1. Introduction

Fundamentally, socially responsible investments (SRI), also known as “ethical investing”, “green investing”, “values-based investing”, “sustainable investing”, and more recently simply “responsible investing,” and “ESG investing” refers to the notion of investing that considers social, ethical, governance, and environmental issues [

1,

2]. SRI has piqued the curiosity of market participants worldwide [

3,

4,

5,

6]. Every reasonable investor has always been concerned with choosing the best investment portfolio for their hard-earned cash. Investment behavior is influenced by elements, including fund safety, current and capital returns, and liquidity.

Furthermore, as awareness of sustainability has expanded, investors have begun to emphasize businesses that have a social and environmental footprint through their products and services. There has been a rise in investors’ integration of social, environmental, and ethical considerations into their investment decisions [

7,

8,

9].

SRI is an investing strategy that seeks to maximize both social impact and financial returns for investors. SRI is a type of investment that takes into account both the value of a company’s larger influence on the world and its prospective monetary gains.

The popularity of SRI has increased substantially, and eighty percent of institutional investors include ESG factors in their investing strategies [

10]. Assuming 15% growth, ESG assets under management may account for more than the predicted

$140.5 trillion global total by 2025 [

11]. Additionally, the performance of SRI funds during times of crisis is better than that of conventional funds [

12]. As discovered during the 2002 technology (ICT) bubble bust and the 2008 global financial crisis, SRI funds outperformed conventional funds in the USA.

The economic and social effects of environmental, societal, and governance concerns were once again brought into sharp focus by the COVID-19 catastrophe. The crisis has also shown that SRI adoption is not some far-off ideal but rather something that can be performed right now to make communities and businesses more resilient [

13]. During the pandemic, investors’ increasing interest in ESG elements of corporations, implies they perceive sustainability as a need [

14]. During the COVID-19 pandemic shutdown, ESG stocks also protected investors against losses [

15].

Funds that allocate investor money according to ESG issues held

$357 billion at the end of 2021 [

16]. In India, SRI funds have been gaining momentum in recent years, and there has been a rise in interest in ESG investing. Companies, governments, market regulators, and others have stepped up to establish ESG indices and funds in order to educate and entice the country’s investors with the concept of sustainable investing.

Under the category of sustainability, the S&P BSE exchange comprises three indices: “S&P BSE GREENEX”, “S&P BSE CARBONEX”, and “S&P BSE 100 ESG Index” and the NSE index includes the “NIFTY100 ESG Index”, “NIFTY100 Enhanced ESG Index”, and “Nifty100 ESG Sector Leader” [

17]. The AUM of ESG Funds in India is now at

$1839 million as of 31 March 2022, and increasing AMCs are aiming to adopt an ESG strategy [

18]. Incorporating social and environmental concerns into investment decision-making processes, sustainable investing aims at ensuring the development of a green economy and has become an increasingly important component of business social responsibility [

19].

As per the Theory of Planned Behavior (TPB) [

20], a person’s attitude determines their purpose to engage in certain behavior. Based on the preceding facts, it is easy to deduce what drives the rational investor, who considers both financial performance and ethics while making investment decisions. One probable explanation is a person’s attitude, which is the result of his or her moral and ethical beliefs that may affect investment decisions [

21,

22,

23]. Personal values, such as collectivism, and environmental attitudes impact investors’ desires for non-financial outcomes [

24].

The understanding of SRI gives information on how to better explain the requirements and motives of investors. The knowledge can help the investors to lead to a positive attitude and helps in developing the intention for SRI [

25,

26]. As the relevance of sustainable investing is growing with time and more such funds are becoming available [

27,

28], social groups are also influencing intentions towards SRI [

29] with perceived behavioral control [

30] in addition to attitudinal beliefs.

The focus of SRI over the past decade has been on determining how these investments stack up against more conventional ones [

31,

32]. Although researchers have addressed investors’ financial circumstances when making investment decisions, Nga and Yien [

33] argued that the inclination of investors to invest in environmentally accountable companies has been largely overlooked by previous studies.

