Carbon Emission Regulation, Green Boards, and Corporate Environmental Responsibility

1

School of Business Administration, Ulsan National Institute of Science and Technology, 50 UNIST-gil, Ulsan 44919, Korea

2

Department of Urban and Environmental Engineering, Ulsan National Institute of Science and Technology, 50 UNIST-gil, Ulsan 44919, Korea

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(8), 4463; https://0-doi-org.brum.beds.ac.uk/10.3390/su13084463

Submission received: 12 March 2021

/

Revised: 9 April 2021

/

Accepted: 13 April 2021

/

Published: 16 April 2021

(This article belongs to the Special Issue Towards Sustainability: Energy and Carbon Efficiency)

Abstract

:In this study, we examine various effects of carbon emission regulation enacted in South Korea. We provide empirical evidence of regulated firms strategically hedging against potential risks by increasing the number of directors with environment-related backgrounds. We also find that this relationship is clearly evidenced when the firm is owned by a lower proportion of foreign investors. Further analysis shows that these directors successfully change their firms to become environmentally friendly. Overall, we conclude that the role of governments in promoting green finance is crucial. The findings of this study may be used as a guideline for decision makers and environmental policymakers to create systems and policies to increase the firm’s awareness about the environment in relation to corporate environmental responsibility (CER) ratings of firms.

1. Introduction

Being environmentally responsible is becoming more important for sustainable growth at both firm and national levels. To effectively reduce greenhouse gases (GHGs), the South Korean government enacted a comprehensive law that compels all firms, regardless of their financial status, to disclose their GHG emission to the public if it exceeded 125,000; 87,500; and 50,000 tons of carbon dioxide equivalent (tCO2-eq) in 2011, 2012, and 2014, respectively. The South Korean government enacted the Framework Act on Low-Carbon, Green Growth in 2010, whereby, in accordance with Article 42 (6), the Minister of Environment issued comprehensive policy measures as the Principles of Target Management for Greenhouse Gases and Energy. The law is established to regulate and reduce firms’ GHG emissions. In addition to the emission history disclosure, firms are regularly monitored by government agencies and are given emission guidelines that should be followed. Therefore, regulated firms are exposed to a number of risks, for example, disclosing previously confidential information about their emissions and their manufacturing details to third parties may result in negative environmental publicity.

However, navigating regulations is difficult as many firms encounter these environmental regulations for the first time, and board members may not be familiar with such laws. Therefore, regulated firms have higher incentives to hire CEOs and directors who have work or academic experience in environment-related fields—hereinafter, we define these as green CEOs and green directors, as components of green boards. Directors’ prior experiences are well reflected in their management styles [1,2]. As green CEOs and directors would have higher level of knowledge of GHG emissions and policies related to them, they may be able to navigate the regulations. Ultimately, they may enhance a firm’s competitive advantage in corporate environmental responsibility (CER).

Therefore, in this study, we investigate the extent to which the compliance with environmental regulations, which compels firms to disclose their emissions data, affects the composition of the boards of these firms. Since green CEOs and green directors constitute environment-field-related expertise, we hypothesize that their management style may be reflected in a firm’s corporate environmental responsibility (CER) performance metrics. If the corporate decisions by newly hired green CEOs or directors are towards firm’s green growth, then the government agencies such as the Korea Corporate Governance Service (KCGS) would note such changes thus reflect on the Corporate Social Responsibility (CSR) grade.

Quantitatively measuring the level of CER or CSR engagement is difficult. Therefore, this study uses firm-level CER and CSR scores from the KCGS database to proxy them. Prior studies often use the KCGS database to measure a firm’s CSR level (Kim, 2009 [1]). The data source provides a firm’s CER scores from grade “D” to grade “A+.” KCGS provides CER scores of all KOSPI exchange listed firms and some companies listed on the KOSDAQ exchange. For KOSDAQ listed firms, KCGS evaluates their CER level if institutions inquire. Furthermore, to mitigate the subjectivity issue, KCGS uses various sources, such as corporate disclosure information, supervisory authority reports, government reports, and news data. In addition, KCGS tries to meet international standards, such as the Organisation for Economic Co-operation and Development (OECD) corporate governance principles and ISO26000, as well as the Korean law. Therefore, prior studies examining the Korean CSR or CER often use the KCGS database [3].

Regression analysis shows that regulated firms would be more likely to hire both green CEOs and green directors. We further show that such relationships manifest when there is lower proportion of foreign institutional ownership. Employing a propensity score matching (PSM) approach [4], we confirm that the relationship does not occur due to endogeneity.

Hereinafter, we assess the effectiveness of green CEOs and directors as factors influencing the firm’s attitude toward CER. The extensive literature commonly postulates that managing CER is beneficial. For example, prior studies show that environmental management positively affects the future performance of firms [5,6,7], reduces the cost of equity [8], and improves corporate innovation [9]. However, there is very little investigation of mechanisms that influence positive CER management. Thus, we test whether green boards successfully lead a firm’s attitude toward CER and report that the proportion of green boards is positively associated with a firm’s attitude toward CER, as measured by CER ratings.

This study makes clear contributions to the literature. While there are many studies on the effects of environmental regulation on financial and operational performance of firms [10,11,12] or on corporate disclosure to develop an environmental strategy [13,14], studies on how regulation influences the composition of board characteristics are limited. Thus, our study contributes to the existing literature by, first, identifying an additional possible outcome of environmental regulations. Second, we highlight the role of governments as their sanctions positively induce firms to have higher awareness of green finance.

2. Literature Review and Hypothesis Development

Classic theories emphasize firm-level or industry-level explanations as primary determinants of firm’s policies and decisions [15,16,17]. Typical example is the trade-off between the tax deductibility and bankruptcy costs. However, recent evidence began to note what has not been clearly predicted in the traditional theories [18]. Studying the role of manager’s behavior and its effects on corporate decisions is an example. A growing literature highlights the importance of the board members for a firm’s policies [19,20,21,22,23]. Bertrand and Schoar (2003) [19] investigate whether individual managers affect corporate behavior. The article finds that managers from earlier birth cohorts appear on average to be more conservative, and that managers who hold an MBA degree seem to more aggressively seek managers.

