Sustainable Business Model of Modern Enterprises in Conditions of Uncertainty and Turbulence

, , , , and

, , , , and

Abstract

:1. Introduction

- Communication with suppliers;

- Communication with consumers;

- Technological connections within the value chains in the same division of the enterprise, as well as the connection between the value chains in several divisions of the enterprise;

- Connections in the processes of design, production, marketing, as well as in the performance of ancillary functions.

- Value proposition, which is in the products and services and which the company offers to their customers;

- Value creation system, which includes the company’s relationships with suppliers, key consumer segments, as well as the value chains themselves;

- Assets that the company uses to create value proposals;

- Financial model of the enterprise, which determines both the structure of income and the structure of costs that the enterprise generates to create value for the consumer.

- (1)

- Focused on a profit and business processes of the enterprise: Afuah, A., Gambardella, A., Debelak, D., Mullins, J., Wheelen, T., Chesbrough, H.;

- (2)

- Focused on internal business processes and structure: Strekalova, N., Kharitonova, G., Klimchuk, A.;

- (3)

- Focused on the formation of value for the external client of the enterprise: Magretta, J., Osterwalder A., Pigneur, Y., Porter, M., Rappa, M., Revutskaya, N., Slávik, Š., Teece, D., Thomson P., Watsons, D., Zott, C., Amit, R., Massa, L.

2. Materials and Methods

- An integrated indicator of corporate sustainability;

- The transparency index of the enterprise.

- Class of efficiency of implementation of the business model of the enterprise and class of the enterprise on corporate sustainability;

- Class of efficiency of implementation of the business model of the enterprise and class of the enterprise on transparency.

- To analyze theoretical approaches to the impact of the openness of a company to its stakeholders on the effectiveness of business models of enterprises;

- To propose a methodological approach to assessing the corporate sustainability and transparency of enterprises as important components of the formation and implementation of their business models;

- To study the activities of Ukrainian enterprises of different types of economic activity and identify their distribution by classes of corporate sustainability and transparency;

- To develop an algorithm for evaluating the effectiveness of the implementation of the business models of Ukrainian enterprises and to divide them into classes;

- To reveal the relationship between corporate sustainability and transparency of enterprises on the one hand and the effectiveness of their business models on the other;

- To formulate proposals by which to increase the efficiency of formation and implementation of business models of Ukrainian enterprises in the conditions of sustainable development.