This study is novel in the sense that, from the outset, we attempted to investigate if collectivism, environmental concerns, financial performance, and awareness about SRI have an impact on attitude for investing in SRI; and second, we examined the impact of attitude, subjective norms, and perceived behavioral control on the investment intention of the investors.

Using structural equation modeling, this research attempts to address the question of how much variance in the desire to invest in SRI, is explained by the factors under study. This study’s research, which is woven into the threads of TPB theory, gives insight into the behavioral traits of investors who are interested in SRI. The added constructs in the TPB model contribute to the theory of sustainable investments with the paradigm shifts in the global financial markets. This comprehension will provide information on how the needs and goals of investors might be better communicated to the key stakeholders. With this information, fund managers may be able to provide a more relevant selection of financial avenues and a more efficient marketing strategy, thereby, improving their ability to service their investors.

The findings of the study have significant implications for policymakers as well, who might apply this knowledge to help promote a capital market that is favorable to SRI. The structure of this study is as described below. The investigation commences with a discussion of the theoretical foundation, followed by the creation of hypotheses and the specification of a model. The section then continues to the research methodology followed by a discussion of the data analysis and study findings. The paper’s conclusion emphasizes the implications, limitations, and scope for further study.

3. Materials and Methods

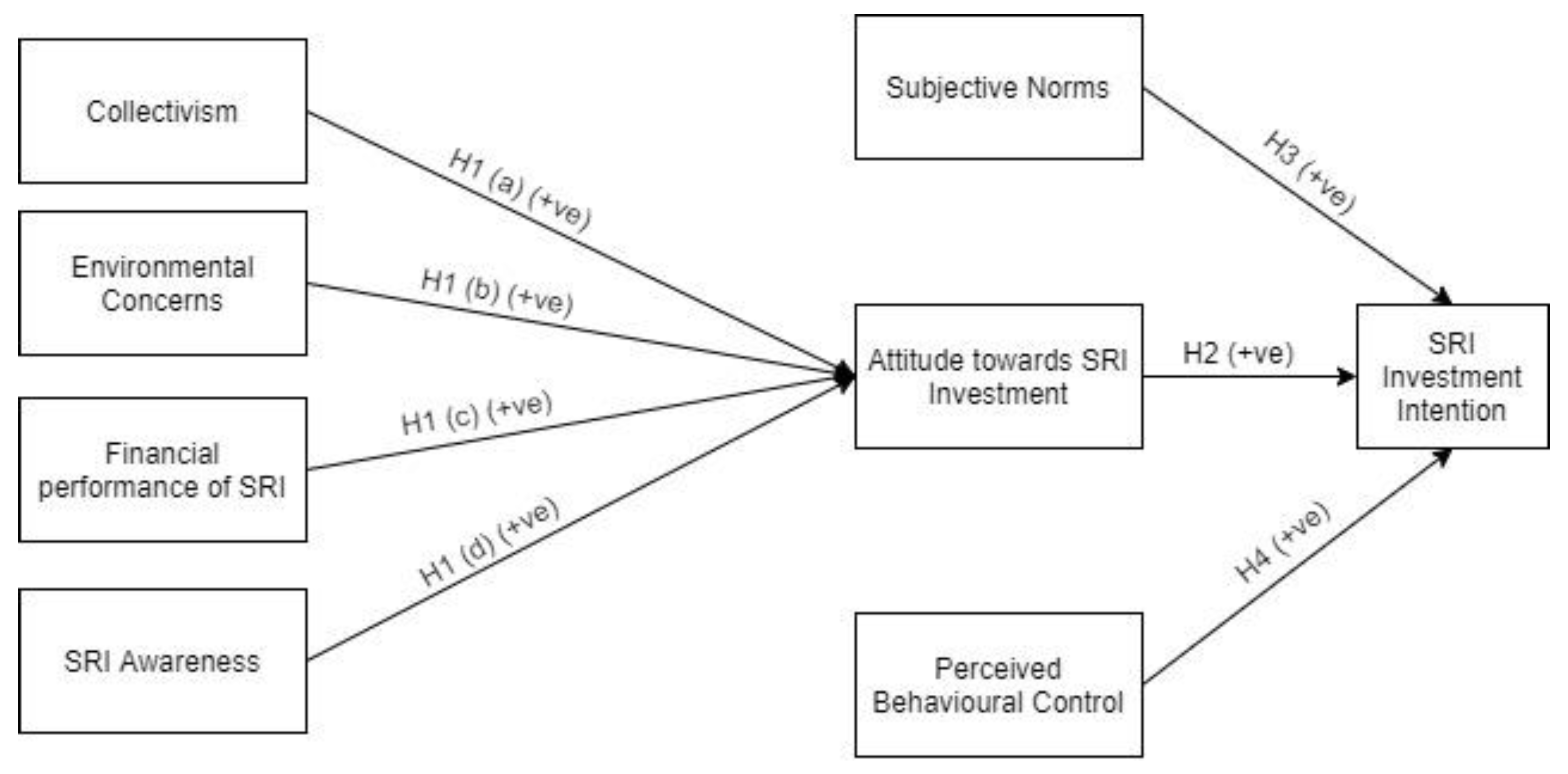

Based on the theoretical model and the hypotheses discussed in the above section, the proposed model is summarized in

Figure 1. The constructs, such as collectivism, environmental concerns, the financial performance of SRI, and SRI awareness, are proposed to have a positive impact on the attitude towards SRI, which is one of the constructs of TPB. Attitude with subjective norms and perceived behavioral control have a direct positive impact on SRI investment intention.

A quantitative approach to research is one that uses numerical data and other quantifiable variables to systematically explore a phenomenon and its relationships [

87]. It is employed to explain, predict, and exert command over a phenomenon by providing answers to questions based on correlations between variables.

