European Green Transition Implications on Africa’s Livestock Sector Development and Resilience to Climate Change

Doctoral School of Regional and Business Administration Sciences, Széchenyi István University, 9026 Győr, Hungary

*

Author to whom correspondence should be addressed.

Sustainability 2022, 14(21), 14401; https://0-doi-org.brum.beds.ac.uk/10.3390/su142114401

Submission received: 26 September 2022

/

Revised: 25 October 2022

/

Accepted: 27 October 2022

/

Published: 3 November 2022

(This article belongs to the Special Issue Sustainable Agri-Food Systems: Environment, Economy, Society and Policy)

Abstract

:Green growth and the transition towards green growth are gaining scientific and public interest across Africa at an unprecedented rate. The Paris Agreement ratification by all 54 member states and the African Union (AU) goals in its Agenda 2063 on green economies are sufficient evidence of this. This is in line with the European Green Deal (EGD) aspirations, which envisages making Europe a carbon neutral economy by 2050. One of the EGD’s four main pillars is sustainable food systems. The success of EGD is premised on its ability to inspire and support green transition and effective climate action globally. The borderless nature of climate change necessitates a holistic approach to ensure the EU’s green transition does not come at the cost of development elsewhere. The main challenge is finding Africa’s space and position within the desired holistic approach, as Africa’s economy is agriculturally driven. One key African agricultural sub-sector significantly impacting livelihoods is livestock, which supports up to 80% of the rural livelihoods and which grapples with challenges in satisfying the needs of a fast-growing population. What could the EU green transition mean to this sector? We established that between 2010–2019, the African livestock population grew exponentially, and feed production followed the same path, with the share of land under forests, grasslands and meadows declining drastically. Over the same period, the percentage of land under arable farming increased while the animal-based protein and meat imports curve grew exponentially. This situation puts the continent in a dilemma about finding a sustainable solution for the food–feed and environmental nexus. Against this backdrop, a myriad of questions arises on how the green transition can be established to promote mitigating any loss that might occur in the process. We conducted a detailed sectoral trend analysis based on Food and Agricultural Organization (FAO) statistics to find plausible solutions and pathways to achieve a greener transition. We coupled it with intensive policy mapping to develop science-policy-driven solutions that could promote the green transition sustainably. To sustainably accelerate the sectoral growth trajectory while addressing climate change, we recommend adopting and implementing raft measures geared towards increased sectoral efficiency, effectiveness, innovativeness and a holistic approach to the problem. Adopting transformative policies can promote the sector’s competitiveness through incentivisation, technological adoption, financial support, market support and increased awareness of its importance in sustainable development. However, exercising caution in implementing these practices is crucial to ensure there is no leakage effect in implementing the EGD across Africa and beyond.

1. Introduction

Development is among the top driving forces for increased demand for livestock-derived foods globally [1]. The world is experiencing a growth of more than four times in absolute and per capita terms compared to 1960 levels [2]. In addition to development, a rapidly growing population has been fuelling the expansion of the livestock sector. However, growth has been associated with environmental externalities ranging from the exploitation of limited natural resources to increased greenhouse gas (GHGs) emissions, exacerbating global warming and, thus, climate change [3,4,5]. Such tendencies are the main drivers that have necessitated the establishment of resilient food systems that can thrive in such environments. Although many factors influence consumer behaviour, evidence-based research shows that the majority now recognise that the livestock sector significantly impacts global ecosystems [2,3,4,6]. Although the trend has been evident on the international stage, in Africa, where population growth over the past decade has surpassed expectations, the impacts are more apparent. However, from a futuristic lens, the situation remains blurred due to conflicting interests of a climate-neutral future, resilient food systems demand and inverse consumption patterns in Africa.

Over the last decade, Africa’s livestock production and product consumption patterns have been experiencing exponential growth. The tendency has been in line with the global demand for livestock products, which is projected to double by 2050 due to rapidly increasing living standards [7,8]. The Food and Agricultural Organization of the United Nations (FAO) estimates that sectors across Africa will experience a growth of 40% by 2050 [9]. Additionally, the demand for animal-based protein from the fast-growing population is expected to double by 2050 [10,11,12].

Doubled population growth and increased consumer behaviour threaten the livestock sector’s sustainability [12]. Addressing sustainability today is one of the grand challenges the world is experiencing despite the dimension under consideration. This can be considered a litmus test for sustainable and resilient food systems aspirations. The livestock sector has contributed immensely by providing diversified products and services. Therefore, the focus is more likely to shift from enhancing the sector’s production capacity to improving its resilience and sustainability towards climate change [12,13,14]. The demand for enhanced resilience across the sector in Africa is highly driven by the increased demand for its output by the fast-growing population in a rapidly changing environment exacerbated by climate change [9]. Consequently, the focus is aligned with the Sustainable Development Goals (SDGs) on people, the planet and livestock.

The sectoral impacts and effects across the continent concerning SDGs and Africa’s Agenda 2063 appear both direct and indirect. In line with these strategic goals, offsetting growth and development in rural areas, creating employment and steering sustainable economic growth are among the roles the sector is expected to contribute to significantly [15]. Adopting multiple commodity approaches and value-addition-driven sectoral markets to ensure highly efficient circular and effective value chains will be a game-changer across a sector that can contribute to the food system’s sustainability. Establishing such state-of-art value chains, especially in rural areas, is a function of transitioning towards attaining intensive efficient and resilient systems or adopting value-added methods. In addition, the associated outcomes must embrace the advocacy for sustainable consumption and production patterns to enhance regional and household capacities in coping with the effects of climate change [16].

Africa’s emergence as one of the fastest-growing regions across the world over the last two decades has increased its likelihood of increased per capita consumption due to excess disposable income availability. This trend is mirrored in an analysis of the comparison of the per capita meat consumption and the per capita GDP over the last decade in Africa, which presents a positive correlation. However, if the growth trajectory persists, sectoral capacity enhancement, resilience and sustainability must be emphasised. On average, in the last decade, the continent average Gross Domestic Product (GDP) growth was 4%, with an upward projected growth trajectory [17]. Similarly, FAO and the World Bank, between 2000 and 2013, reported that the demand for food products from animals was increasing, attributed to gains in per capita income, urbanisation and population growth [16,18,19]. In addition, a policy analysis by USAID [19] reported that the increased demand for animal-sourced foods in Africa outweighed local production, attracting imports. They recommended that governments and relevant stakeholders carefully execute planning while ensuring decision-making is exercised with extreme caution to avoid adverse consequences such as exerting pressure on natural resources (specifically water and land), which are already constrained [20].

ILRI further expounds that, on average, the livestock sector contributes to approximately 40 per cent of agricultural GDP, which goes up to 80 per cent in some member states [21]. Livestock in Africa has been associated with a fundamental role in earning incomes for rural livelihood, increasing the resilience of the smallholder mixed crop/livestock and pastoral systems [16,17,19,22].

Although growth across Africa continues to happen at an unprecedented rate, it combines different forms of growth. One common approach is the green transition which has been characterised by all African member states’ adoption of the Paris Agreement and the African agenda 2063 [23,24]. The green transition has been supported by the AU in different programmes, with the latest being the African Green Stimulus Programme (AGSP) [25,26]. The presence of good roadmaps and initiatives is an indicative path to adopt the practices being championed across Europe. However, the main question is on the practicability and the implementation process bearing in mind that different African countries are experiencing different development paces. This is evident in the evaluation report on the Millennium Development Goals (MDGs) performance, where the countries performed differently [25]. When further scaling down to the sectoral level, the magnitude of the challenge intensifies, necessitating corroborated efforts to ensure a holistic approach to address the challenges at the sectoral level.

Africa, the most vulnerable continent to climatic shocks worldwide, has prioritised the agricultural sector’s adaptation to climate [27]. Severe droughts compound the effects, especially for the livestock sector, which is mainly extensive and relies on rainfed feeds. Increasing resilience and the capacity of the sector to thrive in such an environment coupled with competition for resources becomes essential. In the spirit of green transition, the sector, if well planned, is a source of renewable energy through biogas production. FAO explains how African agriculture is becoming more sensitive to climate change, resulting in an increased demand for climate-smart agricultural practices for green transitions across Africa [28,29].

The European Green Transition necessitates stricter carbon/environmental policies and regulations. The Farm to Fork (F2F) and the Biodiversity Strategy as the implementing strategies are cornerstones of the agricultural sector [30,31,32]. Eco-design and green products for the agricultural sector, especially the exporting economies, are more likely to pressure the sector to meet the requirements envisioned in their impact on global food systems [30,31,32,33]. How could these stringent measures impact the African livestock sector? The effect on the livestock sector has to be associated with the production aspect since Africa deals primarily with primary production and less processing. Any process that can potentially interfere with primary production will produce a ripple effect on the entire value chain and spread worldwide through trade. The existence of plenty of green minerals across Africa makes it a close ally to Europe in the carbon neutrality transition [33]. To meet the objectives of the green transition, Europe’s demand for certain critical raw materials is projected to increase, with that for lithium expected to grow over forty times, whereas graphite, cobalt and nickel demand are expected to grow by around 20 to 25 times by 2040 [33,34]. Increased exploitation of these minerals will significantly reduce the available grazing land competing with the livestock sector. The growth for these green minerals is projected to continue growing to meet the global demand; the input of these materials for batteries, fuel cells, wind turbine turbines, photovoltaic systems for renewables and electric vehicles in the EU are currently in strong demand [33,34,35]. The main question is how Europe can maintain the balance between these green minerals and the livestock sector to ensure the advancement in carbon neutrality does not happen at the expense of mineral resources, which further dilapidates the livestock sector.

The Farm-to-Fork Strategy (F2F) can be simplified to establish resilient and sustainable food systems with a lower environmental footprint [36,37]. Implementing circularity can be a plausible pathway in maximising every aspect of the value chain across the desired food systems [37]. Although primarily the implementing strategies focus on European food systems, supporting other global food systems emerges as part of European external policy instruments [38]. In the determination of the impacts of the F2F strategy, Beckmans et al. 2020 modelled three scenarios on the adoption of the EGD ranging from EU only, EU and other countries and the entire world and the associated impacts of implementing strategies (F2F and Biodiversity) targets on input use and land use change [39,40,41]. They applied the Computable General Equilibrium (CGE) Model and the Global Trade Analysis Project–AgroEcological Zones (GTAP-AEZ) model to understand the impacts associated with implementing the strategies objectives. These models were instrumental in understanding the potential market and economywide impacts of adopting the strategies [39,40]. They reported that significant environmental benefits are achievable in the short run due to reduced food production in the long run. They highlighted the inevitable reduction in the European production of cereals, oilseeds, dairy cows, beef, pork and poultry. These are crucial products for food, feed and biofuel production. A reduction in any of these commodities will translate to increased imports, triggering production and land use change elsewhere [39,40,41]

The results so far predict that the value of European agricultural production could be 12% lower by 2030 because of the F2F’s input and land use targets [40]. The EU has continued to invest heavily in innovation, research and state-of-the-art technologies in the agricultural sector to ensure sustained agricultural production. However, research and historical trends have indicated that across the agricultural sector, such investments can take decades to materialise in productivity improvements [42,43,44]. In addition to production, other projections have been made based on consumption and dietary change, which proposes that if Europeans shift to more sustainable diets, lower production will not attract increased imports. However, they will be associated with fewer exports [45]. Although the modelling by Beckam et al. 2020 did not consider a shift in dietary change, it is a precautionary factor which cannot be avoided in modelling for a holistic view of future changes and scenarios [46,47,48,49].

Relating the impacts of reduced food production across Europe as a result of the implementation of the F2F and Biodiversity Strategy is more likely to impact EU agricultural trade, leading to fewer agricultural exports from the EU and more agricultural imports into the EU [39,41]. As a global leader in agricultural trade, the EU is the largest exporter and second-largest importer of agricultural products [31]. Such changes are more likely to distort global food prices [39,40,41]. An increase in global food prices in the short run is good news for the rural community and agricultural exporting economies such as Africa. However, it is more likely to lead to food insecurity in the long run due to increased competition for scarce commodities, especially for poor economies such as Africa [50,51]. This scenario could further worsen the situation in African countries due to their high food import dependency, which is likely to increase further [52,53,54]. Similarly, this could also increase the farming land resulting in less availability of grazing land and the destruction of forest areas and grasslands. The complexity of the market dynamics could further lead to a spiral effect on consumer prices outweighing that of producer prices, especially in those African countries where the urban population is rapidly growing and depends on declining rural populations’ increasing poverty levels [39,40,50,55,56].

If the above findings on declining production across Europe and triggering production elsewhere globally are anything to go by, then Africa stands the most excellent chance to gain. According to FAO, Africa has 60 per cent of the world’s uncultivated arable land [57,58]. However, most of this uncultivated arable land is under grasslands and forests; thus, a global shift in production is more likely to induce high-risk direct land use change, undermining the environmental benefits aspirated under the EGD [41]. This complicates the green transition process that is predicated on the sustainable implementation of practices. Some of the implementable measures include additionality measures, production in abandoned lands, sequential cropping, agroforestry, eco schemes and silvopastoral systems to promote environmental stewardship and ensure feed production can be met simultaneously.

Another outcome associated with the global shift in production from Europe could be increased GHG emissions. Over recent decades, Europe has established itself as one of the most efficient production systems with fewer emissions per unit of production compared to the rest of the world. Research has shown that shifting the production of 1 kg of chicken meat from Europe to Africa would increase GHG emissions from 0.3 kg to 1.14 GHG eq. This is approximately four times the increase in GHG emissions. Reducing such emissions intensities across Africa would be a nightmare, and long-term investment such as implementing infrastructure and technology would require more time and funds [59].

However, it must be noted that a total change in farming practices across Africa is unavoidable if food security is to be achieved. Currently, the primary African mission is to overcome food insecurity. The prioritisation of green transition is considered a second option across the developing world compared to the European pace [39,40]. To promote the active participation of Africa in the Green transition, the EU, through its trade policy, must promote continued support of small-scale farmers through opening access to the EU market and more financial incentives for Africa to practice sustainable farming practices [60]. In adopting such a joint and blended financing mechanism for African countries, the EU will promote sustainable agricultural practices, which hold a high potential to reduce already experienced land degradation [57,61]. In its current state, the EGD does not advocate external adaptation to climate change, and a lesser budget has been allocated for the Neighbourhood, Development and International Cooperation Instrument (NDICI) in the Multi-annual Financial Framework (MFF). Thus, a limitation to the scope of promoting green transition is beyond its borders (NDICI) [62,63].

