An Integrated MCDM Model for Sustainable Course Planning: An Empirical Case Study in Accounting Education

1

Business School, Nanjing Xiaozhuang University, Nanjing 211171, China

2

ISCTE Business School, BRU-IUL, University Institute of Lisbon, 1649-026 Lisbon, Portugal

3

School of Management and Economics, University of Electronic Science and Technology of China (UESTC), Chengdu 611731, China

*

Author to whom correspondence should be addressed.

Sustainability 2023, 15(6), 5024; https://0-doi-org.brum.beds.ac.uk/10.3390/su15065024

Submission received: 8 February 2023

/

Revised: 28 February 2023

/

Accepted: 10 March 2023

/

Published: 12 March 2023

(This article belongs to the Special Issue Operations Research: Optimization, Resilience and Sustainability)

Abstract

:As an essential element of higher education, course planning at the program level is a complicated multi-criteria decision making (MCDM) problem. In addition, a course planning process tailored to sustainable development is exceptionally important to sustaining the quality of academic programs. However, there is a scarcity of research on the program course planning problem at the operational level due to a diverse set of stakeholder requirements in practice. Motivated by the challenge, this study proposes an innovative MCDM model for sustainable course planning based on He-Xie management theory. In the introduced framework, the best worst method (BWM) can obtain the optimal weights of sustainability competencies, which are then embedded into the fuzzy filter ranking (FFR) method to generate the ranking of candidate courses by each course module, considering the connectivity between courses and the development of sustainability competencies. Finally, multi-choice goal programming (MCGP) is adopted to allocate each selected course to a semester, aiming to balance total credits and average difficulty level among semesters as much as possible. The practicability and reliability of the proposed course planning model is validated through a case study of an undergraduate accounting program. Results show that the proposed framework is a feasible tool for course planning. This research extends the existing literature on course planning by explicitly capturing the fuzzy nature of human decision making and avoids underestimation of the decision. The implications of the paper are not restricted to developing a sustainable course plan for an accounting program.

1. Introduction

As the universal commercial language, accounting is a science of management and an art of interpreting, measuring, and describing economic activities [1]. It serves as the backbone of a business by providing information for making decisions, helping in the evaluation of business performance, and ensuring statutory compliance. Accounting is also a promising field with various career tracks, such as accountant, auditor, tax consultant, business analyst, and financial controller. Despite many accounting tasks being automated, demand for accounting professionals is not expected to wane. The [2] projects a growth of employment by 7% for accountants and auditors from 2020 to 2030 in the United States. The bright job market and the versatility of career opportunities make earning an accounting degree a good option. Accounting education provides a broad range of business courses and prepares students, as future decision makers (DMs), for success in dynamic organizational contexts. Today, accounting is still a popular major among undergraduate students, and accounting degree programs are commonly available at colleges and universities [3].

In order to be sustainable in a competitive environment and meet public expectation, universities continuously try to improve the quality of academic programs [4]. Among the various academic and administrative activities, course planning plays a critical role in operating an accredited degree program. The program course planning problem (PCPP) is a decision process used to determine which compulsory and elective courses should be offered during which semester. The course plan at the program level is a key and core component of the talent cultivation scheme for any major in a higher education institution. No matter whether the academic degree program is newly launched or has existed for a long time, a solid course plan must be developed and updated regularly to align with educational objectives, technological and social change, and industrial demand. A well-designed course plan is the prerequisite and foundation for developing a detailed course timetable of each semester, as well as the guideline for carrying out daily teaching and learning activities. The quality of the program-level course plan could impact a school’s reputation and its attractiveness to potential applicants [5]. As the saying goes, “well begun is half done”. Effective course planning of educational programs could ensure the efficient use of limited educational resources, students’ satisfaction with their learning experiences, and fulfilment of the school’s vision and mission. To this end, in the light of the wide range of potential courses that can be taught in a four-year degree program, it is critical to prioritize candidate compulsory and elective courses that belong to the same course module/type/group, choose the most important ones according to the available resources (e.g., the number of faculty, credits needed for graduation), and then properly assign the selected courses to each semester.

Education for sustainable development (ESD) has received widespread attention in recent years due to its unique and important contribution to a holistic transformation of education systems [6]. ESD aims to develop the knowledge, skills, understanding, values, and actions required to improve quality of life and create a sustainable future, ensuring environmental protection, social equity, and economic development [7]. On the other hand, over recent decades, accounting degree programs have been criticized for failing to develop students’ soft skills and ignoring many problems (e.g., corporate responsibility, ecological environment, and social justice) faced by contemporary society [8,9,10,11]. With a growing interest in sustainability, an increasing number of colleges and universities want to equip students with skills and insights to help society become more sustainable in their future professional careers. However, there has not been major progress in broadening accounting’s boundaries in a sustainability context, and the efforts to reform outdated accounting education has been disappointing [8,12,13]. Currently, only very few accounting programs focus on sustainability issues, including the Bachelor of Accounting and Sustainable Business at the University of Southern Queensland, and the Masters in Sustainable Finance and Accounting at the University of Sussex. Some schools provide specific sustainability courses in their accounting program, such as Sustainability Accounting and Reporting (University of South Australia), Sustainability Accounting and Management (University of Milan), Energy Accounting (Texas A&M University), Social and Environmental Accounting (Charles Sturt University), Issues in Social and Environmental Accounting (University of Glasgow), and Accounting, Sustainability and Finance (University of Edinburgh). In addition, embracing sustainability concepts within the courses is becoming a trend for accounting education [14,15].

Accounting is a practice-oriented discipline, and the accounting profession aims to serve the public interest. To develop students’ potential to manage challenges and uncertain problems facing our planet and enhance employability of graduates, it is crucial for academic programs to prepare graduates with key competencies relevant to sustainable development (SD). In other words, as far as sustainability is concerned, higher education of accounting programs should be designed from a long-term perspective and develop student competencies that are needed by the labor market [16,17]. To enhance the quality of accounting education, this paper attempts to plan the courses of an undergraduate accounting program for sustainable development. Most of the previously published works on the PCPP describe research carried out in the field of pedagogy, and very few studies are conducted at the operational level [5]. Additionally, limited research has been undertaken to assess the relationship between courses and sustainability competencies [18]. The main motivation of this study is to fill these research gaps. In this paper, a novel decision support model integrating best worst method (BWM), fuzzy filter ranking (FFR), and multi-choice goal programming (MCGP) is proposed to develop a course plan at the program level for sustainable development. Specifically, the weights of sustainability competencies are obtained through the BWM approach. By embedding the weights from the BWM, the FFR method is applied to determine the ranking and selection of candidate compulsory and elective courses in each course module, based on their significance to competency development. Finally, based on the course selection results obtained from the BWM-FFR, an MCGP model is constructed to assign the selected courses to corresponding semesters to achieve balance amongst semesters in terms of course credits and course difficulty. A real case study is introduced to illustrate the application of the proposed approach.

The paper has the following threefold contributions:

- There are still many challenges to integrating SD into higher education systems in practice [19]. To the best our knowledge, this is the first study using the multi-criteria decision making (MCDM) method for developing a course plan in an undergraduate accounting program considering sustainability competencies. However, the implications of the study are not limited to course planning of accounting education. The designed decision support model would shed light on implementing other educational activities to achieve the goals of ESD.

- Many articles in the field of operational research (OR) are criticized for their failure to use sound theory to explain the method and outcome [20,21]. Additionally, the gap between theory and talent development practice is a barrier to education improvement [22]. This study proposes a novel process based on He-Xie management theory (HXMT) to address the PCPP, exploring new ways to meaningfully relate theory and practice in higher education.

- This interdisciplinary research makes a modest contribution not only to SD literature but also to accounting education literature. This study also contributes to the quantitative measurement of the correlation between courses and sustainability competencies, termed as a sustainability mapping index. The results of the study show that education administrators can benefit from the proposed decision support model to make more informed decisions in terms of course planning at the program level. The model is also a useful tool for university academic advisors to help students make study plans.

This paper proceeds as follows: Section 2 reviews prior research on course planning and discusses the sustainability competencies to be developed through accounting education. Section 3 proposes an integrated decision support model. The justifications for the use of an integrated BWM-FFR-MCGP method are elaborated upon, and respective mathematical formulations are presented. Section 4 presents a real-life case application based on the proposed model. Section 5 conducts a sensitivity analysis to examine the course evaluation and ranking results under different weights. Finally, Section 6 provides conclusions and avenues for future research.

2. Literature Review

2.1. Course Planning

Prior works have tried to incorporate SD principles within course development. For instance, [13] linked accounting education with sustainable development and suggested potential sustainability/environmental courses that can be integrated into accounting education programs in South African universities. Based on self-determination theory, Ref. [23] proposed a five-stage development cycle to plan an artificial intelligence curriculum for SD. Ref. [24] used concept maps and a qualitative graphical tool for developing a new bachelor’s degree in engineering, enabling evaluation of the sustainability contribution of the degree. However, there is a lack of studies at a micro level that instruct course planning in practice using mathematical analysis to improve the sustainability of academic programs.