Benmelech and Frydman (2015) [1] analyze the relationship between military service of managers and their decisions, financial policies, and outcomes. The authors provide empirical evidence that military service is associated with conservative behavior and conservative corporate policies. Furthermore, they also find that those managers are less likely to engage in corporate investment or corporate fraudulent activities.

Similarly, Cain and McKeon (2016) [2] and Sunder et al. (2017) [23] use a unique pilot license status data to show that managers’ hobbies of flying airplanes are positively associated with the firm’s innovation (Sunder et al., 2017). In addition, Cain and McKeon (2016) [2] show that firms led by those managers have higher equity return volatility above the amount explained by compensation components. A proliferating literature focuses on how managers’ prior experiences affect corporate policies such as leverage [21], corporate innovation [23]. However, not many have observed the effects of managers’ prior experiences in environmental related fields and their future decisions.

Regarding the literature on CER, a vast literature has underscored the importance of CER. Especially, environmental responsibility is an important research topic for sustainable growth [24,25,26]. Prior studies have well examined how environment-related risks affect societies. For instance, Vesalon et al. (2013) [27] examine the environmental risk involved in a proposed gold-mining project and find that environmental risk has a socially constructed horizon and that counter-discourses on risk represent a fundamental contribution of the environmental protesters to the anti-mining movement. Furthermore, Shahzad et al. (2020) [28] find that CSR practices have a significant influence on environmentally sustainable development. Authors argue that CSR activities should be embedded in the organizational environmental strategies for green innovation since CSR dimensions have positive relations with environmentally sustainable development.

Studies thus highlight the importance of policies that could enhance the level of environmental responsibility and also mitigate the climate issues. For instance, Eitan (2021) [29] find that policymakers tend to focus on promoting mitigation strategy rather than an adaptation strategy. The findings shed light on the important role of international influence which tends to emphasize mitigation over adaptation. Furthermore, May Tan-Mullins and Mohan (2013) [30] argue that since the environmental protection is weak in developing countries, there is a need for governments to create a legislative and institutional framework. It is also important to examine the effectiveness of the environmental regulation. Masud et al. (2018) [31] show that banking companies disclosed more green information in line with environmental regulation.

A strand of studies has shown that being environmentally responsible positively affects firm performance [32,33,34,35,36,37,38,39,40,41,42,43,44], and innovation [45]. For instance, Deng and Cheng (2019) [41] find that CER and stock market performance has a positive correlation. In addition, researchers found that CER contributes to lowering a firm’s information risk [46], increases firm risk [47,48], enhances value of shareholders [49], and increases board diversity [50]. However, there also exists studies that ESG activities negatively affect firm performance [51]. For instance, Kim and Lee (2020) criticized the overinvestment behavior to maintain certain ESG performance [52]. There are also researchers that maintain a neutral view on firm’s CER engagement. Chapple et al. (2005) [53] finds that CER strength does not affect firm performance. Kim and Statman (2012) [54] insist that corporation control CER activities consistent with the interest of shareholders.

While studies on examining the effects of CER are proliferating, relatively less attention has been given to investigating factors that drive such decisions. Previous research shows that corporate governance structure [55], board of directors affects the ESG performance [56], institutional ownership structure [57], and outside directors such as corporate social responsibility (CSR) committees also have positive effects on ESG performance [58]. Furthermore, several researchers have shown that environmental regulations [59], business leaders’ governmental intervention [60], religion [61], and lowering financial constraints [62] promote CER decisions. On the other hand, few researchers insist that government has responsibility to encourage corporations to engage in CER [63,64].

Based on prior studies on board characteristics and CER, there is a gap between those two strands of literature. Therefore, this research aims to first show how firms respond to environmental regulations and second show how board diversity, especially a board’s experiences related to its environment, can explain the variation in the CER performances. To formally put the two hypotheses:

Hypothesis 1.

(Other things being equal) Environment regulation induces firms to increase the proportion of green CEOs and green directors.

Hypothesis 2.

(Other things being equal) The proportion of green CEOs and directors is positively associated with CER.

3. Data and Methodology

3.1. Environmental Regulation Data

The regulations compelling those firms emitting GHGs in excess of 125,000 tCO2-eq in disclosing their emission information were enacted in 2010. The emission information is made public in the annual business reports (comparable to the 10-K in the United States of America), which are available from the DART database (comparable to the EDGAR database in the United States of America). We manually transcribe this emissions information from these annual reports.

3.2. Green Boards Data

We identify green CEOs and green directors using the TS2000 database. This database provides information on the education and work experience of CEOs and directors of public firms. We define a green CEO as an indicator variable with an assigned value of one where the CEO has either educational or prior work experiences in an environment-related area. Similarly, we define a green director as a continuous variable with an assigned value equal to the proportion of green directors of the total number of directors.

3.3. CER Rating Data

In many cases, researchers overcome the difficulties of quantitatively measuring the level of CER engagement by using proxy measurements. The Korea Corporate Governance Service (KCGS) database provides an annual CER score for each firm.

