Optimal Contract Design in Contract Farming under Asymmetric Effort Information

1

School of Business and Administration, Hunan University of Finance and Economics, Changsha 410079, China

2

School of Economic and Trade, Hunan University, Changsha 410079, China

*

Author to whom correspondence should be addressed.

Sustainability 2022, 14(22), 15000; https://0-doi-org.brum.beds.ac.uk/10.3390/su142215000

Submission received: 28 August 2022

/

Revised: 2 November 2022

/

Accepted: 6 November 2022

/

Published: 13 November 2022

(This article belongs to the Special Issue Green and Sustainable Supply Chains)

Abstract

:This paper studies the contract design, optimal financing, and pricing decision of the leading agricultural enterprise when the level of effort of the farmer is private information. We use buyer direct finance and add agricultural income insurance to transfer risks to overcome the farmer’s loan difficulty and contract default caused by information asymmetry. We design four kinds of contracts, including the uninsured and symmetric information contract (SN contract), the uninsured and asymmetric information contract (AN contract), the insured and symmetric information contract (SY contract), and the insured and asymmetric information contract (AY contract). Through comparative analysis of the different types of contracts, several results are obtained. First, when there is no insurance, supervision of the leading enterprise can improve the farmer’s level of effort; but supervision costs are incurred, and incentive contracts can avoid the farmer’s moral hazard. Second, agricultural income insurance improves the farmer’s level of effort when information is asymmetric, which transfers risks and saves costs for all the game participants. Third, the leading enterprise prefers an asymmetric information contract and the farmer prefers AN contract when the probability of loan repayment is high.

1. Introduction

Contract farming, which was well practiced in developing countries in Latin America and Asia in recent years, is a system that rejects traditional agricultural production methods and operates with a business mindset [1]. In 2014, Starbucks signed contracts with more than 300,000 farmers in Latin America, Africa, and Asia; purchased more than 1 billion pounds of coffee beans; and established the ‘C.A.F.E.’ program to provide farmers with training in growing methods [2]. However, many problems are gradually exposed during the implementation of contract farming. The critical problem is that the performance rate of the contract cannot be guaranteed [3,4]. The main reasons why the contract cannot be guaranteed are as follows: Farmers’ output is at risk due to natural disasters [5], the limited repayment capacity of farmers, and other risk factors [1], which make it impossible to guarantee the performance of the contract. Meanwhile, farmers’ capital gap [6] and credit restrictions will directly affect output and lead to contract default [7,8,9]. In developing countries, especially in China, traditional credit financial institutions (rural credit cooperatives and agricultural banks) may be reluctant to provide loans to farmers due to the lack of effective collateral and high risk.

Buyer direct finance (BDF), in which the manufacturer directly provides loans to the upstream supplier and signs a purchase contract, is an internal financing method for supply chains [10,11]. Compared with traditional financial institutions, this financing method can greatly improve the overall efficiency of the supply chain. A previous study shows that buyers can provide financing for cash-strapped farmers [12]. In practice, China’s Mengniu Company set up dairy farms in poor areas of Inner Mongolia and other provinces and offered loans to farmers and herdsmen. The application of BDF in contract farming became a new trend in agricultural supply chain finance.

In addition to the shortage of funds, supply chain enterprises are also facing problems caused by information asymmetry [13,14]. Despite BDF solving the financial dilemma of farmers, the original information asymmetry in contract agriculture greatly affects the income of farmers and upstream enterprises, which is mainly reflected in the moral hazard caused by the unobservable efforts of farmers. That is, farmers’ use of loans is difficult to monitor, which can lead to a decline in production. In addition, natural disasters also affect crop yields. When output is uncertain, risk-averse farmers may be willing to pay the price or give up some income to reduce risks [1]. Agricultural income insurance is a new insurance tool that can be used to reduce risks. This kind of insurance is the most important component of the agricultural risk management system, is the globally recognized pillar policy of modern agricultural development, and is also the new agricultural “green box policy” permitted by the WTO. The European Union long explored and improved agricultural income insurance [15], and the most famous tool is the Agricultural Income Insurance Program 2014–2020, implemented by the common agricultural policy (CAP) [16]. As a new type of insurance contract, agricultural income insurance changes the single guaranteed output and guaranteed price into guaranteed income. The Chinese Academy of Agricultural Sciences also proposed document no. 1 of the Central Committee (2017) to explore the establishment of an income insurance system for agricultural products and build an “agricultural safety protection network”.

We hope to solve the two remarkable problems of financial difficulties and moral hazard in contract farming by addressing the following questions: How do we use BDF as an internal financing method in the agricultural supply chain? Can agricultural income insurance transfer contract performance risk? Moreover, how can we design contracts with optimal financing and pricing?

More specifically, we determine how to avoid moral hazard by studying the contract design of a leading enterprise and the incentive related to a farmer’s level of effort under asymmetric information and then compare this situation with the situation of symmetric information. We use the compensation mechanism of agricultural income insurance to transfer contract performance risks.

First, we study the information asymmetry problem, and we design and analyze the contract in which the farmer’s level of effort is observable (SN contract) and the contract in which her level of effort is unobservable (AN contract). We use principal–agent theory to design the incentive contract and avoid the moral hazard of the farmer. Furthermore, in the above problem, we consider the farmer’s purchase of agricultural income insurance. Insured contracts are designed for situations when the farmer’s level of effort is either observable (SY contract) or unobservable (AY contract). Finally, the four different types of contracts are compared horizontally and vertically.

We obtain the equilibrium contracts and the corresponding optimal financing and pricing, as well as the level of farmers’ equilibrium efforts under four conditions, and make a comparative analysis of different contracts. We find that the incentive contract and supervision system of the leading enterprise can avoid the moral hazard problem of the farmer such that the farmer’s level of effort under symmetric information is greater than that under asymmetric information, and the value of information is discussed. Moreover, in the case when insurance is purchased, agricultural income insurance makes the farmer’s level of effort under symmetric information less than that under asymmetric information, which can transfer risks. Although the supervision system of the leading enterprise can obtain information, it has a cost, which will reduce the purchase price of agricultural products. However, the risk-averse farmer already paid part of the insurance premium, and the cost paid by her will be higher under symmetric information. Therefore, the AY contract can better stimulate the farmer’s level of effort. In addition, when the probability of loan repayment is high, the farmer prefers the AN contract. For the leading enterprise, under the traditional uninsured condition, the supervision system can well stimulate her level of effort, but the system will generate a sunk cost, which will damage the enterprise’s profits. Similarly, the addition of agricultural income insurance can not only improve the production initiative of the farmer and the profits of the enterprise, but can also save system costs. Therefore, by comparing the equilibrium profits of the enterprise in the four contracts, it can be concluded that, different from the conventional situation, the leading enterprise prefers asymmetric information contracts on the whole. From the sensitivity analysis of the main parameters, we find that a high effort cost factor increases the farmer’s effort aversion and is more likely to stimulate moral hazard and affect the profits of the leading enterprise. The farmer’s risk aversion is positively correlated with her willingness to buy insurance. An excessive government premium subsidy will not have a long-term positive impact on the profits of the leading enterprise. Finally, in the expanded part of our paper, we study the insurance decision from the perspective of the farmer and find that there is a positive relationship between the farmer’s willingness to buy insurance and the effort cost factor.

