Taxation for a Circular Economy: New Instruments, Reforms, and Architectural Changes in the Fiscal System

1

ICEDE, CRETUS, Applied Economics Department, Faculty of Economics, Campus Norte, University of Santiago de Compostela, 15782 Santiago de Compostela, Spain

2

ICEDE (USC), Faculty of Accounting and Administration, Autonomous University of Sinaloa, 80010 Culiacán, Mexico

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(8), 4581; https://0-doi-org.brum.beds.ac.uk/10.3390/su13084581

Submission received: 15 February 2021

/

Revised: 13 April 2021

/

Accepted: 14 April 2021

/

Published: 20 April 2021

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:This article addresses fiscal policy as a key instrument for promoting the transition to a circular economy. It is based on the hypotheses that (1) the current tax system penalizes circular activities, which are generally labour intensive, as opposed to new product manufacturing activities, which are generally intensive in materials and energy, highly automated and robotized, and (2) that the environmental taxation implemented in recent decades is unable to introduce significant changes to stop climate change or keep the economy within planetary ecological limits. This article examines the basis of an alternative tax system and tax instruments for correcting the current linear economy bias and driving the transition to a circular economy. Proposals are developed for both structural and partial reforms of the fiscal system, focusing on tax measures that can be implemented in the medium or short term to boost a circular economy. More specifically, we suggest a complete redesign of the currently opaque and significant amount of tax expenditure to transform environmentally harmful tax benefits into environmentally friendly tax measures that are suitable for the circular economy.

1. Introduction

The circular economy (CE) implies a radical change with respect to the current paradigm of linear production and consumption. It requires the development of circular business models (CBMs) in productive industries, along with productive activities that extend the useful life of goods and introduce subsequent changes to consumption patterns. This is intended to reduce the consumption of material resources and energy while also reducing waste and pollution.

In the effort to promote the transition to a circular production and consumption model, all policies must integrate sustainability principles. A policy mix should also be developed that combines industrial, regulatory, R&D, and innovation instruments with environmental, fiscal, and financial policies, public purchases, etc. Work is already underway to develop specific financial instruments and even monetary policy instruments. Within this policy-mix approach, we will focus specifically on fiscal policies. Because they affect prices, fiscal policies constitute a potentially effective structural instrument for guiding markets and the behaviour of economic agents. In fact, the extensive literature on environmental policy clearly advocates market instruments based on prices and taxes [1,2,3,4,5,6,7,8,9,10,11,12,13,14,15].

The rationale for conventional environmental taxation is optimal taxation theory. In this theory the principles of a “good tax system” are equity (vertical and horizontal), economic efficiency (does not distort the allocation of free market resources), and easy administration (management efficiency). “The social planner’s goal is to choose the tax system that maximizes the representative consumer’s welfare, knowing that the consumer will respond to whatever incentives the tax system provides. […] Absent any market imperfection such as a pre-existing externality, it is best not to distort the choices of that consumer at all” [16] (pp. 148–149). This theory involves a narrow focus on individual consumer welfare and very unrealistic assumptions. It is very difficult, if not impossible, to calculate the taxes and rates that would be necessary to guarantee optimality in resource allocation and equity. On the contrary, it can be argued that any tax introduces a distortion in equity and allocation of resources [17] (pp. 265–283); the question is how much and in which direction.

It is within this optimal taxation rationale that environmental taxes are used as instruments to correct market failures derived from externalities that cause an inefficient allocation of resources. Pigou [18] was the first to formulate the relevance of taxes to internalize externalities as an ingredient of welfare economics. In this case, Pigouvian tax can increase efficiency and welfare and also raise revenue. In theory, Pigouvian taxes are considered to be pareto-efficient by equalizing tax and marginal costs; however, in reality, it is very difficult for this hypothesis to be fulfilled due to two main reasons: on the one hand, it is very difficult to calculate the economic value of externalities, and, on the other hand, in any case, it would be difficult to set a rate that can exactly compensate for these externalities [1,2]. In fact, the Baumol and Oates [1] and Baumol [2] proposal requires successive experimentation and an adjustment to the target levels, substituting a rational choice and maximizing framework for a bounded rationality and a satisfying one. Moreover, as “We do not know how to calculate the required taxes and subsidies and we do not know how to approximate them by trial and error […] it is perfectly reasonable to act on the basis of a set of minimum standards of acceptability” [2] (p. 318). This means that environmental taxes are conceived as a combination of prices and standards, designed not to achieve a pareto-efficient allocation but to achieve a pre-set arbitrary environmental target. Furthermore, this detour from the theory of optimal taxation leads to a more pragmatic approach precisely because “the level of acceptable pollution is not a question of economics, but of environmental as well as of social (particularly intergenerational) justice considerations and can be set by the government” [19] (p. 275).

Over the last few decades, the implementation of environmental taxation has been focused on the correction of negative externalities and on the Pigouvian principle of forcing polluters to internalize the cost of their negative environmental impact as damage to the public good. Increasing the costs of production or consumption that we wish to discourage is the best instrument for encouraging changes in the behaviour of agents, which reduces this type of production or consumption and thereby reduces pollution [2]. Taxes on very specific activities or consumption that generate highly polluting emissions, effluents, or residues—especially energy taxes and the carbon tax—are the most widely studied environmental tax instruments [4,5,6,13,20,21,22,23,24]. A broader debate has revolved around carbon taxation. In fact, most OECD member countries have established this carbon tax based on agreements to reduce greenhouse gas (GHG) emissions and global warming (from the 1997 Kyoto Protocol or the Paris Summit on Climate Change).

More than 100 types of green taxes based on the “polluter pays” principle (carbon emissions, fossil fuels, waste, water, etc.) are currently in force, but this proliferation does not inherently lead to a significant impact on environmental performance [25] and [26] (p. 7) found that, “over the past 15 years, environmental taxes as a proportion of GDP have decreased in 52 of the 79 countries in the OECD database and, in addition to relatively low levels of environmental taxes, global fossil fuel subsidies increased to $373 billion by 2015”. A recent joint study by the OECD, the World Bank, and the United Nations [27] (p. 22) acknowledged that, despite the progress of the last three decades, the global balance sheet remains openly unsatisfactory, and, accordingly, it is necessary to move “far beyond marginal or incremental changes in policies and behaviour”.

The modest results of that first generation of environmental taxes paved the way for new proposals [4,25,26,28,29]. The three most salient reasons for the unsatisfactory outcome—or, rather, failure—of this first generation of environmental taxes are: (1) the promotion and proliferation of numerous, scarcely relevant taxes that (2) involve a limited portion of polluting activities and (3) apply very low tax rates. Indeed, through the influence of companies and interest groups, tax rates ended up being set so low that they were ineffective at reducing emissions [30] (p. 65); [28] (p. 358 and following). “The problem is in the economy: if the tax is too moderate, it fails to remove enough fossil fuel to help the climate; but if it is high enough to actually reduce it, then business and consumers resist the tax—because without some safety cushion for business and consumers, the whole problem falls on them and they rationally resist—to save profits and jobs” [30] (p. 360). From other perspectives (e.g., the Public Choice), the conundrum for an ambitious environmental policy (e.g., significant taxation) remains the voter’s perceptions of the environmental objectives [31].

The modest results also stem from having too narrow a focus, leaving many other forms of pollution generation that impact the biosphere and the atmosphere untaxed. Along these lines, Rockström [32] and Raworth [33] have identified new planetary limits that are being seriously violated. High levels of solid and liquid waste and excessive use of natural resources alter terrestrial and marine ecosystems, water cycles, and other basic elements. These indirectly accelerate climate change by acting as pollutants that block photosynthesis and have other collateral effects on nature, human health, and the economy. Mitigating and preventing these multiple forms of pollution requires changes in public policy, particularly through taxation.

These extremely limited results, and the conviction that significant and urgent change is needed to address serious global environmental problems, necessitate more far-reaching tax changes, such as those formulated for the circular economy. To move beyond the narrow debate on standard environmental taxation, it is necessary to open up the debate on the very architecture of the tax system. The assumption here is that the transition towards the circular economy justifies a fiscal shift by significant changes in the main taxes (VAT, Corporation, Income…).