3.1. Measurement Scales

The information for the study was gathered by the use of a structured questionnaire. There were three parts to the instrument, the first of which covered the respondents’ demographic data, such as age, gender, marital status, education level, occupation, and yearly income. In the second part of the questionnaire, respondents were questioned to assess the impact of various factors that might affect their intention of making SRI, such as collectivism, environmental concerns, the financial performance of SRI, SRI awareness, attitude towards SRI, subjective norms and perceived behavioral control. The final segment included Likert-scale questions designed to assess respondents’ willingness to invest in SRI. The statements were rated on a Likert scale from 1 (strongly disagree) to 5 (strongly agree), with each statement receiving a score between 1 and 5.

The TPB developed by Ajzen [

20] measure was used in the study to assess the intention of respondents for SRI. This includes (i) items related to the convenience of SRI (three items) to measure the attitude of the investors; (ii) scale based on the referent group and their concern about SRI to measure the subjective norms (three items); and (iii) perceived behavioral control, which states the controlling factors including investor’s skills to invest in SRI (three items).

The scale for collectivism adapted from Singh et al. [

52] includes statements (five items) related to the belief regarding community welfare. The environmental concerns scale (five items) was developed by Singh et al. [

52] and measures the environmental attitude towards SRI. The financial performance of SRI was adopted from Luong and Ha [

88] including statements (three items) of return expectations from SRI and awareness of SRI is taken from Ansu-Mensah et al. [

89] and has statements (five items) related to basic understanding and knowledge of SRI.

3.2. Sample

This cross-sectional descriptive research used a convenient sampling method to gather the required data. Investors in India above the age of 18 participated in the survey. To reach Indian investors, researchers networked with individuals at various brokerage houses in the country, who, in turn, shared the survey link with their clientele. Information was gathered from 557 investors from 15 February 2022, until 6 April 2022. Furthermore, 108 of the 557 replies were discarded because they were incomplete. As a result, 449 responses were processed for additional data analysis (see

Table 1).

