The Nexus of CSR and Co-Creation: A Roadmap towards Consumer Loyalty

by

, , ,

, , ,

Naveed Ahmad

1,* ,

,

Miklas Scholz

2,3,4 ,

,

Zia Ullah

5 ,

,

Muhammad Zulqarnain Arshad

6,

Raja Irfan Sabir

1 and

Waris Ali Khan

7

1

Faculty of Management Studies, University of Central Punjab, Lahore 54000, Pakistan

2

Division of Water Resources Engineering, Department of Building and Environmental Technology, Faculty of Engineering, Lund University, 221 00 Lund, Sweden

3

Department of Civil Engineering Science, School of Civil Engineering and the Built Environment, Kingsway Campus, University of Johannesburg, Johannesburg 2006, South Africa

4

Civil Engineering Research Group, School of Science, Engineering and Environment, The University of Salford, Newton Building, Salford M5 4WT, UK

5

Leads Business School, Lahore Leads University, Lahore 54000, Pakistan

6

Department of Management Sciences, Lahore Garrison University, Lahore 54000, Pakistan

7

Faculty of Business, Economics and Accounting, Universiti Malaysia Sabah, Sabah 88400, Malaysia

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(2), 523; https://0-doi-org.brum.beds.ac.uk/10.3390/su13020523

Submission received: 12 December 2020

/

Revised: 31 December 2020

/

Accepted: 3 January 2021

/

Published: 7 January 2021

(This article belongs to the Special Issue Corporate Social Responsibility (CSR) and CSR Reporting)

Abstract

:Corporate Social Responsibility (CSR) is regarded as an effort to be undertaken by the businesses to contribute towards society at large positively. The idea behind the concept of CSR is that businesses are required to pursue the notion of pro-social objectives along with economic objectives. Research has long established that corporate social responsibility, along with its philanthropic nature, can also produce extraordinary marketing results for businesses. The relationship between CSR and consumer loyalty is well acknowledged in extant literature. Likewise, involving consumers through co-creation in the product/service development process may provide an exciting experience to consumers, which is likely to influence their loyalty. With these arguments, the present research investigates the impact of CSR on consumer loyalty with the mediating role of co-creation in the banking sector of an emerging economy such as Pakistan. Structural equation modeling (SEM) is used for data analysis in the present study. The results validate that CSR improves consumer loyalty, and co-creation partially mediates this relationship. The results of the current survey will help banking institutions to identify how they can develop core strategic considerations based on CSR and co-creation.

1. Introduction

The increasing consumer pressure on businesses to work responsibly in society is largely because of the swift advancement in information technology, which has contributed to a communicative and translucent environment. In this perspective, public opinion and consumers learn more about unfair activities and castigate brands involved in harmful activities to the environment and society [1]. As a result, some strong brands have already begun to base social responsibility at the core of their business plans and have become true symbols of conscience that can honestly show responsibility in dealing with consumers [2]. When consumers see this, their loyalty to the organization may surge, as they tend to respect what is good for society and the planet. In addition, the new digital and connected environments allow consumers to communicate directly with brands [3].

The term co-creation is referred to as a product or service development process in which corporations involve the consumer in product/service-related decisions. More specifically, the notion of co-creating may also be used when referring to anything consumers want to submit to the corporation, such as new ideas, design, or product/service-related content [4]. In other words, co-creation (CC) can be regarded as an efficient, flexible, and social process that aims to create relevant new products or services through communication and interaction with consumers [5]. The perception of co-creation is attractive in nature, as it can lead to many resources of the organization, including economic efficiency [6], risk reduction [7], relationship marketing [8], better understanding, and competitiveness [9]. In addition, co-creation is an inspiring experience for many consumers in different ways [10]. First, consumers can establish warm, deep, and exclusive relationships with other members of the collaborative community. Second, when firms participate in a co-creation project, clients always feel that they are growing as individuals, learning, and being creative with the community [11]. Most importantly, engaging in co-creation activities offers consumers opportunities for self-development along with social and hedonic [12] resources that lead them to feel close to a brand. Remarkably, the same can be said about corporate social responsibility (CSR), which seeks to ensure the value of the environment and community in which most participants interact.

Responsible social businesses are open to pay attention to and understanding the needs and challenges of consumers [13], as well as looking for appropriate solutions. Similarly, a co-creation strategy involves engaging consumers and other innovative processes that allow them to make appropriate decisions [14]. From this point of view, it is reasonable to expect that consumers will recognize their products as open to integration projects when they consider them socially responsible. However, several authors have shown that CSR can affect many companies/brands and consumer variables, such as business/corporate analysis [15], firm-idiosyncratic risk [16], strong market value [17], financial results [18], consumer-oriented commitment [19], and consumer perception [20]. In previous studies, little has been studied concerning socially responsible behavior that can help businesses increase their creative activity, such as co-creation [21,22].

Banks are adapting consumer-centric strategies with a strong position in competition and innovation through consumer involvement and satisfaction. The development of a natural understanding of joint ventures with consumers in the banking sector is a growing trend through innovation in banking and consumer services [23]. Organizations that prioritize their consumers and are aware of the needs of people are inclined to develop a large pool of loyal consumers [24]. Having a large pool of consumers, banks can achieve financial stability. Consumer satisfaction, on the other hand, requires business services and increased product performance [25], as well as increased operational efficiency [26], value creation, and higher returns [27]. Therefore, it is imperative to cultivate and screen strategies to increase consumer satisfaction and profitability in any organization. This is possible by considering the consumer’s preference [28], but it is not easy to work with. At the same time, consumers are always looking for an improved exchange experience via co-creation. Organizations that meet the needs of consumers have the opportunity to design through their own opinion bank, recognized as co-creation.

The present study primarily focuses on the banking sector in Pakistan as it is one of the largest corporate sectors which is involved in CSR activities as a result of the global financial meltdown in 2008 to rebuild consumer loyalty and confidence [29]. We define consumer loyalty in line with the argument of Oliver [30], who describes consumer loyalty as a behavioral tendency of consumers to favor and support a specific brand and consider the competing ones less. Furthermore, consumer loyalty is an outcome of the positive emotion of consumers builds on their experience with a specific brand. In addition, well-reputed banks in the banking industry began to engage in co-creation activities aimed at improving the consumer experience. Consumer loyalty (CL) has a strong impact on corporate efficiency, as it is directly related to lowering marketing expenses and increasing revenues [31]. The present study contributes to extant literature significantly. First, the homogenized character of banking institutions makes it challenging for a specific bank to differentiate its offerings from the rest of the crowd. In this regard, CSR may serve as an effective tool to enhance consumer loyalty [3] and trust [32]. This argument is also acknowledged by recent researchers in existing literature, such as Sun et al. [33] and Iglesias et al. [34]. Second, the previous research has largely focused on emotional integration, such as affective engagement, with limited empirical studies of consumer behavior, particularly on loyal consumer behavior [35,36]. Third, there is limited evidence that CSR and co-creation can enhance loyal consumers in the Asian context, particularly in an emerging economy such as Pakistan. In terms of the author’s knowledge, there are limited studies investigating the overall effect of CSR on consumer loyalty with the mediating impact of co-creation, although there are some studies in the non-Asian context [22,34,37]. Fourth, the majority of extant literature has focused on the direct relation of CSR and consumer loyalty [38,39,40] without considering the intervening variables such as co-creation, which can better explain this relationship. Lastly, the present study contributes to the extant CSR literature pertinent to the Asian context in terms of the banking sector. The study also complements the literature by examining the mediation impact of co-creation amongst the CSR and consumer loyalty relationship. To eliminate these shortcomings, this article examines the impact of the bank’s CSR actions on consumer loyalty with the mediating effect of co-creation. The rationale for the current study is appropriate for strengthening understanding this relationship and supplementing the lack of empirical research in this area related to the Asian context.