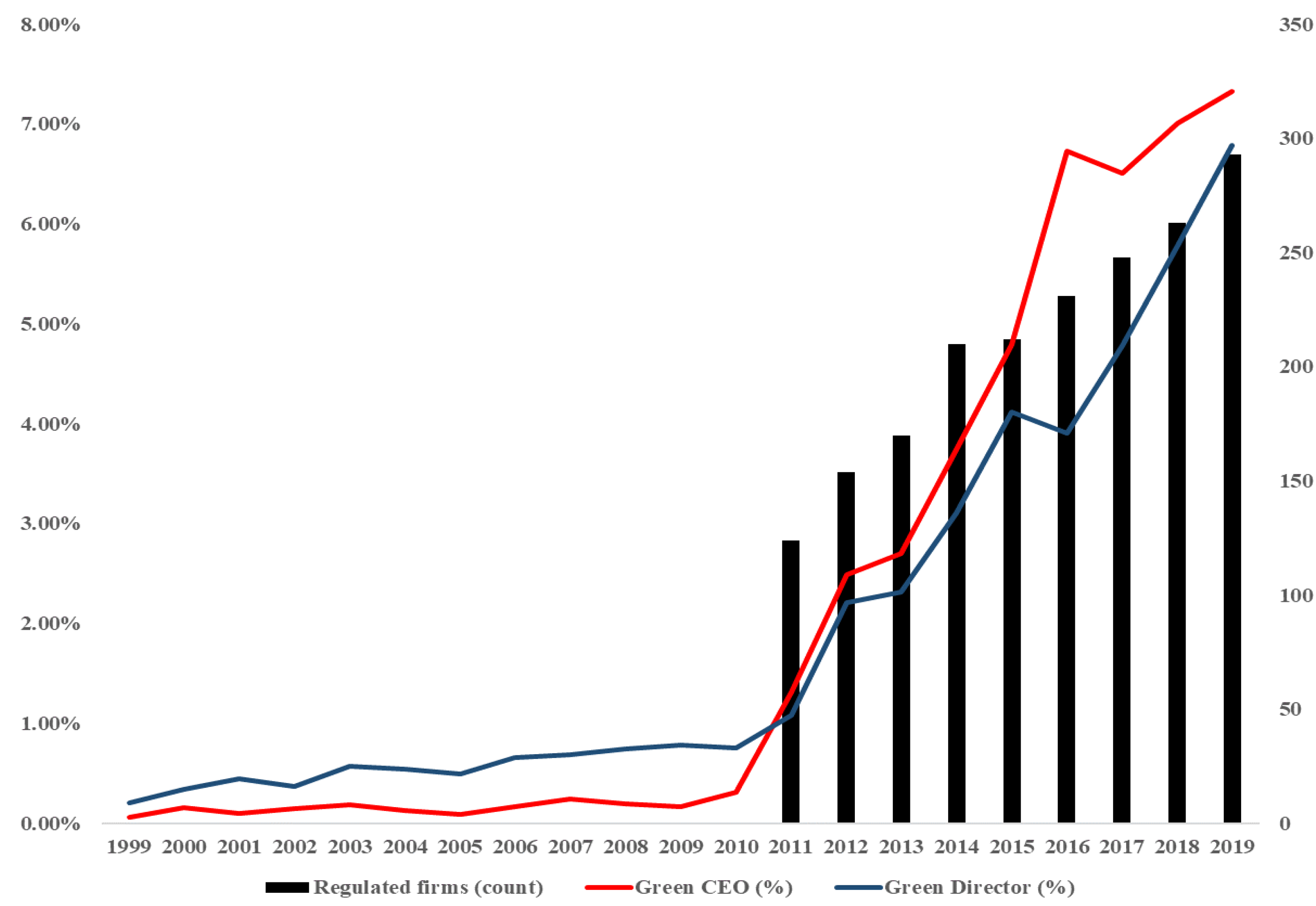

Figure 1 illustrates the green CEO ratio, green director ratio, and the number of regulated firms annually. Note that both the green CEO and green director ratios have increased significantly after enactment of the environmental regulation in 2010. Furthermore, we find that the number of regulated firms also increased because of the stricter emission restriction enacted in 2012 and 2014.

3.4. Control Variables

In addition, we add a number of variables to control for unobserved heterogeneity. These include log(assets), Tobin’s q, log(sales), asset tangibility, leverage, cash, and cash flow. Furthermore, we employ year and industry fixed effects throughout. All errors are clustered for each firm.

3.5. Sample

Although the regulation was enacted in 2010, our final dataset spans from 2012 to 2019 to observe the effects of the regulation after the enactment by lagging all control variables. Furthermore, we limited the data to those of manufacturing firms to which the law exclusively applies. Thus, the data sample comprised 10,240 firms’ financial year observations. All variables and their sources are provided in Table 1.

4. Main Results

4.1. Descriptive Statistics

The descriptive statistics are presented in Table 2. Panel A reports summary statistics for non-regulated firms, and Panel B provides information of regulated firms. By comparison, it should be noted that, on average, compared to non-regulated firms, regulated firms have a higher number of green CEOs and directors. Furthermore, we found that the average CER scores of regulated firms are higher than those of non-regulated firms. However, the differences in the interpretation of the results obtained through a univariate analysis may be ascribed to bias resulting from other, unobserved variables. Therefore, we employed the regression analysis model with a number of control variables and fixed effects to further test our hypotheses.

4.2. Regulation and the Green Board

4.2.1. Baseline Regression Results

In this subsection, we employ a logistic regression and pooled ordinary least squares (OLS) estimation method to test for the relation between the environmental regulation and the board diversity. Thereafter, we use PSM to match the potential effects of endogeneity.

The estimation result is reported in Panel B of Table 3. Column (1) provides the result for the green CEOs, and Column (2) shows the result for the green directors. We found that regulated firms are 56.9% more likely to be managed by green CEOs and have a 2% higher proportion of green directors when compared with non-regulated firms.

We then employ PSM to dilute the effects of endogeneity. PSM quantifies the sensitivity of the results for the primary causal variable to unobserved correlated omitted variables [65]. First, we perform a logit regression on the regulation indicator variable. Thereafter, we selected all control variables to balance the confounding factors in the matching procedure. Panel A of Table 3 provides the matching result. It should be noted that the differences between the treatment and comparison groups are statistically insignificant for all variables, indicating that the samples are well matched. The regression analysis results using PSM are presented in Columns (3) and (4) of Panel B. We found that the regulation has a positive effect on the proportional composition of green boards. Overall results indicate that firms respond to the environmental regulations strategically. As a short-term measure, firms hire green CEOs and directors with the assumption that they will manage compliance with the regulations efficiently and increase their CER.