The rest of the paper is organized as follows: A literature review is presented in Section 2. A problem description and benchmark model are presented in Section 3. Section 4 describes the SY contract, SN contract, and AN contract. Section 5 addresses the value of information and insurance. Section 6 describes the sensitivity analysis. Section 7 presents extensions. Section 8 gives the conclusion.

2. Related Literature

The issues addressed in our study are related to contract farming, supply chain finance, asymmetric information, and agricultural insurance. Among previous works, there are many studies that research contract farming that focus on the contract menu design of heterogeneous farmers, the optimal purchase price of agricultural products, and contract price analysis [12,17]. However, if this method is implemented, then credit institutions will be unwilling to provide loans to farmers due to their lack of collateral and low credit. Therefore, the contract performance rate and farmers’ participation are low [4]. Aiming to address this problem, Kandulu et al. [18] and Webby et al. [19] used the conditional value at risk (CVaR) to investigate the impact of climate change on farmers’ degree of risk aversion. Sharma and Vashishtha [4] concluded that if leading enterprises reserve the right to modify the purchase price when signing a contract, it would damage the income of farmers and lead to order default. Through an empirical study, Beckmann and Boger [17] concluded that only 38.5% of 306 pig farmers who signed agricultural contracts in Poland were willing to guarantee the performance of the contracts by law. However, most of the above literature focuses on farmers and seeks to improve the problems existing in contract farming from the perspective of farmers, but it fails to solve the issue that farmers’ default rate is high due to the contract design.

Compared with the traditional financing methods of financial institutions, BDF is easier to operate and can better improve the operating efficiency of a supply chain. Therefore, BDF is widely used in the field of supply chain finance, which was studied in many previous papers. Deng et al. [10] conducted a comparative analysis that assessed whether multiple heterogeneous suppliers in the assembly system obtained direct financing from the buyer. Tang et al. [11] compared and analyzed buyer direct financing and institution financing in the purchase contract for suppliers with financial constraints. Chod [20] analyzed how financing within the supply chain distorts retailers’ inventory decisions. BDF is applied less in the field of agricultural supply chains. Miller and Jones [21] mentioned buyer financing in the value chain financing model in their book and established a model with the goal of promoting economies of scale and reducing the risks of lenders and buyers. Soundarrajan and Vivek [22] studied enterprises in agricultural value chain financing and provided dynamic innovation services and technical assistance programs with low transaction costs to help participants in the chain improve their output quality and reduce risks. However, research on the use of buyer direct finance in contract farming is still more or less empirical.

There are many forms of insurance contracts in the field of agriculture, and most studies are divided by risk types, among which natural disaster insurance, yield insurance, and deductible insurance are the most studied [23,24,25]. Few scholars applied agricultural income insurance to the internal financing of an agricultural supply chain and contract farming.

The particularity of farmers and the financing structure of the supply chains cause risks in the trade credit process. Among the risks, the moral hazard of farmers is an artificial risk that may lead to the fund provider having difficulty recovering loans. The classic literature studied the uncertainty of farmers’ output using a mathematical model and the Cobb–Douglas function [24,26,27]. However, in terms of agricultural supply chain finance, there is little research on the impacts of output uncertainty and moral hazard on financing and loan repayment.

There are several differences between our paper and previous research: (i) In contract farming, the previous literature mainly started from the perspective of farmers to optimize agricultural contracts, but the financing problem of farmers still existed. Our paper starts from the perspective of the leading enterprise, addresses the financing channel, and takes buyer direct financing as the internal financing method of the supply chain. (ii) In terms of agricultural risk management, there is little research on agricultural income insurance. We use agricultural income insurance to transfer the contract performance risk and loan repayment risk caused by artificial and nonhuman factors in the agricultural production process. (iii) In research on contract farming and financing, there are few problems related to the information asymmetry and incentives related to farmers’ efforts. We use the principal–agent theory to study the incentives of the farmer and avoid moral hazard. Finally, an optimal agricultural contract is designed on the basis of the above three issues, and the financing strategy and purchase price of agricultural products are analyzed.

