.; Zsóka, Á. Environmental Management Practices in the Manufacturing Sector—Hungarian Features in International Comparison. J. East Eur. Manag. Stud. 2010, 15, 312–347. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Y.; Wei, J.; Zhu, Y.; George-Ufot, G. Untangling the Relationship between Corporate Environmental Performance and Corporate Financial Performance: The Double-Edged Moderating Effects of Environmental Uncertainty. J. Clean. Product. 2020, 263, 121584. [Google Scholar] [CrossRef]

- Murakami, S.; Takasu, T.; Islam, K.; Yamasue, E.; Adachi, T. Ecological Footprint and Total Material Requirement as Environmental Indicators of Mining Activities: Case Studies of Copper Mines. Environ. Sustain. Indic. 2020, 8, 100082. [Google Scholar] [CrossRef]

- Freire-Guerrero, A.; Alba-Rodríguez, M.D.; Marrero, M. A Budget for the Ecological Footprint of Buildings Is Possible: A Case Study Using the Dwelling Construction Cost Database of Andalusia. Sustain. Cities Soc. 2019, 51, 101737. [Google Scholar] [CrossRef]

- González-Vallejo, P.; Muñoz-Sanguinetti, C.; Marrero, M. Environmental and Economic Assessment of Dwelling Construction in Spain and Chile. A Comparative Analysis of Two Representative Case Studies. J. Clean. Product. 2019, 208, 621–635. [Google Scholar] [CrossRef]

- Fan, Y.; Qiao, Q.; Xian, C.; Xiao, Y.; Fang, L. A Modified Ecological Footprint Method to Evaluate Environmental Impacts of Industrial Parks. Resour. Conserv. Recycl. 2017, 125, 293–299. [Google Scholar] [CrossRef]

- Eurostat. Road Accident Fatalities—Statistics by Type of Vehicle—Statistics Explained. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php/Road_accident_fatalities_-_statistics_by_type_of_vehicle (accessed on 16 July 2020).

- European Commission. EU Buildings Factsheets. Available online: https://ec.europa.eu/energy/eu-buildings-factsheets_en (accessed on 19 November 2020).

- Ibn-Mohammed, T.; Greenough, R.; Taylor, S.; Ozawa-Meida, L.; Acquaye, A. Operational vs. Embodied Emissions in Buildings—A Review of Current Trends. Energy Build. 2013, 66, 232–245. [Google Scholar] [CrossRef]

- Directive 2010/31/EU of the European Parliament and of the Council of 19 May 2010 on the Energy Performance of Buildings; European Union: Brussels, Belgium, 2010.

- Lux, G. Újraiparosodás Közép-Európában; Studia Regionum; Dialóg Campus Kiadó: Budapest, Hungary, 2017; ISBN 978-615-5376-94-8. [Google Scholar]

- Fekete, D.; Rechnitzer, J. Együtt Nagyok. Város és Vállalat 25 éve; Studia Regionum; Dialóg Campus Kiadó: Budapest, Hungary, 2019; ISBN 978-615-6020-17-8. [Google Scholar]

- Gibbs, D.; Deutz, P. Reflections on Implementing Industrial Ecology through Eco-Industrial Park Development. J. Clean. Product. 2007, 15, 1683–1695. [Google Scholar] [CrossRef]

- Mózner, Z.V. Sustainability and Consumption Structure: Environmental Impacts of Food Consumption Clusters. A Case Study for Hungary. Int. J. Consum. Stud. 2014, 38, 529–539. [Google Scholar] [CrossRef]

- International Energy Agency. Energy Policies of IEA Countries—Hungary 2017 Review; International Energy Agency: Paris, France, 2017; p. 176. [Google Scholar]

- DEFRA. Greenhouse Gas Reporting: Conversion Factors 2018. Available online: https://www.gov.uk/government/publications/greenhouse-gas-reporting-conversion-factors-2018 (accessed on 15 July 2020).

- Świąder, M.; Szewrański, S.; Kazak, J.K.; Van Hoof, J.; Lin, D.; Wackernagel, M.; Alves, A. Application of Ecological Footprint Accounting as a Part of an Integrated Assessment of Environmental Carrying Capacity: A Case Study of the Footprint of Food of a Large City. Resources 2018, 7, 52. [Google Scholar] [CrossRef] [Green Version]

- Csutora, M. Az ökológiai lábnyom számításának módszertani alapjai. In Az Ökológiai Lábnyom Ökonómiája; Csutora, M., Ed.; Aula Kiadó: Budapest, Hungary, 2011; pp. 6–16. [Google Scholar]

- Commission of the European Communities. Commission Recommendation of 6 May 2003 Concerning the Definition of Micro, Small and Medium-Sized Enterprises (Text with EEA Relevance) (Notified under Document Number C(2003) 1422); Commission of the European Communities: Brussels, Belgium, 2003. [Google Scholar]