2. Theory and Hypotheses

To understand consumer response to CSR, most researchers assume that CSR can improve overall consumer behavior [37,41,42]. If there is a strong link between CSR functions and consumers, researchers should consider the link between CSR and other consumer aspects, such as co-creation [43]. Consumers have changed their traditional role in services as they participate not only in services but also in corporate–customer relations [44]. A number of researchers have acknowledged that CSR practices create value for both the community and the organization, as its philanthropic services provide a sense of connection to and recognition by the consumer [5,10,43]. When consumers see the value is more aligned towards community, they are more likely to share their values with organization.

Co-creation is a collaborative business model in which organizations actively ask consumers to select and contribute to the contents of a new product or service. According to O’Hern and Rindfleisch [45], there are four types of co-creation, including (a) collaborating, (b) tinkering, (c) co-designing, and (d) submitting. Collaborating is referred to as an open contribution from consumers to improve the design, content, and features of new products/services. Tinkering is referred to as an open contribution, but that is driven by the organization. In other words, tinkering means organizations welcome the ideas from consumers, but they select only those which are close to their business strategies and objectives. Co-designing means consumers of an organization are identified as co-designers, and organizations invite them to submit their content relevant to a new product or service. In this connection, the organization provides a checklist to the consumers and asks them to contribute within the scope of that list. Finally, submitting is relevant to the traditional concept of new product development in which the organization chooses the central idea of a new product. However, the consumer is invited by the organization to submit their ideas openly without having pre-determined lists or questions.

Co-creation is not a new concept. It dates back to the pre-industrial period when consumers decided on the technology of production [46]. However, during the period of industrialization, co-creation disappeared due to the need for mass production to remain cost-effective. However, with the advent of the post-industrial era, businesses began to acquire a dynamic, flexible production environment for new product development, incorporating decentralization and emerging information technologies. In this case, consumer policies will be different. They can be predicted and managed. This has hampered mass production capacity to meet the existing needs of consumers. Then, in the early 2000s, co-creation re-emerged and has been seen as the future of new products and services [47].

Accordingly, Von Wallpach et al. [48] suggested that the modern business approach would be consumer-oriented by better-involving consumers in the development of market offerings. The literature has revealed that CSR increases consumer satisfaction, and when consumers are satisfied in some way, they have the tendency to participate in the creation of this term [21,34,49]. In addition, Ahen and Zettinig [50] established that as consumers become more conscious of a business’s CSR process, they become more familiar with the firm and eager to create their personal resources (e.g., information, knowledge) to help the company perform co-creation functions in an efficient manner. In the same vein, Simpson, Robertson, and White [22] suggested that consumers’ willingness to do something other than internal and external incentives will depend on past goals, including how they interact with others in the community. Hence, it is logical to think that consumers will be more likely to contribute to co-creating activities with socially responsible organizations. Hence, we propose:

Hypothesis 1 (H1).

CSR is positively related to co-creation.

In the recent era, consumers have more options for purchasing goods and services than ever before, but still, they seem dissatisfied. Organizations focus on producing a variety of products and services but are currently unable to meet the needs of consumers in an exact way. This gap can be overcome by sitting together and listening to each other [12]. At the same time, it is difficult to determine the essence of cost-effective business design. Beirão et al. [51] suggested that the key to basic knowledge of the service depends on the consumer. It focuses on the growth of the buyer–supplier relationship through communication and dialogue. However, to date, little research has been done on how consumers engage in co-creation and focus on creating a value basis for a business and lead to better consumer outcomes. Likewise, Buhalis and Sinarta [52] argued that co-creation is helpful to innovate and improve the consumer experience. They further contended that co-creation promotes transparency in the product/service creation process, which ultimately builds a higher level of satisfaction among consumers, which, in turn, enhances their loyalty. It also provides an example of a key set of controls and maintenance before providing products or services. Ge et al. [53] conducted a study and highlighted the importance of co-creation for the survival of organizations. In addition, interactions between businesses and individuals improve learning in both groups to ensure that organizations can attract and retain consumers and the network to ensure better results [54]. The process of co-creation is a collaborative process that builds interaction between the organization and its stakeholders, including consumers. This collaborative approach motivates consumers to be engaged with a particular brand in the process of new product/service development. Hence, through co-creation, organizations can create positive emotions among consumers, which is likely to boost their level of loyalty with a specific organization [55]. In other words, co-creation creates switching barriers due to which consumers are less likely to pay attention to competing brands [56].

It is important to look at co-creation from a psychological point of view in the context of service. Consumer skills and knowledge affect the value creation process. Thus, value is a co-produced activity of the seller and the buyer and always arises from co-creation [57]. The focus on value creation has expanded as firms and consumers have introduced new and innovative ways to support individual add-on systems. These approaches shift the focus from the traditional perspective of exchange. The essence of creating a partnership as a business concept seeks to observe situations that further overlap the boundaries between firms and consumers by continuing to define this most important transformation of their roles [58]. When consumers are strongly involved in the provision of services, they tend to invest their time and search for information on how they can input to the organization to co-produce the value. If the service satisfies consumers, purchases will frequently occur while there will be a reduction in searching for an alternative. Hence, the loyalty of consumers is enhanced [59]. The essence of co-creation can serve as a form of switching barrier which induces consumer loyalty positively. Therefore, we recommend the following hypothesis.

Hypothesis 2 (H2).

Co-creation is positively related to consumer loyalty.

It is also important to consider the service-dominant logic provided by Lusch et al. [60]. They contended that competing in service is not all about adding values to the product, but it calls for collective efforts from all departments ranging from marketing communication, the strategic intent of business, operations, finance, human resource, and others. They further mentioned in another study that service-dominant logic has to be viewed as an integrating approach in which all units of the organization are interconnected to produce a better output [61]. Likewise, service-dominant logic is a philosophy that is underlined in the theme that there should be collaboration among consumers, partners, and internal stakeholders, such as employees, at all levels of service delivery [62]. Hence, in line with service-dominant logic, the consideration of consumers in product-related decisions is logical.

Consumer loyalty may be attributed to a behavioral tendency of consumers to prefer a particular brand over competing ones. In other words, CL is the likelihood of consumers to buy and keep buying a specific brand. Loyalty is an outcome of positive consumer experiences with an organization, which creates favorable attitudes among consumers [63]. Simply put, when consumers are loyal to a specific brand, there is less probability that they will consider other brands while they make purchase decisions. Moreover, loyal consumers are less price-sensitive, and they are even willing to pay a price premium to the organization to which they are loyal [64]. Specific activities and pressures guide corporations to engage in social roles not mandated or required by law and not expected of businesses in an ethical sense, but which are increasingly strategic in orientation. The development of CSR has largely attracted the attention of many researchers. Carroll [65] described the structure of CSR by describing "the economic, legal, ethical and social expectations of society as expected from the socially responsible organizations". This definition is widely accepted and identifies four types of liability. Financial, legal, ethical, and voluntary. Carroll [66,67] also assumed that this responsibility is primarily administrative and elective. However, the expectation that business will achieve these goals depends on social norms.