OR techniques have been broadly applied to solve educational decision problems in practice, including scheduling, resource allocation, budgeting, and performance measurement [25,26]. To improve education programs and optimize the limited resources of academic institutions, [27] applied the analytical hierarchy process (AHP) to prioritize the required knowledge of students participating in cooperative education (co-op) programs. Ref. [28] also adopted the AHP to measure the relative importance of indicators for teacher training workshops. The AHP, which uses a full pairwise comparison matrix, is more cumbersome than the proposed BWM. Ref. [29] applied the fuzzy AHP (FAHP) method to construct the selection criteria of elective courses in accounting undergraduate and graduate education from the students’ viewpoint. Ref. [30] used the analytic network process (ANP) for the determination of competency indices for the development of a virtual reality course. While the ANP is able to take the interdependent relationship of criteria into consideration, the correlation among the considered elements is unnoticeable and insignificant, which limits its practical applications due to a higher level of complexity and difficulty for DMs to complete pairwise comparison. Ref. [31] proposed a decision support system based on the goal programming (GP) model to help students develop an optimal long-term course plan considering student preferences. However, the GP model is not able to consider the multiple aspiration levels, which may result in an underestimation of decisions. To balance students’ preferences and advisors’ recommendations when assisting students to prepare long-term course plans, [32] proposed an interactive decision support for course planning plus (IDiSC+) approach. Ref. [33] used deep learning models such as long short-term memory (LSTM) and gated recurrent unit (GRU) to select elective courses based on students’ domain interest. Ref. [34] proposed a sequential pattern mining algorithm, evolutionary search of emerging sequential patterns ((ES)2P), to recommend courses to students based on the sequence of courses students had already taken. These studies neglect the real-life implication of simplification to enable users to understand and implement the introduced tools.

To develop a course plan for an industrial engineering program, [4] proposed the AHP and simple additive weighting (SAW) methods to rank courses by evaluating the relationship between courses and qualifications and then classify them into compulsory and elective courses according to the obtained score of each course. However, the process did not consider the necessity of selecting a certain number of courses from a list of candidate courses. In addition, the AHP is criticized for its lack of consistency. Although SAW is simple on computation, its disadvantage—losing fuzzy messages—results in not addressing the uncertainty in the course planning process, which can be improved using the proposed BWM and FFR approach. Ref. [5] designed a three-phase framework to develop a course plan for an undergraduate supply chain management program. A list of potential courses was proposed in the first phase, and the second phase evaluated the importance of each course based on the AHP and the fuzzy comprehensive evaluation (FCE) method. The final phase used a multi-choice goal programming with utility function (MCGP-U) model to select the courses and corresponding credits. However, the FCE result is greatly impacted by the variance among the evaluators, and the course scheduling problem was not addressed in their study. Ref. [35] utilized an integer programming (IP) model to assist an academic department in handling the course scheduling problem, with an objective of minimizing the time needed to graduate. Only this single objective was considered. Also, the relevance between courses and student competencies, as well as the course selection problem, were not discussed in their work. The missing parts in these works will be addressed simultaneously in our study.

Based on the above literature review, previous OR studies pertaining to course planning focused on the development of the content and timeline for an individual course or the recommendation of suitable courses to students to facilitate their graduation based on the existing program-level course plan. In terms of the PCPP, despite the recognition of the importance of implementing a sustainable course planning process for the quality improvement of an academic program, there is very limited research [36]. Therefore, scholars called for further studies on the PCPP to make an impact on practice [37]. Furthermore, in the prior literature on the PCPP using the MCDM approach, the element of SD has not been considered. While a growing collection of accounting education literature attempts to interact with sustainability in particular, the development of a satisfying course plan for an accounting program has not been studied.

2.2. Sustainability Competency in Accounting Education

Previous studies reveal that there is a gap between the demand for sustainability and the current status of accounting education [38,39,40,41]. Meanwhile, sustainability greatly depends on the competences of the population [42].

To achieve the sustainability goal of any area, diverse factors that act as the evaluation metrics associated with the object should be firstly analyzed [43]. As accounting professionals play a critical role in social management and creating sustainable business practices, the determination of sustainability competences is a key step toward integrating sustainability issues into accounting education [44,45]. Ref. [42] introduced SD competencies that engineering students should acquire when graduating. The competencies include three domains: knowledge and understanding, skills and abilities, and attitudes. The competency framework of ESD developed by the United Nations Educational Scientific and Cultural Organization (UNESCO) covers eight key competency domains [46] which have been widely acknowledged as the guidelines of ESD. Based on the literature review on competency requirements of the accounting profession [47,48,49,50,51,52], Table 1 describes the application of UNESCO’s competency framework for sustainable development in accounting education, which is used as the evaluation and selection criteria of accounting program courses in the present study.

3. The Proposed Framework

3.1. Theoretical Foundation

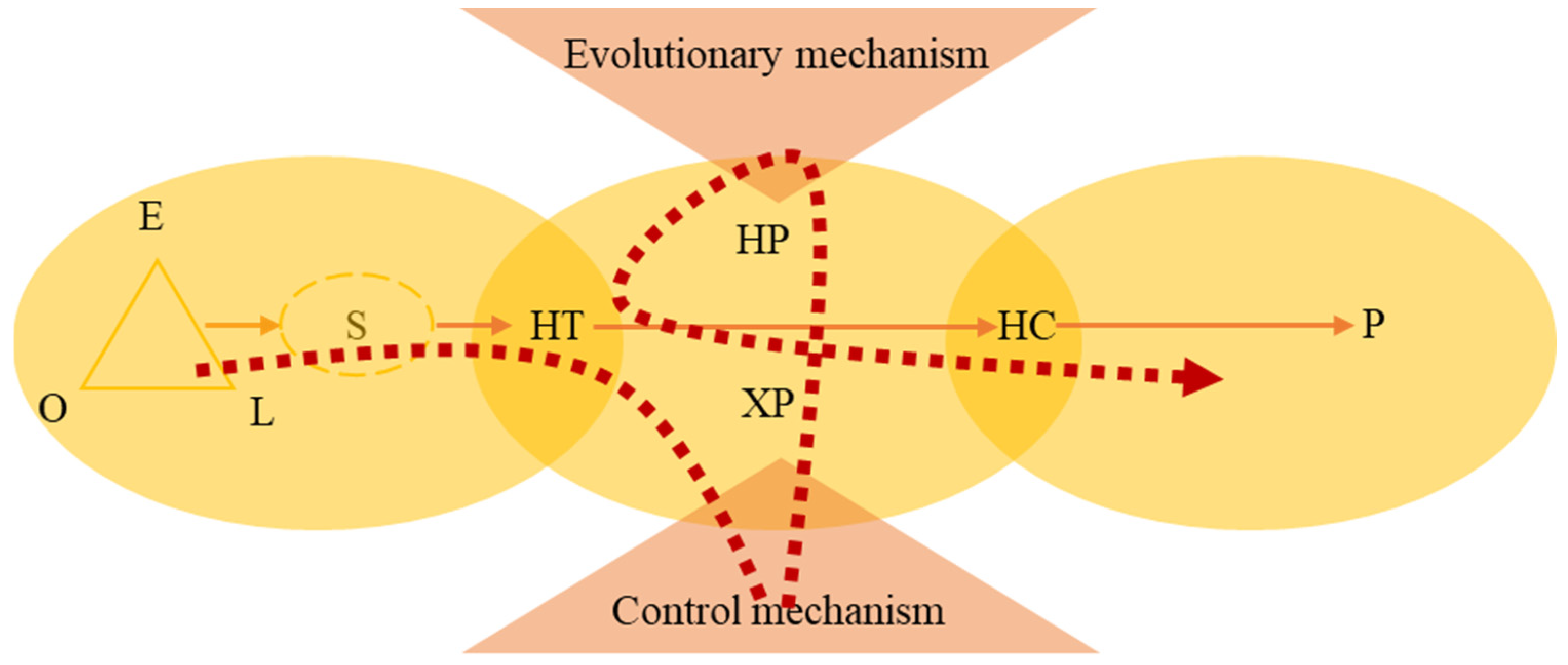

Originated from the core concept of harmony in Confucianism, He-Xie management theory was first introduced by Youmin Xi in 1989, aiming to solve complicated managerial problems in the context of change, ambiguity, and uncertainty [53]. He-Xie is the Chinese pronunciation of harmony and represents two Chinese characters. Specifically, “He” means harmony but not sameness, while “Xie” represents coordination and order. Therefore, He-Xie reflects two different but complementary methodologies for problem-solving. With the development of the HXMT, it has formed an integrated and systematic theoretical framework, as shown in Figure 1 [54].