4.2.2. Effects of the Foreign Investors

In this subsection, we test for the effects of monitoring by foreign investors. In previous studies, it is generally accepted that foreign investors in emerging markets seek out short-term investments [66,67]. As environmental projects are often long term, a higher proportion of foreign shareholders may discourage the firms from hiring green CEOs and green directors.

The results of the analysis are presented in Table 4. As CEOs are considerably important people in firms [19,68], the board would be motivated to recruit green CEOs under the regulations. However, short-term investors such as foreign investors may discourage firms from hiring green CEOs. To test the effects of foreign institutional investors on firm’s willingness to employee green CEOs and green directors, we employed an interaction term analysis where we interacted the regulation status dummy and foreign ownership variable. Our findings concur with those of previous studies in that the likelihood of firms hiring green CEOs is evidenced only in firms managed by foreign minority investors. These results indicate that short-term investors will encourage firms to focus on short-term projects.

4.3. Green Boards and CER Rating

Our second hypothesis is explained by investigating the role of the green board in improving corporate CER competitiveness. It is assumed that the expectation for regulated firms in hiring green CEOs or directors is the improvement of their competitive advantage through CER. Therefore, we assessed the impact of green boards through an empirical analysis of CER scores.

The results of our analysis are shown in Table 5. As CER is graded alphabetically (“A+” and “D”), adopting a pooled OLS regression is not an appropriate method for analysis. Therefore, we used a rank ordered logistic regression, which finds popular acceptance as a method of analysis using sequential variables [69,70]. Columns (1) and (2) show that both green CEOs and green directors increase the CER rating of firms, and Columns (4) and (5) show that green CEOs and green directors are also able to increase the overall CSR score. Interesting result emerged when we ran the regression again using a new variable that indicated that firms that hire both green CEO and green director. Results show that hiring both green CEO and green director in the same year resulted in higher increment in both CER and CSR scores compared to cases where we hired only green CEO or green director. This implies that when both the CEO and directors have a common environment-related background, there exists a synergistic effect that positively affects firm’s CER performance. Overall results indicate that green CEOs and directors impact the CER competitive advantage of firms.

5. Discussion and Conclusions

This study identified the advantages of green finance under the exogenous environmental regulation in South Korea. Unlike previous studies that investigated the effects of regulation on financial or operational performance, we focused on the internal organization of firms. Analysis results show that regulated firms respond to regulations strategically by increasing the proportion of green CEOs and directors. We also examined the role of green CEOs and directors, especially in relation to the CER ratings of firms, and found that green boards succeed in raising the CER ratings of firms. This implies that the regulated firm’s decision to recruit green CEOs and directors as a hedge against the risks of disclosure is successful.

Being environmentally responsible is becoming an important question and task worldwide. Global warming is now a significant factor that needs to be seriously considered. Prior literature has mostly focused on examining the roles of government-level policies and how the introduction of such policies affects global warming. At the same time, it is also important to recognize how companies respond to such policies and changes. Our first finding that companies increase the proportion of green CEOs and directors in response to environmental regulations implies that firms view environmental risk as one of the key risks they have to tackle. Since environmental risk differs from other conventional risks, firms hire managers with a background in environment-related fields. Furthermore, another finding that such firms managed by green managers are more environmentally responsible is encouraging and has policy implications. Prior studies have commonly argued that CER is beneficial for a firm’s sustainable growth. Since our research has shown that hiring green managers benefits firms in multiple ways, policymakers may use this research to design policies that may help firms to hire green managers. Furthermore, the findings of this study may also be used as a guideline for decision makers and environmental policymakers to create systems and policies to increase the firm’s awareness about the environment in relation to CER ratings of firms. Specifically, we emphasize the role of governments in promoting greener production as our results show that the regulation effectively diversifies a firm’s board characteristics and attitude toward green finance.

One clear limitation of the research is on the data. While we were able to obtain the Korean listed firms’ managerial background and information such as their education level and prior work experience, we could not get access to non-listed firms’ data. Since the TS2000 database, which we used to obtain the education and work experience status, updates the information for publicly listed firms, we were not able to access information about other firms. This lack of the data leads to the potential future research. If the data of non-listed firms is available, researchers could compare how small-and-medium sized non-listed firms respond to publicly listed firms. Listed firms are generally larger in size and profitability compare to non-listed firms. Therefore, the statistically significant relationship we have investigated using the data sample of listed firms may not be observed for non-listed firms. Then, this would also imply that governments should impose different policies and sanctions for small-and-medium sized companies.

Author Contributions

Conceptualization, H.J., S.S., and C.-K.S.; methodology, H.J.; software, H.J.; validation, S.S. and C.-K.S.; formal analysis, S.S. and C.-K.S.; investigation, S.S. and C.-K.S.; resources, C.-K.S.; data curation, S.S.; writing—original draft preparation, H.J. and S.S.; writing—review and editing, C.-K.S.; visualization, S.S.; supervision, C.-K.S.; project administration, C.-K.S.; funding acquisition, C.-K.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research is supported by the 2021 Research Fund of UNIST (Ulsan National Institute of Science and Technology) (1.210106.01), and Korea Environment Industry & Technology Institute(KEITI) through Public Technology Program based on Environmental Policy Program, funded by Korean Ministry of Environment (2019000160002).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data is available upon any reasonable requests. Please email the corresponding author ([email protected]).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Benmelech, E.; Frydman, C. Military CEOs. J. Financ. Econ. 2015, 117, 43–59. [Google Scholar] [CrossRef]

- Cain, M.D.; McKeon, S.B. CEO personal risk-taking and corporate policies. J. Financ. Quant. Anal. 2015, 51, 139–164. [Google Scholar] [CrossRef] [Green Version]