Financial incentives are among the most significant challenges for green transition across the African agricultural sector. The African Development Bank (AfDB), in it its annual 2018 report, outlined the current levels of climate financing across the continent as insufficient. Most of the available funding for green transition is in the energy sector, funded by a private partnership. The agricultural sector, with its potential to decarbonise the African economy, needs to receive more funding. Despite the funding being challenged by the energy sector, there exists little information on the true cost associated with degradation and environmental exploitation, degradation and land-use change dues to a greener transition. Therefore, there is a need for an appropriate governance framework and enabling the regulatory environment to prioritise agricultural sector funding for a green transition [64,65].

Therefore, it is paramount for policymakers, when deciding on global trends, to consider the specialities and peculiarities of Africa, especially reducing meat consumption in Africa. Although such orders and initiatives could cause conflict in a continent where food security is a priority rather than sustainability, a friendlier approach is more likely to reduce the foreseen effects. The Joint Research Centre (JRC) of the European Commission predicts a decline in cereals and oilseeds across the EU if the F2F and Biodiversity strategy is to be attained, leading to a 14 per cent decrease in meat supply and triggering increased imports by approximately 22%. Although the EU is a market player in pig meat export, a reduction of 77% is projected by 2030 if the EGD targets are implemented under the adoption of the EGD by the entire world scenario [39,40]. Declined exports due to increased and uncompetitive market prices across Europe could further weaken the accessibility of the commodity in Africa [66,67].

The high number of drivers for increased livestock product demand and consumption across Africa is a solid foundation for the sector’s sustainability if careful, well-defined decision-making, planning and support mechanisms are implemented. Transformative growth for the sector is guided by increased resilience towards externalities, sustainability and increased efficiency and competitiveness in the global market [21,66,67]. This research sought to find out what mechanisms must be implemented based on evidence from the past and present to inform sound decision-making for a sustainable sector’s future. We realised this through a systematic assessment of the sectoral performance in terms of production, consumption and trade-economic growth of member states and regional policies shaping the sectoral performance from a macroeconomic point of view. We addressed the research goals holistically by determining the most in demand and produced meat in Africa and the leading players satisfying the demand to realise this goal by linking them to the effects of the EGD. Additionally, we evaluated how such interaction influences and accelerates climate change. This was further supplemented by mapping the enabling policies, their gaps and proposed measures that can be put in place to promote sectoral sustainability.

2. Materials and Methods

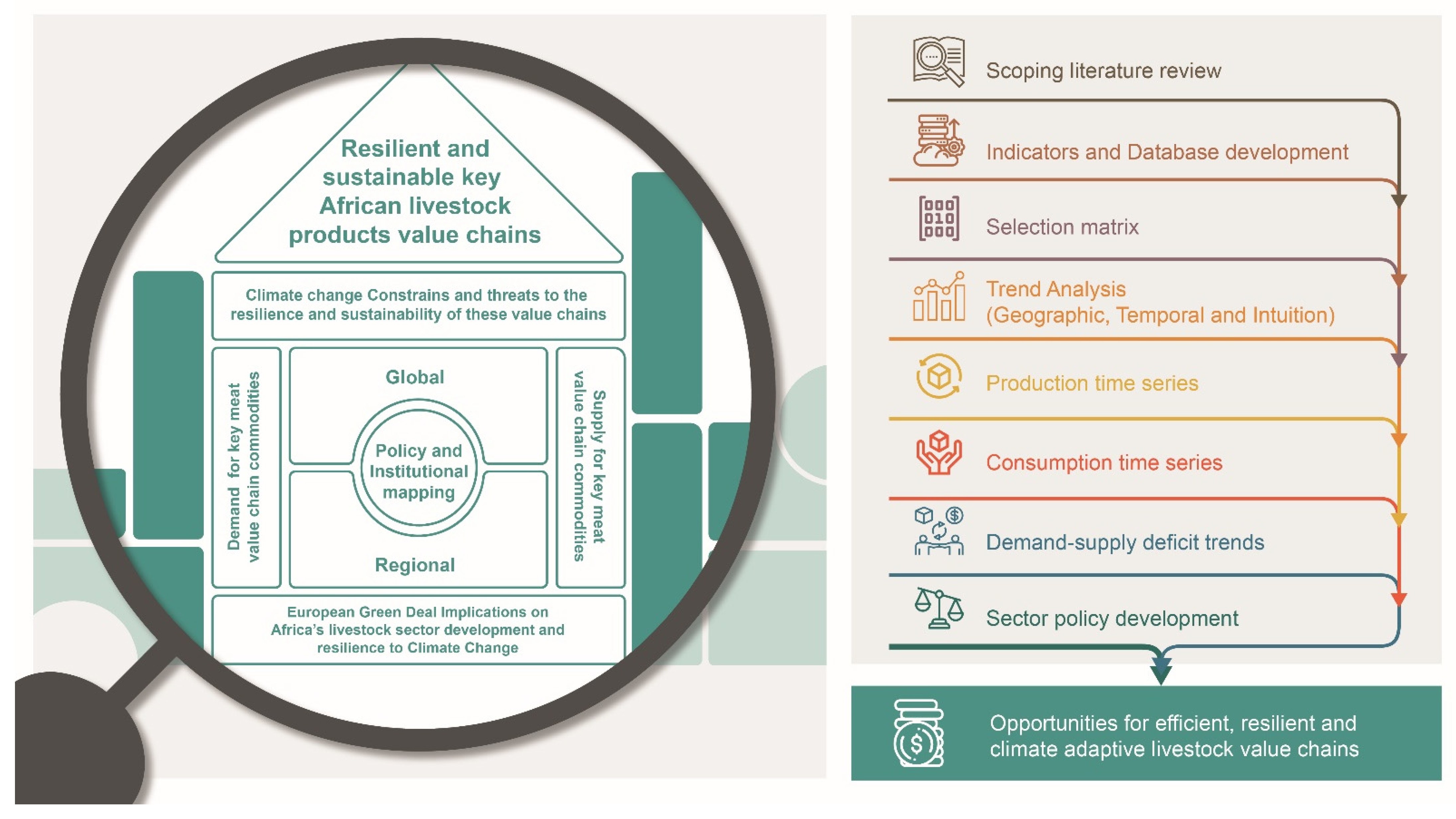

Addressing complexity requires nuanced methodological approaches in their simplest form ever. Therefore, we employed a combination of methodologies to address the above three objectives as conceptualised in Figure 1 below. However, our methodology was premised on the sustainability of the African livestock sector in the face of rapidly growing drivers of climate change that should be integrated and enhanced. The decision and choice of enhancement is a derivative of the development path an economy pursues, its climatic zone and the internal and external market forces.

The first step was to create a linkage between the three objectives. Then, to make an informed decision, we opted for trend analysis [25], building it on three interconnected aspects (Geographical, Temporal and Intuition), which was the guiding methodological framework, with sub-methodologies adopted across each stage. Finally, we related how growth in the drivers for development could accelerate the supply of meat-derived products and how addressing it could exert pressure on the limited natural resources, as presented in Figure 1.

We subjected this scope analysis to African countries to observe their trends. We narrowed it down to specific countries that are key players across sectoral value chains across the continent. Many factors are fuelling economic growth across African countries, with the livestock sector being one [13,68,69]. We based our assumption on the relationship between these factors and how they influence the sector in a rapidly climate-changing environment. System thinking or a holistic approach formed the basis for defining and selecting the right indicators to characterise the complex relationship. This was realised by reviewing the literature on how the sector’s performance could relate to sustainable growth and development and increase resilience to climate change. We collected and analysed the data of the respective indicators from FAOSTAT and the World Bank for the case of the Human Development Index (HDI) and the Gross Development Product (GDP) for all African countries. We further subjected these choices of indicators to their contextual relationship with the livestock sector, establishing how they could influence or be influenced by sectoral developments. Moreover, we conceptualised how such a development path could lead to different outcomes by comparing it to the three scenarios presented in the literature on adoption levels of the EGD [39,40,41]. We construed how living standards influence resilience to climate change and animal production tendencies.

An increase in the development drivers necessitates the demand for more meat, thus increasing demand and triggering increased production, which exerts pressure on available natural resources. Exerting pressure on natural resources increases the likelihood of climate change escalating further [3,5,10,13,16]. Sectoral production under constrained resources grows until a certain level when the ecosystem cannot absorb more effort to produce (carrying capacity) [70]. With the projected drivers to continue growing and widely changing consumer behaviour evident, a market gap arises, necessitating importing constrained products to meet the local demand [71]. Increased trade further exerts pressure on the resources, worsening the situation when the pressure is from a different geographical location [72,73]. Based on the interlinked nature of the value chain and the resources required, shifting production is not a long-term solution but increasing resource utilisation efficiency to produce effectively may be [74,75].

With 54 countries across Africa, carrying out a trend analysis for all the countries is a time-consuming and expensive exercise; thus, selecting those significant countries where the production of primary commodities was imperative. Selecting these countries was based on the outlined indicators, where countries had to appear in the top ten of the selected indicators. The set of indicators was selected based on the assumption that they directly influence livestock production and negatively influence climate change. We further conducted continental policy and institution mapping and their relevant impact over time in transforming the sector.

3. Results

3.1. Indicators and Database Development

The data in this research resulted from intensive data collection from FAOSTAT, and involved cleaning, sorting and aggregating the top 10 countries in each of the selected 11 indicators. As presented in Table 1, the selected indicators were derived from the scooping literature review elaborated on in Section 1. The most frequently occurring countries were selected for specific product analysis in combination with other parameters presented in Figure 1 and literature insights. The outcome resulted in the following selection matrix presented in Table 1: Angola, Benin, Cote d Ivoire, Egypt, Ghana, Malawi, Benin, Rwanda, South Africa and Zambia. However, the list could vary based on the local cultural practices, which could change the demand for the associated livestock product.

3.2. Africa’s Livestock Production Capacity Trends and How They Are Influencing the Sector

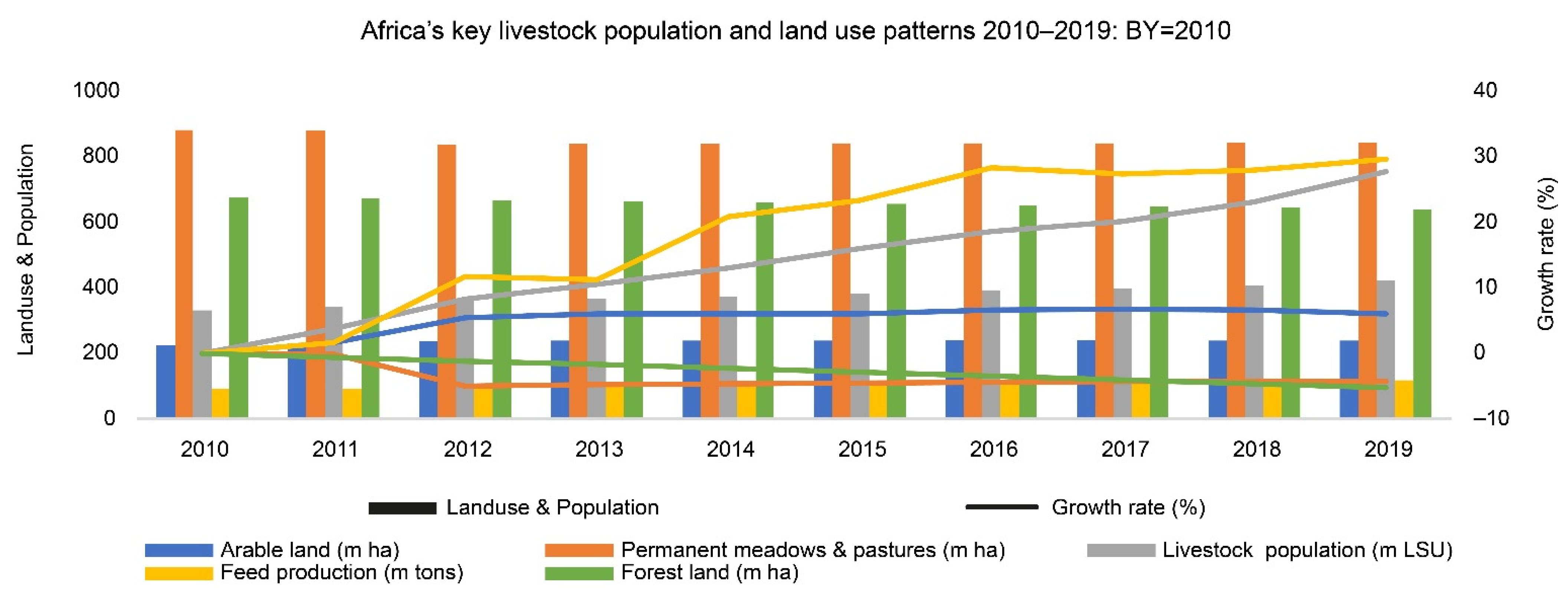

The rapid growth in demand for livestock products across Africa over the past decade has emerged as the new standard [13,14], where demand outpaces production capacity (supply), forcing the increased product flow into the regional market to meet the gap [9,68]. Although material flow is rising, a similar trend in the livestock stocks continues to grow indicating that the production capacity cannot meet local demands despite the upward growth trend [17]. Between 2010 and 2019, livestock stocks grew exponentially by 28 percentage points as summarised in Figure 2. The associated growth increased demand for feed production and outpaced the population.

This represents a positive correlation between increased population growth and feed production. Furthermore, feed production remained constant until 2011, when it grew exponentially until 2013 and stalled due to prevalent drought, and afterwards, average growth resumed.

However, as growth in both population and feed production was evident, the land under permanent grasslands and meadows and that under forests have been declining significantly with a decline of 5 percentage points. We further found that between 2010–2012, the land under arable land increased coupled with increased feed production. Thus, we can conclude that the area under permanent grasslands, meadows and forests was converted to arable lands to facilitate feed production. Although there could be other significant factors that accelerated growth, we cannot afford to out rule this relation where under a business-as-usual scenario, negative synergies will continue to exist between the sector and land-use change, thus exacerbating climate change.

Research by Carnegie University shows that if land use changes and degradation across Africa grows at the same pace as it stands today, there is a higher likelihood that by 2050, all the utilisable agricultural lands will have been degraded [65,66]. This creates an area of cooperation between Africa and the EU to promote combating agroecological challenges while addressing the effects of low indirect land use practices [65,66].