3. Description of the Studies

- -

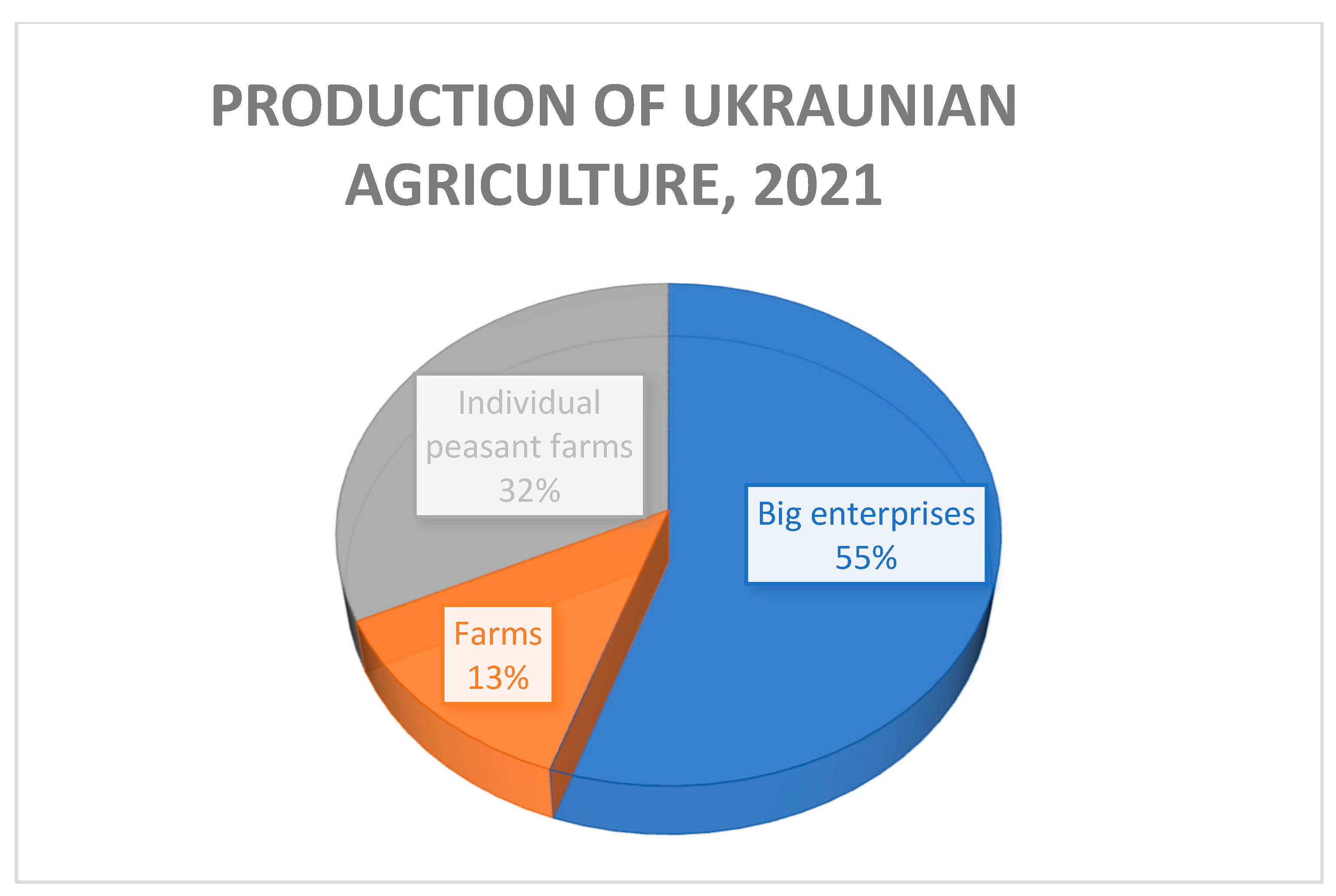

- A favorable geographical location;

- -

- The largest bank of arable land in Europe (around 33 million ha), which represents 12% of arable land in Europe and 2.2% of arable land in the world;

- -

- One-third of black earth in the world.

4. Results and Discussion of Studies

4.1. Methodical Approach to the Evaluation of Enterprises

- (1)

- Depending on the industry to which the company belongs, we get the maximum number of points for the area of important issues to which the indicator belongs;

- (2)

- The maximum score of each indicator in this area of important issues is calculated by dividing the maximum number of points for the area of important issues by the total number of indicators that are part of it;

- (3)

- We calculated the actual scores for the indicator for the company by multiplying the maximum possible score of the indicator by the evaluation of the indicator in percentage, obtained as the arithmetic mean of the scores obtained for the issues that reveal the indicator.

4.2. Assessment of Corporate Sustainability of Enterprises

4.3. Assessment of Enterprise Transparency

4.4. Assessment by Arears of Important Issues by Spheres

- Composition of the highest body of corporate governance;

- The procedure for nominating and selecting candidates for members of the highest body of corporate governance;

- Development, approval and updating of strategic priorities;

- Assessment of the activities of the highest body of corporate governance;

- Corporate governance code;

- Organizational structure and powers of officials of the organization;

- Rules for remuneration of members of the highest corporate governance body and senior executives;

- International management standards and practices;

- Business processes of organization and management;

- Effectiveness of risk management processes;

- Identification, analysis and management of economic, environmental and social issues.

- Values, principles, standards and norms of behavior;

- Regulation and codification of management practice in the field of ethics and integrity;

- Internal and external mechanisms for reporting unethical or illegal behavior/dishonesty.