- Lee, J.; In, F.; Khil, J.; Park, Y.S.; Wee, K.W. Determinants of Shareholder Activism of the National Pension Fund of Korea. Asia-Pac. J. Financ. Stud. 2018, 47, 805–823. [Google Scholar] [CrossRef]

- Armstrong, C.S.; Jagolinzer, A.D.; Larcker, D.F. Chief Executive Officer Equity Incentives and Accounting Irregularities. J. Acc. Res. 2010, 48, 225–271. [Google Scholar] [CrossRef] [Green Version]

- Miles, M.P.; Covin, J.G. Environmental Marketing: A Source of Reputational, Competitive, and Financial Advantage. J. Bus. Ethics 2000, 23, 299–311. [Google Scholar] [CrossRef]

- Konar, S.; Cohen, M.A. Does the Market Value Environmental Performance? Rev. Econ. Stat. 2001, 83, 281–289. [Google Scholar] [CrossRef]

- Derwall, J.; Guenster, N.; Bauer, R.; Koedijk, K. The eco-efficiency premium puzzle. Financ. Anal. J. 2005, 61, 51–63. [Google Scholar] [CrossRef] [Green Version]

- El Ghoul, S.; Guedhami, O.; Kim, H.; Park, K. Corporate environmental responsibility and the cost of capital: International evidence. J. Bus. Ethics 2018, 149, 335–361. [Google Scholar] [CrossRef]

- Lv, M.; Bai, M. Evaluation of China’s carbon emission trading policy from corporate innovation. Financ. Res. Lett. 2020, 39, 101565. [Google Scholar] [CrossRef]

- Sarkis, J.; Cordeiro, J.J. An empirical evaluation of environmental efficiencies and firm performance: Pollution prevention versus end-of-pipe practice. Eur. J. Oper. Res. 2001, 135, 102–113. [Google Scholar] [CrossRef]

- Testa, F.; Iraldo, F.; Frey, M. The effect of environmental regulation on firms’ competitive performance: The case of the building & construction sector in some EU regions. J. Environ. Manag. 2011, 92, 2136–2144. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, J.; Xue, Y.; Yang, J. Impact of environmental regulations on green technological innovative behavior: An empirical study in China. J. Clean. Prod. 2018, 188, 763–773. [Google Scholar] [CrossRef]

- Albertini, E. A Descriptive Analysis of Environmental Disclosure: A Longitudinal Study of French Companies. J. Bus. Ethics 2013, 121, 233–254. [Google Scholar] [CrossRef]

- Lee, S.-Y. Corporate Carbon Strategies in Responding to Climate Change. Bus. Strat. Environ. 2011, 21, 33–48. [Google Scholar] [CrossRef]

- Miller, M.H. Debt and Taxes. J. Financ. 1977, 32, 261. [Google Scholar] [CrossRef]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C. The Capital Structure Puzzle. J. Financ. 1984, 39, 574–592. [Google Scholar] [CrossRef]

- Lemmon, M.L.; Roberts, M.R.; Zender, J.F. Back to the Beginning: Persistence and the Cross-Section of Corporate Capital Structure. J. Financ. 2008, 63, 1575–1608. [Google Scholar] [CrossRef]

- Bertrand, M.; Schoar, A. Managing With Style: The Effect of Managers on Firm Policies. SSRN Electron. J. 2003. [Google Scholar] [CrossRef] [Green Version]

- Graham, J.R.; Narasimhan, K. Corporate Survival and Managerial Experiences during the Great Depression. Ssrn Electron. J. 2004. [Google Scholar] [CrossRef] [Green Version]

- Malmendier, U.; Tate, G. CEO Overconfidence and Corporate Investment. J. Financ. 2005, 60, 2661–2700. [Google Scholar] [CrossRef] [Green Version]

- Bernile, G.; Bhagwat, V.; Rau, P.R. What Doesn’t Kill You Will Only Make You More Risk-Loving: Early-Life Disasters and CEO Behavior. SSRN Electron. J. 2014, 72, 167–206. [Google Scholar] [CrossRef]

- Sunder, J.; Sunder, S.V.; Zhang, J. Pilot CEOs and corporate innovation. J. Financ. Econ. 2017, 123, 209–224. [Google Scholar] [CrossRef]

- Desjardins, J. Corporate Environmental Responsibility. J. Bus. Ethics 1998, 17, 825–838. [Google Scholar] [CrossRef]

- Vãran, C.; Creţan, R. Place and the spatial politics of intergenerational remembrance of the Iron Gates displacements in Romania, 1966–1972. Area 2018, 50, 509–519. [Google Scholar] [CrossRef]

- Vesalon, L.; Crețan, R. Development-Induced Displacement in Romania: The Case of Roşia Montană Mining Project. J. Urban Reg. Anal. 2020, 4. [Google Scholar] [CrossRef]

- Vesalon, L.; Creţan, R. ‘Cyanide Kills!’ Environmental Movements and the Construction of Environmental Risk at Roşia Montană, Romania: ‘Cyanide Kills!’! Area 2013, 45, 443–451. [Google Scholar] [CrossRef]

- Shahzad, M.; Qu, Y.; Javed, S.A.; Zafar, A.U.; Rehman, S.U. Relation of environment sustainability to CSR and green innovation: A case of Pakistani manufacturing industry. J. Clean. Prod. 2020, 253, 119938. [Google Scholar] [CrossRef]

- Eitan, A. Promoting Renewable Energy to Cope with Climate Change—Policy Discourse in Israel. Sustainability 2021, 13, 3170. [Google Scholar] [CrossRef]

- Creţan, R.; Vesalon, L. The Political Economy of Hydropower in the Communist Space: Iron Gates Revisited: The Political Economy of Hydropower in the Communist Space. Tijdschr. Econ. Soc. Geogr. 2017, 108, 688–701. [Google Scholar] [CrossRef]