As seen in Figure 1, the main idea of HXMT is elaborated as follows: firstly, according to an organization’s internal condition (O) and external environment (E), the leadership (L) team determines the organizational strategy (S), which is a long-term goal. In the meantime, under the guidance of vision and mission, the organization should identify core tasks to be completed or key problems to be addressed within a certain period of an organization’s development, which is called as He-Xie theme (HT). Secondly, an organization needs to develop action plans to achieve a specific HT. Among various techniques, tools, and methods, the He principle (HP) is an evolvement mechanism to create organizational value by building organizational culture, improving employee engagement and providing a platform for initiative and self-determination of organizational members. On the other hand, the Xie principle (XP) is a control mechanism and applies a constructivism perspective through process design and optimization. The selection of the principle is determined by the HT. Normally, the XP should be adopted when management problems are mainly caused by predictable or technical factors, while the HP is more appropriate if management problems arise from unpredictable or social factors, such as uncertainty about human behaviors. Finally, in a dynamic environment, HP and XP interact with each other and may convert according to the HT. This process, called He-Xie coupling (HC), contributes to the co-evolution between induced evolution and rational design. In this way, organizations can achieve dynamic coherence, resulting in desired harmony and good performance (P). To summarize, the HXMT, expressed as a double helix model, integrates oriental philosophy (reflected by the HP) and occidental philosophy (reflected by the XP) via HT and HC.

3.2. An Overview of the Course Planning Model

The HXMT can be applied to analyze and direct organizational operations in various contexts, such as human resource management, intellectual property management, nursing management, and university management [55]. In the current uncertain and fast-changing higher education environment, to ensure effective management and better quality of an academic program, a satisfying course plan is necessary. To this end, a management system for course planning is established, as shown in Figure 2, according to the HXMT.

As shown in Figure 2, course planning is identified as the HT in the complex system. To control the uncertainty from individual actors and manage the relationship appropriately, the responsibility of each stakeholder should be clearly defined, which reflects the HP. For example, in the course planning process, the academic affair office should set the tone at the top (e.g., determine the basic structure and modules of the course plan for the whole organization and make the final approval of the submitted course plan of each academic program), the department head should coordinate with other faculty members and external experts to prepare the draft of the course plan, and the dean of the school/institute (i.e., university unit) should conduct the review of the draft plan and provide feedback for revisions as necessary. In addition to the institutional arrangement activities, the workflow and process of course planning can be optimized with mathematical models, following the guide of XP. With an integrative coupling of the HP and the XP, a sustainable course plan can be developed.

To enable the XP to be understood and implemented easily in practice, an integrated decision support model for sustainable course planning is depicted in Figure 3. The proposed model can be applied to any degree program.

As shown, the whole process can be described as the following three phases.

- (1)

- Phase I: Prioritize sustainability competencies (BWM application phase). To develop a sustainable course plan, preparation involves defining a competency matrix for SD (e.g., we use Table 1 as the list of competencies for accounting education), which is the evaluation and selection criteria of the potential courses. To prioritize various competencies according to their importance to ESD, this study applies the BWM model. Specifically, multiple stakeholders are requested to conduct the pairwise comparison of the competencies; then, the weights—the relative importance of the various criteria—can be obtained.

- (2)

- Phase II: course ranking and selection (FFR application phase). In each course module, a list of potential courses with course information (e.g., credits and difficulty level) is determined. In the meantime, the requirement of total credits for each course module must be defined. Then, a sustainability mapping index, which measures the importance/contribution of each course to the development of sustainability competencies, can be calculated using the FFR approach. Candidate courses are ranked in each module based on the result of the respective index, and the top ones are selected to satisfy the credit requirement for graduation.

- (3)

- Phase III: course scheduling (MCGP application phase). Once all the compulsory and elective courses are determined for each course module, the last step is to assign all the courses to corresponding semesters. In the scheduling process, multiple objectives and constraints need to be considered. To achieve the minimum deviations from the aspirations, the decision problem of scheduling can be solved through the MCGP model.

3.3. Methodological Background

3.3.1. BWM

The best worst method, a pairwise comparison-based method, is proposed by [56] to solve MCDM problems. The BWM is one of the most commonly used MCDM methods for obtaining criteria weights. Compared with the AHP method [57], which is another widely adopted MCDM method for weight determination but is relatively cumbersome because it uses a full pairwise comparison matrix, the BWM requires less data and time for comparisons and produces more reliable results due to more consistent comparisons. Therefore, the BWM is suitable for the analysis of the relative importance of different sustainability competencies in this study. The steps of the BWM are described as follows.

Step 1. Define a set of decision criteria. A set of criteria denoted as should be considered in the decision problem. In the present study, the sustainability competencies are used as the selection criteria of the course planning problem.

Step 2. Identify best and worst criteria. The DMs determine the best criterion (e.g., the most desirable, the most important factor for the decision problem) and the worst one (e.g., the least desirable, the least important factor for the decision problem) from the set of determining factors defined in step 1.

Step 3. Determine the degree of preference for the best decision criterion over all the other criteria using a nine-point (1–9) scale. Specifically, a score of 1 means equal importance of the two criteria, while a score of 9 indicates that the best criterion is significantly more important than the other factors. The obtained best-to-others (BO) vector is expressed as (, ,…, ), where represents the preference of the best criterion over criterion and = 1.

Step 4. Determine the degree of preference for all the criteria over the worst criterion using a nine-point (1–9) scale. Similar to the previous step, the obtained other-to-worst (OW) vector would be (, ,…, )T, where represents the preference of criterion over the worst criterion and = 1.

Step 5. Calculate the optimal weights (, ,…, ). The purpose is to determine the optimal weights of the criteria, such that the maximum absolute differences and for all are minimized. The problem can be formulated as model (1).

Model (1) can be translated to model (2):

By solving model (2), the optimal weights (, ,…, ) and can be obtained, where presents a consistency ratio. The closer the value is to zero, the greater the consistency is and, consequently, the more reliable the comparisons become.

3.3.2. FFR

The fuzzy filtering ranking method is a relatively new compromising method proposed by [58] to determine the ranking of alternatives. The FFR method is a combination of filtering method, discrete fuzzy score, and Likert scale [59]. Compared with some well-known traditional ranking methods, such as Technique of Order Preference Similarity to the Ideal Solution (TOPSIS) [60], VIšekriterijumska Optimizacija I KOmpromisno Rešenje (VIKOR) [61], and ELimination Et Choix Traduisant la REalité (ELECTRE) [62], the advantages of FFR are that it does not need to normalize the criterion decision matrix and provides precise ranking results with simple arithmetical calculation and ranking procedure. Therefore, FFR is well suited for quantifying and ranking the importance of potential courses to the development of sustainability competencies. The calculation steps of the FFR method are presented as follows.

Step 1: Classify all the criteria values of the alternatives into five categories, which are mapped to the discrete fuzzy score [0, 1]. The mapping is described below: (1) strongly significant criterion (correspond to fuzzy score 1); (2) significant criterion (correspond to fuzzy score 0.75); (3) normal criterion (correspond to fuzzy score 0.5); (4) non-significant criterion (correspond to fuzzy score 0.25); and (5) strongly non-significant criterion (correspond to fuzzy score 0).

Step 2: Construct four filters to serve as boundaries to the above five scales. The first filter of th criterion = + ; the second filter of th criterion = + ; the third filter of th criterion = + ; and the fourth filter of th criterion = + . The notations , , and are respectively the average value, maximum value, and minimum value of the alternatives in th criterion.

Step 3: Create a transition decision matrix, (transition value of th criterion in th alternative), which reflects the discontinuous perception of the DMs for most MCDM problems. Specifically, if the value of th criterion for th alternative is less than the first filter of th criterion, it should be mapped to 0; if the value falls between the first and second filter, then the output value of the transition decision matrix equals 0.25; likewise, if the value falls between the second and third filter, it should be mapped to 0.5; if the value falls between the third and fourth filter, it is mapped to 0.75; finally, if the input value is above the fourth filter, the output value equals 1.

Step 4: Calculate the weight correctors = 1/. As the output value of the transition decision matrix may not equal for each criterion, which affects the weight deviation of the criterion, a correction value is used to ensure the output value equals 1.

Step 5: Multiply the weight with the weight corrector and transition decision matrix to generate the weighted and corrected decision matrix, denoted as = × × and = 1, where is the weight of the th criterion. Finally, the ranking of the alternatives is determined according to the sum of in each alternative.

3.3.3. MCGP

Goal programming proposed by [63] has been widely used in solving various MCDM problems. The main characteristic of the GP approach is the determination of an aspiration level for each objective, which gives rise to the different goals. The mathematical programming problem behind this approach seeks to minimize the deviation of each objective to its aspiration level. Due to the uncertainty and lack of information in decision problems, it is not practical in many real cases to determine only one aspiration level for the objective. For instance, if the Chief Procurement Officer determines the cost saving goal of the year as USD 10 million, this aspiration level might be underestimated and, thus, the organization may miss the opportunity for better financial performance. MCGP was proposed by [64] to overcome the drawback of the traditional GP model, enabling DMs to consider multi-aspiration levels of the goal (e.g., the more the better, or the less the better) and thus avoids the underestimation of the decision. For the course planning problem, the school desires to assign selected courses to each semester in as balanced a way as possible. As a result, MCGP, which is formulated as Equation (3) to Equation (8), meets the needs of the present study.

s.t.

where is the objective function of th goal. and are respectively the weights attached to the sum of deviational values and , and and . and are allowable positive and negative deviations attached to the th goal . and are positive and negative deviations of or . is the aspiration level (target value) of the th goal and is a continuous variable with a range of interval values . and are the lower and upper bounds of , respectively.