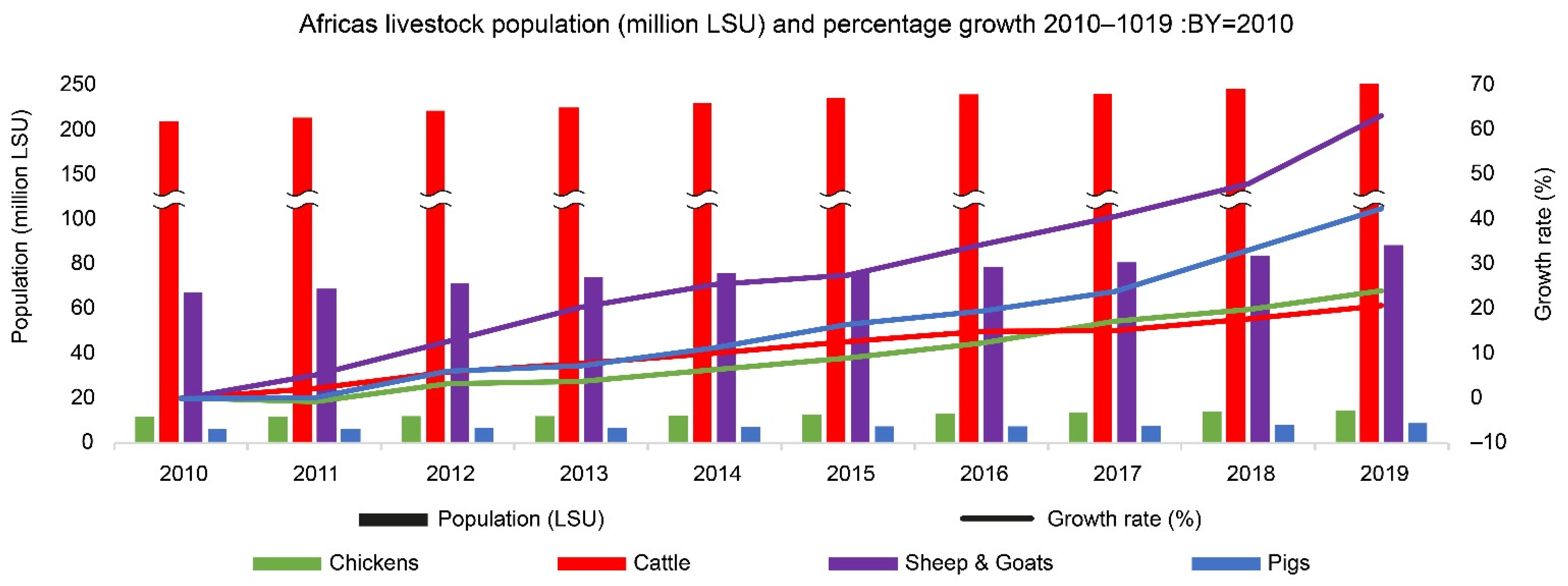

To equally compare the performance in stocks for the crucial livestock, we converted the population in absolute numbers as recorded in an FAO stat to Livestock Units (LSU). In reversing the total population to LSUS, we combined FAOSTAT and European Commission conversion factors [76,77]. For tropics and the peculiarity of the African sector compared to the EU, and for those conversion factors that were missing in the FAO classification, we adopted the EU lowest value of the specific animal category. Although this might not be the reality for tropical, scaling down the factors was crucial.

As a result, Africa’s livestock population between 2010 and 2020 grew by 27.33% from approximately 331.032. to 433.885 million LSUs, as presented in Figure 3. The growth was modest for pigs (97.14%), followed by camels and chickens with 80.60% and 70.65%, respectively. The pig population grew from about 6.22 to 8.804 million LSUs, while that of chickens grew from 11.645 to 14.446 million LSUs. Although camel stock increased upward, the population is only concentrated in a few countries. This confirmed our first criteria in settling for the key-value chains derived from pig, poultry, dairy and egg as alternatives. Although the other value chains are essential, the study focused on these, which emerged with modest performance over the period under analysis.

There is an increasing trend across all livestock population types. The growth trend for pigs and poultry shows a similar growth trajectory, with that of pigs being more pronounced similarly to their respective meat production. Post-2015, all the population types experienced exponential growth, as summarised in Figure 4, attributable to rising livestock density across Africa. As the livestock population density is rising while that of natural resources is reducing, increasing efficiency in feed production, system management and resource utilisation are paramount for reducing the pressure already exerted on natural resources due to declining grasslands cover and forests [22,68]. Furthermore, adopting an integrated approach to the problem for diagnosing the sector ensures increased efficiency and innovativeness while adopting circular business models across the value chains to promote sustainability.

3.3. African Livestock Products Consumption Tendencies and How They Influence the Sector

Africa is experiencing an unprecedented demand for livestock-derived products, characterised by a fast-growing market, as portrayed by consumption tendencies, which are part of an exponential trend. This can be associated with the fast-growing production trend, as presented in Section 3.2 above.

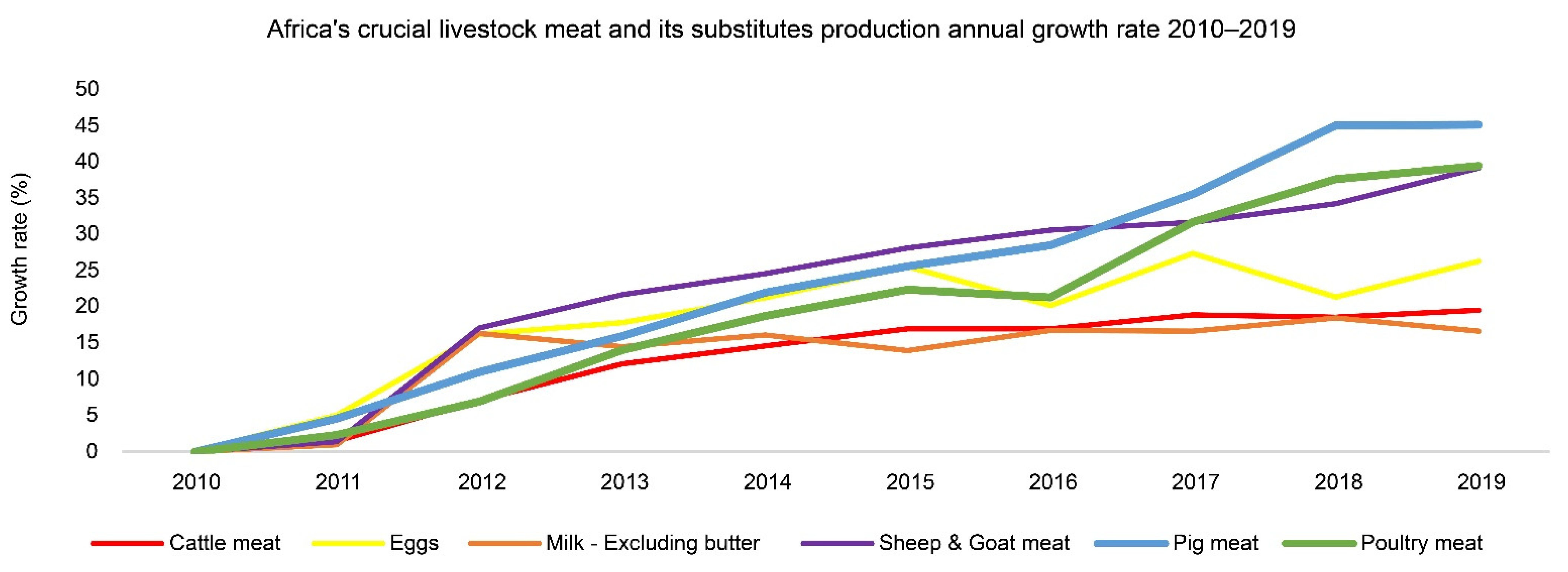

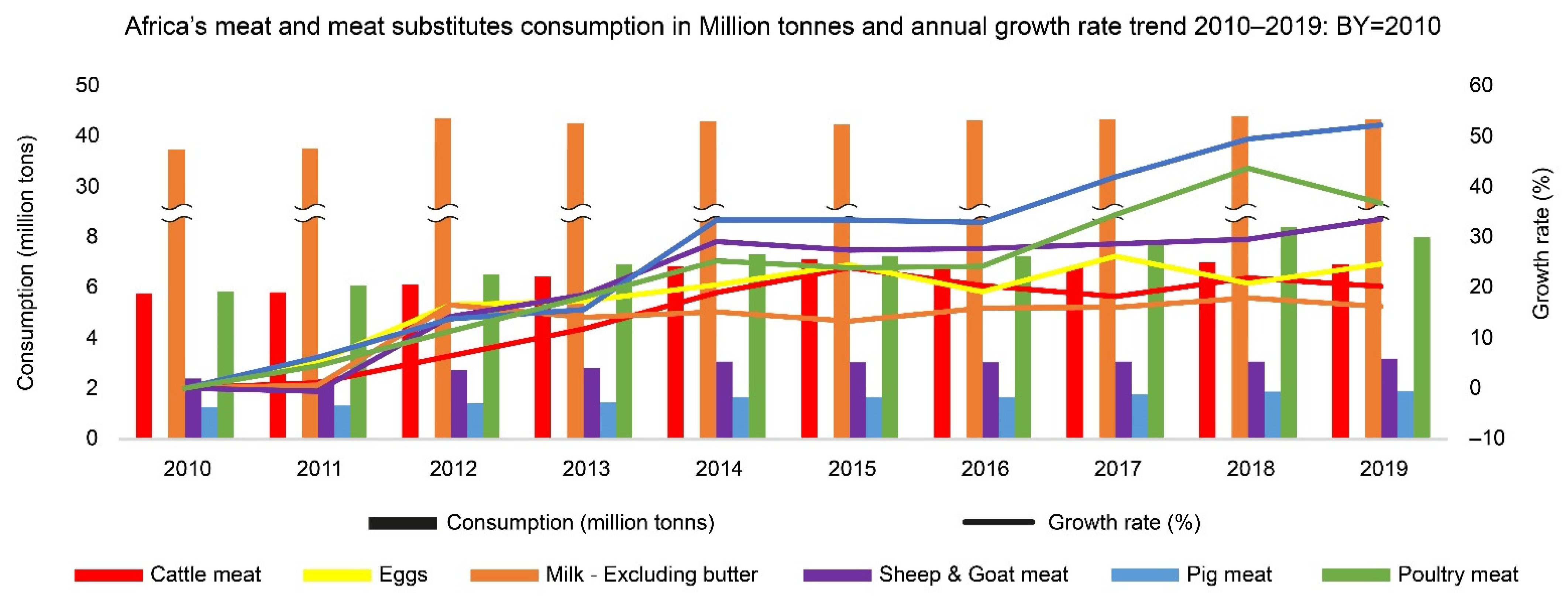

As a result, demand has been growing more rapidly than supply, necessitating growth in import activities to meet the deficit. Although the trend varies by product type, in terms of per capita meat consumption by type between 2010 and 2019, poultry meat consumption grew from 3.2 to 6.73 kg/person/year, while that of pig meat increased from 1.05 to 1.47 kg/person/year as summarised in Figure 5. Globally, meat’s average per capita consumption stood at 14 kg/person/year and is expected to grow to 27 kg/person/year by 2050 [14].

Although per capita consumption is not a good indicator, especially in instances where the population grows faster than output, we thus analysed the absolute consumption in million tonnes of the respective meat types and their substitutes (milk and eggs).

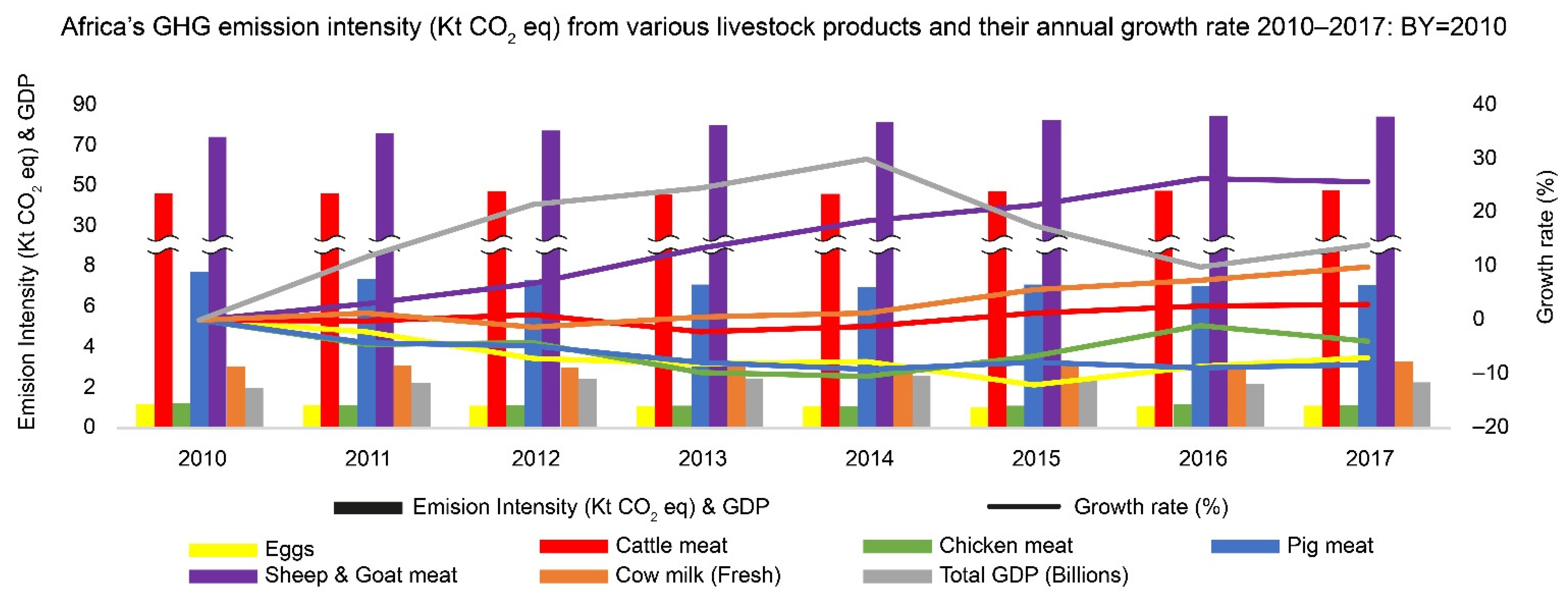

To a greater extent, consumption growth is highly driven by favourable market prices, especially for poultry-derived products and the low environmental impacts of poultry and pig meat. Between 2010–2017, the GHG emission intensity by meat type grew. Although growth in GDP was realised, there was an inverse relationship between GDP growth and emission intensity for poultry and pig meat. This shows that as GDP was growing in Africa, many consumers had disposable income to purchase expensive beef, rendering the emission intensity of poultry and pig meat compared to the others. From 2014 onwards, increases in poultry and pig meat emission intensity have grown, which can also be explained by the high consumption of cheaper meat, as presented in Figure 6.