3. Problem Description and the Benchmark Model

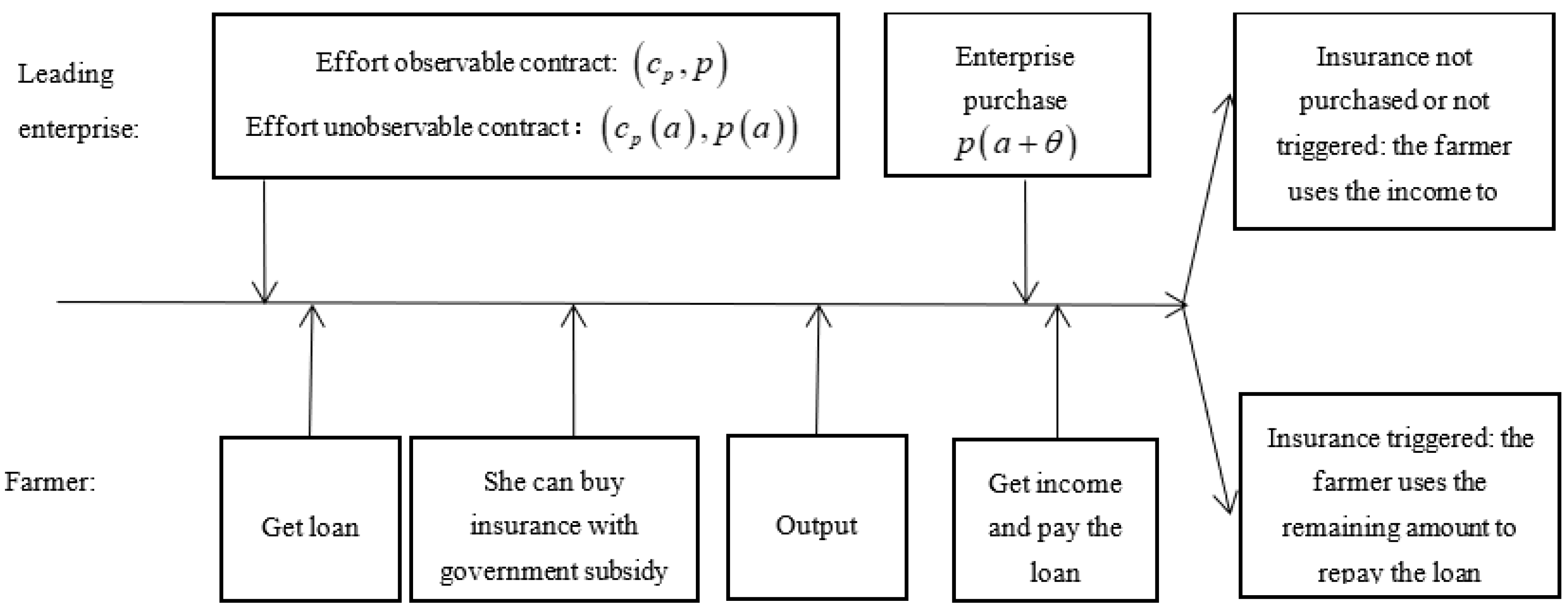

We consider a supply chain composed of a leading enterprise and a farmer. The farmer has a capital constraint, and the leading enterprise has a capital advantage, which can provide direct financing for the farmer. The cooperation and transaction between the enterprise and farmer are in the form of contract farming, which includes a loan amount and the purchase price of agricultural products . The farmer can choose to buy insurance. After the agricultural products mature, the leading enterprise buys the agricultural products according to the contract, and the farmer repays the loan. The event follows a Stackelberg game and is divided into two paths. The game timing depicted in Figure 1.

- (1)

- Case 1: symmetric information. The farmer’s level of effort can be observed during production. The leading enterprise provides a contract . When the farmer accepts the contract, the loan is used to cover the capital gap and production. The farmer can choose to buy agricultural income insurance using a government subsidy to guarantee her output. When the output is realized, the enterprise purchases the agricultural product according to contract, and the farmer’s income is realized. When the terms of the contract are met, the insurance will not be triggered, and the farmer will repay the loan with her income. When the terms of the contract are not met, the insurance company pays compensation according to the insurance contract, and the farmer uses all her remaining assets to repay the loan.

- (2)

- Case 2: asymmetric information. The farmer’s level of effort cannot be observed. The leading enterprise provides a contract . When the farmer accepts the contract, a loan is used to cover production, and the farmer can also choose to buy agricultural income insurance using a government subsidy.

3.1. Yield Uncertainty

After signing the contract with the farmer, the enterprise may face risks due to the uncertainty of the farmer’s output, which is mainly reflected in the following aspects:

- 1.

- Uncertain factors lead to output risks. Examples include drought, frost, hail, insect attacks, livestock diseases, feed shortages, extreme temperatures, and mechanical failures [1]. We define the factors as , and they are uncertain. is a random variable used to measure the state of the natural environment and follows a standard normal distribution.

- 2.

- The unobservable element of the farmer’s level of effort. The level of effort is a one-dimensional variable. When the farmer’s level of effort cannot be observed, is her private information. The level of effort will be changed by moral hazard, resulting in an uncertain output [28]. The uncertainty of the output can be expressed as:

The contract offered by the leading enterprise satisfies:

The principal–agent contract signed by the enterprise and the farmer includes the loan amount, the agricultural product purchase price, and the output. Among the variables, is the unit production cost of the farmer. This paper does not compare financing methods. The interest rate is exogenous and is not considered. p is the unit purchase price of agricultural products. The farmer’s effort cost is (k > 0) [11]. An increase in the effort cost factor k means greater disutility with the same effort. The loan repayment ability of the farmer is affected by exogenous uncertainties, effort, insurance, etc. The probability of her loan repayment is [29].

3.2. The Risk Types of the Client and Agent

As the client of the contract, the leading enterprise is assumed to be risk neutral. The investor is risk neutral regarding the certainty of the equivalent return and his expected return on investment. The farmer is a risk-averse agent [29]. This point also provides a basis for the insured contract included in Section 4.2 and Section 4.3. The farmer’s deterministic equivalent return is equal to her expected return minus the cost of the risk cost.

The utility function of the farmer is , which is characterized by constant absolute risk aversion. The function has a nice property in that it uses r to measure risks. When r = 0, the farmer is risk neutral; when r < 0, the farmer is risk-preferring.

and is defined by the certainty equivalent (CE), and we can obtain:

Equation (4) shows that if the farmer’s utility function is , when the expected return is 0, she still believes that the certainty equivalent return of the investment is , where is the risk premium and her risk cost is .

3.3. The Benchmark Model (SN Contract)

Symmetric information means that the leading enterprise implements a supervision system on the farmer to effectively monitor contract compliance [30]. The leading enterprise has an inspector who can detect the real level of effort of the farmer [31]. The detection cost is , and the reservation income level is 0.

The leading enterprise’s cash flow satisfies:

The formulas show that when the farmer repays the full loan, the income of the leading enterprise is the sales revenue minus the acquisition cost, where is the exogenous selling price of agricultural products. When the farmer cannot repay the entire loan, she has a limited ability to repay the full value of the agricultural products, and the supervision system of the leading enterprise will pay the supervision cost .

The expected utility of the leading enterprise is equal to his expected profit:

The farmer’s cash flow and expected profit are:

When the farmer can repay the entire loan, her income calculated as the income after the loan is repaid. When the farmer cannot repay the full loan, she has to use all her remaining assets to repay the loan. In addition, the farmer needs to pay the effort cost and risk cost.

The farmer’s expected profit satisfies:

The incentive compatibility constraint (IC) does not work when effort is observable. For any level of effort of a, it can be achieved by satisfying the participation constraint (IR) and the mandatory contract. Therefore, the optimal contract and the optimal level of effort a are selected to solve the equilibrium problem. The profit maximization problem of the benchmark model (SN contract) can be written as:

In the optimal case, IR is satisfied (the leading enterprise does not have to pay the farmer more).

By substituting IR into the objective function with , the above problems can be reformulated as:

The first order conditions of the optimization are:

Since these formulas involve practical problems, the parameters are non-negative. When , the equilibrium solutions are and . According to and , the higher that is, the higher the farmer’s level of effort and the purchase price will be.

By substituting the above results into the farmer’s IR, we can obtain:

Proposition 1

When the leading enterprise can observe the farmer’s level of effort, the risk problem and incentive problem can be solved independently. The Pareto optimal risk sharing and optimal level of effort can be realized simultaneously, and the optimal contract can be expressed as follows:

According to Proposition 1, the leading enterprise requires the farmer to choose the level of effort of . If the farmer really chooses , then the leading enterprise will pay her according to the of the contract. Otherwise, the farmer will receive (the minimum reserve income of the farmer under the SN contract).

Under the SN contract, leading enterprises can better supervise farmers, and farmers do not need insurance to cooperate with these enterprises to obtain stable and adequate loan funds. Therefore, if a leading enterprise has sufficient capital strength and an anti-risk capability and likes to implement a supervision system to obtain an information advantage, then he can use the SN contract.