The existing taxation system penalizes labour-intensive activities, including many circular activities (e.g., repair, maintenance, reuse, recycling, and remediation services), in contrast with the resource-intensive activities of the linear economy or the (robotized) manufacture of new products. Waste and resource use could be significantly reduced by decreasing the consumption of new material and energy resources, increasing the offer and consumer demand for circular activities (e.g., reuse, repair, and maintenance) and, of course, recycling waste and returning it to the processing cycle. Undoubtedly, taxes (and subsidies) significantly affect the costs and prices of these activities [34,35,36]. According to Stahel [37], “a shift to a sustainable taxation constitutes a giant booster to multiply the benefits of a circular economy within a national economy”.

Based on the hypothesis that taxes are a key element in altering the relative prices of goods and orienting demand, this paper attempts to systematize different possible levels of fiscal policy reform for a transition towards a circular economy. The literature on potential environmental tax reform focuses primarily on the energy problem and emissions, somewhat less on resources or waste, and very little on the tax regime for circular activities and models. Furthermore, some contributions to “circular taxation” are in fact limited to the introduction of measures and instruments to penalize or discourage waste generation [38,39,40]. However, the circular economy is a new productive paradigm that goes far beyond waste management or recycling. Accordingly, this research will review the main proposals for using the tax system as a key lever for promoting the transition to a circular economy by modifying the relative prices of goods and services to favour circular options, as described by authors writing on the ecological economy and the circular economy. Through a review of their literature, we can establish the basis of a tax system that encourages a circular rather than a linear economy.

This paper is structured as follows. After a critical assessment of the theory and reality of the current environmental taxation system, we develop inputs for a framework for CE taxation. In Section 2, the circular economy is presented conceptually as a new paradigm of production and consumption, emphasizing the relevance of both the reduction in material resources and energy consumption and the extension of the lifespan of goods. Section 3 describes two main types of CE taxation schemes, including a discussion of some critical aspects, flaws, and obstacles. Section 4 contains a feasible short-term proposal to boost the transition towards a circular economy, mainly focusing on shifting tax expenditure. Section 5 contains some final remarks, highlights the main general conclusions, and gives recommendations for future research.

2. The Circular Economy

The concept of the circular economy arose as a contrast to the linear economy: a predominantly resource- and energy-intensive industrial model based on an “extract–produce–use–strip” sequence. The linear economy responds to the capitalistic economic logic of unlimited growth of production and consumption that has driven the compulsive expansion of both in the last two centuries. The linear economy has been operating as if the planet had no ecological limits, neither in terms of resources nor in terms of impacts, but this model ends up being unsustainable for the biosphere and society itself [11,28,41].

The circular economy is a productive paradigm that emphasizes the regenerative capacity of the ecosystem, minimising the consumption of non-renewable resources, prolonging the useful life of goods, and reusing all materials that enter the economic cycle, to minimize waste and emissions [37,42,43,44,45,46,47]. According to Vence and Pereira [48] (p. 3), “the specific objective of the circular economy is to reduce the consumption of resources and energy and reduce waste through the perpetual return of resources within the economy. All resources incorporated into the economic cycle must be managed as permanent and renewable resources.” Because the circular economy concept is a work in progress, no general consensus exists regarding its principles and scope. For example, Kirchherr et al. [49] studied 114 different definitions, codified into 17 dimensions. Conceptualizations depend on the degree of generality, the phase of the production–consumption chain on which the focus is placed, and the theoretical frame of reference, among other factors.

This great diversity of CE concepts can be organized into two major groups [46,50]. On the one hand are those that emphasize the long cycles of materials and molecules, focusing on the optimization of use, full recovery, and continuous reincorporation into the production cycle (what Stahel calls the “Era of D”). On the other hand are those that emphasize the short cycles of products and focus on extending their useful life and functionality (the “Era of R”: Reuse, Repair, Remanufacture).

One representative version from the first group starts with the “Cradle to Cradle” (C2C) concept of McDonough and Braungart [51], which is articulated around three ideas or principles: (a) “Waste equals food”: materials circulate in biological (organic, biodegradable) or technological cycles, which are never wasted in landfill or destroyed, but constantly reused; (b) “Respect for diversity”: natural (biodiversity), cultural, or local forms of knowledge and production; and (c) Income from the use of solar energy and other forms of unlimited renewable energy (wind, kinetic, endomotive, etc.). The emphasis on materials goes far beyond use efficiency or recycling, which normally implies the degradation of material properties in downcycling. In fact, CE proponents tend to be critical of dominant approaches to sustainability that focus on optimization, eco-efficiency, waste, and recycling (official policies in the EU or China), because they reduce damage rather than eliminating it. The same applies to bioeconomics, which advocates burning organic resources as a “green” technique for limited energy use. In contrast to this approach, which is highly focused on recycling, the circular economy proposes production systems in which materials maintain their value and are constantly reused rather than degraded. The optimal way to achieve this is to keep the products containing those materials in use.