Coupling such a trend with natural resources and a rapid growing consumer-driven population creates a demand-supply imbalance, triggering commodity inflow from elsewhere. As a result, growth in imports is dominant across pig and poultry meat and milk, whereas it declined for sheep and goat meat, as summarised in Figure 7. With chicken and pig meat as the most consumed meat by type, a similar trend is observable in their emission intensities and imports. Therefore, under the business-as-usual scenario, the African GHG intensities of meat and derived products will remain high in upcoming decades.

Demand continues to grow exponentially, with annual growth rate projections of 2.2 per cent, with that of both pig and poultry at 3.3 per cent [12,78]. The growth is modest across poultry meat, which is most likely a result of their lower cost than other meat types. Accessibility is also another factor, or making it easily accessible to a rapidly growing class of the middle-income population. Additionally, poultry meat demand growth could be associated with dietary shifts and increased preference for white meat over red meat due to its environmental friendliness [79]. Although the latter might not apply in low-income countries, it could play a pivotal role in global meat markets from a futuristic lens. The difference in demand and supply capacities is projected to result in a trade deficit creating market-driven opportunities for private sectors and partners across Africa [80].

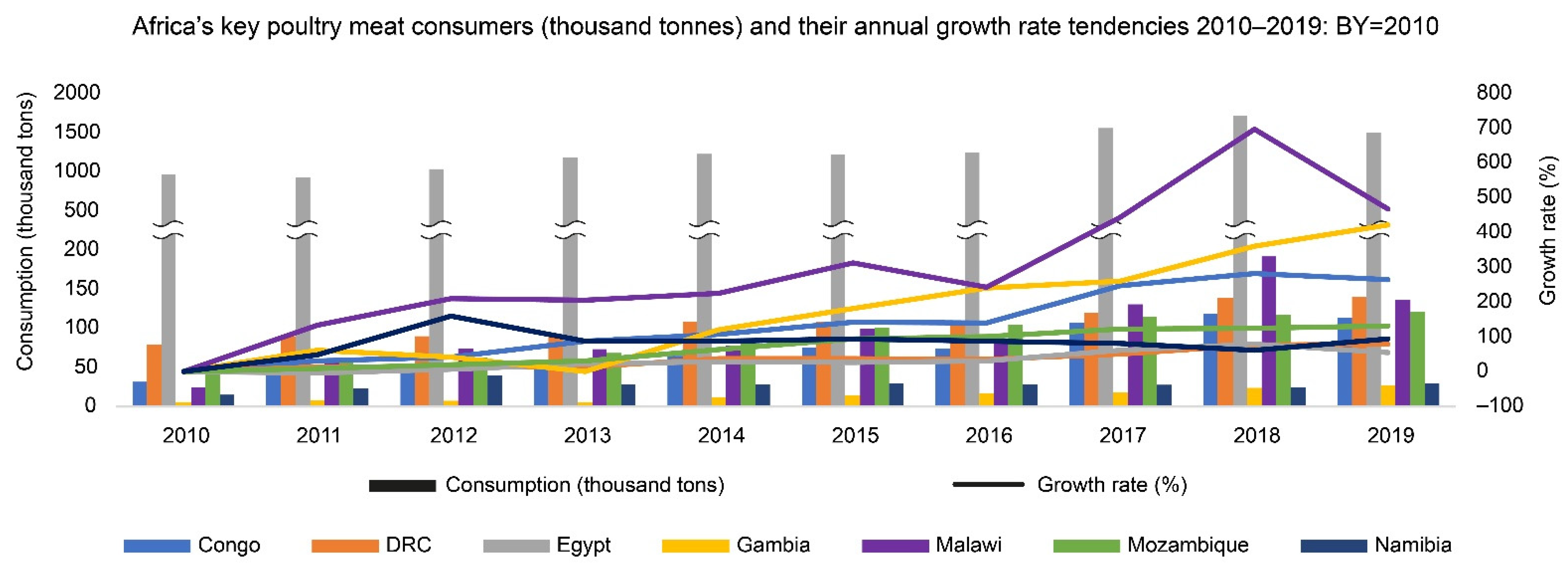

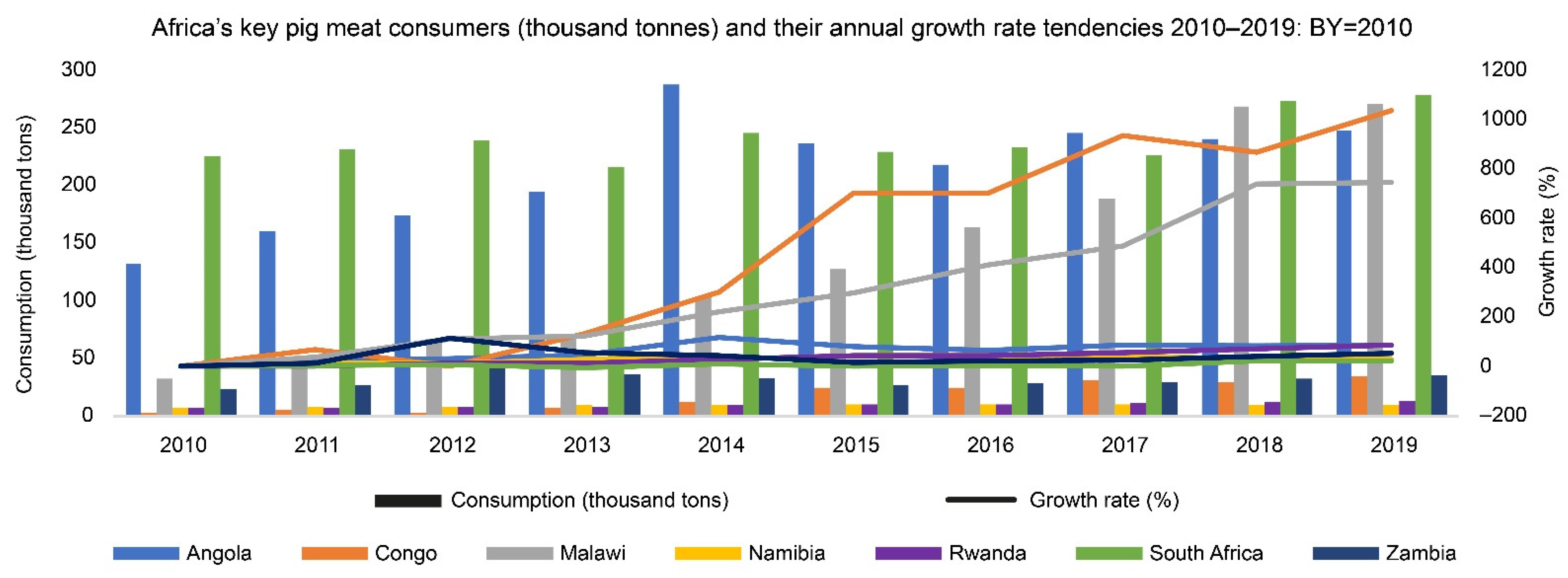

A scenario is already presenting itself with China and other allies from the west positioning themselves to tap into the potential arising from the new markets. Most consumers are in emerging economies, which indicates how the middle class will dictate meat consumption patterns across Africa in the future. Figure 8 and Figure 9 show those countries where poultry and pig meat were most consumed over the last ten years and their growth over time.

Between 2010–2019, African poultry meat consumption grew by 37 per cent. Previous studies had 2050 projections at 61 per cent with 2000 as the baseline, but under business as usual, growth based on our calculations will be surpassed by 2030 [81]. Over the period under study, some of the critical poultry consumers grew fivefold, as presented in Figure 5 above. Per capita, poultry consumption between 2010–2019 was highest in South Africa, with an annual average of 34.45 kg, followed by Morocco and Congo, which had a yearly average of 19.7 kg and 15.8 kg, respectively. The annual growth for South Africa and Morocco has been increasing gradually over the period, where Congo increased from 8.8 kg to 22 kg. Angola had a yearly average of 13.01 kg, which grew steadily until 2017 and started declining.

A comparison between the consumption shares for poultry to total meat available in the country showed that in Morocco, South Africa and Congo, poultry meat is crucial because it accounts for more than 50 per cent of the national meat consumed. Over the period under analysis, it was found that shares of poultry meat in the three countries to the total meat were 59.24%, 57.29% and 49.93%, respectively. We found that all the top poultry consumers were experiencing increased demand for poultry meat. All the top twenty poultry consumer nations over the period under calculation experienced a more than four percentage absolute increase in demand for poultry meat as a share of the real meat. This indicates the growing demand for poultry products across the African continent.

Delving into pig meat consumption by country, the pig meat consumption share of the total meat was highest in Guinea Bissau and Mozambique, with 54.91 and 53.45 per cent, respectively. On the other hand, per capita consumption was modest in Angola over the period under analysis, standing at 7.5 kg in 2017. On the other hand, Congo’s per capita consumption has grown sharply from 1.27 kg to 6.12 kg, whereas South Africa and Namibia’s per capita consumption has remained steady at about 4 kg since 2010.

Growth in absolute consumption comparable across all member states was modest across both Congo and Malawi, which has been growing exponentially. Over the same period, growth rates for pig meat consumption across South Africa, Angola, Namibia and Rwanda grew by over 50 per cent. Moreover, the growth has remained constant from 2017 through 2019.

3.4. Trends and Tendencies in Addressing the Demand-Supply Deficit and Its Associated Impacts

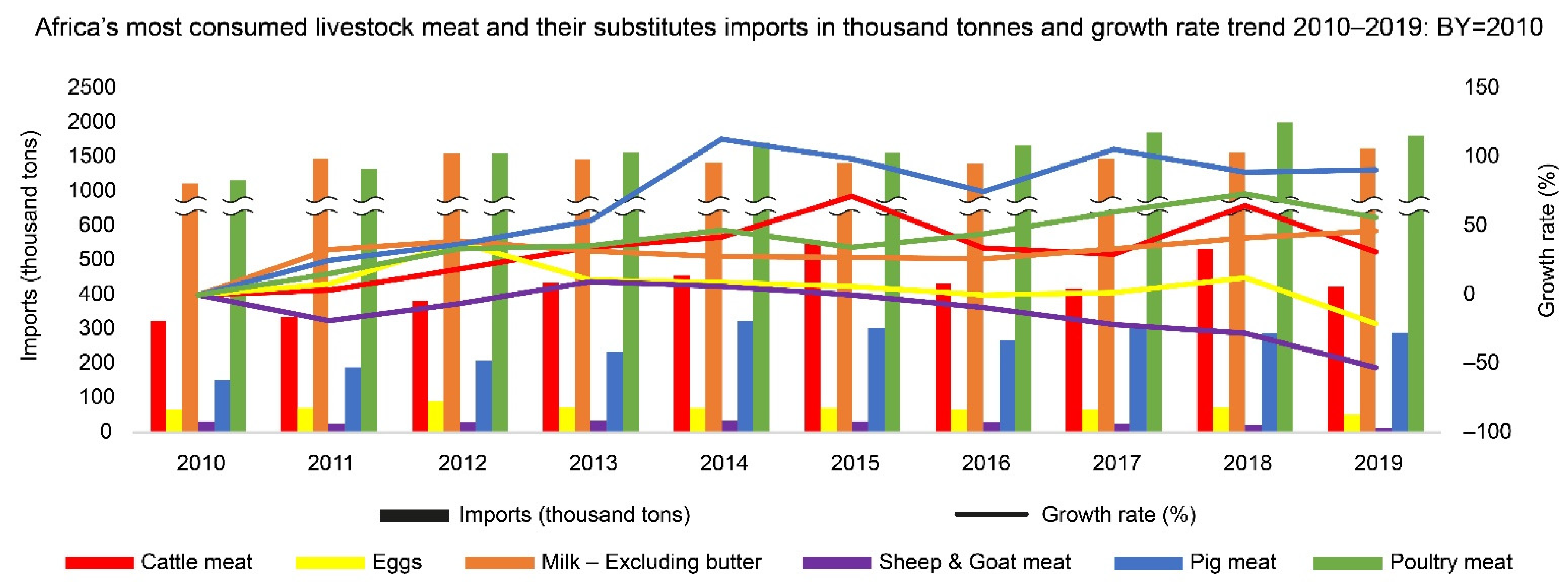

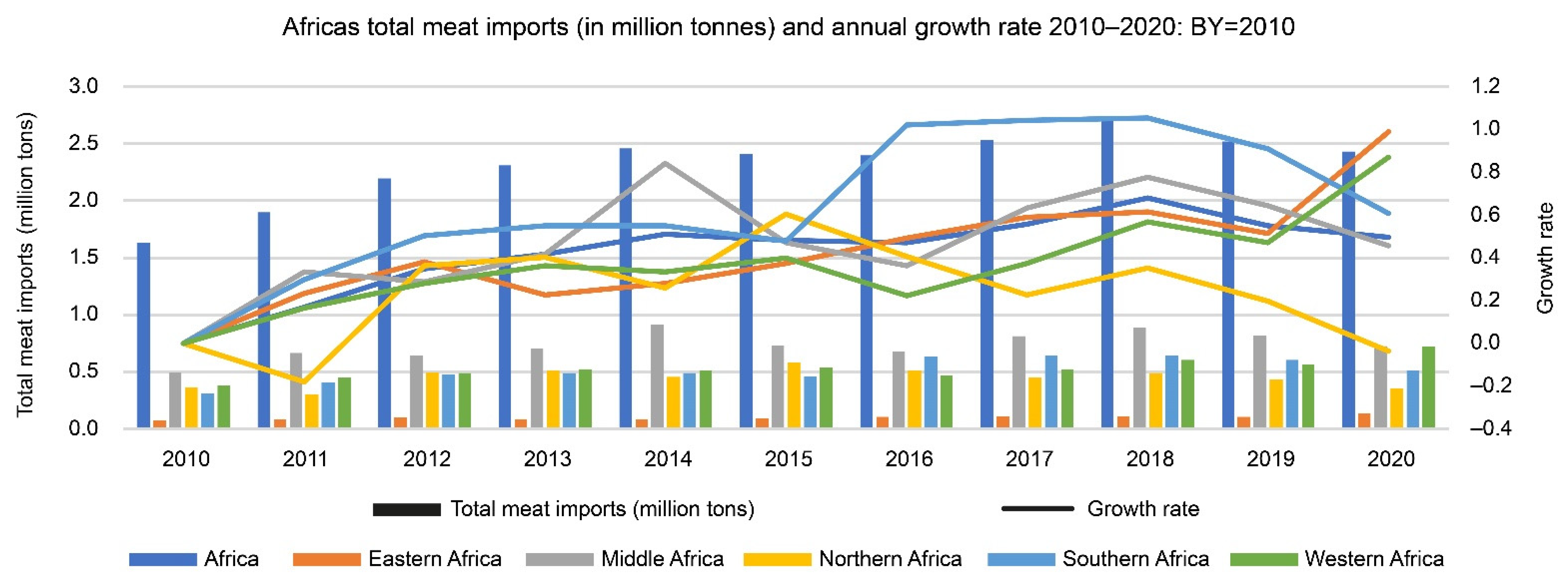

As discussed in Section 3.3 above, poultry and pig meat are the most-consumed products; we look further at their trade tendencies, where the supply–demand deficit for pig and poultry-derived meat products grew exponentially. Between 2010 and 2020, Africa’s total meat imports were approximately 2.55 million tonnes. Moreover, meat imports almost doubled, increasing from 1.6 million to 2.43 million tonnes, as shown in Figure 10 below.