- Complete list of stakeholders and principles of their detection and selection;

- The organization’s approach to interaction with stakeholders and regulation of management practices on these issues;

- Consultations with stakeholders and issues discussed with them.

- Meetings, negotiations;

- Conferences, forums, panel discussions, press events;

- Web-site of the enterprise, the form of online application through the site;

- “Single window” and mailbox for sending documents;

- Social networks: Facebook, LinkedIn, Instagram, YouTube channel, SlideShare presentations.

- Corporate report (integrated report, sustainable development report, non-financial report, annual report, social report, etc.) and reporting cycle;

- Identification of important topics for the enterprise;

- Compliance of the prepared reporting with international standards and verification of data;

- Interaction with stakeholders in the framework of reporting.

- Created and distributed direct economic value;

- Financial support received from the state;

- Wages;

- Violation of the law.

- Supply chain of the organization;

- Costs for local suppliers;

- Negative impact on the practice of labor relations in the supply chain.

- Employees and staff turnover;

- Employees entitled to maternity/paternity leave;

- Collective agreement.

- Regulation and codification of management practices on social investments and local communities;

- Investments in community development;

- Implementation, realization of initiatives on development of local communities;

- Negative impact on local communities.

5. Conclusions

- Use industry indicators and industry areas of significant issues, which will the identification of industry leaders and more accurately assess enterprises in terms of conducting socially responsible business;

- Monitor the media and interview stakeholders in order to identify the reactions of enterprises to adverse events that were caused by their activities or inaction. The result of monitoring should be the adjustment of the values of certain indicators (relating to the area (/areas) of significant issues in which there occurred a negative event that caused (/could cause) image loss, financial damage, etc.) to the correction factor reflecting quality and speed the enterprise’s response is not such a negative event.

- For enterprises—increasing the efficiency of business models by reducing the impact of non-financial risks on their activities;

- For society and the state—increased competition for higher places in the rating, which will lead to real ESG programs and projects that will positively affect the quality of the environment and social processes in the country;

- For enterprises—attracting of cheaper investments in development from the sources of so-called “green investors;

- For enterprises—increasing the investment attractiveness of the enterprise, which is caused by its sustainable development;

- For enterprises—an opportunity to become a partner of a transnational corporation that requires their partners to adhere to the principles of sustainable development and corporate social responsibility.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Dziekański, P.; Prus, P.; Maitah, M.; Wrońska, M. Assessment of Spatial Diversity of the Potential of the Natural Environment in the Context of Sustainable Development of Poviats in Poland. Energies 2021, 14, 6027. [Google Scholar] [CrossRef]

- Afuah, A. Business Models: A Strategic Management Approach; McGraw-Hill Companies: Newyork, NY, USA, 2003; 432 p. [Google Scholar]

- Osterwalder, A.; Pigneur, I.; Bernarda, G.; Smith, A. Value Proposition Design; Wiley: Hoboken, NJ, USA, 2014; p. 320. [Google Scholar]

- Gambardella, A.; McGahan, A. Business-Model Innovation: General Purpose Technologies and their Implications for Industry Structure. Long Range Plan. 2010, 43, 262–271. [Google Scholar] [CrossRef]

- Debelak, D. Business Model Made Easy; McGraw-Hill Companies, Inc.: New York, NY, USA, 2006; 240p. [Google Scholar]

- Jablonski, A.; Jablonski, M. Business Models in Water Supply Companies-Key Implications of Trust. Int. J. Environ. Res. Public Health 2020, 17, 2770. [Google Scholar] [CrossRef] [PubMed]

- Ivashkiv, I.; Kupalova, H.; Goncharenko, N.; Andrusiv, U.; Streimikis, J.; Lyashenko, O.; Yakubiv, V.; Lyzun, M.; Lishchynskyi, I.; Saukh, I. Environmental Responsibility as a Prerequisite for Sustainable Development of Agricultural Enterprises. Manag. Sci. Lett. 2020, 10, 2973–2984. [Google Scholar] [CrossRef]

- Magomedova, A.; Ignatyuk, A.; Liubkina, O.; Murovana, T. FinTech as an innovation challenge: From big data to sustainable development. In Proceedings of the International Conference on Sustainable Futures: Environmental, Technological, Social and Economic Matters, Kyiv, Ukraine, 20–22 May 2020; Volume 166. [Google Scholar] [CrossRef]

- Magretta, J. Why Business Models Matter. HBR Publishing Corporation, 2002. Available online: https://hbr.org/2002/05/why-business-models-matter (accessed on 22 September 2022).

