What Are the Reasons Behind the Economic Performance of the Hungarian Beer Industry? The Case of the Hungarian Microbreweries

Abstract

:1. Introduction

1.1. Introduction

1.2. Global Beer Industry

2. Materials and Methods

- β denotes the estimated coefficients,

- β0 captures the constant term,

- εij represents the error term.

3. Results

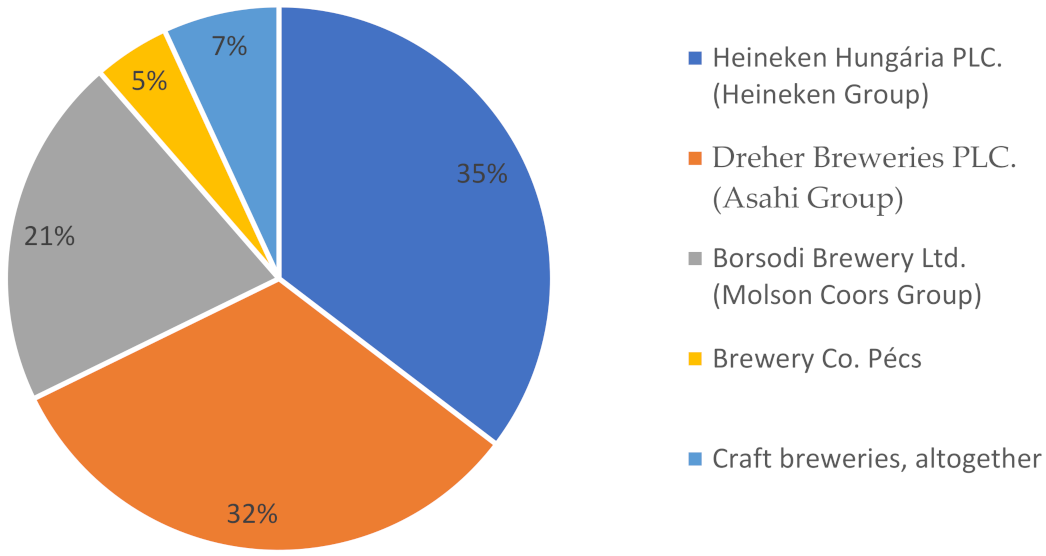

3.1. Performance of the Hungarian Brewing Industry

3.2. Factors Influencing Breweries’ Turnover

3.3. Factors Influencing Breweries’ EBIT

3.4. Factors Influencing Breweries’ Profit

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Feng, J. All About The Beer Industry. Worldatlas. 2017. Available online:https://www.worldatlas.com/articles/all-about-the-beer-industry.html (accessed on 20 October 2020).

- Török, Á.; Szerletics, Á.; Jantyik, L. Factors Influencing Competitiveness in the Global Beer Trade. Sustainability 2020, 12, 5057. [Google Scholar] [CrossRef]

- Kirin Beer University Report. Global Beer Consumption by Country in 2018; Kirin Holdings Company Limited. Available online: https://www.kirinholdings.co.jp/english/news/2019/1224_01.html (accessed on 24 December 2019).

- Brewers Association. 2020. Available online: https://www.brewersassociation.org/ (accessed on 10 January 2021).

- McCullough, M.; Berning, J.; Hanson, J.L. Learning by Brewing: Homebrewing Legalization and the Brewing Industry. Contemp. Econ. Policy 2019, 37, 25–39. [Google Scholar] [CrossRef]

- Bertella, G.; Halland, H.; Reykdal, O.; Martin, P. Sustainable value: The perspective of microbreweries in peripheral northern areas. In Case Studies in the Beer Sector; Capitello, R., Maehle, N., Eds.; Woodhead Publishing: Glossop, UK, 2021. [Google Scholar]

- Deserti, A.; Rizzo, F. Context dependency of social innovation: In search of new sustainability models. Eur. Plan. Stud. 2020, 28, 864–880. [Google Scholar] [CrossRef]

- Wells, P. Economies of Scale Versus Small Is Beautiful: A Business Model Approach Based on Architecture, Principles and Components in the Beer Industry. Bus. Models Sustain. Entrep. Innov. Transform. 2016, 29, 36–52. [Google Scholar] [CrossRef]