Although growth increased sharply, it slowed down between 2014 and 2016. The slowed growth was due to the shrinking global livestock market caused by the African Swine disease outbreak, which resulted in a less than 30% decline in pig sausage import [82]. Between 2017–2018, the imports grew exponentially. However, they fell in 2019, attributable to the health crisis caused by the Corona Virus Disease (COVID-19), which resulted in the limited movement of food products.

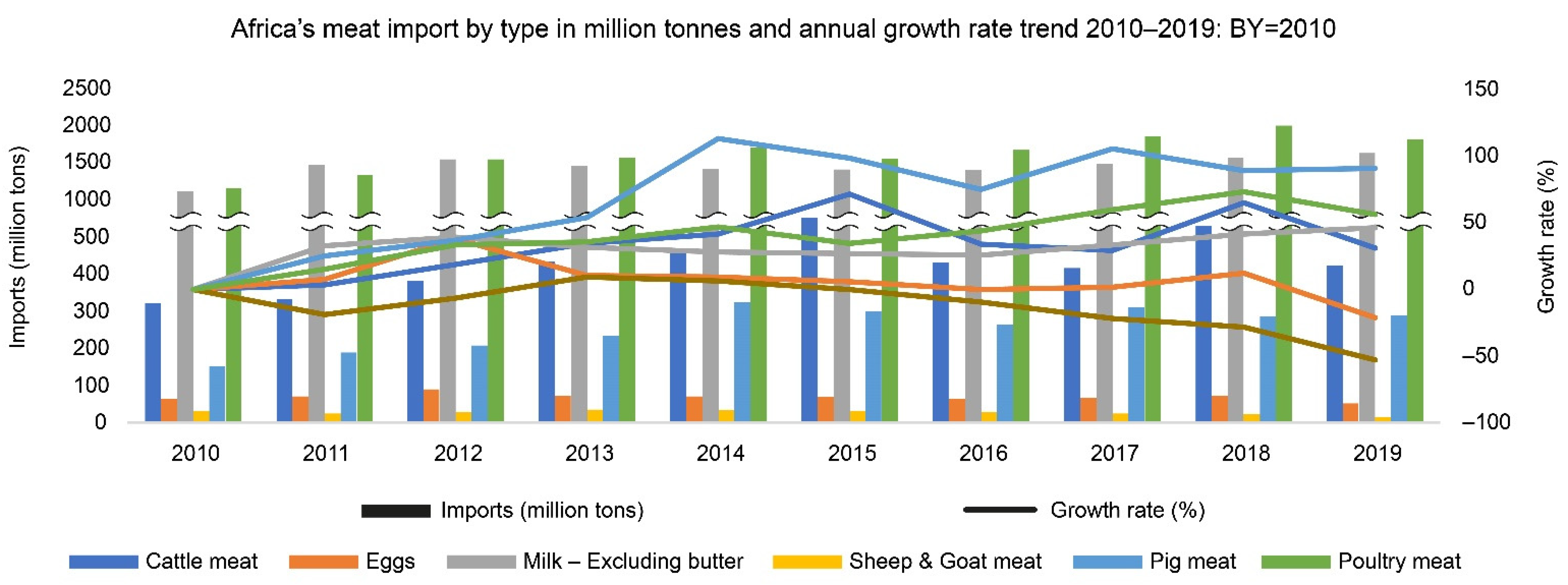

Over the period under analysis, meat imports were dominated by three types: poultry meat (57.95%), bovine meat (29.11%) and pig meat (10.57%), while other meat accounted for only 2.37% as summarised in Figure 11. Almost two-thirds of the meat imports between 2010–2019 were poultry meat at the product level. Poultry meat imports grew from 850,277 tonnes in 2008 to 1,929,676 tonnes in 2019, with the highest import recorded in 2018 at 2,117,514 tonnes.

Although absolute values growth increased sharply, Africa’s total meat import share was unstable due to the increasing demand for pig meat imports. The instability in poultry imports to total meat imports grew from 52.3% in 2008 to 55.5 in 2019, with the highest share recorded in 2011 and 2016, above 59%. Similarly, pig meat imports doubled with exponential growth until 2014, slowed until 2016 due to the African swine flu outbreak and global regulations and increased again post-2017.

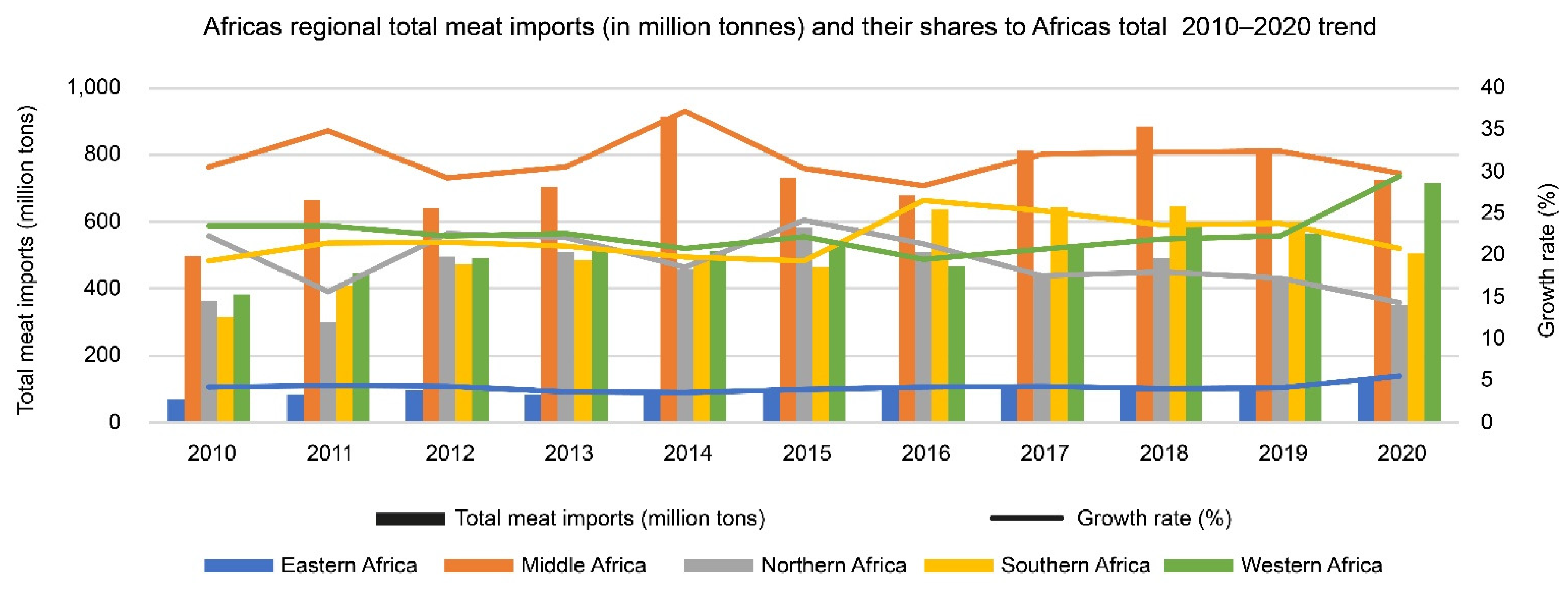

At the regional level, meat imports were highest in middle Africa (29.02%), followed by Northern Africa (24.55%), Western Africa (21.92), Southern Africa (20.73%) and lowest in Eastern Africa (3.77%). However, both Western and Southern Africa imported almost equal amounts of meat. Middle Africa’s main imported meat-types were poultry and pig. Middle Africa pig meat imports grew three-fold from 70,904 tonnes in 2008 to 225,603 tonnes whereas poultry meat remained almost steady and doubled, experiencing growth from 317,880 to 630,954 tonnes as summarised in Figure 12.

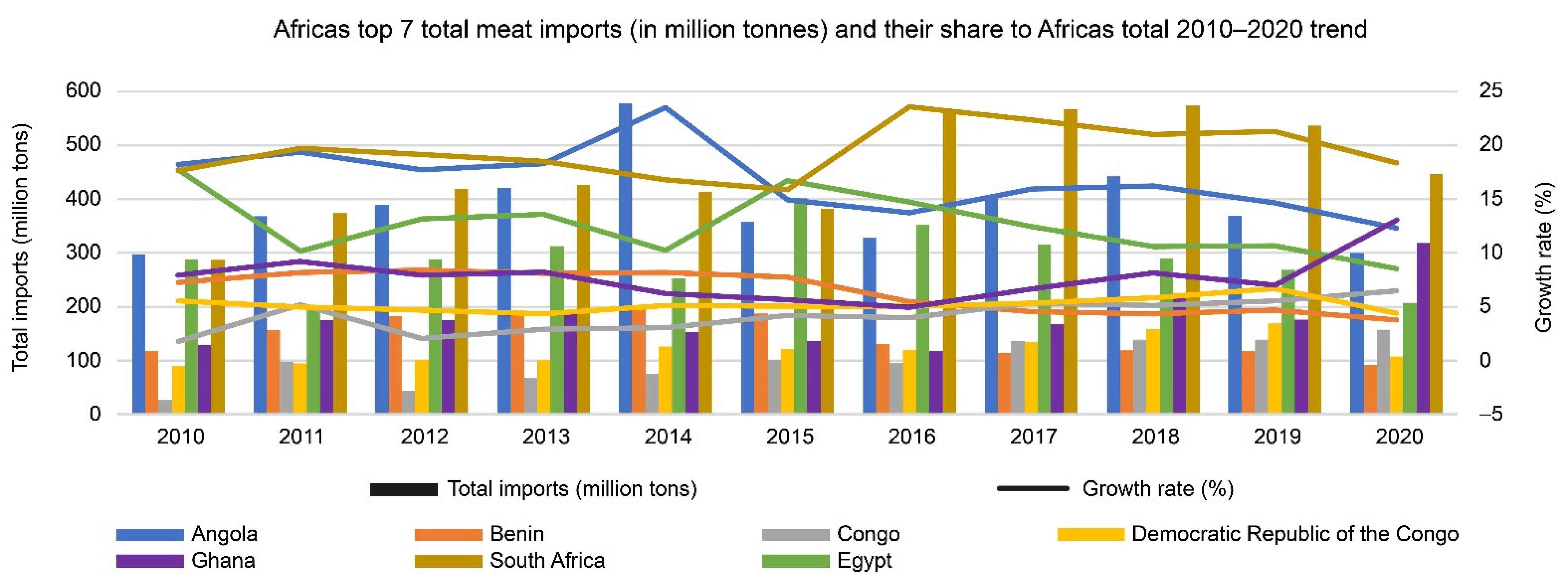

At the country level, the top six meat importers accounted for over 74% of Africa’s meat imports between 2008–2019. These countries’ respective African shares include South Africa, Angola, Egypt, Ghana, Benin, and the Democratic Republic of Congo as summarised in Figure 13. The results of top meat imports are similar to consumption per Capita for South Africa, Angola, Egypt, Congo, and Ghana. Therefore, it is deducible that if holding other factors constant, there will be increased importation of meat in the future into these countries due to a growth trend in per capita consumption.

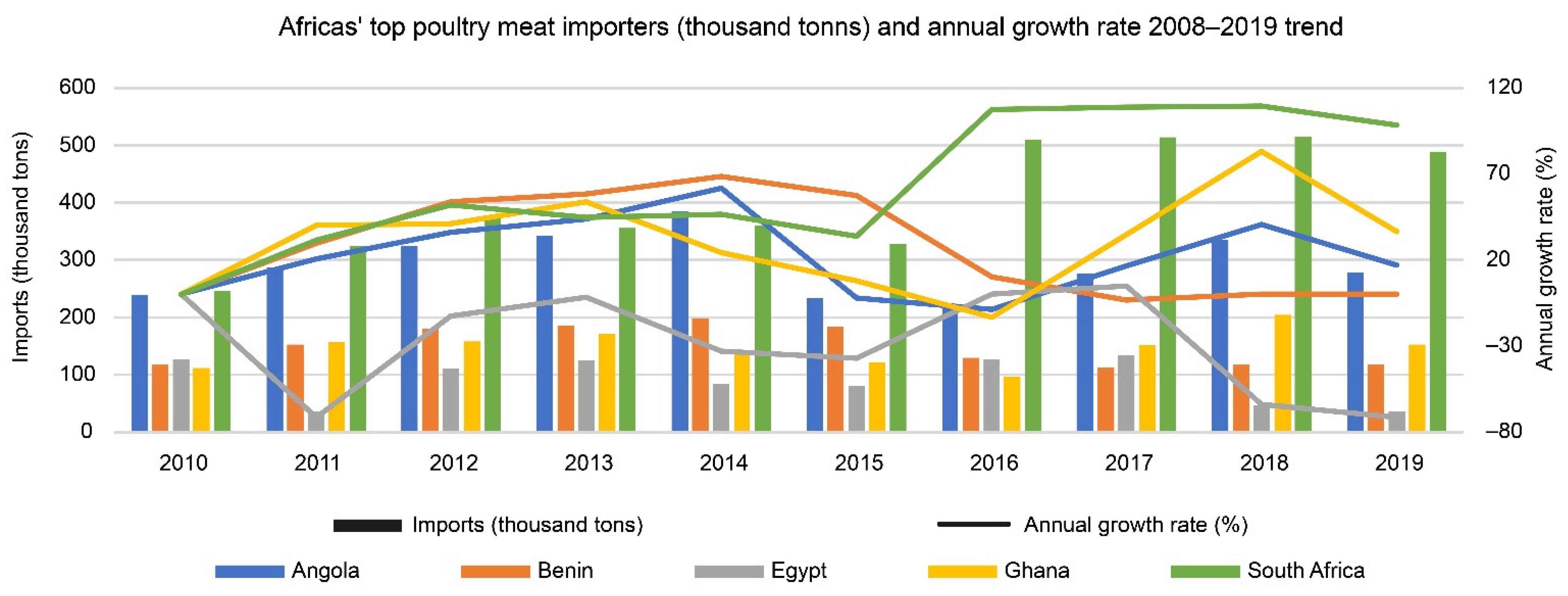

Regarding meat importation by type and destination, the top five chicken importers in Africa contributed to over 55 per cent of the total chicken meat. These included South Africa, Angola, Ghana, Benin and Egypt, as presented in Figure 14. However, Angola’s imports have been declining over time due to increased production in the country [83]. This trend contrasts with the continental trend, where the most demanded poultry meat in Africa is chicken and canned meat [84].