4. Contract Design

4.1. The Uninsured and Asymmetric Information Contract (AN Contract)

Intuitively, according to Proposition 1, the optimal level of effort for the leading enterprise is not optimal for the farmer at a given retained income . Therefore, if the real level of effort is not observed, then the farmer will choose , which can improve her welfare. Because output is not only related to the farmer but is also affected by exogenous uncertainties, she can evade blame from the leading enterprise by blaming her low output on adverse natural environment factors. Similarly, if the leading enterprise fails to observe a, then it cannot prove that low output is the result of the lack of effort of the farmer, which is the so-called moral hazard.

In other words, with the benchmark contract (SN contract), Pareto optimality cannot be achieved if the leading enterprise cannot directly observe the farmer’s level of effort. Given , the farmer will choose the level of effort that maximizes her certainty equivalent return. The first-order condition means:

Therefore, the farmer will choose instead of .

When the level of effort is not observed, the discussion of the AN contract focuses on the determination of the farmer’s incentive compatibility constraint. Given a contract , the first-order condition method (e.g., [32]) is adopted to convert the IC constraint to . The optimization problem of the AN contract can be expressed as:

Among the variables:

(IR) and (IC) are inserted into the maximization problem, which is converted to:

The first order condition can be given as:

This condition means that the farmer has to bear some risk. P is an increasing function of r and k, i.e., , and we can see that for a given p, a greater r means a higher risk cost. However, the negative utility of the farmer’s effort cost is also higher, so the optimal incentive contract should balance the incentive and risk.

We can also obtain:

Proposition 2.

When the leading enterprise cannot observe the farmer’s level of effort, the optimal AN contract can be expressed as:

Under the IC constraint, the farmer can achieve a maximum level of effort of , and the leading enterprise gives the contract after the farmer’s choice. The loan amount is , and the purchase price is .

If a leading enterprise signs an AN contract with farmers, then although the farmers’ level of effort cannot be observed, he can avoid the moral hazard through the IC constraint. If it is inconvenient for some enterprises to implement supervision systems, then the optimal incentive contract under asymmetric information can be designed according to the AN contract.

Lemma 1.

The expected output is , and the farmer’s net loss satisfies:

Through the above comparison of and , it can be obtained that: . The optimal level of effort under asymmetric information is strictly less than that under symmetric information. This situation benefits from the supervision system of the leading enterprise. The farmer’s level of effort is maximally stimulated by the information symmetry, which is consistent with our intuition, but the enterprise has a sunk cost.

4.2. The Insured and Symmetric Information Contract (SY Contract)

The leading enterprise offers the SY contract, which requires the farmer to purchase agricultural income insurance. There are generally four types of agricultural income insurance products in the United States (according to the United States Department of Agriculture Risk Management website annual agricultural insurance policy reports).

Our question applies to type B in Table 1. The compensation method of income insurance is the following: when the income of the farmer is lower than the guaranteed income level of , the difference between the actual compensation income and the guaranteed income of the insurance company is paid. The insurance premium is determined according to a certain percentage of the guaranteed income, which is m, where :

The government will provide a certain premium subsidy to the farmer to cover a proportion of the premium [15], and the ratio of the subsidy is z. The insurance premium is:

When the leading enterprise implements a supervision system, the problem is similar to that of the SN contract. The optimal problem is solved by selecting a contract and level of effort a.

The cash flow of the enterprise is

His expected profit is

The farmer’s cash flow and expected profit are:

The optimization problem of the SY contract can be written as:

In the optimal case where the IR is set up, there is no need for the leading enterprise to pay the farmer more.

The objective function is expressed as follows:

We can obtain:

and

Proposition 3.

The optimal SY contract can be expressed as:

In the SY contract, the leading enterprise chooses to implement a supervision system and requires the farmer to purchase insurance to transfer risks. Similar to the SN contract, when the farmer chooses their level of effort , the leading enterprise will pay her according to ; otherwise, she will receive (her retained income level under the SN contract). If is small enough, then she will not choose .

4.3. The Insured Asymmetric Information Contract (AY Contract)

When the level of effort is not observed, Pareto optimality cannot be realized in the SY contract for the same reason as described in Section 4.1. The AY contract discussion focuses on how the IC constraint is determined when purchasing agricultural income insurance. Given (), the IC constraint can be written as . The optimization problem of the AY contract is

and

By substituting IR and IC into the objective function of Equation (36), the maximization problem of the AY contract is converted into:

The first order condition is

and

The optimal AY contract is as follows:

Similarly, the optimal level of effort of the farmer is , and the leading enterprise pays the farmer according to the corresponding contract. If the leading enterprise cannot implement a supervision system, then he can ask the farmer to buy insurance to guarantee her income. The optimal AY contract conforms to . The loan amount is , and the purchase price is .

Lemma 2.

Comparing and , we can obtain .

This is an interesting and contrary conclusion to Lemma 1. When purchasing insurance, by comparing the SY and AY contracts, we find that the effort under asymmetric information is higher than the effort under supervision. For the leading enterprise, the supervision cost will be passed on to the purchase price, making it lower (). In a symmetric information environment, the farmer’s lost benefits and increased costs are reflected in the insurance premium and purchase price. Therefore, insurance improves the production initiative of the farmer. The AY contract is more attractive to the farmer and better motivates her effort while saving the supervision cost. The leading enterprise’s profit is , and . The supervision cost makes the enterprise prefer the AY contract.

5. The Value of Insurance and Information

When comparing the SN contract and AN contract, the difference in the farmer’s level of effort can be concluded directly from Lemma 1. In addition, the value of information is also reflected in the purchase price and loan amount.

Lemma 3.

If , and .

If the farmer has a high probability of repaying the loan in full, then the leading enterprise under the SN contract (information symmetry) can set a higher purchase price to encourage her, and he does not have to lend her too much. Lemma 1 shows that in the AN contract, the farmer’s effort is low when information is asymmetric, the effort cost and risk cost are small, and the loan amount increases. Therefore, when the repayment probability is higher than 2/3, the risk-preferring farmer prefers the AN contract. However, for the risk-averse farmer, the incentive from the larger loan amount is not strong. The risk-averse farmer likes to obtain more income from a higher purchase price and prefers the SN contract.

Lemma 4.

The profit of the leading enterprise still meets:

Among the four types of contracts, the incentives of the principal –agent contracts achieved good results, improving the profit of the leading enterprise under asymmetric information (Lemma 2). On this basis, the insurance makes the farmer’s level of effort higher when she is not supervised, which can transfer risks and improve her production initiative. Therefore, for the leading enterprise, the asymmetric information contract is better than the symmetric information contract.

Corollary 1.

The profit gap is

When the purchase price changes due to insurance and the guaranteed income satisfies the inequality , there is little difference between the two prices. Therefore, the leading enterprise prefers the AY contract. If the situation is the opposite, then the leading enterprise prefers the SY contract.