4. An Illustrative Case

4.1. Background

To illustrate the validity of the proposed framework for sustainable course planning, a case study of an undergraduate accounting program of a Chinese university is conducted. The vision of the accounting program is to provide an exceptional student learning experience and become the preferred source of professionally trained graduates in the region. The mission of the program is to equip students with the knowledge and skills to be successful as citizens and professionals. In this university, a complete course plan is composed of general education and major education. As courses under general education are provided in the first two years of undergraduate study and are centrally arranged by the university, this study focuses on planning the program-specific courses, which need to be completed by students in the last two years of study.

Currently, the course plan of the undergraduate accounting program is reviewed on an annual basis. However, the revisions of the course plan are manual and merely based on intuitive decisions. A standardized process has not been developed. The importance degree of the desired competencies has not been determined, nor has the relationship between the courses and the competencies been established. The department head often struggles to replace outdated courses with new, suitable courses. The factors to properly assign courses to semesters were not considered. The business school intends to improve the course planning process to ensure the quality of talent development and increase student satisfaction. Developing a satisfying course plan for all the degree programs has been identified as a core task of the 3-year school development plan. To solve the drawbacks of the manual and intuitive process and make the course plan more sustainable, both faculty members and accounting experts are involved to implement the proposed framework.

4.2. Implementation of the Proposed Framework

4.2.1. Prioritization of Sustainability Competencies Using the BWM

The weights of the sustainability competencies listed in Table 1 can be calculated through the BWM model. The DM panel in this case study includes one accounting department head, three accounting professors from the business school, and one accounting professional from a local company. All experts have over 10- years of experience in their fields. The comparison data needed for the BWM were collected individually from each panel member. Table 2 exhibits the response of one of the experts regarding his judgements on the relative importance of the best (i.e., most important) criterion over all the other criteria, on a scale ranging from 1 to 9. Table 3 exhibits his preference for all other criteria over the worst (i.e., least significant) criterion, using the same scale running from 1 to 9. According to this expert (DM1), normative (C3) and self-awareness (C7) are identified as the best criterion and the worst criterion, respectively. The calculated consistency ratio () is 0.21, which is close to zero; therefore, the comparisons are consistent and reliable.

Through the application of the BWM model in a BWM solver, an excel file developed by the creator of the method, criteria weights were obtained for all DMs as summarized in Table 4. Consistency tests of pairwise comparisons made by each DM were passed. Finally, simple averaging [65] was used to aggregate weights across DMs. As can be seen from Table 4, integrated problem-solving (C8) is viewed as the most important competency, followed by critical thinking (C6) and collaboration (C5). The results indicate that anticipatory (C2) is the least important criterion.

4.2.2. Course Ranking and Selection Using FFR

Based on the courses currently offered by the studied program and the reference to courses provided by leading accounting programs of other universities, a total of 53 compulsory and elective courses were proposed for selection. Pj (j = 1, 2,⋯, J) is used to denote the candidate courses. Each course was classified into a module according to the course structure defined by the studied case. To illustrate the calculation process, we used seven courses (P1–P7) under the first course module, compulsory–preliminary courses, as an example.

In the first step, the experts were asked to determine collectively the relevance between the courses and the sustainability competencies. The relevance degree can be expressed using a 10-point scale [66], ranging from 1 (extremely weak) to 10 (extremely strong) with integer values of 2 to 9 as intermediate values. The scale also represents the contribution level of the courses to the development of sustainability competencies. In the second step, based on the rated value of each course given by the panel members, the boundary values can be calculated by course module. The evaluation results and boundary values for the module of compulsory–preliminary courses are shown in Table 5. In the third step, a transition decision matrix () was established according to the evaluation values and boundary values. The fourth step of the FFR was to calculate the weight corrector () according to the constructed transition decision matrix. Table 6 illustrates the results of the third and fourth steps for the seven courses in the example. The last step was to obtain the weighted and corrected decision matrix () and rank the courses based the sustainability mapping index (), which was the sum of the weighted and corrected decision matrix in each course. Table 7 displays the weighted and corrected decision matrix, the results of sustainability mapping index (column “Sum”), and the corresponding ranking.

By repeating the above steps for all course modules, the results of all potential courses were presented in Table 8. The accounting department head and professors who are the members of the DM panel provided information of credits (ranging from 1 to 8) and difficulty level (ranging from 1 to 5) for each course, which is also listed in Table 8. According to the ranking of the course and the total credits needed for the module, the top-ranked courses should be selected. For instance, as the module of compulsory–preliminary courses requires a total of 9 or 10 credits, finally, the top 4 courses were selected to satisfy the credits requirement. As a result, 19 out of 27 compulsory courses and 16 out of 26 elective courses were selected. Figure 4 and Figure 5 respectively depict the selection results of compulsory courses and elective courses.

4.2.3. Course Scheduling Using MCGP

According to the selected courses shown in Figure 4 and Figure 5, compulsory courses and elective course have 52 credits (19 courses) and 38 credits (16 courses) in total, respectively. These courses need to be scheduled within the four semesters in the last two years of an undergraduate program. From a balanced perspective, the most ideal situation is that, on average, each semester is assigned with compulsory courses of 13 credits and elective courses of 9.5 credits. In the meantime, the average difficulty levels for the selected compulsory courses and elective course are respectively 3 and 3.1875.

There are 35 courses that will be provided by the accounting program. To schedule these selected courses within four semesters, multiple objectives were defined as follows:

- (G1)

- For compulsory courses, to distribute the workload of courses as evenly as possible, the total deviation between the allocated credits and the desired credits (13 credits) in each semester should be no more than 10, and the lower the better.

- (G2)

- For compulsory courses, to ensure the course difficulty level among semesters is maintained as balanced as possible, the total deviation between the actual difficulty level on average and the desired difficulty level (score 3) in each semester should be no more than 2.5, and the lower the better.

- (G3)

- Similar to the first goal, for elective courses, the total deviation between the allocated credits and the desired credits (9.5 credits) in each semester should be no more than 8, and the lower the better.

- (G4)

- Similar to the second goal, for elective courses, the total deviation between the actual difficulty level on average and the desired difficulty level (score 3.1875) in each semester should be no more than 2, and the lower the better.

We assign a penalty weight of 5 for missing goals related to compulsory courses and a penalty weight of 3 for missing goals related to elective courses. Let represent the difficulty level of the jth course and denote the credits of the jth course. The binary decision variable determines whether course j is scheduled in semester t. is equal to 1 if the course is assigned to the semester and, otherwise, it is equal to 0. For the convenience of modelling, the selected courses are renumbered according to their order in the original code and, thus, j = 1, 2,⋯, 35, and the first 19 courses are compulsory courses, while the last 16 courses are elective courses. According to the MCGP model, the scheduling problem is formulated as follows.

s.t.

In the above model, Equation (9) is the objective function to minimize the total deviation of each objective to the aspiration levels. Equation (10) to Equation (13) are associated with the defined four goals. Equation (13) and Equation (14) respectively mean the deviation of the aspirational level from its lower bound and the lower and upper bounds of aspiration level. Equation (16) ensures that each course can onlybe assigned to one semester. In terms of Equation (17), for each module of elective courses, there is a limitation to the number of courses that can be offered in the same semester. Elective courses in the same group cannot be provided for more than one to two courses in the same semester. This is to allow students to have broader choices among different modules of electives in one semester and thus satisfy the needs of students with different interest domains. Equation (18) indicates the predecessor-successor relationship. In other words, the successor course should be assigned to a later semester than its predecessor course . is the set of predecessor-successor pairs, and = {(1, 5), (5, 6), (1, 7), (1, 9), (9, 14)}. Equation (19) is a binary (0–1) decision variable. For Equation (20), the identified three courses must be scheduled in the designated semesters.

4.2.4. Results and Discussion

By running the LINGO 18.0 software, the results of variables are obtained, and the detailed course plan of the studied accounting program can be presented as Table 9. As a result, the 19 compulsory courses and 16 elective courses are properly assigned to the four semesters of the last two years of the university education, satisfying all the defined objectives and constraints.

To analyze the results, as can be seen from Table 10, the allocated credits and difficulty level are quite balanced among the semesters. In each semester, the total credits of compulsory courses range from 12 to 14, and the total credits of elective courses range from 9 to 10. In the meantime, in each semester, the average difficulty level of compulsory courses falls between 2.7143 and 4, and the average difficulty level of elective courses is either 3 or 3.25. As a result, all four objectives have been achieved exceptionally as follows:

- (G1)

- for compulsory courses, the total deviation between the allocated credits and the desired credits (13 credits) in each semester is 2, which is only 1/5 of the upper bound of the aspiration level.

- (G2)

- for compulsory courses, the total deviation between the actual average difficulty level and the desired difficulty level (score 3) in each semester is 1.2857, which is about 1/2 of the upper bound of the aspiration level.

- (G3)

- for elective courses, the total deviation between the allocated credits and the desired credits (9.5 credits) in each semester is 2, which is 1/4 of the upper bound of the aspiration level.

- (G4)

- for elective courses, the total deviation between the actual average difficulty level and the desired difficulty level (score 3.1875) in each semester is 0.375, which is about 1/5 of the upper bound of the aspiration level.