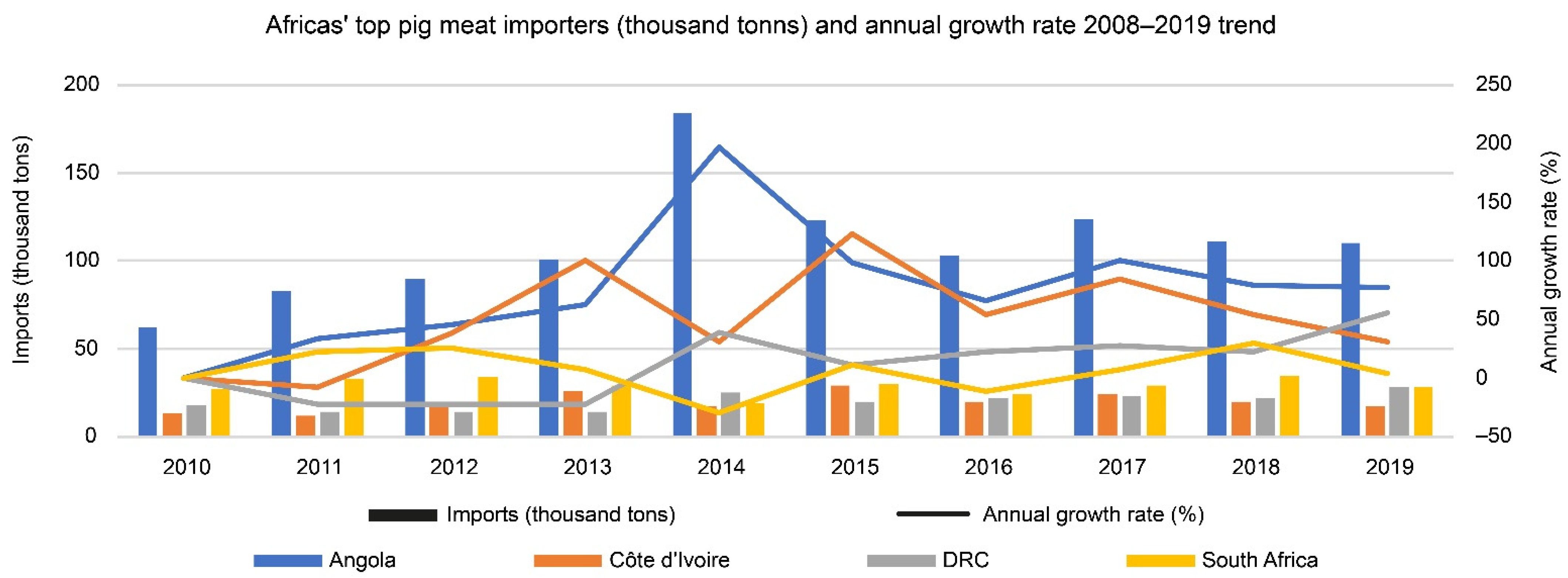

The leading pig meat importers are Angola, South Africa, the Democratic Republic of Congo, Côte d’Ivoire and Congo. In these countries, their cumulative share of Africa’s total was over 70 per cent over the same period as elaborated in Figure 15. Angola’s pig meat grew from 46,209 tonnes in 2008 to 109,979 tonnes in 2019. This growth resulted in Angola’s share of African pig meat growing from 22.39 per cent to 27.52 per cent. All top five net pig meat importers from Angola in 2014 experienced exponential growth.

Angola’s share of pig meat products to Africa’s total is on an increasing trajectory, apart from sausage, whose share of Africa’s total imports of sausages declined from 57.22 to 38.57%. To conclude, for the tendencies of the most demanded meat products, we calculated the average growth rate for the last three years with 2010 as the base year.

Finally, we subjected the eight variables to K-Cluster analysis using IBM SPSS version 26 to group the countries into main groups with similar characteristics. Although there are 54 African countries, only 37 countries had their data complete for cluster analysis. Their Z scores Analysis of Variance (ANOVA) are presented in Table 2 below.

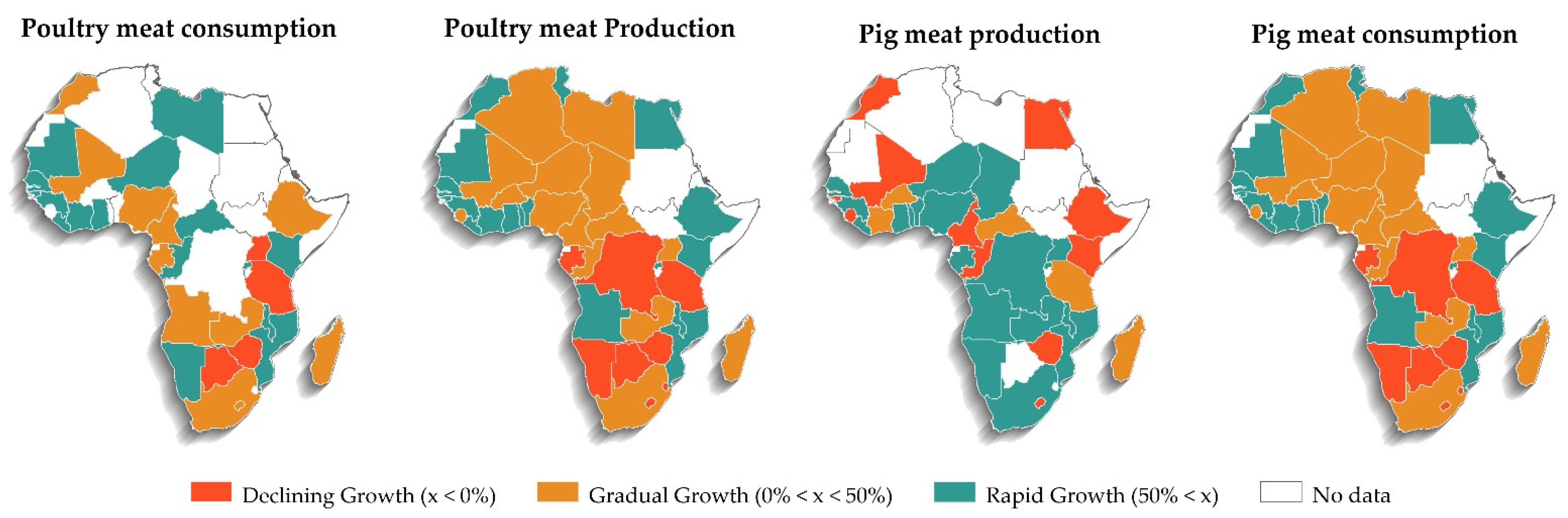

Five out of the eight variables had statistical significance in determining which country was placed in the four clusters, as presented in Figure 16 below. The values were recalculated to visualise the country’s performance, as all the production and consumption variables were statistically significant. We used the data for the four variables to visualise the situation of both pig and poultry production and consumption trends in Africa in a graphical format. Applying Quantum GIS Version 3.22, four main clusters with three main groupings were developed.

The classification was based on three broad categories derived from the tendencies of the evaluated variables. We adopted a simple categorisation using the mean growth values. All those values which had experienced negative growth over the period under calculation are considered as undergoing a declining growth phase. Those with values starting from zero were considered to be experiencing gradual changes over time; thus, the gradual growth phase was marked with yellow. The last category comprised those with values of more than 50 percent growth; they are marked in green and were considered as undergoing a rapid growth phase, as presented in Figure 16.

All the negative values indicated that growth had declined as compared to 2010. Based on the maps, we deduced that poultry consumption was growing across almost all of Africa, with modest growth in Central and Western Africa. Despite production growth, similar trends were evident for the imports. The trends for pig meat revealed that a cluster of unprecedented growth is emerging in Sub-Saharan Africa, especially in Angola and Malawi, where production, consumption and imports are growing at an unprecedented rate.

3.5. Policy Developments on Africa’s Growing Demand for Meat Products and Their Implications on Climate

3.5.1. Policy Approaches and Strategies Defining the Revitalisation of the African Meat Industry

Developing a vibrant, resilient and competitive livestock sector across Africa will be driven to a greater extent by clear, elaborative and sector-specific policies and strategies. Many existing policies and programmes aimed at improving the sector are broad and addressed under the auspice of the ministry or department of agriculture [41]. However, multiple policies influence the livestock sector, and establishing state-of-art implementable policies and strategies customised to the region is imperative [85]. Therefore, while promoting vitality and advocating for sustainable progressive growth of the industry, prominent local, national and regional initiatives are being initiated and implemented across Africa. Many approaches and strategies have been developed, but we summarised the critical relevant instruments in Table 3 below.

3.5.2. Implications of Addressing Policy Gaps and Future Actions to Implement

Establishing and enabling the operationalisation of the right tools and instruments that will allow for the thriving of the sector can ensure that Africa attains food security, improved trade performance, and improved ecosystem services, and would be a game changer [16,31,94,102]. The desired investment mechanisms and policy instruments must be tailored to specific regional and local contexts to adapt to the local African context [31,32,64,101]. Designing and implementing transformative policies to disrupt traditional livestock rearing practices, livestock household ownership and implementing business models that ensure a lean livestock sustainable value-chain is realised must be prioritised. Adopting such a model will ensure rapid sectoral augmentation with global competition while satisfying local needs [103,104].

The desired policy changes must transcend livestock rearing practices and ensure all the actors along the value chain are part of the transformative agenda. Achieving the 6% desired share of the GDP by 2025 calls for jointly setting up disruptive, transformative and robust sectoral growth models [22,64]. The determinant factors for policy development across the sector must be guided by but not be limited to technological changes, improved animal health and welfare, increased public-private partnership, increased extension services, expanded community enlightenment of the importance of quality animals and the role of the sector in establishing resilience and adaptation to climate change while improving livelihoods [16,64,65]. In addition, the competition for the food and feed industry while alleviating poverty and food insecurity across Africa will be a long-term issue to solve [105,106,107]. This is evident from the increasing rate of conversion of grasslands and forest lands into agricultural lands for food and feed production.

Increasing the competitiveness and sustainability of African livestock products in the market will be imperative to promote policies to improve the product’s health. In the 21st century, consumer behaviour is guided by the traceability principle. Traceability and global animal identification are some of the critical factors in driving competitiveness in the market [108]. Key market players and countries with traceability are more likely to be competitive and have higher chances of sustaining their market position in the long run. Therefore, promoting a policy for traceability will ensure that African livestock exports increase their global competitiveness. In addition, a traceability policy will increase public and private motivation as it will have multiple benefits cutting across economic, social and environmental areas [109,110,111,112]. Effective traceability policy implementation will require a well-established information technology infrastructure and open data sharing to ensure all the information is available to the market, which necessitates boosting technological advancement in Africa for sector development.

Based on the nature of the specialities of the local context and conditions in Africa, sound governance is substantial to offset perceived development and improvement strategies in the livestock sector. Accelerating government involvement accelerates incentivisation and protects small-scale farmers from overexploitation in the market. Increased protection of farmers will ensure an increased return on investment, rendering the sector vibrant. According to FAO, the general rule of the governments should be to ensure that the prices paid to domestic producers are equal to those in international markets. Incentivisation across the domestic value chain and protection of domestic producers will reduce their constraints and incur losses [113].

Adopting and implementing digitalisation to enhance the production and competitiveness of African livestock is a clarion call. Innovation-driven policies will ensure that sectoral growth will be achieved without exerting pressure on land use. Implementing and adopting innovative land-use policies will reduce natural resource depletion and promote increased per unit output [39,40,41,42,43,114]. Desired innovation-driven policies must embrace data-driven technologies in the livestock sector. Digitalisation across the region will offset smart farms, increasing the innovativeness of future farms by advocating for data integration and innovative future processing farms. Smart livestock farming will ensure Africa achieves increased productivity while reducing environmental load and improving animal welfare and health [38,39,40,115].

One of African meat producers’ most significant challenges is processing their products [116,117]. Increasing their capacity must be driven by lean logistical processes that will ensure their products are timely on the market [118]. Many barriers hinder African pig and poultry producers from timely delivery of their produce to the processing unit and the market. As they encounter a vicious cycle of drawbacks, the outcome is reduced quality and quantity entering the market, leading to low market returns. Adopting and implementing regulations that will ensure vibrant and innovative meat processing for value addition across Africa at the member states’ level is imperative. The set of policies and regulations must be aligned with the global food standards to ensure that local export processing zones are purely meat-based and are competitive regionally and globally [119]. Policies should advocate for risk co-sharing to improve market access while removing any barrier to market accessibility.