- Mahmoodi, M.; Roman, M.; Prus, P. Features and Challenges of Agritourism: Evidence from Iran and Poland. Sustainability 2022, 14, 4555. [Google Scholar] [CrossRef]

- Osterwalder, A.; Yves, P. Business Model Generation: A Handbook For Visionaries, Game Changers, and Challenger; Wiley: Hoboken, NJ, USA, 2010. [Google Scholar]

- Porter, M. What Is Strategy? Harvard Business Review; Harvard Business School Publishing Corporation: Brighton, MA, USA, 1996; pp. 61–78. [Google Scholar]

- Slávik, Š. Komparatívna analýza podnikateľských modelov. Ekon. A Manaz. 2011, 11, 23–43. [Google Scholar]

- Strekalova, N. The Concept of Business Model: The Methodology of System Analysis; Vestnik (Herald) of Saint Petersburg State University: Saint Petersburg, Russia, 2009; pp. 92–105. [Google Scholar]

- Thomson, P.; Brennan, R. Tickle: Digital Marketing for Tech Companies; London, UK, 2013; 288p. [Google Scholar]

- Kharitonova, G.; Klimchuk, A. The Use of Business Models in Managing a Company in a Crisis. Russia’s Transport Business. 2009, pp. 105–109. Available online: https://cyberleninka.ru/article/v/ispolzovanie-biznes-modeley-pri-upravlenii-kompaniey-v-usloviyah-krizisa-1 (accessed on 22 September 2022).

- Chesbrough, H. Open Business Models; Harvard Business School Press: Boston, MA, USA, 2006; 272p. [Google Scholar]

- Sjödin, D.; Parida, V.; Jovanovic, M.; Visnjic, I. Value Creation and Value Capture Alignment in Business Model Innovation: A Process View on Outcome Based Business Models. J. Prod. Innov. Manag. 2020, 37, 158–183. [Google Scholar] [CrossRef]

- Zott, C.; Amit, R.; Massa, L. The Business Model: Recent Developments and Future Research. J. Manag. 2011, 37, 1019–1042. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Balanced Scorecard. Translating Strategy into Action; Harvard Business Review Press: Brighton, MA, USA, 1996; 336p. [Google Scholar]

- Butenko, N.; Prokopenko, O.; Kazanska, O.; Deineha, I.; Omelyanenko, V. Communication business processes of industrial enterprises in the conditions of globalization. Int. J. Manag. 2020, 11, 884–895. Available online: https://www.iaeme.com/MasterAdmin/uploadfolder/IJM_11_05_081/IJM_11_05_081.pdf (accessed on 22 September 2022). [CrossRef]

- Drucker, P. Effective Enterprise Management; Williams: St. Petersburg, Russia, 2008; 224p. [Google Scholar]

- Govindan, K.; Shankar, K.M.; Kannan, D. Achieving sustainable development goals through identifying and analyzing barriers to industrial sharing economy: A framework development. Int. J. Prod. Econ. 2020, 227, 107575. [Google Scholar] [CrossRef]

- Kaminski, R.; Marcysiak, T.; Prus, P. The development of green care in Poland. In Proceedings of the 2018 International Conference Economic Science for Rural Development, Jelgava, Latvia, 9–11 May 2018; pp. 307–315. [Google Scholar]

- Nesterova, I. Degrowth Business Framework: Implications for Sustainable Development. J. Clean. Prod. 2020, 262, 121382. [Google Scholar] [CrossRef]