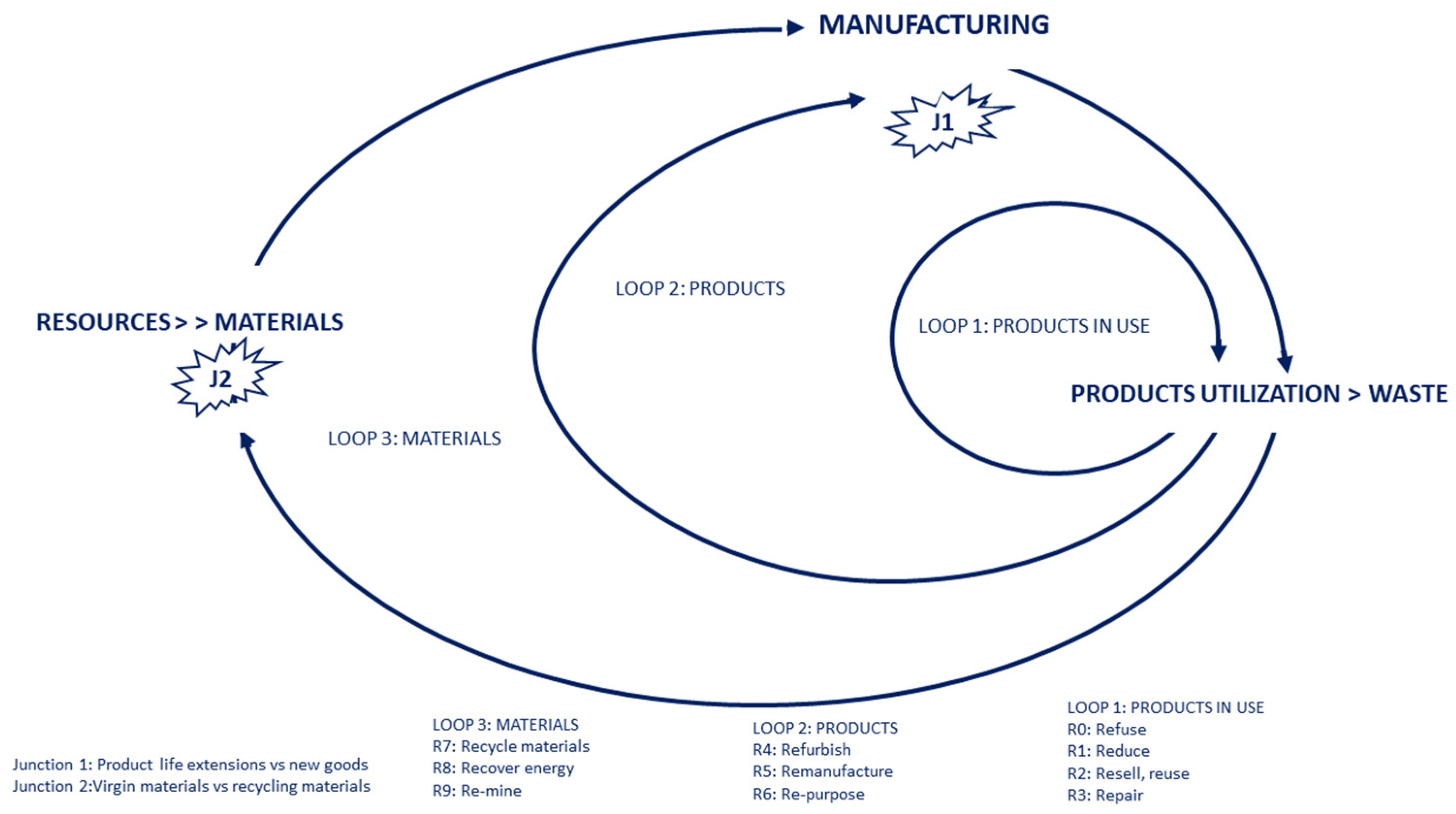

That is precisely what the second type of CE model emphasizes: prolonging the use of the entire stock of produced goods for as long as possible [47,50]. In this approach, “the Circular Industrial Economy [CIE] manages the stock of manufactured assets, such as infrastructures, buildings, vehicles, equipment and consumer goods to maintain their value and utility as long as possible; as regards resources, the CIE maintains the stock of these assets at its maximum level of purity and value. The CIE contrasts with the Linear IE [Industrial Economy] in that its objectives are based on maintaining value (not creating added value), on optimising stock management (not flows), and on increasing efficiency in the use of goods (and not in the production of goods)” [50] (p. 12). This shift towards a CE focused on stock management is based on three cycles. The first two constitute the “Era of R”: (i) the reuse and resale of goods; and (ii) activities to extend the life of the product or goods. The third cycle involves secondary resources or the recycling of molecules and corresponds to the “Era of D” (Figure 1).

Economic factors play an essential role in the two main disjunctives between circular and linear economies. First, a choice must be made between extending the life of products and purchasing new products (Figure 1). In this case, the comparative advantage of used goods grows to the extent that labour costs decrease in relation to services and activities associated with goods’ life extension and the cost of virgin materials in manufactured goods increases. Second, a choice has to be made between recycled versus virgin materials. Here, taxation on non-renewable virgin resources makes recycling (reuse of molecules) a more viable activity. Furthermore, reducing or eliminating taxation on labour would make end-of-life waste collection and sorting cheaper, thereby increasing the quality of secondary resources. All this would lower costs and raise the quality of secondary (recycled) resources, thereby expanding their market.

The circular economy has clear environmental advantages and facilitates others that are equally important [37,50]. Using skilled human labour and creating jobs, especially at local levels, reinforces regional and local development dynamics. CE labour inputs are higher because the geography and volume of their economies of scale are limited and some activities, such as repair and remanufacturing, are labour intensive [46,52]. Consequently, nontaxation on labour would stimulate employment in all labour-intensive economic sectors, including those involving the care and use of local renewable resources: organic farming, fishing, production and repair of wooden furniture, wool, textiles, footwear, leather goods, etc. This would also create qualified employment opportunities linked to improving infrastructures and equipment based on earlier technologies. Such activities tend to be located closer to the consumer and are, therefore, more widely distributed [53].

Unlike approaches focused on waste recovery and recycling, the circular economy proposes production and material systems without a loss of value, in which goods are designed to last, reparability is facilitated, and materials are continuously reused rather than degraded. Encouraging reuse and repair of goods to maximize their life span is an important strategy that involves more than the consumer at the end of the chain. It must start with eco-design for durability (as opposed to programmed or induced obsolescence) and facilitate reparability. This is not a merely technical issue (technological or use-based obsolescence); it requires a complete reversal of the economic logic of linear industry, which aims to sell as many goods as possible and have them renewed and replaced as soon as possible (sociopsychological obsolescence). In fact, despite the rhetoric of sustainable resource management, recent studies indicate that product lifespans are in fact shrinking in many sectors [54].

From a systemic perspective, CE must reduce the actual ecological footprint to keep the economy within the physical limits or carrying capacity of the planet [32]. As summarized by Krysovatky et al. [55] (p. 140), any stable society must ensure that: “(a) the rate of resource utilization does not exceed the rate of regeneration; (b) the rate of resource consumption does not exceed the rate of implementation of renewable substitutes; (c) the emission of pollutants and accumulation of waste does not exceed the rate of their harmless absorption”. Therefore, the scope extends beyond reducing impacts to redefining activities, processes, and behaviour according to natural cycles and reproduction needs.

Instruments for promoting this change of paradigm must clearly involve diverse policies and actions at all levels, to create a complex policy mix capable of altering the basic rules of the current economic model. Changes to the fiscal (tax) system, which we analyse here, are key.

3. Taxation for the Transition towards a Circular Economy

Tax policies have a key role to play in the transition to a CE, as they can affect relative prices. The tax system incorporates, implicitly or explicitly, extrafiscal objectives. It can create incentives and disincentives that guide the behaviour of businesses, consumers, and the public sector while also generating public resources for direct action by public administrations.

The first issue that emerges is what instruments and actions are possible within the tax system, along with their nature and scope. These may include partial and specific measures to modify existing taxes or tax expenditure schemes or to create new environmental taxes to cover gaps in the existing tax system. The architectural design of the tax system could also be altered by significantly modifying or replacing the main existing taxes (VAT, income, corporate, etc.), but it is hard to imagine that this could happen in the near future. Despite the broad consensus regarding the importance of fiscal instruments and the environmental taxes developed in recent decades, actual experience has led to growing dissatisfaction with the proliferation of new, relatively marginal environmental taxes, as implemented in many countries. This has led some researchers to call for a more thorough reform of these taxes and even a deeper reconsideration of the design of the entire tax system.

The rationale for a tax shift towards circular taxation is based on the concept of extrafiscality or extrafiscal taxation (taxation with extrafiscal purposes, e.g., “sin taxes”). This emphasizes that taxation is not limited to raising revenue for the public budget, but also pursues other objectives of an industrial, commercial, social, public health, or environmental nature [56]. Therefore, these objectives are not only established in the public spending programs but also in the determination of the characteristics of taxes and tax expenditure instruments; both have the capacity to influence consumption and production choices, investment capacity, and savings, as well as economic development and the transformation of economic and social structures [56,57,58]. For the purposes of this paper, we want to highlight the relevance of a particular type of extrafiscal taxation: tax expenditure instruments. These are targeted-oriented instruments, operationalized through taxes, not as a targeted increase in taxes but as targeted waivers in taxes. Tax expenditures are the “carrots” in the basket of the tax policy. They include instruments of fiscal incentives and benefits used to favour or stimulate certain sectors, economic activities, economic regions, or agents of the economy whose purpose serves higher economic, social, and sustainability policy objectives.

Within the ecological economy paradigm, different proposals to change the structure of the tax system were launched. Virtually all ecological tax reform proposals prescribe taxes on resources and energy extraction, while reducing labour taxation. The plan developed by Weizsäcker and Jesinghaus [59] would gradually increase energy taxes while reducing taxes on labour and business profits and eliminating all types of environmentally harmful subsidies and benefits. To neutralize feedback effects, Weizsäcker [60] proposed a tax on productivity increase associated with the extraction and use of raw materials, energy, and water. Daly et al. [61] proposed a tax on the increase in the value of land and natural resources and the elimination of business income tax. Daly [41] proposed an ecological tax reform that would change the tax base from the current value-added taxes (on labour and capital) to taxes on resource extraction and pollution. Robertson [62] proposed a tax on the value of land and another on energy production from fossil and nuclear sources while eliminating taxes on income, profits, and VAT. Hawken [63] proposed gradually replacing income and payroll taxes with green taxes on pollution, environmental degradation, and the consumption of non-renewable energy. Paleocrassas [64] proposed a tax on resource extraction and a progressive shift towards a basket of green taxes, including reducing taxes on labour, income, and VAT. Costanza et al. [65] proposed a tax on the reduction of natural capital; Cato [66] proposed taxes on waste, transport, resource extraction at source, carbon, pesticides, etc. Busby and Cato [67] proposed the creation of a Base 1 Planetary Impact Index by which each company would multiply its current taxes. Raworth [33] advocated a Georgian-type land value tax, a tax on non-renewable sources, and property taxes in exchange for reducing taxes on labour and income in general, combined with subsidies for renewable energy and investment in the efficient use of resources. Presently, these proposals remain theoretical outlines, with no development towards implementation.

The emergence of the CE approach could be an opportunity to renew this debate. Notwithstanding, analysis of taxation remains incipient in perspectives that envision the circular economy as an alternative productive paradigm. Some proposals for structural tax reform that align with ecological economy ideas have emerged in the last few years. They start with the idea that the current tax system functions according to the linear capitalist economy paradigm; moreover, the current tax regime reinforces the linear character of the economy [37]. Thus, to shift towards a CE, costs and prices must be positively and negatively influenced to reorient production and consumption decisions in an environmentally responsible direction that benefits society and the economy. To achieve this, structural changes must be applied to the architecture of the current tax system.