Unlike the current course planning process, this case study uses management judgement in a different methodology and is supported by new data, therefore a direct comparison of the results (i.e., the finalized course plan) between the proposed framework and the real-life course planning was not possible. However, the school leaders and academic office head are satisfied with the results and are interested in the designed process.

5. Sensitivity Analysis

To verify the robustness of the solution, a sensitivity analysis is conducted in terms of changes in DMs’ weights on sustainability competency.

In the illustrated case study, namely Case I, when ranking candidate courses using FFR method, the results are based on one set of weights w = (0.0851, 0.0557, 0.1146, 0.0708, 0.1679, 0.1877, 0.0760, 0.2423) from the BWM method. In other words, DMs view integrated problem-solving (C8) as the most important competency, followed by critical thinking (C6) and collaboration (C5), while anticipatory (C2) is the least important criterion. Case II makes the weight of each criterion equal, that is, = [1]8×8. In addition, as shown in Table 11, let each competency be the most critical one in the respective scenario while keeping the rest of the competencies equal. Taking the seven compulsory–preliminary courses as an example; Figure 6 depicts the comparison of the ranking results.

As it is seen, there are five scenarios (i.e., Case I, Case II, Case III, Case IV, and Case X) which have the same ranking results. In all scenarios except Case VIII, course P7 ranks the first. Therefore, this course is sensitive to critical thinking criterion. P3 ranks the last in all cases, identifying it as the least important course in terms of sustainability competency development. P2 becomes a top 3 course only in Case VIII, and P5 becomes a top 3 course in Case VII and Case VIII. On the other hand, P1 is not ranked as a top 3 course only in Case VIII, and P6 is not ranked as a top 3 course in Case VII and Case VIII. To summarize, the DMs’ judgements on the importance of sustainability competency could impact the ranking results to a certain extent. However, the difference of the sustainability mapping index is not significant among the scenarios, ranging from 0.03 to 0.08. Based on the ranking results and the credits required by the module, the same four courses will be selected (i.e., P1, P5, P6, P7) in all scenarios excepted for Case V and Case VIII, where course P2 would replace course P5 and course P6, respectively.

6. Conclusions and Future Work

Course planning is mandatory for initiating any new degree program. It also provides an opportunity to ensure existing degree programs stay current in the job market. A manually generated course plan might contain errors and take a long time to find feasible solutions. Furthermore, education for sustainable development is a key factor in sustaining academic quality. Hence, there is a need for a more possible and realistic process for developing a course plan that considers sustainability competencies. However, scarce research has been conducted to plan program-level courses of higher education at the operational level. This study proposes an integrated MCDM model, based on He-Xie management theory, to address the program course planning problem for sustainable development. In the proposed framework, the BWM method is utilized to obtain the optimal weights of sustainability competencies, the FFR method is adopted to select top-ranked courses in each course module based on the importance of each course to competency development, and then the MCGP model is applied to determine the appropriate semester for each selected course, with the goal of balancing total credits and average difficulty level among semesters as much as possible. Accounting plays a vital role in running a business and is becoming increasingly important in global economic life. A case study of an undergraduate accounting program is performed to illustrate the effectiveness and practicability of the introduced sustainable course planning model.

The success of universities relies on the operation of the system [4]. The strength of the proposed framework is that it enables stakeholders to identify the importance of various factors, prioritize potential courses, and achieve multiple conflicting goals when planning courses at the program level. In each course planning step, stakeholders’ opinions were considered and mathematical models were constructed to provide the requirements under management constraints. The proposed model not only selects more critical courses from a sustainable development perspective, but also balances workload and difficulty level each semester. Although it is time-consuming to implement the framework at the beginning, the practice can be repeated each year, and the total time spent on it would be reduced in the future. Compared with a manual process, the designed process makes more sense, the justification of the course selection can be documented, and the course calendar is more accurate and balanced, resulting in more preferred course plans according to stakeholders’ needs. Compared with previous works on the PCPP, the new decision support model is promising. The novel approach allows the capture of the fuzzy nature of human decision making and avoids underestimation of the decision. The model is flexible and can be easily adjusted according to management preference and objectives. The model also represents a comprehensive process to complete the complex tasks of course planning. Especially, most of the process can be achieved through a spreadsheet without systems, making it easier for users to adopt than other complicated MCDM approaches. The next step of the application is to make the scheduling process workable without the requirement of programming. To this end, our model can be used by collaborating with programming scholars to jointly develop a course planning template or analytical software for use by higher education institutions.

The practical implication of this study is not limited to course planning of accounting programs. The results of the case study also manifest that the proposed model is flexible and can be applied to any degree programs. This paper also contributes to the body of knowledge on educational management and sheds light on linking operational research to theory. Furthermore, the present study invokes interdisciplinary study in education for sustainable development, offering practical directions and guidance for university policy makers to make informed changes and improve administrative efficiency and effectiveness. University academic advisors can also benefit from this research by using the proposed model as a tool to provide consultancy on developing a solid student study plan.

Similar to other studies, this research is subject to some limitations, which can be overcome in future research. In the present study, when applying the BWM to obtain the optimal weights in the context of group decision making, the results might be impacted by extreme values using the simple averaging method. Therefore, other aggregation methods, such as the Bayesian approach and the Delphi approach, can be considered in future research. In addition, unlike the use of single-level evaluation criteria in this study, the main criteria of course evaluation can be further divided into sub-criteria, and then the global weights of the sub-criteria (multiply the local weight of each sub-criterion by the global weight of each main criterion to which it belongs) can be generated. To expand the application areas of the proposed integrated models, further studies also can be conducted by scholars to apply the proposed framework to solve other assignment and scheduling problems, such as university course scheduling problems for assigning faculty to courses and then courses to specific classrooms and timeslots in each semester. Furthermore, some other MCDM methods, such as ANP, FCE, ELECTRE, TOPSIS, and VIKOR, can be used to compare the results of the current study.

Author Contributions

Conceptualization, M.T. and X.W.; methodology, M.T. and X.W.; software, M.T.; validation, X.W.; formal analysis, M.T. and X.W.; investigation, M.T.; resources, M.T.; data curation, M.T. and X.W.; writing—original draft preparation, M.T. and X.W.; writing—review and editing, M.T. and X.W.; visualization, M.T. and X.W.; supervision, X.W.; project administration, M.T.; funding acquisition, M.T. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by the Office of Research of Nanjing Xiaozhuang University (Grant number: 2022NXY47) and the Academic Affairs Office of Nanjing Xiaozhuang University (project title: research on teaching quality evaluation system of new business discipline based on BP neural network).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data that supports the findings of this study are partially included in this article. The complete data is available from the corresponding author upon request.

Conflicts of Interest

The authors declare that there is no conflict of interest regarding the publication of this study.

References

- Kovaleva, V.D.; Rusetskiy, M.G.E.; Efremova, L.A.; Kalakhanova, Z.M.; Kochkarova, Z.R. Cultural and historical aspects in developing the system of accounting. J. Hist. Cult. Art Res. 2018, 7, 48–57. [Google Scholar] [CrossRef] [Green Version]

- Bureau of Labor Statistics. Occupational Outlook Handbook; Bernan Press: Lanham, MD, USA, 2022. [Google Scholar]

- Du, R.; Liang, S.; Schalow, C. What role does mathematics play in accounting performance?—A focus on students’ beliefs and attitudes. J. Account. Financ. 2019, 19, 26–45. [Google Scholar]

- Kırış, Ş. AHP and multichoice goal programming integration for course planning. Int. Trans. Oper. Res. 2014, 21, 819–833. [Google Scholar] [CrossRef]

- Tao, M.; Jiang, J.; Wang, X.; Zhou, J.; Xie, J. A decision support framework for curriculum planning in undergraduate supply chain management program: An integrated approach. Math. Probl. Eng. 2022, 2022, 3494431. [Google Scholar] [CrossRef]

- Holst, J.; Brock, A.; Singer-Brodowski, M.; de Haan, G. Monitoring progress of change: Implementation of Education for Sustainable Development (ESD) within documents of the German education system. Sustainability 2020, 12, 4306. [Google Scholar] [CrossRef]

- Nevin, E. Education and sustainable development. Policy Pract. Dev. Educ. Rev. 2008, 6, 49–61. [Google Scholar]

- Boyce, G.; Greer, S. More than imagination: Making social and critical accounting real. Crit. Perspect. Account. 2013, 24, 105–112. [Google Scholar] [CrossRef]

- Brown, J.; Dillard, J. Accounting education, democracy and sustainability: Taking divergent perspectives seriously. Int. J. Plur. Econ. Educ. 2019, 10, 24–45. [Google Scholar] [CrossRef]

- Douglas, S.; Gammie, E. An investigation into the development of non-technical skills by undergraduate accounting programmes. Account. Educ. 2019, 28, 304–332. [Google Scholar] [CrossRef]

- Rebele, J.E.; Pierre, E.K.S. A commentary on learning objectives for accounting education programs: The importance of soft skills and technical knowledge. J. Account. Educ. 2019, 48, 71–79. [Google Scholar] [CrossRef]

- Cooray, T.; Senaratne, S.; Gunarathne, N. Engagement with sustainable development goals in accounting education: The case of a public university in Sri Lanka. In Engagement with Sustainable Development in Higher Education; Öztürk, M., Ed.; Springer: Berlin, Germany, 2022; pp. 19–37. [Google Scholar]