3.3. Data Analysis Tool

Smart PLS 3.2.9 software was used to test the reliability, validity, theory, and hypothesis. PLS is a variance-based structural equation modeling (SEM) employing the partial least squares path modeling technique. It is a two-stage model: first, it is evaluated for the quality of the measurements (Measurement Model), and then for the interdependence of the variables (Structural Model). PLS’ ability to test the theory development [

90], the complex linear models with high reliability [

91], and the applicability in non-normal and small-to-medium samples [

92,

93] makes it appropriate for use in the current study.

All latent variables are considered reflective in this study and are assessed using their indicators. The two-stage analytical procedure proposed by Anderson and Gerbing [

94], with the measurement model is evaluated first, and then the structural model evaluated for theory and hypothesis testing is employed here.

The measurement model was checked for reliability and validity using “Cronbach’s alpha” (CA), the “composite reliability” (CR), the “Average Variance Extracted” (AVE), the “Fornell–Larcker criterion”, and the “heterotrait–monotrait ratio” (HTMT) [

95]. Second, the Variance inflated factors (VIF), ‘coefficient of determination (R

2)’, “Standardized Root Mean Square Residual” (SRMR)’, and “Normed Fit Index (NFI)” were considered to check the validity and fit of the structural model. The detailed results are presented in the following section.

3.4. Common Method Bias

“Common Method Bias” (CMB) occurs when differences throughout answers are caused by the tool instead of due to the real bias of the respondents, which is what the instrument is attempting to reveal [

96]. This might be owing to the respondent’s social desirability tendencies, dispositional mood states, or impulses to submit or respond in a mild, moderate, or extreme manner [

97]. CMB also occurs when data is collected through a single instrument for both dependent and independent variables from the same respondent [

96]. The presence of CMB in the data can influence the reliability and validity of the instrument.

These might lead to erroneous conclusions regarding the reliability and convergent validity of a scale [

98]. Additionally, CMB also inflates the path coefficients in structural modeling [

99]. In short, the presence of CMB in data may lead to incorrect research findings, and hence, before starting with the analysis, it must be assured that the data is free from CMB. To investigate the CMB in PLS-SEM, Kock [

99] recommends using the full Collinearity assessment (Variance inflated factors, VIF) test, and VIF values below 3.3 nullify the presence of the CMB. All the constructs successfully passed the test as the VIF values are well below 3.3. Hence, it can be concluded that the data is free from CMB.

3.5. Results and Discussion

As the scales used here have been previously tested for their reliability and validity in prior research, CFA was performed to evaluate the reliability and validity of the measure. At the initial screening, two items had a factor loading of below 0.7 (see footnote of

Table 2); thus, they were removed from the analysis, and the model was run again to check for reliability and validity. Internal consistency/reliability was measured using CA and CR tests [

95]. The CA and CR values of all the variables are higher than 0.7 (see

Table 2) and suggest good internal consistency [

95].

The convergent validity of the model was confirmed using outer loading, Average Variance Extracted (AVE), and CR [

95].

Table 2 indicates that the outer loading of all the indicators is greater than 0.7 (at initial screening, two items were removed), the AVE of all the latent variables is above the minimum prescribed level of 0.5, and the composite reliabilities of all the latent variables were higher than 0.7 [

95]. Hence, the measurement model’s convergent validity is good.

Three methods have been suggested for accessing discriminant validity; the cross-loading test, the “Fornell–Larcker criterion”, and “heterotrait–monotrait ratio” (HTMT) [

95]. It has been advocated that the HTMT ratio should be preferred over the other criteria for confirming the discriminant validity [

95]. “Fornell–Larcker criterion”, and “heterotrait–monotrait ratio” (HTMT) tests were used here to confirm the discriminant validity.