Some businesses are affected by the desire to participate in social activities that are not permitted or required by state laws and are not ethically expected from the business but are beyond the strategy of practice. Examples of such efforts include but not limited to volunteering, starting drug rehabilitation programs for drug-addicted people in a society, training the unemployed, and setting up institutes for children’s rights, etc. Mohr et al. [68] divided CSR into two general categories. The first section discusses CSR for different stakeholders in the organization (e.g., employers, customers, employees, and community). The second category stems from Kotler and Lee [69] on the societal marketing approach. Both definitions emphasize that a socially responsible organization should be pro-actively involved in decisions beyond short-term interests. Taking into account stakeholder theory, Freeman and Dmytriyev [70] defined social responsibility as the level of corporate responsibility for stakeholders’ financial, legal, ethical self-determination. Numerous marketing studies have shown that CSR has a positive effect on consumer loyalty with the organization and its resources [3,10,34]. CSR has been reported to directly or indirectly affect customer responses [71]. Park et al. [72] reported a positive relationship between CSR and overall consumer loyalty.

The correlation between CSR and consumer loyalty is defined in the theory of social exchange [73]. It states that the organization has a socially ethical response, which will create social mutuality [74]. Furthermore, the CSR initiatives of an organization create a positive attitude among consumers towards the organization. In response to CSR activities, consumers are more likely to stay connected with the brand for a longer period [33], and they are less likely to think about competing brands [75]. Similarly, the positive association between CSR initiatives of an organization and consumer loyalty is also supported by recent researchers, such as Chang and Yeh [76], Cuesta-Valiño et al. [77], and Iglesias, Markovic, Bagherzadeh, and Singh [34]. CSR practices build social relationships because sometimes, companies do not provide CSR resources directly to their consumers. However, as a member of the public, the client shares these activities [78]. CSR affects and strengthens positive consumer–company relationships with its products and services. The same argument is built in the study of Raza, Saeed, Iqbal, Saeed, Sadiq, and Faraz [10], who found a positive link between CSR and consumer loyalty in the context of Pakistani banks. Moreover, it is long established in the extant literature that CSR and co-creation both are collaborative approaches, and this collaborative nature of both constructs is likely to induce consumer loyalty in positive terms [5,10,34,37]. When consumers believe that a particular bank is actively involved in CSR activities, they form positive feelings about that specific bank. In the same vein, consumers are more likely to participate in co-creation activities with the banks they believe are caring for community. To put it another way, we argue that co-creation activities better explain the relationship of CSR and consumer loyalty. Hence, it is logical to think that co-creation is a potential mediator between CSR and consumer loyalty. Hence, the following two hypotheses are proposed.

Hypothesis 3 (H3).

CSR is positively related to consumer loyalty.

Hypothesis 4 (H4).

Co-creation mediates between CSR and consumer loyalty.

3. Methodology

3.1. Sample, Data, and Handling of Social Desirability

A survey strategy was used for data collection for the present study. For this purpose, we selected three major cities of Pakistan, including Islamabad, Faisalabad, and Lahore. The reason for choosing these three cities lies in the argument that these three cities are the largest cities in the country and multiple branches of all banking institutions exist in these cities in multiple locations. Our argument for selecting these cities is also in line with recent researcher in the context of Pakistan [10,33]. The reason for choosing the banking sector of Pakistan is that this sector has faced tough competition and a pattern of asymmetric performance [79] during the last decade due to several macro- and micro-level factors, such as the global financial crisis of 2008–2010 [80] and the daunting economic conditions of the country [81]. So, it is imperative to suggest some strategies to lift the performance of this sector. Before starting the data collection, we carefully searched for those banks which constituted the largest presence over the country, having several hundred branches all over Pakistan.

Qualification criteria for banks were they must have a CSR activity page on their website, and banks must distribute a CSR update on paper and electronic media and mirror their CSR administrations in their yearly annual reports. These chosen banks are the largest banks of the nation [82] and are scattered over 80% area of Pakistan. We, in this regard, selected four major banks of Pakistan, including the National Bank of Pakistan, United Bank Limited, Habib Bank Limited, and the Muslim Commercial Bank Limited, as these had more than 800 plus branches in the country. To actuate the data collection process, we included individuals who had a bank account in one of these four banks. Initially, we distributed 1000 surveys among the respondents of different banking institutions and finally received 529 completed questionnaires, which were considered for data analysis. We approached the respondents when they were leaving the banks or were present outside these banks at automated teller machines (ATM).

To mitigate the effect of social desirability, we took several steps. For example, the items in the survey were scattered randomly throughout the questionnaire to break any sequence developed on the part of the respondent. Similarly, we used existing scales for all three variables of our study so that the validity and reliability are pre-established. Moreover, the instrument was cross-checked by experts to make sure that it did not contain any jargon or confusing words. Likewise, we visited different branches of these banks on multiple days and different timings, and before distributing the survey to the respondents, we assessed the CSR knowledge of the respondent. All these measures to mitigate the effect of social desirability are in line with Podsakoff et al. [83] and Grimm [84].

3.2. Measures

We adapted already established scales for data collection of the present study. For instance, the scale of CSR was taken from the study of Eisingerich et al. [74]. The scale consisted of three items. A sample item was “this bank is a socially responsible bank”. Similarly, the items for co-creation were adapted from Nysveen and Pedersen [85]. There were four items for measuring the co-creation construct. A sample item includes “I often find solutions to my problems together with this bank”. Lastly, the scale of consumer loyalty was adapted from Dagger et al. [86], which included three items. A sample item for which is “I am loyal to this bank”. All items were rated on a five-point Likert scale. To test the reliability of our adapted instrument, we also checked the reliability results for our instrument, which are reported in Table 1.

4. Results

Common Method Bias

The data for all variables were collected from the same respondents at a specific point in time. Hence, there was potential for common method bias (CMB) to challenge the reliability and validity of our data. To address the issue of CMB, we took several steps. For instance, we performed a confirmatory factor analysis in line with the recommendation of Gliner et al. [87]. For this purpose, we set all items to be free to load on a single factor. The results of this test were not in an acceptable range, whereas these results significantly improved when we executed a three-factor CFA, meaning that the model is well fitted to the data in the three-factor model as compared to a single factor analysis, which is a confirmation that CMB is not a potential threat to our data. Table 2 presents the demographic profile of respondents.

Further, we also checked factor loading using factor analysis to see if all items were well loaded to their respective factors. The results produced good enough results (see Table 3) to establish that there is no issue of factor loading in our data. Likewise, we also checked alpha values for all three variables to ensure inter-item consistency. The results of all variables were in the acceptable range [88]. We checked the convergent validity of our instrument by calculating the values of average variances extracted (AVEs) for all variables, which showed values above 0.5, which is in an acceptable range, which means that convergent validity is highly established (see Table 3). Moreover, the discriminant validity was assured by calculating the square root of AVE for each variable and comparing it to the values of correlation. All variables in this respect produced significant results (see Table 4).

For the purpose of hypothesis testing, we used the covariance-based structural equation modeling (SEM) technique in AMOS through the maximum likelihood method. The results are shown in Table 5, in which we introduce three models along with model fit indices. Among these three models, models 1 and 2 were alternative models, whereas model 3 was the model of our prime interest as it is the hypothesized model of the study. It is evident from Table 5 that χ2/df value for our hypothesized model was reduced as compared to alternate models 1 and 2, which means that our hypothesized model fit the data more accurately as compared to models 1 and 2. Further, to compare the hypothesized model with alternate models, we applied the chi-square difference test. It is obvious from the results in Table 5 that as we moved from model 1 to model 3, there was a significant improvement in model fit values and χ2 value also improved as model 3 produced most suitable values in comparison to model 1 and model 2, which means that our data were well fitted to the hypothesized model. The results further confirmed that the change in chi-square values was also improved from model 1 to model 3 (Δχ2 = 1368.55, Δdf = 4, p-value < 0.05, from model 1 to model 2, and Δχ2 = 109.53, Δdf = 3, p-value < 0.05 from model 2 to model 3). Hence, model 3 was the most appropriate model, which provided us the confidence to take the analysis to a further level of hypotheses testing.