- Flanagan, D.J.; Lepisto, D.A.; Ofstein, L.F. Coopetition among nascent craft breweries: A value chain analysis. J. Small Bus. Enterp. Dev. 2018, 25, 2–16. [Google Scholar] [CrossRef]

- Hart, J. Drink Beer for Science: An Experiment on Consumer Preferences for Local Craft Beer. J. Wine Econ. 2018, 13, 429–441. [Google Scholar] [CrossRef]

- Garavaglia, C.; Swinnen, J. Economic Perspectives on Craft Beer; Springer Nature: Basel, Switzerland, 2018. [Google Scholar]

- Depenbusch, L.; Ehrich, M.; Pfizenmaier, U. Craft Beer in Germany. New Entries in a Challenging Beer Market. In Economic Perspectives on Craft Beer; Garavaglia, C., Swinnen, J., Eds.; Springer: Basel, Switzerland, 2018; pp. 183–210. [Google Scholar] [CrossRef]

- Weersink, A.; Probyn-Smith, K.; Von Massow, M. The Canadian Craft Beer Sector. In Economic Perspectives on Craft Beer; Garavaglia, C., Swinnen, J., Eds.; Springer: Basel, Switzerland, 2018; pp. 89–113. [Google Scholar] [CrossRef]

- Fastigi, M.; Vigano, E.; Esposti, R. The italian microbrewing experience: Features and perspectives. Bio-Based Appl. Econ. 2018, 7, 59–86. [Google Scholar] [CrossRef]

- Corsini, F.; Appio, F.P.; Frey, M. Exploring the antecedents and consequences of environmental performance in micro-enterprises: The case of the Italian craft beer industry. Technol. Forecast. Soc. Chang. 2019, 138, 340–350. [Google Scholar] [CrossRef]

- Alfeo, V.; Todaro, A.; Migliore, G.; Borsellino, V.; Schimmenti, E. Microbreweries, brewpubs and beerfirms in the Sicilian craft beer industry. Int. J. Wine Bus. Res. 2019, 32, 122–138. [Google Scholar] [CrossRef]

- Koch, E.S.; Sauerbronn, J.F.R. “To love beer above all things”: An analysis of Brazilian craft beer subculture of consumption. J. Food Prod. Mark. 2019, 25, 1–25. [Google Scholar] [CrossRef]

- Meyerding, S.G.H.; Bauchrowitz, A.; Lehberger, M. Consumer preferences for beer attributes in Germany: A conjoint and latent class approach. J. Retail. Consum. Serv. 2019, 47, 229–240. [Google Scholar] [CrossRef]

- Molnár, L.; Tátrai, M. A kézműves sörpiac helyzete és lehetőségei Magyarországon. Gki Gazdaságkutató Zrt 2017, 5–25. Available online: https://www.gki.hu/wp-content/uploads/2018/01/GKI-So%CC%88rtanulma%CC%81ny.pdf (accessed on 22 February 2021).

- Hajdók, F.; Kelemen, B.; Turjánszki, B. Nemzetközi üzleti stratégia kidolgozása a MONYO Brewing Co. számára. Bp. Corvinus Egy. 2020. [Google Scholar]

- Bojnec, Š.; Ferto, I. European enlargement and agro-food trade. Can. J. Agric. Econ. 2008, 56, 563–579. [Google Scholar] [CrossRef]

- Fertő, I.; Major, A.; Podruzsik, S.; Fogarasi, J. Be- és kilépés egy érett iparágban: A magyar kisüzemi sőrfőzdék esete. Hung. J. Food Nutr. Mark. 2016, 11, 39–46. [Google Scholar]

- Statista. Global Market Share of the Leading Beer Companies 2019, Based on Volume Sales. Available online: https://0-www-statista-com.brum.beds.ac.uk/statistics/257677/global-market-share-of-the-leading-beer-companies-based-on-sales/ (accessed on 10 December 2020).