- Ngwakwe, C.C. Towards integrating sustainable development in South African universities’ accounting education. Int. J. Sustain. Dev. 2014, 17, 348–373. [Google Scholar] [CrossRef]

- Sharma, U.; Stewart, B. Enhancing sustainability education in the accounting curriculum: An effective learning strategy. Pac. Account. Rev. 2022, 34, 614–633. [Google Scholar] [CrossRef]

- Yüksel, F. Sustainability in Accounting Curriculum of Turkey Higher Education Institutions. Turk. Online J. Qual. Inq. 2020, 11, 393–416. [Google Scholar] [CrossRef]

- Jelonek, M.; Urbaniec, M. Development of sustainability competencies for the labour market: An exploratory qualitative study. Sustainability 2019, 11, 5716. [Google Scholar] [CrossRef]

- Piwowar-Sulej, K. Human resources development as an element of sustainable HRM–with the focus on production engineers. J. Clean. Prod. 2021, 278, 124008. [Google Scholar] [CrossRef]

- Gil-Doménech, D.; Magomedova, N.; Sánchez-Alcázar, E.J.; Lafuente-Lechuga, M. Integrating sustainability in the business administration and management curriculum: A sustainability competencies map. Sustainability 2021, 13, 9458. [Google Scholar] [CrossRef]

- Ramos, T.B.; Caeiro, S.; Van Hoof, B.; Lozano, R.; Huisingh, D.; Ceulemans, K. Experiences from the implementation of sustainable development in higher education institutions: Environmental management for sustainable universities. J. Clean. Prod. 2015, 106, 3–10. [Google Scholar] [CrossRef]

- Eden, C.; Ackermann, F. Theory into practice, practice to theory: Action research in method development. Eur. J. Oper. Res. 2018, 271, 1145–1155. [Google Scholar] [CrossRef]

- Mehregan, M.R.; Hosseinzadeh, M. Investigating the development of operations research through the lens of Kuhn’s model of scientific development. Int. J. Humanit. 2012, 19, 155–182. [Google Scholar]

- Furman Shaharabani, Y.; Yarden, A. Toward narrowing the theory–practice gap: Characterizing evidence from in-service biology teachers’ questions asked during an academic course. Int. J. STEM Educ. 2019, 6, 21. [Google Scholar] [CrossRef]

- Chiu, T.K.; Chai, C.S. Sustainable curriculum planning for artificial intelligence education: A self-determination theory perspective. Sustainability 2020, 12, 5568. [Google Scholar] [CrossRef]

- Lozano, F.J.; Lozano, R. Developing the curriculum for a new bachelor’s degree in engineering for sustainable development. J. Clean. Prod. 2014, 64, 136–146. [Google Scholar] [CrossRef]

- Johnes, J. Operational research in education. Eur. J. Oper. Res. 2015, 243, 683–696. [Google Scholar] [CrossRef] [Green Version]

- Smilowitz, K.; Keppler, S. On the use of operations research and management in public education systems. INFORMS TutORials Oper. Res. 2020, 84–105. [Google Scholar] [CrossRef]

- Wudhikarn, R. An approach to enhancing the human capital of enterprises associated with cooperative education. Int. J. Learn. Intellect. Cap. 2015, 12, 61–81. [Google Scholar] [CrossRef]

- Lucas, R.I.; Promentilla, M.A.; Ubando, A.; Tan, R.G.; Aviso, K.; Yu, K.D. An AHP-based evaluation method for teacher training workshop on information and communication technology. Eval. Program Plan. 2017, 63, 93–100. [Google Scholar] [CrossRef]

- Onay, A.; Karamasa, C.; Sarac, B. Application of fuzzy AHP in selection of accounting elective courses in undergraduate and graduate level. J. Account. Financ. Audit. Stud. 2016, 1, 20–42. [Google Scholar]

- Chung, C.C.; Tung, C.C.; Lou, S.J. Research on optimization of VR welding course development with ANP and satisfaction evaluation. Electronics 2020, 9, 1673. [Google Scholar] [CrossRef]

- Shakhsi-Niaei, M.; Abuei-Mehrizi, H. An optimization-based decision support system for students’ personalized long-term course planning. Comput. Appl. Eng. Educ. 2020, 28, 1247–1264. [Google Scholar] [CrossRef]

- Mohamed, A. A decision support model for long-term course planning. Decis. Support Syst. 2015, 74, 33–45. [Google Scholar] [CrossRef]

- Premalatha, M.; Viswanathan, V.; Čepová, L. Application of Semantic Analysis and LSTM-GRU in Developing a Personalized Course Recommendation System. Appl. Sci. 2022, 12, 10792. [Google Scholar] [CrossRef]

- Al-Twijri, M.I.; Luna, J.M.; Herrera, F.; Ventura, S. Course Recommendation based on Sequences: An Evolutionary Search of Emerging Sequential Patterns. Cogn. Comput. 2022, 14, 1474–1495. [Google Scholar] [CrossRef]

- Khamechian, M.; Petering, M.E. A mathematical modeling approach to university course planning. Comput. Ind. Eng. 2022, 168, 107855. [Google Scholar] [CrossRef]

- Tadesse, T.; Mengistu, S.; Gorfu, Y. Using research-based evaluation to inform changes in the development of undergraduate sports science education in Ethiopia. J. Hosp. Leis. Sport Tour. Educ. 2016, 18, 42–50. [Google Scholar] [CrossRef]

- Torrisi-Steele, G. Context and participation: Program-level curriculum design in higher education. In Handbook of Research on Program Development and Assessment Methodologies in k-20 Education; Wang, V., Ed.; IGI Global: Hershey, PA, USA, 2018; pp. 49–66. [Google Scholar]

- Boulianne, E.; Keddie, L.S.; Postaire, M. (Non) coverage of sustainability within the French professional accounting education program. Sustain. Account. Manag. Policy J. 2018, 9, 313–335. [Google Scholar] [CrossRef]

- Ebaid, I.E.S. Sustainability and accounting education: Perspectives of undergraduate accounting students in Saudi Arabia. J. Appl. Res. High. Educ. 2021, 14, 1371–1393. [Google Scholar] [CrossRef]

- Frizon, J.A.; Eugénio, T. Recent developments on research in sustainability in higher education management and accounting areas. Int. J. Manag. Educ. 2022, 20, 100709. [Google Scholar] [CrossRef]

- Mburayi, L.; Wall, T. Sustainability in the professional accounting and finance curriculum: An exploration. High. Educ. Ski. Work.-Based Learn. 2018, 8, 291–311. [Google Scholar] [CrossRef]

- Segalàs, J.; Ferrer-Balas, D.; Mulder, K.F. Introducing Sustainable Development in Engineering Education: Competences, Pedagogy and Curriculum. In Proceedings of the 37th Annual Conference of the European Society for Engineering Education, Rotterdam, The Netherlands, 1–4 July 2009. [Google Scholar]

- Krishankumar, R.; Ecer, F.; Mishra, A.R.; Ravichandran, K.S.; Gandomi, A.H.; Kar, S. A SWOT-Based Framework for Personalized Ranking of IoT Service Providers with Generalized Fuzzy Data for Sustainable Transport in Urban Regions. IEEE Trans. Eng. Manag. 2022, 1–14. [Google Scholar] [CrossRef]

- Makarenko, I.; Plastun, A. The role of accounting in sustainable development. Account. Financ. Control. 2017, 1, 4–12. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Marx, B.; Van der Watt, A. Sustainability in accounting education: An analysis of the teaching thereof at accredited South African universities. S. Afr. J. Account. Res. 2013, 27, 59–86. [Google Scholar] [CrossRef]

- UNESCO [United Nations Educational Scientific and Cultural Organisation]. Education for Sustainable Development Goals: Learning Objectives; UNESCO Publishing: Paris, France, 2017. [Google Scholar]

- Chaffer, C.; Webb, J. An evaluation of competency development in accounting trainees. Account. Educ. 2017, 26, 431–458. [Google Scholar] [CrossRef]

- De Lange, P.; Jackling, B.; Gut, A.M. Accounting graduates’ perceptions of skills emphasis in undergraduate courses: An investigation from two Victorian universities. Account. Financ. 2006, 46, 365–386. [Google Scholar] [CrossRef]

- Halverson, J. Competency-based education in business and accounting. N. Am. Account. Stud. 2020, 3, 1–20. [Google Scholar]

- Lawson, R.A.; Blocher, E.J.; Brewer, P.C.; Cokins, G.; Sorensen, J.E.; Stout, D.E.; Sundem, G.L.; Wolcott, S.K.; Wouters, M.J. Focusing accounting curricula on students’ long-run careers: Recommendations for an integrated competency-based framework for accounting education. Issues Account. Educ. 2014, 29, 295–317. [Google Scholar] [CrossRef] [Green Version]

- Mohamed, E.K.; Lashine, S.H. Accounting knowledge and skills and the challenges of a global business environment. Manag. Financ. 2003, 29, 3–16. [Google Scholar] [CrossRef]