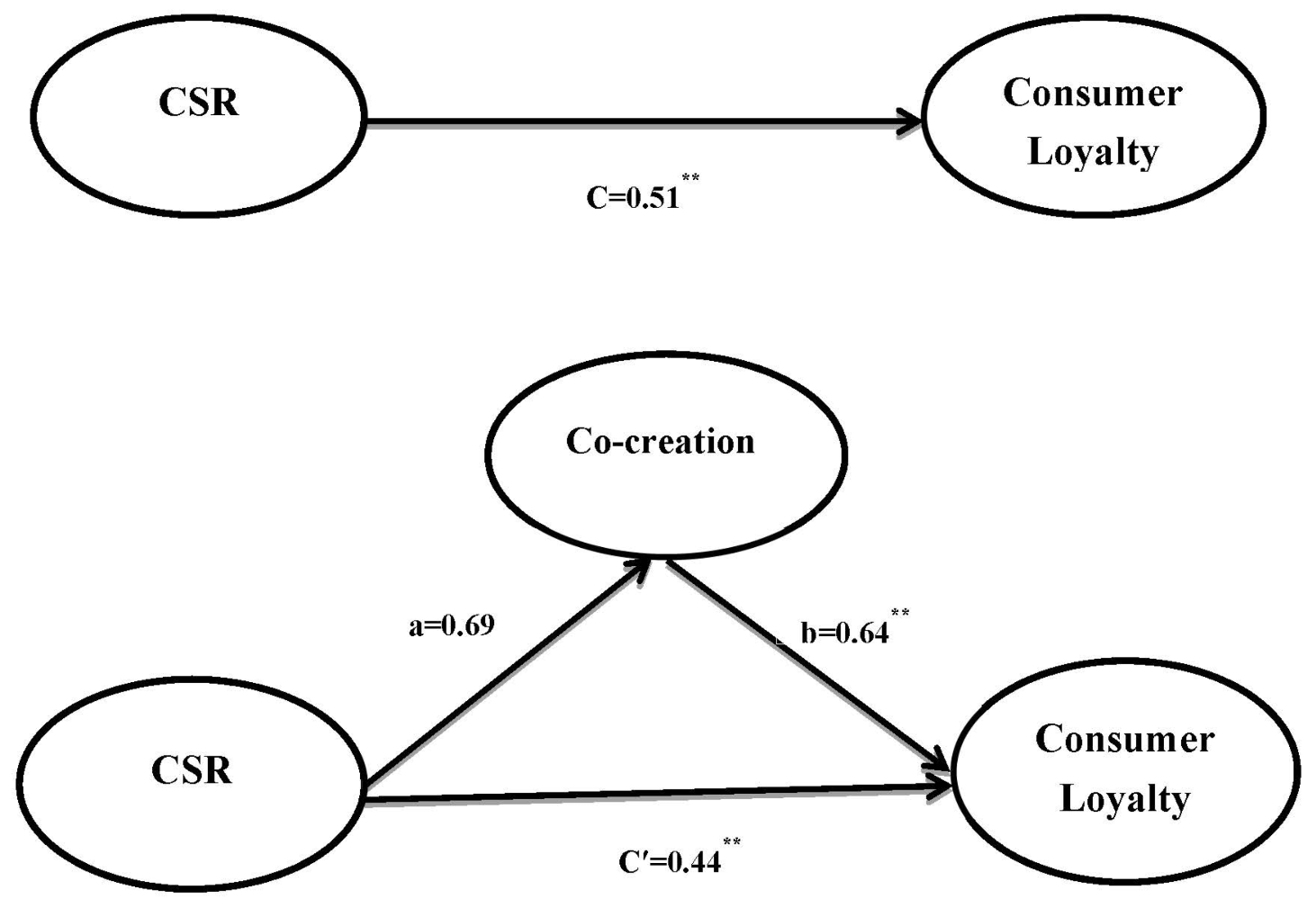

The results of hypothesis testing were significant for all four hypotheses of the present study (Table 6 and Table 7). First, we checked the direct effect for H1, H2, and H3 (Table 6), which produced significant results, meaning that our H1, H2, and H3 were positive and significant. Finally, we used bootstrapping by using a large bootstrap sample of 3000 to check the indirect effect for Hypothesis 4. The results of bootstrapping (Table 7) showed significance in line with the statement of Hypothesis 4. Hence, based on statistical results, we concluded that all four hypotheses are significant and true. The beta values for direct and indirect effects can also be seen in Figure 1.

5. Discussion

Our results supported the hypotheses that CSR and co-creation are optimally linked to consumer loyalty. Previous studies have shown that consumers who are involved in the creation of value-added products are more loyal to a bank. Loyalty can often be seen as a strong bond between repetition and acquisition of a product/service, which is influenced by social norms and circumstances [89]. To be competitive, strategies aimed at retaining existing consumers and increasing consumer loyalty are of paramount importance. Loyal consumers who participate in repurchases from the same organization or seller can suggest the product or service to people who know it and have a positive attitude [90]. Consumer participation in the bank service creation process affects their loyalty or otherwise. Consumer loyalty has had a positive impact, as they feel influenced by the design and characteristics of the service they buy from the bank. Consumers provide information and knowledge in co-creation process which ultimately results in increased loyalty. This often affects the establishment of a long-term relationship with the service provider. Our results also received support from Raza, Saeed, Iqbal, Saeed, Sadiq, and Faraz [10], Cossío-Silva, Francisco-José, Revilla-Camacho, María-Ángeles, Vega-Vázquez, Manuela, Palacios-Florencio, and Beatriz [24], Iglesias, Markovic, Bagherzadeh, and Singh [34], Malik and Ahsan [54], Woratschek, Horbel, and Popp [59] who argued that co-creation is positively related to consumer loyalty. The findings of the present study provide additional support to existing research studies that demonstrate that involving banking consumers in co-creation has a significant impact on their loyalty. Well planned CSR initiatives of a bank may create marketing related outcomes along with the philanthropic objectives. For instance, if banks plan their CSR initiatives in a decent manner and communicate these initiatives with the consumers using different communication media, then such communication may promote a positive attitude among consumers, and they will be happy to pay a price premium to socially responsible organizations. It is worth mentioning here that although the concept of CSR is philanthropic in nature, it can also create marketing outcomes for an organization. These arguments are in line with the finding of Nyilasy et al. [91].

6. Conclusions

The banking sector of Pakistan is concentrated and facing a high level of competition in recent times. The homogenized character of this industry makes the situation even worse from the marketing perspective, as creating a strong base for consumer loyalty in a homogenized industry is challenging. CSR, in this regard, may be considered as a promising strategy to increase the loyalty of consumers as the modern consumers are well informed about a banks’ CSR practices to see if their bank is socially responsible or not. Likewise, the integration of CSR and co-creation further boost consumer loyalty because involving consumers in product/service design makes the process of product/service creation more transparent. This sense of transparency and the sense of community care in the form of CSR investment is an energizer for consumer loyalty.

Consumers want to see the initiative of their banking partners. To stay in the growing digital world, banks need to work beyond their formal goals. The realization of consumer loyalty by a bank creates better marketing-related results, which are of utmost importance for any organization. Consumer engagement (co-creation) creates a positive relationship, and the more positive this relationship is, the more loyal consumers will be. It is well-known that today’s consumers are quick to doubt, distrust, and quit a brand. At the same time, consumer trust is essential for decisions that help build long-term relationships, reduce consumer agitation, and build those relationships by offering specialized services via engaging the consumer for co-creating the product/service. Consumers favor supporting organizations about which they feel their money is being spent for the social cause and that decision-makers care about them and their communities, and that money is returning to society. It also shows how consumers choose a particular bank to be involved with, how loyal they are to it, and whether they would recommend it to others. The importance of social responsibility in banks will continue to grow as today’s consumers research their banks to know how to spend money and look to the public and consumer feedback before contacting the organization. Investing in a social responsibility system helps to have a positive impact on the bank, which is beneficial to potential consumers and for the growth of an organization.