- Moore, M.S.; Reid, N.; McLaughlin, R.B. The locational determinants of micro-breweries and brewpubs in the United States. In Brewing, Beer and Pubs; Springer: Berlin/Heidelberg, Germany, 2016; pp. 182–204. [Google Scholar]

- Rishika, R.; Kumar, A.; Janakiraman, R.; Bezawada, R. The Effect of Customers’ Social Media Participation on Customer Visit Frequency and Profitability: An Empirical Investigation. Inf. Syst. Res. 2013, 24, 108–127. [Google Scholar] [CrossRef]

- Cabras, I.; Bamforth, C. “From reviving tradition to fostering innovation and changing marketing: The evolution of microbrewing in the UK and US, 1980–2012. Bus. Hist. 2015, 58, 625–646. [Google Scholar] [CrossRef]

- Kleban, J.; Nickerson, I. To brew, or not to brew–that is the question: An analysis of competitive forces in the craft brew industry. J. Int. Acad. Case Stud. Agric. Econ. 2012, 18, 59–81. [Google Scholar]

- Török, Á.; Agárdi, I. Társadalmi vállalkozások gasztronómiai lehetőségei a rövid élelmiszerellátási láncok bevonásával Magyarországon. Vez. Bp. Manag. Rev. 2020, 51, 74–84. [Google Scholar] [CrossRef]

- Inwood, S.M.; Sharp, J.S.; Moore, R.H.; Stinner, D.H. Restaurants, chefs and local foods: Insights drawn from application of a diffusion of innovation framework. Agric. Hum. Values 2008, 26, 177–191. [Google Scholar] [CrossRef]

- Malak-Rawlikowska, A.; Majewski, E.; Wąs, A.; Borgen, S.O.; Csillag, P.; Donati, M.; Freeman, R.; Hoàng, V.; Lecoeur, J.-L.; Mancini, M.C.; et al. Measuring the Economic, Environmental, and Social Sustainability of Short Food Supply Chains. Sustainability 2019, 11, 4004. [Google Scholar] [CrossRef] [Green Version]

- Givens, G.; Dunning, R. Distributor intermediation in the farm to food service value chain. Renew. Agric. Food Syst. 2018, 34, 268–270. [Google Scholar] [CrossRef] [Green Version]

- Carter, E. Desperately seeking happy chickens: Producer dynamics and consumer politics in quality agricultural supply chains. Int. J. Soc. Econ. 2020. ahead-of-print. [Google Scholar] [CrossRef]

- Mason, C.M.; McNally, K.N. Market change, distribution, and new firm formation and growth: The case of real-ale breweries in the United Kingdom. Environ. Plan. A 1997, 29, 405–417. [Google Scholar] [CrossRef]

- Low, S.; Vogel, S. Direct and Intermediated Marketing of Local Foods in the United States. USDA-Ers Econ. Res. Rep. 2011, 128, 1–38. Available online: https://www.ers.usda.gov/webdocs/publications/44924/8276_err128_2_.pdf?v=0 (accessed on 13 February 2021). [CrossRef] [Green Version]

- Lee, B.; Liu, J.Y.; Chang, H.H. The choice of marketing channel and farm profitability: Empirical evidence from small farmers. Agribusiness 2020, 36, 402–421. [Google Scholar] [CrossRef]

- Bond, J.; Thilmany, D.; Bond, C. What influences consumer choice of fresh produce purchase location? J. Agric. Appl. Econ. 2009, 41, 61–74. [Google Scholar] [CrossRef] [Green Version]

- Gumirakiza, J.; Curtis, K.; Bosworth, R. Who attends farmers’ markets and why? Understanding consumers and their motivations. Int. Food Agribus. Manag. Rev. 2014, 17, 65–82. [Google Scholar]

- Maples, M.; Morgan, K.; Interis, M.; Harri, A. Who buys food directly from producers in the Southeastern United States? J. Agric. Appl. Econ. 2013, 45, 509–518. [Google Scholar] [CrossRef] [Green Version]

- Thilmany, D.; Bond, C.; Bond, J. Going local: Exploring consumer behavior and motivations for direct food purchases. Am. J. Agric. Econ. 2008, 90, 1303–1309. [Google Scholar] [CrossRef]

- Detre, J.; Mark, T.; Mishra, A.; Adhikari, A. Linkage between direct marketing and farm income: A double-hurdle approach. Agribusiness 2011, 27, 19–33. [Google Scholar] [CrossRef]