- Masud, A.K.; Hossain, M.S.; Kim, J.D. Is Green Regulation Effective or a Failure: Comparative Analysis between Bangladesh Bank (BB) Green Guidelines and Global Reporting Initiative Guidelines. Sustainability 2018, 10, 1267. [Google Scholar] [CrossRef] [Green Version]

- Wahba, H. Does the market value corporate environmental responsibility? An empirical examination. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 89–99. [Google Scholar] [CrossRef]

- Li, D.; Cao, C.; Zhang, L.; Chen, X.; Ren, S.; Zhao, Y. Effects of corporate environmental responsibility on financial performance: The moderating role of government regulation and organizational slack. J. Clean. Prod. 2017, 166, 1323–1334. [Google Scholar] [CrossRef]

- Xu, F.; Yang, M.; Li, Q.; Yang, X. Long-term economic consequences of corporate environmental responsibility: Evidence from heavily polluting listed companies in China. Bus. Strat. Environ. 2020, 29, 2251–2264. [Google Scholar] [CrossRef]

- Jiang, Y.; Xue, X.; Xue, W. Proactive Corporate Environmental Responsibility and Financial Performance: Evidence from Chinese Energy Enterprises. Sustainability 2018, 10, 964. [Google Scholar] [CrossRef] [Green Version]

- Testa, M.; D’Amato, A. Corporate environmental responsibility and financial performance: Does bidirectional causality work? Empirical evidence from the manufacturing industry. Soc. Responsib. J. 2017, 13, 221–234. [Google Scholar] [CrossRef]

- Dang, V.T.; Nguyen, N.; Bu, X.; Wang, J. The Relationship between Corporate Environmental Responsibility and Firm Performance: A Moderated Mediation Model of Strategic Similarity and Organization Slack. Sustainability 2019, 11, 3395. [Google Scholar] [CrossRef] [Green Version]

- Sohn, J.; Lee, J.; Kim, N. Going Green Inside and Out: Corporate Environmental Responsibility and Financial Performance under Regulatory Stringency. Sustainability 2020, 12, 3850. [Google Scholar] [CrossRef]

- Ferrero-Ferrero, I.; Fernández-Izquierdo, M.Á.; Muñoz-Torres, M.J. The Effect of Environmental, Social and Governance Consistency on Economic Results. Sustainability 2016, 8, 1005. [Google Scholar] [CrossRef] [Green Version]

- Taliento, M.; Favino, C.; Netti, A. Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe. Sustainability 2019, 11, 1738. [Google Scholar] [CrossRef] [Green Version]

- Deng, X.; Cheng, X. Can ESG Indices Improve the Enterprises’ Stock Market Performance?—An Empirical Study from China. Sustainability 2019, 11, 4765. [Google Scholar] [CrossRef] [Green Version]

- Badía, G.; Pina, V.; Torres, L. Financial Performance of Government Bond Portfolios Based on Environmental, Social and Governance Criteria. Sustainability 2019, 11, 2514. [Google Scholar] [CrossRef] [Green Version]

- Yoon, B.; Lee, J.H.; Byun, R. Does ESG Performance Enhance Firm Value? Evidence from Korea. Sustainability 2018, 10, 3635. [Google Scholar] [CrossRef] [Green Version]

- Zhao, C.; Guo, Y.; Yuan, J.; Wu, M.; Li, D.; Zhou, Y.; Kang, J. ESG and Corporate Financial Performance: Empirical Evidence from China’s Listed Power Generation Companies. Sustainability 2018, 10, 2607. [Google Scholar] [CrossRef] [Green Version]

- Wu, W.; Liang, Z.; Zhang, Q. Effects of corporate environmental responsibility strength and concern on innovation performance: The moderating role of firm visibility. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1487–1497. [Google Scholar] [CrossRef]

- Choi, D.; Chung, C.Y.; Kim, D.; Liu, C. Corporate Environmental Responsibility and Firm Information Risk: Evidence from the Korean Market. Sustainability 2019, 11, 6518. [Google Scholar] [CrossRef]

- Cai, L.; Cui, J.; Jo, H. Corporate Environmental Responsibility and Firm Risk. J. Bus. Ethics 2016, 139, 563–594. [Google Scholar] [CrossRef]

- Salama, A.; Anderson, K.; Toms, J.S. Does Community and Environmental Responsibility Affect Firm Risk? Evidence from UK Panel Data 1994–2006. Bus. Ethics 2011, 20, 192–204. [Google Scholar] [CrossRef]

- Miralles-Quirós, M.M.; Miralles-Quirós, J.L.; Hernández, J.R. ESG Performance and Shareholder Value Creation in the Banking Industry: International Differences. Sustainability 2019, 11, 1404. [Google Scholar] [CrossRef] [Green Version]

- Romano, M.; Cirillo, A.; Favino, C.; Netti, A. ESG (Environmental, Social and Governance) Performance and Board Gender Diversity: The Moderating Role of CEO Duality. Sustainability 2020, 12, 9298. [Google Scholar] [CrossRef]

- Ruan, L.; Liu, H. Environmental, Social, Governance Activities and Firm Performance: Evidence from China. Sustainability 2021, 13, 767. [Google Scholar] [CrossRef]

- Lee, J.; Kim, E. The Influence of Corporate Environmental Responsibility on Overinvestment Behavior: Evidence from South Korea. Sustainability 2020, 12, 1901. [Google Scholar] [CrossRef] [Green Version]

- Chapple, W.; Paul, C.J.M.; Harris, R. Manufacturing and corporate environmental responsibility: Cost implications of voluntary waste minimisation. Struct. Chang. Econ. Dyn. 2005, 16, 347–373. [Google Scholar] [CrossRef] [Green Version]

- Kim, Y.; Statman, M. Do Corporations Invest Enough in Environmental Responsibility? J. Bus. Ethics 2011, 105, 115–129. [Google Scholar] [CrossRef] [Green Version]

- Yang, D.; Wang, Z.; Lu, F. The Influence of Corporate Governance and Operating Characteristics on Corporate Environmental Investment: Evidence from China. Sustainability 2019, 11, 2737. [Google Scholar] [CrossRef] [Green Version]