6.1. Implications for Practice

The implications of this study lie in demonstrating how a bank’s social responsibility affects consumer loyalty. This study expands previous literature on social identity, as well as social exchanges, by combining the mediation effect of social exchange variables, such as co-creation. The co-creation is found to play an important mediating role in the proposed relationship of this study. Consumer awareness of CSR activities helps make “ethical capital” for banks that promotes consumer engagement and interest in a specific bank, which leads to an increase in consumer loyalty. Consumers are likely to believe that banks involved in socially responsible activities take into account the concerns of all stakeholders, which, in turn, contributes to the credibility of the bank. Likewise, consumers are more likely to connect more with a bank with an image of social responsibility as part of self-reliance. CSR and co-creation facilitate long-term relationships with consumers to promote overall consumer loyalty.

The results of this study can be used by professionals to increase consumer loyalty, especially in the context of the banking sector and generally to other service sectors. Managers can realize the fact that CSR and co-creation activities can boost consumer behavior on positive terms because both approaches are collaborative in nature. Moreover, the co-creation activities of a bank have a significant effect on various outcomes of consumer behavior. The results show that CSR involvement of banks encourages banking consumers to be proactively involved in the co-creation process to co-produce banking products/services. All these activities are likely to produce a large umbrella of loyal consumers. The banking sector in Pakistan needs to realize that although CSR initiatives are philanthropic in nature, these initiatives may serve as a strong marketing strategy to bond the consumers with a particular bank. In addition, the transparent nature of CSR and co-creation also increase banking consumers’ loyalty. Therefore, policymakers need to invest more in social responsibility initiatives, as consumers tend to support socially responsible banks.

Our results showed that the banking sector in Pakistan is concerned with CSR activities and implements socially responsible programs for their banks. It is also important to note that although CSR directly affects consumer loyalty, its indirect effect through co-creation is more meaningful as compared to the direct effect. Consumers identify a bank when they determine that it matches their social norms. The current study found that the bank’s image, built on socially responsible practices, helps consumers identify with the bank and the company’s long-term orientation. Given the importance of the relationship between CSR and co-creation and co-creation between CSR and loyalty, the bank should invest more in CSR and co-creation initiatives. In fact, it is suggested that banking institutions in Pakistan should place CSR and co-creation at the core of their business objectives if they want to reap the benefits of consumer loyalty to the fullest. By managing a strategic partnership with consumers, banks can improve consumer involvement in banking decisions, which can improve the consumers’ feeling that their bank designs product after considering consumers’ input. This builds positive feelings and bonds consumers to a particular bank. Therefore, banking policymakers should be encouraged to develop CSR-based initiatives that surpass customer expectations. Thus, banks can strengthen their marketing strategy by investing in CSR activities that consumers consider important. When designing consumer loyalty programs, the bank should not only be associated with CSR but also pay attention to the interests and branding with consumers through co-creation.

Co-creation promotes consumer participation in product/service development and can be used as a tool to develop a competitive business environment in a particular bank. Banks become consumer-oriented by involving them in product/service-related decisions through co-creation, which places them in a strong position in a competitive environment through increased loyalty. The development and understanding of the design of a collaborative model in the banking sector is a growing trend in the services of banks and consumers. Banks that prioritize their consumers and are aware of the needs of people are more likely to develop a large pool of loyal customers. Having a large consumer pool of loyalty, banks can achieve financial stability, which is, dare we say, the ultimate objective of any business. On the other hand, improved loyalty requires an increase in quality and banking services and requires improved operational efficiency, value creation, and higher returns.

6.2. Limitations and Suggestions for Future

The present write-up faces some limitations, but we consider these limitations an opening for upcoming researchers in the same area. First, the study is limited to only the banking sector in Pakistan, and we only considered three cities of Pakistan. Although these three cities cover the largest banking distribution in the country, we still consider it a limitation because of the potential issue of external validity. To address this limitation, we propose two suggestions for future researchers. One, the present study should be replicated in other service sectors, such as the insurance sector, hospitality, and health sector. Two, future researchers should prepare a large sample, including respondents from different cities and provinces of Pakistan.

Second, the cross-sectional nature of data also limits the study in the prediction of the causality of relationships among study variables. In this respect, one suggestion for future researchers is to conduct the research in the same area with longitudinal data so that the confidence in causality may be established further. Third, although we took different steps to address the issue of common method bias, we suggest to future researchers to collect data from respondents in two waves so that their genuine responses may be collected. One potential issue in this regard may be the availability and accessibility of the sampling frame. Lastly, future researchers may consider the leadership style as a potential moderator amongst CSR and co-creation because servant leadership and transformational leadership styles may have different effects on this relationship.

Author Contributions

All authors have contributed equally to all sections of this manuscript. All authors have read and agreed to the published version of the manuscript.

Funding

The research received no external funding.

Informed Consent Statement

Informed consent was obtained from the respondents of the survey.

Data Availability Statement

The data will be made available on request from corresponding author.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abbas, J. Impact of total quality management on corporate green performance through the mediating role of corporate social responsibility. J. Clean. Prod. 2020, 242, 118458. [Google Scholar] [CrossRef]

- Jeon, M.M.; Lee, S.; Jeong, M. Perceived corporate social responsibility and customers’ behaviors in the ridesharing service industry. Int. J. Hosp. Manag. 2020, 84, 102341. [Google Scholar] [CrossRef]

- Servera-Francés, D.; Piqueras-Tomás, L. The effects of corporate social responsibility on consumer loyalty through consumer perceived value. Econ. Res. Ekon. Istraživanja 2019, 32, 66–84. [Google Scholar] [CrossRef] [Green Version]

- Schallehn, H.; Seuring, S.; Strähle, J.; Freise, M. Defining the antecedents of experience co-creation as applied to alternative consumption models. J. Serv. Manag. 2019, 30, 209–251. [Google Scholar] [CrossRef]

- Luu, T.T. CSR and customer value co-creation behavior: The moderation mechanisms of servant leadership and relationship marketing orientation. J. Bus. Ethics 2019, 155, 379–398. [Google Scholar] [CrossRef]

- Kim, D.W.; Trimi, S.; Hong, S.G.; Lim, S. Effects of co-creation on organizational performance of small and medium manufacturers. J. Bus. Res. 2020, 109, 574–584. [Google Scholar] [CrossRef]

- Fernando, Y.; Chukai, C. Value co-creation, goods and service tax (GST) impacts on sustainable logistic performance. Res. Transp. Bus. Manag. 2018, 28, 92–102. [Google Scholar] [CrossRef]

- Hajli, N.; Shanmugam, M.; Papagiannidis, S.; Zahay, D.; Richard, M.-O. Branding co-creation with members of online brand communities. J. Bus. Res. 2017, 70, 136–144. [Google Scholar] [CrossRef]

- Cimbaljević, M.; Stankov, U.; Pavluković, V. Going beyond the traditional destination competitiveness–reflections on a smart destination in the current research. Curr. Issues Tour. 2019, 22, 2472–2477. [Google Scholar] [CrossRef]