As per Fornell–Larcker criterion “the square root of the AVE of each construct should be higher than the construct’s highest correlation with any other construct in the model.”

Table 3 shows that the square root of the AVE of each construct is higher than the construct’s highest correlation with any other construct (diagonal values in bold). As per the HTMT criterion, the constructs’ HTMT values should not exceed 0.85 [

95].

Table 4 shows that all values are well below 0.85; this reconfirms the discriminant validity [

100].

The assessment of VIF is the prerequisite for the assessment of the structural model [

95]. The Collinearity issue in the construct is fixed with the VIF values less than 5. It can be seen from

Table 5 that all the constructs have VIF values well below 5. After a successful assessment of Collinearity, the structural model was tested using the bootstrapping method with a sample of 5000.

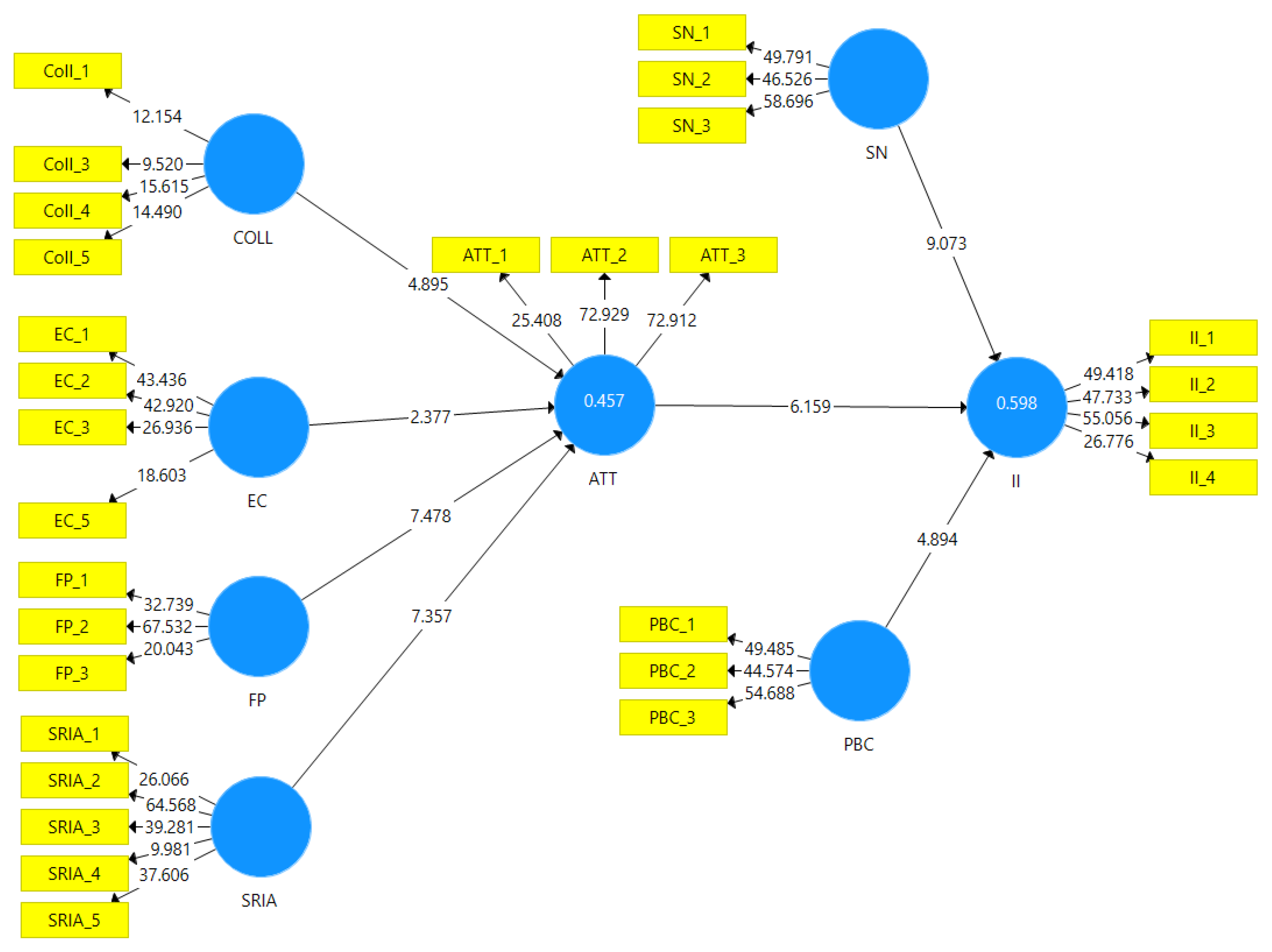

The structural model of the study is presented in

Figure 2.

The ‘model fit’ was confirmed by evaluating ‘coefficient of determination (R

2)’, Standardized Root Mean Square Residual (SRMR)’, and ‘Normed Fit Index (NFI)’. Q

2 was checked for the model’s predictive relevance. The substantial significance of SEM is in examining the level of variance the underlying independent variable explains for the dependent variable [

90]. The values of the coefficient of determination (R

2) are used for this purpose (R

2).

In this current study, investment intention towards SRI is the prime dependent variable, and the R2 for it is 0.598, which indicates that 59.8 percent of change in the investment intention towards SRI can be explained by collectivism, environmental concerns, financial performance, SRI awareness, attitude, subjective norms, and perceived behavioral control.

The predictive relevance of the model was accessed by deriving Q

2 values by performing a blindfolding procedure. Q

2 values greater than 0 suggest that the model has predictive relevance for the [

101] and values greater than 0.02, 0.15, and 0.35 indicate the small, medium, and large predictive relevance of an independent variable to a dependent variable. The current model has Q