6. Sensitivity Analysis

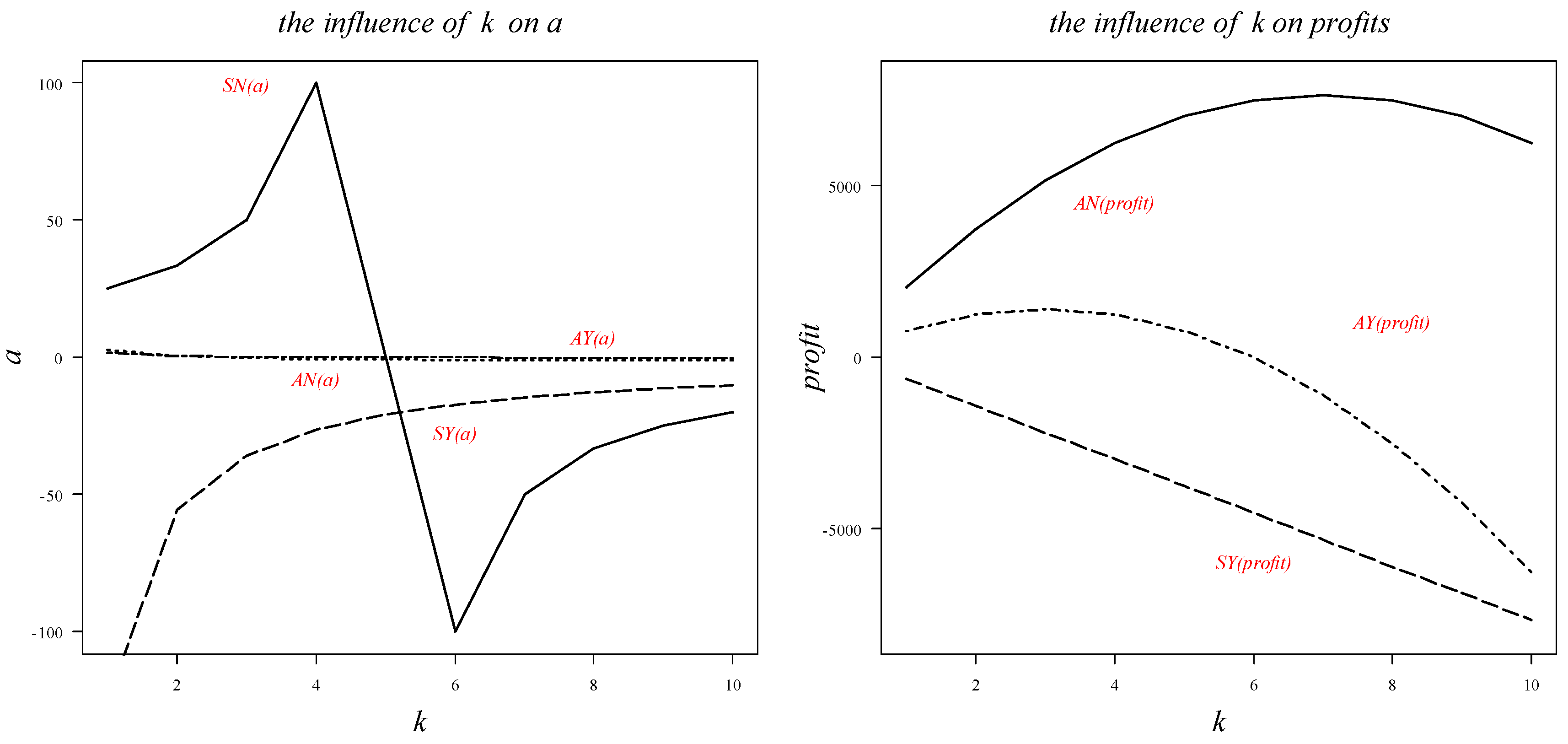

The main parameters studied in this section include the effects of k (the effort cost factor), r (the farmer’s risk aversion), and z (the government subsidy ratio) on the influence of the four contracts; the level of effort; the loan amount; and the purchase price. When analyzing the impact of k on contracts, we mainly consider its relationship with a and its impact on the profit of the leading enterprise. The parameters are all expanded by ten times so that , , , and k is changed within the range of 1:10. The impacts of k on the profit of the leading enterprise and a are shown in Figure 2.

In the left subfigure of Figure 2, the effort cost factor k in the AN contract, SY contract, and AY contract has a roughly positive diminishing marginal relationship with the equilibrium solution. As the disutility of the effort cost increases, the level of effort slowly increases. In the SN contract, the effort cost turns at k = 4 and k = 6. The effect of k on the profit of the leading enterprise is negatively correlated in the three contracts (the profit of the leading enterprise in the SN contract is 0, which is not shown in Figure 2). The higher the farmer’s effort cost is, the more it will hurt the profit of the leading enterprise.