- Remme, J.; de Waal, A. High performance stakeholder management: What is needed? Meas. Bus. Excell. 2020, 24, 367–376. [Google Scholar] [CrossRef]

- Oleksiv, I.; Kharchuk, V. Theoretical and methodological ambushes of enterprise management at ambushes of interests of stakeholders. Democr. Vryduvannya 2014, 13, 48–53. [Google Scholar]

- Akulenko, K.; Fyliuk, G. Methodological principles of evaluation of investment attractiveness of enterprise. Balt. J. Econ. Stud. 2018, 4, 387–395. [Google Scholar]

- Seroka-Stolka, O.; Fijorek, K. Enhancing Corporate Sustainable Development: Proactive Environmental Strategy, Stakeholder Pressure and the Moderating Effect of Firm Size. Bus. Strategy Environ. 2020, 29, 2338–2354. [Google Scholar] [CrossRef]

- Temperli, C.; Blattert, C.; Stadelmann, G.; Brändli, U.-B.; Thürig, E. Trade-Offs between Ecosystem Service Provision and the Predisposition to Disturbances: A NFI-Based Scenario Analysis. 2020. Available online: https://0-link-springer-com.brum.beds.ac.uk/article/10.1186/s40663-020-00236-1 (accessed on 22 September 2022).

- Pimenova, O.; Fylyuk, H.; Pimenov, S. Model of assessment of competitiveness and sustainable development of Ukrainian agricultural enterprises. Manag. Theory Stud. Rural. Bus. Infrastruct. Dev. 2020, 42, 330–338. [Google Scholar] [CrossRef]

- Butenko, N.; Kot, L. Methodological approaches to the evaluation of the effectiveness of partnership relations. Balt. J. Econ. Stud. 2019, 5, 42–49. Available online: http://www.baltijapublishing.lv/index.php/issue/article/view/703 (accessed on 22 September 2022). [CrossRef]

- Graves, S.; Waddock, S. Institutional Owners and Corporate Social Performance. Acad. Manag. J. 1994, 37, 1034–1046. [Google Scholar] [CrossRef]

- Komarova, K.; Kovalchuk, N. Social responsibility as a component of business development strategy at Ukrainian enterprises. Innov. Econ. 2016, 162, 25–30. [Google Scholar]

- Fitch. Rating Criteria. Available online: https://www.fitchratings.com/criteria (accessed on 22 September 2022).

- Dyduch, J.; Krasodomska, J. Determinants of Corporate Social Responsibility Disclosure: An Empirical Study of Polish Listed Companies. Sustainability 2017, 9, 1934. [Google Scholar] [CrossRef]

- Tarasiuk, H.; Mostenska, T.; Pashchenko, O.; Rudkivskyi, O.; Burachek, I. Optimization of operation program of manufacturing. Int. J. Sci. Technol. Res. 2020, 9, 24–28. Available online: http://www.ijstr.org/final-print/jan2020/Optimization-Of-Operation-Program-Of-Manufacturing-Enterprise-.pdf (accessed on 22 September 2022).

- SAM Corporate Sustainability Assessment-Annual Scoring & Methodology Review. 2019. Available online: https://www.spglobal.com/esg/csa/static/docs/DJSI_CSAMethodology_MethodologyReview.pdf (accessed on 22 September 2022).

- Ministry of Agrarian Policy and Food of Ukraine. K: Ministry of Agrarian Policy and Food of Ukraine. 2022. Available online: http://surl.li/dzcda (accessed on 22 September 2022).

- State Statistics Service of Ukraine. K: State Statistics Service of Ukraine. 2022. Available online: http://ukrstat.gov.ua/ (accessed on 22 September 2022).