Market accessibility barriers to most producers are attributed to their economies of scale [31,39,40,41,64,65,66,120]. With over 80% being small-scale producers, establishing policies that promote the establishment of cooperatives will increase their chances of entering the market by pooling resources together. The rebound effect of adopting cooperatives will be increased bargaining power to reap more from the markets. This will further be strengthened by the national government and the African Union to promote negotiations and implement the Free Trade Agreements [121,122]. The African domestic market has over 1.2 billion consumers who present a sustainable market for the next five decades, with meat consumption projected to grow by five times by 2050 compared to 2020 [123,124].

Most of the pig and poultry production across Africa occurs in rural areas that are not well connected with the urban centres. Therefore, linking producers and the market is a potential avenue for revitalising the sector across Africa. However, formulating effective policies to overcome these barriers requires the availability of information on the market situation. Thus, the future of the African meat sector must be guided by openness and data sharing to ensure that root cause impediments are detectable to ensure future lean and resilient logistical processes are attained [19,82,125].

Inadequate addressing of the discussed issues may accelerate climate change and fuel negative changes in the sector. Enhanced resilience and sustainability of the sector will be a subset of the adaptation and mitigation capacity and link it to climate. This is more likely to be achieved through linking increased efficiency in production to ensure attained lowered emissions. Unfortunately, less across Africa has been done to ensure climate-friendly livestock financing has been reached.

Although increased production efficiency has the potential to improve the overall GHG emitted, reducing per-unit GHG emission while increasing productivity is better than doing nothing. A win-win situation for both economic-social and environmental growth avenues must be embraced. Embracing a win-win scenario by establishing a climate financing framework for the sector could reduce the trade-off for increased production as access to the finance will be determined by the implementation of the reduction of associated externalities.

Lastly, zero tolerance for corruption must be embraced to implement efficiently and effectively the above-explained good practices, which will address the sustainability of the sector. Corruption, as an essential but poorly understood element in the meat value chain, hinders the establishment of resilient, sustainable meat value chains, and is a phenomenon with the potential to paralyse the whole value chain if not addressed. Global food systems are threatened by political rhetoric that is not directly associated with food security, biodiversity, climate change, sustainability or the environment.

4. Conclusions

Despite the significant growth in the demand for livestock value chains in Africa, less research has been conducted on region and country-specific impacts. According to the analysis, it was clear that the need for livestock products, especially poultry and pig-derived products, is growing at an unprecedented rate. Several drivers drive the growth. Although not directly associated, there is a higher likelihood that the livestock sector is responsible for the declining share of land under grasslands, meadows and forests, the reduction in inland waters and the share of the shrub-covered areas. However, the levels of benefits and the associated risks with the fast-growing demand for livestock-derived products is still unknown, and the uncertainty results in a more complex situation than envisaged.

African farmers are more likely not aware of their environmental impacts as well as the consumers. Satisfying the demands has resulted in pressure on natural resources already constrained by the fast-growing population and climate change. A complex interaction between drivers for change in the sector and those for increased demand for the final products is creating a situation that raises a sustainability dilemma in the livestock sector in Africa. Based on the continent’s natural endowment, ensuring the right way to enhance the livestock community’s resilience and promoting sustainable intensive livestock systems is a viable option. However, effectively addressing these gaps goes beyond the continent and requires global solutions.

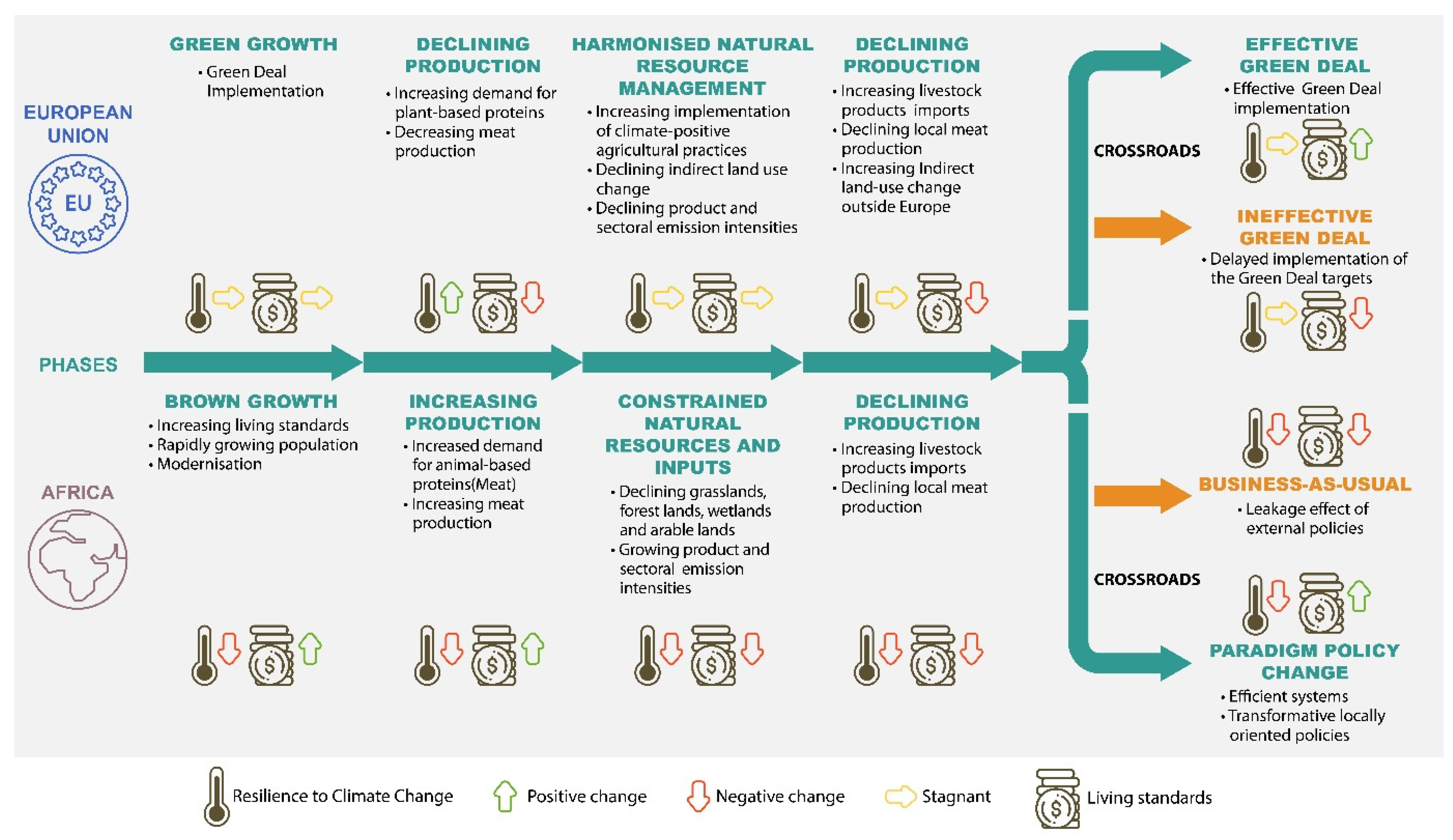

From a macro point of view, decisions are shaped by environmental aspects in today’s world. Taming agricultural emissions is critical, especially in Europe, where the continents aspire to be carbon neutral by 2050. Attaining carbon neutrality is a subset of production capacity, and increased prices in Europe accelerate increased imports, thus increasing production elsewhere outside Europe. As a net meat and livestock products importer, Africa relies heavily on European imports. Reducing European production would adversely affect the availability of the products in Africa, necessitating increased production and emission intensity and capacity, thus worsening climate change. However, adopting a model of intensification per unit animal across Africa would mean doubling availability at the global level as opposed to Europe, where it would translate to increased environmental and economic costs and hunger in Africa, as visualised in Figure 17 below.

From Figure 17, we can further deduce that each player is striving their level best to achieve the SDGs by 2030. These aspirations have been perceived differently across different regions depending on their level and stages of development. Africa and the EU are under different growth trajectories. Although different growth models and development history prevails, these regions suffer from similar climate change impacts. Therefore, the perceived mechanism to establish shock-absorbing mechanisms against climate-related risks is a clarion call for all. However, despite a concerted effort by all to mitigate these shocks, strengthening the ability to withstand and thrive in such conditions (resilience) is not an option. To establish such resilient systems, the EU adopted its green growth strategy, aiming to be carbon neutral by 2050. Different sectoral strategies are being implemented under the framework of the EGD, with the F2F and the biodiversity strategy being crucial to the agricultural sector. Different scenarios are envisaged, with all these strategies laying targets to be achieved by 2030 and even further by 2050, depending on the chosen development paths. In the short run, concerted efforts are geared towards implementing the Green Deal across each member state. This will create a hibernation period where the sector’s environmental and production capacity is trying to figure out what works well, and where and how. At this stage, sectors are adapting to the new regulations and procedures, which leads to agricultural/economic production remaining constant.

Under a business-as-usual scenario (fewer European countries implement the EGD), in the next five years, the established practices are more likely to yield premium outcomes resulting in higher environmental, thus intensifying adaptation capacity and resilience to climatic shocks. Increased harmonisation in natural resource management will be responsible for attaining the increasing steady state. As a result, growth in environmental stewardship will be sustained or even magnified at the expense of the agricultural output performance. This tendency will grow to a certain point where ecological stewardship cannot be sustained further because the demand for agricultural products will grow. At that critical point, the countermeasure will be to increase local production under conventional methods, increase imports or globally shift production to developing countries. This places Europe at a crossroads as to how effectively the EGD transition can be implemented to regulate the spillover effect.

Contrarily, Africa’s development path is experiencing different phases to those being experienced by European Agriculture. Africa’s 2015 MDGs review recommended transitioning towards greener economies, resulting in Agenda 2063, a growth strategy geared towards increasing economic growth and industrialisation to alleviate poverty. Africa aims to grow its sector by 25% from the Agricultural sector under the Malabo Declaration. It was driven by a fast-growing population and a significant share of the middle-income population with higher purchasing power and dynamic consumption behaviour, especially high demand for meat-derived products. This situation will accelerate the increase in production at the expense of natural resources. However, constraining natural resources in a climate-changing environment will increase the vulnerability of the sector, exposing the sector to extreme shocks and deteriorating the sector’s resilience level. Operating in such a situation and increased demand for the same European commodities will place the region at a crossroads.

The crossroads’ outcome for Europe and Africa can be perceived under two scenarios. With effective implementation of the EGD (where EGD adoption is entirely global), the chances are more likely for Europe to achieve a win-win for the environment and the agricultural sector. Effective implementation means that there will be zero leakage effect to other regions in the world with zero land use change. These will be driven by ensuring all investment and bilateral agreements are tied to the objectives to ensure the world also transitions in a just manner with Europe. Cascading such practices to the African continent will support the implementation of transformative policies and promote efficiency to ensure output maximisation while protecting the environment. Failure to effectively implement the EGD will accelerate increased investment in the developing world and shift the environmental burden to Africa, further exposing the African continent to unforeseen climatic shocks and leading to reduced resilience.

Increasing production intensity when there exists low technological adoption and capacity across Africa will not meet the European market regulations because of failure to meet the environmental goodwill, which will be part of carbon-neutral consumer markets. Therefore, before policymakers in developed economies initiate production intensity reduction as a strategy to reduce GHGs, or shifting of production regions, due diligence and further research must be done on the impacts of such constraints on developing economies. Solving the climate problem in one part of the world should not exacerbate it in another region.

Addressing the complexity across the African value chain context will not be defined by a one-size-fits-all approach. Instead, adopting a transformative approach by implementing transdisciplinary mechanisms and incentivising the sector to promote technological innovations to increase resource utilisation efficiency and protect the farmers from overexploitation will create favourable market conditions. Furthermore, implementing a sustainable value chain approach to the sector will ensure a strong linkage between the farm and the market. The region has well-defined speculative policies aligned with international development strategies but is very weak in implementation.

To reduce the bottlenecks stemming from the policy aspect, adopting transformative policy design and implementation by involving all the stakeholders is imperative. Furthermore, to revitalise and improve the sector’s competitiveness, addressing leakages that could exacerbate climate change by prioritising inclusive and enhanced conditional access to climate financing framework is important. Conditionality to financial support for livestock farmers has the potential to reduce per capita emissions of GHGs and reduce the trade-off between increased productivity, sectoral adaptation and mitigation and land-use change. Additionally, from the global perspective, any attempt to increase production capacity for export purposes must be regulated to ensure the sector does not contribute to increased climatic-associated changes.

Author Contributions

Both authors contributed significantly to all sections of the article. All authors have read and agreed to the published version of the manuscript.

Funding

This research APC was supported by the Doctoral Publications Support Program of Széchenyi Istvan University-Győr (Hungary) 2022.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data on any figure and table in this study are readily available upon request to the authors.