- Raza, A.; Saeed, A.; Iqbal, M.K.; Saeed, U.; Sadiq, I.; Faraz, N.A. Linking corporate social responsibility to customer loyalty through co-creation and customer company identification: Exploring sequential mediation mechanism. Sustainability 2020, 12, 2525. [Google Scholar] [CrossRef] [Green Version]

- Chen, J.S.; Kerr, D.; Chou, C.Y.; Ang, C. Business co-creation for service innovation in the hospitality and tourism industry. Int. J. Contemp. Hosp. Manag. 2017, 29, 1522–1540. [Google Scholar] [CrossRef]

- Park, J.; Ha, S. Co-creation of service recovery: Utilitarian and hedonic value and post-recovery responses. J. Retail. Consum. Serv. 2016, 28, 310–316. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate social responsibility: Strategic implications. J. Manag. Stud. 2006, 43, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Lindgreen, A.; Swaen, V. Corporate social responsibility. Int. J. Manag. Rev. 2010, 12, 1–7. [Google Scholar] [CrossRef] [Green Version]

- Yoo, D.; Lee, J. The effects of corporate social responsibility (CSR) fit and CSR consistency on company evaluation: The role of CSR support. Sustainability 2018, 10, 2956. [Google Scholar] [CrossRef] [Green Version]

- Chen, R.C.; Hung, S.-W.; Lee, C.-H. Corporate social responsibility and firm idiosyncratic risk in different market states. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 642–658. [Google Scholar] [CrossRef]

- Crisóstomo, V.L.; de Souza Freire, F.; De Vasconcellos, F.C. Corporate social responsibility, firm value and financial performance in Brazil. Soc. Responsib. J. 2011, 7, 295–309. [Google Scholar] [CrossRef]

- Mallin, C.; Farag, H.; Ow-Yong, K. Corporate social responsibility and financial performance in Islamic banks. J. Econ. Behav. Organ. 2014, 103, S21–S38. [Google Scholar] [CrossRef]

- Lacey, R.; Kennett-Hensel, P.A. Longitudinal effects of corporate social responsibility on customer relationships. J. Bus. Ethics 2010, 97, 581–597. [Google Scholar] [CrossRef]

- Arli, D.I.; Lasmono, H.K. Consumers’ perception of corporate social responsibility in a developing country. Int. J. Consum. Stud. 2010, 34, 46–51. [Google Scholar] [CrossRef] [Green Version]

- Biggemann, S.; Williams, M.; Kro, G. Building in sustainability, social responsibility and value co-creation. J. Bus. Ind. Mark. 2014, 29, 304–312. [Google Scholar] [CrossRef]

- Simpson, B.; Robertson, J.L.; White, K. How co-creation increases employee corporate social responsibility and organizational engagement: The moderating role of self-construal. J. Bus. Ethics 2020, 166, 331–350. [Google Scholar] [CrossRef] [Green Version]

- Mainardes, E.W.; Teixeira, A.; da Silveira Romano, P.C. Determinants of co-creation in banking services. Int. J. Bank Mark. 2017, 35, 187–204. [Google Scholar] [CrossRef]

- Cossío-Silva, F.-J.; Revilla-Camacho, M.-Á.; Vega-Vázquez, M.; Palacios-Florencio, B. Value co-creation and customer loyalty. J. Bus. Res. 2016, 69, 1621–1625. [Google Scholar] [CrossRef]

- Williams, P.; Naumann, E. Customer satisfaction and business performance: A firm-level analysis. J. Serv. Mark. 2011, 25, 20–32. [Google Scholar] [CrossRef]

- Chang, M.; Jang, H.-B.; Li, Y.-M.; Kim, D. The relationship between the efficiency, service quality and customer satisfaction for state-owned commercial banks in China. Sustainability 2017, 9, 2163. [Google Scholar] [CrossRef] [Green Version]

- Mahmoud, M.A.; Hinson, R.E.; Anim, P.A. Service innovation and customer satisfaction: The role of customer value creation. Eur. J. Innov. Manag. 2018, 21, 402–422. [Google Scholar] [CrossRef]

- Adebiyi, S.O.; Shitta, H.A.; Olonade, O.P. Determinants of customer preference and satisfaction with Nigerian mobile telecommunication services. BVIMSR’s J. Manag. Res. 2016, 8, 1. [Google Scholar]

- Emeseh, E.; Ako, R.; Okonmah, P.; Ogechukwu, L. Corporations, CSR and self regulation: What lessons from the global financial crisis? Ger. Law J. 2010, 11, 230–259. [Google Scholar] [CrossRef] [Green Version]

- Oliver, R.L. Whence consumer loyalty? J. Mark. 1999, 63, 33–44. [Google Scholar] [CrossRef]

- Skryhun, N.; Kapinus, L.; Petrovych, M. Consumer loyalty assessment as an important means of increasing company’s profitability. National University of Food Technology: Kiev, Ukraine, 2020; Volume 5, pp. 3–8. [Google Scholar]

- Moliner, M.A.; Tirado, D.M.; Estrada-Guillén, M. CSR marketing outcomes and branch managers’ perceptions of CSR. Int. J. Bank Mark. 2019, 38, 63–85. [Google Scholar] [CrossRef] [Green Version]

- Sun, H.; Rabbani, M.R.; Ahmad, N.; Sial, M.S.; Cheng, G.; Zia-Ud-Din, M.; Fu, Q. CSR, Co-Creation and Green Consumer Loyalty: Are Green Banking Initiatives Important? A Moderated Mediation Approach from an Emerging Economy. Sustainability 2020, 12, 10688. [Google Scholar] [CrossRef]

- Iglesias, O.; Markovic, S.; Bagherzadeh, M.; Singh, J.J. Co-creation: A key link between corporate social responsibility, customer trust, and customer loyalty. J. Bus. Ethics 2020, 163, 151–166. [Google Scholar] [CrossRef]

- Ji, S.; Jan, I.U. The Impact of Perceived Corporate Social Responsibility on Frontline Employee’s Emotional Labor Strategies. Sustainability 2019, 11, 1780. [Google Scholar] [CrossRef] [Green Version]

- Ipsen, C.; Goe, R. Factors associated with consumer engagement and satisfaction with the Vocational Rehabilitation program. J. Vocat. Rehabil. 2016, 44, 85–96. [Google Scholar] [CrossRef]

- Tuan, L.T.; Rajendran, D.; Rowley, C.; Khai, D.C. Customer value co-creation in the business-to-business tourism context: The roles of corporate social responsibility and customer empowering behaviors. J. Hosp. Tour. Manag. 2019, 39, 137–149. [Google Scholar] [CrossRef]

- Mercadé-Melé, P.; Molinillo, S.; Fernández-Morales, A.; Porcu, L. CSR activities and consumer loyalty: The effect of the type of publicizing medium. J. Bus. Econ. Manag. 2018, 19, 431–455. [Google Scholar] [CrossRef] [Green Version]

- Raman, M.; Lim, W.; Nair, S. The impact of corporate social responsibility on consumer loyalty. Kajian Malays. J. Malays. Stud. 2012, 30, 71–93. [Google Scholar]

- Mandhachitara, R.; Poolthong, Y. A model of customer loyalty and corporate social responsibility. J. Serv. Mark. 2011, 25, 122–133. [Google Scholar] [CrossRef]

- Ijabadeniyi, A.; Govender, J.P. Coerced CSR: Lessons from consumer values and purchasing behavior. Corp. Commun. Int. J. 2019, 24, 515–531. [Google Scholar] [CrossRef]

- Palihawadana, D.; Oghazi, P.; Liu, Y. Effects of ethical ideologies and perceptions of CSR on consumer behavior. J. Bus. Res. 2016, 69, 4964–4969. [Google Scholar] [CrossRef]