- Moldavan, L.; Pimenova, O. “Holdingization” of the agricultural sector of Ukraine: Consequences and ways of their prevention. Manag. Theory Stud. Rural. Bus. Infrastruct. Dev. 2021, 43, 217–224. [Google Scholar] [CrossRef]

- Lupenko, Y.; Kropyvko, M. Agroholdings in Ukraine and strengthening the social orientation of their activities. Econ. Agro-Ind. Complex 2017, 7, 5–21. [Google Scholar]

- ISO 26000; 2010 Guide on Social Responsibility. Translated and published by EY. 2010; 129. Available online: http://meraua.com/files/ISO_26000_-Rus--draft.pdf (accessed on 22 September 2022).

- ISO 9001; Family Quality Management. Translated and published by Gorbunkov. 2022; 28. Available online: https://pqm-online.com/assets/files/pubs/translations/std/iso-9001-2015-(rus).pdf (accessed on 22 September 2022).

- Coca-Cola System Sustainability Report in Ukraine. 2018. Available online: https://www.coca-colaukraine.com/content/dam/journey/ua/uk/private/2019/July/Coca-Cola-Corporate-Report-GRI-2018.pdf (accessed on 22 September 2022).

- Pimenov, S. Choosing a location for a logistics center as a strategic advantage. Coll. Science. In Proceedings of the International Scientific and Practical Conference “Small and Medium Business: Problems and Prospects for Development in Ukraine, Kyiv, Ukraine, September 2016; pp. 168–171. [Google Scholar]

- Integrated Report of PJSC Ukrzaliznytsia. 2017. Available online: https://www.uz.gov.ua/files/file/Интегрoваний%20звіт%202017.pdf (accessed on 22 September 2022).

- Integrated Report of JSC Ukrzaliznytsia. 2018. Available online: https://www.uz.gov.ua/files/file/Book%20UZ_18_Final(new).pdf (accessed on 22 September 2022).

- Non-Financial Services of NJEC “Energoatom”. 2018. Available online: http://nfr2018.energoatom.kiev.ua/ua/Chiste-dovkIllya.php (accessed on 22 September 2022).

{kind=link}

| Sphere | Area of Important Issues |

|---|---|

| Financial and economic sphere | Financial results |

| Anticompetitive actions | |

| Anti-corruption | |

| Supply chain | |

| Ecological sphere | Resource efficiency |

| Energy efficiency and energy saving | |

| Aquatic resources | |

| Biodiversity | |

| Emissions into the atmosphere | |

| Waste | |

| Social sphere | Labor relations |

| Occupational safety and health | |

| Personnel management and development | |

| Human Rights | |

| Local communities | |

| Marketing and labeling | |

| Confidentiality of information | |

| Sphere of corporate governance | Ethics and integrity |

| Corporative management | |

| Reporting practice | |

| Interaction with stakeholders |

| Sphere | Area | Indicator | Question | Evaluation Model | Enterprise 1 | … | Enterprise X |

| Corporate Governance sphere | SU200: Corporate governance | SU200.1—«The structure of corporate governance» | 200.1.1 Please indicate what is the supreme corporate governance body of your organization. | Boolean | 1 | 1 | 0 |

| 200.1.2 Please describe the corporate governance structure of the organization. If available, provide a snippet of the corporate governance structure. | Qualitative | 1 | 0 | 0.7 | |||

| 200.1.3 Please indicate whether there are officials in the higher body who are responsible for making decisions on the economic, environmental and social impact of the organization. If so, provide provisions for such organizational units. | Qualitative | 0 | 0 | 1 | |||

| SU200.2—«The composition of the supreme body of corporate governance» | 200.2.1 Please provide information on the composition of the supreme body of corporate governance, indicating: (a) The general composition; (b) The number of executive directors; (c) The number of independent members; (d) The number of women. | Plural | 1 | 0.7 | 1 | ||

| 200.2.2 Please specify the term of office of each member of the supreme body of corporate governance. | Plural | 0.7 | 0.4 | 1 |

| Class | Characteristics of the Class |

|---|---|

| AAA | Highest level of corporate sustainability |

| AA | Very high level of corporate sustainability |

| A | High level of corporate sustainability |

| BBB | Sufficiently high level of corporate sustainability |

| BB | Sufficient level of corporate sustainability |

| B | The level of corporate sustainability is not high enough |

| CCC | The level of corporate sustainability is below sufficient |

| CC | Significantly insufficient level of corporate sustainability |

| C | Corporate sustainability is uncertain |

| D | Absolutely uncertain and unpredictable level of corporate sustainability. The enterprise is completely closed |