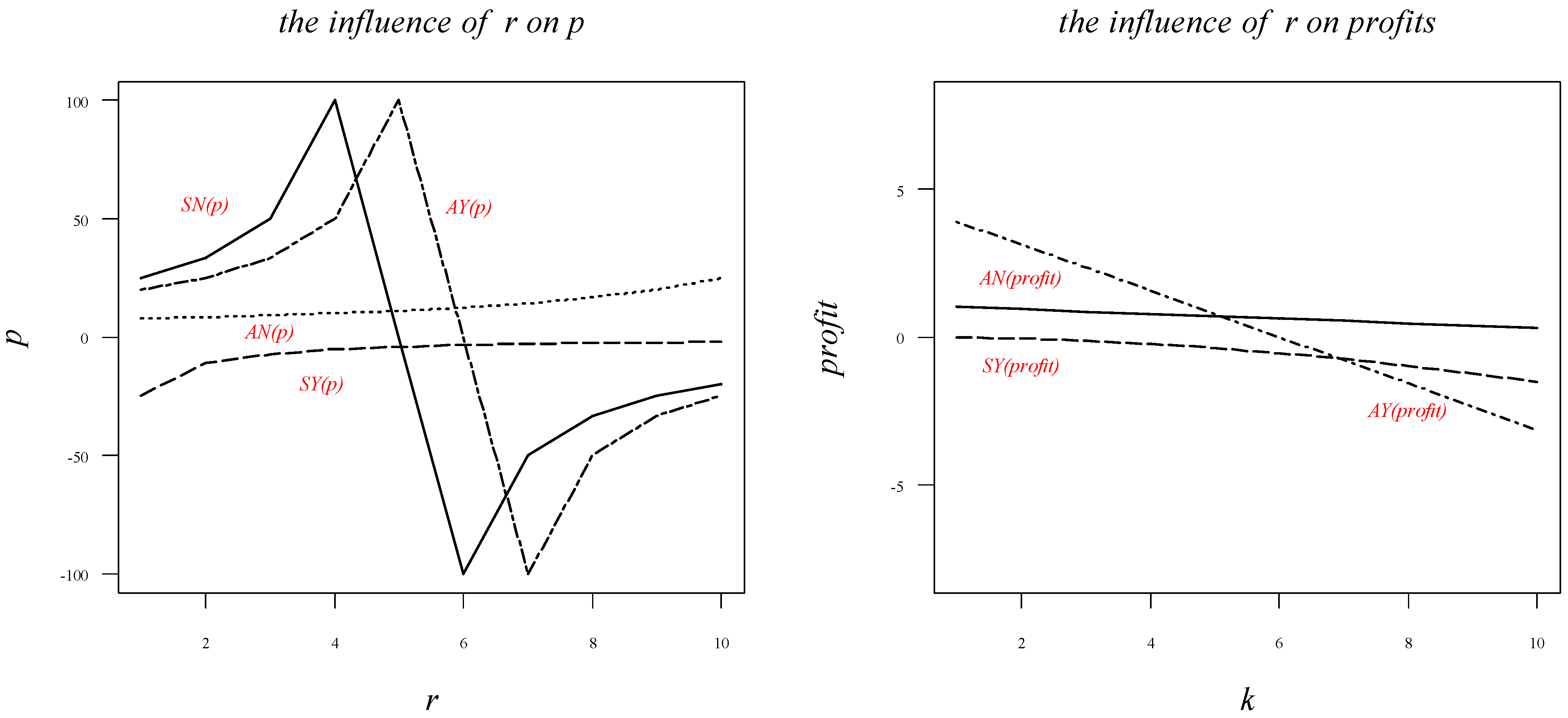

When analyzing the impact of the farmer’s risk aversion on contracts, the relationship among the degree of risk aversion, risk cost, and profit of the leading enterprise are mainly considered. , , , and r varies in the range of 1:10.

In Figure 3, when the degree of risk aversion is small, the risk cost of the farmer shows an increasing trend. As the degree of risk aversion increases, the risk cost has a certain decreasing trend. As r increases, the profit of the leading enterprise gradually decreases and the risk cost of the farmer increases; therefore, she is more inclined to buy insurance. When purchasing insurance, the moral hazard may reduce the farmer’s level of effort and ability to repay the loan, as well as the profit of the leading enterprise. Compared with the AY contract, the SY contract has a supervision mechanism, which slows down the profit decline.

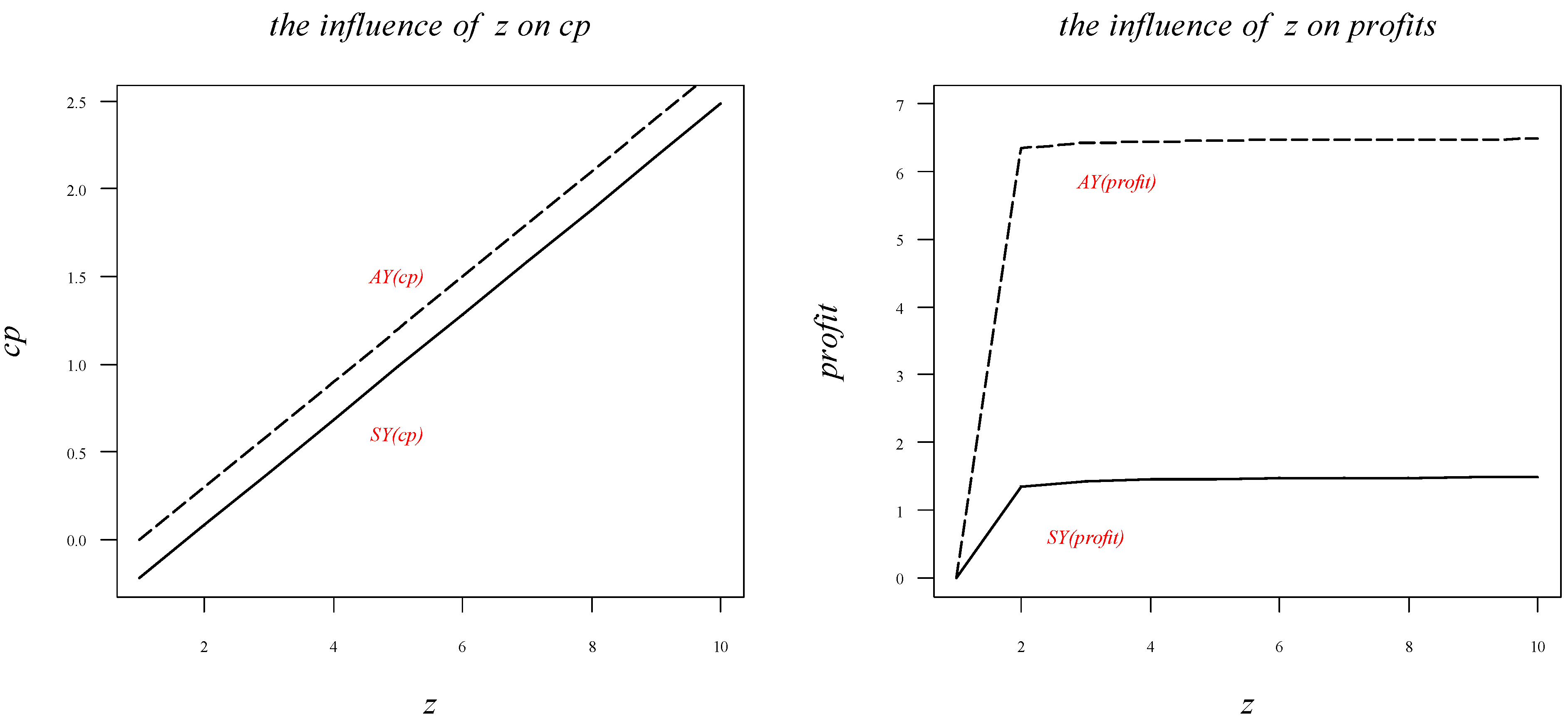

When analyzing the impact of the government subsidy ratio z on contracts, we mainly consider its impact on the loan amount and profit of the leading enterprise. Let p = 100, , r = 5, , , m = 5, and z change within the range of 0:5.

In Figure 4, the relationship between z and the loan is quite intuitive. From the perspective of the farmer, the higher the premium subsidy the government provides to her, the stronger her willingness to buy insurance will be. The loan amount from the leading enterprise will also increase. The subsidy ratio will initially increase his profit and then gently increase it. After the farmer receives the subsidy, the amount of insurance she purchases will not increase indefinitely. The leading enterprise’s income insurance claim also has an upper bound.

In summary, for the farmer, too high of an effort cost factor will increase her effort aversion and make it more likely that the moral hazard problem occurs; in addition, her risk aversion is negatively correlated with the risk cost. The increase in r makes the farmer more willing to buy insurance. The government subsidy will increase the farmer’s willingness to buy insurance and increase the loan amount. For the leading enterprise, too high of a k will decrease the farmer’s level of effort, which is bad for him. The increase in r may cause the farmer to become lazy and indirectly hurt his profit. A higher government subsidy will not make his profit continue to increase.