What distinguishes ecological and circular taxation from current environmental taxation is that the first aims to go beyond putting a patch on the problem by “correcting” a specific market failure or a certain type of pollution. Rather, it advocates a comprehensive overhaul of the taxation system. The general idea is to modify or eliminate current taxes that imply costs for circular (and renewable) activities, reinforce taxes on non-renewable resources and capital (intensive activities in the linear economy), and eliminate the current benefits and subsidies for environmentally adverse activities. Conventional environmental taxation is considered insufficient because it focuses on taxing the harmful consumption of specific products at the end of the production chain. This overlooks many externalities such as resource extraction and depletion, increasing amount of all kinds of waste, water and air pollution, biodiversity, etc.

Two scenarios are described below, along with proposals for ambitious changes in the tax system towards environmental sustainability and a circular economy. We will focus on a critical assessment of two comprehensive proposals, the first formulated by Beeks and Lambert [68], and the second formulated by Stahel [37], The Ex’tax Project for the Netherlands [69], The Ex’tax Project for Europe [70], and Barret and Makale for New Zealand [71]. In Section 4, we discuss a short-term scenario and suggest a feasible short-term proposal.

3.1. Integral Reform of the Tax System with Proposals that Cover All Externalities

The most general and holistic proposal was developed by Beeks and Lambert [68] (2018). In this scenario, fiscal instruments influence market forces by inducing broad, crosscutting, socio-environmentally positive changes in production and consumption. Thus, it is not about correcting the most serious single impacts but transforming the entire economic system [11].

Beeks and Lambert [68] argue that negative externalities will be produced as long as they are economically viable. They will inevitably be transmitted to current and future societies in the absence of government actions capable of counteracting them. One way to reduce these externalities involves acting through market mechanisms—prices, in particular—to decrease associated profitability. For the authors, the objective is not only to transfer certain externalities to prices in accordance with a cost–benefit criterion—as mainstream environmental economics does—but also to design a comprehensive pricing system that incorporates sufficient incentives to change the behaviour of economic agents towards sustainable patterns. They explicitly agree with Daly [41] that reducing consumption-related impact may be the best way to reorient the current economic system, which is based on hyper-consumption and works by appropriating the natural (free) system, negatively affecting humanity and the economy itself. To do so, Beeks and Lambert [68] (p. 7) proposed estimating a new cost factor for all services and products, which would integrate all externalities generated in production and consumption. The aim is to fully cover all negative and positive externalities by means of an externality factors (EF) system. These would include estimates for not only CO2 and GHG emissions, but also all pollutants affecting water, the atmosphere, soil, biodiversity, the ecological system, and human well-being.

Rather than designing or assessing single taxes to correct a specific externality, this proposal involves creating a tax system that attempts to counteract the combined sum of the various externalities. Another novel element is that it adds on the estimated cost of negative externalities and discounts positive externalities, so that the external factor added to the price of the good reflects the balance of them all. Using market forces, the EF system would raise the selling price to discourage negative production and consumption or reduce it to encourage positive production and consumption. The important thing here is that the tax system itself (taxes, subsidies, benefits) promotes a transition to environmentally friendly and safe practices.

Calculating externalities precisely is one of the first difficulties to overcome when defining and implementing such a tax. This complexity has always invited critique, especially by those who doctrinally defend the need for optimum taxes in which the amount tax corresponds exactly to the value of the externality. However, the authors suggest moving on from this limiting debate: precise calculation of externalities or setting the tax at an amount that exactly compensates the calculated externalities is not the most important issue. Rather, a reference estimate can be used to determine—through a policy process—the amount of tax. This pragmatic proposal assumes that taxation is not strictly or exclusively a technical matter. The important thing is the willingness to account for socio-environmental costs (negative externalities) that are not currently included in corporate calculations of the cost of goods and understanding the specific configuration and determination of the tax as part of a sociopolitical and institutional decision-making process. Governments, on the basis of dialogue with social agents, must then work out the specifics of tax design and amount. In fact, these authors assume that such discretion may lead to diverse taxes on the same goods in different countries or territories.

Below, we summarize the key elements and prevailing logic for EFS configuration from Beeks and Lambert [68] (pp. 2–10):

- A.

- Limited rationality versus optimality. In line with what has been proposed by Martínez Alier [11,72], Daly [41] and Hawken [63], Beeks and Lambert [68] consider that the important thing is the decision to tax externalities, accepting limited rationality and approximation over obsession with precision and optimality. It is generally accepted that determining the cost of externalities “is neither practical nor possible” [11] but that “trying to measure negative costs is preferable to ignoring them completely, that it is better to be approximately right than completely wrong” [63] (p. 101). Accordingly, it is acceptable and advisable to “tax polluting activities, resource extraction and resource depletion, all without connecting the precise cost of these activities to the tax” [41] (p. 4). The key is to accept a commitment to a “cost approach” that enables tentative and evolutionary means of addressing pervasive problems such as natural impacts. In other words, an estimated or approximated tax would suffice to reduce the gap between the private and socio-environmental costs of the objective it seeks to influence.

The tax essentially imposes a non-negotiable price that will bring about the desired results of less pollution, healthier ecosystems, and less use of natural resources, while generating equity and revenue. Benefits and subsidies can then be directed towards environmentally positive activities.

- B.

- The price must be able to influence the behaviour of consumers and producers towards positive, long-term change. First, it would be reasonable and timely to set the tax rate low and eventually increase it, to internalize costs as fully as possible. The system should be flexible enough to allow for tax adjustments on goods with high or low externalities.

- C.

- Ideally, high taxes would be applied to obviously “harmful” goods and services, though attention should be given to the effects of these cost increases on the price index and, hence, on the economy (e.g., inflation). Even so, it would be reasonable to set comparatively high taxes on these “harmful” goods in the short term, to discourage consumption. The intent is to affect the entire cost dimension, penalising or incentivising with taxes and benefits (and subsidies). Economic agents who make a positive effort will benefit economically from tax reductions and possible support for sustainable investments.

- D.

- General coverage that reflects all implicit and explicit externalities. The point of the proposal is to integrate all categories of externalities, trying to assess the damage in a multidimensional way: “the EF system is intended to take into account production externalities, consumption externalities, monetary and non-monetary externalities, and whether they are positive or negative” [68] (p. 7). To achieve this, seven categories are proposed for the general coverage of externalities, especially negative ones: 1. air pollution; 2. water pollution; 3. soil (earth) pollution; 4. impact on the ecological system; 5. impact on human and animal welfare; 6. social and cultural impact; 7. contribution to global climate change. All categories are included in the final cost assessment.

All these negative impacts will be accounted for throughout the production chain. This includes extraction, refining, processing, transport, distribution, and the potential effects (including damage) of the whole process up to the time of purchase. It even incorporates the location of the production system and the logistics line used. Thus, proximity to production would imply lower costs because the incidence of externalities would obviously be lower (in absolute terms).

- E.

- Application of the externality factor system (EFS) involves estimating the value of each category of externalities for each product, finding the balance between negative and positive ones for each category and adding it to the standard cost. Each balance of negative and positive externalities would be placed on a base 1 scale, with a conventional range of variation from 0.8 for those with a more positive balance to 1.3 for those with a more negative balance (as suggested by the authors [68] (p. 9). Multiplying by values below 1 implies a reduction in cost, while multiplying by values above 1 would increase the cost. Multiplying the standard production cost by each of the seven externality factors (for each category) gives us the final cost of each product. The difference between the standard cost and the final cost is the total externality factor cost, which can be positive or negative depending on whether negative or positive externalities predominate. Thus, the cost of a good or service at final sale results from the cumulative effect of the combination and application of all EF categories. In such a situation, a lower EF cost implies a benefit for the retailer—as a form of “subsidy”—and a higher EF cost signifies higher penalties.