| Range | Scale | Class |

|---|---|---|

| [≥BV] | ≥829 | AAA |

| [≥BV—Step] AND [<BV] | ≥737 AND <829 | A |

| [≥BV—Step × 2] AND [<BV—Step] | ≥645 AND <737 | A |

| [≥BV—Step × 3] AND [<BV—Step × 2] | ≥553 AND <645 | BBB |

| [≥BV—Step × 4] AND [<BV—Step × 3] | ≥461 AND <553 | BB |

| [≥BV—Step × 5] AND [<BV—Step × 4] | ≥368 AND <461 | B |

| [≥BV—Step × 6] AND [<BV—Step × 5] | ≥276 AND <368 | CCC |

| [≥BV—Step × 7] AND [<BV—Step × 6] | ≥184 AND <276 | CC |

| [≥BV—Step × 8] AND [<BV—Step × 7] | ≥ 92 AND <184 | C |

| [<BV—Step × 8] | <92 | D |

| Class | Number of Enterprises |

|---|---|

| AAA | 1 |

| AA | 3 |

| A | 4 |

| BBB | 1 |

| BB | 1 |

| B | 0 |

| CCC | 2 |

| CC | 6 |

| C | 6 |

| D | 16 |

| Range | Scale | Class |

|---|---|---|

| [≥BV] | ≥92.1% | AAA |

| [≥BV—Step] AND [<BV] | ≥81.8% AND <92.1% | AA |

| [≥BV—Step × 2] AND [<BV—Step] | ≥71.6% AND <81.8% | A |

| [≥BV—Step × 3] AND [<BV—Step × 2] | ≥61.4% AND <71.6% | BBB |

| [≥BV—Step × 4] AND [<BV—Step × 3] | ≥51.1% AND <61.4% | BB |

| [≥BV—Step × 5] AND [<BV—Step × 4] | ≥40.9% AND <51.1% | B |

| [≥BV—Step × 6] AND [<BV- Step × 5] | ≥30.7% AND <40.9% | CCC |

| [≥BV—Step × 7] AND [<BV—Step × 6] | ≥20.5% AND <30.7% | CC |

| [≥BV—Step × 8] AND [<BV—Step × 7] | ≥10.2% AND <20.5% | C |

| [<BV—Step × 8] | <10.2% | D |

| Class | Number of Enterprises |

|---|---|

| AAA | 2 |

| AA | 5 |

| A | 2 |

| BBB | 1 |

| BB | 0 |

| B | 6 |

| CCC | 6 |

| CC | 3 |

| C | 3 |

| D | 12 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pimenowa, O.; Pimenov, S.; Fyliuk, H.; Sitnicki, M.W.; Kolosha, V.; Kurinskyi, D. Sustainable Business Model of Modern Enterprises in Conditions of Uncertainty and Turbulence. Sustainability 2023, 15, 2654. https://0-doi-org.brum.beds.ac.uk/10.3390/su15032654

Pimenowa O, Pimenov S, Fyliuk H, Sitnicki MW, Kolosha V, Kurinskyi D. Sustainable Business Model of Modern Enterprises in Conditions of Uncertainty and Turbulence. Sustainability. 2023; 15(3):2654. https://0-doi-org.brum.beds.ac.uk/10.3390/su15032654

Chicago/Turabian StylePimenowa, Olena, Serhii Pimenov, Halyna Fyliuk, Maksym W. Sitnicki, Vasylyna Kolosha, and Dmytro Kurinskyi. 2023. "Sustainable Business Model of Modern Enterprises in Conditions of Uncertainty and Turbulence" Sustainability 15, no. 3: 2654. https://0-doi-org.brum.beds.ac.uk/10.3390/su15032654