7. Extensions: Decision-Making on the Level of Insurance from the Perspective of the Farmer

This study assumes that the farmer will buy insurance based on the advice of an insurance company t, but in practice, insurance companies sell different types of insurance programs. The farmer will base her level of insurance on her degree of risk aversion, the government subsidy, and her financial conditions. This section focuses on the farmer’s level of insurance and level of effort after buying insurance.

We assume the following: the farmer chooses the level of insurance by herself. To simplify the problem, we consider that the farmer decides to buy insurance when the purchase price and loan amount are known. We defined as the unit level of insurance, and exogenous uncertainties are uniformly distributed (0,1). The risk premium of the farmer is .

In line with Wang and Luo (2015), we assume the insurance premium is

The minimum repayment demand function is

We denote as the zero bound for the repayment of the loan, i.e., .

The farmer’s cash flow is

The expected income of the farmer is

According to the Stackelberg game, in the sequence of the event, the first-order condition for effort is

Inserting the reaction function into the profit function, we can obtain:

Thus, and at the equilibrium level of insurance. When the premium subsidy ratio increases, the reduced insurance cost will increase the amount of insurance coverage purchased by the farmer. The increase in the effort cost factor will increase the disutility of effort, and the risk of her not repaying the loan will increase. At this time, the farmer will be more willing to buy insurance.

Proposition 4.

The equilibrium level of effort and insurance premium of the farmer are:

We can see that there is also a positive correlation between the premium subsidy ratio and premium.

The farmer’s equilibrium profit is

We can conclude that if the premium subsidy ratio is higher when the farmer selects a level of insurance, then the premium will be higher when her effort cost factor is larger. The level of effort is positively correlated with the premium subsidy ratio and profit, and the government subsidy has a promotional effect on the farmer’s level of effort and willingness to buy insurance.

8. Conclusions

In contract farming, information asymmetry incurs problems related to farmers’ moral hazards. We consider an agricultural supply chain that consists of a leading enterprise and a farmer. In the supply chain, the leading enterprise provides a loan to the farmer. We design four contracts, including the SN contract, AN contract, SY contract, and AY contract. The key issues are the optimal decisions on contracts (loan amounts and farm product purchase prices), how the leading enterprise forms contracts to incentivize the farmer when her effort is private information, and whether the use of agricultural income insurance optimizes contracts. Specifically, in the four types of contracts, we obtain the optimal contracts that all game participants need to follow when the leading enterprise is faced with different situations.

We obtained the following results: (i) Insurance (the SY contract and AY contract) makes the farmer’s unobservable level of effort higher than that in the observable situation, which can better transfer risks. The leading enterprise can save the supervision cost. The decisions and benefits of both sides are optimized. (ii) Regarding the leading enterprise’s contract preferences, our conclusions are different from those of previous studies: an asymmetric information contract is more beneficial to the leading enterprise. When insurance is not considered, the supervision cost causes him to prefer the AN contract. When insurance is considered, the cost saving, risk transfer, and promotion of the farmer’s effort make him prefer the AY contract. In addition, the farmer’s contract preferences are related to the probability of repayment. When the probability is high, the farmer prefers the AN contract. (iii) According to the sensitivity analysis, an increase in the effort cost factor is more likely to increase the moral hazard caused by the farmer. Increases in the risk cost factor and government premium subsidy ratio will make the farmer more willing to buy insurance. However, an excessive government subsidy will not keep increasing the profits of the enterprise. In the extensions, we find that the premium subsidy and cost factor of the farmer’s effort have positive promotional effects on the farmer’s willingness to purchase insurance. In addition, the effect of insurance on the farmer’s effort is strengthened.

Finally, we highlight some interesting future research directions. When the purchase price is used as the decision-making factor of the leading enterprise, the farmer can make the financing and premium decisions. In addition, we can consider how the leading enterprise can overcome the moral hazard of the farmer in this situation and encourage her level of effort.

Author Contributions

Conceptualization: H.Z.; methodology: H.Z. and J.X.; writing-original draft: H.Z.; writing-review & editing: H.Z. and J.X.; formal analysis: C.T. and H.Z.; software: H.Z.; investigation: H.Z.; visualization: H.Z.; funding acquisition: C.T.; project administration: C.T.; supervision: C.T. All authors have read and agreed to the published version of the manuscript.

Funding

This research was supported by the Hunan Province Natural Science Foundation of China under Grants 2022JJ30110.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- MacDonald, J.M.; Perry, J.; Ahearn, M.C.; Banker, D.; Chambers, W.; Dimitri, C.; Southard, L.W. Contracts, markets, and prices: Organizing the production and use of agricultur-al commodities. USDA-ERS Agric. Econ. Rep. 2004, 837. [Google Scholar] [CrossRef]

- Gruley, B.; Patton, L. To Stop the Coffee Apocalypse, Starbucks Buys a Farm. 2018. Available online: https://www.bloomberg.com/news/articles/2014-02-13/to-stop-the-coffee-apocalypse-starbucks-buys-a-farm#:~:text=To%20Stop%20the%20Coffee%20Apocalypse%2C%20Starbucks%20Buys%20a,the%20end%20of%20joe%20as%20we%20know%20it (accessed on 27 August 2022).

- Beckmann, V.; Boger, S. Courts and contract enforcement in transition agriculture: Theory and evidence from Poland. Agri-Cult. Econ. 2004, 31, 251–263. [Google Scholar] [CrossRef]

- Sharma, P.; Vashishtha, S. Contract farming: The survey on different issues. Int. J. Comput. Sci. Manag. Stud. 2012, 12, 20–25. [Google Scholar]

- Amadu, F.O.; Miller, D.C.; McNamara, P.E. Agroforestry as a pathway to agricultural yield impacts in climate-smart agriculture investments: Evidence from southern Malawi. Ecol. Econ. 2020, 167, 106443. [Google Scholar] [CrossRef]

- Maia, A.G.; Miyamoto BC, B.; Garcia, J.R. Climate change and agriculture: Do environmental preservation and ecosystem ser-vices matter? Ecol. Econ. 2018, 152, 27–39. [Google Scholar] [CrossRef]

- Egwu, P.N. Impact of agricultural financing on agricultural output, economic growth and poverty alleviation in Nigeria. J. Biol. Agric. Healthc. 2016, 6, 36–42. [Google Scholar]

- Odoemenem, I.U.; Obinne, C.P.O. Assessing the factors influencing the utilization of improved cereal crop production tech-nologies by small-scale farmers in Nigeria. Indian J. Sci. Technol. 2010, 3, 180–183. [Google Scholar] [CrossRef]