- Wojtyra, B.; Kossowski, T.M.; Březinová, M.; Savov, R.; Lančarič, D. Geography of craft breweries in Central Europe: Location factors and the spatial dependence effect. Appl. Geogr. 2020, 124, 102325. [Google Scholar] [CrossRef]

- Gatrell, J.D.; Nemeth, D.J.; Yeager, C.D. Sweetwater, mountain springs, and Great lakes: A hydro-geography of beer brands. In The Geography of Beer, Regions, Environment, and Societies; Patterson, M., Hoalst-Pullen, N., Eds.; Springer: Berlin/Heidelberg, Germany, 2014; pp. 89–98. [Google Scholar]

- Elzinga, K.G.; Tremblay, C.H.; Tremblay, V.J. Craft beer in the United States: History, numbers, and geography. J. Wine Econ. 2015, 10, 242–274. [Google Scholar] [CrossRef] [Green Version]

- Baginski, J.; Bell, T.L. Under-tapped?: An analysis of craft brewing in the southern United States. Southeast. Geogr. 2011, 51, 165–185. [Google Scholar] [CrossRef]

- Hungarian Central Statistical Office. Agglomerációk, Településegyüttesek. Available online: www.ksh.hu/docs/hun/xftp/idoszaki/mo_telepuleshalozata/agglomeracio.pdf (accessed on 13 February 2021).

- Akben-Selcuk, E. Does Firm Age Affect Profitability? Evidence from Turkey. Int. J. Econ. Sci. 2016, 3, 1–9. [Google Scholar] [CrossRef]

- Hopenhayn, H.A. Entry, exit and firm dynamics in long run equilibrium. Econometrica 1992, 60, 1127–1150. [Google Scholar] [CrossRef]

- Fertő, I.; Fogarasi, J.; Major, A.; Podruzsik, S. The Emergence and Survival of Microbreweries in Hungary. In Economic Perspectives on Craft Beer; Palgrave Macmillan, 1st ed.; Palgrave Macmillan: Cham, Switzerland, 2018; pp. 211–228. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Econometric Analysis of Cross Section and Panel Data; MIT Press: Cambridge, MA, USA, 2002; Volume 108. [Google Scholar]

- Choi, I. Unit root tests for panel data. J. Int. Money Financ. 2001, 20, 249–272. [Google Scholar] [CrossRef]

- Driscoll, J.C.; Kraay, A.C. Consistent covariance matrix estimation with spatially dependent panel data. Rev. Econ. Stat. 1998, 80, 549–560. [Google Scholar] [CrossRef]

- Brewers of Europe. European Beer Trends. Available online: https://brewersofeurope.org/uploads/mycms-files/documents/publications/2019/european-beer-trends-2019-web.pdf (accessed on 11 December 2020).

- Hungarian Central Statistical Office. Sörmérleg. Available online: https://www.ksh.hu/docs/hun/xstadat/xstadat_hosszu/elm12.html (accessed on 22 December 2020).

- Pécsi Sörfőzde Zrt. Available online: https://pecsisor.hu (accessed on 5 November 2020).

- Belyaeva, Z.; Rudawska, E.D.; Lopatkova, Y. Sustainable business model in food and beverage industry-a case of Western and Central and Eastern European countries. Br. Food J. 2020, 122, 1573–1592. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable | Description | Data Source | Expected Sign |

|---|---|---|---|

| Dependent | |||

| lnturn | the logarithm of the brewery′s turn-over, expressed in Euro | M and A Research Catalyst (2018) | |

| lnEBIT | the logarithm of the brewery′s EBIT, expressed in Euro | M and A Research Catalyst (2018) | |

| lnProfit | the logarithm of the brewery′s EBIT, expressed in Euro | M and A Research Catalyst (2018) | |

| Independent | |||

| FBlike | number of the brewery′s Facebook likes (30 June 2020) | own data collection from the companies site | + |

| OwnPub | dummy variable, =1 if the brewery has its own pub, 0 otherwise | own data collection | + |

| lnDistanceBP | the distance of the brewery head-quarters from Budapest in kilometre | own data collection | - |

| BreweryAge | the number of closed business years | M and A Research Catalyst (2018) | + |

| TaxReduction | dummy variable, =1 if a reduced tax applied for microbreweries in the given year, 0 otherwise | own data collection | + |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| Simple OLS | xtpcse | xtscc | |