Introducing this cost factor to reflect externalities is intended to influence consumption by significantly altering the price of goods and services. Unlike traditional environmental taxation that addresses specific externalities, this proposal assumes that externalities are everywhere and, accordingly, we should adjust the tax system to consider all externalities arising from economic activity in all sectors. It is worth noting that the cost/value of each externality factor is not calculated precisely with an optimality criterion, according to some cost–benefit analyses, but that its determination involves a social and political decision. Therefore, considering the social circumstances and preferences (e.g., aiming to limit global warming to 1.5 °C instead of 2 °C), the expected positive effects should include reduced goods consumption; changes in demand and lifestyles (less harmful to the environment); changes in industrial production, such as improving development and technological innovation to reduce pollution, substituting raw materials, reusing products and materials, extending the life of goods, etc.

3.2. Integral Tax Reform Based on Taxation of Natural Resources and Reduction of Labour Taxes

A second type of proposal to design a new and sustainable tax system for a circular economy prioritizes taxes on non-renewable resources, eliminating subsidies to polluting sectors and reducing or eliminating taxation of renewable resources (including labour, which is considered the most renewable resource). Along these lines, Stahel [67] introduced a pioneering scheme that has been developed with adaptations to the specific circumstances of certain countries. Examples include [69,70,73,74]. Milios [36] provides an interesting review of raw material tax, repairing, and the hierarchy of waste.

The basic idea is that the actual tax system inhibits the emergence of a sustainable CE and taxation is essential to facilitating the emergence and expansion of circular activities. Because taxation is a key instrument for altering market forces and prices, it can influence all stages of the chain, from innovation to design and manufacturing patterns to consumption.

As Stahel [50] argues, “the linear economy is resource and capital intensive, while the circular economy is labour intensive. Current fiscal policies in many countries impose heavy taxes on labour, while subsidizing the production and consumption of fossil fuels and other non-renewable resources. Reversing taxes on these two factors of production, favouring renewable resources over non-renewable ones, would give economic agents direct incentives to change towards the circular economy and sustainability” (p. 72). With similar proposals, Raworth [33] (p. 164) insists that the shift “from taxing labour to using non-renewable resources […] would help erode the unfair tax advantages currently given to companies investing in machines (a tax deduction rather than in humans (a payroll spend)”.

The objective of the EC and the new form of taxation would be not so much to increase efficiency as, above all, to promote goods and consumption that do not alter environmental capacity. It emphasizes eco-design, reduction, repair (and maintenance), remanufacture, and reuse of items related to consumption and production, to avoid waste generation and the consumption of new non-renewable resources.

The implementation of sustainable, pro-circular taxation can have favourable effects on the different cycles. Figure 1, based on Stahel [37], lists the foreseeable impacts of sustainable taxation on material and resource sufficiency and efficiency, which are summarized as follows:

- (a)

- Taxation on non-renewable resources is an incentive to minimize resource consumption, by-products of production, and waste. Water and energy savings, together with waste prevention, become profitable activities, especially if resource prices increase continuously.

- (b)

- At Junction 1 (J1), nontaxation on labour favours reuse, repair, and remanufacturing activities. The regional nature of the circular economy, compared to global manufacturing chains, significantly reduces the energy involved in transport.

- (c)

- At Junction 2 (J2), many materials used today are more expensive than virgin materials. Sustainable taxation favours labour-intensive approaches to high quality, lowering the labour cost of sorting used material while increasing the price of non-renewable virgin materials.

- (d)

- It should also create virtuous cycles for more efficient use of materials, saving money and thereby reducing material-intensive consumption.

These approaches can be developed for application in specific countries, such as [69,70] and [73]. The guiding ideas for The Ex’tax Project proposal are to change the tax system by taxing natural resources, to eliminate environmentally harmful subsidies, and to reduce labour taxes (see Table 1). Its most outstanding contribution involves efforts to create a toolkit of instruments and measures adapted to the fiscal reality of each country, starting with the full range of existing taxes and all available quantitative measures (rates, deductions, exemptions, allowances, subsidies, etc.).

The proposal to reduce labour-related taxes and replace them with natural resource taxes takes the whole range of tax bases into account. The first group includes taxes that burden human effort (income tax, social contributions, corporate income tax, VAT), to which actions involving rates, deductions, exemptions, allowances, and subsidies can be applied. The second group includes taxes related to the destruction of natural resources, such as air pollution, building materials, ecosystem services, energy, food production, fossil fuels, metals and minerals, traffic (air freight, road transport, air traffic, plane tickets, maritime transport, traffic congestion, road traffic), waste, various other resources, and VAT. Within these 12 families of taxes on non-renewables (NR), there are up to 104 taxable assumptions or subcategories [69].

This comprehensive “toolkit” allows policymakers to combine, time, and prioritize measures according to their urgency, degree of short-term feasibility, potential benefits, and accessibility. Because it is flexible, it can adapt to the changing needs of public systems. Adequate management of the toolkit can facilitate a path that reduces labour taxes and increases resource taxes according to the principle of neutrality.

To summarize, this proposal starts with the current configuration of the existing tax system in each country. It then offers an entire battery of changes that constitute a complex toolkit. The options range from creating new taxes on the use and consumption of non-renewable resources to easing the burden on circular activities by changing existing taxes to reducing existing tax benefits for environmentally harmful activities.

3.3. Discussion

3.3.1. Circular Taxation as an Alternative to Environmental Taxation

Comparatively, we can affirm that the objectives of circular economy taxation are more ambitious than those of environmental taxation in recent decades. In range and reach, they far exceed policies involving small, super specific environmental taxes or the green tax par excellence: the carbon tax. Existing environmental taxes aim to reduce some externalities and give small impulses to change economic behaviour, but they leave the basic structure of the linear economy intact. On the contrary, circular taxation aims to contribute to a more radical change in the economic structure, significantly altering relative prices and changing the behaviour of firms and consumers to achieve an economy that respects the limits of the planet.

Based on a preliminary contribution by [71], we have identified five main differences between circular and environmental taxation, which are summarized in Table 2. They involve (a) the recalibration of existing environmental taxes to incorporate the real prices of externalities and bring about effective change in the behaviour of economic agents, production, and consumption; (b) encouraging extension of the useful life of goods as much as possible (taking into account the whole chain from design to consumption, repair, and reuse); (c) encouraging recycling (cradle to cradle) in a fundamental way; (d) moving from taxes on labour to taxes on the use of resources; and (e) greater use of the concepts of merit and demerit to push consumers towards the desired behaviour.

3.3.2. Potential Effects of Circular Taxation and Necessary Precautions

Having identified the characteristics of circular taxation, we move on to the expected effects and consequences. Among those indicated by the authors of the proposals themselves, circular taxation would: (a) accelerate the transformation from a current economy focused on “flow optimization” (the essential logic of national accounting and GDP) to an economy focused on “stock optimization”; (b) expand the circular economy to new economic actors and sectors; (c) increase the competitive advantage of existing economic actors in the circular economy; (d) by not taxing renewable resources (including labour), it contribute to greater resource security, job creation, and lower GHG emissions; and (e) strengthen regional distribution and social cohesion.

Circular taxation reinforces the incentives to boost eco-innovation in all sectors, increase optimization in the use of resources and energy, look for new eco-materials, reuse/recycle materials, and develop innovations for eco-design, long-lasting products, and reparability [48,71]. Of course, specific tax measures could be adopted into the schemes of R&D tax policy in order to enhance and prioritize eco-innovation and eco-R&D.

Not taxing labour increases the competitiveness of labour-intensive activities of the regional circular economy compared with the global industrial manufacturing; regional activities mean lower transport volumes and shorter transport distances in the processing chain. Applying the principles of sustainability to the economy means decoupling wealth and welfare (stock) from resource consumption (flow). A shift in taxation from renewable resources, including work, to non-renewable ones will boost regional job creation, employment, and occupation of all forms in labour-intensive industrial and service sectors [37] (p. 16).

Therefore, a change towards CE would bring about environmental benefits and positive economic impact. Estimates from 2016 based on Cambridge Econometrics Models [70] showed that shifting 554 billion euros of taxes from labour to pollution and resource use in the European Union would allow 6.6 million more people to be employed, reduce carbon emissions by 8.2% by 2020, and save 27.7 billion euros on energy imports over a five-year period.