2 values of 0.400 (see

Table 6) indicating that the model has a large predictive relevance.

The SRMR value is 0.072, which is less than 0.08 [

95]. The NFI value is 0.83, which is closer to 1 [

102]. Overall, the ‘model fit’ indices show that the model is a ‘good fit’ (see

Table 6).

4. Results and Discussion

Path coefficients were calculated using the bootstrap run in PLS-SEM. This study found a positive effect of collectivism on attitude towards SRI (β = 0.193,

p < 0.05), and these findings are in line with [

51,

52]. Therefore, we conclude that SRI is based on the value system specifically in the countries, such as India, with high cultural values and beliefs. There is a positive impact of environment concerns on attitude towards SRI (β = 0.109,

p < 0.05), which is supported by the studies [

29,

57,

58,

103]. This confirms that economic aspirations are also a driving force for leading to SRI intention.

Thus, a rational and cultured society is likely to strengthen its efforts to ensure sustainable human well-being as individuals become more conscious of the importance of the environment and its long-term impact on society. The financial performance of SRI also has a positive impact on attitude towards SRI (β = 0.354,

p < 0.05), and the results are similar to [

4,

29]. Although SRI carries non-monetary goals, if they generate lucrative financial returns, even investors with weaker SRI values would also become attracted to such funds.

The awareness of SRI positively affected the attitude towards SRI (β = 0.342,

p < 0.05), and the results are supported by [

71,

72,

73]. The financial products are complex to understand so literacy and awareness of such financial products will enhance their investments specifically in emerging countries, such as India. The construct of the TPB model—as with attitude—has a positive impact on the SRI investment intention (β = 0.263,

p < 0.05) and supports the studies [

81,

82]. As a result, it is envisaged that investors who have a favorable attitude toward SRI would have a strong desire to invest in SRI.