| lnturn | lnturn | lnturn | |

| FBlike | 0.000112 ** | 0.000112 *** | 0.000112 * |

| (4.85 × 10−5) | (3.92 × 10−5) | (5.04 × 10−5) | |

| OwnPub | 0.796 *** | 0.796 *** | 0.796 *** |

| (0.263) | (0.220) | (0.225) | |

| lnDistanceBP | −0.0219 | −0.0219 | −0.0219 |

| (0.105) | (0.0833) | (0.115) | |

| BreweryAge | 0.0428 *** | 0.0428 *** | 0.0428 *** |

| (0.0150) | (0.00892) | (0.0104) | |

| TaxReduction | 0.713 ** | 0.713 ** | 0.713 ** |

| (0.301) | (0.296) | (0.236) | |

| Constant | 8.483 *** | 8.483 *** | 8.483 *** |

| (0.566) | (0.395) | (0.342) | |

| Observations | 421 | 421 | 421 |

| R-squared | 0.070 | 0.070 | 0.070 |

| Number of groups | 79 | 79 |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| Robust OLS | xtpcse | xtscc | |

| lnEBIT | lnEBIT | lnEBIT | |

| FBlike | 0.000154 *** | 0.000154 *** | 0.000154 *** |

| (0.000) | (0.000) | (0.000) | |

| OwnPub | 0.527 ** | 0.527 *** | 0.527 *** |

| (0.255) | (0.162) | (0.162) | |

| lnDistanceBP | −0.170 * | −0.170 ** | −0.170 ** |

| (0.0917) | (0.0685) | (0.0685) | |

| BreweryAge | 0.0256 * | 0.0256 *** | 0.0256 *** |

| (0.0149) | (0.00765) | (0.00765) | |

| TaxReduction | 0.758 ** | 0.758 *** | 0.758 *** |

| (0.365) | (0.266) | (0.266) | |

| Constant | 7.658 *** | 7.658 *** | 7.658 *** |

| (0.564) | (0.344) | (0.344) | |

| Observations | 259 | 259 | 259 |

| R-squared | 0.115 | 0.115 | 0.115 |

| Number of TaxID | 65 | 65 |

| xtpcse | (1) | (2) | (3) |

|---|---|---|---|

| Variables | simple OLS | xtpcse | xtscc |

| lnProfit | lnProfit | lnProfit | |

| FBlike | 0.000177 *** | 0.000177 *** | 0.000177 *** |

| (0.000) | (0.000) | (0.000) | |

| OwnPub | 0.439 | 0.439 ** | 0.439 |

| (0.284) | (0.210) | (0.252) | |

| lnDistanceBP | −0.162 | −0.162 * | −0.162 |

| (0.110) | (0.0897) | (0.0914) | |

| BreweryAge | 0.0110 | 0.0110 | 0.0110 |

| (0.0159) | (0.0141) | (0.0166) | |

| TaxReduction | 0.931 *** | 0.931 *** | 0.931 *** |

| (0.342) | (0.228) | (0.193) | |

| Constant | 7.394 *** | 7.394 *** | 7.394 *** |

| (0.599) | (0.312) | (0.265) | |

| Observations | 254 | 254 | 254 |

| R-squared | 0.124 | 0.124 | 0.124 |

| Number of TaxID | 65 | 65 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jantyik, L.; Balogh, J.M.; Török, Á. What Are the Reasons Behind the Economic Performance of the Hungarian Beer Industry? The Case of the Hungarian Microbreweries. Sustainability 2021, 13, 2829. https://0-doi-org.brum.beds.ac.uk/10.3390/su13052829

Jantyik L, Balogh JM, Török Á. What Are the Reasons Behind the Economic Performance of the Hungarian Beer Industry? The Case of the Hungarian Microbreweries. Sustainability. 2021; 13(5):2829. https://0-doi-org.brum.beds.ac.uk/10.3390/su13052829

Chicago/Turabian StyleJantyik, Lili, Jeremiás Máté Balogh, and Áron Török. 2021. "What Are the Reasons Behind the Economic Performance of the Hungarian Beer Industry? The Case of the Hungarian Microbreweries" Sustainability 13, no. 5: 2829. https://0-doi-org.brum.beds.ac.uk/10.3390/su13052829