Having pointed out the potential virtues of reducing labour-related taxes to favour the development of circular activities, which are generally labour-intensive [52], it is necessary to acknowledge some risks. A drastic and immediate decrease in labour-related taxes could have unforeseen consequences, especially in countries with a weak tax base, or where current public revenues are highly dependent on certain taxes, or where social benefits (pensions, health services, etc.) are basically financed by social contributions [11] (p. 173). Any change in the tax system towards environmental sustainability must guarantee social sustainability by ensuring progressivity and sufficient revenue to maintain essential welfare state services. Of course, this is a key issue that requires extensive research in the future.

When formulating a general, transversal tax system for all types of consumption, unexpected or undesired problems and effects may arise (such as inequalities or poverty) that will require corrective or compensatory measures. One potential problem is that it is a broad-based indirect tax scheme, in which a higher level of pollution is attributed a higher value (EF) over cost. Given the general experience with such taxes (VAT, for example), citizens at the lower end of the income distribution scale may experience a regressive effect when it comes to meeting their consumption needs.

To address this, Beeks and Lambert [68] introduced some factors that can be used to reduce the regressive effect that normally accompanies environmental taxes (such as excise taxes). One of these, the “social and cultural impacts” factor, can take social and distributive effects into account, so that the overall effect of the tax is inclusive and favourable to social cohesion. To this end, the authors suggest that “it will be necessary to cap out the highest EF tax initially for most necessary goods in order to protect low-income consumers from the higher costs of essential goods” [68] (p. 14).

Furthermore, because this system affects all phases of production, consumers can opt for more local consumption, which normally incurs fewer negative externalities, or use collective and public services to avoid high consumption and choose savings. To encourage more sustainable practices, these authors propose that this tax system not be applied uniformly to a product or activity sector but calculated at a micro level, according to the characteristics of the productive process of each company.

Importantly, even though EFs are assigned to goods and services either at the point of retail sale or at different points in the supply chain, they can be adjusted depending on the practices of a given retailer, distributor, wholesaler, and/or producer. As an example, if a firm depends too heavily on the worldwide shipment of goods, participates in deforestation activities because of the goods they purchase, has inefficient and unsustainable practices, or is known to rely on unsafe working conditions for the production of goods, among other things, then the EFs can be increased specifically for this firm. Therefore, another firm purchasing the exact same goods that does not use excessive amounts of fossil fuel for shipping, does not purchase goods that lead to deforestation activities, and does not purchase from factories with unsafe working conditions may be assigned lower EFs for the same product [68] (p. 10).

Finally, beyond the inevitable complexity, it is necessary to point out some weaknesses that require reconsideration. Firstly, calculating externalities and EF at the company level introduces unwieldy complexity and a potential source of fraud. Moreover, this predilection for micro-level differentiation, as opposed to setting standards by product or sector, is likely to contribute relatively little to the objectives. The complex calculation system poses a cumbersome challenge for public finances and companies. Given that companies would be tasked with implementing this EF system in which multiple externalities are calculated and reflected in the price of each product, a rigorous control and computer data system would have to be activated, with modern programming systems and algorithms supported by Artificial Intelligence, control and compliance audits, etc. Permanent monitoring at macro and micro levels has also been suggested, with special attention to inflation aspects.

This degree of individualization introduces many random or arbitrary factors that would invite distortion of company calculations for certain externalities, to reduce taxation or increase competitiveness (possible dumping issues). To avoid this, it would be necessary to strengthen the partnership between the private and public sectors [68] (p. 13). This would require public financing, along with the appropriate instruments for inspection and control.

Secondly, the suggested price adjustment range of −20% to +30% means that the actual tax is relatively low and does not sufficiently penalize the most serious consumption.

Thirdly, balancing and offsetting prices transfers the desired effect to the consumer. The resulting tax revenues may be too low, which could severely reduce public revenue, the financing of basic state functions, or resources for welfare and environmental investment policies. Moreover, it is not clear from the proposal what part of the EFS revenue goes to the government. In fact, the authors mention other changes to the tax system such as gradual reduction of income and more active use of land and property taxes, along the lines of “Georgian taxes”, which were proposed by the American economist Henry George [75]. This would cover possible drops in collection or correct undesirable consequences in the distribution of tax burdens among people or territories [68] (p. 14).

3.3.3. Challenges and Barriers to Circular Taxation

The transition to a circular economy involves extensive systemic change that alters the features of the economic–productive model and the basic rules of the game, including determinants of value, social priorities, and the choices of individuals. The relative prices of goods and services must be modified to orient economic activities and consumption towards those that are less intensive in natural resources and non-renewable energy. The tax system is a powerful instrument in this arena. It can affect the profitability of activities, thereby altering investor behaviour and the relative prices of goods and services, which can change consumer consumption patterns.

It is increasingly evident that the inherited fiscal architecture reinforces an unsustainable economic model. Therefore, changing the architecture of the tax system—rather than specific areas or individual taxes—is central to creating framework conditions for the transition to a circular economy and sustainability throughout the economic system.

Despite the advantages it would bring, there are numerous obstacles that slow progress in a change of this magnitude. First, it would require strong social and political consensus and a relatively stable long-term transition strategy that can withstand clashes stemming from relatively short policy cycles. Second, breaking fiscal habits is difficult, especially if it means paying for something that was previously not taxed. Third, industries with vested interests often form powerful lobbies for change, with significantly greater force and voice than other interest groups, such as nongovernmental organizations (NGOs), health organizations, or small and medium-sized enterprises interested in transition [31]. Fourth, a change in the tax architecture requires some international coordination in the design and pace of implementing tax reform. Finally, fiscal change on this scale modifies essential characteristics of the current economic model and globalization dynamics. Changing financial incentives will change trade patterns, financial flows, and development strategies in many countries.

4. Short-Term Feasible Tax Reforms for Circular Transition

Since a radical and comprehensive change of this magnitude is unlikely to occur in the short term, it may be more effective to think of a sequence of target-oriented changes for the transition to CE. A correct sequencing of the change is crucial to achieve safe progress. Being aware of the difficulties in moving towards a change in the architecture of the tax model as proposed, it is advisable to explore more easily traversable paths which, although more modest, move in the direction of circular taxation and can be implemented in the short term. The strategy we suggest here tries to take advantage of the existing weaknesses in the current fiscal model and focuses on a radical change in the tax expenditure schemes.

As mentioned before, tax expenditure is a particular type of extrafiscal taxation. It is a target-oriented instrument operationalized through taxes, not as a targeted increase in taxes but as a targeted waiver in taxes. Tax expenditures are the “carrots” in the basket of the tax policy. Since Surrey’s seminal contribution to the topic, which considered tax expenditures and direct expenditures as equivalent [76,77], new work on the nature and applications of different tax expenditure instruments has been emerging. According to Villela, Lemgruber, and Jorrat [78] (p. 2), ECLAC/Oxfam [58] (p. 118), and Ashiabor [79], tax expenditures are instruments of fiscal incentives and benefits used to favour or stimulate certain sectors, economic activities, economic regions, or agents of the economy whose purpose serves higher economic, social, and sustainability policy objectives. “Both tax (expenditure) as well as direct expenditures serve programmatic objectives, as they have an economic and social purpose. With tax expenditure, a government forgoes tax revenues to subsidize various social and economic activities […] One of the many features that set tax expenditures apart from direct expenditures is that unlike the latter, the former invariably involves the transfer of money by lowering an individual’s or corporation’s taxes […] Tax expenditures are rarely subjected to the same annual appropriations process as direct expenditure. Their true fiscal cost is hidden as revenue forgone...even if analysed, can sometimes be difficult to estimate” [79] (pp. 22–23).

In real tax policy, tax expenditure has been an increasingly used instrument since the 1980s. Tax expenditure is currently a big black hole in the taxation of almost all countries. The debatable issue is the specific direction, beneficiary agents, and effects of the measures that have been implemented over the years. Although tax benefits have been adopted for environmental purposes, the vast majority of them serve other objectives.