- Birindelli, G.; Dell’Atti, S.; Iannuzzi, A.P.; Savioli, M. Composition and Activity of the Board of Directors: Impact on ESG Performance in the Banking System. Sustainability 2018, 10, 4699. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; Lozano, M.-B. The Nonlinear Relation between Institutional Ownership and Environmental, Social and Governance Performance in Emerging Countries. Sustainability 2021, 13, 1586. [Google Scholar] [CrossRef]

- Baraibar-Diez, E.; Odriozola, M.D. CSR Committees and Their Effect on ESG Performance in UK, France, Germany, and Spain. Sustainability 2019, 11, 5077. [Google Scholar] [CrossRef] [Green Version]

- Peng, B.; Tu, Y.; Wei, G. Can Environmental Regulations Promote Corporate Environmental Responsibility? Evidence from the Moderated Mediating Effect Model and an Empirical Study in China. Sustainability 2018, 10, 641. [Google Scholar] [CrossRef] [Green Version]

- Dummett, K. Drivers for Corporate Environmental Responsibility (CER). Environ. Dev. Sustain. 2006, 8, 375–389. [Google Scholar] [CrossRef]

- Du, X.; Jian, W.; Zeng, Q.; Du, Y. Corporate Environmental Responsibility in Polluting Industries: Does Religion Matter? J. Bus. Ethics 2013, 124, 485–507. [Google Scholar] [CrossRef] [Green Version]

- Goetz, M.R. Financial Constraints and Environmental Corporate Social Responsibility. Ssrn Electron. J. 2018. [Google Scholar] [CrossRef]

- He, M.; Chen, J. Sustainable Development and Corporate Environmental Responsibility: Evidence from Chinese Corporations. J. Agric. Environ. Ethics 2009, 22, 323–339. [Google Scholar] [CrossRef]

- Meng, X.H.; Zeng, S.X.; Leung, A.W.T.; Tam, C.M. Relationship between Top Executives’ Characteristics and Corporate Envi-ronmental Responsibility: Evidence from China. Hum. Ecol. Risk Assess. 2015, 21, 466–491. [Google Scholar] [CrossRef]

- Kim, C. Corporate social responsibility and firm value. Korean J. Financ. Stud. 2009, 38, 507–545. [Google Scholar]

- Choi, S.; Jung, H. Director liability reduction and stock price crash risk: Evidence from Korea. Int. Rev. Financ. 2020. [Google Scholar] [CrossRef]

- Vo, X.V. Foreign Investors and Stock Price Crash Risk: Evidence from Vietnam. Int. Rev. Financ. 2020, 20, 993–1004. [Google Scholar] [CrossRef]

- Graham, J.R.; Harvey, C.R.; Puri, M. Managerial attitudes and corporate actions. J. Financ. Econ. 2013, 109, 103–121. [Google Scholar] [CrossRef] [Green Version]

- Marden, I.J. Analyzing and Modeling Rank Data; CRC Press: Boca Raton, FL, USA, 2014. [Google Scholar]

- Punj, G.N.; Staelin, R. The choice process for graduate business schools. J. Mark. Res. 1978, 15, 588–598. [Google Scholar] [CrossRef]

Figure 1.

Green CEOs, green directors, and the number of regulated firms.

{kind=link}

Table 1.

Variable description.

| Variable Name | Description | Source |

|---|---|---|

| Green CEO | An indicator variable that equals one if the firm is managed by a CEO with an academic or work experience in environment related fields | TS2000 |

| Green Director | A proportion of directors who have academic or work experiences in environment related fields | TS2000 |

| Regulation | An indicator variable that equals one if the firm is regulated under the environment regulation act | DART |

| CER Score | Firm’s score on the environment section from the CSR score, ranging from “D” to “A+”. | KCGS |

| CSR Score | Firm’s aggregated score from the environment, social, and governance sections, ranging from “D” to “A+” | KCGS |

| Tobin’s q | Tobin’s q calculated as follows: (the market value of common stock + book value of preferred stock + (current liabilities − current assets) + long-term debts)/book value of total assets | COMPUSTAT |

| Log(sales) | Log of a firm’s sales | COMPUSTAT |

| Tangibility | Net tangible assets calculated as follows: total assets − intangible assets − total liabilities | COMPUSTAT |

| Cashflow | Free cash flow calculated as follows: net income + (depreciation/amortization) − change in working capital − capital expenditure | COMPUSTAT |

Table 2.

Descriptive statistics.

| Panel A. Non-Regulated Firms | |||||

| Obs. | Average | S.D. | Min. | Max. | |

| Green CEO | 8693 | 0.013 | 0.112 | 0 | 1 |

| Green director | 8693 | 0.001 | 0.016 | 0 | 0.467 |

| CER score | 2967 | 3.859 | 1.149 | 0 | 7 |

| Tobin’s q | 8693 | 1.335 | 1.333 | 0.038 | 55.823 |

| Log(sales) (million KRW) | 8693 | 5.151 | 0.64 | 2.379 | 8.362 |

| Tangibility (million KRW) | 8693 | 32,603.95 | 219,000 | 0 | 1.40 × 107 |

| Cashflow (million KRW) | 8693 | 11,507.05 | 121,000 | −295,000 | 1.02 × 107 |

| Panel B. Regulated firms | |||||

| Green CEO | 1547 | 0.095 | 0.293 | 0 | 1 |

| Green director | 1547 | 0.007 | 0.028 | 0 | 0.429 |

| CER score | 1249 | 4.825 | 0.977 | 0 | 7 |

| Tobin’s q | 1547 | 1.012 | 0.536 | 0.165 | 8.26 |

| Log(sales) (million KRW) | 1547 | 6.089 | 0.735 | 4.512 | 8.387 |

| Tangibility (million KRW) | 1547 | 359,000 | 951,000 | 1421.263 | 1.35 × 107 |

| Cashflow (million KRW) | 1547 | 149,000 | 693,000 | −226,000 | 1.31 × 107 |

Note. Panel A reports the descriptive statistics of non-regulated firms and Panel B provides the statistics for regulated firms. The data period spans from 2012 to 2019. Green CEO is an indicator variable, which is equal to one if the firm is managed by a CEO who has a prior job or academic experience in environment-related fields. Green director is a proportion of directors with prior job or academic experiences in environment field. CER score is a continuous variable of scores with 0 representing “D” grade and 7 representing “A+” grade. Other control variables are Log(asset), Tobin’s q, Log(sales), Tangibility, Leverage, Cash, and Cashflow.