- Mubushar, M.; Jaafar, N.B.; Ab Rahim, R. The influence of corporate social responsibility activities on customer value co-creation: The mediating role of relationship marketing orientation. Span. J. Mark. ESIC 2020, 24, 309–330. [Google Scholar] [CrossRef]

- Boccia, F.; Malgeri Manzo, R.; Covino, D. Consumer behavior and corporate social responsibility: An evaluation by a choice experiment. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 97–105. [Google Scholar] [CrossRef] [Green Version]

- O’Hern, M.S.; Rindfleisch, A. Customer co-creation: A typology and research agenda. Rev. Mark. Res. 2010, 6, 84–106. [Google Scholar]

- Barile, S.; Saviano, M. An introduction to a value co-creation model, viability, syntropy and resonance in dyadic interaction. Syntropy 2013, 2, 69–89. [Google Scholar]

- Terblanche, N.S. Some theoretical perspectives of co-creation and co-production of value by customers. Prof. Account. 2014, 14, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Von Wallpach, S.; Voyer, B.; Kastanakis, M.; Mühlbacher, H. Co-creating stakeholder and brand identities: Introduction to the special section. J. Bus. Res. 2017, 70, 395–398. [Google Scholar] [CrossRef]

- Assiouras, I.; Skourtis, G.; Giannopoulos, A.; Buhalis, D.; Koniordos, M. Value co-creation and customer citizenship behavior. Ann. Tour. Res. 2019, 78, 102742. [Google Scholar] [CrossRef]

- Ahen, F.; Zettinig, P. Critical perspectives on strategic CSR: What is sustainable value co-creation orientation? Crit. Perspect. Int. Bus. 2015, 11, 92–109. [Google Scholar] [CrossRef]

- Beirão, G.; Patrício, L.; Fisk, R.P. Value cocreation in service ecosystems. J. Serv. Manag. 2017, 28, 227–249. [Google Scholar] [CrossRef]

- Buhalis, D.; Sinarta, Y. Real-time co-creation and nowness service: Lessons from tourism and hospitality. J. Travel Tour. Mark. 2019, 36, 563–582. [Google Scholar] [CrossRef]

- Ge, J.; Xu, H.; Pellegrini, M.M. The effect of value co-creation on social enterprise growth: Moderating mechanism of environment dynamics. Sustainability 2019, 11, 250. [Google Scholar] [CrossRef] [Green Version]

- Malik, M.I.; Ahsan, R. Towards innovation, co-creation and customers’ satisfaction: A banking sector perspective. Asia Pac. J. Innov. Entrep. 2019, 13, 311–325. [Google Scholar] [CrossRef] [Green Version]

- Chen, C.-F.; Wang, J.-P. Customer participation, value co-creation and customer loyalty—A case of airline online check-in system. Comput. Hum. Behav. 2016, 62, 346–352. [Google Scholar] [CrossRef]

- Thuy, P.N.; Hau, L.N.; Evangelista, F. Service value and switching barriers: A personal values perspective. Serv. Ind. J. 2016, 36, 142–162. [Google Scholar] [CrossRef]

- Nadeem, W.; Juntunen, M.; Shirazi, F.; Hajli, N. Consumers’ value co-creation in sharing economy: The role of social support, consumers’ ethical perceptions and relationship quality. Technol. Forecast. Soc. Chang. 2020, 151, 119786. [Google Scholar] [CrossRef]

- Cluley, V.; Radnor, Z. Rethinking co-creation: The fluid and relational process of value co-creation in public service organizations. Public Money Manag. 2020, 1–10. [Google Scholar] [CrossRef]

- Woratschek, H.; Horbel, C.; Popp, B. Determining customer satisfaction and loyalty from a value co-creation perspective. Serv. Ind. J. 2020, 40, 777–799. [Google Scholar] [CrossRef]

- Lusch, R.F.; Vargo, S.L.; O’brien, M. Competing through service: Insights from service-dominant logic. J. Retail. 2007, 83, 5–18. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F. Service-dominant logic: Continuing the evolution. J. Acad. Mark. Sci. 2008, 36, 1–10. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F.; Akaka, M.A.; He, Y. Service-dominant logic. In The Routledge Handbook of Service Research Insights and Ideas; Routledge: Abingdon, UK, 2020; Volume 3. [Google Scholar]

- Luarn, P.; Lin, H.-H. A customer loyalty model for e-service context. J. Electron. Commer. Res. 2003, 4, 156–167. [Google Scholar]

- Izogo, E.E. Customer loyalty in telecom service sector: The role of service quality and customer commitment. TQM J. 2017, 29, 19–36. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate Performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef] [Green Version]

- Carroll, A.B. Corporate social responsibility: Evolution of a definitional construct. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Carroll, A.B. Carroll’s pyramid of CSR: Taking another look. Int. J. Corp. Soc. Responsib. 2016, 1, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Mohr, L.A.; Webb, D.J.; Harris, K.E. Do consumers expect companies to be socially responsible? The impact of corporate social responsibility on buying behavior. J. Consum. Aff. 2001, 35, 45–72. [Google Scholar] [CrossRef]

- Kotler, P.; Lee, N. Social Marketing: Influencing Behaviors for Good; Sage: London, UK, 2008. [Google Scholar]

- Freeman, R.E.; Dmytriyev, S. Corporate social responsibility and stakeholder theory: Learning from each other. Symph. Emerg. Issues Manag. 2017, 1, 7–15. [Google Scholar] [CrossRef] [Green Version]

- Li, Y.; Liu, B.; Huan, T.-C.T. Renewal or not? Consumer response to a renewed corporate social responsibility strategy: Evidence from the coffee shop industry. Tour. Manag. 2019, 72, 170–179. [Google Scholar] [CrossRef]

- Park, E.; Kim, K.J.; Kwon, S.J. Corporate social responsibility as a determinant of consumer loyalty: An examination of ethical standard, satisfaction, and trust. J. Bus. Res. 2017, 76, 8–13. [Google Scholar] [CrossRef]

- Chadwick-Jones, J.K. Social Exchange Theory: Its Structure and Influence in Social Psychology; Academic Press: Cambridge, MA, USA, 1976. [Google Scholar]

- Eisingerich, A.B.; Rubera, G.; Seifert, M.; Bhardwaj, G. Doing good and doing better despite negative information?: The role of corporate social responsibility in consumer resistance to negative information. J. Serv. Res. 2011, 14, 60–75. [Google Scholar] [CrossRef]

- Aramburu, I.A.; Pescador, I.G. The effects of corporate social responsibility on customer loyalty: The mediating effect of reputation in cooperative banks versus commercial banks in the Basque country. J. Bus. Ethics 2019, 154, 701–719. [Google Scholar] [CrossRef]

- Chang, Y.-H.; Yeh, C.-H. Corporate social responsibility and customer loyalty in intercity bus services. Transp. Policy 2017, 59, 38–45. [Google Scholar] [CrossRef]

- Cuesta-Valiño, P.; Rodríguez, P.G.; Núñez-Barriopedro, E. The impact of corporate social responsibility on customer loyalty in hypermarkets: A new socially responsible strategy. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 761–769. [Google Scholar] [CrossRef]

- Ailawadi, K.L.; Neslin, S.A.; Luan, Y.J.; Taylor, G.A. Does retailer CSR enhance behavioral loyalty? A case for benefit segmentation. Int. J. Res. Mark. 2014, 31, 156–167. [Google Scholar] [CrossRef]

- Ullah, A.; Zhao, X.; Kamal, M.A.; Riaz, A.; Zheng, B. Exploring asymmetric relationship between Islamic banking development and economic growth in Pakistan: Fresh evidence from a non-linear ARDL approach. Int. J. Financ. Econ. 2020. [Google Scholar] [CrossRef]

- Laeven, M.L.; Valencia, M.F. Systemic Banking Crises Revisited; International Monetary Fund: Washington, DC, USA, 2018. [Google Scholar]

- Haris, M.; Yao, H.; Tariq, G.; Malik, A.; Javaid, H.M. Intellectual capital performance and profitability of banks: Evidence from Pakistan. J. Risk Financ. Manag. 2019, 12, 56. [Google Scholar] [CrossRef] [Green Version]

- SBP. Credit Information Bureau. Available online: https://www.sbp.org.pk/ecib/members.htm (accessed on 27 December 2020).