Tax expenditure (tax benefits) materializes into governments’ fiscal waivers [58,79,80], which can be granted to economic agents in diverse ways (incentives, tax relief, deductions, accelerated depreciation, etc.). Tax expenditure includes both incentives and benefits that affect consumption and investments that favour the environment or reduce environmental impacts and, on the opposite side, fiscal measures promoting productive activities and consumption practices with clearly unsustainable components that contradict the objectives of environmental policy (incentives for diesel and fuel consumption, which generate CO2 emissions, or benefits for resource-extractive industries and the consumption of materials, etc.). What is striking is that the environmentally harmful subsidies (EHS) turn out to be much more important than the pro-environmental ones [58,79,81]

Due to the extensive usage of tax expenditure in the current tax regimes, we suggest focusing on these categories to pave the way for a transition towards a circular taxation system. Although this is an opaque and little studied subject, existing estimates place tax expenditure at 14–24% of total revenue in most countries, in some cases (e.g., the USA and the UK) exceeding 30%; as a proportion of GDP, the available estimation ranges from 3.7% in the Latin American countries to 8% in the USA [58] (p. 6); [81]. Moreover, only a very small part of it responds to environmental criteria and the vast majority benefits environmentally damaging activities [79,81]. For example, the 2018 tax expenditure in Mexico amounts to 20.7% of total revenue (3.24% of GDP), whereas environmental benefits account for only 0.07% of total revenue and the vast majority are not environmentally friendly; about 1.66% of total revenue is waivers, most of which are harmful to the environment (see Table 3). As an example, the full benefit (tax 0 rate) on VAT for repair and maintenance activities in Mexico would have a fiscal cost of only 0.71% of total revenue [82].

Consequently, there is ample scope in all countries (14–40% of total revenues, without a tax burden increase) for changing the priorities and relative prices of different activities, goods, and services to induce changes favourable to the circular economy and sustainability, simply by eliminating environmentally harmful tax expenditure or introducing tax benefits for circular activities.

In recent years, some countries have formulated ambitious strategies (e.g., the European Green Deal) to encourage the transition towards a circular economy. In moving towards a circular economy, the first steps should focus on ambitious reform and make use of available tax expenditure measures, including the many tax benefits, exemptions, deductions, and allowances applicable to existing large taxes (e.g., VAT, Corporate Tax, etc.). As mentioned earlier, these instruments have been acquiring enormous presence in the general tax policy (mainly for non-environmental purposes) and, to a very modest extent, in environmental policies [79]. Therefore, if the political will exists, there is an opportunity to transform many discredited anti-environmental fiscal benefits into tax benefits that favour the promotion of circular activities and circular business models that prolong the life of products and reduce the consumption of natural resources and energy.

Feasible changes could be implemented in the short term by significantly altering the overly broad and opaque tax expenditure schemes in different ways, primarily focusing on good and service taxes, complemented by a reinforcement of taxes on non-renewable resources.

- Application of VAT exemption or zero rate to encourage circular activities extending the life span of products and materials such as reuse, repair, remanufacturing, recycling, or remediation; minimum VAT should be applied to building rehabilitation and regeneration activities, etc. It is worth noting that the suggested measures are far more far-reaching than the tax relief on repairs introduced in a very limited way in some countries and, precisely for that reason, have not produced the expected results [35,36,84]. Of course, an assessment of the environmental benefits and the estimated fiscal cost should be made. In any case, this fiscal cost can be neutralized by the elimination of other anti-environmental tax benefits.

- The accelerated elimination of tax benefits and subsidies that are harmful to the environment or that protect and promote polluting, unsustainable, and noncircular activities (especially tax benefits for energy taxes, corporate taxes, and VAT).

- These first steps towards CE would be reinforced by measures to significantly increase effective taxation along the life-cycle stages, in particular of non-renewable resources, non-renewable energy and GHGs, and waste hierarchy tax. Evaluation of recent experiences in Sweden suggests that applying such individual instruments with moderate ambition may limit their effectiveness [36]. To exploit their potential, it is necessary to combine the different instruments to substantially increase the tax base by broadening the degree of coverage of resources, activities, and consumption and by increasing the respective tax rates. In particular, tax on non-renewable resources should be combined with tax benefits on reuse, repair, remanufacturing, and improved recycling to induce a significant change in relative prices and incentivize circular consumption, replacing the purchase of new products by extending the life of existing products.

- The allocation of carbon credits for activities that contribute to the prevention of GHG emissions and not only to their reduction. Avoiding emissions merits greater tax benefits than those granted for reducing emissions (but continuing to emit), as is currently the case. This essentially rewards existing polluters when they choose to reduce pollution rather than rewarding those who avoid pollution in the first place.

- Although Stahel [37] (pp. 15–16) considers that the CE does not need subsidies, from our point of view, certain transitional and temporary subsidies could be justified as a way of pushing forward new CE business models and correcting the negative effects of the current fiscal system or power imbalances in the markets (oligopolies, dominance of big companies in linear sectors like commodities, the car industry, fast fashion, etc.).

5. Conclusions

There is a broad consensus regarding the importance of fiscal policy and the tax system as a fundamental tool for promoting transformations aimed at meeting environmental challenges. However, the proliferation of new, specific, and relatively marginal taxes with environmental objectives is proving to be a failure. Their modest results have fallen far short of expectations and fail to mitigate the serious environmental problems affecting the planet and society today. Furthermore, the capacity to even collect these taxes has decreased over the years.

It is increasingly evident that the inherited fiscal architecture of the past reinforces the unsustainability of the linear economic model. The transition towards a circular economy implies systemic changes that affect all aspects of economic life and require implementation of a policy mix that integrates a wide range of policies and instruments. The question is, what kind of changes in the tax system can effectively contribute to this transition? Systemic change towards CE must be accompanied by systemic change in the architecture of the tax system. However, here we suggest the need for a strategic roadmap that sets out a sequence of gradual, step-by-step changes that allow for major but feasible changes in the short term, clearly oriented to the objectives of long-term architectural change.

The strategic proposal, which can be implemented in the medium to long term, is based on the idea of prioritising taxes on non-renewable resources (“Georgian taxes”) and eliminating or reducing the tax on renewable resources (including labour, which is considered the most renewable resource). Alternatively, a general and transversal tax could be created that reflects the combined value of all the externalities associated with each product or the chain of activities involved in its production, from the extraction of the raw material to consumption. Favourable tax treatment of renewable versus non-renewable resources would change relative prices in favour of the former, giving economic agents direct incentives to change towards a circular economy and sustainability. This radical shift towards circularity in the fiscal architecture would entail replacing current large taxes—designed within the framework of the linear economy and beneficial to it—and introducing new types of circular tax with great collection capacity.

When introducing radical structure changes to the tax system, powerful barriers will inevitably arise. Defining and refining policies, then gaining minimum international consensus among relevant countries, is a long and arduous social and policy process. With such formidable obstacles to overcome, these ambitious proposals could suffer the same fate as their green economy predecessors have since the 1990s.

Given the urgency of the serious environmental challenges we face, waiting is not an option. It, therefore, seems reasonable to propose changes to the current tax system that are feasible and viable in the short term and that will foster the transition towards a circular economy and sustainability. The starting point is an essentially dysfunctional fiscal framework, given the principles on which large taxes are based and because many tax benefits are available to key sectors of the linear economy that have a high environmental impact. In moving towards a circular economy, the first steps should focus on ambitious reform and make use of available tax expenditure measures, including the many tax benefits, exemptions, deductions, and allowances applicable to existing large taxes (e.g., VAT, income tax, corporate tax, etc.). Due to the current huge presence of tax expenditure in the general tax policy (mainly with nonenvironmental purposes) they could be reshaped and used to promote the transition towards a circular economy, in line with the proposals discussed above. First of all, we must do away with all environmentally harmful subsidies and tax benefits and replace them with a tax treatment favourable to all circular and sustainable activities.

Such a transition would be reinforced by measures to facilitate the shift from the current taxation of labour-related activities to taxation of resources, non-renewable energy, and GHGs. This would substantially increase the coverage of the environmental tax base and progressively increase the applied tax rates. Of course, future research is needed to develop the specific measures of the tax package and their detailed design. Furthermore, to complement these fiscal measures, it would also be necessary to keep a comprehensive policy mix, including a set of environmental plans and programs, going, such as incentives for green technological development, introduction of technical standards, regulations against polluting activities, conservation programs, etc.

Author Contributions

Conceptualization, X.V.; investigation, X.V. and S.d.J.L.P.; writing-original draft preparation, X.V. and S.d.J.L.P.; writing—review and editing, X.V. and S.d.J.L.P.; supervision, X.V.; project administration, X.V.; funding acquisition, X.V. All authors have read and agreed to the published version of the manuscript.