Table 3.

Effects of the environmental regulation on the board characteristics.

| Panel A. Summary Statistics between the Treated Group and the Control Group | ||||

| Variable (Lagged) | Treated | Control | Bias | t-Statistics |

| Tobin’s q | 1.3527 | 1.6198 | −22.5 | −1.32 |

| Log(sales) | 5.7749 | 5.7656 | 1.1 | 0.15 |

| Tangibility | 4.6 × 105 | 3.5 × 105 | 10.8 | 1.47 |

| Cashflow | 2.3 × 105 | 1.9 × 105 | 16.9 | 0.42 |

| Industry | 36.138 | 37.144 | −5.6 | −0.84 |

| Year | 2015.0 | 2014.9 | 2.9 | 0.45 |

| Panel B. Results of the OLS regression with and without PSM | ||||

| (1) | (2) | (3) | (4) | |

| Variable (Lagged) | Non-PSM Green CEO | Non-PSM Green Director | PSM Green CEO | PSM Green Director |

| Regulation | 0.002 ** | 0.002 ** | 0.079 * | 0.012 * |

| (2.337) | (2.337) | (1.665) | (1.824) | |

| Tobin’s q | 0.000 | 0.000 | −0.004 | −0.001 |

| (1.076) | (1.076) | (−0.890) | (−1.449) | |

| Log(sales) | −0.001 ** | −0.001 ** | −0.006 | −0.024 *** |

| (−2.288) | (−2.288) | (−0.215) | (−6.943) | |

| Tangibility | 0.000 | 0.000 | −0.000 * | −0.000 |

| (0.986) | (0.986) | (−1.723) | (−0.272) | |

| Cashflow | −0.000 | −0.000 | 0.000 *** | 0.000 |

| (−0.573) | (−0.573) | (3.160) | (1.173) | |

| Constant | 0.010 *** | 0.010 *** | 0.524 *** | 0.192 *** |

| (3.744) | (3.744) | (3.489) | (9.731) | |

| Observations | 10,649 | 10,649 | 982 | 982 |

| Adjusted R-squared | 0.291 | 0.291 | 0.174 | 0.510 |

| Year FE | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes |

Note. This table provides the estimation result of the regression analyzing the effects of the environmental regulation on the board characteristics. Panel A reports the result of propensity score matching (PSM), and Panel B reports the regression results using the matched sample. Columns (1) and (2) show the result without PSM samples, and Columns (3) and (4) provide results of PSM samples. We used logit regressions on Columns (1) and (3). Furthermore, these results include control variables as well as industry and year fixed effects. Reported in parentheses are t-value based on standard errors clustered by firm. *, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Table 4.

Effects of the foreign institutional investors.

| (1) | (2) | |

|---|---|---|

| Variable (Lagged) | Green CEO | Green Director |

| Regulation * Foreign Ownership | −0.003 *** | −0.005 |

| −9.122 | −1.369 | |

| Observations | 10,158 | 10,649 |

| Adjusted R-squared | 0.162 | 0.01 |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

Note. This table shows the results of further analysis. The table provides subsample analysis results with before and after the emission trading scheme regulation enacted in 2014 and low and high proportion of the foreign institutional ownership (low if the stock ownership by foreign investors is below 50% and high for the rest). Furthermore, all results include control variables used in Table 3 as well as industry and year fixed effects. Reported in parentheses are t-value based on standard errors clustered by firm. * and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Table 5.

Effects of the green CEOs and directors on firm’s CER score and CSR score.

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable (Lagged) | CER | CER | CER | CSR | CSR | CSR |

| Green CEO only | 0.398 *** | 0.305 ** | ||||

| (4.470) | (2.690) | |||||

| Green director only | 3.719 ** | 2.344 *** | ||||

| (2.230) | (3.520) | |||||

| Both Green CEO & director | 4.047 ** | 6.975 *** | ||||

| (2.430) | (4.400) | |||||

| Observations | 4206 | 4206 | 4206 | 4206 | 4206 | 4206 |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

Note. This table provides the estimation result of the regression analyzing the effects of the green board on the CER score. Columns (1) and (2) provide the results for the green CEO and the green director, respectively. Columns (3) and (4) show the results for the overall CSR score, which is calculated by the sum of three categories: environmental (E), social (S), and governance (G). Furthermore, results include control variables as well as industry and year fixed effects. Reported in parentheses are t-value based on standard errors clustered by firm. ** and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Jung, H.; Song, S.; Song, C.-K. Carbon Emission Regulation, Green Boards, and Corporate Environmental Responsibility. Sustainability 2021, 13, 4463. https://0-doi-org.brum.beds.ac.uk/10.3390/su13084463

AMA Style

Jung H, Song S, Song C-K. Carbon Emission Regulation, Green Boards, and Corporate Environmental Responsibility. Sustainability. 2021; 13(8):4463. https://0-doi-org.brum.beds.ac.uk/10.3390/su13084463

Chicago/Turabian StyleJung, Hail, Seyeong Song, and Chang-Keun Song. 2021. "Carbon Emission Regulation, Green Boards, and Corporate Environmental Responsibility" Sustainability 13, no. 8: 4463. https://0-doi-org.brum.beds.ac.uk/10.3390/su13084463

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.