- Qasim, A.; Issa, H.; El Refae, G.A.; Sannella, A.J. A model to integrate data analytics in the undergraduate accounting curriculum. J. Emerg. Technol. Account. 2020, 17, 31–44. [Google Scholar] [CrossRef]

- Xi, Y.; Cao, X.; Xiangli, L. A Chinese view on rebuilding the integrity of management research: The evolving He-Xie management theory. Chin. Manag. Stud. 2010, 4, 197–211. [Google Scholar] [CrossRef]

- Xi, Y.; Zhang, X.; Ge, J. Replying to management challenges: Integrating oriental and occidental wisdom by HeXie management theory. Chin. Manag. Stud. 2012, 6, 395–412. [Google Scholar] [CrossRef]

- Cao, X.; Zhang, X.; Xi, Y. Ambidextrous organization in harmony: A multi-case exploration of the value of HeXie management theory. Chin. Manag. Stud. 2011, 5, 146–163. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method. Omega 2015, 53, 49–57. [Google Scholar] [CrossRef]

- Saaty, T.L. The Analytical Hierarchy Process, Planning, Priority Setting, Resource Allocation; Decision Making Series; McGraw-Hill: New York, NY, USA, 1980. [Google Scholar]

- Chang, T.Y.; Ku, C.C.Y. Fuzzy filtering ranking method for multi-criteria decision making. Comput. Ind. Eng. 2021, 156, 107217. [Google Scholar] [CrossRef]

- Likert, R. A technique for the measurement of attitudes. Arch. Psychol. 1932, 140, 1–55. [Google Scholar]

- Hwang, C.L.; Yoon, K. Methods for multiple attribute decision making. In Multiple Attribute Decision Making; Springer: Berlin, Germany, 1981; pp. 58–191. [Google Scholar]

- Opricović, S. Višekriterijumska Optimizacija Sistema u Građevinarstvu; Građevinski Fakultet Univerziteta: Belgrade, Serbia, 1998. [Google Scholar]

- Benayoun, R.; Roy, B.; Sussman, N. Manual de reference du programme electre. Note Synth. Form. 1966, 25, 79. [Google Scholar]

- Charnes, A.; Cooper, W.W. Management Models and Industrial Applications of Linear Programming; John Wiley: Hoboken, NJ, USA, 1961. [Google Scholar]

- Chang, C.T. Revised multi-choice goal programming. Appl. Math. Model. 2008, 32, 2587–2595. [Google Scholar] [CrossRef]

- Srdjevic, B.; Srdjevic, Z.; Reynolds, K.M.; Lakicevic, M.; Zdero, S. Using analytic hierarchy process and best–worst method in group evaluation of urban park quality. Forests 2022, 13, 290. [Google Scholar] [CrossRef]

- Frick, T.W.; Chadha, R.; Watson, C.; Zlatkovska, E. Improving course evaluations to improve instruction and complex learning in higher education. Educ. Technol. Res. Dev. 2010, 58, 115–136. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

The theoretical framework of HXMT (reproduced from [54]).

Figure 1.

The theoretical framework of HXMT (reproduced from [54]).

Figure 2.

Application of HXMT to course planning.

Figure 3.

An integrated decision support model for course planning.

Figure 4.

Selection results of compulsory courses.

Figure 5.

Selection results of elective courses.

Figure 6.

Ranking results under 10 scenarios.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Framework of sustainability competency in accounting education.

| Key Sustainability Competence | Description in Accounting Education |

|---|---|

| System thinking (C1) |

|

| Anticipatory (C2) |

|

| Normative (C3) |

|

| Strategic (C4) |

|

| Collaboration (C5) |

|

| Critical thinking (C6) |

|

| Self-awareness (C7) |

|

| Integrated problem-solving (C8) |

|

Table 2.

Best criterion preference over the other criteria for DM1.

| Best to Others | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 |

|---|---|---|---|---|---|---|---|---|

| C3 | 7 | 6 | 1 | 6 | 4 | 3 | 8 | 2 |

Table 3.

Preference of all criteria over the worst criterion for DM1.

| Others to the Worst | C7 |

|---|---|

| C1 | 2 |

| C2 | 3 |

| C3 | 8 |

| C4 | 3 |

| C5 | 5 |

| C6 | 6 |

| C7 | 1 |

| C8 | 7 |

Table 4.

Results of BWM: individually derived criteria weights.

| Decision Makers | w1 | w2 | w3 | w4 | w5 | w6 | w7 | w8 |

|---|---|---|---|---|---|---|---|---|

| DM1 | 0.0577 | 0.0673 | 0.3365 | 0.0673 | 0.1010 | 0.1346 | 0.0337 | 0.2019 |

| DM2 | 0.0765 | 0.0547 | 0.0638 | 0.0335 | 0.3252 | 0.1913 | 0.0638 | 0.1913 |

| DM3 | 0.0594 | 0.0354 | 0.0743 | 0.0743 | 0.2546 | 0.2546 | 0.1485 | 0.0990 |

| DM4 | 0.1475 | 0.0369 | 0.0632 | 0.0738 | 0.0885 | 0.1475 | 0.0738 | 0.3688 |

| DM5 | 0.0842 | 0.0842 | 0.0351 | 0.1052 | 0.0701 | 0.2104 | 0.0601 | 0.3507 |

| Average | 0.0851 | 0.0557 | 0.1146 | 0.0708 | 0.1679 | 0.1877 | 0.0760 | 0.2423 |

| Rank | 5 | 8 | 4 | 7 | 3 | 2 | 6 | 1 |

Table 5.

Course rating and boundaries.

| Courses | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 |

|---|---|---|---|---|---|---|---|---|

| P1 | 6 | 6 | 8 | 5 | 4 | 5 | 3 | 7 |

| P2 | 7 | 3 | 6 | 3 | 2 | 7 | 3 | 5 |

| P3 | 3 | 1 | 4 | 2 | 5 | 4 | 2 | 4 |

| P4 | 5 | 3 | 4 | 5 | 8 | 5 | 3 | 5 |

| P5 | 4 | 5 | 4 | 5 | 6 | 7 | 5 | 5 |

| P6 | 6 | 5 | 5 | 8 | 4 | 5 | 6 | 6 |

| P7 | 5 | 5 | 10 | 8 | 7 | 4 | 8 | 7 |

| 5.1429 | 4 | 5.8571 | 5.1429 | 5.1429 | 5.2857 | 4.2857 | 5.5714 | |

| 7 | 6 | 10 | 8 | 8 | 7 | 8 | 7 | |

| 3 | 1 | 4 | 2 | 2 | 4 | 2 | 4 | |

| 6.2571 | 5.2000 | 8.3429 | 6.8571 | 6.8571 | 6.3143 | 6.5143 | 6.4286 | |

| 5.5143 | 4.4000 | 6.6857 | 5.7143 | 5.7143 | 5.6286 | 5.0286 | 5.8571 | |

| 4.7143 | 3.4000 | 5.4857 | 4.5143 | 4.5143 | 5.0286 | 3.8286 | 5.2571 | |

| 3.8571 | 2.2000 | 4.7429 | 3.2571 | 3.2571 | 4.5143 | 2.9143 | 4.6286 |

Table 6.

The transition decision matrix () and weight corrector ().

| Courses | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 |

|---|---|---|---|---|---|---|---|---|

| P1 | 0.75 | 1 | 0.75 | 0.5 | 0.25 | 0.25 | 0.25 | 1 |

| P2 | 1 | 0.25 | 0.5 | 0 | 0 | 1 | 0.25 | 0.25 |

| P3 | 0 | 0 | 0 | 0 | 0.5 | 0 | 0 | 0 |

| P4 | 0.5 | 0.25 | 0 | 0.5 | 1 | 0.25 | 0.25 | 0.25 |

| P5 | 0.25 | 0.75 | 0 | 0.5 | 0.75 | 1 | 0.5 | 0.25 |

| P6 | 0.75 | 0.75 | 0.25 | 1 | 0.25 | 0.25 | 0.75 | 0.75 |

| P7 | 0.5 | 0.75 | 1 | 1 | 1 | 0 | 1 | 1 |

| 0.0851 | 0.0557 | 0.1146 | 0.0708 | 0.1679 | 0.1877 | 0.0760 | 0.2423 | |

| 0.2667 | 0.2667 | 0.4000 | 0.2857 | 0.2667 | 0.3636 | 0.3333 | 0.2857 |

Table 7.

The weighted and corrected decision matrix () and sustainability mapping index ().

| Courses | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | Sum | Rank |

|---|---|---|---|---|---|---|---|---|---|---|

| P1 | 0.0170 | 0.0148 | 0.0344 | 0.0101 | 0.0112 | 0.0171 | 0.0063 | 0.0692 | 0.1802 | 2 |

| P2 | 0.0227 | 0.0037 | 0.0229 | 0 | 0 | 0.0683 | 0.0063 | 0.0173 | 0.1412 | 5 |

| P3 | 0 | 0 | 0 | 0 | 0.0224 | 0 | 0 | 0 | 0.0224 | 7 |

| P4 | 0.0113 | 0.0037 | 0 | 0.0101 | 0.0448 | 0.0171 | 0.0063 | 0.0173 | 0.1106 | 6 |

| P5 | 0.0057 | 0.0111 | 0 | 0.0101 | 0.0336 | 0.0683 | 0.0127 | 0.0173 | 0.1587 | 4 |

| P6 | 0.0170 | 0.0111 | 0.0115 | 0.0202 | 0.0112 | 0.0171 | 0.0190 | 0.0519 | 0.1590 | 3 |

| P7 | 0.0113 | 0.0111 | 0.0458 | 0.0202 | 0.0448 | 0 | 0.0253 | 0.0692 | 0.2279 | 1 |

Table 8.