Perceived behavioral control on SRI investment intention has a positive impact on SRI investment intention (β = 0.487,

p < 0.05), which is similar to [

78,

85,

86]. This depicts that perceived behavioral control is a factor in investing ethically. The final hypothesis was to analyze the impact of subjective norms positively affecting the SRI investment intention (β = 0.227,

p < 0.05), similar to the studies [

25,

84,

104]. It depicts that, in terms of sustainable investment, peer-group expectations and behavior had a substantial influence on decision-making.

Financial performance was the most significant variable followed by SRI awareness, which influences investors’ attitudes regarding SRI. Perceived behavioral control was the most significant variable influencing the investment intention in SRI followed by attitude and subjective norms (see

Table 7 Standardized regression weight (β) values).

The study’s findings propose valuable contributions toward policy development for various stakeholders, such as the government, regulatory authorities, and fund managers. The findings of the study are significant, as collectivism and environmental concerns not only affect the attitudes of investors but also the investment intentions of investors. A balanced approach should be adopted for designing and offering these funds. The study has significant results showing that investment intentions are highly influenced by subjective norms i.e., peer-group influence. These results reaffirm that investors are less confident in their investment decisions and more likely to follow the advice of their friends, family, co-workers, and acquaintances.

Finance companies and financial advisors can utilize the results to increase the penetration of SRI. We recommend that financial advisers take a more progressive and practical perspective by looking at more than simply demographics and instead paying attention to characteristics, such as attitude, subjective norms, and perceived behavioral control beliefs. Regulatory authorities, fund managers, and the MF companies dealing with SRI funds can market these investment products by considering the findings of the study. They can develop seminars to educate and enlighten investors about SRI investments. To preserve the investors’ individual beliefs on the topic of sustainability, businesses can focus on making the appropriate social and environmental disclosures in their reporting methods, which may also help the investors to make informed investment decisions.

5. Conclusions

Investments have always been centered on making a profit, and this has been true for centuries. The focus of traditional investment decisions has been almost exclusively on this one factor, at the expense of social and environmental considerations. However, the COVID-19 predicament highlighted once again how governance, social, and environmental problems may have significant effects on the economy and society. The crisis also indicated that adopting SRI is not some hazy long-term ideal but something that can quickly boost the agility of our society and enterprises. In this vein, it is important to study the factors that can further accelerate the growth of SRI investments.

In the present study, we concluded that collectivism, environmental concerns, financial performance, and awareness about SRI have significant positive effects on attitudes toward SRI, which, in turn, resulted in SRI investment intention. Intention toward SRI investment was also highly influenced by subjective norms and perceived behavioral control. According to the findings, the subjective norm was the most significant predictor of SRI investment intention, and peer relatives’ perspectives were important in directing sustainable investments.

This indirectly emphasizes that there is a lack of literacy about SRI products amongst investors, and hence investors attempt to mimic the behavior of their friends and peers. In response to this need, financial institutions and mutual fund companies may launch educational initiatives to help savers and prospective investors learn more about socially responsible investing (SRI). In addition, they may provide in-depth training on SRI investing to financial planners and advisers, who can then serve as advocates for the cause.

There are a few caveats to the study’s findings. First, it was done at a certain period in time (a cross-sectional study). Extending the time frame of the investigation is a necessary next step in this field’s study. Changes in investors’ intentions may be tracked over time by collecting (and evaluating) data at regular intervals. Second, although this study’s sample size is sufficient for doing structural equation modeling [

105], future research should explore a larger sample to account for sampling mistakes.

Third, this research focused on SRI and found that the attitude and intention toward these investments are influenced by collectivism, which is influenced by each culture, and thus the finding cannot be extended to all cultures. Fourth, the study was conducted adopting the TPB model. In the future, other studies will include the Stimulus–Organism–Response (SOR) model for adoption intention. Lastly, the current study focused on four factors: collectivism, environmental concerns, financial performance, and SRI awareness towards attitude toward SRI, whereas there are many other factors related to the investor personality or moral values that were not considered and can be included in future research.

,

,

{kind=link}

{kind=link}