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879. [Google Scholar] [CrossRef]

- Grimm, P. Social desirability bias. In Wiley International Encyclopedia of Marketing; Wiley: Hoboken, NJ, USA, 2010. [Google Scholar]

- Nysveen, H.; Pedersen, P.E. Influences of cocreation on brand experience. Int. J. Mark. Res. 2014, 56, 807–832. [Google Scholar] [CrossRef]

- Dagger, T.S.; David, M.E.; Ng, S. Do relationship benefits and maintenance drive commitment and loyalty? J. Serv. Mark. 2011, 25, 273–281. [Google Scholar] [CrossRef]

- Gliner, J.A.; Morgan, G.A.; Harmon, R.J. Single-factor repeated-measures designs: Analysis and interpretation. J. Am. Acad. Child Adolesc. Psychiatry 2002, 41, 1014–1016. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Chinomona, R.; Maziriri, E.T. The influence of brand awareness, brand association and product quality on brand loyalty and repurchase intention: A case of male consumers for cosmetic brands in South Africa. J. Bus. Retail. Manag. Res. 2017, 12, 12. [Google Scholar] [CrossRef] [Green Version]

- Ahmad, Z.; Jun, M.; Khan, I.; Abdullah, M.; Ghauri, T.A. Examining mediating role of customer loyalty for influence of brand related attributes on customer repurchase intention. J. Northeast Agric. Univ. Engl. Ed. 2016, 23, 89–96. [Google Scholar] [CrossRef]

- Nyilasy, G.; Gangadharbatla, H.; Paladino, A. Perceived greenwashing: The interactive effects of green advertising and corporate environmental performance on consumer reactions. J. Bus. Ethics 2014, 125, 693–707. [Google Scholar] [CrossRef]

Figure 1.

Direct and Indirect effect models. ** means beta values are significant

{kind=link}

Table 1.

Measurement items and reliability.

| Construct | Items |

|---|---|

| CSR [85] (α = 0.792) | This bank is a socially responsible bank. |

| This bank is more beneficial to society’s welfare than other banks. | |

| This bank contributes to society in positive ways. | |

| Co-creation [86] (α = 0.774) | I often express my personal needs to this bank. |

| I often find solutions to my problems together with this bank. | |

| I am actively involved when this bank develops new solutions for me. | |

| The bank encourages customers to create new solutions together. | |

| Loyalty [87] (α = 0.840) | I consider this bank my first choice when I purchase the services they supply. |

| I am willing to maintain my relationship with this bank. | |

| I am loyal to this bank. |

Table 2.

Demographic information of the sample.

| Frequency | % | |

|---|---|---|

| Gender | ||

| Male | 349 | 66.0 |

| Female | 180 | 34.0 |

| Age | ||

| 18–20 | 59 | 11.1 |

| 21–30 | 148 | 28.0 |

| 31–40 | 233 | 44.0 |

| Above 40 | 89 | 16.8 |

| Education | ||

| Matric | 53 | 10.0 |

| Intermediate | 112 | 21.1 |

| Graduate | 117 | 22.1 |

| Master | 203 | 38.3 |

| Higher | 44 | 8.3 |

Table 3.

Factor loadings, Reliability, and average variance extracted (AVE).

| Variable | Items | FL b (min–max) | t-Value (min–max) | α b | CR b | AVE |

|---|---|---|---|---|---|---|

| CSR | 3 | 0.78–0.84 | 11.15–21.33 | 0.79 | 0.82 | 0.57 |

| CC | 4 | 0.76–0.89 | 14.45–23.49 | 0.77 | 0.80 | 0.63 |

| CL | 3 | 0.79–0.87 | 17.93–22.89 | 0.84 | 0.84 | 0.60 |

b FL factor- loading; α b, Cronbach’s α coefficient; CR b, composite reliability; AVE average variance extracted.

Table 4.

Discriminant validity.

| Mean | SD | 1 | 2 | 3 | |

|---|---|---|---|---|---|

| CSR | 3.29 | 1.31 | 0.754 a | ||

| CC | 3.46 | 1.39 | 0.49 ** | 0.793 a | |

| CL | 3.59 | 1.11 | 0.56 ** | 0.58 ** | 0.774 a |

a Squared root of AVE in bold; ** represents significant values of correlation

Table 5.

Model fit comparison: alternate vs. hypothesized models.

| Model 1 | Model 2 | Model 3 | |

|---|---|---|---|

| Model Fit | Direct Effect of CSR and CC on CL | Hypothesized Model without Direct Effect b/w CSR and CL | Hypothesized Model |

| χ2 (df) | 1672.58 (59) | 316.90 (55) | 207.37 (52) |

| χ2/df | 28.35 | 5.76 | 3.98 |

| GFI | 0.861 | 0.910 | 0.972 |

| CFI | 0.811 | 0.907 | 0.938 |

| RMSEA | 0.139 | 0.067 | 0.049 |

| SRMR | 0.327 | 0.036 | 0.030 |

| TLI | 0.810 | 0.904 | 0.969 |

| AGFI | 0.833 | 0.881 | 0.929 |

Table 6.

Direct effects.

| Coefficients | SE | p-Value | 95% Bias Corrected CI | Decision | |

|---|---|---|---|---|---|

| H1: CSR → CC | 0.68 | 0.049 | <0.05 | 0.76; 0.85 | Supported |

| H2: CC → CL | 0.63 | 0.073 | 0.05 | 0.29; 0.61 | Supported |

| H3: CSR → CL | 0.51 | 0.198 | <0.05 | 0.18; 0.46 | Supported |

Table 7.

Mediation effect.

| Standardized Indirect Effect | 95% Bias Corrected CI * | Decision | |

|---|---|---|---|

| H4: CSR → CC → CL | 0.44 (0.144) * | 0.153–0.629 | Supported |

* bootstrap standard error in bold, CI = confidence interval.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Ahmad, N.; Scholz, M.; Ullah, Z.; Arshad, M.Z.; Sabir, R.I.; Khan, W.A. The Nexus of CSR and Co-Creation: A Roadmap towards Consumer Loyalty. Sustainability 2021, 13, 523. https://0-doi-org.brum.beds.ac.uk/10.3390/su13020523

AMA Style

Ahmad N, Scholz M, Ullah Z, Arshad MZ, Sabir RI, Khan WA. The Nexus of CSR and Co-Creation: A Roadmap towards Consumer Loyalty. Sustainability. 2021; 13(2):523. https://0-doi-org.brum.beds.ac.uk/10.3390/su13020523

Chicago/Turabian StyleAhmad, Naveed, Miklas Scholz, Zia Ullah, Muhammad Zulqarnain Arshad, Raja Irfan Sabir, and Waris Ali Khan. 2021. "The Nexus of CSR and Co-Creation: A Roadmap towards Consumer Loyalty" Sustainability 13, no. 2: 523. https://0-doi-org.brum.beds.ac.uk/10.3390/su13020523

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.