Ranking of potential courses.

| Module | Credits Range | Code (Pj) | Courses | Credits | Difficulty Level | Calculated Index (pij) | Rank |

|---|---|---|---|---|---|---|---|

| Compulsory–preliminary courses | 9–10 | 1 | Introductory Accounting | 3 | 2 | 0.1802 | 2 |

| 2 | Economic Law | 2 | 2 | 0.1412 | 5 | ||

| 3 | English for Accounting | 2 | 1 | 0.0224 | 7 | ||

| 4 | Human Resources Management | 3 | 2 | 0.1106 | 6 | ||

| 5 | Business Communication | 2 | 2 | 0.1587 | 4 | ||

| 6 | Organizational Behavior | 2 | 3 | 0.1590 | 3 | ||

| 7 | Corporate Social Responsibility | 2 | 2 | 0.2279 | 1 | ||

| Compulsory–core courses | 20–21 | 8 | Financial Management | 3 | 3 | 0.0751 | 8 |

| 9 | Intermediate Financial Accounting I | 3 | 3 | 0.1148 | 4–5 | ||

| 10 | Intermediate Financial Accounting II | 3 | 3 | 0.1148 | 4–5 | ||

| 11 | Auditing | 3 | 4 | 0.1553 | 2 | ||

| 12 | Advanced Financial Accounting | 3 | 5 | 0.0576 | 9 | ||

| 13 | Financial Statement Analysis | 3 | 3 | 0.0808 | 7 | ||

| 14 | Managerial Accounting | 3 | 3 | 0.1341 | 3 | ||

| 15 | Taxation Laws | 3 | 4 | 0.1119 | 6 | ||

| 16 | Accounting, Sustainability and a Changing Environment | 2 | 3 | 0.1557 | 1 | ||

| Compulsory–practice- based courses | 8–9 | 17 | Accounting Simulated Operation | 1 | 3 | 0.1263 | 4 |

| 18 | Labor Education | 1 | 2 | 0.1833 | 1 | ||

| 19 | Accounting Information Systems | 2 | 2 | 0.0922 | 7 | ||

| 20 | Application of Excel in Accounting | 2 | 2 | 0.0645 | 8 | ||

| 21 | Simulated Sand-table Exercise | 2 | 3 | 0.1301 | 3 | ||

| 22 | Statistical Software Application | 1 | 3 | 0.1178 | 5 | ||

| 23 | Social Practice | 2 | 4 | 0.1765 | 2 | ||

| 24 | Seminar in Professionalism | 2 | 2 | 0.1092 | 6 | ||

| Compulsory–concentrated professional training | 13–14 | 25 | Graduation Practice | 6 | 4 | 0.3469 | 2 |

| 26 | Graduation Thesis | 8 | 4 | 0.3688 | 1 | ||

| 27 | Capstone Projects in Accounting | 5 | 4 | 0.2843 | 3 | ||

| Elective–major related (general track) | 12–13 | 28 | Government Accounting | 3 | 4 | 0.0968 | 7 |

| 29 | Accounting of Financial Institutions | 2 | 2 | 0.1005 | 6 | ||

| 30 | Python Data Analysis | 2 | 3 | 0.0807 | 8 | ||

| 31 | Big Data Technology and Application | 2 | 4 | 0.1399 | 2 | ||

| 32 | Securities Investment | 2 | 3 | 0.1182 | 3 | ||

| 33 | Academic Paper Writing | 2 | 2 | 0.0795 | 9 | ||

| 34 | Lectures on Academic Frontiers | 1 | 2 | 0.1179 | 4 | ||

| 35 | Accounting and Society | 3 | 3 | 0.1644 | 1 | ||

| 36 | Financial Economics | 2 | 3 | 0.1020 | 5 | ||

| Elective–major related (taxation track) | 7–9 | 37 | Tax Accounting | 3 | 3 | 0.1090 | 5 |

| 38 | Tax Planning | 2 | 4 | 0.2414 | 2 | ||

| 39 | Asset Evaluation | 3 | 4 | 0.2054 | 3 | ||

| 40 | International Taxation | 3 | 3 | 0.1281 | 4 | ||

| 41 | Tax Examination | 2 | 4 | 0.3161 | 1 | ||

| Elective–major related (audit track) | 7–9 | 42 | Internal Auditing | 3 | 4 | 0.2004 | 1 |

| 43 | Internal Control | 3 | 3 | 0.1614 | 4 | ||

| 44 | IT Audit | 3 | 5 | 0.1215 | 6 | ||

| 45 | Fraud Examination | 2 | 3 | 0.1898 | 2 | ||

| 46 | Corporate Strategy and Risk Management | 3 | 4 | 0.1718 | 3 | ||

| 47 | Government Auditing | 2 | 4 | 0.1550 | 5 | ||

| Elective–interdisciplinary in business area | 10–12 | 48 | Introduction to International Trade | 3 | 2 | 0.1386 | 4 |

| 49 | Introduction to Electronic Commerce | 3 | 2 | 0.1147 | 6 | ||

| 50 | Operations Management | 3 | 4 | 0.2277 | 1 | ||

| 51 | International Corporate Finance | 2 | 3 | 0.1342 | 5 | ||

| 52 | Introduction to Marketing | 2 | 2 | 0.1656 | 3 | ||

| 53 | Introduction to Supply Chain Management | 3 | 3 | 0.2192 | 2 |

Table 9.

The course plan for the undergraduate accounting program (exclude general education part).

| Semester 1 (Year 3) | Semester 2 (Year 3) | ||||||

| No. | Original Code | Compulsory Course | Credits | No. | Original Code | Compulsory Course | Credits |

| 1 | M1 | Introductory Accounting | 3 | 5 | P9 | Intermediate Financial Accounting I | 3 |

| 4 | M7 | Corporate Social Responsibility | 2 | 7 | P11 | Auditing | 3 |

| 8 | M13 | Financial Statement Analysis | 3 | 9 | P14 | Managerial Accounting | 3 |

| 10 | M15 | Taxation Laws | 3 | 12 | P17 | Accounting Simulated Operation | 1 |

| 16 | M23 | Social Practice | 2 | 17 | P24 | Seminar in Professionalism | 2 |

| No. | Original code | Elective Course | Credits | No. | Original code | Elective Course | Credits |

| 22 | P32 | Securities Investment | 2 | 23 | P34 | Lectures on Academic Frontiers | 1 |

| 24 | P35 | Accounting and Society | 3 | 27 | P39 | Asset Evaluation | 3 |

| 26 | P38 | Tax Planning | 2 | 31 | P46 | Corporate Strategy and Risk Management | 3 |

| 34 | P52 | Introduction to Marketing | 2 | 35 | P53 | Introduction to Supply Chain Management | 3 |

| Semester 3 (Year 4) | Semester 4 (Year 4) | ||||||

| No. | Original code | Compulsory Course | Credits | No. | Original code | Compulsory Course | Credits |

| 2 | P5 | Business Communication | 2 | 18 | P25 | Graduation Practice | 6 |

| 3 | P6 | Organizational Behavior | 2 | 19 | P26 | Graduation Thesis | 8 |

| 6 | P10 | Intermediate Financial Accounting II | 3 | ||||

| 11 | P16 | Accounting, Sustainability and a Changing Environment | 2 | ||||

| 13 | P18 | Labor Education | 1 | ||||

| 14 | P21 | Simulated Sand-table Exercise | 2 | ||||

| 15 | P22 | Statistical Software Application | 1 | ||||

| No. | Original code | Elective Course | Credits | No. | Original code | Elective Course | Credits |

| 21 | P31 | Big Data Technology and Application | 2 | 20 | P29 | Accounting of Financial Institutions | 2 |

| 25 | P36 | Financial Economics | 2 | 28 | P41 | Tax Examination | 2 |

| 29 | P42 | Internal Auditing | 3 | 30 | P45 | Fraud Examination | 2 |

| 32 | P48 | Introduction to International Trade | 3 | 33 | P50 | Operations Management | 3 |

Table 10.

Actual results analysis.

| Semester | Compulsory Courses | Elective Courses | ||

|---|---|---|---|---|

| Total Credits | Average Difficulty Level | Total Credits | Average Difficulty Level | |

| Semester 1 | 13 | 3 | 9 | 3 |

| Semester 2 | 12 | 3 | 10 | 3.25 |

| Semester 3 | 13 | 2.7143 | 10 | 3.25 |

| Semester 4 | 14 | 4 | 9 | 3.25 |

| Total deviation | 2 | 1.2857 | 2 | 0.375 |

Table 11.

Competency weights under 10 scenarios.

| w1 | w2 | w3 | w4 | w5 | w6 | w7 | w8 | |