- Harangozó, G.; Kovács, Z.; Kondor, A.C.; Szabó, B. A budapesti várostérség fogyasztási alapú ökológiai lábnyomának változása 2003 és 2013 között. Ter. Stat. 2019, 59, 97–123. [Google Scholar] [CrossRef]

- Rossi, M.; Nerino, M.; Capasso, A. Corporate Governance and Financial Performance of Italian Listed Firms. The Results of an Empirical Research. Corp. Ownersh. Control 2015, 12, 628–643. [Google Scholar] [CrossRef]

- Widyaningsih, I.U.; Gunardi, A.; Rossi, M.; Rahmawati, N.A. Expropriation by the Controlling Shareholders on Firm Value in the Context of Indonesia: Corporate Governance as Moderating Variable. IJMFA 2017, 9, 322. [Google Scholar] [CrossRef]

- Gjergji, R.; Vena, L.; Sciascia, S.; Cortesi, A. The Effects of Environmental, Social and Governance Disclosure on the Cost of Capital in Small and Medium Enterprises: The Role of Family Business Status. Bus. Strategy Environ. 2021, 30, 683–693. [Google Scholar] [CrossRef]

{kind=link}

| Element of EF | Description | Calculation Method | Literature |

|---|---|---|---|

| EFmeals | Food consumption during work time, calculated on the base of Hungarian national average values. | Equation (1) | Mózner [70] |

| EFwater consumption | Water consumed by employees during work time. Industrial water consumption is excluded. | Equation (2) | Chambers et al. [35] |

| EFbuilt-up area | Total area of non-water absorbent surfaces. | Equation (3) | Lin et al. [29] |

| EFelectricity consumption | Electricity consumption from electricity grid, included heating and boiling with electric devices. | Equation (4) | IEA [71] DEFRA 2018 [72] |

| EFheating and boiling | Heating and boiling with fossil fuels, e.g., natural gas, coal, or wood. | Equation (5) | DEFRA 2018 [72] |

| EFtransportation | All transportation-related EF, including commuting (both public transport and vehicles owned by employees or by the enterprise), transportation of goods, using of corporate cars, flying, etc., petrol, gasoline, and gas consumption of equipment (e.g., generators) are included. | n/a | DEFRA 2018 [72] |

| Name of Group | Common Sense | Related Subsection |

|---|---|---|

| construction | Extensive use of machines, heavy-duty vehicles. EF is determined mostly by fossil fuel consumption. | Section 4.1 |

| white-collar jobs | Knowledge-intensive activities, moderate land use, equipment with low consumption (e.g., laptops, plotters, etc.). Vehicle usage is limited for passenger cars and only for field visits or commuting. EF is rather balanced among determining factors. | Section 4.2 |

| production | Technology-intensive activities, significant usage of equipment and land. EF is determined mostly by energy and fossil fuel consumption, but built-up land usage and food consumption are also significant. | Section 4.3 |

| retail and/or wholesale trade | Significant land use (buildings and parking lots), moderate use of equipment (e.g., refrigerators). Moderate vehicle usage. EF is determined significantly by heating and boiling; fuel consumption could be significant in case of home delivery or other vehicle usage. | Section 4.4 |

| transportation | Extensive use of trucks and other resource usage is negligible. EF is determined most of all by gasoline consumption. | Section 4.5 |

| Construction | White-Collar Jobs | Production | Retail and Wholesale Trade | Transportation | |||

|---|---|---|---|---|---|---|---|

| Valid cases | 17 | 17 | 15 | 20 | 4 | ||

| specific EF (global hectares/employee) | Mean | 1.25 | 0.46 | 1.47 | 1.10 | 20.15 | |

| 95% Confidence Interval for Mean | Lower Bound | 0.87 | 0.32 | 0.85 | 0.73 | 17.00 | |

| Upper Bound | 1.62 | 0.60 | 2.08 | 1.47 | 23.30 | ||

| 5% Trimmed Mean | 1.20 | 0.43 | 1.42 | 1.06 | 20.20 | ||

| Median | 0.93 | 0.44 | 1.21 | 0.81 | 20.56 | ||

| Std. Deviation | 0.72 | 0.27 | 1.11 | 0.79 | 1.98 | ||

| eco-efficiency (global hectares/th. EUR) | Mean | 0.089 | 0.051 | 0.067 | 0.088 | 1.055 | |

| 95% Confidence Interval for Mean | Lower Bound | 0.065 | 0.029 | 0.033 | 0.050 | 0.410 | |