Funding

The authors belong to the ICEDE-Galician Competitive Research Group GRC ED431C 2018/23 and to the “R2π: Transition from linear 2 circular: Policy and Innovation” H2020 Project. This research was supported by the Spanish Innovation Agency (AEI) through the project ECO-CIRCULAR: “La estrategia europea de transición a la economía circular: un análisis jurídico prospectivo y cambios en las cadenas globales de valor”—ECO2017-87142-C2-1-R. All these projects are co-funded by FEDER (UE).

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: CIATData Tax Expenditures “TEDLAC 2018 by Country”. 2020. Available online: https://www.ciat.org/gastos-tributarios/ (accessed on 4 May 2020).

Acknowledgments

The authors are grateful to the comments and suggestions made by the four anonymous reviewers.

Conflicts of Interest

The authors declare no conflict of interest. The founders had no role in the design of the study, in the collection, analyses, or interpretation of data; in the writing of the manuscript, or in the decision to publish the results.

References

- Baumol, W.J.; Oates, W.E. The Use of Standards and Prices for Protection of the Environment. Swed. J. Econ. 1971, 73, 42–54. [Google Scholar] [CrossRef]

- Baumol, W.J. On Taxation and the Control of Externalities. Am. Econ. Rev. 1972, 62, 307–322. [Google Scholar]

- Metcalf, G.E.; Weisbach, D. Design of a Carbon Tax. U of Chicago Law & Economics, Olin Working Paper No. 447, U of Chicago, Public Law Working Paper No. 254. SSRN, 2009. Available online: https://ssrn.com/abstract=1324854 (accessed on 16 September 2019).

- Metcalf, G.E. On the Economics of a Carbon Tax for the United States. Brook. Pap. Econ. Act. 2019, 405–484. Available online: https://www.brookings.edu/wp-content/uploads/2019/03/On-the-Economics-of-a-Carbon-Tax-for-the-United-States.pdf (accessed on 2 December 2019). [CrossRef]

- Nordhaus, W.D. Carbon taxes to move towards fiscal sustainability. Econ. Voice 2010, 7. [Google Scholar] [CrossRef]

- OECD. Taxation, Innovation and the Environment; OECD: Paris, France, 2010; Available online: https://www.oecd-ilibrary.org (accessed on 16 September 2019).

- Pearse, R.; Böhm, S. Ten reasons why carbon markets will not bring about radical emissions reduction. Carbon Manag. 2014, 4, 325–337. [Google Scholar] [CrossRef]

- Stiglitz, J.E.; Stern, N. Report de la Comisión de Alto Nivel sobre los Precios del Carbono; World Bank Group: Washington, DC, USA, 2017; Available online: https://openknowledge.worldbank.org/handle/10986/28510 (accessed on 20 April 2019).

- Andrew, J.; Kaidonis, M.A.; Jones, B. Carbon tax: Challenging neoliberal solutions to climate change. Crit. Perspect. Account. 2010, 21, 611–618. [Google Scholar] [CrossRef]

- Böhm, S.; Misoczky, M.C.; Moog, S. Greening capitalism? A Marxist critique of carbon markets. Organ. Stud. 2012, 33, 1617–1638. [Google Scholar] [CrossRef] [Green Version]

- Martínez Alier, J.; Roca, J. Economía Ecológica y Política Ambiental, 3rd ed.; Fondo de la Cultura Económica: Mexico City, Mexico, 2013. [Google Scholar]

- Coelho, R.S. The High Cost of Cost Efficiency: A Critique of Carbon Trading. Ph.D. Thesis, Universidade de Coimbra, Coimbra, Portugal, 2015. [Google Scholar]

- World Bank; Ecofys; Vivid Economics. State and Trends of Carbon Pricing 2017’ (November); World Bank: Washington, DC, USA, 2017. [Google Scholar] [CrossRef]

- Zhu, Y.; Ghosh, M.; Luo, D.; Macaluso, N.; Rattray, J. Revenue recycling and cost effective GHG abatement: An exploratory anaysis using a global multi-sector multi-region CGE model. Clim. Chang. Econ. 2018, 9, 1840009. [Google Scholar] [CrossRef] [Green Version]

- Milne, J.E. Environmental taxes. In Policy Instruments in Environmental Law; Richards, K., van Zeben, J., Eds.; Edvard Elgar: Cheltenham, UK, 2020. [Google Scholar]

- Mankiw, N.G.; Weinzierl, M.; Yagan, D. Optimal Taxation in Theory and Practice. J. Econ. Perspect. 2009, 23, 147–174. [Google Scholar] [CrossRef] [Green Version]

- Baumol, W.; Bradford, D. Optimal Departures from Marginal Cost Pricing. Am. Econ. Rev. 1970, 60, 265–283. [Google Scholar]

- Pigou, A.C. The Economics of Welfare; McMillan: London, UK, 1920. [Google Scholar]

- Rudolph, S.; Kawakatsu, T.; Lerch, A. Regional Market Based Climate Policy in North America: Efficient, Effective, Fair? In Environmental Taxation and Green Fiscal Reform: Theory and Impact; Kreiser, L., Lee, S., Ueta, K., Milne, J., Eds.; Edvard Elgar: Cheltenham, UK, 2014; pp. 273–289. [Google Scholar]

- Pegels, A. Taxing Carbon as an Instrument of Green Industrial Policy in Developing Countries; Deutsches Institut für Entwicklungspolitik gGmbH.: Bonn, Germany, 2016. [Google Scholar]

- Reynoso, L.H.; Montes, A.L. Impuestos ambientales al Carbono en México y su progresividad: Una revisión analítica. Econ. Inf. 2016, 398, 23–39. [Google Scholar] [CrossRef] [Green Version]

- Gago, A.; Labandeira, X.; López-Otero, X. Las Nuevas Reformas Fiscales Verdes. 2016. Available online: https://eforenergy.org/docpublicaciones/documentos-de-trabajo/wp_05_2016_v2.pdf (accessed on 28 April 2019).

- Freire-González, J. Environmental taxation and the double dividend hypothesis in CGE modelling literature: A critical review. J. Policy Model. 2018, 40, 194–223. [Google Scholar] [CrossRef]

- Labandeira, X.; Labeaga, J.M.; López-Otero, X. New Green Tax Reforms: Ex-Ante Assessments for Spain. Sustainability 2019, 11, 5640. [Google Scholar] [CrossRef] [Green Version]

- IPCC. Global Warming of 1.5 C. An IPCC Special Report on the Impacts of Global Warming of 1.5 C above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, Sustainable Development, and Efforts to Eradicate Poverty. 2018. Available online: https://www.ipcc.ch/sr15/ (accessed on 13 September 2019).

- Groothuis, F. Tax as a Force for Good Rebalancing Our Tax Systems to Support a Global Economy Fit for the Future; The Association of Chartered Certified Accountants: London, UK, 2018. [Google Scholar]

- OECD; The World Bank; UN Environment. Financing Climate Futures: Rethinking Infrastructure; OECD: Paris, France, 2018. [Google Scholar]

- Smith, R. An ecosocialist path to limiting global temperature rise to 1.5 °C. In Economics and the Ecosystem; Morgan, J., Ed.; World Economic Association Books: Bristol, UK, 2019. [Google Scholar]

- IMF (International Monetary Fund). Macroeconomic and Financial Policies for Climate Change Mitigations: A Review of the Literature, WP/19/185; IMF: Washington, DC, USA, 2019. [Google Scholar]

- Smith, R. Green Capitalism. The God That Failed; WEA and College Publications; World Economics Association: Bristol, UK, 2016. [Google Scholar]

- Rudolph, S.; Aydos, E.; Kawakatsu, T.; Lerch, A. How to Build Truly Sustainable Carbon Markets. Solutions. 28 December 2017. Available online: https://thesolutionsjournal.com/2017/12/28/build-truly-sustainable-carbon-markets/ (accessed on 16 February 2021).

- Rockström, J.; Steffen, W.; Noone, K.; Persson, Å.; Chapin, F.S., III; Lambin, E.; Lenton, T.M.; Scheffer, M.; Folke, C.; Schellnhuber, H.J.; et al. Planetary Boundaries: Exploring the Safe Operating Space for Humanity. Ecol. Soc. 2009, 14, 32. [Google Scholar] [CrossRef]