- Zylbersztajn, D.; Gualberto, A.P.L.; Nadalini, L.B. Tomatoes and Courts: Strategy of the agro-industry facing weak contract en-forcement. In Proceedings of the Annual Conference of the International Society for New Institutional Economics, Budapest, Hungary, 1–13 September 2003. [Google Scholar]

- Deng, S.; Gu, C.; Cai, G.; Li, Y. Financing Multiple Heterogeneous Suppliers in Assembly Systems: Buyer Finance vs. Bank Finance. Manuf. Serv. Oper. Manag. 2018, 20, 53–69. [Google Scholar] [CrossRef]

- Tang, C.S.; Yang, S.A.; Wu, J. Sourcing from suppliers with financial constraints and performance risk. Manuf. Serv. Oper. Manag. 2018, 20, 70–84. [Google Scholar] [CrossRef] [Green Version]

- Federgruen, A.; Lall, U.; Şimşek, A.S. Supply chain analysis of contract farming. Manuf. Serv. Oper. Manag. 2019, 21, 361–378. [Google Scholar] [CrossRef]

- Xu, J.; Wang, P.; Xu, Q. Impact of Information Asymmetry on the Operation of Green Closed-Loop Supply Chain under Government Regulation. Sustainability 2022, 14, 7999. [Google Scholar] [CrossRef]

- Sun, H.; Wang, H.; Steffensen, S. Mechanism design of multi-strategy health insurance plans under asymmetric information. Omega 2022, 107, 102554. [Google Scholar] [CrossRef]

- Meuwissen, M.P.M.; Huirne, R.B.M.; Skees, J.R. Income insurance in European agriculture. EuroChoices 2003, 2, 12–17. [Google Scholar] [CrossRef]

- Pérez-Blanco, C.D.; Delacámara, G.; Gómez, C.M. Revealing the willingness to pay for income insurance in agriculture. J. Risk Res. 2016, 19, 873–893. [Google Scholar] [CrossRef] [Green Version]

- Boyabatlı, O.; Kleindorfer, P.R.; Koontz, S.R. Integrating long-term and short-term contracting in beef supply chains. Manag. Sci. 2011, 57, 1771–1787. [Google Scholar] [CrossRef] [Green Version]

- Kandulu, J.M.; Bryan, B.A.; King, D.; Connor, J.D. Mitigating economic risk from climate variability in rain-fed agriculture through enterprise mix diversification. Ecol. Econ. 2012, 79, 105–112. [Google Scholar]

- Webby, R.B.; Adamson, P.T.; Boland, J.; Howlett, P.G.; Metcalfe, A.V.; Piantadosi, J. The Mekong—Applications of value at risk (VaR) and conditional value at risk (CVaR) simulation to the benefits, costs and consequences of water resources development in a large river basin. Ecol. Model. 2007, 201, 89–96. [Google Scholar]

- Chod, J. Inventory, risk shifting, and trade credit. Manag. Sci. 2017, 63, 3207–3225. [Google Scholar] [CrossRef] [Green Version]

- Miller, C.; Jones, L. Agricultural Value Chain Finance: Tools and Lessons; FAO and Practical Action Publishing: Rugby, UK, 2010. [Google Scholar]

- Soundarrajan, P.; Vivek, N. A study on the agricultural value chain financing in India. Agric. Econ. 2015, 61, 31–38. [Google Scholar] [CrossRef] [Green Version]

- Jørgensen, S.L.; Termansen, M.; Pascual, U. Natural insurance as condition for market insurance: Climate change adaptation in agriculture. Ecol. Econ. 2020, 169, 106489. [Google Scholar] [CrossRef]

- Nelson, C.H.; Loehman, E.T. Further toward a theory of agricultural insurance. American J. Agric. Econ.-Ics 1987, 69, 523–531. [Google Scholar]

- Wang, W.; Luo, J. Optimal financial and ordering decisions of a firm with insurance contract. Technol. Econ. Dev. Econ. 2015, 21, 257–279. [Google Scholar] [CrossRef]

- Just, R.E.; Pope, R.D. Stochastic specification of production functions and economic implications. J. Econom. 1978, 7, 67–86. [Google Scholar] [CrossRef]

- Coyle, B.T. Risk aversion and yield uncertainty in duality models of production: A mean-variance approach. Am. J. Agric. Econ. 1999, 81, 553–567. [Google Scholar] [CrossRef]

- Zhang, H.; Kong, G.; Rajagopalan, S. Contract design by service providers with private effort. Manag. Sci. 2018, 64, 2672–2689. [Google Scholar] [CrossRef]

- Salanié, B. The Economics of Contracts: A Primer; MIT Press: Cambridge, MA, USA, 2005. [Google Scholar]

- Eaton, C.; Shepherd, A. Contract Farming: Partnerships for Growth; Food and Agriculture Organization of the United Nations: Rome, Italy, 2001; 166p. [Google Scholar]

- Kuksov, D.; Liao, C. When showrooming increases retailer profit. J. Mark. Res. 2018, 55, 459–473. [Google Scholar] [CrossRef]

- Mirrless, J. The optimal structure of authority and incentives within an organization. Bell J. Econ. 1976, 7, 105–131. [Google Scholar] [CrossRef]

Figure 1.

Sequence of events.

Figure 2.

Impact of k on the profit of the leading enterprise and a.

Figure 3.

Impacts of r on p and the profit of the leading enterprise.

Figure 4.

Impact of z on cp and the profit of the leading enterprise.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Main types of agricultural income insurance.

| American Agricultural Income Insurance Product System | |

|---|---|

| A | Individual farm income insurance with term price options (RP-HPO): guaranteed income per unit area = historical average yield per unit area × max (forecast price and market price at harvest time) × guaranteed level |

| B | Individual farm income insurance with no term price option (RP-HPE): guaranteed income per unit area = historical average yield per unit area × forecast price × guaranteed level |

| C | Regional crop income insurance with term price options (ARP-HPO): guaranteed income per unit area = county average historical yield × max (forecast price, market price during harvest) × guaranteed level |

| D | Regional crop income insurance with no term price options (ARP-HPE): guaranteed income per unit area = county average historical yield × forecast price × guaranteed level |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Tang, C.; Zhang, H.; Xie, J. Optimal Contract Design in Contract Farming under Asymmetric Effort Information. Sustainability 2022, 14, 15000. https://0-doi-org.brum.beds.ac.uk/10.3390/su142215000

AMA Style

Tang C, Zhang H, Xie J. Optimal Contract Design in Contract Farming under Asymmetric Effort Information. Sustainability. 2022; 14(22):15000. https://0-doi-org.brum.beds.ac.uk/10.3390/su142215000

Chicago/Turabian StyleTang, Chunhua, Huiyuan Zhang, and Jiamuyan Xie. 2022. "Optimal Contract Design in Contract Farming under Asymmetric Effort Information" Sustainability 14, no. 22: 15000. https://0-doi-org.brum.beds.ac.uk/10.3390/su142215000

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.