| Upper Bound | 0.113 | 0.074 | 0.100 | 0.126 | 1.701 | ||

| 5% Trimmed Mean | 0.086 | 0.047 | 0.064 | 0.079 | 1.040 | ||

| Median | 0.076 | 0.041 | 0.047 | 0.071 | 0.918 | ||

| Std. Deviation | 0.047 | 0.043 | 0.061 | 0.081 | 0.406 | ||

| specific value added (th EUR/employee) | Mean | 15.40 | 15.29 | 32.98 | 17.24 | 20.64 | |

| 95% Confidence Interval for Mean | Lower Bound | 11.94 | 7.23 | 14.04 | 12.64 | 11.79 | |

| Upper Bound | 18.85 | 23.34 | 51.93 | 21.84 | 29.49 | ||

| 5% Trimmed Mean | 14.99 | 13.01 | 27.78 | 16.83 | 20.74 | ||

| Median | 14.96 | 11.38 | 22.97 | 15.78 | 21.57 | ||

| Std. Deviation | 6.71 | 15.67 | 34.21 | 9.83 | 5.56 | ||

| Activity | Specific EF (gha/empl) | Eco-Efficiency (gha/th EUR) | Specific Value Added (th EUR/empl) | Activity | Specific EF (gha/empl) | Eco-Efficiency (gha/th EUR) | Specific Value Added (th EUR/empl) | Activity | Specific EF (gha/empl) | Eco-Efficiency (gha/th EUR) | Specific Value Added (th EUR/empl) | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| construction | specific EF (gha/empl) | Pearson Correlation | 1 | 0.778 ** | 0.177 | white-collar jobs | 1 | 0.524 * | −0.042 | production | 1 | 0.788 ** | −0.209 |

| Sig. (2-tailed) | 0.000 | 0.497 | 0.037 | 0.878 | 0.001 | 0.472 | |||||||

| N | 17 | 17 | 17 | 16 | 16 | 16 | 14 | 14 | 14 | ||||

| eco-efficiency (gha/th EUR) | Pearson Correlation | 0.778 ** | 1 | −0.408 | 0.524 * | 1 | −0.507 * | 0.788 ** | 1 | −0.378 | |||

| Sig. (2-tailed) | 0.000 | 0.104 | 0.037 | 0.045 | 0.001 | 0.182 | |||||||

| N | 17 | 17 | 17 | 16 | 16 | 16 | 14 | 14 | 14 | ||||

| specific value added (th EUR/empl) | Pearson Correlation | 0.177 | −0.408 | 1 | −0.042 | −0.507 * | 1 | −0.209 | −0.378 | 1 | |||

| Sig. (2-tailed) | 0.497 | 0.104 | 0.878 | 0.045 | 0.472 | 0.182 | |||||||

| N | 17 | 17 | 17 | 16 | 16 | 16 | 14 | 14 | 14 | ||||

| retail and wholesale trade | specific EF (gha/empl) | Pearson Correlation | 1 | 0.379 | 0.245 | transportation | 1 | 0.591 | −0.406 | ||||

| Sig. (2-tailed) | 0.099 | 0.298 | 0.409 | 0.594 | |||||||||

| N | 20 | 20 | 20 | 4 | 4 | 4 | |||||||

| eco-efficiency (gha/th EUR) | Pearson Correlation | 0.379 | 1 | −0.543 * | 0.591 | 1 | −0.960 * | ||||||

| Sig. (2-tailed) | 0.099 | 0.013 | 0.409 | 0.040 | |||||||||

| N | 20 | 20 | 20 | 4 | 4 | 4 | |||||||

| specific value added (th EUR/empl) | Pearson Correlation | 0.245 | −0.543 * | 1 | −0.406 | −0.960 * | 1 | ||||||

| Sig. (2-tailed) | 0.298 | 0.013 | 0.594 | 0.040 | |||||||||

| N | 20 | 20 | 20 | 4 | 4 | 4 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Szennay, Á.; Szigeti, C.; Beke, J.; Radácsi, L. Ecological Footprint as an Indicator of Corporate Environmental Performance—Empirical Evidence from Hungarian SMEs. Sustainability 2021, 13, 1000. https://0-doi-org.brum.beds.ac.uk/10.3390/su13021000

Szennay Á, Szigeti C, Beke J, Radácsi L. Ecological Footprint as an Indicator of Corporate Environmental Performance—Empirical Evidence from Hungarian SMEs. Sustainability. 2021; 13(2):1000. https://0-doi-org.brum.beds.ac.uk/10.3390/su13021000

Chicago/Turabian StyleSzennay, Áron, Cecília Szigeti, Judit Beke, and László Radácsi. 2021. "Ecological Footprint as an Indicator of Corporate Environmental Performance—Empirical Evidence from Hungarian SMEs" Sustainability 13, no. 2: 1000. https://0-doi-org.brum.beds.ac.uk/10.3390/su13021000