Acknowledgments

We sincerely thank Vrana Atilla for his immense support in designing the figures.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Philip, K.T. Livestock Production: Recent Trends, Future Prospects. Philos. Trans. R. Soc. B 2010, 365, 2853–2867. [Google Scholar] [CrossRef] [Green Version]

- Ndue, K.; Pál, G. Life Cycle Assessment Perspective for Sectoral Adaptation to Climate Change: Environmental Impact Assessment of Pig Production. Land 2022, 11, 827. [Google Scholar] [CrossRef]

- Havlík, P.; Valin, H.; Herrero, M.; Obersteiner, M.; Schmid, E.; Rufino, M.C.; Mosnier, A.; Thornton, P.K.; Böttcher, H.; Conant, R.T.; et al. Climate change mitigation through livestock system transitions. Proc. Natl. Acad. Sci. USA 2014, 111, 3709–3714. [Google Scholar] [CrossRef] [Green Version]

- Weiss, F.; Leip, A. Greenhouse gas emissions from the EU livestock sector: A life cycle assessment carried out with the CAPRI model. Agric. Ecosyst. Environ. 2012, 149, 124–134. [Google Scholar] [CrossRef]

- Kiebert, G.M.; Curran, D.; Aaronson, N.K.; Bolla, M.; Menten, J.; Rutten, E.H.; Nordman, E.; Silvestre, M.E.; Pierart, M.; Karim, A.B. Quality of life after radiation therapy of cerebral low-grade gliomas of the adult: Results of a randomised phase III trial on dose response (EORTC trial 22844). Eur. J. Cancer 1998, 34, 1902–1909. [Google Scholar] [CrossRef]

- Rojas-Downing, M.M.; Nejadhashemi, A.P.; Harrigan, T.; Woznicki, S.A. Climate change and livestock: Impacts, adaptation, and mitigation. Clim. Risk Manag. 2017, 16, 145–163. [Google Scholar] [CrossRef]

- Leinonen, I. Achieving environmentally sustainable livestock production. Sustainability 2019, 11, 246. [Google Scholar] [CrossRef] [Green Version]

- Lezoche, M.; Hernandez, J.E.; Díaz, M.D.; Panetto, H.; Kacprzyk, J. Agri-food 4.0: A survey of the supply chains and technologies for the future agriculture. Comput. Ind. 2020, 117, 103187. [Google Scholar] [CrossRef]

- Simpkin, P.; Cramer, L.; Ericksen, P.J.; Thornton, P.K. Current situation and plausible future scenarios for livestock management systems under climate change in Africa. In CCAFS Working Paper No. 307; CCAFS: Wagenningen, The Netherland, 2020. [Google Scholar]

- Schmitz, C.; Van Meijl, H.; Kyle, P.; Nelson, G.C.; Fujimori, S.; Gurgel, A.; Havlik, P.; Heyhoe, E.; d’Croz, D.M.; Popp, A.; et al. Land-use change trajectories up to 2050: Insights from a global agro-economic model comparison. Agric. Econ. 2014, 45, 69–84. [Google Scholar] [CrossRef]

- Bishop, M.L.; Payne, A. Steering towards reglobalization: Can a reformed G20 rise to the occasion? Globalizations 2021, 18, 120–140. [Google Scholar] [CrossRef]

- Enahoro, D.; Mason-D’Croz, D.; Mul, M.; Rich, K.M.; Robinson, T.P.; Thornton, P.; Staal, S.S. Supporting sustainable expansion of livestock production in South Asia and Sub-Saharan Africa: Scenario analysis of investment options. Glob. Food Secur. 2019, 20, 114–121. [Google Scholar] [CrossRef]

- Herrero, M.; Havlik, P.; McIntire, J.; Palazzo, A.; Valin, H. African Livestock Futures: Realising the Potential of Livestock for Food Security, Poverty Reduction and the Environment in Sub-Saharan Africa; Office of the Special Representative of the UN Secretary General for Food Security and Nutrition and the United Nations System Influenza Coordination (UNSIC): Geneva, Switzerland, 2014; p. 118. [Google Scholar]

- Amole, T.; Augustine, A.; Balehegn, M.; Adesogoan, A.T. Livestock feed resources in the West African Sahel. Agron. J. 2022, 114, 26–45. [Google Scholar] [CrossRef] [PubMed]

- Filho, W.L.; Sousa, L.O.; Pretorius, R. Future Prospects of Sustainable Development in Africa. In Sustainable Development in Africa; Springer: Cham, Switzerland, 2021; pp. 733–741. [Google Scholar]

- Baumüller, H.; von Braun, J.; Admassie, A.; Badiane, O.; Baraké, E.; Börner, J.; Bozic, I.; Chichaibelu, B.B.; Daum, T.; Gatiso, T.; et al. From Potentials to Reality: Transforming Africa’s Food Production; University of Bonn: Bonn, Germany, 2020. [Google Scholar]

- Otte, J.; Pica-Ciamarra, U.; Morzaria, S. A comparative overview of the livestock-environment interactions in Asia and Sub-Saharan Africa. Front. Vet. Sci. 2019, 6, 37. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sakho-Jimbira, S.; Hathie, I. The future of agriculture in Sub-Saharan Africa. Policy Brief 2020, 2, 18. [Google Scholar]

- Rampa, F.; Knaepen, H. Sustainable Food Systems through Diversification and Indigenous Vegetables. An Analysis of the Southern Nakuru County; ECDPM: Maastricht, The Netherlands, 2019. [Google Scholar]

- Magnusson, U. Sustainable Global Livestock Development for Food Security and Nutrition Including Roles for SWEDEN; Ministry of Enterprise and Innovation, Swedish FAO Committee: Stockholm, Sweden, 2016.

- Food and Agriculture Organization (FAO). Africa Sustainable Livestock 2050; FAO: Stockholm, Sweden, 2017. [Google Scholar]

- Nakimbugwe, D.; Ssepuuya, G.; Male, D.; Lutwama, V.; Mukisa, I.M.; Fiaboe, K.K. Status of the regulatory environment for utilisation of insects as food and feed in Sub-Saharan Africa-a review. Crit. Rev. Food Sci. Nutr. 2021, 61, 1269–1278. [Google Scholar] [CrossRef]

- Beckman, J.; Ivanic, M.; Jelliffe, J.L.; Baquedano, F.G.; Scott, S.G. Economic and Food Security Impacts of Agricultural Input Reduction Under the European Union Green Deal’s Farm to Fork and Biodiversity Strategies; USDA: Washington, DC, USA, 2020. [Google Scholar]

- Greiner, S.; Hoch, S.; Victoria, G.A.; Singh, A. Cop26 Digest: The Significance of Article 6 and CDM Transition Outcomes for Africa; Climate Focus: Amsterdam, The Netherlands, 2022. [Google Scholar]

- Hackenesch, C.; Högl, M.; Knaepen, H.; Iacobuta, G.; Asafu-Adjaye, J. Green Transitions in Africa–Europe Relations: What Role for the European Green Deal; ETTG: Brussel, Belgium, 2021. [Google Scholar]

- Union, A. Agenda 2063 Report of the Commission on the African Union Agenda 2063 the Africa We Want in 2063; African Union: Addis Ababa, Ethiopia, 2020; p. 59. [Google Scholar]

- Chambiwa, E.; Majoni, J.; Mapuranga, L.L. The African Union and its Role in Ensuring African Economic and Environmental Sovereignty. Sovereignty Becoming Pulvereignty: Unpacking the Dark Side of Slave 4.0 Within Industry 4.0 in Twenty-First Century Africa. In Sovereignty Becoming Pulvereignty: Unpacking the Dark Side of Slave 4.0 Within Industry 4.0 in Twenty-First Century Africa; Langaa Research & Publishing Common Initiative Group: Bamenda, Cameroon, 2022; p. 299. [Google Scholar]

- Rennkamp, B. Negotiating Climate Change between Unequal Parties: COP25 from an African Perspective. Available online: https://www.africaportal.org/features/negotiating-climate-change-between-unequal-parties-cop25-african-perspective/ (accessed on 19 October 2022).

- Cilliers, J. The future of work in Africa. In The Future of Africa; Palgrave Macmillan: Cham, Switzerland, 2021; pp. 195–219. [Google Scholar]

- Sonnino, R.; Callenius, C.; Lähteenmäki, L.; Breda, J.; Cahill, J.; Caron, P.; Damianova, Z.; Gurinovic, M.; Lang, T.; Lapperière, A.; et al. Research and Innovation Supporting the Farm to Fork Strategy of the European Commission. Available online: https://research.vu.nl/en/publications/research-and-innovation-supporting-the-farm-to-fork-strategy-of-t (accessed on 5 September 2022).

- Dekeyser, K.; Rampa, F. Implications for Ireland’s Development Programming and Policy Influencing; ECDPM: Masstricht, The Netherlands, 2021. [Google Scholar]

- European Comission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: A Farm to Fork Strategy for a Fair, Healthy and Environmentally-Friendly Food System COM/2020/381 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:52020DC0381 (accessed on 5 September 2022).

- Plan, C.E. For a Cleaner and More Competitive Europe; European Commission (EC): Brussels, Belgium, 2020. [Google Scholar]

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions Critical Raw Materials Resilience: Charting a Path towards Greater Security and Sustainability; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- Hammond, D.R.; Brady, T.F. Critical minerals for green energy transition: A United States perspective. Int. J. Min. Reclam. Environ. 2022, 1–8. [Google Scholar] [CrossRef]

- Outlook, S.A. World Energy Outlook Special Report; International Energy Agency: Paris, France, 2015; p. 135. [Google Scholar]

- Schebesta, H.; Candel, J.J. Game-changing potential of the EU’s Farm to Fork Strategy. Nat. Food 2020, 1, 586–588. [Google Scholar] [CrossRef]

- Cantore, N. The Potential Impact of a Greener CAP on Developing Countries; Overseas Development Institute: London, UK, 2012. [Google Scholar]

- Paarlberg, R. The trans-Atlantic conflict over “green” farming. Food Policy 2022, 108, 102229. [Google Scholar] [CrossRef]

- Beckman, J.; Ivanic, M.; Jelliffe, J. Market impacts of Farm to Fork: Reducing agricultural input usage. Appl. Econ. Perspect. Policy 2021. [Google Scholar] [CrossRef]

- Hurle, J.B.; Bogonos, M.; Himics, M.; Hristov, J.; Dominguez, I.P.; Sahoo, A.; Salputra, G.; Weiss, F.; Baldoni, E.; Elleby, C. Modelling Environmental and Climate Ambition in the Agricultural Sector with the CAPRI Model; Joint Research Centre: Brussel, Belgium, 2021. [Google Scholar]

- Dekeyser, K.; Woolfrey, S. A greener Europe at the expense of Africa? In Why the EU Must Address the External Implications of the Farm to Fork Strategy; ECDPM: Masstricht, The Netherlands, 2020. [Google Scholar]

- Hedrick, B.P.; Heberling, J.M.; Meineke, E.K.; Turner, K.G.; Grassa, C.J.; Park, D.S.; Kennedy, J.; Clarke, J.A.; Cook, J.A.; Blackburn, D.C.; et al. Digitisation and the future of natural history collections. BioScience 2020, 70, 243–251. [Google Scholar] [CrossRef]

- Bataille, C.; Waisman, H.; Briand, Y.; Svensson, J.; Vogt-Schilb, A.; Jaramillo, M.; Delgado, R.; Arguello, R.; Clarke, L.; Wild, T.; et al. Net-zero deep decarbonisation pathways in Latin America: Challenges and opportunities. Energy Strat. Rev. 2020, 30, 100510. [Google Scholar] [CrossRef]

- Zimmer, Y. EU Farm to Fork Strategy: How Reasonable is the Turmoil Predicted by USDA. Available online: https://www.globalaginvesting.com/contributed-content-eu-farm-fork-strategy-reasonable-turmoil-predicted-usda/ (accessed on 5 September 2022).

- Springmann, M.; Clark, M.; Mason-D’Croz, D.; Wiebe, K.; Bodirsky, B.L.; Lassaletta, L.; de Vries, W.; Vermeulen, S.J.; Herrero, M.; Carlson, K.M.; et al. Options for keeping the food system within environmental limits. Nature 2018, 562, 519–525. [Google Scholar] [CrossRef] [PubMed]

- Willett, W.; Rockström, J.; Loken, B.; Springmann, M.; Lang, T.; Vermeulen, S.; Garnett, T.; Tilman, D.; DeClerck, F.; Wood, A.; et al. Food in the Anthropocene: The EAT–Lancet Commission on healthy diets from sustainable food systems. Lancet 2019, 393, 447–492. [Google Scholar] [CrossRef]

- Sanchez-Sabate, R.; Sabaté, J. Consumer attitudes towards environmental concerns of meat consumption: A systematic review. Int. J. Environ. Res. Public Health 2019, 16, 1220. [Google Scholar] [CrossRef] [Green Version]

- Eker, S.; Reese, G.; Obersteiner, M. Modelling the drivers of a widespread shift to sustainable diets. Nat. Sustain. 2019, 2, 725–735. [Google Scholar] [CrossRef] [Green Version]

- Headey, D.; Fan, S. Anatomy of a crisis: The causes and consequences of surging food prices. Agric. Econ. 2008, 39, 375–391. [Google Scholar] [CrossRef] [Green Version]

- Trade Policy and Food Security: Improving Access to Food in Developing Countries in the Wake of High World Prices; Gillson, I.; Fouad, A. (Eds.) World Bank Publications: Washington, DC, USA, 2014. [Google Scholar]

- d’Amour, C.B.; Wenz, L.; Kalkuhl, M.; Steckel, J.C.; Creutzig, F. Teleconnected food supply shocks. Environ. Res. Lett. 2016, 11, 035007. [Google Scholar] [CrossRef]

- Smith, V.H.; Glauber, J.W. Trade, policy, and food security. Agric. Econ. 2020, 51, 159–171. [Google Scholar] [CrossRef] [Green Version]

- van Ittersum, M.K.; van Bussel, L.G.; Wolf, J.; Grassini, P.; van Wart, J.; Guilpart, N.; Claessens, L.; de Groot, H.; Wiebe, K.; Mason-D’Croz, D.; et al. Can sub-Saharan Africa feed itself? Proc. Natl. Acad. Sci. USA 2016, 113, 14964–14969. [Google Scholar] [CrossRef] [Green Version]

- Hertel, T.W. Food security under climate change. Nat. Clim. Chang. 2016, 6, 10–13. [Google Scholar] [CrossRef]

- Fellmann, T.; Witzke, P.; Weiss, F.; van Doorslaer, B.; Drabik, D.; Huck, I.; Salputra, G.; Jansson, T.; Leip, A. Major challenges of integrating agriculture into climate change mitigation policy frameworks. Mitig. Adapt. Strat. Glob. Chang. 2018, 23, 451–468. [Google Scholar] [CrossRef] [PubMed]

- OECD; FAO. OECD-FAO Agricultural Outlook 2021–2030; OECD: Paris, France; FAO: Rome, Italy,, 2021. [Google Scholar]

- Jayne, T.S.; Chapoto, A.; Sitko, N.; Nkonde, C.; Muyanga, M.; Chamberlin, J. Is the scramble for land in Africa foreclosing a smallholder agricultural expansion strategy? J. Int. Aff. 2014, 67, 35–53. [Google Scholar]

- Crippa, M.; Solazzo, E.; Guizzardi, D.; Monforti-Ferrario, F.; Tubiello, F.N.; Leip, A.J. Food systems are responsible for a third of global anthropogenic GHG emissions. Nat. Food 2021, 2, 198–209. [Google Scholar] [CrossRef]

- Laborde, D.; Parent, M.; Smaller, C. Ending Hunger, Increasing Incomes, and Protecting the Climate: What Would It Cost Donors; IFPRI: Wahington, DC, USA, 2020. [Google Scholar]

- Vieira, A.C.; da Silva, E.M.; Odakura, V.V. Development of a Web Application for Individual Carbon Footprint Calculation. In Proceedings of the 2021 XLVII Latin American Computing Conference (CLEI), Cartago, Costa Rica, 25–29 October 2021; IEEE: Manhattan, NY, USA, 2021; pp. 1–8. [Google Scholar]

- Matthews, A. Greening CAP Payments: A Missed Opportunity; Institute for International and European Affairs: Dublin, Ireland, 2013. [Google Scholar]